8-1 forecasting supply chain requirements cr (2004) prentice hall, inc. chapter 8 i hope you'll...

TRANSCRIPT

8-1

Forecasting Supply Chain Requirements

CR (2004) Prentice Hall, Inc.

Chapter 8

I hope you'll keep in mind that economic forecasting is far from a perfect science. If recent history's any guide, the experts have some explaining to do about what they told us had to happen but never did.

Ronald Reagan, 1984

8-2

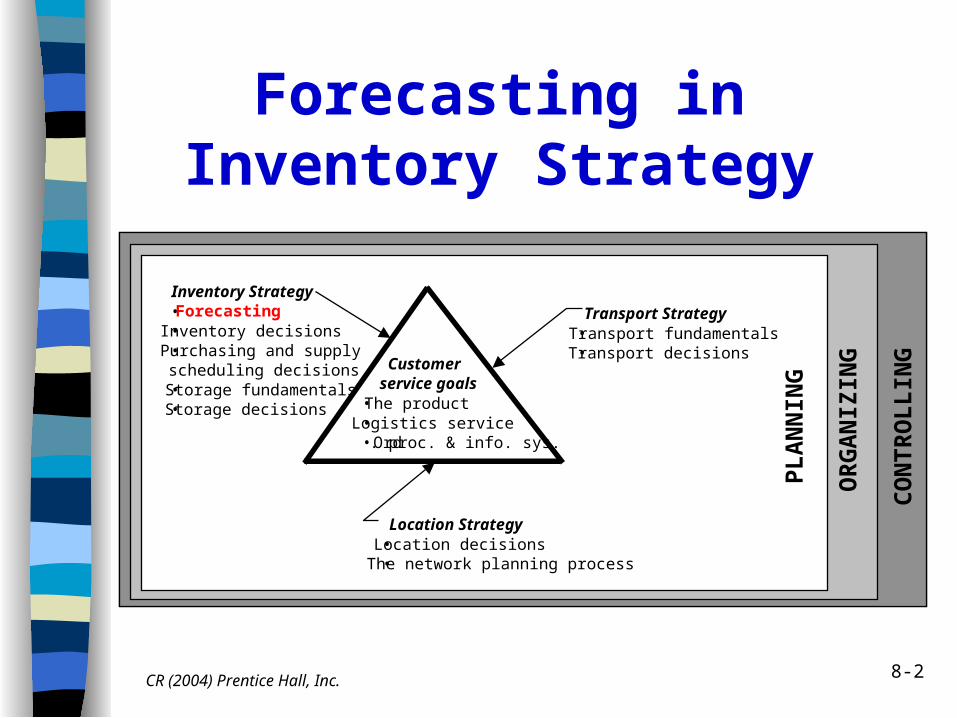

Forecasting in Inventory Strategy

CR (2004) Prentice Hall, Inc.

PL

AN

NIN

G

OR

GA

NIZ

ING

CO

NT

RO

LL

ING

Transport Strategy• Transport fundamentals• Transport decisions

Customer service goals

• The product• Logistics service• Ord. proc. & info. sys.

Inventory Strategy• Forecasting• Inventory decisions• Purchasing and supply

scheduling decisions• Storage fundamentals• Storage decisions

Location Strategy• Location decisions• The network planning process

PL

AN

NIN

G

OR

GA

NIZ

ING

CO

NT

RO

LL

ING

Transport Strategy• Transport fundamentals• Transport decisions

Customer service goals

• The product• Logistics service• Ord. proc. & info. sys.

Inventory Strategy• Forecasting• Inventory decisions• Purchasing and supply

scheduling decisions• Storage fundamentals• Storage decisions

Location Strategy• Location decisions• The network planning process

8-3

What’s Forecasted in the Supply Chain?

•Demand, sales or requirements

•Purchase prices

•Replenishment and delivery times

CR (2004) Prentice Hall, Inc.

8-4CR (2004) Prentice Hall, Inc.

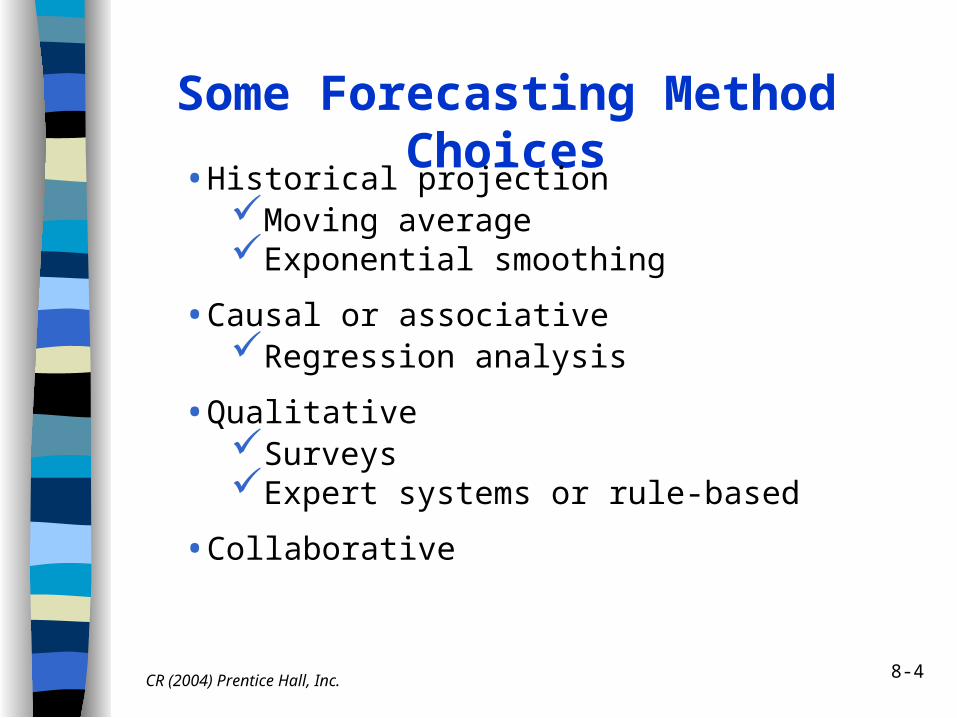

Some Forecasting Method Choices

•Historical projectionMoving averageExponential smoothing

•Causal or associativeRegression analysis

•QualitativeSurveysExpert systems or rule-based

•Collaborative

8-5CR (2004) Prentice Hall, Inc.

