world bank documentdocuments.worldbank.org/curated/en/514331468034126056/pdf/multi-page.pdfghb -...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 16042

IMPLEMENTATION COMPLETION REPORT

INDIA

GUJARAT URBAN DEVELOPMENT PROJECT(CREDIT 1643-IN)

September 30, 1996

Infrastructure and Energy Operations DivisionCountry Department IISouth Asia Region

This document has restricted distribution and may be used by recipients only in the performance of their official duties.Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Units = Rupee (Rs)Fiscal Year Averages:

US$ 1.00 (FY85) = 11.6 Rs = 0.98 SDRUS$ 1.00 (FY86) = 12.4 Rs = 0.95 SDRUS$ 1.00 (FY88) 13.2 Rs = 0.76 SDRUS$ 1.00 (FY90) = 16.5 Rs = 0.75 SDRUS$ 1.00 (FY92) = 23.5 Rs = 0.72 SDRUS$ 1.00 (FY94) = 31.1 Rs = 0.72 SDR

MEASURES

The metric system is used throughout this report

ABBREVIATIONS

AUDA - Ahmedabad Urban Development AuthorityAMC - Ahmedabad Municipal CorporationGHB - Gujarat Housing Board

GMFB - Gujarat Municipal Finance BoardGOG - Government of Gujarat StateGWSSB - Gujarat Water Supply and Sanitation BoardTA - Technical AssistanceTPVD - Town Planning and Valuation DepartmentUPC - Urban Project Cell

FISCAL YEAR

April 1 - March 31

FOR OFFICIAL USE ONLY

INDIA

GUJARAT URBAN DEVELOPMENT PROJECT(CREDIT NO. 1643-IN)

IMPLEMENTATION COMPLETION REPORT

Table of Contents

PREFACE

EVALUATION SUMMARY ................................................... i

PART I: PROJECT IMPLEMENTATION ASSESSMENT

A. Statement and Evaluation of Project Objectives ................................... 1B. Evaluation of Objectives ........................................... 3C. Achievement of Objectives ........................................... 3D. Major Factors Affecting the Project ......................................... 5E. Project Sustainability ........................................... 6F. Bank Performance ........................................... 7G. Borrower's Performance ........................................... 8H. Assessment of Outcome ........................................... 8I. Future Operations ........................................... 9J. Key Lessons Learned .......................................... 10

PART II: STATISTICAL TABLES

Table 1: Summary of Assessments .......................................... 12Table 2: Related Bank Credits .......................................... 14Table 3: Project Timetable .......................................... 15Table 4: Credit Disbursements - Cumulative .......................................... 15Table 5: Key Indicators for Project Implementation .......................................... 15Table 6: Key Indicators for Project Operations .......................................... 15Table 7: Studies Included in the Project .......................................... 16Table 8A: Project Costs .. ........................................ 17Table 8B: Project Financing .......................................... 18Table 9: Economic Costs and Benefits .......................................... 18Table 10: Status of Legal Covenants ........................................... l9Table 11: Compliance with Operational Manual Statements ....................................... 23Table 12: Bank Resources - Staff Inputs .......................................... 23Table 13: Bank Resources - Missions .......................................... 24

This document has a restricted distribution and may be used by recipients only in the performance of their|offlcial duties. Its contents may not othenmise be disclosed without World Bank authorization.

ANNEXES

Annex 1: Composition and Approximate Cost Breakdown ......................................... 26Annex 2: Base Costs and Physical Contingencies ............................................. 28Annex 3: The Project, Its Restructuring and Benefits Achieved .................................. 30Annex 4: Operating Plans - Project Implementing Agencies ....................................... 33Annex 5: Borrower's Comments on the ICR .............................................. 37Annex 6: Final Supervision Mission's Aide Memoire ............................................. 39

INDIA

GUJARAT URBAN DEVELOPMENT PROJECT(CREDIT 1643-IN)

Preface

This is the Implementation Completion Report (ICR) for the Gujarat Urban DevelopmentProject in India (the Project) which IDA supported with Credit 1643-IN of SDR 58.5 million(1985 US$ 62.0 million), approved on 12/17/85, and made effective on 11/11/86.

Following five extensions of the disbursement period, the credit was closed on 03/31/95compared to the original closing date of 12/31/92. After cancellation of SDR 11 million (1985US$ 11.7 million) in connection with both a 1989 restructuring of the Project, and theexperienced changes in exchange rates, a further SDR 0.76 million (1985 US$ 0.84 million) wascanceled at credit closing. There was no external co-financing of the Project.

The ICR was prepared by Messrs. B.S. Bhavanishankar (Consultant),E. A. Huning (Task Manager), and R.A. Ribi (Consultant) on behalf of the Energy andInfrastructure Operations Division, Country Department II, South Asia Region, with theparticular assistance of W. S. Humphrey (Consultant/former Project Adviser, SA2DR), C.Godavitarne (Consultant/former Senior Operations Officer, India Resident Mission), S. Sarkar(Sanitary Engineer, India Resident Mission), W. J. Roach (former Task Manager, now retired)and T. Kanaley (former Task Manager, now Director General, AusAID, Australia). It wasreviewed by Mr. Jean-Francois Bauer, Chief, SA2EI, and Mrs. Kazuko Uchimura, ProjectAdvisor, SA2DR.

The ICR is based on material in the Project file, interviews with and contributions fromIDA personnel involved in project implementation, and the results of discussions with theBorrower and Beneficiary agencies during IDA's 03/95 Final Supervision Mission. The resultsof this mission are summarized in the aide-memoire of March 1995, attached to the presentreport. The local authorities contributed to the ICR by supplying the 10/95 completion reportprepared by the Urban Project Cell and by commenting on the draft ICR. The comments areappended verbatim to the present report whereas the contributions, which have been taken intoaccount in the report, are available in IDA's regional files.

INDIA

GUJARAT URBAN DEVELOPMENT PROJECT(CREDIT 1643-IN)

IMPLEMENTATION COMPLETION REPORT

Evaluation Summary

The Project and its Objectives

1. The Gujarat Urban Development Project (the Project) aimed at helping reduce the deficitsin urban shelter, infrastructure, and services in the main centers of the state. To this effect itincluded the following items addressing a complex set of sub-objectives: (i) development of 100ha in six cities, (ii) town planning schemes covering 570 ha in three cities including land re-adjustment and basic infrastructure, (iii) upgrading of 250 ha of slums in five cities, (iv)improvement of solid waste disposal services in five cities, (v) other urban infrastructure (watersupply, sewerage, storm drainage, etc. in four areas, and (vi) institutional strengthening at localand state level through technical assistance. See paras. 3 and 4.

2. From the start, progress on the Project was disappointing, and already in 1987, the firstyear after IDA had made the credit effective, it became increasingly clear that the chances wereslim that the Project's objectives, as originally set, could be achieved. The drought that afflictedthe state in the mid- 1 980s disrupted the local economy and induced a re-channeling of theBorrower's resources state-wide to high priority endeavors, especially those related to relief fromthe consequences of the drought. Therefore, it undoubtedly was the main factor for the Project'spoor prospects at the time. However, other factors that hampered Project progress were thecomplexity of the operation involving a large number of sub-projects and executing agencies, aswell as the deficient ownership of the Project shown until the later stages by GOG and theimplementing agencies. These shortcomings were also in part related to IDA's wish to quicklygenerate a major impact on the sector, without adequate preparations. See paras. 3 and 4.

3. In 1989, the Government of Gujarat (GOG) and IDA agreed on a restructuring of theProject to: (i) concentrate the Project on particularly urgent urban items with a good chance ofsuccess; and (ii) use the IDA resources that became available in connection with the precedingcurtailment for improving water supply and sanitation in rural areas particularly affected by thedrought. The latter, new, component represented about 40% of the revised Project andcomplemented similar items of the preceding Gujarat Water Supply and Sewerage Project, whichGOG and IDA agreed to restructure in parallel with the operation discussed here. See paras. 5and 6, and Annex 3.

- ii -

Project Outcome

4 . The physical objectives of the urban component of the revised Project were achieved inpart. Some of the municipalities, especially Surat, Vadodara, and Jamnagar, were reasonablysuccessful, though in the case of Ahmedabad, substantial progress was only achieved at the veryend of the Project. The Gujarat Water Supply and Sanitation Board (GWSSB), the entityresponsible for the rural water supply and sanitation component of the re-structured Project, wasmore successful, though it also fell short of some of the revised Project's implied sub-objectives.Indeed, some of the sanitation objectives were exceeded. See para. 9.

5. The sustainable institutional strengthening that resulted from the Project was modest, atbest. In particular, the improvements in cost recovery from urban services, both at the level ofthe tax and tariff assessment and of the collection of dues, were limited during the Project untilthe closing stages. This was also largely the case in the GWSSB component. Nevertheless, theProject and the influence of its covenanted requirements on implementing agencies' financialperformance and capacities are likely to have contributed to the gradual improvements and policyshifts that finally emerged. This change is also based in part on the creation by the Borrower, inthe late 1 980s and early 1 990s, of municipal service corporations which are, at least in principle,less prone to direct political influences on day-to-day municipal management than branches ofgovernment directly beholden to a political executive. See paras. 10 and 1 1.

6. Despite the relative success of the rural component, the overall outcome of therestructured Project rates as "unsatisfactory" (para. 18). A similar assessment seems indicatedfor both the Borrower's and IDA's performance, although IDA quickly acknowledged thedeficiencies of the original Project and tried with various degrees of success to correct them.Accordingly, in contrast to the original operation, which was grossly over-optimistic in itsassessment of the Borrower's and the other local entities' institutional capability, the revisedProject was more realistic but still fell substantially short of adequately assessing what wasachievable, both in physical and institutional terms, in the Gujarat environment. Further, thescarcity of available information makes it difficult to evaluate reliably whether the resultsachieved stand in reasonable relation to the human and financial resources that were invested inthe Project. In particular, it is impossible to determine ex-post economic returns for the Projector its main items. See paras. 18 to 25.

Sustainability of Benefits

7. The sustainability of the limited benefits from the Project is uncertain, as it largely dependson the continuation of the institutional improvements that started to materialize at the very end ofProject implementation. In particular, it is not enough that taxes and utility tariffs continue toimprove but the collection of the dues must also turn substantially more efficient than it was at thetime IDA closed the operation. See paras. 16,17 and GOG comments in Annex 5.

