yemen environmental scanning “macro” 2013

TRANSCRIPT

Environmental Scanning “Macro” 2013

HSA MARKETING SECTOR

Content• Environmental Scanning “Macro”

Demographical analysis Economical analysis

HSA MARKETING SECTOR

Environmental

Macro Scanning

HSA MARKETING SECTOR

POPULATION..

•Yemen is the second largest state by area on the Arabian Peninsula, has a population of

around 25 million, more than double that of 1975, with population growth of around 3%

annually, Yemen’s population is expected to double in less than 25 years.

• It is an overwhelmingly young population, with around 43% under the age of 15, and a

median age of 18.1 years.

•The urban population makes up around one-third of the total, with an urbanization rate of

about 4.6% per year.

•It was ranked 154th. in the Human Development Index, a ranking that has generally held

steady since 1990.

WATER SCARCITY..

• It’s one of the most water-scarce countries in the world, lacking rainfall and surface water.

High population growth and water scarcity result in a chronic imbalance between water needs

and availability, The per capita water resources stand at 125 m3 compared to 1,250 m3 in the

Middle East and North Africa region, Agriculture uses by far the most water, with 96% of

water use, while QAT alone accounts for around 40%

Environmental Scanning “Macro”Executive Summary…

HSA MARKETING SECTOR

NATIONAL ECONOMY..

•After unification in 1990, the Government had to work to integrate two distinct economic

systems. Their efforts were hampered by the immediate return of some 850,000 Yemenis from

the Persian Gulf states, major reductions in aid flows, and the 1994 civil war. In 2009, Yemen

exported its first liquefied natural gas as part of wider efforts to diversify its economy.

Petroleum products make up around 70% of government revenue and some 25% of Yemen’s

GDP.

•The national currency, the RIAL, has depreciated significantly from 50 RIALS per dollar in 1995

to over 220 RIALS to the dollar by early 2010. During the peak of the crisis in 2011, the RIAL

reached close to 240 to the dollar. Given the country’s high reliance on imported commodities

–particularly food commodities – the currency’s deflation has contributed to significant,

broad-based inflationary pressures to the basic cost of living

•One-third of Yemen’s population is unemployed, while around 45% live below the poverty

line. In 2011, inflation was estimated to be 20%.

•Yemen is ranked as the 11th most food-insecure country globally with one in three Yemenis

suffering from acute hunger

Environmental Scanning “Macro”Executive Summary…

HSA MARKETING SECTOR

REVOLUTION & CHANGE..

2011 was a hugely unsettling year for Yemen. The country is facing a profound and complex

political and economic crisis, which both leads to and continues to be stimulated by social

unrest and outbreaks of violence. The backdrop to the recent violence are trends of

deteriorating economic fundamentals – declining oil production, an increasing current

account deficit, expanding fiscal deficit, depreciating currency and rising inflation. The World

Bank predicts that Yemen's oil and gas revenues will plummet over the next two years and

could fall to zero by 2017 as supplies run out. Given that oil provides around 90% of the

country's exports.

A SHOCK TO PURCHASING POWER..

When broad based inflation to the basic cost of living, including the cost of food, is

coupled with economic contraction

Environmental Scanning “Macro”Executive Summary…

HSA MARKETING SECTOR

Demographical analysisPopulation Amount & Growth TRENDS…

Y00 Y01 Y02 Y03 Y04 Y05 Y06 Y07 Y08 Y09 Y10 Y11 Y120

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

-2%

-1%

0%

1%

2%

3%

4%

17,479,210.018,078,040.018,701,260.019,349,880.020,024,870.020,727,060.021,456,190.022,230,530.023,013,380.023,822,780.023,495,360.024,133,490.024,771,810.0

3.4% 3.4% 3.4% 3.5% 3.5% 3.5% 3.5% 3.6% 3.5% 3.5%

-1.4%

2.7% 2.6%

PopulationAmount & Growth TRENDS

Population Growth

•Population growth trend gives good opportunity for annual consumption growth

•Consistency of population growth rate gives high certainty for growth strategy

formulation

•Comparing population growth rates trend with our actual sales growth trend; give

the real actual sales growth excluding normal growth came from the population

HSA MARKETING SECTOR

Demographical analysisGenerations & Age groups…

•64% of Yemen population age localized under 24 years, gives:

Amazing consumption opportunity

Opportunity to build loyalty

Higher consumption rate vs. other age segment

•Should to rescan & rediscover the NEW GENERATION

“behavior , thoughts , concepts , self attitude, buying motives, trends“

0-14 years 15-24 years 25-54 years 55-64 years Over 65 years0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

0%5%10%15%20%25%30%35%40%45%

10,533,096.0 5,232,712.0 7,464,921.0 893,660.0 647,420.0

43%

21%

30%

4% 3%

Yemen PopulationBy Age Group

Amount Weight

In such virgin markets,

companies can’t rely on the

heritage & loyalty anymore

BUT need to building again

with the new generation which

will be absolutely more tough

HSA MARKETING SECTOR

Demographical analysisLiteracy & Education RATES…

Increasing of Yemeni citizens literacy rate generally in both genders gives an

indication for culture upgrading which will automatically influence consumer

behavior and preferences

(15Y-24Y) (Over 15Y) (15Y-24Y) (Over 15Y) (15Y-24Y) (Over 15Y)Female Male Population

35%

17%

83%

57%

60%

37%

60%

35%

93%

74%

77%

55%

74%

47%

96%

81% 85

%

64%

Literacy Rate Per Age Group

Y94 Y04 Y10

•We should upgrade & modernize our future theme & spirit in all what we do

“consumer touch points” however in quality, packaging, media messages and so on ..