Typical Time Series Patterns:Random

0

50

100

150

200

250

0 5 10 15 20 25

Time

Sa

les

Actual salesAverage sales

8-6CR (2004) Prentice Hall, Inc.

Typical Time Series Patterns:Random with Trend

0

50

100

150

200

250

0 5 10 15 20 25

Time

Sa

les

Actual salesAverage sales

8-7CR (2004) Prentice Hall, Inc.

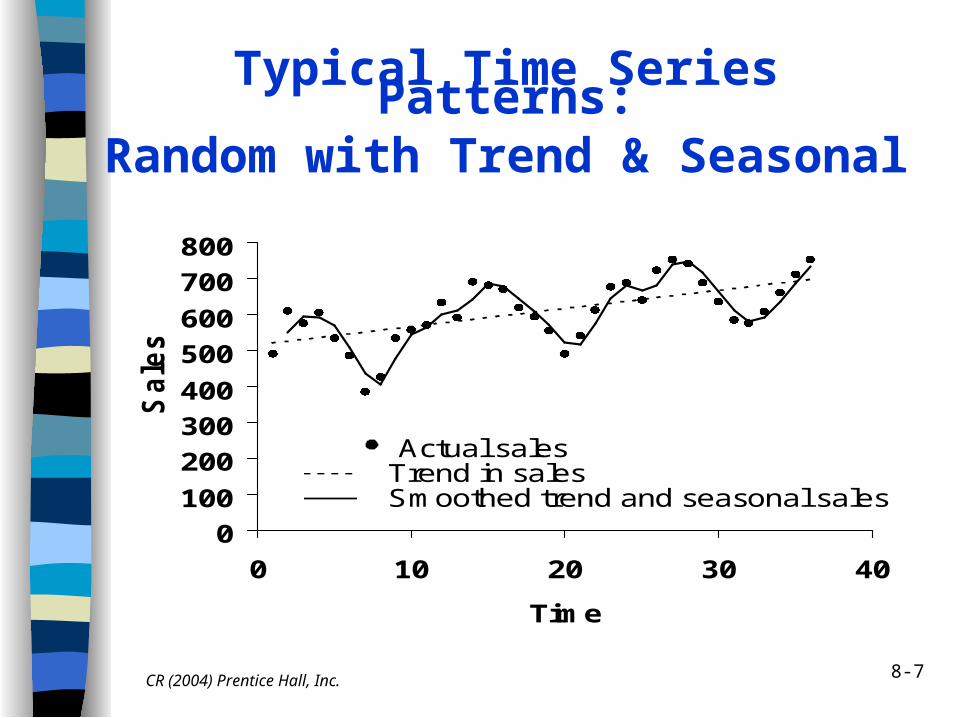

Typical Time Series Patterns:Random with Trend & Seasonal

0

100

200

300

400

500

600

700

800

0 10 20 30 40

Time

Sa

les

Actual salesTrend in salesSmoothed trend and seasonal sales

8-8CR (2004) Prentice Hall, Inc.

Typical Time Series Patterns:Lumpy

Time

Sal

es

8-9CR (2004) Prentice Hall, Inc.

Is Time Series PatternForecastable?

Whether a time series can be reasonably forecasted often depends on the time series’ degree of variability. Forecast a regular time series, but use other techniques for lumpy ones. How to tell the difference:

RuleA time series is lumpy if

3Xwhere

series, of deviation standard series the of mean

X

regular, otherwise.

8-10

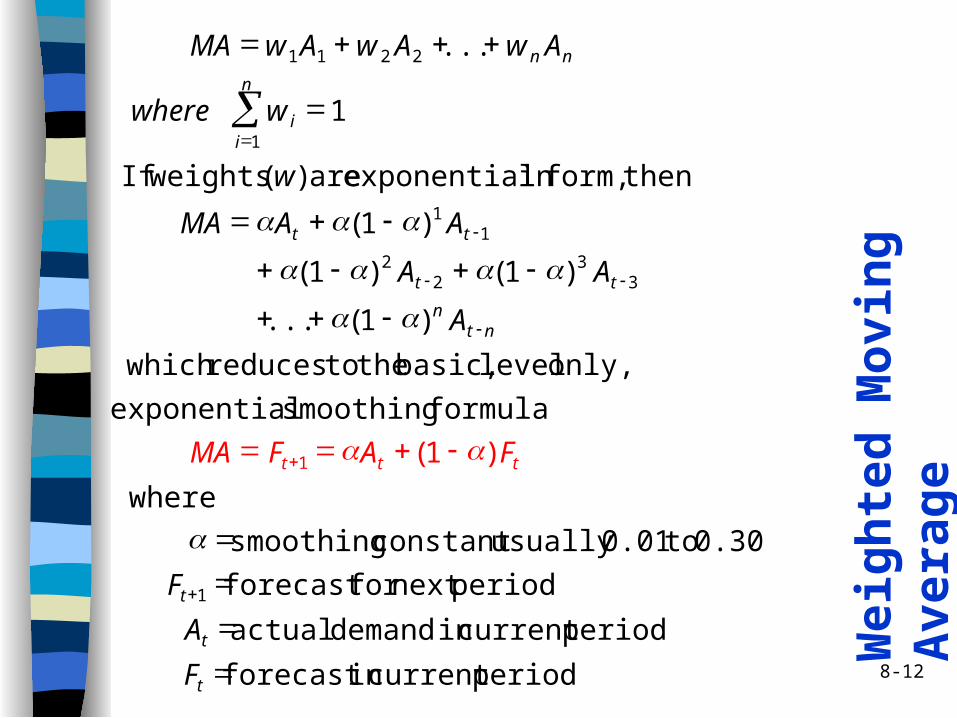

Moving Average

Basic formula

t

nti iAn

MA1

1

where

i = time period

t = current time period

n = length of moving average in periods

Ai = demand in period i

CR (2004) Prentice Hall, Inc.

8-11

Example 3-Month Moving Average Forecasting

Month, iDemand formonth, i

Total demandduring past 3months

3-monthmovingaverage

.

.

....

.

.

....

20 120 . .21 130 360/3 12022 110 380/3 126.6723 140 360/3 12024 110 380/3 126.6725 13026 ?

CR (2004) Prentice Hall, Inc.

8-12

Wei

gh

ted

Mo

vin

g A

vera

ge

period current in forecast

period current in demand actual

period next for forecast

0.30 to 0.01 usually constant smoothing

where

)1(

formula smoothing exponential

only, level basic, the to reduces which

)1(...

