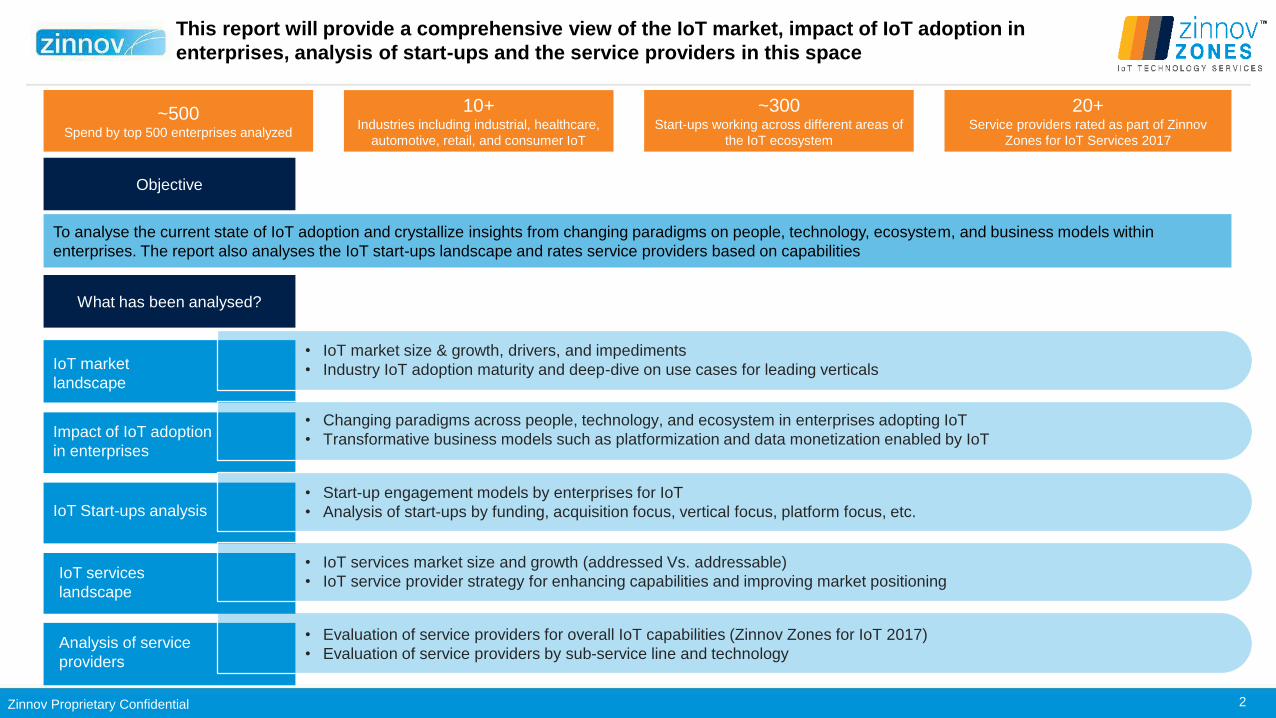

zinnov zones 2017 · 2018-04-27 · zinnov proprietary confidential 2 ~300 start-ups working across...

TRANSCRIPT

Zinnov Proprietary Confidential 1

This document is solely for the use of Zinnov Client and Zinnov Personnel only. No part of it may be quoted, circulated or reproduced for the distribution outside the client organization

without prior written approval from Zinnov

REDACTED VERSION

Zinnov Zones 2017 IoT Technology Services

zinnovzones.com

Zinnov Proprietary Confidential 2

~300Start-ups working across different areas of

the IoT ecosystem

20+Service providers rated as part of Zinnov

Zones for IoT Services 2017

~500Spend by top 500 enterprises analyzed

10+Industries including industrial, healthcare,

automotive, retail, and consumer IoT

Objective

To analyse the current state of IoT adoption and crystallize insights from changing paradigms on people, technology, ecosystem, and business models within

enterprises. The report also analyses the IoT start-ups landscape and rates service providers based on capabilities

This report will provide a comprehensive view of the IoT market, impact of IoT adoption in

enterprises, analysis of start-ups and the service providers in this space

What has been analysed?

IoT market

landscape

Impact of IoT adoption

in enterprises

IoT Start-ups analysis

IoT services

landscape

Analysis of service

providers

• IoT market size & growth, drivers, and impediments

• Industry IoT adoption maturity and deep-dive on use cases for leading verticals

• Changing paradigms across people, technology, and ecosystem in enterprises adopting IoT

• Transformative business models such as platformization and data monetization enabled by IoT

• Start-up engagement models by enterprises for IoT

• Analysis of start-ups by funding, acquisition focus, vertical focus, platform focus, etc.

• IoT services market size and growth (addressed Vs. addressable)

• IoT service provider strategy for enhancing capabilities and improving market positioning

• Evaluation of service providers for overall IoT capabilities (Zinnov Zones for IoT 2017)

• Evaluation of service providers by sub-service line and technology

Zinnov Proprietary Confidential 3

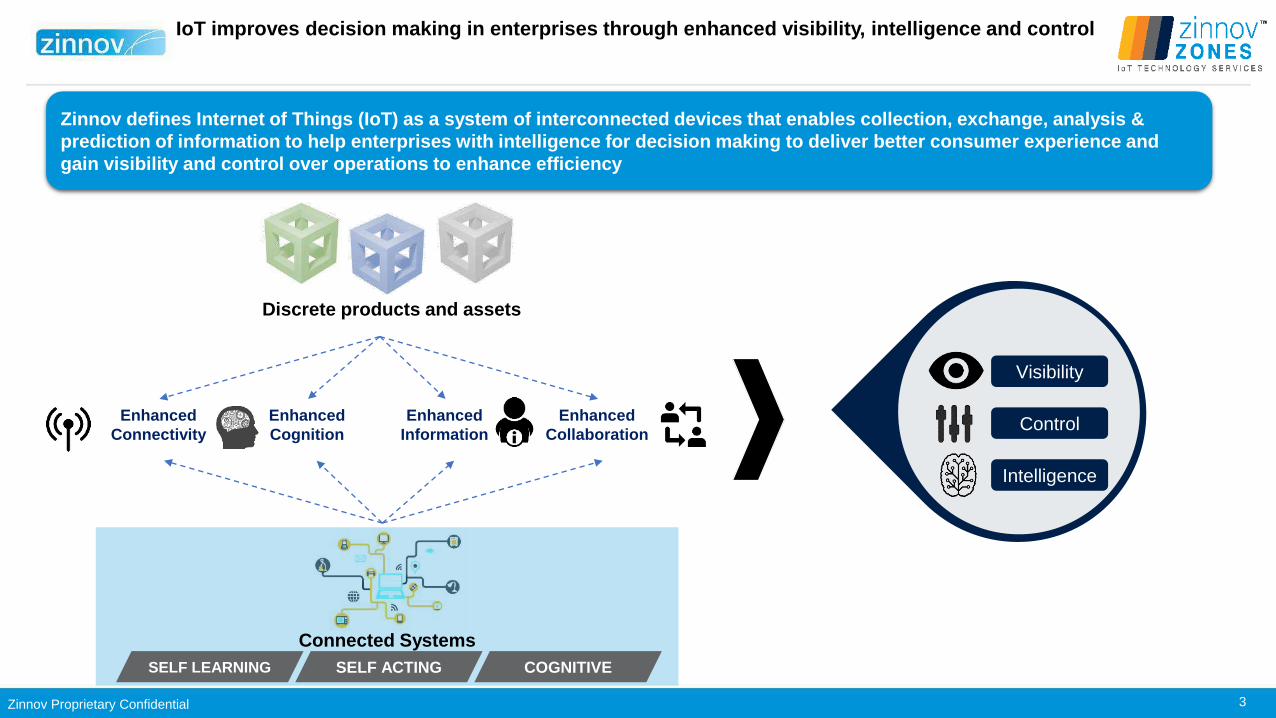

IoT improves decision making in enterprises through enhanced visibility, intelligence and control

Enhanced

Connectivity

Enhanced

Cognition

Enhanced

Information

Enhanced

Collaboration

Connected Systems

Discrete products and assets

SELF LEARNING COGNITIVESELF ACTING

Zinnov defines Internet of Things (IoT) as a system of interconnected devices that enables collection, exchange, analysis &

prediction of information to help enterprises with intelligence for decision making to deliver better consumer experience and

gain visibility and control over operations to enhance efficiency

Visibility

Control

Intelligence

Zinnov Proprietary Confidential 4

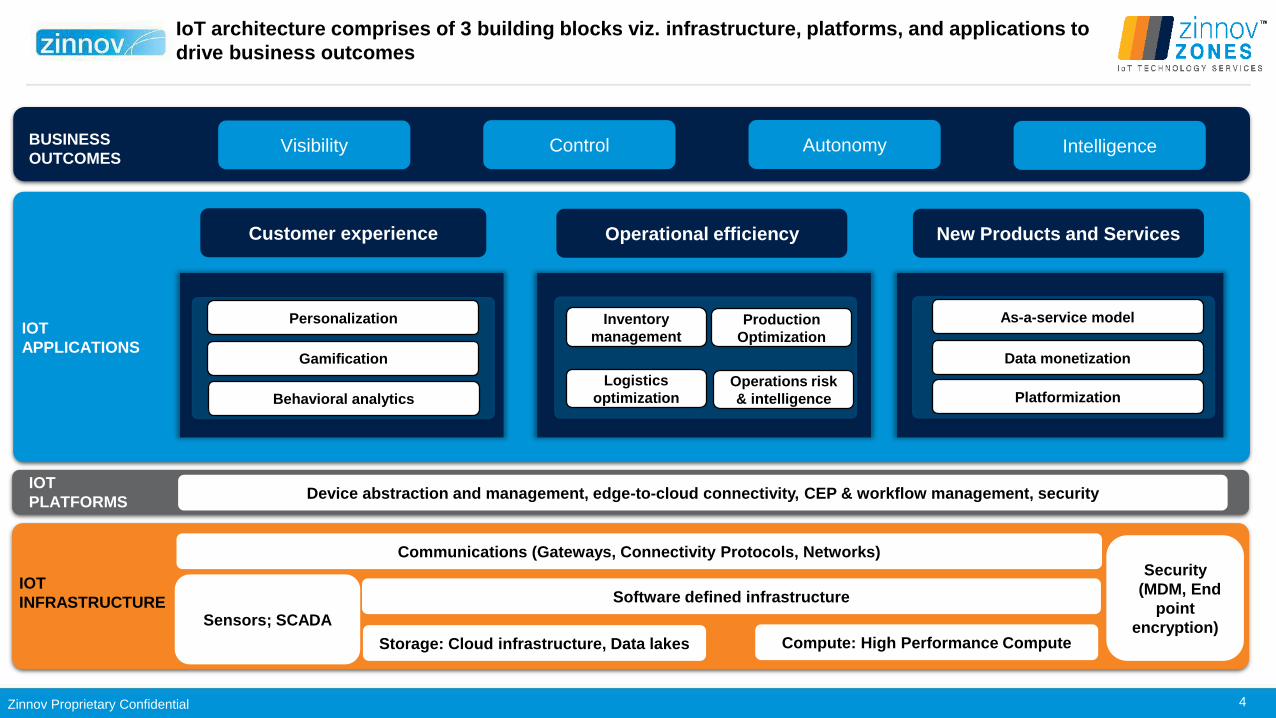

IoT architecture comprises of 3 building blocks viz. infrastructure, platforms, and applications to

drive business outcomes

IOT

APPLICATIONS

IOT

INFRASTRUCTURE

Personalization

Gamification

Inventory

management

Logistics

optimization

As-a-service model

Data monetization

BUSINESS

OUTCOMESVisibility Control IntelligenceAutonomy

IOT

PLATFORMS

Customer experience Operational efficiency New Products and Services

Device abstraction and management, edge-to-cloud connectivity, CEP & workflow management, security

