fortumapps.fortum.fi/gallery/fortum_investor_presentation_may_2015.pdf · investor / analyst...

TRANSCRIPT

FORTUM Power and heat company in the Nordic area, Russia, Poland and the Baltics

Investor / Analyst material

May 2015

2

Disclaimer

This presentation does not constitute an invitation to underwrite, subscribe for,

or otherwise acquire or dispose of any Fortum shares.

Past performance is no guide to future performance, and persons needing

advice should consult an independent financial adviser.

Content

3

Fortum today pages 4 – 17

European and Nordic power markets pages 18 – 29

Fortum’s nuclear fleet pages 30 – 33

Russia pages 34 – 39

Capacity payments pages 37 – 38

Fortum’s investment programme page 39

Financials and outlook pages 40 – 45

Hedging pages 46

Distribution business page 47

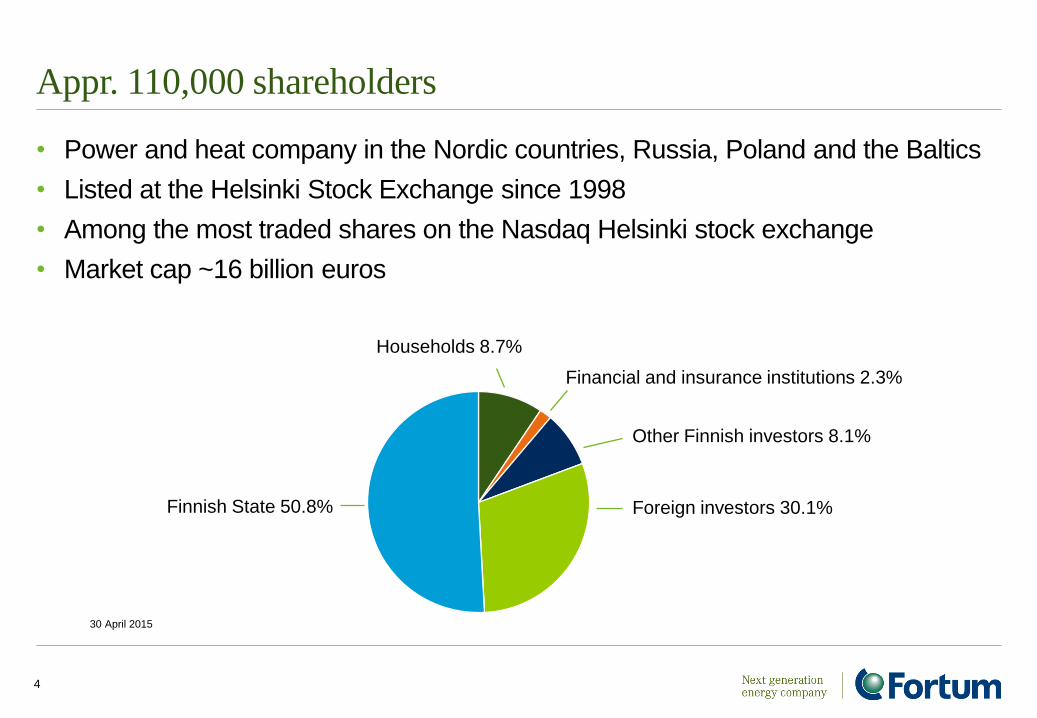

Appr. 110,000 shareholders

• Power and heat company in the Nordic countries, Russia, Poland and the Baltics

• Listed at the Helsinki Stock Exchange since 1998

• Among the most traded shares on the Nasdaq Helsinki stock exchange

• Market cap ~16 billion euros

4

30 April 2015

Foreign investors 30.1% Finnish State 50.8%

Other Finnish investors 8.1%

Households 8.7%

Financial and insurance institutions 2.3%

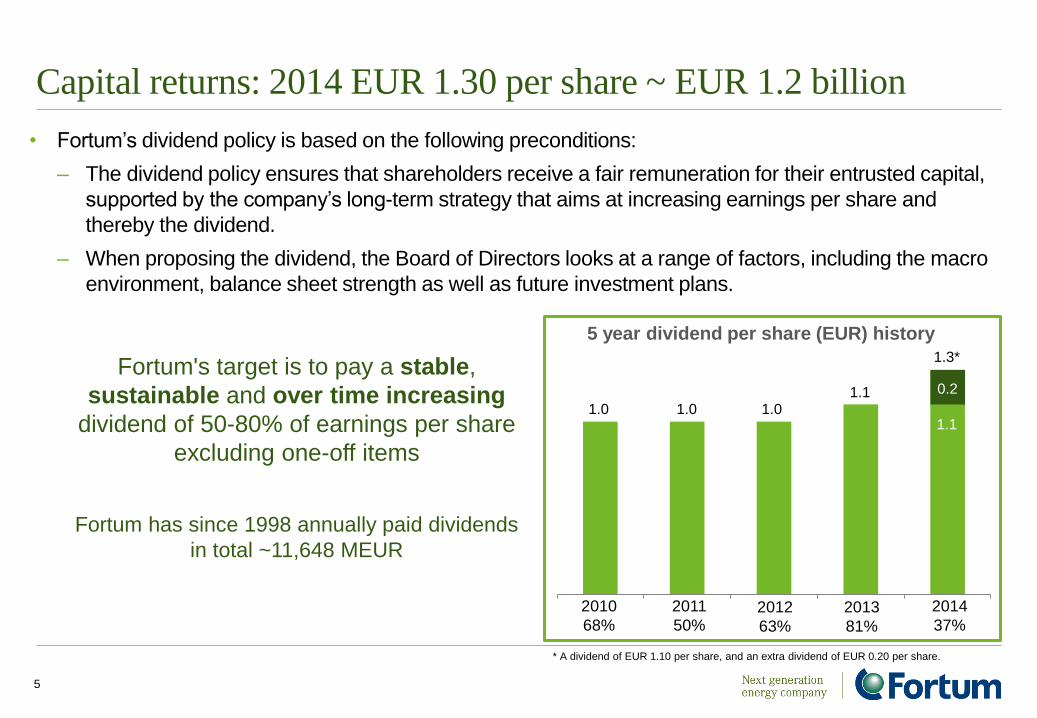

Capital returns: 2014 EUR 1.30 per share ~ EUR 1.2 billion

• Fortum’s dividend policy is based on the following preconditions:

– The dividend policy ensures that shareholders receive a fair remuneration for their entrusted capital,

supported by the company’s long-term strategy that aims at increasing earnings per share and

thereby the dividend.

– When proposing the dividend, the Board of Directors looks at a range of factors, including the macro

environment, balance sheet strength as well as future investment plans.

5

Fortum's target is to pay a stable,

sustainable and over time increasing

dividend of 50-80% of earnings per share

excluding one-off items

Fortum has since 1998 annually paid dividends

in total ~11,648 MEUR

2010

68%

2011

50% 2012

63%

2013

81%

2014

37%

1.0 1.0 1.0 1.1

1.3*

5 year dividend per share (EUR) history

0.2

1.1

* A dividend of EUR 1.10 per share, and an extra dividend of EUR 0.20 per share.

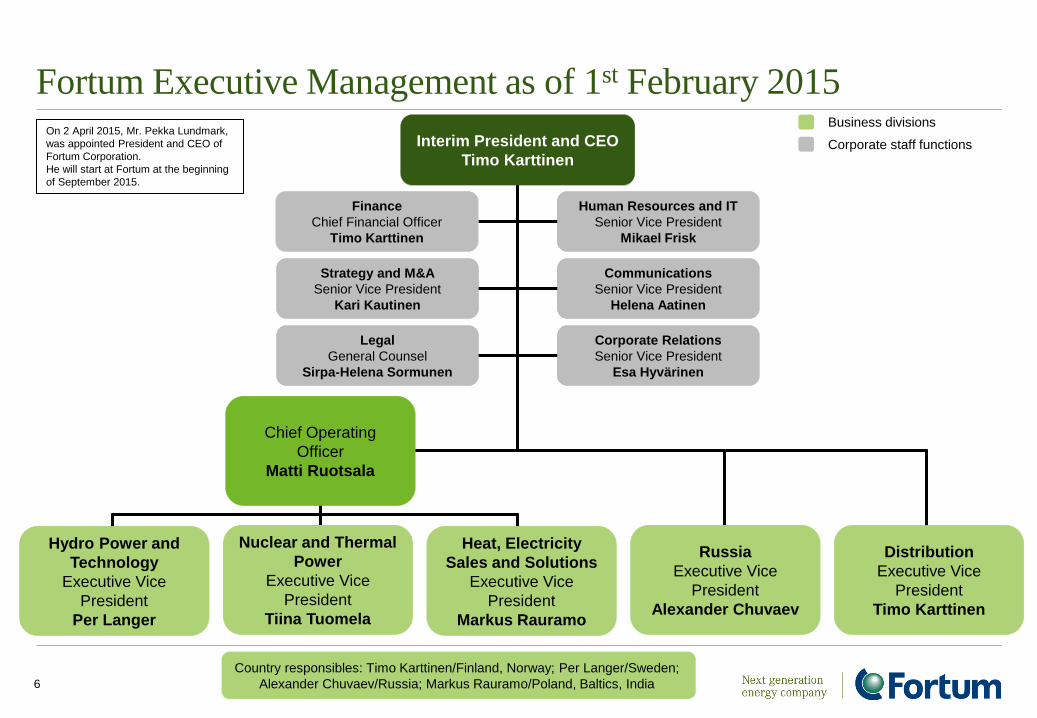

Fortum Executive Management as of 1st February 2015

6

Country responsibles: Timo Karttinen/Finland, Norway; Per Langer/Sweden;

Alexander Chuvaev/Russia; Markus Rauramo/Poland, Baltics, India

Human Resources and IT

Senior Vice President

Mikael Frisk

Finance

Chief Financial Officer

Timo Karttinen

Strategy and M&A

Senior Vice President

Kari Kautinen

Communications

Senior Vice President

Helena Aatinen

Corporate Relations

Senior Vice President

Esa Hyvärinen

Legal

General Counsel

Sirpa-Helena Sormunen

Business divisions

Corporate staff functions Interim President and CEO

Timo Karttinen

Chief Operating

Officer

Matti Ruotsala

Distribution

Executive Vice

President

Timo Karttinen

Russia

Executive Vice

President

Alexander Chuvaev

Nuclear and Thermal

Power

Executive Vice

President

Tiina Tuomela

Hydro Power and

Technology

Executive Vice

President

Per Langer

Heat, Electricity

Sales and Solutions

Executive Vice

President

Markus Rauramo

On 2 April 2015, Mr. Pekka Lundmark,

was appointed President and CEO of

Fortum Corporation.

He will start at Fortum at the beginning

of September 2015.

Fortum’s Mission and Strategy

7

Strategy

Fortum’s purpose is to create energy that improves life for present and future

generations. We provide sustainable solutions for society and deliver excellent

value to our shareholders.

Mission

Build on the strong

Nordic core

Create solid earnings

growth in Russia

Build a platform for

future growth

Strong competence in CO2-free hydro and nuclear, efficient CHP production and

energy markets

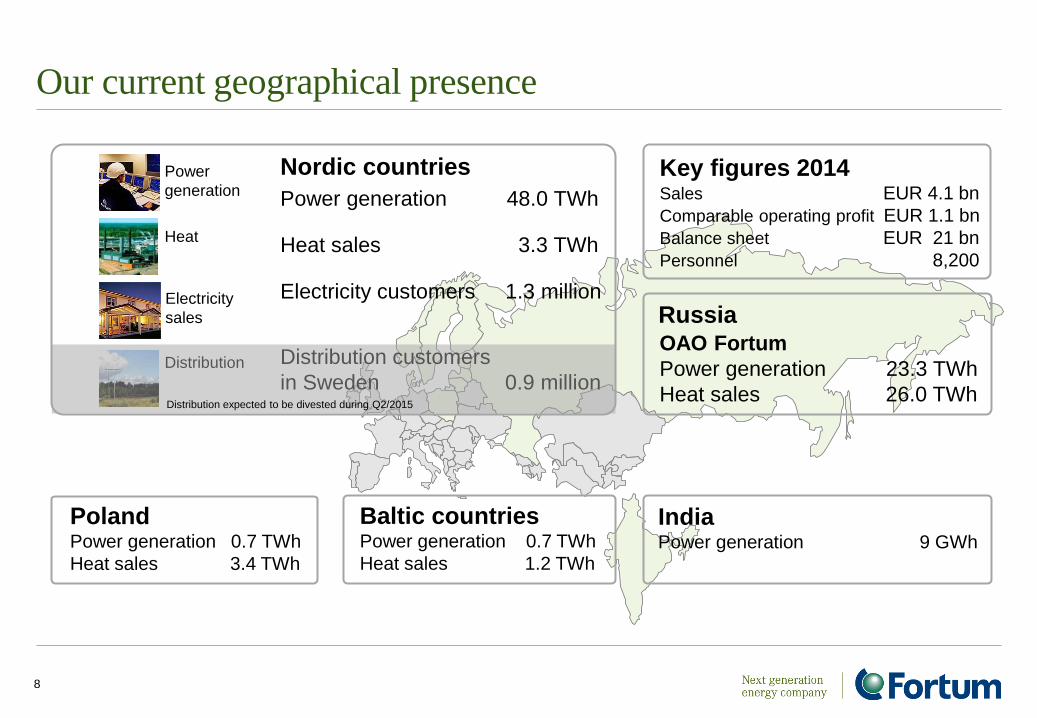

Our current geographical presence

8

Nordic countries

Power generation 48.0 TWh

Heat sales 3.3 TWh

Electricity customers 1.3 million

Distribution customers

in Sweden 0.9 million

Distribution

Power

generation

Electricity

sales

Heat

OAO Fortum

Power generation 23.3 TWh

Heat sales 26.0 TWh

Russia

Poland Power generation 0.7 TWh

Heat sales 3.4 TWh

Baltic countries Power generation 0.7 TWh

Heat sales 1.2 TWh

India Power generation 9 GWh

Key figures 2014 Sales EUR 4.1 bn

Comparable operating profit EUR 1.1 bn

Balance sheet EUR 21 bn

Personnel 8,200

Distribution expected to be divested during Q2/2015

Fortum’s reporting segments and divisions

9

Distribution

• Electricity distribution

activities

• Divestment of the business

is expected to be

concluded during H1 2015.

