yum! brands - 2014 analyst meeting presentation

TRANSCRIPT

Steve Schmitt

Safe Harbor Statement

This announcement, any related announcements and the related webcast may contain “forward-looking statements” within the meaning of

Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. We intend all forward-looking statements to

be covered by the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified

by the fact that they do not relate strictly to historical or current facts. Our forward-looking statements are subject to risks and uncertainties,

which may cause actual results to differ materially from those projected. Factors that can cause our actual results to differ materially include, but

are not limited to: food safety and food borne-illness issues; changes in economic conditions, consumer preferences, tax rates and laws and the

regulatory environment, as well as increased competition and other risks in China, where a significant and growing portion of our restaurants are

located; changes in economic and political conditions in the other countries outside the U.S. where we operate; the impact or threat of any

widespread illness or outbreaks of viruses or other diseases; our ability to protect the integrity and security of individually identifiable data of our

customers and employees; our ability to secure and maintain distribution and adequate supply to our restaurants; the success of our

international development strategy; commodity, labor and other operating costs; the continued viability and success of our franchise and license

operators; consumer preferences and perceptions of our brands; the impact of social media; a potential suspension of the Chinese affiliate of

our independent auditor; pending or future litigation and legal claims or proceedings; changes in or noncompliance with government regulations;

tax matters, including disagreements with taxing authorities; significant changes in global economic conditions, including consumer spending,

consumer confidence and unemployment; and competition within the retail food industry, including with respect to price and quality of food

products, new product development, advertising levels and promotional initiatives, customer service, reputation, restaurant location, and

attractiveness and maintenance of properties. You should consult our filings with the Securities and Exchange Commission (including the

information set forth under the captions “Risk Factors” and “Forward-Looking Statements” in our Annual Report on Form 10-K) for additional

detail about factors that could affect our financial and other results. Forward-looking statements are based on current expectations and

assumptions and currently available data and are neither predictions nor guarantees of future events or performance. You should not place

undue reliance on forward-looking statements, which speak only as of the date hereof. We are not undertaking to update any of these

statements.

GLOBAL

PORTFOLIO

THREE

ICONIC BRANDS

VERSATILE

OWNERSHIP

EMERGING

MARKET LEADER

41,000+ Restaurants

125+ Countries

Franchise

Company

15,000+Units

~50%

Operating Profit

Yum! Brands, Inc.

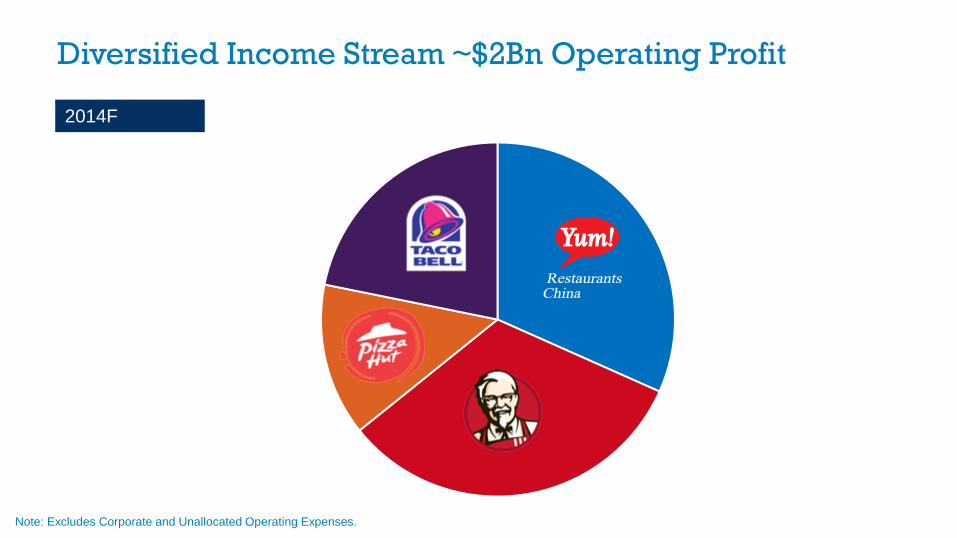

Diversified Income Stream ~$2Bn Operating Profit

Note: Excludes Corporate and Unallocated Operating Expenses.

2014F

Tremendous Growth Opportunity for Each Division

New-Unit Development, SSSG and High Returns

David Novak

13% 13%15%

13%14%

15%14%

13%

17%

14%13%

-9%

MSD

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

Yum! Dynasty Growth Model At Least 10% EPS EveryYear

EPS Growth, Ex Special Items

At Least

10 %

GOAL: RESTORE CONSISTENCY

#1 Priority: China Turnaround

2012 2014F Future

$1.7

$1.4

Average Unit Volumes ($’MM)

6,100+

Units

$2Bn

System

Sales~$1.7+

$600MM+ PROFIT

TREMENDOUS LEVERAGE

Note: Excludes Little Sheep, East Dawning and Pizza Hut Home Service.

The POWER of

Diversification

• Three Iconic Brands

• Strong in Developed Markets

• Lead in Emerging Markets

• Global Control

100% Focused Teams

• By Brand Centrally & Locally

• China & India (1Bn+ People)

• Yum! Added Value

Massive Scale

• Supply Chain

• Talent Magnet / Leadership Development

• Know-how Sharing

• Financial Strength

International Franchise Infrastructure

• 1,000+ Franchisees

– Goal: ~95% Franchised Outside of China/India

– 40% of Restaurants Owned By Franchisees

Who Operate More than One Brand

– Huge Advantage for Taco Bell

Focused Equity to Accelerate Growth

• First Mover in China Where Franchising

Capability Remains Nascent

• Prove Business Models & Honor

Contracts

• Earn Right to Own

The POWER ofDiversification

100% Focused

Teams

Massive Scale

International

Franchise

Infrastructure

Focused Equity

to Accelerate

Growth

• Over 10X Total Shareholder Return Since

Spin from PepsiCo

• Ten Consecutive Double-Digit Percentage

Dividend Increases

• Meaningful & Consistent Share Repurchases

• An Industry Leader in ROIC

Shareholder-Driven Mindset

Greg CreedCEO, Yum! Brands

EVOLUTIONNOT REVOLUTION

Continuing to Win Together

Vision &

Observations

Opportunities Financial

Goals

1 2 3

CourageSmart with Heart

Focusing on What Matters

Cultural Inspiration

Brand Evolution

Food Revolution

Focusing on What Matters

PRE 1960’s

Productivity & Physical Health

Personal Wellness Societal Wellness

Definition of Health is Changing

1960’s–2010 TODAY

Demand for Fresh & Real is on the Rise

PROCESSED FOOD PERCEPTIONS

Industrial

Predictable

Factory-made

Traditional fast food branded

Over-packaged

Difficult to replicate

REAL FOOD PERCEPTIONS

Authentic & timeless

Discovery

Local, artisan qualities

Ethnic flavors & foods

Minimally packaged

Restaurant style & quality

VISCERAL PROOF

It’s About Good for Me and Good for We

Rise of Real

CULTURE CONSUMER

The Situation is Clear

We Must Shatter Category Conventions

Cheap & Unhealthy

Impersonal & Industrial

Don’t Care

Money Hungry

Real & Affordable

Relevant & Consistent

Show We Care

Good for Me & We

FOOD AS FUEL

FOOD AS

EXPERIENCETHAT IS SHAREABLE

If it’s not worth sharing

it’s not worth doing.

Focusing on What Matters

LEADING INNOVATION

MORE TRANSPARENCY

VARIETY & CUSTOMIZATION

UNWAVERING ON FOOD SAFETY & INTEGRITY

Focusing on What Matters

BRANDS PEOPLE TRUST & CHAMPION

BRAND

TRUTHS

BRAND

PERSONALITY

BREAKTHROUGH

BRAND FILTERS

True North Positioning

HUMAN TRUTH PRODUCT TRUTH

BRAND TRUTHS

Focusing on What Matters

How to Reach our DESTINATION:

Brands that are…

More

More

More

More

RELEVANT

ENGAGED

CONNECTED

CARING

Brand Filters for Everything We Do

Innovating

Value

Disruptive

Genuine

&

&

&

&

Elevating

Values

Distinctive

Transparent

Brands People TRUST & CHAMPION

WE ARE ALL

BRAND CHAMPIONS

People Brands

1 2

Observations

World Class Leadership

Portfolio of Iconic Brands

Tremendous Growth Opportunity

New-Unit

Development

Same-Store

Sales Growth

1 2

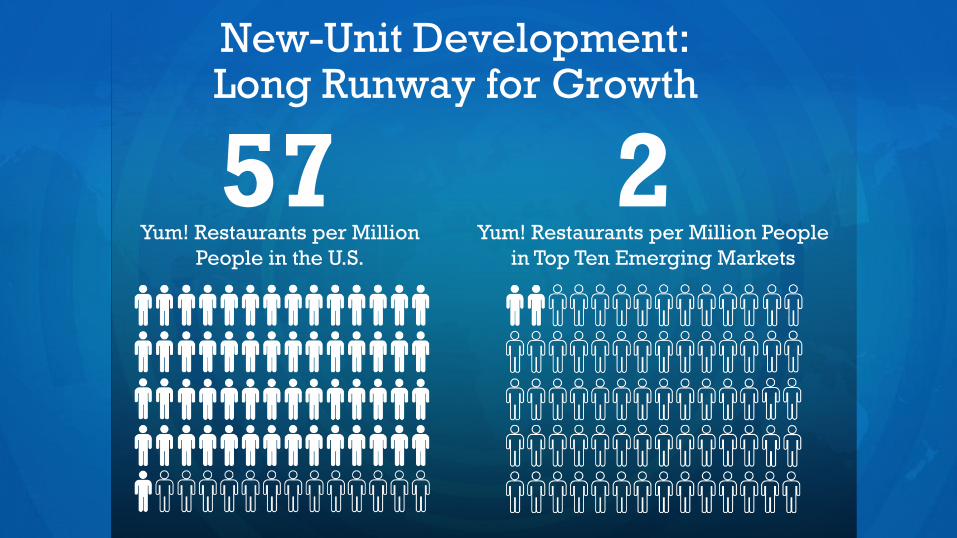

57 2Yum! Restaurants per Million

People in the U.S.

Yum! Restaurants per Million People

in Top Ten Emerging Markets

New-Unit Development: Long Runway for Growth

Huge Opportunity to Leverage Assets Globally

2013 AUVs ($MM)

*Company Reports.

Note: Taco Bell excludes License and International units.

$2.5

$1.6 $1.4 $1.4

$1.2

$0.8

$2.8 $2.6

$2.1

$2.5

$1.7

$-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

McDonalds PH China KFC China Taco Bell KFC Pizza Hut

System AUV Top 10% system units AUV

*

CHINA: #1 OPPORTUNITY

$-

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

$1.6

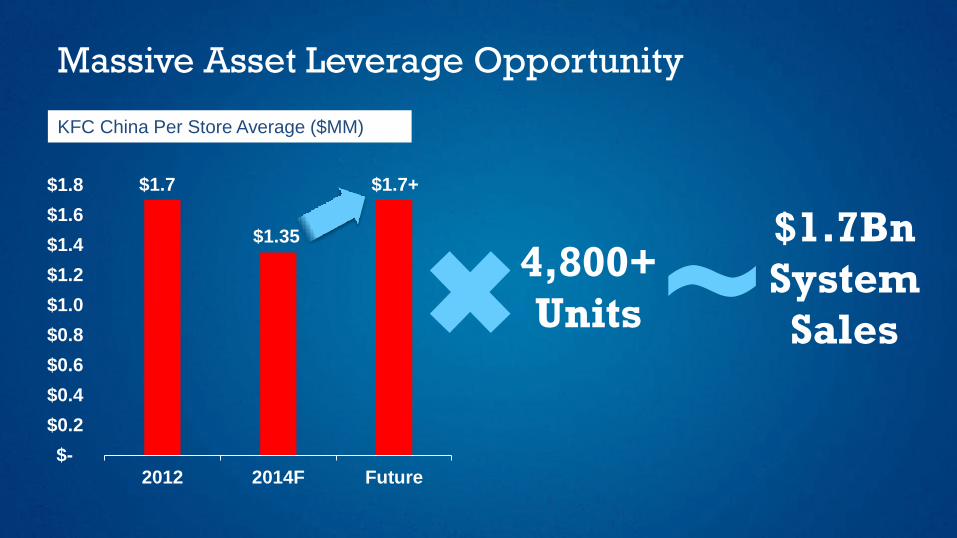

$1.8

2012 2014F Future

$1.7

$1.35

Massive Asset Leverage Opportunity

KFC China Per Store Average ($MM)

4,800+

Units

$1.7Bn

System

Sales~$1.7+

DESTINATION: Build 3 Global Iconic

Brands that People Trust and Champion

At least

10% ONGOING

EPS GROWTH

Growing

DIVIDEND

AnIndustry Leader in

ROIC

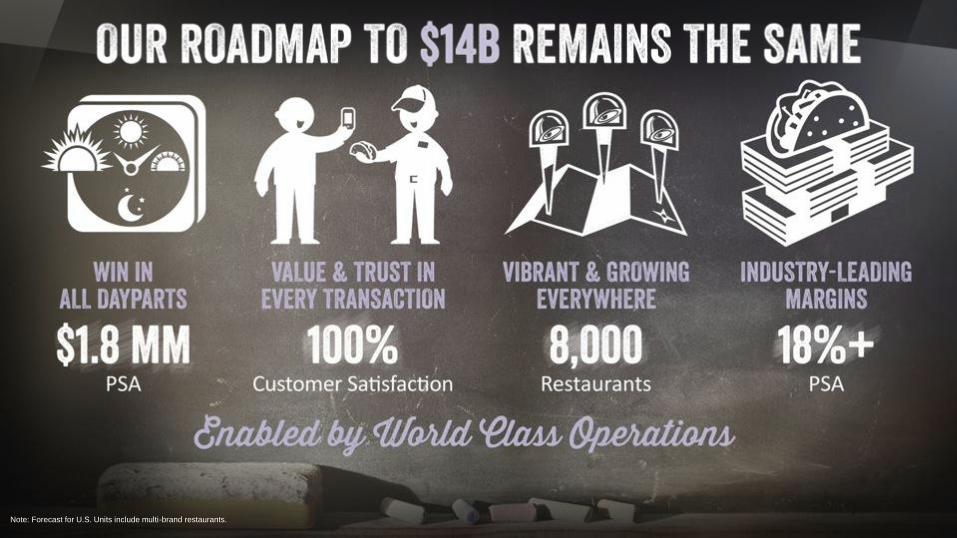

Brian NiccolChief Executive Officer,Taco Bell

Note: Forecast for U.S. Units include multi-brand restaurants.

We Have Brand Clarity...

...and Solid Momentum

Continued Leader in Operational Excellence

SOCIAL DEVELOPMENTMOBILEORDERING

BREAKFAST

Note: All trademarks and logos are the property of their respective owners.

58

Social ExplorerEdgy Craver

Dudes Status Feeders

Morning

Hustler

We Know Our Consumer

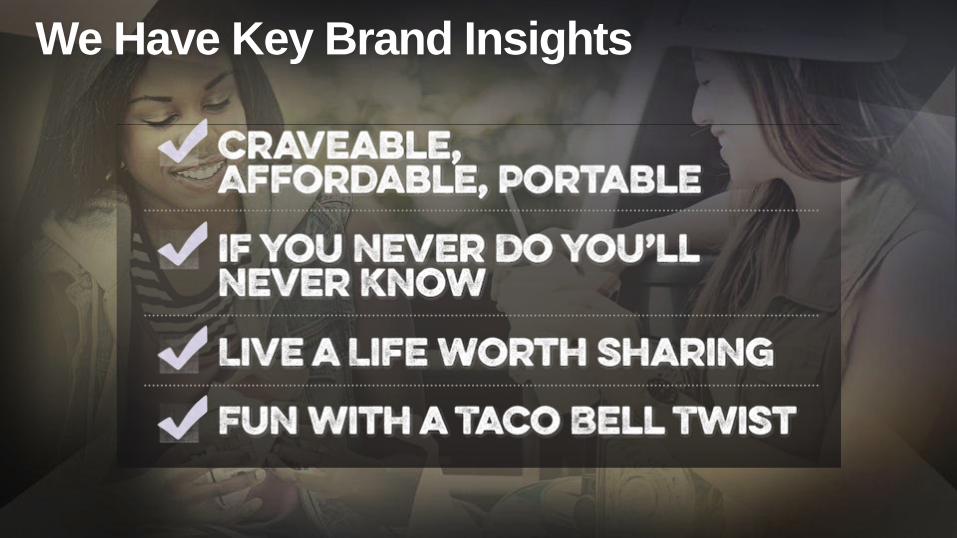

We Have Key Brand Insights

We’re Telling Deeper, Richer Stories

“SHOW WE CARE” TO INFLUENCERS

SOCIAL MEDIA LEADERSHIP

CONNECTING WITH HISPANICS

MOBILE APP GETS US CLOSER THAN

EVER TO CONSUMERS

From Marketing to PublishingNote: All trademarks and logos are the property of their respective owners.

Note: All trademarks and logos are the property of their respective owners.

Source: Taco Bell Brand Health Monitor.

Breakfast Off to a Great StartAwareness Strong & Growing

Incremental & Profitable

$90,000 Daypart

Positive Halo to Brand

24%

59%

95% 93%

PrePre Jul’14 Jul’14

TotalAwareness

40 Years4 Months

Note: All trademarks and logos are the property of their respective owners.

