your - mascoma bank - mutually owned community …€¦ · 15 years 15 years: john ziegler, judy...

TRANSCRIPT

Deborah J. BlancSenior Asset Manager

Hanover, NH

Mascoma Savings Bank2016 Statement of ConditionMascoma Mutual Financial Services Corporation and Mascoma Savings Bank

Your Community Mutual Bank Since 1899

2016 was another year of steady progress and growth for Mascoma Savings Bank, coupled with some very significant changes. The biggest change came at the start of the year with the announcement of the impending retirement of Stephen Christy, who had led the Bank for the past 27 years. Steve and the Bank Board discussed his plans to retire and prepared their next steps for a full year before officially announcing that he would step down at the end of 2016. The Board worked diligently to define and catalog the techniques Steve used to serve the Bank so well for so many years, then examined the challenges the Bank expects to face in the coming decades, creating a picture of the skills necessary to build a bridge from our current success to a thriving future. With criteria in place for the new CEO, they engaged the consultant services of Kaplan Partners of Philadelphia, Pennsylvania, to help cast a sufficiently wide net.

After a broad search that included more than 100 candidates, the Board found the ideal new leader right in our backyard. In June, the Board of Directors announced that Clayton R. Adams, a graduate of Dartmouth College and the Amos Tuck School of Business, with experience as CEO of two local companies that have national track records of success, would become the Bank’s next Chief Executive Officer. Clay not only showed the Board that he possesses the vision and knowledge to lead the Bank forward, but also his proven commitment to community perfectly serves the ideals on which the Bank is based. It was clear that he was the right choice. Clay officially began his employment at the Bank on November 1, but he had already spent quite a bit of time working with Steve in other capacities, learning about the Bank both as a Board member and the CEO-to-be.

STEADY GROWTH and a New Chapter

Stephen F. Christy

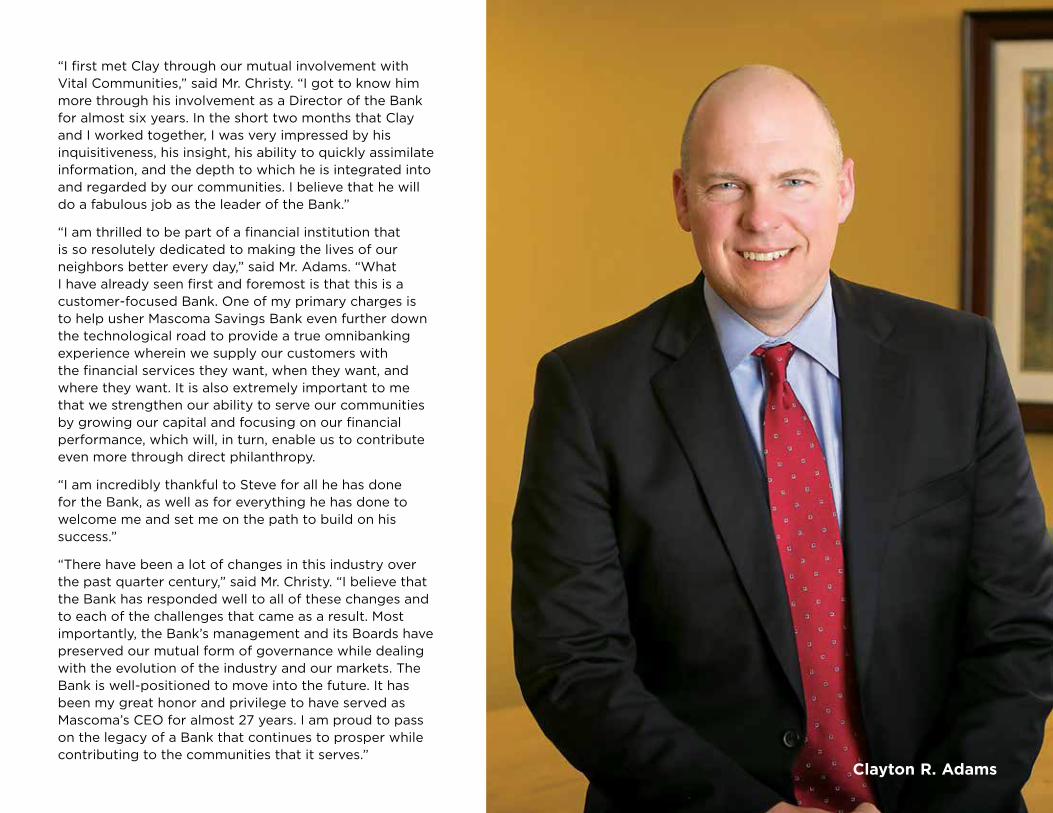

“I first met Clay through our mutual involvement with Vital Communities,” said Mr. Christy. “I got to know him more through his involvement as a Director of the Bank for almost six years. In the short two months that Clay and I worked together, I was very impressed by his inquisitiveness, his insight, his ability to quickly assimilate information, and the depth to which he is integrated into and regarded by our communities. I believe that he will do a fabulous job as the leader of the Bank.”