Russia

• Power and heat

generation and sales in

Russia

• Includes OAO Fortum

and Fortum’s slightly

over 29% holding in

TGC-1

Power and Technology

• Hydro, nuclear and

thermal power generation

• Power Solutions with

expert services

• Portfolio management and

trading

• Technology and R&D

functions

The segment incorporates

two business divisions:

• Hydro Power and

Technology

• Nuclear and Thermal

Power

Heat, Electricity Sales

and Solutions

• Combined heat and

power (CHP) production

• District heating activities

and business to business

heating solutions

• Solar business

• Electricity sales and

related customer offering

• Corporate Sustainability

10

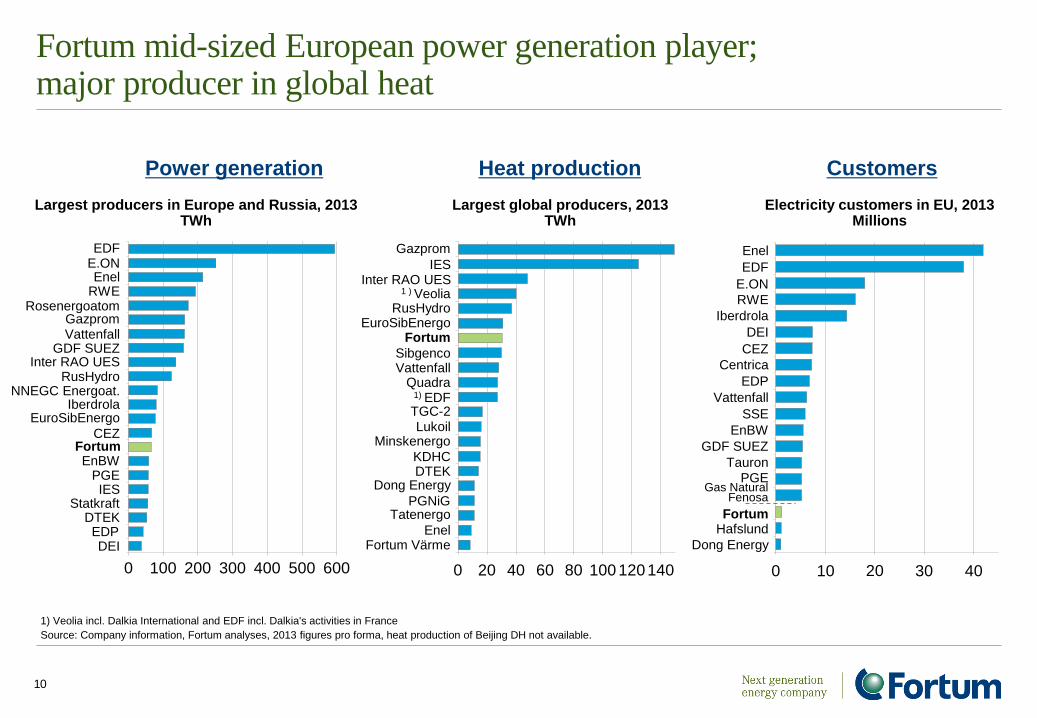

Fortum mid-sized European power generation player; major producer in global heat

1) Veolia incl. Dalkia International and EDF incl. Dalkia's activities in France

Source: Company information, Fortum analyses, 2013 figures pro forma, heat production of Beijing DH not available.

Largest global producers, 2013 TWh

Largest producers in Europe and Russia, 2013 TWh

Power generation Heat production

Electricity customers in EU, 2013 Millions

Customers

Gazprom

DEI

EuroSibEnergo Iberdrola

Fortum EnBW

Vattenfall

CEZ

RWE

IES

DTEK

PGE

Rosenergoatom

NNEGC Energoat.

Enel E.ON EDF

GDF SUEZ

Statkraft

Inter RAO UES RusHydro

EDP

0 100 200 300 400 500 600

GDF SUEZ

DEI

CEZ

Enel

Centrica

EDP

Iberdrola

SSE

EnBW

Fortum

EDF

E.ON

RWE

Gas Natural Fenosa

PGE Tauron

Hafslund

Dong Energy

0 20 40 10 30

Vattenfall

0 20 40 60 80 100 120 140

KDHC

Quadra

Tatenergo

Minskenergo

DTEK

EuroSibEnergo

TGC-2

Fortum

Dong Energy

Enel

Lukoil

Sibgenco

IES

Vattenfall

PGNiG

Inter RAO UES

1) EDF

RusHydro

1 ) Veolia

Gazprom

Fortum Värme

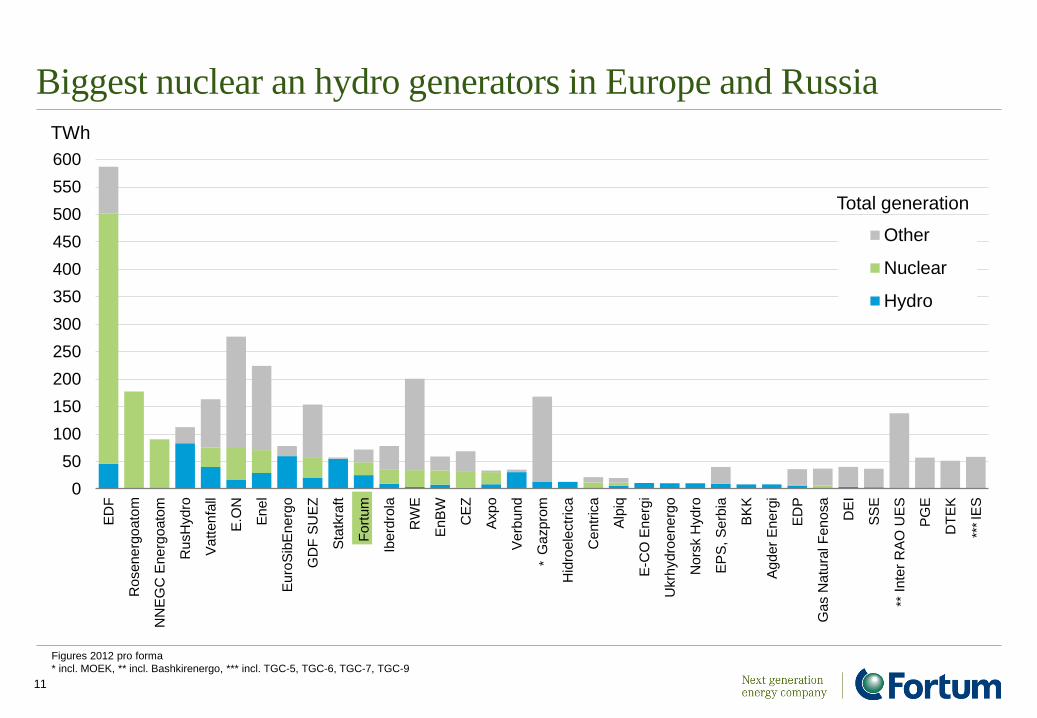

Biggest nuclear an hydro generators in Europe and Russia

11

Figures 2012 pro forma

* incl. MOEK, ** incl. Bashkirenergo, *** incl. TGC-5, TGC-6, TGC-7, TGC-9

TWh

Total generation

0

50

100

150

200

250

300

350

400

450

500

550

600

ED

F

Ro

sen

erg

oa

tom

NN

EG

C E

nerg

oato

m

Ru

sH

ydro

Vatt

enfa

ll

E.O

N

Enel

Euro

Sib

Energ

o

GD

F S

UE

Z

Sta

tkra

ft

Fo

rtum

Iberd

rola

RW

E

EnB

W

CE

Z

Axpo

Verb

und

Gazpro

m

Hid

roele

ctr

ica

Centr

ica

Alp

iq

E-C

O E

nerg

i

Ukrh

ydro

energ

o

Nors

k H

ydro

EP

S, S

erb

ia

BK

K

Agder

Energ

i

ED

P

Ga

s N

atu

ral F

en

osa

DE

I

SS

E

Inte

r R

AO

UE

S

PG

E

DT

EK

IES

Other

Nuclear

Hydro

*

***

**

Fortum a forerunner in sustainability

• Nordic Climate Disclosure Leadership Index (CDLI)

• STOXX® Global ESG Leaders indices

• oekom

• OMX GES Sustainability Finland Index

• ECPI® Indices

12

0

200

400

600

800

1 000

1 200

DE

I

RW

E

Dra

x

SS

E

CE

Z

E.O

N

Vatt

en

fall

ED

P

Enel

Edip

ow

er

EnB

W

Gas N

atu

ral F

enosa

GD

F S

UE

Z

Do

ng

En

erg

y

Fo

rtu

m to

tal

Iberd

rola

PV

O

ED

F

Verb

und

Fort

um

EU

Sta

tkra

ft

64

g CO2/kWh electricity, 2013

2014

64% of Fortum's total power generation CO2-free

94% of Fortum’s power generation in the EU CO2-free

Close to 100% of the ongoing investment programme

in the EU is CO2-free.

Average 328 g/kWh

200

Fortum's carbon exposure among the lowest in Europe

13

Note: : Fortum’s specific emissions of the power generation in 2014 in the EU were 39 g/kWh and in total 177 g/kWh.

Only European generation except “Fortum total“ which includes Russia.

Source:

PWC & Enerpresse, December 2014

Climate Change and Electricity, Fortum

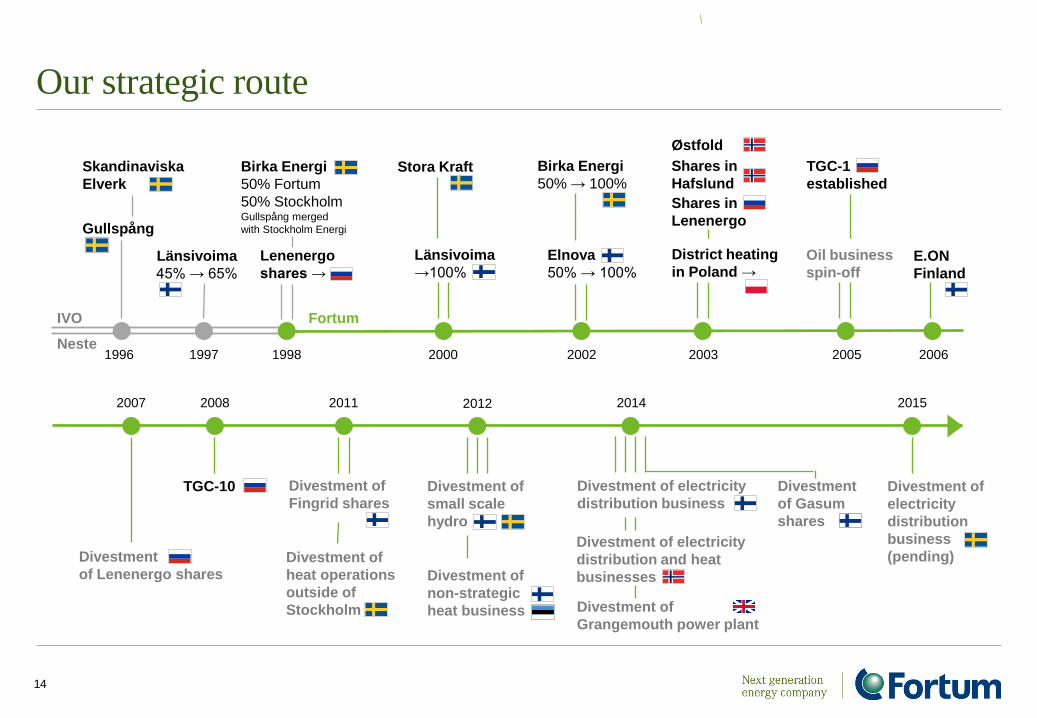

Our strategic route

14

Birka Energi

50% → 100%

Gullspång

Neste

Divestment of

non-strategic

heat business

2007

Skandinaviska

Elverk

Länsivoima

45% → 65%

Birka Energi

50% Fortum

50% Stockholm Gullspång merged

with Stockholm Energi

TGC-10 Divestment of

Fingrid shares

Divestment of

heat operations

outside of

Stockholm

Divestment

of Lenenergo shares

1996

IVO Fortum

Divestment of

small scale

hydro

2012 2008 2015

1997

Lenenergo

shares →

Stora Kraft

Länsivoima

→100%

2000

Elnova

50% → 100%

Østfold

Shares in

Lenenergo

Shares in

Hafslund

District heating

in Poland →

2003

Oil business

spin-off

TGC-1

established

2005

2011

1998 2002

Divestment of electricity

distribution and heat

businesses

Divestment of electricity

distribution business

Divestment of

Grangemouth power plant

Divestment

of Gasum

shares

2014

2006

E.ON

Finland

Divestment of

electricity

distribution

business

(pending)

15

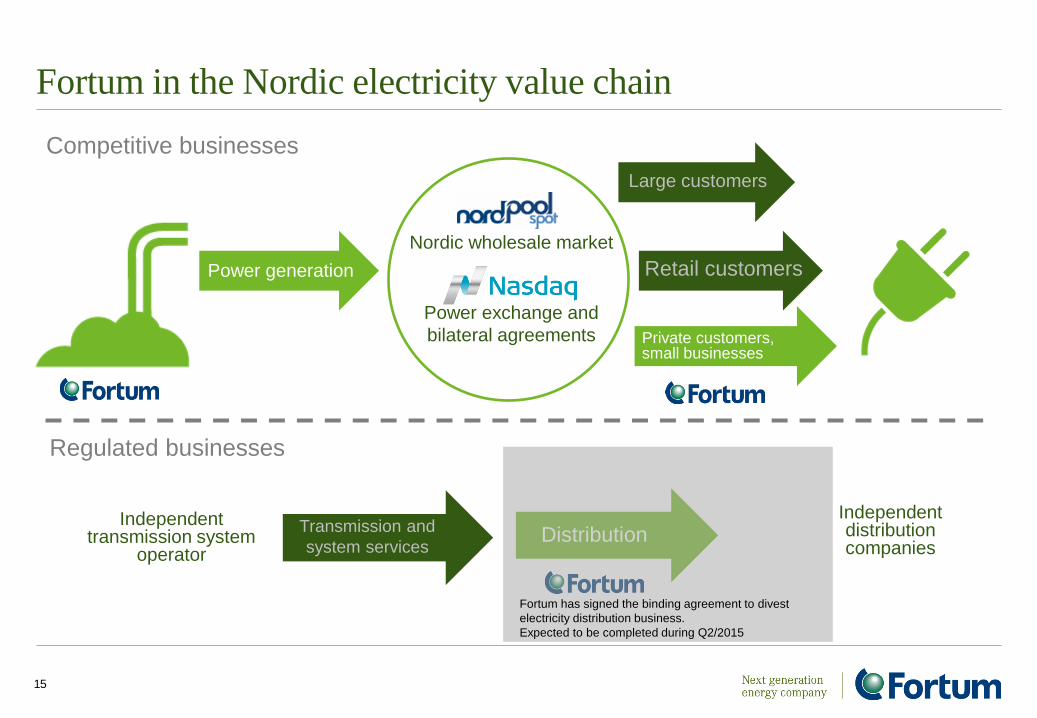

Fortum in the Nordic electricity value chain

Competitive businesses

Regulated businesses

Power generation

Nordic wholesale market

Power exchange and

bilateral agreements

Large customers

Retail customers

Private customers, small businesses

Independent transmission system

operator

Independent distribution companies

Distribution Transmission and

system services

Fortum has signed the binding agreement to divest

electricity distribution business.