)1()1(

)1(

then form, in exponential are )( weightsIf

1

...

1

1

33

22

11

1

2211

t

t

t

ttt

ntn

tt

tt

n

ii

nn

F

A

F

FAFMA

A

AA

AAMA

w

wwhere

AwAwAwMA

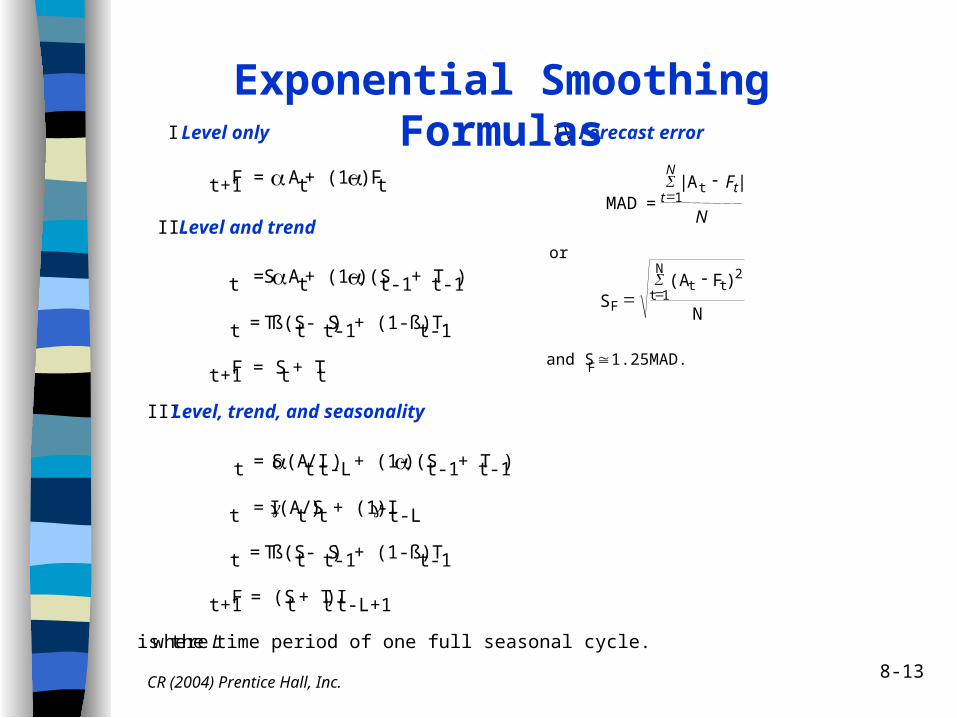

8-13

I. Level only

Ft+1 = At + (1-)Ft

II. Level and trend

St = At + (1-)(St-1 + Tt-1)

Tt = ß(St - St-1) + (1-ß)Tt-1

Ft+1 = St + Tt

III. Level, trend, and seasonality

St = (At/It-L) + (1-)(St-1 + Tt-1)

It = (At/St) + (1-)It-L

Tt = ß(St - St-1) + (1-ß)Tt-1

Ft+1 = (St + Tt)It-L+1

where L is the time period of one full seasonal cycle.

IV. Forecast error

MAD =|A t

F

N

tt

N|

1

or

S(A F )

NF

t t2

t 1

N

and SF 1.25MAD.

Exponential Smoothing Formulas

CR (2004) Prentice Hall, Inc.

8-14CR (2004) Prentice Hall, Inc.

Example Exponential Smoothing Forecasting

Time series data

1 2 3 4Last year 1200 700 900 1100This year 1400 1000 ?

Quarter

Getting started

Assume = 0.2. Average first 4 quarters of data and use for previous forecast, say Fo

8-15CR (2004) Prentice Hall, Inc.

Example (Cont’d)

Begin forecasting

9754/)11009007001200(0

F

First quarter of 2nd year

1000)975(8.0)1100(2.0

)2.01(2.0001

FAF

Second quarter of 2nd year

1080)1000(8.0)1400(2.0

)2.01(2.0112

FAF

8-16CR (2004) Prentice Hall, Inc.

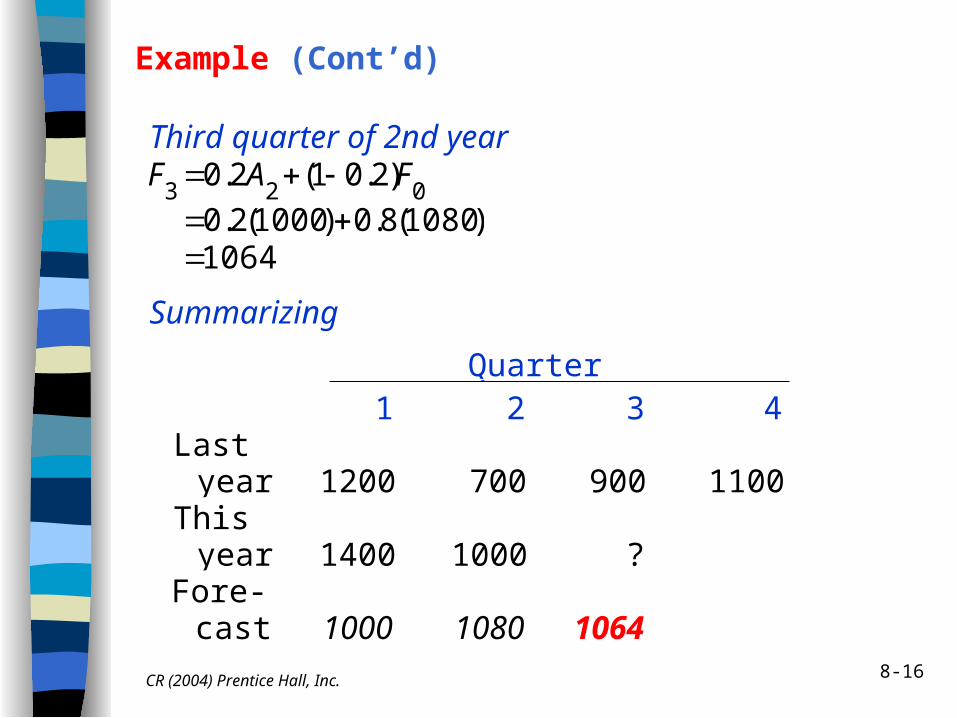

Example (Cont’d)

Third quarter of 2nd year

1064)1080(8.0)1000(2.0

)2.01(2.0023

FAF

Summarizing

1 2 3 4Last year 1200 700 900 1100This year 1400 1000 ?Fore- cast 1000 1080 1064

Quarter

8-17CR (2004) Prentice Hall, Inc.