Early Mobile Results Promising

By The Numbers

1,000,000 downloads so far

97% of stores have had a mobile order

4.5 star rating (out of 5) on app store

20% higher Mobile check vs. non-Mobile

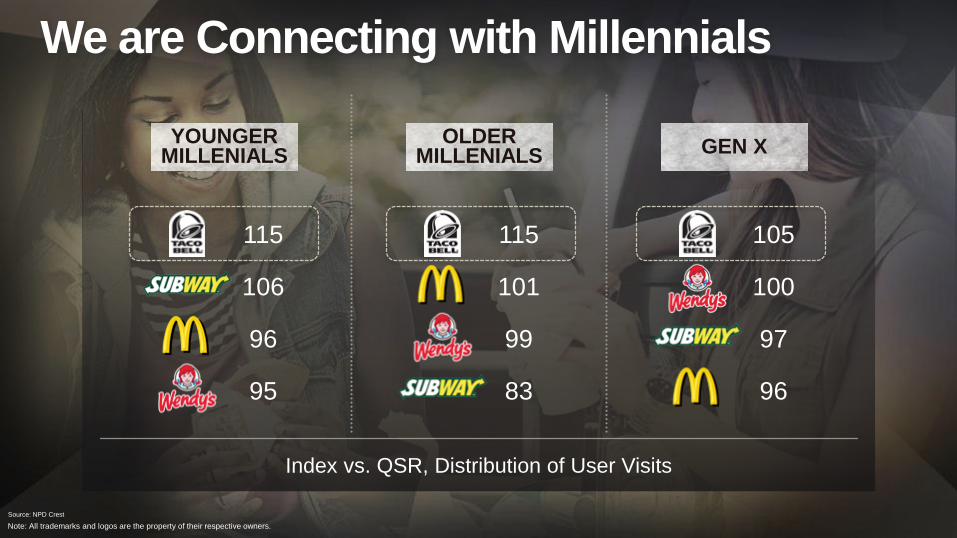

We are Connecting with Millennials

Source: NPD Crest

Index vs. QSR, Distribution of User Visits

115

106

96

95

YOUNGERMILLENIALS

OLDERMILLENIALS GEN X

115

101

99

83

105

100

97

96

Note: All trademarks and logos are the property of their respective owners.

We’re Not Standing Still

EVOLVING WITH OUR CUSTOMERS

MOVE FAST, BUT STRATEGICALLY

DEVELOPMENTINNOVATIONBREAKFAST MOBILE EDUCATION

Broadening the Brand in 2015

Big EatsValueRevolutionizing

the Taco

Breakfast Snacking & Beverages

Catering& Delivery

FoodieRevolution

Unique Craveable Tastes

WE SUPPORT TEENS...

Developing 21st Century Leaders

Enable

Inspire

Celebrate

WE SUPPORT TEAM MEMBERS...

WE FIGHT FOR EDUCATION

URBAN

+200 Units

RURAL

+300 Units

SUBURBAN

+500 Units

Line of Sight to 1,000 More Units in 5 Years...

Optimizing Our Presence through Next-Gen Footprints

DTO/WALK-UP OPEN KITCHENINLINE

...and Thinking Differently for Future Growth

Just Getting Started Globally

MADRID, SPAIN SHEFFIELD, UK

On Our Way

2012

$7 Billion

2022

$14 Billion

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

AN ICONIC BRAND POSITIONED FOR TAKE OFF

Poised For A Turnaround

Primed For Explosive Growth

Keep information

above this mark

Keep information

above this mark

BRAND

Keep information

above this mark

Keep information

above this mark IT STARTS WITH OUR HERITAGE

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

BRAND PROMISEPioneering The Most Flavorful

Food Experiences That Are

Share-Worthy

HUMAN TRUTHLife Is More

Flavorful

When We Share It

“BRING MORE FLAVOR TO LIFE”

Keep information

above this mark

Keep information

above this mark

OUR WINNING EQUATION

Keep information

above this mark

Keep information

above this mark

EVERYTHING WAS REFRESHED

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

25NEW MENU ITEMS

ADDED

CRUST FLAVORS

10

SAUCE DRIZZLES

4

NEW CREATE YOUR OWN

SAUCES

5NEW

CRUST

1

NEW INGREDIENTS

5

A RADICAL PRODUCT TRANSFORMATION!

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

Keep information

above this mark

MAKING “THE FLAVOR OF NOW” BIG NEWS

In-Store

Broadcast

PackagingRadio

PR & Media

IntegrationsE-Commerce Social

Media

Digital

Engagement

Online Advertising

#PromotedTweet

Experiential

Note: All trademarks and logos are the property of their respective owners.

Keep information

above this mark

Keep information

above this mark

A MORE BALANCED APPROACH TO VALUE…

PREVIOUS CURRENT

Keep information

above this mark

Keep information

above this mark

…BROUGHT TO LIFE ONLINE

Keep information

above this mark

Keep information

above this mark

BACK IN THE GAME ON DIGITAL

25%+

40%+U.S. DIGITAL SALES %*

2013 2014 YTD

Activation Deal Website Improvements

Online Deal

* Excludes Dine-In & Express.

Keep information

above this mark

Keep information

above this mark

INVESTING IN OUR DIGITAL FUTURE

31MM Global Fans

Keep information

above this mark

Keep information

above this mark

THE CATEGORY LEADER ENTERING A NEW PHASE OF GROWTH

7,900 Units

$5.7Bn System Sales

+260 Net New Units In Last 3 Years

Keep information

above this mark

Keep information

above this mark

AN ICONIC BRAND POSITIONED FOR TAKE OFF

Poised For A Turnaround

Primed For Explosive Growth

Keep information

above this mark

Keep information

above this mark

RAPIDLY GROWING INTERNATIONAL PRESENCE

5,700 Units

$4.5Bn System Sales

+610 Net New Units In Last 3 Years

Note: Excludes U.S. & India and China Divisions

Keep information

above this mark

Keep information

above this mark 2011 2012 2013 2014F

Note: Excludes U.S. & India and China Divisions

TRIPLED INTERNATIONAL NET BUILDS

84

International Net New Units

179 183

250+

Keep information

above this mark

Keep information

above this mark

ENTERED NEW MARKETS IN 2014

South Africa

Mongolia

Keep information

above this mark

Keep information

above this mark

EXPLODING GROWTH IN EXISTING MARKETS

Vietnam

Japan

Hong Kong

Brazil

Russia

Thailand

Keep information

above this mark

Keep information

above this mark

TREMENDOUS FUTURE GROWTH OPPORTUNITY

< 4 Stores per 1MM Pop

> 20 Stores per 1MM Pop

> 4 and < 20 Stores per 1MM Pop

Yum! China & Yum! India

No Locations

Keep information

above this mark

Keep information

above this mark

SMALL BOX MODELS: WINNING ECONOMICS

EXPRESS

Malls, Universities, etc.

Payback~2yr

DELCO “PLUS”

Seats / Slice Bar

Payback~3yr

DELCO

Growth Workhorse

Payback~3yr

Keep information

above this mark

Keep information

above this mark

MAKING RAPID PROGRESS 0N DIGITAL

~35%

~20%

International Digital Sales %*

* Excludes Dine-In & Express.

2012 2014

Keep information

above this mark

Keep information

above this mark

THE MOST LOVED AND FASTEST GROWING GLOBAL PIZZA

COMPANY IN THE WORLD!

OUR VISION:

Keep information

above this mark

Keep information

above this mark

Micky Pant

CEO

IT’S A

BRAND NEW DAYAT

KFC Brand Agenda

1. Reinforce: Consumer belief that

KFC tastes better

2. Build: Consumer visit frequency

with more choice and locations

3. Change: Perception that KFC is expensive

Brand Split has Provided Focus

UK & Asia Box - Indonesia

New Store FormatsProduct Innovation Value

Spain, US, Australia

& Singapore

114Countries & Territories

$700+ MMOp Profit

An Iconic Global Brand

14,200+Restaurants

$17 Bn+ System Sales

Note: 2014F.

New Market Openings in 2014

Italy Uganda Paraguay

2011 2012 2013 2014F

307 324

419 ~420

2011 2012 2013 2014F

Consistent Profit and

Development Track Record

+11%

+11%

Bulgaria, Sofia-Boyanna

Net Development

Op Profit

Note: Op Profit growth calculated using 2014 FX rates. Net Development is International Only. Percentages are CAGRs.

