2017 final annual report - easternbank.comreserve bank of boston. 5. ernst & young llp 200...

TRANSCRIPT

'(-(+*,*-0.+#&*00*.#

#)'(*#PCN#C#MFDKME#QFCM#GKM#/CNOFMJ#HJ#ICJQ#MFNLFDON&#C\Y#UL[#PUJVTL#YLHJOLK#HU#HSS+[PTL#OPNO#VM#'53,4#TPSSPVU*#HSTVZ[#1-#WLYJLU[#OPNOLY#

[OHU#[OH[#NLULYH[LK#PU#/-.3*#L_JLLKPUN#V\Y#WYL]PV\Z#YLJVYK#PU#/-..,#FV[HS#HZZL[Z#]H\S[LK#WHZ[#[OL#'.-#IPSSPVU#THYR#HUK#LUKLK#[OL#`LHY#

Q\Z[#ZO`#VM#'..#IPSSPVU,##

@VHUZ*#KLWVZP[Z#HUK#JHWP[HS#SL]LSZ#HSZV#HSS#ZL[#YLJVYK#OPNOZ#^P[O#SVHUZ#LUKPUN#[OL#`LHY#H[#'5,/#IPSSPVU#VY#4#WLYJLU[#HIV]L#/-.37#KLWVZP[Z#

^LYL#'5,5#IPSSPVU*#\W#5#WLYJLU[#MYVT#/-.37#HUK#JHWP[HS#L_JLLKLK#'.,0#IPSSPVU*#VY#3#WLYJLU[#HIV]L#/-.3#SL]LSZ,#C\Y#SVHU#JYLKP[#X\HSP[`#YL+

THPULK#Z[LSSHY#^P[O#]LY`#SV^#SVHU#SVZZLZ#VM#,-/#WLYJLU[#HUK#UVU+WLYMVYTPUN#HZZL[Z#ILSV^#'/-#TPSSPVU*#SLHKPUN#TLHZ\YLZ#HTVUN#IV[O#

UH[PVUHS#HUK#SVJHS#IHURZ,##

=HZ[LYU#[VVR#HK]HU[HNL#VM#YPZPUN#PU[LYLZ[#YH[LZ#HUK#H#]LY`#Z[YVUN#SVJHS#LJVUVT`#[V#NLULYH[L#[O5D5 C53@C4 C5DF=EDO /85 3@>A1?JPD ?5E

PU[LYLZ[#PUJVTL#([OL#KPMMLYLUJL#IL[^LLU#PU[LYLZ[#LHYULK#VU#SVHUZ#HUK#PU]LZ[TLU[Z#SLZZ#PU[LYLZ[#WHPK#VU#KLWVZP[Z#HUK#V[OLY#M\UKPUN#

ZV\YJLZ)#^HZ#'005,2#TPSSPVU*#VY#'11,6#TPSSPVU#HIV]L#/-.3*#HZ#OPNOLY#PU[LYLZ[#YH[LZ#VU#SVHUZ#HUK#PU]LZ[TLU[Z#L_JLLKLK#OPNOLY#JVZ[Z#VU#

KLWVZP[Z#HUK#V[OLY#M\UKPUN,#C\Y#UL[#PU[LYLZ[#THYNPU#PTWYV]LK#[V#0,32#WLYJLU[#MYVT#0,00#WLYJLU[#PU#/-.3#HUK#^HZ#PU#[OL#[VW#.2#WLYJLU[#VM#

V\Y#ZLSLJ[LK#WLLY#NYV\W,##

8S[OV\NO#^L#OHK#Z[YVUN#SLUKPUN#]VS\TLZ#PU#HSS#V\Y#I\ZPULZZLZ*#V\Y#;VTTLYJPHS#9HURPUN#>YV\W#OHK#HU#L_JLW[PVUHS#`LHY#HZ#JVTTLYJPHS#

SVHUZ#PUJYLHZLK#MYVT#'2,-#IPSSPVU#[V#'2,1#IPSSPVU*#VY#5#WLYJLU[,#C\Y#JVTTP[TLU[#[V#ETHSS#9\ZPULZZ#YLTHPUZ#HZ#Z[YVUN#HZ#L]LY*#^P[O#SVHU#

NYV^[O#VM#.0#WLYJLU[*#HUK#^L#^LYL#VUJL#HNHPU#YHURLK#[OL#&.#E98#SLUKLY#PU#BL^#=UNSHUK,##

AHU`#VM#V\Y#V[OLY#I\ZPULZZLZ#OHK#]LY`#Z\JJLZZM\S#`LHYZ#HZ#^LSS,#FV[HS#WYLTP\TZ#^YP[[LU#I`#=HZ[LYU#?UZ\YHUJL#>YV\W#L_JLLKLK#'.#IPSSPVU#

MVY#[OL#MPYZ[#[PTL*#YLZ\S[PUN#PU#YLJVYK#YL]LU\LZ#VM#V]LY#'5-#TPSSPVU*#\W#./#WLYJLU[#MYVT#/-.3*#Z\WWVY[LK#I`#[^V#PUZ\YHUJL#HNLUJ`#

HJX\PZP[PVUZ#JVTWSL[LK#K\YPUN#/-.4,#=HZ[LYU#GLHS[O#AHUHNLTLU[#ZH^#PU]LZ[TLU[#THUHNLTLU[#MLLZ#PUJYLHZL#5#WLYJLU[#[V#'.4,3#TPSSPVU,#

C\Y#YL[HPS#I\ZPULZZLZ*#IV[O#JVUZ\TLY#SLUKPUN#HUK#V\Y#IYHUJO+IHZLK#KLWVZP[#NYV\WZ*#OHK#V\[Z[HUKPUN#`LHYZ#HZ#^LSS,##

GL#SL]LYHNLK#V\Y#L_PZ[PUN#WSH[MVYTZ#[V#NLULYH[L#[OLZL#NYLH[#YLZ\S[Z#^P[O#L_WLUZLZ#VM#'056,1#TPSSPVU*#^OPJO#^HZ#\W#3#WLYJLU[#MYVT#/-.3,#

GL#HYL#Z[HY[PUN#[V#L_WLYPLUJL#ILULMP[Z#MYVT#THU`#VM#V\Y#PU]LZ[TLU[Z#PU#[LJOUVSVN`#HUK#WLVWSL#V]LY#[OL#SHZ[#ML^#`LHYZ,#GL#OHK#H#

Z\JJLZZM\S#YVSS#V\[#VM#UL^#VUSPUL#TVIPSL#WYVK\J[Z*#UL^#JVTTLYJPHS#HUK#JVUZ\TLY#SLUKPUN#VYPNPUH[PVU#Z`Z[LTZ*#HUK#TVYL#ZVWOPZ[PJH[LK#

KH[H#HUHS`[PJZ#[OH[#^PSS#HSSV^#\Z#[V#JVTWS`#^P[O#Z[YLZZ#[LZ[PUN#HUK#YLN\SH[VY`#YLX\PYLTLU[Z#UV^#[OH[#^L#L_JLLK#'.-#IPSSPVU#PU#HZZL[Z,##

FOLZL#YLJVYK#YLZ\S[Z#^LYL#PU#ZWP[L#VM#H#OPNOLY#[H_#JOHYNL#VM#HWWYV_PTH[LS`#'4,/#TPSSPVU#[V#JVTWS`#^P[O#[OL#FH_#DLMVYT#8J[#LUHJ[LK#PU#

<LJLTILY#/-.4,#GL#L_WLJ[#[OL#FH_#DLMVYT#8J[#[V#SV^LY#V\Y#M\[\YL#[H_#YH[L#HUK#HKK#[V#LHYUPUNZ#PU#/-.5#HUK#IL`VUK,##

8Z#H#T\[\HS#PUZ[P[\[PVU*#V\Y#JHWP[HS#IHZL#PZ#JYP[PJHS#[V#V\Y#OLHS[O#HUK#M\[\YL#Z\JJLZZ,#GL#HKKLK#'42,3#TPSSPVU#[OYV\NO#YL[HPULK#LHYUPUNZ#PU#

/-.4#HUK#LUKLK#[OL#`LHY#^P[O#V]LY#'.,0#IPSSPVU#PU#JHWP[HS,#C\Y#JHWP[HS#YH[PVZ#MHY#L_JLLK#[OL#IHUR#YLN\SH[VY`#TPUPT\TZ#HUK#^L#TLL[#[OL#

QH5==+31A9E1=9K54R DE1?41C4D D5E 2J @FC C57F=1E@CDO (? 1449E9@?M @FC 21=1?35 D855E 9D 5IEC5>5=J DEC@?7 H9E8 5I35==5?E =@1? BF1=9EJM#HTWSL#

SPX\PKP[`#HUK#YVI\Z[#JHWP[HS#SL]LSZ,##

GL#^LYL#]LY`#WSLHZLK#^P[O#[OLZL#YLJVYK#YLZ\S[Z#PU#/-.4#HUK#^V\SK#SPRL#[V#[OHUR#V\Y#V]LY#.*6--#=HZ[LYU#JVSSLHN\LZ#MVY#THRPUN#[OLT#

OHWWLU,#GL#ILSPL]L#^L#HYL#^LSS#WVZP[PVULK#MVY#JVU[PU\LK#Z\JJLZZ#HUK#SVVR#MVY^HYK#[V#HJOPL]PUN#UL^#OPNOZ#PU#/-.5,#

# # # # # #

<9,/<>#0&#<3@/<=# # # # ./,9<+2#-+-5=98#

)728>#2<4#)7856#+C53A@8B5#/66835Y# # # -524#*8>53@=>#

#

# # # # #

;?38-A#6᳆/<# # # # 4+7/=#,>B1/<+6.#

1835#)728>#2<4#0>5?845<@# # # # 1835#)728>'#)7856#,8<2<3829#/66835>#&#)7856#(4;8<8?@>2@8B5#/66835>#

# # # # #

# # # # ##

2

Financial Highlights #

December 31 (Dollars in thousands) 2017 2016 2015 2014 ## ## 2013

Balance Sheet Data Total assets $ 10,873,073 $ 9,801,109 $ 9,588,786 $ 9,447,895 $ 8,662,265 Securities and short-term

investments 1,766,213 1,284,080 1,651,562 1,892,865 2,649,731 Residential loans 1,290,461 1,153,735 1,041,072 1,032,066 923,231 Consumer loans 1,548,287 1,539,534 1,607,804 1,587,400 1,343,702 Commercial loans and

leases 5,388,293 5,011,862 4,482,592 4,148,394 3,002,543 Total loans and leases 8,227,041 7,705,131 7,131,468 6,767,860 5,269,476 Total deposits 8,815,452 8,188,950 8,133,730 7,802,133 7,058,794 Repurchase agreements - - - 268,189 243,603 Total retained earnings 1,330,514 1,254,927 1,205,014 1,143,256 1,112,413