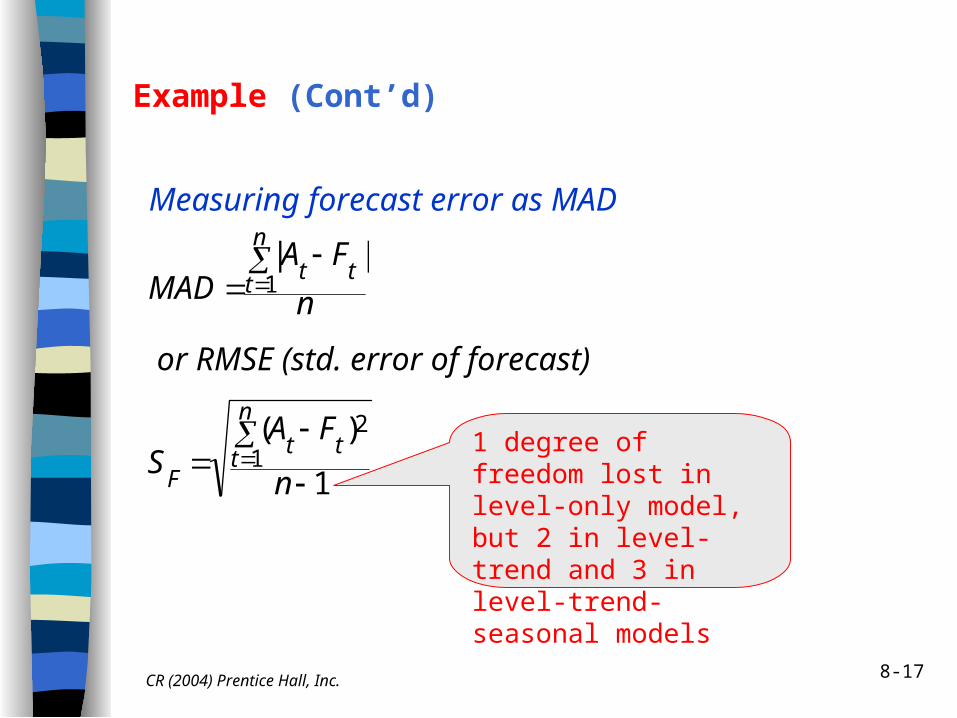

Example (Cont’d)

Measuring forecast error as MAD

or RMSE (std. error of forecast)

n

FAMAD

n

ttt

1||

1

)(1

2

n

FAS

n

ttt

F

1 degree of freedom lost in level-only model, but 2 in level-trend and 3 in level-trend-seasonal models

8-18CR (2004) Prentice Hall, Inc.

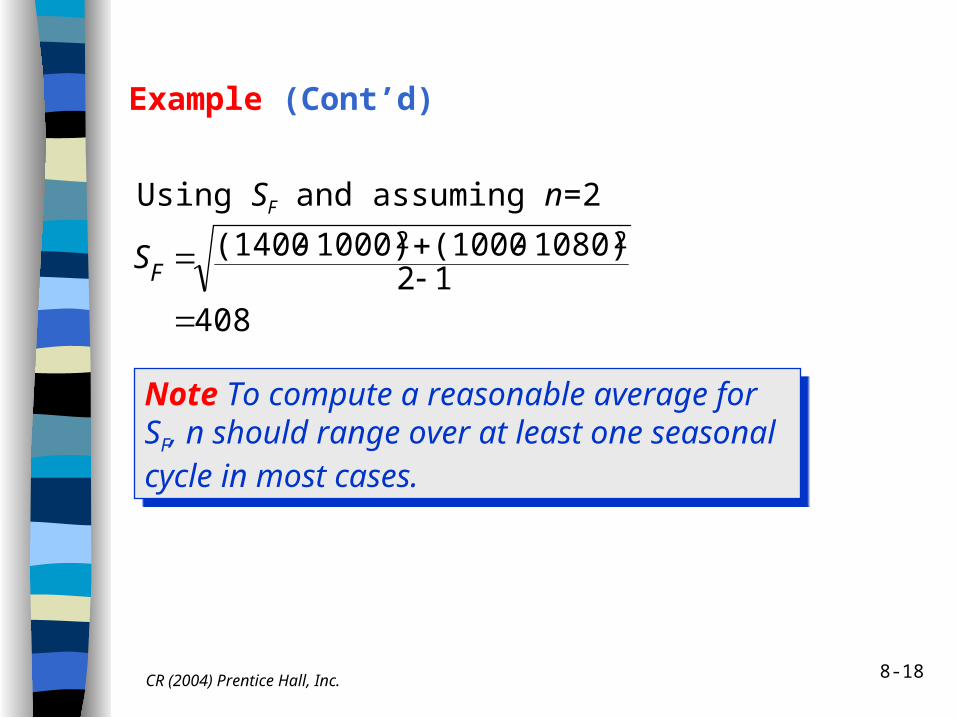

Example (Cont’d)

Using SF and assuming n=2

40812

1080)(10001000)(1400 22

FS

Note To compute a reasonable average for SF, n should range over at least one seasonal cycle in most cases.

Note To compute a reasonable average for SF, n should range over at least one seasonal cycle in most cases.

SF= 408

Example (Cont’d)

Range of the forecast

0Bias

n

FAn

ttt

1

F3=1064

Range

If forecast errors are normally distributed and the forecast

is at the mean of the distribution, i.e., ,

a forecast confidence band can be computed. The error distribution for the level-only model results is:

Bias should be 0 or

close to it in a model of

good fit

CR (2004) Prentice Hall, Inc. 8-19

8-20CR (2004) Prentice Hall, Inc.

Example (Cont’d)

From a normal distribution table, z@95%=1.96. The actual time series value Y for quarter 3 is expected to range between:

or264 Y 1864

8001064)408(96.11064

)(3

F

SzFY

8-21CR (2004) Prentice Hall, Inc.

Correcting for Trend in ES

The trend-corrected model is

St = At (1 – )(St-1 Tt-1)

Tt = (St – St-1) (1 – )Tt-1

Ft+1 = St Tt

where S is the forecast without trend correction.

