1 introduction to project funding. 2 the firm’s business environment - relevant factors ...

TRANSCRIPT

1

Introduction to Project Funding

2

The firm’s business environment - Relevant

Factors Government policy Fiscal policy and legislation Financial sector Macro-economic developments Past and current practices in

project financing

3

Options for project financing

Internal funds Private sector:

1. Commercial banks2. Development corporations3. Equipment vendors & subsidiary finance Companies4. Trade finance (suppliers and customers)5. Equity

Government sector

4

Internal funds

Internal funds can be generated from:

– Capital introduced by the owner

– Profits & cash flows generated by the business and retained within it

5

Capital from the private sector

Long-term loans to purchase fixed assets: secured or unsecured

Short-term loans (including lines of credits without conditions on use)

Leasing

Equity (issue of shares/stock) ...

6

Capital from the government sector

Grants

Subsidies

Government-managed development funds

7

Firms’ criteria in raising finance

Profitability Risk of excessive debt (‘Leverage’, or ‘gearing’) Matching duration of finance to

duration of project Procedures for application

8

Participants’ Experiencesof Financing Projects

9

Project finance - Issues and questions (1)

What was the project? Which sources were considered? Which sources were then

approached? What information did they require? Could you provide this information? What were their criteria? (Were

these clear to the firm?)

10

Project finance - Issues and questions (2)

Was the application successful? If not - why not?

Did any problems arise during the process of applying?

What requirements did the financier set concerning post-funding project management?

11

Project finance - Issues and questions (3)

What do you consider the firm did well? … and not-so-well?

Would you do anything differently another time?

What advice can you offer to others from this experience?

Does this experience prompt any questions?