Average total assets 10,391,796 9,913,145 9,667,907 8,927,931 8,540,635 Average earning assets 9,566,544 9,077,633 8,871,112 8,205,256 7,854,060 Average total deposits 8,684,043 8,416,777 8,031,975 7,282,736 6,938,013

Operating Data Net interest income $ 338,514 $ 293,574 $ 274,977 $ 234,588 $ 219,907

Provision for credit losses 5,800 7,900 (325) 1,750 (6,500)Noninterest income 197,727 169,128 153,007 147,382 149,436 Noninterest expense 389,413 367,643 333,695 298,131 284,594 Income before income

taxes 141,028 87,159 94,614 82,089 91,249 Net income 86,697 62,714 62,564 55,050 61,502

Other Data Return on average assets 0.83% 0.63% 0.65% 0.62% 0.72%Return on average equity 6.62% 5.06% 5.33% 4.78% 5.76%Net interest margin (FTE) 3.65% 3.33% 3.17% 2.93% 2.86%Equity to assets ratio 12.24% 12.80% 12.57% 12.06% 12.84%

#

#

#

#

3

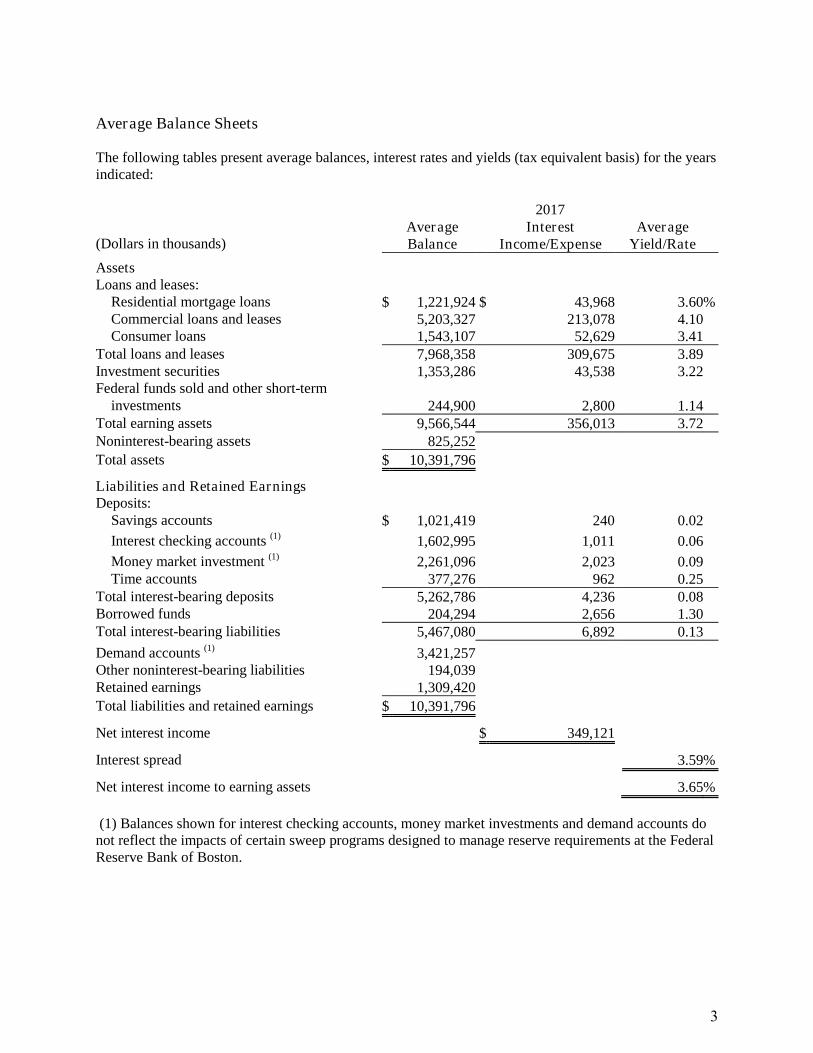

Average Balance Sheets

The following tables present average balances, interest rates and yields (tax equivalent basis) for the years indicated: #

2017 Average Interest Average

(Dollars in thousands) Balance Income/Expense Yield/Rate

Assets Loans and leases:

Residential mortgage loans $ 1,221,924 $ 43,968 3.60%Commercial loans and leases 5,203,327 213,078 4.10Consumer loans 1,543,107 52,629 3.41

Total loans and leases 7,968,358 309,675 3.89Investment securities 1,353,286 43,538 3.22Federal funds sold and other short-term

investments 244,900 2,800 1.14Total earning assets 9,566,544 356,013 3.72Noninterest-bearing assets 825,252

Total assets $ 10,391,796

Liabilities and Retained Earnings Deposits:

Savings accounts $ 1,021,419 240 0.02

Interest checking accounts (1) 1,602,995 1,011 0.06

Money market investment (1) 2,261,096 2,023 0.09Time accounts 377,276 962 0.25

Total interest-bearing deposits 5,262,786 4,236 0.08Borrowed funds 204,294 2,656 1.30Total interest-bearing liabilities 5,467,080 6,892 0.13

Demand accounts (1) 3,421,257Other noninterest-bearing liabilities 194,039Retained earnings 1,309,420

Total liabilities and retained earnings $ 10,391,796

Net interest income $ 349,121

Interest spread 3.59%

Net interest income to earning assets 3.65%

(1) Balances shown for interest checking accounts, money market investments and demand accounts do not reflect the impacts of certain sweep programs designed to manage reserve requirements at the Federal Reserve Bank of Boston.

#

4

2016

Average Interest Average

(Dollars in thousands) Balance Income/Expense Yield/Rate

Assets

Loans and leases:

Residential mortgage loans $ 1,096,417 $ 39,921 3.64%

Commercial loans and leases 4,725,676 182,597 3.86

Consumer loans 1,575,471 48,597 3.08

Total loans and leases 7,397,564 271,115 3.66

Investment securities 992,316 32,888 3.31

Federal funds sold and other short-term

investments 687,753 3,463 0.50

Total earning assets 9,077,633 307,466 3.39

Noninterest-bearing assets 835,512

Total assets $ 9,913,145

Liabilities and Retained Earnings

Deposits:

Savings accounts $ 956,936 453 0.05

Interest checking accounts (1) 1,473,303 474 0.03

Money market investment (1) 2,271,011 2,020 0.09

Time accounts 445,313 2,139 0.48

Total interest-bearing deposits 5,146,563 5,086 0.10

Borrowed funds 44,444 534 1.20

Total interest-bearing liabilities 5,191,007 5,620 0.11

Demand accounts (1) 3,270,214

Other noninterest-bearing liabilities 212,262

Retained earnings 1,239,662

Total liabilities and retained earnings $ 9,913,145

Net interest income $ 301,846

Interest spread 3.28%

Net interest income to earning assets 3.33%

#

(1) Balances shown for interest checking accounts, money market investments and demand accounts do not reflect the impacts of certain sweep programs designed to manage reserve requirements at the Federal Reserve Bank of Boston.

5

Ernst & Young LLP200 Clarendon StreetBoston, Massachusetts 02116-5072

Tel: + 1 617 266 2000Fax: + 1 617 266 5843www.ey.com

A member firm of Ernst & Young Global Limited

Report of Independent Auditors

The Board of DirectorsEastern Bank Corporation

We have audited the accompanying consolidated financial statements of Eastern Bank Corporation,which comprise the consolidated balance sheets as of December 31, 2017 and 2016, and the relatedconsolidated statements of income, comprehensive income, changes in retained earnings and cash flowsfor the years then ended, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial StatementsManagement is responsible for the preparation and fair presentation of these financial statements inconformity with U.S. generally accepted accounting principles; this includes the design,implementation and maintenance of internal control relevant to the preparation and fair presentation offinancial statements that are free of material misstatement, whether due to fraud or error.

Auditor’s ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audits. Weconducted our audits in accordance with auditing standards generally accepted in the United States.Those standards require that we plan and perform the audit to obtain reasonable assurance aboutwhether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosuresin the financial statements. The procedures selected depend on the auditor’s judgment, including theassessment of the risks of material misstatement of the financial statements, whether due to fraud orerror. In making those risk assessments, the auditor considers internal control relevant to the entity’spreparation and fair presentation of the financial statements in order to design audit procedures that areappropriate in the circumstances. An audit also includes evaluating the appropriateness of accountingpolicies used and the reasonableness of significant accounting estimates made by management, as wellas evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour audit opinion.

66

A member firm of Ernst & Young Global Limited

OpinionIn our opinion, the financial statements referred to above present fairly, in all material respects, theconsolidated financial position of Eastern Bank Corporation at December 31, 2017 and 2016, and theconsolidated results of its operations and its cash flows for the years then ended in conformity withU.S. generally accepted accounting principles.

February 23, 2018

77

Eastern Bank Corporation

Consolidated Balance Sheets

AssetsCash and due from banks $ 96,541 $ 79,929Other short-term investments 214,612 24,821Cash and cash equivalents 311,153 104,750

Trading securities 46,791 51,663Securities available for sale 1,504,810 1,207,596Loans held for sale 2,354 2,038Loans and leases, net of allowance for credit losses of$74,111 in 2017 and $70,188 in 2016 8,153,986 7,635,838

Federal Home Loan Bank stock, at cost 24,270 15,342Premises and equipment 73,725 75,125Bank-owned life insurance 76,161 73,834Goodwill and other intangibles, net 373,042 362,980Deferred income taxes, net 28,205 69,757Rabbi trust assets 70,924 70,930Other assets 207,652 131,256Total assets $ 10,873,073 $ 9,801,109

Liabilities and retained earningsLiabilities:Deposits:Demand $ 358,817 $ 376,686Savings 1,033,520 978,947Interest checking 270,030 133,274Money market investment 6,777,091 6,326,432Time 294,713 339,666Time - $250,000 and over 81,281 33,945

Total deposits 8,815,452 8,188,950

Borrowed funds 526,505 154,331Other liabilities 200,602 202,901Total liabilities 9,542,559 8,546,182

Retained earnings 1,379,006 1,292,309Accumulated other comprehensive income, net of tax:Unrealized appreciation on securities available for sale 9,212 4,971Funded status of defined benefit postretirement plans (57,704) (42,353)

Total retained earnings 1,330,514 1,254,927Total liabilities and retained earnings $ 10,873,073 $ 9,801,109

See accompanying notes.