Communications (Gateways, Connectivity Protocols, Networks)

Sensors; SCADA

Software defined infrastructure

Storage: Cloud infrastructure, Data lakes Compute: High Performance Compute

Security

(MDM, End

point

encryption)

Behavioral analytics

Production

Optimization

Operations risk

& intelligence Platformization

Zinnov Proprietary Confidential 5

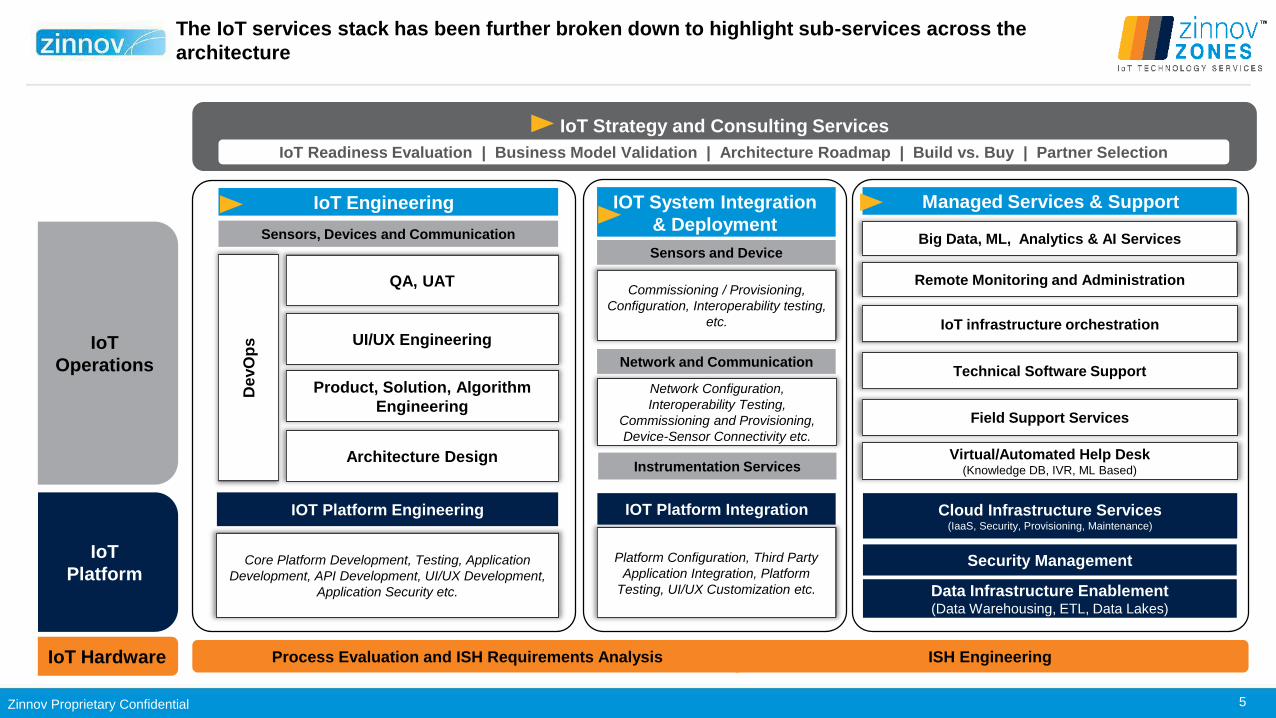

The IoT services stack has been further broken down to highlight sub-services across the

architecture

Process Evaluation and ISH Requirements Analysis ISH Engineering

Instrumentation Services

IoT Engineering IOT System Integration

& Deployment

Managed Services & Support

IOT Platform Engineering Cloud Infrastructure Services(IaaS, Security, Provisioning, Maintenance)

Data Infrastructure Enablement (Data Warehousing, ETL, Data Lakes)

IOT Platform Integration

UI/UX Engineering

Product, Solution, Algorithm

Engineering

DevO

ps

Architecture Design

QA, UAT

Security Management

IoT Strategy and Consulting Services

Sensors, Devices and Communication

IoT Readiness Evaluation | Business Model Validation | Architecture Roadmap | Build vs. Buy | Partner Selection

Sensors and Device

Commissioning / Provisioning,

Configuration, Interoperability testing,

etc.

Network and Communication

Network Configuration,

Interoperability Testing,

Commissioning and Provisioning,

Device-Sensor Connectivity etc.

Big Data, ML, Analytics & AI Services

Remote Monitoring and Administration

IoT infrastructure orchestration

Technical Software Support

Field Support Services

Virtual/Automated Help Desk(Knowledge DB, IVR, ML Based)

Platform Configuration, Third Party

Application Integration, Platform

Testing, UI/UX Customization etc.

Core Platform Development, Testing, Application

Development, API Development, UI/UX Development,

Application Security etc.

IoT

Platform

IoT

Operations

IoT Hardware

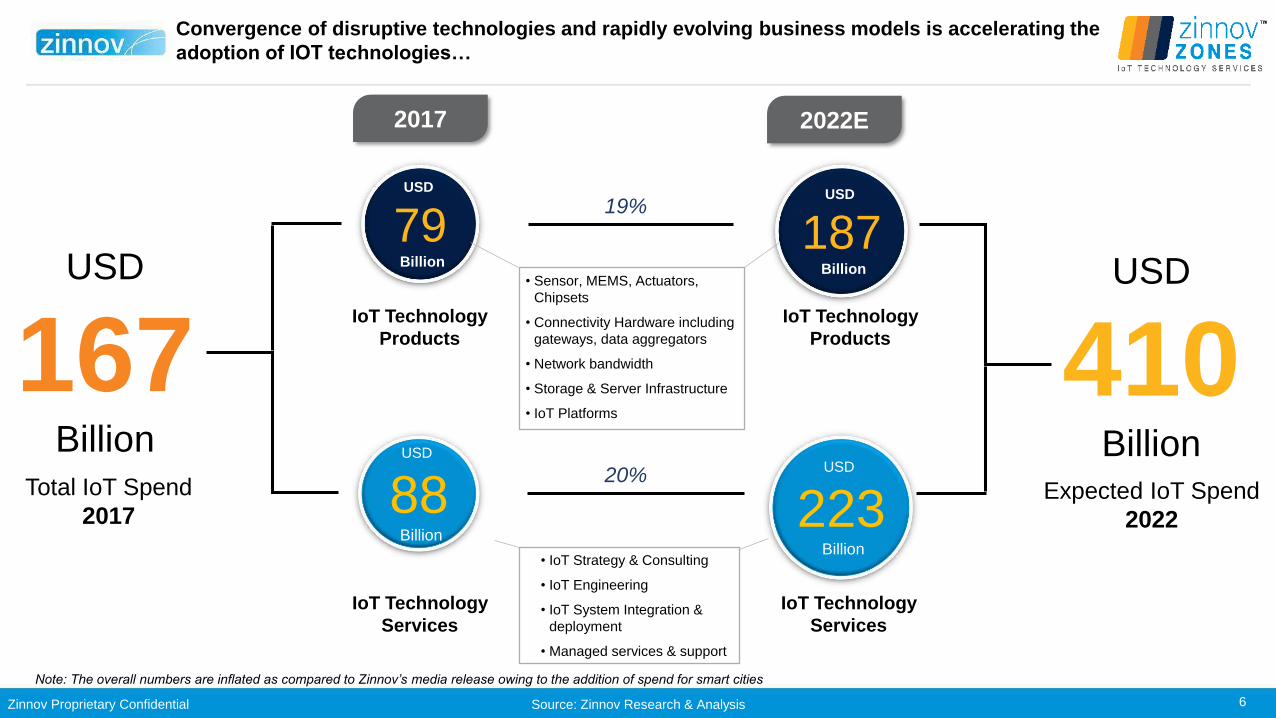

Zinnov Proprietary Confidential 6

USD

79Billion

IoT Technology

Products

USD

88Billion

IoT Technology

Services

USD

410Billion

USD

167Billion

Total IoT Spend

2017

USD

187Billion

IoT Technology

Products

USD

223Billion

IoT Technology

Services

2017 2022E

Expected IoT Spend

2022

19%

20%

• Sensor, MEMS, Actuators,

Chipsets

• Connectivity Hardware including

gateways, data aggregators

• Network bandwidth

• Storage & Server Infrastructure

• IoT Platforms

• IoT Strategy & Consulting

• IoT Engineering

• IoT System Integration &

deployment

• Managed services & support

Note: The overall numbers are inflated as compared to Zinnov’s media release owing to the addition of spend for smart cities

Source: Zinnov Research & Analysis

Convergence of disruptive technologies and rapidly evolving business models is accelerating the

adoption of IOT technologies…

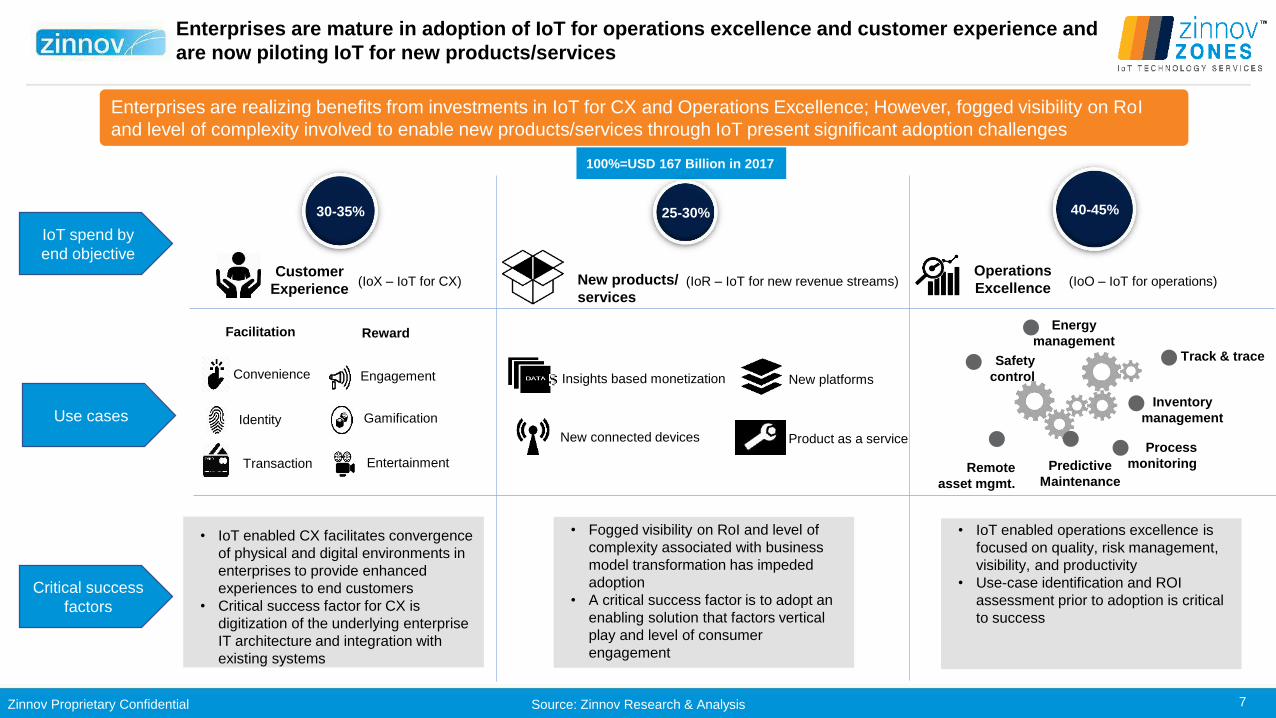

Zinnov Proprietary Confidential 7

100%=USD 167 Billion in 2017

Customer

Experience

Operations

ExcellenceNew products/

services

Remote

asset mgmt.

