2010 dodd-frank wp - ibat · dodd‐frank wall street reform act ... their motives, objectives and...

TRANSCRIPT

AN EXECUTIVE SUMMARY FOR COMMUNITY BANKERS VOLUME 20 SEPTEMBER 2010

Implementing the Dodd‐Frank Wall Street Reform and Consumer Protection Act

Independent Bankers Association of Texas 1700 Rio Grande Street, Suite 100

Austin, Texas 78701 www.ibat.org

©Independent Bankers Association of Texas Austin, Texas, 2010. All Rights Reserved.

WHITE PAPER

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting or other professional advice or service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought—from a Declaration of Principles Adopted by the

American Bar Association and a committee of Publishers and Associations.

©Independent Bankers Association of Texas Austin, Texas, 2010. All Rights Reserved.

i

Table of Contents

Introduction ............................................................................................................................ 1

Interest on Corporate Checking ............................................................................................... 2

Dodd‐Frank Wall Street Reform Act Title VII: Wall Street Transparency and Accountability .... 4

Definition of a Swap .................................................................................................................... 5

Definition of a Swap Dealer or Major Swap Participant ............................................................. 6

Central Clearing of Swap Transactions ....................................................................................... 7

Swap Reporting ........................................................................................................................... 8

Capital and Margin Requirements .............................................................................................. 8

Implications for Community Banks ............................................................................................. 8

Executive Compensation Provisions ........................................................................................ 9

Mandatory Recovery (“Clawback”) of Unearned Compensation (Sec. 954 of Dodd‐Frank) ...... 9

Incentive Compensation Arrangements At Large Financial Institutions (Sec. 956 of Dodd‐Frank) ........................................................................................................................................ 10

Non‐binding “Say‐On‐Pay” (Section 951 of Dodd‐Frank) ......................................................... 10

Compensation Committee Independence (Section 952 of Dodd‐Frank) ................................. 11

Additional Executive Compensation Disclosure (Section 953 of Dodd‐Frank) ......................... 11

Deposit Insurance Fund and Deposit Insurance Changes ....................................................... 13

Bill Language/Requirements ..................................................................................................... 13

Implementation Date/Effective Date ....................................................................................... 13

Strategic Implications/Ponderables For Bank Management .................................................... 13

Miscellaneous Provisions....................................................................................................... 16

Effective Date ............................................................................................................................ 16

De Novo Branching ................................................................................................................... 16

Insider Transactions .................................................................................................................. 16

Bureau of Consumer Financial Protection – Title X ................................................................ 17

Residential Mortgage Changes .............................................................................................. 20

Title XIV – Mortgage Reform and Anti‐Predatory Lending Act................................................. 20

Loan Origination Compensation and Steering Provisions (Section 1403) ................................ 21

Reasonable Ability to Repay (Subtitle B, Section 1411 et seq) ................................................. 22

Prepayment Penalties (Section 1414) ....................................................................................... 22

Lowered HOEPA Threshold (Section 1431) .............................................................................. 23

ii

Mandatory Arbitration (Section 1414) .................................................................................... 23

Enhanced Disclosures ............................................................................................................... 23

Counseling Programs (Subtitle D – Office of Housing Counseling, Section 1441 et seq) ........ 24

Servicing (Subtitle E – Mortgage Servicing, Sections 1461 et seq) .......................................... 24

HMDA Data Expansion (Section 1094) ..................................................................................... 25

Consumer Reports (Section 1100F) ......................................................................................... 26

Impact of the “Volcker Rule” on Community Bank Investment Activities .............................. 26

Impact on Bank Holding Companies ...................................................................................... 27

The Fate of the Federal Savings Bank Charter and Thrift Holding Companies ......................... 27

Financial Holding Companies .................................................................................................... 28

Capital ....................................................................................................................................... 28

Source‐of‐Strength .................................................................................................................... 28

Transactions with Affiliates ....................................................................................................... 29

SARBOX ..................................................................................................................................... 29

Regulation D .............................................................................................................................. 30

The Durbin Amendment ........................................................................................................ 30

Overview ................................................................................................................................... 30

Discussion.................................................................................................................................. 31

Path to Implementation ............................................................................................................ 32

Things You Should Be Doing Now ............................................................................................. 32

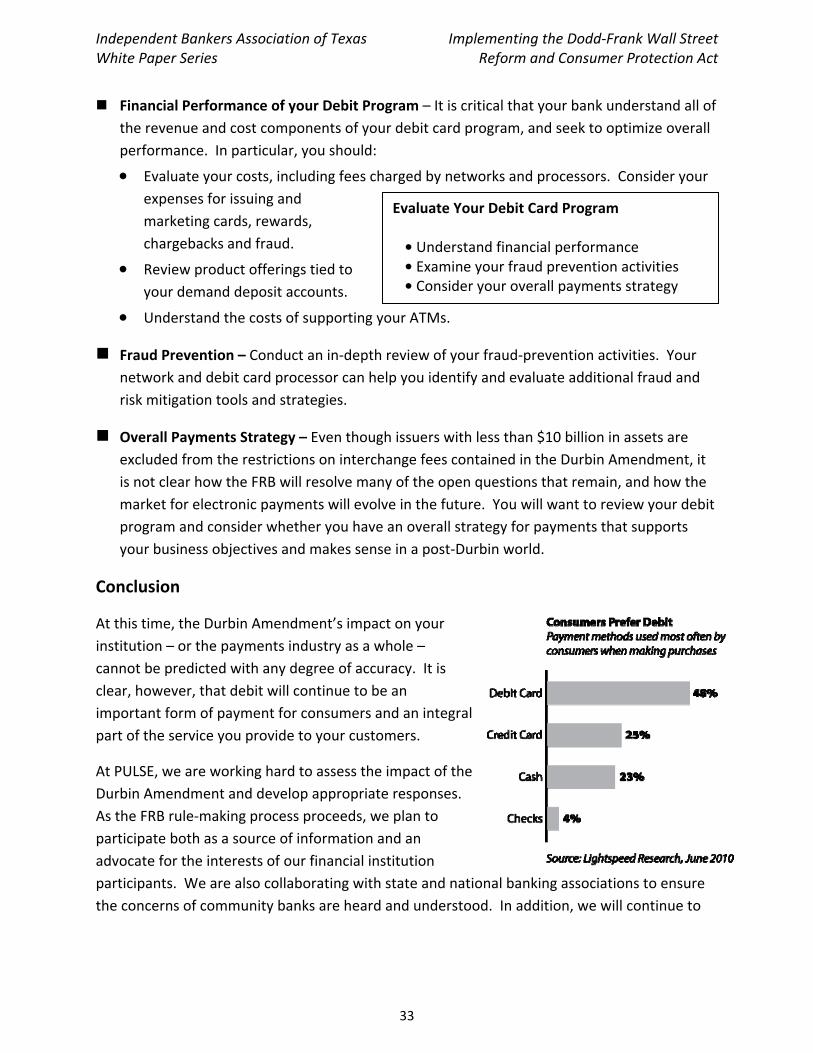

Conclusion ................................................................................................................................. 33

A Few Other Things to Consider............................................................................................. 34