December 312017 2016

(In Thousands)

8

Eastern Bank Corporation

Consolidated Statements of Income

Interest and dividend income:

Loans, including fees $ 304,601 $ 266,895

Trading securities 748 853

Taxable securities available for sale 28,157 21,718

Tax-exempt securities available for sale 9,100 6,265Federal funds sold and other short-term investments 2,800 3,463

Total interest and dividend income 345,406 299,194

Interest expense:

Deposits 4,236 5,086Borrowed funds 2,656 534

Total interest expense 6,892 5,620

Net interest income 338,514 293,574Provision for allowance for credit losses 5,800 7,900

Net interest income after provision for credit losses 332,714 285,674

Noninterest income:

Insurance commissions 83,147 74,369

Service charges on deposit accounts 26,677 24,456

Debit card processing fees 20,173 19,282Trust and investment advisory fees 17,642 16,262

Interest rate swap income 4,380 7,734

Income from investments held in rabbi trusts 6,587 2,161Trading securities gains, net 2,235 2,085

Net gain on sales of mortgage loans held for sale 822 1,771

Gains on sales of securities available for sale, net 11,356 261

Gains on sales of other assets 6,075 2,698Other 18,633 18,049

Total noninterest income 197,727 169,128

Noninterest expense:

Salaries and employee benefits 229,315 222,323

Office occupancy and equipment 35,773 35,893Data processing 44,475 37,730

Professional services 13,253 13,956

Charitable contributions 8,701 7,012

Marketing 10,922 7,983

FDIC insurance 3,295 4,121Amortization of intangible assets 3,488 2,908

Other 40,191 35,717

Total noninterest expense 389,413 367,643

Income before income tax expense 141,028 87,159

Income tax expense 54,331 24,445

Net income $ 86,697 $ 62,714

See accompanying notes.

Year Ended December 312017 2016

(In Thousands)

9

Eastern Bank Corporation

Consolidated Statements of Comprehensive Income

#

#

#

#

#

#

#

#

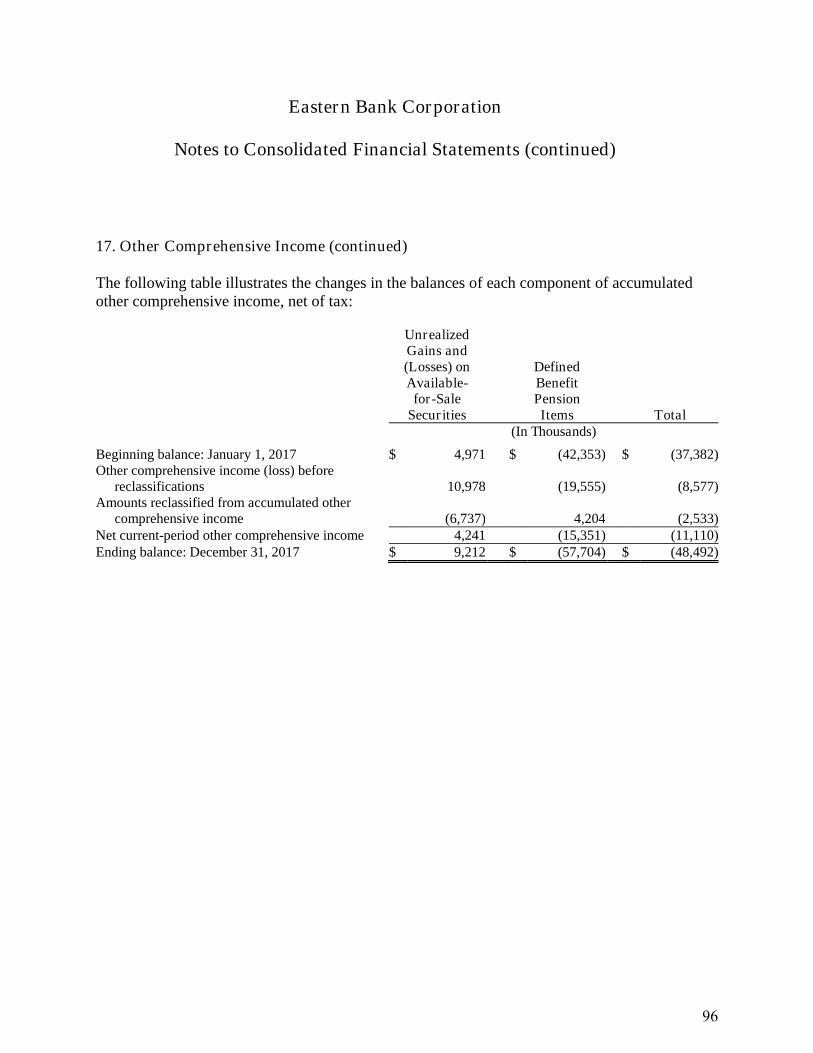

Net incomeOther comprehensive income, net of tax: $ 86,697 $ 62,714Unrealized gains (losses) on securities available for sale:Change in fair value of securities available for sale 10,978 (11,177)Less: reclassification adjustment for (gains) losses included in net income (6,737) (167)

Net change in fair value of securities available for sale 4,241 (11,344)Defined benefit pension plans:Amortization of actuarial net loss 4,172 3,280Change in actuarial net loss (19,555) (4,763)Amortization of prior service cost 32 26Net change in actuarial net loss (15,351) (1,457)

Total other comprehensive income (11,110) (12,801)Comprehensive income $ 75,587 $ 49,913

See accompanying notes.

Year Ended December 312017 2016

(In Thousands)

;

Eastern Bank Corporation

Consolidated Statements of Changes in Retained Earnings

#

Accumulated

OtherRetained ComprehensiveEarnings Income Total

Balance at December 31, 2015 $ 1,229,595 $ (24,581) $ 1,205,014

Net income 62,714 - 62,714Other comprehensive income, net of tax - (12,801) (12,801)Balance at December 31, 2016 1,292,309 (37,382) 1,254,927

Net income 86,697 - 86,697Other comprehensive income, net of tax - (11,110) (11,110)Balance at December 31, 2017 $ 1,379,006 $ (48,492) $ 1,330,514

See accompanying notes.

(In Thousands)

21

Eastern Bank Corporation

Consolidated Statements of Cash Flows

Operating activitiesNet income $ 86,697 $ 62,714 Adjustments to reconcile net income to net cash provided byoperating activities:Provision for allowance for credit losses 5,800 7,900 Depreciation 15,381 12,039 Amortization of intangible assets 3,488 2,908 Deferred income tax expense (benefit) 45,698 (3,461)Amortization of premiums, discounts, and fees, net 2,874 357 Increase in cash surrender value of bank-owned life insurance,net of benefit proceeds (2,327) (1,891)

Decrease in trading securities, net 4,872 9,387 Gain on sale of securities available for sale, net (11,356) (261)Net gain on sale of mortgage loans held for sale (822) (1,771)Net decrease in loans held for sale 506 19,960 (Increase) decrease in prepaid pension expense (69,875) 12,160 Other, net (30,097) (19,759)

Net cash provided by operating activities 50,839 100,282

Investing activitiesProceeds from sales of securities available for sale 83,501 6,728 Proceeds from maturities and principal paydowns of securitiesavailable for sale 185,919 171,295

Purchases of securities available for sale (552,217) (425,895)Proceeds from sale of Federal Home Loan Bank stock 5,538 3,256 Purchases of Federal Home Loan Bank stock (14,467) (8,050)Net increase in outstanding loans (524,052) (570,887)Acquisitions, net of cash and cash equivalents acquired (15,900) (2,648)Purchased bank-owned life insurance - (12)Proceeds from sale of other real estate owned, net of acquired 909 331 Proceeds from sale of premises held for sale 66 - Purchased banking premises and equipment, net (12,409) (9,949)Net cash used in investing activities (843,112) (835,831)

Financing activitiesNet increase in demand, savings, interest checking, and moneymarket investment deposit accounts 624,119 171,491

Net increase (decrease) in time deposits 2,383 (116,271)Net increase in borrowed funds 372,174 101,283 Net cash provided by financing activities 998,676 156,503

Net increase (decrease) in cash and cash equivalents 206,403 (579,046)Cash and cash equivalents at beginning of year 104,750 683,796

Cash and cash equivalents at end of year $ 311,153 $ 104,750

See accompanying notes.

Year Ended December 312017 2016

(In Thousands)

22

Eastern Bank Corporation Notes to Consolidated Financial Statements

December 31, 2017

1. Summary of Significant Accounting Policies

Nature of Operations

Eastern Bank Corporation (the Corporation) is a Massachusetts chartered mutual bank holding company. Through its wholly owned subsidiary, Eastern Bank (the Bank), the Corporation provides a variety of banking, trust and investment, and insurance services.

The activities of the Corporation and the Bank are subject to the regulatory supervision of the Federal Reserve Board and the Federal Deposit Insurance Corporation (FDIC), respectively. The Corporation is also subject to various Massachusetts business and banking regulations, and the Bank is also subject to various Massachusetts and New Hampshire business and banking regulations.

Basis of Presentation

The consolidated financial statements include the accounts of the Corporation, its wholly-owned subsidiaries and a consolidated tax credit investment company. All significant intercompany accounts and transactions have been eliminated in consolidation. The Corporation consolidates: wholly-owned subsidiaries; any variable interest entities (VIEs) where the Corporation or one of j^[ ?ehfehWj_ed{i m^ebbo-owned subsidiaries was determined to be the primary beneficiary of the VIE; and any voting interest entities (VOEs) where either the Corporation or a wholly-owned subsidiary is determined to have control of the VOE.