Track & trace

Inventory

management

Predictive

Maintenance

Energy

management

Safety

control

Process

monitoring

New platforms

Product as a serviceNew connected devices

Facilitation

Convenience

Identity

Transaction

Reward

Engagement

Gamification

Entertainment

30-35% 25-30% 40-45%

Enterprises are mature in adoption of IoT for operations excellence and customer experience and

are now piloting IoT for new products/services

IoT spend by

end objective

Use cases

Critical success

factors

(IoX – IoT for CX) (IoR – IoT for new revenue streams) (IoO – IoT for operations)

Source: Zinnov Research & Analysis

Enterprises are realizing benefits from investments in IoT for CX and Operations Excellence; However, fogged visibility on RoI

and level of complexity involved to enable new products/services through IoT present significant adoption challenges

• IoT enabled CX facilitates convergence

of physical and digital environments in

enterprises to provide enhanced

experiences to end customers

• Critical success factor for CX is

digitization of the underlying enterprise

IT architecture and integration with

existing systems

• Fogged visibility on RoI and level of

complexity associated with business

model transformation has impeded

adoption

• A critical success factor is to adopt an

enabling solution that factors vertical

play and level of consumer

engagement

• IoT enabled operations excellence is

focused on quality, risk management,

visibility, and productivity

• Use-case identification and ROI

assessment prior to adoption is critical

to success

Insights based monetization

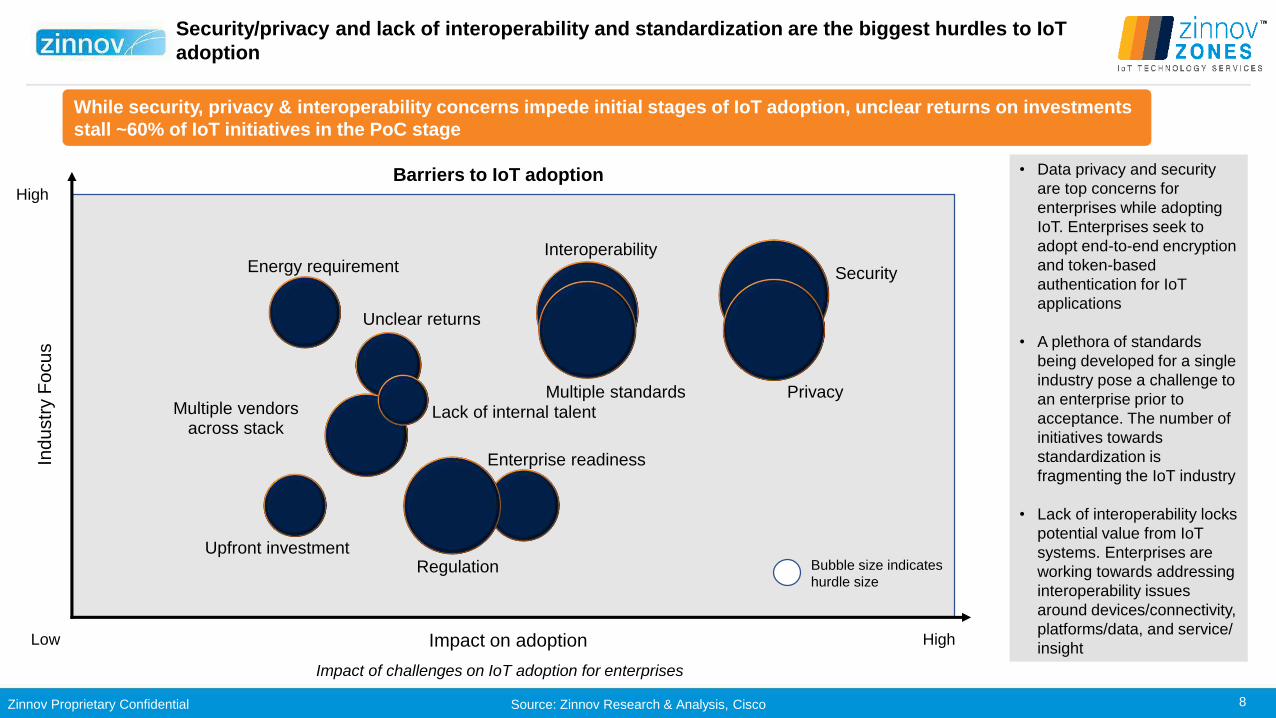

Zinnov Proprietary Confidential 8

Security

Privacy

Unclear returns

Interoperability

Multiple standardsMultiple vendors

across stackLack of internal talent

Upfront investment

Enterprise readiness

Energy requirement

Regulation

Ind

ustr

y F

ocu

s

Impact on adoptionLow

High

High

Impact of challenges on IoT adoption for enterprises

Security/privacy and lack of interoperability and standardization are the biggest hurdles to IoT

adoption

Source: Zinnov Research & Analysis, Cisco

Barriers to IoT adoption • Data privacy and security

are top concerns for

enterprises while adopting

IoT. Enterprises seek to

adopt end-to-end encryption

and token-based

authentication for IoT

applications

• A plethora of standards

being developed for a single

industry pose a challenge to

an enterprise prior to

acceptance. The number of

initiatives towards

standardization is

fragmenting the IoT industry

• Lack of interoperability locks

potential value from IoT

systems. Enterprises are

working towards addressing

interoperability issues

around devices/connectivity,

platforms/data, and service/

insight

While security, privacy & interoperability concerns impede initial stages of IoT adoption, unclear returns on investments

stall ~60% of IoT initiatives in the PoC stage

Bubble size indicates

hurdle size

Zinnov Proprietary Confidential 9

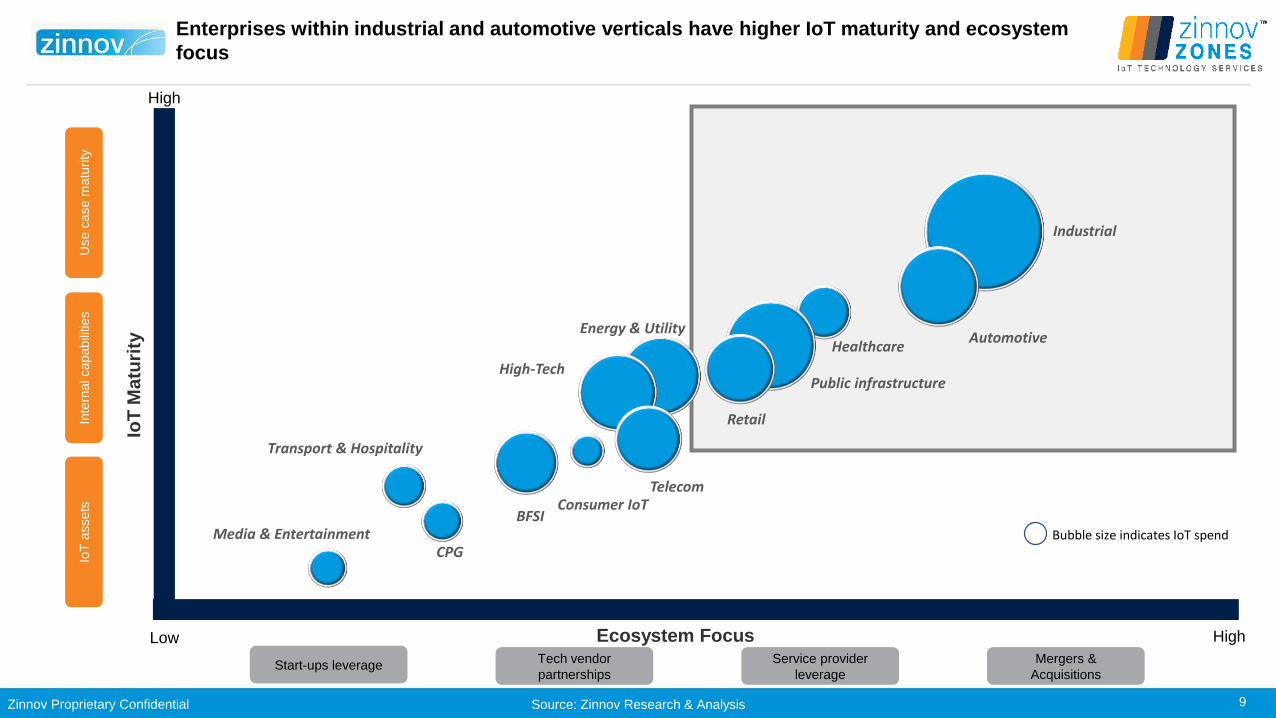

Industrial

AutomotiveHealthcare

Public infrastructureHigh-Tech

Telecom

BFSI

CPGMedia & Entertainment

Transport & Hospitality

Retail

Bubble size indicates IoT spend

High

HighLow

Energy & Utility

Consumer IoT

Inte

rnal capabili

ties

IoT

assets

U

se c

ase m

atu

rity

IoT

Ma

turi

ty

Start-ups leverageTech vendor

partnerships

Service provider

leverage

Mergers &

Acquisitions

Ecosystem Focus

Enterprises within industrial and automotive verticals have higher IoT maturity and ecosystem

focus

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 10

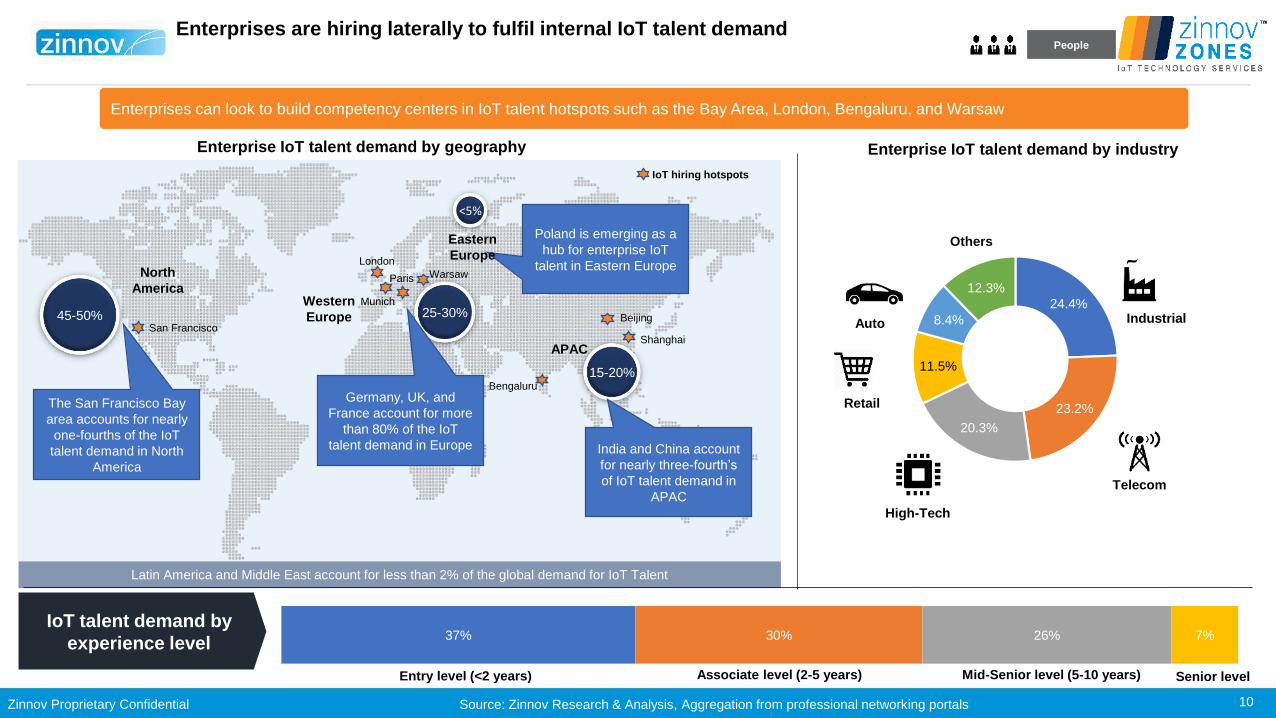

<5%

15-20%

45-50%

Latin America and Middle East account for less than 2% of the global demand for IoT Talent