Assuming = 0.2, = 0.3, S-1 = 975, and T-1 = 0

Forecast for quarter 1 of this year

S0 = 0.2(1100) 0.8(975 + 0) = 1000

T0 = 0.3(1000 – 975) 0.7(0) = 8

F1 = 1000 8 = 1008

8-22

Forecast for quarter 2 of this year

S0 T0

S1 = 0.2(1400) 0.8(1000 8) = 1086.4

T1 = 0.3(1086.4 – 1000) 0.7(8) = 31.5

F2 = 1086.4 31.5 = 1117.9

Forecast for quarter 3 of this year

S2 = 0.2(1000) 0.8(1086.4 31.5) = 1094.3

T2 = 0.3(1094.3 – 1086.4) 0.7(31.5) = 24.4

F3 = 1094.3 24.4 = 1118.7, or 1119

CR (2004) Prentice Hall, Inc.

Correcting for Trend in ES (Cont’d)

8-23CR (2004) Prentice Hall, Inc.

Correcting for Trend in ES (Cont’d)

Summarizing with trend correction

1 2 3 4Last year 1200 700 900 1100This year 1400 1000 ?Fore- cast 1008 1118 1119

Quarter

0 1

Fore-casterror

CR (2004) Prentice Hall, Inc.

Optimizing for ES

Minimize averageforecast error

8-24

CR (2004) Prentice Hall, Inc.

Controlling Model Fit in ES

MSEFA

tt

signal Tracking

Tracking signal monitors the fit of the model to detect when the model no longer accurately represents the data

where the Mean Squared Error (MSE) is

nt

Ft

AMSE

n

t

1

2)(

If tracking signal exceeds a specified value (control limit), revise smoothing constant(s).

n is a reasonable numberof past periods depending

on the application

8-25

8-26

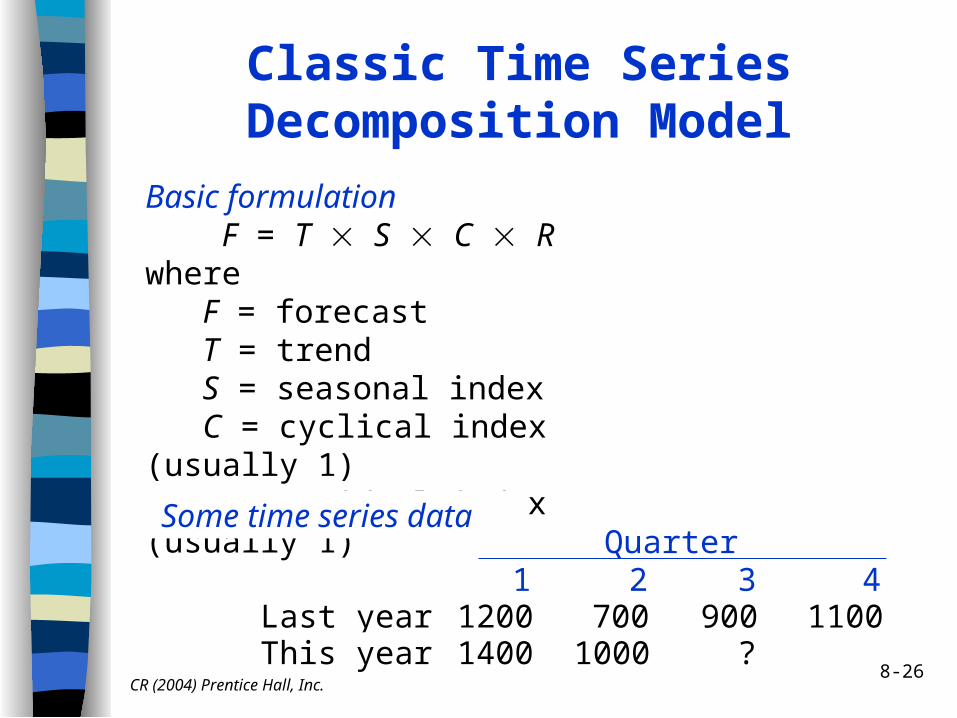

Classic Time Series Decomposition Model

Basic formulation F = T S C Rwhere F = forecast T = trend S = seasonal index C = cyclical index (usually 1) R = residual index (usually 1)

Some time series data

1 2 3 4Last year 1200 700 900 1100This year 1400 1000 ?

Quarter

CR (2004) Prentice Hall, Inc.

8-27CR (2004) Prentice Hall, Inc.

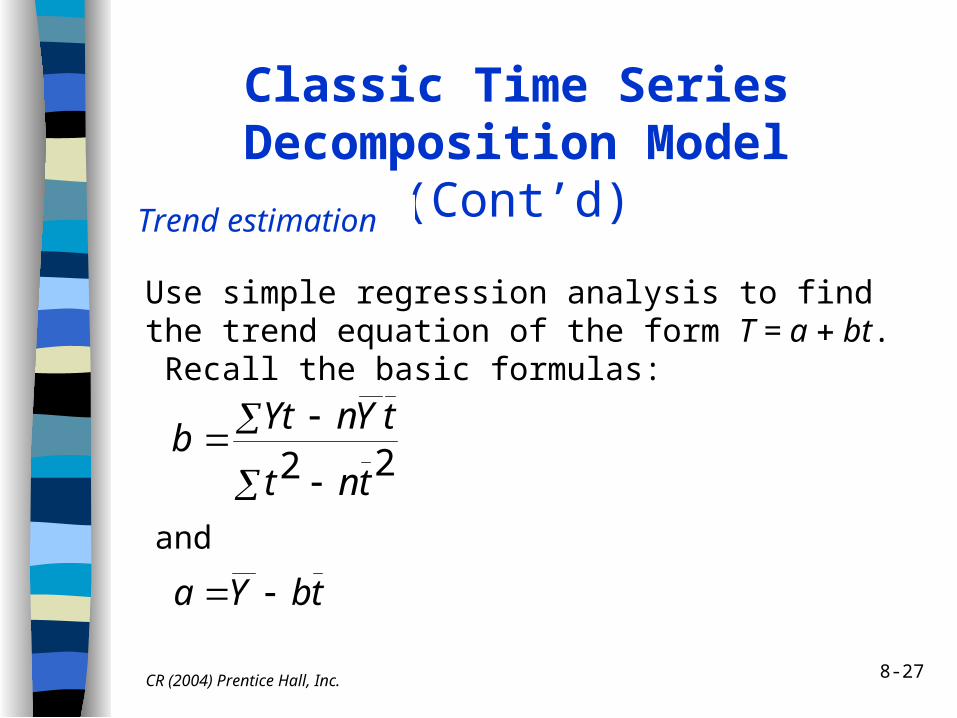

Classic Time Series Decomposition Model (Cont’d)

Trend estimation

Use simple regression analysis to find the trend equation of the form T = a bt. Recall the basic formulas:

22 tnt

tYnYtb

and

tbYa

8-28CR (2004) Prentice Hall, Inc.