Certain previously reported amounts have been reclassified to conform to the current year presentation.

The accounting and reporting policies of the Corporation conform to accounting principles generally accepted in the United States (GAAP) and to the general practices of the banking industry. In preparing the consolidated financial statements, management is required to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the date of the balance sheet and revenues and expenses for the period. Actual results could differ from those estimates.

Material estimates that are particularly susceptible to change relate to the determination of the allowance for credit losses, valuation and fair value measurements, other-than-temporary impairment on investment securities, the liabilities for benefit obligations (particularly pensions) and the provision for income taxes.

23

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

The Corporation has evaluated subsequent events through February 23, 2018, which is the date that the consolidated financial statements were available to be issued.

Business Combinations

Acquisitions of businesses are accounted for using the acquisition method of accounting. Accordingly, the net assets of the companies acquired are recorded at their fair values at the date of acquisition. Goodwill represents the excess of purchase price over the fair value of net assets acquired. Other intangible assets represent acquired assets that lack physical substance, but can be distinguished from goodwill because of contractual or other legal rights, or because the asset is capable of being sold or exchanged either on its own, or in combination with a related contract, asset, or liability.

The Corporation evaluates goodwill for impairment on an annual basis or whenever there is an indicator of impairment. Other intangible assets are reviewed for impairment whenever there is an indicator of impairment, however, useful lives are evaluated annually. Any impairment losses are charged to earnings. The Corporation amortizes other intangible assets over their respective estimated useful lives. The estimated useful life of core deposit identifiable intangible assets fall within a range of seven to ten years and the estimated useful life of customer lists from insurance agency acquisitions is ten years. The estimated useful life of non-compete agreements resulting from insurance agency acquisitions are dependent upon the terms of the agreement. Intangible assets are stated at cost less accumulated amortization.

Cash and Cash Equivalents

Cash and cash equivalents include cash and due from banks, Federal funds sold, and other short-term investments, all of which mature within 90 days.

Securities

Debt and equity securities that are bought and held principally for the purpose of resale in the near term are classified as trading and reported at fair value, with unrealized gains and losses included in earnings.

24

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Debt and equity securities classified as available for sale are reported at fair value, with unrealized gains and losses reported as a separate component of other comprehensive income, net of tax.

Management evaluates impaired securities available for sale (e.g., those for which fair value is less than cost) for other-than-temporary impairment (OTTI) at least on a quarterly basis, and more frequently when economic or market concerns warrant such evaluation. Consideration is given to the length of time and the extent to which the fair value has been less than cost, current market conditions, the financial condition and near-term prospects of the issuer, performance of collateral underlying the securities, the ratings of the individual securities, the interest rate environment, the Corporation{s intent to sell the security or whether it is more likely than not that the Corporation will be required to sell the debt security before its anticipated recovery, as well as other qualitative factors.

Premiums and discounts on investments and mortgage-backed securities are amortized or accreted to income using the effective interest rate method. If a decline in fair value below the amortized cost basis of an investment is judged to be other than temporary, the investment is written down to fair value. The portion of the impairment related to credit losses is included in earnings, and the portion of the impairment related to other factors is included in other comprehensive income. Gains and losses on sales of investments are recognized at the time of sale on the specific-identification basis.

Loans

Loans are reported at their principal amount outstanding, net of deferred loan fees and any unearned discount or unamortized premium for acquired loans. Unearned discount and unamortized premium are accreted and amortized, respectively, to income on a basis that results in level rates of return over the terms of the loans. Origination fees and related direct incremental origination costs are offset, and the resulting net amount is deferred and amortized over the life of the related loans using the interest method, assuming a certain level of prepayments. When loans are sold or repaid, the unamortized fees and costs are recorded to income.

25

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

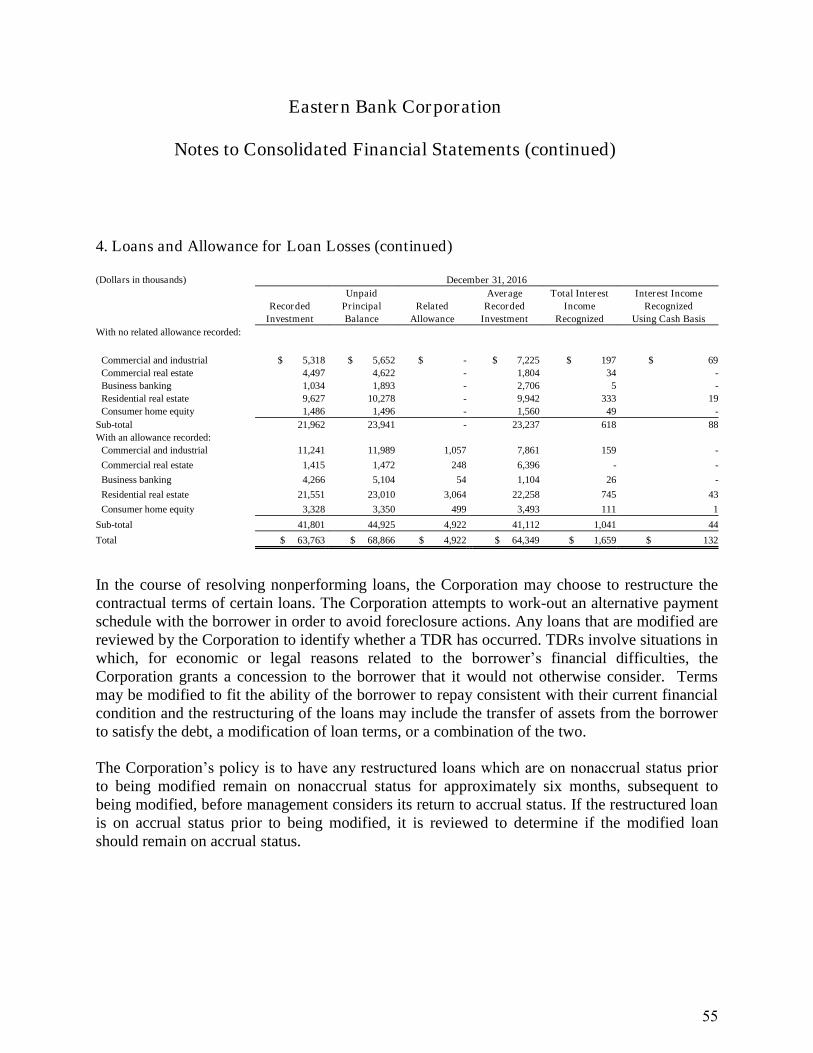

Interest accruals are generally discontinued when management has determined that the borrower may be unable to meet contractual obligations and/or when loans are 90 days or more in arrears, unless management believes that collateral held by the Corporation is clearly sufficient and full satisfaction of both principal and interest is highly probable or the loan is accounted for as a purchased credit-impaired loan. When a loan is placed on nonaccrual, all interest previously accrued but not collected is reversed against current period income and amortization of deferred loan fees is discontinued. Interest received on nonaccrual loans is either applied against principal or reported as income according to management{s judgment as to the collectability of principal. Nonaccrual loans may be returned to an accrual status when principal and interest payments are no longer delinquent, and the risk characteristics of the loan have improved to the extent that there no longer exists a concern as to the collectability of principal and interest. Loans are considered past due based upon the number of days delinquent according to their contractual terms.

Impaired loans consist of all loans for which management has determined it is probable the Corporation will be unable to collect all amounts due according to the contractual terms of the loan agreements. Factors considered by management in determining impairment include payment status, collateral value, and the probability of collecting scheduled principal and interest payments when due. The Corporation measures impairment of loans using a discounted cash flow method, the loan{s observable market price, or the fair value of the collateral if the loan is collateral dependent.

The Corporation periodically may agree to modify the contractual terms of loans. When a loan is modified and a concession is made to a borrower experiencing financial difficulty, the modification is considered a troubled debt restructuring (TDR). All TDR loans are considered impaired and therefore are subject to a specific review for impairment loss. The impairment analysis discounts the present value of the anticipated cash flows by the loan{s contractual rate of interest in effect prior to the loan{s modification or the fair value of collateral if the loan is collateral dependent. The amount of impairment loss, if any, is recorded as a specific loss allocation to each individual loan in the allowance for loan losses. Commercial loans (commercial and industrial, commercial real estate, commercial construction, and small business loans) and residential loans that have been classified as TDRs and which subsequently default are reviewed to determine if the loan should be deemed collateral dependent. In such an instance, any shortfall between the value of the collateral and the book value of the loan is determined by measuring the recorded investment in the loan against the fair value of the collateral less costs to sell.

26

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Acquired Loans

All acquired loans are recorded at fair value with no carryover of the allowance for loan losses. At acquisition, loans are also reviewed to determine if the loan has evidence of deterioration in credit quality since origination and for which it is probable, at acquisition, that all contractually required payments will not be collected. Such loans are deemed to be purchased credit impaired (PCI) loans. Under the accounting model for PCI loans, the excess of cash flows expected to be collected over the carrying amount of the loans, referred to as the xaccretable yieldy, is accreted into interest income over the life of the loans using the effective yield method. Accordingly, PCI loans are not subject to classification as nonaccrual in the same manner as originated loans. Rather, acquired loans are considered to be accruing loans because their interest income relates to the accretable yield recognized and not to contractual interest payments at the loan level. The difference between contractually required principal and interest payments and the cash flows expected to be collected, referred to as the xnonaccretable differencey, includes estimates of both the impact of prepayments and future credit losses expected to be incurred over the life of the loans.

The estimate of cash flows expected to be collected is regularly re-assessed subsequent to acquisition. These re-assessments involve updates, as necessary, of the key assumptions and estimates used in the initial estimate of fair value. Generally speaking, expected cash flows are affected by:

u Changes in the expected principal and interest payments over the estimated life wChanges in expected cash flows may be driven by the credit outlook and actions taken with borrowers. Changes in expected future cash flows resulting from loan modifications are included in the assessment of expected cash flows.

u Change in prepayment assumptions w Prepayments affect the estimated life of the loans, which may change the amount of interest income expected to be collected.

u Change in interest rate indices for variable rate loans w Expected future cash flows are based, as applicable, on the variable rates in effect at the time of the assessment of expected cash flows.