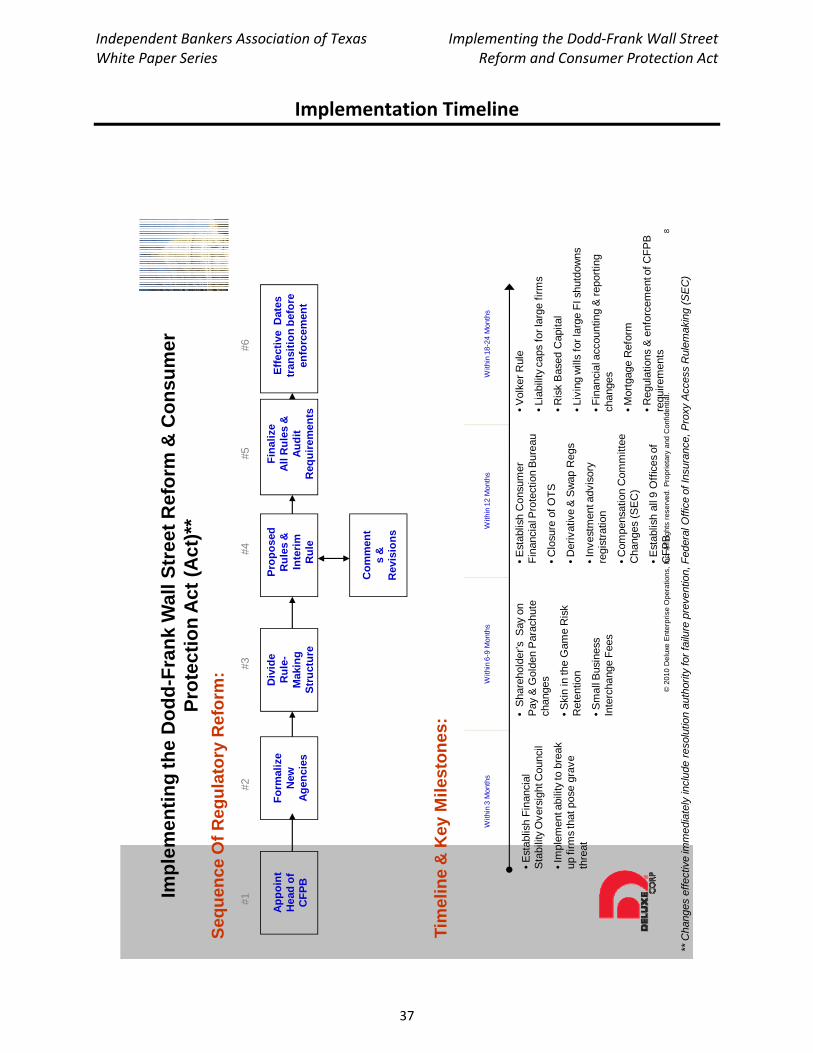

Implementation Timeline ...................................................................................................... 37

About the Authors ................................................................................................................. 38

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

1

Introduction

On July 21, 2010 President Barack Obama signed the 2,319 page Dodd‐Frank Wall Street Reform and Consumer Protection Act, a.k.a. the financial reform bill (the “Dodd‐Frank Act” or the “Act”). The signing ceremony followed nearly eighteen months of hearings, testimony and lobbying on what has been described as the most comprehensive reform of our Nation’s financial system since the Great Depression. It will be many months and perhaps even years before the Act’s provisions will be fully implemented and its effects fully realized.

But for Texas community bank management, careful and precise planning should begin now. Bank interest and non‐interest expense and income will be altered immediately and factored into budget projections for 2011 and beyond.

The Independent Bankers Association of Texas (“IBAT”) commissioned this White Paper almost immediately following the bill’s signing. We endeavored and found some of the brightest minds working in community bank consulting, legal and academia to assist us in preparing and presenting many of the strategic implications of the Act from a community bank perspective. This paper is not intended to inform bankers with another resource summarizing the Act, but rather provide IBAT members with a working tool for implementing the Act’s provisions tomorrow and beyond.

We wish to acknowledge the contributions of the following individuals who authored one or more of the sections, or provided editorial and layout expertise:

Sanford “Sandy” Brown, Bracewell & Giuliani Ken Derks, Clark Consulting Keith Hughey, Consultant Bonnie Kankel, IBAT Ed Krei, The Baker Group Scott MacDonald, SWGSB Cliff McCauley, Frost Bank Milton McGee, Citizens National Bank, Henderson Karen M. Neeley, Cox Smith Shannon Phillips, IBAT Dave Schneider, PULSE Steve Scurlock, IBAT Peter Weinstock, Hunton & Williams Chris Williston, IBAT

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

2

Special thanks to Deluxe for providing the Implementation Timeline

As future rules are promulgated and studies completed that are mandated in the Act, it is our intent to provide you with meaningful supplements to this document.

Interest on Corporate Checking

By Cliff McCauley and Keith Hughey

Sec. 11001. INTEREST‐BEARING TRANSACTION ACCOUNTS AUTHORIZED

(a) Repeal of Prohibition on Payment of Interest on Demand Deposits‐

(1) FEDERAL RESERVE ACT ‐ Section 19(I) of the Federal Reserve Act (12 U.S.C. 371a) is amended to read as follows:

‘(I) [Repealed]’.

(b) Effective Date ‐ The amendments made by subsection (a) shall take effect at the end of the 1‐year period beginning on the date of the enactment of this Act.

That, ladies and gentlemen, is it. In less than seventy‐five words, one word actually – “Repealed,” the decades old prohibition on the payment of interest on commercial checking accounts and the final vestige of Reg Q has been sent packing. In short order, you and your competitors will be able (or obliged, depending upon your point of view) to begin paying interest on a large percentage of heretofore “free” funds.

Among the many questions you must ask as you face this inevitability are:

What will it do to your operating costs (net interest margin) when you begin paying interest on commercial checking accounts?

What’s the likely impact on your reserve requirement (non‐investable funds level) if monies that have been held in non‐transaction account forms (such as MMA and savings) are repatriated into commercial checking account balances with the resulting ten percent reserve requirement?

How much, if any, of that impact may depend upon your past efforts to lower your reserve requirements by reclassifying these funds. What about pricing of your commercial product suite going forward? At what point are you better off with some of the commercial

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

3

deposits remaining in a no‐reserve requirement form, i.e, what sort of rate differential works and when does the differential lose some of its benefit?

What are the implications for your commercial account analysis system? If you’ve been giving an above market earnings credit rate in this low rate environment, what happens when you move from a notional, implied premium rate to an explicit market rate of interest?

What about the fees and per item charges? Do you need to revise your entire commercial service charge fee schedule?

Will you elect to pay interest on the entire balance and collect 100% of the fees? Will you credit your commercial customers’ accounts with interest only in excess of the amount of the fees? Are you capturing all of the services you provide to your commercial accounts? Should you make the effort?

What about small business accounts not on your commercial account analysis system? Will you need to revise those fees and perhaps do a better job of capturing activity levels for those accounts when you begin paying interest on those balances?

What might the implications be for the entire customer relationship? For instance, does the deposit relationship affect loan rates or the fees charged or waived on tied accounts?

What sort of competitive strategy will you adopt? That is, will you pursue commercial account relationships with an aggressive pricing posture? Will you be defensive and only look to remain generally competitive with the market?

Consider the following: At current levels, if you pay 0.05% on commercial account balances while a competitor promotes a rate of 0.30%, how will that competing rate look to your customers? On the surface it is 6x the 0.05% you are paying. Might that differential tempt some of your commercial account holders to move? What about when rate levels reach the 3.00% range? If you are paying 3.05% and the competition 3.30%, it is the same 25 basis points; yet it is only an 8.2% premium. Will that produce a similar movement? Probably not.

If you are aggressive in your pricing and successful such that you grow deposits, where will you invest them?

Might one or more of your competitors adopt an aggressive rate strategy with a goal of reducing their dependence on “volatile liabilities” and “borrowed funds?” In other words, their motives, objectives and expected benefits may differ from yours. Should you follow them anyway?

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

4

How might this change affect your franchise value? What about the “core deposit intangible?” What, if any, implications might there be for changes (reductions) in the valuations provided by third parties for thinly traded stock?

What are the ALCO implications? Suddenly, a lot more liability dollars may be deemed rate sensitive, causing some banks that were thought to be asset sensitive to look very different in 2011 in a rising rate environment.

If so, what might that suggest for macro and micro loan pricing and investment strategies a year from now?

Speaking of models, we strongly recommend every bank begin modeling a range of rate and even pricing strategies to determine what might work best in terms of future earnings streams.

What are you going to do to educate your employees about these changes?

What are you going to do to educate your commercial customers about these changes?

This certainly isn’t a finite list of questions that you need to be thinking about going forward. Nonetheless, we hope it will get your thoughts flowing in the right direction as well as permit you to be proactive in your approach to these changes rather than reacting to your competition and the market.

