world bank document · pdf filedocument of the world bank ... 19. participatory approach .13...

TRANSCRIPT

Document ofTHE WORLD BANK

Report No. 17019-ZA

PROJECT APPRAISAL DOCUMENT

1TE REPUBLIC OF ZAMBIA

POWER REHABILITATION PROJECT

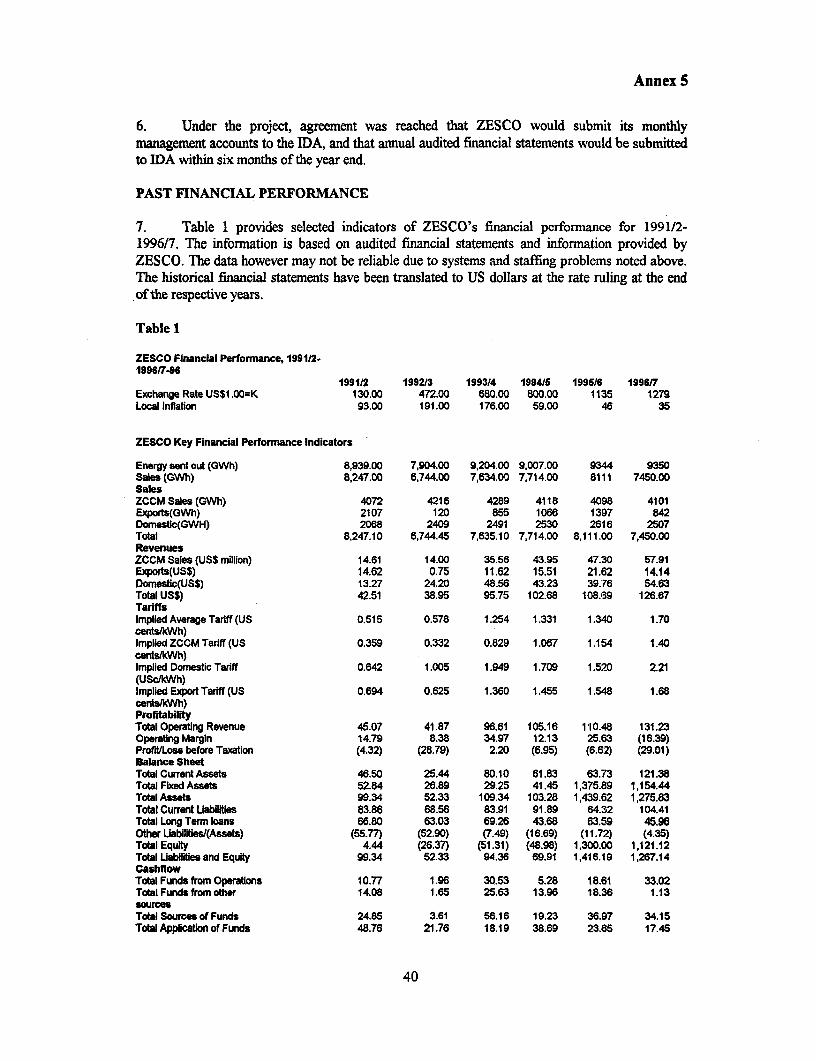

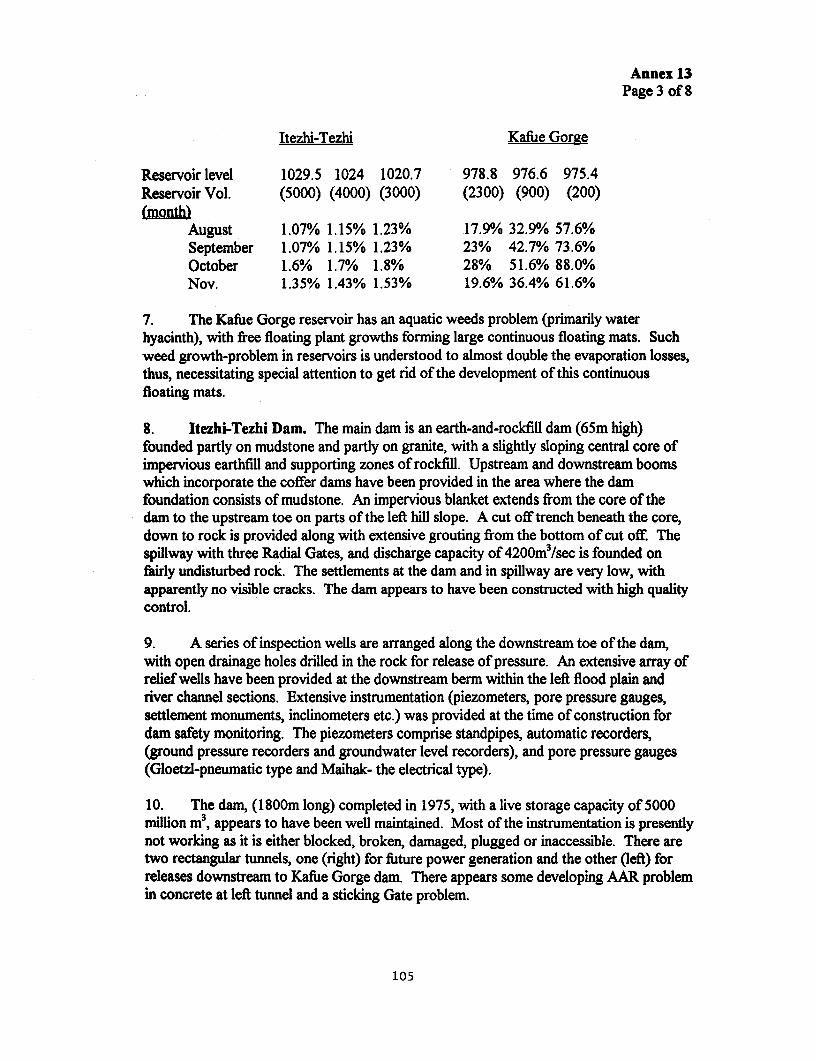

January 14, 1998

Energy TeamAfrica Region

Pub

lic D

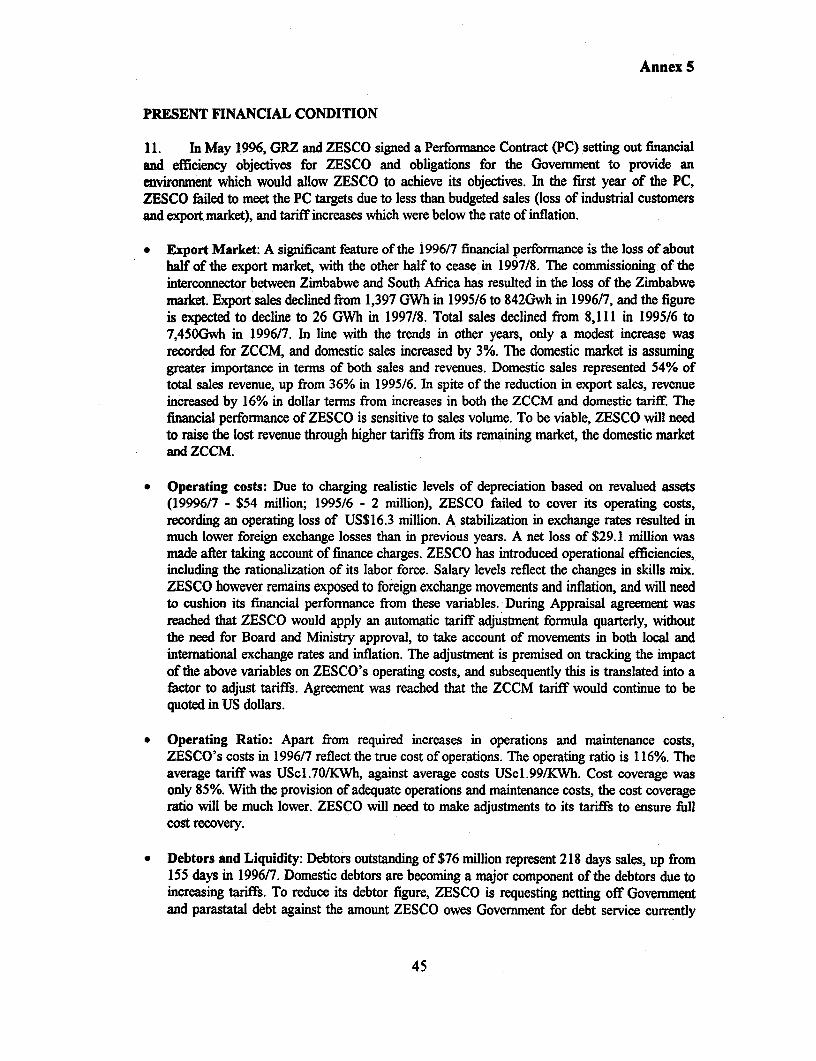

iscl

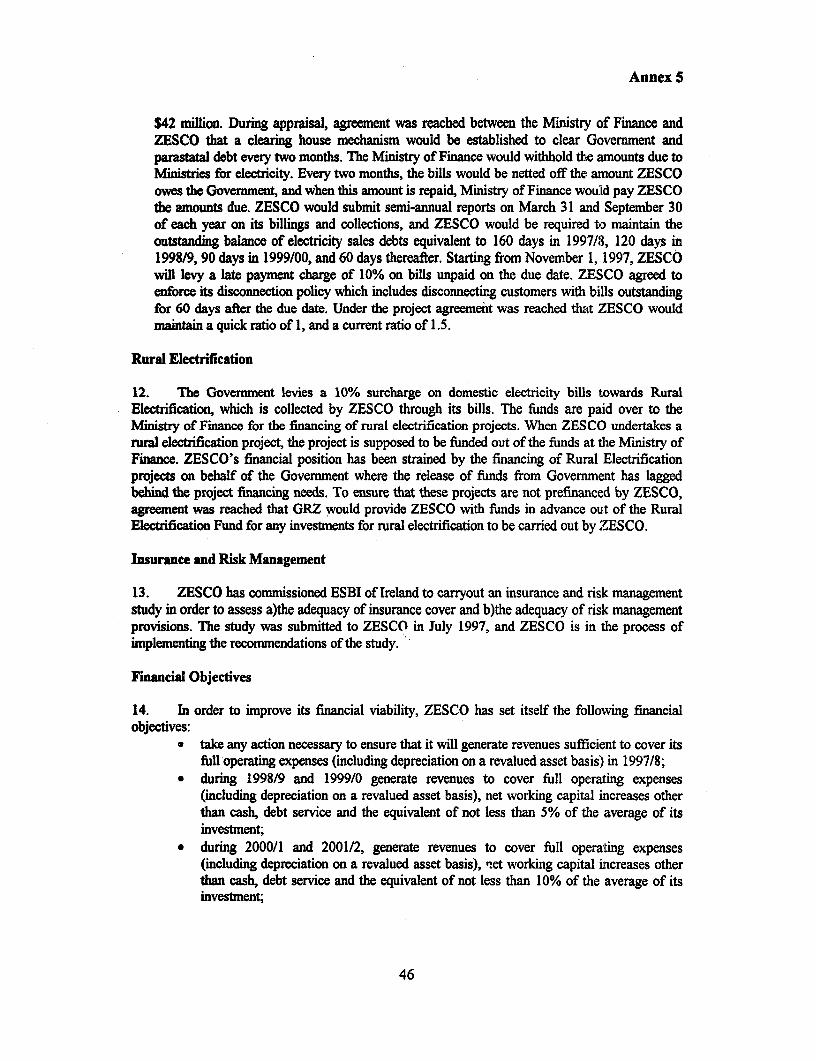

osur

e A

utho

rized

Pub

lic D

iscl

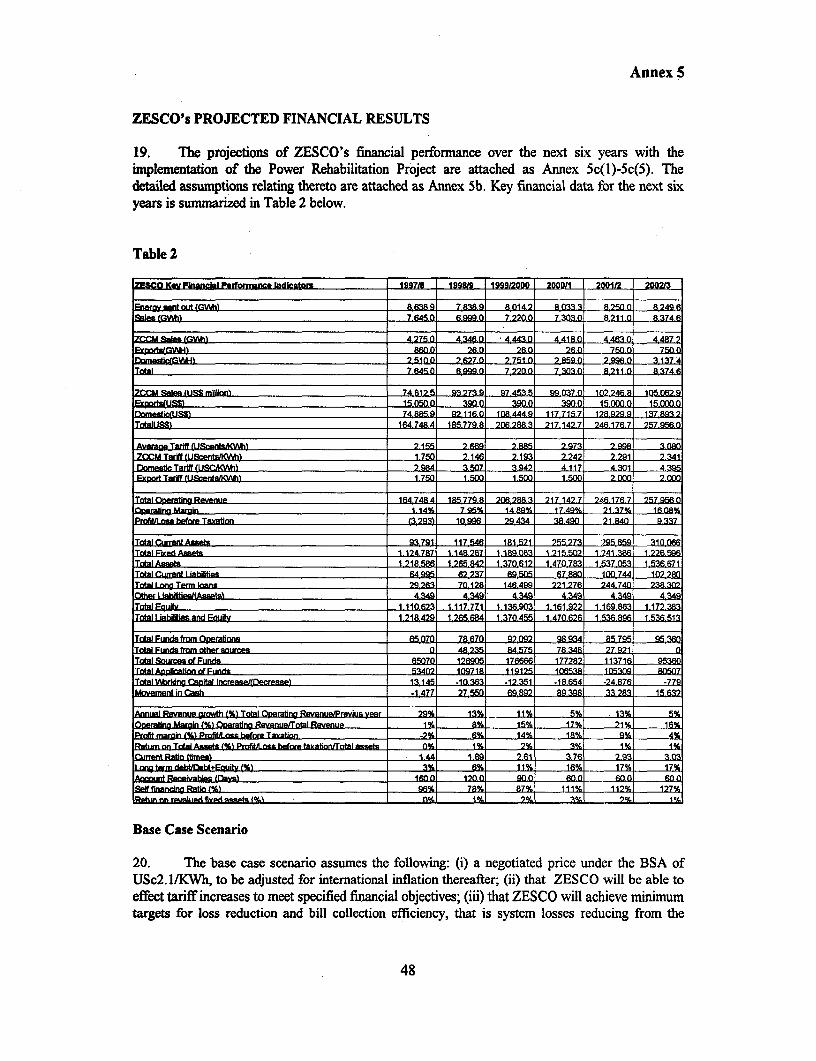

osur

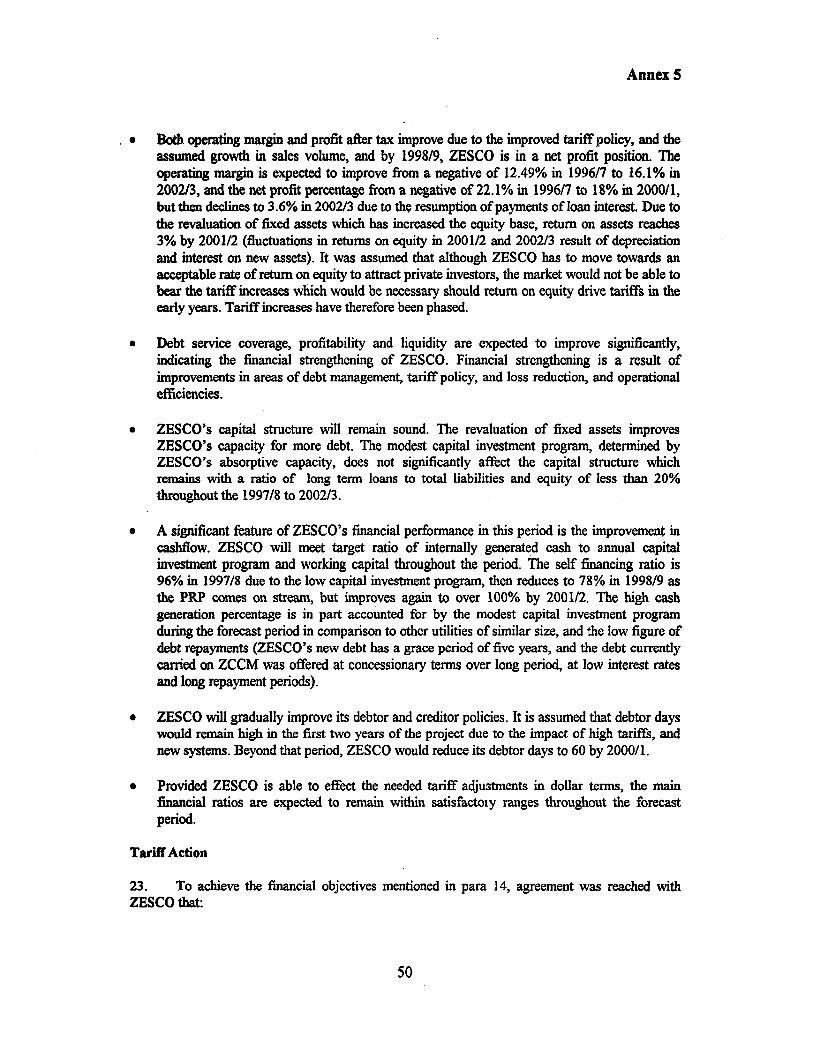

e A

utho

rized

Pub

lic D

iscl

osur

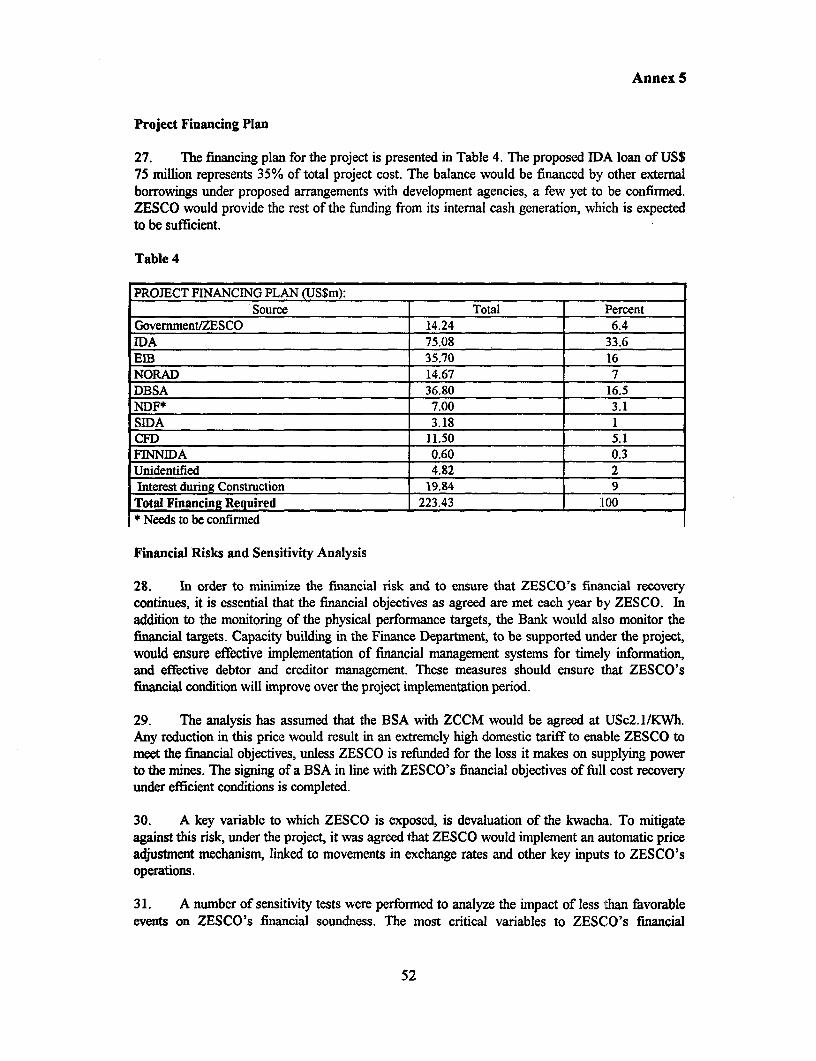

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

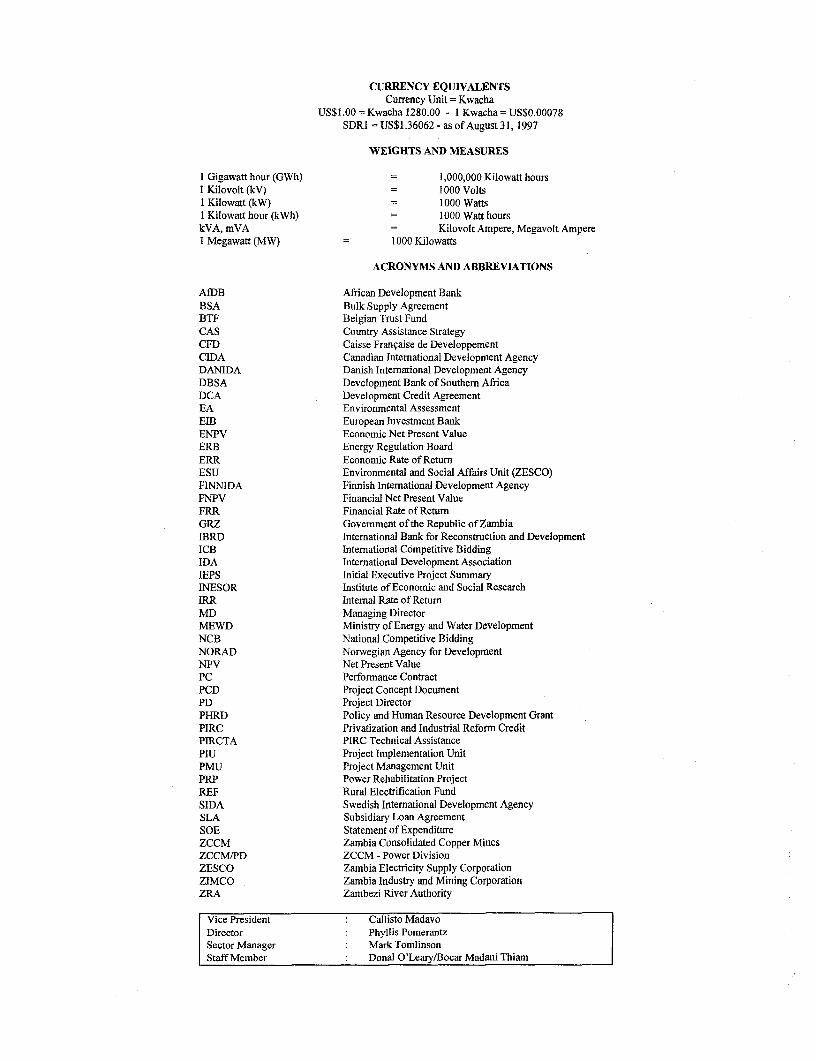

CURRENCY EQUIVALENTSCurrency Unit = Kwacha

US$1.00 = Kwacha 1280.00 - 1 Kwacha = US$0.00078SDRI = US$1.36062 - as of August 31, 1997

WEIGHTS AND MEASURES