IoT talent demand by

experience level

25-30%

The San Francisco Bay

area accounts for nearly

one-fourths of the IoT

talent demand in North

America

Germany, UK, and

France account for more

than 80% of the IoT

talent demand in Europe India and China account

for nearly three-fourth’s

of IoT talent demand in

APAC

Poland is emerging as a

hub for enterprise IoT

talent in Eastern Europe

24.4%

23.2%

20.3%

11.5%

8.4%

12.3%

Industrial

Telecom

High-Tech

Retail

Auto

Others

Senior level

37% 30% 26% 7%

Entry level (<2 years) Associate level (2-5 years) Mid-Senior level (5-10 years)

Enterprise IoT talent demand by geography Enterprise IoT talent demand by industry

North

AmericaWestern

Europe

Eastern

Europe

APAC

People

Source: Zinnov Research & Analysis, Aggregation from professional networking portals

Enterprises are hiring laterally to fulfil internal IoT talent demand

Enterprises can look to build competency centers in IoT talent hotspots such as the Bay Area, London, Bengaluru, and Warsaw

San Francisco

London

Paris

Munich

Warsaw

Bengaluru

IoT hiring hotspots

Shanghai

Beijing

Zinnov Proprietary Confidential 11

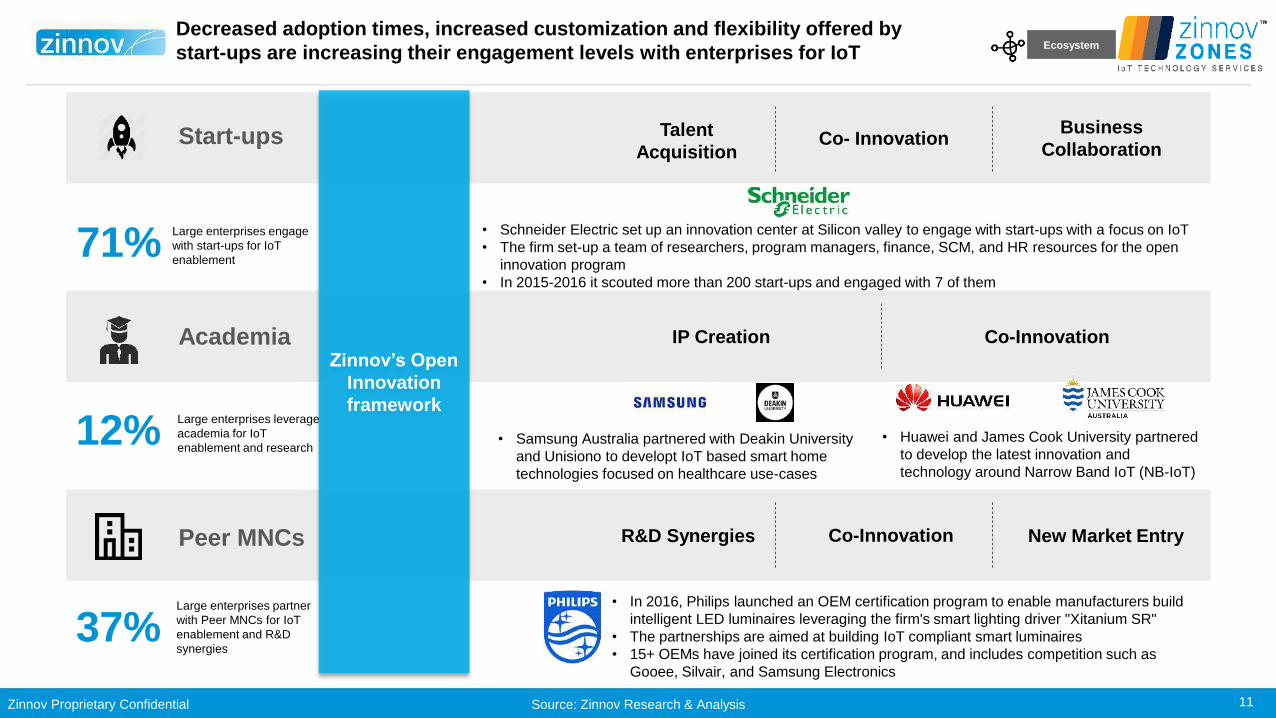

Start-ups

Academia

Peer MNCs

Zinnov’s Open

Innovation

framework

Talent

AcquisitionCo- Innovation

Business

Collaboration

IP Creation Co-Innovation

R&D Synergies Co-Innovation New Market Entry

• Samsung Australia partnered with Deakin University

and Unisiono to developt IoT based smart home

technologies focused on healthcare use-cases

• Huawei and James Cook University partnered

to develop the latest innovation and

technology around Narrow Band IoT (NB-IoT)

• Schneider Electric set up an innovation center at Silicon valley to engage with start-ups with a focus on IoT

• The firm set-up a team of researchers, program managers, finance, SCM, and HR resources for the open

innovation program

• In 2015-2016 it scouted more than 200 start-ups and engaged with 7 of them

• In 2016, Philips launched an OEM certification program to enable manufacturers build

intelligent LED luminaires leveraging the firm's smart lighting driver "Xitanium SR"

• The partnerships are aimed at building IoT compliant smart luminaires

• 15+ OEMs have joined its certification program, and includes competition such as