Expected to be completed during Q2/2015

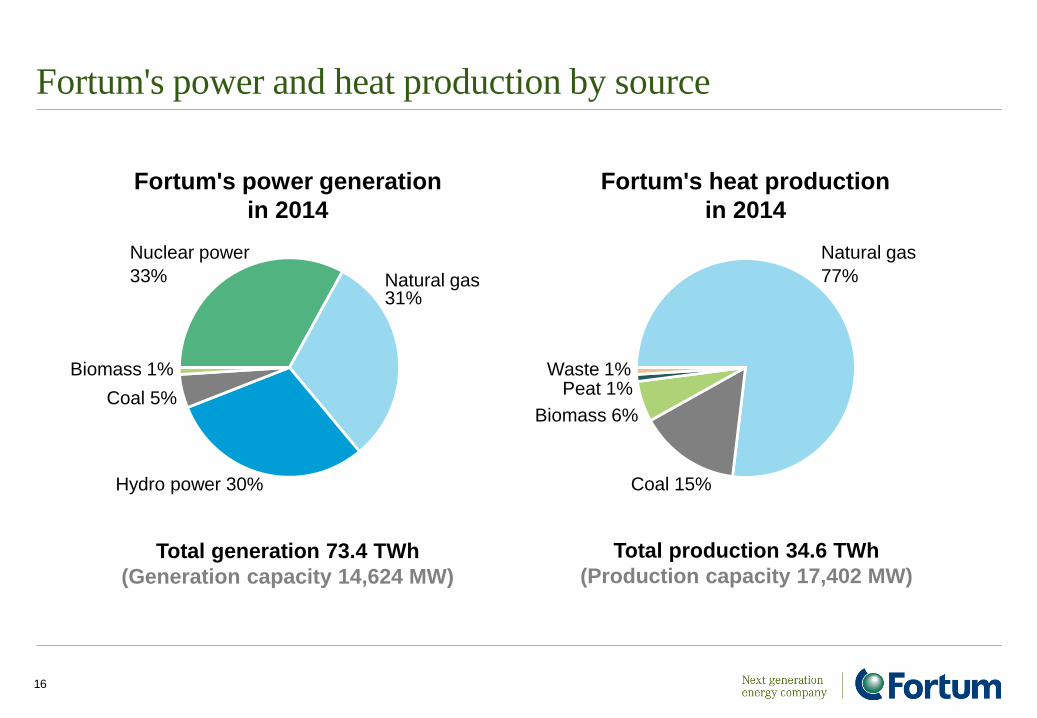

Fortum's power and heat production by source

16

Natural gas 31%

Nuclear power

33%

Coal 5%

Biomass 1%

Total generation 73.4 TWh

(Generation capacity 14,624 MW)

Hydro power 30%

Fortum's power generation

in 2014

Total production 34.6 TWh

(Production capacity 17,402 MW)

Fortum's heat production

in 2014

Peat 1% Waste 1%

Biomass 6%

Natural gas

77%

Coal 15%

Nuclear power

48%

Coal 4%

Hydro power 44%

Natural gas 2%

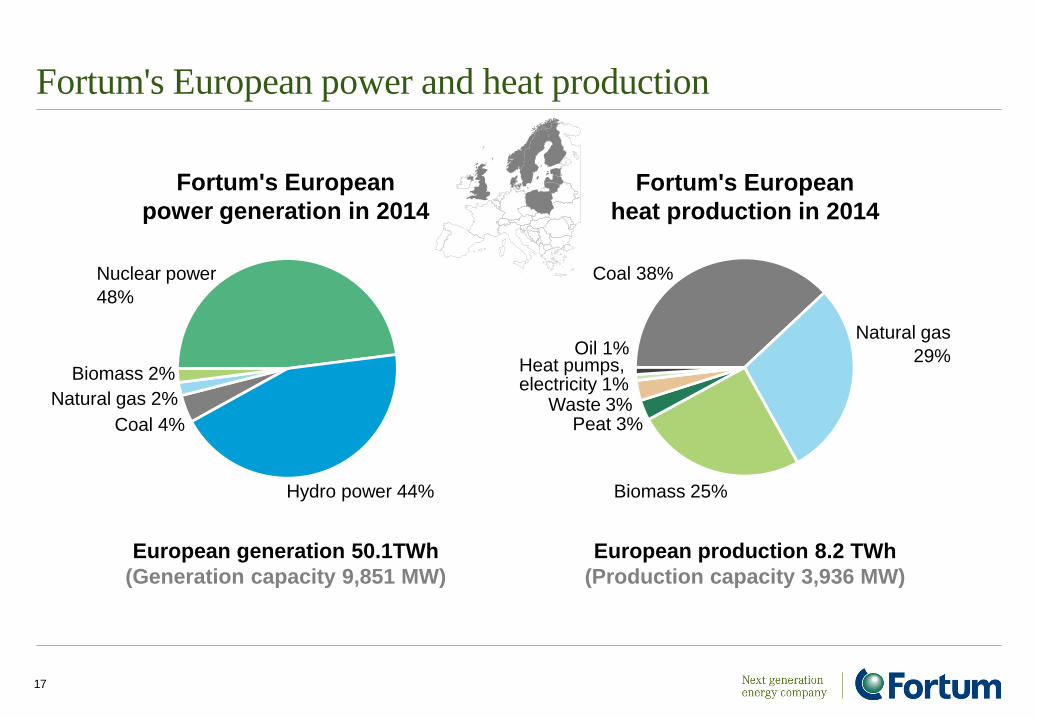

European generation 50.1TWh

(Generation capacity 9,851 MW)

Fortum's European

power generation in 2014

Biomass 2%

Natural gas

29%

Fortum's European

heat production in 2014

Peat 3%

Oil 1%

Waste 3%

Biomass 25%

Heat pumps, electricity 1%

Coal 38%

European production 8.2 TWh

(Production capacity 3,936 MW)

Fortum's European power and heat production

17

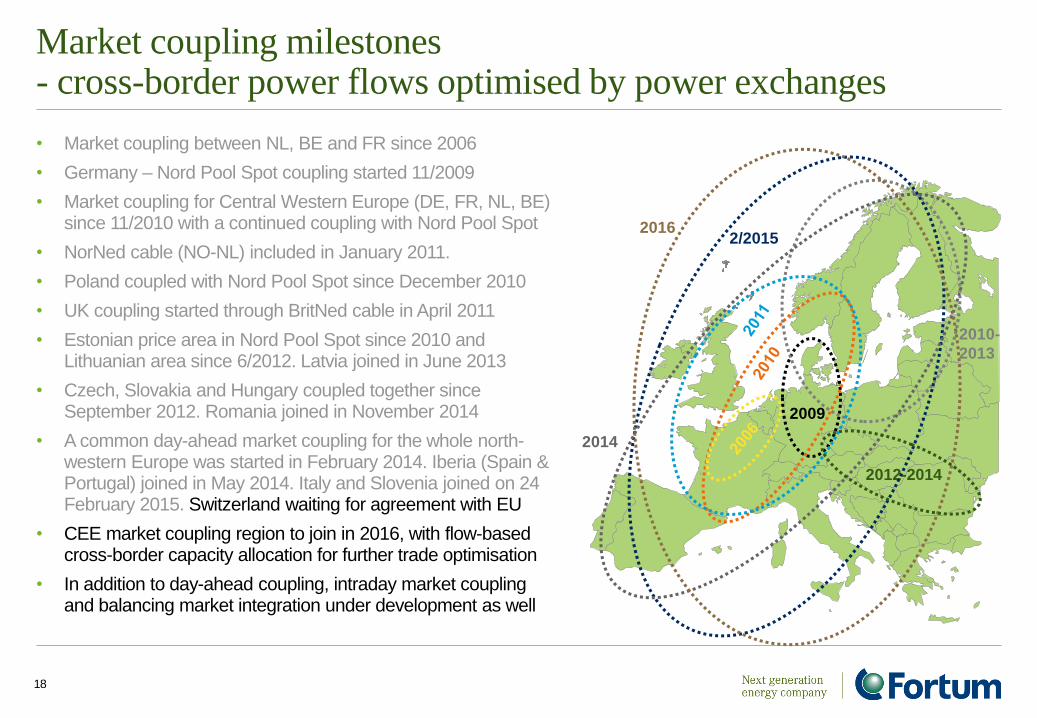

Market coupling milestones - cross-border power flows optimised by power exchanges

• Market coupling between NL, BE and FR since 2006

• Germany – Nord Pool Spot coupling started 11/2009

• Market coupling for Central Western Europe (DE, FR, NL, BE) since 11/2010 with a continued coupling with Nord Pool Spot

• NorNed cable (NO-NL) included in January 2011.

• Poland coupled with Nord Pool Spot since December 2010

• UK coupling started through BritNed cable in April 2011

• Estonian price area in Nord Pool Spot since 2010 and Lithuanian area since 6/2012. Latvia joined in June 2013

• Czech, Slovakia and Hungary coupled together since September 2012. Romania joined in November 2014

• A common day-ahead market coupling for the whole north-western Europe was started in February 2014. Iberia (Spain & Portugal) joined in May 2014. Italy and Slovenia joined on 24 February 2015. Switzerland waiting for agreement with EU

• CEE market coupling region to join in 2016, with flow-based cross-border capacity allocation for further trade optimisation

• In addition to day-ahead coupling, intraday market coupling and balancing market integration under development as well

18

2009

2/2015

2012-2014

2010-

2013

2016

2014

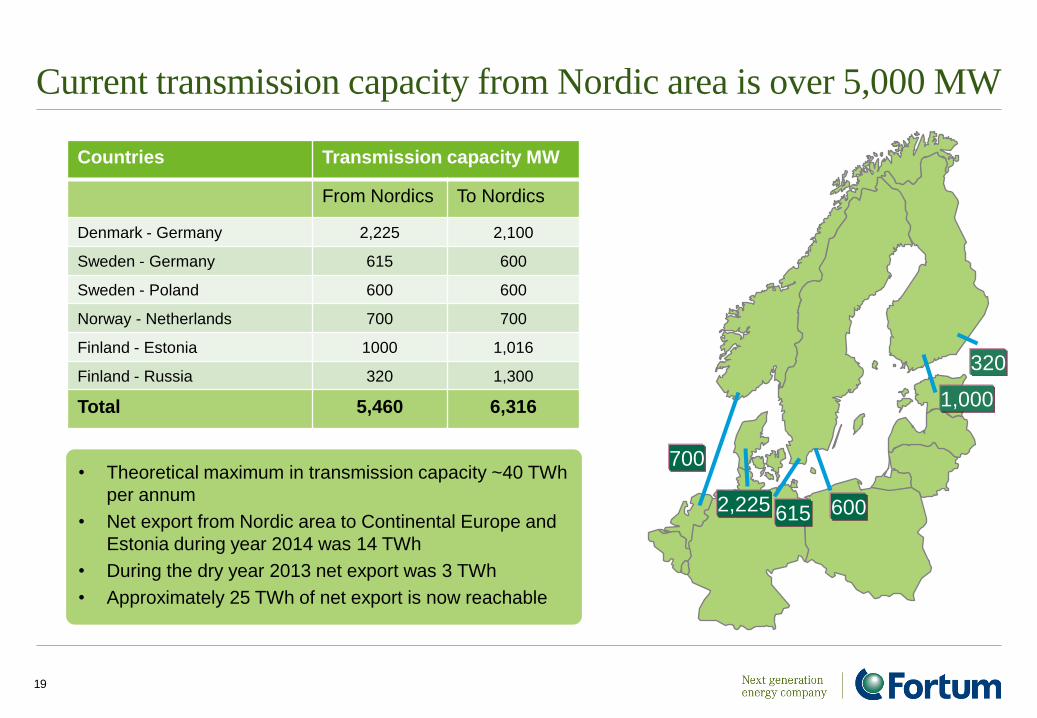

Current transmission capacity from Nordic area is over 5,000 MW

19

• Theoretical maximum in transmission capacity ~40 TWh

per annum

• Net export from Nordic area to Continental Europe and

Estonia during year 2014 was 14 TWh

• During the dry year 2013 net export was 3 TWh

• Approximately 25 TWh of net export is now reachable

Countries Transmission capacity MW

From Nordics To Nordics

Denmark - Germany 2,225 2,100

Sweden - Germany 615 600

Sweden - Poland 600 600

Norway - Netherlands 700 700

Finland - Estonia 1000 1,016

Finland - Russia 320 1,300

Total 5,460 6,316

700

2,225 615 600

1,000

320

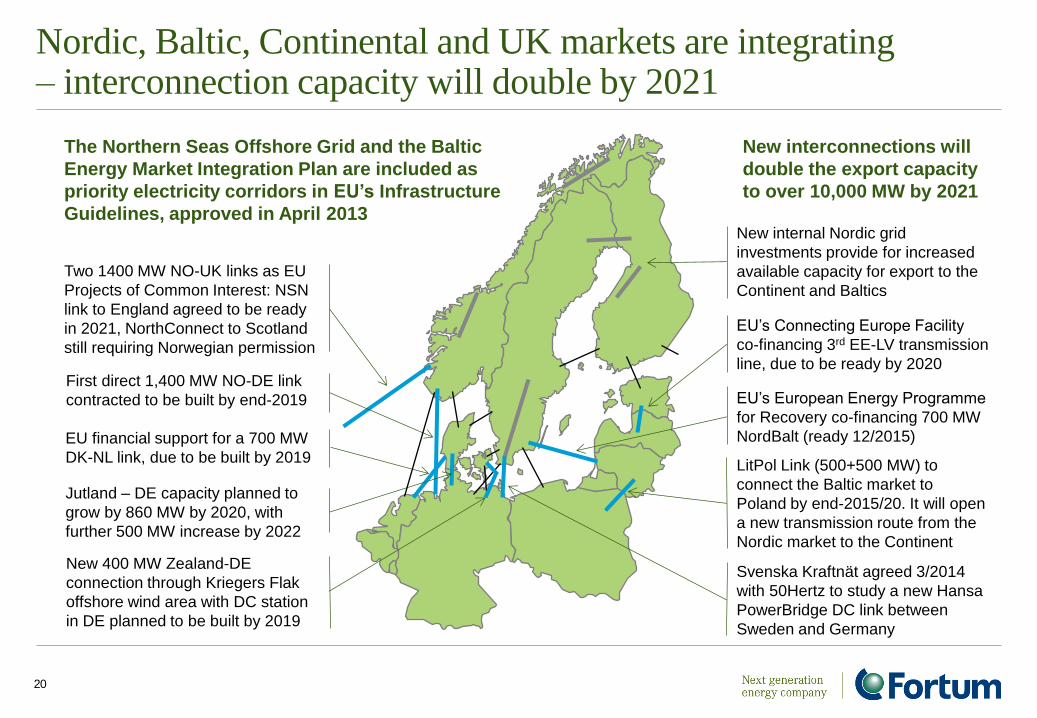

Nordic, Baltic, Continental and UK markets are integrating – interconnection capacity will double by 2021

