wright report2 2012

TRANSCRIPT

July - December, 2012

www.WrightRealEstate.us Page 1 (916) 726-8308

Wright Report

Perspectives and Overview of Northern California’s

Residential Real Estate Market:

Including Statistics and Trends for the United States, State of California, and Northern

California Counties. Research, Charts, and Graphs for areas within Sacramento, Placer, Yolo,

El Dorado & San Joaquin Counties.

July to December, 2012

TTHHEE WWRRIIGGHHTT RREEPPOORRTT

July - December, 2012

www.WrightRealEstate.us Page 2 (916) 726-8308

Wright Report

The Wright Report

Prepared by:

Prepared By: Joel Wright

Document Version: Final

Last Updated On: March, 2013

July - December, 2012

www.WrightRealEstate.us Page 3 (916) 726-8308

Wright Report

This work is licensed under the Creative Commons Attribution-ShareAlike 3.0 Unported

License. To view a copy of this license, visit http://creativecommons.org/licenses/by-sa/3.0/

or send a letter to Creative Commons, 171 Second Street, Suite 300, San Francisco,

California, 94105, USA.

July - December, 2012

www.WrightRealEstate.us Page 4 (916) 726-8308

Wright Report

TABLE OF CONTENTS

TABLE OF CONTENTS ....................................................................................................................... 4

EXECUTIVE SUMMARY:.................................................................................................................... 5

THE EXPERTS WEIGH IN: .................................................................................................................. 6

Sacramento Appraiser: Ryan Lundquist ....................................................................... 6

Real Estate Attorney: Stephen Beede .......................................................................... 7

Mortgage Broker: Jeff Marr .......................................................................................... 9

MARKET FOCUS: The Budding Recovery ....................................................................................... 10

MARKET UPDATE: .......................................................................................................................... 14

THE ECONOMY: ............................................................................................................................. 18

BANKING & LENDING: ................................................................................................................... 20

DISTRESSED PROPERTIES: .............................................................................................................. 22

COUNTY STATISTICS: ..................................................................................................................... 25

Sacramento County .................................................................................................... 25

Placer County .............................................................................................................. 26

El Dorado County ........................................................................................................ 28

Yolo County ................................................................................................................ 29

San Joaquin County ....................................................................................................................... 30

HISTORICAL PRICE GRAPHS: .......................................................................................................... 31

PLACER COUNTY: ........................................................................................................................... 32

SACRAMENTO COUNTY: ................................................................................................................ 34

RESOURCES: ................................................................................................................................... 42

July - December, 2012

www.WrightRealEstate.us Page 5 (916) 726-8308

Wright Report

EXECUTIVE SUMMARY:

The current residential real estate market for the greater Sacramento

Metro area is poised for one of the greatest increases in appreciation

ever seen. Not only are rates at all time lows, but rents remain

strong, demand is increasing, and prices are being driven

progressively higher by forces on all sides.

By examining the real estate market, banking, lending, economic

issues, new homes, distressed inventory and sales, and up to date

market statistics one can see that the market is moving upward

rapidly and those who purchase now will realize huge price gains over

the next few years.

The turnaround in the residential market has two causes, both of

which have been artificially created to generate recovery: first, low

interest rates and second, low inventory (low supply and rising

demand). Interest rates are near 3.5%, and inventory is around 3

weeks of homes for sale.

As the two forces play out, prices rise: developers build new homes

and construction results in new jobs; reducing unemployment and

increasing tax revenues which leads to an overall economic recovery.

This situation is occurring not only in Sacramento County but in other

surrounding counties as well: Placer, Yolo, El Dorado, and San Joaquin.

Because of the rapid rise in prices there are numerous offers on each

property with many offers over asking price. It has definitely switched

to a seller’s market and it takes patience, persistence, and a great

team of professionals to navigate a real estate transaction successfully

in this turbulent market place.

July - December, 2012

www.WrightRealEstate.us Page 6 (916) 726-8308

Wright Report

THE EXPERTS WEIGH IN:

Sacramento Appraiser: Ryan Lundquist

The Market Shift in Sacramento

The Sacramento market from July through December 2012 can best be described as having shifted. Housing inventory saw a dramatic decline as the percentage of foreclosures dropped from 31.6% of the market in Q1 of 2012 to only 11% of the market in Q4 2012 in Sacramento County. This alone created heightened competition among buyers, but on top of that investor cash became a very dominant force in the market. By the end of 2012, 35.6% of all sales in Sacramento County were cash sales, and 49% of all sales under $200,000 were cash deals.

Beginning in August 2012 we began to see the private equity fund Blackstone purchase properties in mass in multiple counties surrounding Sacramento, but mostly in first-time buyer neighborhoods in Sacramento County under $200,000. They purchased close to 500 properties on MLS (and many off MLS too). With about 80% of their focus under $200,000, and combined with many other investors entering the market, we began to see buyers make more aggressive offers and even write purchase contracts well over asking price. Essentially we saw the market appreciate rapidly in the last two quarters of the year. One of the other byproducts of the increase of cash in the market was a 10% decline of FHA financing in the first-buyer market, and an increase in conventional financing across the board.

July - December, 2012

www.WrightRealEstate.us Page 7 (916) 726-8308

Wright Report

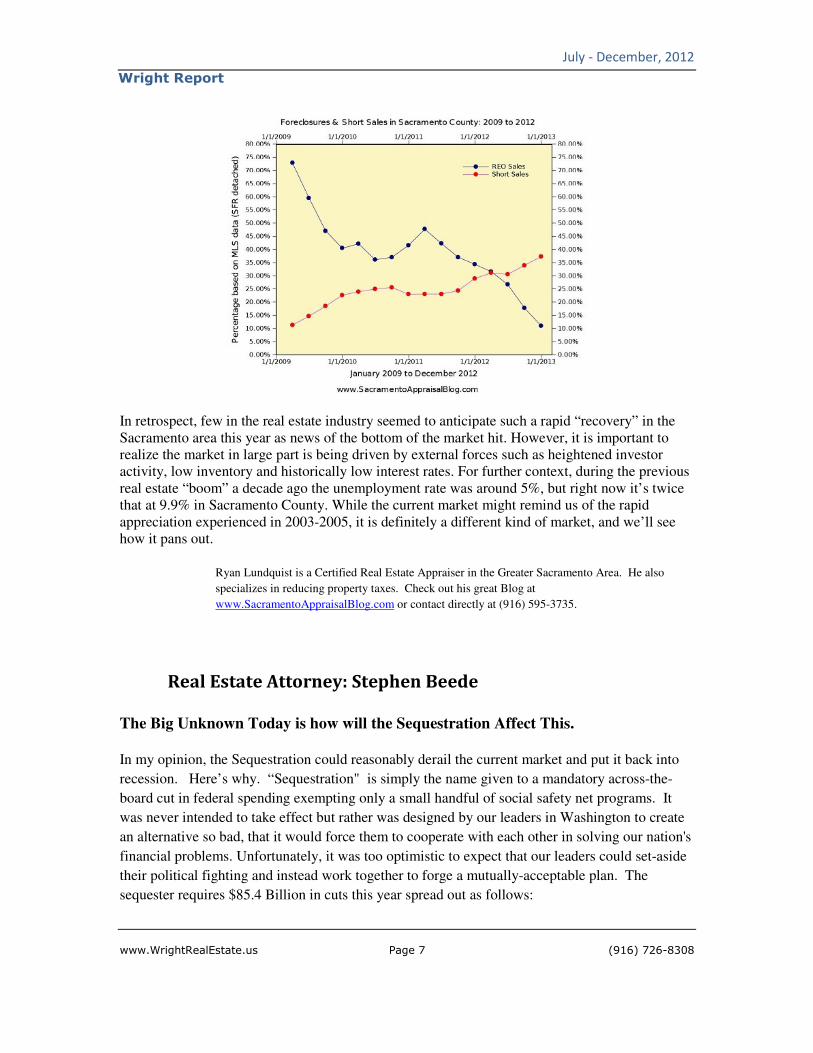

In retrospect, few in the real estate industry seemed to anticipate such a rapid “recovery” in the Sacramento area this year as news of the bottom of the market hit. However, it is important to realize the market in large part is being driven by external forces such as heightened investor activity, low inventory and historically low interest rates. For further context, during the previous real estate “boom” a decade ago the unemployment rate was around 5%, but right now it’s twice that at 9.9% in Sacramento County. While the current market might remind us of the rapid appreciation experienced in 2003-2005, it is definitely a different kind of market, and we’ll see how it pans out.