“I am thrilled to be part of a financial institution that is so resolutely dedicated to making the lives of our neighbors better every day,” said Mr. Adams. “What I have already seen first and foremost is that this is a customer-focused Bank. One of my primary charges is to help usher Mascoma Savings Bank even further down the technological road to provide a true omnibanking experience wherein we supply our customers with the financial services they want, when they want, and where they want. It is also extremely important to me that we strengthen our ability to serve our communities by growing our capital and focusing on our financial performance, which will, in turn, enable us to contribute even more through direct philanthropy.

“I am incredibly thankful to Steve for all he has done for the Bank, as well as for everything he has done to welcome me and set me on the path to build on his success.”

“There have been a lot of changes in this industry over the past quarter century,” said Mr. Christy. “I believe that the Bank has responded well to all of these changes and to each of the challenges that came as a result. Most importantly, the Bank’s management and its Boards have preserved our mutual form of governance while dealing with the evolution of the industry and our markets. The Bank is well-positioned to move into the future. It has been my great honor and privilege to have served as Mascoma’s CEO for almost 27 years. I am proud to pass on the legacy of a Bank that continues to prosper while contributing to the communities that it serves.”

Clayton R. Adams

Nothing we do exemplifies the value of being a mutual Bank more than Mascoma Community Development. The establishment of Mascoma Community Development was the next progressive step in the work we have been doing for the past eight years in utilizing New Markets Tax Credit (NMTC) allocations from the U.S. Treasury CDFI Fund to direct capital investment into underserved communities through mission-focused projects.

Mascoma Community Development focuses primarily on helping to ensure that distressed communities throughout Northern New England have access to flexible capital that will increase employment and community services where they are needed the most—it also has the ability to help launch and support projects throughout the United States. The NMTC program has proven to be an effective tool, helping us achieve our mission of supporting community development and stimulating economic growth in low-income communities across our region. We are pleased the CDFI is supportive of our efforts.

Mascoma Community Development

FOCUS ON

SUPPORTING COMMUNITY DEVELOPMENT AND STIMULATING ECONOMIC GROWTH

Mascoma Community Development received its first NMTC allocation of $55 million from the U.S. Treasury in 2015. In 2016, we made our first NMTC allocation, along with a NMTC leveraged loan, for a project in Berlin, New Hampshire, that built a new, state-of-the-art steel fabrication plant, creating new jobs for the skilled employees in the North Country. We currently have multiple projects in the development phase.

On November 17, the Bank learned that it had received its second NMTC allocation from the U.S. Treasury. This allocation was for $50 million. Mascoma Community Development is using a portion of these NMTCs to fund a $5.5 million small business loan pool, which includes investment directly from Mascoma Savings Bank.

Eligible borrowers will benefit by receiving 50-percent- below-market interest rates, among other flexible debt features. This loan pool will be used to finance eligible business expansion or equipment purchases ranging from $500,000 to $2 million. This fund focuses solely on projects and businesses in Vermont, New Hampshire, and Maine that serve communities classified as severely distressed or highly distressed by the U.S. Census Bureau. These loans are prioritized for job creation, downtown redevelopment, community facilities, and business expansion projects that enhance opportunities for quality jobs and community services.

“ Through our NMTC program, Mascoma Community

Development enabled Capone Iron Works to build an all

new steel fabrication plant in Berlin, New Hampshire. In a

community where another plant had closed eight years

earlier, now 25 skilled laborers are again fabricating steel

and helping grow the local economy.”