Dodd‐Frank Wall Street Reform Act Title VII: Wall Street Transparency and Accountability

By Scott MacDonald

This portion of the bill significantly modifies how the derivative markets are regulated, the definition of derivatives or swaps, establishes additional requirements for swap dealers or major swap participants, imposes new clearing and reporting requirements for swaps, as well as new margin and capital requirements. A recent report by Hunton & Williams suggests that all firms (banks) should determine:1

1. Whether any of the derivatives they enter into are swaps 2. If they are a swap dealer or major swap participant

1 OTC Derivatives Reform: Wall Street Transparency and Accountability Act of 2010, Hunton & Williams, Derivatives and Trading Update, July 2010, http://www.hunton.com/files/tbl_s10News/FileUpload44/17199/otc_derivatives_reform.pdf.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

5

3. If their swaps must be centrally cleared or traded on an exchange 4. What swaps they must report; and 5. Whether or not they, or their counterparty, must provide margin or meet capital

requirements.

The following sections of this report summarize these five areas.

Definition of a Swap

Plain English: Basically the new definition of a swap is just about any derivative contract except: futures; forward contracts with physical delivery; and foreign currency derivatives if the Treasury so determines. There is now a difference between “swaps” and “security‐based swaps” with the most critical difference being swaps are regulated by the Commodity Futures Trading Corporation (CFTC) and security‐based swaps regulated by the SEC. Broad index derivatives are swaps where narrow index (single company or security) are security‐based swaps. Throughout this document, we will generally refer to both “swaps” and “security‐based swaps” as swaps unless there is a need to differentiate the two.

More Detail: A swap is any agreement, contract, or transaction from the following:

1. A long list of financial contracts and agreements generally considered “swaps” such as: interest rate, currency, basis, cross‐currency, foreign exchange, total return, equity index, equity, debt, debt index, credit and credit default, weather, energy, metal, agricultural, emissions and commodity swaps.

2. The legislation broadens the general definition of a swap to include: credit spreads, calls, puts, caps, floors, collars or similar options for the purchase or sale or based on value of interest rates, currencies, commodities, securities, debt instruments, indices or quantitative measures or other financial or economic interest or property.

3. “That provides for any purchase, sale, payment, or delivery (other than a dividend on an equity security) that is dependent on the occurrence, nonoccurrence or the extent of the occurrence of an event or contingency associated with the potential financial economic or commercial consequence.”2

NOTE: This definition could be broadly interpreted to include all variable rate bank loans and insurance policies. WHY? Since a variable rate loan will change rate with an economic event (changes in interest rates) and an insurance policy pays off as a result of a commercial consequence. MOSTLY LIKELY: the definition of a swap will not be that broad.

2 “The Dodd‐Frank Wall Street Reform and Consumer Protection Act,” http://frwebgate.access.gpo.gov/cgi‐bin/getdoc.cgi?dbname=111_cong_bills&docid=f:h4173enr.txt.pdf

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

6

4. A catch‐all, which includes any contract or transaction which are commonly known as swaps; as well as any security‐based swaps defined in the Gramm‐Leach‐Bliley Act; and any combination of an option or agreement described above.

5. EXCLUSIONS: Commodity futures contracts, commodity option contracts or the sale of nonfinancial commodity or security for future delivery; i.e., forward contracts. In addition, the act excludes any put, call, or straddle option currently subject to the Securities Act of 1933 or Securities Exchange Act of 1934, unless the agreement or contract is a credit default swap. Also excluded from the definition of a swap are agreements with the Federal Government, the Federal Reserve, or a federal agency (backed by the full faith and credit of the Federal Government), as well as securities such as notes and bonds. Finally, the bill also excludes a “security‐based swap” which are those swaps regulated by the SEC.

6. The exclusions and the term “security‐based swap” ultimately separate swaps by the primary regulator of the swap. Security‐based swaps are swap transactions regulated by the SEC and include trades that most of us would consider swaps but: use a narrowly defined security index; or a single security or loan; or a CDS related to a single company or entity. The Commodity Futures Trading Commission (CFTC) would have jurisdiction over broad index (10 or more securities) based swaps and CDS based on a broad index while the SEC has jurisdiction over swaps using a narrowly defined index or single entities; i.e., security‐based swaps. CONCERN: These definitions will be confusing and most likely overlap—hence most “swaps” will be regulated by both the SEC and the CFTC.

Definition of a Swap Dealer or Major Swap Participant

Plain English: A “swap dealer” is someone who presents themselves or is commonly known as a swap dealer; makes a market in swaps; or enters the swap market as part of their normal business. A “major swap participant” is someone who maintains a substantial position in swaps. Banks are excluded from the definition to the extent they enter into a swap with a customer for the purpose of a loan or use swaps to mitigate commercial risk. Generally, as a community bank, you don’t want to be a swap dealer or a major swap participant or you will be subject to significant requirements under this portion of the Act.

More Detail: a swap dealer is defined as anyone who presents itself as a swap dealer; makes a market in swaps; regularly enters into swaps as an ordinary course of business for its own account; or engages in activities such that they are commonly known as a dealer in swaps. Swap dealers must register with the CFTC while security‐based swap dealers must register with the SEC.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

7

NOTE: “…in no event shall an insured depository institution be considered a swap dealer to the extent they offer or enter into a swap with a customer for the purpose of a loan with that customer.”3

NOTE: FDIC insured institutions are effectively prohibited from acting as a swap entity. They must divest themselves, or push out the swaps entity into a separately capitalized entity.

Major swap participant is defined as an entity that maintains a substantial position in swaps; or an entity whose swaps create substantial counterparty risk that could be a risk to the financial system; or an entity that is highly leveraged, not subject to U.S. capital requirements and holds a substantial position in swaps. Swaps held for mitigation of commercial risk are not included in the determination of a substantial position.

NOTE: The CFTC and SEC must define “commercial risk” and “substantial position.”

Central Clearing of Swap Transactions

Plain English: Most “standardized swaps or derivatives” will eventually be required to be traded on an exchange. “Specialized swaps” will not be subject to this requirement. Unfortunately, this creates a significant issue in how the exchanges or participants will “standardize” the swaps. If the terms of a swap are altered to meet the needs of a user, the question becomes how similar or dissimilar must the contract be to be required to be cleared or not cleared? Occasional users of swaps or parties who use swaps as part of their risk management practices should obtain clarity from the swap dealer as to the clearing requirement of any swaps they participate in. It does not appear, however, that this requirement will apply to existing swaps already on the books.

More Detail: The act makes it “…unlawful for any person to engage in a swap unless that person submits such swap for clearing to a derivatives clearing organization that is registered under this Act…” The Act requires centralized clearing for all swaps the CFTC or the SEC determines should be cleared through a registered clearinghouse. The agency must allow for a 30 day comment period from submission of each swap and make its determination within 90 days.

NOTE: No swaps have been determined to require central clearing as of the time of the writing. The agencies have up to one year after the enactment of the Act to establish and adopt rules for reviewing a derivatives clearing organization’s clearing of a swap or the types and groups of swaps it has accepted for clearing.

3 “The Dodd‐Frank Wall Street Reform and Consumer Protection Act,” http://frwebgate.access.gpo.gov/cgi‐bin/getdoc.cgi?dbname=111_cong_bills&docid=f:h4173enr.txt.pdf

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

8

Exceptions to the Clearing Requirement: The clearing requirement will not apply if one of the parties to the transaction: is not a financial entity; is using the swap to mitigate commercial risk; notifies either the CFTC or SEC as to how they will meet their financial obligations associated with the un‐cleared swap. This exception is referred to as the “end user.” The term financial entity does include banks; however, the CFTC or SEC “shall consider whether to exempt small banks, savings associations, farm credit system institutions, and credit unions with total assets of $10 billion or less.”

Swap Reporting

All swaps are subject to reporting requirements regardless of whether they are cleared or not. For those swaps subject to mandatory clearing, the Act requires real time public reporting, similar to stock and bond exchanges. This also applies to those not subject to mandatory clearing but are cleared at a registered clearing organization. Those swaps not required to be cleared and not cleared at a registered clearing organization are required to be reported to a swap data repository or the CFTC or SEC as well as real time reporting of the transaction that does not disclose the business transaction and position of any person.