I Gigawatt hour (GWh) 1,000,000 Kilowatt hoursI Kilovolt (kV) = 1000 VoltsI Kilowatt (kW) 1000 Watts1 Kilowatt hour (kWh) 1000 Watt hourskVA, mVA = Kilovolt Ampere, Megavolt AmpereI Megawatt (MW) = 1000 Kilowatts

ACRONYMS AND ABBREVIATIONS

AfDB African Development BankBSA Bulk Supply AgreementBTF Belgian Trust FundCAS Country Assistance StrategyCFD Caisse Fran,aise de DeveloppementCIDA Canadian Intemational Development AgencyDANIDA Danish International Development AgencyDBSA Development Bank of Southern AfricaDCA Development Credit AgreementEA Environmental AssessmentEIB European Investment BankENPV Economic Net Present ValueERB Energy Regulation BoardERR Economic Rate of ReturnESU Environmental and Social Affairs Unit (ZESCO)FINNIDA Finnish Intemational Development AgencyFNPV Financial Net Present ValueFRR Financial Rate of ReturnGRZ Government of the Republic of ZambiaIBRD International Bank for Reconstruction and DevelopmentICB International Competitive BiddingIDA International Development AssociationIEPS Initial Executive Project SummaryINESOR Institute of Economic and Social ResearchIRR Intemal Rate of ReturnMD Managing DirectorMEWD Ministry of Energy and Water DevelopmentNCB National Competitive BiddingNORAD Norwegian Agency for DevelopmentNPV Net Present ValuePC Performance ContractPCD Project Concept DocumentPD Project DirectorPHRD Policy and Human Resource Development GrantPIRC Privatization and Industrial Reform CreditPIRCTA PIRC Technical AssistancePIU Project Implementation UnitPMU Project Management UnitPRP Power Rehabilitation ProjectREF Rural Electrification FundSIDA Swedish International Development AgencySLA Subsidiary Loan AgreementSOE Statement of ExpenditureZCCM Zambia Consolidated Copper MinesZCCM/PD ZCCM - Power DivisionZESCO Zambia Electricity Supply CorporationZIMCO Zambia Industry and Mining CorporationZRA Zambezi River Authority

Vice President Callisto MadavoDirector Phyllis PomerantzSector Manager Mark TomlinsonStaff Member Donal O'Leary/Bocar Madani Thiam

ZAMBIAPOWER REHABILITATION

PROJECT APPRAISAL DOCUMENT

CONTENTS

Page No.