Make an Iconic Brand

Even Stronger

Leverage Franchise-Led Model

Win in Emerging Markets

Be a Strong #2 in W. Europe, UK and Australia

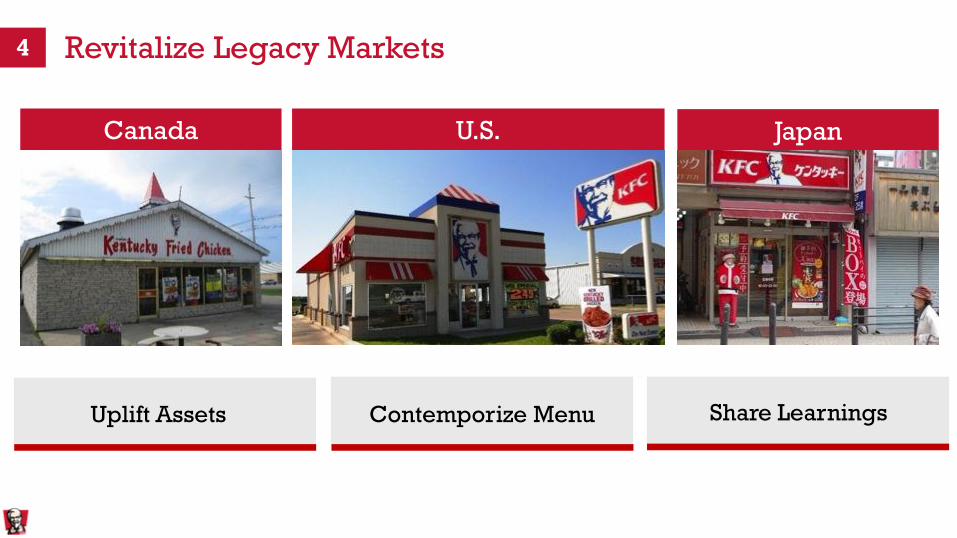

Revitalize Legacy Markets

1

2

3

4

750 550

8,200

4,700

Franchise

Equity

Leverage Franchise-Led Model

5,250

Developed Markets

8,950

Emerging Markets

Note: 2014F.

90%+ Franchise Ownership

1

Store Count

Win in Emerging Markets

Indonesia

Brazil

Pakistan

Nigeria

Russia

250

200

182

174

143

Mexico

Philippines

Vietnam

Egypt

Turkey

122

98

90

82

75

Top 10 KFC Emerging Markets Represent 1.4Bn People

Source: World Bank, Company Estimates for 2013.

Only 1.2 Units/MM Today

2

Country Population (MM) Country Population (MM)

Emerging Market

Powerhouse

Emerging

Countries KFC McD

South Africa 736 197

Malaysia 579 259

Thailand 492 193

Indonesia 466 149

Russia 245 413

Egypt 138 77

Vietnam 137 1 Malaysia, SeriIskandar

Note: 2013 YE Store Count; Vietnam updated for 2014 McD opening.

19 Units/MM 14 Units/MMSouth AfricaMalaysia

Highly Penetrated Markets Deliver Significant Profits

Note: 2014F. Op Profit growth calculated using 2014 FX rates.

• 2-Year Op Profit CAGR +14%

• Profit Contribution ~55MM

• 2-Year Op Profit CAGR +15%

• Profit Contribution ~$40MM

~$40MM Op Profit

2-Year CAGR +15%~$55MM Op Profit

2-Year CAGR +11%

KFC McD*

Be a strong #2 in

Western Europe, UK and

Australia

117* Company Estimates for 2013.

$1Bn+

$20MM+

Grow Western Europe through Franchise

capital and a variety of asset formats

France & Germany

2014F Op Profit

3

Profit and Innovation Powerhouses

AustraliaUK Netherlands

+5% SSS

15% Margins

$100MM+ Profit

+3% SSS

17% Margins

$100MM+ ProfitNote: 2014F.

+9% SSS

18% Margins

$9MM Profit

Revitalize Legacy Markets

U.S.Canada Japan

Uplift Assets Contemporize Menu Share Learnings

4

Building Company Margins to a Higher Plane

Positive Trend

Supply Chain Savings

Operations Efficiency

Managing Portfolio

Building Smarter

All Areas of the P&L

KFC Division Restaurant Margin

15%

Core

Margins

12.6%

~13%

~14%

2013 2014F 2015F

Note: Core margins represent stores that have been open for a minimum of one year.

$1.2

Significant Room to Grow Existing Business

$1.2

$2.7

System Average Top 10% of System

AUVs ($MM)

Note: 2014F.

Late NightBreakfast A.M. Coffee Happy Hour

South AfricaSouth AfricaUK Thailand

Leveraging Our Assets Across All Dayparts

Innovating for Today’s Consumer

Next Generation

Payment TechnologyTotally Digital Store

Engaging & Relevant

Digital Content

Note: All trademarks and logos are the property of their respective owners.

Leverage Franchise-Led Model

Win in Emerging Markets

Be a Strong #2 in W. Europe, UK and Australia

Revitalize Legacy Markets

1

2

3

4

ALWAYS ORIGINAL

KFC: An Iconic Brand, Poised for Greatness

A BRAND New Day in China

Sam Su

Yum! Brands Vice Chairman & CEO Yum! China

Casual Dining Leader Home Service LeaderQSR Leader

Since We Last Met

Trust Regained with ConsumersMassive Actions to Address

Upstream Vulnerabilities

Operation Thunder “I Commit” Campaign

Successful Brand Restage

• Menu Revamp at Unprecedented Scale

• Exciting Advertising and Promotions

• New Brand Look Positively Received

Outstanding First-Half Performance

19.8%Restaurant

Margin

116% Operating

Profit Growth

12% Same-Store

Sales Growth

1H 2H

12%

1H 2H

19.8%

1H 2H

116%

Same-Store

Sales GrowthRestaurant Margin Operating Profit Growth

Frustrating Set Back in Second Half

Triggered by OSI Supplier Incident

• Successive Incidents

• Prolonged Investigation

Recovery Slower than Anticipated

But, the Recovery is Happening

20%

25%

30%

35%

40%

45%

50%

55%

60%

2013 2014

KFC Reliable Brand

We Need to Earn the Right to Lead Everyday

KFC and Pizza Hut Remain the Best Options

“If KFC food is not safe, then nothing is safe in China.”

- Focus Group Consensus

Competition is Intensifying

Number of

Restaurants in Malls

1,122

30,000

2014

Number of

Shopping Malls 472

7,900

2010

• Scale & Lead over Competition

• Affordability & Convenience

• More Advertising Dollars

• Unmatched Capability: Ops, Supply Chain, Development

Significant Competitive Advantages

Driving Faster, More Relevant Innovation

Think Big, Test Quick, Execute Fast

Maintain Value Leverage Celebrities Broaden Menu Variety

We Will Lead in Technology

• Yum! China has the ability and

leadership position to take advantage

of technology

• We will continue to make the

necessary changes

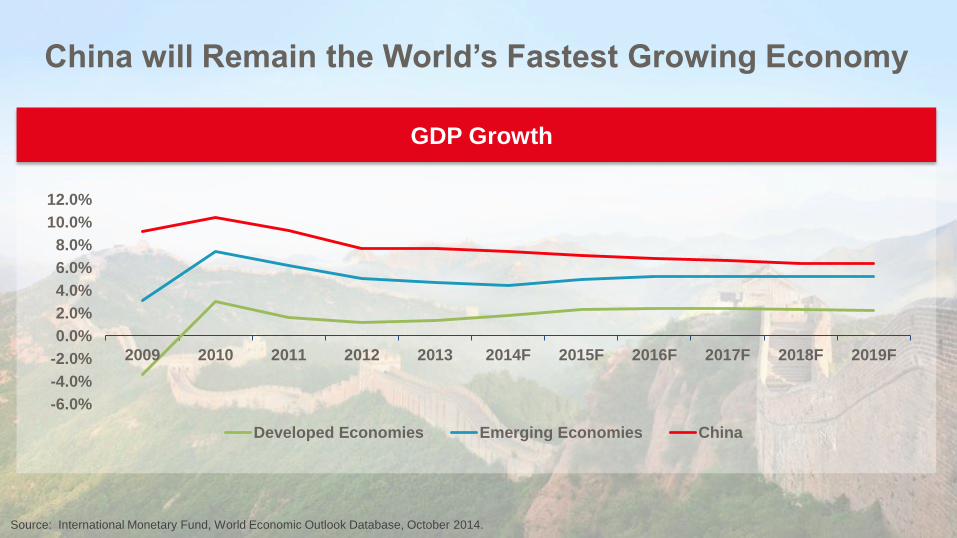

China will Remain the World’s Fastest Growing Economy

GDP Growth

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2009 2010 2011 2012 2013 2014F 2015F 2016F 2017F 2018F 2019F

Developed Economies Emerging Economies China

Source: International Monetary Fund, World Economic Outlook Database, October 2014.

Growing Consuming Class: Modern, Mainstream

Consuming Class

300 million in 2012

to

600 million by 2020

Looking Ahead

Urban Migration

+15 million per year

Tremendous Growth Opportunity Remains

1,300+

250+

3X

3X

10X

Today Potential

4,800+

Joey Wat, President KFC China

Previously:

Managing Director, Superdrug & Savers in UK

McKinsey & Company in China

Kellogg Graduate School

Fluent in English and Chinese (Mandarin, Cantonese and Fujianese)

A BRAND New Day at KFC China

Joey Wat

KFC China President

Why I Chose Yum!