Ryan Lundquist is a Certified Real Estate Appraiser in the Greater Sacramento Area. He also

specializes in reducing property taxes. Check out his great Blog at

www.SacramentoAppraisalBlog.com or contact directly at (916) 595-3735.

Real Estate Attorney: Stephen Beede

The Big Unknown Today is how will the Sequestration Affect This.

In my opinion, the Sequestration could reasonably derail the current market and put it back into

recession. Here’s why. “Sequestration" is simply the name given to a mandatory across-the-

board cut in federal spending exempting only a small handful of social safety net programs. It

was never intended to take effect but rather was designed by our leaders in Washington to create

an alternative so bad, that it would force them to cooperate with each other in solving our nation's

financial problems. Unfortunately, it was too optimistic to expect that our leaders could set-aside

their political fighting and instead work together to forge a mutually-acceptable plan. The

sequester requires $85.4 Billion in cuts this year spread out as follows:

July - December, 2012

www.WrightRealEstate.us Page 8 (916) 726-8308

Wright Report

Defense - $42.7 Billion (7.9%)

Domestic Programs - $28.7 Billion (5.3%)

Medicare - $9.9 Billion (2%)

Other mandatory cuts - $4 Billion

The administrators running each of those government departments will have the discretion as to

how those cuts will be made within their agencies. Here is an analysis of specifics put out by the

Office of Management and Budget (OMB):

For most of us, none of the above cuts will have a direct impact such as loss of jobs. But the

indirect impacts will touch us all with a trickle-down layering. For example:

1. Every cut in a government program will result in a loss of some employee jobs and a cut of

that departments purchasing. This will reduce the money being spent on everything from

groceries to travel to office supplies and more;

2. This will cause a reduction in income, first to businesses contracting with the government

which in turn will result in their reduction of jobs and spending; and secondarily to all the other

businesses and individuals below as the reductions in spending trickle down through the

economy.

3. The still fragile recovering real estate market is dependent upon jobs to fuel new buyers to

acquire the remaining upside-down properties which still number in the millions. More people

may find themselves unable to hang on. With more homes hitting the market and less buyers

available, price growth will stall and maybe even drop.

Lastly, it is critical to understand that these $85.4 Billion in cuts is just a first step in a 10 year

process to reduce our Federal deficit by $1.5 Trillion by 2021. Under the sequester plan there will

be additional cuts of $109.3 Billion a year from 2014-2021. Overall, the net effect is to reduce the

size of government and reduce our Federal Deficit.

These goals are something that we all may recognize needs to be done, but no-one really wants

the effects to hurt them directly. The reality is however, that whether it is by the Sequester or

some other agreed-upon Plan, every one of us will feel the pain in one way or another. That will

be the price of leaving our grandchildren a Nation that is economically solvent rather than

drowning them in unsustainable debt payments. I personally believe that the future of our nation

rides on the deficit-reducing budget decisions our leaders make. Whether it is organized

negotiation or a messy sequestration, these are steps that we know we must take.

Stephen Beede is a prominent local attorney with very wide experience with residential real estate

that he brings to his law practice. He can be reached online at www.bpelaw.com and

[email protected]. He also keeps an excellent blog at www.stevebeede.com; contact him

directly at (916) 966-2260.

July - December, 2012

www.WrightRealEstate.us Page 9 (916) 726-8308

Wright Report

Mortgage Broker: Jeff Marr

Mortgages and the Fed’s Role.

When I got started in the lending field roughly 9 years ago (early 2005), our economy was on the

tail edge of economic expansion, and one of the most common questions I got was ‘I hear the

Fed’s going to raise rates at their next meeting, should I lock my rate before this happens’? My

common response was ‘the Fed only controls short term rates (primarily the Fed Funds and

Discount rates, which set lending costs for banks needing over-night loans for reserve

requirements), and has no influence on mortgages, which are longer term debts (30 year pay back

periods in most cases). I would then typically go on to explain the factors that DID influence

interest rates, namely the outcome of economic reports indicating whether our economy is

growing or contracting. Though the Fed’s role was very limited back then related to mortgage

rates, this has changed in the past few years, and changed dramatically!

In response to the financial meltdown that occurred, beginning in late 2008, the Fed began taking

some extraordinary measures to boost the economy, purchasing immense amounts of both

mortgage-backed securities (MBS or simply called mortgage bonds), and similar amounts of US

Treasuries. These purchase programs came to be known as ‘Quantitative Easing, or ‘QE’, and the

Fed has performed three rounds of QE so far, accounting for several Trillion dollars-worth of

bond purchases……

When the first round of QE was announced in Nov of 2008, the mortgage market’s response was

immediately positive and rates fell sharply, roughly ¼ % in a single day upon this

announcement….we saw a similar response when QE 2 began in Nov of 2010…..by the time QE

3 was announced in Sept of 2011, which had been widely expected for many months, the impact

on rates wasn’t as dramatic, but has mostly acted as lid for keeping rates low…If we look at

where rates were in late 2008 compared to current levels, we’ve seen them drop roughly 1.5 – 2%

over this period (they were in the 5.5% range, fell as low as 3.5% in late 2012)…and prior to this,

we had never seen sustained levels this low, ever!

So given that our economy, and especially the housing market, seems to be improving, what will

be the impact to mortgage rates when the Fed ends QE 3? There’s been some who expect that QE

3 will end later year, so will rates slowly move higher, or could it happen more abruptly? Or

could we retest the last year’s low rates given all the international economic uncertainty (debt

crisis in Europe, slowing China economy, etc.)? We’ll have to wait and see!

Jeff Marr is a mortgage lender with Alpine Mortgage and a Financial Planner before that. He has

been in Mortgage Lending since 2005 and financial services since 1997. He can be reached at

(916) 947-1312.

July - December, 2012

www.WrightRealEstate.us Page 10 (916) 726-8308

Wright Report

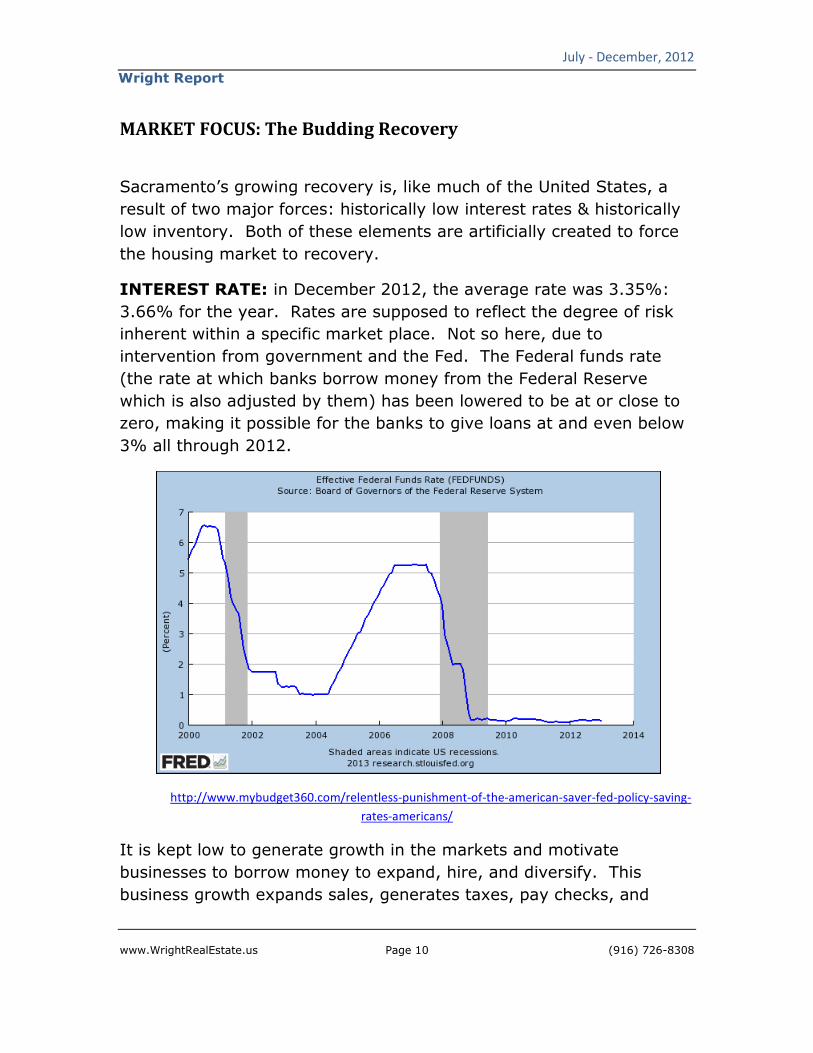

MARKET FOCUS: The Budding Recovery

Sacramento’s growing recovery is, like much of the United States, a

result of two major forces: historically low interest rates & historically

low inventory. Both of these elements are artificially created to force

the housing market to recovery.