Gooee, Silvair, and Samsung Electronics

71%Large enterprises engage

with start-ups for IoT

enablement

12%Large enterprises leverage

academia for IoT

enablement and research

Large enterprises partner

with Peer MNCs for IoT

enablement and R&D

synergies37%

Ecosystem

Source: Zinnov Research & Analysis

Decreased adoption times, increased customization and flexibility offered by

start-ups are increasing their engagement levels with enterprises for IoT

Zinnov Proprietary Confidential 12

Cu

sto

me

r e

ng

ag

em

en

t le

ve

ls

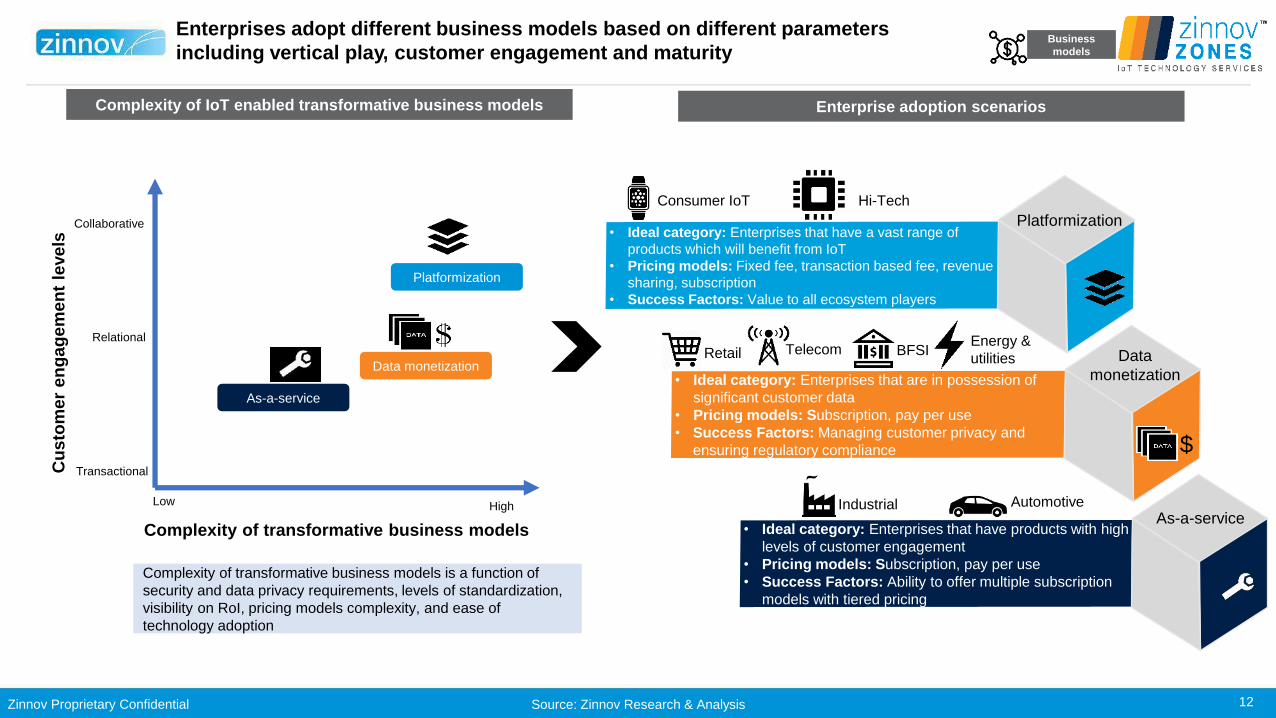

Complexity of transformative business models

As-a-service

Data monetization

Platformization

Complexity of IoT enabled transformative business models

Transactional

Relational

Collaborative

Low High

Complexity of transformative business models is a function of

security and data privacy requirements, levels of standardization,

visibility on RoI, pricing models complexity, and ease of

technology adoption

Enterprise adoption scenarios

Business

models

Source: Zinnov Research & Analysis

Enterprises adopt different business models based on different parameters

including vertical play, customer engagement and maturity

1• Ideal category: Enterprises that have a vast range of

products which will benefit from IoT

• Pricing models: Fixed fee, transaction based fee, revenue

sharing, subscription

• Success Factors: Value to all ecosystem players

• Ideal category: Enterprises that are in possession of

significant customer data

• Pricing models: Subscription, pay per use

• Success Factors: Managing customer privacy and

ensuring regulatory compliance

• Ideal category: Enterprises that have products with high

levels of customer engagement

• Pricing models: Subscription, pay per use

• Success Factors: Ability to offer multiple subscription

models with tiered pricing

Consumer IoT Hi-Tech

Retail Telecom BFSIEnergy &

utilities

Industrial Automotive

$

Platformization

Data

monetization

As-a-service

Zinnov Proprietary Confidential 13

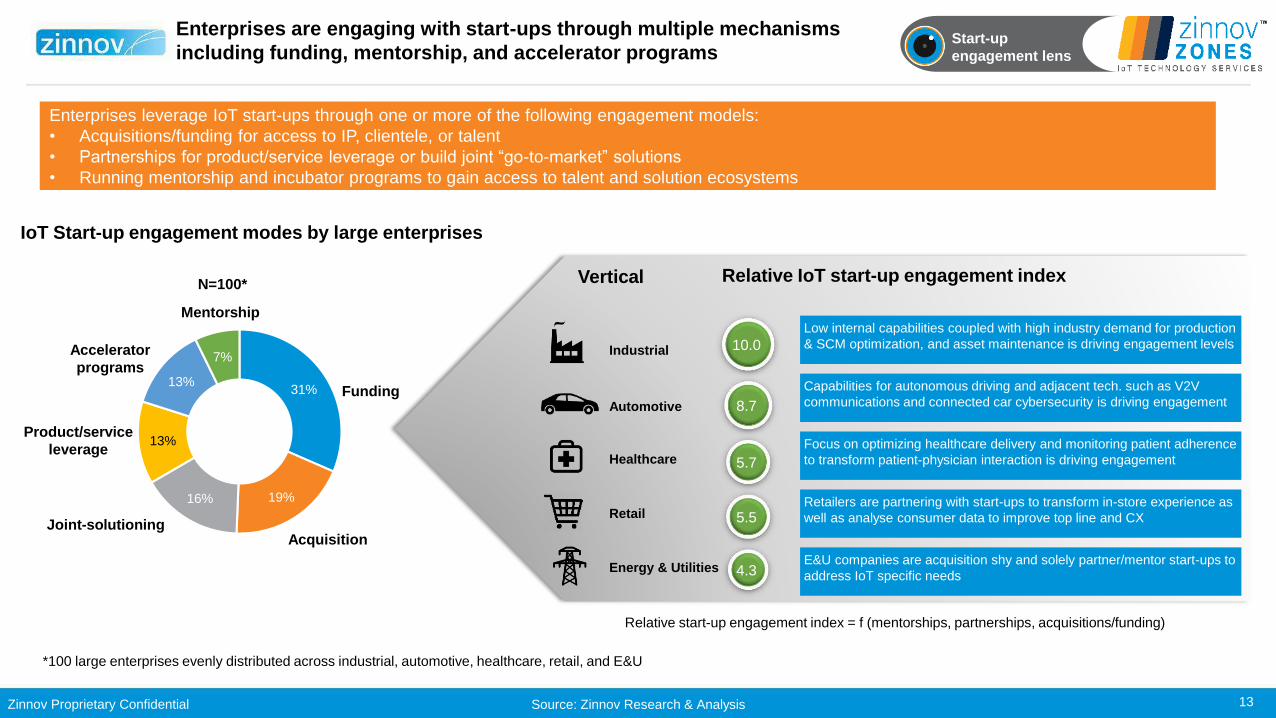

31%

19%16%

13%

13%

7%

Funding

Product/service

leverage

Accelerator

programs

Enterprises leverage IoT start-ups through one or more of the following engagement models:

• Acquisitions/funding for access to IP, clientele, or talent

• Partnerships for product/service leverage or build joint “go-to-market” solutions

• Running mentorship and incubator programs to gain access to talent and solution ecosystems

Vertical

Industrial

Automotive

Healthcare

Retail

Energy & Utilities

10.0

8.7

5.7

5.5

4.3

Relative IoT start-up engagement index

Relative start-up engagement index = f (mentorships, partnerships, acquisitions/funding)

IoT Start-up engagement modes by large enterprises

AcquisitionJoint-solutioning

Mentorship

Source: Zinnov Research & Analysis

Start-up

engagement lens

Enterprises are engaging with start-ups through multiple mechanisms

including funding, mentorship, and accelerator programs

Low internal capabilities coupled with high industry demand for production

& SCM optimization, and asset maintenance is driving engagement levels

Capabilities for autonomous driving and adjacent tech. such as V2V

communications and connected car cybersecurity is driving engagement

Focus on optimizing healthcare delivery and monitoring patient adherence

to transform patient-physician interaction is driving engagement

Retailers are partnering with start-ups to transform in-store experience as

well as analyse consumer data to improve top line and CX

E&U companies are acquisition shy and solely partner/mentor start-ups to

address IoT specific needs

N=100*

*100 large enterprises evenly distributed across industrial, automotive, healthcare, retail, and E&U

Zinnov Proprietary Confidential 14

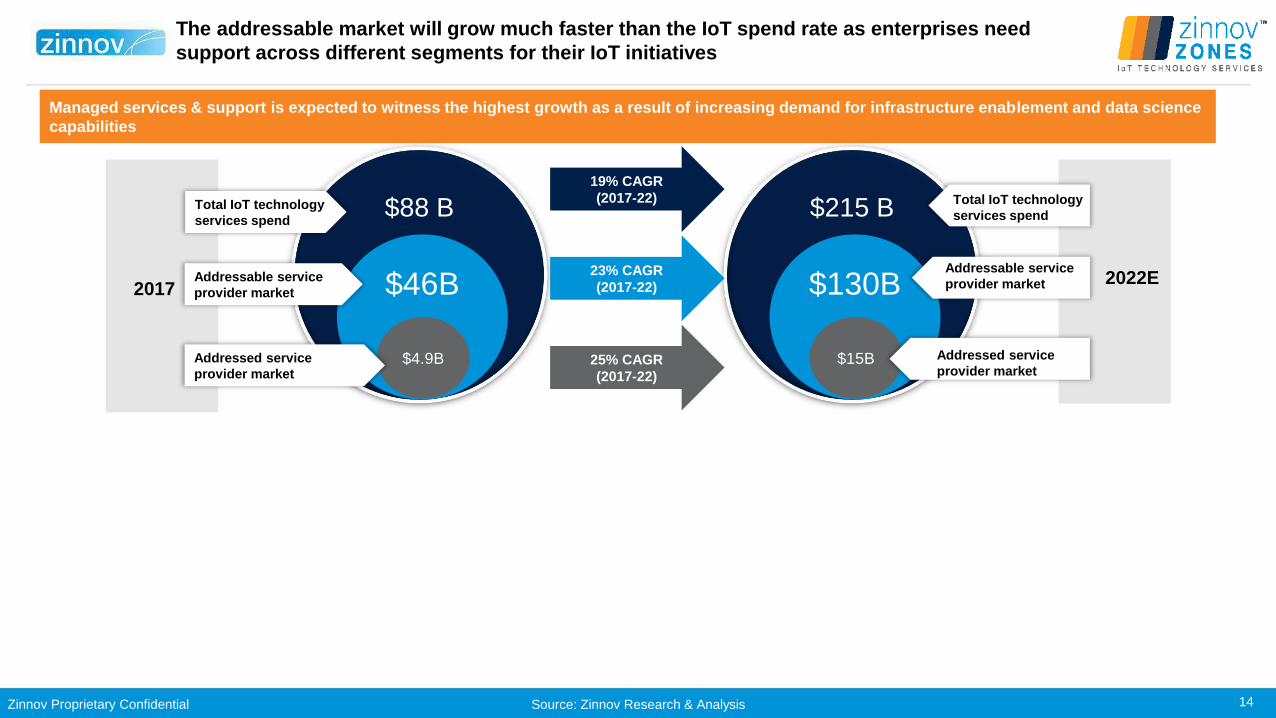

The addressable market will grow much faster than the IoT spend rate as enterprises need

support across different segments for their IoT initiatives

Source: Zinnov Research & Analysis

Managed services & support is expected to witness the highest growth as a result of increasing demand for infrastructure enablement and data science

capabilities

$88 B

20172022E

Total IoT technology

services spend

$46B

$4.9B

Addressable service

provider market

Addressed service

provider market

$215 B

$130B

$15B

19% CAGR

(2017-22)

Addressed service

provider market

Addressable service

provider market

Total IoT technology

services spend

23% CAGR

(2017-22)

25% CAGR

(2017-22)