•Higher education levels might be opportunity and threat at the same time, however

companies can take it or not

HSA MARKETING SECTOR

Demographical analysisMobile & Internet Users GROWTH…

Internet & Cell phones rapid growth reflects the trend of Yemen population for

Urbanization maturity, cognition, realization and discernment

Are we using the right and efficient media tool ?

Are we able to adapt the right attractive messages which able to inspire consumers?

Are we creative enough to deliver our consumers with tomorrow’s needs today ?

Y00 Y02 Y05 Y07 Y08 Y09 Y10 Y11 Y12 -

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

0%

5%

10%

15%

20%

25%

12,000.0100,000.0220,000.0320,000.0370,000.02,349,000.03,053,700.03,969,810.05,160,753.00% 1% 1% 1% 2%

10%

13%

16%

21%

Internet UsersAmount & Share

Internet Users %Poplution

Y95 Y00 Y02 Y05 Y06 Y09 2010 2011 2012 -

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

0%

10%

20%

30%

40%

50%

60%

8,250.0 32,042.0411,100.02,000,000.02,978,000.011,085,000.011,085,344.012,349,860.013,893,265.00% 0% 2%

10%14%

47% 47%51%

56%

Mobiles UsersAmount & Share

Mobile Users %Poplution

HSA MARKETING SECTOR

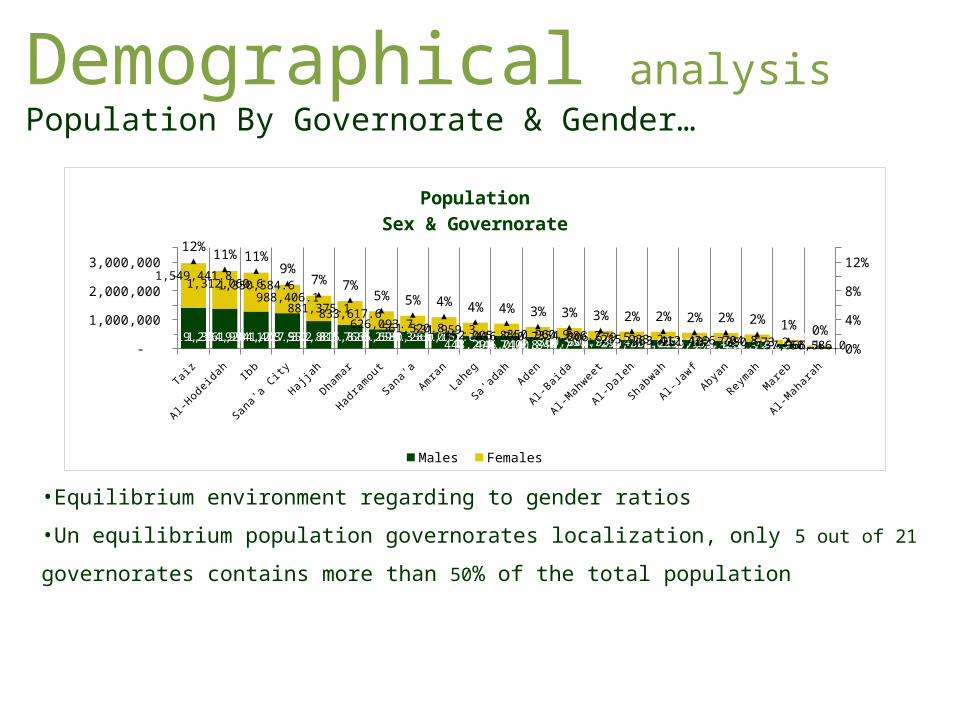

Demographical analysisPopulation By Governorate & Gender…

Taiz

Al-Hodeid

ah Ibb

Sana'a

City

Hajjah

Dhamar

Hadram

out

Sana'a

AmranLa

heg

Sa'ad

ahAden

Al-Baid

a

Al-Mah

weet

Al-Dale

h

Shab

wah

Al-Jaw

f

Abyan

Reymah

Mareb

Al-Mah

arah

- 500,000

1,000,000 1,500,000 2,000,000 2,500,000 3,000,000 3,500,000

0%2%4%6%8%10%12%14%

1,419,276.91,384,994.11,284,403.51,227,312.8952,887.7815,826.2665,699.3580,283.0560,163.6448,291.7446,016.8400,844.7360,953.7307,936.4299,771.6301,219.7296,156.4276,439.3237,729.5158,182.4

