2016 analyst day - files.shareholder.comfiles.shareholder.com/downloads/qcom/6362260405x0x... · in...

TRANSCRIPT

1

2016 Analyst Day

February 11, 2016

2

In addition to the historical information contained herein, this presentation and the conference call that accompanies it contain forward-looking statements that are inherently subject to risks and uncertainties, including but not limited to statements regarding our business and financial strategies, priorities, plans, drivers, opportunities, outlook, estimates and expectations; our business and growth opportunities and initiatives, including licensing, core and adjacent opportunities and initiatives, and our positioning to take advantage thereof; our technology, products, product roadmap, innovation and investments; industry trends; 5G and LTE; operational performance; mergers, acquisitions and joint ventures; our strategic realignment plan, including cost reduction initiatives, and our progress vs. that plan; our capital return commitments; our regulatory and compliance challenges, including compliance and reporting challenges in China and our progress, expectations and intentions with respect to resolving those challenges, and the timing thereof, as well as the impact on our business and financial results; and estimates including 3G/4G device shipments and sales, global cellular connections, handset replacement rates, non-handset device shipments and ASPs. Forward-looking statements are generally identified by words such as “estimates,” “guidance,” “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks” and similar expressions. Actual results may differ materially from those referred to in the forward-looking statements due to a number of important factors, including but not limited to risks associated with commercial network deployments, expansions and upgrades of CDMA, OFDMA and other communications technologies, our customers’ and licensees’ sales of products and services based on these technologies and our ability to drive our customers’ demand for our products and services; competition in an environment of rapid technological change; our dependence on a small number of customers and licensees; attacks on our licensing business model, including current and future legal proceedings or actions of governmental or quasi-governmental bodies or standards or industry organizations; the enforcement and protection of our intellectual property rights; the continued and future success of our licensing programs; government regulations and policies, or adverse rulings in enforcement or other proceedings; the commercial success of our new technologies, products and services; our dependence on a limited number of third-party suppliers; claims by third parties that we infringe their intellectual property; acquisitions, strategic transactions and investments; the execution of our strategic realignment plan; our stock price and earnings volatility; our indebtedness; our ability to attract and retain qualified employees; foreign currency fluctuations; global economic conditions that impact the mobile communications industry and failures in our products or services or in the products or services of our customers or licensees, including those resulting from security vulnerabilities, defects or errors. These and other risks are set forth in our most recent Quarterly Report on Form 10-Q filed with the SEC. Our reports filed with the SEC are available on our website at www.qualcomm.com. We undertake no obligation to update, or continue to provide information with respect to, any forward-looking statement or risk factor, whether as a result of new information, future events or otherwise.

This presentation includes “non-GAAP financial measures” as that term is defined in Regulation G. The most directly comparable GAAP financial measures and information reconciling these non-GAAP financial measures to our financial results prepared in accordance with GAAP are included at the end of this presentation.

We refer to “Qualcomm” for ease of reference. However, in connection with our fiscal 2013 reorganization, Qualcomm Incorporated continues to operate QTL and own the vast majority of our patent portfolio, while Qualcomm Technologies, Inc., its wholly-owned subsidiary, now operates, along with its subsidiaries, substantially all of our products and services businesses, including QCT, and substantially all of our research and development functions.

Safe Harbor

3

Steve Mollenkopf10:00am

10:40am Matt Grob

11:00am Derek Aberle

11:45am Lunch Break

12:30pm Cristiano Amon

1:15pm George Davis

1:45pm Q&A

Agenda

Steve Mollenkopf

CEO, Qualcomm Incorporated

5

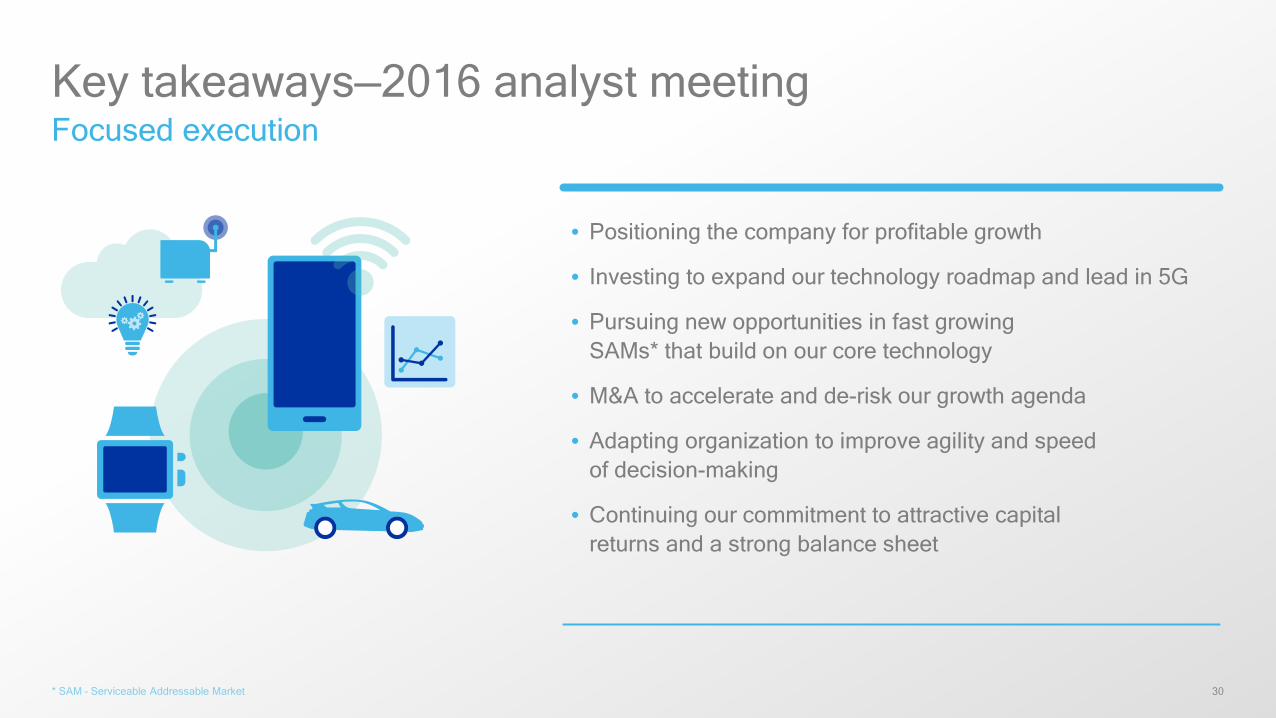

• Positioning the company for profitable growth

• Investing to expand our technology roadmap and lead in 5G

• Pursuing new opportunities in fast growing SAMs* that build on our core technology

• M&A to accelerate and de-risk our growth agenda

• Adapting organization to improve agility and speed of decision-making

• Continuing our commitment to attractive capital returns and a strong balance sheet

Focused execution

* SAM – Serviceable Addressable Market

Transitioning Qualcomm for the next phase of growth

6

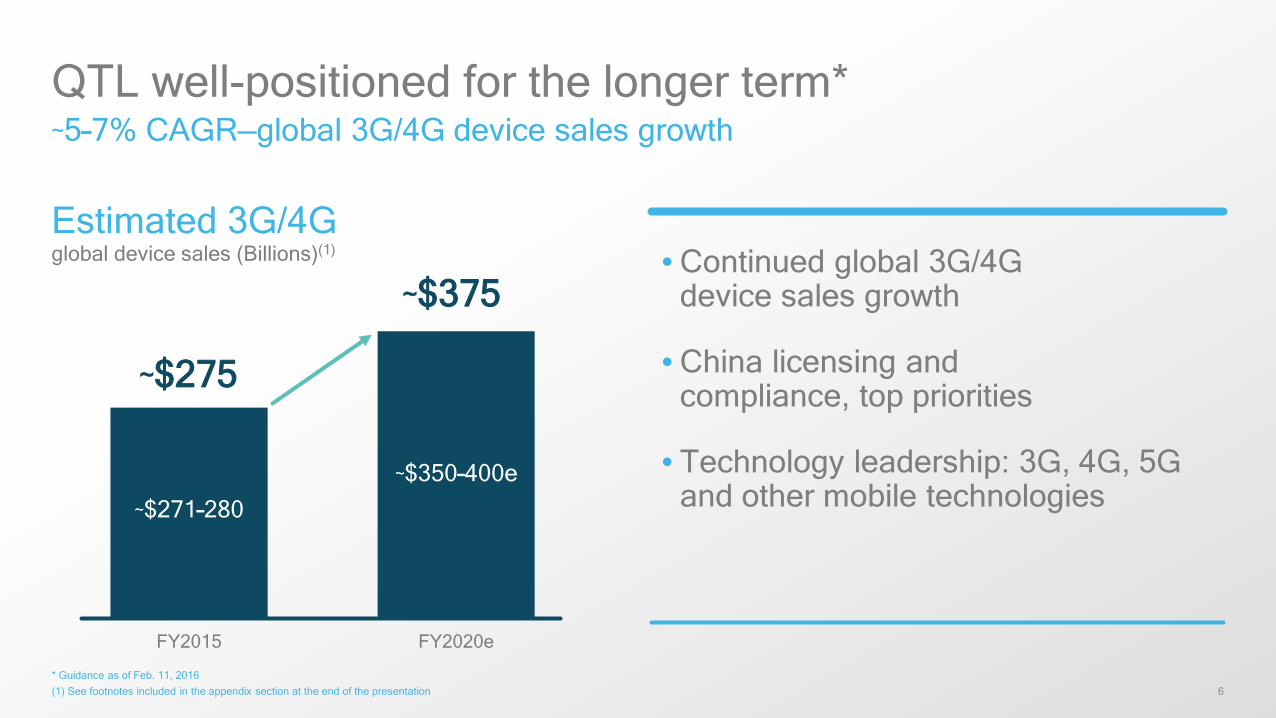

• Continued global 3G/4G device sales growth

• China licensing and compliance, top priorities

• Technology leadership: 3G, 4G, 5G and other mobile technologies

~5–7% CAGR—global 3G/4G device sales growth

* Guidance as of Feb. 11, 2016(1) See footnotes included in the appendix section at the end of the presentation

QTL well-positioned for the longer term*

FY2015 FY2020e

~$271–280~$350–400e

~$275

~$375

Estimated 3G/4G global device sales (Billions)(1)

7

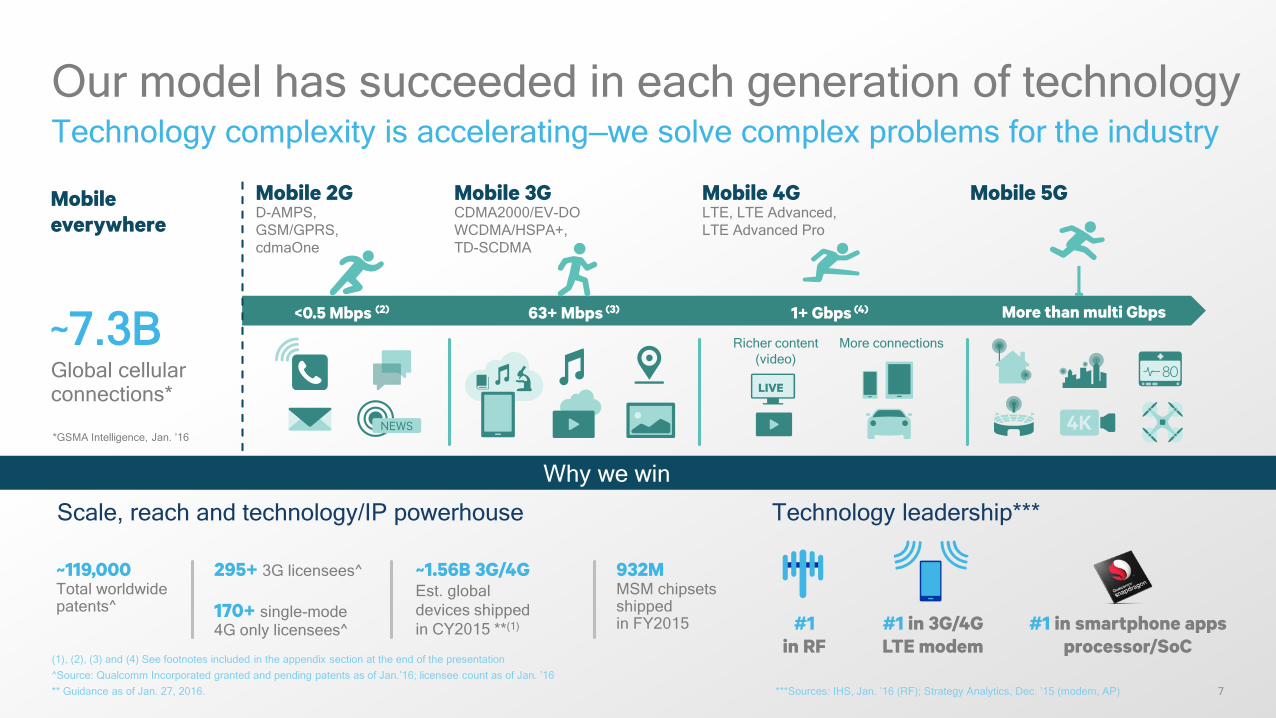

Our model has succeeded in each generation of technologyTechnology complexity is accelerating—we solve complex problems for the industry

(1), (2), (3) and (4) See footnotes included in the appendix section at the end of the presentation^Source: Qualcomm Incorporated granted and pending patents as of Jan.’16; licensee count as of Jan. ’16** Guidance as of Jan. 27, 2016. ***Sources: IHS, Jan. ’16 (RF); Strategy Analytics, Dec. ’15 (modem, AP)

932MMSM chipsets shipped in FY2015

170+ single-mode 4G only licensees^

295+ 3G licensees^ ~1.56B 3G/4GEst. global devices shipped in CY2015 **(1)

~119,000Total worldwide patents^

#1 in 3G/4G LTE modem

Scale, reach and technology/IP powerhouse

#1 in RF

Technology leadership***

Why we win

#1 in smartphone apps processor/SoC

Mobile everywhere

~7.3B

*GSMA Intelligence, Jan. ’16

Global cellular connections*

Richer content(video)

More connections

LIVE

Mobile 2G Mobile 3G Mobile 4G Mobile 5GD-AMPS, GSM/GPRS,cdmaOne

CDMA2000/EV-DOWCDMA/HSPA+, TD-SCDMA

LTE, LTE Advanced,LTE Advanced Pro

<0.5 Mbps (2) 63+ Mbps (3) More than multi Gbps1+ Gbps (4)

8

Providing technology at scale

Transforming industries and the world

Transformexisting industries

Enable new industries

Lead in core

9

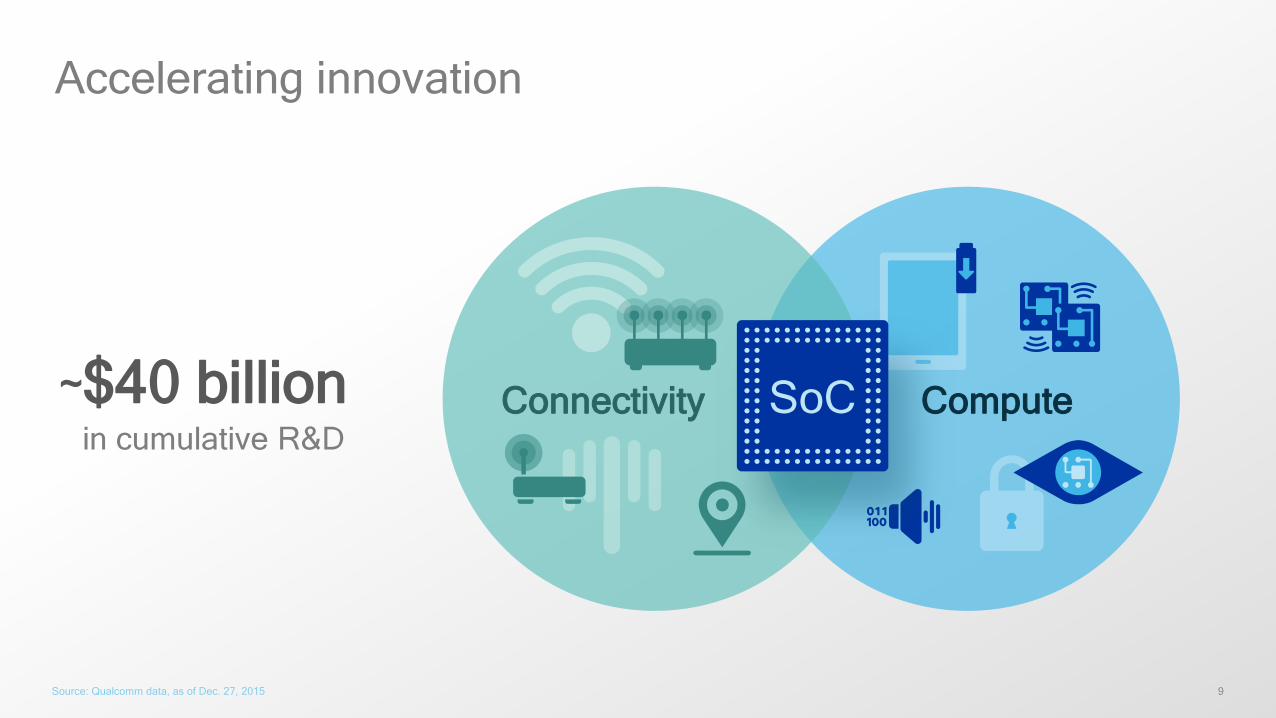

Accelerating innovation

Source: Qualcomm data, as of Dec. 27, 2015

~$40 billionin cumulative R&D

Connectivity ComputeSoC

10

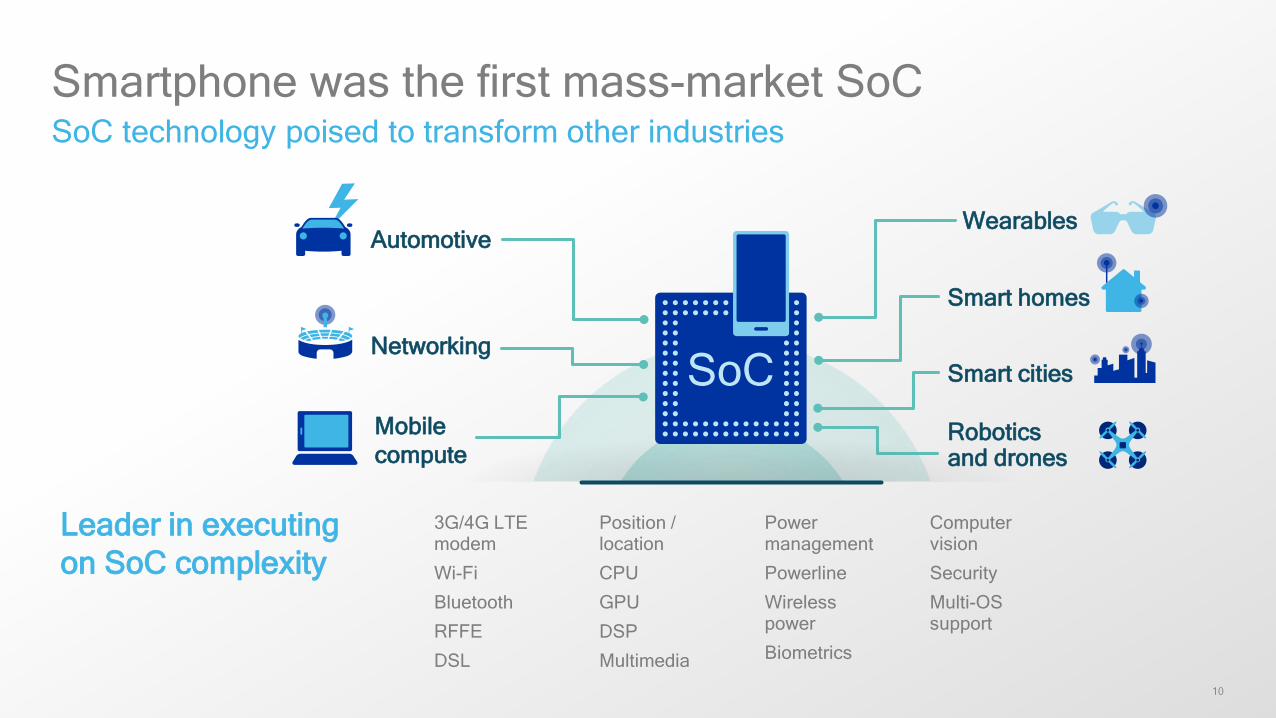

SoC

Smartphone was the first mass-market SoCSoC technology poised to transform other industries

3G/4G LTE modem

Wi-Fi

Bluetooth

RFFE

DSL

Position / location

CPU

GPU

DSP

Multimedia

Power management

Powerline

Wireless power

Biometrics

Computer vision

Security

Multi-OS support

Leader in executing on SoC complexity

WearablesAutomotive

NetworkingSmart cities

Robotics and drones

Smart homes

Mobile compute

11

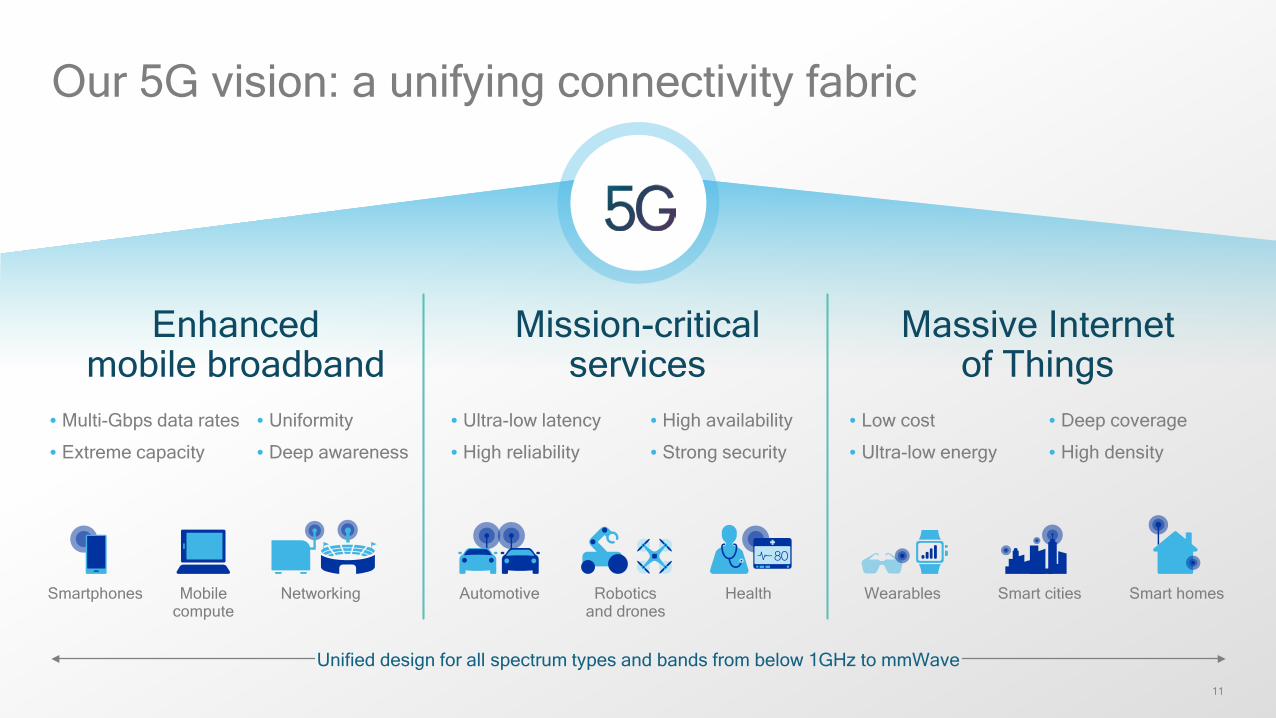

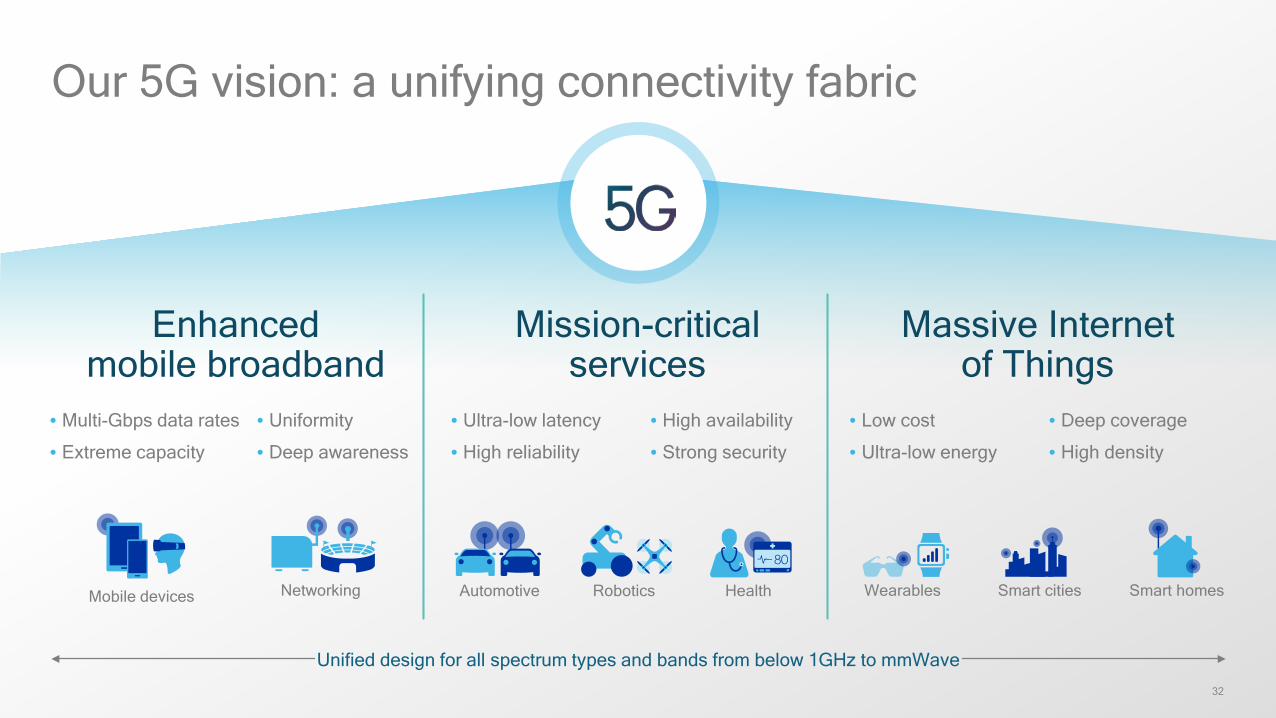

Our 5G vision: a unifying connectivity fabric

Mission-criticalservices

Enhancedmobile broadband

Massive Internetof Things

NetworkingSmartphones Robotics and drones

Automotive Health Smart cities Smart homesWearables

Unified design for all spectrum types and bands from below 1GHz to mmWave

• Ultra-low latency

• High reliability

• High availability

• Strong security

• Multi-Gbps data rates

• Extreme capacity

• Uniformity

• Deep awareness

• Low cost

• Ultra-low energy

• Deep coverage

• High density

Mobilecompute

12

Expansion Adjacentopportunities

Additional growth opportunities

Building on mobile strength—grow into new opportunities

RFFE

Fingerprint

Automotive

Networking

Healthcare

Data center

Wi-Fi 11ad (60GHz)

Touch

IoT

Mobile

Mobile compute

13

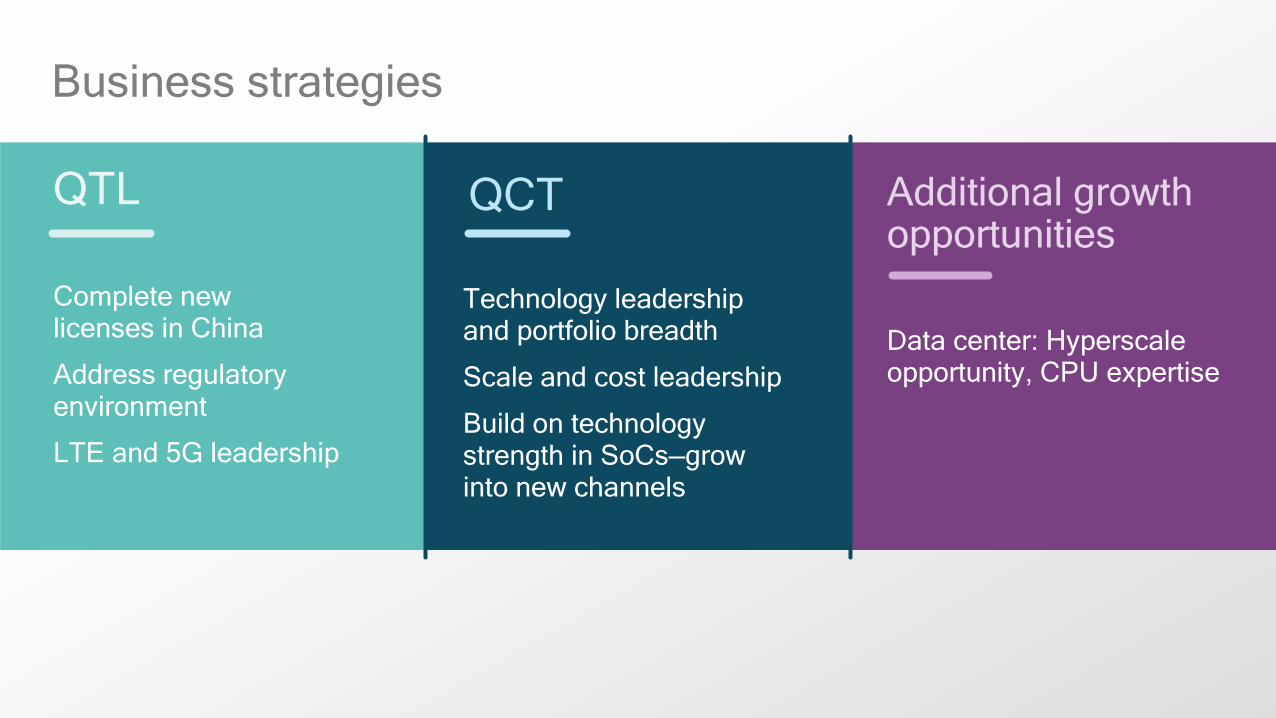

QTL Additional growth opportunities

Complete new licenses in China

Address regulatory environment

LTE and 5G leadership

Data center: Hyperscaleopportunity, CPU expertise

QCT

Technology leadership and portfolio breadth

Scale and cost leadership

Build on technology strength in SoCs—grow into new channels

Business strategies

14

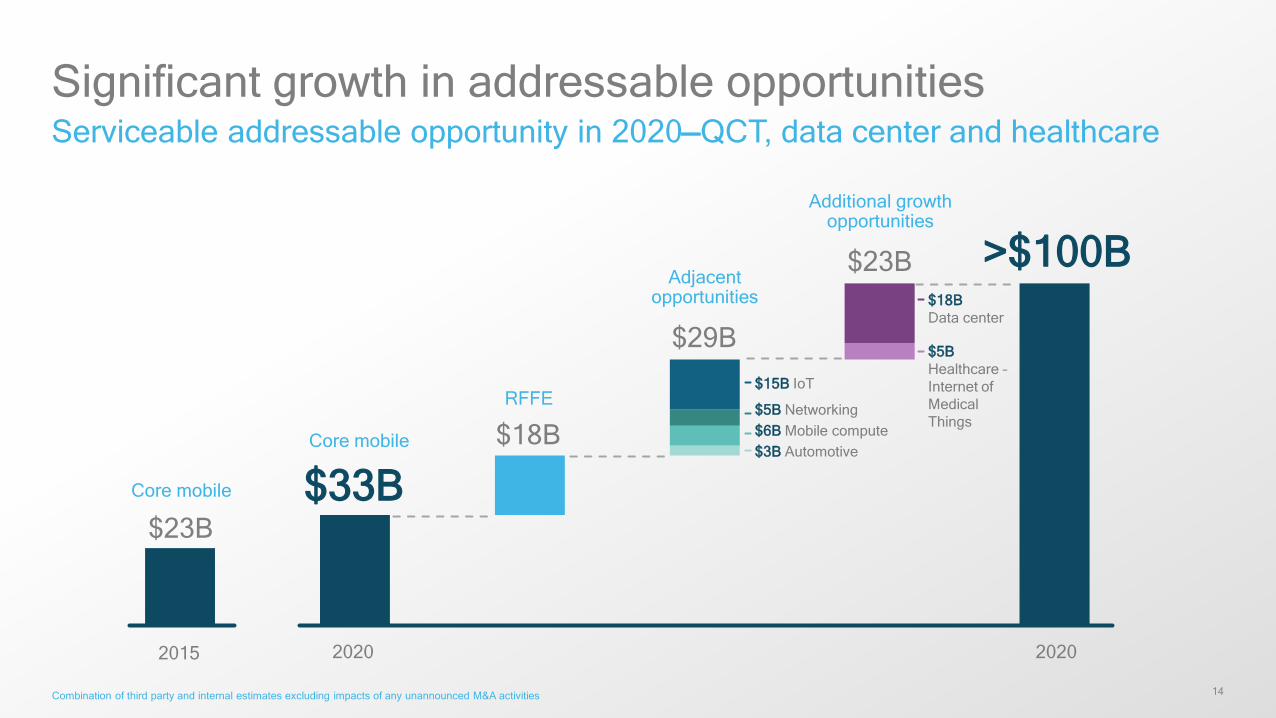

Significant growth in addressable opportunitiesServiceable addressable opportunity in 2020—QCT, data center and healthcare

Combination of third party and internal estimates excluding impacts of any unannounced M&A activities

Core mobile

RFFE

Adjacentopportunities

$15B IoT

$5B Networking

$3B Automotive

Additional growth opportunities

$18B Data center

$5B Healthcare –Internet of Medical Things

$33B

>$100B

$6B Mobile compute

2015 2020

$18B

$29B

$23B

$23B

Core mobile

2020

15

M&A approach

• Strong alignment with core competency

• Tuck-in acquisitions to support platforms

• Differentiated intellectual property

• Industry consolidation will continue and create opportunities

• Inorganic overall likely to increase

• Balance sheet strength critical to retaining optionality given industry scale

Mobile

17

Mobile

8.5B+Cumulative smartphone unit shipments forecast 2015–2019*

>$50BChipset opportunity by 2020**

* Source: Gartner, Dec. ’15 ** Serviceable Addressable Market, combination of third party and internal estimates excluding impacts of any unannounced M&A activities

Core mobile | RF Front-End | Wi-Fi 11ad | Touch and (60GHz) fingerprint

18

Ongoing technology innovation drives smartphone demand

LTE Unlicensed

CDMA 1x EV-DO

GSM/GPRSNFC Wi-Fi 11ac MU-MIMO Multimode, multiband transceivers

Bluetooth Wi-Fi 11adSecurity Antenna switchPower amplifiers

Machine intelligence 64-bit processing and OS Wireless charging Voice codecs Filters

Quick charging PMICsAntenna tunerConsole quality graphics Always-on sensor processing

VoLTEGNSS Fingerprint sensorsTouch screen controllers

LTE FDD/TDD

Multi-SIM TD-SCDMA Envelope tracker Computer vision

LTE-Wi-Fi aggregationHSPA+/WCDMA Computational photographyAll-mode

Virtual and augmented reality

19

Qualcomm® Snapdragon™ 820

100+ designsin development Increased

performance

More immersive experiences

More secure

Improved battery life

Qualcomm Snapdragon is a product of Qualcomm Technologies, Inc.