Project Fmancing Data ................................... 1

BLOCK 1:

Project Description1. Project Development Objetives .22. Project Components ................. 23. Benefits and Target Populaion .34. Institutional and Inplementation Arrangements ................................... 3

BLOCK 2:

Project Rationale5. CAS Objectives Supported by the Project .46. Main Sector Issues and Govemment Strateg .47. Sector issues to be Addressed by the Project and Strategic Choices .48. Project Altematives Considered and Reasons for Rejection .S9. Major Related Projects Finnced by the Bank and/or Other Development Agencies 510. Lessons Learned and Reflected in the Project Design .511. Indicaions of Borrow Commitment and Ownership .512. Value Added of Bank Support .6

BLOCK 3:

Summary Project Assessments13. Economic Assessent .614. Financial Assessment .815. Technical Assessment .1116. InstitutionalAssessment ................... 1117. Social Assessmet .1218. Environmental Assessment .1219. Participatory Approach .1320. Sustainability .1321. Critical Risks .1322. Possible Controversial Aspects .14

iv

BLOCK 4:

Main Loan Conditions23. Effectiveness Conditions ..................... 1424. Other ..................... 15

BLOCK 5:

Compliance with Bank Policies ................... 15

Annexes

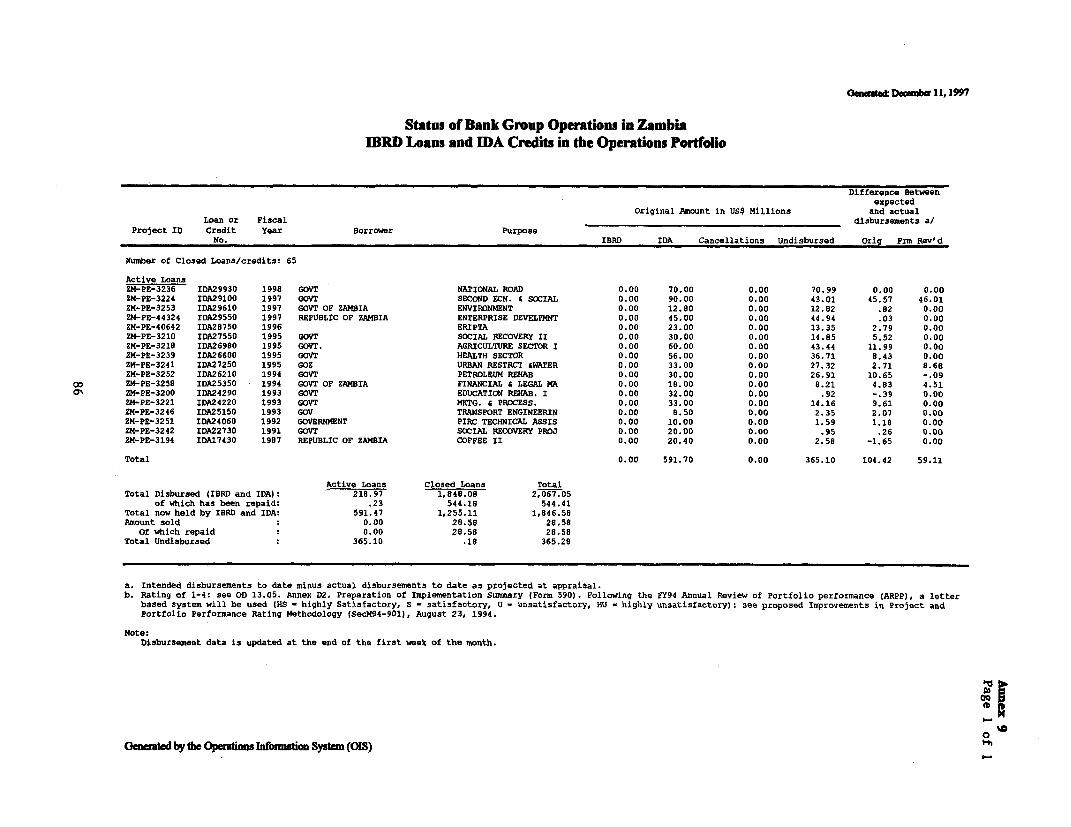

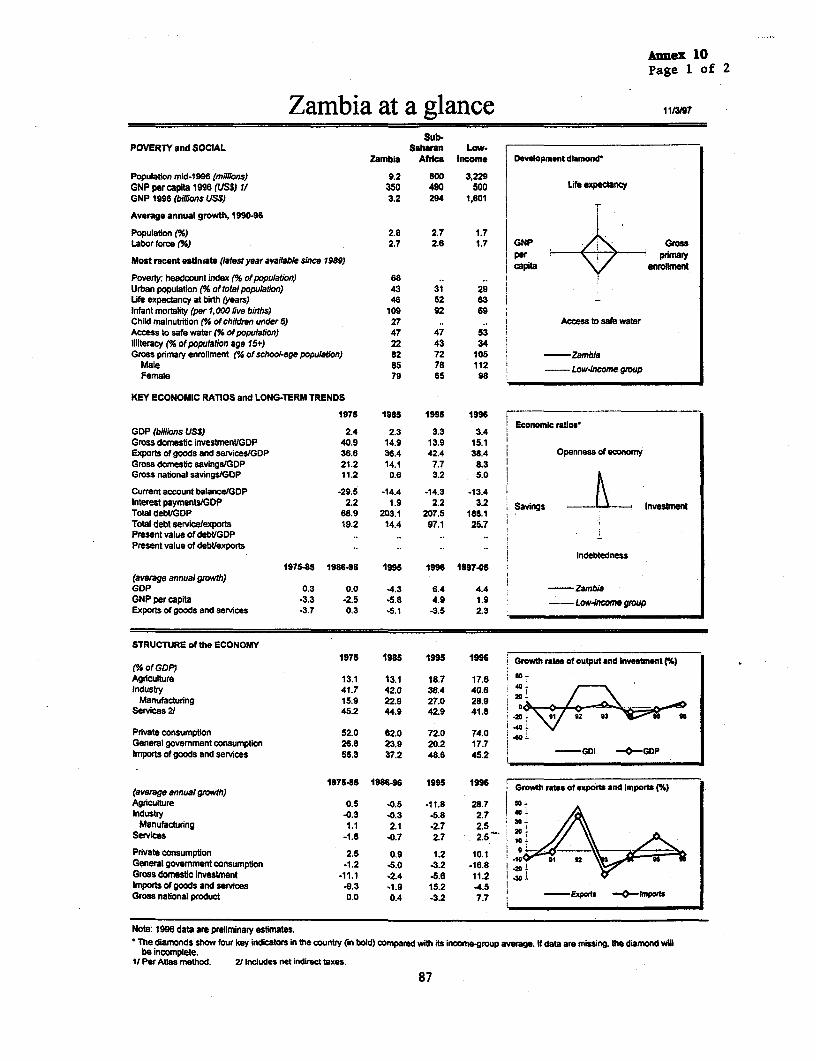

Annex 1: Project Design SummaryAnnex 2: Detailed Project DescriptionAnnex 3: Estimated Project CostAnnex 4: Economic AnalysisAnnex 5: Financial AnalysisAnnex 6: Procurement and Disbursement ArrangementsAnnex 7: Project Processing, Budget and ScheduleAnnex 8: Documents in the Project FileAnnex 9: Statement of Loans and CreditsAnnex 10: Zambia at a GlanceAnnex 11: Letter of Sector PolicyAnnex 12: Environmental and Social ConsiderationsAnnex 13: Dam Safety Aspects

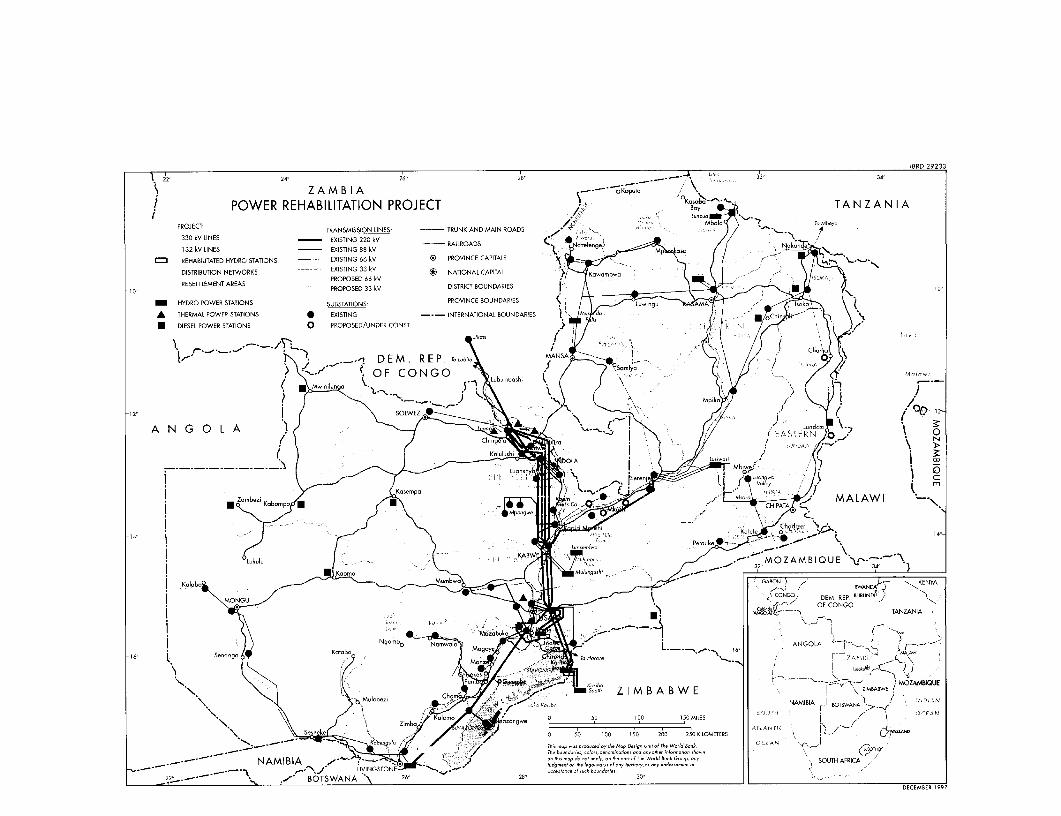

Map:

Zambia - IBRD No. 29233

v

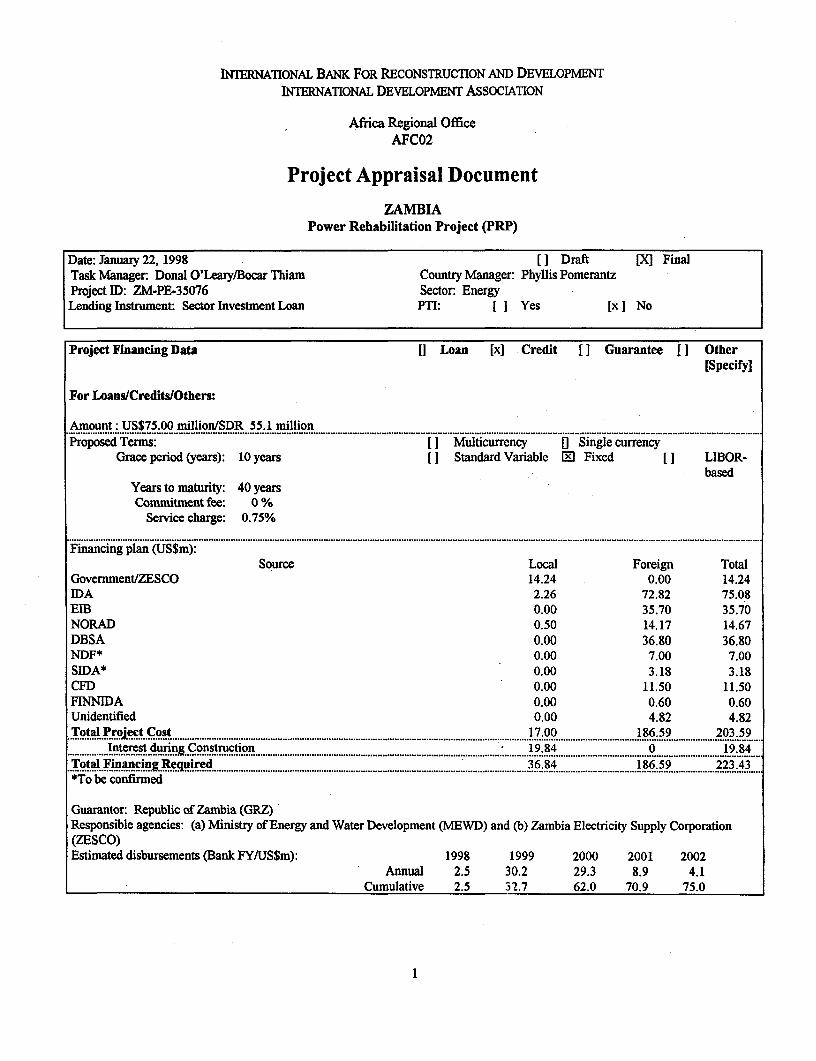

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENTINTERNAIONAL DEVELOPMENT ASSOCIATION

Africa Regional OfficeAFC02

Project Appraisal Document

ZAMBIAPower Rehabilitation Project (PRP)

Date: January 22, 1998 [ Draft [X1 FinalTask Manager: Donal O'Leary/Bocar Thiam Country Manager: Phyllis PomerantzProject ID: ZM-PE-35076 Sector: EnergyLending Instrument: Sector Investment Loan PTI: [ I Yes [x] No

Project Financing Data [I Loan [x] Credit [I Guarantee f I Other[Specify]

For Loans/Credits/Others:

Amount : US$75.00 million./SDR 55.1 million......................... ................................................. ........................................................................................................................................................Proposed Terms: [ ] Multicurrency [] Single currency

Grace period (years): 10 years [ Standard Variable 0M Fixed [] LIBOR-based

Years to maturity: 40 yearsCommitment fee: 0 %

Service charge: 0.75%........................................................................................................................................................................................................................................

Financing plan (US$m):Source Local Foreign Total

Government/ZESCO 14.24 0.00 14.24IDA 2.26 72.82 75.08EIB 0.00 35.70 35.70NORAD 0.50 14.17 14.67DBSA 0.00 36.80 36.80NDF* 0.00 7.00 7.00SIDA* 0.00 3.18 3.18CFD 0.00 11.50 11.50FINNIDA 0.00 0.60 0.60Unidentified 0.00 4.82 4.82Total Project Cost 17.00 186.59 203.59

................................. .......... ................. ........................................................................................................................... ........................................................................... I t r s u i ,C n tu to 9 8 9 8Interest duin Construction 19.84 0 19.84Total Financing Required 36.84 186.59 223.43~~~~~~~~~~~~~................................. ................................ .......................... ..... ............................

*To be confirmed

Guarantor: Republic of Zambia (GRZ)Responsible agencies: (a) Ministry of Energy and Water Development (MEWD) and (b) Zambia Electricity Supply Corporation(ZESCO)Estimated disbursements (Bank FY/US$m): 1998 1999 2000 2001 2002

Annual 2.5 30.2 29.3 8.9 4.1Cumulative 2.5 32.7 62.0 70.9 75.0

1

For Guarantees: 0 Partial Credit [ Partial risk

Proposed coverage:Project sponsor:Nature of udryn lacnTerms offnancing:

Principal amount (US$)Final maturity

Amortization profileFinancing available without guarantee?: l[l Yes [ ] NoIf yes, estimated cost or maturity:Estimated financing cost or maturty with guarantee:

Expected effectiveness date:4/15/1998 Closing date: 12/31/2002

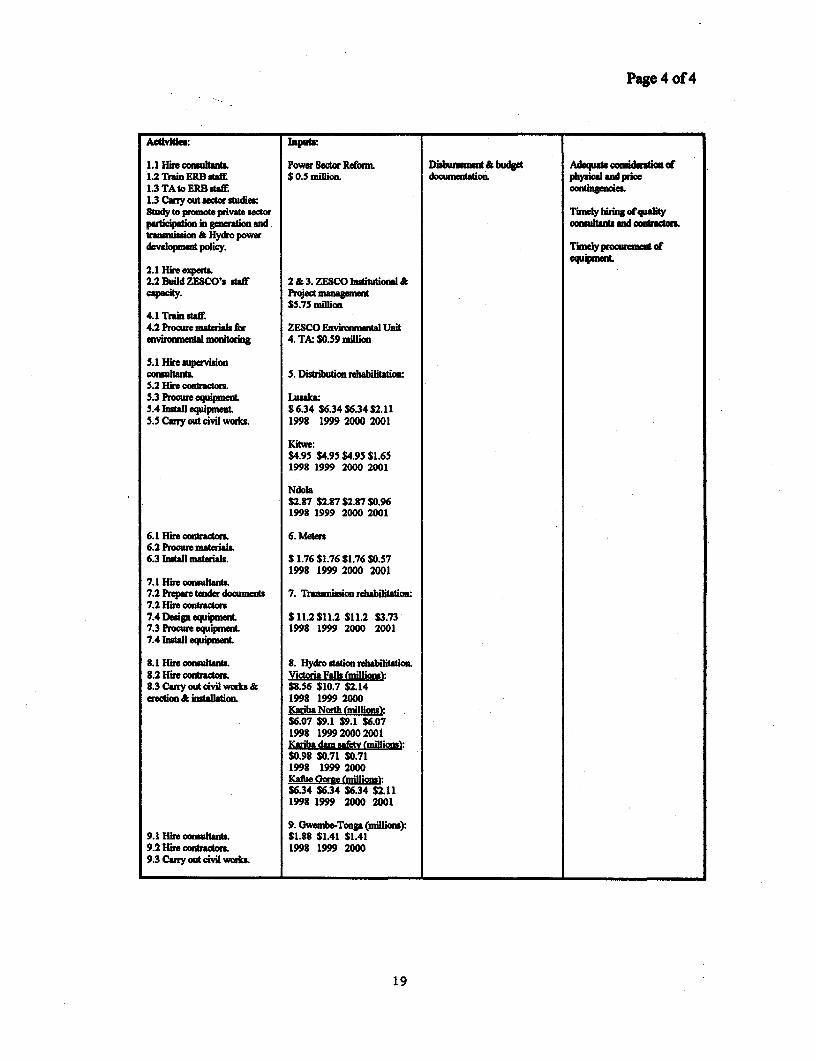

Block 1: Project Description1. Project development objectives (see Annex 1 for key performance indicators):The Project's overall objective is to support the Borrower's aim of enhancing the ability of Zambia's electricity supply industry toprovide electricity at least cost and in an efficient, sustainable manner to stimulate more and inclusive growth in the Zambianeconomy (see section 5). To assist GRZ in realizing this objective, the Project will support:(a) the Borrower's policy of establishing an institutional and regulatory framework conducive to sustainable efficiency and privateparticipation in the power sector,(b) improving the efficiency of ZESCO, the national electricity utility, through capacity-building measures and a commercializationplan based on corporate autonomy and management accountability which will enhance the Company's resource mobilization andinclude such actions as separating the accounting for generation, transmission and distribution;(c) improving technical efficiency and the quality and reliability of supply in ZESCO's physical system through rehabilitation of, andloss reduction in, the existing generation, transmission and distribution systems; and(d) implementing a Rehabilitation and Development Program for the Gwembe-Tonga, a group who were unsuccessfully resettledduring the construction of the Kariba Dam project.

2. Project components (see Annex 2 for a detailed description and Annex 3 for a detailed cost breakdown):

Component Categorv Cost Incl. Contingencies % of Total

(i) Hydropower Stations Rehabilitation(a) Kafue Gorge Physical 20.82 10.23(b) Victoria Falls Physical 23.36 11.47(c) Kariba North Physical 35.25 17.31(d) Kariba Dam Safety Physical 3.53 1.73

(ii) Distribution System Rehabilitation(a) Lusaka Physical 33.19 16.30(b) Copperbelt (Kitwe) Physical 14.50 7.12(c) Copperbelt (Ndola) Physical 10.68 5.25(d) Loss Reduction Physical 3.50 1.72

(iii) Transmission System Rehabilitation Physical 39.99 19.65

(iv) Gwemnbe-Tonga Rehabilitation and Socio-environmental 7.99 3.92Development Program Mitigation/Physical

(v) Environmental-Social Affairs Unit Institution Building 0.59 0.29Strengthening (ZESCO)

2

(vi) ZESCO Capacity Building and Project Institution Building 5.74 2.82Management

(vii) Support to implement Zambia Hydropower Sectoral Reform 2.40 1.18and Transmission Policies

(viii) PPF Refinancing Sectoral Reform/Institution 2.05 1.01Building/Consultancy

Total 203.59 100.003. Benefits and target population:The project benefits derive from: (a) Facilitating power sector reform aimed at putting the power sector on a least cost andfinancially sustainable path, to be achieved by support for: (i) setting tariffs on a cost-recovery basis, (ii) commercializing ZESCO,(iii) operationalizing the Energy Regulation Board (ERB), and (iv) attracting private sector financing for new generation andtransmission projects; (b) Improving the quality and reliability of supply of electricity, primarily for the industrial and commercialconsumers, which account for more than 80 percent of ZESCO's sales; and (c) support for the improvement of the socio-economic/environmental conditions of the Gwembe-Tonga who were displaced by the Kariba dam.

4. Institutional and implementation arrangements:Implementation period: S years

Executing agencies: MEWD and ZESCO

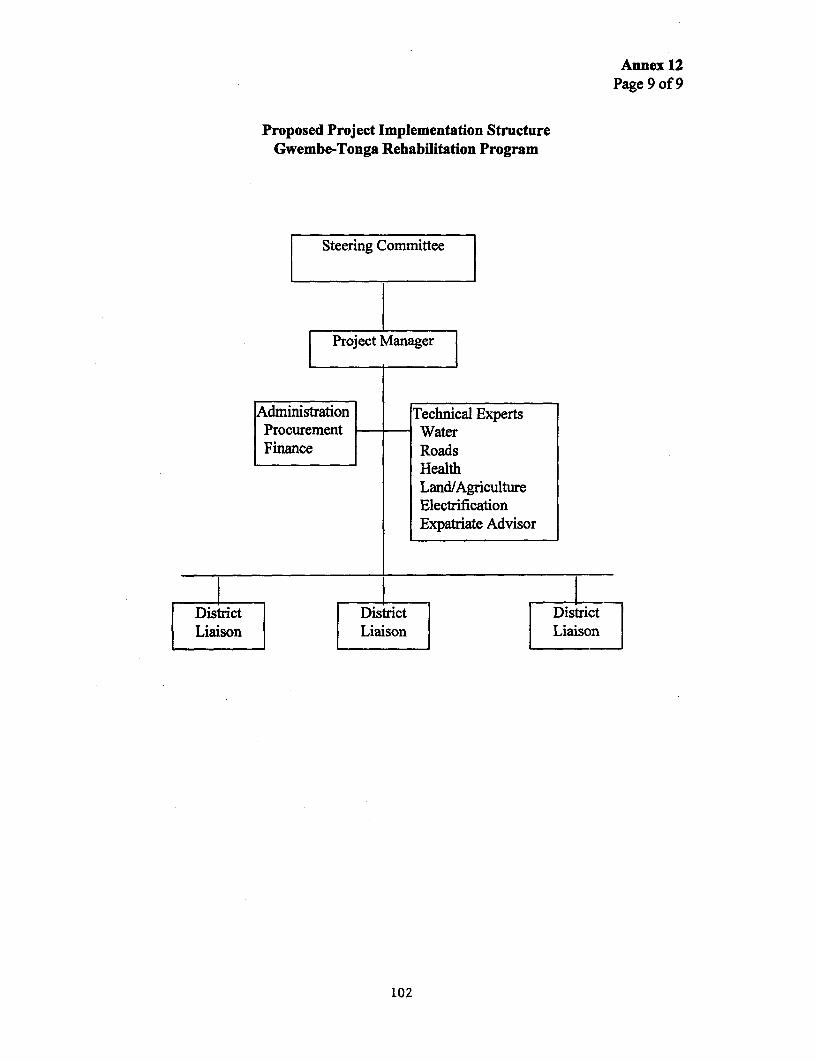

Project coordination: (a) ZESCO has created a project implementation management unit (PIU) headed by a Project Directorreporting directly to ZESCO's Managing Director. The Project Director will be assisted by project managers appointed to carry outgeneration rehabilitation, transmission system rehabilitation and distribution network rehabilitation works (See Section 16b). TheEnvironmental and Social Affairs Unit (ESU) of ZESCO will execute the environmental aspects of the project, except for theGwembe-Tonga Rehabilitation Development Program (see (b) below). A steering comunittee headed by the Managing Director willmaintain coordination with ZESCO management. The steering committee will also facilitate transferringvarious projectcomponents to the relevant ZESCO directorates after their completion.(b) For the Gwembe-Tonga Rehabilitation and Development Program, ZESCO will set up a Project Management Unit (PMU) in thefield, in Siavonga. The PMU will report to a steering committee chaired by the Permanent Secretary of the MEWD. To providecontinuity and transparency for the project, the Vice-Chairman of the Committee would be a distinguished Tonga (eminent person)from the Gwembe valley. In addition, the steering committee will include representatives of the other involved ministries (e.g.agriculture, health, transport), local government, and will have a strong representation from within the community. The PMUManager (from ZESCO) will be assisted by technical specialists, skilled in the areas of road construction, water resourcesdevelopment, land use, rural electrification and health services and an international advisor.(c) The Zambezi River Authority (ZRA) will coordinate the Kariba Dam Safety program.

Project oversight (policy guidance, etc.): The Government of the Republic of Zambia (GRZ), through its Ministry of Energy andWater Development (MEWD) as well as ZESCO's Board.

Accounting, financial reporting and auditing arrangements: ZESCO's accounts, including financial statements, special accountsand statements of expenditures will be audited by an independent auditor acceptable to IDA. For the Gwembe-Tonga Rehabilitationand Development component as well as the implementation of the Zambia Hydropower Development Policy (HPP) component,MEWD has been requested to open a project account. MEWD's project account, special account and statement of expenditures willbe audited by an independent auditor acceptable to the Bank.