27

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

A decrease in expected cash flows in subsequent periods may indicate that the loan is impaired which would require the establishment of an allowance for loan losses by a charge to the provision for loan losses. An increase in expected cash flows in subsequent periods serves, first, to reduce any previously established allowance for loan losses by the increase in the present value of cash flows expected to be collected, and results in a recalculation of the amount of accretable yield for the loan. The adjustment of accretable yield due to an increase in expected cash flows is accounted for as a change in estimate. The additional cash flows expected to be collected are reclassified from the nonaccretable difference to the accretable yield, and the amount of periodic accretion is adjusted accordingly over the remaining life of the loans.

A PCI loan may be resolved either through receipt of payment (in full or in part) from the borrower, the sale of the loan to a third party, or foreclosure of the collateral. For PCI loans accounted for on an individual loan basis and resolved directly with the borrower, any amount received from resolution in excess of the carrying amount of the loan is recognized and reported within interest income.

A refinancing or modification of a PCI loan accounted for individually is assessed to determine whether the modification represents a TDR. If the loan is considered to be a TDR, it will be included in the total impaired loans reported by the Company. The loan will continue to recognize interest income based upon the excess of cash flows expected to be collected over the carrying amount of the loan.

Allowance for Credit Losses

The allowance for credit losses is established to provide for probable losses incurred in the Corporation{s loan portfolio at the balance sheet date and is established through a provision for credit losses charged to earnings. The allowance is based on management{s assessment of many factors, including the risk characteristics of the loan portfolio, current economic conditions, and trends in loan delinquencies and charge-offs. Charge-offs, net of recoveries, are charged directly to the allowance. Commercial and residential loans are charged-off in the period in which they are deemed uncollectible. Delinquent loans in these product types are subject to ongoing review and analysis to determine if a charge-off in the current period is appropriate. For consumer finance loans, policies and procedures exist that require charge-off consideration at various stages of delinquency depending on the product type. Other credit quality indicators are also considered, such as collateral position and adequacy.

28

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

The allowance for credit losses is evaluated on a regular basis by management. While management uses current information in establishing the allowance for losses, future adjustments to the allowance may be necessary if economic conditions or conditions relative to borrowers differ substantially from the assumptions used in making the evaluation. Management uses a methodology to systematically estimate the amount of credit loss incurred in the portfolio. Commercial real estate and commercial and industrial loans are evaluated using a loan rating system, historical losses and other factors which form the basis for estimating incurred losses. Portfolios of more homogeneous populations of loans, including residential mortgages and consumer loans, are analyzed as groups taking into account delinquency ratios, historical loss experience and charge-offs.

The allowance consists of specific and general components. The specific component consists of reserves for impaired loans (defined as those where management has determined it is probable it will not collect all payments when due), typically classified as either doubtful or substandard. For impaired loans, an allowance is established when the discounted cash flows (or collateral value or observable market price) of the loan is lower than the carrying value of the loan. The general component covers non-impaired non-classified loans, and is based on historical loss experience adjusted for qualitative factors.

In the ordinary course of business, the Corporation enters into commitments to extend credit and standby letters of credit. Such financial instruments are recorded in the financial statements when they become payable. The credit risk associated with these commitments is evaluated in a manner similar to the allowance for loan losses. The reserve for unfunded lending commitments is included in other liabilities in the balance sheet.

Additionally, various regulatory agencies, as an integral part of j^[ ?ehfehWj_ed{i examination process, periodically assess the appropriateness of the allowance for loan losses and may require the Corporation to increase its provision for loan losses or recognize further loan charge-offs, in accordance with U.S. GAAP.

29

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Mortgage Banking Activities

Mortgage loans held for sale to the secondary market are carried at the lower of cost or estimated market value. The Corporation enters into commitments to fund residential mortgage loans with an offsetting forward commitment to sell them in the secondary markets in order to mitigate interest rate risk. Gains or losses on sales of mortgage loans are recognized at the time of sale. Interest income is recognized on loans held for sale between the time the loan is funded and the loan is sold. Direct loan origination costs and fees are deferred upon origination and are recognized on the date of sale.

Premises and Equipment Used in Operations

Land is carried at cost. Buildings, leasehold improvements and equipment are stated at cost less accumulated depreciation and amortization, computed principally on the straight-line method over the estimated useful lives of the related assets or the terms of the leases, if shorter.

Premises and Equipment Held for Sale

Banking premises and equipment held for sale are carried at the lower of cost or estimated fair value less costs to sell.

Retirement Plans

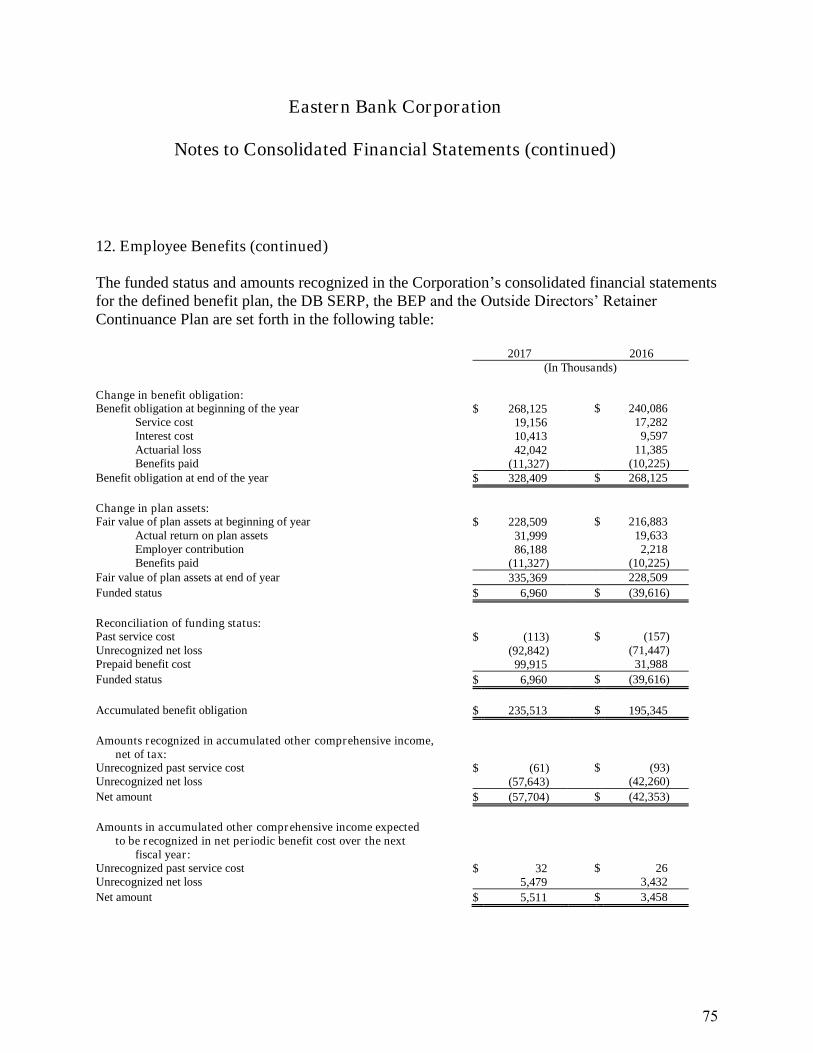

The Corporation provides pension benefits to its employees through various pension plans. At the measurement date, plan assets are determined based on fair value, generally representing observable market prices. The actuarial cost method used to compute the pension liabilities and related expense is the projected unit credit method. The projected benefit obligation is principally determined based on the present value of the projected benefit distributions at an assumed discount rate. The discount rate which is utilized is based on the investment yield of high quality corporate bonds available in the marketplace with maturities equal to projected cash flows of future benefit payments as of the measurement date. Periodic pension expense (or income) includes service costs, interest costs based on the assumed discount rate, the expected return on plan assets, if applicable, based on an actuarially derived market-related value and amortization of actuarial gains and losses. The overfunded or underfunded status of the plans is recorded as an asset or liability on the consolidated balance sheets, with changes in that status recognized through other comprehensive income, net of related taxes.

2;

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Variable Interest Entities and Voting Interest Entities

The Corporation is involved in the normal course of business with various types of special purpose entities, some of which meet the definition for VIEs and VOEs. The Corporation is required by GAAP to consolidate a VIE when the Corporation is deemed to be the primary beneficiary. This determination is evaluated periodically as facts and circumstances change.

A legal entity is referred to as a VIE if any of the following conditions exist: 1) the total equity investment at risk is insufficient to permit the legal entity to finance its activities without additional subordinated financial support from other parties; 2) as a group, the holders of the equity investment at risk lack any of the characteristics of a controlling financial interest; or 3) j^[ [gk_jo _dl[ijehi{ lej_d] h_]^ji Wh[ dej fhefehjional to the economics, and substantially all of the activities of the entity either involve or are conducted on behalf of an investor that has disproportionately few voting rights. The Corporation consolidates entities deemed to be VIEs when either the Corporation or a wholly-owned subsidiary is determined to be the primary beneficiary. The primary beneficiary analysis is a qualitative analysis based on power and benefits. An enterprise has a controlling financial interest in a VIE if it has both power and benefits w that is, it has 1) the power to direct the activities of a VIE that most significantly impact the VIEs economic performance (power); and 2) the obligation to absorb losses of the VIE that potentially could be significant to the VIE and/or the right to receive benefits from the VIE that potentially could be significant to the VIE (benefits).

Under GAAP, investments in limited partnerships and similar entities that are not VIEs should be evaluated for potential consolidation under the voting model. The Corporation consolidates VOEs when either the Corporation or a wholly-owned subsidiary is determined to have control of the VOE.