INTEREST RATE: in December 2012, the average rate was 3.35%:

3.66% for the year. Rates are supposed to reflect the degree of risk

inherent within a specific market place. Not so here, due to

intervention from government and the Fed. The Federal funds rate

(the rate at which banks borrow money from the Federal Reserve

which is also adjusted by them) has been lowered to be at or close to

zero, making it possible for the banks to give loans at and even below

3% all through 2012.

http://www.mybudget360.com/relentless-punishment-of-the-american-saver-fed-policy-saving-

rates-americans/

It is kept low to generate growth in the markets and motivate

businesses to borrow money to expand, hire, and diversify. This

business growth expands sales, generates taxes, pay checks, and

July - December, 2012

www.WrightRealEstate.us Page 11 (916) 726-8308

Wright Report

expands the economy. It seems to have mostly benefited home

buyers by creating low monthly payments: the lower the rate, the

lower the payment, regardless of the price.

This has caused affordability to go to all time highs nationally in 2012

and made the possibility of home ownership accessible to most anyone

with good credit and stable employment.

Incidentally the Fed says they expect to keep the rate down into 2014.

INVENTORY: The other side of the equation is lack of inventory.

Inventory is a direct result of supply and demand economics and it has

been driven to historical lows by the restriction of supply and the

increasing demand.

Supply-

The primary factors currently affecting supply are (1) the lack of REO

properties for sale and (2) the lack of Short Sales, (3) Institutional

Investors entering the market and (4) the rise of Bulk Sales.

REO Inventory (homes for sale by banks) has dramatically declined

through 2012, and it is likely to continue to decrease. The reason?

Banks don’t want to own or sell property. The five largest lenders

were hit with a judgment from the robosigning scandal for 25 Billion

dollars, so they are more than hesitant to foreclose and cautious with

the process. They also see the market rising and realize that if they

put foreclosures off they will make back some of their losses.

Foreclosures are also in decline in California due to the “Homeowner’s

Bill of Rights” which states that if the owner is negotiating with the

bank to modify their loan or trying to do a short sale the bank must

stop any foreclosure process. This too will limit foreclosure notices

and sales in CA.

Short Sales are also dropping for several reasons. HARP, the

government’s refinance program for underwater homeowners, made

changes to their criteria in 2012 making it possible for a larger number

of homeowner with negative equity to be able to take advantage of the

July - December, 2012

www.WrightRealEstate.us Page 12 (916) 726-8308

Wright Report

low interest rates and refinance. They came in droves. Also, lenders

are now actively pursuing loan modifications to help delinquent

borrowers get back on track. In addition, the type of homeowners

currently having trouble making payments are very different from

those in 2008. While those in 2008 probably should never have been

given a loan in the first place, owners in trouble in 2012 have

weathered 4 years of a down economy and frequently just need a little

help to get back on their feet. This makes loan modifications and work

outs an efficient way to limit losses for the banks. Also as prices rise

fewer owners are underwater and more can sell at a profit without

short sale.

Institutional Investors are one of the biggest shifts occurring in real

estate this year. It heralds the entrance of Wall Street into the

residential market. Hedge funds, trusts, corporations, pension funds &

private investors are all jumping in. Perhaps the most well know

entrant into residential real estate is Blackstone (NYSE:BX) which

purchased some 17,000 homes during 2012 with an estimated 2.2

Billion dollars. These investors have dominated foreclosure auctions

and are providing stiff competition to homebuyers in under $200,000

neighborhoods. They pay all cash and don’t mind overpaying to get a

property.

The intention of these large investors is to buy, fix and hold as a long

term investment where they can get regular cash flow and eventually

sell for a sizable profit.

Bulk Sales unfortunately have become part of the landscape as

Fannie Mae, Freddie Mac and HUD are testing out the method to rid

themselves of nonperforming loans and undesirable inventory. HUD

plans to sell up to 40,000 delinquent loans over the next year; a

process they began in 2012.

Fannie Mae made a bulk sale of some 3 Billion dollars in homes in

2012. These homes are also intended to be rentals and part of the

agreement stipulates they must hold them for a minimum term so

none will be coming to the market as flips.

July - December, 2012

www.WrightRealEstate.us Page 13 (916) 726-8308

Wright Report

Demand-

The primary factors affecting demand are (1) New household

formation, (2) Boomerang buyers, (3) Bottom bouncers, and (4)

Investors.

New Household Formation. Across the U.S. household creation has

declined since 2006. Young people are postponing marriage and

staying at home after graduation. That is expected to change in 2013

where it is estimated that more than one million new households will

be created. When this occurs they will be looking for a place to live.

Boomerang Buyers are home buyers who previously owned and lost

their houses to foreclosure or short sale between 2007 and 2010. The

process to resurrect their credit takes a minimum of three years (five

years for foreclosure) so many will be coming back into the market in

2013. These are buyers who have already owned and are committed

to home ownership and the benefits it provides.

Bottom Bouncers are buyers who have waited for the bottom to

arrive and now that the market is rebounding are trying to get in as

fast as possible. They try to time the market and are afraid of getting

left behind.

Investors, like the bottom bouncers, they see the benefits of the

rising prices, positive cash flow, and low interest rates and are buying

all they can. They frequently buy all cash, so they are tough

competitors in the market place.

www.WrightRealEstate.us

Wright Report

http://www.doctorhousingbubble.com/all

In addition to all of these

down, or sideways who are also looking to buy in the growing market

of rising prices, low rates, and multiple offers. Together it turns the

market into a feeding frenzy fueling price inflation.

Conclusions: rates and la

industry growth, which will drive the U.S. economic recovery. It is

unlikely that any of the

rapid growth in housing prices and sales

MARKET UPDATE:

The median price across the U.S. hit $176,000 in 2012, up 6.3% from

2011. In January 2013 the median sold price in CA

24% from January 201

2006.

July - December

Page 14

http://www.doctorhousingbubble.com/all-cash-real-estate-buying-trend-all-cash-

2012-2013-cash-trend/

these there are the regular buyers moving up,

who are also looking to buy in the growing market

of rising prices, low rates, and multiple offers. Together it turns the

market into a feeding frenzy fueling price inflation.

Conclusions: rates and lack of inventory are driving the housing

industry growth, which will drive the U.S. economic recovery. It is

unlikely that any of these contributing factors will reverse in 2013 so

rapid growth in housing prices and sales can be expected.

The median price across the U.S. hit $176,000 in 2012, up 6.3% from

January 2013 the median sold price in CA hit $337,040

2012 and down 28.2% from the $469,500 peak in

December, 2012

(916) 726-8308

-buying-record-

are the regular buyers moving up,

who are also looking to buy in the growing market

of rising prices, low rates, and multiple offers. Together it turns the

ck of inventory are driving the housing

industry growth, which will drive the U.S. economic recovery. It is

contributing factors will reverse in 2013 so

The median price across the U.S. hit $176,000 in 2012, up 6.3% from

337,040, up

% from the $469,500 peak in

July - December, 2012

www.WrightRealEstate.us Page 15 (916) 726-8308

Wright Report

Affordability also came to an all time high in 2012 across the nation

due to already low prices and declining interest rates. In CA

affordability hit 48% in Q4-2012, down 1 point from Q3-12 and 7

points from 55% in Q4-11.

In December 2012 NAR (National Association of Realtors) showed price

increases in 135 of 152 metro areas that it tracks. Dataquick showed

price increases in 201 of 361 metro areas it tracks.

According to CAR (California Association of Realtors) the median home

price for California in December 2012 was $366,930; 28.3% higher

than the $285,920 in December of 2011. That median price is up 50%

from the 2009 bottom of $245,000.

In Sacramento County the median price rose to $195,000 in

December, up 21% from the median price in Dec. 2011. The average

sold price for Sacramento County for Dec. 2012 was $224,752; up

21% from the year before.

COUNTY Average Sold Price % Change

Dec-11 Dec-12

Sacramento $186,329 $224,752 20.62%

Placer $298,550 $338,571 13.41%

El Dorado $306,305 $336,308 9.80%

Yolo $268,652 $312,310 16.25%

Since the market turned downward in September 2005 it declined 59%

in median price for single family homes (SFR) with the lowest point

being $160,000 in January 2012. Since that point the market rose

22% through December and is showing strong signs of potential

growth.

