20151210 presentatie 'being agile in a fintech world

TRANSCRIPT

Pascal Spelier, 11 december 2015

Being Agile in a FinTech World

2

The Golden Circle: Start with WHY

4

Three drivers for change

Changingcustomer behaviour

New technology

Changingregulations &

legislation

5

The customer wants changeLack of trust has changed the relationship between Insurers, banks and customer

The credit crisis changed the purchase drivers

Traditional banking & insurance customer is shifting to A new generation banking & insurance customer

Customers demand transparency and simplicity

Customers become more and more self-directed

Social medial create a fundamental shift in the way we communicate

6

Technology creates new opportunities28 years ago, introduction of internet

13 years ago, introduction of social media

8 years ago, introduction of smartphones

Big data

Quantified self

Internet of things

7

Regulatory challengesBasel III

Solvency II

Payment Service Directive 2

Local regulations & legislation

8

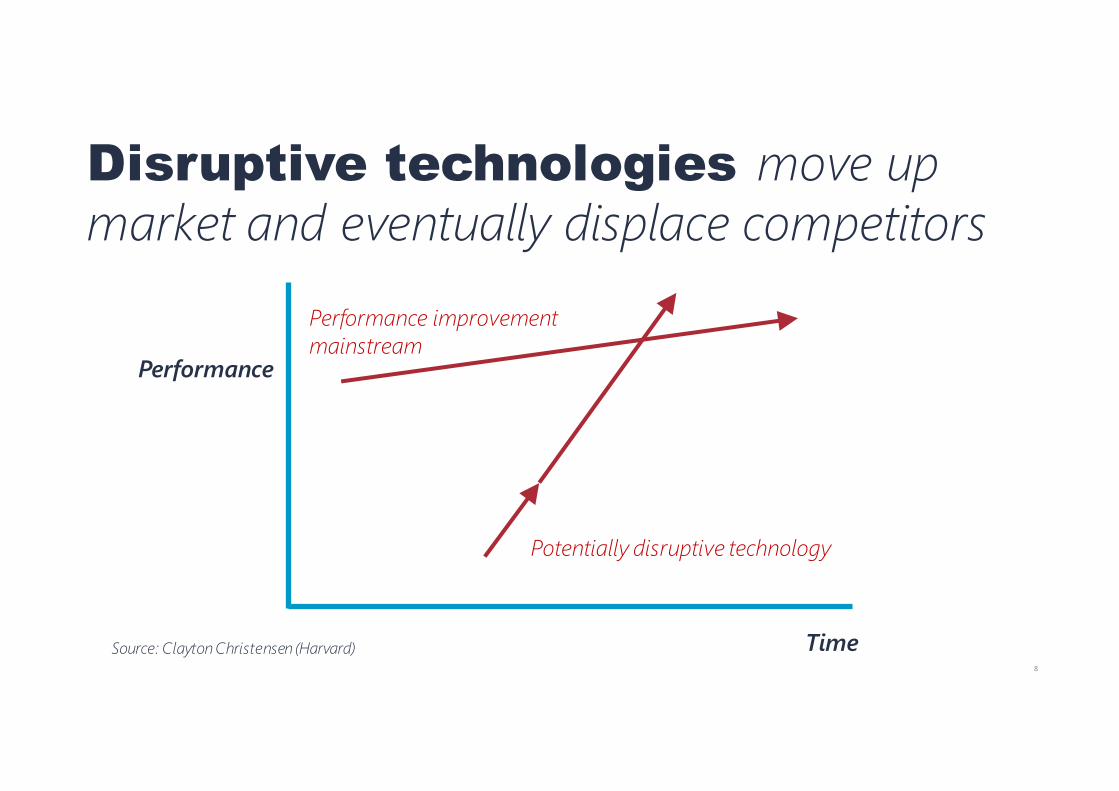

Source: Clayton Christensen (Harvard)

Performance

Time

Performance improvementmainstream

Potentially disruptive technology

Disruptive technologies move up market and eventually displace competitors

9

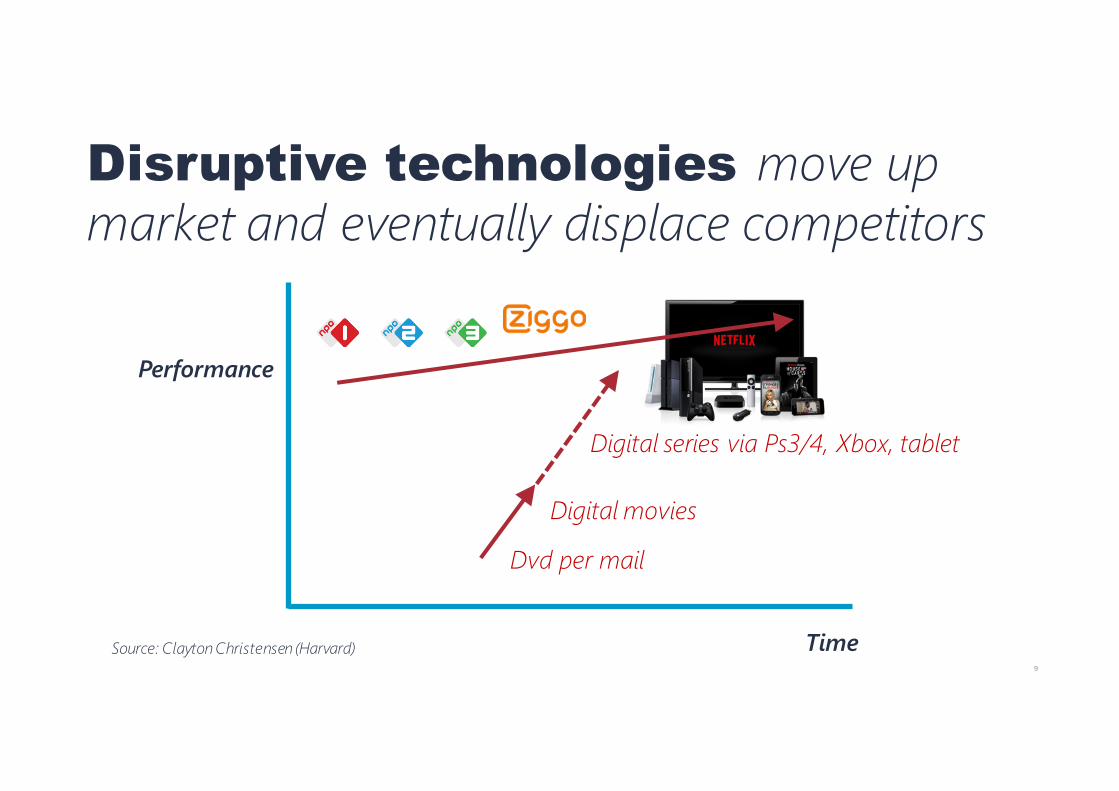

Source: Clayton Christensen (Harvard)