31

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Rabbi Trust VIE

The Corporation established a rabbi trust to meet its obligations under certain executive non-qualified retirement benefits and deferred compensation plans and to mitigate the expense volatility of the aforementioned retirement plans. The rabbi trust is considered a VIE as the equity investment at risk is insufficient to permit the trust to finance its activities without additional subordinated financial support from the Corporation. The Corporation is considered the primary beneficiary of the rabbi trust as it has the power to direct the activities of the rabbi jhkij j^Wj i_]d_\_YWdjbo W\\[Yj j^[ hWXX_ jhkij{i [Yedec_Y f[h\ehcWdY[ WdZ _j ^Wi j^[ eXb_]Wj_ed je absorb losses of the rabbi trust that could potentially be significant to the rabbi trust by virtue of its contingent call opt_edi ed j^[ hWXX_ jhkij{i Wii[ji _d j^[ [l[dj e\ j^[ ?ehfehWj_ed{i XWdahkfjYo. As the primary beneficiary of this VIE, the Corporation consolidates the rabbi trust investments, executive retirement benefits liabilities and deferred compensation plan liabilities. These rabbi trust investments consist primarily of cash and cash equivalents, U.S. government agency obligations, equity securities, mutual funds and other exchange-traded funds, and are recorded at fair value.

Tax Credit Investment VIE

A wholly-owned subsidiary of the Corporation is the sole member of a tax credit investment company through which it consolidates a community development entity (CDE) that is considered a VIE. The CDE is considered a VIE because as a group, the holders of the equity investment at risk lack any of the characteristics of a controlling financial interest. The tax credit investment company is considered the primary beneficiary of the CDE as it has the power to direct the activities of a VIE that most significantly impact the VIEs economic performance and the obligation to absorb losses of and the right to receive benefits from the VIE that potentially could be significant to the VIE.

Prior to the adoption of Accounting Standards Update (ASU) 2015-02, Consolidation, this company was considered as a voting interest entity (VOE). Due to changes in the VIE and VOE analyses prescribed in ASU 2015-02, this company is now deemed to be a VIE. There were no Y^Wd][i je j^[ ?ehfehWj_ed{i Yedieb_ZWj[Z \_dWdY_Wb fei_j_ed Wi W result in the change in classification as the tax credit investment company consolidated the VOE.

32

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Bank Owned Life Insurance

Primarily as a result of mergers and acquisitions, the Corporation holds life insurance on the lives of certain participating executives. The amount reported as an asset on the balance sheet is the sum of the cash surrender values reported to the Corporation by the various insurance carriers. Certain policies are split-dollar life insurance policies whereby the Corporation recognizes a liability for the postretirement benefit related to the arrangement. This postretirement benefit is included in other liabilities on the balance sheet.

Income Taxes

The Corporation accounts for income taxes under the asset and liability method. Under this method, deferred tax assets and liabilities are established for the temporary differences between the accounting basis and the tax basis of the Corporation{s assets and liabilities at enacted tax rates expected to be in effect when the amounts related to such temporary differences are realized or settled. Interest and penalties paid on the underpayment of income taxes are classified as income tax expense.

The Corporation periodically evaluates the sustainability of its tax positions as to whether it is more likely than not its position would be upheld upon examination by the appropriate taxing authority. A tax position that meets the more-likely-than-not recognition threshold is measured to determine the amount of benefit to recognize in the consolidated financial statements. The tax position is measured at the largest amount of benefit that is greater than 50% likely of being realized upon settlement.

Low Income Housing Tax Credits and Other Tax Credit Investments

As part of its community reinvestment initiatives, the Corporation invests in qualified affordable housing projects and other tax credit investment projects. The Corporation receives low-income housing tax credits, investment tax credits, rehabilitation tax credits and other tax credits as a result of its investments in these limited partnership investments.

33

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

The Corporation accounts for its investments in qualified affordable housing projects using the proportional amortization method and amortizes the initial cost of the investment in proportion to the tax credits and other tax benefits allocated to the Corporation. The amortization of the excess of the carrying amount of the investment over its estimated residual value is included as a component of income tax expense. At investment inception, the Corporation records a liability for the committed amount of the investment. This liability is reduced as contributions are made.

The Corporation evaluates investments in tax credit investment companies for consolidation based on the variable or voting interest entity guidance, as appropriate.

Other tax credit investment projects are accounted for using either the cost method or equity method.

Advertising Costs

All advertising costs are expensed in the period in which they are incurred.

Insurance Commissions

The Corporation acts as an agent in offering property, casualty and life and health insurance to both personal and commercial customers. Personal lines insurance products include life, accident and health, automobile, and property and liability insurance including fire, condominium, home and tenants, among others. Commercial insurance products include group life and health, commercial property and liability, surety, and workers compensation insurance, among others. The Corporation recognizes insurance commission revenues when earned based upon the effective date of the insurance policy.

Trust Operations

The Bank is a full-service trust company that provides a wide range of trust services to customers that includes managing customer investments, safekeeping customer assets, supplying disbursement services, and providing other fiduciary services. Trust assets held in a fiduciary or agency capacity for customers are not included in the accompanying consolidated balance sheets as they are not assets of the Corporation. Revenue from administrative and management activities associated with these assets is recorded on an accrual basis.

34

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

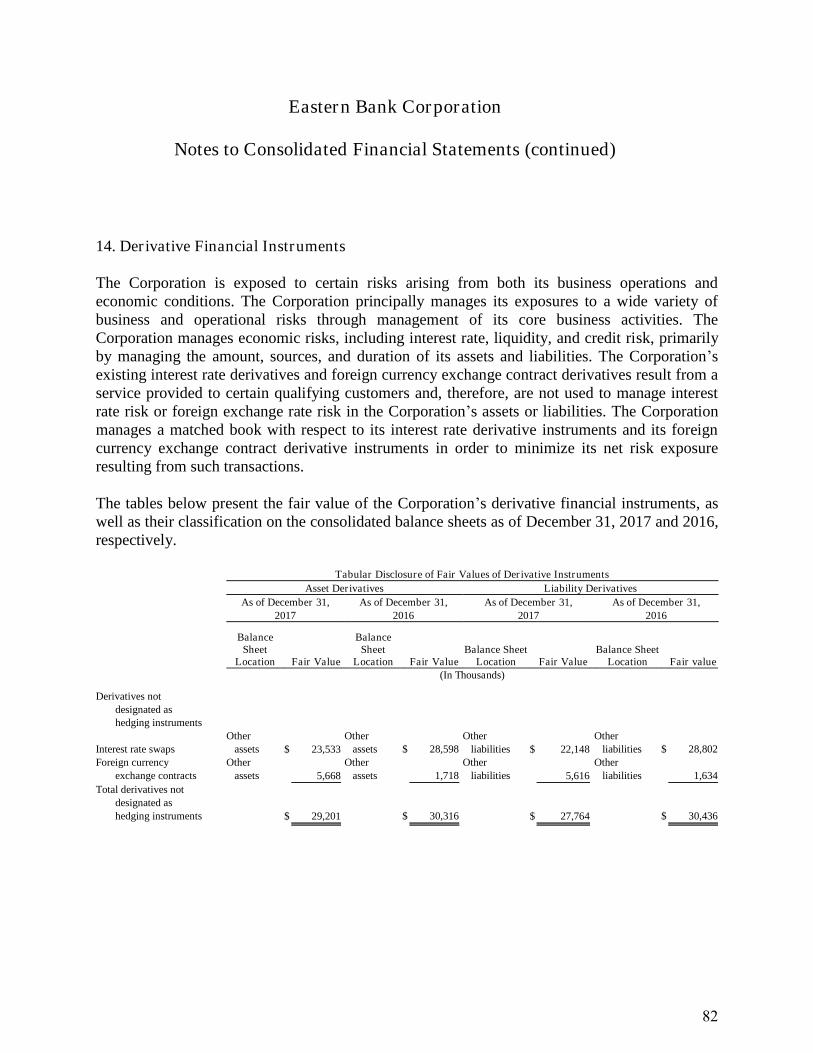

Derivative Financial Instruments

The Corporation enters into interest rate swap agreements to provide for the needs of its commercial customers. An interest rate swap is an agreement whereby one party agrees to pay a floating rate of interest on a notional principal amount in exchange for receiving a fixed rate of interest on the same notional amount for a predetermined period of time from a second party. The Corporation believes that its exposure to commercial customer derivatives is limited because these contracts are simultaneously matched at inception with an offsetting dealer transaction. The program allows the Corporation to retain variable rate commercial loans while allowing the commercial customer to synthetically fix the loan rate by entering into a variable to fixed rate interest rate swap. Exposure with respect to these derivatives is largely limited to nonperformance by either the customer or the dealer. These interest rate derivative instruments do not qualify for hedge accounting and are recorded on the consolidated balance sheets as either an asset or liability measured at fair value. All changes in fair value of these derivative instruments are included in other noninterest income.

The Corporation also enters into foreign currency forward exchange contracts to provide for the needs of its customers. These customer derivatives are offset with matching derivatives with correspondent bank counterparties in order to minimize foreign exchange rate risk to the Corporation. Exposure with respect to these derivatives is largely limited to nonperformance by either the customer or the other counterparty. These derivatives do not qualify for hedge accounting. As such, all changes in fair value are included in other noninterest income.