20

Two 1400 MW NO-UK links as EU

Projects of Common Interest: NSN

link to England agreed to be ready

in 2021, NorthConnect to Scotland

still requiring Norwegian permission

First direct 1,400 MW NO-DE link

contracted to be built by end-2019

EU financial support for a 700 MW

DK-NL link, due to be built by 2019

Jutland – DE capacity planned to

grow by 860 MW by 2020, with

further 500 MW increase by 2022

Svenska Kraftnät agreed 3/2014

with 50Hertz to study a new Hansa

PowerBridge DC link between

Sweden and Germany

The Northern Seas Offshore Grid and the Baltic

Energy Market Integration Plan are included as

priority electricity corridors in EU’s Infrastructure

Guidelines, approved in April 2013

New interconnections will

double the export capacity

to over 10,000 MW by 2021

LitPol Link (500+500 MW) to

connect the Baltic market to

Poland by end-2015/20. It will open

a new transmission route from the

Nordic market to the Continent

EU’s European Energy Programme

for Recovery co-financing 700 MW

NordBalt (ready 12/2015)

New internal Nordic grid

investments provide for increased

available capacity for export to the

Continent and Baltics

EU’s Connecting Europe Facility

co-financing 3rd EE-LV transmission

line, due to be ready by 2020

New 400 MW Zealand-DE

connection through Kriegers Flak

offshore wind area with DC station

in DE planned to be built by 2019

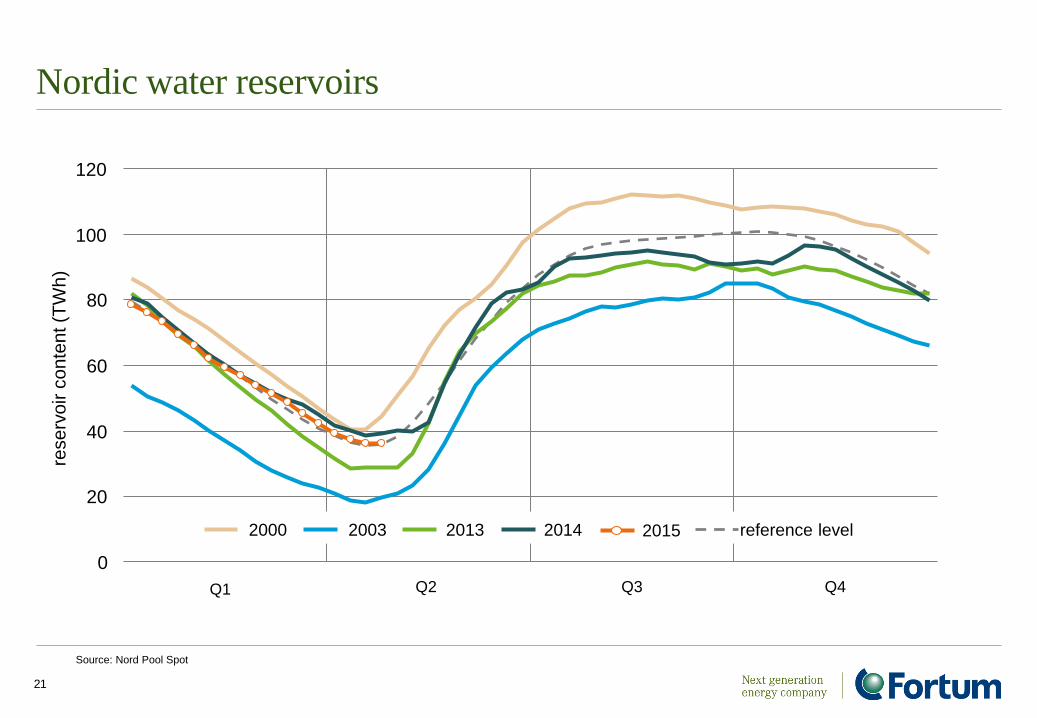

Nordic water reservoirs

21

Source: Nord Pool Spot

Q1 Q2 Q3 Q4

20

40

60

80

100

120

rese

rvo

ir c

on

ten

t (T

Wh

)

0

2000 2003 2014 2013 reference level 2015

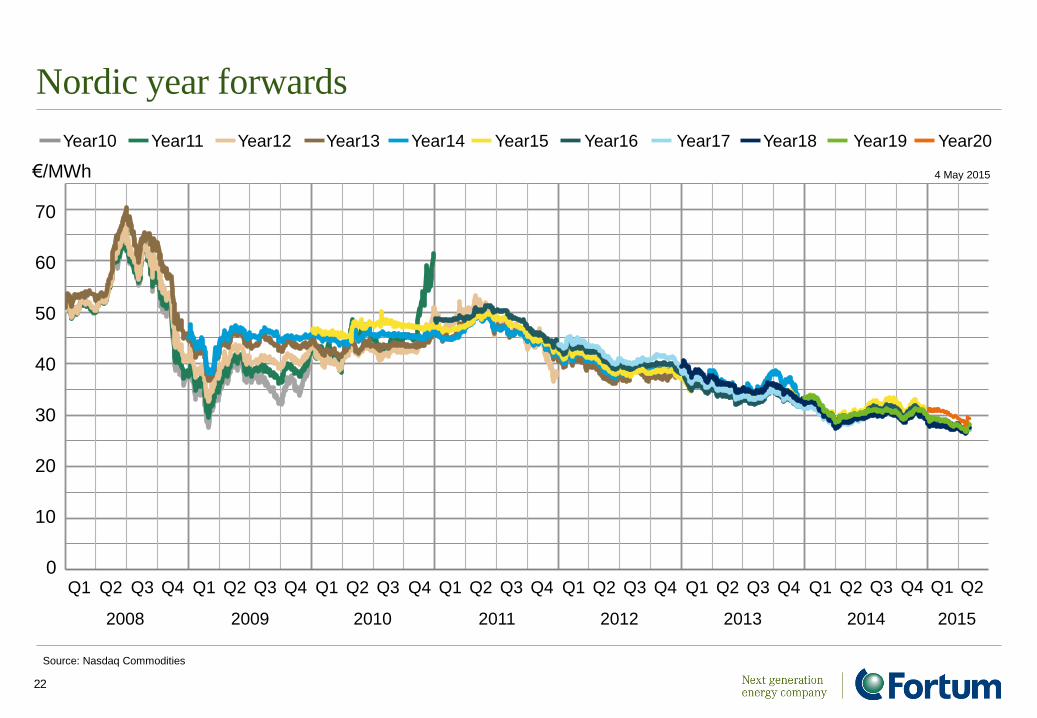

Nordic year forwards

22

Source: Nasdaq Commodities

0

10

20

30

40

50

60

70

€/MWh 4 May 2015

Year15 Year17 Year19 Year10 Year11 Year12 Year13 Year14 Year16 Year18 Year20

2014

Q1

2008

Q2 Q3 Q4 Q1

2009

Q2 Q3 Q4 Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3 Q4 Q1

2012

Q2 Q3 Q4 Q1

2013

Q2 Q3 Q4 Q1 Q2 Q3 Q4

2015

Q1 Q2

0

10

20

30

40

50

60

70

80

90

100

110

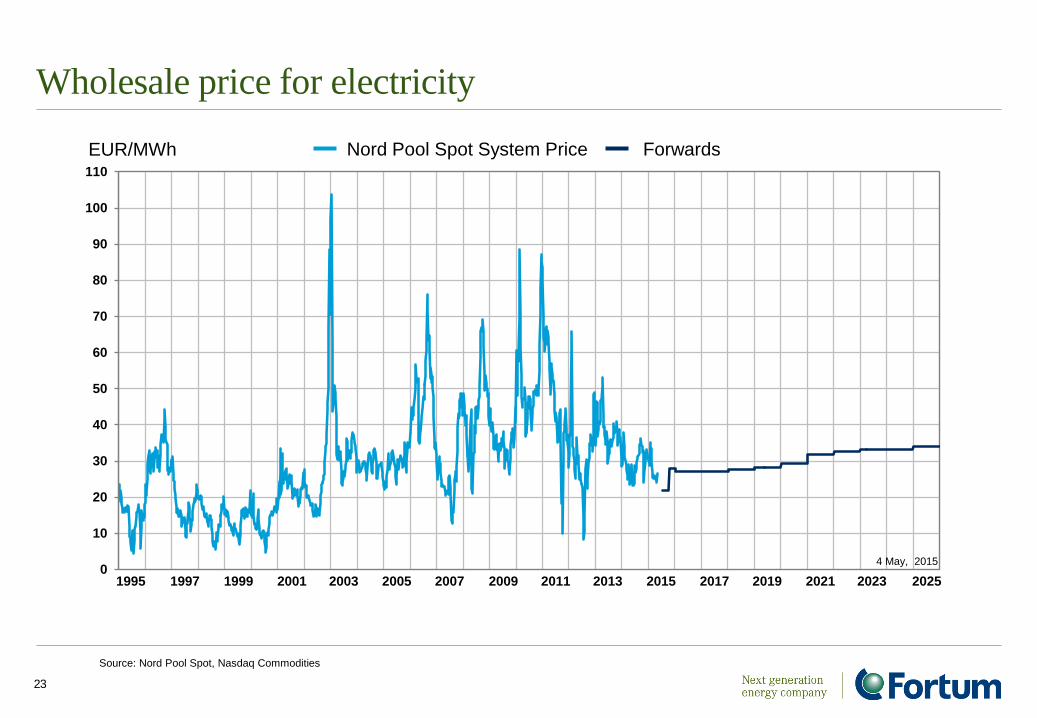

Wholesale price for electricity

23

Source: Nord Pool Spot, Nasdaq Commodities

EUR/MWh Nord Pool Spot System Price Forwards

4 May, 2015

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

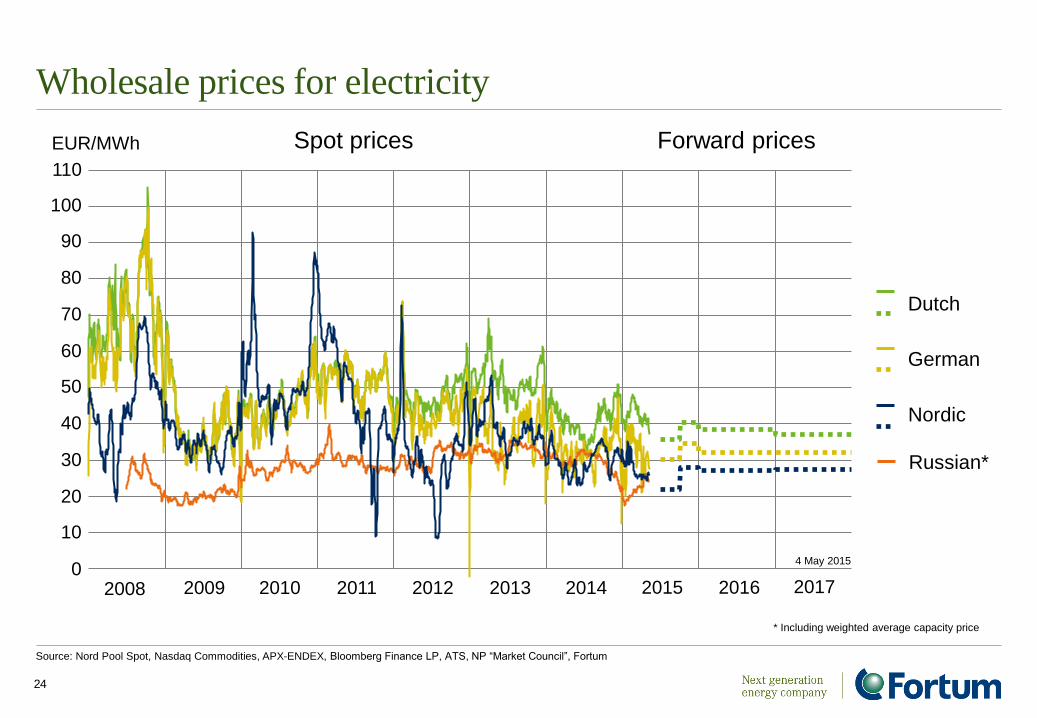

Wholesale prices for electricity

24

Source: Nord Pool Spot, Nasdaq Commodities, APX-ENDEX, Bloomberg Finance LP, ATS, NP “Market Council”, Fortum

* Including weighted average capacity price

Dutch

German

Nordic

Russian*

Spot prices Forward prices EUR/MWh

10

20

30

40

50

60

70

80

90

100

110

0 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

4 May 2015

0

30

60

90

120

150

US

D /

bb

l

Crude oil price (ICE Brent)

2007 2008 20112009 2010 20132012 2014 2015 20160

7

14

21

28

35

EU

R /

tC

O2

CO2 price (ICE ECX EUA)

2007 2008 20112009 2010 20132012 2014 2015 2016

0

50

100

150

200

250

US

D /

t

Coal price (ICE Rotterdam)

2007 2008 20112009 2010 20132012 2014 2015 20160

20

40

60

80

100

GB

p /

th

erm

Gas price (ICE NBP)