Performance

Time

Disruptive technologies move up market and eventually displace competitors

Dvd per mail

Digital movies

Digital series via Ps3/4, Xbox, tablet

10

Rethink your business model

11

12

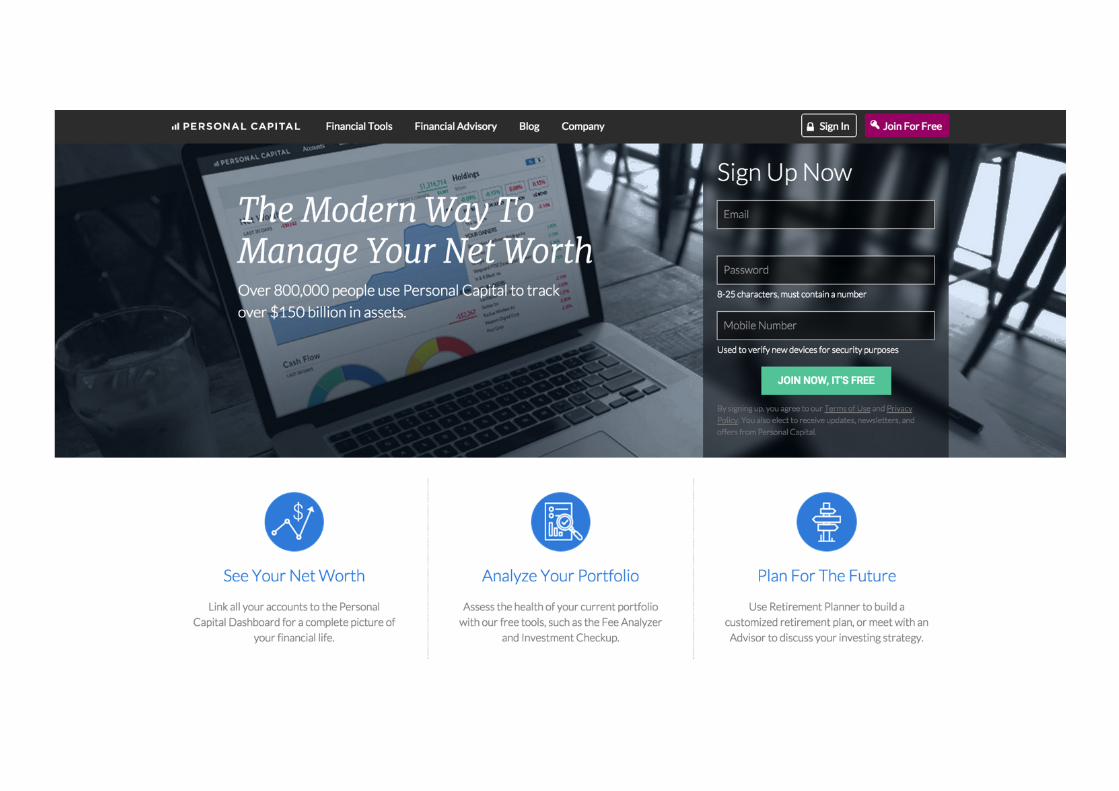

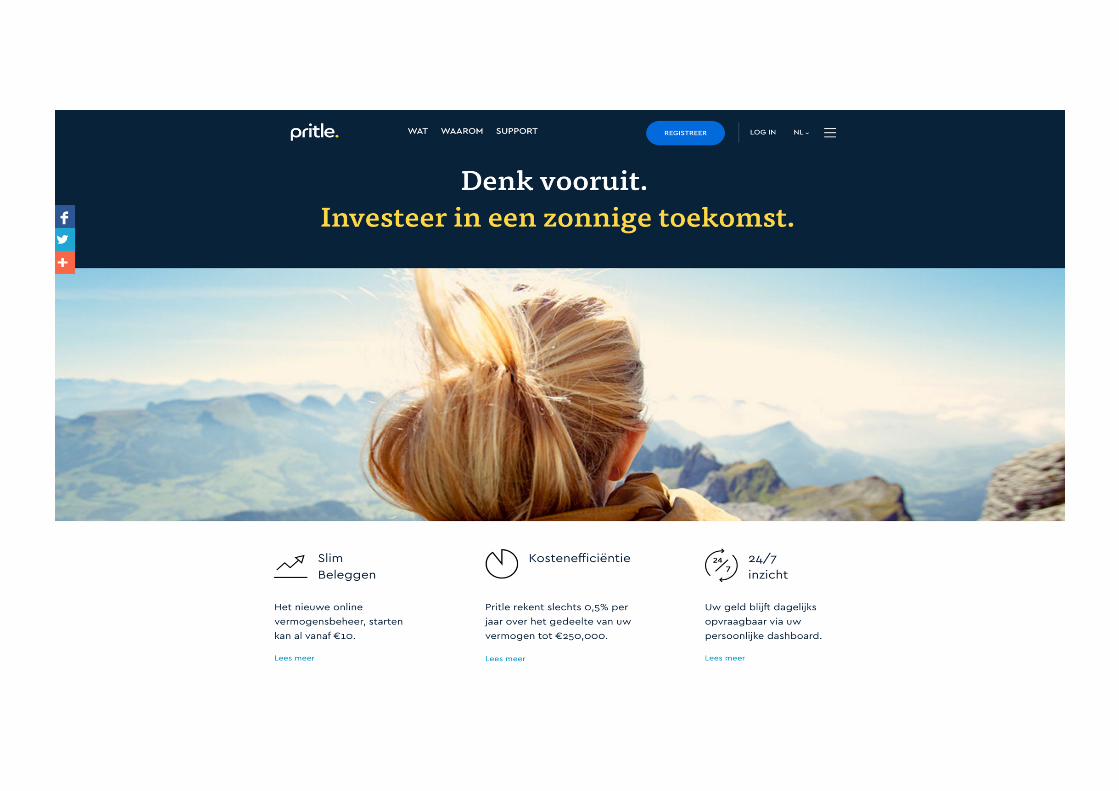

New generation settingnew standards for banking

13

New generation setting new standards for banking

14

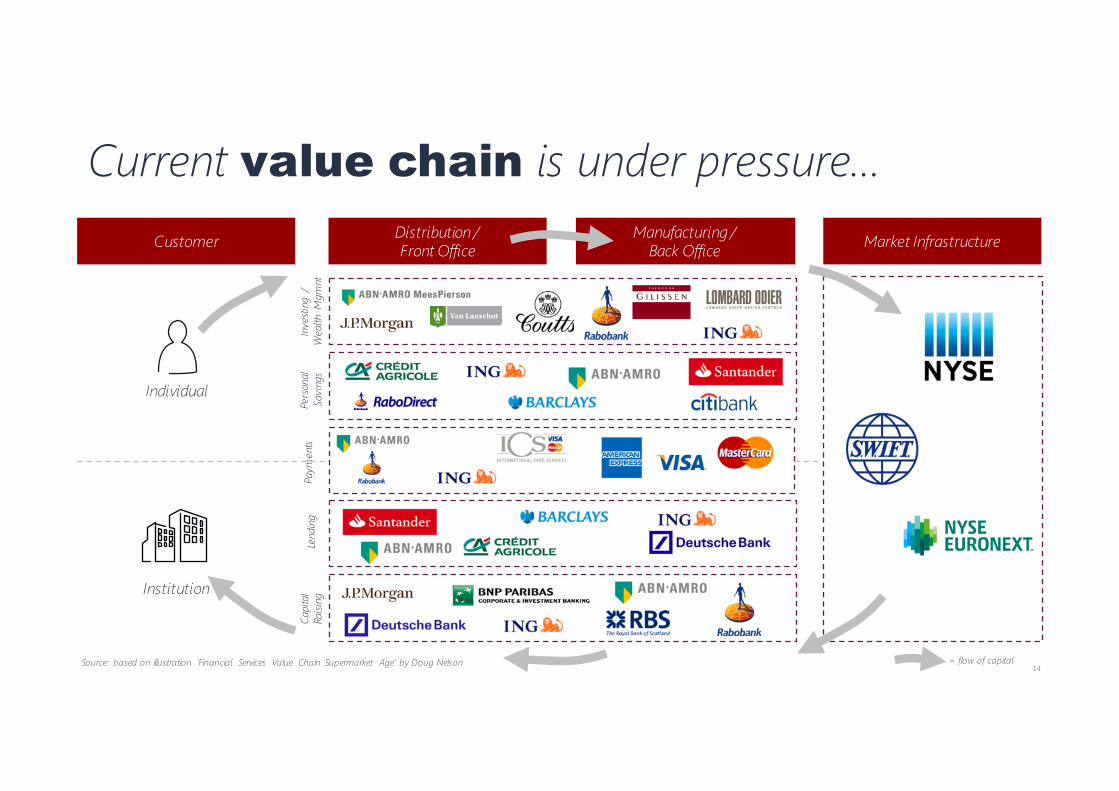

Customer Distribution / Front Office

Manufacturing / Back Office Market Infrastructure

Individual

Institution

Inve

sting

/W

ealth

Mgm

ntPe

rson

al

Savi

ngs

Lend

ing

Capi

tal

Raisi

ng

Source: based on illustration ‘Financial Services Value Chain Supermarket Age’ by Doug Nelson