12

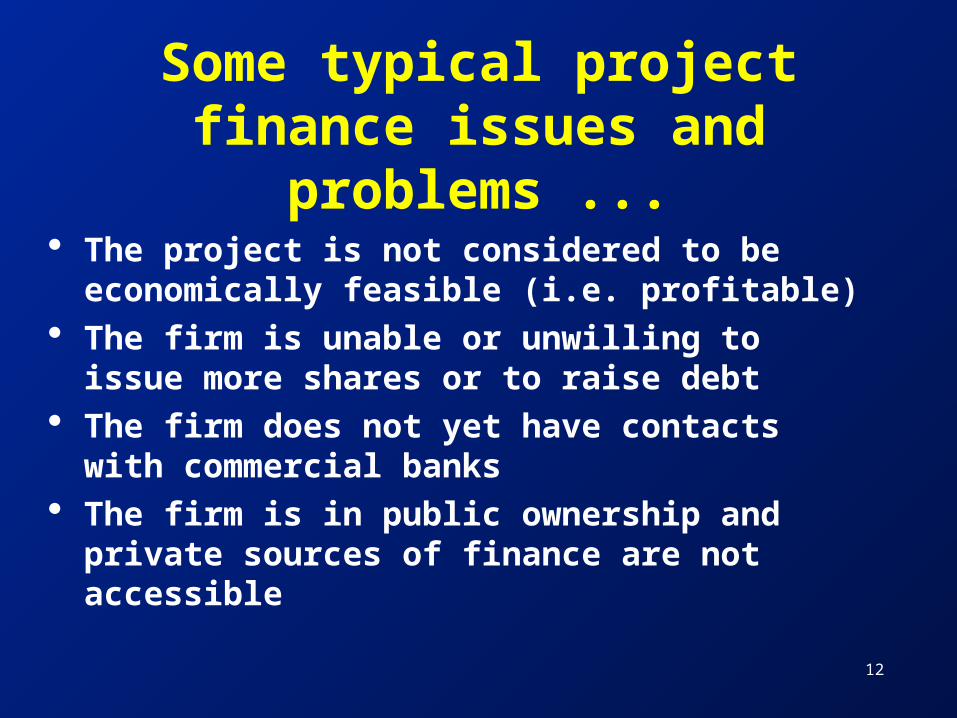

Some typical project finance issues and

problems ... The project is not considered to be

economically feasible (i.e. profitable) The firm is unable or unwilling to issue

more shares or to raise debt The firm does not yet have contacts

with commercial banks The firm is in public ownership and

private sources of finance are not accessible

13

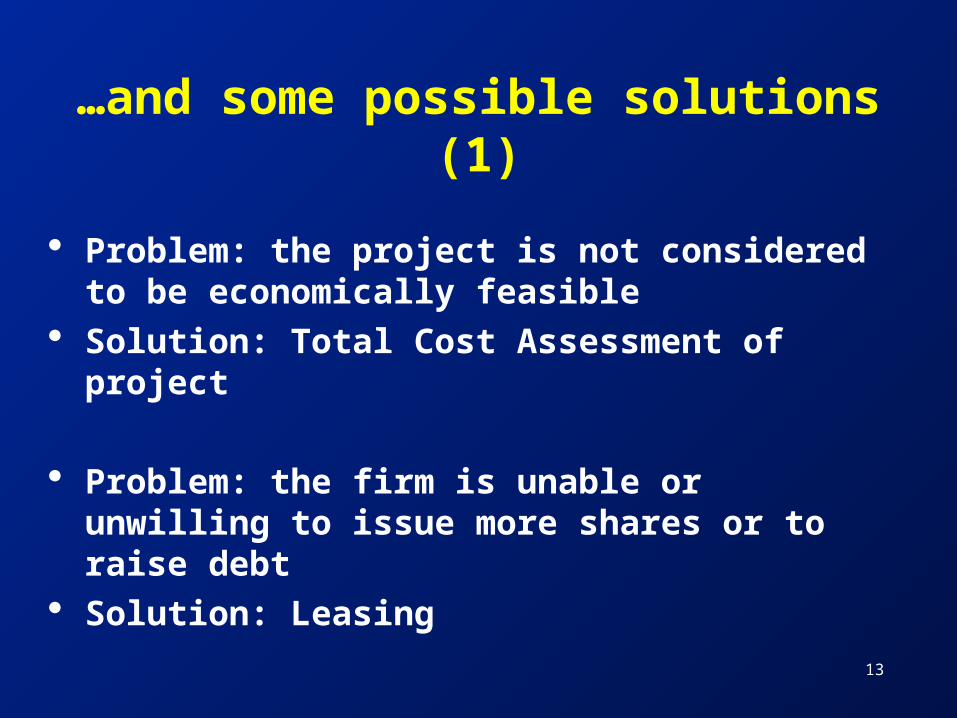

…and some possible solutions (1)

Problem: the project is not considered to be economically feasible

Solution: Total Cost Assessment of project

Problem: the firm is unable or unwilling to issue more shares or to raise debt

Solution: Leasing

14

…and some possible solutions (2)

Problem: the firm does not yet have contacts with commercial banks

Solution: contact chamber of commerce, local accountants, NGOs funds managers, for assistance

Problem: the firm is in public ownership and private sources of finance are not accessible