60,610.8

1,549,441.81,312,060.61,350,584.6

988,406.1881,375.1833,617.6

626,093.7561,520.8531,959.3452,005.8416,740.7350,960.9354,086.2306,679.5285,933.2283,412.4251,192.7266,704.8250,673.2137,965.150,586.0

12%11% 11%

9%7% 7%

5% 5% 4% 4% 4% 3% 3% 3% 2% 2% 2% 2% 2% 1% 0%

PopulationSex & Governorate

Males Females

•Equilibrium environment regarding to gender ratios

•Un equilibrium population governorates localization, only 5 out of 21 governorates

contains more than 50% of the total population

HSA MARKETING SECTOR

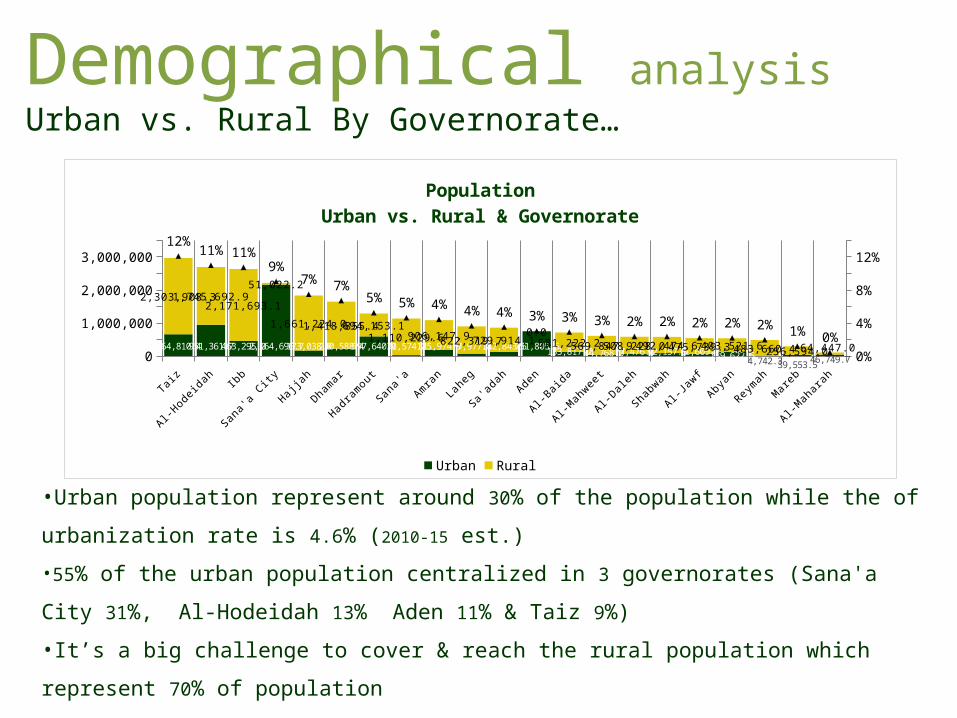

Demographical analysisUrban vs. Rural By Governorate…

•Urban population represent around 30% of the population while the of

urbanization rate is 4.6% (2010-15 est.)

•55% of the urban population centralized in 3 governorates (Sana'a City 31%, Al-

Hodeidah 13% Aden 11% & Taiz 9%)

•It’s a big challenge to cover & reach the rural population which represent 70% of

population

Taiz

Al-Hodeid

ah Ibb

Sana'a

City

Hajjah

Dhamar

Hadram

out

Sana'a

AmranLa

heg

Sa'ad

ahAden

Al-Baid

a

Al-Mah

weet

Al-Dale

h

Shab

wah

Al-Jaw

f

Abyan

Reymah

Mareb

Al-Mah

arah

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

0%

2%

4%

6%

8%

10%

12%

14%

664,810.4951,361.7463,295.02,164,696.7173,038.8230,588.4597,640.031,574.2185,974.977,977.8132,843.5751,805.6133,817.744,768.077,476.892,157.571,609.7139,622.54,742.3 39,553.546,749.7

2,303,908.31,745,692.92,171,693.1

51,022.2

1,661,224.01,418,855.4694,153.11,110,229.6906,147.9822,319.7729,914.1

0.0581,222.2569,847.9508,228.0492,474.6475,739.3403,521.6483,660.4256,594.064,447.0