The reporting hierarchy is fairly straightforward when either party is a swap dealer or major swap participant. The swap dealer, then the major swap participant is required to fulfill the reporting requirement. If neither party is a dealer or participant, then the two parties must agree who will report. All parties, therefore, must establish a compliance policy to ensure they are in compliance with reporting requirements.

Capital and Margin Requirements

Capital and margin requirements will be established by the CFTC, SEC and bank regulators. In general, swap dealers and major swap participants will be subject to capital rules that apply to banks. Margin requirements will be imposed by central clearing counterparties for all cleared swaps. Regulators will impose margin requirements for all swaps not cleared. Bank regulators will establish initial and variation margin requirements, in consultation with the CFTC and SEC for banks.

Implications for Community Banks

As a community bank, you are likely not to be a swap dealer or major swap participant. If you determine that you might be, this brief document is not sufficient to explain the magnitude of requirements this section of the Act requires of you. We recommend you discuss this with counsel.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

9

If you are not a swap dealer or major swap participant, then you should make sure you are aware of the clearing requirements of any swap you are a party to. This will likely be the requirement of the exchange you purchase the swap through or by the swap dealer or major swap participant you transact with. All swap contracts are subject to reporting requirements. You must establish a compliance procedure to ensure the swap is being reported. Typically, the community bank will not be the party required to report, but if two “not” swap dealers or “not” major swap participants are transacting, the bank would be required to report the transaction. Capital and margin requirements will be imposed on all swap contracts.

Community banks can continue to use swaps (derivatives) to hedge commercial risks. It is possible that banks with less than $10 billion in assets will not be subject to the mandatory clearing requirement, but will be subject to reporting, capital and margin requirements.

Executive Compensation Provisions

By Clark Consulting

This legislation adds new rules pertaining to executive compensation for publicly‐traded companies and certain financial institutions. This portion does not directly impact the majority of Texas community banks. However, with the increasing emphasis on restrictions to executive compensation, a quick review could be predictive of future regulatory direction for nonpublic entities. In particular, remember that on June 21, 2010, the Federal Reserve, the Office of the Comptroller of the Currency, the Office of Thrift Supervision, and the Federal Deposit Insurance Corporation (collectively, the “Agencies”) issued their interagency Guidance on Sound Incentive Compensation Policies, effective June 25, 2010.

Many of the new rules discussed below will be significantly impacted by subsequent rulemaking by the Securities and Exchange Commission (SEC) and other regulatory bodies.

Mandatory Recovery (“Clawback”) of Unearned Compensation (Sec. 954 of Dodd‐Frank)

Dodd‐Frank adds a new Section 10D to the Securities Exchange Act of 1934 (Exchange Act). This new section directs the SEC to issue rules barring the listing on any national exchange of any equity security of an issuer who has not developed and implemented a policy:

Providing for disclosure of the policy of the issuer on incentive‐based compensation that is based upon financial information required to be reported under the securities laws (including in a public company’s financial statements); and

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

10

In the event the issuer is required to prepare an accounting restatement due to the material noncompliance of the issuer with any financial reporting requirement, providing for the recovery of incentive‐based compensation based on the erroneous data that was paid to a current or former executive officer of the issuer during the three year period immediately prior to the restatement.

Incentive Compensation Arrangements At Large Financial Institutions (Sec. 956 of Dodd‐Frank)

The legislation requires that the “appropriate Federal regulators” (i.e., Federal Reserve, OCC, FDIC, OTS, NCUA, SEC and FHFA), within nine months of enactment, jointly issue regulations or guidelines applicable to each “Covered Financial Institution” (CFI) which:

Require each CFI to disclose to its regulator the structure of all incentive compensation arrangements offered by the CFI (actual compensation need not be disclosed for this purpose); and

Prohibit any types of incentive‐based payment arrangement (or any feature thereof) that encourages inappropriate risk (i) by providing excessive compensation, fees or benefits to an employee, executive officer, director or principal shareholder of the CFI; or (ii) that could lead to a material financial loss to the CFI.

For purposes of this section of Dodd‐Frank, the term “Covered Financial Institution” includes, among others: (i) depository institutions; (ii) depository institution holding companies; (iii) credit unions; and (iv) any other financial institution that the appropriate Federal Regulators jointly determine. Importantly, the requirements of this section of Dodd‐Frank do not apply to financial institutions with assets of less than $1 billion. However, it does apply to all institutions that meet the asset threshold—not just publicly traded ones.

Non‐binding “Say‐On‐Pay” (Section 951 of Dodd‐Frank)

Dodd‐Frank adds a new Section 14A to the Exchange Act that requires disclosure of certain executive compensation matters and provides shareholders of publicly‐traded companies with a non‐binding vote (frequently, described as “say‐on‐pay”) on:

The compensation of the company’s executives, as required to be disclosed pursuant to existing regulations; and

Certain “golden parachute” provisions for named executive officers if the shareholders are also being asked to vote on an acquisition, merger, consolidation, or proposed sale or other disposition of all or substantially all of the assets of the company.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

11

Shareholders must be given a say‐on‐pay vote at least once every three years. In addition, shareholders must be given a vote to determine the frequency of the say‐on‐pay vote at least once every six years. An initial say‐on‐pay and frequency vote must occur at the first shareholder meeting occurring more than six months after Dodd‐Frank’s enactment. Discretion has been left to the SEC to exempt any issuer or class of issuers from the say‐on‐pay provisions.

Compensation Committee Independence (Section 952 of Dodd‐Frank)

New Section 10C of the Exchange Act directs the SEC to issue rules to generally prohibit the listing on any national exchange of any equity security of an issuer unless all members of the compensation committee for such issuer are members of the board of directors and independent.

New Section 10C also provides explicit authorization for compensation committees to hire outside advisors (e.g., compensation consultants and legal counsel). However, these outside advisors may only be retained after the committee has considered certain factors that would affect the independence of such outside advisors. Disclosure of the use of compensation consultants and any conflicts of interest of such consultants is mandatory.

Additional Executive Compensation Disclosure (Section 953 of Dodd‐Frank)

Dodd‐Frank also directs the SEC to issue rules requiring publicly‐traded companies to annually provide a clear description of any compensation required to be disclosed under existing regulations by including information that delineates the relationship between the compensation actually paid and the financial performance of the company. Publicly traded companies would also be required to disclose (i) the median annual total compensation of all employees, exclusive of the CEO; (ii) the annual compensation of the CEO; and (iii) the ratio determined by comparing CEO compensation and the median employee annual compensation.

As a community banker, what should you be doing now?

1. Continue the education process and keep up to date on developments.

• Review the recently issued Guidance on Sound Incentive Compensation Policies (“Interagency Guidance”). The Interagency Guidance substantially adopts the Federal Reserve’s Proposed Guidance on Sound Incentive Compensation Policies, which was published in the Federal Register on October 27, 2009. The Interagency Guidance became effective on June 25, 2010 upon its publication in the Federal Register. A complete copy of the Agencies’ Guidance on Sound Incentive Compensation Policies, as published in the Federal Register, is available at http://edocket.access.gpo.gov/2010/pdf/2010‐15435.pdf. The Act reinforces this Interagency Guidance and is important to review.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

12

• Understand that the regulators may be asking more questions about your compensation plans

2. Assess management and the board’s role in compensation planning and related decisions.

• Review board structure for compensation decisions.

• Consider a formal compensation committee and ongoing education.

• Consider formalizing your compensation philosophy to help in making pay decisions.

• Develop a strategic compensation plan to attract and retain your key people.

3. Evaluate your compensation strategy and plans.

• Evaluate total compensation programs and assess alignment with business strategy and shareholder interests.

• Ensure compensation focuses on driving sustained, long‐term performance that supports your unique business goals and strategies.

• Consider a balanced total compensation strategy to include: base salary, annual incentive plan, long term incentive plan, retirement benefit plan and any formal agreements.

• Quantify the total compensation payout for executives and benchmark to other sources for comparison purposes and to reflect compensation philosophy.

• Ensure performance is measured using a balanced portfolio of performance criteria.

• Evaluate long‐term and short‐term performance based plans and design options.

• Consider developing and implementing a comprehensive compensation recoupment program that addresses both the front‐end (holdbacks) and the back‐end (clawbacks). Non‐qualified deferred compensation plans could be used as a vehicle for recovering incentive compensation.