Fair Value Measurements

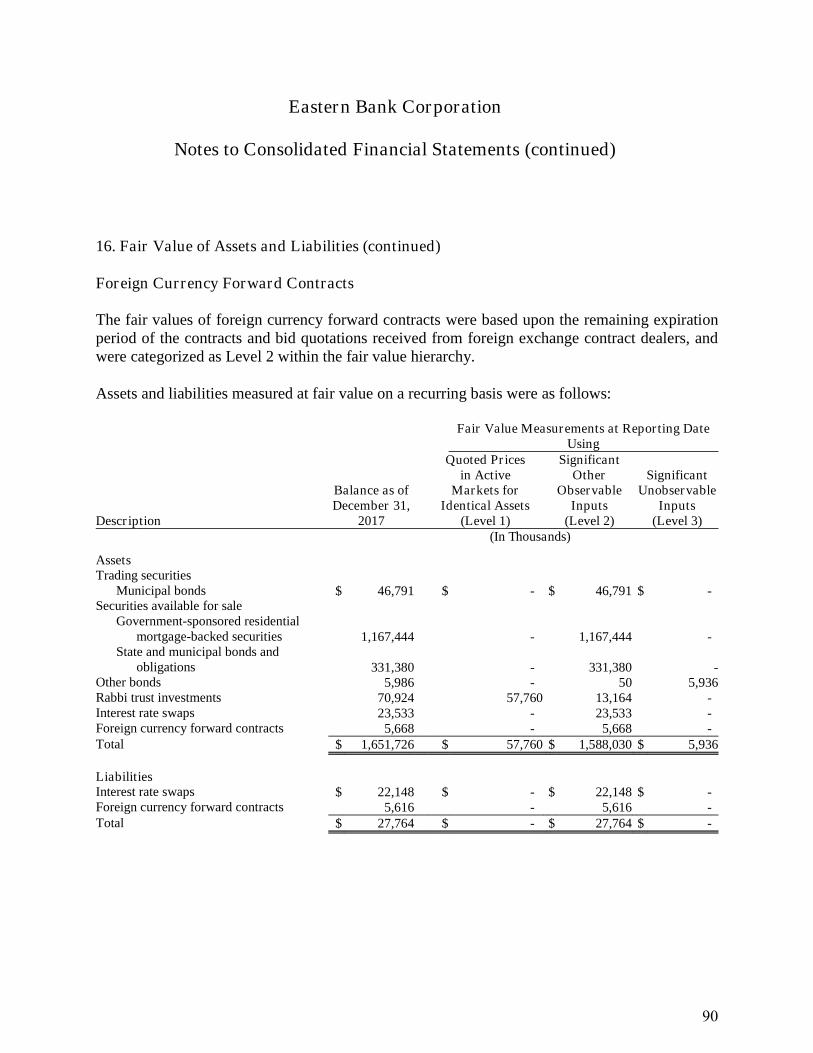

The Fair Value Measurements and Disclosures Topic of the Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. This Topic also establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements), and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy are described below:

Level 1 w Inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that the reporting entity has the ability to access at the measurement date.

35

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Level 2 w Valuations based on quoted prices in markets that are not active or for which all significant inputs are observable, either directly or indirectly.

Level 3 w Prices or valuations that require inputs that are both significant to the fair value measurement and unobservable.

To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised by the Corporation in determining fair value is greatest for instruments categorized in Level 3. A financial instrument{s level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement.

Statements of Cash Flows

Supplemental disclosures of cash flow information for the years ended December 31 follows: #

2017 2016 (In Thousands)

Cash paid for: Interest $ 6,999 $ 5,854

Income taxes $ 37,978 $ 25,928

Non-cash investing activities: Transfer of loans to other real estate owned $ 265 $ 189

36

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Recent Accounting Pronouncements

FASB ASC Topic 606 "Revenue from Contracts with Customers" Update No. 2014-09. Issued in May 2014, the purpose of this update is to address the previous revenue recognition requirements in GAAP that differ from those in International Financial Reporting Standards (IFRS). Accordingly, the FASB and the International Accounting Standards Board (IASB) initiated a joint project to clarify the principles for recognizing revenue and to develop a common revenue standard for U.S. GAAP and IFRS. The largely converged revenue recognition standards will supersede virtually all revenue recognition guidance in GAAP and IFRS. The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. Since the issuance of Update 2014-09, the FASB has finalized various amendments to the standard as summarized below:

FASB ASC Topic 606 "Revenue from Contracts with Customers" Update No. 2016-12. FASB ASC Topic 606 "Revenue from Contracts with Customers" Update No. 2016-10.FASB ASC Topic 606 "Revenue from Contracts with Customers" Update No. 2016-08. FASB ASC Topic 606 "Revenue from Contracts with Customers" Update No. 2015-14.

Through Updates 2016-12, 2016-10 and 2016-08, the FASB amended its new revenue guidance on licenses of intellectual property, identification of performance obligations, collectability, noncash consideration and the presentation of sales and other similar taxes. The FASB also clarified the definition of a completed contract at transition and added a practical expedient to ease transition for contracts that were modified prior to adoption. The FASB also amended the new revenue recognition guidance on determining whether an entity is a principal or an agent in an arrangement which affects whether revenue should be reported gross or net.

37

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Following the issuance of Update 2015-14, Update 2014-09, as amended, is effective for the Corporation for annual reporting periods beginning after December 15, 2018, including interim reporting periods within that reporting period. Earlier adoption is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period. A full or modified retrospective transition method is required. The Corporation's revenue is comprised of net interest income on financial assets and liabilities, which is explicitly excluded from the scope of the new guidance, and noninterest income. Certain components of noninterest income such as interest rate swap income, income from rabbi trust investments, trading securities gains, gains on sales of mortgage loans and gains on sales of securities available for sale are accounted for under other U.S. GAAP standards, and are therefore out of scope of the ASC 606 revenue standard. Insurance commissions, service charges on deposit accounts, debit card processing fees, and trust and investment advisory fees are within the scope of the ASC 606 revenue standard. As such, the Corporation is currently reviewing contracts related to these revenue streams and at this point does not anticipate any cWj[h_Wb Y^Wd][i je h[l[dk[ h[Ye]d_j_ed kfed WZefj_ed+ ^em[l[h+ j^[ ?ehfehWj_ed{i h[l_[m _i still ongoing. The Corporation plans to adopt the revenue recognition guidance on January 1, 2019 and anticipates using the modified retrospective transition method upon adoption.

38

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

94E5 4E6 FVWQK 1*) a6VUZVSQLI[QVU3 4TMULTMU[Z [V [PM 6VUZVSQLI[QVU 4UIS_ZQZb GWLI[M

No. 2015-02. Eiik[Z _d B[XhkWho 1/04+ j^[ fkhfei[ e\ j^_i kfZWj[ _i je h[ifedZ je ijWa[^ebZ[hi{ concerns about the current accounting for consolidation of certain legal entities. The amendments in this Update change the analysis that a reporting entity must perform to determine whether it should consolidate certain types of legal entities. Specifically, the amendments: 1) Modify the evaluation of whether limited partnerships and similar legal entities are VIEs or voting interest entities; 2) Eliminate the presumption that a general partner should consolidate a limited partnership; 3) Affect the consolidation analysis of reporting entities that are involved with VIEs, particularly those that have fee arrangements and related party relationships; and 4) Provide a scope exception from consolidation guidance for reporting entities with interests in legal entities that are required to comply with or operate in accordance with requirements that are similar to those in Rule 2a-7 of the Investment Company Act of 1940 for registered money market funds. The amendments are effective for public business entities for reporting periods beginning after December 15, 2015. For all other entities, the amendments are effective for reporting periods beginning after December 15, 2016. The adoption of this standard on January 1, 2017 did not have W cWj[h_Wb _cfWYj ed j^[ ?ehfehWj_ed{i Yedieb_ZWj[Z \_dWdY_Wb ijWj[c[dji-

FASB ASC Topic 805 aBusiness Combinations: Simplifying the Accounting for Measurement-CMYQVL 4LR\Z[TMU[Zb GWLI[M AV( +)*.-16. Issued in September 2015, the purpose of this update is to eliminate the requirement that acquirers in business combinations retrospectively apply adjustments made to provisional amounts recognized in a business combination. The amendments in the update require that an acquirer recognize adjustments to provisional amounts that are identified during the measurement period in the reporting period in which the adjustment amounts are determined. The amendments in this update require that the WYgk_h[h h[YehZ+ _d j^[ iWc[ f[h_eZ{i \_dWdY_Wb ijWj[c[dji+ j^[ [\\[Yj ed [Whd_d]i e\ Y^Wd][i _d depreciation, amortization, or other income effects, if any, as a result of the change to the provisional amounts, calculated as if the accounting had been completed at the acquisition date. The amendments are effective for public business entities for reporting periods beginning after December 15, 2015. For all other entities, the amendments are effective for reporting periods beginning after December 15, 2016. The adoption of this standard on January 1, 2017 did not ^Wl[ W cWj[h_Wb _cfWYj ed j^[ ?ehfehWj_ed{i Yedieb_ZWj[Z \_dWdY_Wb ijWj[c[dji-

39

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

FASB ASC Topic 825-*) a9QUIUKQIS =UZ[Y\TMU[Z ` Overall: Recognition and Measurement of 9QUIUKQIS 4ZZM[Z IUL 9QUIUKQIS ?QIJQSQ[QMZb GWLI[M AV( +)*/-01. Issued in January 2016, the purpose of this update is to enhance the reporting model for financial instruments to provide users of financial statements with more decision-useful information. The amendments in this update: 1) Require equity investments (except those accounted for under the equity method of accounting or those that result in consolidation of the investee) to be measured at fair value with changes in fair value recognized in net income; 2) Simplify the impairment assessment of equity investments without readily determinable fair values by requiring a qualitative assessment to identify impairment; 3) Eliminate the requirement to disclose the fair value of financial instruments measured at amortized cost for entities that are not public business entities; 4) Eliminate the requirement for public business entities to disclose the method(s) and significant assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost on the balance sheet; 5) Require public business entities to use the exit price notion when measuring the fair value of financial instruments for disclosure purposes; 6) Require an entity to present separately in other comprehensive income the portion of the total change in the fair value of a liability resulting from a change in the instrument-specific credit risk when the entity has elected to measure the liability at fair value in accordance with the fair value option for financial instruments; 7) Require separate presentation of financial assets and financial liabilities by measurement category and form of financial asset on the balance sheet or accompanying notes to the financial statements; 8) Clarify that an entity should evaluate the need for a valuation allowance on a deferred tax asset related to available-for-sale i[Ykh_j_[i _d YecX_dWj_ed m_j^ j^[ [dj_jo{i ej^[h deferred tax assets. The amendments are effective for public business entities for reporting periods beginning after December 15, 2017. For all other entities, the amendments are effective for reporting periods beginning after December 15, 2018. Early adoption is permitted for all other entities, but not before the public business entity effective date. Entities that are not considered public business entities may early adopt the provision that eliminates the requirement to disclose the fair value of financial instruments measured at amortized cost, and the Corporation has early adopted this provision in 2016. The Corporation is considering the impacts of the other provisions of this standard on the consolidated financial statements.