Leading

China Brands

Growth

OpportunitiesGreat Team

RGM #1

Culture

KFC Will be an Even Stronger Leading Brand

• #1 Foreign Brand

• 4,800+ Units

• 1,000 Cities

Evolving KFC Strategy for Our

Changing Consumers

“New Fast Food” with Rich Food Varieties

Tomorrow

5+ Years ago

10+ Years ago

Day One

Life is so Much Fun with Today’s KFC

Position Brand as “Rooted in China” with Local Food

Western Brand with KFC Heritage (Fried Chicken)

1. Menu

Innovation

2. Interactive Digital

Campaigns

3. Continuing

Operations Focus

4 Strategic Pillars

4. One Brand…

Multiple Models

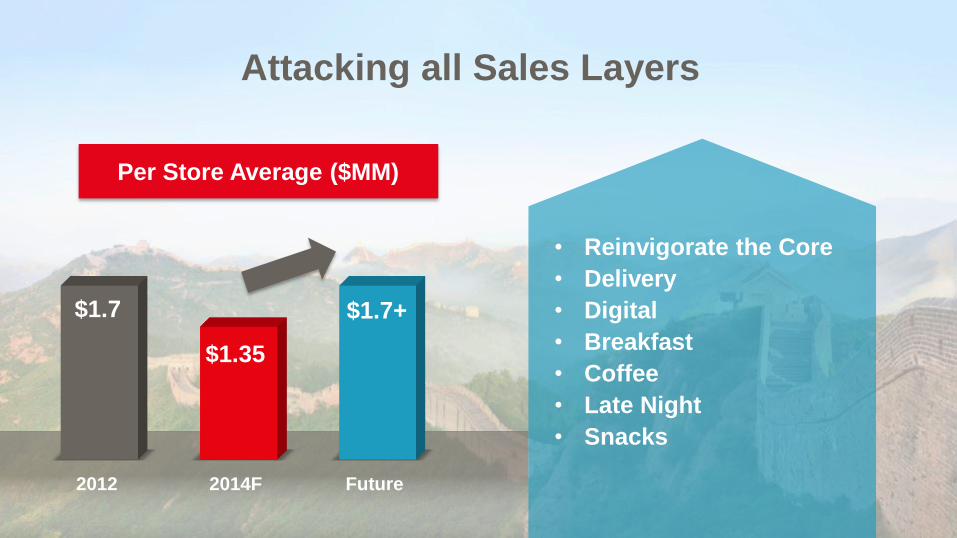

Attacking all Sales Layers

2012 2014F Future

$1.7

$1.35

$1.7+

Per Store Average ($MM)

• Reinvigorate the Core

• Delivery

• Digital

• Breakfast

• Coffee

• Late Night

• Snacks

Two Menu Revamps

Breakfast & Beverages

1. Menu Innovation

Lunch & Dinner

Maintaining our Value Anchors

Extending Successful Celebrity Advertising

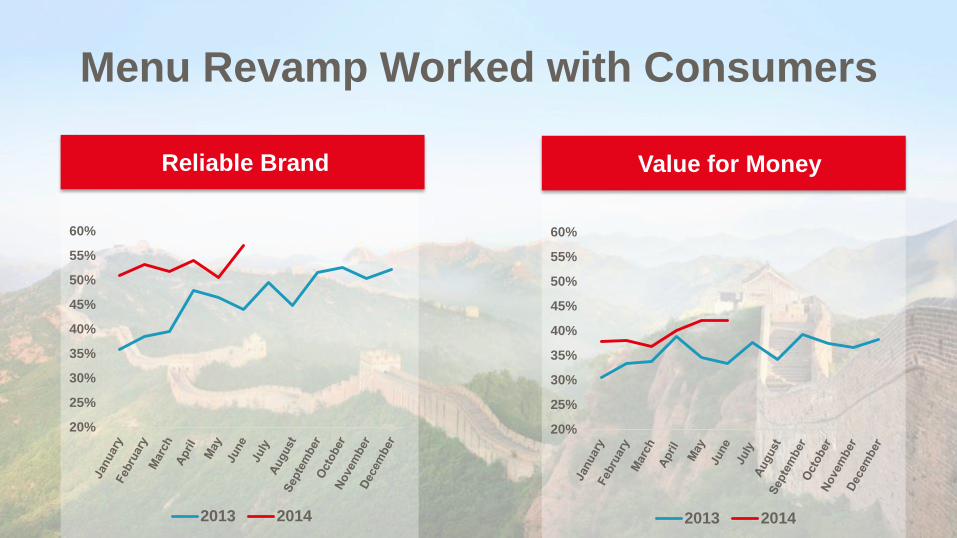

Menu Revamp Worked with Consumers

20%

25%

30%

35%

40%

45%

50%

55%

60%

2013 2014

20%

25%

30%

35%

40%

45%

50%

55%

60%

2013 2014

Reliable Brand Value for Money

Introducing Premium KFC Coffee

with Everyday Great Value

Expanding Afternoon Daypart

2. Interactive Digital Campaigns

Even Greater Focus on Youth

• Reinvigorate Kids Program

• More Focus on Family with Kids Promotions

• More Focus on Millennials

1. Brand

Communication

2. e-Commerce

3. In-Store

Experience

Leading with Digital

• 10 MM Brand Apps Activated

• WIFI in T1 & T2 Cities

• Mobile Ordering Peak 43M

Daily Transactions

3. Continued Focus on Operations

Distinctive

Branded ServiceSuperior TrainingFood Safety

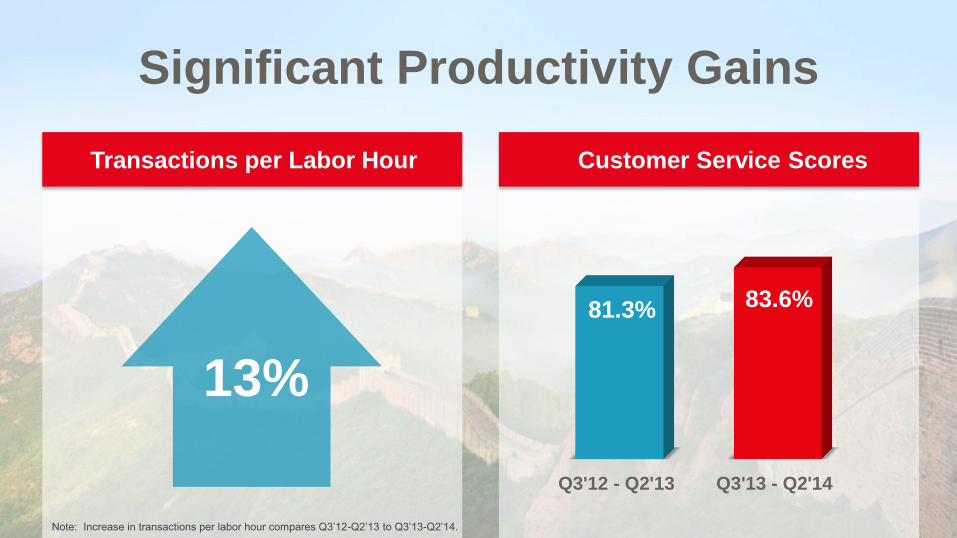

Significant Productivity Gains

Transactions per Labor Hour Customer Service Scores

Q3'12 - Q2'13 Q3'13 - Q2'14

81.3% 83.6%

Note: Increase in transactions per labor hour compares Q3’12-Q2’13 to Q3’13-Q2’14.

13%

4. One Brand…Multiple Business Models

• Menu Localization

• Asset Options

• Localized Pricing

• Franchising

Re-Accelerating New Restaurants Over Time

KFC Gross New-Unit Openings

2010 2011 2012 2013 2014F

414

515

621

428360

First-Half Returns Give Us Confidence

in KFC Development

Payback 3-4 Years

Tier 1 – 2 Cities Tier 3 – 6 Cities

Average Unit Volume ($MM) $1.1 $1.0

Cash Margin 18% 18%

Cash Investment ($M) $600 $610

Note: Includes units opened August 2012 – July 2013.