Monitoring and evaluation arrangements:(a) AU physical components of the project will be undertaken by competent contractors under the supervision of qualifiedconsultants. All project components, (except the Gwembe-Tonga Rehabilitation and Development component) will be overseen by aZESCO Project Implementation Unit (PIM), headed by a Director, reporting directly to the Managing Director. The PIU will beassisted by an Advisor with international experience in project management. For the Gwembe-Tonga component, this will beoverseen by a ZESCO PMU, reporting directly to the Permanent Secretary of MEWD. The PMU will be assisted by an internationaladvisor, skilled in implementing rural development projects. In addition, the ESU will regularly monitor and report on all theenvironment aspects of the project; and(b) Regular IDA and other Donor missions at least every six months.

3

Block 2: Project Rationale5. CAS objective(s) supported by the project The Zambia CAS report 15761-ZA, dated June 25, 1996 was discussed by the

Board on July 18, 1996.The project supports the GRZ and CAS objective to promote private sector development and greater public sector efficiency tostimulate more and inclusive growth. The Power Rehabilitation Project is included in the lending program of the most recentlydiscussed CAS. The project supports the objective of fostering growth through the rehabilitation of the existing grid and therebyproviding reliable power for Zambia's development and particularly for the copper industry which accounts for some 80 percent ofZambia's export earnings. The Project also promotes private sector development through: (a) facilitating the operationalization ofthe Energy Regulation Board and (b) supporting the preparation of and promulgation by GRZ of a Hydropower Development andTransmission Policy to attract private sector financing of all new major generation and transmission projects. Finally, the projectsupports public sector efficiency through emphasizing the paramount importance of putting the power sector on a sound financialfooting including ZESCO's commercialization.

6. Main sector issues and Government Strategy:Main Sector Issues:.The main issues in Zambia's power sector relate to its efficiency, commercialization, financing and coverage.Efficiency performance is mixed, with transmission performance being good and performance on generation and distribution beinglow, due to low generator availability and high distribution losses respectively.Commercial performance has been extremely poor. ZESCO's rate-of-return (ROR) on revalued assets was unsatisfactory over thelast five years for which audited accounts were available; in three of these years the ROR was negative. ZESCO was unable to settleits debts satisfactorily due to very low tariffs for both the mining and non-mining sectors, poor cost controls and high debt volume.In addition, there is evidence of overstaffing in ZESCO.Financing of new investments in the power sector has been difficult because of ZESCO's very weak financial position and because ofthe many other priorities on the Government's budget.Coverage is low and varies markedly by province. According to the 1990 census, around 14 percent of households use electricity forlighting. ZESCO added about 20,000 consumers during the period 1990/91-1994/95.

Government Strategy:GRZ's strategy for realizing its goal of optimal development of Zambia's electricity supply industry is to establish an institutionaland regulatory environment to enable private sector participation. In the short-term, the aim is to improve sector performance bycommercializing ZESCO in order to enhance resource mobilization. The instruments of the strategy include GRZ's promulgation ofits National Energy Policy (1994), a new Electricity Act which permits private investment (1995) and the Energy Regulation Act(1995) under which an Energy Regulation Board (ERB) was established in 1997. In 1996, the GRZ signed a Performance Contractwith ZESCO which emphasized commercial operation and efficient technical supply. The Performance Contract has proved to be auseful tool for setting and monitoring performance targets in Zambia's power sector. In relation to increasing electricity coverage,GRZ created a Rural Electrification Fund (REF) through a 10 percent levy on electricity sales. Guidelines on the selection of ruralelectrification projects for financing by this Fund were promulgated in January 1995.

To develop a sector restructuring plan, the GRZ, under the preparation of this Project, sponsored a study (undertaken by LondonEconomics) to advise on the restructuring of the Zambian power sector and submit an action plan for consideration. In addition,with assistance provided under preparation of this project, GRZ initiated the formulation of a Hydropower Development andTransmission Policy aimed towards inducing private sector development of major hydroelectric and transmission projects.

7. Sector issues to be addressed by the project and strategic choices:Sector IssuesThe principal sector issues addressed by the project include efficiency; commercialization; and financing.(a) The Project will support regulatory and institutional reform through the following activities:

(i) Support the efficient operation of the ERB and assist in its capacity building; and(ii) Support the preparation and promulgation of a Hydropower Development and Transmission Policy to promote the private

sector,(1) The Project will support the commercialization of ZESCO through supporting:

(iii) Sound tariff policy, including adequate sales arrangements with the mining sector,(iv) Separation of accounts for the generation, transmission and distribution functions; and(v) Capacity building in ZESCO; and

(c) The Project will support the least-cost development of the power sector, through focusing on efficiency improvements, lossreduction, and the rehabilitation of ZESCO's generation, transmission and distribution systems.Strategic ChoicesSection 8 below discusses the key strategic choices made in addressing sectoral issues under the proposed Project.

4

8. Project alternatives considered and reasons for rejection:Alternatives were evaluated for the sectoral reform and restructuring components; for the physical components of the proposedProject (economic analysis); and the possible inclusion of a rural electrification (RE) component.

(a) The issue of private vs. public participation in the proposed Project was considered in the preparation of the sector restructuringcomponent and was addressed by the London Economics Study "Re-structuring Zambia's Power Sector." The finding was thatprivate sector participation will develop once the sector is profitable and it is clear how the sector will be regulated. Therefore,Project actions in this regard will aim at strengthening sector operations and developing an enabling regulatory framework forprivate participation (see Section 7a). In the medium-term, the distribution sub-sector may provide an entry for the private sectorthrough a competitively-bid operations contract.

(b) Economic Evaluation of Alternatives. The economic analysis verifies that the Project meets the aimed objectives better than thealternatives (alternative expansion plans, different technical specifications, scales and timing). See Section 13 and Annex 4.

(c) Rural electrification. The Project does not include a rural electrification component because the GRZ is raising funds for ruralelectrification through its REF (section 6). However, there are some problems with the management of these funds, particularly thecollection and release of funds to ZESCO so that the company can efficiently implement the Rural Electrification program. GRZ hasagreed to prepare an action plan to speed up the collections and release of Rual Electrification funds and ensure efficientmanagement of the Fund.

(d) The project team also considered including a demand-side management component in the project. However, it was decided notto include this component (except for limited training/TA for some exceptional cases) because of the poor prospects for success,given the financial state of many of the potential industry beneficiaries and their imminent transition to private ownership.

9. Major related projects financed by the Bank and/or other dcv elopment agencies (completed, ongoing and planned):The Bank has a long-standing relationship with the Government going back to pre-independence times. Altogether, the Bank hashad 10 operations (loanstcredits) in the energy sector of which five were in the power sector, four in the petroleum sector and one inthe coal mining sector. Over the last twelve years, the Bank approved only one operation in the energy sector: the Petroleum SectorRehabilitation Project (Credit No. 2621). Two years elapsed between Board Presentation and effectiveness of this project. This waspartly due to the fact that it took a long time to sign a contract with a consortium of international oil marketing companies tomanage the oil products terminal in Ndola. No power operation has been prepared for more than twenty years. Under the twoPrivatization and Industrial Reform Credits (PIRCs), (Credit Nos. 2405 and 2523) and the PIRCTA Credit, IDA has supported theinitiation of power sector reform including the dissolution of Zambia Industry and Mining Corporation (ZIMCO); the preparation ofa Performance Contract between the GRZ and ZESCO, that sets out agreed expectations and obligations relating to the performanceof Zambia's power sector; and a detailed training program for, inter alia, stakeholders on issues relating to the institutionalization ofthe Energy Regulation Board.

Several donors including AfDB, CIDA, DANIDA, EIB, FINNIDA, NORAD, SIDA, and the Governmuent of Ireland have providedor are providing financial project support to ZESCO and MEWD.

10. Lessons learned and reflected in the project design: The major lesson learned from the projects in section 9 is the need toaddress sectoral, regulatory, tariff, institutional as well as project policies/issues prior to project approval. (See the Conditions ofEffectiveness set out in Section 23.) The key issue in implementing the physical components relates to the need to minimize start-updelays. Project design addresses this by initiating procurement as early as possible in project preparation. Accordingly, submittal ofdraft bidding documents for all the major project components (except for the rehabilitation of the Victoria Falls Power Station) wasmade a condition of Negotiations.

11. Indications of borrower commitment and ownership:This project has been prepared at the specific request of the Government. Specific actions demonstrate GRZJZESCO commitment tothe project and its objectives. First, though project preparation costs were substantial - reaching approximately US$7 million (SeeAnnex 7 for more detail) -- GRZtZESCO picked up a considerable amount of these costs (estimated at US$1.5 million) when somedonors found it difficult to support project preparation because of concerns about governance issues. Second, ZESCO increasedtariffs by approximately 5 percent, in USS terms, for sales to Zambia Consolidated Copper Mines' Power Division (ZCCM/PD)(effective 1/1/1997) and by approximately 30 percent for all other consumers in Zambia (effective 2/1/1997). ZESCO implemented asecond substantial tariff increase of approximately 40 percent for all consumers (except ZCCM) in Zambia on 7/1/1997 and anotherincrease will become effective from January 1998. As of 12/1/97, ZESCO has implemented a tariff increase of approximately 50percent in US$ terms for sales to the new owners of ZCCM/PD.