In California 36.4% of sales in December were distressed sales (short

sales or REO). In Sacramento County that was 51.4%, down from

63% at the end of 2011. Across the State short sales make up an

average of 25% of sales. In Sacramento County it is 40.7%. REOs

July - December, 2012

www.WrightRealEstate.us Page 16 (916) 726-8308

Wright Report

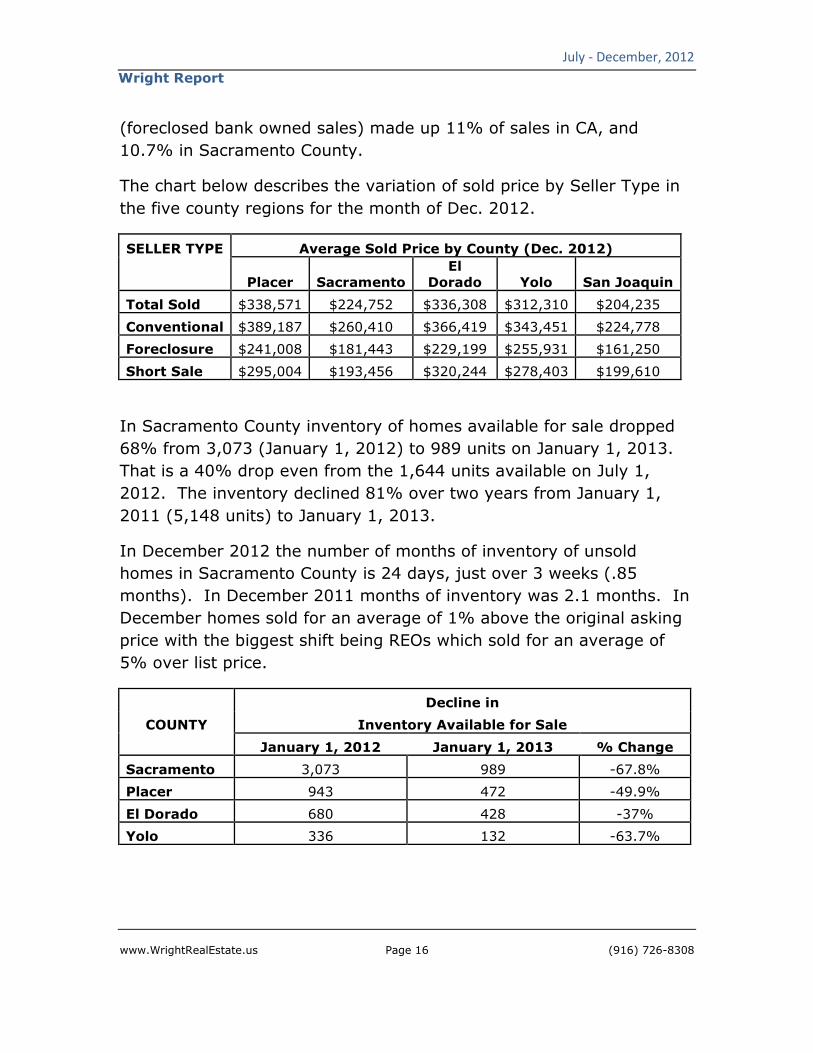

(foreclosed bank owned sales) made up 11% of sales in CA, and

10.7% in Sacramento County.

The chart below describes the variation of sold price by Seller Type in

the five county regions for the month of Dec. 2012.

SELLER TYPE Average Sold Price by County (Dec. 2012)

Placer Sacramento El

Dorado Yolo San Joaquin

Total Sold $338,571 $224,752 $336,308 $312,310 $204,235

Conventional $389,187 $260,410 $366,419 $343,451 $224,778

Foreclosure $241,008 $181,443 $229,199 $255,931 $161,250

Short Sale $295,004 $193,456 $320,244 $278,403 $199,610

In Sacramento County inventory of homes available for sale dropped

68% from 3,073 (January 1, 2012) to 989 units on January 1, 2013.

That is a 40% drop even from the 1,644 units available on July 1,

2012. The inventory declined 81% over two years from January 1,

2011 (5,148 units) to January 1, 2013.

In December 2012 the number of months of inventory of unsold

homes in Sacramento County is 24 days, just over 3 weeks (.85

months). In December 2011 months of inventory was 2.1 months. In

December homes sold for an average of 1% above the original asking

price with the biggest shift being REOs which sold for an average of

5% over list price.

COUNTY

Decline in

Inventory Available for Sale

January 1, 2012 January 1, 2013 % Change

Sacramento 3,073 989 -67.8%

Placer 943 472 -49.9%

El Dorado 680 428 -37%

Yolo 336 132 -63.7%

July - December, 2012

www.WrightRealEstate.us Page 17 (916) 726-8308

Wright Report

Inventory continues to remain extremely low, especially distressed

inventory which has declined substantially during the year.

Affordability, on the other hand, is still very high with the affordability

index in Q4-2012 for Sacramento County dropped slightly to 71% (23

points higher than the state). In California affordability dropped 7

percentage points to 48% from Q4-11 to Q4-12, meaning that 48% of

workers can afford the median priced home within the state.

Economists believe that housing will be a primary driver in the 2013

economy and is expected to contribute more than one million jobs to

U.S. employment this year.

Growth in housing construction also raises the manufacturing

industries that support housing, as well as real estate sales, lending,

insurance and other industries directly related to housing. The rest of

the economy will also experience the ripple effect.

http://www.doctorhousingbubble.com/all-cash-real-estate-buying-trend-all-cash-

buying-record-2012-2013-cash-trend/

July - December, 2012

www.WrightRealEstate.us Page 18 (916) 726-8308

Wright Report

Across America there were approximately 367,000 new homes sold in

2012, up 20% from 2011’s all time historical low of 305,000 sales.

New homes also accounted for 8% of all home sales in 2012. 2013 is

expected to rise as much as 23% as sales, starts, prices, permits and

builder confidence all increase with demand.

The boons to new construction are historically low interest rates,

housing affordability and rising household formation. The detractors

are tight lending conditions, inaccurate appraisals, rising material costs

and lack of buildable lots.

Growth will initially be constricted by government fees which have not

reduced much since they rose with the last building cycle. Lack of

redevelopment funds will also postpone building in Sacramento’s

downtown region. Another issue that will arise with increased demand

is the availability of buildable lots.

THE ECONOMY:

U.S. economists predict a continued recovery in 2013 and expect

housing to lead the economic turnaround. Unemployment is expected

to go down, home purchases up, and interest rates to stay the same.

The economy is expected to see a 2.2 – 2.4% increase in 2013, and

the housing market is expected to be an overall contributor. U.S.

growth in 2012 was 2.2% so 2013 will be another recovery year.

The Fed funds rate is expected to remain low, not only for the housing

mortgage market, but to stimulate business borrowing and loans, and

generate internal growth within the economy. Another benefit of

keeping rates low is the U.S. will be to reduce the payment amount on

Federal debt being sold annually to cover the deficit.

July - December, 2012

www.WrightRealEstate.us Page 19 (916) 726-8308

Wright Report

All indicators are that the housing market is recovering and December

showed signs of growth in 201 metro areas across the nation. Prices

are rising and the number of home owners under water is decreasing.

Despite this positivity there are certain difficulties ahead. Major

concerns include the “Fiscal Cliff”, Federal spending cuts, renewed

talks on the debt ceiling, E.U. debt crisis, increased government

regulation, and continued high unemployment all still need to be

resolved.

One major issue for the future is the increasing federal debt. Even

with massive proposed spending cuts the U.S. annual spending still far

exceeds income, and the balance must be made up by selling bonds-

debt obligations. The current short term solution is QE3 (Quantitative

Easing 3) where the Federal Reserve simply buys up all the excess

bonds no one else is willing to purchase with an open checkbook and

unlimited (literally) amount of funds.

Up to January 2013 the Fed has purchased $3,000,000,000,000 (3

Trillion) dollars in U.S. bonds and continues to purchase at the rate of

$85,000,000,000 (85 Billion) dollars per month. That is spending the

U.S. government is doing monthly not covered by taxes or other

buyers of debt. The current government deficit (as of this writing) is

estimated to be around $16,400,000,000,000 (16.4 Trillion) dollars;

and we thought California had a big problem with a $12 Billion deficit.

On a happier note the “Debt Relief Act” was extended to the end of

2013, but it is not likely to be renewed beyond this year because the

real estate market is in a recovery cycle. This act says that the IRS

will not count (it forgives) the amount a seller could have been forced

to show as income as a result of a lender losing money on a short sale.