3;

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

FASB ASC Topic 842 "Leases" Update No. 2016-02. Issued in February 2016, this update affects any entity that enters into a lease (as that term is defined in this update), with some specified scope exemptions. The core principle of this update is that a lessee should recognize in the statement of financial position a liability to make lease payments and a right-of-use asset representing its right to use the underlying asset for the lease term. For leases with a term of 12 months or less, a lessee is permitted to make an accounting policy election by class of underlying asset not to recognize lease assets and lease liabilities. The recognition, measurement, and presentation of expenses and cash flows arising from a lease have not significantly changed from previous GAAP. In addition, the accounting applied by a lessor is largely unchanged from that applied under previous GAAP. For public business entities, the amendments in this update are effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. For all other entities, the amendments in this update are effective for fiscal years beginning after December 15, 2019. The Corporation is currently assessing the impact of the adoption of this standard on the ?ehfehWj_ed{i consolidated financial position.

FASB ASC Topic 323 "Investments -Equity Method and Joint Ventures" Update No. 2016-07.Issued in March 2016, this update eliminates the requirement that when an investment qualifies for use of the equity method as a result of an increase in the level of ownership interest or degree of influence, an investor must adjust the investment, results of operations, and retained earnings retroactively on a step-by-step basis as if the equity method had been in effect during all previous periods that the investment had been held. The amendments require that the equity method investor add the cost of acquiring the additional interest in the investee to the current basis of the investor's previously held interest and adopt the equity method of accounting as of the date the investment becomes qualified for equity method accounting. Therefore, upon qualifying for the equity method of accounting, no retroactive adjustment of the investment is required. The amendments in this update require that an entity that has an available-for-sale equity security that becomes qualified for the equity method of accounting recognize through earnings the unrealized holding gain or loss in accumulated other comprehensive income at the date the investment becomes qualified for use of the equity method. The amendments in this update are effective for fiscal years beginning after December 15, 2016, including interim periods within those fiscal years. The amendments should be applied prospectively upon their effective date to increases in the level of ownership interest or degree of influence that result in the adoption of the equity method. Early adoption is permitted. The adoption of this standard on January 1, 2017 did not have a material impact on the ?ehfehWj_ed{i consolidated financial position.

41

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

FASB ASC Topic 605 "Revenue Recognition" and Topic 815 "Derivatives and Hedging" Update No. 2016-11. Issued in May 2016, this update is a rescission of SEC guidance because of ASU Updates 2014-09 and 2014-16 pursuant to staff announcements at the March 3, 2016 Emerging Issues Task Force meeting. The amendments in this update are effective upon adoption of Topic 606 "Revenue from Contracts with Customers" (for periods beginning after December 15, 2018 for the Corporation). The Corporation is currently assessing the impact of the adoption of this standard on the ?ehfehWj_ed{i consolidated financial position.

FASB ASC Topic 326 "Financial Instruments - Credit Losses" Update No. 2016-13. Issued in June 2016, this update was intended to provide financial statement users with more decision-useful information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity at each reporting date. To achieve this objective, the amendments in this update replace the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. The amendments affect entities holding financial assets and net investment in leases that are not accounted for at fair value through net income. The amendments affect loans, debt securities, trade receivables, net investments in leases, off-balance sheet credit exposures, reinsurance receivables, and any other financial assets not excluded from the scope that have the contractual right to receive cash. For public business entities, the amendments in this update are effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years, with earlier adoption permitted as of fiscal years beginning after December 15, 2018, including interim periods with those fiscal years. For all other entities, the amendments in this update are effective for fiscal years beginning after December 15, 2020. The Corporation is currently assessing the impact of the adoption of this standard on the ?ehfehWj_ed{i consolidated financial position.

42

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

FASB ASC Topic 230 "Statement of Cash Flows" Update No. 2016-15. Issued in August 2016, this update was intended to reduce diversity of practice in how certain cash receipts and cash payments are presented and classified in the statement of cash flows. The amendments in this update provide guidance on the following eight specific cash flow issues; (1) debt prepayment or debt extinguishment costs, (2) settlement of zero-coupon debt instruments or other debt instruments with coupon interest rates that are insignificant in relation to the effective interest rate of the borrowing, (3) contingent consideration payments made after a business combination, (4) proceeds from the settlement of insurance claims, (5) proceeds from the settlement of corporate-owned life insurance policies, including bank-owned life insurance policies, (6) distributions received from equity method investees, (7) beneficial interests in securitization transactions, and (8) separately identifiable cash flows and application of the Predominance Principle. The amendments in this topic will provide guidance for these eight issues, thereby reducing the current and potential future diversity in practice. For public business entities, the amendments in this update are effective for annual periods and interim periods within those annual periods beginning after December 31, 2017. For all other entities, the amendments in this update are effective for fiscal years beginning after December 15, 2018. Earlier adoption is permitted, including interim reporting periods within that reporting period. If an entity early adopts the amendments in an interim period, any adjustments should be reflected as of the beginning of the fiscal year that includes that interim period. An entity that elects early adoption must adopt all of the amendments in the same period. The adoption of this standard is not [nf[Yj[Z je ^Wl[ W cWj[h_Wb _cfWYj ed j^[ ?ehfehWj_ed{i Yedieb_ZWj[Z \_dWdY_Wb fei_j_ed-

43

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

94E5 4E6 FVWQK 1). a5\ZQUMZZ 6VTJQUI[QVUZb GWLI[M AV( +)*0-01. Issued in January 2017, the purpose of this update is to clarify the definition of a business with the objective of adding guidance to assist entities with evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses. The amendments in this update provide a screen to determine when an integrated set of assets and activities is not a business. The screen requires that when substantially all of the fair value of the group of assets acquired (or disposed of) is concentrated in a single identifiable asset or a group of similar identifiable assets, the set is not a business. If the screen is not met, the amendments in this update: 1) require that to be considered a business, a set must include, at a minimum, an input and a substantive process thattogether significantly contribute to the ability to create output and; (2) remove the evaluation of whether a market participant could replace missing elements. The amendments provide a framework to assist entities in evaluating whether both an input and a substantive process are present. The framework includes two sets of criteria to consider that depend on whether a set has outputs. Although outputs are not required for a set to be a business, outputs generally are a key element of a business; therefore, the Board has developed more stringent criteria for sets without outputs. For public business entities, the amendments in this update are effective for annual periods and interim periods within those annual periods beginning after December 15, 2017. For all other entities, the amendments in this update are effective for fiscal years beginning after December 15, 2018. The adoption of this standard is not expected to have a material impact on j^[ ?ehfehWj_ed{i Yedieb_dated financial position.

44

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

94E5 4E6 FVWQK ,.) a=U[IUOQJSMZ ` ;VVL^QSS IUL B[PMYb GWLI[M AV( +)*0-04. Issued in January 2017, the purpose of this update is to simplify the subsequent measurement of goodwill for public business entities and other entities that have goodwill reported in their financial statements and have not elected the private company alternative for the subsequent measurement of goodwill. This update eliminates Step 2 from the goodwill impairment test, whereby an entity had to perform procedures to determine the fair value at the impairment testing date of its assets and liabilities following the procedure that would be required in determining the fair value of assets acquired and liabilities assumed in a business combination. Under the amendments in this update, an entity should instead perform its annual or interim goodwill impairment test by comparing the fair value of a reporting unit with its carrying amount. An entity should recognize Wd _cfW_hc[dj Y^Wh][ \eh j^[ Wcekdj Xo m^_Y^ j^[ YWhho_d] Wcekdj [nY[[Zi j^[ h[fehj_d] kd_j{i fair value; however, the loss recognized should not exceed the total amount of goodwill allocated to that reporting unit. Additionally, an entity should consider income tax effects from any tax deductible goodwill on the carrying amount of the reporting unit when measuring the goodwill impairment loss, if applicable. The Board also eliminated the requirements for any reporting unit with a zero or negative carrying amount to perform a qualitative assessment and, if it fails that qualitative test, to perform Step 2 of the goodwill impairment test. Therefore, the same impairment test applies to all reporting units. For public business entities that are U.S. Securities and Exchange (SEC) filers, the amendments in this update are effective for annual goodwill impairment tests and any interim goodwill impairment tests in fiscal years beginning after December 15, 2019. For public business entities that are not SEC filers, the amendments in this update are effective for annual goodwill impairment tests and any interim goodwill impairment tests in fiscal years beginning after December 15, 2020. For all other entities, the amendments in this update are effective for annual goodwill impairment tests and any interim goodwill impairment tests in fiscal years beginning after December 15, 2021. Early adoption is permitted for interim or annual goodwill impairment tests performed on testing dates after January 1, 2017.The Corporation elected to early adopt this standard in 2017 and the adoption did not have a cWj[h_Wb _cfWYj ed j^[ ?ehfehWj_ed{i Yedieb_ZWj[Z \_dWdY_Wb position.

45

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

FASB ASC Topic 610-+) aB[PMY =UKVTM ` Gains and Losses from the Derecognition of AVUNQUIUKQIS 4ZZM[Zb GWLI[M AV( +)*0-05. Issued in February 2017, the purpose of this update is to clarify that a financial asset is within the scope of Subtopic 610-20 if it meets the definition of an in substance nonfinancial asset. The amendments define the term in substance nonfinancial asset, in part, as a financial asset promised to a counterparty in a contract if substantially all of the fair value of the assets (recognized and derecognized) that are promised to the counterparty in the contract is concentrated in nonfinancial assets. The amendments in this update also clarify that nonfinancial assets within the scope of Subtopic 610-20 may include nonfinancial assets transferred within a legal entity to a counterparty. A contract that includes the transfer of ownership interests in one or more consolidated subsidiaries is within the scope of Subtopic 610-20 if substantially all of the fair value of the assets that are promised to the counterparty in a contract is concentrated in nonfinancial assets. For purposes of that evaluation, the amendments require an entity to evaluate the underlying assets in consolidated subsidiaries to determine whether those assets are within the scope of Subtopic 610-20. For public business entities, certain non-for-profit entities, and certain employee benefit plans, the amendments in this update are effective for annual reporting periods beginning after December 15, 2017, including interim reporting periods within that reporting period. For all other entities, the amendments in this update are effective for annual reporting periods beginning after December 15, 2018, and interim periods within annual periods beginning after December 15, 2019. Earlier application is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period. An entity is required to apply the amendments in this update at the same time that it applies the amendments in Update 2014-09. The adoption of this standard is not expected to have a material impact on j^[ ?ehfehWj_ed{i consolidated financial position.

46

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)