Classic Time Series Decomposition Model (Cont’d)

Redisplaying the data for ease of computation.

t Y Yt t2

1 1200 1200 12 700 1400 43 900 2700 94 1100 4400 165 1400 7000 256 1000 6000 36

t=21 Y=6300 Yt=22700 t2=91

8-29

Classic Time Series Decomposition Model (Cont’d)

Hence,

and

then

26(21/6)9100/6)6(21/6)(6322700

b

920.01)37.14(21/66

6300 a

T = 920.01 27.14t

Forecast for 3rd quarter of this year is:

T = 920.01 37.14(7) = 1179.99CR (2004) Prentice Hall, Inc.

8-30CR (2004) Prentice Hall, Inc.

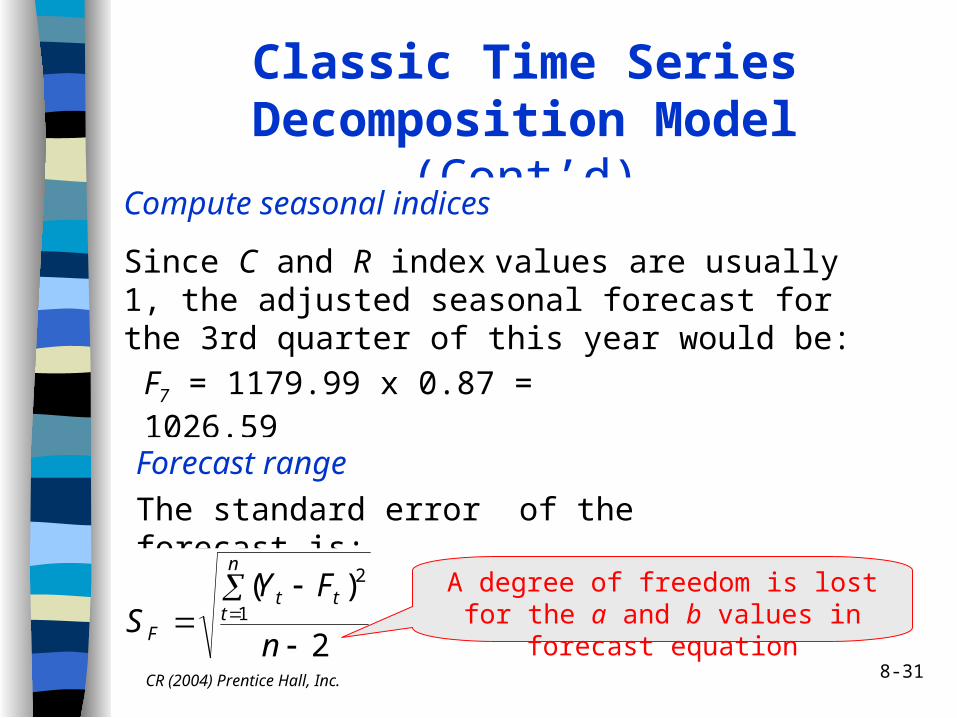

Classic Time Series Decomposition Model (Cont’d)

Compute seasonal indices

The procedure is to form a ratio of actual demand to the estimated demand for a full seasonal cycle (4 quarters). One way is as follows.

t Y TSeasonalIndex, St

1 1200 957.15* 1.25**2 700 994.29 0.703 900 1031.43 0.874 1100 1068.57 1.03

*T=920.01 37.14(1)=957.15**St=1200/957.15=1.25

8-31CR (2004) Prentice Hall, Inc.

Classic Time Series Decomposition Model (Cont’d)

Compute seasonal indices

Since C and R index values are usually 1, the adjusted seasonal forecast for the 3rd quarter of this year would be:

F7 = 1179.99 x 0.87 = 1026.59

Forecast range

The standard error of the forecast is:

2

)(1

2

n

FYS

n

ttt

F

A degree of freedom is lost for the a and b values in forecast equation

8-32CR (2004) Prentice Hall, Inc.

Classic Time Series Decomposition Model (Cont’d)

Qtr t Yt Tt St Ft

1 1 1200 957.15 1.252 2 700 994.29 0.703 3 900 1031.43 0.874 4 1100 1068.57 1.031 5 1400 1105.71 1.27 1404.25*2 6 1000 1142.85 0.88 1005.71**3 7 1179.99 1026.59

*1105.71x1.27=1404.25**1142.85x0.88=1005.71

Tabled computations

8-33CR (2004) Prentice Hall, Inc.

Classic Time Series Decomposition Model (Cont’d)

There is inadequate data to make a meaningful estimate of SF. However, we would proceed as follows:

infinity 22

1005.71)(10001404.25)(1400 22

FS

Then,

Ft z(SF) Y Ft z(SF)

Normally, a larger sample size would be used giving

a positive value for SF

8-34CR (2004) Prentice Hall, Inc.

Regression Analysis

Basic formulation

F = o 1X1 2X2 … nXn

Example

Bobbie Brooks, a manufacturer of teenage women’s clothes, was able to forecast seasonal sales from the following relationship

F = constant 1(no. nonvendor accounts) 2(consumer debt ratio)

CR (2004) Prentice Hall, Inc.