—Richard Jennings,

Managing Director, Mascoma Community Development

SUPPORTING COMMUNITY DEVELOPMENT AND STIMULATING ECONOMIC GROWTH

15 Years

15 YEARS: John Ziegler, Judy Gilbert, Leslie Ashley, Jessica Danner, Tom Hoyt, Daryl Dean, Patti Putnam, Jerri Danieli, Rich Kozlowski, Alice DeNike, Lora Lee Collins, Jackie Geer, Scott Hartell, Shirley Mower-Fenoff

(not shown: Holly Ueda, Heather Shepard, Kasie Dirkse, Patrick Eufemia, Cindy McClain, Jessica Berardino)

MUTUALLY OWNED

Chartered to Serve

the Community

20 Years 30 Years

35 Years

25 Years

20 YEARS: Addy Williams, Heather Powers, Gayle McFarland, Don Thompson, Donna Burnham (not shown: Teresa Fazio) 25 YEARS: Doreen McKinney, Samantha Pause 30 YEARS: Cheryl White (not shown: Janet Bishop)

35 YEARS: Cindy Paulhus, Glen Valentine, Ester Dobbins-Marsh

Mascoma Savings Bank is a mutually owned bank, which means it is chartered to serve the community and is not owned by stockholders. Today, only 8 percent of banks in the United States are mutually owned, yet mutual banks are some of the best stewards of community prosperity and rank among the most stable financial institutions.

Mascoma Savings Bank’s organizational structure further underlines its commitment to community. The Bank’s Board of Directors is elected by the Mascoma Savings Bank corporators, who reflect the breadth and needs of the area where we live, and our 340 employees are integral parts of the communities we serve.

Our long term commitment to our employees, together with their commitment to the Bank and the communities we serve, constantly strengthen these bonds.

FOCUS ON

Mascoma Savings Bank Foundation

Mascoma Savings Bank and the Mascoma Savings Bank Foundation together gave $937,479 in community grants in 2016, supporting community organizations such as the Vermont Institute for Natural Science (VINS).

VINS is a nonprofit, member-supported, environmental education, research, and avian rehabilitation organization headquartered at the VINS Nature Center in Quechee, Vermont. Open year-round, the 47-acre campus, adjacent to Quechee State Park, features 17 state-of-the-art raptor enclosures, four exhibit spaces, two classrooms, and miles of interpretive nature trails. VINS places a priority on making high-quality, compelling, fun environmental education programs and learning opportunities accessible to more people and communities. Mascoma Savings Bank has been a decades-long supporter of VINS because the organization entices and excites people of all ages to care for the natural world around us and to appreciate the uniqueness of this area of the world.

MUTUAL SAVINGS BANKS HAVE THEIR ROOTS IN PHILANTHROPY

Mutual savings banks have their roots in philanthropy. The first mutual savings bank was organized by the Reverend Henry Duncan in Ruthwell, Scotland, more than 200 years ago. Mascoma Savings Bank was founded in 1899 by a group of individuals who “invested” small sums of money to capitalize the Bank with no expectation of any personal financial return.

Mascoma Savings Bank was the first mutual bank in either New Hampshire or Vermont to form and fund a charitable foundation, and the Bank is always looking for ways to do more and make an even greater impact. Step one is helping to grow the Foundation, so that its ability to give can increase year after year—this comes through our annual contribution from the Bank’s earnings.

In turn, the Foundation directly supports entities in the community. Since its establishment in 1988, the Mascoma Savings Bank Foundation has contributed more than $3.9 million to local nonprofit organizations.

During the past 30 years, the sprouts of giving and direct support that started with the Foundation have grown exponentially. Today, Mascoma Savings Bank’s commitment to the community builds on the gifts from the Foundation by directly supporting local nonprofits and municipalities to help them thrive more every year. Together with the Foundation’s contributions, Mascoma Savings Bank was the source of $937,479 of direct support for community organizations based in New Hampshire and Vermont in 2016.

Foundation $85,320

Bank $129,957

Foundation $104,030

Bank $281,602

Foundation $5,688

Total Giving $215,277

Total Giving $385,632

Total Giving $625,394

1996

1988

2000

MUTUAL SAVINGS BANKS HAVE THEIR ROOTS IN PHILANTHROPY

Foundation $196,872

Bank $428,522

Foundation $227,237

Bank $710,242

Total Giving $625,394

Total Giving $937,479

2008

2016

SENIOR Leadership Team

Donald N. Thompson Senior Vice President, Chief Financial Officer and Treasurer

Robert T. Boon Senior Vice President, Wealth Management

Samantha L. Pause Senior Vice President,

Marketing, Sales, and Service

Kenneth D. Wells Senior Vice President, Retail Lending

Beverly A. Widger Senior Vice President,

Human Resources

Christine E. Morin Senior Vice President,

Operations and Chief Risk Officer

Debra L. Carter Senior Vice President,

Retail Services

Kenneth E. Howe Senior Vice President, Commercial Services

Richard S. Jennings Senior Vice President,

Mascoma Community Development

Philip S. Latvis CEO, Centurion Insurance Group

Barry E. McCabe Executive Vice President, Chief Operating Officer

Clayton R. Adams President & CEO

As a mutually owned community bank, we derive our strength from serving our neighbors and from their support of us. We are proud to be the bank of choice for many of the municipalities that we serve, including the City of Lebanon. The geographic diversity among our Corporators and Board of Directors brings the perspectives and needs of the broad range of the towns and cities that surround us to our leadership. We are grateful for their commitment and their willingness to share their time and knowledge to make the Bank better and our communities better places to live.