20

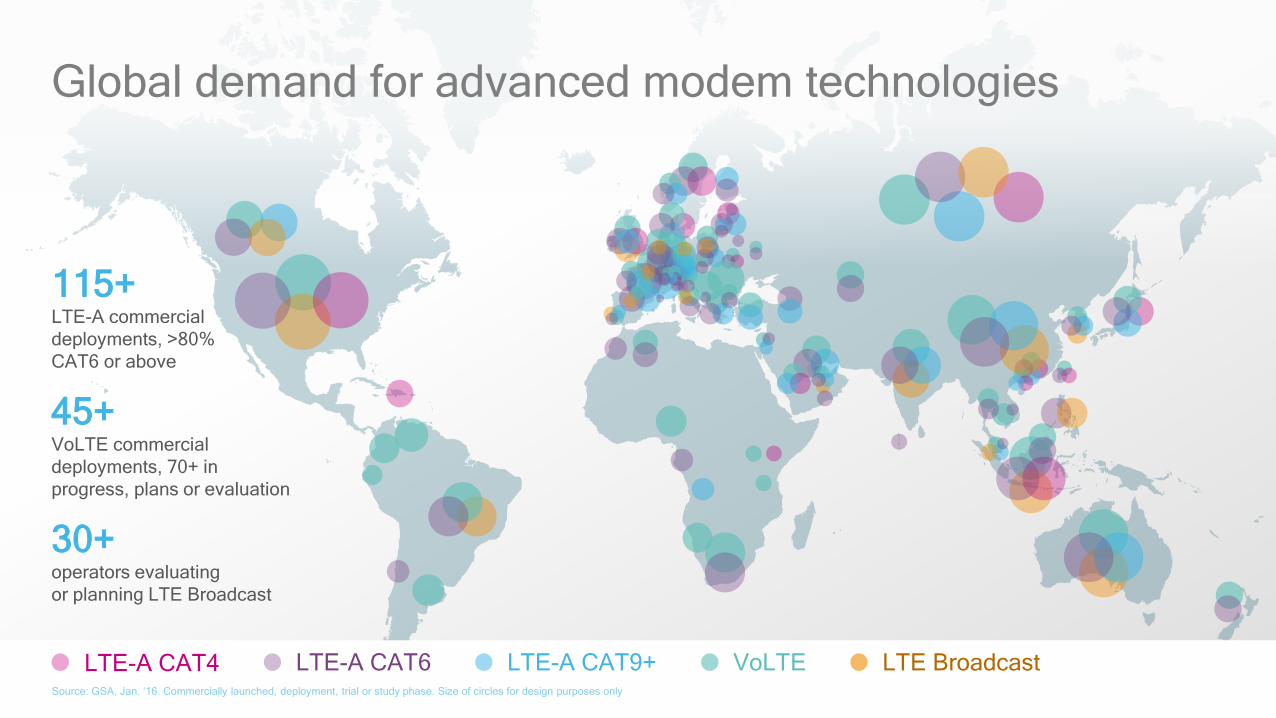

Global demand for advanced modem technologies

115+ LTE-A commercial deployments, >80% CAT6 or above

45+ VoLTE commercial deployments, 70+ in progress, plans or evaluation

30+ operators evaluating or planning LTE Broadcast

LTE-A CAT4 LTE-A CAT6 LTE-A CAT9+ VoLTE LTE BroadcastSource: GSA, Jan. ‘16. Commercially launched, deployment, trial or study phase. Size of circles for design purposes only

21

Meeting data demand with licensed + unlicensed spectrumEvolution of small cells and Wi-Fi expands opportunities

Aggregating unlicensed with a licensed spectrum anchor

Operates solely in unlicensed spectrum

LTE-U

LWA(LTE-Wi-Fi link aggregation)

LAA(Licensed-Assisted Access)

For mobile operators, ISPs*, cable companies, enterprises, venues, etc.

For mobile operators

Wi-Fi 802.11ac/ad(802.11 technology)

MulteFire(LTE-based technology)

*Internet Service Providers

22

Increasing QCT content within the smartphoneSignificant growth opportunities beyond modem and SoC

RF Front-End• Global mode

• Accelerated time-to-market

• Design flexibility

• Complete solutionsWi-Fi 11ad (60GHz)• Multi-gigabit speeds

• Multiple 4K video streams

• Virtually lag-free docking

• Near instantaneous media syncing and cloud access

Touch and fingerprint• Low power

• Enhanced security

• Fast, smooth operation

23

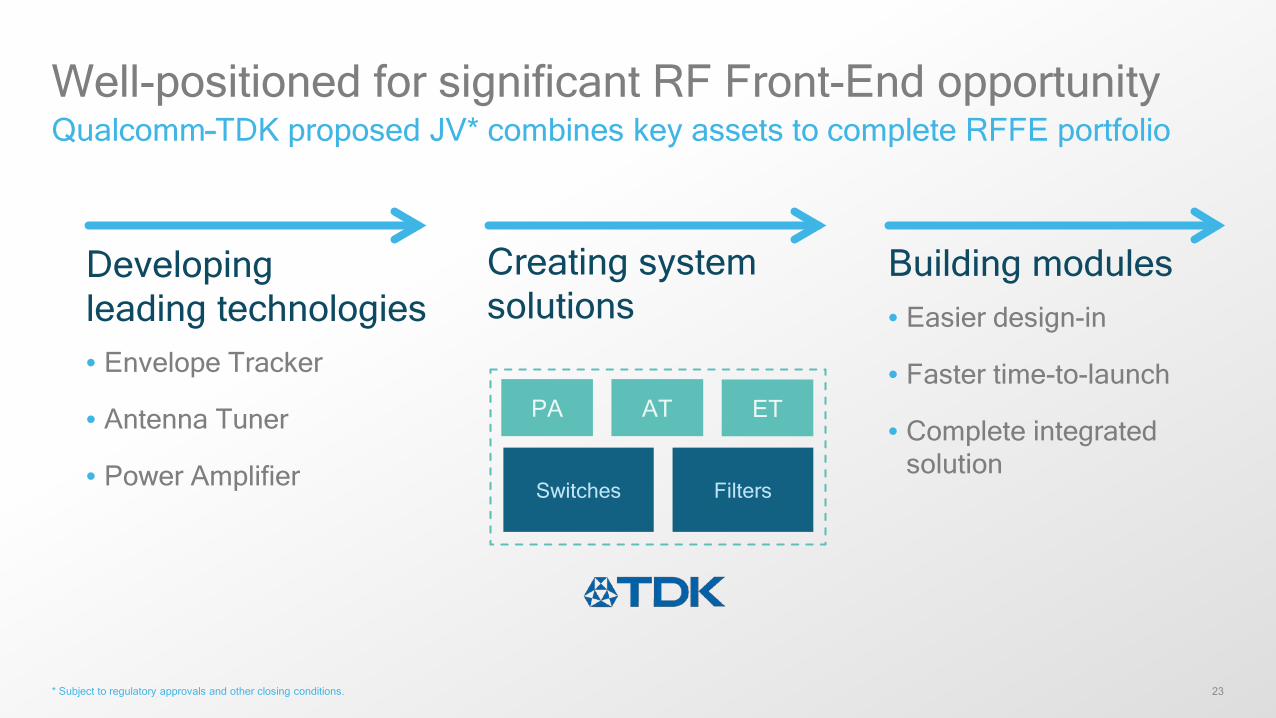

Developing leading technologies• Envelope Tracker

• Antenna Tuner

• Power Amplifier

Qualcomm–TDK proposed JV* combines key assets to complete RFFE portfolio

* Subject to regulatory approvals and other closing conditions.

Well-positioned for significant RF Front-End opportunity

Creating system solutions

Building modules• Easier design-in

• Faster time-to-launch

• Complete integrated solution

PA AT ET

Switches Filters

Adjacent QCT opportunities

25

Opportunity by 2020*

3G/4G modem

Wi-Fi

Bluetooth

RF

Position/Location

CPU

GPU

DSP

Multimedia

Power management

Wireless power

Biometrics

Computer vision

Security

Multi-OS support

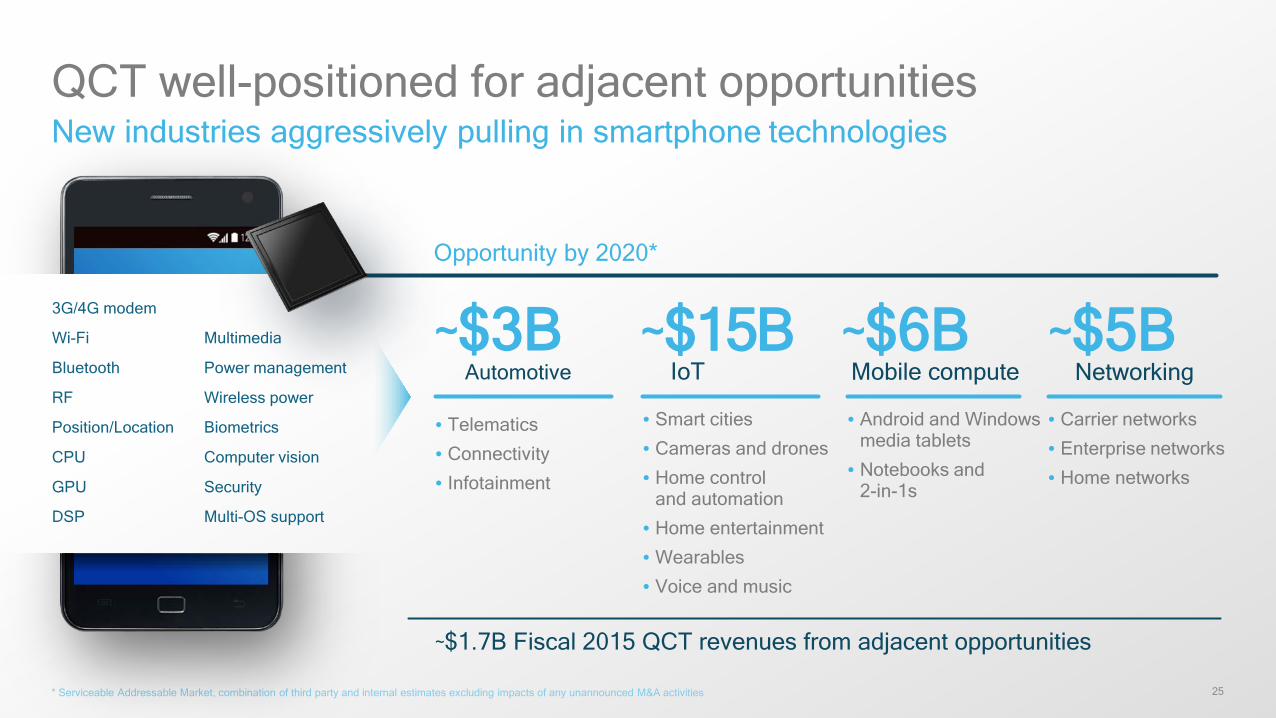

QCT well-positioned for adjacent opportunitiesNew industries aggressively pulling in smartphone technologies

~$1.7B Fiscal 2015 QCT revenues from adjacent opportunities

* Serviceable Addressable Market, combination of third party and internal estimates excluding impacts of any unannounced M&A activities

~$3BAutomotive

• Telematics

• Connectivity

• Infotainment

~$5B• Carrier networks

• Enterprise networks

• Home networks

~$15B• Smart cities

• Cameras and drones

• Home control and automation

• Home entertainment

• Wearables

• Voice and music

• Android and Windows media tablets

• Notebooks and 2-in-1s

~$6BIoT Mobile compute Networking

26

• General Manager leadership structure implemented

• R&D investment aligned with growth opportunities

• Building out segment-specific channels

• Supplemental M&A — CSR mapped to new structure

• Detailed product roadmaps to extend core technologies into adjacent opportunities

Improving agility and speed of decision-makingAdapting organization

Additional growth opportunities

28

Extension opportunities

Opportunity by 2020*

Additional growth opportunities

~$18BData center

~$5BHealthcareInternet of Medical Things

Focused investments in large opportunities outside QCT and QTL

* Serviceable Addressable Market, combination of third party and internal estimates excluding impacts of any unannounced M&A activities

Strategic focus

30

• Positioning the company for profitable growth

• Investing to expand our technology roadmap and lead in 5G

• Pursuing new opportunities in fast growing SAMs* that build on our core technology

• M&A to accelerate and de-risk our growth agenda

• Adapting organization to improve agility and speed of decision-making

• Continuing our commitment to attractive capital returns and a strong balance sheet

Focused execution

* SAM – Serviceable Addressable Market

Key takeaways—2016 analyst meeting

Matt Grob

Executive Vice President, Qualcomm Technologies, Inc. and Chief Technology Officer

32

Our 5G vision: a unifying connectivity fabric

Mission-criticalservices

Enhancedmobile broadband

Massive Internetof Things

NetworkingMobile devices RoboticsAutomotive Health Smart cities Smart homesWearables

Unified design for all spectrum types and bands from below 1GHz to mmWave

• Ultra-low latency

• High reliability

• High availability

• Strong security

• Multi-Gbps data rates

• Extreme capacity

• Uniformity

• Deep awareness

• Low cost

• Ultra-low energy

• Deep coverage

• High density

33

Wireless/OFDM technology and chipset

leadership

Pioneering 5G technologies tomeet extreme requirements

End-to-end systemapproach with advanced

prototypes

Driving 5G from standardizationto commercialization

Leading globalnetwork experience

and scale

Providing the experience andscale that 5G demands

Qualcomm, leading the world to 5GInvesting in 5G for many years—building upon our leadership foundation

34

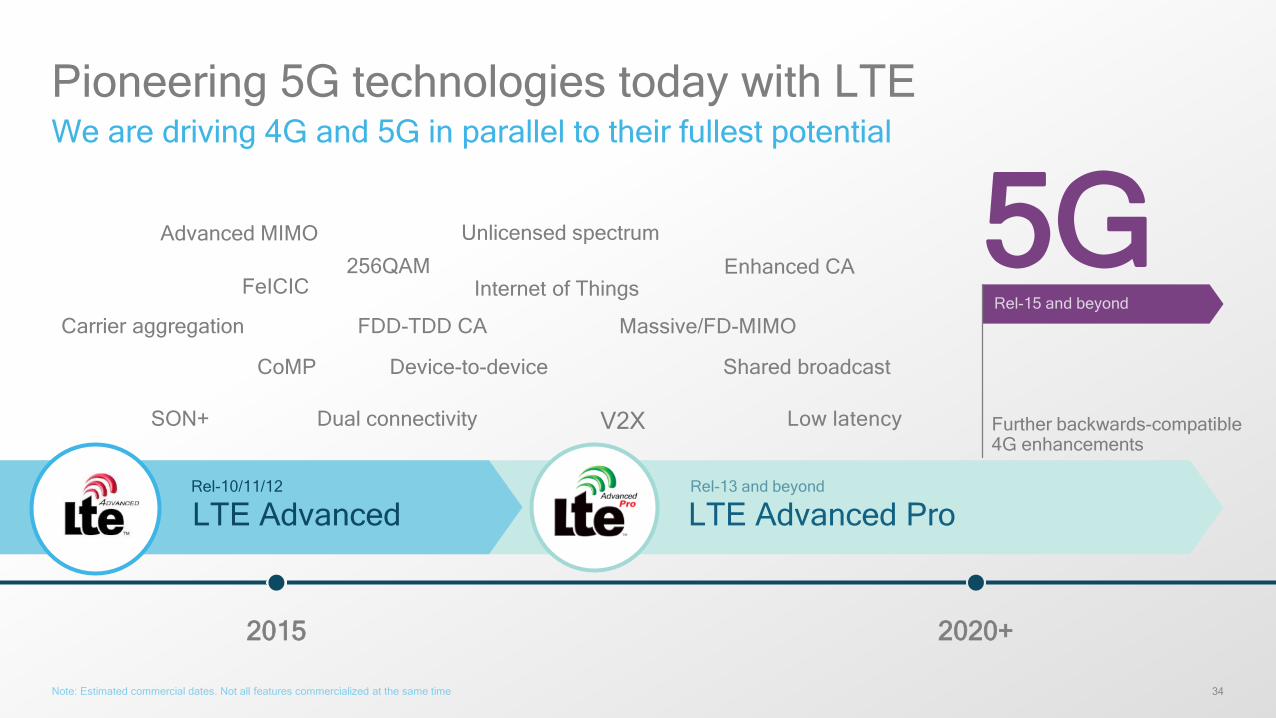

Pioneering 5G technologies today with LTEWe are driving 4G and 5G in parallel to their fullest potential

Note: Estimated commercial dates. Not all features commercialized at the same time

Further backwards-compatible 4G enhancements

5GCarrier aggregation

Dual connectivitySON+

Massive/FD-MIMO

CoMP Device-to-device

Unlicensed spectrum

Enhanced CA

Shared broadcast

Internet of Things256QAM

V2X

FeICIC

Advanced MIMO

FDD-TDD CA

Low latency

LTE Advanced ProLTE AdvancedRel-10/11/12

2015 2020+

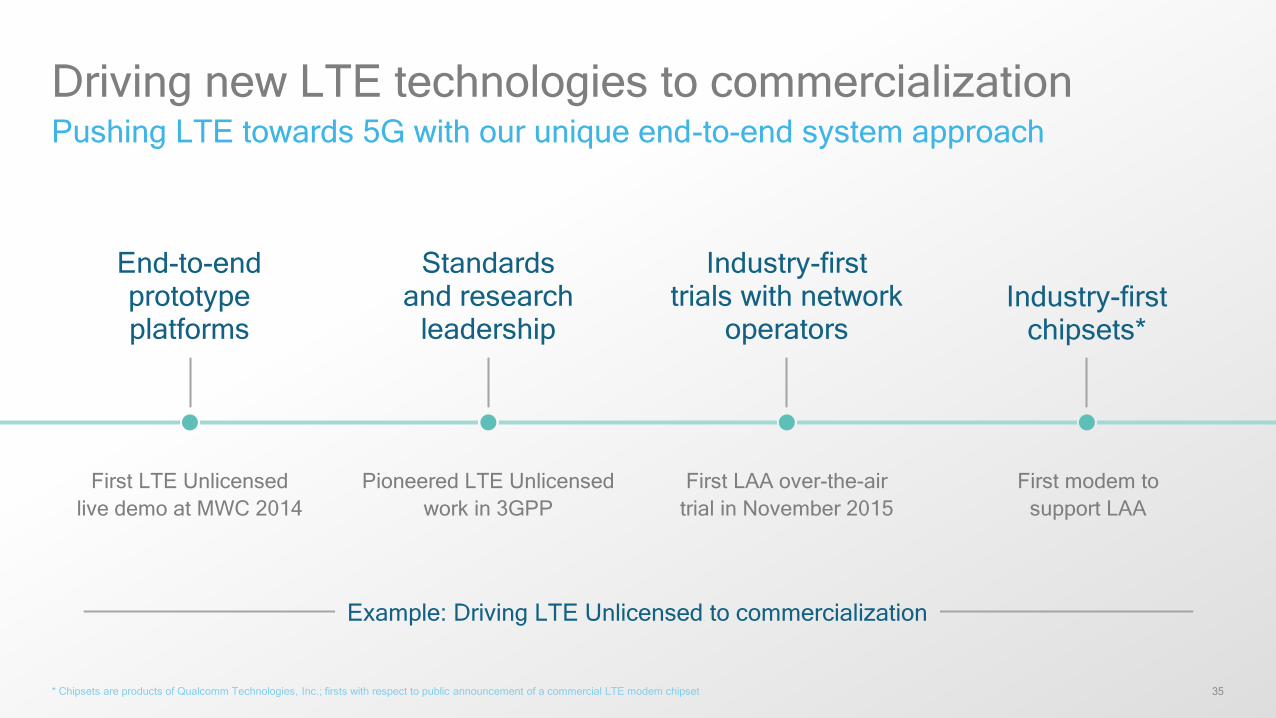

35

Driving new LTE technologies to commercializationPushing LTE towards 5G with our unique end-to-end system approach

* Chipsets are products of Qualcomm Technologies, Inc.; firsts with respect to public announcement of a commercial LTE modem chipset

Pioneered LTE Unlicensedwork in 3GPP

First modem to support LAA

First LTE Unlicensedlive demo at MWC 2014

First LAA over-the-airtrial in November 2015

End-to-end prototype platforms

Standards and research

leadership

Industry-first trials with network

operatorsIndustry-first

chipsets*

Example: Driving LTE Unlicensed to commercialization

36

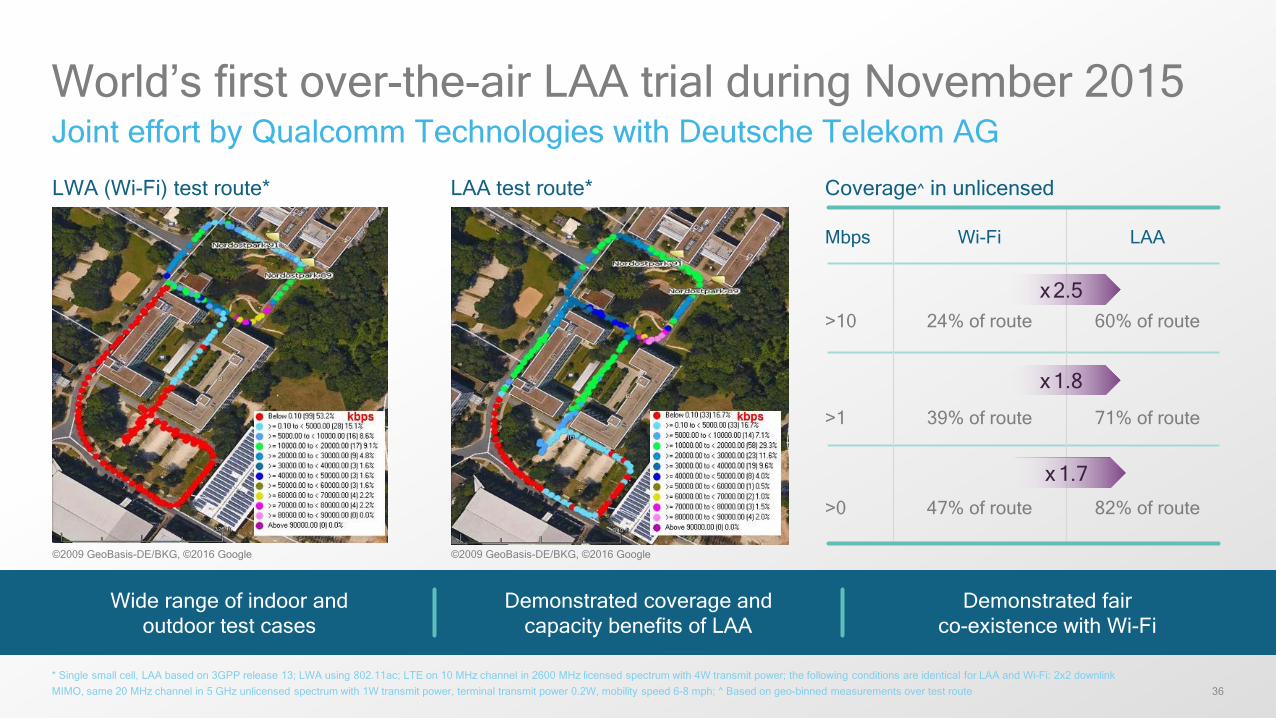

World’s first over-the-air LAA trial during November 2015Joint effort by Qualcomm Technologies with Deutsche Telekom AG

* Single small cell, LAA based on 3GPP release 13; LWA using 802.11ac; LTE on 10 MHz channel in 2600 MHz licensed spectrum with 4W transmit power; the following conditions are identical for LAA and Wi-Fi: 2x2 downlink MIMO, same 20 MHz channel in 5 GHz unlicensed spectrum with 1W transmit power, terminal transmit power 0.2W, mobility speed 6-8 mph; ^ Based on geo-binned measurements over test route

LAA test route* Coverage^ in unlicensed

Mbps Wi-Fi LAA

>10 24% of route 60% of route

>1 39% of route 71% of route

>0 47% of route 82% of route

x2.5

x1.8

x1.7

LWA (Wi-Fi) test route*

©2009 GeoBasis-DE/BKG, ©2016 Google©2009 GeoBasis-DE/BKG, ©2016 Google

Demonstrated coverage and capacity benefits of LAA

Wide range of indoor and outdoor test cases

Demonstrated fair co-existence with Wi-Fi

37

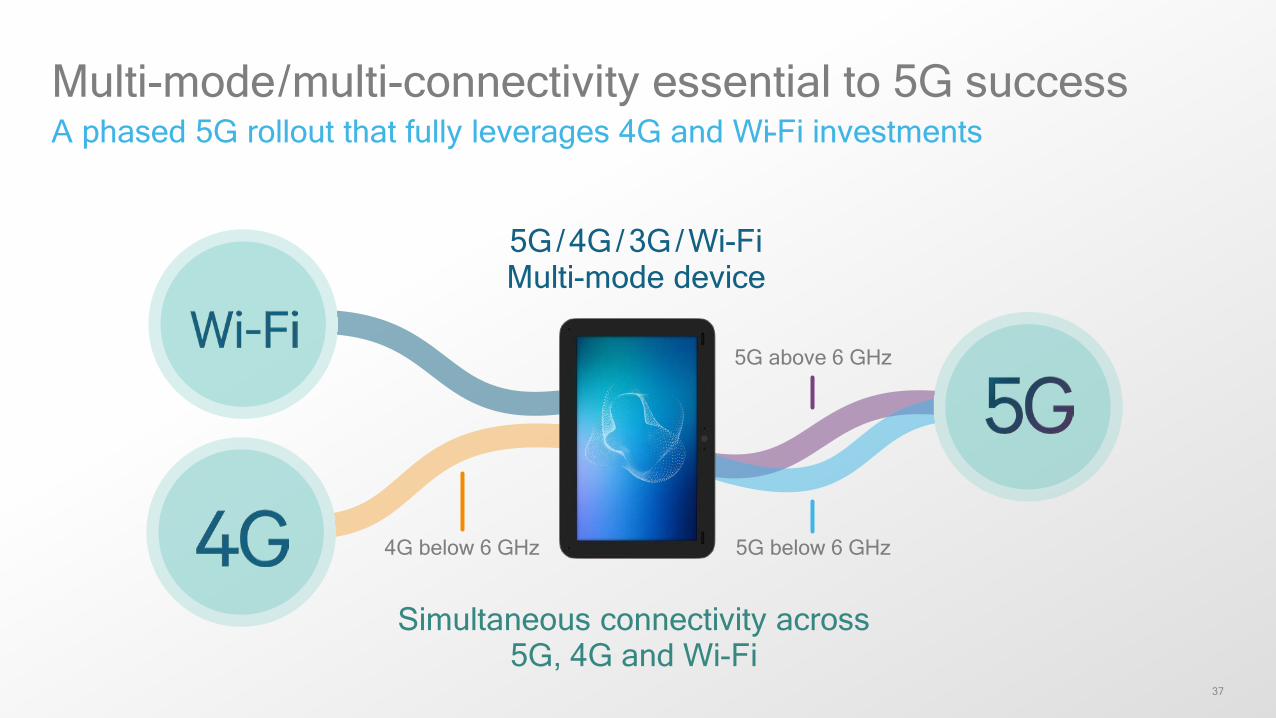

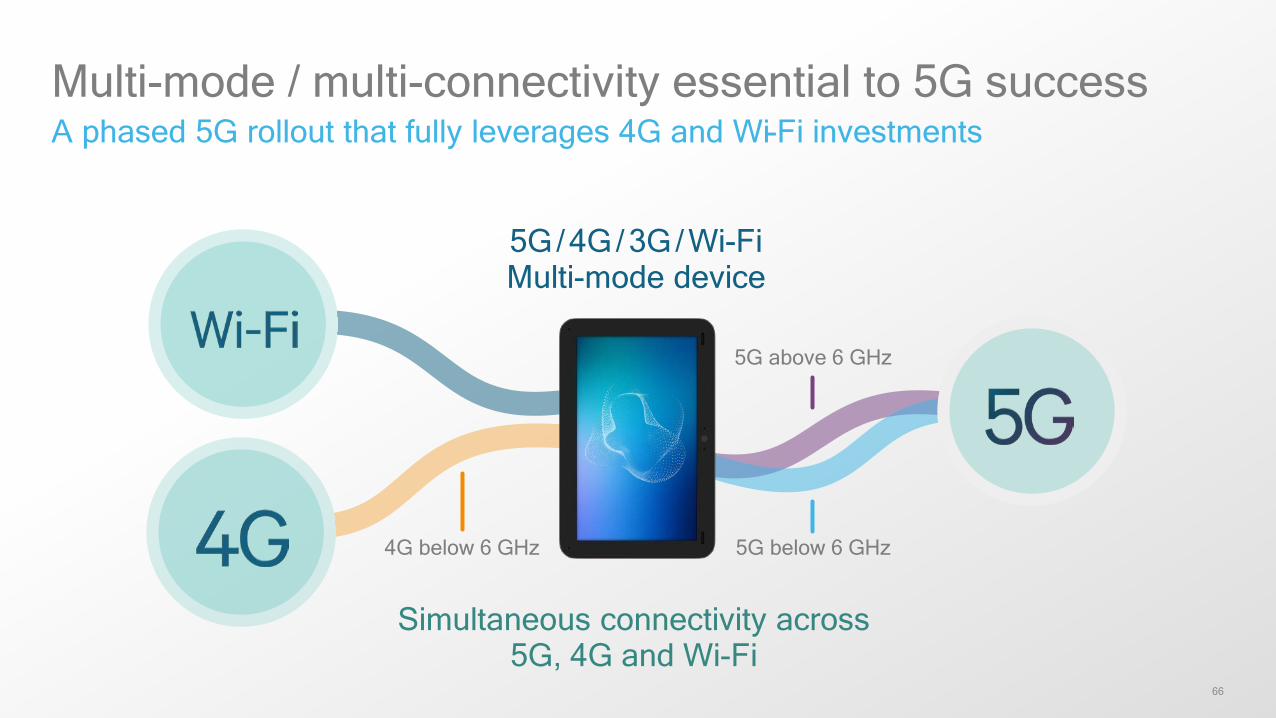

Multi-mode/multi-connectivity essential to 5G successA phased 5G rollout that fully leverages 4G and Wi-Fi investments

4G below 6 GHz

5G above 6 GHz

5G below 6 GHz

5G/4G/3G/Wi-FiMulti-mode device

Simultaneous connectivity across 5G, 4G and Wi-Fi

38

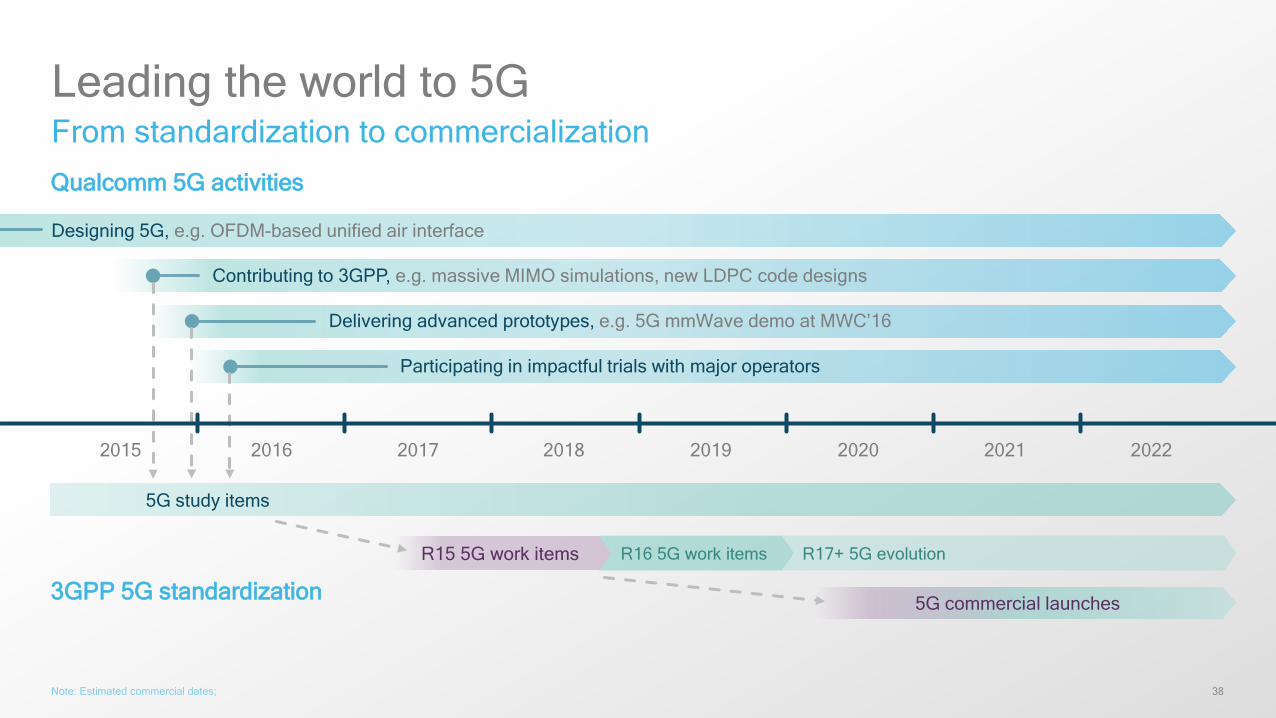

Delivering advanced prototypes, e.g. 5G mmWave demo at MWC’16

R17+ 5G evolution

Leading the world to 5G

Note: Estimated commercial dates;

R16 5G work items

5G commercial launches

R15 5G work items

5G study items

3GPP 5G standardization

Qualcomm 5G activities

Designing 5G, e.g. OFDM-based unified air interface

Participating in impactful trials with major operators

Contributing to 3GPP, e.g. massive MIMO simulations, new LDPC code designs

2016 20212017 2019 2020 20222015 2018

From standardization to commercialization

39

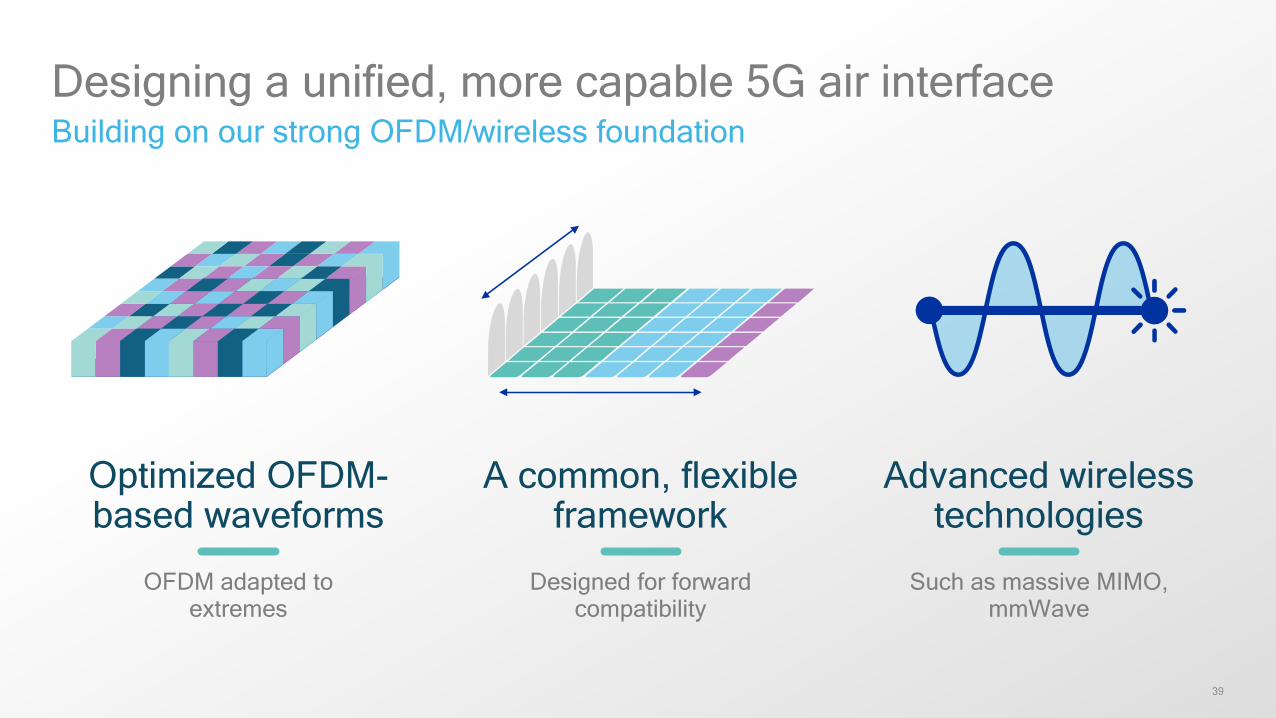

Designing a unified, more capable 5G air interfaceBuilding on our strong OFDM/wireless foundation