- Ill -

Findings and Lessons

8. The Project lacked realism, partly due to hasty preparation which was apparently related toIDA's concern to have a large impact on the sector quickly. This fact is somewhat obscured by theoccurrence and consequences of the major drought, mostly identified as the main factor thatnegatively affected Project implementation and forced IDA to restructure the operation. However,even without this uncontrollable factor, the operation had little prospect for success. A basicprinciple which should have been applied more firmly is that, at any point in time, the Project'simplementing agencies must have the capability (if necessary, through Technical Assistance and/orother measures) to carry out the Project measures foreseen for that time. The ability to implementthe initial measures should have been in place already at the Project's start.

9. The Project should have had less components and objectives to account for the weakness ofthe implementing agencies which were already evident at Project preparation. A concentration onadvancing reforms and institutional strengthening in "core" public urban activities such as watersupply, waste management and other crucial environmental aspects, could have fulfilled thiscondition, provided such measures were clearly identified as feasible in the project environmentprevailing at the time. Even so, the earliest possible setting up of a strong Project coordinatingbody, like the Urban Project Cell as it worked in the later years, would have substantially improvedthe prospects. Such a body should be tasked inter alia with unifying the approach to design,procurement and execution of similar Project components in different places by different executingagencies. However, the part of such an organization should be designed to progressively transcendthe initial role in the project, to extend its expertise and growing capacities throughout the Project'sinstitutional context. Otherwise, the institutional impacts of the coordinating body tend to disappearon project completion, reducing the sustainability of the operation's benefits.

10. The implementation prospects for complex projects involving urban services andinvestments would also be strengthened if, at project launch, a strong intermediary capacity isestablished. The role and authority of such an entity should considerably exceed those of UPC asthey should include wide responsibility for (i) project implementation performance, (ii)developmental support to implementing agencies, and (iii) a clear focus on financial objectives andmanagement in the participating entities.

11. In complex projects, even if much less complicated than this Project, monitoring physicalprogress and procurement should be more streamlined from the outset to ensure that the BankGroup staff responsible for project supervision are better able to focus on the main issues, whichshould only occasionally be in procurement. The monitoring framework should be aimed atensuring that supervision missions avoid spending excessive time checking on procurement statusand physical progress in many sub-projects, at cost to more strategic issues.

12. A project restructuring should address the core weaknesses that prompted the projectmodification. In this case, the restructuring of the Project made it, if anything, more complex, asmore items were added than deleted, though the goals of the new components were prima facieeasier to achieve than those for the deleted items. Furthermore, the addition of a rural water supply

- iv -

and sanitation component introduced an essentially new type of specialty into the Project mix,increasing the difficulties for IDA's supervision.

13. There is a need to take fuller account of the lessons learned from past urban projects duringpreparation of future projects, particularly with regard to size and the impact of complexity onproject outcomes. Clearly, a tradeoff must be made between the desire for quick, large scaleprojects with perceived major sectoral impacts, and smaller, more manageable, and ultimately moresustainable projects that are more in line with the existing reality of weak institutions and, in thecase of municipalities, the slow pace of financial devolution.

14. IDA's budgeting for supervision should take more account of the complexity of a projectand the capabilities of the Borrower and Beneficiary agencies. The corollary is that IDA shouldavoid committing itself to very complex projects which, in view of the institution's budgetarysituation (already tightening in the 1980s), are likely to be too costly to effectively supervise.

INDIA

GUJARAT URBAN DEVELOPMENT PROJECT(CREDIT 1643-IN)

IMPLEMENTATION COMPLETION REPORT

PART I: PROJECT IMPLEMENTATION ASSESSMENT

A. Evaluation of Project Objectives

Project Context

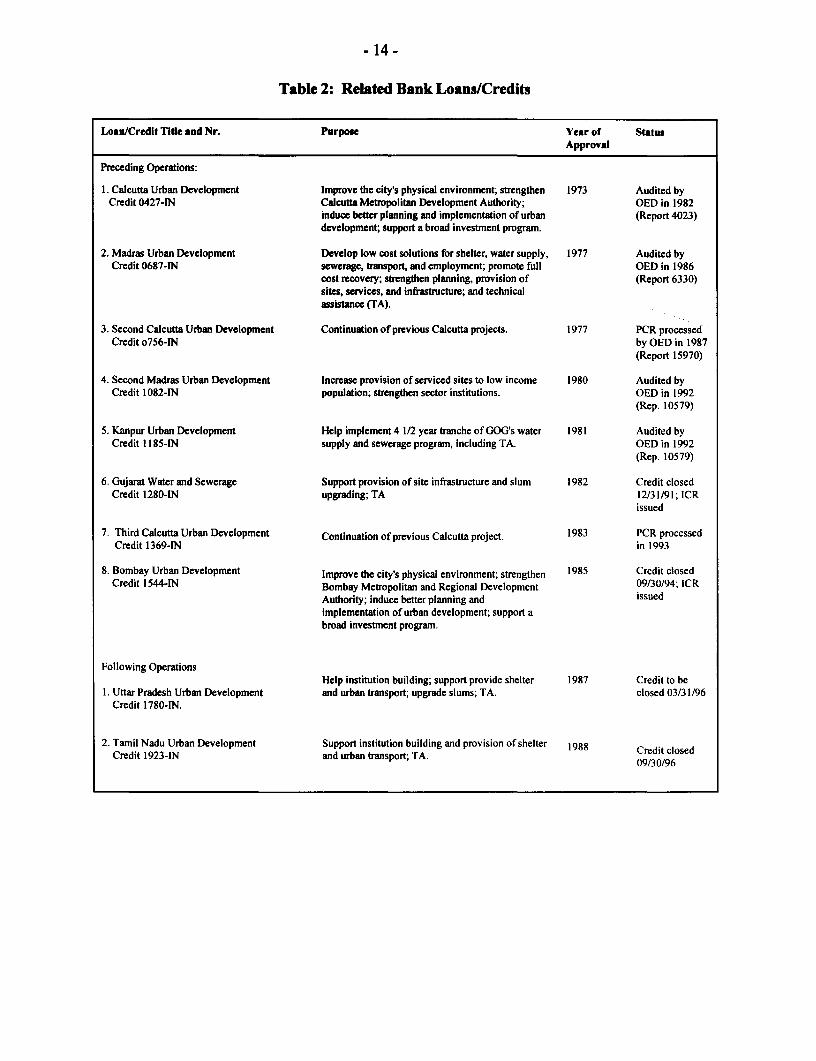

1. The Bank Group's lending for urban development in India started with the large watersupply and sewerage operation in Bombay (Credit 0390 of 1973) and the Calcutta UrbanDevelopment Project (Credit 0427 also of 1973) which had an important water supply andsewerage component. These were followed, between 1975 and 1981, by three further projectscovering mainly urban water supply and sanitation in Uttar Pradesh, Bombay, and Maharashtra, aswell as by three urban development operations addressing a wider range of issues (including areadevelopment, slum upgrading, and improvement of municipal services) in Kanpur in Uttar Pradesh,Madras (2 projects), and Calcutta (2 projects)..

2. Starting in the first half of the 1980s, IDA encouraged the preparation by state governmentsand appropriate consultants of Urban Sector Memoranda for the respective states; the second of thisseries was that for Gujarat State, which was completed in 1983 and which served as a basis for theproject discussed here (the Project). In 12/85, two years after its formal identification by IDA, theinstitution's Board of Directors approved the operation. The parties signed the correspondingagreements four months later. In 1987 and 1988, IDA approved two further projects with similarobjectives for the Uttar Pradesh and Tamil Nadu states, respectively. To the present, these were toremain the last specific urban development projects in India.

Project Objectives and Content

3. The Project's broad objectives were to reduce the deficits in urban shelter, infrastructure,and services in the main centers of the state. To assure progress in this direction in the longer run,the Project was to strengthen planning, administration, and financial management in localgovernment and state agencies in the urban sector. Through this operation and the similar ones inUttar Pradesh and Tamil Nadu, IDA further aimed at helping catalyze policy reform in India's urbansector. The general objectives were well in line with IDA's broad policies both in the urban sectorand in India. They also were in agreement with the state governments' objectives for the urbansector set forth in the Sector Memorandum mentioned earlier, and compatible with CentralGovernment's goals. However, IDA's wish to produce quickly a large impact on the sector, paired

- 2 -

with the Borrower's and the sector's urgent needs for funds and other support, contributed to theelaboration of a project that was unrealistically ambitious.

4. The main Project components addressing a complex set of sub-objectives were: (i)development of about 100 ha in six cities with 65% of the resulting plots affordable to low incomegroups, all the plots to be allocated on the basis of criteria agreeable to IDA, at market prices forhigher income beneficiaries, lower income families being able to avail themselves of low costshelter loans; (ii) town planning schemes covering some 570 ha in three cities and including landre-adjustment as well as basic infrastructure; (iii) upgrading of some 250 ha of slums in five citieswith appropriate cost recovery schemes; (iv) improvement in collection, storage, transportation anddisposal of solid waste as well as in maintenance of the corresponding facilities and equipment, alsoin five cities; (v) other priority investments in urban infrastructure and services such as watersupply, storm sewerage, waste water collection and treatment, in four areas; and (vi) institutionalstrengthening at local and state level through technical assistance (TA) to the Gujarat HousingBoard (GHB) of the Governnent of Gujarat, (GOG), the Gujarat Municipal Finance Board(GMFB) also of GOG, the Town Planning and Valuation Department (TPVD) of GOG, theAhmedabad Municipal Corporation (AMC), the Ahmedabad Urban Development Authority(AUDA), and other municipal entities.