BOARD and Corporators

Clayton R. Adams Norwich, VT

Joel J. Bedor Littleton, NH

Timothy C. Briglin Thetford Center, VT

Stephen F. Christy Lebanon, NH

Paul B. Gardent Etna, NH

Deirdre B. Goodrich Norwich, VT

Gary W. Gray Westmoreland, NH

Daniel P. Jantzen Etna, NH

Sara L. Kobylenski North Hartland, VT

Barry E. McCabe West Hartford, VT

Daniel B. McGee Lebanon, NH

Catherine Richmond Norwich, VT

CHAIR Gretchen E. Cherington Meriden, NH

VICE CHAIR Frank J. Leibly III Taftsville, VT

SECRETARY Edward T. Kerrigan Hanover, NH

Clayton R. AdamsNorwich, VT

Joel J. BedorLittleton, NH

Jay BoucherEnfield, NH

Robert E. Bowers, Jr.New London, NH

Timothy C. BriglinThetford Center, VT

Gretchen E. CheringtonMeriden, NH

Stephen F. ChristyLebanon, NH

Stuart T. CloseNorwich, VT

Susan E. CoburnSouth Strafford, VT

Doug CooleyWindsor, VT

Philip N. CronenwettEnfield, NH

Carol Ann CunninghamWoodstock, VT

James L. DamrenWest Lebanon, NH

Lang DurfeeBethel, VT

Patti E. FriedmanLebanon, NH

Paul B. GardentEtna, NH

Deirdre B. GoodrichNorwich, VT

Gary W. GrayWestmoreland, NH

Rebecca HamiltonGilsom, NH

Judy L. HaywardSouth Royalton, VT

Allen J. Hinkle, M.D. Lebanon, NH

John A. HochreiterEtna, NH

Katharyn R. HokeNew London, NH

Ralph Degnan HoughGrantham, NH

Joy L. Hutchins,Plainfield, NH

Daniel P. JantzenEtna, NH

Meredith M. JohnsonLebanon, NH

Jean E. KennedyPlainfield, NH

Edward T. KerriganHanover, NH

Sara L. KobylenskiNorth Hartland, VT

Mary Ann KristiansenRoxbury, NH

Patricia A. LaddChelsea, VT

David P. LaurinWhite River Junction, VT

Teresa J. LeBlancNew London, NH

Frank J. Leibly IIITaftsville, VT

Jennifer F. LevyNorwich, VT

Joseph M. LongacreNorth Haverhill, NH

Peter A. Mason, M.D.Lebanon, NH

Barry E. McCabeWest Hartford, VT

Sally A. McEwenLebanon, NH

Daniel B. McGeeLebanon, NH

Edward D. McGee, Jr.Canaan, NH

Deborah Field McGrathGrantham, NH

Virginia L. McGrodyEnfield, NH

Robert L. MeyersWoodstock, VT

Katherine J. MilliganThetford, VT

Margaret N. MitchellCanaan, NH

Dr. Susan E. MooneyGrantham, NH

Robert E. MosesLebanon, NH

Gary R. NeilQuechee, VT

Sonia O. O’BanionWilder, VT

Hildegard OjibwayWhite River Junction, VT

Patricia O. O’NeillWindsor, VT

Patricia PalmiottoHanover, NH

Chester R. PashoHartland, VT

Rebecca S. PowellEnfield, NH

Scott W. PutneyBethel, VT

Susan A. ReevesNew London, NH

Catherine RichmondNorwich, VT

Robert N. RickerLebanon, NH

Shelley M. Seward Brownsville, VT

Anne M. Sprague Plainfield, NH

Victor St. Pierre Charlestown, NH

Thomas F. Terry, O.D. White River Junction, VT

Tami J. Weeks Windsor, VT

Todd P. WinslowWilder, VT

CORPORATORS (as of 12/31/16)

BOARD OF DIRECTORS (as of 12/31/16)

Cash and Cash

Equivalents

$21,447,583

U.S. Government

Securities and

Obligations

$133,733,340

Other Investments

$54,377,116

Consumer and

Other Loans

$206,358,169

Less: Allowance

for Loan Losses

–$13,522,238Bank Building and Equipment

$25,721,278

Other Assets

$59,502,414

2016 was a year of exceptional asset growth in a slow-growth economy. On October 24, assets topped $1.5 billion for the first time in its history.