When a lender loses money at sale they send the borrower a 1099 and

it shows on the borrower’s taxes as a gain in income for the year. The

Act also restored the tax deduction for Mortgage Insurance Premiums

which will directly benefit owners with FHA loans.

July - December, 2012

www.WrightRealEstate.us Page 20 (916) 726-8308

Wright Report

BANKING & LENDING:

The big news in banking is the 11.6 Billion dollar settlement Bank of

America made with Fannie Mae for restitution for the bad loans sold

since 2004. The settlement allows for 1.3 Billion as compensation to

reimburse for servicing issues and 10.3 Billion for repurchases of

defaulted loans and to cover losses from unpaid interest that accrued

on delinquent loans over that time.

It is estimated that the five largest lenders (Wells Fargo, Bank of

America, Citibank, Chase, and Ally financial Inc.) have lost upwards of

84 Billion dollars since 2007 in foreclosures, legal costs and loan

buybacks. Bank of America has paid the lion’s share – 50 Billion –

largely due to its purchase of Countrywide and their toxic loan

portfolio.

Here is the 2012 income for the 4 largest banks in the U.S. Some

doing well, others not so well.

BANK Bank Income for 2012

Quarter 4 Annual

Wells Fargo 5.1 B 18.9 B

Chase 5.7 B 24.4 B

Bank of America .732 B 4.2 B

Citibank 1.2 B 7.5 B

2012 saw a historic high in lending activity with 8.6 million loans

originated. That is a 34% increase over 2011. Much of this is due to

historically low rates, a recovering real estate market, and the

government raising the limits on the HARP refinance program allowing

borrowers to refinance even if they owe more than 125% of the value

of their home. This allows underwater borrowers to refinance their

home at current low rates.

July - December, 2012

www.WrightRealEstate.us Page 21 (916) 726-8308

Wright Report

http://www.doctorhousingbubble.com/negative-equity-home-owners-2013-negative-equity-

california-reo/

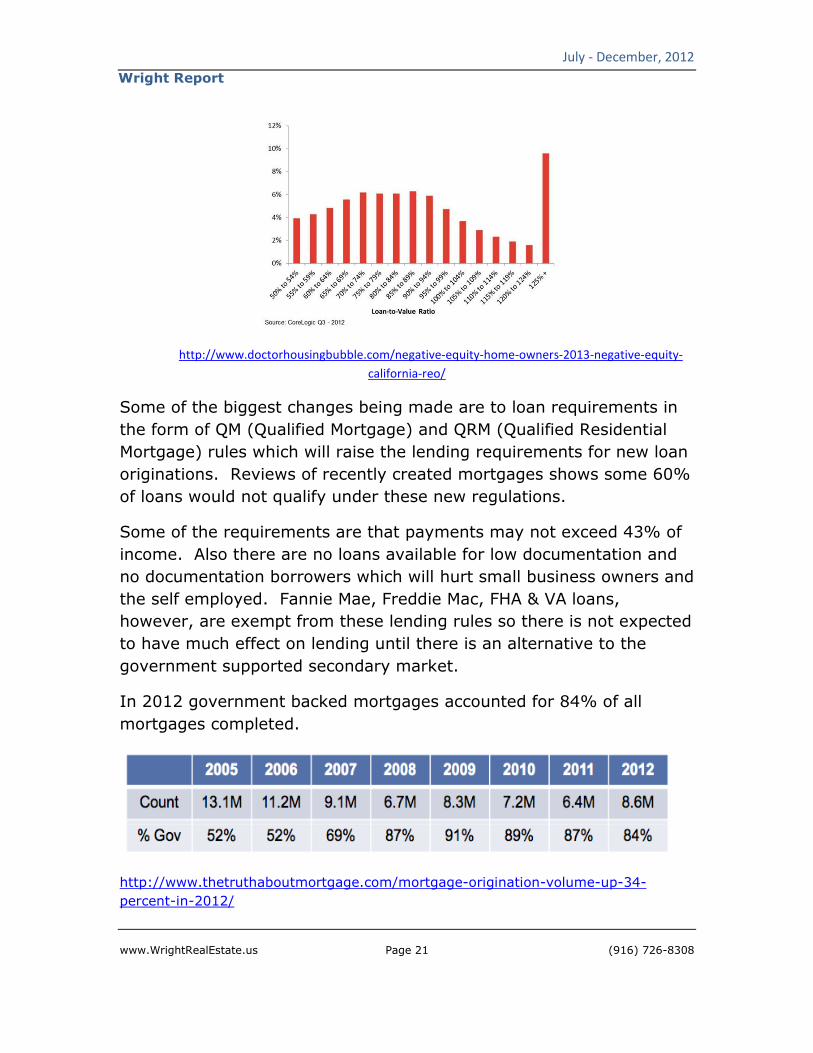

Some of the biggest changes being made are to loan requirements in

the form of QM (Qualified Mortgage) and QRM (Qualified Residential

Mortgage) rules which will raise the lending requirements for new loan

originations. Reviews of recently created mortgages shows some 60%

of loans would not qualify under these new regulations.

Some of the requirements are that payments may not exceed 43% of

income. Also there are no loans available for low documentation and

no documentation borrowers which will hurt small business owners and

the self employed. Fannie Mae, Freddie Mac, FHA & VA loans,

however, are exempt from these lending rules so there is not expected

to have much effect on lending until there is an alternative to the

government supported secondary market.

In 2012 government backed mortgages accounted for 84% of all

mortgages completed.

http://www.thetruthaboutmortgage.com/mortgage-origination-volume-up-34-

percent-in-2012/

July - December, 2012

www.WrightRealEstate.us Page 22 (916) 726-8308

Wright Report

FHA is still struggling with a 9.6% delinquency rate (over 730,000 of

its more than 7,000,000 loans) and because their reserves are far

below the mandated 2% they are raising rates on the required PMI

(Private Mortgage Insurance) on April 1, this year. They are also

keeping the PMI on all new FHA loans for the life of the loan rather

than knocking it off after the loan drops below 80% of the value of

home.

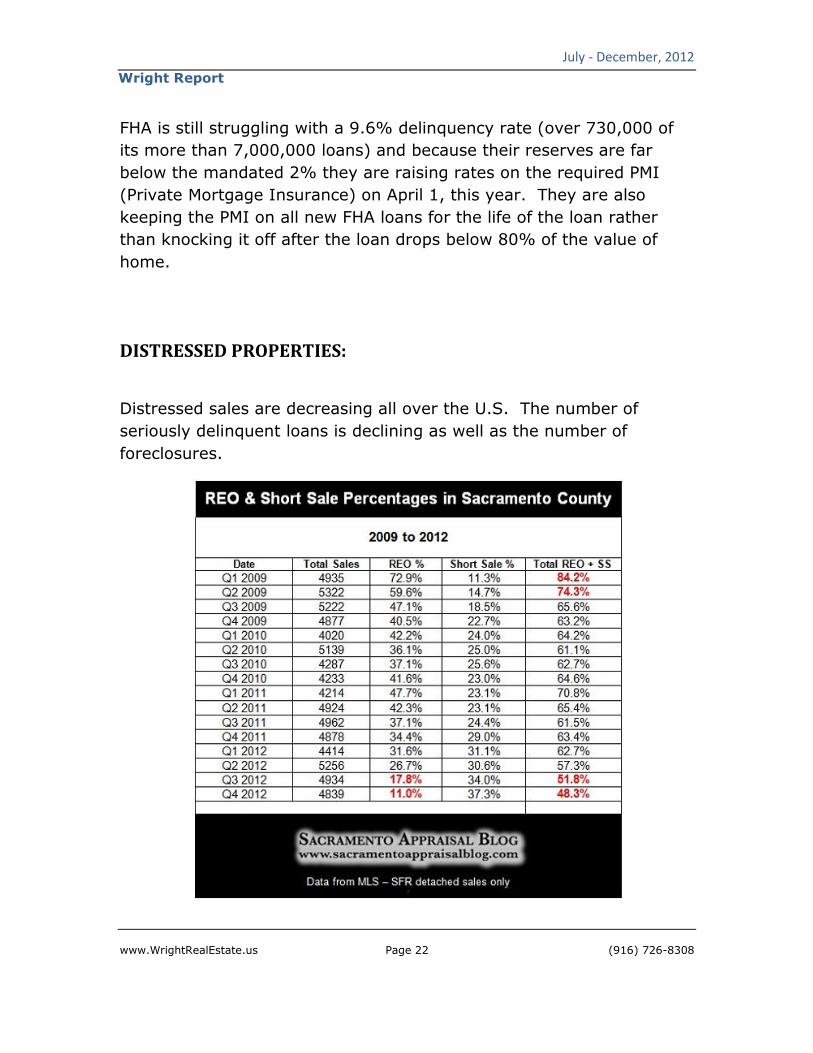

DISTRESSED PROPERTIES:

Distressed sales are decreasing all over the U.S. The number of

seriously delinquent loans is declining as well as the number of

foreclosures.