12%11% 11%

9%7% 7%

5% 5% 4%4% 4% 3% 3% 3% 2% 2% 2% 2% 2%

1% 0%

PopulationUrban vs. Rural & Governorate

Urban Rural

HSA MARKETING SECTOR

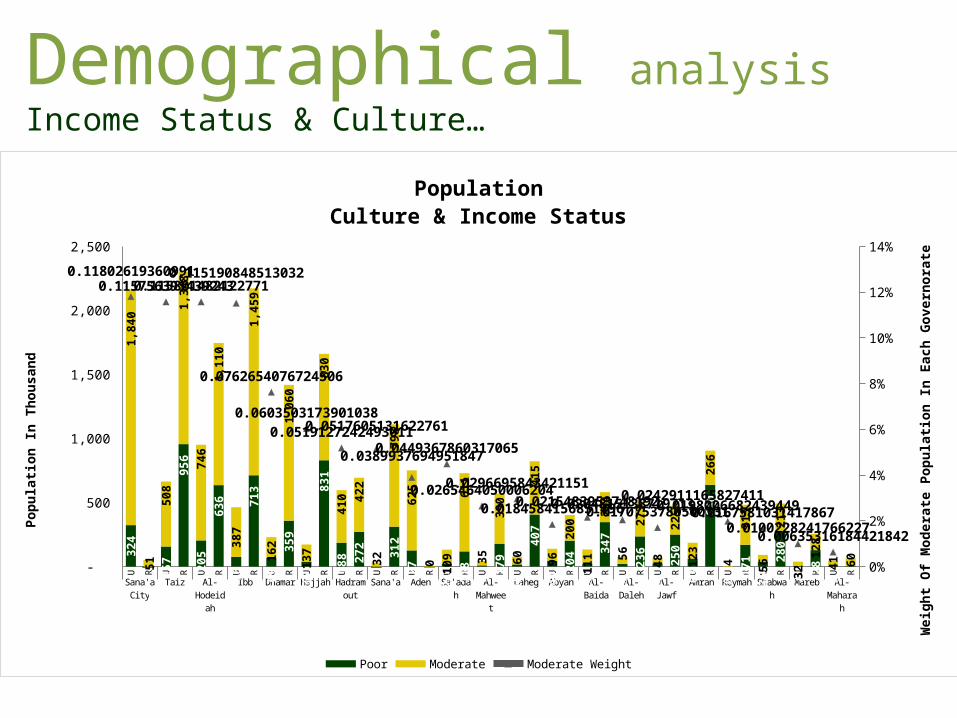

Demographical analysisIncome Status & Culture…

•Only 65% of the population have a good purchase power “moderate” while the

rest 35% are poor with low purchase power half of them considered as below the

poverty line population

•65% of moderate population “10.4mil” lives in rural areas, while only 35% “5.6mil”

lives in urban areas which means that rural areas contains double urban moderate

population

Poor Moderate -

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

1,457,497.8

5,618,606.8

7,043,845.2

10,407,050.2

PopulationCulture & Income Status

Urban Rural

23%

42%

29%

6%

What is our strategy to reach & cover urban ??

HSA MARKETING SECTOR

Demographical analysisIncome Status & Culture…

U R U R U R U R U R U R U R U R U R U R U R U R U R U R U R U R U R U R U R U R U R

Sana'a City

Taiz Al-Hodeidah

Ibb Dhamar Hajjah Hadramout

Sana'a Aden Sa'adah Al-Mah-weet

Laheg Abyan Al-Baida Al-Daleh Al-Jawf Amran Reymah Shabwah Mareb Al-Ma-

harah

-

500

1,000

1,500

2,000

2,500

0%

2%

4%

6%

8%

10%

12%

14%

324

- 1

57

956

205

636

76

713

69

359

36

831

188

272

-

312

127

-

24 1

18

10

179

18

407

44

204

22

347

22

236

23

250

63

640

0 1

71

36

280

7 1

28

5

4

1,84

0

5150

8

1,34

8

746

1,11

0

387

1,45

9

162

1,06

0

137

830

410 42

2

32

798

625

0 109

611

35

390

60

415

96

200

111

234

56

273

48

225

123

266

4

313

56

213

32

128

41 60

0.118026193609910.1157563914392430.115801482122771

0.115190848513032

0.0762654076724506

0.0603503173901038

0.05191272424930110.0517605131622761

0.03899376949518470.0449367860317065

0.02654640500062040.0296695843421151

0.01845841568514960.02154839537481920.02048151387197130.0170753780500331

0.02429111658274110.01980066824394490.0167581031417867

0.01002282417662270.00635316184421842

PopulationCulture & Income Status

Poor Moderate Moderate Weight

Popu

latio

n In

Tho

usan

d

Wei

ght O

f Mod

erat

e Po

pula

tion

In E

ach

Gove

rnor

ate

HSA MARKETING SECTOR

Shaping an effective & efficient distribution strategy require a deeply look into

previous rich graph which shows district opportunities and prioritizing them:

Only 4 governorates owns 46% of moderate population overall Yemen “Sana'a

City, Taiz, Ibb Al-Hodeidah” with 12% share for each

Rural areas considered “Goldmine”, Easily we can find the bulk of moderates

in each governorate in the urban areas “73% of Taiz, 79% of Ibb, 60% of Al-

Hodeidah, 87% of Dhamar, 86% of Hajjah, 51% of Hadramout and 97% of

Sana'a” This is what proves that 44% of total moderates localized in 6

governorate in RURAL areas only around 7 mil

Demographical analysisIncome Status & Culture…

Does our turnover breakdown by district match population & income status breakdown by

district ?

