6. audit techniques

TRANSCRIPT

Audit TechniquesBY

Atta-ur-Rahman Arif

INTRODUCTION

Audit techniques are tools, methods

or processes by means of which an

auditor collects necessary evidence

to support his opinion in respect of

the propositions or assertions

submitted by the client to him for his

examination.

AUDIT PROCEDURES• Audit procedures are ways of

applying techniques to particularphase of an audit.

• Generally, the attainment of the auditobjectives required the collection ofthe evidence to support a decision.

Kinds of audit techniques

• Posting verification

• Extension verification

• Vouching

• Confirmations

• Physical examination

• Reconciliation

• Testing

Kinds of audit techniques

• Analysis of financial statements

• Scanning

• Documentary examination

• Flow charting

• Electronic data processing

• Inspection

• Observation

Kinds of audit techniques

• Enquiry

• Computations

• Management representations

• Sampling techniques

• Compliance test

• Substantive tests

• Analytical review

• Use of computer- assisted audit techniques

KINDS• Posting Verification

–Verification of items by one source to

another source

–To establish the authencity and

consistency of recording process

• Extension Verification

–Multiplying two or more accounts to

prove the accuracy of the total

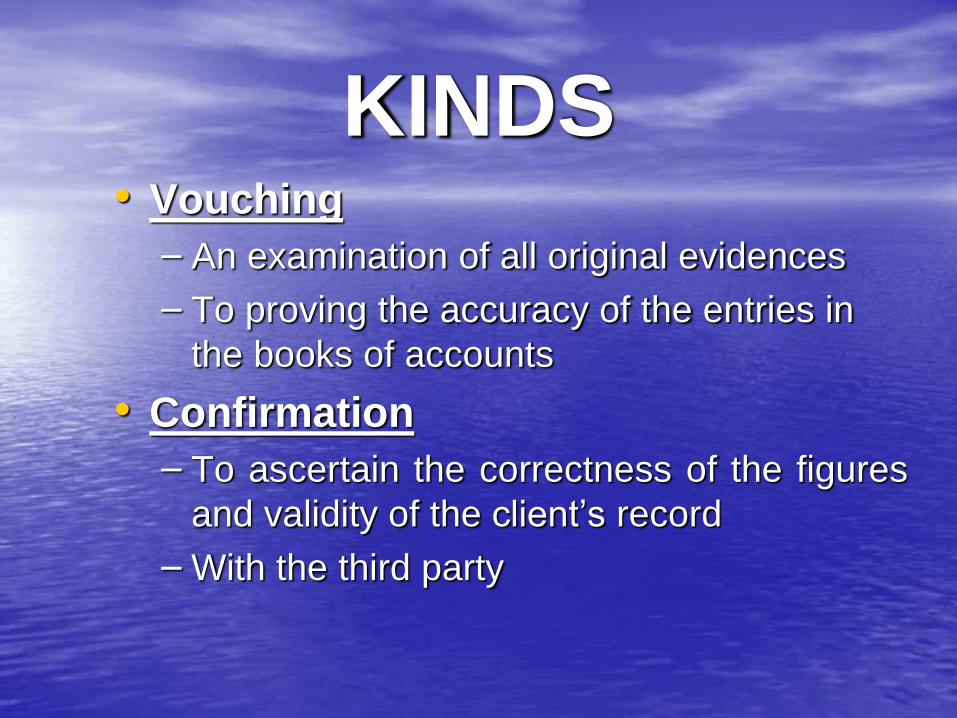

KINDS• Vouching

– An examination of all original evidences

– To proving the accuracy of the entries in

the books of accounts

• Confirmation

– To ascertain the correctness of the figures

and validity of the client’s record

–With the third party

KINDS• Testing

–Selection of representative items from

the records and examining them for

reaching on conclusion about the

trend

• Analysis of Financial Statement

–Uses various Financial Ratios

horizontally and vertically

KINDS• Physical Examination

– Includes inspection, counting,

identification and measurement of

quantity

–May observe the process of

stocktaking

• Reconciliation

–Reconcile two or more related items if

they are not agree or match with each

other

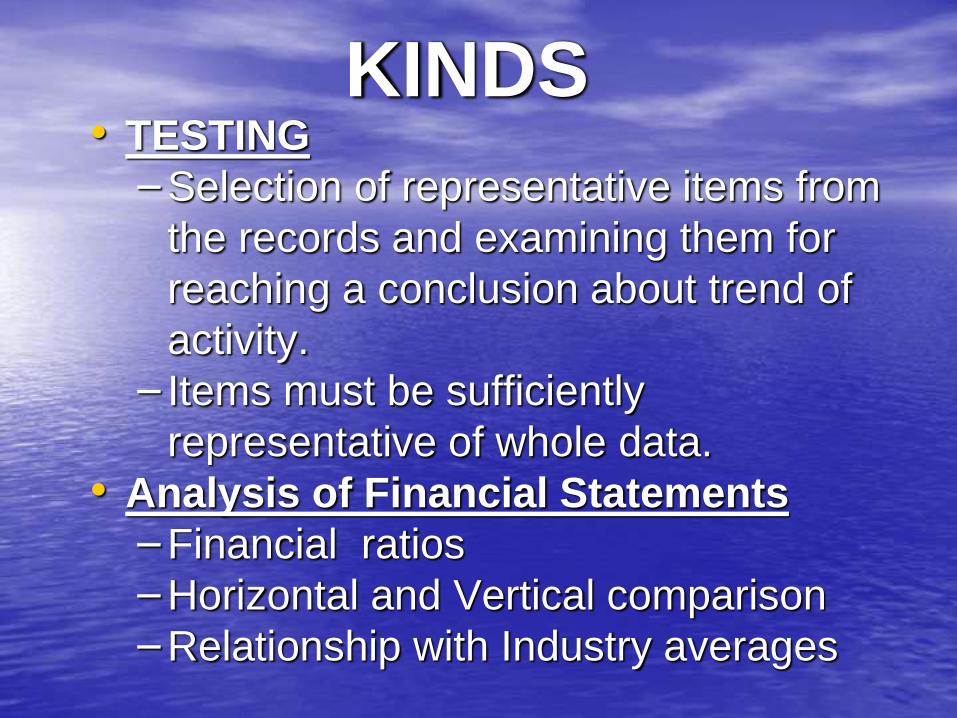

KINDS• TESTING

–Selection of representative items from

the records and examining them for

reaching a conclusion about trend of

activity.

– Items must be sufficiently

representative of whole data.

• Analysis of Financial Statements

–Financial ratios

–Horizontal and Vertical comparison

–Relationship with Industry averages

KINDS• Documentary Examination