2007 2008 20112009 2010 20132012 2014 2015 2016

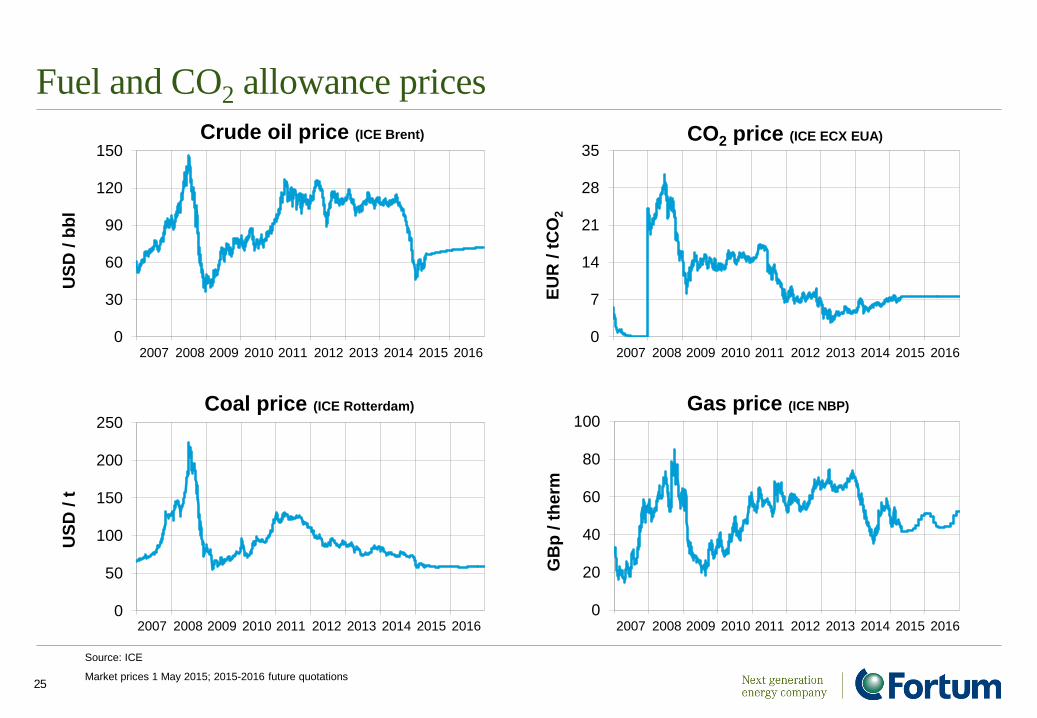

25

Source: ICE

Market prices 1 May 2015; 2015-2016 future quotations

Fuel and CO2 allowance prices

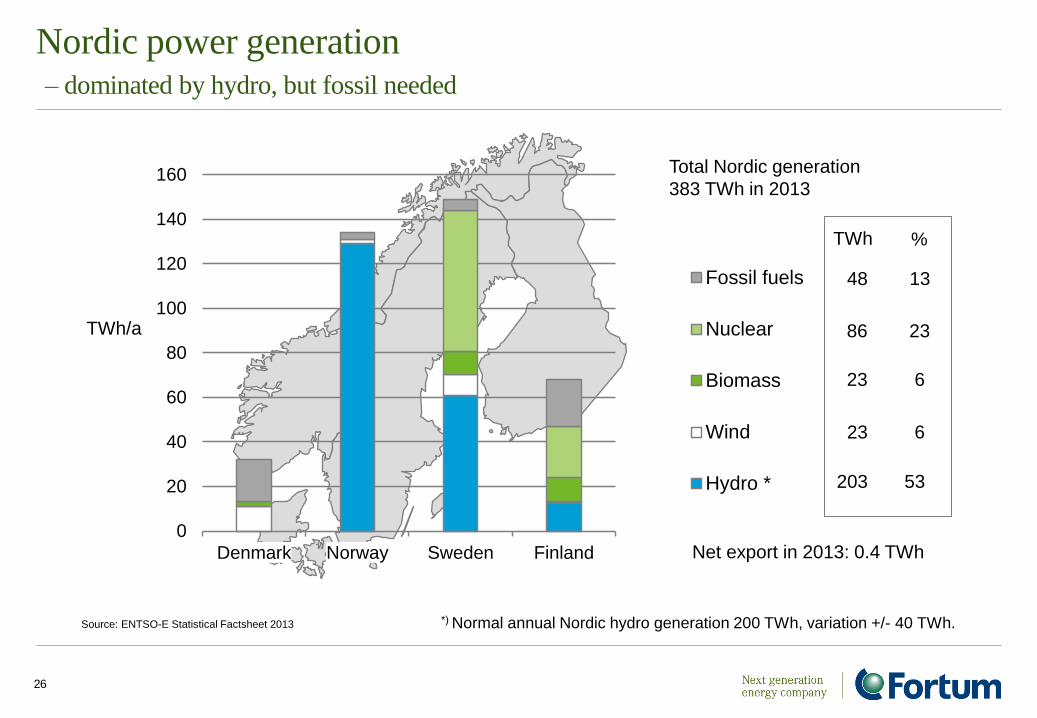

Nordic power generation – dominated by hydro, but fossil needed

26

Source: ENTSO-E Statistical Factsheet 2013 *) Normal annual Nordic hydro generation 200 TWh, variation +/- 40 TWh.

0

20

40

60

80

100

120

140

160

Denmark Norway Sweden Finland

Fossil fuels

Nuclear

Biomass

Wind

Hydro *

TWh/a

Total Nordic generation

383 TWh in 2013

Net export in 2013: 0.4 TWh

23

86

TWh %

48

203

23

6

23

13

53

6

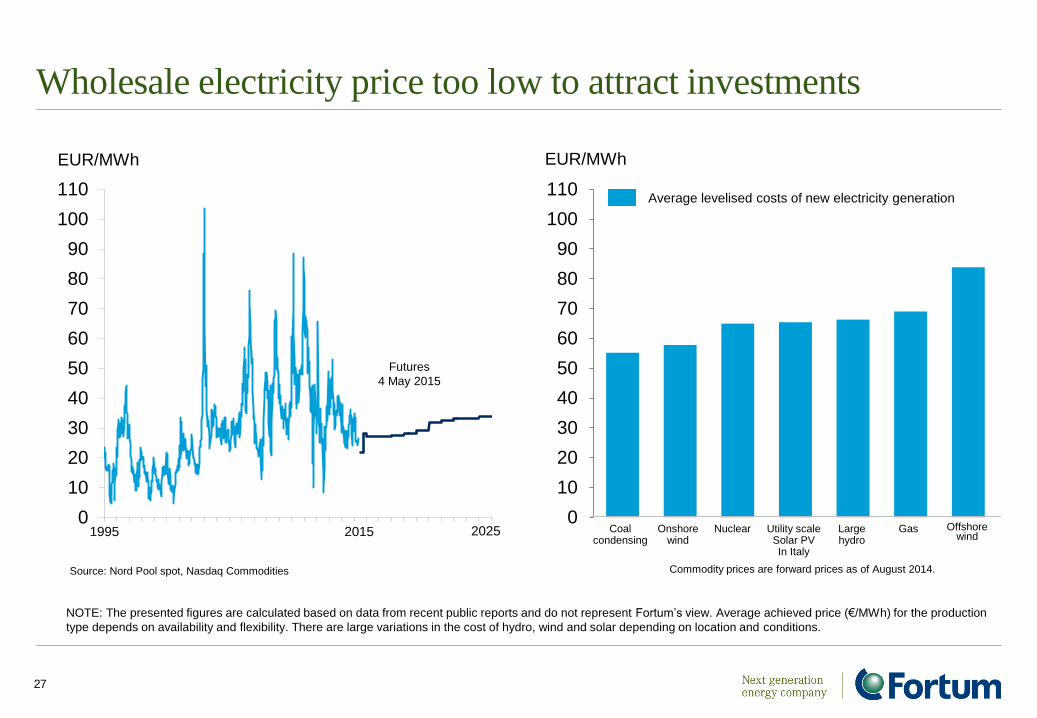

Wholesale electricity price too low to attract investments

27

NOTE: The presented figures are calculated based on data from recent public reports and do not represent Fortum’s view. Average achieved price (€/MWh) for the production

type depends on availability and flexibility. There are large variations in the cost of hydro, wind and solar depending on location and conditions.

0

10

20

30

40

50

60

70

80

90

100

110

Source: Nord Pool spot, Nasdaq Commodities

EUR/MWh

Futures

4 May 2015

1995 2015 2025 0

10

20

30

40

50

60

70

80

90

100

110

Onshore wind

Nuclear Utility scale Solar PV In Italy

Large hydro

Offshore wind

EUR/MWh

Average levelised costs of new electricity generation

Coal condensing

Gas

Commodity prices are forward prices as of August 2014.

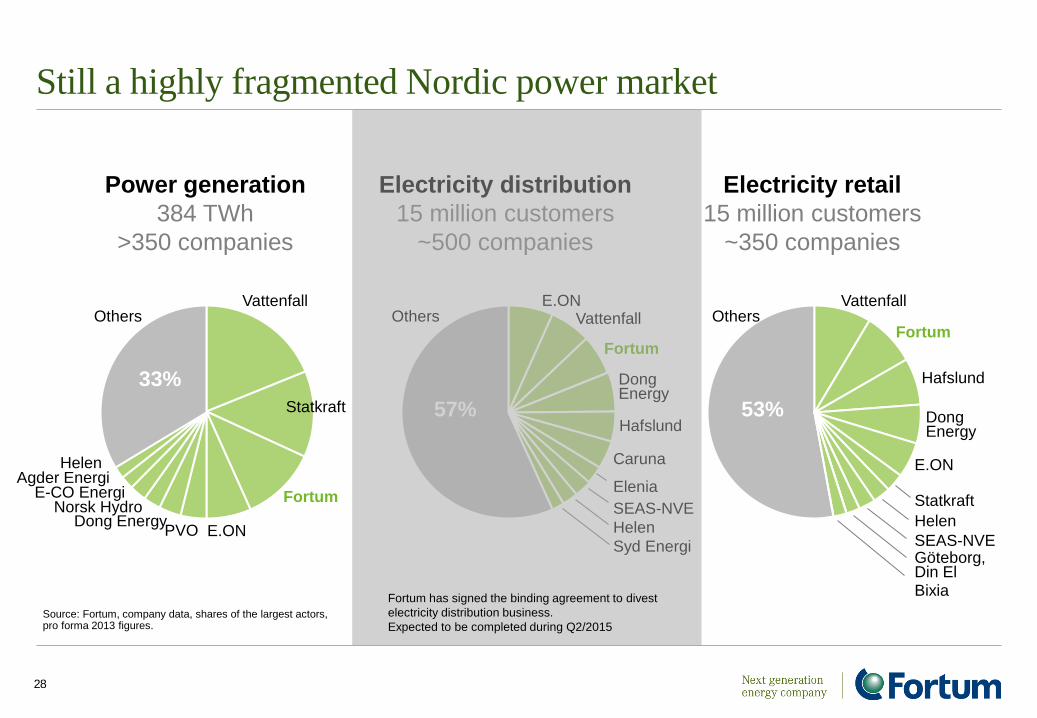

Still a highly fragmented Nordic power market

28

Power generation

384 TWh

>350 companies

Electricity distribution

15 million customers

~500 companies

Electricity retail

15 million customers

~350 companies

Vattenfall

33%

Dong Energy

Others

Fortum

E.ON PVO

E-CO Energi Agder Energi

Norsk Hydro

Helen

Statkraft

Others

53%

Vattenfall

Fortum

Dong Energy

Hafslund

E.ON

Göteborg, Din El

SEAS-NVE

Helen

Statkraft

Bixia

Caruna

Vattenfall

Fortum

Others E.ON

57%

SEAS-NVE

Hafslund

Helen

Syd Energi

Dong Energy

Elenia

Source: Fortum, company data, shares of the largest actors, pro forma 2013 figures.

Fortum has signed the binding agreement to divest

electricity distribution business.

Expected to be completed during Q2/2015

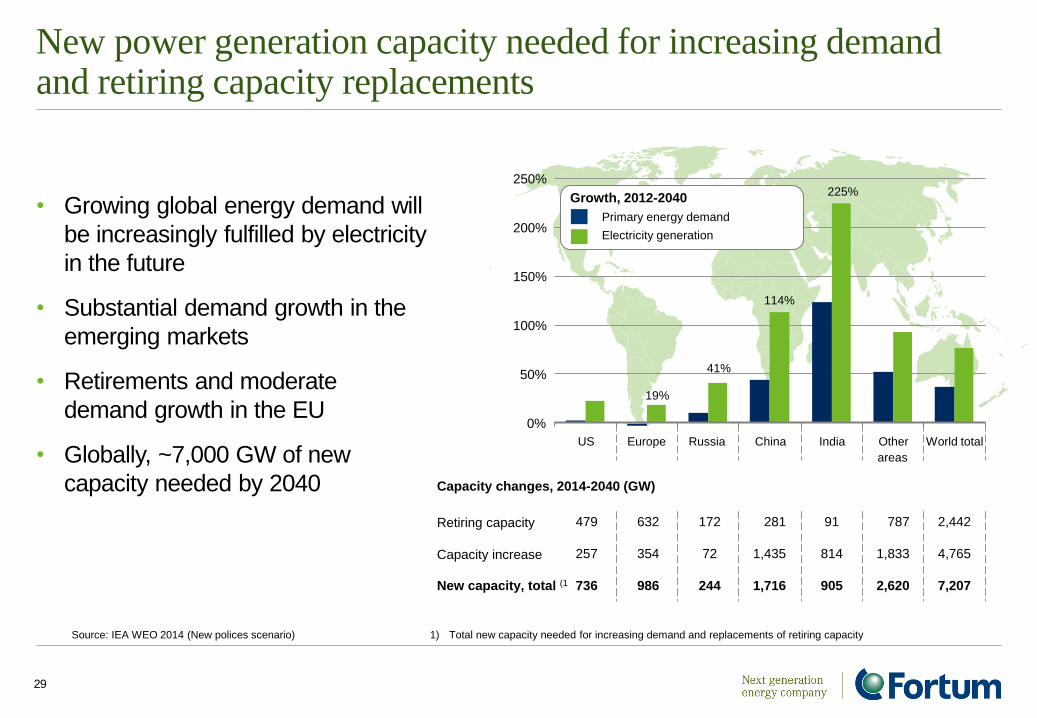

New power generation capacity needed for increasing demand and retiring capacity replacements

29

• Growing global energy demand will

be increasingly fulfilled by electricity

in the future

• Substantial demand growth in the

emerging markets

• Retirements and moderate

demand growth in the EU

• Globally, ~7,000 GW of new

capacity needed by 2040

Source: IEA WEO 2014 (New polices scenario) 1) Total new capacity needed for increasing demand and replacements of retiring capacity

479

257

736

632

354

986

172

72

244

281

1,435

1,716

91

814

905

787

1,833

2,620

2,442

4,765

7,207 New capacity, total (1

Capacity changes, 2014-2040 (GW)

Retiring capacity

Capacity increase

19%

41%

114%

225%

0%

50%

100%

150%

200%

250%

US Europe Russia China India Other

areas

World total

Growth, 2012-2040

Primary energy demand

Electricity generation

Overview of Fortum’s nuclear fleet

30

LOVIISA OLKILUOTO OSKARSHAMN FORSMARK

Commercial operation started

Unit 1: 1977

Unit 2: 1981

Unit 1: 1978

Unit 2: 1980

Unit 3: (Under construction)

Unit 1: 1972

Unit 2: 1974

Unit 3: 1985

Unit 1: 1980

Unit 2: 1981

Unit 3: 1985

Generation Capacity

Fortum’s share

Unit 1: 496 MW

Unit 2: 496 MW

Total: 992 MW

Unit 1: 880 MW

Unit 2: 880 MW

(Unit 3: 1,600 MW)

Total: 1,760 MW (3,360)

27% 468 MW

Unit 1: 473 MW

Unit 2: 638 MW

Unit 3: 1,400 MW

Total: 2,511 MW

43% 1,089 MW

Unit 1: 984 MW

Unit 2: 1,120 MW

Unit 3: 1,170 MW

Total: 3,274 MW

22% 720 MW

Yearly production

Fortum’s share of production

8 TWh

8 TWh

14 TWh

4 TWh

17 TWh

7 TWh

25 TWh

5.5 TWh

Share of Fortums Nordic production

18% 9% 16% 13%

Majority owner

Fortum’s share

Fortum

Pohjolan Voima

26.6%

E.ON

43.4%

Vattenfall

22.2%

Operated by Fortum Teollisuuden Voima (TVO)

OKG Aktiebolag Forsmarks Kraftgrupp

Responsibilities Loviisa: Fortum is the owner, licensee and operator with all the responsibilities specified in the Nuclear Energy Act, Nuclear Liability Act, and other relevant nuclear legislation

Other units: Fortum is solely an owner with none of the responsibilities assigned to the licensee in the nuclear legislation. Other responsibilities are specified in the

Companies Act and the Articles of Association and are mostly financial.