July - December, 2012

www.WrightRealEstate.us Page 23 (916) 726-8308

Wright Report

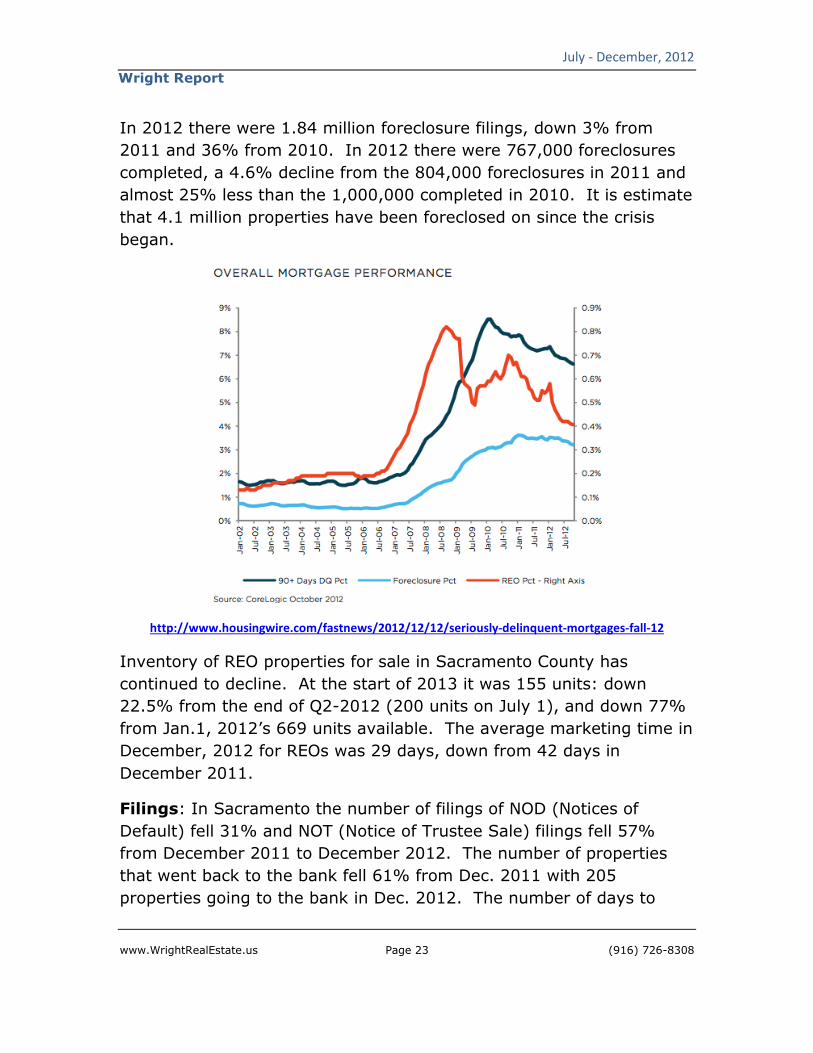

In 2012 there were 1.84 million foreclosure filings, down 3% from

2011 and 36% from 2010. In 2012 there were 767,000 foreclosures

completed, a 4.6% decline from the 804,000 foreclosures in 2011 and

almost 25% less than the 1,000,000 completed in 2010. It is estimate

that 4.1 million properties have been foreclosed on since the crisis

began.

http://www.housingwire.com/fastnews/2012/12/12/seriously-delinquent-mortgages-fall-12

Inventory of REO properties for sale in Sacramento County has

continued to decline. At the start of 2013 it was 155 units: down

22.5% from the end of Q2-2012 (200 units on July 1), and down 77%

from Jan.1, 2012’s 669 units available. The average marketing time in

December, 2012 for REOs was 29 days, down from 42 days in

December 2011.

Filings: In Sacramento the number of filings of NOD (Notices of

Default) fell 31% and NOT (Notice of Trustee Sale) filings fell 57%

from December 2011 to December 2012. The number of properties

that went back to the bank fell 61% from Dec. 2011 with 205

properties going to the bank in Dec. 2012. The number of days to

July - December, 2012

www.WrightRealEstate.us Page 24 (916) 726-8308

Wright Report

foreclosure in Sacramento County dropped 20% to 252 days and the

number of days it took for the banks to sell increased to 247 days on

average.

California NOD filings fell 33% and NOT filings fell 52% from December

to December. The number of properties that went back to the bank

fell 56% during the same period to 3,544 in Dec. 2012.

Inventory: Pre-foreclosure inventory (NOD - Notice of Default) in

Sacramento County went down 38% from 5,359 in Dec. 2011 to 3,340

in Dec. 2012. NOT (Notice of Trustee Sale) inventory went down 33%

for the same period to 2,702 units, and the number of bank owned

inventory (REOs) is down 41% to 2,731 units (Dec. 12), from 4,665

units in December 2011.

California inventory of NODs is also down 35% to 59,208 (Dec. 2012)

from 91,000 (Dec. 2011). NOT inventory is down 29% year over year

to 59,987 units, and the number of bank owned inventory (REOs) is

down 36.4% to 59,781 in Dec. units from 94,000 units in December

2011.

http://www.thetruthaboutmortgage.com/mortgage-origination-

volume-up-34-percent-in-2012/

July - December, 2012

www.WrightRealEstate.us Page 25 (916) 726-8308

Wright Report

COUNTY STATISTICS:

Sacramento County

The year started (January 1, 2012) with 3,073 listings and ended with

989 listing on the market on Jan. 1, 2013. That is a drop of 68% for

the year. REO (foreclosure) inventory is down 77% since Jan. 1, 2012

and Active Short Sales are down 88% over the same period.

Conventional sales inventory is down 44% over the same period.

July - December, 2012

www.WrightRealEstate.us Page 26 (916) 726-8308

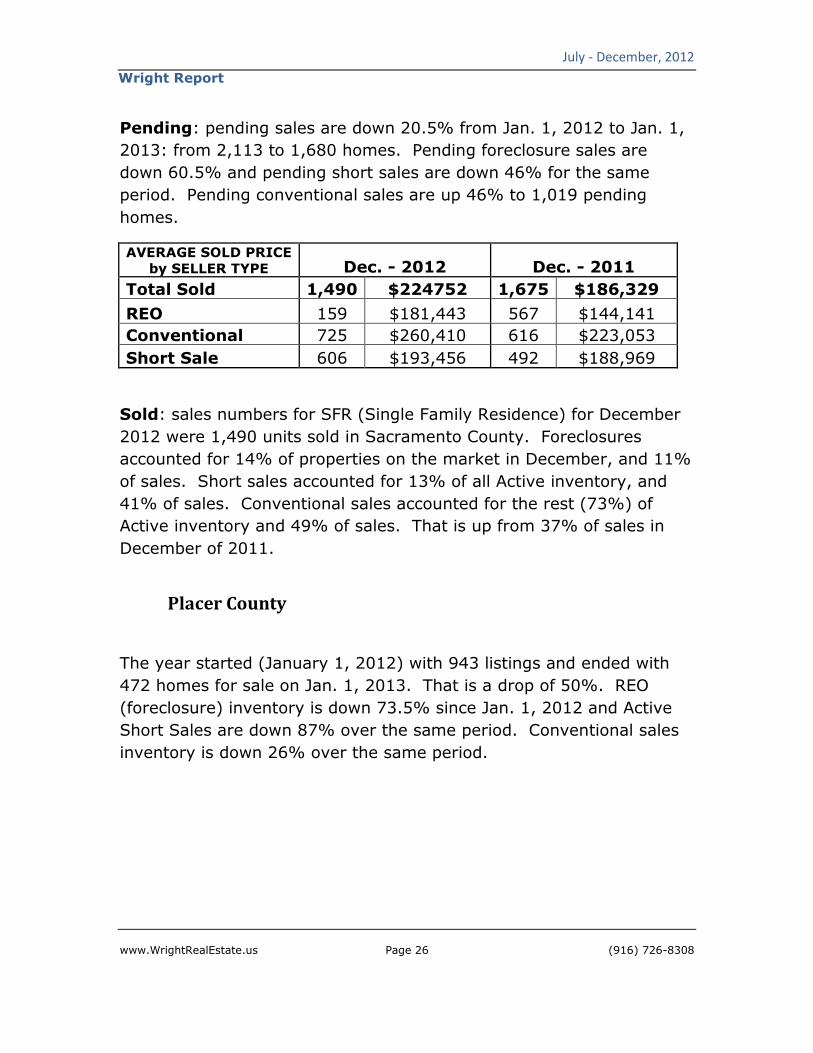

Wright Report

Pending: pending sales are down 20.5% from Jan. 1, 2012 to Jan. 1,

2013: from 2,113 to 1,680 homes. Pending foreclosure sales are

down 60.5% and pending short sales are down 46% for the same

period. Pending conventional sales are up 46% to 1,019 pending

homes.