Solution: contact local national CP centre for institutional assistance

15

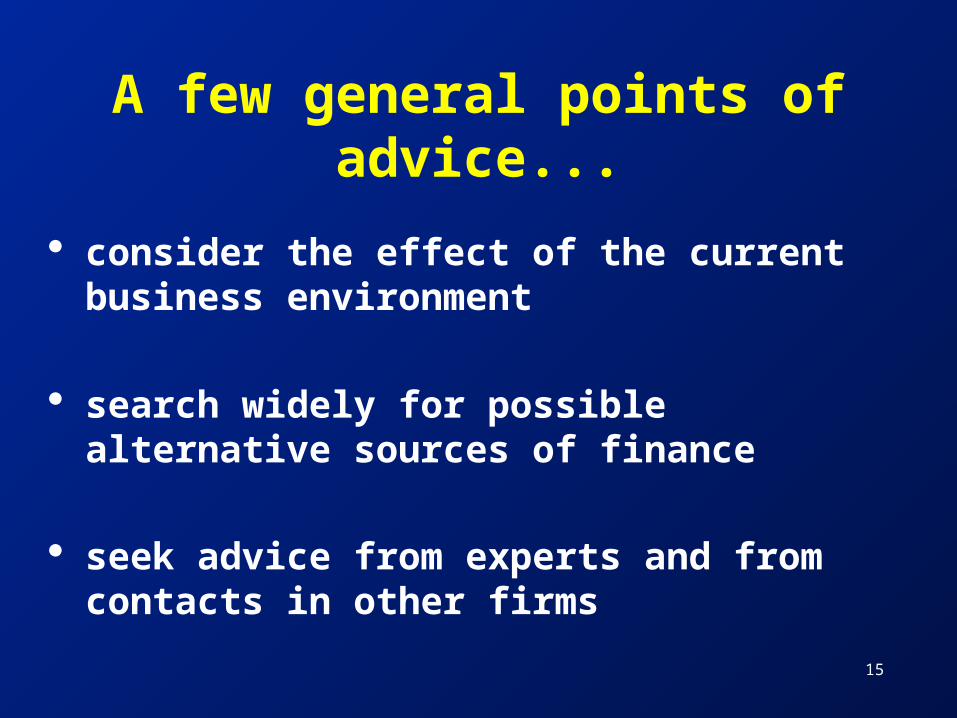

A few general points of advice...

consider the effect of the current business environment

search widely for possible alternative sources of finance

seek advice from experts and from contacts in other firms

16

Other Potential Sources for Project Financing

17

Checklist:

“Funding Options”

Checklist:

“Funding Options”

18

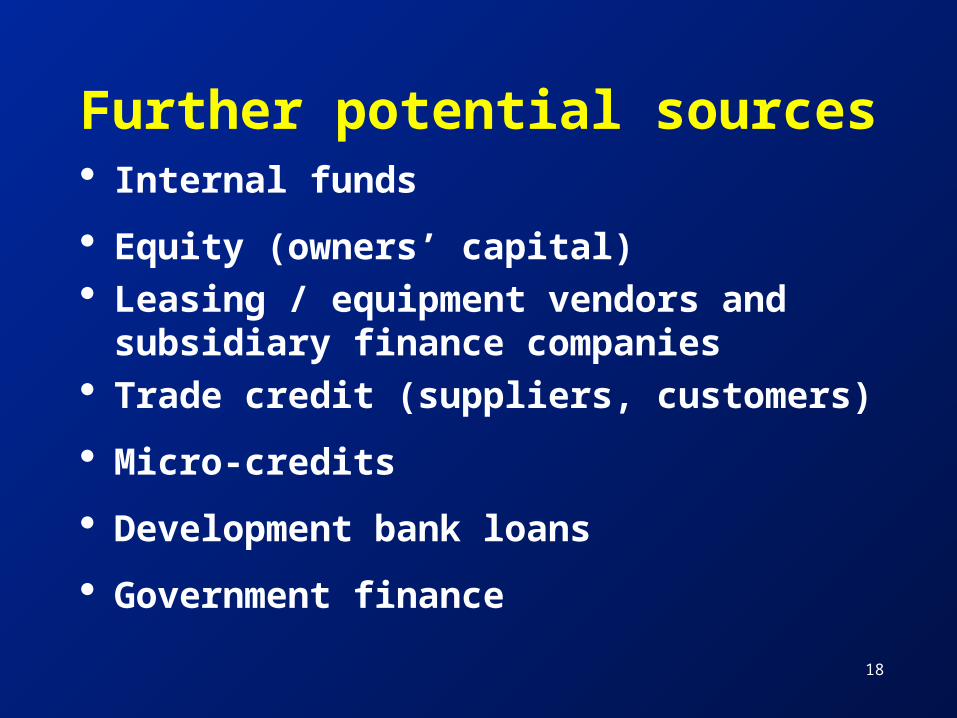

Further potential sources Internal funds

Equity (owners’ capital) Leasing / equipment vendors and

subsidiary finance companies Trade credit (suppliers, customers)