–Same as Vouching in nature

–To examine the adequacy and

reliability

• Scanning

–Make a wide search to find out which

of the entries are regular, consistent

and logical

KINDS

• Observation

–Observe the various policies and

procedures or plans followed by the

client

• Flow Charting

–To describe graphically the issue of

transactions through different stages

KINDS• Inspection

–Arrange an inspection of the client’s

office, plant, branches etc.

–To obtain the understanding of plant

layout, manufacturing processes,

product, control and safeguard of

inventories etc.

–Should inspect before examination and

review

OTHERS• Enquiry

• Computation

• Management Representation

• Sampling Techniques

• Compliance Techniques

• Substantive Testing

• Analytical Review

• Computer Assisted Accounting Techniques

Obtaining Management

Representation

• Important evidence in form of

– summary of oral discussions with

management

–Written representation from management

• Should be addressed to the auditor

contain Specified information

• Its procedure must be agreed with client

in early stage of audit.

Audit sampling techniques

• Audit sampling technique is the application

of a compliance or substantive procedure

to less than 100% of the items within an

account or class of transaction to enable

the auditor to obtain and evaluate

evidence of some characteristics of the

entire class and enable the auditor to form

a conclusion concerning the whole class.

Design of the sample

• Audit objectives

• Population

• Risk and assurance

• Tolerable errors

• Expecting errors in the population

• Sratification

Evaluation of the sample

• Analyse any errors detected in the sample

• Project the errors found in the sample to

the population

• Assess the sampling

Compliance test

• Compliance tests are the proceduers

desugned to obtain reasonable assurance

of the internal control, that it is effective

and reliable

• These tests include procedures requiring

inspections of documents suporting

transactions to gain evidence that control

have operated properly.

Substantive test

• Substantive tests are those tests of

transactions and balances and other

procedures which privides audit evidence

as to the completeness, accuracy and

validity of the information contain in the

accounting records or in the financial

statements., like analytical review

Methods of substantive test:

1. Inspection of the documents

2. Inspection of assets

3. Direct confirmations

4. Reperformance of

computations