Olkiluoto

Loviisa Forsmark

Oskarshamn

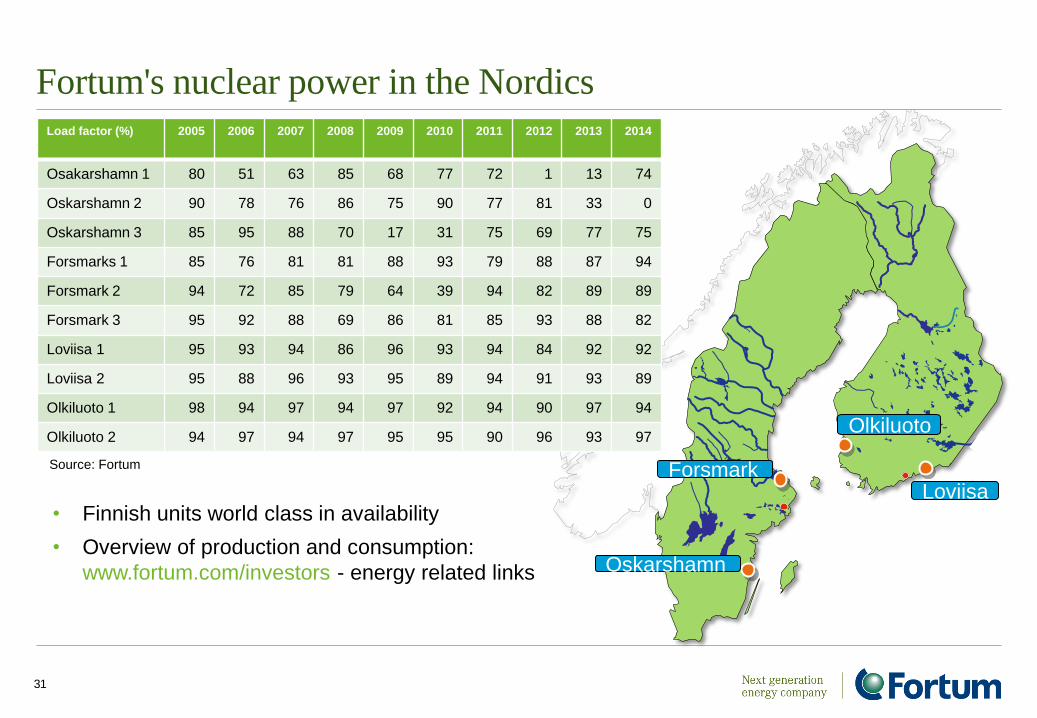

Fortum's nuclear power in the Nordics

31

• Finnish units world class in availability

• Overview of production and consumption:

www.fortum.com/investors - energy related links

Source: Fortum

Load factor (%) 2005 2006 2007 2008 2009 2010 2011 2012 2013

2014

Osakarshamn 1 80 51 63 85 68 77 72 1 13 74

Oskarshamn 2 90 78 76 86 75 90 77 81 33 0

Oskarshamn 3 85 95 88 70 17 31 75 69 77 75

Forsmarks 1 85 76 81 81 88 93 79 88 87 94

Forsmark 2 94 72 85 79 64 39 94 82 89 89

Forsmark 3 95 92 88 69 86 81 85 93 88 82

Loviisa 1 95 93 94 86 96 93 94 84 92 92

Loviisa 2 95 88 96 93 95 89 94 91 93 89

Olkiluoto 1 98 94 97 94 97 92 94 90 97 94

Olkiluoto 2 94 97 94 97 95 95 90 96 93 97

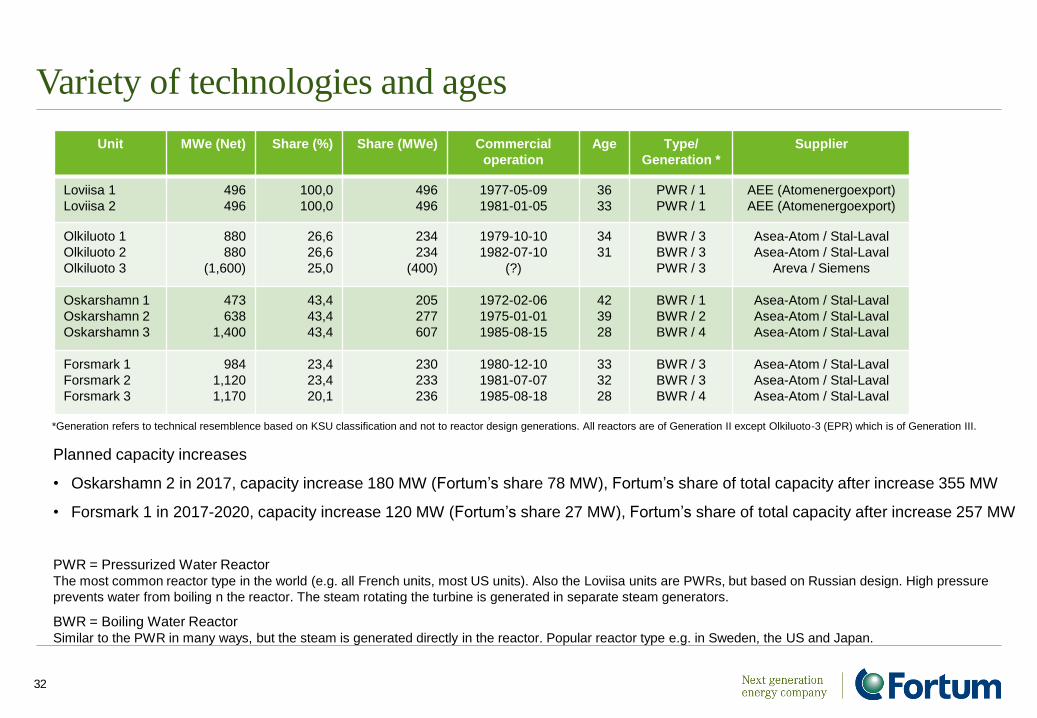

Variety of technologies and ages

32

Planned capacity increases

• Oskarshamn 2 in 2017, capacity increase 180 MW (Fortum’s share 78 MW), Fortum’s share of total capacity after increase 355 MW

• Forsmark 1 in 2017-2020, capacity increase 120 MW (Fortum’s share 27 MW), Fortum’s share of total capacity after increase 257 MW

PWR = Pressurized Water Reactor The most common reactor type in the world (e.g. all French units, most US units). Also the Loviisa units are PWRs, but based on Russian design. High pressure

prevents water from boiling n the reactor. The steam rotating the turbine is generated in separate steam generators.

BWR = Boiling Water Reactor Similar to the PWR in many ways, but the steam is generated directly in the reactor. Popular reactor type e.g. in Sweden, the US and Japan.

*Generation refers to technical resemblence based on KSU classification and not to reactor design generations. All reactors are of Generation II except Olkiluoto-3 (EPR) which is of Generation III.

Unit MWe (Net) Share (%) Share (MWe) Commercial

operation

Age Type/

Generation *

Supplier

Loviisa 1

Loviisa 2

496

496

100,0

100,0

496

496

1977-05-09

1981-01-05

36

33

PWR / 1

PWR / 1

AEE (Atomenergoexport)

AEE (Atomenergoexport)

Olkiluoto 1

Olkiluoto 2

Olkiluoto 3

880

880

(1,600)

26,6

26,6

25,0

234

234

(400)

1979-10-10

1982-07-10

(?)

34

31

BWR / 3

BWR / 3

PWR / 3

Asea-Atom / Stal-Laval

Asea-Atom / Stal-Laval

Areva / Siemens

Oskarshamn 1

Oskarshamn 2

Oskarshamn 3

473

638

1,400

43,4

43,4

43,4

205

277

607

1972-02-06

1975-01-01

1985-08-15

42

39

28

BWR / 1

BWR / 2

BWR / 4

Asea-Atom / Stal-Laval

Asea-Atom / Stal-Laval

Asea-Atom / Stal-Laval

Forsmark 1

Forsmark 2

Forsmark 3

984

1,120

1,170

23,4

23,4

20,1

230

233

236

1980-12-10

1981-07-07

1985-08-18

33

32

28

BWR / 3

BWR / 3

BWR / 4

Asea-Atom / Stal-Laval

Asea-Atom / Stal-Laval

Asea-Atom / Stal-Laval

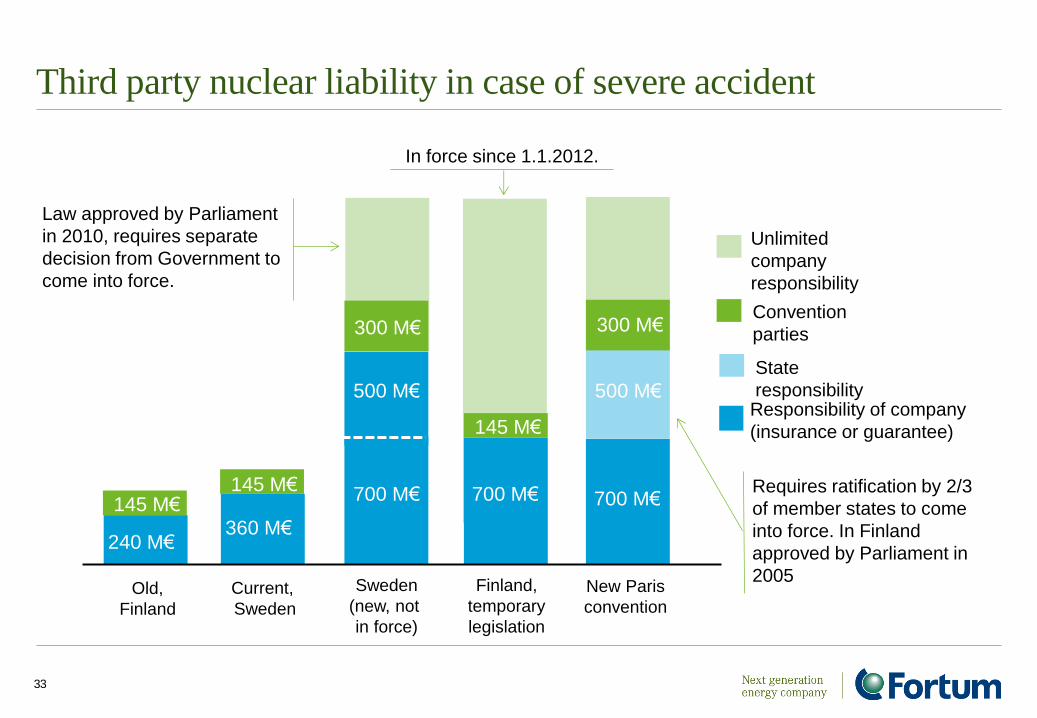

Third party nuclear liability in case of severe accident

33

Sweden

(new, not

in force)

Finland,

temporary

legislation

Current,

Sweden

700 M€

200 M€ 360 M€

500 M€ Responsibility of company

(insurance or guarantee)

Unlimited

company

responsibility

Convention

parties 300 M€

State

responsibility

300 M€

500 M€

700 M€

New Paris

convention

700 M€

145 M€

145 M€

Old,

Finland

240 M€

145 M€

In force since 1.1.2012.

Law approved by Parliament

in 2010, requires separate

decision from Government to

come into force.

Requires ratification by 2/3

of member states to come

into force. In Finland

approved by Parliament in

2005

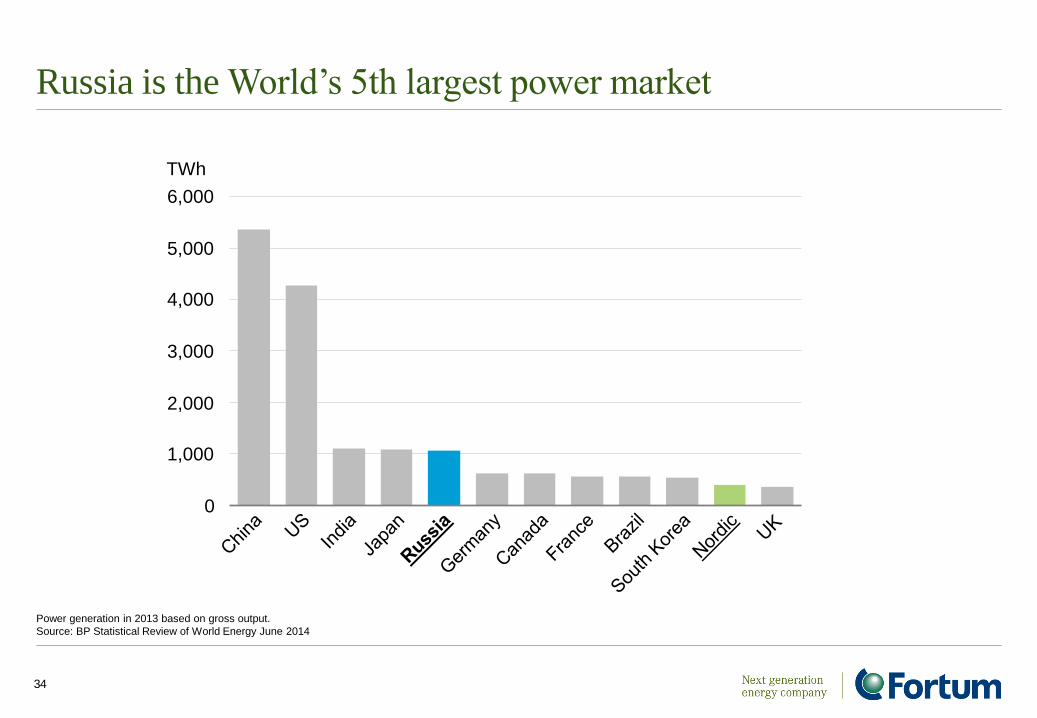

Russia is the World’s 5th largest power market

34

Power generation in 2013 based on gross output.