Zinnov Proprietary Confidential 15

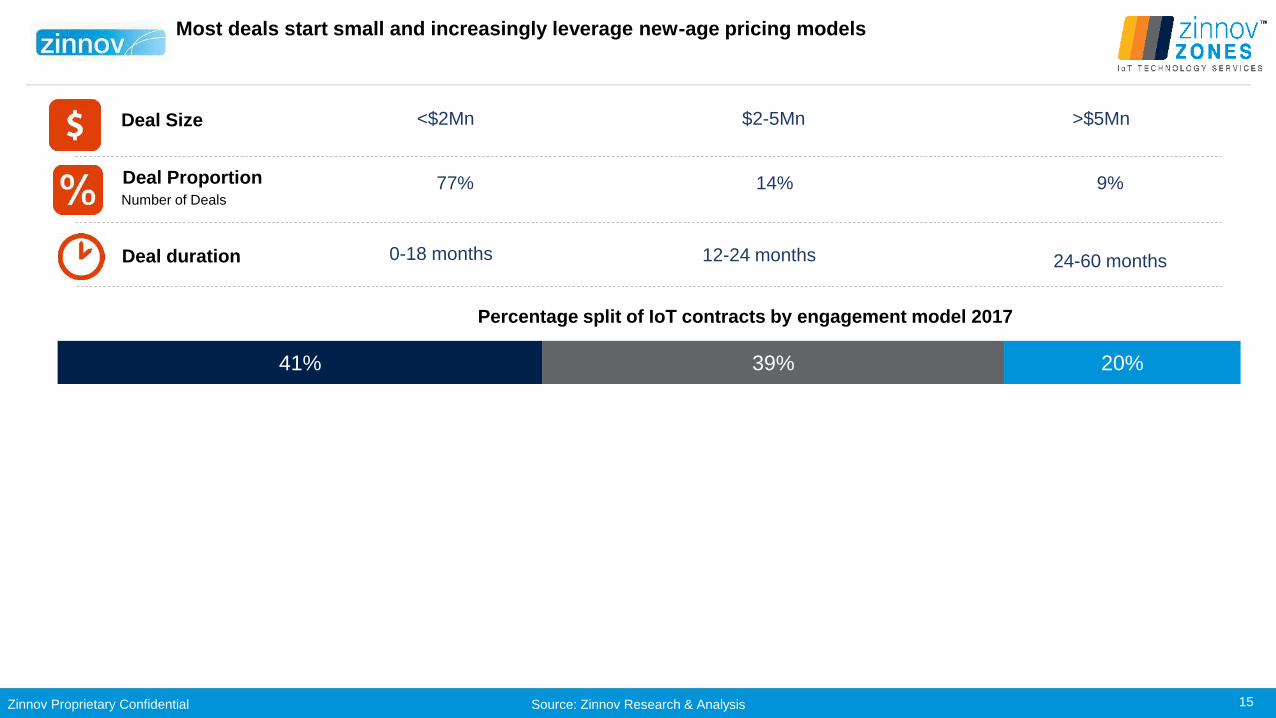

Most deals start small and increasingly leverage new-age pricing models

<$2Mn $2-5MnDeal Size >$5Mn

Deal Proportion

0-18 months

14% 9%Number of Deals

Deal duration

77%

12-24 months 24-60 months

41% 39% 20%

Percentage split of IoT contracts by engagement model 2017

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 16

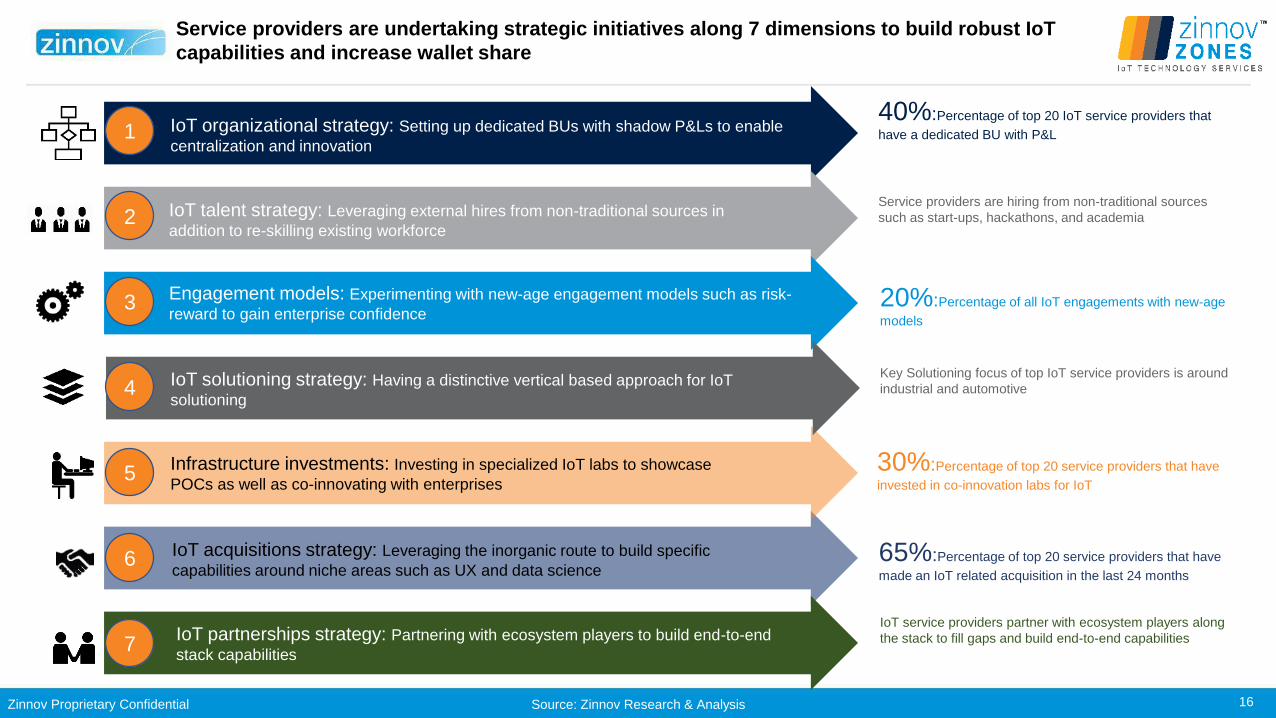

1

2

3

4

5

6

7

IoT organizational strategy: Setting up dedicated BUs with shadow P&Ls to enable

centralization and innovation

IoT talent strategy: Leveraging external hires from non-traditional sources in

addition to re-skilling existing workforce

Engagement models: Experimenting with new-age engagement models such as risk-

reward to gain enterprise confidence

IoT solutioning strategy: Having a distinctive vertical based approach for IoT

solutioning

Infrastructure investments: Investing in specialized IoT labs to showcase

POCs as well as co-innovating with enterprises

IoT acquisitions strategy: Leveraging the inorganic route to build specific

capabilities around niche areas such as UX and data science

IoT partnerships strategy: Partnering with ecosystem players to build end-to-end

stack capabilities

40%:Percentage of top 20 IoT service providers that

have a dedicated BU with P&L

Service providers are hiring from non-traditional sources

such as start-ups, hackathons, and academia

20%:Percentage of all IoT engagements with new-age

models

Key Solutioning focus of top IoT service providers is around

industrial and automotive

65%:Percentage of top 20 service providers that have

made an IoT related acquisition in the last 24 months

30%:Percentage of top 20 service providers that have

invested in co-innovation labs for IoT

IoT service providers partner with ecosystem players along

the stack to fill gaps and build end-to-end capabilities

Service providers are undertaking strategic initiatives along 7 dimensions to build robust IoT

capabilities and increase wallet share

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 17

Nurture Zone Breakout Zone Execution Zone Leadership Zone

Wipro

TCS

Tata Elxsi

Tech Mahindra

LTI*

Genpact

HARMAN Connected

Services

Low

High

Scalability

Zinnov Zones – Leading Service Providers

Aricent

Infosys

Happiest Minds

Altran

L&T TS

HCL

EPAM

Persistent Systems

ProdaptHughes

Systique

Innominds

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity

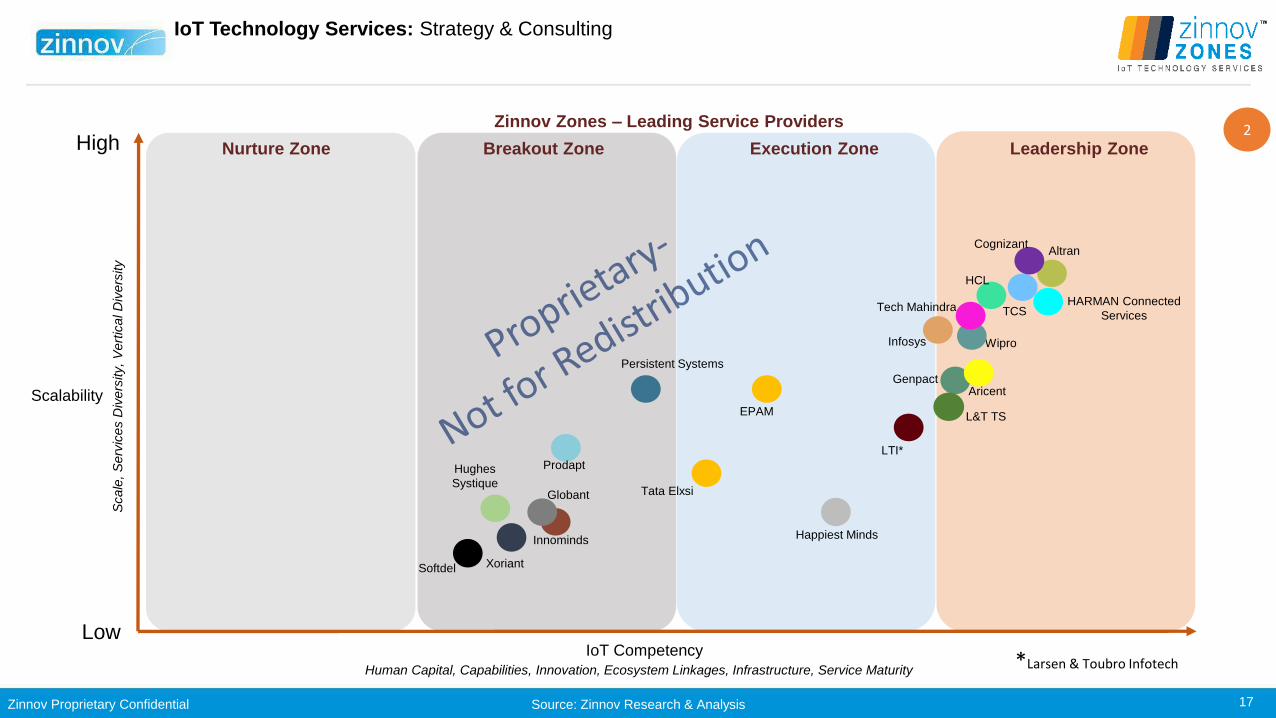

IoT Technology Services: Strategy & Consulting

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Softdel

Cognizant

Xoriant

Globant

2

*Larsen & Toubro Infotech

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 18

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHighZinnov Zones – Leading Service Providers

Infosys

Tata Elxsi

Tech Mahindra

Genpact

Altran

Aricent

Wipro

Happiest

Minds

HARMAN

Connected

Services

L&T TS

EPAMPersistent

Systems

Prodapt

eInfochips

Innominds

GlobalEdgeHughes

Systique

Low

Scalability

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity

TCS

HCL

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Softdel

Cognizant

LTI*

Xoriant

Globant

3

*Larsen & Toubro Infotech

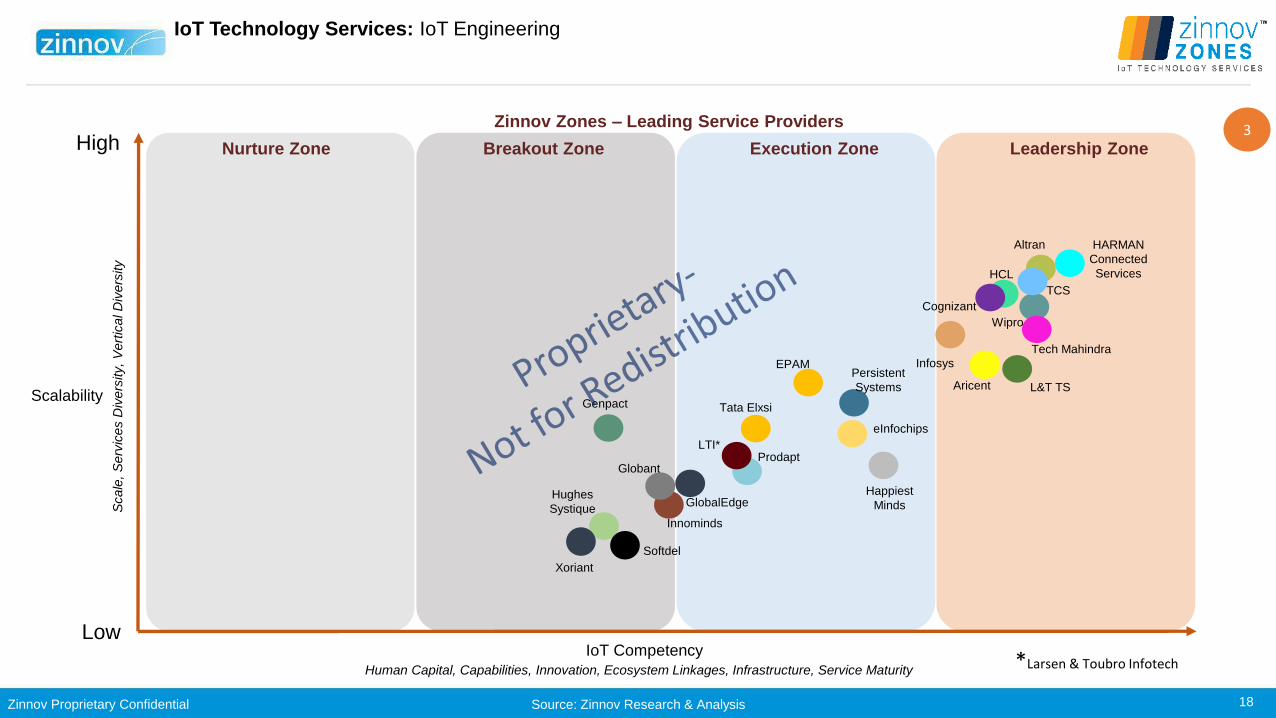

IoT Technology Services: IoT Engineering

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 19

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHighZinnov Zones – Leading Service Providers