Paym

ents

= flow of capital

Current value chain is under pressure…

15

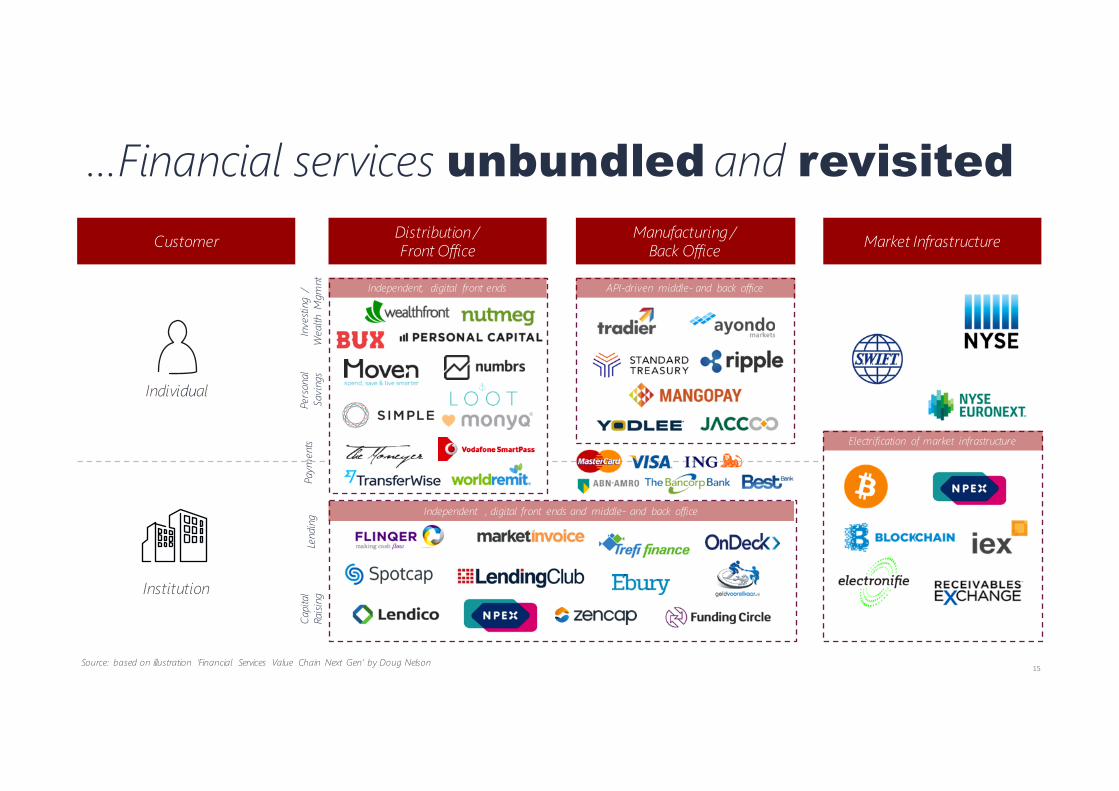

Customer Distribution / Front Office

Manufacturing / Back Office Market Infrastructure

Individual

Institution

Inve

sting

/W

ealth

Mgm

ntPe

rson

al

Savi

ngs

Lend

ing

Capi

tal

Raisi

ng

Source: based on illustration ‘Financial Services Value Chain Next Gen’ by Doug Nelson

Paym

ents

…Financial services unbundled and revisited

Independent, digital front ends API-driven middle- and back office

Electrification of market infrastructure

Independent , digital front ends and middle- and back office

16

It is not the strongest of the species that survives,

nor the most intelligent that survives.

It is the one that is the most adaptable to

change.- Darwin -

17

“We must learn whatcustomers really want, not what they say theywant or what we thinkthey should want.”EricRies– TheLean Startup

18

Bent u de tanker of het loodsbootje?

19

Bent u de tanker of het loodsbootje?

20

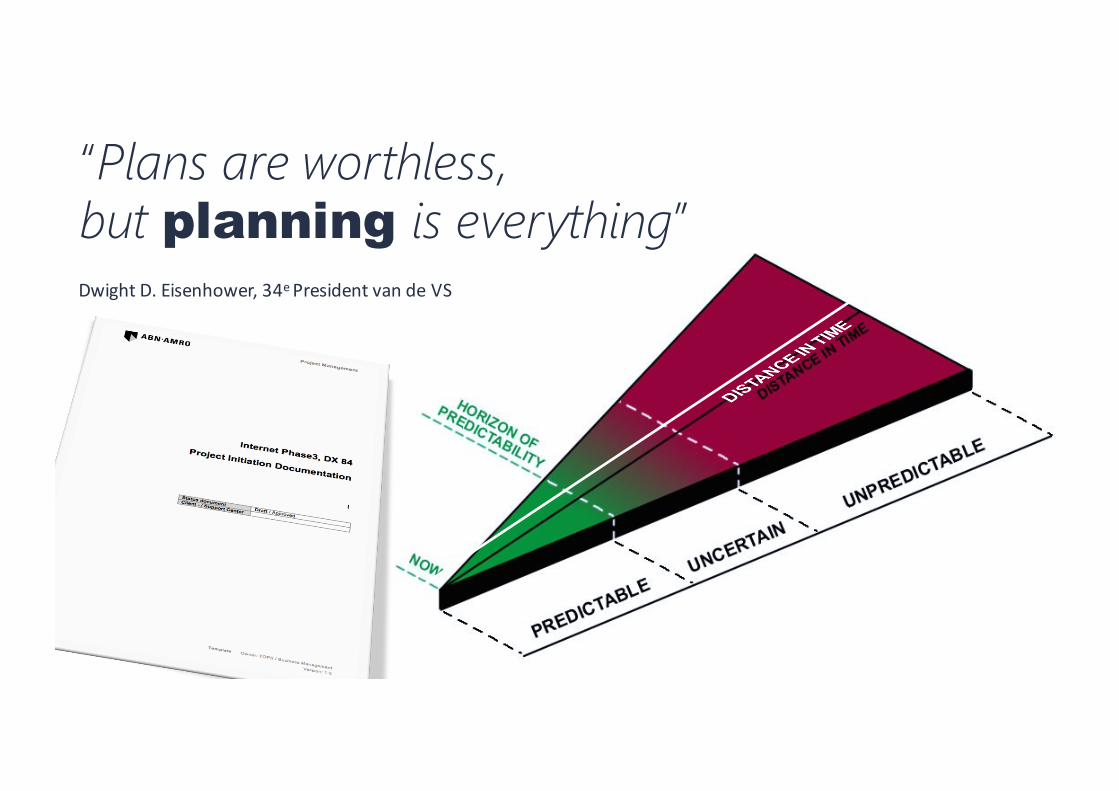

“Plans are worthless, but planning is everything”DwightD.Eisenhower,34ePresidentvandeVS