2014 New Unit Economics - KFC

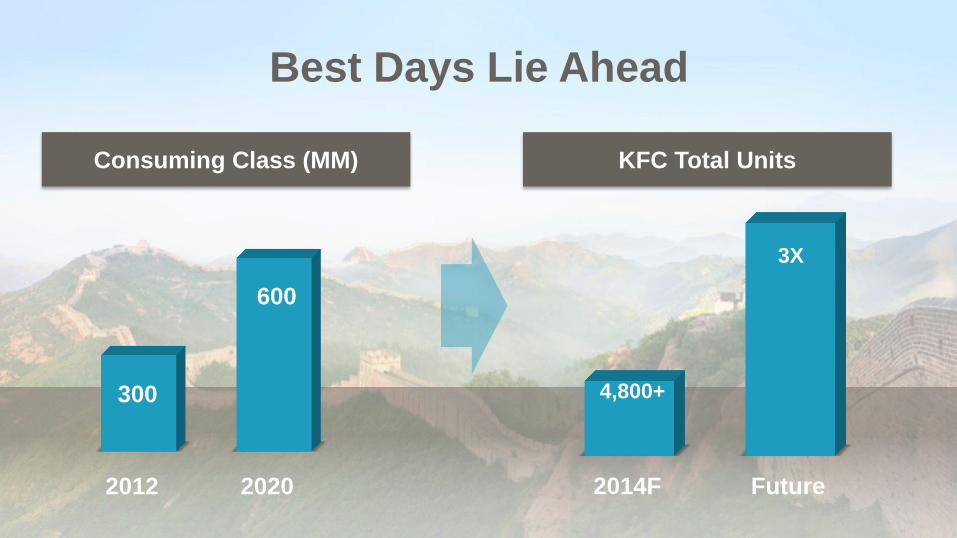

Best Days Lie Ahead

Consuming Class (MM)

2012 2020

300

600

KFC Total Units

2014F Future

4,800+

3X

Remain Confident in KFC China Growth

Disruptive

Innovation

#1 Foreign

Brand in

China

Unrivaled

Capability

Strong

Macros in a

Changing

China

A BRAND New Day at Pizza Hut China

Sam Su

Yum! Brands Vice Chairman & CEO Yum! China

China’s Casual Dining Powerhouse

• #1 Western Casual Dining Restaurant

• 1,300+ Units

• 315+ Cities

Powerful Business Model

Even in a Down Year

• $1.5MM PSA

• 18% Restaurant Margin

• <3 Year Cash Return

Note: 2014F

Pizza Hut was Built on a Strong Foundation

• 5 Star Service at 3 Star Prices

• Extensive Menu offering Covering All Categories

• Over 20 New Menu Items Twice a Year

• “You can eat like a rich man or eat like a poor man”

• Compelling Value (e.g. Afternoon Tea or Breakfast)

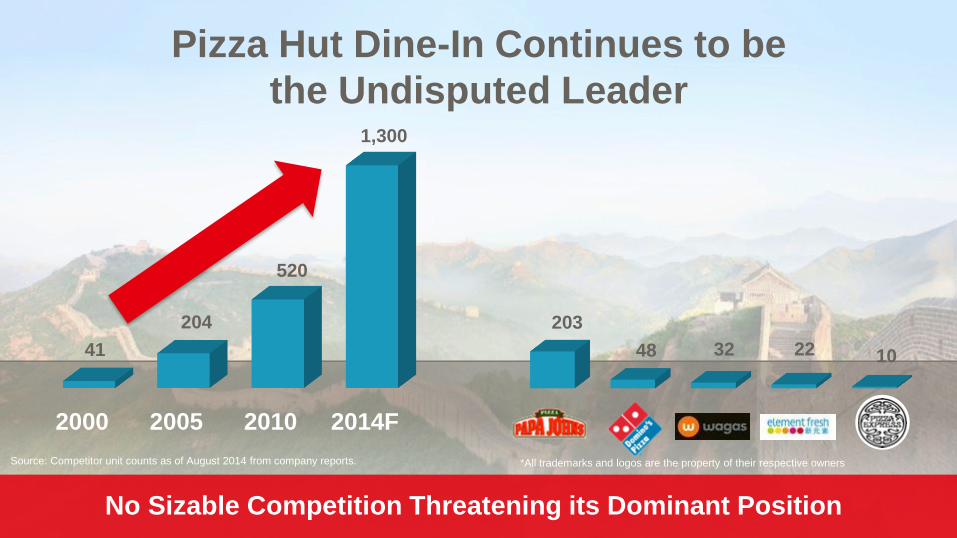

Pizza Hut Dine-In Continues to be

the Undisputed Leader

2000 2005 2010 2014F

41

204

520

1,300

203

48 32 22 10

No Sizable Competition Threatening its Dominant Position

Source: Competitor unit counts as of August 2014 from company reports. *All trademarks and logos are the property of their respective owners

*All trademarks and logos are the property of their respective owners.

Chinese Consumers’ Tastes are Rapidly Evolving

Continuing to Elevate the Brand

171

Disruptive Innovation

• Go Beyond Regular Menu Revamp

• Comprehensive Review of the Menu

• New, Better, Fresher Ingredients

• More Sophisticated Menu Options

Supported by Breakthrough

Marketing and Technology

Along with Asset Upgrades

Continuing to Leverage the Asset

700+Breakfast Units

100+Late Night Units

Pizza Hut China: A Fantastic Growth Story

675

550

Net New Units Last 3 Years

95%

80%

System Sales Growth Last 3 Years

* Compares Pizza Hut Casual Dining in China to Chipotle in the U.S. from YE 2011 to YE 2014F.

Note: All trademarks and logos are the property of their respective owners.

Pizza Hut Home Service…

Leader in Delivery

• 250+ Units

• 25+ Cities

Leader in Fast Expanding China Food Delivery

2010 2014F

120

250+

Units

Delivery

Category

Time Has Come for Food Delivery

Mobile Technology is Fast Becoming the Norm

Sept. 2014Sept. 2012 Sept. 2013

Online

52%Mobile

27%

Call

Center

21%

Online

66%

Call

Center

34%

Online

70%

Call

Center

22%

Mobile

8%

Emerging Online Delivery Platforms and Expansion

of Virtual Stores Intensifies Competition

Note: All trademarks and logos are the property of their respective owners.

Consumers are Experiencing and Learning

• Attracted by Significant Discounts and Deals

• But are Beginning to See the Difference

Between Pros and Amateurs (and Even Fakes)

181Chinese

Diverse Menu50% Asian 50% Western

• Dedicated team

• Tech-savvy leader

• More technology

• Offer More and Better Food Options

• Leverage 3rd Party Platform

& Resources

• Accelerate Development

2015 Strategic Initiatives

Yum! China Remains the Best Restaurant Opportunity

Today Future

6,700+

ENVIABLE POSTION

China Division Units

3X

Stronger

BrandRedefine

Casual DiningThird Growth

Engine

Our Mission Stays the Same

“To become the best restaurant company, not only

in China, but in the world”

Yum Restaurants China

Team Mission Statement

At Pepsi spin off (October 1997)

A Brand New Day in India

Niren Chaudary

President, Yum! India

Youngest

Population*

Largest

Workforce*

India USA

+200MM

+20MM

Highest

Urbanization**

India will be the Largest

Consumer Market in the World

Growth in Workforce

through 2030**

*Source: Deloitte, India Matters: Winning in growth markets, 2013.

**Source: Standard Chartered, India in the Super-Cycle, 2011.

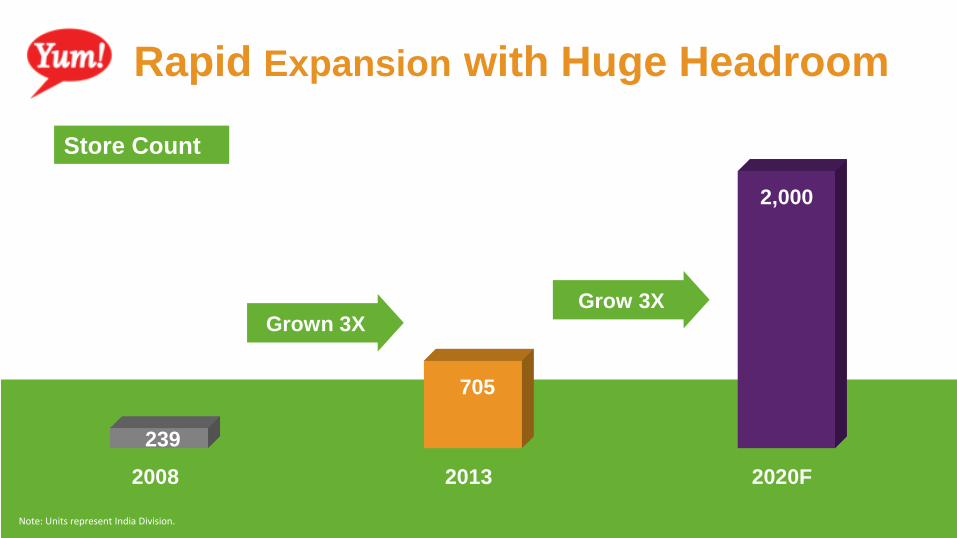

2008 2013 2020F

239

705

2,000

Rapid Expansion with Huge Headroom

Will Grow 3XGrown 3X

Note: Units represent India Division.