Project Restructuring

5. In 1987, the first year after Credit 1643-IN had become effective, progress wasdisappointing, the main reason given being the drought conditions prevailing at the time in thestate, weakening several of the main agencies involved in Project implementation (especiallyAMC), and making them unable to carry out the agreed programs, both in the context of the Projectand the closely related Gujarat Water Supply and Sewerage Project supported by Credit 1280-INapproved in 1982. Therefore, towards the end of 1987, IDA started the planning of a re-structuringof both projects. For the Project, IDA's Board of Directors agreed to the new scope and conditionsin 08/89. The adjustments to the Project took into account that: (i) the disruption in the state'seconomy, which the drought had caused, had made it highly unlikely that Borrower andBeneficiaries would be able to implement successfully several of the Project components (indeed,several beneficiaries declared themselves unable to do so); (ii) the emergency justified a furthersupport to GOG rather than the cancellation of the credit; (iii) the scarcity of the drinking water inmany regions, especially drought-prone rural areas placed the population in such areas at risk andmade the pursuit of a regular economic activity exceedingly difficult; and (iv) the Gujarat WaterSupply Project already included a rural water supply component whose impact could bestrengthened through the inclusion in the Project of further rural schemes. Thus, the restructuredProject camne to include a reduced urban component and a new rural water supply part. The broadobjectives for the urban items were essentially the same as those of the original operation. Thosefor the water supply and sanitation component were the alleviation of the critical health situation indrought affected rural areas.

6. The restructuring (i) substantially reduced the area development component, (ii) cut thetown planning schemes to about one third of their original scope, (iii) halved the slum upgradingand solid waste management programs, (iv) reduced urban infrastructure components by about

- 3 -

20%, and (v) left essentially intact the originally planned investments in institutional strengthening.However, the previous poor progress of the Project had demonstrated the need for extensiveinstitutional strengthening beyond that foreseen in the original Project. Therefore, the revisionadded some US$ 2 million to the latter, leaving the specification of the items to be covered for theimplementation phase. This drastic curtailing of the urban component allowed the integration intothe Project of rural water supply and sanitation schemes that came to represent some 40% of therevised Project.

B. Evaluation of Objectives

7. Both the Project's broad objectives and the more specific sub-objectives were relevant andappropriate for Gujarat, one of the most industrialized states of India, that faced pressing needsbrought out in the previously mentioned sector memorandum. However, the detailed goals to beachieved through the various Project components did not adequately take into account the chronicfinancial and institutional weakness of the mostly municipal institutions that were to implementthese components, nor the absence of any GOG capability to compensate for this weakness. Thus,the operation was unrealistically ambitious and poorly designed. IDA's Staff Appraisal Report(SAR) acknowledges such institutional weaknesses and foresees an array of measures to overcomethem. However, it assumes that, even before the shortcomings could be eliminated, the sectorwould be able to carry out a program far more substantial (even in physical terms) than what it hadimplemented in the years preceding the Project. For example, the SAR assumes that AhmedabadMunicipal Corporation (AMC) was about to double its annual investment (in current terms) in thefirst two years of Project implementation and to quadruple it until the assumed closing date of theIDA credit. Further, IDA might have foreseen that it would have difficulties properly supportingthe sector through Project supervision, as the set of sub-objectives called for the involvement ofabout twelve different agencies, implementing a great number of sub-projects in various fields.

8. At restructuring, the elimination of a series of non-performing Project items and of severalexecuting agencies made the remaining urban sub-objectives more achievable. However, at thesame time, the modification introduced into the Project numerous new sub-projects aiming at ruralwater supply and sanitation, an area essentially extraneous to the original Project. It also broughtinto the Project a new executing agency, the Gujarat Water Supply and Sanitation Board (GWSSB).The latter also needed strengthening, a drawback that was somewhat compensated by the fact thatthe entity had already substantial experience with a Bank Group project (the Gujarat Water SupplyProject). Nevertheless, the number of sub-projects increased rather than decreased, as would havebeen desirable, and the time schedule remained unrealistically tight for the urban components takenover from the original Project. For the new rural component the timetable also was overlyambitious.

C. Achievement of Objectives

9. It is evident that, in 1985-89, the Project was advancing in a way that it would have fallenfar short of most of the sub-objectives spelled out in the SAR or implied by the choice of

- 4 -

components. In the fields of area development, town planning, and slum upgrading, progress wasespecially disappointing in Ahmedabad, the state's main urban center. Therefore, Projectrestructuring drastically curtailed these urban components. But implementation continued at a slowpace and with poor results. Nevertheless, some of the institutions in Surat, Vadodara, andJamnagar, proved able to implement substantial parts of the envisaged programs in the areas ofsolid waste management and low cost sanitation, where ultimately, after long delays, even AMCachieved a modest measure of success. The GWSSB component was, by the Credit's closing date,implemented in a reasonably satisfactory way and some of the sanitation targets were evenexceeded. However, delays with respect to the 1989 time schedule were still substantial andimpeded the completion of several sub-projects by late 1995. See also Annexes 2 and 3.

10. The institutional strengthening that resulted from the Project was modest, at best. Thisapplies especially in relation to the objective of full cost recovery in municipal services, which wasan ultimate objective in most areas touched by the Project (SAR, paras. 4.01 to 4.07). However,success in this area implied the introduction of sweeping reforms in tax and tariff assessment aswell as in the collection of the corresponding dues, objectives that, during the Project, the executingagencies achieved only to a very limited degree. Recently, some movement towards the abovegoals seems to have set in, especially in AMC, where the prospects for improved financialperformance substantially improved. This progress was doubtlessly tied to IDA's efforts,especially its relentless insistence during the post-restructuring stages of the Project on improvedfinancial performance by the beneficiaries and on their meeting the covenants agreed with IDA.However, only a substantial change of focus and approach on the Borrower's side finally made theturnabout possible, and this was long after the Project had de facto been completed. The extent towhich this change is directly attributable to IDA activities can only be a matter of speculation.Nevertheless, in the strict context of the Project, TPVD benefited through its increased capacity tohelp develop urban planning in the individual centers increased, and GMFB was able to supportseveral cities in improving their financial management, inter alia through helping introduce accrualaccounting. These are positive results, although they fall short of the corresponding Project sub-objectives.

11. The Project did not address GWSSB's institutional weaknesses until the last two years ofProject implementation, when it helped finance a study of the institutional strengthening of theBoard, which should strengthen the planning for and future development of the institution. Duringthe Project, though not directly related to it, some promising changes occurred in the sector, whichultimately may also benefit GWSSB. Progressively, in Gujarat, in towns and cities of varying size,branches of municipal government responsible for urban services were transfonned (partly afteraggregation) into municipal corporations. While no panacea, this may have helped lessen the directpolitical influence on day-to-day management of such services, often pervasive before this.

- 5 -

D. Major Factors Affecting the Project

Factors Generally not Subject to Government Control

12. The main such factor was the series of droughts in Gujarat in the mid-1980s that severelystrained the financial and managerial resources of most implementing agencies, especially AMC. Itresulted in major drains on and reallocation of GOG resources otherwise needed for Projectactivities. In particular, funds originally earnarked as couterpart contributions to the Project werediverted to drought relief and could not be replaced, the more so as most municipalities, even undernormal circumstances, were then chronically failing to raise appropriate revenues and to collecttaxes, though the level of these had not been raised in a long time. Several major instances of civilunrest in Gujarat also negatively affected Project outcomes. Another factor which, as in many otherprojects, added a measure of difficulty to Project co-ordination, was India's federal setup and itsvarious effects on planning, project decision-making and accountability by and within anyindividual state such as Gujarat. Last but not least, ownership by GOG and the implementingagencies of various Project components, especially those aiming at institutional improvement, wasweak, especially during and after the droughts. GOG and the other implementing agenciesconcentrated their limited resources during these periods of emergency on ventures consideredmore urgent than the Project, with significant after-effects of overall progress.

Factors Generally Subject to Government Control

13. To improve the Project's chances of success, the responsible authoritiesshould -- much earlier than was actually done -- have enacted legislation to empower the localbodies to enhance tax structure and levels to meet at least the O&M expenses of the urban sector.They similarly should have de-linked at the earliest stage possible fees for services such as watersupply and sewerage from property tax and rationally fixed the latter on the basis of market rentsrather than on outdated standard rents. An early and more generalized introduction of accrualaccounting would also have been possible and helpful. In more recent years, the creation ofmunicipal corporations to run urban services, though probably only loosely connected with anyimpetus provided by the Project, helped improve the prospects for these services and thus for theurban Project components.

14. The SAR sets forth the creation of an Urban Project Cell to co-ordinate Projectimplementation as desirable. However, GOG set up such a body only after Project restructuring, asa result of substantial prodding by IDA,and even then, GOG support for the new body was initiallyweak. It was the appointment, in 1991, of a senior person to head the UPC that finally got theProject moving and led inter alia to: (i) much improved project monitoring and reporting; (ii)generally satisfactory procurement measures and actions; and (iii) better coordination of andsupport to the various Project agencies. Such strong guidance earlier in the Project would havebeen particularly valuable, as it would have facilitated e.g., the adoption of unified design andexecution criteria, as well as standard procurement procedures which were in agreement with IDA'sGuidelines. However, it is worth noting that the very success of the UPC subtly shiftedresponsibility (or at least the perception of such responsibility) away from the implementingagencies, which may have weakened the Project's effect on the institutions.

- 6 -

Factors Generally Subject to Implementing Agency Control

15. The institutional weakness of most implementing agencies led to delays in design,procurement, and implementation. The outcome was further negatively affected by frequentchanges by these agencies of composition and specifications of Project components. Theimplementing bodies themselves should have pressed for a stronger co-ordination of theirrespective Project activities. Improved tax collection by the participating agencies (even within thedeficient prevailing framework) could have substantially improved Project success. Staff trainingin general and, in particular, guidance towards a clear understanding of the Project and of thevarious agencies' responsibilities in its context, were often keenly missed during Projectimplementation.

E. Project Sustainability

16. The Project brought improved solid waste management in various cities. In Ahmedabad,AMC brought about belatedly yet finally, in a short time, notable improvements such as singlehandling of the city waste and disposal by more efficient means (albeit mainly after Projectclosure). The municipal bodies have in general increased the capacity of their mechanicalworkshops to maintain the additional fleet provided under the Project. Thanks in part to thetraining provided to municipal staff through GMFB and also the delegation of power from GOG,tax and charges collection has improved. There still needs to be further progress, in particularadjustments to the level of these taxes and charges to assure the longer term sustainability of thebenefits from the corresponding Project components. AMC's raising of the water supply andsewerage rates by almost 300% over 2 years for major user groups is, however, highly encouraging.It should lead to substantial improvements, provided collection of dues improves in a reasonablycommensurate and sustained way.