21

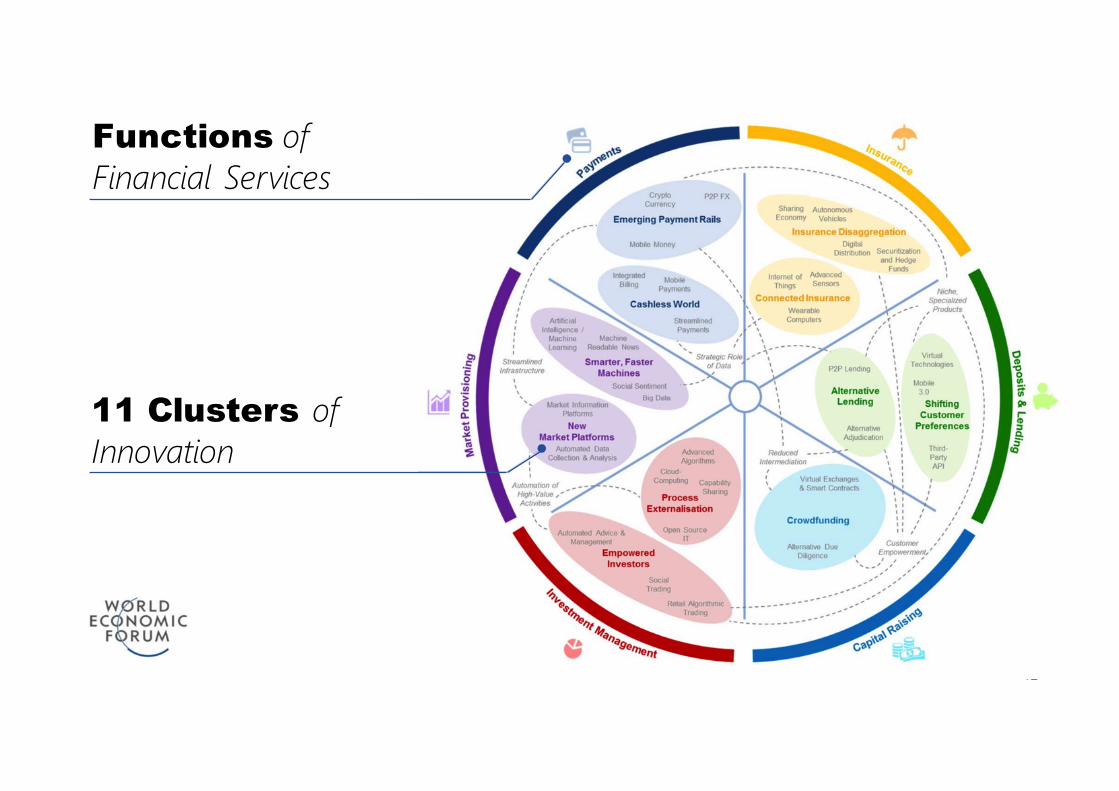

Functions of Financial Services

11 Clusters of Innovation

22

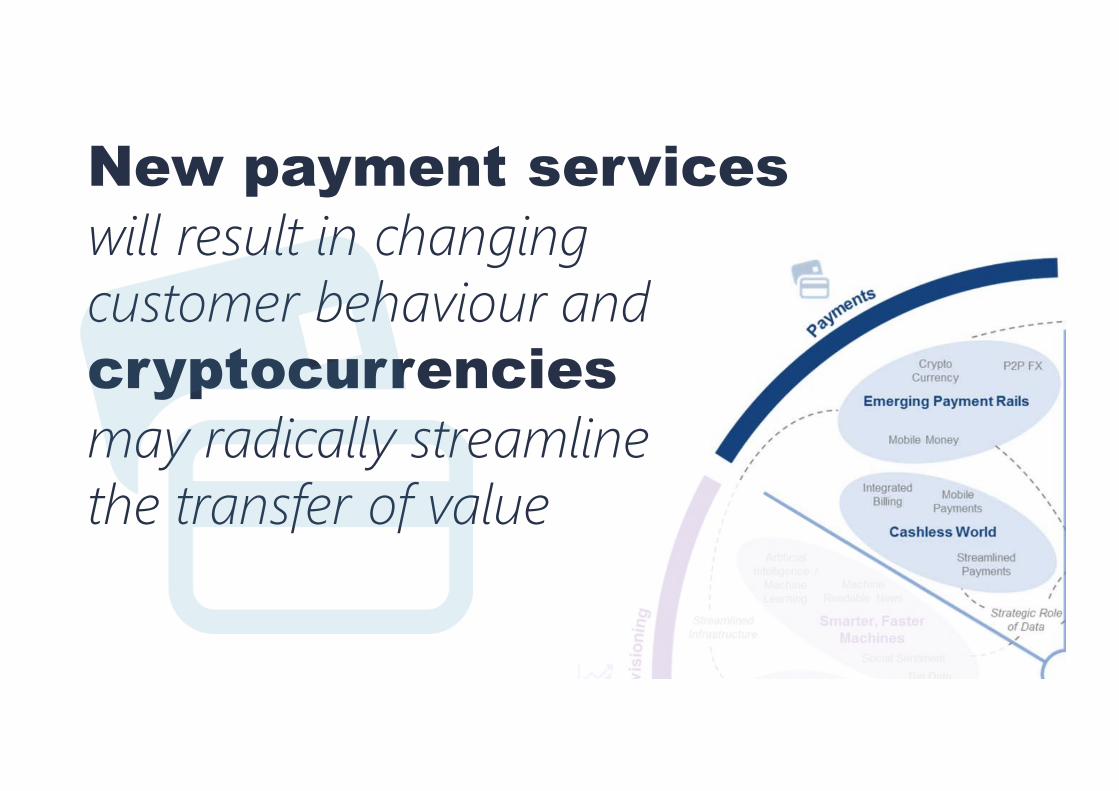

New payment services will result in changingcustomer behaviour andcryptocurrenciesmay radically streamlinethe transfer of value

23

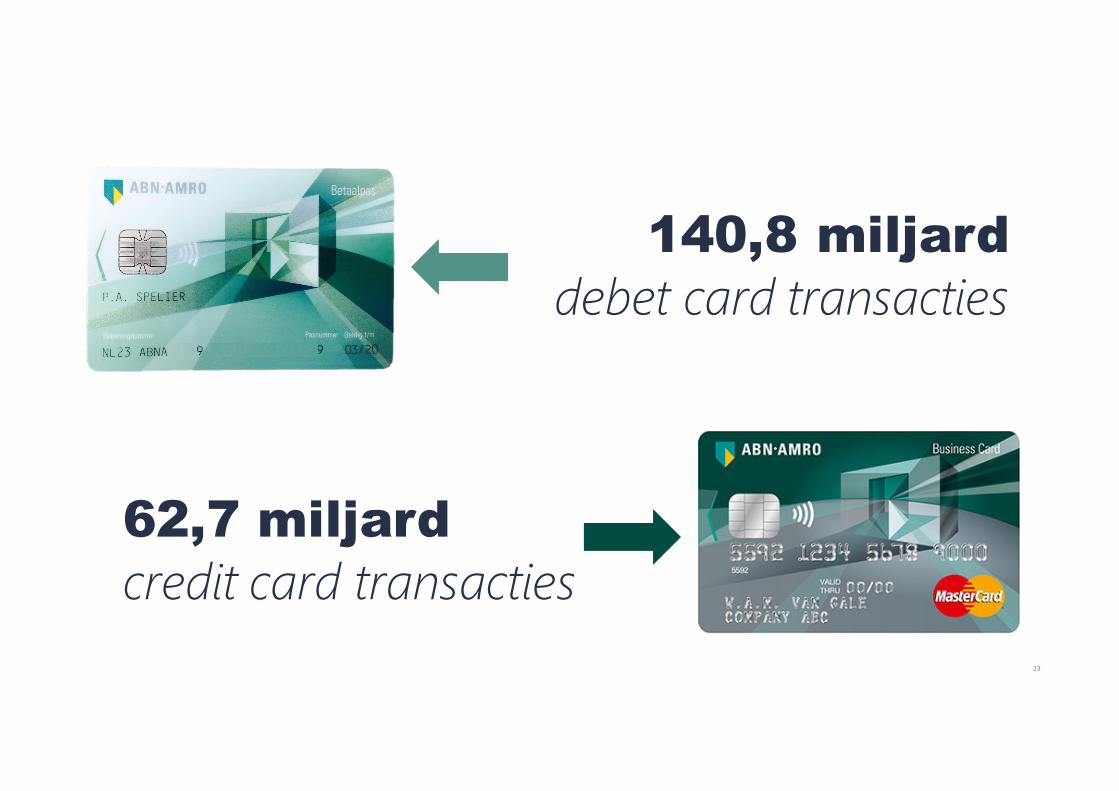

140,8 miljard debet card transacties

62,7 miljard credit card transacties

24

25

26

27

Pay Pay

28

Wat doet ABN AMRO als Apple Pay naar Nederland komt?

29

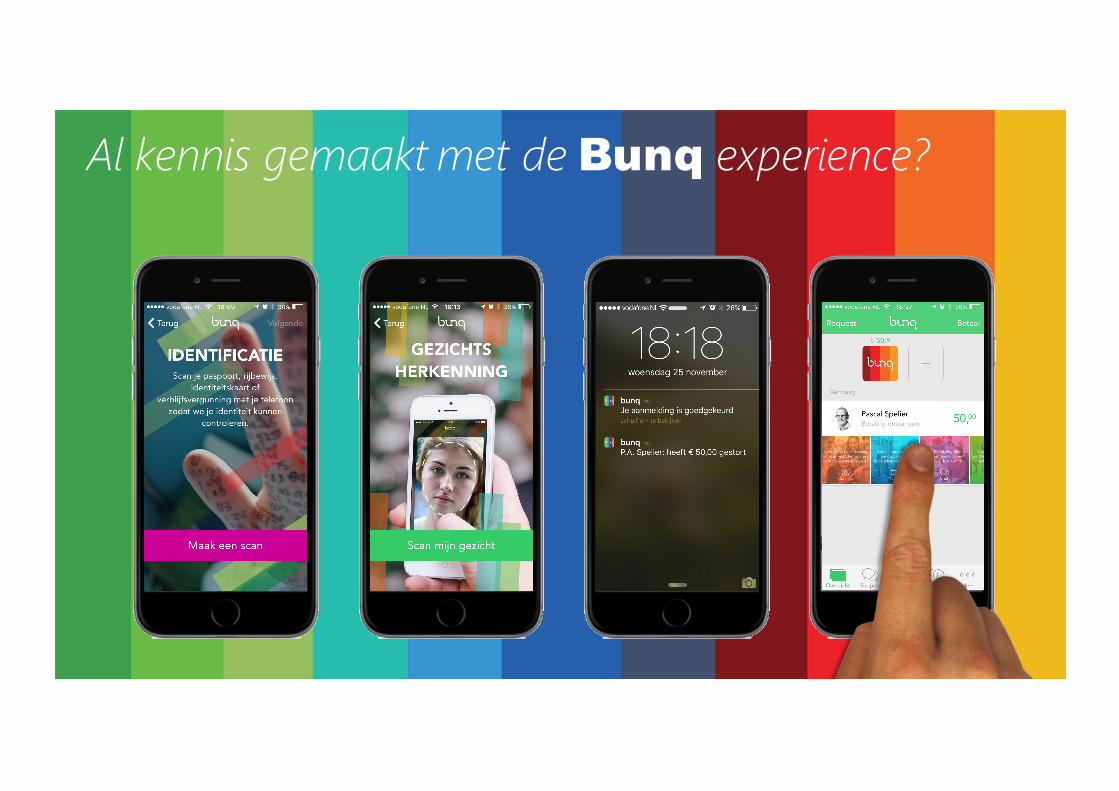

Al kennis gemaakt met de Bunq experience?