4. Assess risk in your compensation plans.

• Inventory and evaluate your incentive plans.

• Assess the risk in relation to the bank, department and individual criteria in the plans.

• Explore a process for assessing incentive plan risk and ongoing reviews/compliance.

• Assess roles of the board, compensation committee and management in this risk assessment.

Given the Dodd‐Frank Act and along with the recently released Interagency Guidance, it is more important to assess and formalize your compensation plans which many high performing banks have already implemented. For most community banks, their objective is to attract and retain the best people and while compensation is only a part of fulfilling this objective, developing and

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

13

implementing an overall compensation plan along with a corporate governance structure will help you achieve this objective as well as allow you to adopt any key issues discussed in this section. Perhaps use this time as an opportunity to improve on the work you have already accomplished related to compensation and continue with using the good business judgment rule.

Deposit Insurance Fund and Deposit Insurance Changes

By Shannon Phillips

Bill Language/Requirements

Assessment base (Sec. 331). The FDIC must amend its regulations to define the term “assessment base” as average total consolidated assets minus average tangible equity.

Minimum reserve ratio (Sec. 334). The reserve ratio maximum is eliminated and the minimum is set at not less than 1.35 percent of estimated insured deposits or the comparable percentage of the assessment base. The FDIC must attain 1.35 percent by September 30, 2020.

Increase in deposit insurance amount (Sec. 335). Maximum deposit insurance is increased to $250,000 retroactive to January 1, 2008.

Transaction Account Guarantee Program Extension (Sec. 343). Noninterest bearing transaction accounts are fully insured from December 31, 2010 to December 31, 2012.

Implementation Date/Effective Date

Amend definition of assessment base There is no timeline.

Minimum reserve ratio (1.35%) Must attain 1.35% by September 30, 2020.

Increase deposit insurance amount Retroactive to January 1, 2008.

Transaction Account Guarantee Program December 31, 2010 to December 31, 2012.

Strategic Implications/Ponderables For Bank Management

Increase in deposit insurance amount.

The increase should help level the playing field with the TBTF financial institutions by making it easier for community banks to obtain and retain deposits.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

14

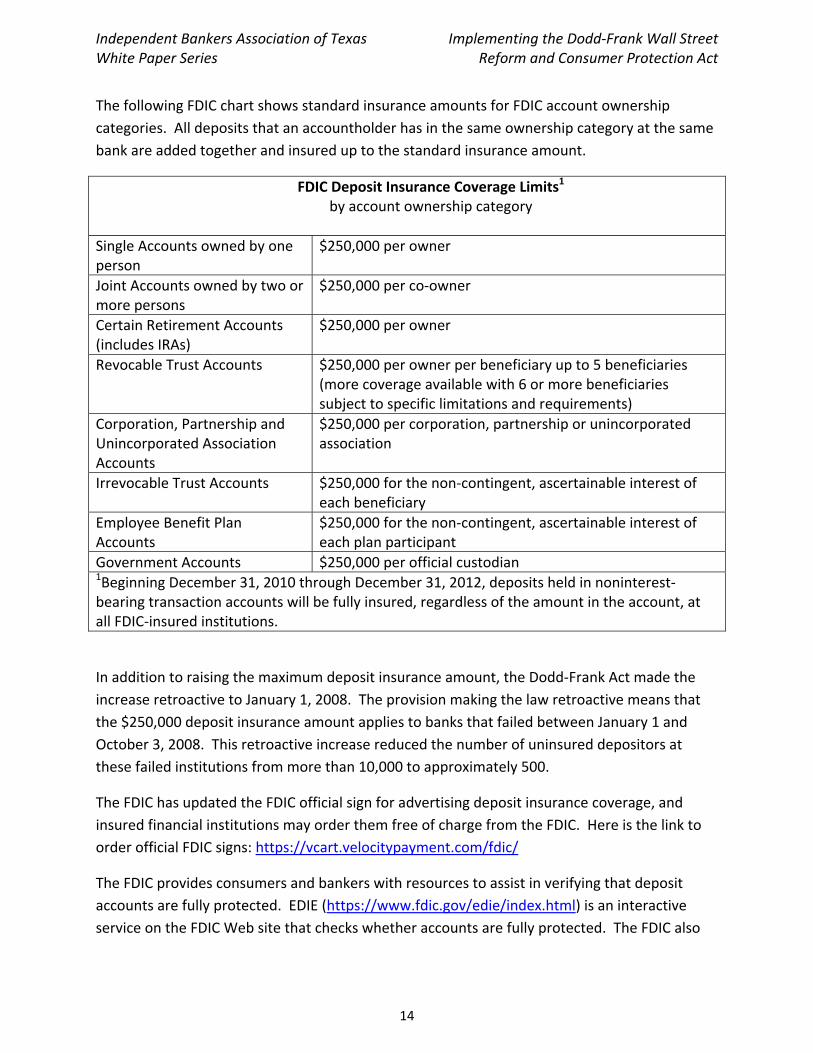

The following FDIC chart shows standard insurance amounts for FDIC account ownership categories. All deposits that an accountholder has in the same ownership category at the same bank are added together and insured up to the standard insurance amount.

FDIC Deposit Insurance Coverage Limits1 by account ownership category

Single Accounts owned by one person

$250,000 per owner

Joint Accounts owned by two or more persons

$250,000 per co‐owner

Certain Retirement Accounts (includes IRAs)

$250,000 per owner

Revocable Trust Accounts $250,000 per owner per beneficiary up to 5 beneficiaries (more coverage available with 6 or more beneficiaries subject to specific limitations and requirements)

Corporation, Partnership and Unincorporated Association Accounts

$250,000 per corporation, partnership or unincorporated association

Irrevocable Trust Accounts $250,000 for the non‐contingent, ascertainable interest of each beneficiary

Employee Benefit Plan Accounts

$250,000 for the non‐contingent, ascertainable interest of each plan participant

Government Accounts $250,000 per official custodian 1Beginning December 31, 2010 through December 31, 2012, deposits held in noninterest‐bearing transaction accounts will be fully insured, regardless of the amount in the account, at all FDIC‐insured institutions.

In addition to raising the maximum deposit insurance amount, the Dodd‐Frank Act made the increase retroactive to January 1, 2008. The provision making the law retroactive means that the $250,000 deposit insurance amount applies to banks that failed between January 1 and October 3, 2008. This retroactive increase reduced the number of uninsured depositors at these failed institutions from more than 10,000 to approximately 500.

The FDIC has updated the FDIC official sign for advertising deposit insurance coverage, and insured financial institutions may order them free of charge from the FDIC. Here is the link to order official FDIC signs: https://vcart.velocitypayment.com/fdic/

The FDIC provides consumers and bankers with resources to assist in verifying that deposit accounts are fully protected. EDIE (https://www.fdic.gov/edie/index.html) is an interactive service on the FDIC Web site that checks whether accounts are fully protected. The FDIC also

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

15

has insurance coverage brochures on its Web site: Deposit Insurance Summary, which is a basic guide, and the comprehensive guide, Your Insured Deposits. There is also a toll free assistance hotline: 1‐877‐275‐3342 (1‐877‐ASK‐FDIC) Monday – Friday, 8:00 a.m. to 8:00 p.m. Eastern.

Amend definition of assessment base.

Deposit insurance assessments will be based on total consolidated assets during an assessment period less average tangible equity. Because deposit insurance assessments will no longer be calculated exclusively on total domestic deposits, the big financial institutions will pay a more equitable portion. Community banks will likely experience reduced assessment rates and premiums. This will be implemented through FDIC rulemaking. The ICBA estimates this will save community banks $4.5 billion over the next three years.

Transaction Account Guarantee Program Extension.

Extending this program should level the playing field with large financial institutions with respect to business deposits.

Section 343 of the Dodd‐Frank Act provides full deposit insurance coverage for “noninterest‐bearing transaction accounts” for two years starting December 31, 2010. This effectively extends the Transaction Account Guarantee Program. The statutory program features:

Mandatory participation for all insured depository institutions.