Optimized OFDM-based waveforms

A common, flexibleframework

Advanced wireless technologies

OFDM adapted to extremes

Such as massive MIMO, mmWave

Designed for forward compatibility

40

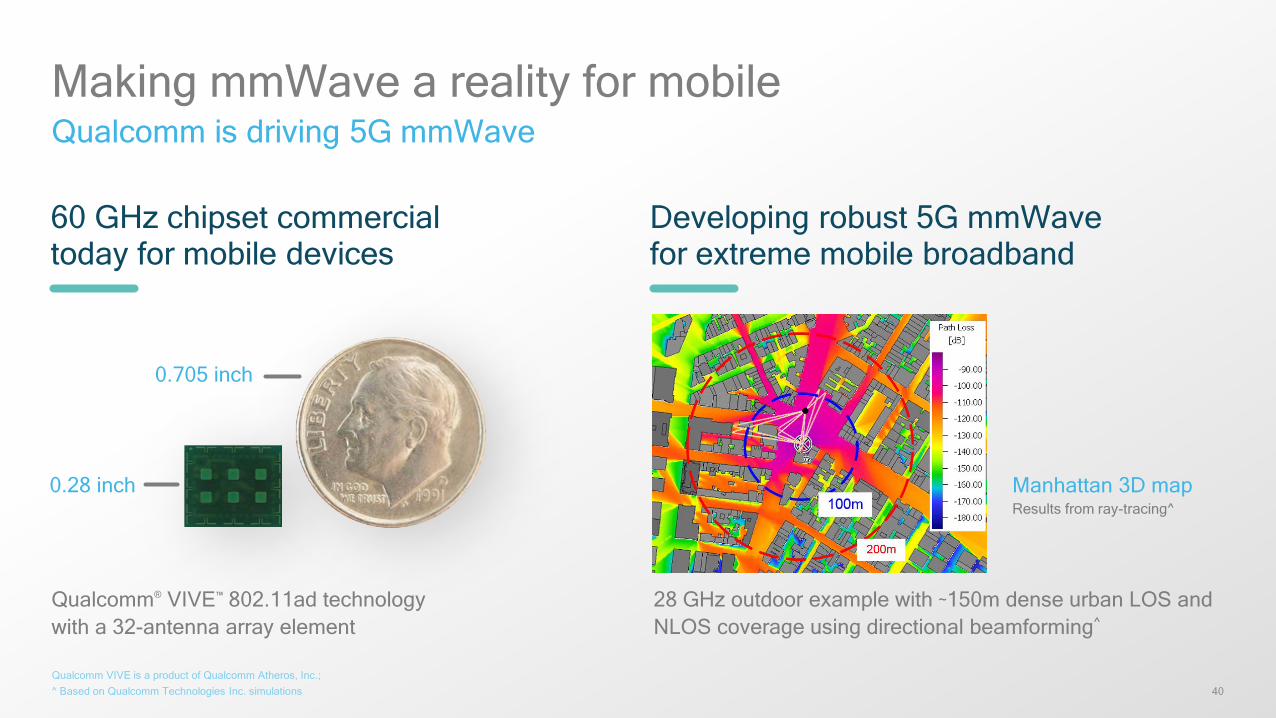

Making mmWave a reality for mobileQualcomm is driving 5G mmWave

Qualcomm VIVE is a product of Qualcomm Atheros, Inc.;^ Based on Qualcomm Technologies Inc. simulations

Qualcomm® VIVE™ 802.11ad technology with a 32-antenna array element

60 GHz chipset commercial today for mobile devices

Developing robust 5G mmWavefor extreme mobile broadband

0.705 inch

0.28 inch

28 GHz outdoor example with ~150m dense urban LOS and NLOS coverage using directional beamforming^

Manhattan 3D mapResults from ray-tracing^

41

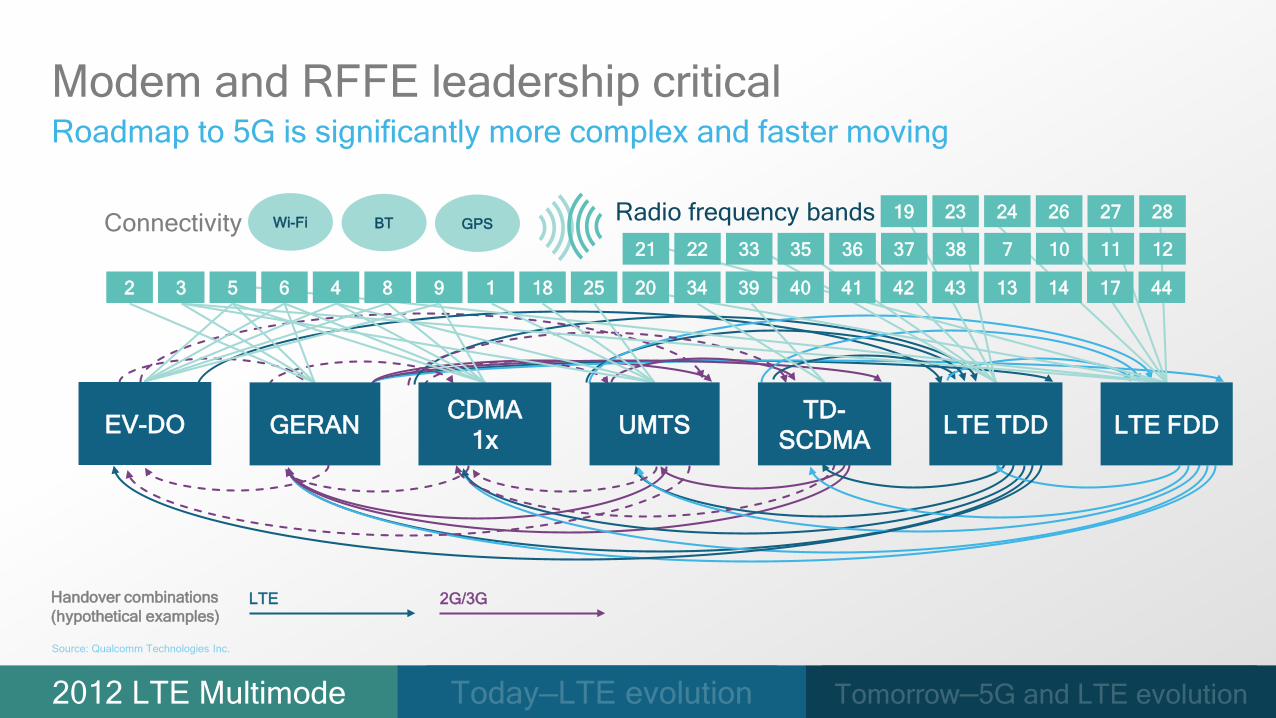

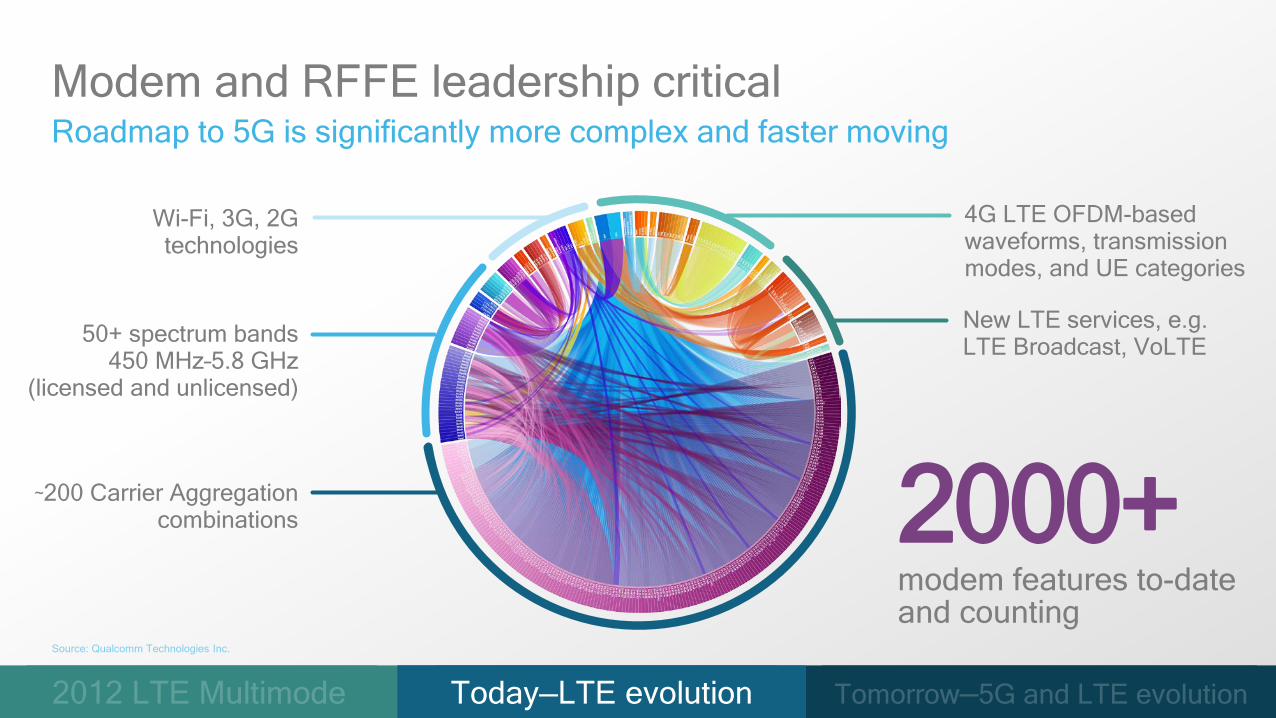

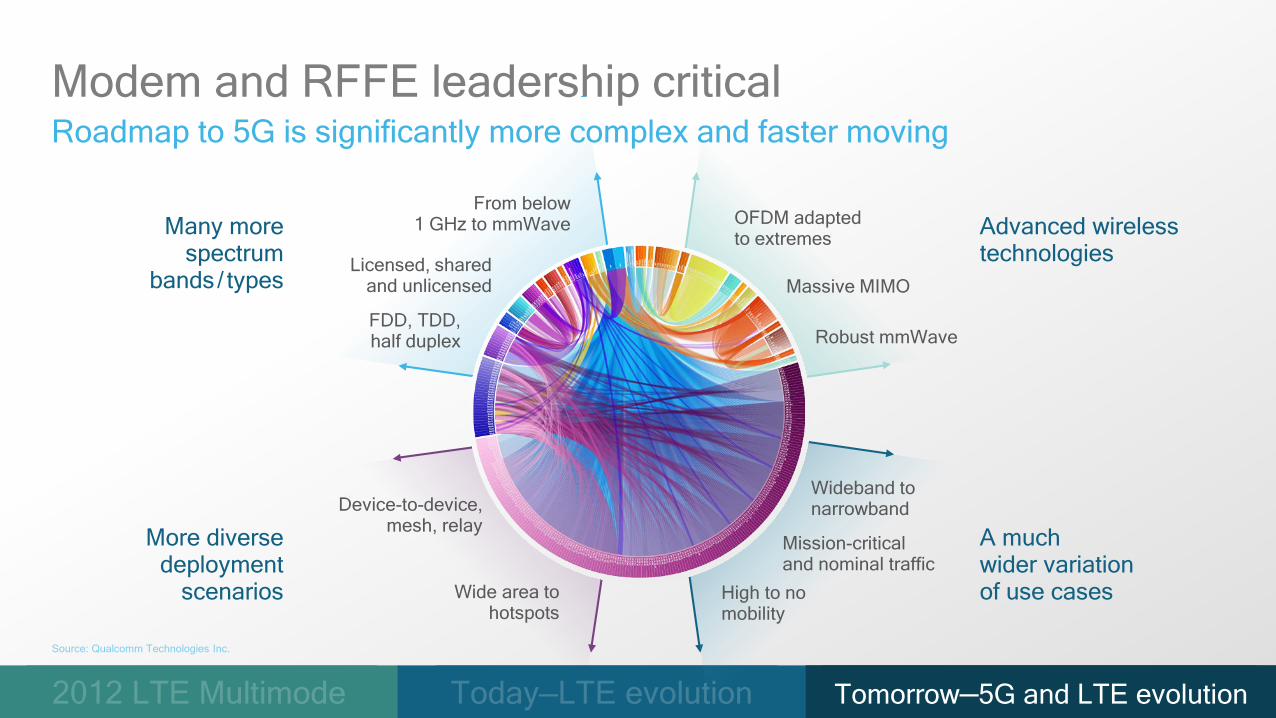

Modem and RFFE leadership critical Roadmap to 5G is significantly more complex and faster moving

Source: Qualcomm Technologies Inc.

2012 LTE Multimode Today—LTE evolution Tomorrow—5G and LTE evolution

LTE 2G/3GHandover combinations (hypothetical examples)

GERAN CDMA 1x UMTS TD-

SCDMA LTE TDD LTE FDDEV-DO

Connectivity Wi-Fi BT GPS

22 33

27

35 36 37 38

39 40 41 42 4312 83 45 6 9

28

34

7 10 11 12

13 14 17 4418

19

20

21

23 24

25

26Radio frequency bands

42

GERAN CDMA 1x UMTS TD-

SCDMA LTE TDD LTE FDDEV-DO

Connectivity Wi-Fi BT GPS

22 33

27

35 36 37 38

39 40 41 42 4312 83 45 6 9

28

34

7 10 11 12

13 14 17 4418

19

20

21

23 24

25

26Radio frequency bands

Modem and RFFE leadership critical Roadmap to 5G is significantly more complex and faster moving

Source: Qualcomm Technologies Inc.,

2000+modem features to-date and counting

50+ spectrum bands450 MHz–5.8 GHz

(licensed and unlicensed)

~200 Carrier Aggregationcombinations

New LTE services, e.g. LTE Broadcast, VoLTE

Wi-Fi, 3G, 2G technologies

4G LTE OFDM-based waveforms, transmission modes, and UE categories

2012 LTE Multimode Tomorrow—5G and LTE evolution

Source: Qualcomm Technologies Inc.

Today—LTE evolutionToday—LTE evolution

43

Modem and RFFE leadership critical Roadmap to 5G is significantly more complex and faster moving

Source: Qualcomm Technologies Inc., 2012 LTE Multimode Tomorrow – 5G and LTE evolutionToday—LTE evolution Tomorrow—5G and LTE evolution

More diverse deployment

scenarios

Many more spectrum

bands/ types

A much wider variation of use cases

Advanced wireless technologies

FDD, TDD, half duplex

Licensed, shared and unlicensed

From below 1 GHz to mmWave OFDM adapted

to extremes

Massive MIMO

Robust mmWave

Mission-critical and nominal traffic

High to no mobility

Device-to-device, mesh, relay

Wide area to hotspots

Wideband to narrowband

Source: Qualcomm Technologies Inc.

44

Empowering new user experiences

Connecting new industries and devices

Enabling new services

Delivering new levels of efficiency

Leading the world to 5GA unifying connectivity fabric for the next decade and beyond

Derek Aberle

President, Qualcomm Incorporated

46

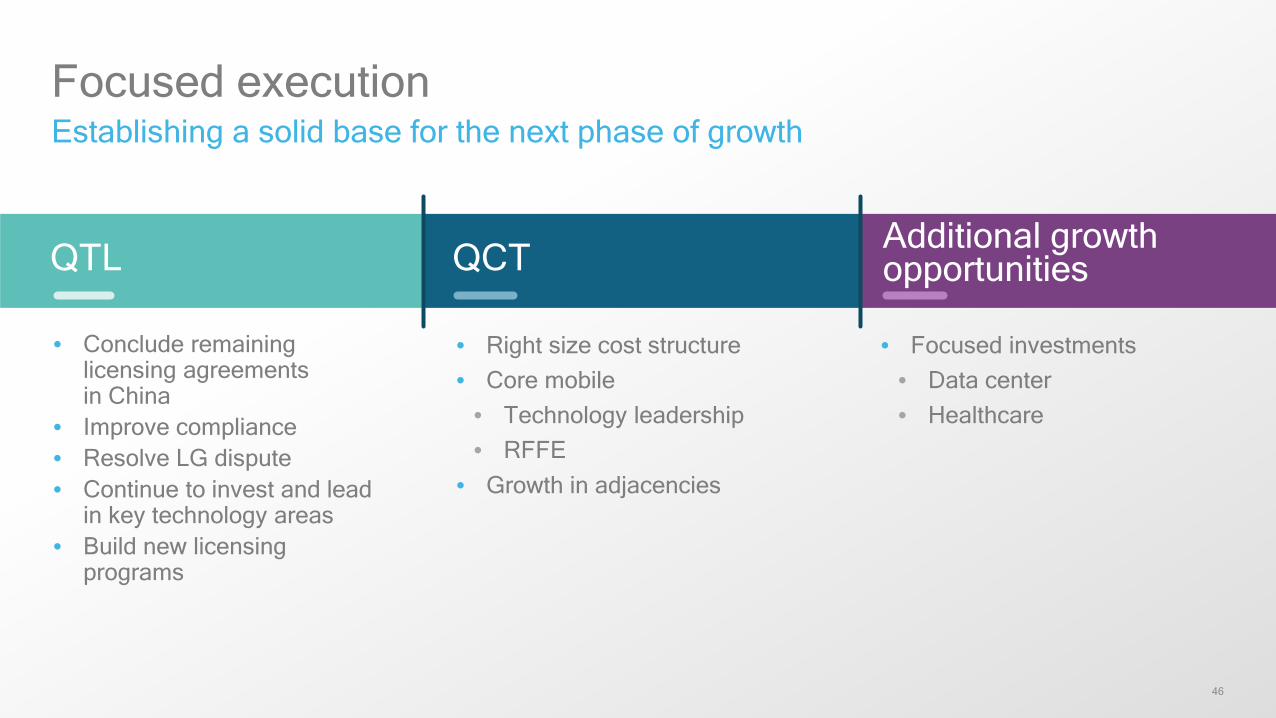

Focused executionEstablishing a solid base for the next phase of growth

QTL Additional growth opportunities

• Right size cost structure• Core mobile

• Technology leadership• RFFE

• Growth in adjacencies

• Conclude remaining licensing agreements in China

• Improve compliance• Resolve LG dispute• Continue to invest and lead

in key technology areas• Build new licensing

programs

• Focused investments• Data center• Healthcare

QCT

QTL: China update

48

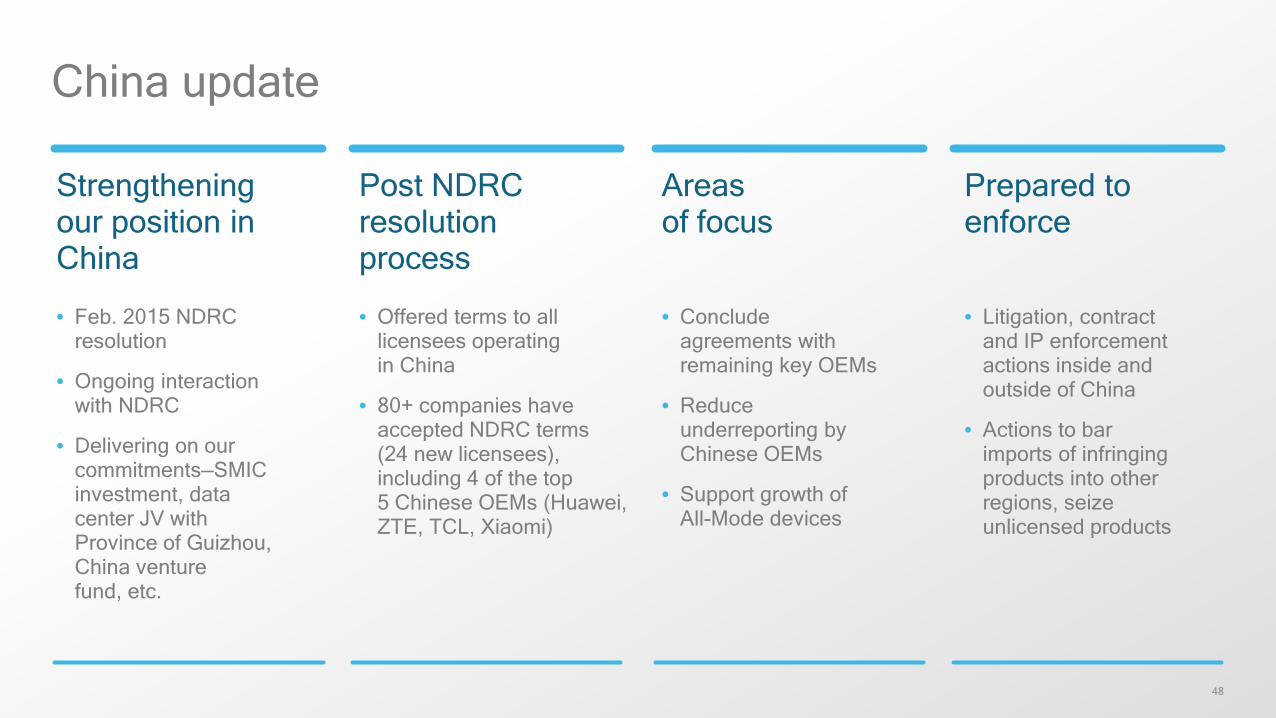

China update

Strengthening our position in China

• Feb. 2015 NDRC resolution

• Ongoing interaction with NDRC

• Delivering on our commitments—SMIC investment, data center JV with Province of Guizhou, China venture fund, etc.

Post NDRC resolution process

• Offered terms to all licensees operating in China

• 80+ companies have accepted NDRC terms (24 new licensees), including 4 of the top 5 Chinese OEMs (Huawei, ZTE, TCL, Xiaomi)

Areas of focus

Prepared to enforce

• Litigation, contract and IP enforcement actions inside and outside of China

• Actions to bar imports of infringing products into other regions, seize unlicensed products

• Conclude agreements with remaining key OEMs

• Reduce underreporting by Chinese OEMs

• Support growth of All-Mode devices

49

Compliance program

• Quarterly licensee reporting• Active ongoing engagement between QTL and licensees

• Increasing presence in China and other emerging regions

• Extensive licensee audits, ~120 planned in FY2016

• Market analysis and research• Data from multiple third-party sources

• Tear-downs of devices purchased

• Import and export customs data

• Device network activation data

• Contractual dispute resolution mechanisms

• Actions to bar imports of infringing products, seize unlicensed products

• Educating customers of risks of buying unlicensed devices

• Civil and criminal infringement actions

Source: Company data.

50

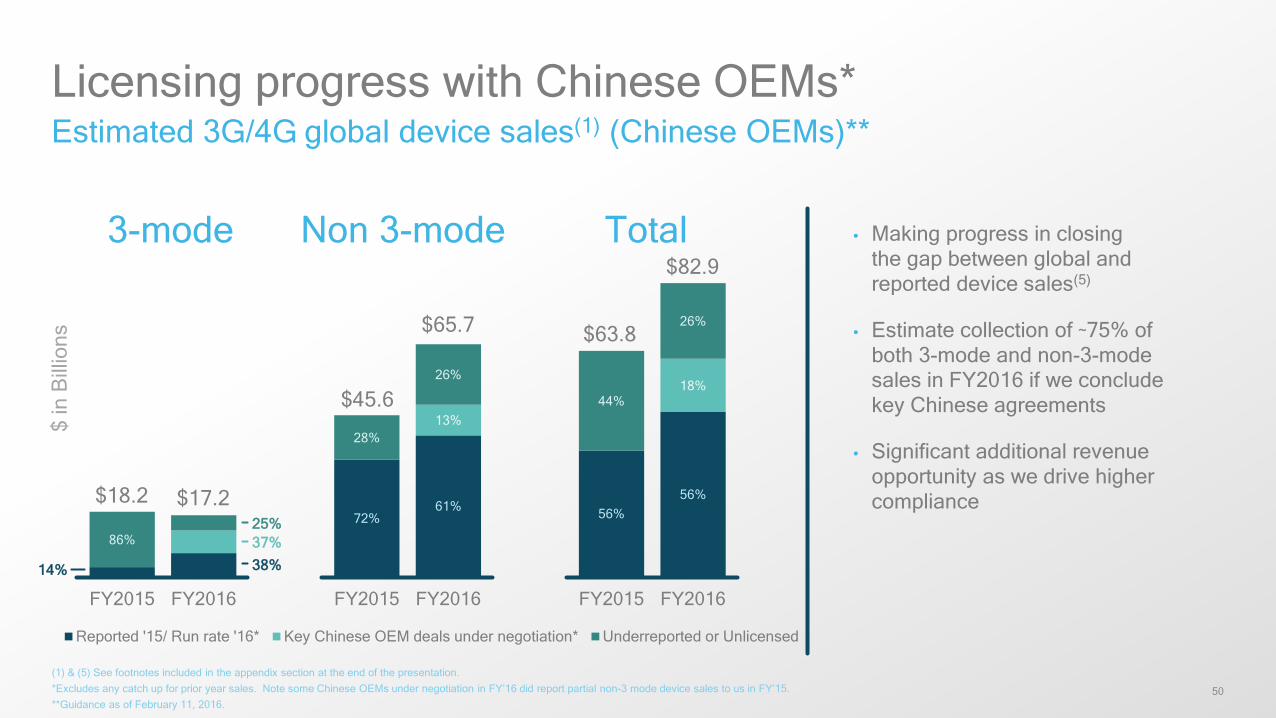

Licensing progress with Chinese OEMs*Estimated 3G/4G global device sales(1) (Chinese OEMs)**

(1) & (5) See footnotes included in the appendix section at the end of the presentation. *Excludes any catch up for prior year sales. Note some Chinese OEMs under negotiation in FY’16 did report partial non-3 mode device sales to us in FY’15. **Guidance as of February 11, 2016.

72%61% 56%

56%

13%

18%

86%

28%

26%

44%

26%

FY2015 FY2016 FY2015 FY2016 FY2015 FY2016

Reported '15/ Run rate '16* Key Chinese OEM deals under negotiation* Underreported or Unlicensed

$ in

Bill

ions

$17.2$18.2

$82.9

$63.8$65.7

$45.6

3-mode Non 3-mode Total • Making progress in closing the gap between global and reported device sales(5)

• Estimate collection of ~75% of both 3-mode and non-3-mode sales in FY2016 if we conclude key Chinese agreements

• Significant additional revenue opportunity as we drive higher compliance

25%37%

14% 38%

3G/4G deviceopportunity

3G 4G

52

FY2013 FY2014 FY2015 FY2020e

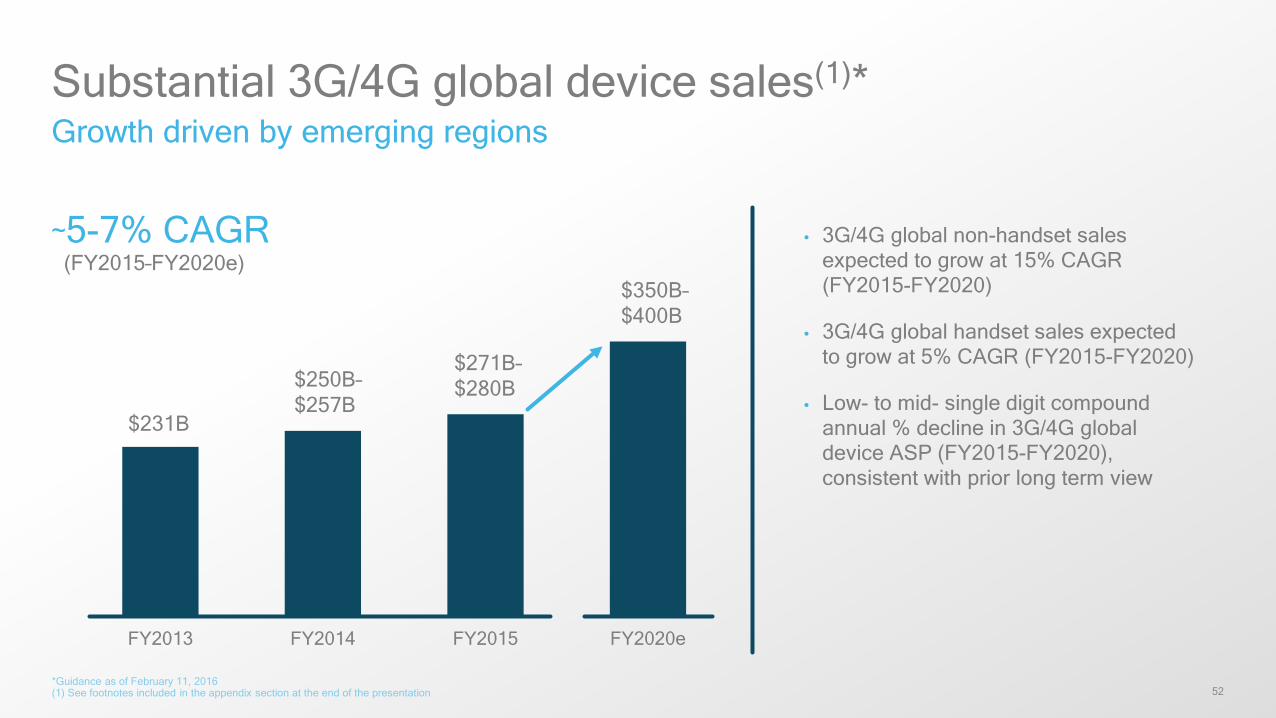

Substantial 3G/4G global device sales(1)*Growth driven by emerging regions

• 3G/4G global non-handset sales expected to grow at 15% CAGR (FY2015-FY2020)

• 3G/4G global handset sales expected to grow at 5% CAGR (FY2015-FY2020)

• Low- to mid- single digit compound annual % decline in 3G/4G global device ASP (FY2015-FY2020), consistent with prior long term view

$231B

$250B–$257B

$271B–$280B

$350B–$400B

~5-7% CAGR(FY2015–FY2020e)

*Guidance as of February 11, 2016(1) See footnotes included in the appendix section at the end of the presentation

53

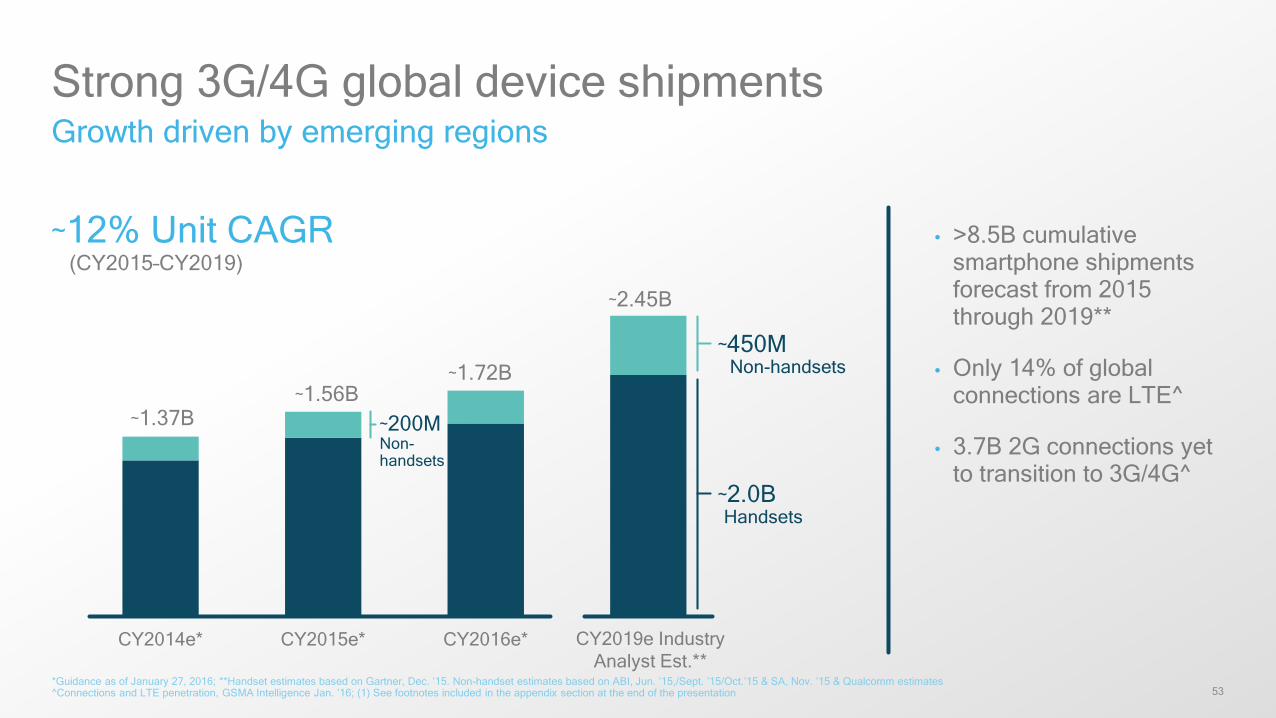

CY2014e* CY2015e* CY2016e* CY2019e **

Strong 3G/4G global device shipmentsGrowth driven by emerging regions

• >8.5B cumulative smartphone shipments forecast from 2015 through 2019**

• Only 14% of global connections are LTE^

• 3.7B 2G connections yet to transition to 3G/4G^

*Guidance as of January 27, 2016; **Handset estimates based on Gartner, Dec. ’15. Non-handset estimates based on ABI, Jun. ’15,/Sept. ’15/Oct.’15 & SA, Nov. ’15 & Qualcomm estimates^Connections and LTE penetration, GSMA Intelligence Jan. ’16; (1) See footnotes included in the appendix section at the end of the presentation

CY2019e Industry Analyst Est.**

~200MNon-handsets

~450M Non-handsets

~1.37B~1.56B

~1.72B

~2.45B

~12% Unit CAGR(CY2015–CY2019)

~2.0B Handsets

Smartphones

55

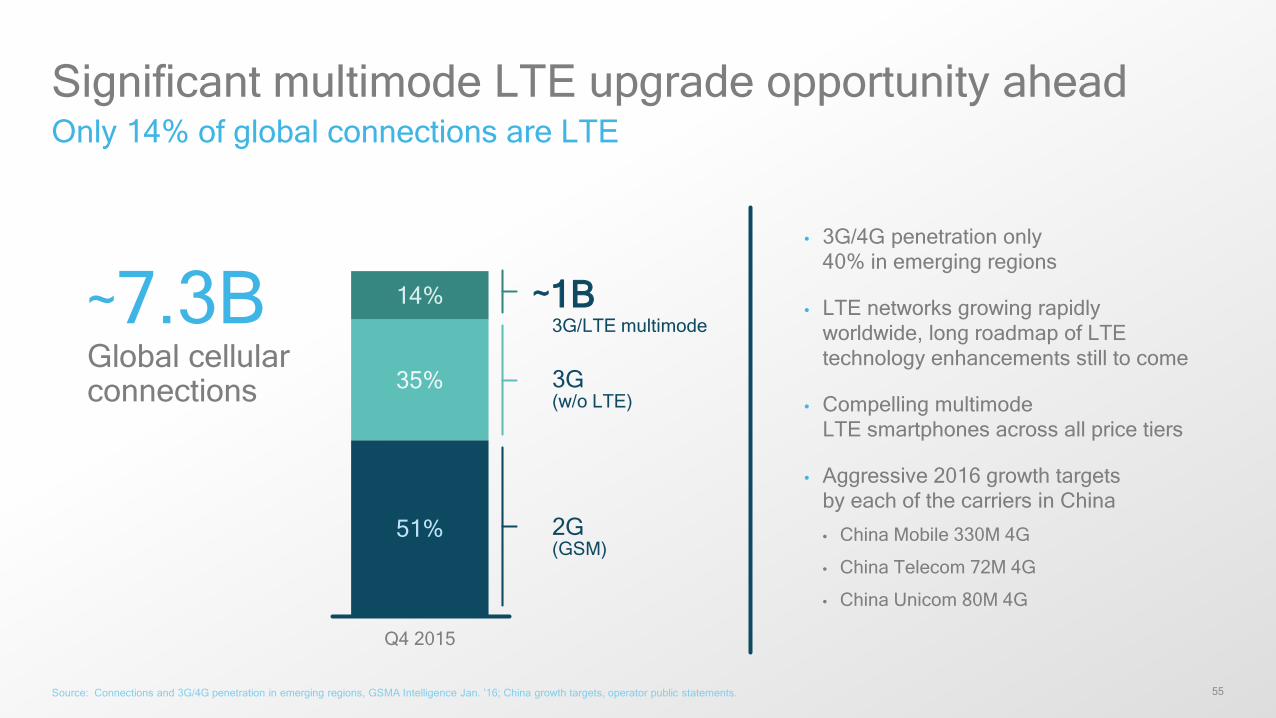

51%

35%

14%

Q4 2015

Significant multimode LTE upgrade opportunity aheadOnly 14% of global connections are LTE

~7.3BGlobal cellular connections

~1B3G/LTE multimode

3G (w/o LTE)

2G(GSM)

• 3G/4G penetration only 40% in emerging regions

• LTE networks growing rapidly worldwide, long roadmap of LTE technology enhancements still to come

• Compelling multimode LTE smartphones across all price tiers

• Aggressive 2016 growth targets by each of the carriers in China

• China Mobile 330M 4G

• China Telecom 72M 4G

• China Unicom 80M 4G

Source: Connections and 3G/4G penetration in emerging regions, GSMA Intelligence Jan. ’16; China growth targets, operator public statements.