How to prioritize the governorate penetration based on each market attractiveness ?

Is it possible to capitalize on distribution & covering as one of the main competitive

advantages ?

Rural is “Goldmine” with high population, high purchase power “twice of rural”, lower

competition relatively to urban and hard to reach. Do we have smart tactics to penetrate ?

HSA MARKETING SECTOR

Next 4 slides contains graphs which classify regional market attractiveness based

on each region:

•Population

Percentage of (Urban/Rural/Total) Population to National Population

Percentage of (Urban/Rural) Population to Governorate Population

• Food Spending

Percentage of (Urban/Rural/Total) Food Spending to National Food Spending

Percentage of (Urban/Rural) Food Spending to Governorate Food Spending

(Urban/Rural/Total) Food Spending Per Capita in YER

• Income

Percentage of (Urban/Rural/Total) Moderates to National Moderates

Percentage of (Urban/Rural) Moderates to Governorate Moderates

Demographical analysisMarkets Attractiveness By Region…

NOW .. It’s time to prioritize our Penetration/ Expansion/ Market Development plan

Let’s formulate our DISTRIBUTION STRATEGY

IbbAbya

n

Sana'a

City

Al-Baid

aTa

iz

Al-Jawf

Hajjah

Al-Hodeid

ah

Hadram

out

Dhamar

Shab

wah

Sa'ad

ahSa

na'aAden

Laheg

Mareb

Al-Mah

weet

Al-Mah

arah

Amran

Al-Dale

h

Reymah

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10,000

20,000

30,000

40,000

50,000

60,000

11%2%

9%3%

12%2%

7% 11% 5% 7% 2% 4% 5% 3% 4% 1% 3% 0%4% 2% 2%

70%54%

85%

48%

62%

50% 52%

68% 64%74%

46%

83% 72%83%

53% 54%69%

91%

36%

56% 66%

12%

2%

12%

2%

12%

2%6%

12% 5%

8%

2%

5% 5%

4%

3% 1%3%

1%

2%

2% 2%

38% 42%

25%

44%39% 44%

53%

43% 44%38%

44%

42% 39%

29%

43% 42%46%

34%

44%

35% 41%

11%2%

11%3%

11%2%

8% 11%6% 7% 3% 3% 4% 3% 3% 1% 2% 1%

3% 2% 2%

Yemen Regional Total Markets AttractivenessBased on Purchasing Power Variables

%Population Nationaly %Moderate Governorate %Moderate Nationaly%Governorat Spending %National Food Spending Food Spending Per Capita in YER

Demographical analysisMarkets Attractiveness By Region…

IbbAbya

n

Sana'a

City

Al-Baid

aTa

iz

Al-Jawf

Hajjah

Al-Hodeid

ah

Hadram

out

Dhamar

Shab

wah

Sa'ad

ahSa

na'aAden

Laheg

Mareb

Al-Mah

weet

Al-Mah

arah

Amran

Al-Dale

h

Reymah

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

18%26% 98%

19% 22% 13%9%

35%46%

14% 16% 15%

3% 100%

9%13%

7%

42%

17% 13%

1%

7%

2%

31%

2%9%

1%

2%

13%

8%

3%1% 2%

0%11%

1%

1%

1%

1%

3% 1%

0%

15%18%

83%

16%

17%

9%

7%

28%32%

10%

10%13%

3%

83%

7%

11%

6%

37%

11%10%

1%

7% 2%

33%

2%

9%

1%

2%

13%7%

3%

1%

2%

1%

11%

1%

1%

1%

1%

2%1%

0%

29%38%

25%

35%29%

35%

42%

32% 38%

27%

45%38%

29%

29%

31%

36%

34%

36% 31%

30%

7%2%

35%

2%8%

1% 3%11% 8% 3% 2% 2% 0%

10% 1% 1% 1% 1% 3% 1% 0%

Yemen Regional Urban Markets AttractivenessBased on Purchasing Power Variables

%Urban Population Governorate %Urban Population Nationaly %Urban Moderate Governorate %Urban Moderate Nationaly%Urben Food Spending Governorate %Urben Food Spending Nationaly Urben Food Spending Per Capita in YER