17. GWSSB not only implemented the five water supply and sanitation schemes introducedinto the Project in 1989, it essentially also operated and maintained them once they arecommissioned. In view of its substantial experience, it has the technical know-how to do thissuccessfully. However, the financial prospects are less encouraging. GWSSB expects to meetthe O&M expenses by water charges collected from the users. At the end of the Project, theserevenues did not meet expenses and GOG was unable to fill entirely the gap. GWSSB plans togradually increase the charges, but actual adjustments, until Project completion, remainedlimited. It also envisages handing over the completed village schemes to the correspondingpanchayats for operation and maintenance. The panchayats, under the guidance of GWSSB,would then be responsible for collecting the charges from the consumers. GWSSB itself wouldkeep the responsibility for maintaining the production of the water and for its delivery to thelocal systems.

18. However, all these arrangements and especially the setting of new levels of the charges,both on the part of GWSSB and of the panchayats, are not yet implemented, hence thesustainability of the benefits to be reaped from this Project component is still uncertain. Thesustainability of the benefits from the low cost sanitation component, by contrast, seems likely as

- 7 -

the rural families own and operate these facilities to which they have contributed their share ofthe capital costs and are therefore likely to adequately maintain these conveniences, (althoughGWSSB occasionally may have to provide some guidance with respect to the cleaning of thetwin pit latrines). Similar conclusions apply to the water supply and sanitation componentsexecuted in Ahmedabad, Surat, Vadodara, and Anand.

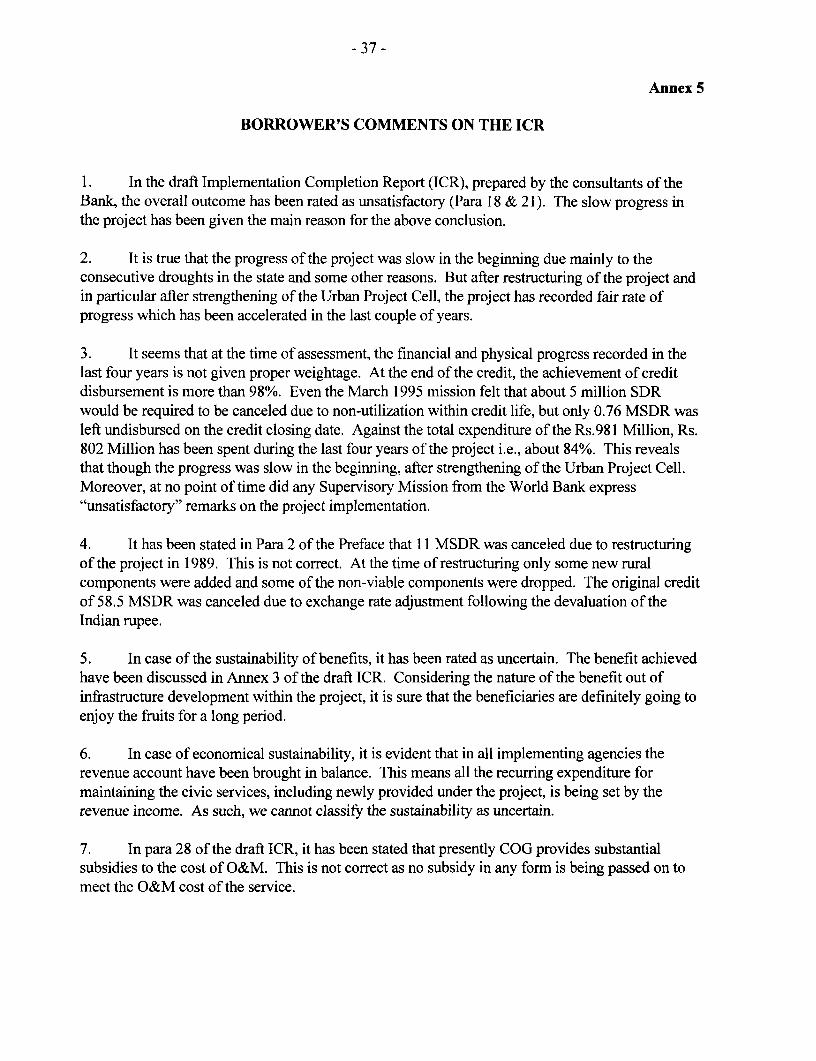

19. Overall however, the wider sustainability of the Project's intended benefits must presentlybe deemed uncertain (see COG comments in Annex 5).

F. Bank Performance

20. In the first half of the 1980s, IDA appropriately identified an urban project as one of thehighest priorities for Gujarat state. During project preparation, it was imaginative and constructivein assisting GOG and the municipalities develop a project that, at the time, must have seemedpromising. However, it appears to have grossly overestimated the technical and implementationcapability of the various institutions that were to carry out the components of the Project. WhileGOG and the senior representatives of the main entities to be involved in the Project manifestedtheir agreement with the broad objectives, the Bank appears to have downplayed the lack ofownership of the detailed sub-objectives by the bodies concerned. Therefore, while the resultingProject addressed pressing issues and was in agreement with IDA's policies for the country, thestate, and the sector, the Project ultimately suffered from a substantial lack of realism thatexacerbated the effects of the partly interconnected natural and political difficulties that the Projectfaced nearly from the beginning.

21. In 1987, IDA correctly saw that the prospects for the Project were poor and startedconsidering the restructuring of the operation, together with that of the Gujarat Water Supply andSewerage Project. The overhaul took some 18 months of major efforts. Though the inclusion ofthe rural water supply and sanitation component did not simplify the Project, it introduced a newimplementing agency, GWSSB, which at the time was showing improved capability to successfullycomplete the the separate (and also restructured) Gujarat Water Supply Project. It therefore seemedto be able to do the same in the context of the new rural water supply and sanitation component ofthe Project. In 1991, IDA perceived that the urban component of the Project still had not progressedsatisfactorily and appropriately insisted with GOG to strengthen the UPC by: (i) enlarging itsauthority in coordinating, centrally controlling and guiding the sector entities; and (ii) by placing asenior technical official at the head of the cell.

22. The Project was complex and IDA showed flexibility in adjusting components that did notwork or replacing them by more promising elements. During the entire implementation period, therelations between IDA personnel and the officers of GOG, the Beneficiaries and the executingagencies were cordial and cooperative. However, the various personnel changes in IDA's Projectsupervision and management weakened the effectiveness of the institution's supervision, which inthe early stages might have benefited from an increased and sustained stress on policy issues and oncovenant compliance. This could have possibly been offset by less tight control of procurement,which in any event should have been more streamlined from the start. In this respect, IDA, to some

- 8 -

extent, hampered itself by establishing an exceedingly low threshold for the value of the contractswhich it would review ex ante. Furthermore, IDA personnel involved in the Project felt that thesupervision budget, at times, failed to account adequately for the Project's complexity andprocurement-related supervision needs. The present ICR judges that, on balance, IDA'sperformance qualifies as "unsatisfactory", mainly due to the basic flaws of the initial Project scopeand implementation framework, which the restructuring only partly corrected, and to theinsufficiently effective IDA project supervision during the early stages.

G. Borrower Performance

23. The financial performance of the main municipal entities was poor before Project start.Indeed, the Project aimed inter alia at improving this aspect of sector performance, especially withrespect to the tax collection and recovery of service charges. However, as no quick improvementtook place, from early on in the Project, counterpart funding was deficient, and became even morealarmingly so, when the effects of the state-wide drought became increasingly evident. This andthe original Project's inherent weaknesses (complexity, lack of realism, and weak ownership by thelocal entities) discussed previously and exacerbated by the municipal entities' lack of experiencewith IDA procedures, led to the re-structuring of the Project in an effort to avoid outrightcancellation. Even after restructuring, overall performance, especially in the context of the Project'sremaining urban components, was less than satisfactory. It improved only after the UPC, at longlast, was strengthened. Then, at least some of the urban programs were carried out with reasonablesuccess, in Ahmedabad with the assistance of non-governmental organizations. The execution ofthe rural water supply and sanitation component proceeded from the start under better auspices, inpart because the implementing agency, GWSSB, had previous experience with IDA. As alreadymentioned, at the very end of the Project, the prospects for the financial recovery of the municipalentities, especially AMC, substantially improved, as the latter was permitted to apply large tariffincreases. The corresponding sustained improvements in collection still need to take place.

24. In summary, the Borrower's performance, which was clearly "unsatisfactory" under theoriginal Project, was better under the restructured operation but still rates as "unsatisfactory".

H. Assessment of Outcome

25. For the original Project, it is obvious that the outcome must be qualified as unsatisfactory.Though some progress was achieved toward the general goal of reducing deficits in urbaninfrastructure and services, the sector reached only very few of the relevant sub-objectives and hadlittle chance to fare better without the drastic change that the restructuring brought. Even after therestructuring had taken place, success on the urban components remained limited. (See COGcomments in Annex 5.)

26. Nevertheless, solid waste management in Ahmedabad was enhanced, and water supplyfacilities in East Ahmedabad have benefited some 40,000 people. In Surat, the completed stormdrains reduced flooding in areas inhabited by some 1.1 million people, the water supply component

- 9 -

provided an additional 50,000 people with safe water, area development made new living facilitiesavailable to 2,000 families, and some 5,000 families enjoy improved living conditions due to theslum upgrading programs. In Vadodara, new storm drainage provided flood relief to a populationof some 460,000, the strengthening of water supply will benefit some 80,000 people, and the slumupgrading reached about 850 families. Rajkot and Jamnagar have enhanced their capabilities insolid waste management towards a better urban environment. The essentially rural component,once completed, which is expected to take place in 1996/97, will provide safe water in over 1000individual villages with a total population of some 1.7 million. Further, over 70,000 low cost ruralsanitation units in 19 districts will benefit some 350,000 people and about 20,000 urban sanitationunits will improve the well-being of some 130,000 people in Ahmedabad. See also Annex 3.

27. At GOG level, TPVD has improved its planning capability through acquisition of aerialphotography interpretation equipment to develop improved town planning schemes. The cities thatparticipated in the training through GMFB developed better accounting, in part by the adoption ofaccrual systems and the use of computers acquired under the Project. Employing consultants underthe Project, municipal entities improved their planning and operational performance. There alsoseems to have been in the latest stages of the Project an improvement in the attitudes of municipalpersonnel concerned, promising improved ownership of endeavors similar to the Project's. In partas a consequence of the training through GMFB included in the Project's institutional improvementcomponent, the municipalities have raised their financial performance.