56

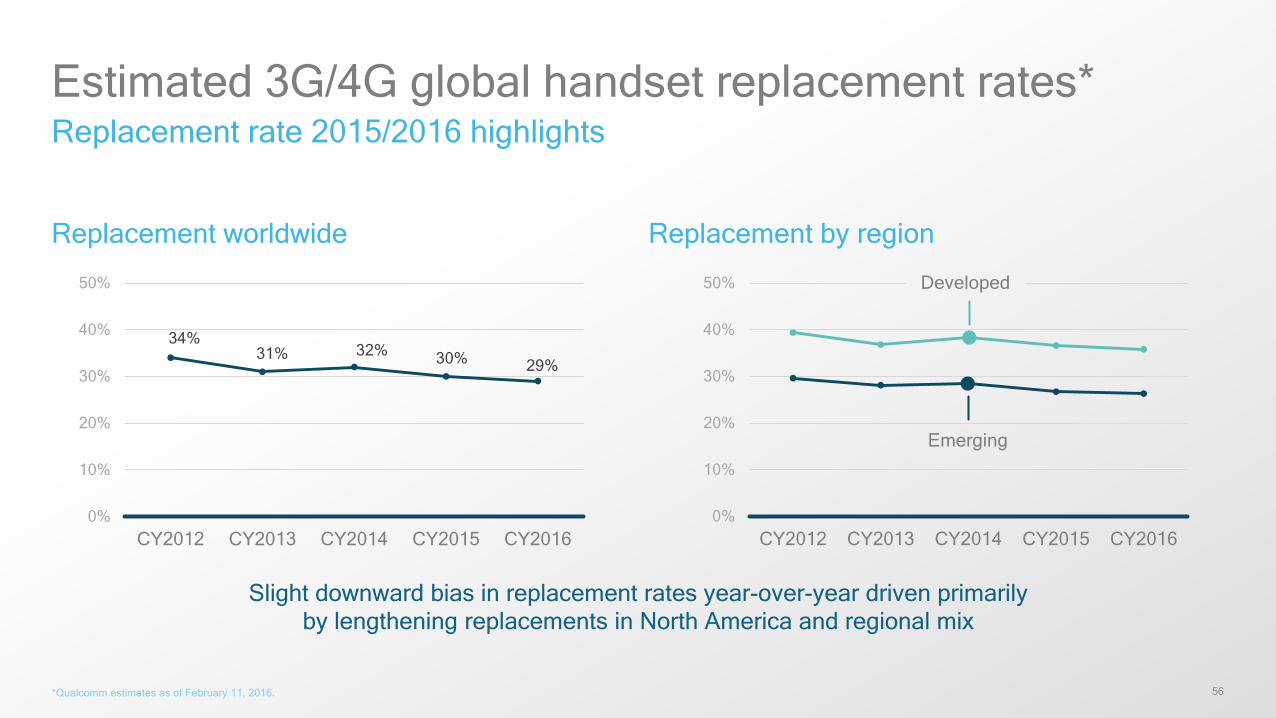

Estimated 3G/4G global handset replacement rates*Replacement rate 2015/2016 highlights

Replacement worldwide

Slight downward bias in replacement rates year-over-year driven primarily by lengthening replacements in North America and regional mix

34%31% 32% 30% 29%

0%

10%

20%

30%

40%

50%

CY2012 CY2013 CY2014 CY2015 CY20160%

10%

20%

30%

40%

50%

CY2012 CY2013 CY2014 CY2015 CY2016

Developed

Emerging

Replacement by region

*Qualcomm estimates as of February 11, 2016.

57

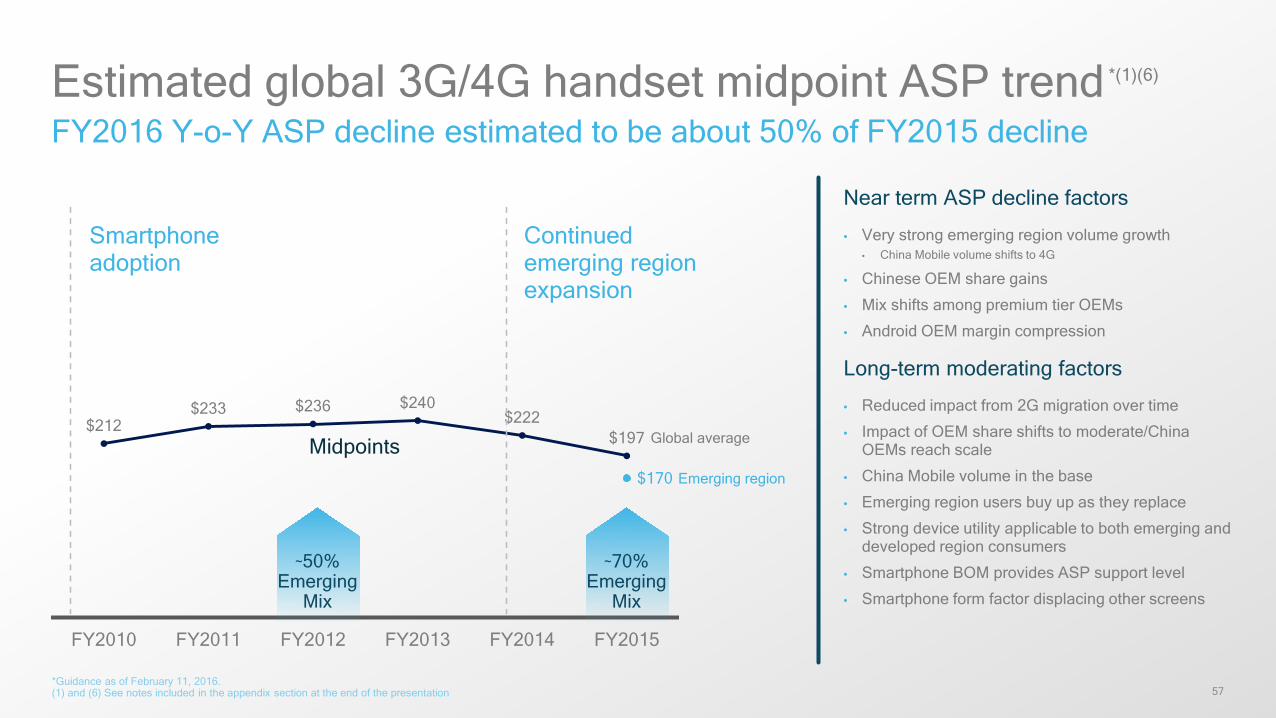

$212$233 $236 $240

$222$197

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

Estimated global 3G/4G handset midpoint ASP trend *(1)(6)

Smartphone adoption

Midpoints

Continued emerging region expansion

Near term ASP decline factors

• Very strong emerging region volume growth• China Mobile volume shifts to 4G

• Chinese OEM share gains

• Mix shifts among premium tier OEMs

• Android OEM margin compression

Long-term moderating factors

• Reduced impact from 2G migration over time

• Impact of OEM share shifts to moderate/China OEMs reach scale

• China Mobile volume in the base

• Emerging region users buy up as they replace

• Strong device utility applicable to both emerging and developed region consumers

• Smartphone BOM provides ASP support level

• Smartphone form factor displacing other screens

*Guidance as of February 11, 2016. (1) and (6) See notes included in the appendix section at the end of the presentation

FY2016 Y-o-Y ASP decline estimated to be about 50% of FY2015 decline

~70% Emerging

Mix

$170

Global average

Emerging region

~50% Emerging

Mix

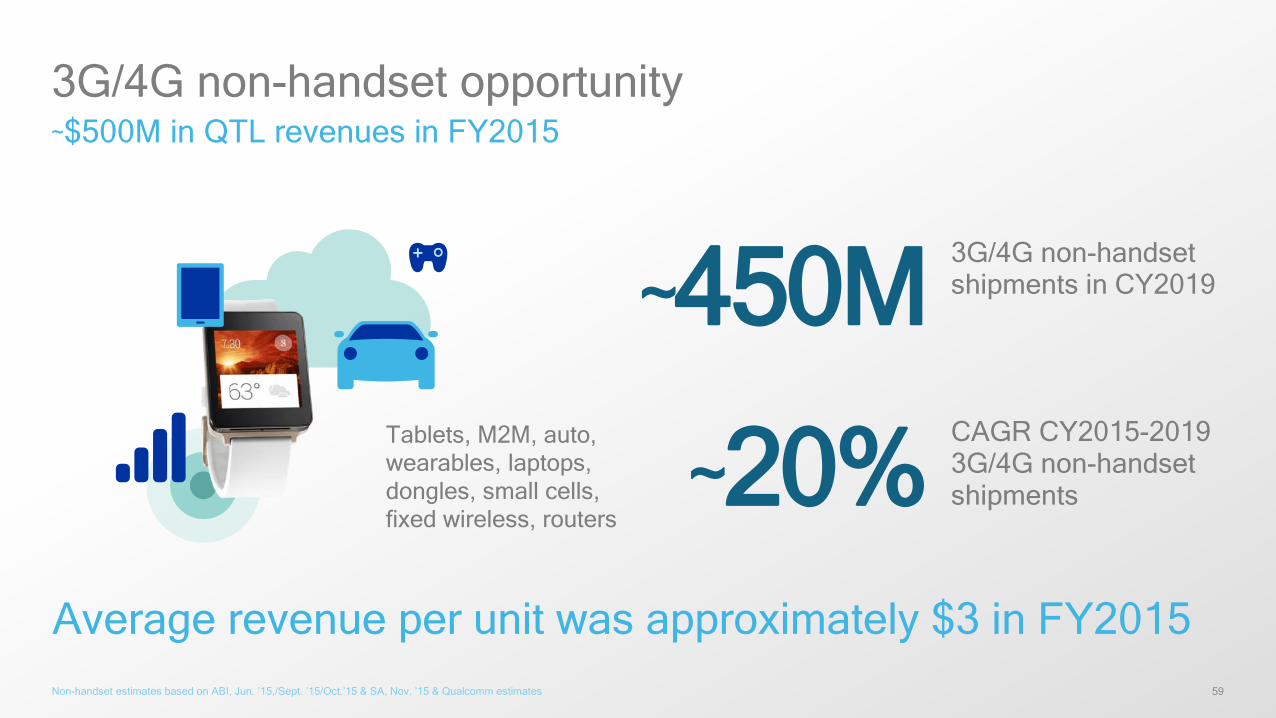

Non-handsets

59

3G/4G non-handset opportunity~$500M in QTL revenues in FY2015

Non-handset estimates based on ABI, Jun. ’15,/Sept. ’15/Oct.’15 & SA, Nov. ’15 & Qualcomm estimates

~20% CAGR CY2015-20193G/4G non-handset shipments

Tablets, M2M, auto, wearables, laptops, dongles, small cells, fixed wireless, routers

~450M 3G/4G non-handset shipments in CY2019

Average revenue per unit was approximately $3 in FY2015

60

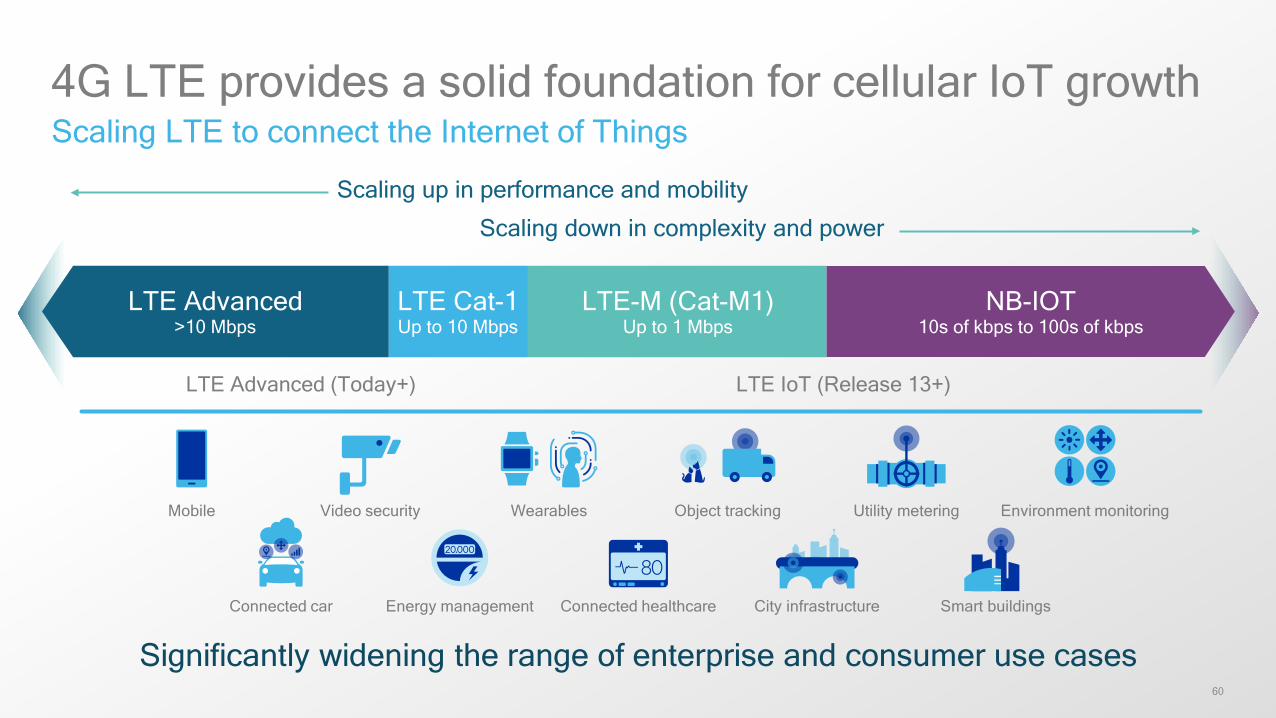

4G LTE provides a solid foundation for cellular IoT growthScaling LTE to connect the Internet of Things

Significantly widening the range of enterprise and consumer use cases

Scaling up in performance and mobility

Scaling down in complexity and power

LTE Advanced (Today+) LTE IoT (Release 13+)

LTE Advanced>10 Mbps

LTE Cat-1Up to 10 Mbps

LTE-M (Cat-M1)Up to 1 Mbps

NB-IOT10s of kbps to 100s of kbps

Object trackingMobile

Connected car Energy management

Video security Utility meteringWearables

Connected healthcare

Environment monitoring

Smart buildingsCity infrastructure

Implied royalty rate

3G

4G

62

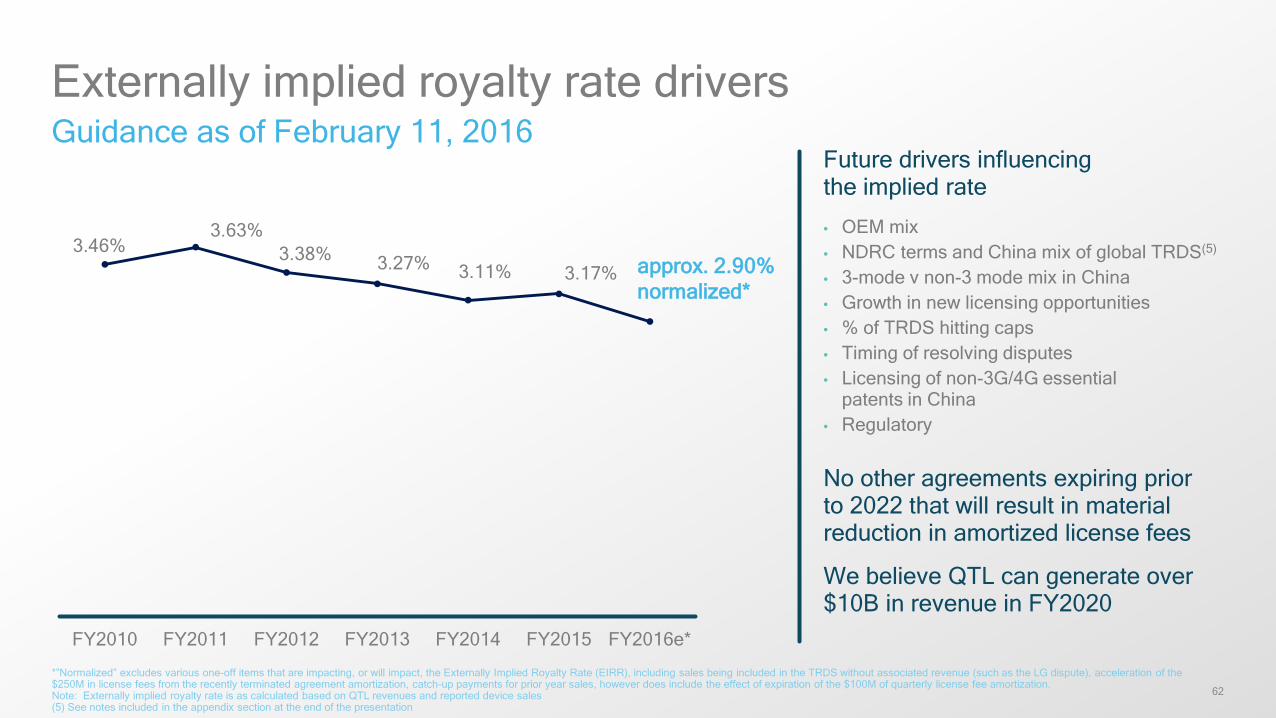

3.46%3.63%

3.38% 3.27% 3.11% 3.17%

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 FY2016e*

Externally implied royalty rate drivers Guidance as of February 11, 2016

Future drivers influencing the implied rate

• OEM mix• NDRC terms and China mix of global TRDS(5)

• 3-mode v non-3 mode mix in China• Growth in new licensing opportunities• % of TRDS hitting caps • Timing of resolving disputes• Licensing of non-3G/4G essential

patents in China• Regulatory

No other agreements expiring prior to 2022 that will result in material reduction in amortized license fees

We believe QTL can generate over $10B in revenue in FY2020

*”Normalized” excludes various one-off items that are impacting, or will impact, the Externally Implied Royalty Rate (EIRR), including sales being included in the TRDS without associated revenue (such as the LG dispute), acceleration of the $250M in license fees from the recently terminated agreement amortization, catch-up payments for prior year sales, however does include the effect of expiration of the $100M of quarterly license fee amortization. Note: Externally implied royalty rate is as calculated based on QTL revenues and reported device sales(5) See notes included in the appendix section at the end of the presentation

approx. 2.90% normalized*

Licensing model

64

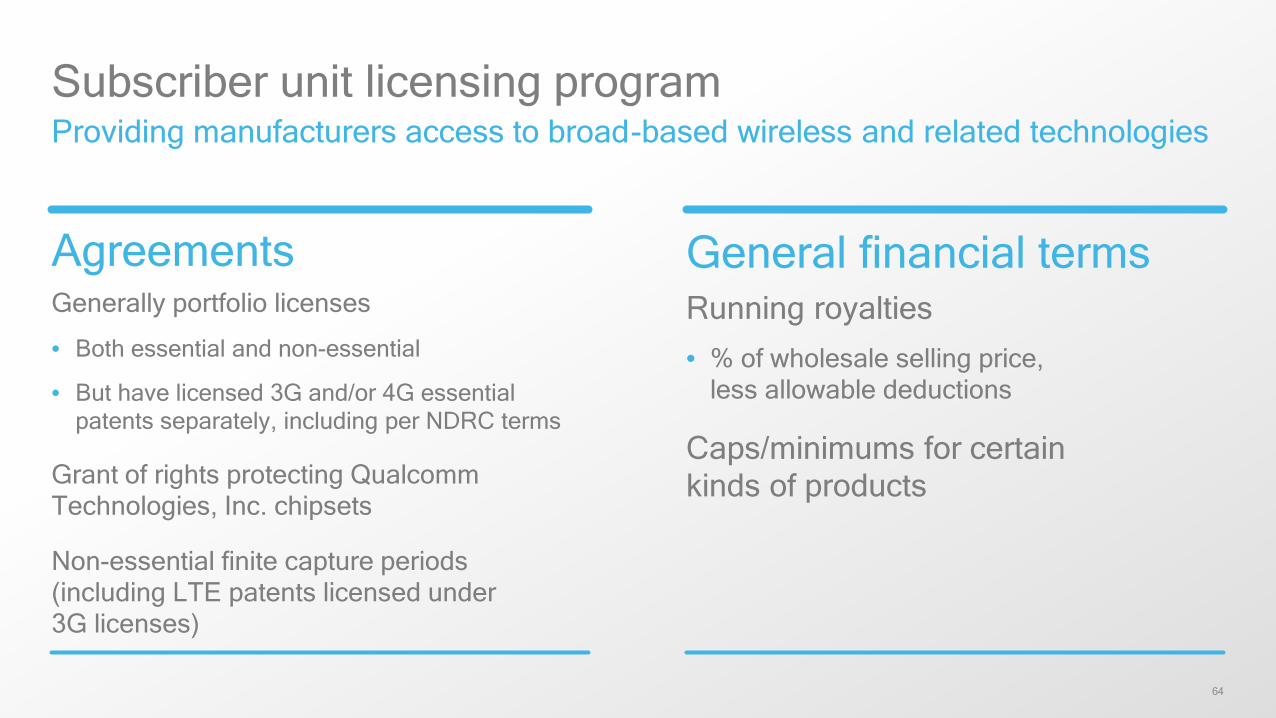

Subscriber unit licensing programProviding manufacturers access to broad-based wireless and related technologies

General financial termsRunning royalties• % of wholesale selling price,

less allowable deductions

Caps/minimums for certain kinds of products

AgreementsGenerally portfolio licenses

• Both essential and non-essential

• But have licensed 3G and/or 4G essential patents separately, including per NDRC terms

Grant of rights protecting Qualcomm Technologies, Inc. chipsets

Non-essential finite capture periods (including LTE patents licensed under 3G licenses)

65

Qualcomm’s key contributions to LTE and beyond

Multi-radio support• Inter-RAT handover • Mobile device multi-radio

coexistence • Circuit switched fallback

(CSFB) • Mobile device-assisted

network optimization

Lower power consumptiontechnologies• Uplink communications:

“Single Carrier FDMA” • Downlink communications:

OFDMA

LTE-TDD specific features• Base station synchronization • Utilization of channel reciprocity • Allocation of resources between

uplink and downlink transmissions

Improved positioning technology

Speech improving technology

Qualcomm continues to drive technology and standards evolution in 3GPP for LTE-A, LTE Pro, 5G and beyond

Higher data rate technologies

Core LTE features

Higher system capacity technologies• Proportional-fair scheduling and other scheduling techniques • Inter-cell interference coordination (ICIC) • Heterogeneous networks (HetNet) • Enhanced inter-cell interference coordination (eICIC) • Interference cancellation • VoLTE optimization

LTE-Direct

LTE in unlicensed spectrum• Licensed-assisted

access

• Uplink communications: “Single Carrier FDMA” • Downlink communications: OFDMA• LTE network architecture • LTE cell acquisition

• Hybrid ARQ • Fast link adaptation • MIMO • Carrier aggregation

• Channel estimation enhancements

• Interferencecancellation

66

Multi-mode / multi-connectivity essential to 5G successA phased 5G rollout that fully leverages 4G and Wi-Fi investments

4G below 6 GHz

5G above 6 GHz

5G below 6 GHz

5G/4G/3G/Wi-FiMulti-mode device

Simultaneous connectivity across 5G, 4G and Wi-Fi

67

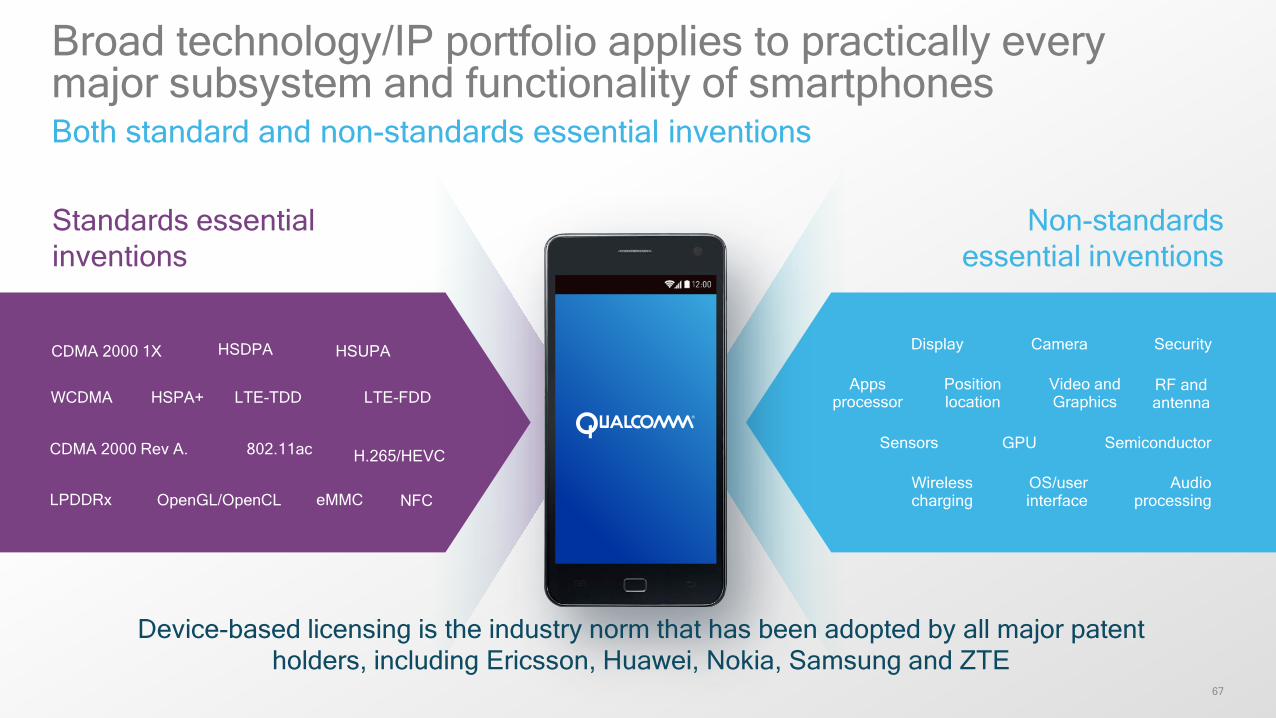

Broad technology/IP portfolio applies to practically every major subsystem and functionality of smartphones Both standard and non-standards essential inventions

Standards essential inventions

Non-standardsessential inventions

GPUSensors Semiconductor

Appsprocessor

Position location

Video and Graphics

RF andantenna

Camera SecurityDisplay

OS/user interface

Wireless charging

Audio processing

WCDMA HSPA+ LTE-TDD LTE-FDD

CDMA 2000 1X HSDPA HSUPA

CDMA 2000 Rev A. 802.11ac H.265/HEVC

LPDDRx OpenGL/OpenCL eMMC NFC

Device-based licensing is the industry norm that has been adopted by all major patent holders, including Ericsson, Huawei, Nokia, Samsung and ZTE

68

Additional licensing opportunities

• Mobile technologies being adopted across many new industries/segments (e.g., multimedia/video compression)

• Remaining unlicensed patents in China

• Qualcomm Halo™ technology

69

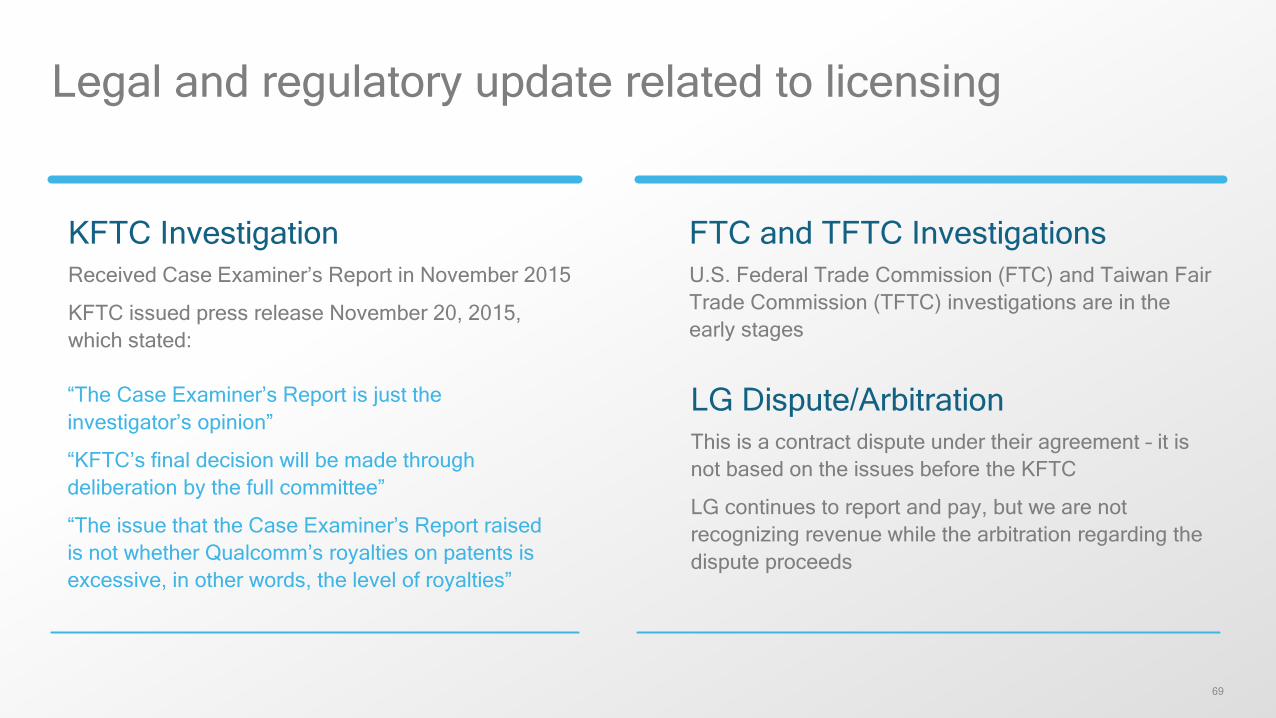

Legal and regulatory update related to licensing

KFTC InvestigationReceived Case Examiner’s Report in November 2015

KFTC issued press release November 20, 2015, which stated:

FTC and TFTC InvestigationsU.S. Federal Trade Commission (FTC) and Taiwan Fair Trade Commission (TFTC) investigations are in the early stages

LG Dispute/ArbitrationThis is a contract dispute under their agreement – it is not based on the issues before the KFTC

LG continues to report and pay, but we are not recognizing revenue while the arbitration regarding the dispute proceeds

“The Case Examiner’s Report is just the investigator’s opinion”

“KFTC’s final decision will be made through deliberation by the full committee”

“The issue that the Case Examiner’s Report raised is not whether Qualcomm’s royalties on patents is excessive, in other words, the level of royalties”

Additional growth opportunities

71

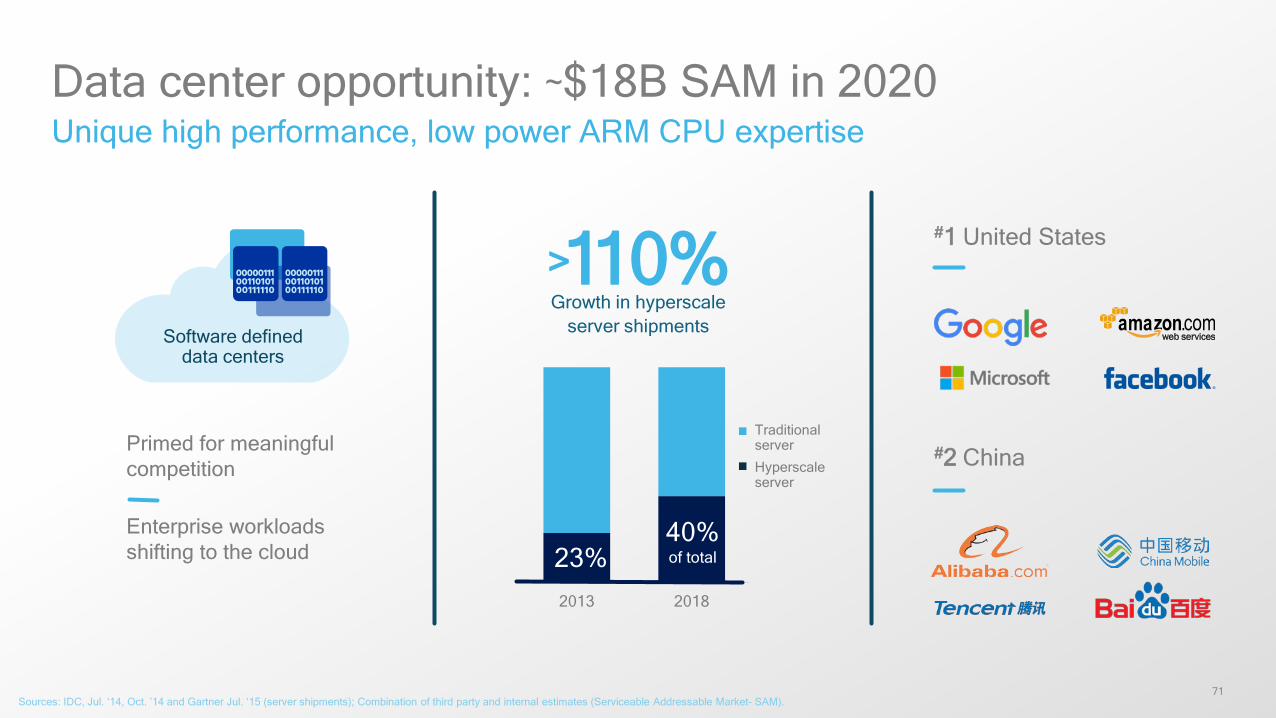

2013 2018

Data center opportunity: ~$18B SAM in 2020Unique high performance, low power ARM CPU expertise

Sources: IDC, Jul. ‘14, Oct. ’14 and Gartner Jul. ‘15 (server shipments); Combination of third party and internal estimates (Serviceable Addressable Market- SAM).