Demographical analysisUrban Markets Attractiveness By Region…

IbbAbya

n

Sana'a

City

Al-Baid

aTa

iz

Al-Jawf

Hajjah

Al-Hodeid

ah

Hadram

out

Dhamar

Shab

wah

Sa'ad

ahSa

na'aAden

Laheg

Mareb

Al-Mah

weet

Al-Mah

arah

Amran

Al-Dale

h

Reymah

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10,000

20,000

30,000

40,000

50,000

60,000

82%74%

2%

81%

78%

87%91%

65% 54%86%

84%

85% 97%

0%

91% 87%93%

58%

83% 87% 99%

12%

2%

0%

3%

13%

3%

10%

10% 4%8%

3%

4%6%

0%

5% 1%

3%

0%

5% 3%3%

55%37%

2%

33%

45%

41%

45%

41% 33%

64%36%

71%70%

0%

46% 43% 64%54%

24%47% 64%

14% 2%

0%

2% 13%2%

8%

11%4%

10%2%

6%8%

0%

4% 1%4% 1%

3%

3% 3%

42% 45%

24%

47% 44%47%

55%52% 51%

41% 44%44% 39%

45% 46% 47% 33%

47%

35% 42%

13%2% 0% 3%

13%2%

11% 11% 5% 9% 3% 4% 7%

0%

4% 1% 3% 0% 4% 2% 2%

Yemen Regional Rural Markets AttractivenessBased on Purchasing Power Variables

%Rural Population Governorate %Rural Population Nationaly %Rural Moderate Governorate %Rural Moderate Nationaly%Rural Food Spendin Governorate %Rural Food Spending Nationaly Rural Food Spending Per Capita in YER

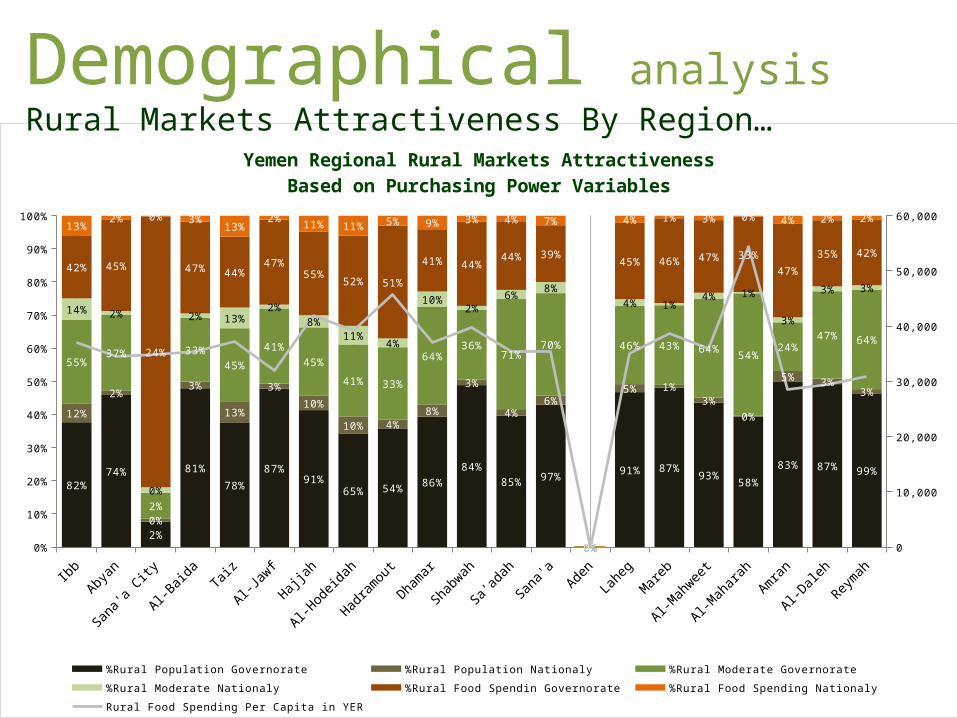

Demographical analysisRural Markets Attractiveness By Region…

11%

2%9%

3%

12%

2%

7%

11%

5% 7%2%

4%

5%

3%

4%

1%3%0%

4%

2%2%

11%

2%11%

3%

11%

2%

8%

11%

6% 7%

3%

3%

4%

3%

3%

1%

2%1%

3%

2%

2%

Ibb12%

Abyan2%

Sana'a City12%

Al-Baida2%

Taiz12%

Al-Jawf2%

Hajjah6%

Al-Hodeidah12%

Hadramout5%

Dhamar8%

Shabwah2%

Sa'adah5%

Sana'a5%

Aden4%

Laheg3%

Mareb1%

Al-Mahweet3%

Al-Maharah1%

Amran2%

Al-Daleh2%

Reymah2%

Yemen Regional Total Markets AttractivnessBased on Purchasing Power Variebles

1st. Moderate Nationally (Biggest)