No separate assessment fees for banks. Unlimited insurance for covered accounts (separate from the $250,000 standard insurance amount)

Only true noninterest‐bearing accounts are covered. (NOW accounts and any interest‐bearing accounts are not covered under this category of insurance coverage. IOLTAs also are not included.)

The current TAG program, which expires at the end of the year, was not changed by the Act. For banks that opted into the TAG program, nothing will change—they will pay for the additional coverage until the end of the year. Banks that opted out will remain opted out until the end of the year. At the end of the year, they won’t have to post whether or not they participate in the TAG program because it will no longer exist. For the next two calendar years, coverage of noninterest‐bearing transaction accounts will be part of the standard FDIC coverage. Unlike the TAG program, interest‐bearing NOW accounts and IOLTAs will not be covered.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

16

Minimum reserve ratio.

The minimum Deposit Insurance Fund reserve ratio will increase from 1.15% of insured deposits or comparable percentage of the assessment base to 1.35%. The FDIC must reach this target by September 30, 2020. In setting the assessments necessary to meet this requirement, the FDIC must offset the effect on insured depository institutions with total consolidated assets of less than $10 billion. The FDIC will adopt rules to implement this. IBAT opposed this in favor of a total exemption for community banks, but the requirement to “offset the effect” on banks with less than $10 billion in total assets should mean that most community banks will not pay an additional premium.

Miscellaneous Provisions

By Karen Neeley

Effective Date

Section 4 provides for an effective date of one day after date of enactment unless a section provides otherwise.

“Transfer date” is defined in Section 311 as the date that is one year after the date of enactment. Effective dates can be extended by following certain procedures and notice.

De Novo Branching

While one of the hallmarks of this bill is a turnaround in approach on preemption of state laws, the de novo branching section (section 613 of the Act) permits banks to establish branches as if the bank were a state bank chartered by such state. Thus, the Riegle‐Neal provision allowing states to limit branching by out of state banks is gone.

Significance. Texas had adopted the requirement that out of state banks acquire an existing institution that was at least five years old. This provision will no longer be effective as to out of state banks that wish to branch into Texas. Theoretically, this has the effect of devaluing existing Texas charters, particularly shell charters.

Effective date: Immediate.

Insider Transactions

Additional limits are placed on certain transactions with insiders. First, the provisions implemented by Regulation O are expanded to include credit exposure arising from a derivative

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

17

transaction, repurchase agreement, reverse repurchase agreement, securities lending transaction or securities borrowing transaction between the bank and the insider. (Section 614)

Effective date: One year after the transfer date.

Next, the FDI Act is amended to prohibit an insured institution from purchasing an asset from or selling an asset to an insider (executive officer, director or principal shareholder or related interest of such) unless the transaction is on market terms. If the transaction is more than 10% of the institution’s capital and surplus, then it has to be approved in advance by a majority of disinterested directors. (Section 615)

Rules. The Fed, after consulting with the OCC and FDIC, can make rules to carry this out. Logically this should be an addition to Reg O.

Significance. State chartered banks are already subject to an insider sale/lease/purchase rule that is very similar. See Section 33.109 Texas Finance Code.

Effective date: Transfer date. It is possible that this one could get extended due to the need to develop rules.

Bureau of Consumer Financial Protection – Title X

By Karen Neeley

One of the much ballyhooed provisions of the Dodd‐Frank Act is the creation of the Bureau of Consumer Financial Protection (the “Bureau”). It is a new federal regulator with extensive rule‐making authority. For community banks (i.e. $10 Billion and under in assets), the primary federal regulator will continue to examine for consumer compliance.

The director will be appointed by the President for a five year term, subject to Senate confirmation. The selection of this director will significantly affect the direction that the Bureau takes. The function units include Research, Community Affairs and Complaints. There are several offices within the bureau including:

Office of Fair Lending and Equal Opportunity Office of Financial Education Office of Service Members Affairs Office of Financial Protection of Older Americans.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

18

The Bureau will be housed at the Fed but will be independent. However, it will be funded through the Federal Reserve System. Congressional appropriations are also possible. There will be a victims relief fund to be funded with civil money penalties. Could this create an incentive for more civil money penalty actions? The staffing will be drawn from banking agencies, FTC and HUD.

The Bureau is empowered to regulate the offering and provision of “consumer financial products or services.” These include:

Brokering, extending and servicing loans or other credit Extending or brokering leases of personal or real property Real estate settlement and appraisal services Deposit‐taking activities and transmission and exchange of funds Selling, providing, issuing or reloading stored value or payment instruments if seller exercises substantial control over the terms or conditions

Check cashing, collection or guaranty services Providing financial advisory services or advice on an individualized basis (e.g. credit counseling; debt modification)

Providing consumer credit reports expected to be used in connection with any consumer financial product or service

Collecting consumer debt

Several industries lobbied successfully to stay out from under the purview of the Bureau. These include:

Attorneys Accountants Real estate brokers Tax preparers Insurance companies Merchants not significantly engaged in business of selling financial products or services Auto dealers!

The Bureau has general authority to exempt any class of covered persons, considering asset size of class and volume of transactions.

Most of the consumer protection laws and fair lending will be within the Bureau’s authority. The FTC Act is not, but the title goes further and authorizes the Bureau to regulate unfair, deceptive or abusive acts or practices. The banking regulators have recently been using the FTC Act’s prohibition against unfair or deceptive acts or practices to find overdraft privilege programs out of compliance with law. The unknown is how the Bureau will define and regulate “abusive” acts or practices. The act itself indicates that the Bureau shall have no authority to

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

19

declare an act or practice abusive in connection with the provision of a consumer financial product or service unless it:

Materially interferes with a consumer’s ability to understand a term or condition of a product or service, or

Takes unreasonable advantage of:

• the consumer’s lack of understanding of the material risks, costs or conditions of the product

• inability to protect his or her interests in selecting or using a product, or

• reasonable reliance on a covered person to act in the interests of the consumer.

A “covered person” is any person who engages in offering or providing a consumer financial product or service, and any affiliate who acts as a service provider to such person. Thus, covered person also includes officers and directors, management employees, joint venture partners and independent contractors who knowingly or recklessly participate in violations or breaches of duty. This latter could include attorneys, appraisers and accountants.

Certain existing laws and rules that will be transferred to the Bureau include: Truth in Lending Act (TILA) and Fair Credit Billing Act Truth in Savings Act Real Estate Settlement Services Procedures Act Equal Credit Opportunity Act Electronic Fund Transfer Act Consumer Leasing Act Alternative Mortgage Transaction Parity Act Fair Credit Reporting Act Fair Debt Collection Practices Act Home Ownership and Equity Protection Act SAFE Mortgage Licensing Act Home Mortgage Disclosure Act Privacy sections from Gramm Leach Bliley Act

Significance. The Bureau will initially be staffed up (we hope!) by experienced staff from the banking regulators, FTC and HUD. As it gears up, we expect to see more restrictive, cookie‐cutter requirements for retail products and services. At the same time, there is likely to be a strong drive to collect data and then develop products and services for underserved communities. Potentially, there could be a certain tension between stronger consumer “protections” and safety and soundness focus on risk analysis.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

20

The biggest area to watch is the potential paradigm shift. Currently, consumer regulatory interpretations come from banking regulators, who are familiar with the industry and the need to operate under an array of risk assessments. The Bureau could be driven to act in response to consumer complaints. Also, it has authority to issue regulations to enable a consumer to obtain information from a covered person. What impact does that have on the confidentiality of exam reports? Also, state attorneys general (which include a number of strong consumer advocates) can force the Bureau to engage in rulemaking. The emphasis shifts to whether a loan/deposit/practice is “fair” as it is structured and implemented.

Effective Date: Date of enactment; within 18 months for transfers of authority from other agencies.