Grow 3X

Store Count

2014: Getting Stronger, More Relevant

Stronger

Buisness ModelsStronger

Brands

ANYONE,

ANYTIME

Established a Broad Concept

60%

Strong Core

Mix

… Accessible at Street-food Prices

8% 11% 12%7%

Krushers Oven Veg. Rice

Changing the Game with Rice

Indian

Flavored

Rice

Spicy Gravy

Chicken Popcorn

or Veg. Strips

Disruptive Innovation

to Drive Access

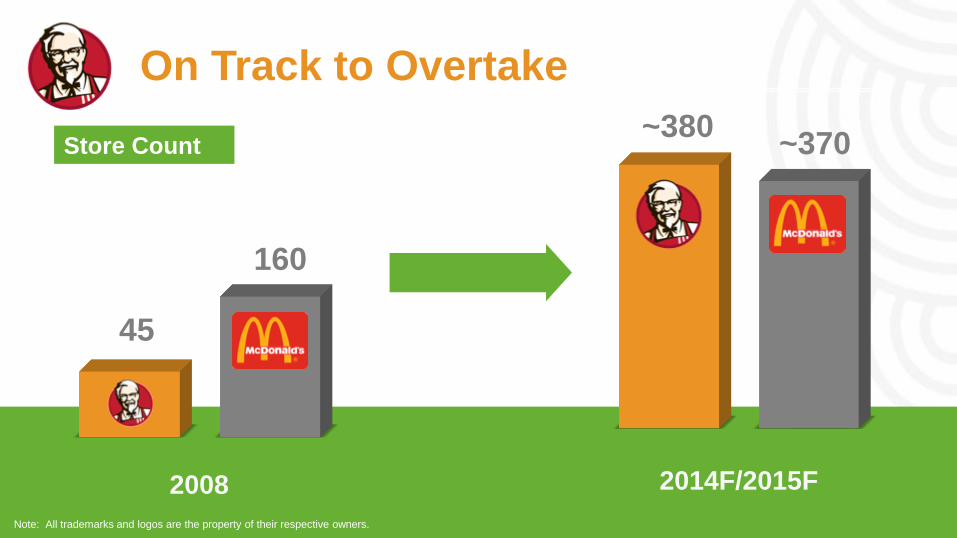

On Track to Overtake

45

160

2008 2014F/2015F

~380~370Store Count

Note: All trademarks and logos are the property of their respective owners.

Pizzas & Much More Food Delivery Expert

Most Trusted

Huge Opportunity, Gaining Ground

SSSG (YTD ‘14)

7%

-4%**

380

815*

Domino’s Market Cap $1.5Bn

* Source: Analyst Estimates. ** Source: Reported financials.

Note: All trademarks and logos are the property of their respective owners.

Store Count 2014F Same-Store Sales 2014F

Broaden RelevanceDisruptive Value

Our Plan to Win

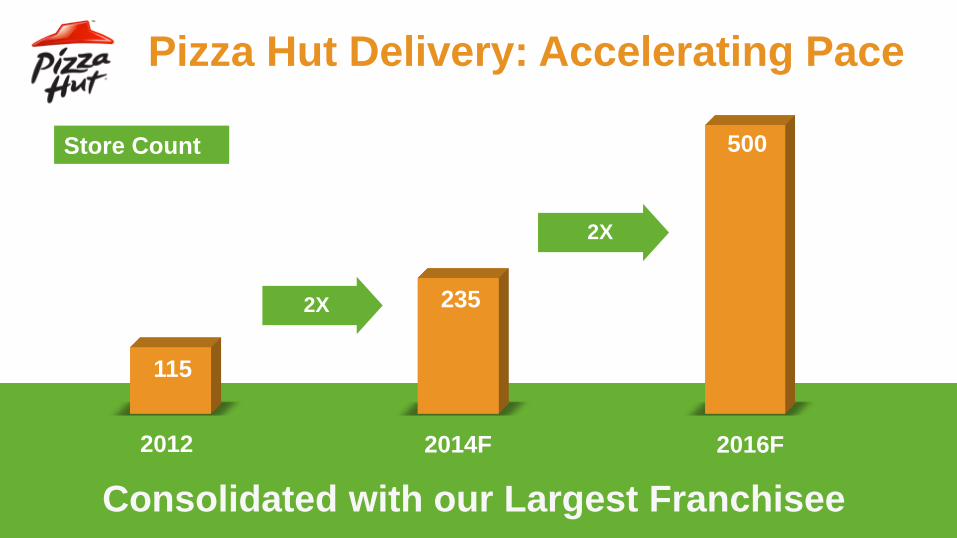

Pizza Hut Delivery: Accelerating Pace

115

235

500

2X

2012 2014F

2X

2016F

Consolidated with our Largest Franchisee

Store Count

Food

Adventure

Taco Bell: Exciting Start

$10

$12 $12

$14

2012 TB

Current2016F

(Scalable)

ATL

KFC

2008

WPSA $M

+20%

+17%

WPSA= Weekly per store average.

2015F

1,000 Units

2020F

2,000 UnitsNote: Units represent India Division.

Huge Opportunity with All Brands

Pat GrismerCFO, Yum! Brands

Driving Higher ReturnsFor Our Shareholders

2014: 1H China Success Dampened by Supplier Incident

Operating Profit Performance

116%

~(60%)

1H 2H

(6%)

10%+

1H 2H

Upward Momentum at Global Brand Divisions

China KFC / Pizza Hut / Taco Bell Divisions

Note: 2H is forecasted. Operating profit is before Special Items.

How We Create Value for Shareholders

NEW-UNITDEVELOPMENT

SAME-STORE SALES GROWTH

HIGHRETURNS

Our Formula for High Shareholder Returns

Franchise

Led with

Purposeful

Equity

Meaningful

Cash

Returned to

Shareholders

Double-Digit

Growth

Model+ + +

Optimal

Capital

Structure

Our Formula for Higher Shareholder Returns

Even More

Franchise Led with

Purposeful

Equity

Meaningful

Cash

Returned to

Shareholders

Double-Digit

Growth

Model+ + +

Optimal

Capital

Structure

Purposeful Equity: Earning the Right to Own

Key Ownership Criteria

Financial Strategic

High Return Provide Concept Leadership

High Growth Stimulate Franchise Development

Strong Operating Capability Develop/Export Talent

Purposeful Equity in China

• Compelling Investment Returns

• Vast Growth Potential

• Unmatched Capability & Infrastructure

First-Half Returns Give Confidence in China Development

Payback

3-4 Years <3 Years

2014 New Unit Economics - KFC

Tier 1 – 2 Cities Tier 3 – 6 Cities

Average Unit

Volume ($MM) $1.1 $1.0

Cash Margin 18% 18%

Cash Investment

($M)$600 $610

Note: Includes units opened August 2012 – July 2013.

2014 New Unit Economics – Pizza Hut

Tier 1 – 2 Cities Tier 3 – 6 Cities

Average Unit

Volume ($MM) $1.2 $1.2

Cash Margin 20% 24%

Cash Investment

($M)$620 $660

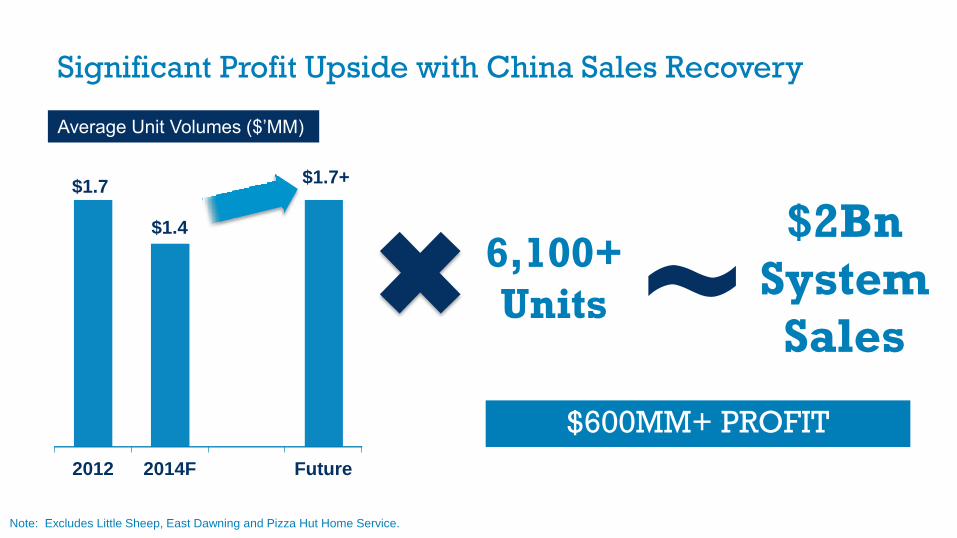

Significant Profit Upside with China Sales Recovery

2012 2014F Future

$1.7

$1.4

Average Unit Volumes ($’MM)

6,100+

Units

$2Bn

System

Sales

Note: Excludes Little Sheep, East Dawning and Pizza Hut Home Service.

~$1.7+

$600MM+ PROFIT

2013 2017F

Franchise Ownership Percentage

6%

~10%

Building Momentum on China Franchising

• Refranchising

• Franchise Development

75%

85-90%

2014F 2017F

Also Increasing Franchising in India

Franchise Ownership Percentage

• Refranchising

• Franchise Development

Over 90% Franchised Outside of China and India

90%

95%

85%

Franchise Ownership Percentage 2014F

Balanced with Purposeful Equity Positions

Franchising: A Powerful Business Model

Low Capital Low Volatility High Growth High Returns

80%

91%Mid 90s

2004 2014F By 2017F

Evolving to More Franchised Ownership

Franchise Ownership Percentage*

*Excluding China & India. Note: Ownership percentages indicate % of total units.