>110%Growth in hyperscale

server shipments

23%40%of total

#2 ChinaHyperscaleserver

Traditionalserver

#1 United States

Software defined data centers

Primed for meaningful competition

Enterprise workloads shifting to the cloud

72

Data centersBalanced solution for performance, power and cost

Focus on true server class features and performance

Partnering with Tier 1 cloud operators for product definition

Utilizing latest process node (e.g. FinFET)

Decade of experience with custom ARM CPU architectures

Utilizing low power and power management experience from mobile

73

Executing well on our data center planEngaged with major Tier-1 hyper-scale cloud operators worldwide

Announced 24-core customer samples and developmentsystem based on FinFET technology in October 2015

Have shipped development platform to Tier-1 customers and partners

Established collaborations with Mellanox and Xilinx

Red Hat and Canonical solutions being enabled on Qualcomm Technologies server SoC solution

Announced formation of Guizhou Huaxintong Semiconductor Technology Inc.- A joint venture for server chipsets in China

74

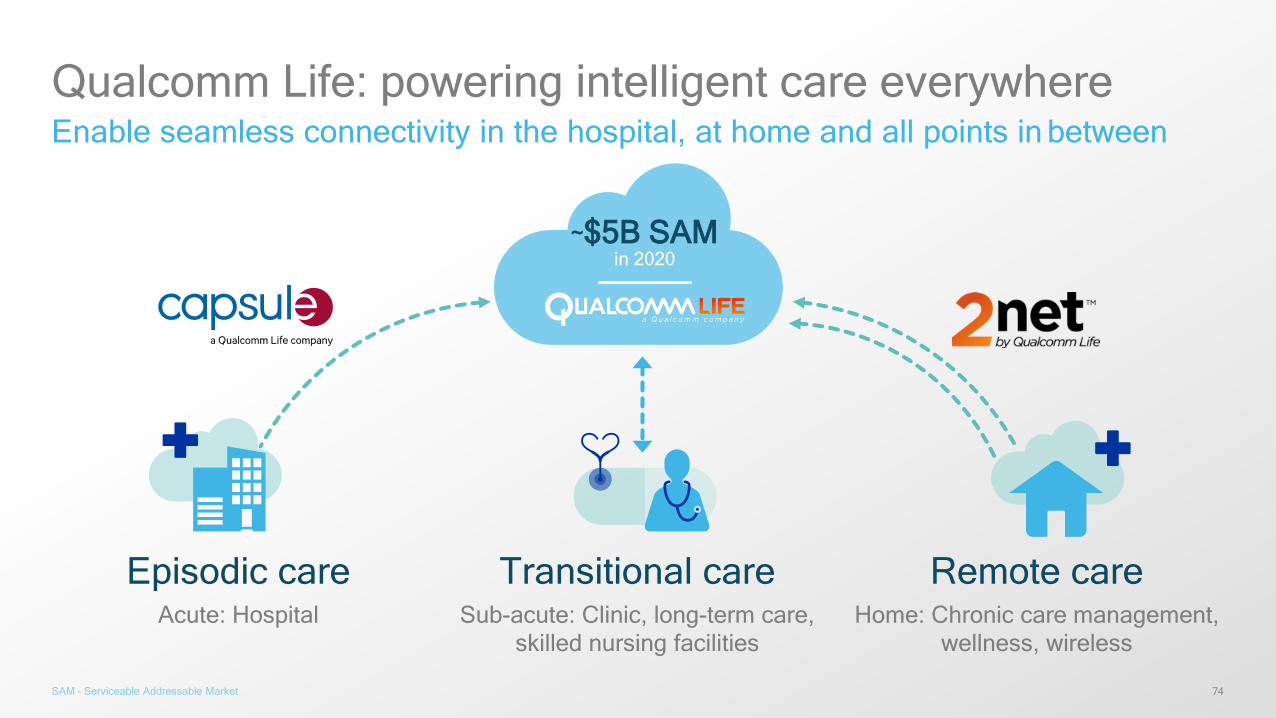

Qualcomm Life: powering intelligent care everywhereEnable seamless connectivity in the hospital, at home and all points in between

Transitional careSub-acute: Clinic, long-term care,

skilled nursing facilities

Episodic careAcute: Hospital

Remote careHome: Chronic care management,

wellness, wireless

~$5B SAM in 2020

SAM - Serviceable Addressable Market

75

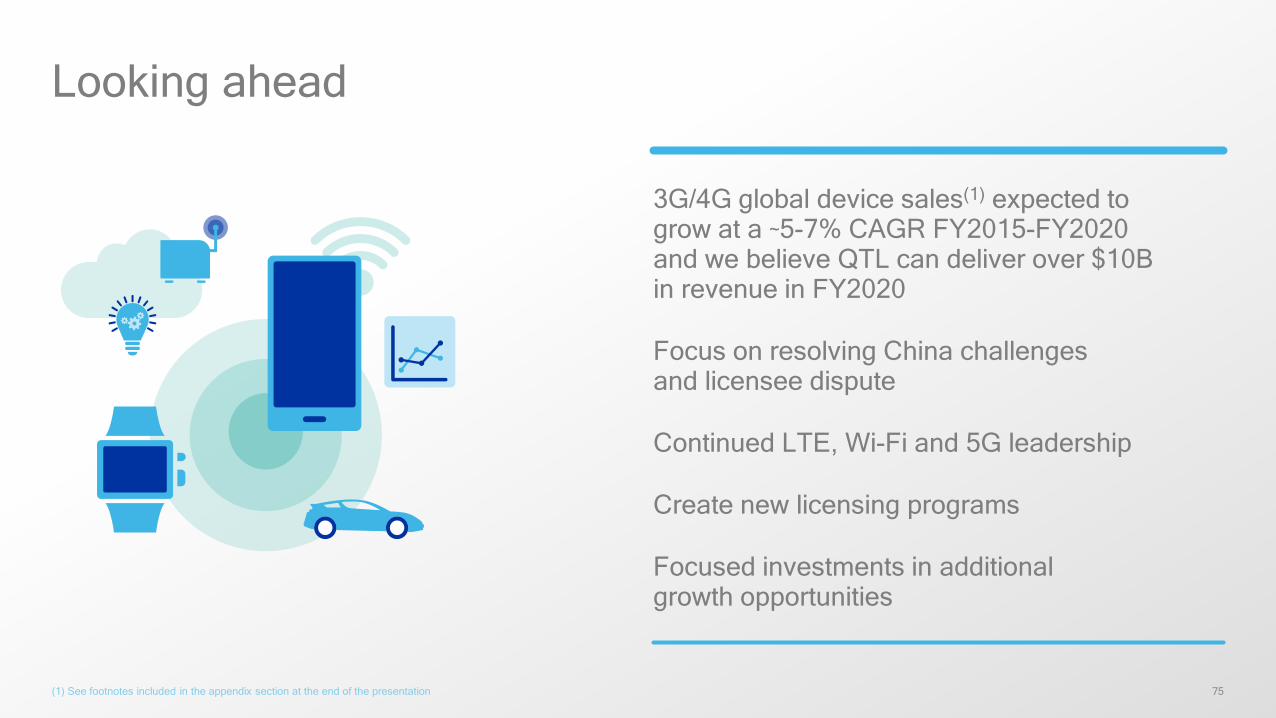

3G/4G global device sales(1) expected to grow at a ~5-7% CAGR FY2015-FY2020 and we believe QTL can deliver over $10B in revenue in FY2020

Focus on resolving China challenges and licensee dispute

Continued LTE, Wi-Fi and 5G leadership

Create new licensing programs

Focused investments in additional growth opportunities

Looking ahead

(1) See footnotes included in the appendix section at the end of the presentation

Cristiano Amon

EVP, Qualcomm Technologies, Inc. and President, QCT

77

QCT operating priorities

Focused execution

Growth strategy

Margin expansion

Mobile technology leadership

Adjacent opportunities

Mobile

78

Focused executionOn track with Strategic Realignment Plan (SRP) commitments

Right-sized cost structure withlong-term revenue opportunity

Maintaining technology andindustry leadership

Completed comprehensive review of cost structure and developed plan

Implemented detailed plan to reduce operating expenses by ~$800 million

Focused investments in advanced differentiated technology areas

Created specific efforts to address growth vectors: Auto, IoT, Mobile Compute, Networking, RFFE

4Q FY2016 operating margin of 16%+ On-Track

Long term operating margin target of 20%+ On-Track

79

Strategy for growth in mobile and adjacent opportunities

The powerof our mobile

channel

New technologiesin existing channel

Growth in adjacent

opportunities

Existing technologiesin new channels

80

The power of our mobile channelProven over time

Continued growth

Expansion intonew technology

LTE

Wi-Fi

Bluetooth

Sensor hub

Graphics

Video

Security

CDMA

DSP

Transceiver

GPS

PMIC

WCDMA

Multimode

CPU

Camera

Audio/Music

Memory

60GHz

Envelope tracker

Antenna tuner

PA/Switch

Filters

RF modules

Codec

Charging

Fingerprint

Touch

BASEBAND

81

Adjacent opportunities transformed by mobile

Mobile

Networking

Auto IoT

Mobile compute

82

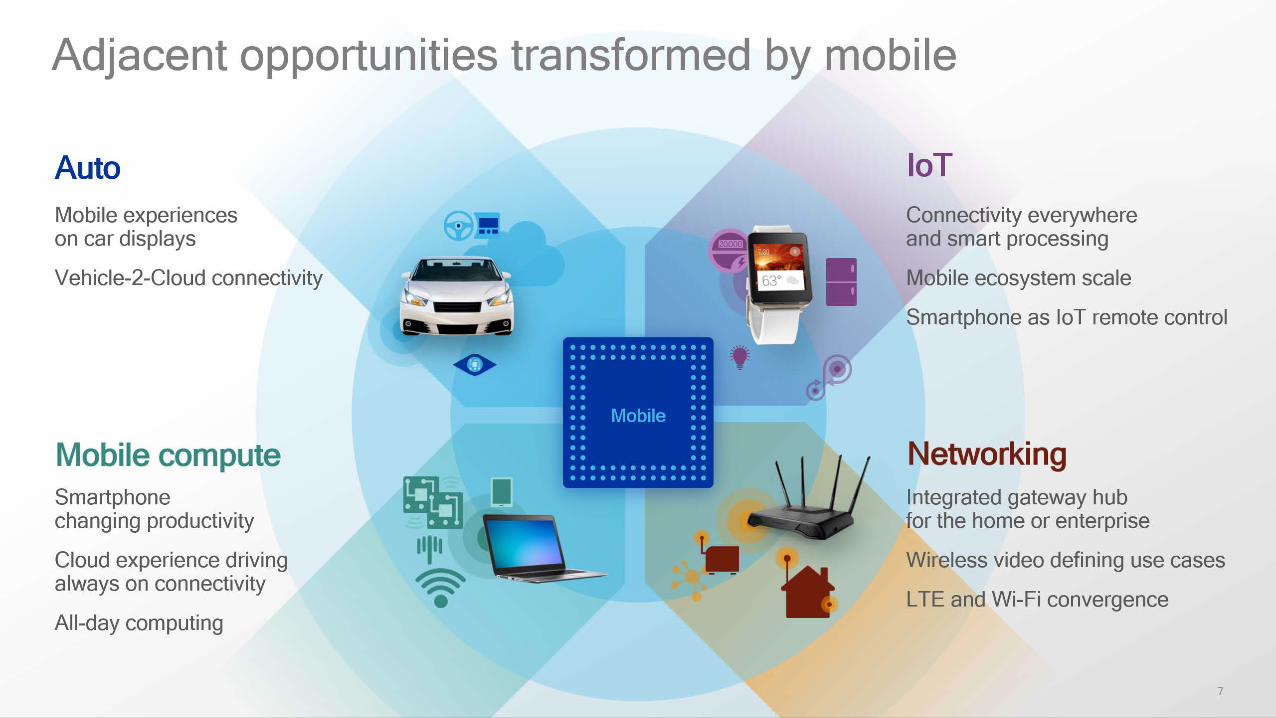

Adjacent opportunities transformed by mobile

Mobile

Networking

Auto IoT

Mobile compute

Mobile experiences on car displays

Vehicle-2-Cloud connectivity

Connectivity everywhere and smart processing

Mobile ecosystem scale

Smartphone as IoT remote control

Integrated gateway hub for the home or enterprise

Wireless video defining use cases

LTE and Wi-Fi convergence

Smartphone changing productivity

Cloud experience driving always on connectivity

All-day computing

83

New technologies into mobile channel

Growth in adjacent opportunities and new channels

Leadership and differentiation across technologies

Optimized product cost by tier and segment

Growth in adjacent opportunities accretive to margins

Maximize technology and R&D reuse

Focus investments in low cost regions

Driving growth and margin expansion

Revenue diversification

and growth

Margin expansion

Cost structure and operating

efficiency

Drivers for 20%+operating margin

84

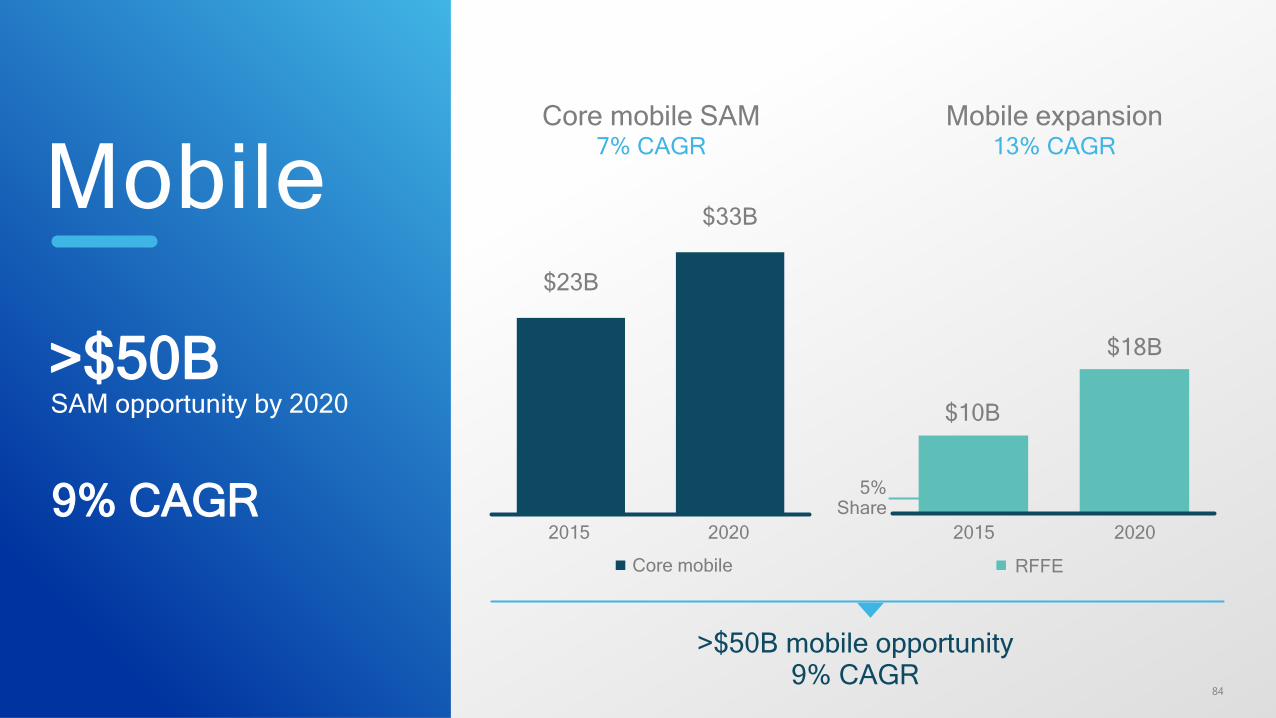

Mobile

2020

$33B

2015

$23B

Core mobile SAM7% CAGR

Mobile expansion13% CAGR

2020

$18B

2015

$10B

5% Share

Core mobile

>$50B mobile opportunity9% CAGR

RFFE

>$50BSAM opportunity by 2020

9% CAGR

85

LTE platform leadership – a history of technology firsts

2010 2016

LTE multimode

LTE voice(CSFB)

LTE SoC

28nm LTE

LTE CA

7-mode LTE

LTEBroadcast

LTEDual SIM

VoLTEMultimode

20nmLTE

Cat10modem

LTE acrossall tiers

Gigabit LTE

LTE-U, LWA,4x4 MIMO

LTECat 12/13

FinFet LTE

LAA, 4x CA

LTE SOC LTE CALTE multimode

Merchant competitors atleast 2 generations behind

Gen 1 Gen 2 Gen 3 Gen 4 Gen 5 Gen 6

600Mbps LTE hotspot

Cat 6 in smartphone

Cat 9SoC

86

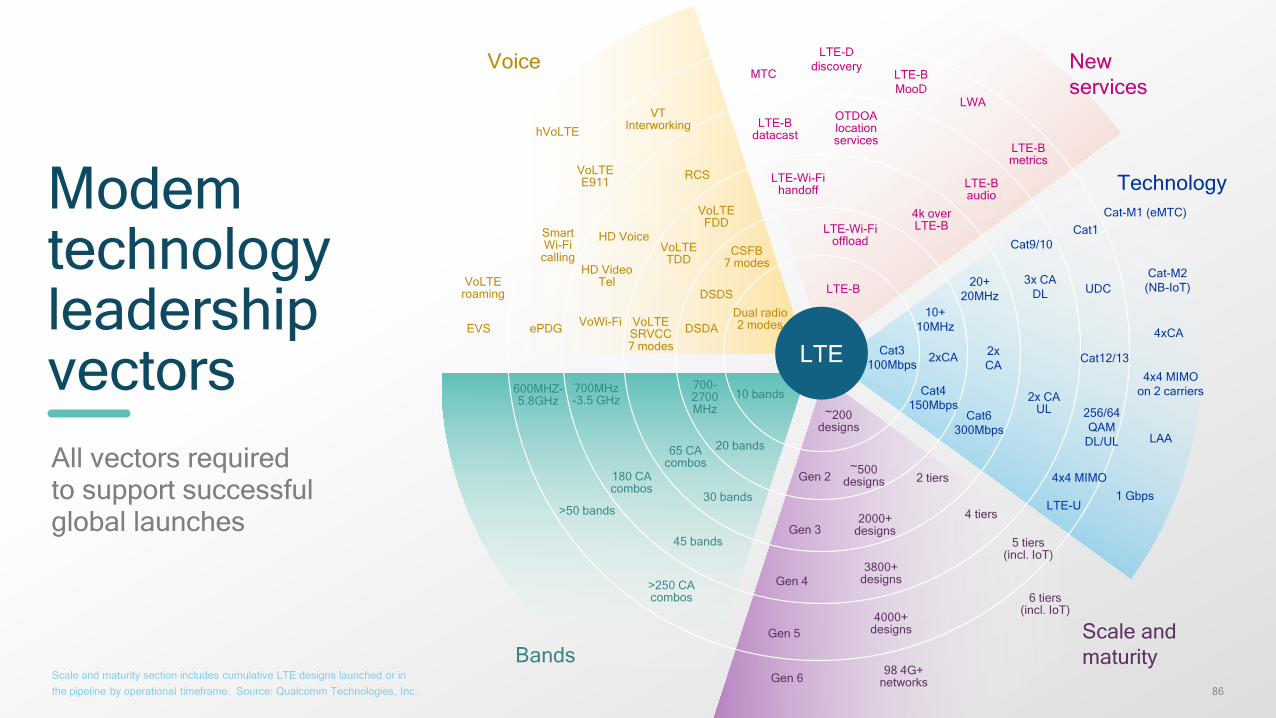

Modem technologyleadershipvectorsAll vectors requiredto support successful global launches

LTE

Bands

10 bands

20 bands

30 bands

65 CAcombos

700-2700MHz

45 bands

700MHz-3.5 GHz

180 CAcombos

>50 bands

>250 CAcombos

600MHZ-5.8GHz

LTE-B

LTE-Wi-Fioffload

4k over LTE-B

LTE-Wi-Fihandoff

LTE-B datacast

LTE-Baudio

OTDOAlocationservices

LWA

LTE-B MooD

LTE-Ddiscovery

MTC

LTE-B metrics

Newservices

Technology

Cat4150Mbps

2xCA

10+10MHz

Cat3100Mbps

Cat6300Mbps

2xCA

20+20MHz

Cat9/10

LTE-U

2x CAUL

Cat1

4x4 MIMO

256/64QAM

DL/UL

3x CADL UDC

Cat12/13

Scale andmaturity

~500designsGen 2

~200 designs

2 tiers

2000+designsGen 3

4 tiers

Gen 43800+

designs

98 4G+networks

6 tiers(incl. IoT)

5 tiers(incl. IoT)

Gen 54000+

designs

Gen 6

CSFB 7 modes

DSDS

DSDADual radio 2 modes

VoLTEFDD

VoLTESRVCC7 modes

HD Voice

RCS

VoWi-Fi

VT Interworking

ePDG

VoLTEE911

EVS

hVoLTE

Voice

SmartWi-Fi

calling

VoLTEroaming

Cat-M1 (eMTC)

Cat-M2(NB-IoT)

4xCA

4x4 MIMOon 2 carriers

LAA

1 Gbps

VoLTETDD

HD Video Tel

Scale and maturity section includes cumulative LTE designs launched or inthe pipeline by operational timeframe. Source: Qualcomm Technologies, Inc.

87

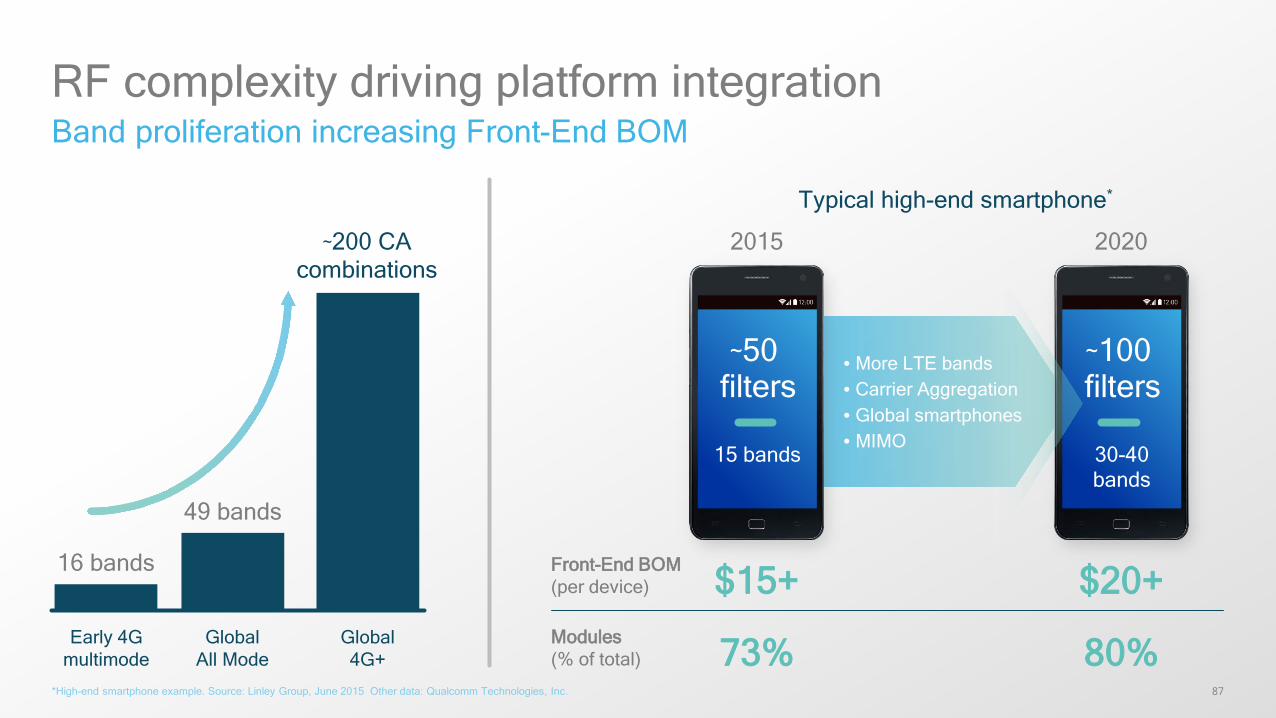

RF complexity driving platform integrationBand proliferation increasing Front-End BOM

*High-end smartphone example. Source: Linley Group, June 2015 Other data: Qualcomm Technologies, Inc.

Global 4G+

GlobalAll Mode

49 bands

Early 4G multimode

16 bands

~200 CA combinations

• More LTE bands• Carrier Aggregation• Global smartphones• MIMO

2015 2020

~100 filters

30-40 bands

~50 filters

15 bands

Typical high-end smartphone*

Modules (% of total) 73% 80%

Front-End BOM(per device) $15+ $20+

88

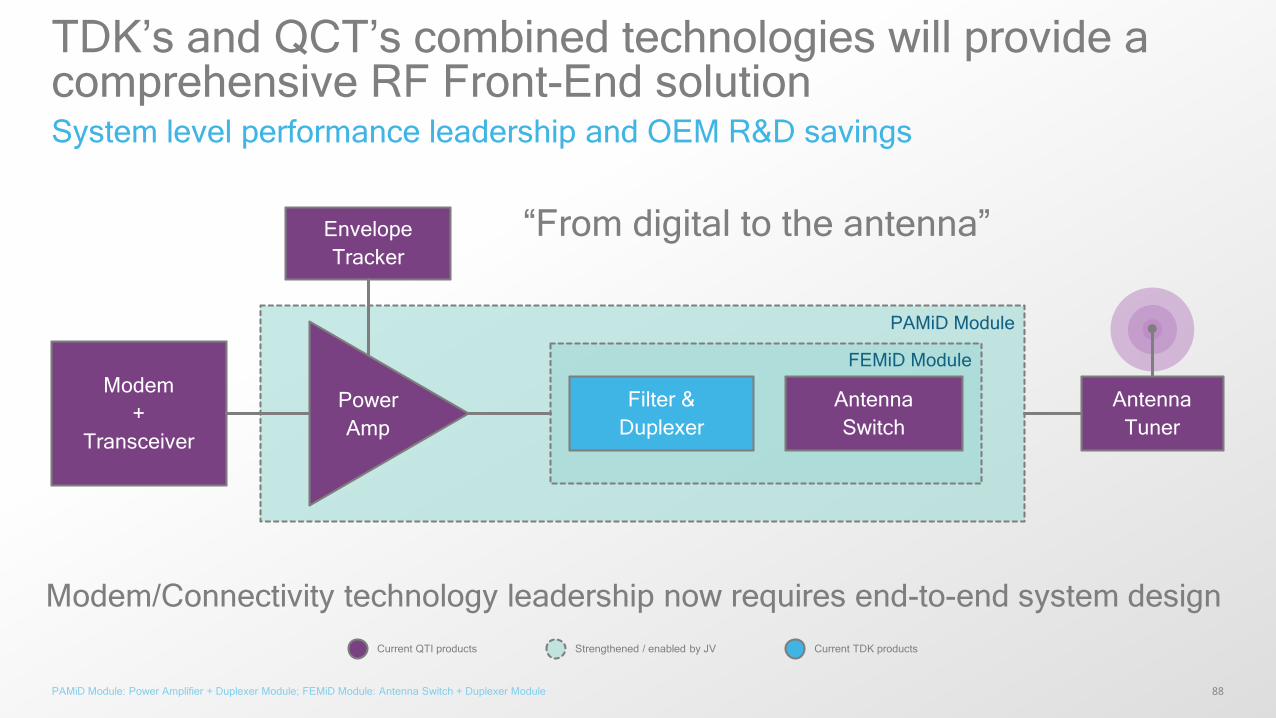

TDK’s and QCT’s combined technologies will provide a comprehensive RF Front-End solutionSystem level performance leadership and OEM R&D savings

PAMiD Module: Power Amplifier + Duplexer Module; FEMiD Module: Antenna Switch + Duplexer Module

“From digital to the antenna”

Modem/Connectivity technology leadership now requires end-to-end system designStrengthened / enabled by JV Current TDK productsCurrent QTI products

Modem+

Transceiver

AntennaSwitch

Filter &Duplexer

EnvelopeTracker

PAMiD Module

AntennaTuner

PowerAmp

FEMiD Module

89

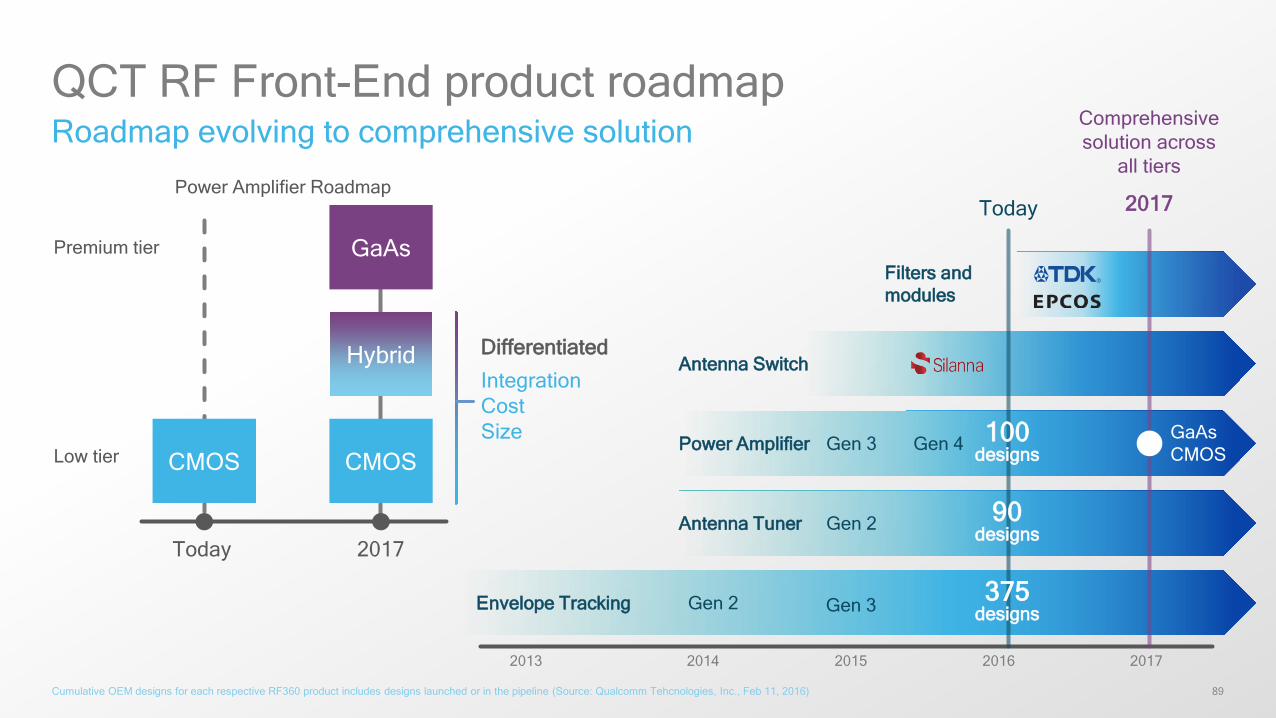

QCT RF Front-End product roadmapRoadmap evolving to comprehensive solution

Cumulative OEM designs for each respective RF360 product includes designs launched or in the pipeline (Source: Qualcomm Tehcnologies, Inc., Feb 11, 2016)

Comprehensivesolution across

all tiers

2017

2013 2014 2015 2016 2017

Today

Filters and modules

Antenna Switch

Power Amplifier Gen 3 Gen 4GaAsCMOS

Antenna Tuner Gen 2

Envelope Tracking Gen 2

100designs

90designs

375designs

Today 2017

CMOS CMOS

Hybrid

GaAsPremium tier

Low tier

Differentiated

IntegrationCostSize

Power Amplifier Roadmap

Gen 3

90

Qualcomm® Snapdragon™ processor is the reference point for mobile SoCs

Qualcomm Adreno™

530 GPU

X16 LTE Modem

Top shipping smartphone GPU*

World’s first announcedGigabit class LTE modem

Home and enterprise wireless networks First to launchMU-MIMO and 11ad

*Based on smartphone application processor unit shipments, Strategy Analytics, December 2015. Qualcomm Snapdragon, Qualcomm Adreno, Qualcomm Kryo, Qualcomm Hexagon, and Qualcomm Quick Charge are products of Qualcomm Technologies, Inc.^DXOMARK 2015.