Sales period

(1)

Timeperiod, t

(2)

Sales (Dt )($000s)

(3)

Dt t

(4)

t2

(5)

Trend value(Tt )

(6)=(2)/(5)

Seasonalindex

Forecast($000s)

Summer 1 $9,458 9,458

1 $12,053 0.78Trans-season 2 11,542 23,084 4 12,539 0.92Fall 3 14,489 43,467 9 13,025 1.11Holiday 4 15,754 63,016 16 13,512 1.17Spring 5 17,269 86,345 25 13,998 1.23

Summer 6 11,514 69,084 36 14,484 0.79Trans-season 7 12,623 88,361 49 14,970 0.84Fall 8 16,086 128,688 64 15,456 1.04Holiday 9 18,098 162,882 81 15,942 1.14Spring 10 21,030 210,300 100 16,428 1.28

Summer 11 12,788 140,668 121 16,915 0.76Trans-season 12 16,072 192,864 144 17,401 0.92Fall 13 ? 17,887* $18,602Holiday 14 ? 18,373* 20,945

Totals 78 176,723 1,218,217 650

Regression Forecasting Using Bobbie Brooks Sales Data

N = 12 Dt t = 1,218,217 t2 = 650 = =( , / ) , .176 723 12 14 726 92 = =78 12 6 5/ .Regression equation is: Tt = 11,567.08 + 486.13t *Forecasted values

D t

8-35

8-36

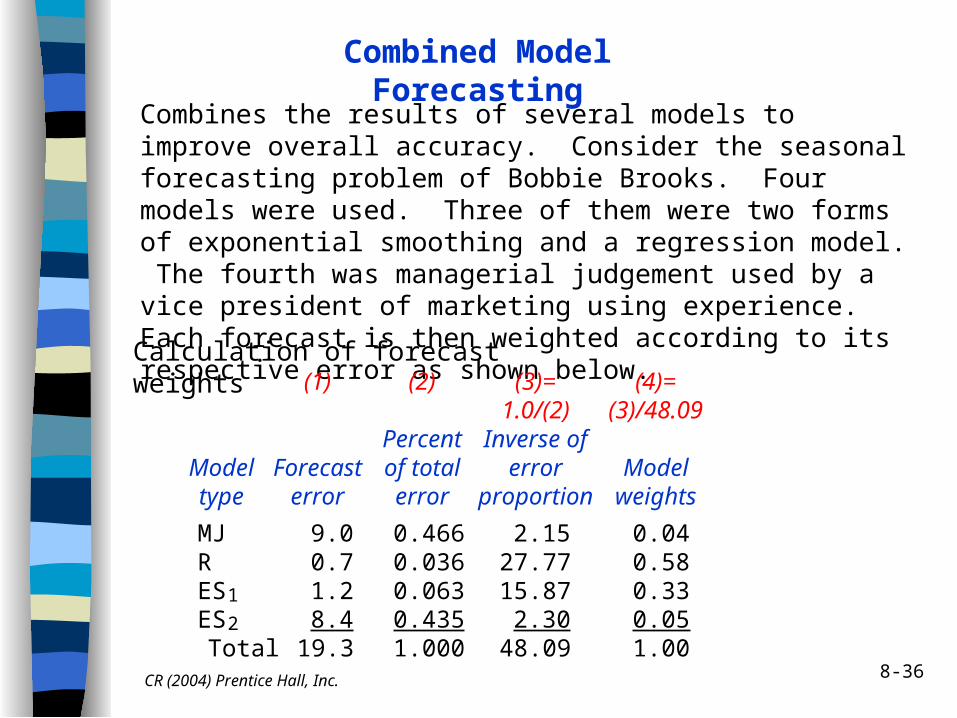

Combined Model Forecasting

Combines the results of several models to improve overall accuracy. Consider the seasonal forecasting problem of Bobbie Brooks. Four models were used. Three of them were two forms of exponential smoothing and a regression model. The fourth was managerial judgement used by a vice president of marketing using experience. Each forecast is then weighted according to its respective error as shown below.

Calculation of forecast weights

Modeltype

(1)

Forecasterror

(2)

Percentof totalerror

(3)=1.0/(2)

Inverse oferror

proportion

(4)=(3)/48.09

Modelweights

MJ 9.0 0.466 2.15 0.04R 0.7 0.036 27.77 0.58ES1 1.2 0.063 15.87 0.33ES2 8.4 0.435 2.30 0.05 Total 19.3 1.000 48.09 1.00

CR (2004) Prentice Hall, Inc.

8-37

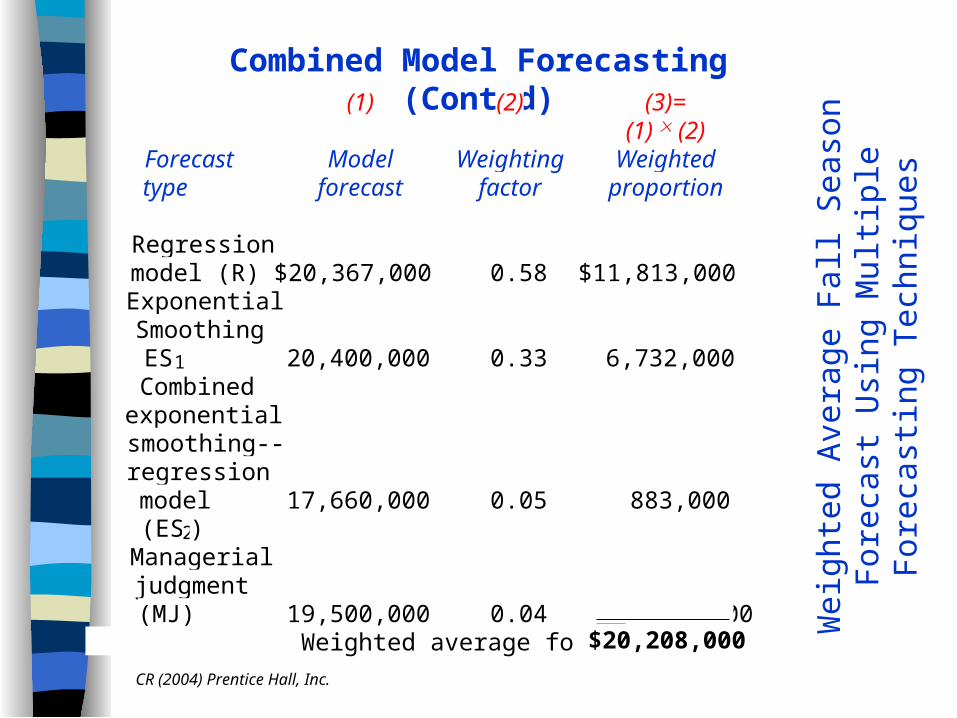

Combined Model Forecasting (Cont’d)

Wei

ghte

d A

vera

ge F

all S

easo

n F

orec

ast

Usi

ng M

ultip

le F

orec

astin

g T

echn

ique

s

Forecasttype

(1)

Modelforecast

(2)

Weightingfactor

(3)=(1) (2)

Weightedproportion

Regressionmodel (R) $20,367,000 0.58 $11,813,000ExponentialSmoothingES1 20,400,000 0.33 6,732,000Combinedexponentialsmoothing--regressionmodel(ES2)

17,660,000 0.05 883,000

Managerialjudgment(MJ) 19,500,000 0.04 780,000

Weighted average forecast $20,208,000

CR (2004) Prentice Hall, Inc.