28. Even if the outcome of the restructured project was substantially better than that which theoriginal Project was on the way to achieve, it still rates all-in all as "unsatisfactory". The fact that itis impossible, on the basis of the available information, to calculate ex-post economic returns on theProject and/or its components, and to define satisfactorily whether the achievements arecommensurate with the invested IDA resources, both human and financial, is felt to re-inforce thisassessment.

-. Future Operations

29. The implementing agencies have prepared operating plans for some important water supplyfacilities to which the Project provided significant additions. Other agencies are still preparingsimilar outlooks for Project items they operate. GWSSB, in particular, plans to set forth such plansfor the rural water supply schemes. The documents presently available are essentially roughprojections of the operations without concrete proposals for measures to assure that the assumedgoals are achieved. Therefore, they do not qualify as operation plans, as required by IDA for itsICR. The validity of the submitted projections largely depends on the municipal bodies' ability toraise the resources for appropriate O&M. Presently, GOG still (directly and/or indirectly) providessubsidies to the cost of debt service, replacement, and future investment. There are encouragingsigns that, in the future, such subsidies will be substantially reduced and that the municipal bodieswill gradually improve their ability to sustain themselves. How fast this will be achieved dependsto a large extent on the continuation of the institutional improvements in part set in motion underthe Project and, last but not least, on the political will to achieve self-sustainability, whichinvariably is at a high political cost.

- 10-

J. Key Lessons Learned

30. The Project and its outcomes suggest the following main lessons, some of which are notnew but seem difficult to incorporate effectively in the preparation and implementation of the BankGroup's projects:

(a) The Project lacked realism, partly due to hasty preparation apparently related to IDA'sconcern to have a large impact on the sector quickly. This fact is somewhat obscured by theoccurrence and consequences of the major drought, mostly identified as the main factor thatnegatively affected Project implementation and forced IDA to restructure the operation.However, even without this uncontrollable factor, the operation had little prospect forsuccess. A basic principle which should have been applied more firmly is that, at any pointin time, the Project implementing agencies must have the capability (if necessary, assistedby consultants and other entities) to carry out the Project measures foreseen for that time. Inparticular, the basic ability to implement the initial strategies and measures must be in placealready at the Project's start.

(b) The Project should have had less components and objectives, to allow for the weakness ofthe implementing agencies which were already evident at Project preparation. Aconcentration on advancing reforms and institutional strengthening in "core" public urbanactivities such as water supply, waste management and other crucial environmental aspects,rather than allowing more diversified minicipal interests to be encompassed within theProject, could have better fulfilled this condition, wherever such measures in "core" areaswere clearly identified as feasible (with appropriate early Technical Assistance and/orsupporting consultancy services) in the project environment prevailing at the time. Theearliest possible setting up of a strong Project coordinating body, like the Urban Project Cellas it worked in the later years, would have substantially improved these prospects,particularly if such a body is clearly tasked with unifying the approach to design,procurement and execution of similar Project components in different places by differentexecuting agencies. However, such an entity should also be designed to progressivelytranscend its initial role in the Project, to extend its expertise and demonstrated capacitiesthroughout the Project's institutional context. Otherwise the coordinating body tends todisappear on project completion, thus reducing the longer-term institutional impact andsustainability of the operation.

(c) The implementation prospects for complex projects involving urban services andinvestments would be strengthened if, at project launch, a strong intermediary capacity isestablished. The role, mandate and authority of such an entity should considerably exceedthose of UPC, as they should include wide responsibility for: (i) project implementationperformance; (ii) developmental support to all implementing agencies; and (iii) a clear focuson achievement of financial objectives and improvements to financial management in theparticipating entities.

(d) In complex projects, even if much less complicated than this Project, monitoring physicalprogress and procurement should be more streamlined from the outset to ensure that the

- 11 -

Bank Group staff responsible for project supervision are better able to focus on the mainissues, which should only occasionally be in procurement. The monitoring frameworkshould be aimed at ensuring that supervision missions avoid spending excessive timechecking on procurement status and physical progress in many sub-projects, and can focuson more strategic issues.

(e) A project restructuring should address the core weaknesses that prompted the projectmodification. In this case, the restructuring of the Project made it, if anything, morecomplex, as more items were added than deleted, though the goals of the new componentswere prima facie easier to achieve than those for the deleted items. Furthermore, theaddition of a rural water supply and sanitation component introduced an essentially newtype of specialty into the Project mix, increasing the difficulties for IDA's supervision.

(f) There is a need to take fuller account of the lessons learned from past urban projects duringpreparation of future projects, particularly with regard to size and the impact of complexityon project outcomes. Clearly, a tradeoff must be made between the desire for quick, largescale projects with perceived major sectoral impacts, and smaller, more manageable, andultimately more sustainable projects that are more in line with the existing reality of weakinstitutions and, in the case of municipalities, the slow pace of financial devolution.

(g) IDA's budgeting for supervision should take more account of the complexity of a projectand the capabilities of the Borrower and Beneficiary agencies. The corollary is that IDAshould avoid committing itself to particularly complex projects which, in view of theinstitution's budgetary situation (already tightening in the 1980s), are likely to be too costlyto effectively supervise.

- 12-

PART II. STATISTICAL TABLES

Table la: Summary of Assessments (for Original Project)

A. Achievement of Objectives Substantial Partial Negligible Not Applicable

(x) (x) (x) (x)

Macroeconomic policies ( ) () ( ) (x)

Sector policies ( ) () (x)

Financial objectives () ( (x) ()

Institutional Development () (x) ( ) ()

Physical objectives () (x) ( ) ()

Poverty reduction () () (x) ()

Gender concems () ( ) ( ) (x)

Other social objectives () () () (x)

Environmental objectives () (x) () ()

Public sector management () (x) (

Private sector management ( ) ( ) () (x)

B. Proiect sustainabilitv Likelv Unlikely Uncertain

(x) (x) (x)

O) O) (x)

C. Bank Performance Highly Satisfactory Satisfactor Deficient

(x) (x) (x)

Identification () () (x)

Preparation assistance () () (x)

Appraisal () () (x)

Supervision () () (x)

D. Borrower performance HkighIy Safisfacor Satisfactoyn Deficient

(x) (x) (x)

Preparation () () (x)

Implementation () () (x)

Covenant compliance () () (x)

Operation (if applicable) () () (x)

D. Assessment of Outcome Higby satisfactorv Satisfactory Unsatisfactov Highlyunsatisfactorv

(x) (x) (x) (x)

O) O) (x) O

- 13 -

Table lb: Summary of Assessments (for Restructured Project)

A. Achievement of Objectives Substantial Partial Negligible Not Applicable

(x) (x) (x) (x)

Macroeconomic policies () ( ) ( ) (x)

Sector policies () (x) ( ) ()

Financial objectives ( ) (x) (

Institutional Development () (x) () ()

Physical objectives ( ) (x) ( )

Poverty reduction () () (x) ()

Gender concems () () () (x)

Other social objectives ( ) ( ) ( ) (x)

Environmental objectives (x) ( ) (

Public sector management (x) () (

Private sector management ( ) ( ) ( ) (x)

B. Proiect sustainability Like( Unlikely Uncertain

(x) (x) (x)

O O ~~~~~~~~~~~~~~~~~~(x)C. Bank Performance Highly Satisfactoa Satisfactory Deficient

(x) (x) (x)

Identification () (x) ()

Preparation assistance () (x) ()

Appraisal () (x) C)

Supervision C) (x) C)

D. Borrower performance Highlv Satisfactory Satisficto Deficient

(x) (x) (x)

Preparation () (x) ()

Implementation () C) (x)

Covenant compliance () (x) ()

Operation (if applicable) C) C ) (x)

D. Assessment of Outcome Highly satisfactory Satisfactory Unsatisfactory Highiyunsatisfactorv

(x) (x) (x) (x)

O) O) (x) O

- 14-

Table 2: Related Bank Loans/Credits

Loan/Credit Tide and Nr. Purpose Year of StatusApproval

Preceding Operations:

1. Calcutta Urban Development Improve the city's physical environment; strengthen 1973 Audited byCredit 0427-IN Calcutta Metropolitan Development Authority; OED in 1982

induce better planning and implementation of urban (Report 4023)development; support a broad investment program.

2. Madras Urban Development Develop low cost solutions for shelter, water supply, 1977 Audited byCredit 0687-IN sewerage, transport, and employment; promote full OED in 1986

cost recovery; strengthen planning, provision of (Report 6330)sites, services, and infrastructure; and technicalassistance (TA).

3. Second Calcutta Urban Development Continuation of previous Calcutta projects. 1977 PCR processedCredit o756-IN by OED in 1987

(Report 15970)

4. Second Madras Urban Development Increase provision of serviced sites to low income 1980 Audited byCredit 1082-IN population; strengthen sector institutions. OED in 1992

(Rep. 10579)

5. Kanpur Urban Development Help implement 4 1/2 year tranche of GOG's water 1981 Audited byCredit 1185-IN supply and sewerage program, including TA. OED in 1992

(Rep. 10579)

6. Gujarat Water and Sewerage Support provision of site infrastructure and slum 1982 Credit closedCredit 1280-IN upgrading; TA 12/31/91; ICR

issued

7. Third Calcutta Urban Development Continuation of previous Calcutta project. 1983 PCR processedCredit 1369-IN in 1993

8. Bombay Urban Development Improve the city's physical environment; strengthen 1985 Credit closedCredit 1544-IN Bombay Metropolitan and Regional Development 09/30/94; ICR

Authority; induce better planning and issuedimplementation of urban development; support abroad investment program.

