2c the funding pick n' mix

TRANSCRIPT

Nov-14©LCVS 1

“The Funding Pick n’ Mix”

Ged Simpson

Capacity Building Manager

LCVS

Nov-14©LCVS 2

Whilst every effort has been

made to ensure accuracy,

Liverpool Charity and Voluntary

Services accept no liability for

any loss suffered as a result of

following any advice contained

in this document.

Nov-14©LCVS 3

“Today I will solve all your

funding problems in 45 mins…

…and have time for questions”

“Yeah, whatever !”

Nov-14©LCVS 4

Let’s start with some more realistic

truths….we will look at

• Some current messages you hear

• Where are you now?

• Types of income – pros and cons

• Next steps

Nov-14©LCVS 5

Confusing messages?

“Well they all need to become social enterprises”

“As the state contracts there will be more opportunities for

contracts with local and central government”

“We need to seek more donations and legacies”

“You can’t keep relying on grants”

“Just follow a sustainable business model like the private sector”

“Can’t you merge and cut your costs?”

Nov-14©LCVS 6

Social Entrepreneur or charity worker ?

Social entrepreneur :“a person who establishes an enterprise with the aim of solving social

problems or effecting social change” (Oxford Dictionary)

Charity worker………………..any different ?

Nov-14©LCVS 7

A quick snapshot

Nov-14©LCVS 8

Funding of VCF Sector - National Trends

• 11.1 billion in contracts and received £2.6 billion in grants in

2011/12.

• 80% of the government funding now in the form of contracts

for delivering services rather than grants to support their

work, compared to 49% in 2000/01.

• Grant income has fallen in real terms, and this has been most

pronounced in grants from local government. Those grants

decreased in real terms by 53%

Nov-14©LCVS 9

National trends

Grant income from central government over the same period fell

by only 4%, to £1.7billion.

Nov-14©LCVS 10

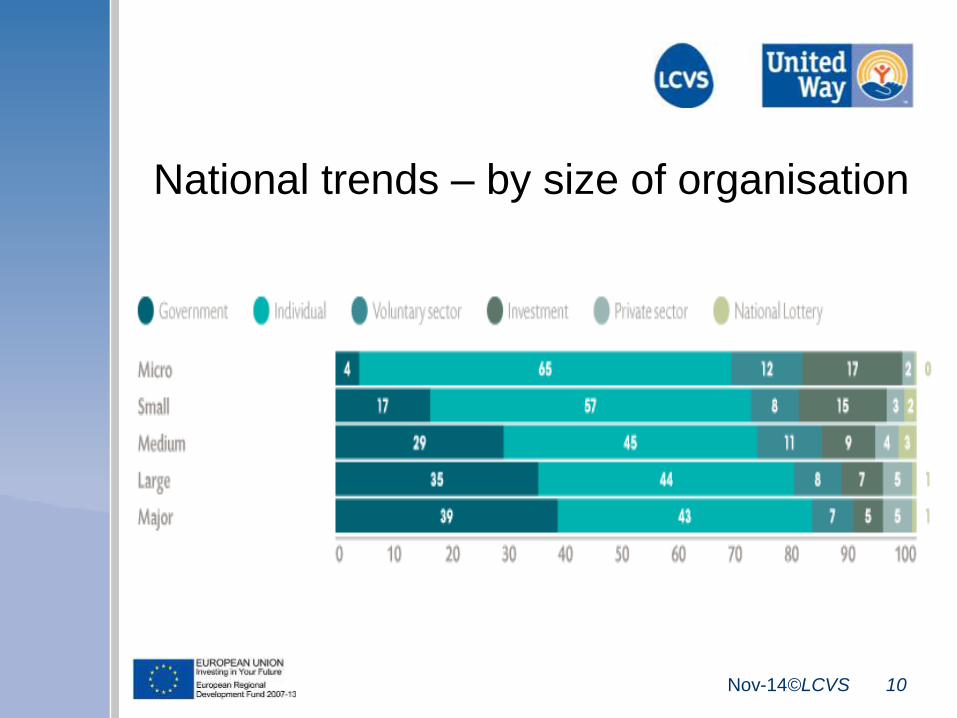

National trends – by size of organisation

Nov-14©LCVS 11

65%

proportion of micro organisations’

income from individuals’ donations

Source : NCVO UK Civil Society Almanac and NCVO/ The Third Sector Research Centre

Nov-14©LCVS 12

Your partners/competitors views93% of fundraisers reported that the climate has got tougher over the

last twelve months

58% of charities reported Government measures had a negative impact

on levels of funding

50% had taken steps to reduce wages and salary costs

85% were exploring new fundraising options

21% had merged or were considering merging

63% are considering or planning to draw on reserves

67% of respondents reporting an increase in demand 2012 and 72%

expecting a higher demand for services in 2013

Donor attrition has improved since last year. 14% fewer charities

reported an increase in attrition

55% had increased trading or social enterprise activity since the start of

the downturn Institute of Fundraising/the Charity Finance Group

Nov-14©LCVS 13

Diversity of income

– an old old concept ?

What’s out there ?

• Gifts

• Grants

• Contracts

• Open market

Nov-14©LCVS 14

Gifts

Donor relationship ?

Gifts made to further the mission of the organisation.

e.g. community fundraising, individual giving, regular

donations, philanthropy, corporate support, legacies and

much more.

Often this income is unrestricted, as the donor trusts the

organisation to use the money to achieve its aims

Nov-14©LCVS 15

Grants

Funder relationship ?

Restricted funding to deliver specified outputs or mutually

agreed outcomes.

Most often there is an application process,

The funder has clear expectations about what will be

achieved and they will monitor how the grant is used.

Nov-14©LCVS 16

Contracts

Purchaser relationship ?

Payment for provision of products or services according to

agreed terms with a third party purchaser from the public,

private or voluntary sectors.

There is usually a competitive tendering process at the start

and contract management throughout to check that the

objectives are being achieved.

Nov-14©LCVS 17

Open market

Customer relationship?

Selling products or services to customers, not as part of a

long-term structured contract.

The open market includes trading and enterprise activity such

as providing education, training, paid-for advice, selling

publications or other retail.

Trading can directly further the organisation’s mission or can

be purely to generate profit. Any surplus income is

unrestricted.

Nov-14©LCVS 18

Gifts

• Opportunities

• Challenges

• The way in

Nov-14©LCVS 19

Grants

• Opportunities

• Challenges or barriers

• The way in

Nov-14©LCVS 20

Contracts

• Opportunities

• Challenges or barriers

• The way in

Google : The Chest

Nov-14©LCVS 21

Open Market

• Opportunities

• Challenges or barriers

• The way in

Nov-14©LCVS 22

Conclusions – by way of clichés!

“Eggs all in one basket”

Not the wisest – crisis to crisis

“Horses for courses”

Not every income source works for every organisation but others can surprise

you

“In my day…..”

Was there a golden age of funding ?

“It’ll change once this lot are out…………”

Not getting into that debate but will it ?

“Ummm………may have a look at that”

Have you explored what possibilities there are?

Nov-14©LCVS 23

LCVS Capacity Building Team

0151 227 5177

www.lcvs.org.uk