2nd. National Food Spending

3rd. %Population Nationally

4th. Food Spending Per Capita

HSA MARKETING SECTOR

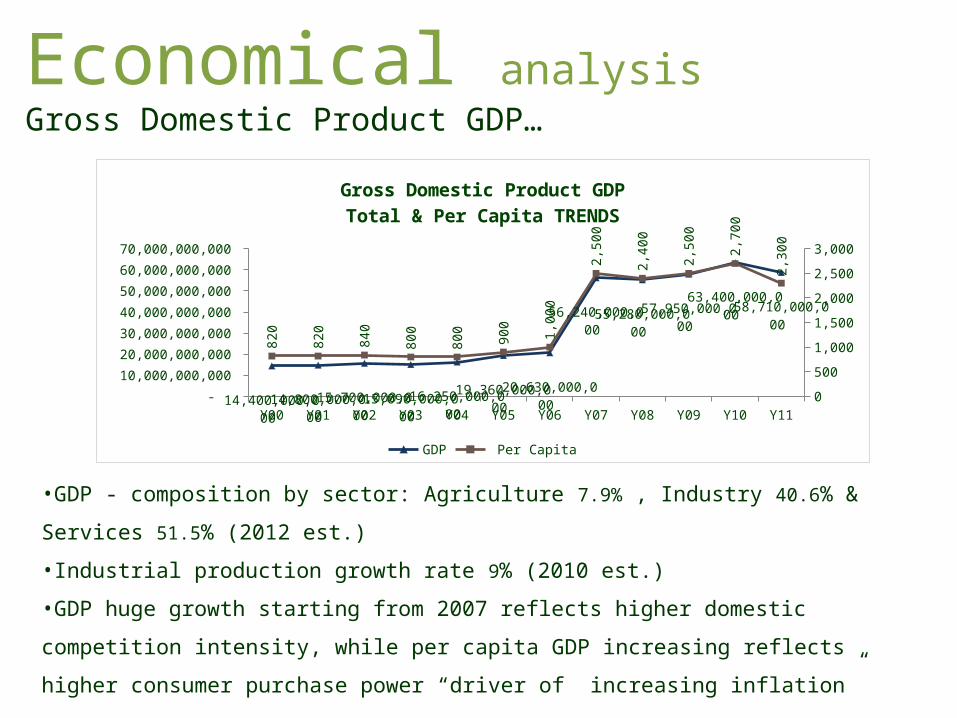

Economical analysisGross Domestic Product GDP…

•GDP - composition by sector: Agriculture 7.9% , Industry 40.6% & Services 51.5%

(2012 est.)

•Industrial production growth rate 9% (2010 est.)

•GDP huge growth starting from 2007 reflects higher domestic competition

intensity, while per capita GDP increasing reflects higher consumer purchase

power “driver of increasing inflation”

Y00 Y01 Y02 Y03 Y04 Y05 Y06 Y07 Y08 Y09 Y10 Y11 -

10,000,000,000

20,000,000,000

30,000,000,000

40,000,000,000

50,000,000,000

60,000,000,000

70,000,000,000

0

500

1,000

1,500

2,000

2,500

3,000

14,400,000,000 14,800,000,000 15,700,000,000 15,090,000,000 16,250,000,000 19,360,000,000 20,630,000,000

56,240,000,000 55,280,000,000 57,950,000,000 63,400,000,000

58,710,000,000

820

820

840

800

800

900

1,00

0

2,50

0

2,40

0

2,50

0

2,70

0

2,30

0

Gross Domestic Product GDPTotal & Per Capita TRENDS

GDP Per Capita

HSA MARKETING SECTOR

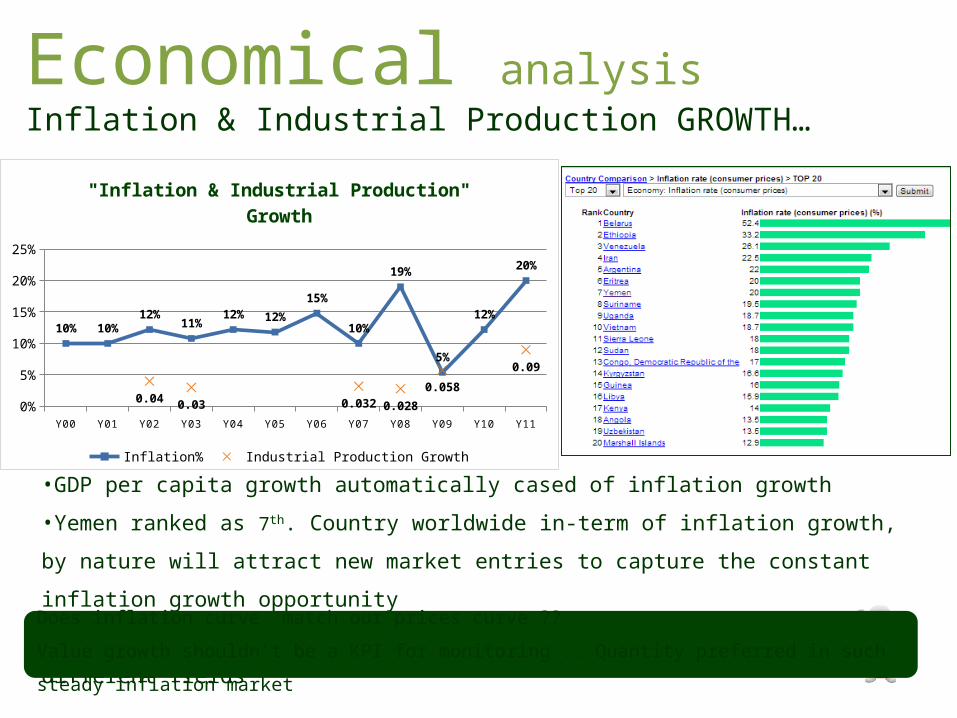

Economical analysisInflation & Industrial Production GROWTH…

•GDP per capita growth automatically cased of inflation growth

•Yemen ranked as 7th. Country worldwide in-term of inflation growth, by nature will