Following OperationsHelp institution building; support provide shelter 1987 Credit to be

1. Uttar Pradesh Urban Development and urban transport; upgrade slums; TA. closed 03/31/96Credit 1780-IN.

2. Tamil Nadu Urban Development Support institution building and provision of shelter 1988 Credit closedCredit 1923-IN and urban transport; TA. 09/30/96

- 15 -

Table 3: Project Timetable

Steps in Project Cycle Date Planned Actual Date

Identification 11/83

Preparation 01-10/84

Appraisal 11/84

Negotiations 11/85

Board presentation 12/85

Signing 04/86

Effectiveness 07/86 11/86

Project completion 06/92 1996

Loan closing 12/92 03/95

Table 4: Loan/Credit Disbursements; Cumulative (Estimated and Actual)

FY87 FY88 FY89 FY90 FY91 FY92 FY93 FY94 FY95 FY96

Appraisal Estimate 3.10 11.78 21.08 31.00 42.16 55.80 62.00(million US$)

Revised Estimate 0.00 5.01 5.38 62.00(million US$)

Actual (million US$) 0.00 5.01 5.38 25.88 32.27 34.30 43.07 47.33 52.2 64.67

Actual in Terms of 0% 43% 26% 83% 77% 61% 69% 76% 84% 104%Appraisal Estimate

Actual (million SDR) 0.00 3.84 4.12 19.88 24.58 26.05 32.29 35.32 38.67 46.74

Table 5: Key Indicators for Project Implementation

Not applicable as the Project predates the standard requirement for key indicators.

Table 6: Key Operators for Project Operation

Not available; only the larger implementing agencies have prepared operating plans for municipalwater supply services (see Annex 4).

- 16 -

Table 7: Studies Included in Project

Purpose as DefinedStudy at Appraisal/Redefined Status Impact of Study

1. Urban Strategy for To analyze existing Completed Report submitted byState of Gujarat urban growth patterns NIUA is utilized for

and suggest alternate various developmentstrategies of purposes.development.

2. Urban Monitoring To study the existing Completed Report submitted bySystem monitoring system and TCS is implemented

to suggest suitable for monitoring themonitoring system for WB projects.WB projects.

3. Financial To study the prevailing Report completed SMC, VMC andConsultancy accounting system in JMC have

Municipal Corporations introduced theand to introduce the accrual accountingaccrual accounting system and otherssystem. are on process.

4. Mehsana Fluoride To detect the excessive Completed On the basis of theStudy fluoride concentration in finding of the study

Mehsana district, study GWSSB preparedits impact and suggest Second Rural Watersuitable improvements. Supply Project.

5. GWSSB To strengthen and Completed Report is underInstitutional Studies improve the institutional review by GOG.

capacity of GWSSB.

6. Mehsana Water To provide potable Completed Report is underSupply Project drinking water to review by GWSSB.

villages affected byexcessive fluoride in theexisting ground watersupply.

- 17 -

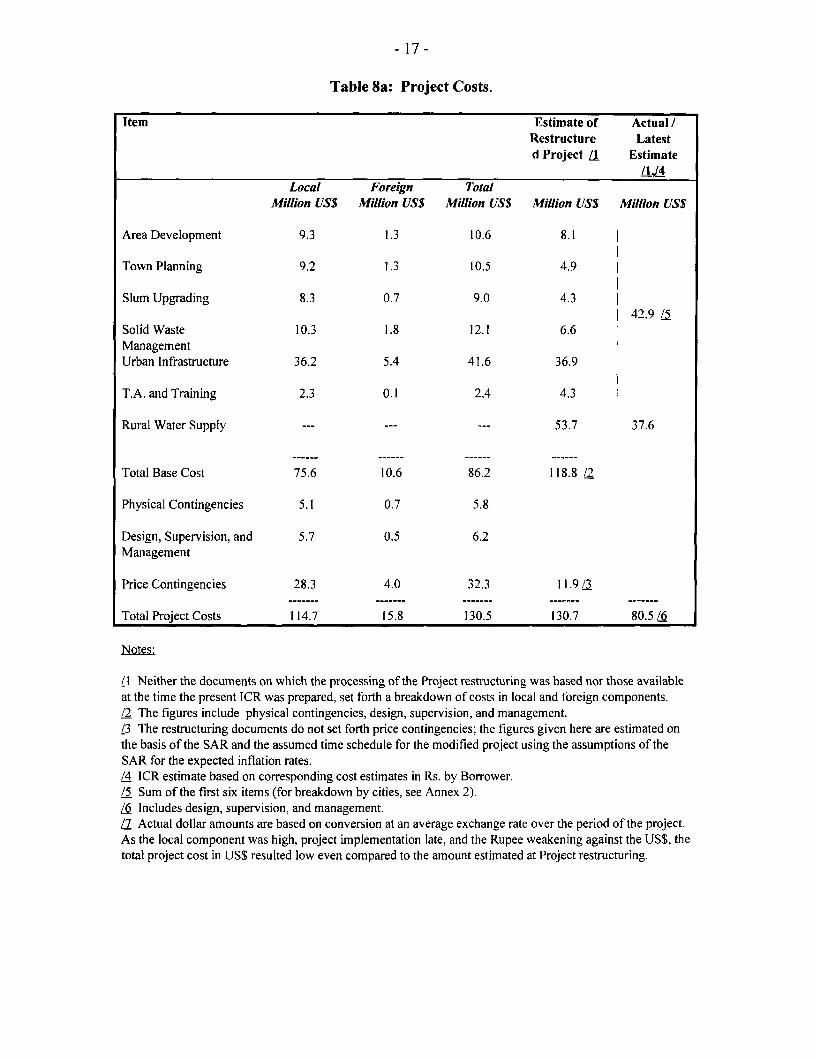

Table 8a: Project Costs.

Item Estimate of Actual /Restructure Latestd Project /1 Estimate

/I L4Local Foreign Total

Million US$ Million US$ Million USS Million US$ Million USS

Area Development 9.3 1.3 10.6 8.1

Town Planning 9.2 1.3 10.5 4.9

Slum Upgrading 8.3 0.7 9.0 4.3 I42.9 /5

Solid Waste 10.3 1.8 12.1 6.6ManagementUrban Infrastructure 36.2 5.4 41.6 36.9

T.A. and Training 2.3 0.1 2.4 4.3 I

Rural Water Supply --- --- --- 53.7 37.6

Total Base Cost 75.6 10.6 86.2 118.8 /2

Physical Contingencies 5.1 0.7 5.8

Design, Supervision, and 5.7 0.5 6.2Management

Price Contingencies 28.3 4.0 32.3 11.9 /3

Total Project Costs 114.7 15.8 130.5 130.7 80.5 /

Notes:

ll Neither the documents on which the processing of the Project restructuring was based nor those availableat the time the present ICR was prepared, set forth a breakdown of costs in local and foreign components./2 The figures include physical contingencies, design, supervision, and management.l3 The restructuring documents do not set forth price contingencies; the figures given here are estimated onthe basis of the SAR and the assumed time schedule for the modified project using the assumptions of theSAR for the expected inflation rates./4 ICR estimate based on corresponding cost estimates in Rs. by Borrower./5 Sum of the first six items (for breakdown by cities, see Annex 2)./6 Includes design, supervision, and management./7 Actual dollar amounts are based on conversion at an average exchange rate over the period of the project.As the local component was high, project implementation late, and the Rupee weakening against the US$, thetotal project cost in US$ resulted low even compared to the amount estimated at Project restructuring.

- 18-

Table 8b: Project Financing

Source Appraisal Estimate(million US$)

Local Foreign Total Restructured LatestCosts Costs Project Estimate/

Actual

IBRD/IDA: 46.27 15.73 62.00 73.10 64.67

Cofinancing institutions: 0.00 0.00 0.00 0.00 0.00

Other external sources: 0.00 0.00 0.00 0.00 0.00

Domestic contribution: 68.50 0.00 69.50 57.65 15.84

Total: 114.77 15.73 130.51 130.75 80.51

Table 9: Economic Costs and Benefits

At the time of Project restructuring, project content was fundamentally changed, but no new EIRRsdetermined. This applies in particular to the rural water supply and sanitation component, whichwas a new component. Therefore, the ICR cannot set forth a re-evaluation of the returns.

- 19 -

Table 10: Status of Legal Covenants

Agree- Section Covenant Present Original Revised Description of Commentsment type status fulfill- fulfill- covenant

ment mentdate date

Project 2.01(a) 3 C Gujarat shall relend funds Complied with terms of loans. Atequivalent to $41.7 million out restructuring costs of AMCof the proceeds of the Credit to components reduced by 1/2AMC under a Subsidiary Loan (covenant not changed). The loanAgreement to be entered into would have met 62% of SAR est.between Gujarat and AMC. costs & now after adjusting for XRThese funds are to be on-lent at & AMC component would meetan interest rate of not less than 250% of AMC est. costs.8.75% pa and repaid over aperiod of 20 years, including a4-year grace period

2.01(a) 4 C GOG shall provide, or cause to GOG provides loans to urbanbe provided, the funds, agencies to meet 2/3 of projectfacilities, services and other costs, 100% grant funds for urbanresources required for the inst. strengthening & for GWSSBproject by the implementing Rural WS components. UrbanAgencies Agencies cannot meet counterpart

contributions; GOG from late 1991agreed to provide funds.

2.01(b), 2 C 12/31/86 GOG shall ensure that Last results for FY 1993/94 show

Sch. beginning with financial year compliance.2(3) 1985/86, the Municipal

Corporations are able to meetall expenditure chargeable torevenue from local taxes andcharges, income from property,and normal grants, and that afterfinancial year 1985/86, theirrevenue accounts shall be keptin balance.

2.0 1(b), 2 C 3/31/90 GOG shall cause AMC to

Sch. apply, as appropriate, revenue2(4) increases and/or cost reduction

increases and/or cost reduction(b); policies so as to ensure that by3.0(i) March31, 1990, the cost of

operation, includingdepreciation, and maintenanceare covered by user charges forwater supply and special taxesfor sewerage imposed andcollected from said users.

- 20 -

Table 10: Status of Legal Covenants (cont'd)

Agree Section Covenant Present Original Revised Description of Comments-ment type status fulfill- fulfill- covenant

ment mentdate date

2.01(b), 2 C 03/31/93 After 03/31/88, GOG shall cause AMC in consultation withSch. 2(4) AMC to apply as appropriate, GOG has implemented a

revenue increases and/or cost time-based action plan to(c), reduction policies so as to ensure achieve compliance.3.0(iii) that by 03/31/93 the cost of

operation and maintenance anddebt service, excludingdepreciation, are covered by usercharges for water supply andspecial taxes for sewerageimposed and collected from saidusers.