Infosys

Tata Elxsi

Tech Mahindra

Genpact

Altran

Aricent

Wipro

Happiest

Minds

HARMAN

Connected

Services

L&T TS

EPAM

Persistent

Systems

Prodapt

eInfochips

Innominds

Low

Scalability

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity TCS

HCL

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Softdel

Cognizant

LTI*Xoriant

Globant

4

*Larsen & Toubro Infotech

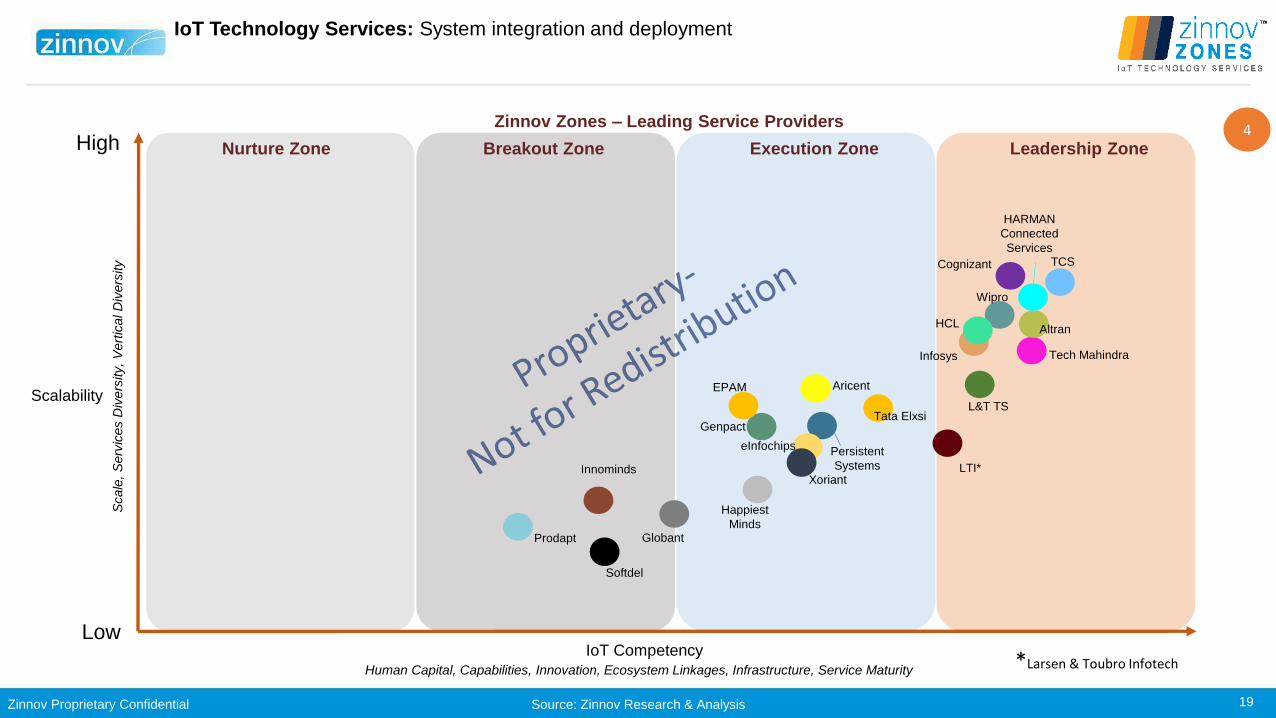

IoT Technology Services: System integration and deployment

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 20

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHighZinnov Zones – Leading Service Providers

Low

Scalability

Wipro

TCS

Tata Elxsi

Tech Mahindra

LTI*

GenpactHARMAN Connected

Services

Aricent

Infosys

Happiest Minds

Altran

L&T TS

EPAM

Persistent Systems

Prodapt

eInfochips

Innominds

GlobalEdge

HCL

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Cognizant

Globant

5

*Larsen & Toubro Infotech

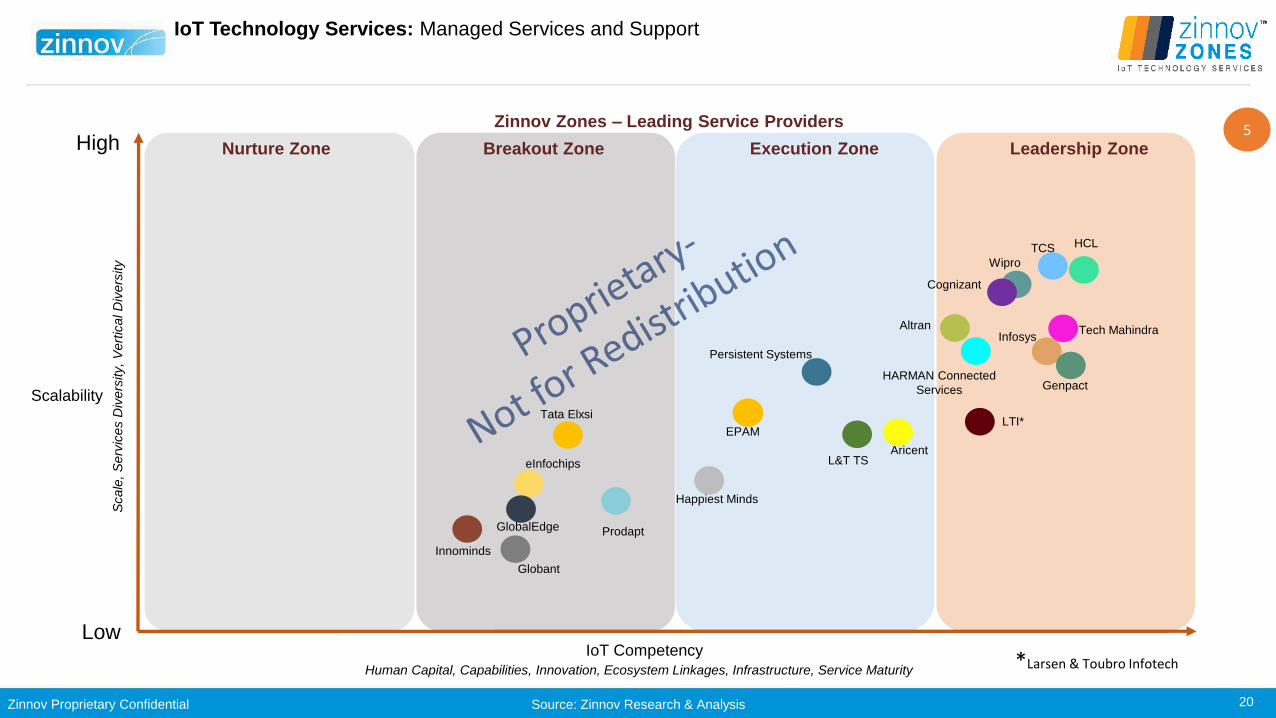

IoT Technology Services: Managed Services and Support

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 21

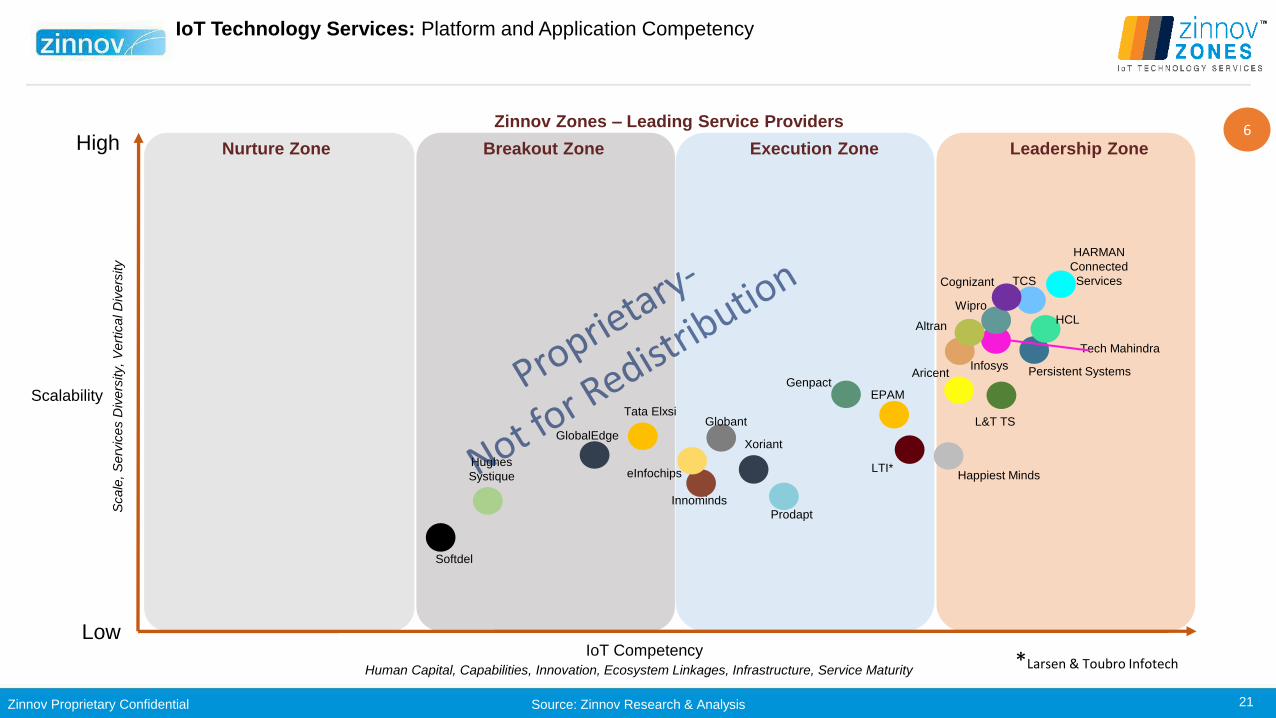

IoT Technology Services: Platform and Application Competency

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHighZinnov Zones – Leading Service Providers

Low

Scalability

Tech Mahindra

LTI*Happiest Minds

EPAM

Persistent Systems

Innominds

L&T TS

Genpact

Prodapt

HARMAN

Connected

ServicesTCS

HCLAltran

Aricent

eInfochipsHughes

Systique

Tata Elxsi

GlobalEdge

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity

Wipro

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Infosys

Softdel

Cognizant

Xoriant

Globant

6

*Larsen & Toubro Infotech

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 22

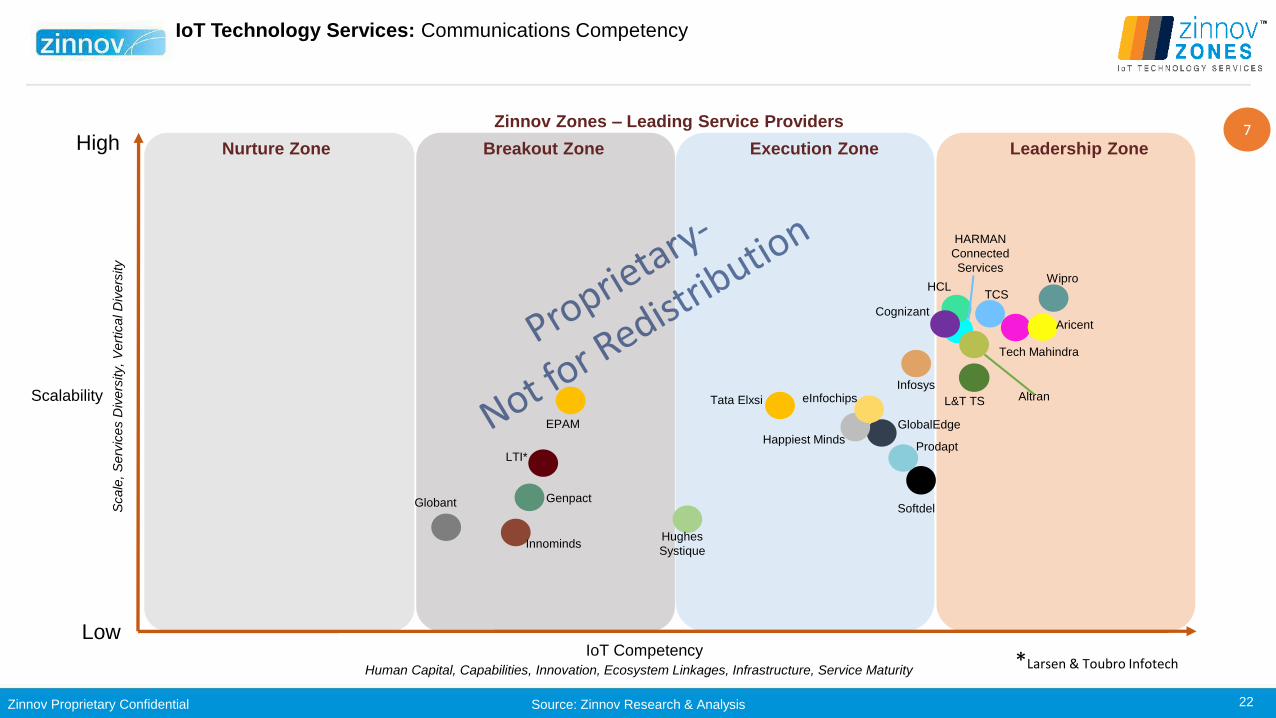

IoT Technology Services: Communications Competency

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHighZinnov Zones – Leading Service Providers