#1

#1

#1

QualcommKryo™ CPU

Qualcomm Hexagon™

680 DSP

First Qualcomm custom 64bit CPU

First to implement wide vector SIMD extensions (HVX)

CameraISP7 of top 10 phone cameras^

#1

#1

#1

Display processing

Memory

Multimedia processing

Wi-Fi

LTE modem

CPU

DSP

GPU

GNSS

BT FM

ISP

USBPCI

Sensor processing

91

Envelope Tracker

PowerAmplifier

Antenna Tuner

Antenna Switch

RF TransceiverFilters

Speakeramp

Quick charge

Codec

802.11acMU-MIMO

802.11adWiGig

Power management

interface

Touch

Fingerprint

End-to-end design

Tri-band Wi-Fi

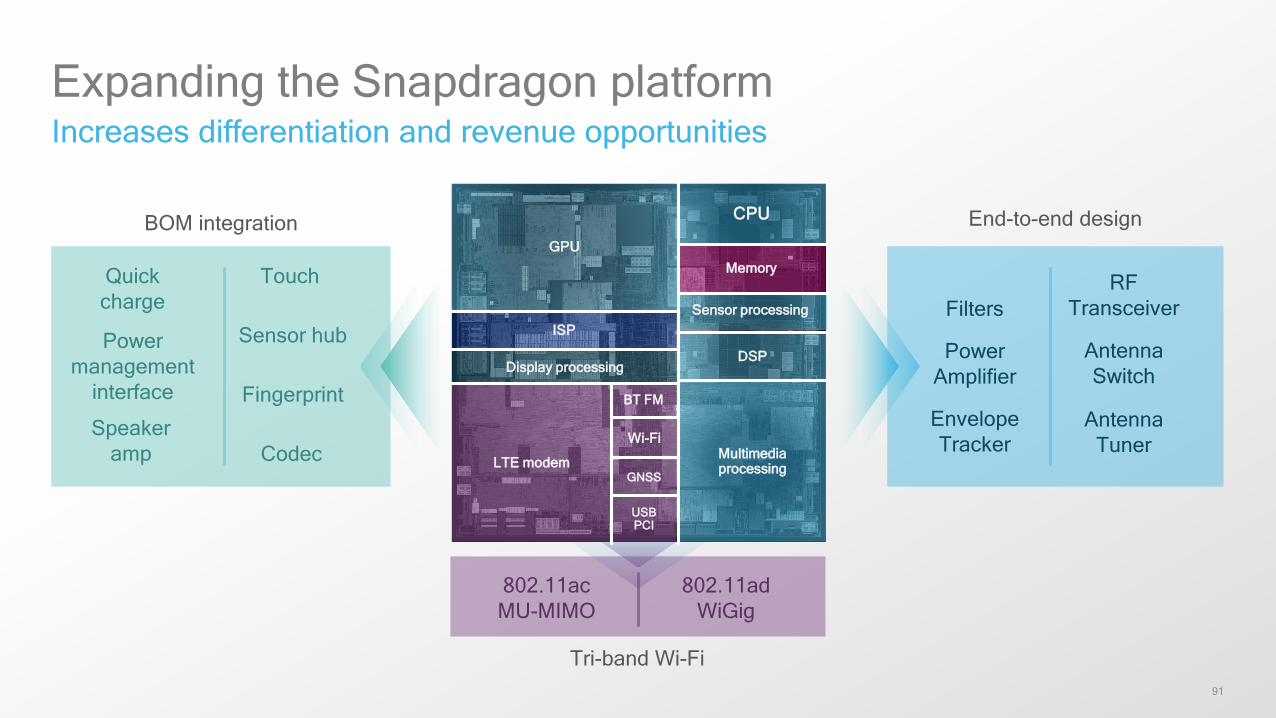

BOM integration

Expanding the Snapdragon platformIncreases differentiation and revenue opportunities

Display processing

Memory

Multimedia processing

Wi-Fi

LTE modem

CPU

DSP

GPU

GNSS

BT FM

ISP

USBPCI

Sensor processing

Sensor hub

92

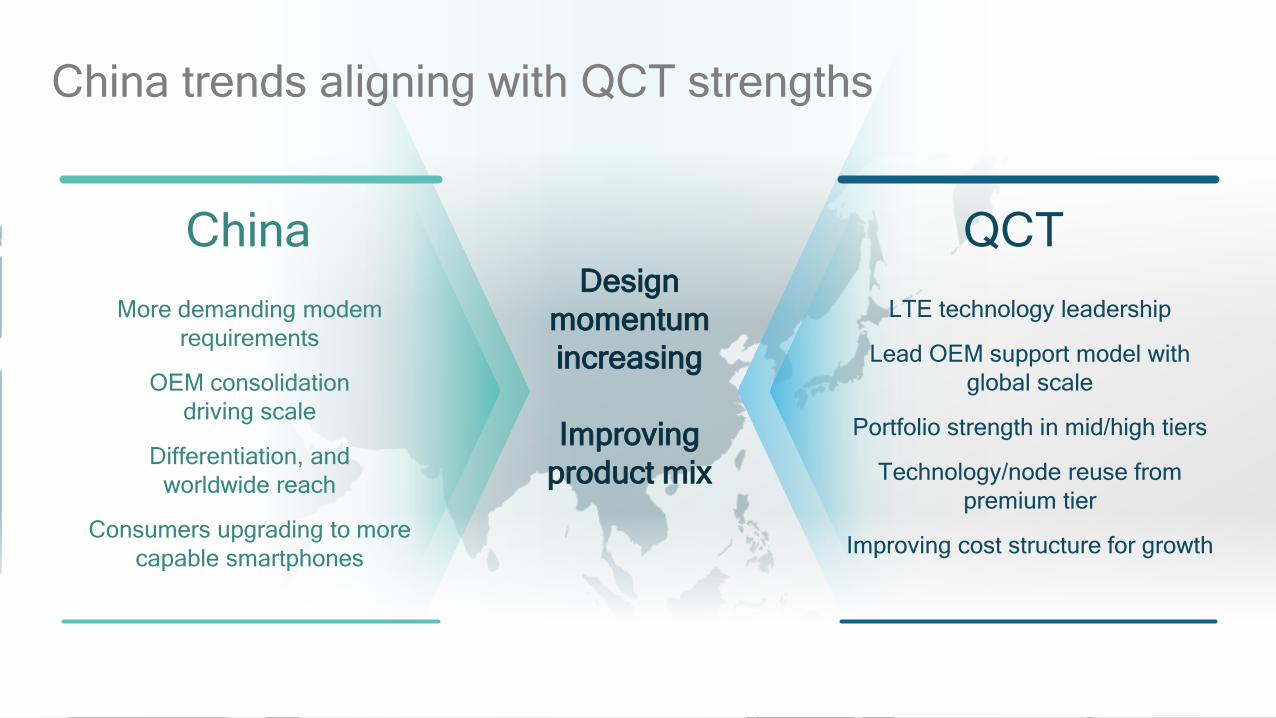

China trends aligning with QCT strengths

China QCTMore demanding modem

requirements

OEM consolidationdriving scale

Differentiation, andworldwide reach

Consumers upgrading to more capable smartphones

LTE technology leadership

Lead OEM support model with global scale

Portfolio strength in mid/high tiers

Technology/node reuse from premium tier

Improving cost structure for growth

Design momentumincreasing

Improvingproduct mix

93

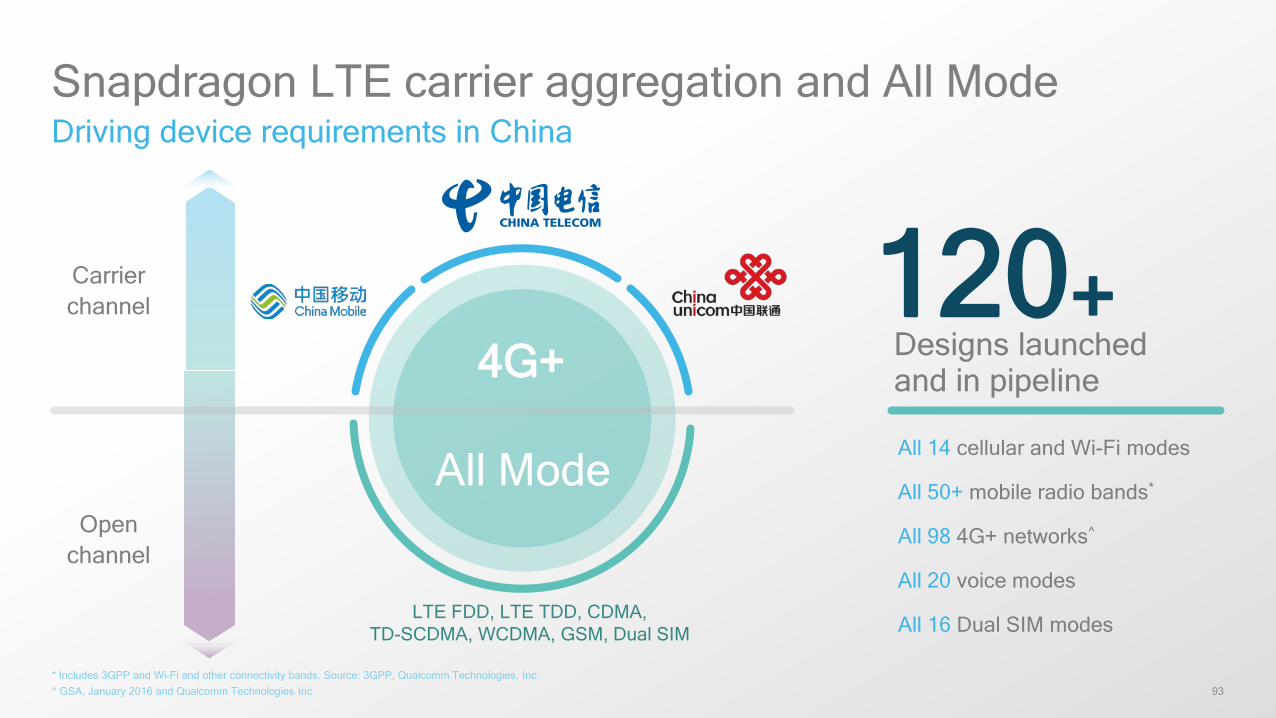

Snapdragon LTE carrier aggregation and All ModeDriving device requirements in China

4G+

All Mode

Carrier channel

Open channel

All 14 cellular and Wi-Fi modes

All 50+ mobile radio bands*

All 98 4G+ networks^

All 20 voice modes

All 16 Dual SIM modes

120+Designs launchedand in pipeline

LTE FDD, LTE TDD, CDMA,TD-SCDMA, WCDMA, GSM, Dual SIM

* Includes 3GPP and Wi-Fi and other connectivity bands. Source: 3GPP, Qualcomm Technologies, Inc.^ GSA, January 2016 and Qualcomm Technologies Inc.

94

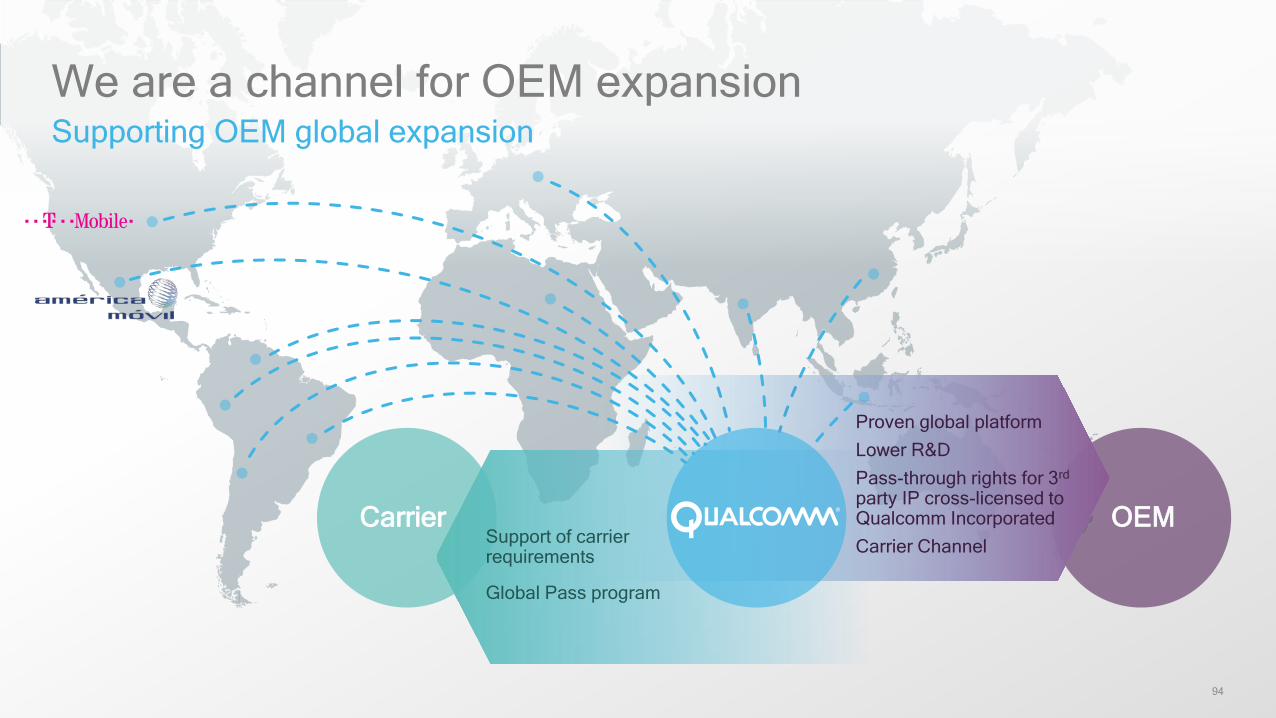

We are a channel for OEM expansionSupporting OEM global expansion

OEMSupport of carrierrequirements

Global Pass program

Proven global platformLower R&DPass-through rights for 3rd

party IP cross-licensed toQualcomm IncorporatedCarrier Channel

Carrier

95

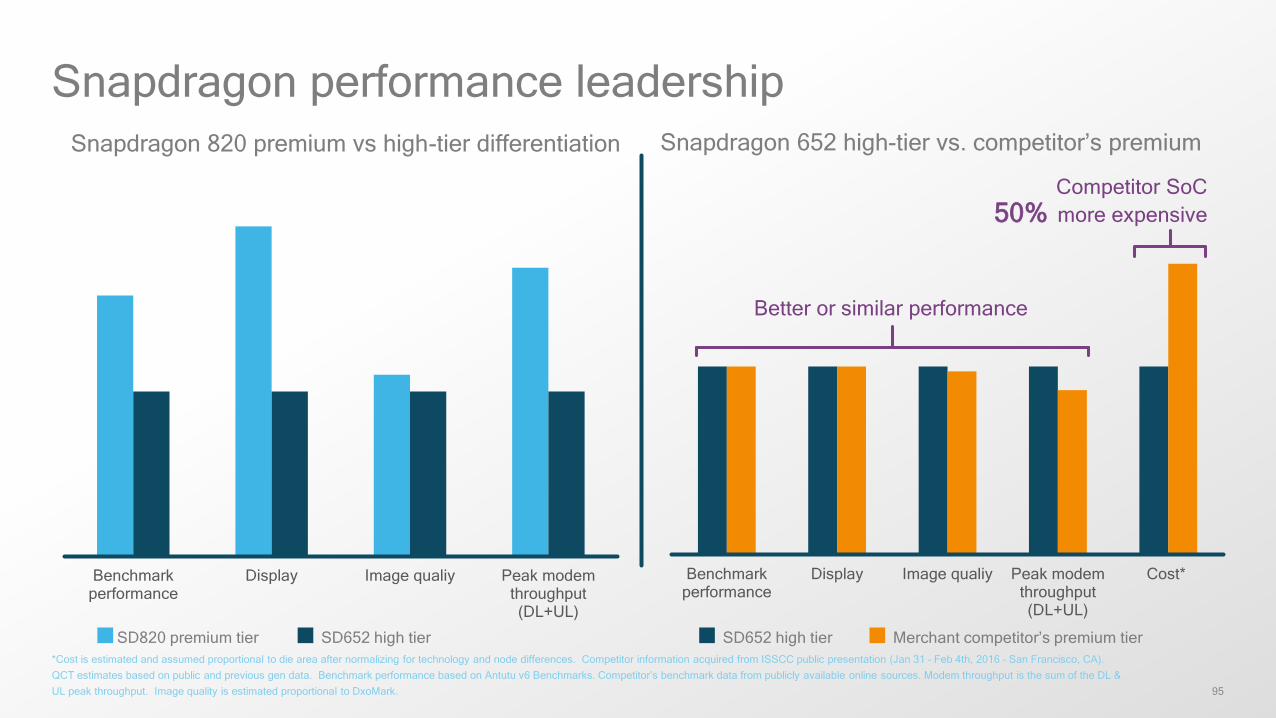

Benchmarkperformance

Display Image qualiy Peak modemthroughput(DL+UL)

Benchmarkperformance

Display Image qualiy Peak modemthroughput(DL+UL)

Cost*

Snapdragon 652 high-tier vs. competitor’s premium

Better or similar performance

Competitor SoC50% more expensive

Snapdragon 820 premium vs high-tier differentiation

Snapdragon performance leadership

*Cost is estimated and assumed proportional to die area after normalizing for technology and node differences. Competitor information acquired from ISSCC public presentation (Jan 31 – Feb 4th, 2016 – San Francisco, CA). QCT estimates based on public and previous gen data. Benchmark performance based on Antutu v6 Benchmarks. Competitor’s benchmark data from publicly available online sources. Modem throughput is the sum of the DL & UL peak throughput. Image quality is estimated proportional to DxoMark.

SD820 premium tier SD652 high tier SD652 high tier Merchant competitor’s premium tier

96

Supply chain scale drives competitive advantageMost geographically diversified, drives investment in leading nodes while having cost leadership

~5BChip shipments in FY15

2xFoundry spend of next competitor

3xWafer consumption in leading node of next competitor

Comparisons in foundry spend and wafer consumption in leading node are based on merchant semiconductor players.

97

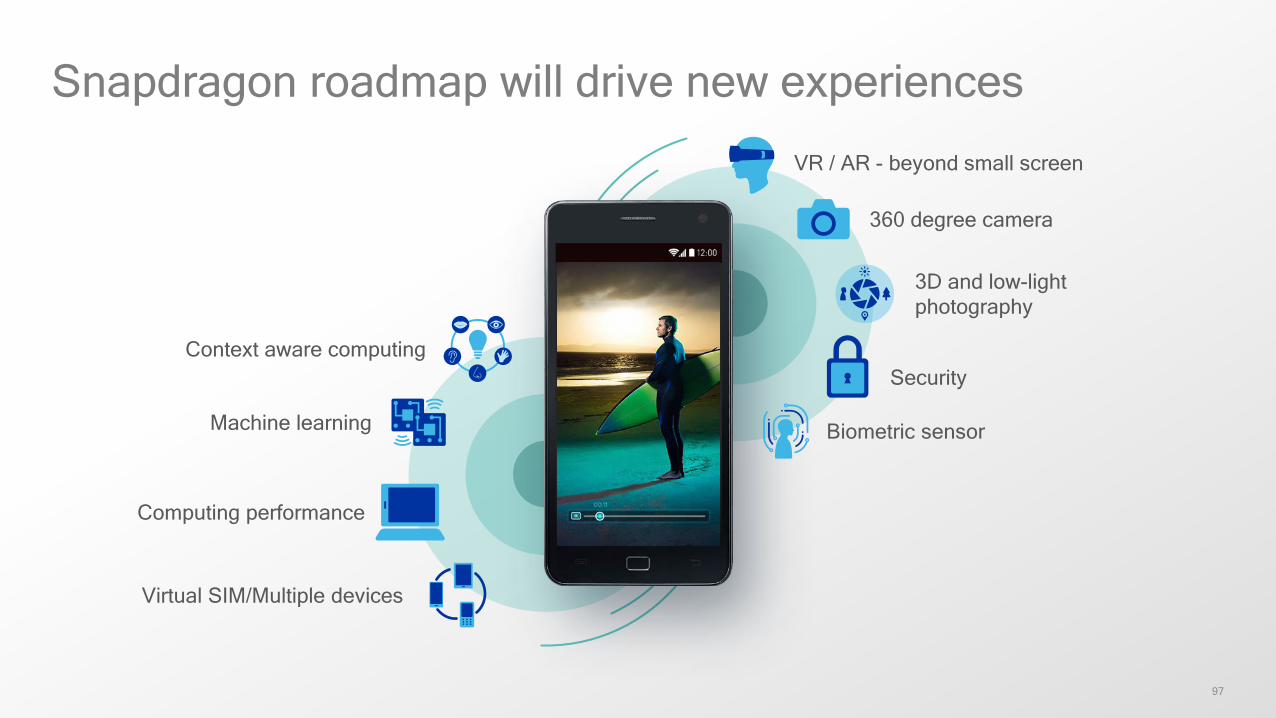

Snapdragon roadmap will drive new experiences

Context aware computing

Machine learning

Computing performance

VR / AR - beyond small screen

360 degree camera

3D and low-light photography

Security

Biometric sensor

Virtual SIM/Multiple devices

98

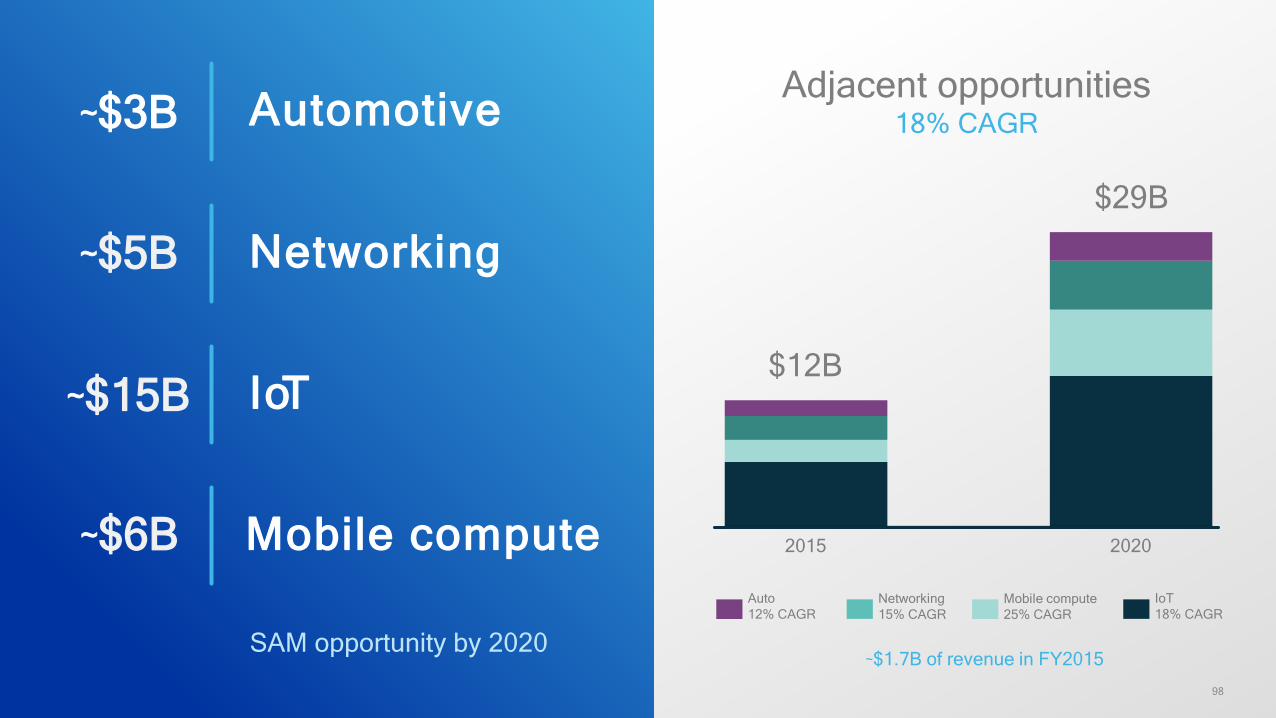

Adjacent opportunities18% CAGR

2020

$29B

2015

$12B

Mobile compute25% CAGR

Networking15% CAGR

Auto12% CAGR

IoT18% CAGR

~$1.7B of revenue in FY2015SAM opportunity by 2020

Automotive~$3B

Networking~$5B

IoT~$15B

Mobile compute~$6B

99

Auto experiences evolving with mobileBuilding from technology leadership in smartphones

Voice

Automaker

Consumer

Enterprise

Expected newuser experiences

Enabling new business models

100

QCT solutions for automotive

S602A

S820AModule

CSR Connectivity

#1 in Telematics* | #1 in Connectivity**Qualcomm Technologies, Inc. company data, 2015. Qualcomm APQ8064 is a product of Qualcomm Technologies, Inc.

LTE

101

QCT automotive ecosystem

102

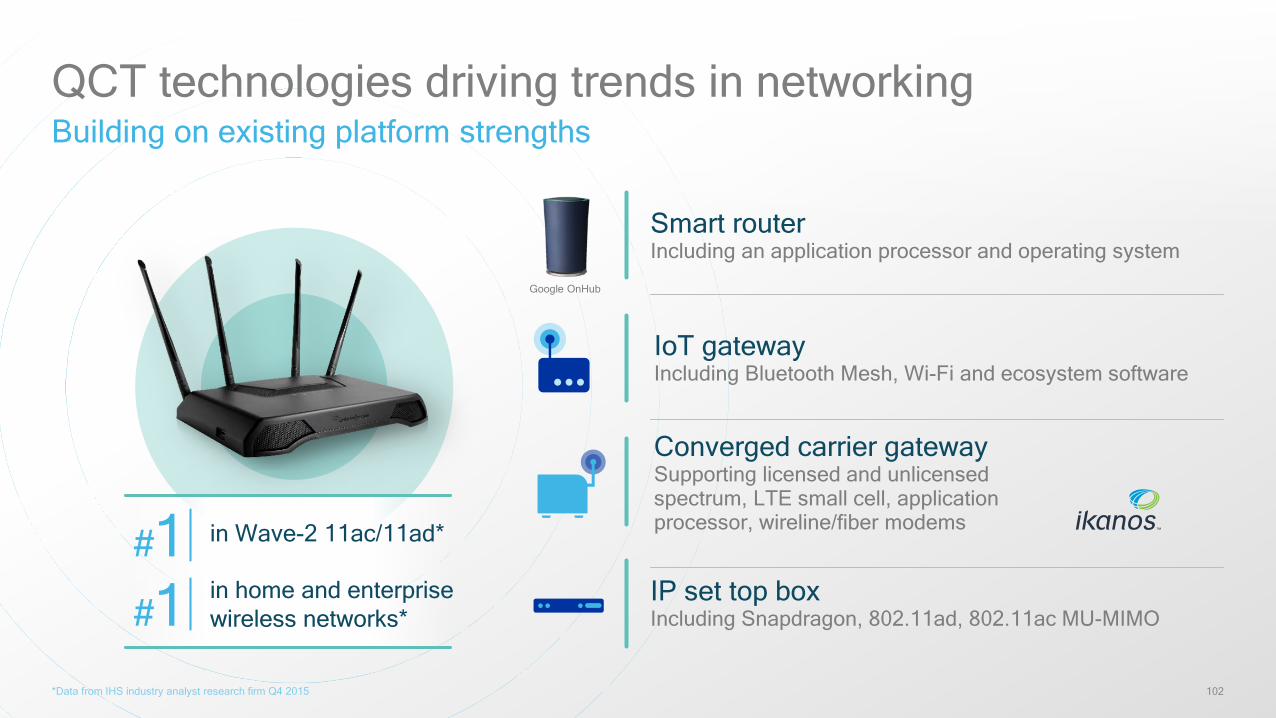

QCT technologies driving trends in networkingBuilding on existing platform strengths

IP set top boxIncluding Snapdragon, 802.11ad, 802.11ac MU-MIMO

Google OnHub

Smart routerIncluding an application processor and operating system

IoT gatewayIncluding Bluetooth Mesh, Wi-Fi and ecosystem software

Converged carrier gatewaySupporting licensed and unlicensed spectrum, LTE small cell, application processor, wireline/fiber modems