Source: BP Statistical Review of World Energy June 2014

0

1,000

2,000

3,000

4,000

5,000

6,000

TWh

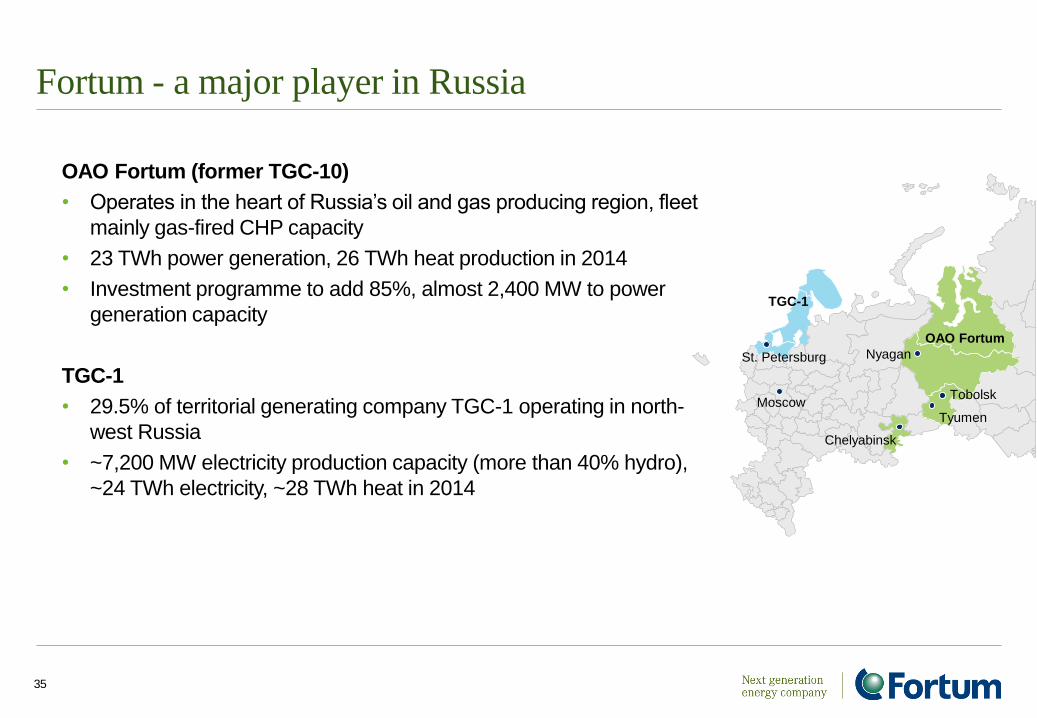

Fortum - a major player in Russia

OAO Fortum (former TGC-10)

• Operates in the heart of Russia’s oil and gas producing region, fleet

mainly gas-fired CHP capacity

• 23 TWh power generation, 26 TWh heat production in 2014

• Investment programme to add 85%, almost 2,400 MW to power

generation capacity

TGC-1

• 29.5% of territorial generating company TGC-1 operating in north-

west Russia

• ~7,200 MW electricity production capacity (more than 40% hydro),

~24 TWh electricity, ~28 TWh heat in 2014

35

OAO Fortum

Tyumen

Tobolsk

Chelyabinsk

Nyagan

TGC-1

St. Petersburg

Moscow

36

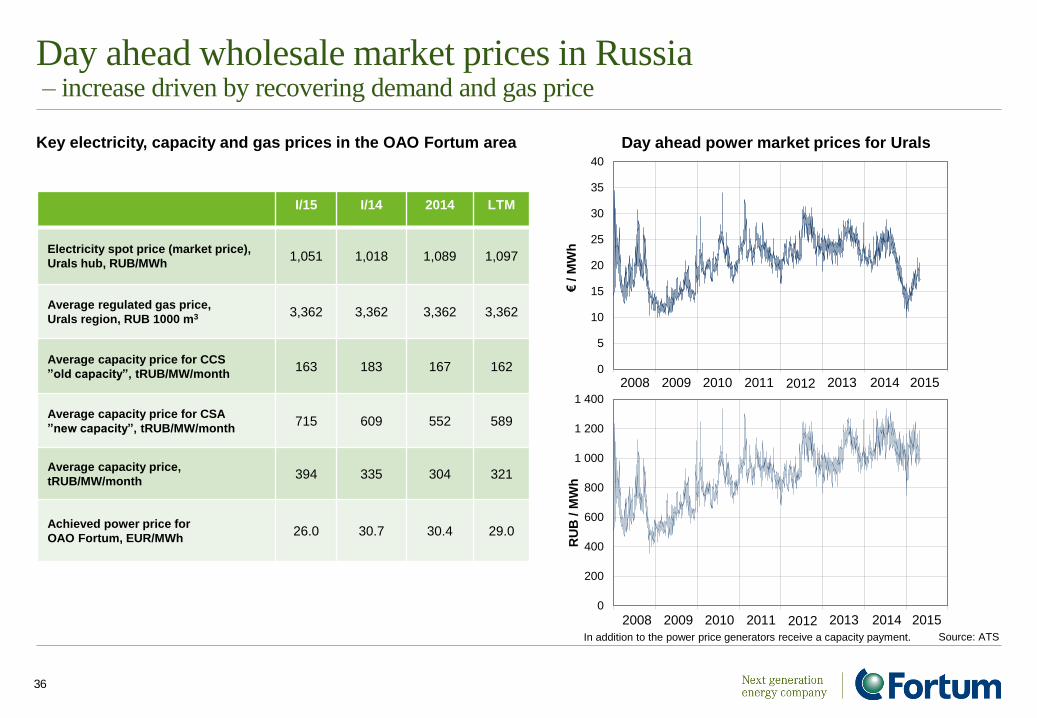

Day ahead wholesale market prices in Russia – increase driven by recovering demand and gas price

Key electricity, capacity and gas prices in the OAO Fortum area

0

200

400

600

800

1 000

1 200

1 400

RU

B / M

Wh

0

5

10

15

20

25

30

35

40

€/

MW

h

In addition to the power price generators receive a capacity payment. Source: ATS

2008 2009 2010 2011 2012 2013 2014 2015

Day ahead power market prices for Urals

2008 2009 2010 2011 2012 2013 2014 2015

I/15 I/14 2014 LTM

Electricity spot price (market price),

Urals hub, RUB/MWh 1,051 1,018 1,089 1,097

Average regulated gas price,

Urals region, RUB 1000 m3 3,362 3,362 3,362 3,362

Average capacity price for CCS

”old capacity”, tRUB/MW/month 163 183 167 162

Average capacity price for CSA

”new capacity”, tRUB/MW/month 715 609 552 589

Average capacity price,

tRUB/MW/month 394 335 304 321

Achieved power price for

OAO Fortum, EUR/MWh 26.0 30.7 30.4 29.0

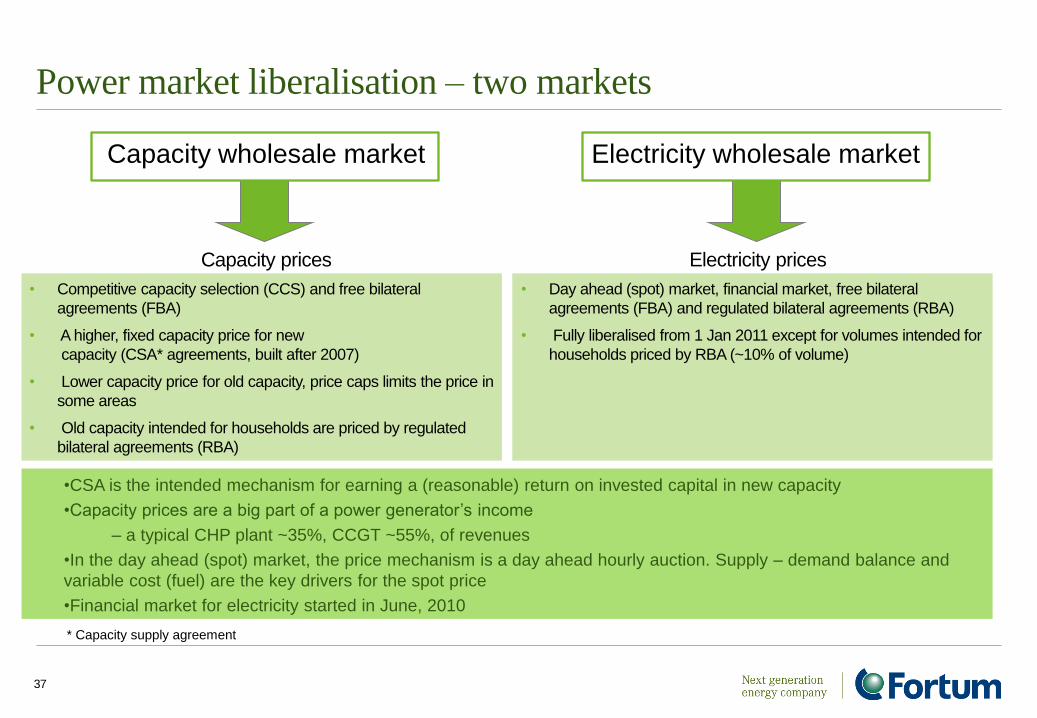

Power market liberalisation – two markets

37

Capacity wholesale market Electricity wholesale market

Capacity prices

• Competitive capacity selection (CCS) and free bilateral

agreements (FBA)

• A higher, fixed capacity price for new

capacity (CSA* agreements, built after 2007)

• Lower capacity price for old capacity, price caps limits the price in

some areas

• Old capacity intended for households are priced by regulated

bilateral agreements (RBA)

Electricity prices

• Day ahead (spot) market, financial market, free bilateral

agreements (FBA) and regulated bilateral agreements (RBA)

• Fully liberalised from 1 Jan 2011 except for volumes intended for

households priced by RBA (~10% of volume)

* Capacity supply agreement

•CSA is the intended mechanism for earning a (reasonable) return on invested capital in new capacity

•Capacity prices are a big part of a power generator’s income

– a typical CHP plant ~35%, CCGT ~55%, of revenues

•In the day ahead (spot) market, the price mechanism is a day ahead hourly auction. Supply – demand balance and

variable cost (fuel) are the key drivers for the spot price

•Financial market for electricity started in June, 2010

38

Capacity prices for new capacity considerably higher than prices for old capacity prices

• Long term rules and price parameters approved

• Both “old” and “new” capacity can participate in capacity auctions

• Old capacity (pre 2007) and new capacity priced differently – Old capacity is priced by capacity auctions; price cap possibility

– New capacity under capacity supply agreements to receive guaranteed payments

• The payments for new capacity are based on approved pricing formulas – Vary according to plant size, fuel, geographic location, capital costs

– Allow the recovery of capital costs and include return on invested capital; the targeted ROCE level 12-14% (with current government benchmark bond yields)

– After three years (2014), the regulator will review the earnings from the electricity-only market and can revise the payments, same goes after 6 years.

“Old” capacity prices will depend on auction outcomes, but will likely remain

relatively low; potentially price caps could limit the price

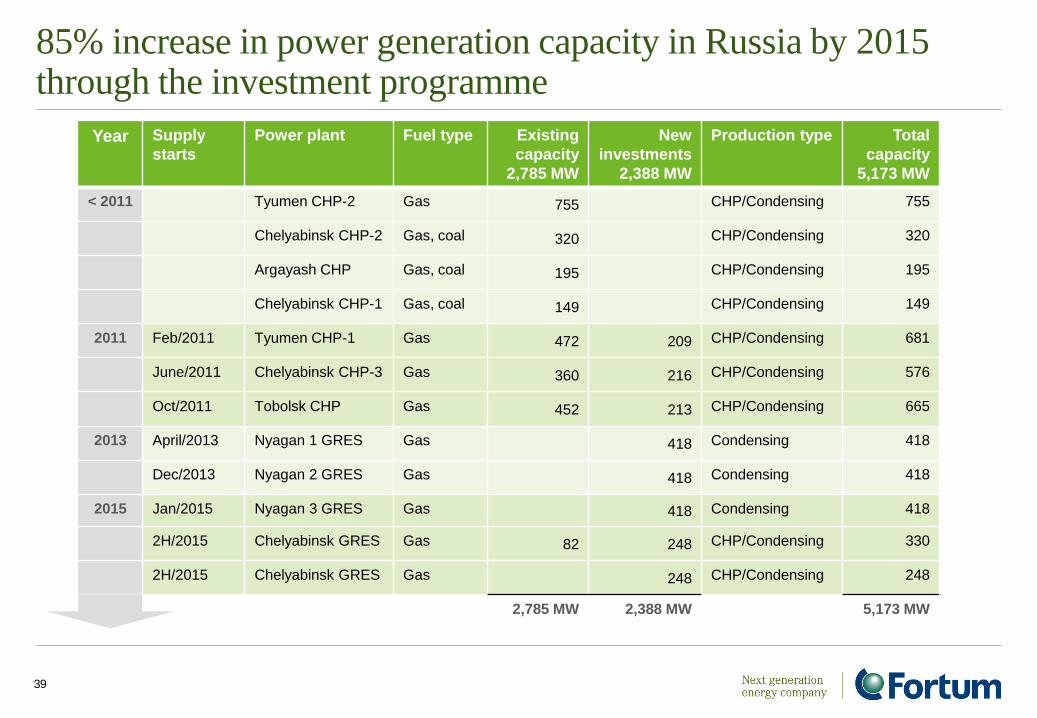

85% increase in power generation capacity in Russia by 2015 through the investment programme