This growth took place exclusively in our loan portfolio. For the year, residential loans increased by almost $71.5 million, or 14 percent. Commercial real estate loans increased by $45.5 million, or 10.5 percent. Overall the Bank’s total assets grew by $117.1 million, or 8.2 percent.

Concurrent with these increases in loan balances, the Bank has continued to reduce the rate of delinquency and general market conditions have continued to improve. During the past three years, management has worked to resolve several delinquent credits and, as a result, the Bank has been able to reduce reserve requirements. As of December 31, 2016, the Bank’s required allowance for loan loss has been reduced to 1.14% from the end of 2015 when the Bank was required to hold 1.34% in reserves to offset potential losses.

MASCOMA Mutual Financial

Services Corp

Real Estate

Mortgage Loans

$1,061,535,624

Total Assets

2016

$1,549,153,287

CONSOLIDATED STATEMENT OF CONDITION12 months ending

12-31-201512 months ending

12-31-2016

ASSETS

Cash and Cash Equivalents 19,936,279 21,447,583

U.S. Government Securities and Obligations 105,349,990 133,733,340

Other Investments 81,482,966 54,377,116

Real Estate Mortgage Loans 944,557,005 1,061,535,624

Consumer and Other Loans 208,163,063 206,358,169

Total Loans 1,152,720,068 1,267,893,793

Less: Allowance for Loan Losses (13,741,238) (13,522,238)

Net Loans 1,138,978,830 1,254,371,555

Bank Building and Equipment 27,169,343 25,721,278

Other Assets 59,145,998 59,502,414

TOTAL ASSETS $1,432,063,407 $1,549,153,287

LIABILITIES

Demand and NOW Deposits 424,600,404 446,033,920

Savings, Time and Other Deposits 784,386,929 786,098,218

Total Deposits 1,208,987,333 1,232,132,138

Sweep Accounts 18,026,854 15,552,715

Subordinated Debt 14,502,531 14,602,580

FHLB Borrowings 53,040,684 142,295,903

Total Borrowings 85,570,068 172,451,198

Other Liabilities 12,784,483 15,630,899

TOTAL LIABILITIES 1,307,341,884 1,420,214,235

CAPITAL

Retained Earnings/Surplus 126,957,063 134,251,483

Unrealized Gain/Loss on Investments/Pension, Net (2,235,540) (5,312,432)

TOTAL CAPITAL 124,721,522 128,930,052

TOTAL LIABILITIES AND CAPITAL FUNDS $1,432,063,407 $1,549,153,287

CONSOLIDATED INCOME STATEMENT12 months ending

12-31-201512 months ending

12-31-2016

INCOME

Interest Income on Loans & Investments 48,812,172 51,073,266

Interest Expense on Deposits & Borrowings (5,153,141) (6,599,160)

Net Interest Income 43,659,031 44,474,106

Provision for Loan Losses (2,225,000) (2,313,000)

Net Income After Provision for Loan Losses 41,434,031 42,161,106

Other Non-interest Income misc fees, overdrafts, service charges 11,888,789 11,409,403

Gains/Losses on Sales of Securities 1,002,690 80,999

Other Non-interest Expenses personnel, occupancy, other overhead (43,268,631) (44,727,284)

Income Before Income Taxes 11,056,879 8,924,225

Applicable Income Taxes (2,720,587) (1,630,220)

NET INCOME $8,336,291 $7,294,004

Quickvoice 800.707.3553 Toll Free 888.627.2662

www.mascomabank.com

Gwen Johns Float Branch Supervisor

Joe Scearbo Assistant Vice President,

Branch Manager

Norm Frates Vice President, Mortgage Lender

Jen Ellms Human Resources and Recruitment Assistant

Jazmin Guyette Head Teller

OUR VISION is to remain a mutually owned financial services company committed to exceeding the expectations of our customers, community, and employees.

OUR MISSION is to profitably provide, with knowledgeable service and convenient access, a broad array of financial products and services designed to meet the changing needs of our consumer and business customers.

OUR PURPOSE is to deliver exceptional customer service while improving our community and customers’ lives.