Micro-credits

Development bank loans

Government finance

19

Internal funds (1)

Internal funds = retained profits (‘reserves’)

Size of reserves depends on:-– Past profitability of business– Minimizing tax liabilities– Proportion of profits retained

vs. Paid out to owners in dividends

20

avoids having to approach external sources (and transaction costs)

preserve borrowing power for future projects

have an indirect opportunity cost not available to new firms must be built up over time

Internal funds (2)

21

Equity capital

Equity = ordinary shares, i.e. owners’ capital

Potential sources of new equity:-– more capital from the current owners

(shareholders)– new shareholders, by private

approaches– venture capital– a public share offering

22

Equipment vendors and subsidiary finance

companies Leasing has become a major source of

financing that is provided by some equipment vendors and subsidiary finance companies (‘lease-providers’).

With ‘financial leases’ (or ‘capital leases’):– Title to the equipment is held by the firm which

operates it (the ‘lease-holder’)– The lease-provider retains a first security

interest in the equipment– The lease-holder faces the risks and receives

the rewards of ownership

23

Trade finance potential sources

– suppliers of raw materials– suppliers of other goods and services– key customers

their motive: to secure a key customer or source of supply

risk: being tied to a particular supplier or customer and unable to develop business freely

24

Micro-Credits (MC) aim: ‘to match appropriate technologies and financing, through the development of packages that build on community values’ local initiatives, depending on MC managers’ knowledge of their own localities and markets an expanding source for socially desirable projects - but little-known

25

Grameen Bank (1) Grameen Bank,Bangladesh: the

pioneer (founder: Mohammed Yunus)

core belief: the credit-worthiness of the poorest members of a community

aim: to break out of the poverty cycle, using innovative technologies

a model for many similar banks operating across the world

Micro Credit example

26

finance derived from international sources (e.g. development banks) Grameen uses this to make ‘soft’ loans to local borrowers several projects in renewable energy and other environmental investments website: www.Grameen-info.org

Grameen Bank (2)Micro Credit example

27

Grameen’s lending policy no requirement for security repayable in weekly instalments eligibility for subsequent loans depends on full repayment of any earlier loans transparency in bank transactions helps to encourage repayments by borrowers, through social pressure

Micro Credit example

28

Grameen - the results

2.34 million borrowers in Bangladesh

94% are women loans for projects in 39,000 of

86,000 villages in Bangladesh 1977-1997, total lending - US$2

billion now, 223 Grameen-type

programmes in 58 countries

Micro Credit example

29

Development banks (1)

examples:– World Bank– International Finance Corporation– Inter-American Development Bank– Asian Development Bank

wide and diverse range of programmes and projects

30

Development banks (2)development banks aim:-

– to lend large amounts…– … but at low transaction costs

therefore, traditionally, mainly large projects in the public sector stringent guidelines on project characteristics and lending criteria (e.g. to be environmental, social,

developmental, technically innovative)

31

Development banks (3)

Benefits of development bank finance:

can help with technological and managerial advice on the project

project packaging

liaison with other potential sources of finance

32

Raising finance from government schemes

identify the available schemes find out:-

– the criteria and conditions of the scheme– the procedures for application

develop the firm’s application:-– to match the scheme’s criteria – to identify how the project supports public policy objectives

33

Grants low or zero cost of capital may be available for only part of a

project, or on restrictive terms preserves borrowing power for other

purposes accessible via local brokers and/or

international development agencies BUT:-

– can conceal true long-term costs– misses opportunity to build long-term

relationship with financiers

34

Past funding experience successful past experiences with

financing projects?

how might CP projects be different? Why might they be ...

– more difficult to finance?– easier to finance?

could these further sources be relevant? If so - when and how?

35

Summary a wide range of potential sources means:-

– more likely to be able to raise finance...– … and on better terms

the range varies between countries

and over time an early search for a wide range of sources can be very worthwhile each source will have its own criteria and procedures

36

Acme Electroplaters:Part 2