attract new market entries to capture the constant inflation growth opportunity

•Industrial production growth reflects competition intensity in different fields

Y00 Y01 Y02 Y03 Y04 Y05 Y06 Y07 Y08 Y09 Y10 Y110%

5%

10%

15%

20%

25%

10% 10%12%

11%12% 12%

15%

10%

19%

5%

12%

20%

0.040.03 0.032 0.028

0.058

0.09

"Inflation & Industrial Production" Growth

Inflation% Industrial Production Growth

Does inflation curve match our prices curve ??

Value growth shouldn’t be a KPI for monitoring .. Quantity preferred in such steady inflation

market

HSA MARKETING SECTOR

Economical analysisNational Trend For Foreign Investments Acquisition…

42

HSA MARKETING SECTOR

Economical analysisTrade Balance -Import & Export…

•Imports:

Commodities: Food & Live Animals, Machinery & Equipment and Chemicals

Partners: UAE 18.8%, China 11.8%, Saudi Arabia 8.9%, Kuwait 6.6%, India 6.5%,

France 4.7% and USA 4.2% (2011)

Y00 Y01 Y02 Y03 Y04 Y05 Y06 Y07 Y08 Y09 Y10 Y11 -

1,000,000,000 2,000,000,000 3,000,000,000 4,000,000,000 5,000,000,000 6,000,000,000 7,000,000,000 8,000,000,000 9,000,000,000

10,000,000,000

010000000002000000000300000000040000000005000000000600000000070000000008000000000900000000010000000000

4,200,000,000.04,200,000,000.03,900,000,000.03,400,000,000.0

3,920,000,000.04,470,000,000.0

6,390,000,000.0

8,210,000,000.08,980,000,000.0

5,810,000,000.07,460,000,000.07,590,000,000.0

2,300,000,000.02,700,000,000.03,000,000,000.02,900,000,000.03,040,000,000.03,730,000,000.0

4,190,000,000.05,040,000,000.0

8,830,000,000.0

7,520,000,000.0

8,350,000,000.08,260,000,000.0

Trade BalanceImport & Export TRENDS

Export Import

HSA MARKETING SECTOR

•Export growth gives a brilliant opportunity for company international expansion

•Imported growth reflects Yemeni consumer positive response toward the imported

products also indicates the increasing of consumer purchase power

We should continuously search for new opportunities beyond our national

boundaries; we have never been in a more internationalized and economically

competitive society than today.

A strategic plan should be conducted including answers for flowing questions:

Where is the attractive markets, Which countries to penetrate, How to enter (as an

exporter, licenser, joint venture partner or solo manufacturer), How to adapt our

products

and services features to fit each country, How to price our products in different

countries

& how to adapt effective communications which suits countries different cultures.

Economical analysisTrade Balance -Import & Export…

HSA MARKETING SECTOR

There are many potentially advantageous reasons to initiate, continue and

expanding exports:

Total turnover growth

Absorb excess capacity

Reduce overall unit cost

Spread economic risk over a wider number of markets

Extending product life cycle – existing products which are in the maturity or

declining stage might be reintroduced in another virgin market

Foreign market maybe has lower competition intense

Power and prestige in the domestic market will significantly enhance

companies bargaining power with consumers, customers, suppliers and local

manufactures

Increase media spending effectiveness through extending the prospects

segments

Economical analysisTrade Balance -Import & Export…

HSA MARKETING SECTOR

Environmental Scanning “Macro”Challenges…

Hard geographical natural, It's too tough to

get the full access for prospective

consumers

Economical and currency

fluctuation

Political instability & lack of

safety

Imported goods penetration characterized as (high quality, reasonable margins & affordable

prices)

Yemen consumer’s progressive trend toward

imported products to (Satisfy Ego & Better

quality perception)Result of Tribalism and Ethnicity, Clustered Demand formed “Consumer needs and desires

grouped into too many identical clusters (segments), each with its own set of purchase criteria

and preferences”

HSA MARKETING SECTOR

Environmental Scanning “Macro”What To Do !!

MANAGE THE CHANGE

In today’s Yemen business

environment more than in

any era, the only constant

is change, we should

effectively manage this

change, continuously

adapt bureaucracy,

strategies, system,

products and culture to

survive the shocks and

prosper from the forces

that decimate the

competition

VALUE

DIFFERENTIATION

We should find something

that rival firms can’t do,

or own something that

rival firm’s desire, which

can provide us with

competitive advantage,

gaining and sustaining

competitive advantage is

essential for long-term

success

STP

Companies can rarely

satisfy everyone in the

market, so we need to

clearly identify & profile

distinct groups who might

prefer or require varying

products and services

mixes by examining

demographic,

psychographic and

behavioral differences

among buyers

Thank YouAhmed Hamdy