30

Disruption in banking will be most imminent;

but the greatest impact of disruption is likely

to be felt in theinsurance sector

31

Delenis het nieuwe bezit

32Credits:YvonneKroese

Meten is wetenQuantified Self

33

Internet of thingsVan zelf naar vanzelf

34

35

36

37

38

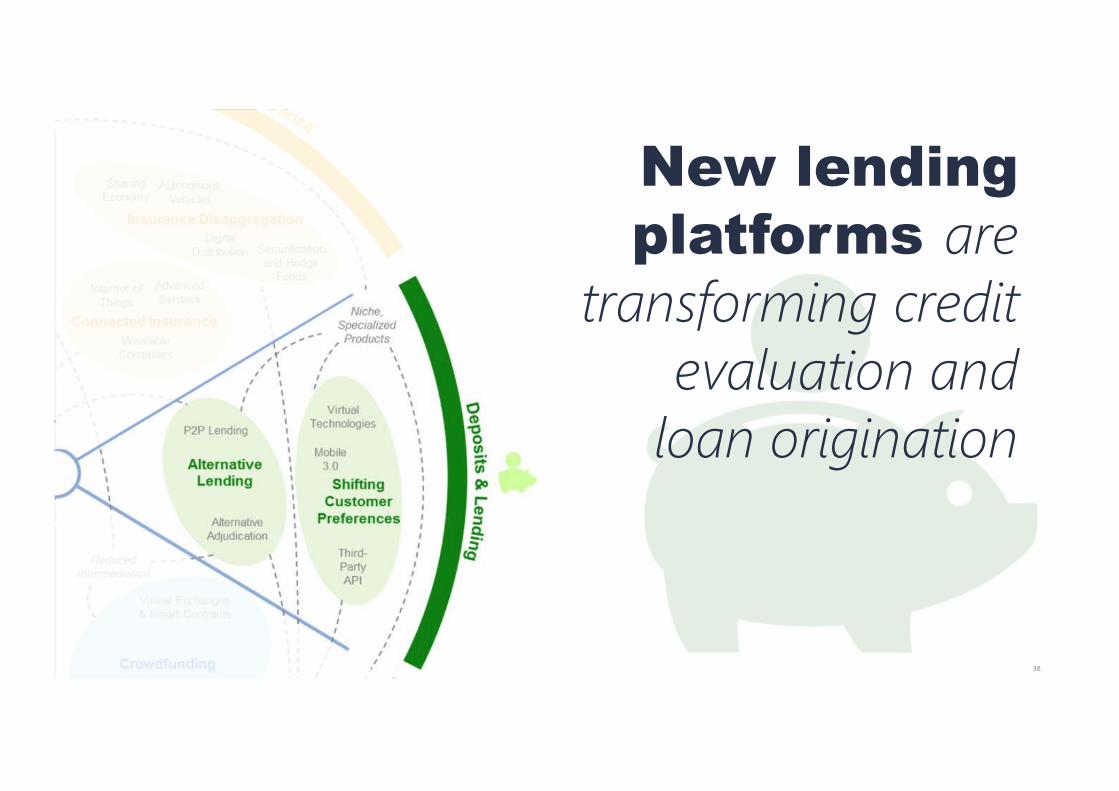

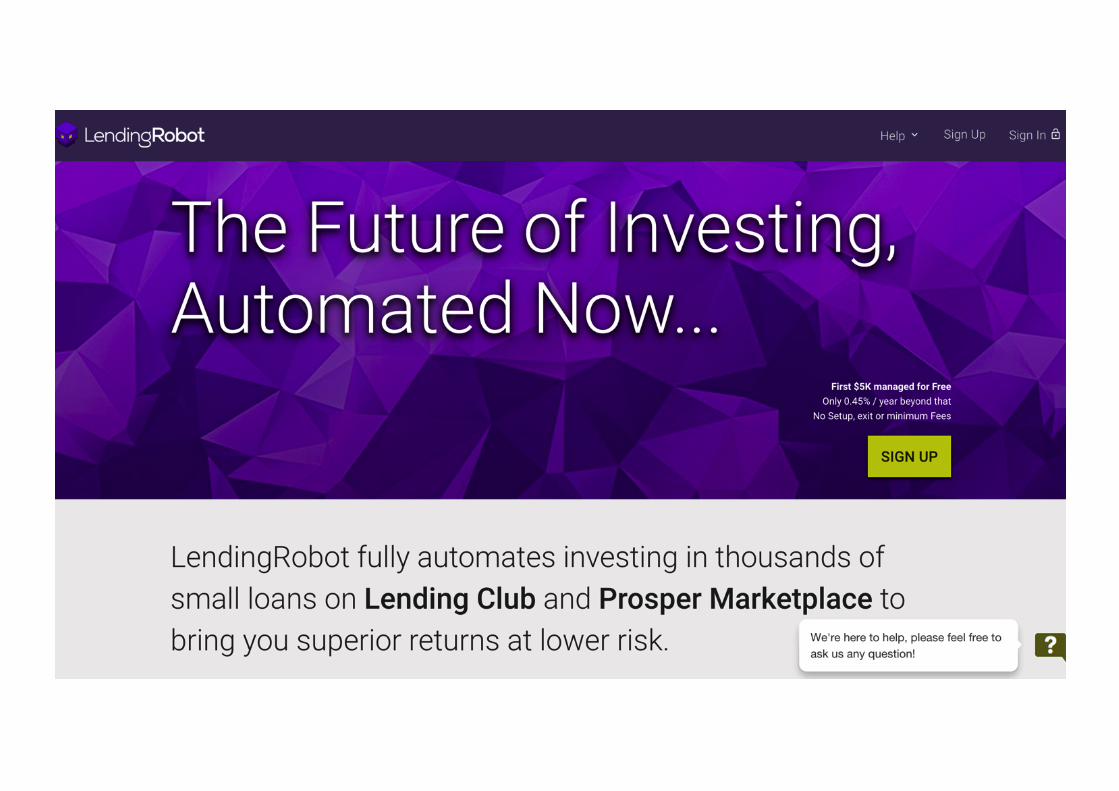

New lending platforms are

transforming credit evaluation and

loan origination

39

Mensen organiseren zich buiten de instituten om: desintermediatie

40

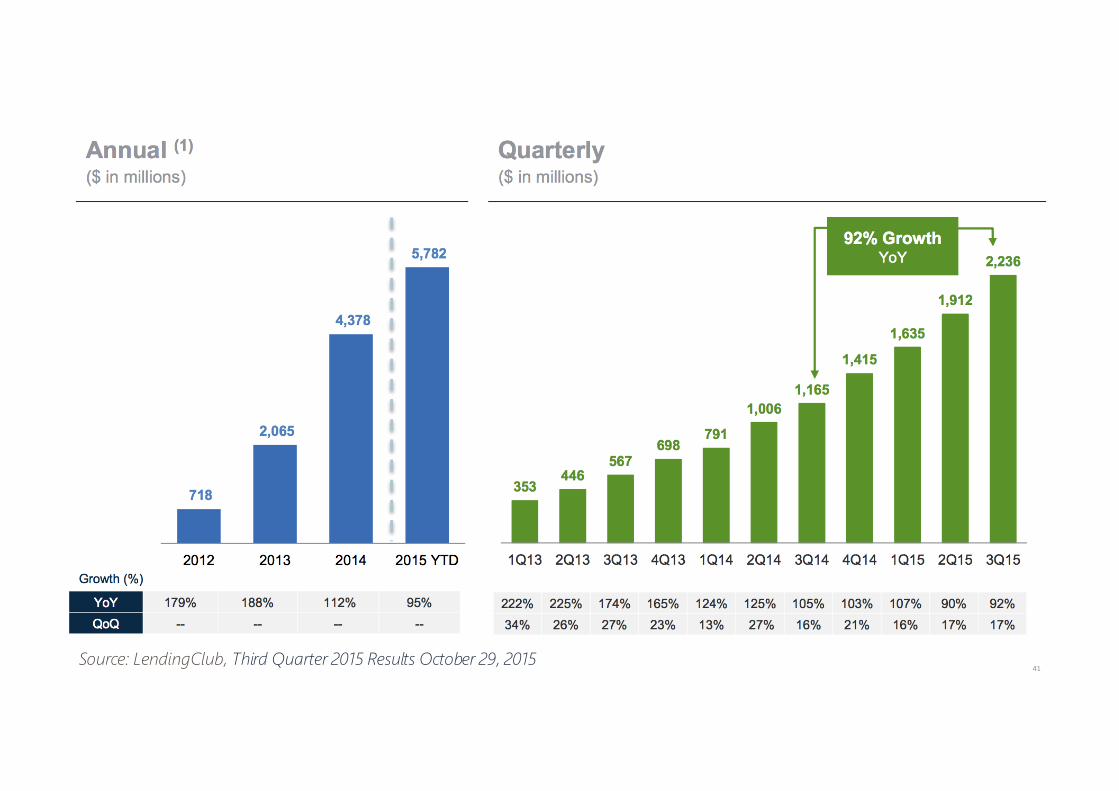

41Source: LendingClub, Third Quarter 2015 Results October 29, 2015