#1#1 in Wave-2 11ac/11ad*

in home and enterprise wireless networks*

*Data from IHS industry analyst research firm Q4 2015

103

Building comprehensive platforms

SoC and system level integration

Smart routers, IoTgateways, smart carrier gateway, IP set top box

First mover advantage in technology transitions

1+ year leadwith Wave-2 11ac and 11ad

IP cores shared across mobile, auto, computing and IoT

Extending connectivity leadership across client devices

LTE Wi-Fi integration

Licensedand unlicensed spectrum

Converged carrier gateway

Convergenceof WAN and WLAN

Broad portfolio

Wi-FiLTELTE-UProcessorsxDSLG.fastPowerlineEthernetBluetooth15.4

Networking strategy

SAM and ASP growth

104

QCT networking ecosystem

105

IoTHome control

and automationHome

entertainment

Voice and music

Wearables

Cameras and drones

Smart cities and Industrial

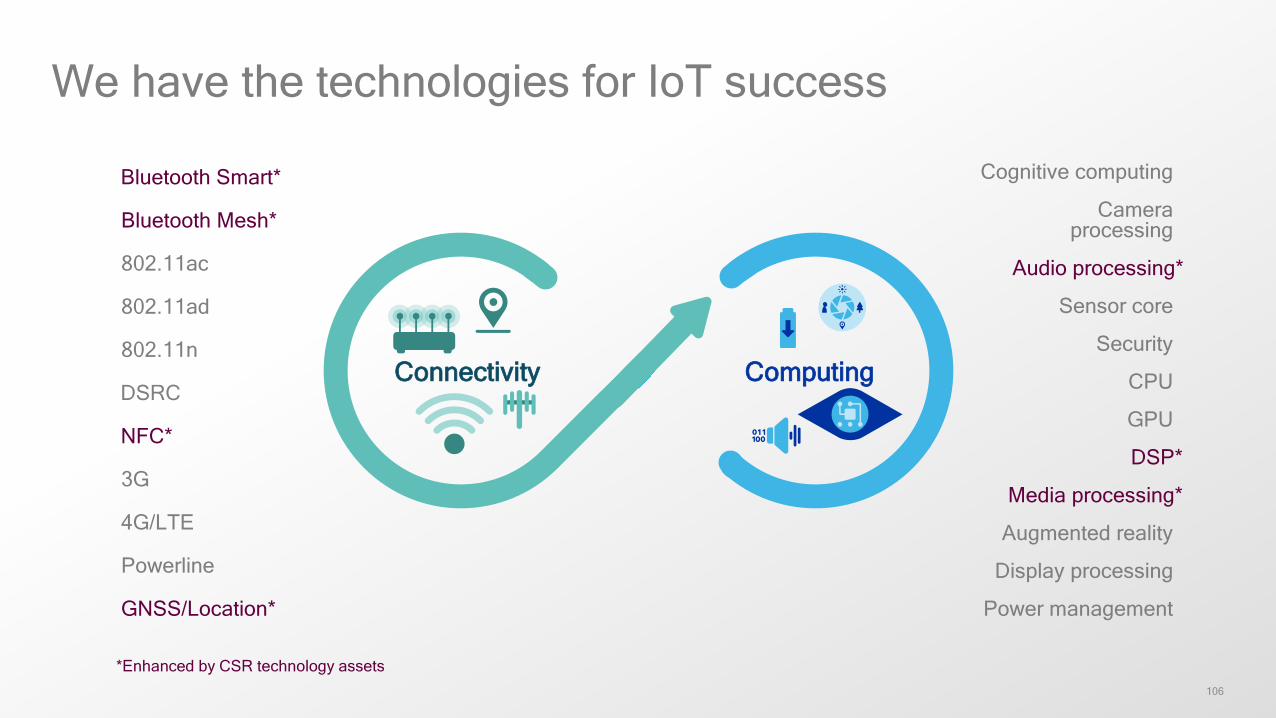

106

Connectivity Computing

We have the technologies for IoT success

802.11ad

Bluetooth Smart*

802.11ac

3G

4G/LTE

802.11n

Powerline

DSRC

NFC*

Sensor core

Display processing

Media processing*

CPU

Augmented reality

GNSS/Location*

GPU

Camera processing

DSP*

Security

Power management

Cognitive computing

Bluetooth Mesh*

Audio processing*

*Enhanced by CSR technology assets

107

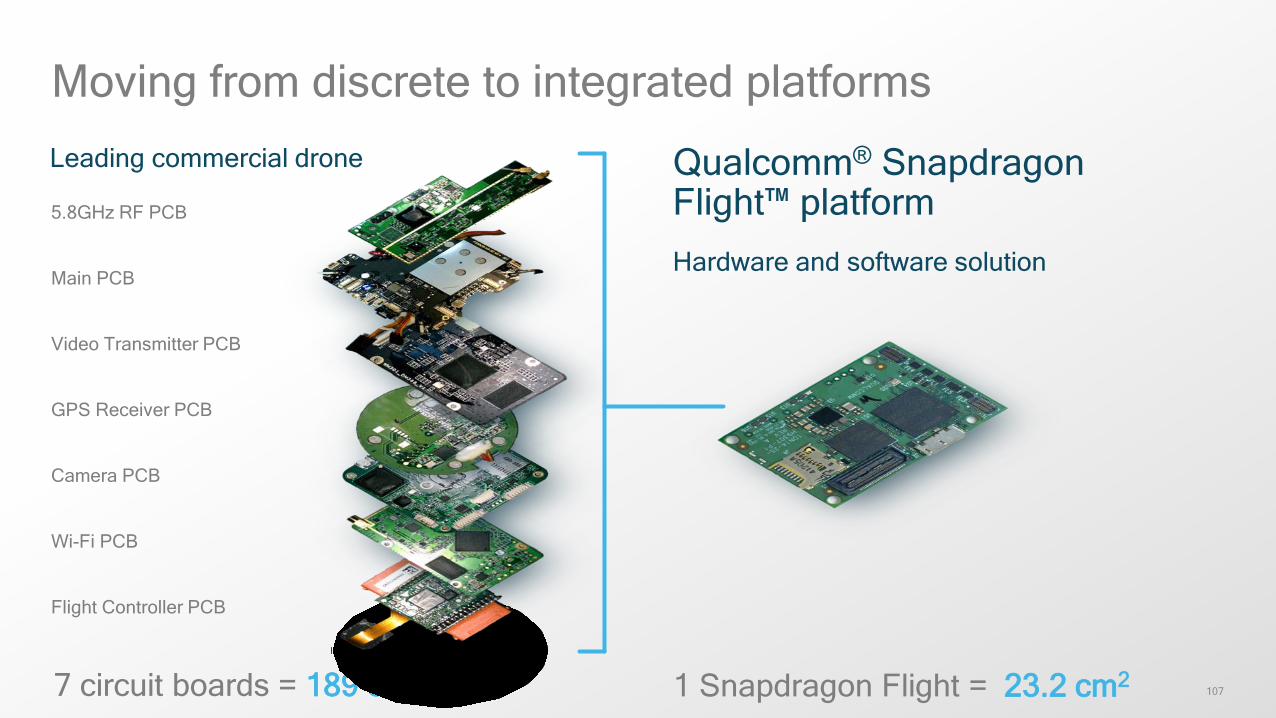

Moving from discrete to integrated platforms

Qualcomm® Snapdragon Flight™ platform Hardware and software solution

1 Snapdragon Flight = 23.2 cm2

Main PCB

Flight Controller PCB

Wi-Fi PCB

Video Transmitter PCB

5.8GHz RF PCB

GPS Receiver PCB

Camera PCB

7 circuit boards = 189 cm2

Leading commercial drone

108

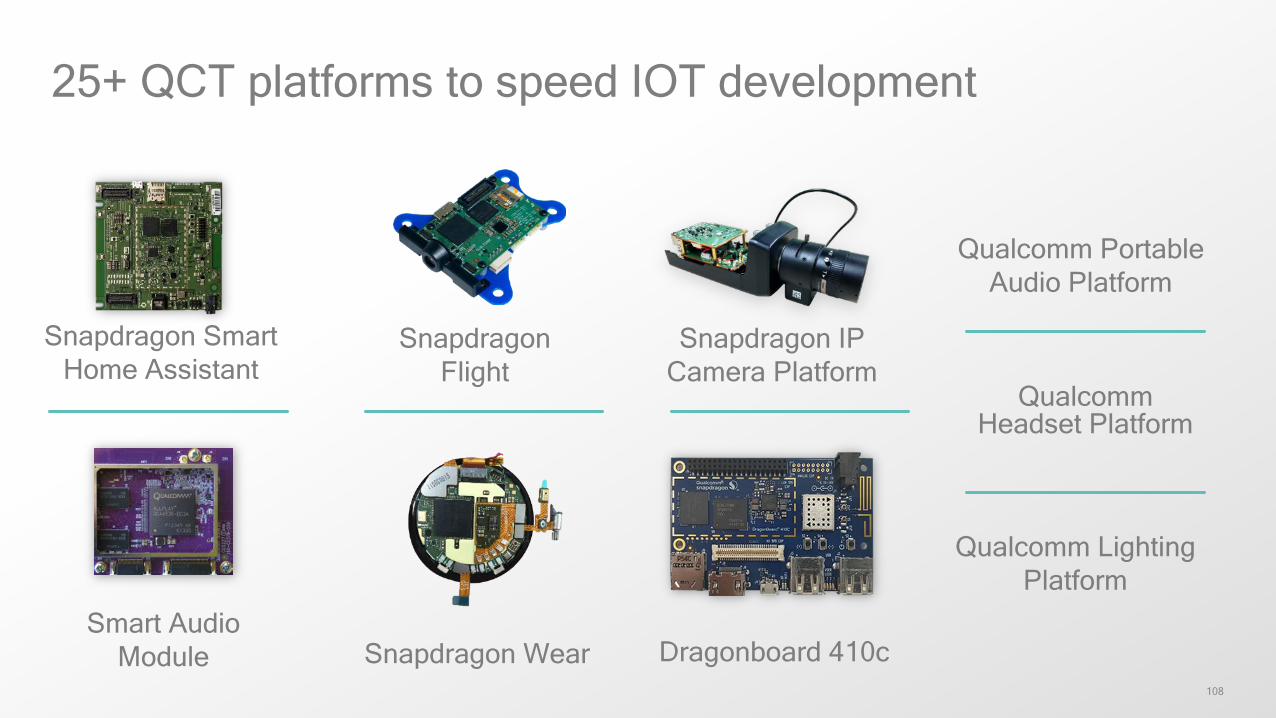

25+ QCT platforms to speed IOT development

Smart AudioModule

Snapdragon SmartHome Assistant

Qualcomm LightingPlatform

Qualcomm PortableAudio Platform

QualcommHeadset Platform

Snapdragon IPCamera Platform

SnapdragonFlight

Dragonboard 410cSnapdragon Wear

109

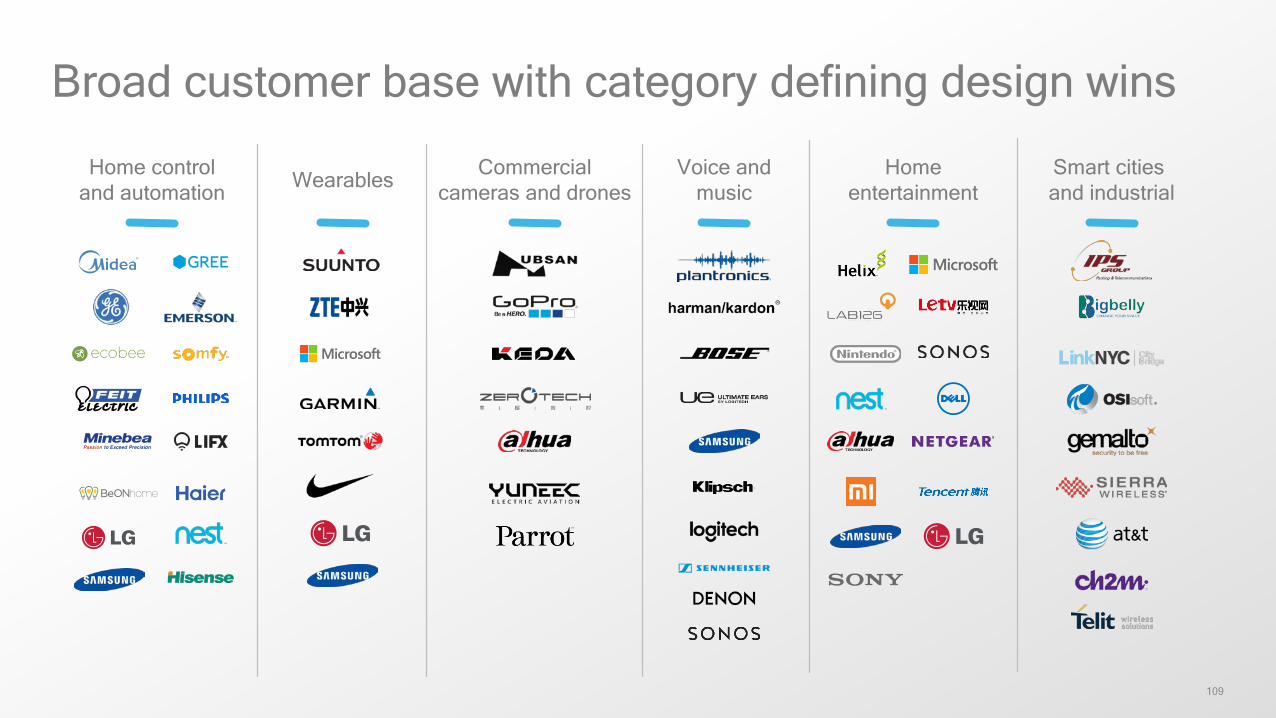

Broad customer base with category defining design wins

Home controland automation Wearables Commercial

cameras and dronesVoice and

musicHome

entertainmentSmart cities and industrial

Product announcements

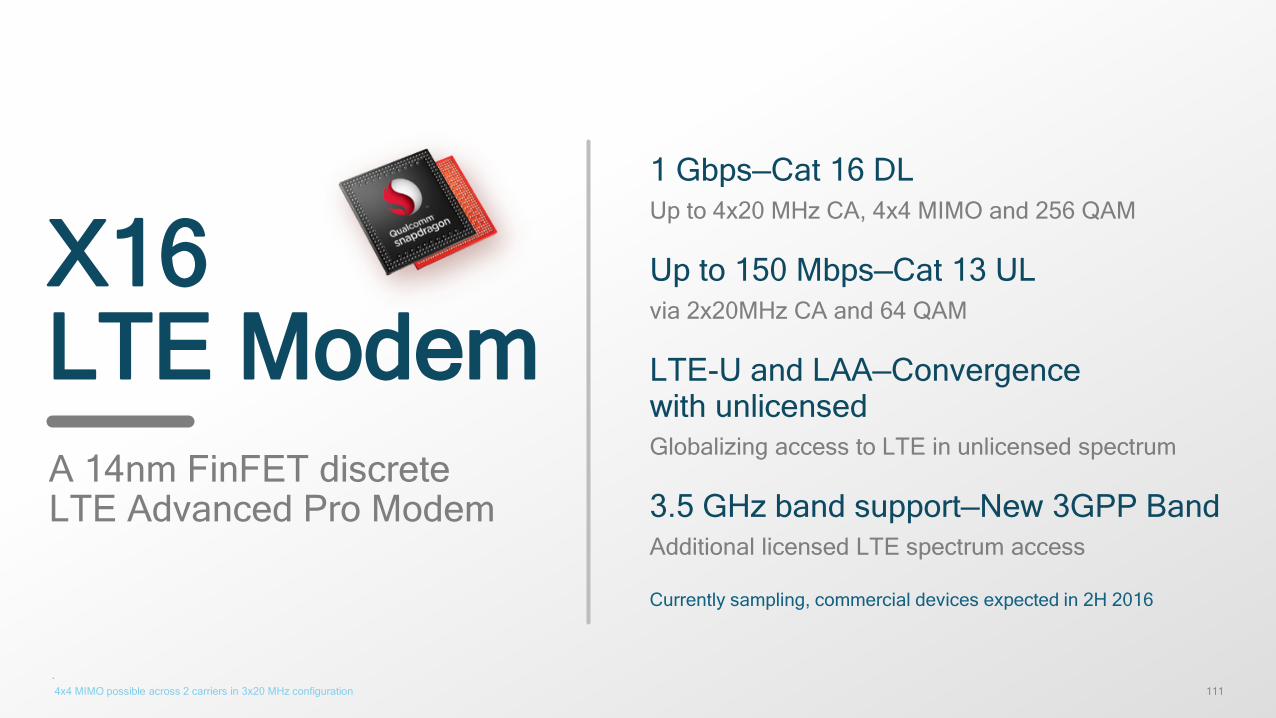

111.4x4 MIMO possible across 2 carriers in 3x20 MHz configuration

X16LTE ModemA 14nm FinFET discreteLTE Advanced Pro Modem

1 Gbps—Cat 16 DLUp to 4x20 MHz CA, 4x4 MIMO and 256 QAM

Up to 150 Mbps—Cat 13 ULvia 2x20MHz CA and 64 QAM

LTE-U and LAA—Convergence with unlicensedGlobalizing access to LTE in unlicensed spectrum

3.5 GHz band support—New 3GPP BandAdditional licensed LTE spectrum access

Currently sampling, commercial devices expected in 2H 2016

112* Performance against previous generation. ^ Strategy analytics, global smartphone reviews, ASPs and price tier forecasts: 2003-2020, July 2015. Growth rates for Asia Pacific [$100-$299 price band, 2015-2016]

Introducing

Qualcomm® Snapdragon™

First 14 FinFET in 600 tier Performance leadership combined with 35%* lower power

4G+ All Mode X9 LTESupports up to 300Mbps DL / 150Mbps UL (Cat 7/13)and 802.11ac MU-MIMO

Leading high-tier user experiencesFull HD display, 4K HEVC Camcorder, Premium camera experience, PC-class graphics

Designed for high-growth segmentsMid-High tier growing faster than total handset sales^

625

113

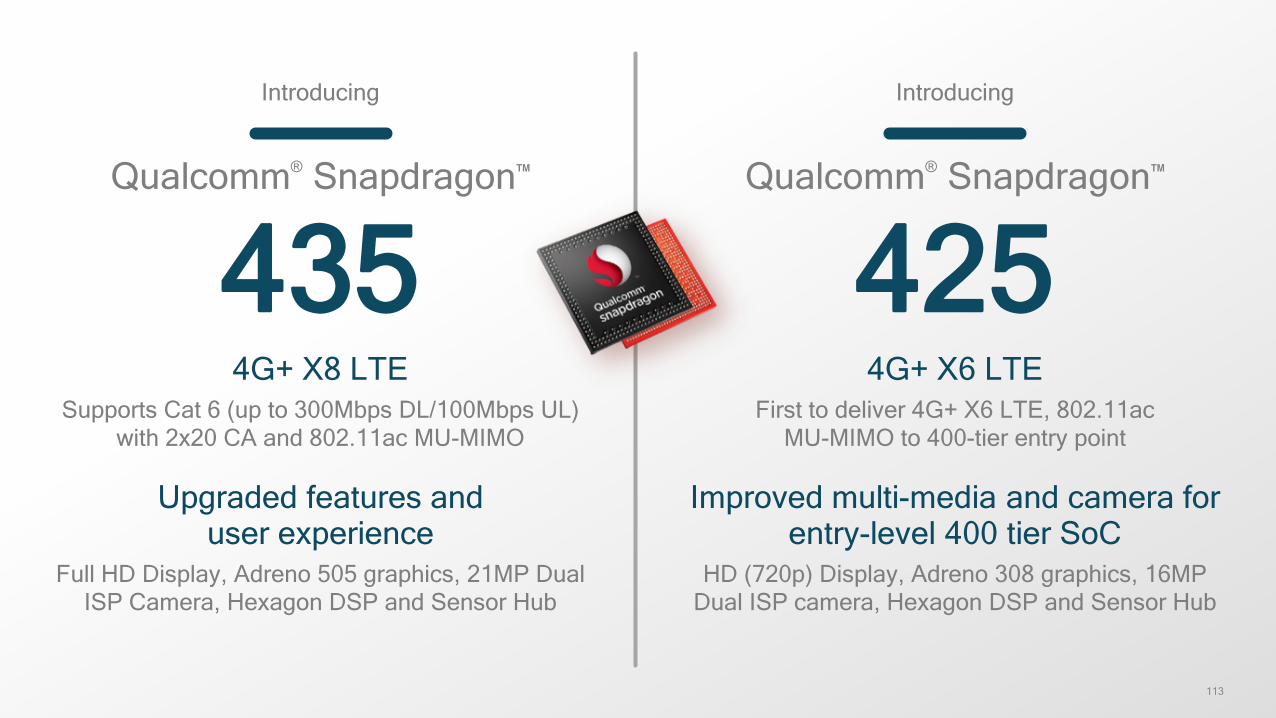

4G+ X8 LTESupports Cat 6 (up to 300Mbps DL/100Mbps UL)

with 2x20 CA and 802.11ac MU-MIMO

Upgraded features anduser experience

Full HD Display, Adreno 505 graphics, 21MP Dual ISP Camera, Hexagon DSP and Sensor Hub

4G+ X6 LTEFirst to deliver 4G+ X6 LTE, 802.11ac

MU-MIMO to 400-tier entry point

Improved multi-media and camera for entry-level 400 tier SoC

HD (720p) Display, Adreno 308 graphics, 16MP Dual ISP camera, Hexagon DSP and Sensor Hub

Introducing

Qualcomm® Snapdragon™

435

Introducing

Qualcomm® Snapdragon™

425

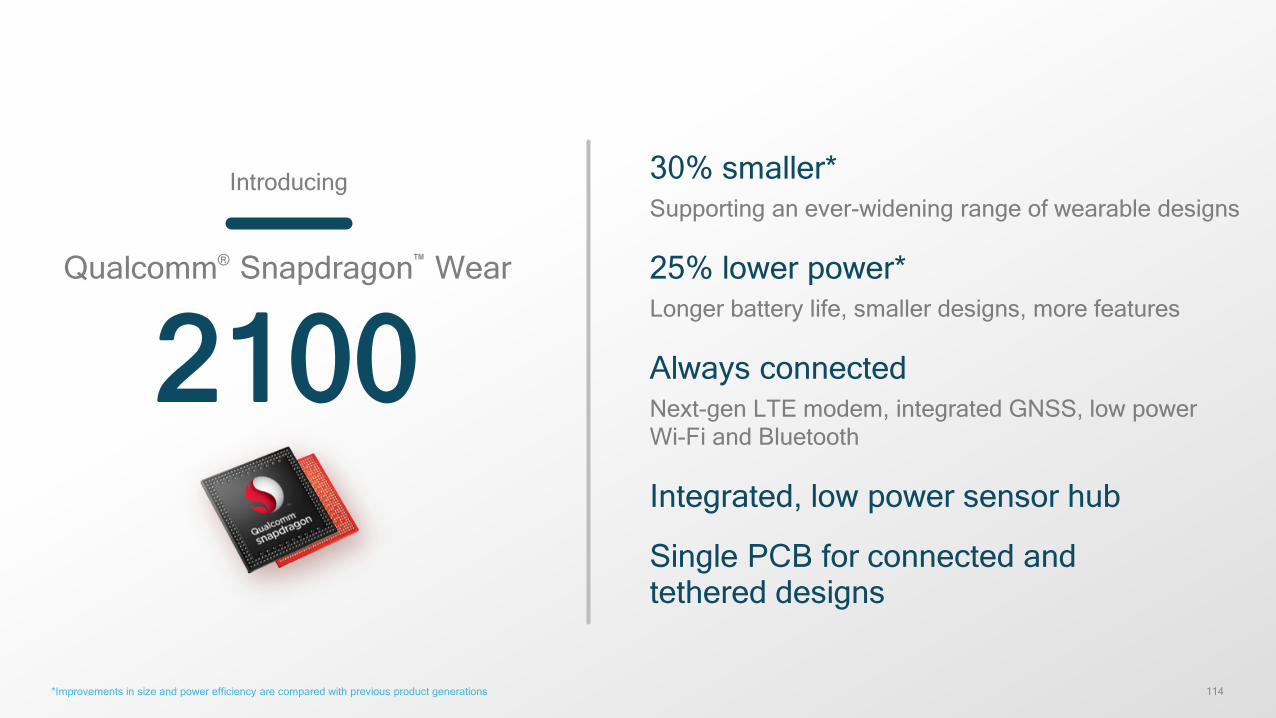

114*Improvements in size and power efficiency are compared with previous product generations

Introducing

Qualcomm® Snapdragon™ Wear

30% smaller*Supporting an ever-widening range of wearable designs

25% lower power*Longer battery life, smaller designs, more features

Always connectedNext-gen LTE modem, integrated GNSS, low powerWi-Fi and Bluetooth

Integrated, low power sensor hub

Single PCB for connected andtethered designs

2100

115

Summary

Focused execution

Growth strategy

Margin expansion

Mobile technology leadership

Adjacent opportunities

Mobile

George Davis

EVP and Chief Financial Officer,Qualcomm Incorporated

117

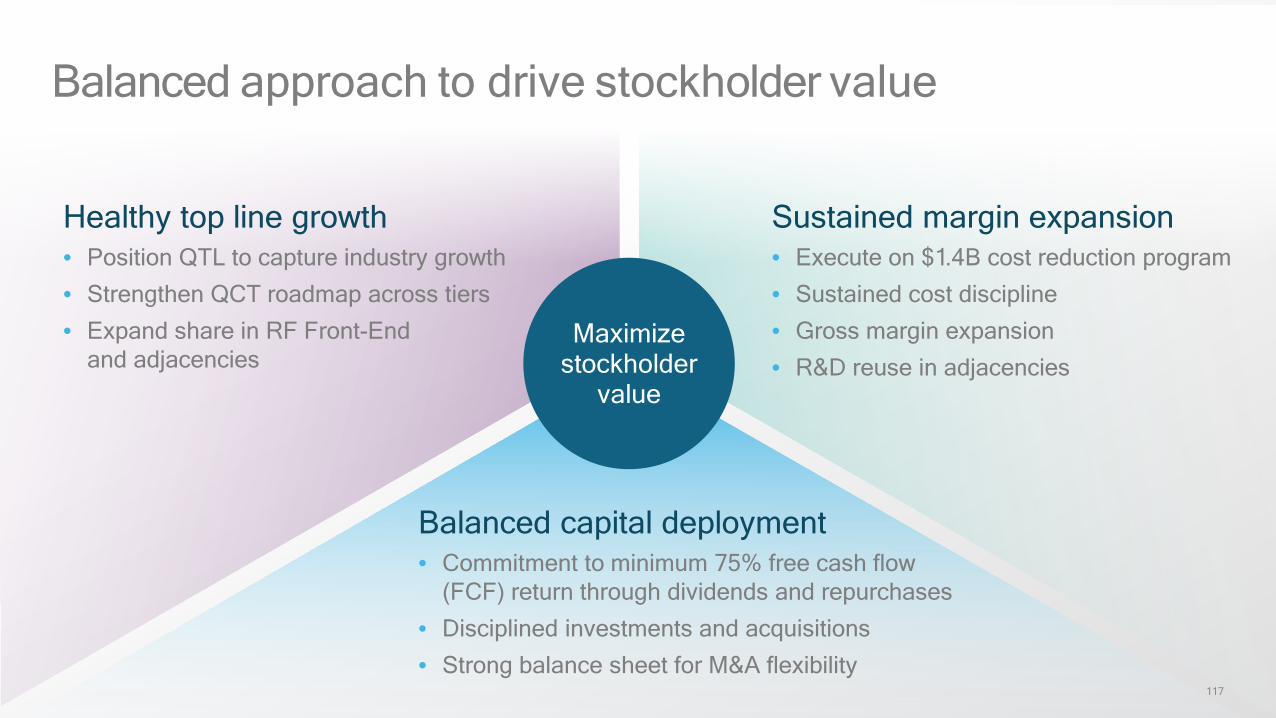

Balanced approach to drive stockholder value

Maximizestockholder

value

Healthy top line growth• Position QTL to capture industry growth

• Strengthen QCT roadmap across tiers

• Expand share in RF Front-Endand adjacencies

Sustained margin expansion • Execute on $1.4B cost reduction program

• Sustained cost discipline

• Gross margin expansion

• R&D reuse in adjacencies

Balanced capital deployment• Commitment to minimum 75% free cash flow

(FCF) return through dividends and repurchases

• Disciplined investments and acquisitions

• Strong balance sheet for M&A flexibility

Top-line growth

119

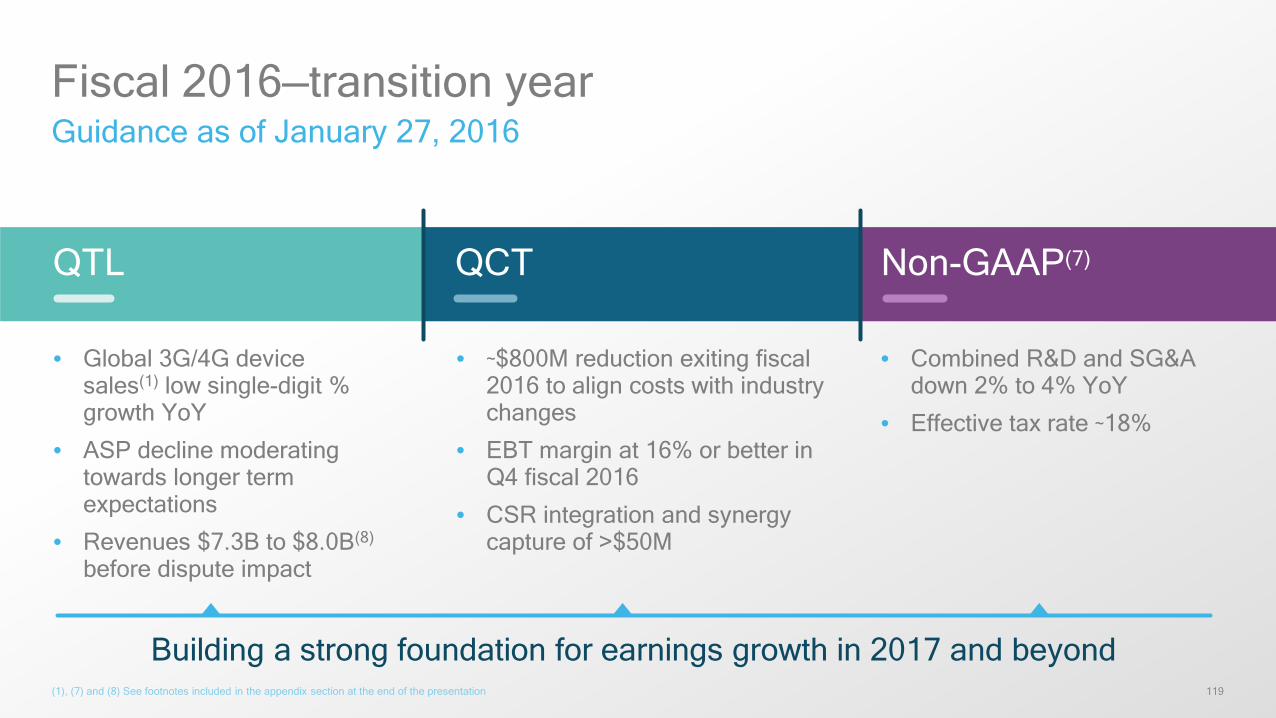

Fiscal 2016—transition yearGuidance as of January 27, 2016

(1), (7) and (8) See footnotes included in the appendix section at the end of the presentation

QTL Non-GAAP(7)

• ~$800M reduction exiting fiscal 2016 to align costs with industry changes

• EBT margin at 16% or better in Q4 fiscal 2016

• CSR integration and synergy capture of >$50M

• Global 3G/4G device sales(1) low single-digit % growth YoY

• ASP decline moderating towards longer term expectations

• Revenues $7.3B to $8.0B(8)

before dispute impact

• Combined R&D and SG&A down 2% to 4% YoY

• Effective tax rate ~18%

Building a strong foundation for earnings growth in 2017 and beyond

QCT

120

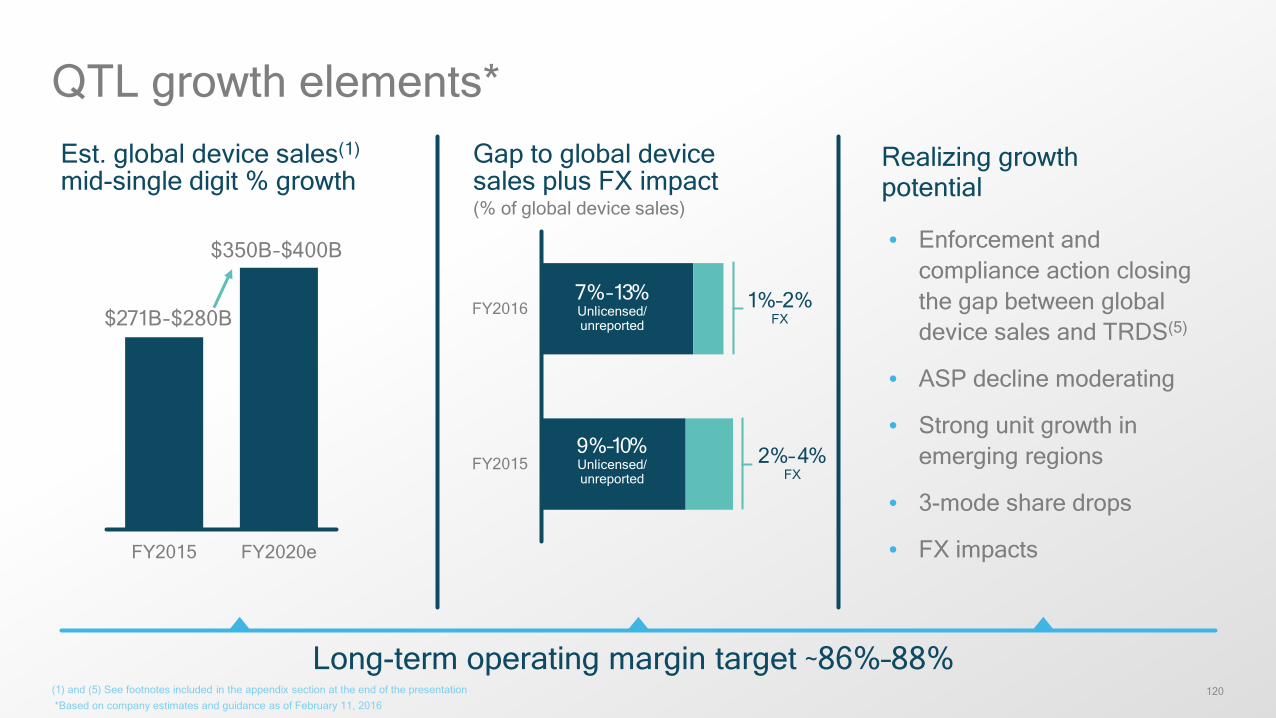

FY2015 FY2020e

QTL growth elements*

(1) and (5) See footnotes included in the appendix section at the end of the presentation*Based on company estimates and guidance as of February 11, 2016

FY2015

FY2016

$350B–$400B

$271B–$280B

Est. global device sales(1)

mid-single digit % growthGap to global device sales plus FX impact(% of global device sales)

2%–4%FX

• Enforcement and compliance action closing the gap between global device sales and TRDS(5)

• ASP decline moderating

• Strong unit growth in emerging regions

• 3-mode share drops

• FX impacts

Realizing growthpotential

1%–2%FX

7%–13%Unlicensed/unreported

9%–10%Unlicensed/unreported

Long-term operating margin target ~86%–88%

121

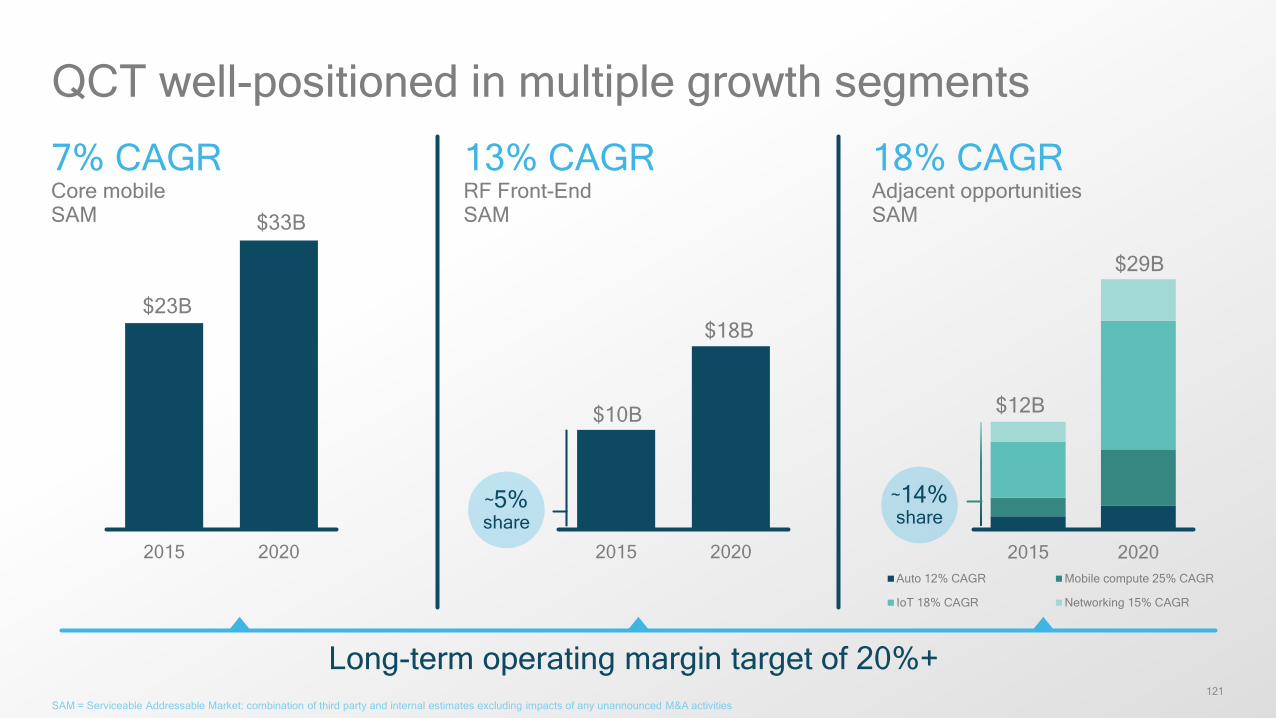

2015 2020Auto 12% CAGR Mobile compute 25% CAGR

IoT 18% CAGR Networking 15% CAGR

2015 20202015 2020

QCT well-positioned in multiple growth segments

SAM = Serviceable Addressable Market: combination of third party and internal estimates excluding impacts of any unannounced M&A activities

$23B

$33B

$12B

$29B

Long-term operating margin target of 20%+

~14%share

~5%share

$18B

$10B

7% CAGRCore mobile SAM

13% CAGRRF Front-EndSAM

18% CAGRAdjacent opportunities SAM

122

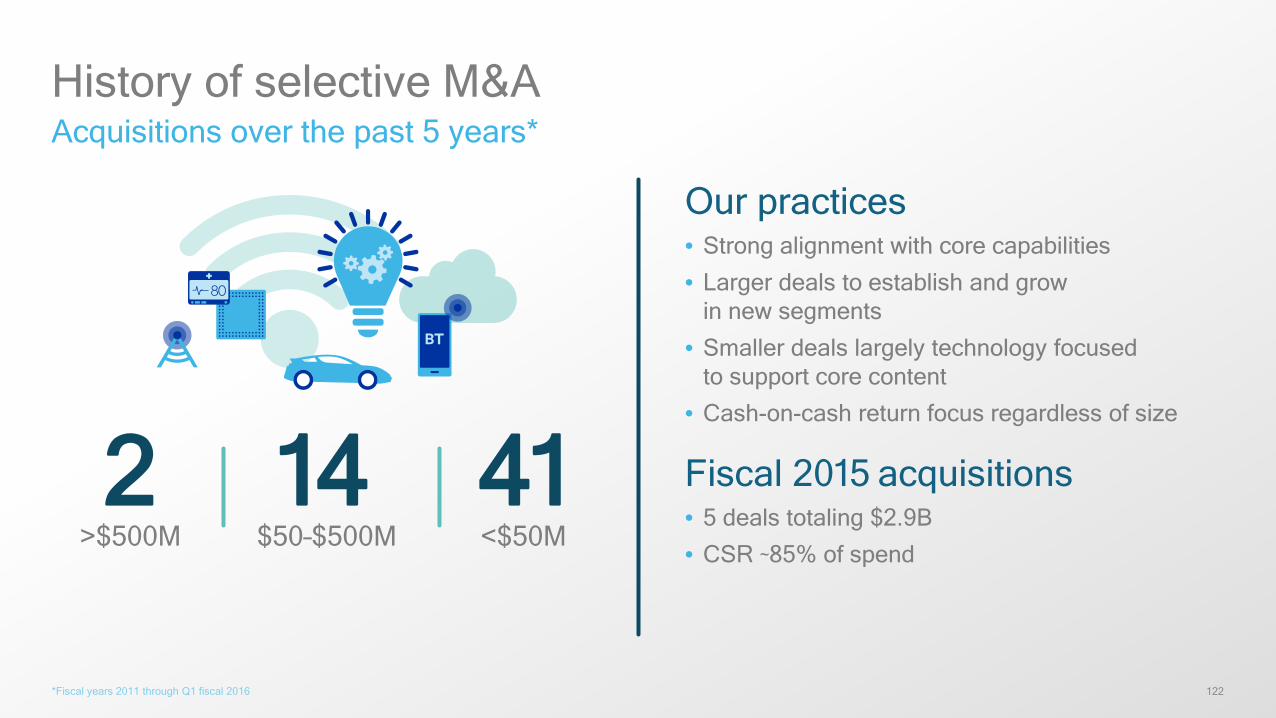

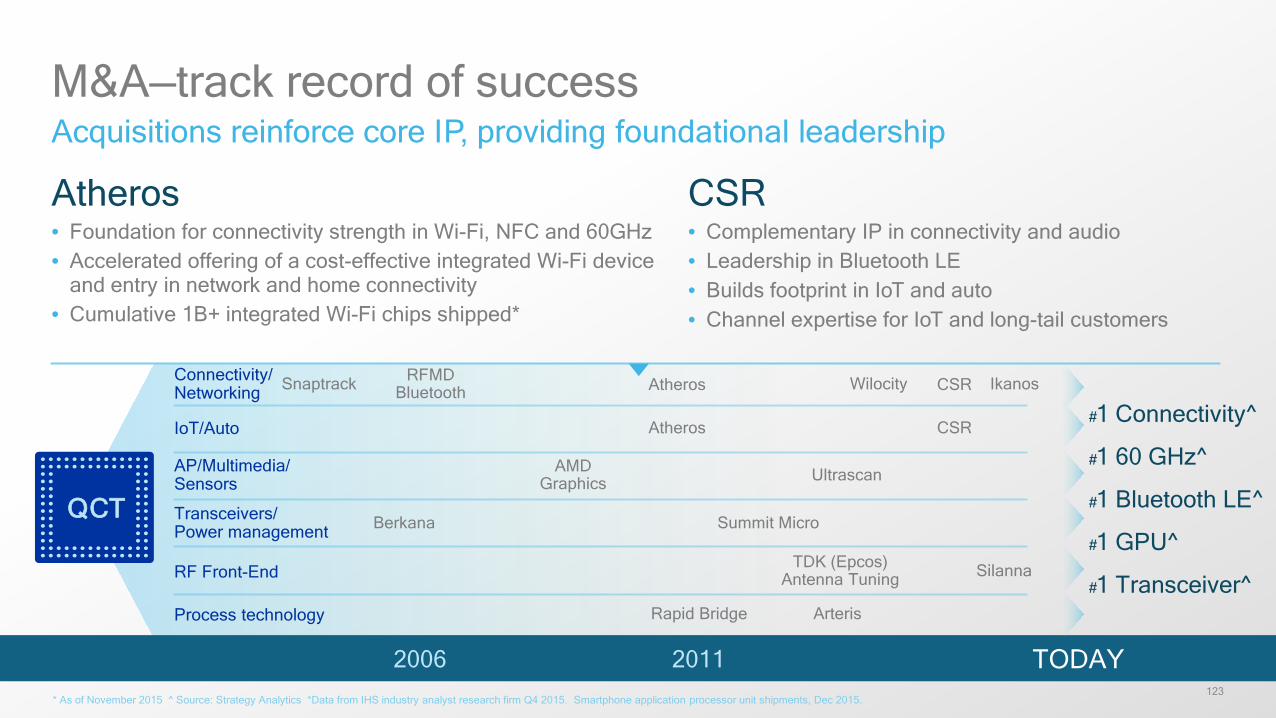

History of selective M&AAcquisitions over the past 5 years*

*Fiscal years 2011 through Q1 fiscal 2016

Our practices• Strong alignment with core capabilities

• Larger deals to establish and grow in new segments

• Smaller deals largely technology focused to support core content

• Cash-on-cash return focus regardless of size

Fiscal 2015 acquisitions• 5 deals totaling $2.9B

• CSR ~85% of spend>$500M2

$50–$500M14

<$50M41

123

CSR• Complementary IP in connectivity and audio• Leadership in Bluetooth LE• Builds footprint in IoT and auto• Channel expertise for IoT and long-tail customers

M&A—track record of successAcquisitions reinforce core IP, providing foundational leadership

* As of November 2015 ^ Source: Strategy Analytics *Data from IHS industry analyst research firm Q4 2015. Smartphone application processor unit shipments, Dec 2015.