2.01(b), 2 C Beneficiary selection criteria, All but one AreaSch. 2(5) including price levels, the terms Development Scheme has

and conditions of lease and of been deleted from thehire/purchase arrangements in project. In Surat ADS anArea Development Schemes existing community of slumshall be satisfactory to the residents are theAssociation and include, inter beneficiaries. Cost recoveryalia, an interest rate of not less is acceptable to the Bank.than 12% pa to the beneficiaries.

2.01(b), 2 C GOG shall ensure that the cost of Cost recovery is acceptableSch. 2(6) land and improvements shall be to the Bank.

recovered from the beneficiaries(in respect of slum upgrading)and the terms and conditions ofsale or lease shall be such asshall be satisfactory to theAssociation which shall include,inter alia, an interest rate of notless than 12% pa.

2.01 (b), 2 C GOG shall ensure that water Cost recovery is acceptableSch. 2(7) supply and sewerage facilities to the Bank.

provided on slum upgrading sitesshall be transferred to the localmunicipal govermments formanagement and the prevailingwater and sewerage rates shall becharged to the beneficiaries withindividual connections.

- 21 -

Table 10: Status of Legal Covenants (cont'd)

Agree Section Covenant Present Original Revised Description of Comments-ment type status fulfill- fulfill- covenant

ment mentdate date

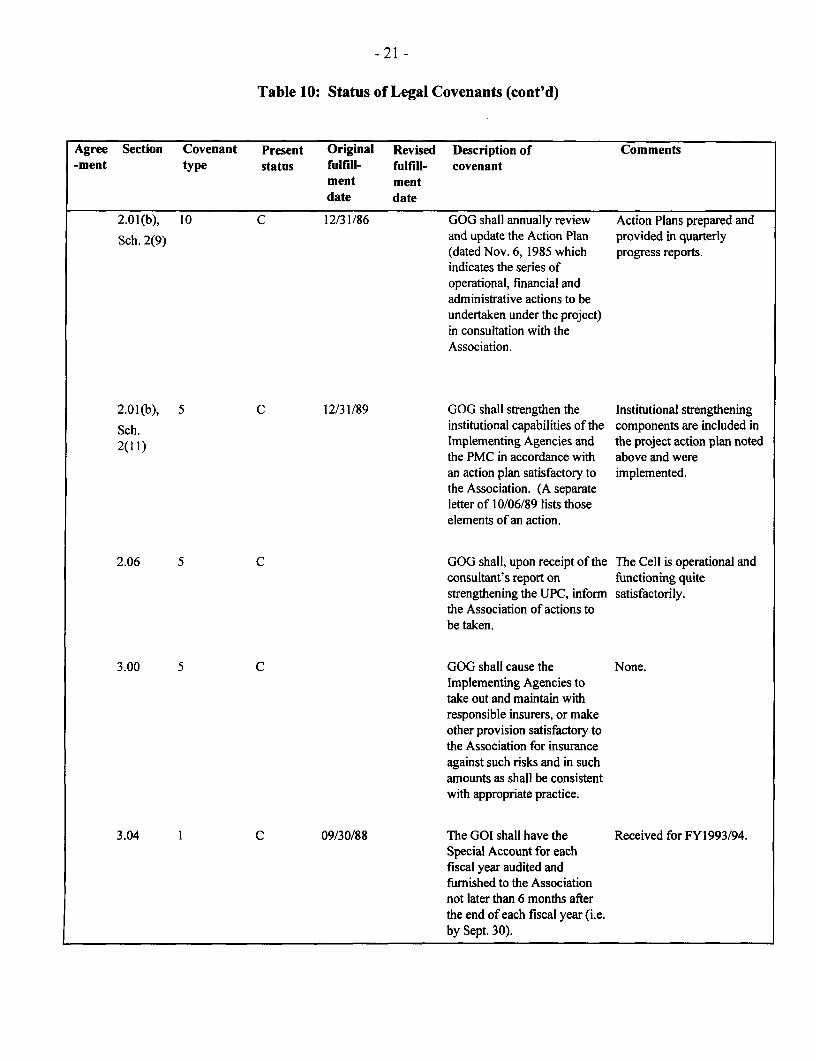

2.01(b), 10 C 12/31/86 GOG shall annually review Action Plans prepared andSch. 2(9) and update the Action Plan provided in quarterly

(dated Nov. 6, 1985 which progress reports.indicates the series ofoperational, financial andadministrative actions to beundertaken under the project)in consultation with theAssociation.

2.01(b), 5 C 12/31/89 GOG shall strengthen the Institutional strengtheningSch. institutional capabilities of the components are included in2(11) Implementing Agencies and the project action plan noted

the PMC in accordance with above and werean action plan satisfactory to implemented.the Association. (A separateletter of 10/06/89 lists thoseelements of an action.

2.06 5 C GOG shall, upon receipt of the The Cell is operational andconsultant's report on functioning quitestrengthening the UPC, inform satisfactorily.the Association of actions tobe taken.

3.00 5 C GOG shall cause the None.Implementing Agencies totake out and maintain withresponsible insurers, or makeother provision satisfactory tothe Association for insuranceagainst such risks and in suchamounts as shall be consistentwith appropriate practice.

3.04 1 C 09/30/88 The GOI shall have the Received for FY1993/94.Special Account for eachfiscal year audited andfurnished to the Associationnot later than 6 months afterthe end of each fiscal year (i.e.by Sept. 30).

- 22 -

Table 10: Status of Legal Covenants (cont'd)

Agree Section Covenant Present Original Revised Description of Comments-ment type status fulfill- fulfill- covenant

ment mentdate date

4.01 1 C 12/31/87 GOG shall cause the None.(a&b), Implementing Agencies to

Sch. maintain separate records2(a&b) and accounts related to the

Project and to furnish tothe Association auditedcopies within 9 months ofthe end of each financialyear (i.e. by December 31).The audit is to be inaccordance withappropriate auditingprinciples consistentlyapplied by independentauditors acceptable to theAssociation..

4.01(c), I C 12/31/87 Implementing Agencies to None.

2(c) maintain separate recordsand accounts of SOEs.Such accounts are to beincluded in the annualaudit of the projectaccounts, but a separateaudit opinion is required tothe effect that suchexpenditures have beenused for the purposes forwhich they were provided.

Credit 5.01 3 C A Subsidiary Loan Agreement executed Sept.Agreement may be 12, 1986.executed on behalf ofGujarat and AMC.

Covenant types: 8. = Indigenous people9. = Monitoring, review, and reporting

I. = Accounts/audits 10. = Project implementation not covered by categories 1-92. = Financial performance/revenue generation from 11. = Sectoral or cross-sectoral budgetary or other resource

beneficiaries allocation3. = Flow and utilization of project funds 12. = Sectoral or cross-sectoral policy/4. = Counterpart fiunding regulatory/institutional action5. = Management aspects of the project or executing 13. = Other

agency C = covenant complied with6. = Environmental covenants CD = complied with after delay

7. = Involuntary resettlement CP = complied with partially8. = Present Status: NC = not complied with

- 23 -

Table 11: Compliance with Operational Manual Statements

The ICR did not identify any deviation of substance from the relevant OMS.

Table 12: Bank Resources - Staff Inputs

Stage of Planned Revised ActualProject Cycle

Weeks 1OOOUSS Weeks 1OOOUS$ Weeks 1000US$

Through appraisal n.a. n.a. 109.2 140.7

Appraisal - Board n.a. n.a. 10.9 18.7

Board - effectiveness n.a. n.a. /I L1

Supervision n.a. n.a. 164.3 310.6

Completion n.a. n.a. 5.0 a2 11.2 /2

Total n.a. n.a. 289.4 481.2

L. Included under Supervision.

12 Estimated.

- 24 -

Table 13: Bank Resources - Missions

Stage of Month/ Number of Days Specialized Staff Performance rating Types of ProblemsProject Cyde Year Persons in Field Skills Represented

hiyem-nt Stat Develop.us Inpact

Through 09/82 6 15 ME,FA,UE,BISappraisal

06/83 5 12 AP,ME,FA,UD

11- 5 12 AP,ME,FA,UP,L12/83

6 12 AP,ME,FA,UE,MF05-06/84 3 4 AP,ME

09/84

Appraisal 11/84 4 14 AP,ME,FA -- -- --

throughBoardapproval

Board 05/86 3 9 FA,PM -- -- --

approvalthrougheffectiveness

Supervision 02/87 4 12 AP,ME,FA,PM 2 3 slow start

10/87 3 11 FA,PM 2 2 Continued slow progress,a project restructuring

envisaged.

Restructuring mission.01- 4 19 AP,FA,PM 2 2 Progress slow.02/88a

1 4 AP 2 2 Progress slow on restructured10/88 project.

3 12 AP,FA 2 202/89 Progress slightly improved.a Difficulties in design of slum

upgrading.4 12 AP,FA,UP,RW 2 2

04/90 Weak implementing agencies

a and central monitoring.

Progress on urban componentstill slow.