CR (2004) Prentice Hall, Inc.

Mul

tiple

Mod

el E

rror

s

8-38

8-39CR (2004) Prentice Hall, Inc.

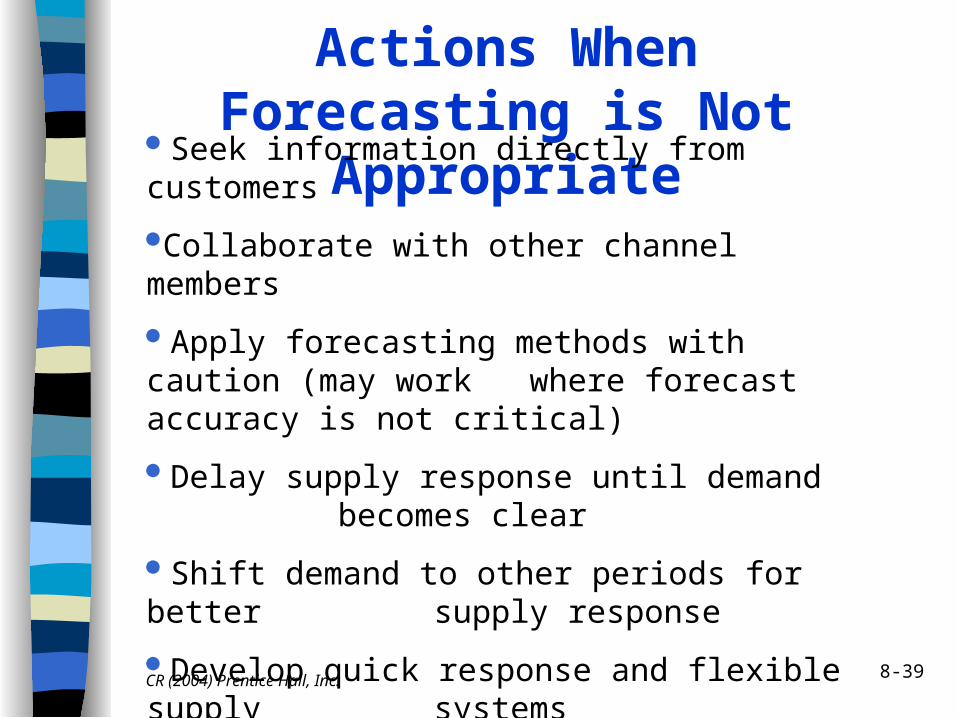

Actions When Forecasting is Not Appropriate

Seek information directly from customers

Collaborate with other channel members

Apply forecasting methods with caution (may work where forecast accuracy is not critical)

Delay supply response until demand becomes clear

Shift demand to other periods for better supply response

Develop quick response and flexible supply systems

8-40CR (2004) Prentice Hall, Inc.

Collaborative Forecasting

• Demand is lumpy or highly uncertain• Involves multiple participants each with

a unique perspective—“two heads are better than one”

• Goal is to reduce forecast error• The forecasting process is inherently

unstable

8-41CR (2004) Prentice Hall, Inc.

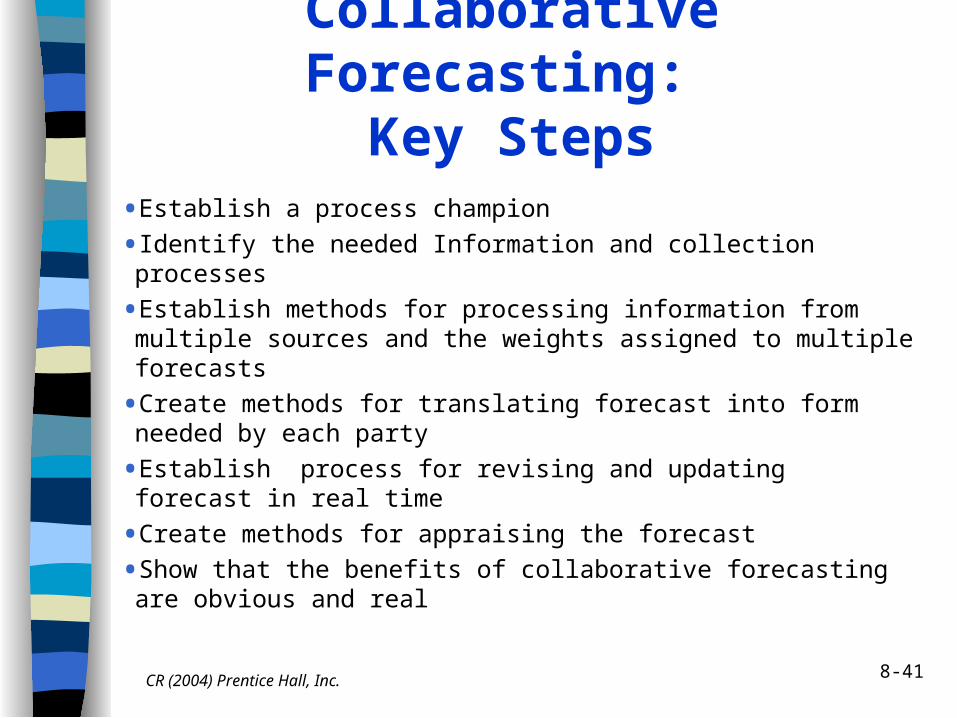

Collaborative Forecasting: Key Steps

•Establish a process champion

• Identify the needed Information and collection processes

•Establish methods for processing information from multiple sources and the weights assigned to multiple forecasts

•Create methods for translating forecast into form needed by each party

•Establish process for revising and updating forecast in real time

•Create methods for appraising the forecast

•Show that the benefits of collaborative forecasting are obvious and real

8-42CR (2004) Prentice Hall, Inc.

Managing Highly Uncertain Demand

Delay forecasting as long as possible

Prioritize supply by product’s degree of uncertainty (supply to the more certain products first)

Apply the principle of postponement to the most uncertain products (delay committing to a final product form until an order is received)

Create flexible supply to changing demand (alter capacity and output rates through subcontracting, computer technology, multi-purpose processes, etc.)

Be able to respond quickly to uncertain demand levels