• Selective Refranchising

• Franchise Development

18%

24%

2010 2014F

Operating Margin for KFC, Pizza Hut, Taco Bell

Evolving to a Higher-Margin Business

Note: Excludes China & India.

by 2017F

30%+

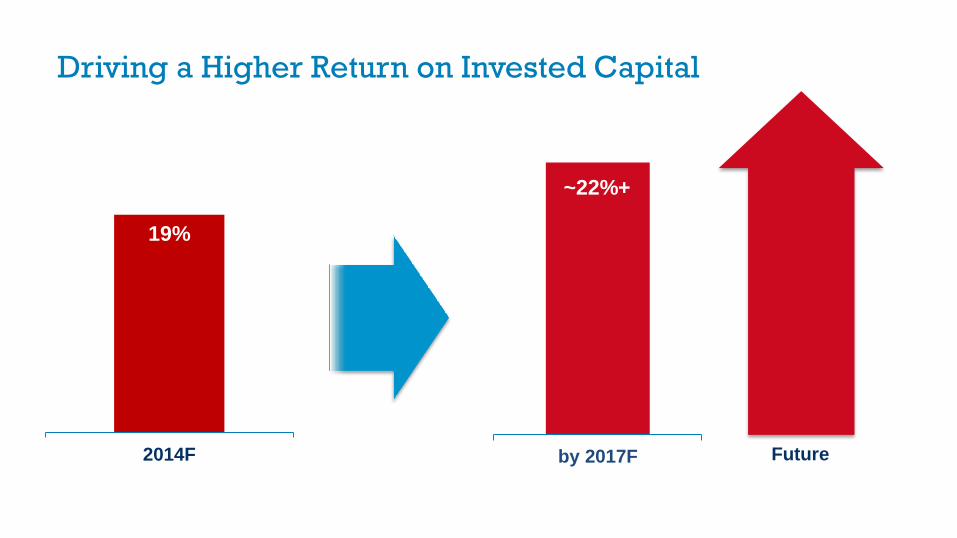

Driving a Higher Return on Invested Capital

19%

2014F by 2017F

~22%+

Future

And Sustaining Rapid Growth in Franchise Fees

2004 2009 2014F

24,600

27,700

32,900

Franchise Units

2004 2009 2014F

$1.0

$1.5

$2.0

Franchise Fees ($Bn)

Note: Franchised units include unconsolidated affiliates.

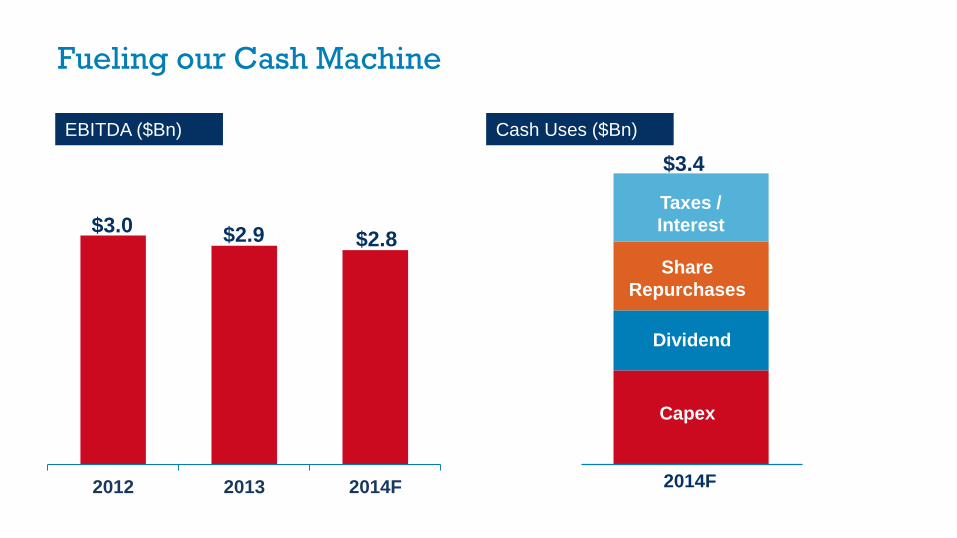

2012 2013 2014F

Fueling our Cash Machine

$2.8$2.9

EBITDA ($Bn) Cash Uses ($Bn)

$3.4

2014F

Capex

Share

Repurchases

Dividend

Taxes /

Interest$3.0

Sustaining High Shareholder Cash Returns

2004 2014F

Average Diluted Shares Outstanding (MM) Quarterly Dividend Per Share

$-

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

2004 2014

610

450

Note: Quarterly dividend and shares are split adjusted (May 2007 2-for-1 stock split.)

Averaging 3.5% Annual Cash Return

2010 2011 2012 2013 2014F

Dividend Share Repurchases

$6.4Bn

Returned

Over Last 5

Years

$0.8

Cash Returned ($Bn)

$1.2

$1.5

$1.4

$1.5

Maintaining Investment-Grade Credit Rating

1.5x1.3x

1.1x 1.2x

'09 '11 '13 '14F

3.4x 3.3x 3.2x3.4x

'09 '11 '13 '14F

3.5x Baa3

Debt/EBITDA Ratio Moody’s Adjusted Debt/EBITDAR Ratio

3.0x Baa3

Note: 3.0x to 3.5x is Moody’s target range for companies rated Baa3.

Low Investment Grade Rating Optimizes Capital Structure

Independent Bank Reviews: Sub-IG Leverage = Higher Cost of Capital + Limited Flexibility + Modest Accretion

75%

25%

Baa Drives Lowest

WACC Across

Economic CyclesBaa

Other

% of Time Yum! WACC is Optimized

Over the Long Term

China KFC PizzaHut

TacoBell

Financial

+1%

+3%

+7%

+1% +13%

ModeledGrowth

+1%

At least

10%

Ongoing Model Delivers Double-Digit Growth

Forecasted EPS Growth Before Special Items

Op Profit

Growth+15% +10% +8% +6%

China KFC/PH/TB Financial 2015F

Potential for Outsized Year in 2015

Forecasted EPS Growth Before Special Items

+6%

+6%

+1% +13% At least

10% excluding

KFC China

growth

(Ex KFC)

Strong Second Half will Fuel

2015 EPS Growth

KFC China SSSG is

Key Variable

2H’161H’162H’15

Yum! China: Potential for an Outsized Year in 2016 As Well

Recovery Recovered Ongoing …

1H’15

China KFC PizzaHut

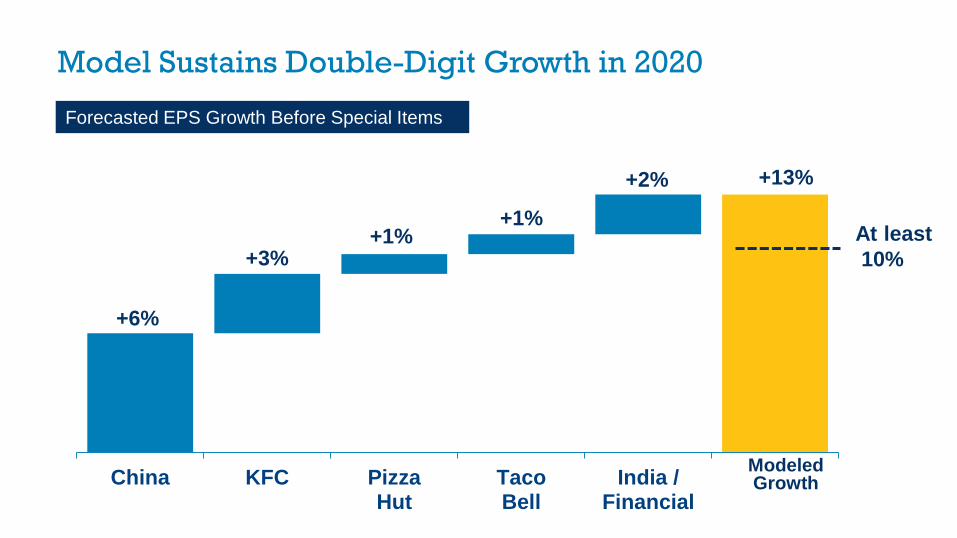

TacoBell

India /Financial

ModeledGrowth

At least

10%

+1%

+3%

+6%

+2% +13%

+1%

Model Sustains Double-Digit Growth in 2020

Forecasted EPS Growth Before Special Items

Our Formula for Higher Shareholder Returns

Even More

Franchise Led with

Purposeful

Equity

Meaningful

Cash

Returned to

Shareholders

Double-Digit

Growth

Model+ + +

Optimal

Capital

Structure