42

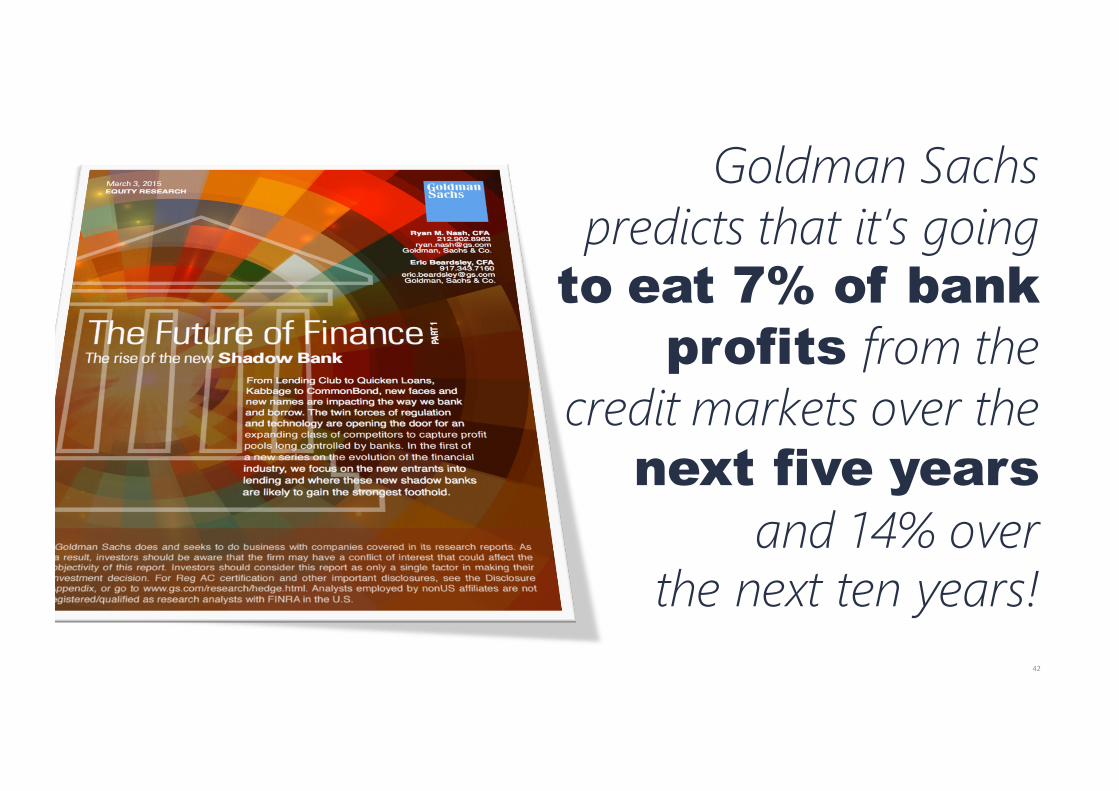

Goldman Sachs predicts that it’s going

to eat 7% of bank profits from the

credit markets over the next five years

and 14% over the next ten years!

43

“Mortgages andsubordinated loans are pre-eminently suitable

instruments for investorsthat want to optimize

their bond portfolio”Eric van der Maarel,

Head of Aegon Asset Management Europe

44

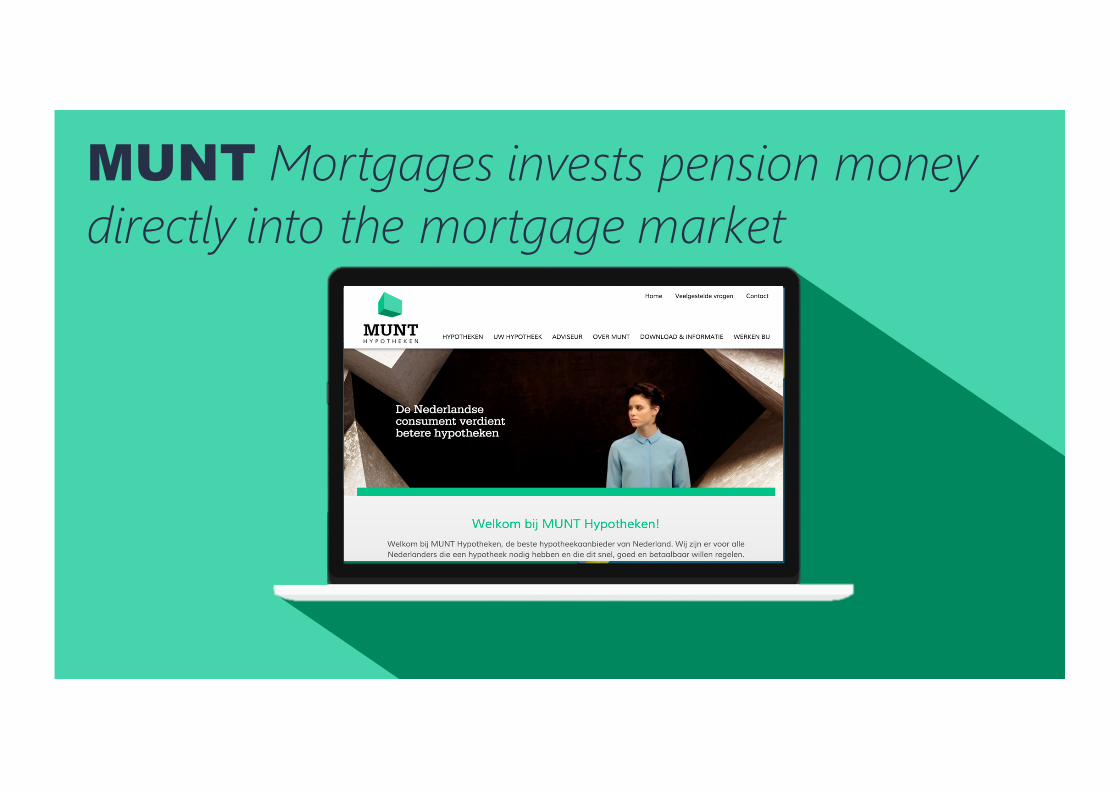

MUNT Mortgages invests pension money directly into the mortgage market

45

FinTech startup Jungo brings crowdlendingto the Dutch mortgage market

46

Interest%

Mortgagesaccording to*:

80%institutional investors

interest %Se

nior

mor

tgag

eco

llate

ral Junior m

ortgagecollateral

20% crowdlenders

* example, interest levels are indicative

Jungo combines institutional funding withcrowdlending

47

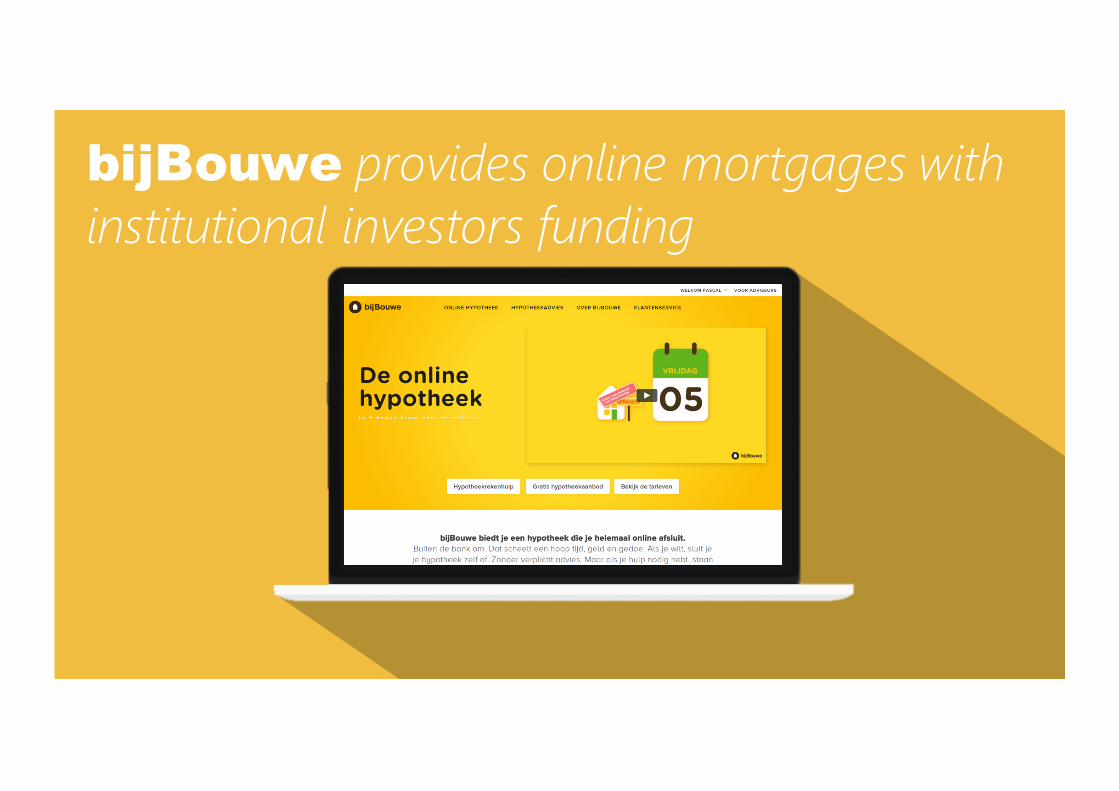

bijBouwe provides online mortgages withinstitutional investors funding

48

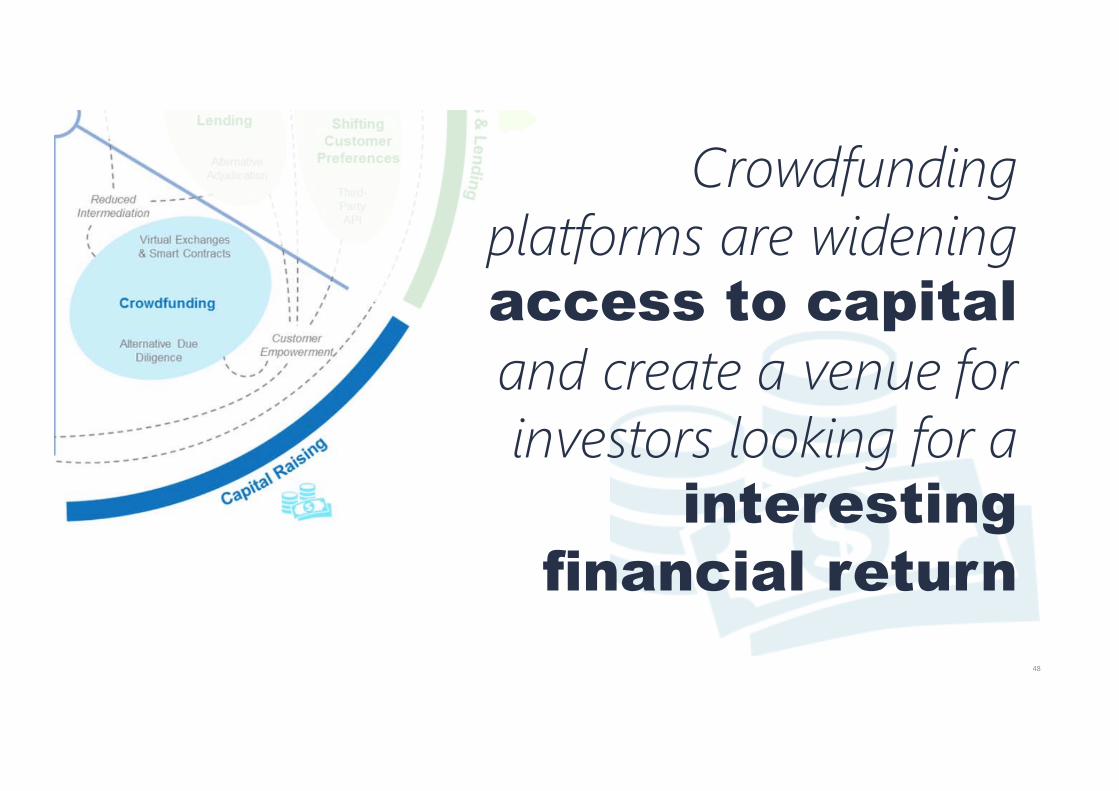

Crowdfundingplatforms are widening access to capital and create a venue for investors looking for a

interesting financial return

49

Robo-advisors are improving accessibilityto sophisticatedfinancial management and creating marginpressure, forcing traditional advisors to evolve

50

Eersteonlinebeleggings-coach van Nederland

51

52

53

54

55

56

57

58

59

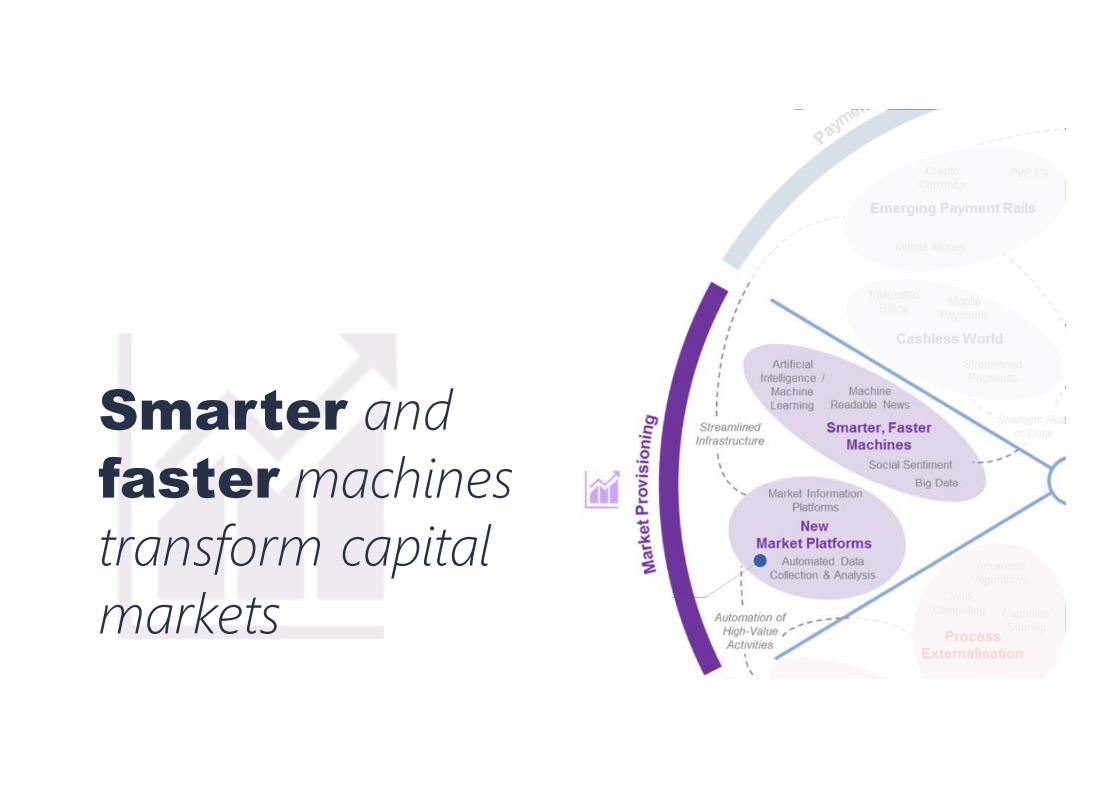

Smarter andfaster machinestransform capitalmarkets

60

61

62

63

Customer Distribution / Front Office

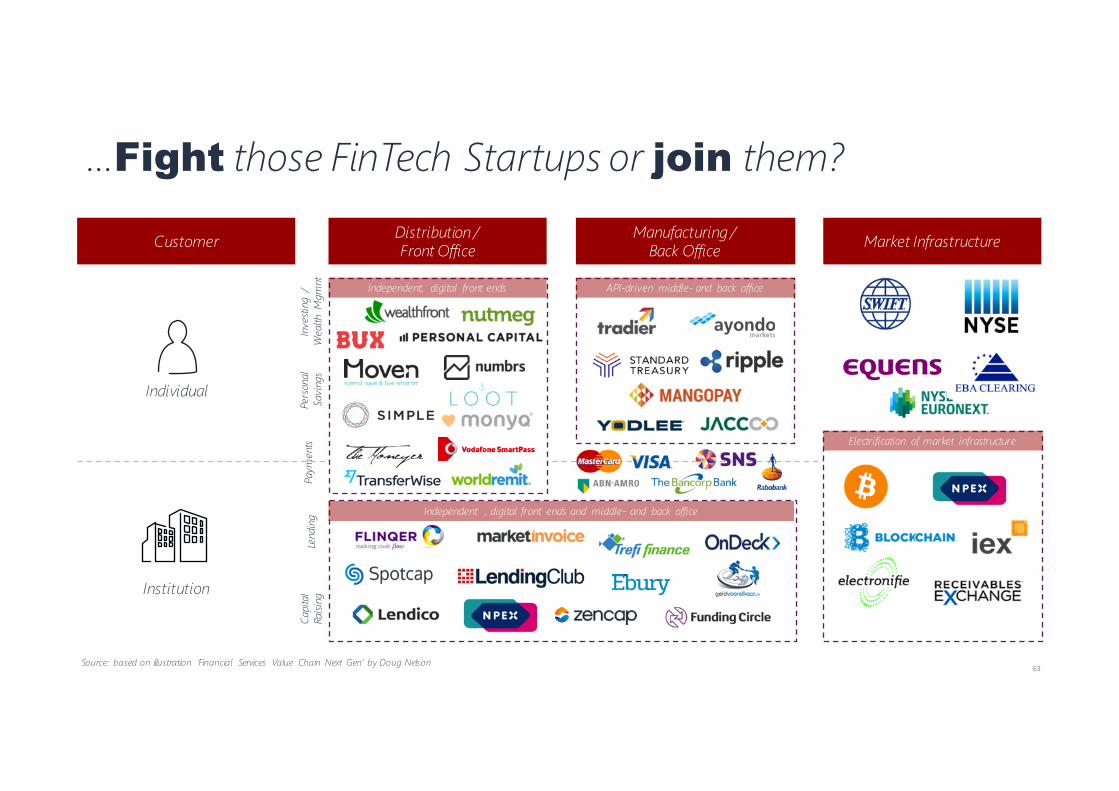

Manufacturing / Back Office Market Infrastructure

Individual

Institution

Inve

sting

/W

ealth

Mgm

ntPe

rson

al

Savi

ngs

Lend

ing

Capi

tal

Raisi

ng

Source: based on illustration ‘Financial Services Value Chain Next Gen’ by Doug Nelson

Paym

ents

…Fight those FinTech Startups or join them?