2006 2011 TODAY

Atheros• Foundation for connectivity strength in Wi-Fi, NFC and 60GHz• Accelerated offering of a cost-effective integrated Wi-Fi device

and entry in network and home connectivity• Cumulative 1B+ integrated Wi-Fi chips shipped*

#1 Connectivity^

#1 60 GHz^

#1 Bluetooth LE^

#1 GPU^

#1 Transceiver^

Berkana

Arteris

TDK (Epcos)Antenna Tuning

AMDGraphics

Wilocity

Summit Micro

RF Front-End

Connectivity/Networking

AP/Multimedia/ Sensors

Transceivers/ Power management

RFMDBluetooth

IoT/Auto

Ikanos

Ultrascan

Process technology Rapid Bridge

Snaptrack

Silanna

QCT

Atheros CSR

Atheros CSR

124

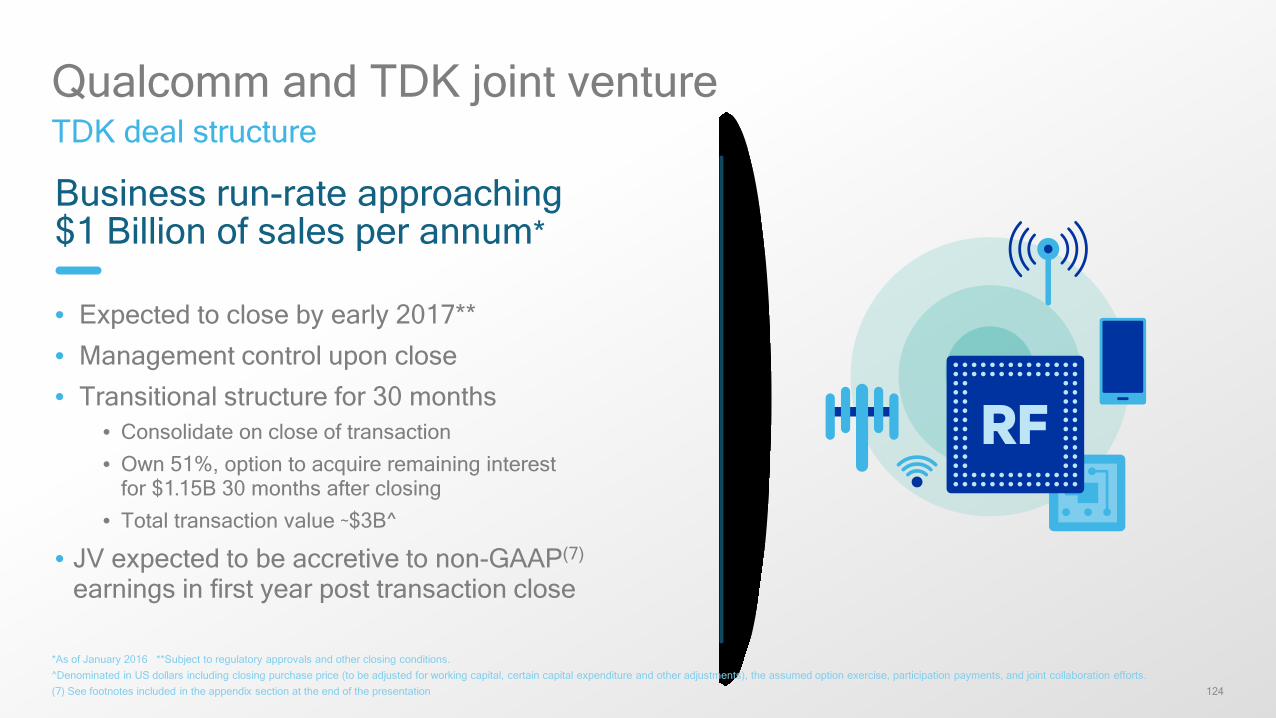

Qualcomm and TDK joint ventureTDK deal structure

*As of January 2016 **Subject to regulatory approvals and other closing conditions. ^Denominated in US dollars including closing purchase price (to be adjusted for working capital, certain capital expenditure and other adjustments), the assumed option exercise, participation payments, and joint collaboration efforts.(7) See footnotes included in the appendix section at the end of the presentation

Business run-rate approaching$1 Billion of sales per annum*

• Expected to close by early 2017**

• Management control upon close

• Transitional structure for 30 months• Consolidate on close of transaction • Own 51%, option to acquire remaining interest

for $1.15B 30 months after closing• Total transaction value ~$3B^

• JV expected to be accretive to non-GAAP(7)

earnings in first year post transaction close

Focus on margin expansion

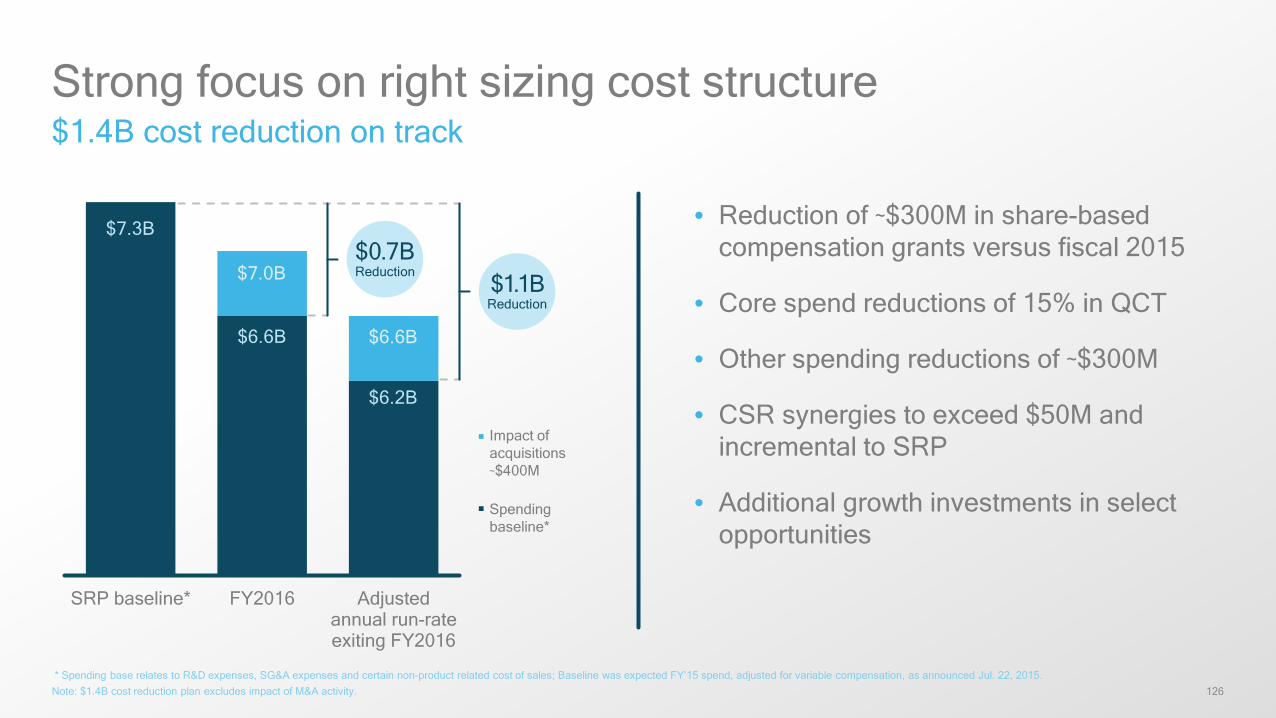

126

SRP baseline* FY2016 Adjustedannual run-rateexiting FY2016

$6.2B

$7.3B

$6.6B

$7.0B

$6.6B

Strong focus on right sizing cost structure$1.4B cost reduction on track

* Spending base relates to R&D expenses, SG&A expenses and certain non-product related cost of sales; Baseline was expected FY’15 spend, adjusted for variable compensation, as announced Jul. 22, 2015.Note: $1.4B cost reduction plan excludes impact of M&A activity.

• Reduction of ~$300M in share-based compensation grants versus fiscal 2015

• Core spend reductions of 15% in QCT

• Other spending reductions of ~$300M

• CSR synergies to exceed $50M and incremental to SRP

• Additional growth investments in select opportunities

$1.1BReduction

$0.7BReduction

Impact of acquisitions ~$400M

Spending baseline*

127

Margin expansion

Improved IP/Tech R&D reuse

Supply chain optimization

Aligned incentive structure

BU structure—accountability, agility

Value-based feature selection

Sustained focus on cost

efficiency

128

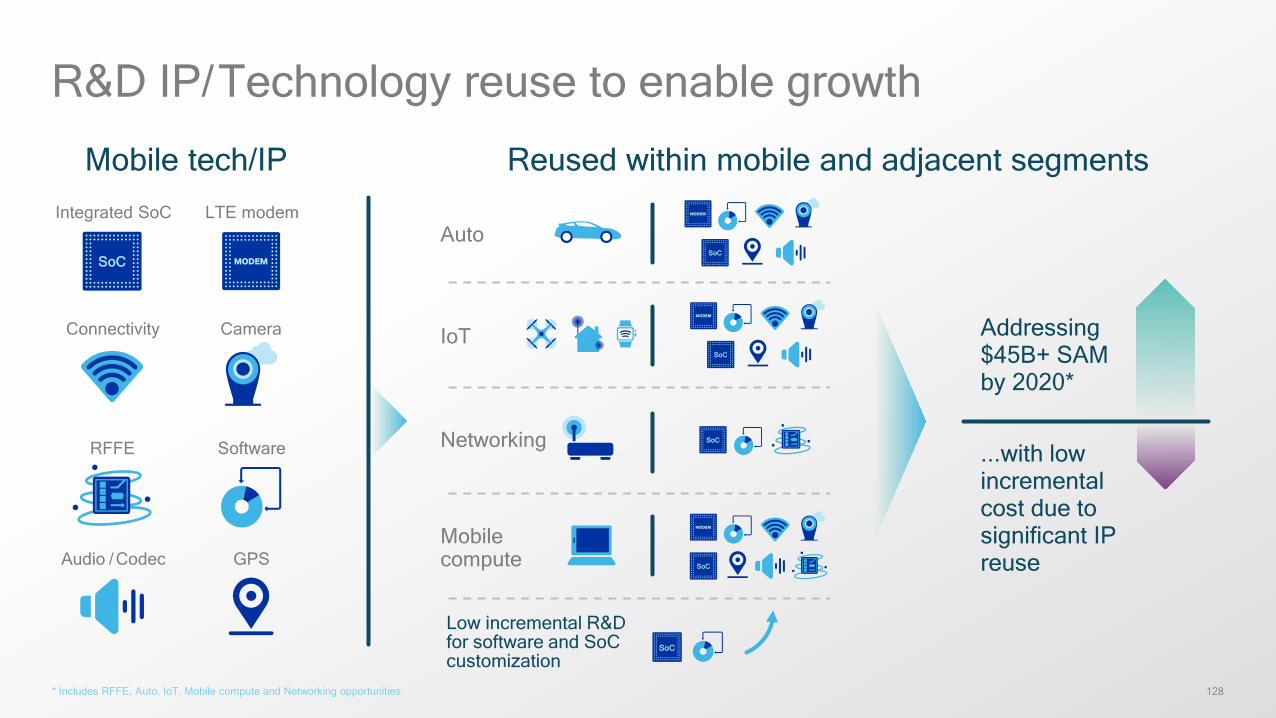

R&D IP/ Technology reuse to enable growth

* Includes RFFE, Auto, IoT, Mobile compute and Networking opportunities

Mobile tech/IP Reused within mobile and adjacent segments

Addressing $45B+ SAM by 2020*

...with low incremental cost due to significant IP reuse

Integrated SoC

Camera

LTE modem

Connectivity

RFFE Software

Audio / Codec GPS

SoC

Auto

IoT

Networking

Low incremental R&D for software and SoCcustomization

SoC

SoC

SoC

SoC

Mobilecompute SoC

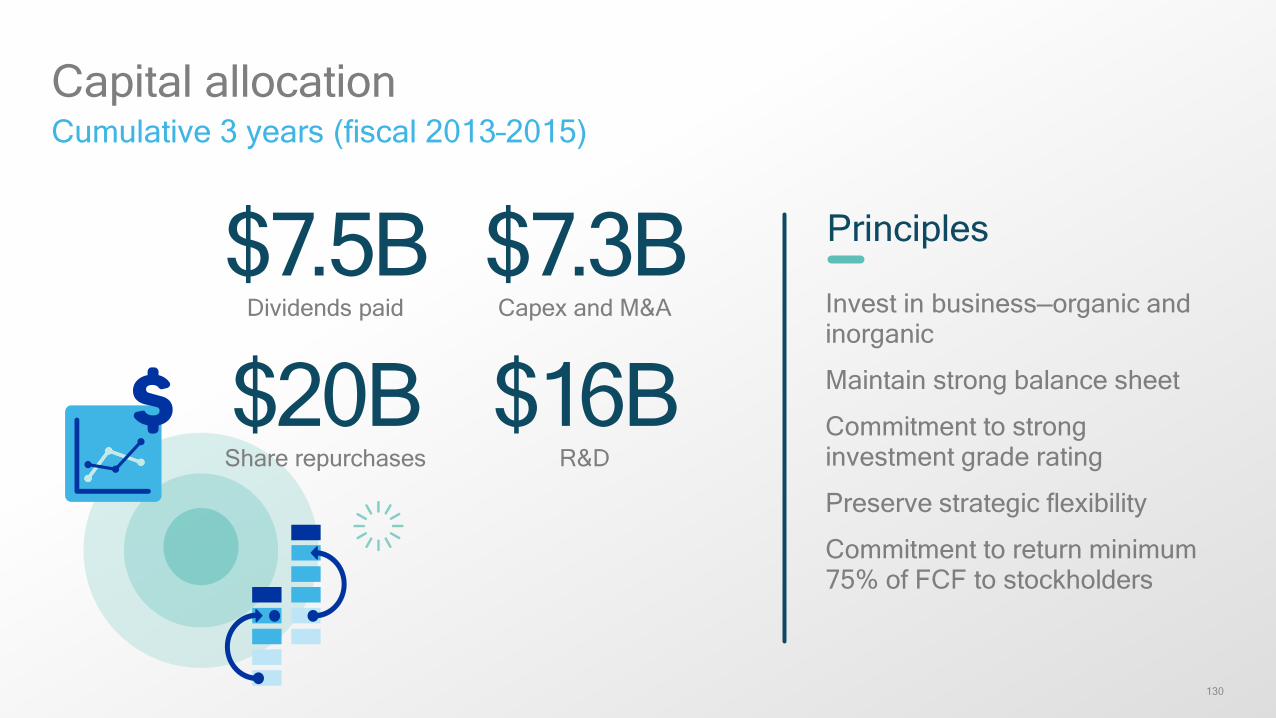

Balanced capital deployment

130

Capital allocationCumulative 3 years (fiscal 2013–2015)

Principles

Invest in business—organic and inorganic

Maintain strong balance sheet

Commitment to strong investment grade rating

Preserve strategic flexibility

Commitment to return minimum 75% of FCF to stockholders

$7.5BDividends paid

$7.3BCapex and M&A

$20BShare repurchases

$16BR&D

131

Focused executionKey takeaways—2016 analyst meeting

• Positioning the company for profitable growth

• Investing to expand our technology roadmap and lead in 5G

• Pursuing new opportunities in fast growing SAMs that build on our core technology

• M&A to accelerate and de-risk our growth agenda

• Adapting organization to improve agility and speed of decision-making

• Continuing our commitment to attractive capital returns and a strong balance sheet

Nothing in these materials is an offer to sell any of the components or devices referenced herein.

©2016 Qualcomm Incorporated and/or its subsidiaries. All Rights Reserved.

Qualcomm, Snapdragon, Adreno, Hexagon, and Qualcomm RF360 are trademarks of Qualcomm Incorporated, registered in the United States and other countries. Kryo, Qualcomm Spectra, Qualcomm Halo, Quick Charge and Snapdragon Flight are trademarks of Qualcomm Incorporated. Qualcomm VIVE is a product of Qualcomm Atheros, Inc. 2net is a product of Qualcomm Life, Inc. Other products and brand names may be trademarks or registered trademarks of their respective owners.

References in this presentation to “Qualcomm” may mean Qualcomm Incorporated, Qualcomm Technologies, Inc., and/or other subsidiaries or business units within the Qualcomm corporate structure, as applicable.

Qualcomm Incorporated includes Qualcomm’s licensing business, QTL, and the vast majority of its patent portfolio. Qualcomm Technologies, Inc., a wholly-owned subsidiary of Qualcomm Incorporated, operates, along with its subsidiaries, substantially all of Qualcomm’s engineering, research and development functions, and substantially all of its product and services businesses, including its semiconductor business, QCT.

Thank you

Follow us on:For more information, visit us at: www.qualcomm.com & www.qualcomm.com/blog

Appendix

134

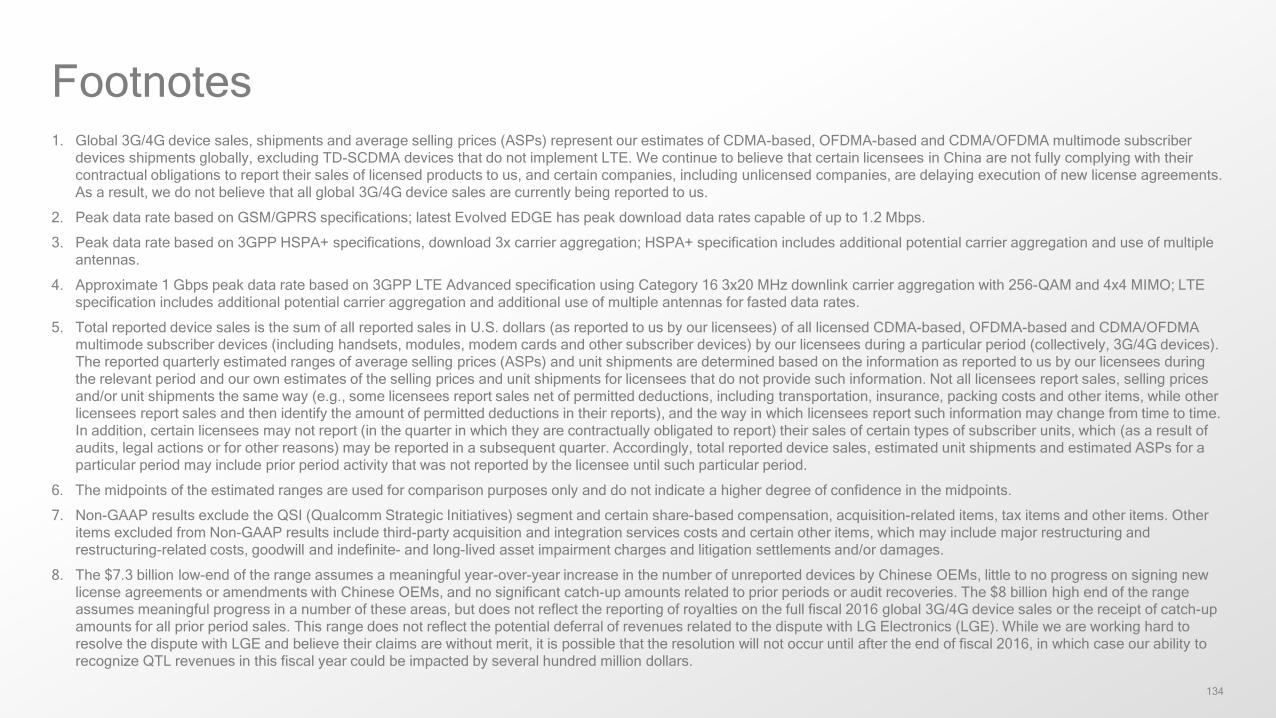

1. Global 3G/4G device sales, shipments and average selling prices (ASPs) represent our estimates of CDMA-based, OFDMA-based and CDMA/OFDMA multimode subscriber devices shipments globally, excluding TD-SCDMA devices that do not implement LTE. We continue to believe that certain licensees in China are not fully complying with their contractual obligations to report their sales of licensed products to us, and certain companies, including unlicensed companies, are delaying execution of new license agreements. As a result, we do not believe that all global 3G/4G device sales are currently being reported to us.

2. Peak data rate based on GSM/GPRS specifications; latest Evolved EDGE has peak download data rates capable of up to 1.2 Mbps.

3. Peak data rate based on 3GPP HSPA+ specifications, download 3x carrier aggregation; HSPA+ specification includes additional potential carrier aggregation and use of multiple antennas.

4. Approximate 1 Gbps peak data rate based on 3GPP LTE Advanced specification using Category 16 3x20 MHz downlink carrier aggregation with 256-QAM and 4x4 MIMO; LTE specification includes additional potential carrier aggregation and additional use of multiple antennas for fasted data rates.

5. Total reported device sales is the sum of all reported sales in U.S. dollars (as reported to us by our licensees) of all licensed CDMA-based, OFDMA-based and CDMA/OFDMA multimode subscriber devices (including handsets, modules, modem cards and other subscriber devices) by our licensees during a particular period (collectively, 3G/4G devices). The reported quarterly estimated ranges of average selling prices (ASPs) and unit shipments are determined based on the information as reported to us by our licensees during the relevant period and our own estimates of the selling prices and unit shipments for licensees that do not provide such information. Not all licensees report sales, selling prices and/or unit shipments the same way (e.g., some licensees report sales net of permitted deductions, including transportation, insurance, packing costs and other items, while other licensees report sales and then identify the amount of permitted deductions in their reports), and the way in which licensees report such information may change from time to time. In addition, certain licensees may not report (in the quarter in which they are contractually obligated to report) their sales of certain types of subscriber units, which (as a result of audits, legal actions or for other reasons) may be reported in a subsequent quarter. Accordingly, total reported device sales, estimated unit shipments and estimated ASPs for a particular period may include prior period activity that was not reported by the licensee until such particular period.

6. The midpoints of the estimated ranges are used for comparison purposes only and do not indicate a higher degree of confidence in the midpoints.

7. Non-GAAP results exclude the QSI (Qualcomm Strategic Initiatives) segment and certain share-based compensation, acquisition-related items, tax items and other items. Other items excluded from Non-GAAP results include third-party acquisition and integration services costs and certain other items, which may include major restructuring and restructuring-related costs, goodwill and indefinite- and long-lived asset impairment charges and litigation settlements and/or damages.

8. The $7.3 billion low-end of the range assumes a meaningful year-over-year increase in the number of unreported devices by Chinese OEMs, little to no progress on signing new license agreements or amendments with Chinese OEMs, and no significant catch-up amounts related to prior periods or audit recoveries. The $8 billion high end of the range assumes meaningful progress in a number of these areas, but does not reflect the reporting of royalties on the full fiscal 2016 global 3G/4G device sales or the receipt of catch-up amounts for all prior period sales. This range does not reflect the potential deferral of revenues related to the dispute with LG Electronics (LGE). While we are working hard to resolve the dispute with LGE and believe their claims are without merit, it is possible that the resolution will not occur until after the end of fiscal 2016, in which case our ability to recognize QTL revenues in this fiscal year could be impacted by several hundred million dollars.

Footnotes

Reconciliations

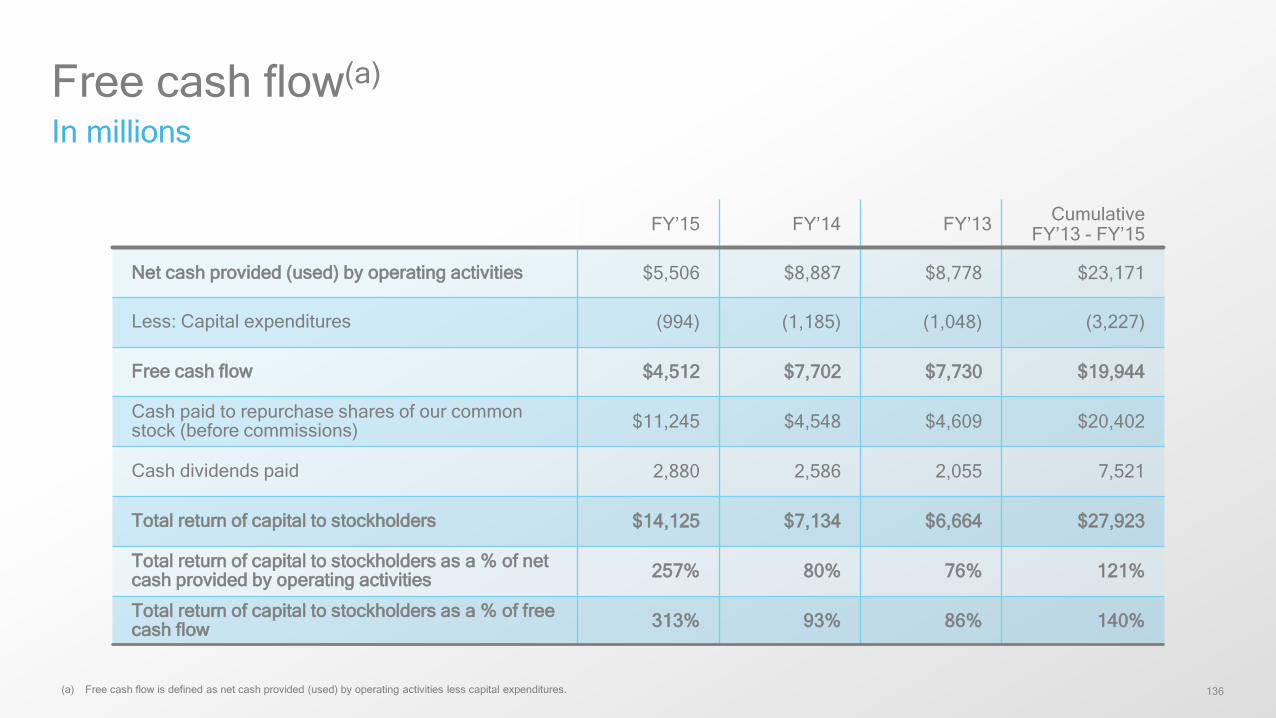

136

FY’15 FY’14 FY’13 Cumulative FY’13 - FY’15

Net cash provided (used) by operating activities $5,506 $8,887 $8,778 $23,171

Less: Capital expenditures (994) (1,185) (1,048) (3,227)

Free cash flow $4,512 $7,702 $7,730 $19,944

Cash paid to repurchase shares of our commonstock (before commissions) $11,245 $4,548 $4,609 $20,402

Cash dividends paid 2,880 2,586 2,055 7,521

Total return of capital to stockholders $14,125 $7,134 $6,664 $27,923

Total return of capital to stockholders as a % of net cash provided by operating activities 257% 80% 76% 121%

Total return of capital to stockholders as a % of free cash flow 313% 93% 86% 140%

Free cash flow(a)

In millions

(a) Free cash flow is defined as net cash provided (used) by operating activities less capital expenditures.

137

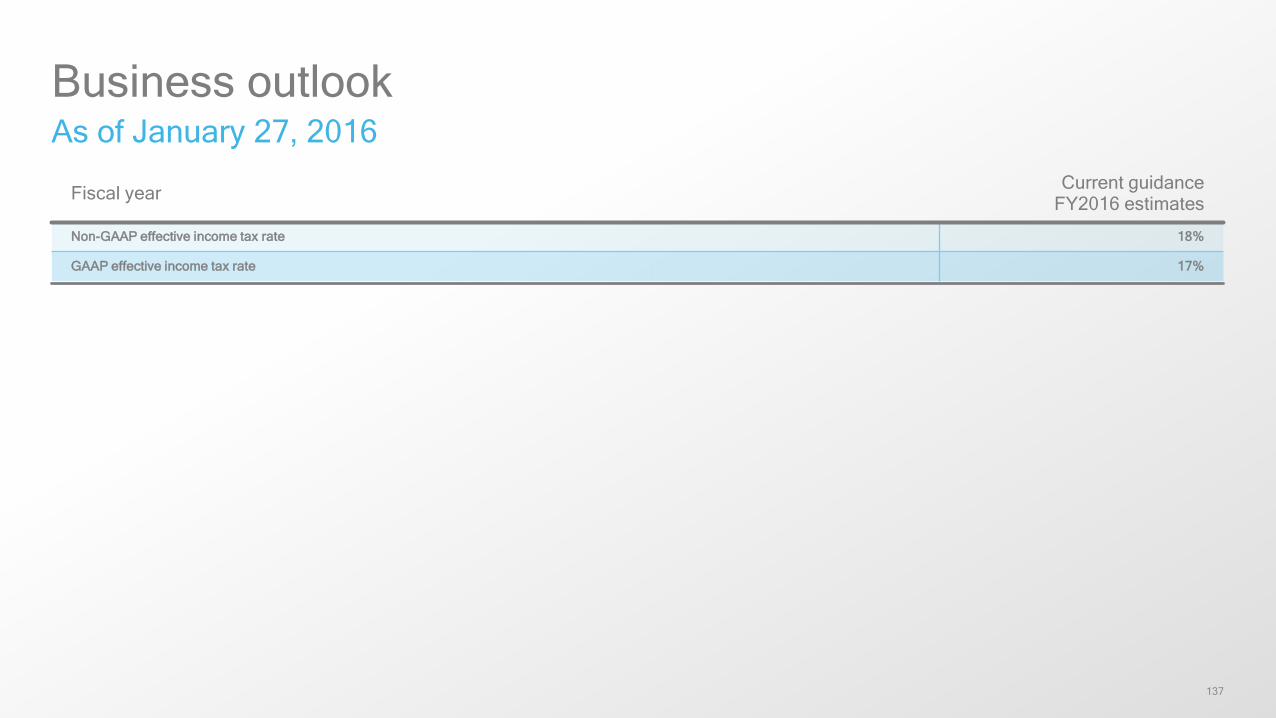

Business outlookAs of January 27, 2016

Fiscal year Current guidance FY2016 estimates

Non-GAAP effective income tax rate 18%

GAAP effective income tax rate 17%

138

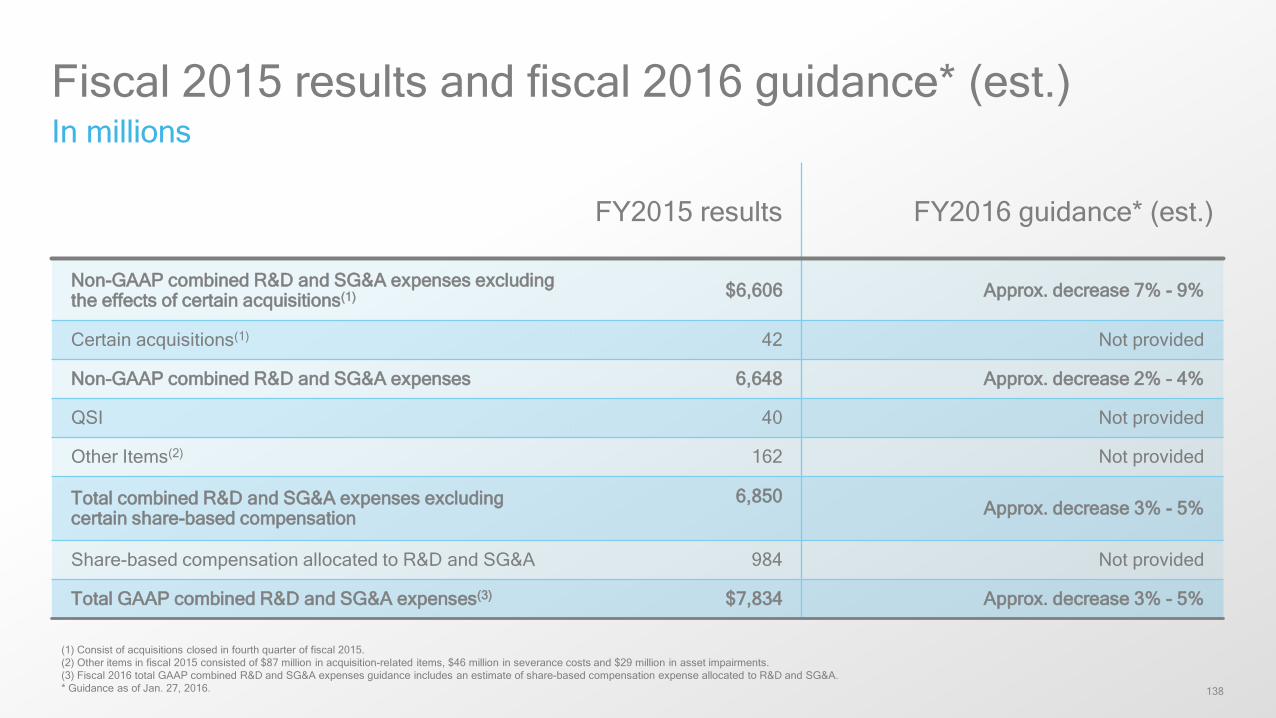

Fiscal 2015 results and fiscal 2016 guidance* (est.)In millions

(1) Consist of acquisitions closed in fourth quarter of fiscal 2015.(2) Other items in fiscal 2015 consisted of $87 million in acquisition-related items, $46 million in severance costs and $29 million in asset impairments.(3) Fiscal 2016 total GAAP combined R&D and SG&A expenses guidance includes an estimate of share-based compensation expense allocated to R&D and SG&A.* Guidance as of Jan. 27, 2016.

FY2015 results FY2016 guidance* (est.)

Non-GAAP combined R&D and SG&A expenses excluding the effects of certain acquisitions(1) $6,606 Approx. decrease 7% - 9%

Certain acquisitions(1) 42 Not provided

Non-GAAP combined R&D and SG&A expenses 6,648 Approx. decrease 2% - 4%

QSI 40 Not provided

Other Items(2) 162 Not provided

Total combined R&D and SG&A expenses excluding certain share-based compensation

6,850Approx. decrease 3% - 5%

Share-based compensation allocated to R&D and SG&A 984 Not provided

Total GAAP combined R&D and SG&A expenses(3) $7,834 Approx. decrease 3% - 5%