39

Year Supply

starts

Power plant Fuel type Existing

capacity

2,785 MW

New

investments

2,388 MW

Production type Total

capacity

5,173 MW

< 2011 Tyumen CHP-2 Gas 755 CHP/Condensing 755

Chelyabinsk CHP-2 Gas, coal 320 CHP/Condensing 320

Argayash CHP Gas, coal 195 CHP/Condensing 195

Chelyabinsk CHP-1 Gas, coal 149 CHP/Condensing 149

2011 Feb/2011 Tyumen CHP-1 Gas 472 209 CHP/Condensing 681

June/2011 Chelyabinsk CHP-3 Gas 360 216 CHP/Condensing 576

Oct/2011 Tobolsk CHP Gas 452 213 CHP/Condensing 665

2013 April/2013 Nyagan 1 GRES Gas 418 Condensing 418

Dec/2013 Nyagan 2 GRES Gas 418 Condensing 418

2015 Jan/2015 Nyagan 3 GRES Gas 418 Condensing 418

2H/2015 Chelyabinsk GRES Gas 82 248 CHP/Condensing 330

2H/2015 Chelyabinsk GRES Gas 248 CHP/Condensing 248

2,785 MW 2,388 MW 5,173 MW

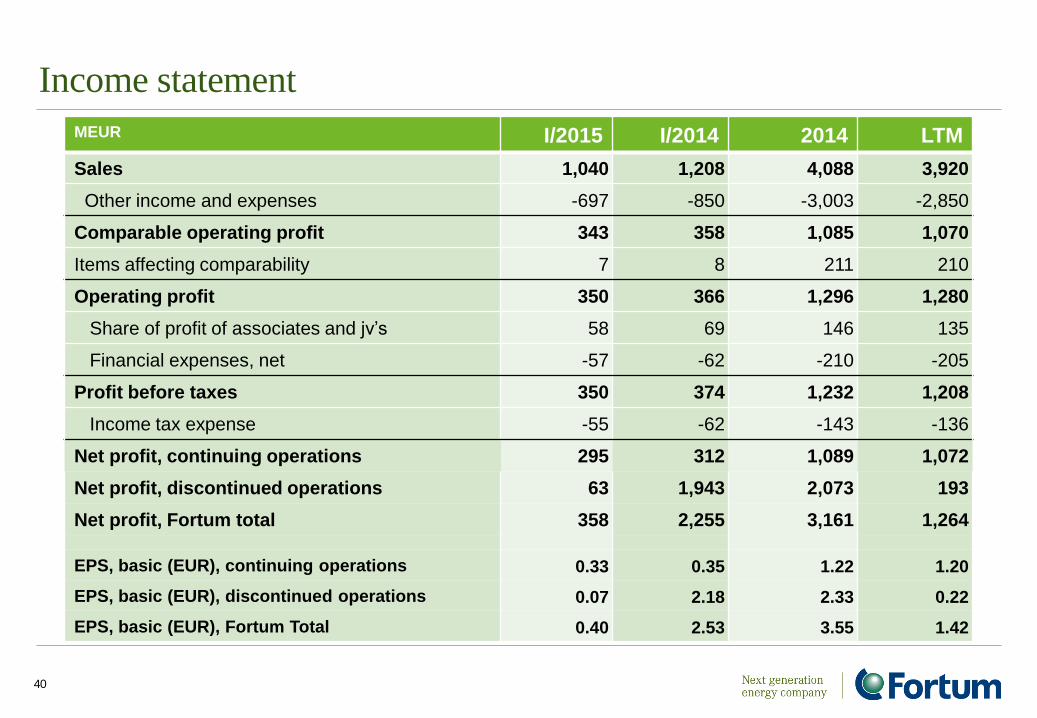

Income statement

MEUR I/2015 I/2014 2014 LTM

Sales 1,040 1,208 4,088 3,920

Other income and expenses -697 -850 -3,003 -2,850

Comparable operating profit 343 358 1,085 1,070

Items affecting comparability 7 8 211 210

Operating profit 350 366 1,296 1,280

Share of profit of associates and jv’s 58 69 146 135

Financial expenses, net -57 -62 -210 -205

Profit before taxes 350 374 1,232 1,208

Income tax expense -55 -62 -143 -136

Net profit, continuing operations 295 312 1,089 1,072

Net profit, discontinued operations 63 1,943 2,073 193

Net profit, Fortum total 358 2,255 3,161 1,264

EPS, basic (EUR), continuing operations 0.33 0.35 1.22 1.20

EPS, basic (EUR), discontinued operations 0.07 2.18 2.33 0.22

EPS, basic (EUR), Fortum Total 0.40 2.53 3.55 1.42

40

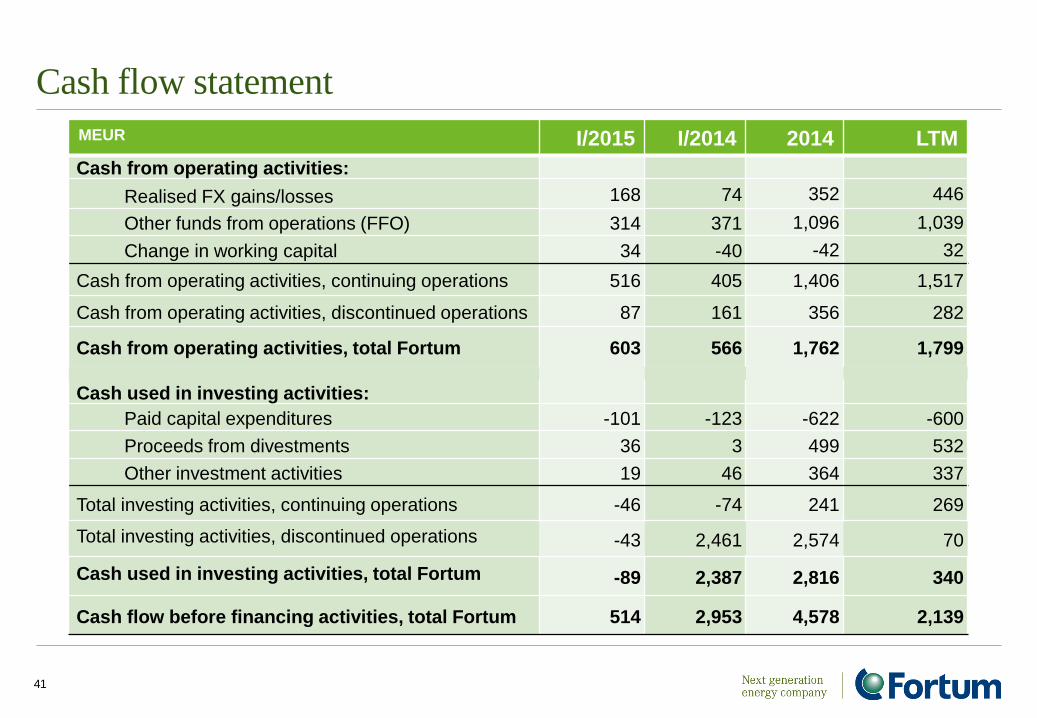

Cash flow statement

MEUR I/2015 I/2014 2014 LTM

Cash from operating activities:

Realised FX gains/losses 168 74 352 446

Other funds from operations (FFO) 314 371 1,096 1,039

Change in working capital 34 -40 -42 32

Cash from operating activities, continuing operations 516 405 1,406 1,517

Cash from operating activities, discontinued operations 87 161 356 282

Cash from operating activities, total Fortum 603 566 1,762 1,799

Cash used in investing activities:

Paid capital expenditures -101 -123 -622 -600

Proceeds from divestments 36 3 499 532

Other investment activities 19 46 364 337

Total investing activities, continuing operations -46 -74 241 269

Total investing activities, discontinued operations

-43 2,461 2,574 70

Cash used in investing activities, total Fortum

-89 2,387 2,816 340

Cash flow before financing activities, total Fortum 514 2,953 4,578 2,139

41

Key ratios

MEUR LTM 2014

Comparable EBITDA, continuing operations 1,397 1,457

Comparable EBITDA, total Fortum 1,754 1,873

Interest-bearing net debt, total Fortum 3,714 4,217

Comparable net debt/EBITDA, total Fortum 2.1 2.3

excluding Värme financing 1.8 2.0

42

ROCE % Return on capital employed, total Fortum 9.0 19.5

Good liquidity – committed credit lines total EUR 2.2 billion

Debt Maturity Profile 31 March 2015

0

250

500

750

1000

1250

1500

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025+

Bonds Financial institutions Other long-term debt Other short-term debt

MEUR

2015 1,036

2016 863

2017 538

2018 621

2019 821

2020 75

2021 549

2022 1,087

2023 110

2024 3

2025+ 1,279

TOTAL 6,982

43

per 31 March 2015 per 31 Dec, 2014

Average Interest Rate 4.3% 3.7%

Portion of floating / fixed debt 47 / 53% 46 / 54%

Outlook

Nordic markets

• Fortum continues to expect that the average annual electricity demand

growth will be on average approximately 0.5% in the coming years

• Electricity is expected to continue to gain share of total energy consumption

Russia

• The run-rate operating profit (EBIT) level for the Russia Segment, RUB 18.2

billion, is targeted to be reached during 2015, but the euro result level will be

volatile, due to the translation effect

Key drivers and risks

• Economic

• Political

• Currency

• Wholesale price of electricity and volumes

• demand and supply • fuels

• hydrological situation • power plant availability

• CO2 emissions allowance prices

44

Outlook

Annual capex estimate, excluding potential acquisitions

• 2015 approximately EUR 0.8 billion

Hedging

• Rest of 2015 approx. 50% hedge ratio at approx. EUR 41/MWh

• 2016 approx. 20% hedge ratio at approx. EUR 37/MWh

Taxation

• Effective tax rate for 2015 for the Group 19-21%

• The Swedish Government decided to re-propose an increase of 17%

on the tax on installed nuclear capacity to the spring budget

45

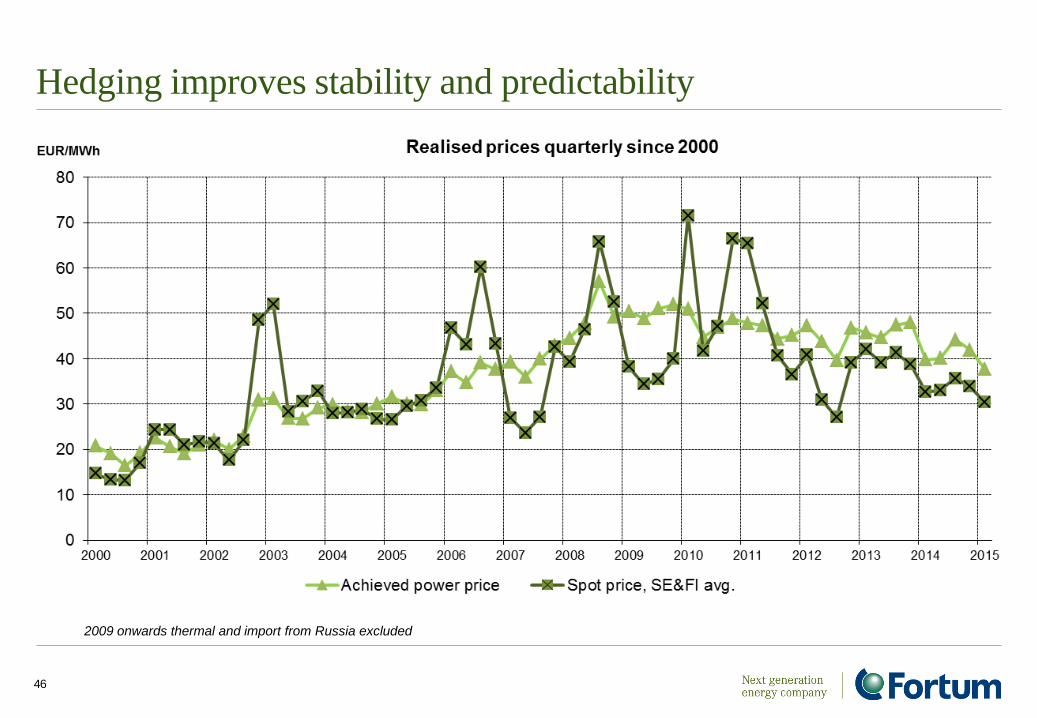

Hedging improves stability and predictability

46

2009 onwards thermal and import from Russia excluded

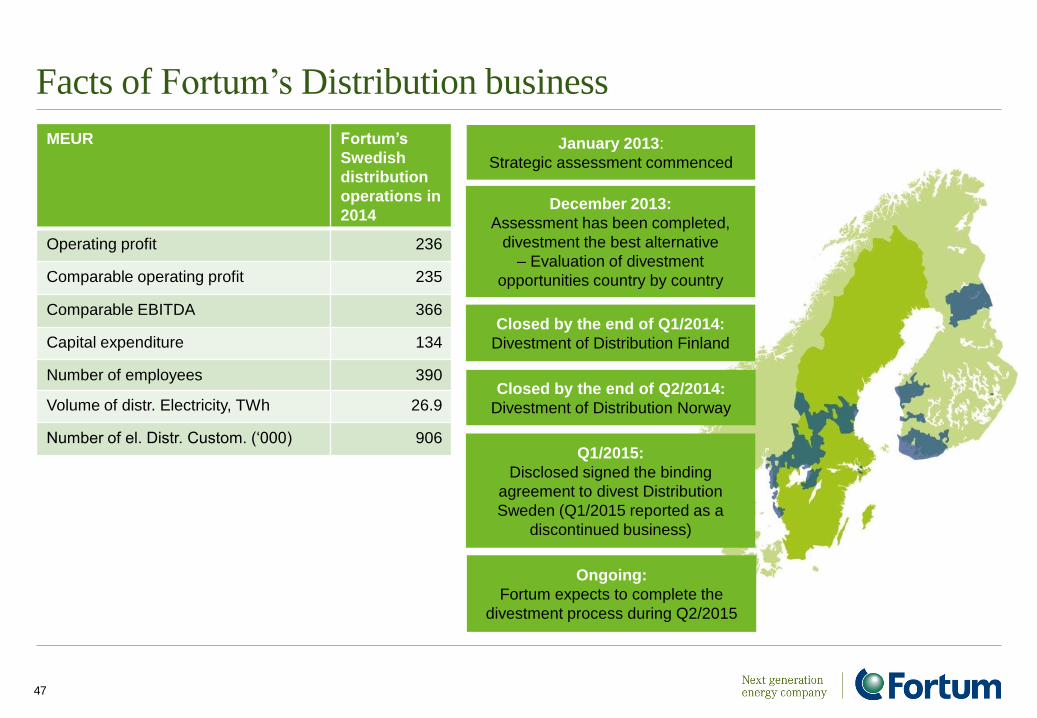

Facts of Fortum’s Distribution business

MEUR Fortum’s

Swedish

distribution

operations in

2014

Operating profit 236

Comparable operating profit 235

Comparable EBITDA 366

Capital expenditure 134

Number of employees 390

Volume of distr. Electricity, TWh 26.9

Number of el. Distr. Custom. (‘000) 906

47

January 2013:

Strategic assessment commenced

December 2013:

Assessment has been completed,

divestment the best alternative

– Evaluation of divestment

opportunities country by country

Closed by the end of Q1/2014:

Divestment of Distribution Finland

Q1/2015:

Disclosed signed the binding

agreement to divest Distribution

Sweden (Q1/2015 reported as a

discontinued business)

Closed by the end of Q2/2014:

Divestment of Distribution Norway

Ongoing:

Fortum expects to complete the

divestment process during Q2/2015

For more information, please visit www.fortum.com/investors