Independent, digital front ends API-driven middle- and back office

Electrification of market infrastructure

Independent , digital front ends and middle- and back office

64

“BBVA wants to promote an open and collaborativeculture between the bank and the community of developers to enablethem to participate in our creative and innovation process” Marco Bressan, Open Platform manager at BBVA

“Fintech start-ups are often agile, lean and nimble. There are obvious advantages for RBS to partner with some of these

firms. That’s where the APIs come in.”

James Lynn, head of e-channels, GTS at RBS

“We wanted to provide the developer community a platform that will allow them to invent tomorrow's banking applications, which are both innovative and practical everyday for ourcustomers."Pierre Janin , CEO of AXA Bank

Banks need to open up!

65

66

67

Banken moeten de ‘agility’ van startups

adopteren

68

Bron:

69

Bron:

70

Bron:

71

Bron:

72

Wat echt een enorme verbetering is, is de

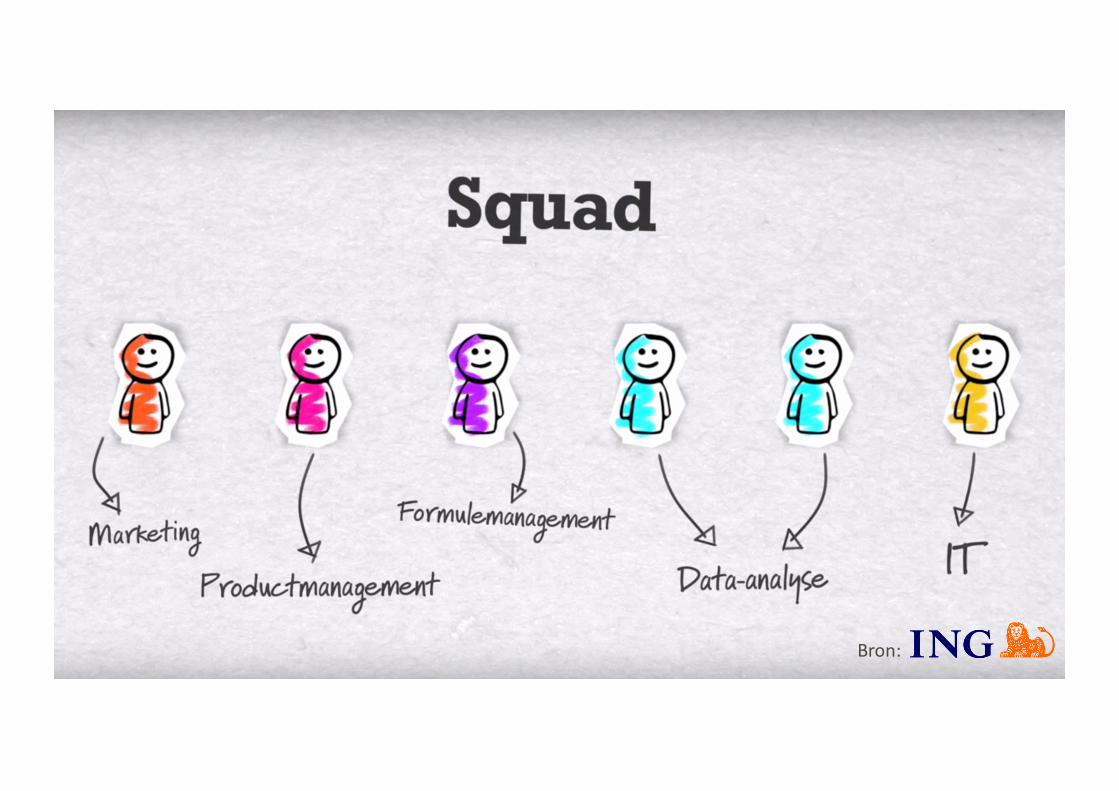

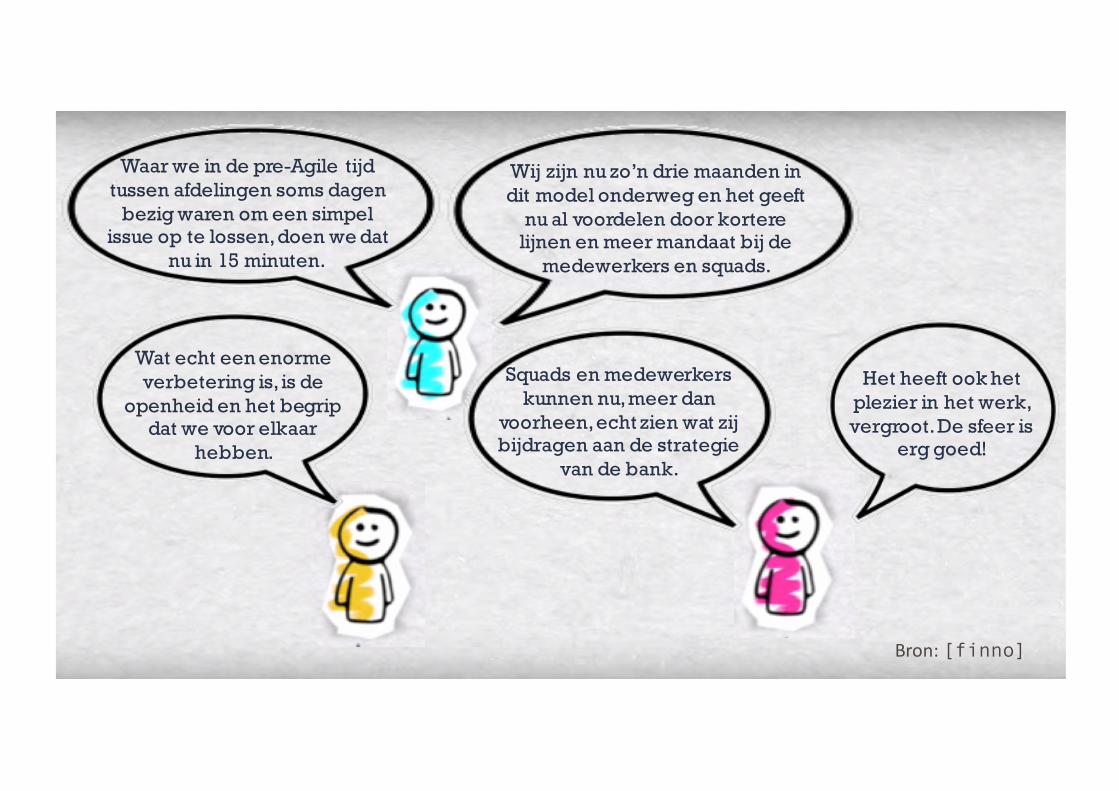

openheid en het begrip dat we voor elkaar

hebben.

Squads en medewerkers kunnen nu, meer dan

voorheen, echt zien wat zij bijdragen aan de strategie

van de bank.

Wij zijn nu zo’n drie maanden in dit model onderweg en het geeft

nu al voordelen door kortere lijnen en meer mandaat bij de

medewerkers en squads.

Het heeft ook het plezier in het werk, vergroot. De sfeer is

erg goed!

Bron:[finno]

Waar we in de pre-Agile tijd tussen afdelingen soms dagen

bezig waren om een simpel issue op te lossen, doen we dat

nu in 15 minuten.

73

74

PascalSpelierChiefInspiration OfficerBanking&Insurance

Reykjavikplein 1,Utrecht,TheNetherlands

Mobile:+31(0)[email protected]

Thank you!@spelier

www.slideshare.net/pascal.spelier

www.linkedin.com/in/pascalspelier