3 15 FA,UP 2 211/90 (see above)a

(see above)

3 11 AP,FA,UP 2 203-04/91 Cost recovery

(see above)

- 25 -

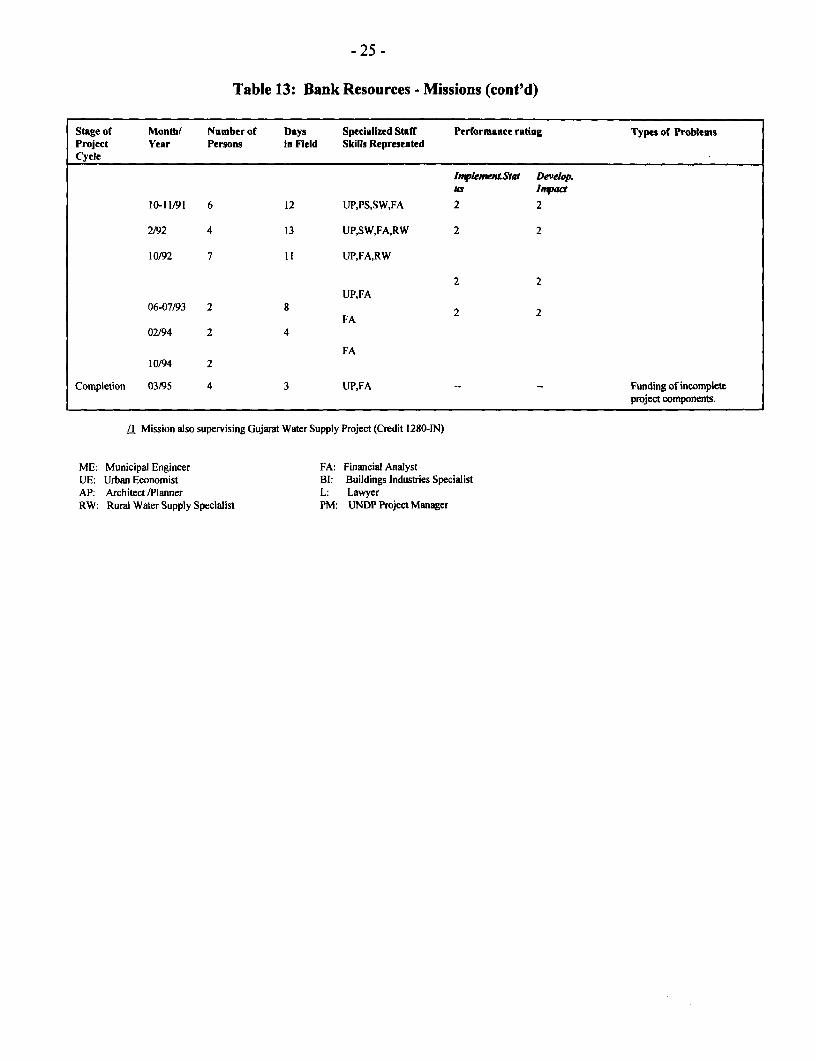

Table 13: Bank Resources - Missions (cont'd)

Stage of Month/ Number of Days Specialized Staff Performance rating Types of ProblemsProject Year Persons in Field Skills RepresentedCycle

IyplemenJStat Develpous Ir,ad

10-11/91 6 12 UP,PS,SW,FA 2 2

2/92 4 13 UP,SW,FA,RW 2 2

10/92 7 11 UP,FA,RW

2 2UP,FA

06-07/93 2 8 2 2FA22

02/94 2 4

FA10/94 2

Completion 03/95 4 3 UP,FA -- - Funding of incompleteproject components.

/I Mission also supervising Gujarat Water Supply Project (Credit 1280-IN)

ME: Municipal Engineer FA: Financial AnalystUE: Urban Economist Bl: Buildings Industries SpecialistAP: Architect/Planner L: LawyerRW: Rural Water Supply Specialist PM: UNDP Project Manager

- 26 -

AnnexIGUJARAT URBAN DEVELOPMENT PROJECT

Composition and Approximate Cost Breakdown of Original andRestructured Project

Crores Rs. Crores Rs. Million USS Million USS

Item Original Restructured Original Restructured

Project Project Project Project

Area Development

- Ahmedabad 3.60 0.00 3.00 0.00

- Surat 1.92 1.92 1.60 1.47

-Gorwa 6.08 7.27 5.06 5.59

- Ankleshwar 0.98 0.00 0.82 0.00

-Palanpur 1.35 1.35 1.13 1.04

Subtotal 13.93 10.54 11.61 8.11

Town Planning Schemes

- Ahmedabad 10.77 0.00 8.97 0.00

- Surat 3.32 3.32 2.77 2.56

- Ankleshwar 1.23 0.00 1.03 0.00

- Anand 0.00 1.40 0.00 1.08

- Petland 0.00 1.60 0.00 1.23

Subtotal 15.32 6.32 12.77 4.86

Slum Upezradone

- Ahmedabad 7.37 3.03 6.15 2.33

- Vadodara 0.34 0.34 0.28 0.26

- Surat 1.13 1.13 0.94 0.87

- Janinagar 3.02 1.10 2.52 0.85

- Jetpur 0.75 0.00 0.63 0.00

Subtotal 12.61 5.59 10.51 4.30

Solid Waste Manaaement

- Ahmedabad 5.47 2.31 4.56 1.78

- Vadodara 2.64 2.64 2.20 2.03

- Surat 3.76 2.61 3.13 2.01

- Rajkot 2.19 1.06 1.82 0.82

- Jamnagar 1.33 0.00 1.11 0.00

Subtotal 15.38 8.62 12.82 6.63

- 27 -

Annex I (con'd)

Urban Infrastructure

-Ahmedabad 52/09 35.16 43.41 27.05

-Vadodara 1.62 1.62 1.35 1.24

- Surat 4.01 9.00 3.34 6.92

- Jamnagar 0.00 0.75 0.00 0.58

- Anand 0.00 1.48 0.00 1.14

Subtotal 57.72 48.01 48.10 36.93

Institutionall StrEnoithning

-Ahmedabad 1.47 1.47 1.22 1.13

- Surat 0.04 0.00 0.03 0.00

- Rajkot 0.02 0.02 0.02 0.02

- Jamnagar 0.02 0.02 0.02 0.02

- GHB 0.04 0.04 0.03 0.03

- GMFB 0.95 0.95 0.79 0.73

- Survey/Photog./Mapping 0.28 0.65 0.23 0.50

- Unallocated 0.00 2.39 0.00 1.84

Subtotal 2.82 5.54 2.35 4.27

Totl

- Ahmedabad 80.77 41.97 67.31 32.28

- Vadodara 4.59 4.59 3.83 3.53

- Surat 14.17 17.98 11.81 13.83

-Rajkot 2.21 1.08 1.84 0.83

-Jarnnagar 4.37 1.87 3.65 1.44

-Gorwa 6.08 7.27 5.06 5.59

- Ankleshwar 2.21 0.00 1.84 0.00

- Palanpur 1.35 1.35 1.13 1.04

- Jetpur 0.75 0.00 0.63 0.00

- Anand 0.00 2.88 0.00 2.22

- Petland 0.00 1.60 0.00 1.23

- GHB 0.04 0.04 0.03 0.03

- GMFB 0.95 0.95 0.79 0.73

- Survey/Photog./Mapping 0.28 0.65 0.23 0.50

- Unallocated (Others) 0L 11 gm0 192

117.90 84.74 98.25 65.18

- 28 -

Annex 2

GUJARAT URBAN DEVELOPMENT PROJECT (CREDIT 1643-IN)

Base Costs and Physical Contingencies

Crores Rs. Crores Rs. Crores Rs. Million US$ Million USS Million USS

Item Original Restr. Actual Original Restr. Actual

Project Project Estimated Project (#I) Project (#2) (#4)

- Ahmedabad 80.77 41.97 62.98 67.31 32.28 24.22

-Varodha 4.59 4.59 16.51 3.83 3.53 6.35

- Surat 14.17 17.98 22.62 11.81 13.83 8.70

- Rajkot 2.21 1.08 1.57 1.84 0.83 0.60

-Jamnagar 4.37 1.87 1.15 3.65 1.44 0.44

-Gorwa 6.08 7.27 - - - - 5.06 5.59 0.00

- Ankleshwar 2.21 0.00 - -. - - 1.84 0.00 0.00

-Palanpur 1.35 1.35 - - 1.13 1.04 0.00

- Jetpur 0.75 0.00 - -. - - 0.63 0.00 0.00

- Anand 0.00 2.88 4.39 0.00 2.22 1.69

- Petland 0.00 1.60 - - . - 0.00 1.23 0.00

- GHB 0.04 0.04 - -. - - 0.03 0.03 0.00

-GMFB 0.95 0.95 1.01 0.79 0.73 0.39

- Survey/Photog./Mapping 0.28 0.65 0.75 0.23 0.50 0.29

- Unallocated (Others) 0.11 2.50 0.65 0.09 1.92 0.25

117.90 84.74 111.63 98.25 65.18 42.93

SAR 117.89 98.24 0.00 0.00

UPC Report 117.88 84.76 98.23 65.20 0.00

Rural Water Supply and Sanitation

- GWSSB 0.00 69.75 97.70 0.00 53.65 37.58

Total Excluding Price Contingencies

117.89 154.49 209.33 98.24 118.84 80.51

- 29 -

Annex 2 (con1

Crores Rs. Crores Rs. Crores Rs. Million USS Million USS Million USS

Original Restr. Actual Original Restr. Actual

Project Project Estimated Project (#I) Project (#2) (#4)

Price Contingencies (#3)

38.72 15.49 0.00 32.27 11.91 0.00

Total Including Price Contingencies

156.61 169.97 209.33 130.51 130.75 80.51

1: I US$ = Rs 12 (as per SAR

2: 1 US$ = Rs 13 (as per restructuring documents

3: The restructuring documents do not set forth the price contingencies; the figures given here areestimated on the basis of the SAR and the assumed time schedule for the modified projectusing the assumptions of the SAR for the expected inflation rates.

4: ICR estimate based on corresponding cost estimates in Rs.

- 30 -

Annex 3

GUJARAT URBAN DEVELOPMENT PROJECT (CREDIT 1643-IN)

THE PROJECT, ITS RESTRUCTURING, AND THE BENEFITS ACHIEVED

1. As mentioned under table 9, the ICR cannot quantify the benefits resulting from theproject. Therefore, the following discusses the main project items, how they were modified byproject restructuring, and roughly sets forth the results achieved, though it is difficult to relatethese to the quantitative goals of the project, both original and restructured. See also Annexes Iand 2.

Original Items As Modified At Project Restructuring

2. Ahmedabad Municipal Corporation (AMC) was expected to carry out a US$ 67 millionprogram covering area development, town planning schemes, slum upgrading, solid wastemanagement, priority urban infrastructure, and institutional strengthening. At restructuring, thefirst two items were eliminated and the other ones roughly cut by half. Nevertheless, by 1995,AMC was able, at least in part due to the project, to provide better water supply as well asimproved sewerage pumping and solid waste disposal. It also had made available 20,000 additionallatrines to individual low income families.

3. Originally, Surat Municipal Corporation (SMC) was planned to implement a US$ 12million program in the same six above main fields addressed by the project. At restructuring, theprogram was increased by some US$ 2 million, whereby the area development, town planning, andsolid waste management components were slightly reduced, but the urban infrastructure itemsabout doubled. During project implementation, SMC laid 27 km of storm drains serving some 45km2, considerably easing the city's water logging problems. It strengthened the water distributionsystem benefiting about 50,000 people; 2000 families could be accommodated in newly developedareas; some 5000 families benefited from slum upgrading; and solid waste management wasimproved.