Residential Mortgage Changes

By Karen Neeley

Congress perceived that a significant factor in the economic downturn was the unusual practices in the residential mortgage market. An unholy combination of poor underwriting practices resulting in loans to borrowers who could only repay if they could “flip” the mortgage plus predatory practices by (usually) unscrupulous brokers helped home values to escalate, creating an unstable bubble. A securities market, with largely unregulated credit rating agencies, made it possible to package and sell loans that, by themselves, were unattractive. But, apparently securitizing a lot of bad loans together could magically spin straw into gold. Although the Act addresses the securities issues, eliminates the OTS as a regulator (although leaving the thrift charter in place), and subjects some otherwise unregulated consumer lenders to new federal rules, to a large extent the Act misses the mark. Heavily regulated banks will be subject to even more heavy handed regulation while the shadow financial industry skates…to some extent. Nowhere is the Act more burdensome than in the residential mortgage lending arena.

Title XIV – Mortgage Reform and Anti‐Predatory Lending Act

An entire title is devoted to mortgage practices, including loan origination compensation, requirements relating to repayment ability, prepayment penalty limitations, changes to HOEPA threshold, prohibition on mandatory arbitration clauses, disclosures of credit score components, changes to Truth in Lending (and RESPA), counseling, escrow, and more HMDA report data. The entire title is subject to the purview of the Bureau of Consumer Financial Protection.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

21

Effective date: Regulations are to be finalized before the end of the 18‐month period beginning on the designated transfer date and then take effect not later than 12 months after the issuance of regs in final form. But just in case the Bureau drags its heels in finalizing regs, the effective date for sections for which regs have not been issued on the 18‐month deadline shall take effect on that date. Clear?

Qualified mortgage. This is a critical definition as compliance with it results in a carve‐out in several areas. A “qualified mortgage” (Section 1412) is one in which:

No negative amortization Can’t defer repayment of principal except for certain balloon notes No balloon payment unless certain criteria are met Income and financial resources of obligors is verified For fixed rate, underwriting is based on payment schedule that fully amortizes over the loan term, taking into account taxes, insurance and assessments

For ARM, underwriting is based on maximum rate permitted during first 5 years and a payment schedule that fully amortizes over term, taking into account taxes, insurance and assessments

Complies with DTI ratios required by regs Total points and fees don’t exceed 3% of total loan amount Term doesn’t exceed 30 years (except as may be extended for certain high cost areas) For reverse mortgage, meets reg requirements

For balloon loans to qualify, the creditor must: determine that the borrower can make all scheduled payments (except final balloon) out of income or assets other than the collateral

base underwriting on a payment schedule that fully amortizes over 30 years or less and considers all taxes, insurance and assessments

operate predominantly in a rural or underserved area, together with affiliates have total annual residential mortgage loan originations that don’t exceed a limit set by the Fed, keep the balloon notes in portfolio, and meet other to‐be‐specified asset and other criteria.

Loan Origination Compensation and Steering Provisions (Section 1403)

Loan originators may not pay loan officers or brokers compensation that varies based on the terms of the loan other than the amount of principal. So, an officer’s bonus couldn’t be higher for loans with higher interest rates.

Also, loan originators may not arrange for a consumer to finance any origination fees or costs except bona fide third‐party settlement charges not retained by the creditor or loan originator.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

22

The purpose of this is to prevent lenders from placing borrowers in loans with rates and fees that are higher than appropriate in light of the borrowers’ qualifications.

Originators are prohibited from steering consumers from a qualified mortgage to a non‐qualified one, to a loan that the consumer lacks the ability to repay or to one that has predatory characteristics (e.g. excessive fees or abusive terms).

The Bureau is empowered to write regs to prohibit abuse or unfair lending practices that promote disparities among consumers of equal creditworthiness but of different race, ethnicity, gender or age. (Isn’t this already prohibited by Equal Credit Opportunity Act and Fair Housing Act?)

Violating the steering ban creates a defense to a foreclosure without regard to the statute of limitations.

Response: Banks should begin reviewing their incentive comp programs. This provision is only the latest in a series of assaults on bonus and other incentive comp programs. The Fed and FDIC have both issued guidance in this area. Consider adopting a “policy” to cover this area generally.

Reasonable Ability to Repay (Subtitle B, Section 1411 et seq)

Mortgage lenders must determine, based on “verified and documented information,” that the consumer has a reasonable ability to repay the loan. The determination must be made based on credit history, income, obligations, debt to income ratio, employment status and other information. A fully amortizing payment schedule must be used. Failure to comply = foreclosure defense.

Response: Update, if necessary, underwriting checklists to be sure that you are obtaining W‐2s, tax returns, etc. to verify income and that you are verifying obligations. Document your calculation of critical ratios, like debt‐to‐income.

Prepayment Penalties (Section 1414)

Prepayment penalties are prohibited except for qualified mortgages. More requirements are added to the definition here. “Qualified mortgages” excludes ARMs and fixed rate mortgages with rates that exceed the average prime offer rate (“APOR”) by 1.5% for first lien loan whose principal is less than the Freddie Mac maximum or 2.5% for first lien whose principal exceeds that; or 3.5% for secondary lien transactions. The APOR will be calculated by the Fed and should reflect market conditions. Hopefully it will be more rational than the current rate, which is secondary market based and doesn’t reflect real market conditions in rural communities!

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

23

Texas law already prohibited prepayment penalties for residential mortgages with a rate of 12% or higher. For now (and unless rates really skyrocket), the threshold at which prepayment penalties are prohibited is much lower.

Lowered HOEPA Threshold (Section 1431)

New triggers are: Points and fees exceed 5% of loan amount on loans of at least $20,000 or 8% or specified dollar amount for smaller loans

APR exceeds APOR by 6.5% on first lien loans for $50,000 or more APR exceeds APOR by 8.5% on smaller and second lien loans Prepayment penalty applicable more than 3 years after closing or that exceeds 2% of prepayment

The “points and fees” that are to be considered are expanded. Only bona fide third party charges not retained by the creditor or an affiliate may be excluded. Bona fide discount points are defined and limited.

Single premium credit insurance may not be financed for residential mortgage loans and HELOCs. Insurance premiums and debt cancellation fees calculated and paid monthly are not considered “financed” and thus are okay.

Significance: This will create more pressure on rates (and loan broker “junk” fees) to stay below these thresholds. Remember, though, that Texas law (Chapter 343 Texas Finance Code) already essentially eliminated single premium credit insurance on residential mortgages through new disclosures and other limitations.

Mandatory Arbitration (Section 1414)

Mandatory arbitration clauses in residential mortgages and HELOCs are banned. After a controversy arises, however, the parties may agree to arbitrate or mediate. Also, waivers of statutory causes of action are prohibited.

Also, section 1028 requires a study of arbitration for other types of consumer loans. The Bureau could then ban mandatory arbitration across the board.

Enhanced Disclosures

The Act directs the Bureau to propose a new joint RESPA/TILA disclosure statement. This was considered before but came to naught since statutory changes were needed to make it truly feasible! However, other new disclosures in TILA are required for residential mortgages, which could facilitate this merger of the two into a single, more rational closing statement.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

24

New settlement charge (aggregate, amount payable at closing, etc.) Originator fees Total amount of interest consumer will pay over life of loan, expressed as percent of principal

New ARM disclosures relating to payments and escrows

Other, new TILA disclosures for residential mortgages include six month notice before reset of hybrid ARMs and monthly statement disclosures (which look a lot like open end periodic statement requirements!). The Fed will create a new model form. The required information includes:

Amount of principal obligation Current interest rate in effect Date on which rate may next reset or adjust Amount of any prepayment fee to be charged, if any Description of any late payment fees Phone and email address to obtain info regarding the mortgage Contact info for home counseling

A coupon book that includes substantially the same info can be used to comply with these criteria.

Counseling Programs (Subtitle D – Office of Housing Counseling, Section 1441 et seq)

HUD gets a new Office of Housing Counseling. It will be responsible for, among other things, the development and funding of housing counseling programs and foreclosure rescue education programs. The HUD Secretary must provide for certification of various computer software programs for consumers to use in evaluating different residential mortgage loan proposals to make a better, informed decision. These programs must be widely available through the Internet and at public locations (like the local library). The HUD Secretary must make an extensive study of the root causes of default and foreclosure of home loans and create a database of such info after consulting with the bank regulators. This will then be used by Congress for new legislation.

I think that I can save them some time on this. Most consumers go into default because they can’t pay. Usually they can’t pay because they have lost a job or gotten divorced.