AVERAGE SOLD PRICE by SELLER TYPE Dec. - 2012 Dec. - 2011

Total Sold 1,490 $224752 1,675 $186,329

REO 159 $181,443 567 $144,141

Conventional 725 $260,410 616 $223,053

Short Sale 606 $193,456 492 $188,969

Sold: sales numbers for SFR (Single Family Residence) for December

2012 were 1,490 units sold in Sacramento County. Foreclosures

accounted for 14% of properties on the market in December, and 11%

of sales. Short sales accounted for 13% of all Active inventory, and

41% of sales. Conventional sales accounted for the rest (73%) of

Active inventory and 49% of sales. That is up from 37% of sales in

December of 2011.

Placer County

The year started (January 1, 2012) with 943 listings and ended with

472 homes for sale on Jan. 1, 2013. That is a drop of 50%. REO

(foreclosure) inventory is down 73.5% since Jan. 1, 2012 and Active

Short Sales are down 87% over the same period. Conventional sales

inventory is down 26% over the same period.

July - December, 2012

www.WrightRealEstate.us Page 27 (916) 726-8308

Wright Report

Pending: pending sales are down just 10% from Jan. 1, 2012 to Jan.

1, 2013: from 503 to 454 homes. Pending foreclosure sales are down

56% and pending short sales are down 56% for the same period.

Pending conventional sales are up 90% to 302 pending homes.

AVERAGE SOLD

PRICE by SELLER TYPE Dec. - 2012 Dec. - 2011

Total Sold 459 $338,571 425 $298,550

REO 57 $241,008 74 $251,205

Conventional 245 $389,187 202 $341,600

Short Sale 157 $295,004 149 $263,700

Sold: sales numbers for SFR (Single Family Residence) for December

2012 were 459 units sold. Foreclosures accounted for 8% of

properties on the market in December, and 12% of sales. Short sales

accounted for 8% of all Active inventory, and 34% of sales.

Conventional sales accounted for the rest (84%) of Active inventory

and 53% of sales. That is up from 17.4% of sales in December of

2011.

July - December, 2012

www.WrightRealEstate.us Page 28 (916) 726-8308

Wright Report

El Dorado County

The year started (January 1, 2012) with 680 listings and ended with

428 homes for sale on Jan. 1, 2013. That is a drop of 37%. REO

(foreclosure) inventory is down 61% since Jan. 1, 2012 and Active

Short Sales are down 78% over the same period. Conventional sales

inventory is down 16% over the same period.

Pending: pending sales are down 21% from Jan. 1, 2012 to Jan. 1,

2013: from 259 to 204 homes. Pending foreclosure sales are down

60.4% and pending short sales are down 55.4% for the same period.

Pending conventional sales are up 45% to 135 pending homes.

AVERAGE SOLD PRICE

by SELLER TYPE Dec. - 2012 Dec. - 2011

Total Sold 186 $336,308 226 $306,305

REO 25 $229,199 62 $187,530

Conventional 114 $366,419 93 $353,511

Short Sale 47 $320,244 71 $348,190

Sold: sales numbers for SFR (Single Family Residence) for December

2012 were 186 units sold. Foreclosures accounted for 12.3% of

properties on the market in December, and 13.4% of sales. Short

sales accounted for 10.3% of all Active inventory, and 25% of sales.

Conventional sales accounted for the rest (84%) of Active inventory

and 61.3% of sales. That is up from 41% of sales in December of

2011.

July - December, 2012

www.WrightRealEstate.us Page 29 (916) 726-8308

Wright Report

Yolo County

The year started (January 1, 2012) with 336 listings and ended with

132 homes for sale on Jan. 1, 2013. That is a drop of 61%. REO

(foreclosure) inventory is down 82% since Jan. 1, 2012 and Active

Short Sales are down 76.5% over the same period. Conventional

sales inventory is down 45% over the same period.

Pending: pending sales are down just 6% from Jan. 1, 2012 to Jan.

1, 2013: from 157 to 148 homes. Pending foreclosure sales are down

56% and pending short sales are down 35% for the same period.

Pending conventional sales are up 78% to 91 pending homes.

AVERAGE SOLD PRICE

by SELLER TYPE Dec. - 2012 Dec. - 2011

Total Sold 118 $312,310 145 $268,652

REO 13 $255,931 47 $185,676

Conventional 66 $343,451 52 $373,858

Short Sale 39 $278,403 46 $234,503

Sold: sales numbers for SFR (Single Family Residence) for December

2012 were 118 units sold. Foreclosures accounted for 11% of

properties on the market in December, and 14% of sales. Short sales

accounted for 10% of all Active inventory, and 25% of sales.

Conventional sales accounted for the rest (79%) of Active inventory

and 56% of sales. That is up from 35% of sales in December of 2011.

July - December, 2012

www.WrightRealEstate.us Page 30 (916) 726-8308

Wright Report

San Joaquin County

The year started (January 1, 2012) with 636 listings for sale on Jan. 1,

2013. REOs (foreclosure) are 17% of available inventory on Jan. 1,

2013 and Active Short Sales are 17.5% of active listings.

Conventional sales inventory is 65.5% of total.

Pending: pending sales are 844 units at the end of the year on Jan. 1,

2013. Pending foreclosure sales are 24% of pending properties.

Pending short sales are 24%, and pending conventional sales are up

52% of pending homes.

AVERAGE SOLD PRICE by SELLER TYPE Dec. - 2012

Total Sold 725 $204,235

REO 135 $161,250

Conventional 339 $224,778

Short Sale 251 $199,610

Sold: sales numbers for SFR (Single Family Residence) for December

2012 were 459 units sold. Foreclosures accounted for 18.6% of all

sold properties. Short sales accounted for 35% of all sales.

Conventional sales accounted for the rest 46.8%.

July - December, 2012

www.WrightRealEstate.us Page 31 (916) 726-8308

Wright Report

HISTORICAL PRICE GRAPHS:

July - December, 2012

www.WrightRealEstate.us Page 32 (916) 726-8308

Wright Report

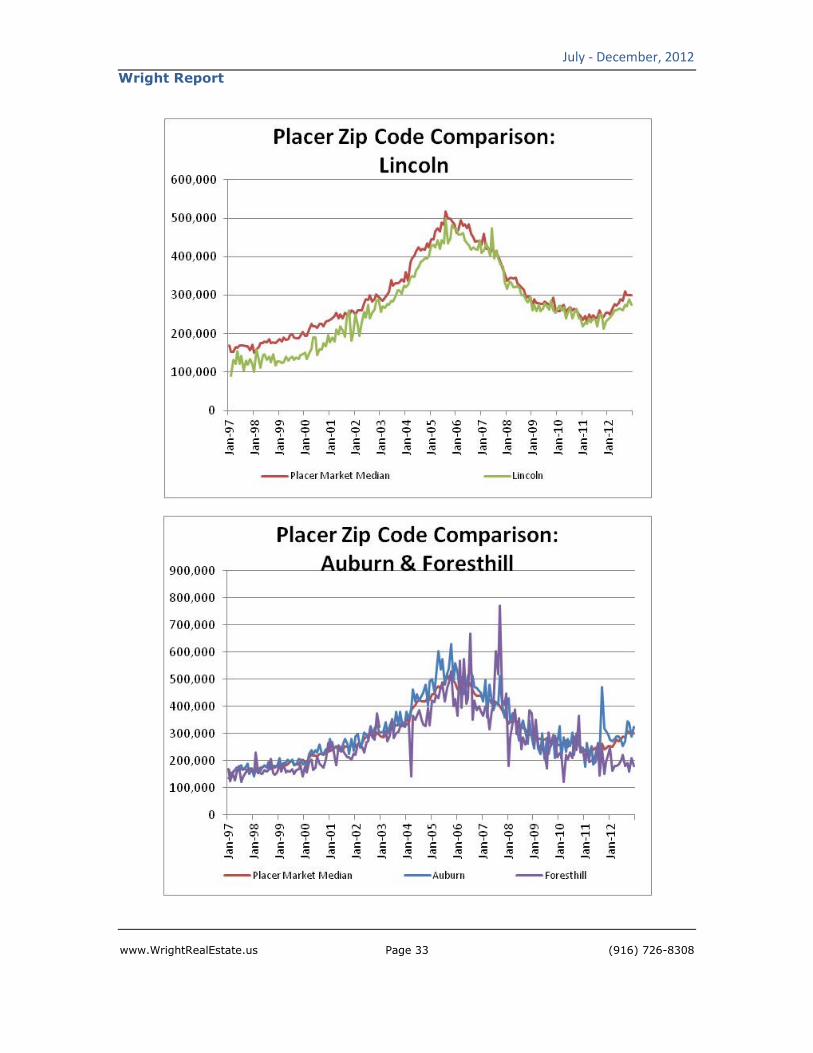

PLACER COUNTY:

July - December, 2012

www.WrightRealEstate.us Page 33 (916) 726-8308

Wright Report

July - December, 2012

www.WrightRealEstate.us Page 34 (916) 726-8308

Wright Report

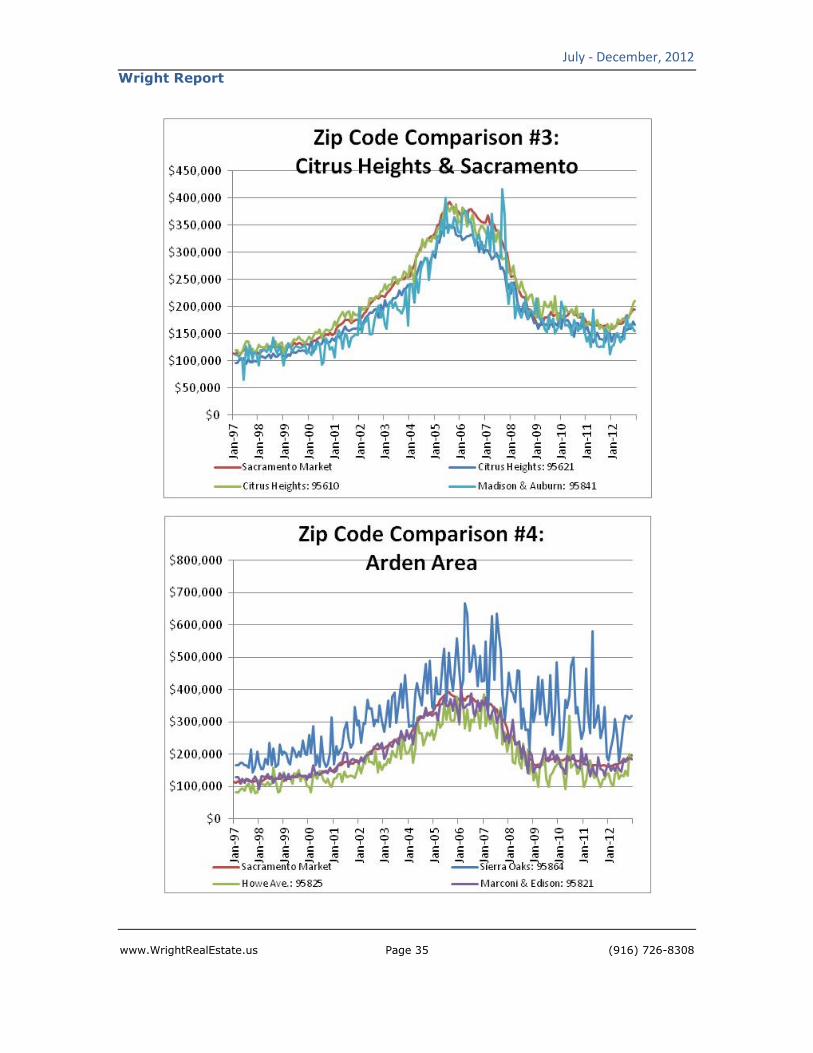

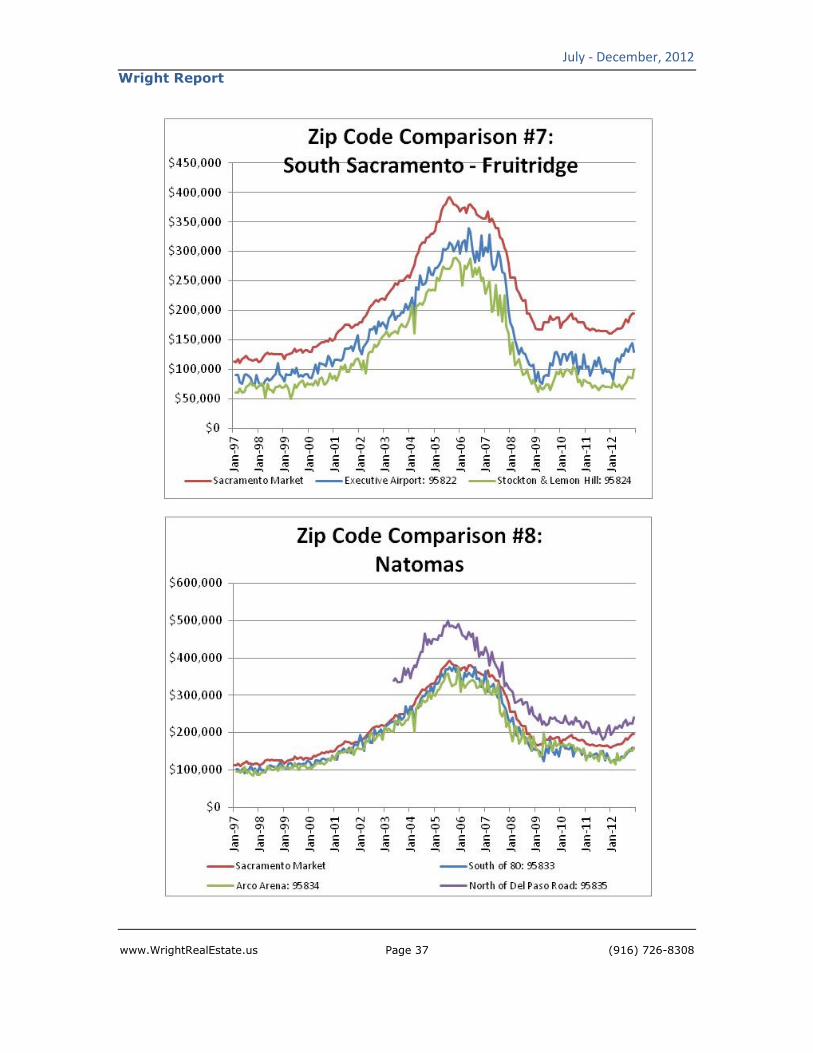

SACRAMENTO COUNTY:

July - December, 2012

www.WrightRealEstate.us Page 35 (916) 726-8308

Wright Report

July - December, 2012

www.WrightRealEstate.us Page 36 (916) 726-8308

Wright Report

July - December, 2012

www.WrightRealEstate.us Page 37 (916) 726-8308

Wright Report

July - December, 2012

www.WrightRealEstate.us Page 38 (916) 726-8308

Wright Report

July - December, 2012

www.WrightRealEstate.us Page 39 (916) 726-8308

Wright Report

July - December, 2012

www.WrightRealEstate.us Page 40 (916) 726-8308

Wright Report

July - December, 2012

www.WrightRealEstate.us Page 41 (916) 726-8308

Wright Report

July - December, 2012

www.WrightRealEstate.us Page 42 (916) 726-8308

Wright Report

RESOURCES:

ABREVIATIONS

CAR = California Association of Realtors

HAFA = Home Affordable Foreclosure Alternative

HAMP = Home Affordable Mortgage Program

MLS = Multiple Listing Service

NAR = National Association of Realtors

NOD = Notice of Default

NOT = Notice of Trustee Sale

REO = Real Estate Owned by a bank, or foreclosure

SAR = Sacramento Association of Realtors

WRE = Wright Real Estate

ADDITIONAL RESOURCES

MetrolistMLS.com - to search for properties. www.metrolistmls.com

NorthState Building Industry Association (BIA) www.northstatebia.org

Rental Housing Association (RHA) www.rha.org

Sacramento Association of Realtors (SAR) www.sacrealtor.org

July - December, 2012

www.WrightRealEstate.us Page 43 (916) 726-8308

Wright Report

Serving Sacramento since 2000.

Check out our BLOG and additional STATISTICS on the web at:

www.WrightRealEstate.US

For FREE Information and Consulting Services contact us:

Office: 916.726.8308 [email protected]