Low

ScalabilityInfosys

TCS

Tata Elxsi

Tech Mahindra

HARMAN

Connected

Services

Aricent

Wipro

EPAM

L&T TS

Happiest Minds

Innominds

GlobalEdge

Hughes

Systique

AltraneInfochips

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity

Genpact

HCL

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Softdel

ProdaptLTI*

Globant

7

Cognizant

*Larsen & Toubro Infotech

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 23

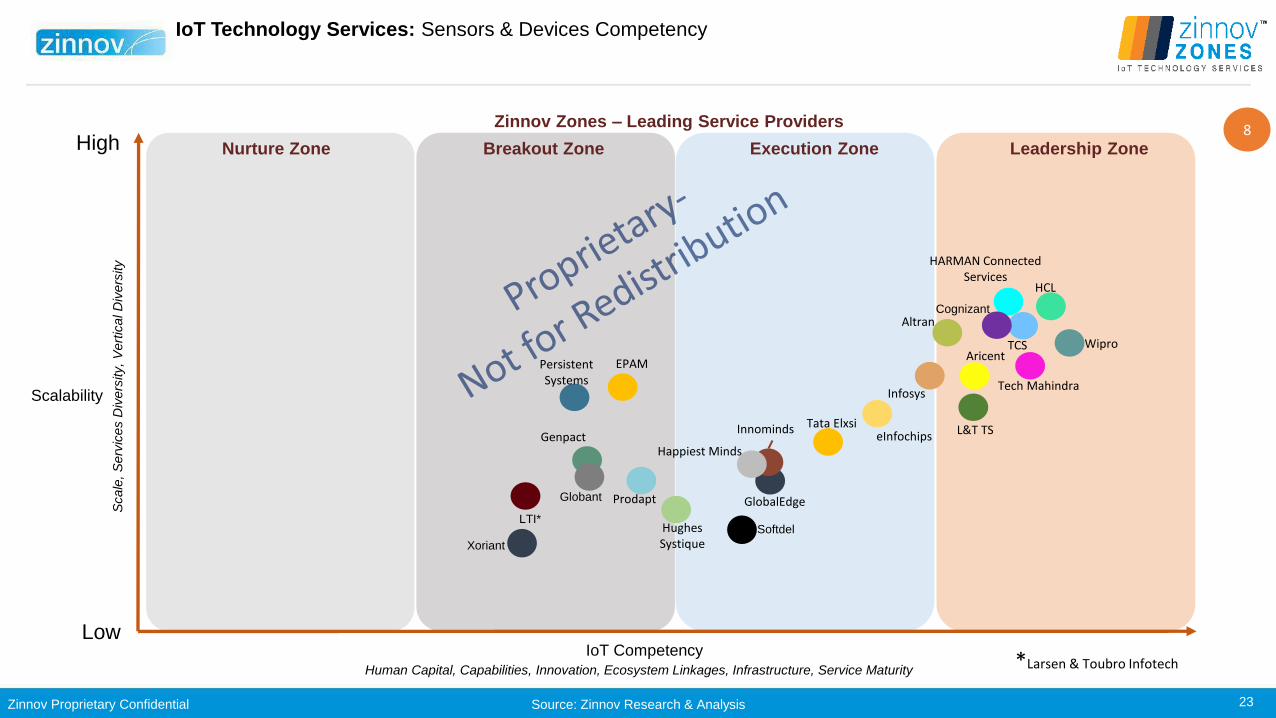

IoT Technology Services: Sensors & Devices Competency

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHighZinnov Zones – Leading Service Providers

Low

Scalability Infosys

TCS

Tata Elxsi

Tech Mahindra

HARMAN Connected Services

Wipro

Happiest Minds

Altran

L&T TS

HCL

EPAM

Innominds

GlobalEdge

Hughes Systique

eInfochips

PersistentSystems

Prodapt

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity

Genpact

Aricent

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Softdel

Cognizant

LTI*

Xoriant

Globant

8

*Larsen & Toubro Infotech

Source: Zinnov Research & Analysis

Zinnov Proprietary Confidential 24

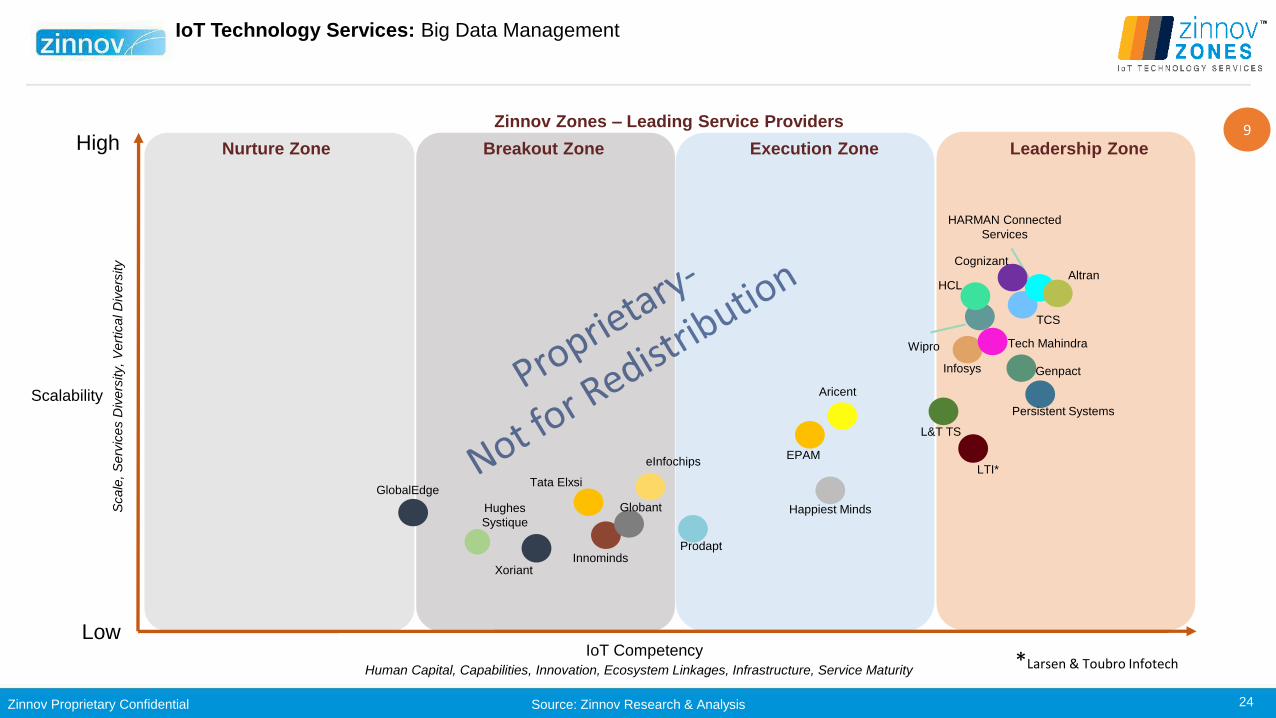

IoT Technology Services: Big Data Management

`

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHighZinnov Zones – Leading Service Providers

Low

Scalability

TCS

Tech Mahindra

LTI*

Genpact

Wipro

HCL

EPAM

Persistent Systems

Innominds

Aricent

eInfochips

GlobalEdge

HARMAN Connected

Services

Infosys

L&T TS

Prodapt

Happiest Minds

Altran

Hughes

Systique

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Tata Elxsi

Cognizant

Xoriant

Globant

9

*Larsen & Toubro Infotech

Source: Zinnov Research & Analysis

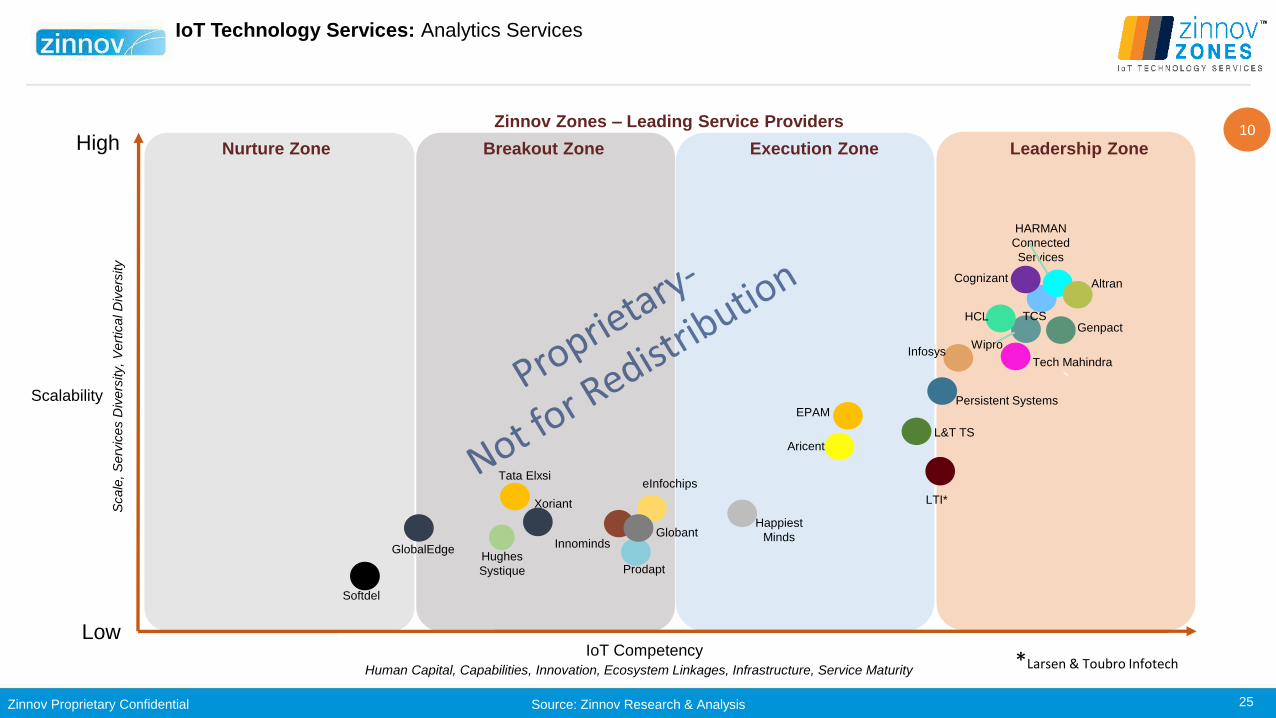

Zinnov Proprietary Confidential 25

IoT Technology Services: Analytics Services

`

Nurture Zone Breakout Zone Execution Zone Leadership ZoneHighZinnov Zones – Leading Service Providers

Low

Scalability

TCS

LTI*

Wipro

HCL

EPAMPersistent Systems

Innominds

Aricent

eInfochips

GlobalEdge

HARMAN

Connected

Services

Infosys

L&T TS

Prodapt

Happiest

Minds

Altran

Hughes

Systique

IoT Competency

Scale

, S

erv

ices D

ivers

ity,

Vert

ical D

ivers

ity

Human Capital, Capabilities, Innovation, Ecosystem Linkages, Infrastructure, Service Maturity

Softdel

Tata Elxsi

Cognizant

Xoriant

Globant

Tech Mahindra

Genpact

10

*Larsen & Toubro Infotech

Source: Zinnov Research & Analysis