Servicing (Subtitle E – Mortgage Servicing, Sections 1461 et seq)

Escrows for taxes, insurance and assessments will be required on first lien mortgages on borrower’s principal dwellings in certain circumstances:

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

25

Required by federal or state law Loan is made, guaranteed, or insured by a state or federal entity When original principal and interest rate meet certain thresholds

• Principal doesn’t exceed Freddie Mac maximum and

• APR exceeds APOR by 1.5% or

• Principal does exceed Freddie Mac maximum and

• APR exceeds APOR by 2.5%

Community banks have a potential exemption. The Fed can exempt creditors that operate predominantly in rural or underserved areas, keep loans in portfolio, and meet Fed established size criteria for mortgage portfolio and bank’s assets. With some exceptions, borrowers can’t get out of escrow for five years.

RESPA is amended to define when and how a servicer may obtain force placed insurance. The requirements are extremely similar to those in chapter 307 of the Texas Finance Code with regard to timing, content of notice, and second notice requirement.

TILA is amended to prohibit servicers from failing to credit a payment to the consumer’s loan account as of the date of receipt, except when a delay doesn’t harm the consumer (i.e. no charge or report of negative info to credit bureau).

HMDA Data Expansion (Section 1094)

Bank regulators use HMDA data—particularly outlier info—to initiate and conduct fair lending exams. However, the current set of information required on the HMDA LAR is a blunt instrument. It doesn’t include underwriting info like credit scores. The act fixes that by requiring expansion to include:

Credit score Borrower’s age Total points and fees Loan pricing Prepayment penalty info Loan to value ratio Period of introductory interest rate Interest only or negative amortization Term of the loan Channel of origination

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

26

Significance. HMDA LAR errors are already a common exam violation. This expanded list of required info is guaranteed to result in even more record keeping nightmares. On the other hand, it may also result in fewer fair lending targeted exams!

Consumer Reports (Section 1100F)

The Fair Credit Reporting Act is amended to require a lender to provide a consumer with their numerical credit score as well as the factors that affected it if the lender took any adverse action against the consumer based at least in part on the score. Adverse action would include denial or higher interest rate.

Impact of the “Volcker Rule” on Community Bank Investment Activities

By Ed Krei

Bill Language/Requirements: The Volcker Rule (Title VI, Section 619 of the Dodd‐Frank Legislation) will become a new Section 13 of the Bank Holding Company Act of 1956. Under the rule banks and bank holding companies (along with nonbank financial companies that are supervised by the Federal Reserve) will be

restricted from “proprietary trading” significantly restricted from the sponsorship or investment in hedge funds and private equity funds

required to retain credit risk in asset‐backed investments that they package, sell or securitize

The legislation’s proprietary trading restrictions prohibit engaging as principal for the financial firm’s own trading account in the purchase or sale of securities, options, derivatives, futures, or certain other instruments. A trading account is defined as an account utilized to make trades or take positions for short term profits or price movements. The legislation’s trading restrictions do not apply to transactions in government securities including agency and state/municipal obligations. Also excluded are transactions on behalf of customers as long as there is no conflict of interest between the banking entity and the customer.

The legislation defines private equity funds and hedge funds as entities that are not Investment Companies subject to the Investment Company Act of 1940 or similar such funds as defined by rules to be issued by regulatory authorities. The legislation allows financial firms to hold not more than three percent of Tier One capital in such investments.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

27

The Volcker Rule does not restrict a bank’s ability to sell or securitize loans but it, along with new SEC rules, does require lenders and loan securitizers to retain credit risk (an investment position) in the assets they sell.

Implementation Date/Effective Date: The requirements of the Volcker Rule will become

effective two years from the enactment of the legislation (July 21, 2010) or one year following the issuance of substantive regulations, if earlier. The Federal Reserve is required to issue initial regulations not later than January 21, 2011 and to establish a time table of at least two years for institutions subject to the rule to divest themselves of prohibited investments.

Strategic Implications For Community Bank Management: This rule has very limited

impact on community bank portfolios and investing activities. The vast majority of community based financial institutions do not maintain trading accounts or engage in trading account activities nor do they sponsor or invest in hedge funds or private equity funds.

Nonetheless, the full impact of the financial reform legislation including the Volcker Rule will not be fully understood until extensive rulemaking, required by the legislation, has been completed by the applicable financial regulatory authorities.

The consensus of analysts and experts who track the financial reform legislation believe that the securitization requirements of the Dodd‐Frank legislation will not apply to loan participations sold by banks.

Impact on Bank Holding Companies

By Sanford Brown and Peter Weinstock

The Fate of the Federal Savings Bank Charter and Thrift Holding Companies

The Federal Reserve will regulate thrift holding companies and their nonbank subsidiaries. The 10(l) election under the Home Owners’ Loan Act (“HOLA”) that currently authorizes holding companies over state savings banks to elect to be regulated either by the OTS or the Federal Reserve is eliminated.

For the first time, thrift holding companies will now be subject to regulations related to capital requirements. In contrast, under existing law, thrift holding companies are not subject to any quantitative capital requirements or leverage limitations. The Federal Reserve’s leverage and risk‐based capital requirements, however, will not become applicable for five years. This delayed effectiveness is intended to enable thrift holding companies to de‐leverage as need be.

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

28

As discussed below, the impact of such provisions will be lessened for thrift holding companies with under $500 million of total assets by the small one‐bank holding company policy statement.

Financial Holding Companies

For thrift holding companies that are engaged in activities that are financial in nature under the authority created by the Gramm‐Leach‐Bliley Act, the Act permits the Federal Reserve to require that such activities be contained in an intermediate thrift holding company. Such intermediate holding companies, as well as financial holding companies (and not just their financial institution subsidiaries), will now be subject to the Federal Reserve’s capital and management requirements. The Act, however, does not change the grandfathered status of unitary thrift holding companies.

Capital

Senator Collins proposed an amendment (the “Collins Amendment”) that was incorporated into the Act requiring bank regulators to establish for holding companies minimum capital levels that are at least of the same nature as those applicable to financial institutions. In doing so, however, the Act requires that the Federal Reserve seek to make any capital requirements counter‐cyclical, “so that the amount of capital required to be maintained by a company increases in times of economic expansion and decreases in times of economic contraction, consistent with the safety and soundness of the company.”

All trust preferred securities (“TRUPs”) issued by bank or thrift holding companies prior to December 31, 2009 (or mutual holding companies prior to May 19, 2010) continue to count as Tier I capital for holding companies with assets under $15 billion at December 31, 2009. Starting on January 1, 2013, holding companies with assets above the $15 billion threshold will deduct one‐third of TRUPs a year for the following three years from Tier I capital. (The TRUPs will become Tier II capital.) Within 18 months, the GAO is to conduct a study of hybrid capital instruments.

Holding companies that received funding under TARP will continue to be able to count such securities as Tier I capital. The $500 million Regulation Y small bank holding company exemption has been preserved.

Source‐of‐Strength

The Act codifies the Federal Reserve’s Source‐of‐Strength Policy Statement. Interestingly, while the Federal Reserve requires holding companies to serve as a source of financial and managerial strength, the statute only requires a holding company to serve as a source of

Independent Bankers Association of Texas Implementing the Dodd‐Frank Wall Street White Paper Series Reform and Consumer Protection Act

29

financial strength to its subsidiary financial institutions. Thrift holding companies, as well as bank holding companies, are subject to the source‐of‐strength requirement. Commercial firms that own ILCs4 also are subject to the source‐of‐strength requirement.

Transactions with Affiliates

The Act provides that the borrowing or lending of securities (including a guaranty, acceptance, or letter of credit issued on behalf of a securities borrowing or lending transaction) will be a “covered transaction” under the Affiliates Act and Regulation W to the extent it causes a financial institution to have credit exposure to the affiliate. Similarly, a derivative transaction will be subject to restrictions on transactions with affiliates if it creates a credit exposure for the bank. The Federal Reserve may issue regulations or interpretations considering the effect of a netting agreement on the amounts outstanding and collateral coverage requirements. Exceptions for transactions with financial subsidiaries have been eliminated. All of these changes would take effect one year from the enactment of the Act.