5

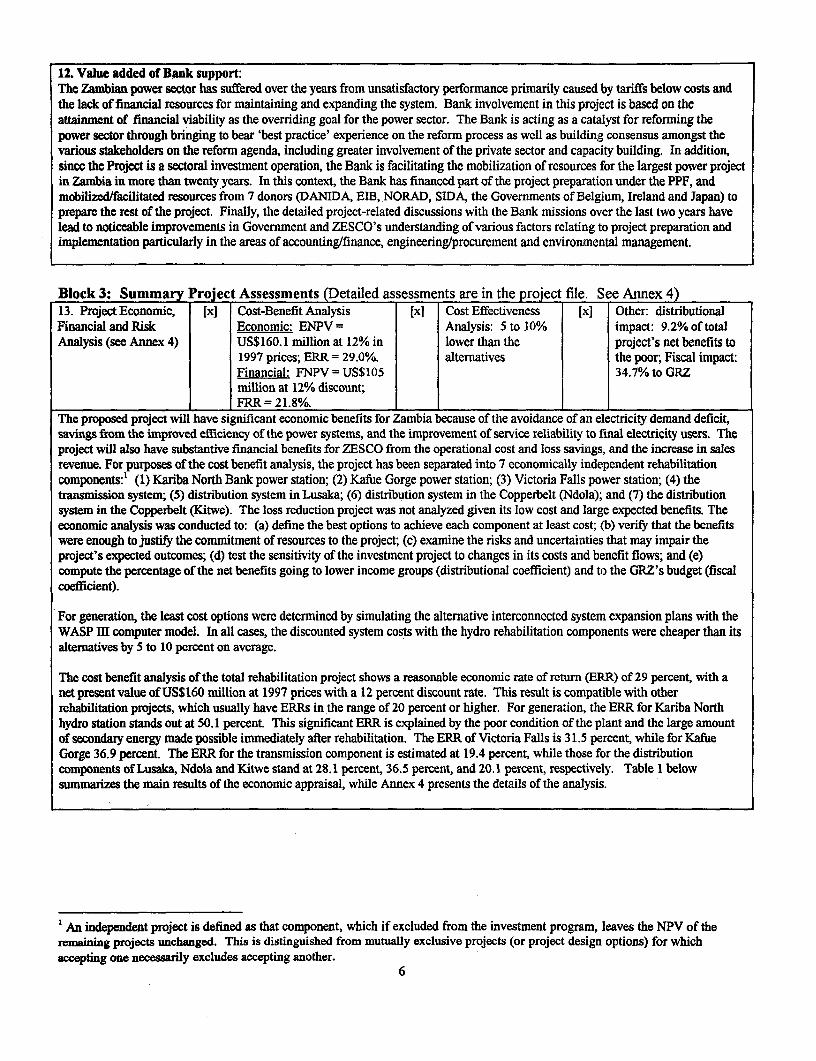

12. Value added of Bank support:The Zambian power sector has suffered over the years from unsatisfactory performance primarily caused by tariffs below costs andthe lack of financial resources for maintaining and expanding the system. Bank involvement in this project is based on theattainment of financial viability as the overriding goal for the power sector. The Bank is acting as a catalyst for reforming thepower sector through bringing to bear 'best practice' experience on the reform process as well as building consensus amongst thevarious stakeholders on the reform agenda, including greater involvement of the private sector and capacity building. In addition,since the Project is a sectoral investment operation, the Bank is facilitating the mobilization of resources for the largest power projectin Zambia in more than twenty years. In this context, the Bank has financed part of the project preparation under the PPF, andmobilized/facilitated resources from 7 donors (DANIDA, EIEB, NORAD, SIDA, the Governments of Belgium, Ireland and Japan) toprepare the rest of the project. Finally, the detailed project-related discussions with the Bank missions over the last two years havelead to noticeable improvements in Govermnent and ZESCO's understanding of various factors relating to project preparation andimplementation particularly in the areas of accounting/finance, engineering/procurement and environmental management.

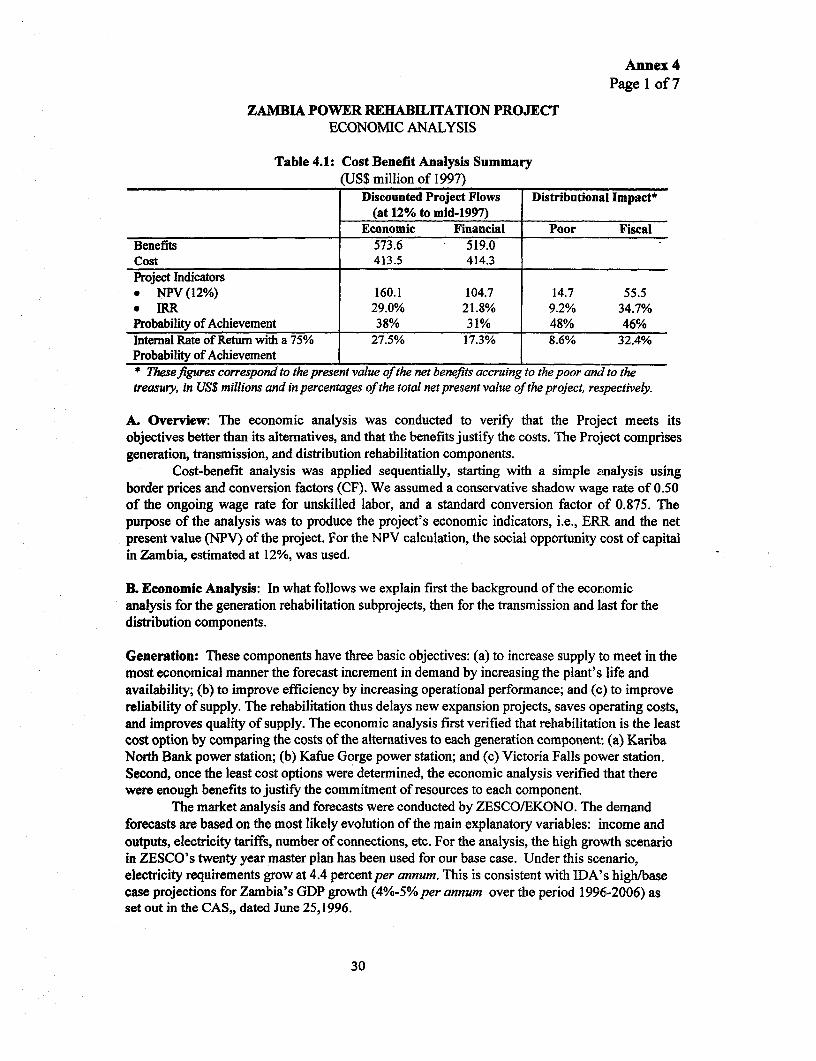

Block 3: Summary Project Assessments (Detailed assessments are in the project file. See Annex 4)13. Project Economic, [xl Cost-Benefit Analysis [xl Cost Effectiveness [x] Other: distributionalFinancial and Risk Economic: ENPV = Analysis: 5 to 10% impact: 9.2% of totalAnalysis (see Annex 4) US$160.1 million at 12% in lower than the project's net benefits to

1997 prices; ERR = 29.0%. alternatives the poor; Fiscal impact:Financial: FNPV = US$105 34.7% to GRZmillion at 12% discount;FRR = 21.8%. _

The proposed project will have significant economic benefits for Zambia because of the avoidance of an electricity demand deficit,savings from the improved efficiency of the power systems, and the improvement of service reliability to final electricity users. Theproject will also have substantive financial benefits for ZESCO from the operational cost and loss savings, and the increase in salesrevenue. For purposes of the cost benefit analysis, the project has been separated into 7 economically independent rehabilitationcomponents:' (1) Kariba North Bank power station; (2) Kafue Gorge power station; (3) Victoria Falls power station; (4) thetransmission system; (5) distribution system in Lusaka; (6) distribution system in the Copperbelt (Ndola); and (7) the distributionsystem in the Copperbelt (Kitwe). The loss reduction project was not analyzed given its low cost and large expected benefits. Theeconomic analysis was conducted to: (a) define the best options to achieve each component at least cost; (b) verify that the benefitswere enough to justify the commitment of resources to the project; (c) examine the risks and uncertainties that may impair theproject's expected outcomes; (d) test the sensitivity of the investment project to changes in its costs and benefit flows; and (e)compute the percentage of the net benefits going to lower income groups (distributional coefficient) and to the GRZ's budget (fiscalcoefficient).

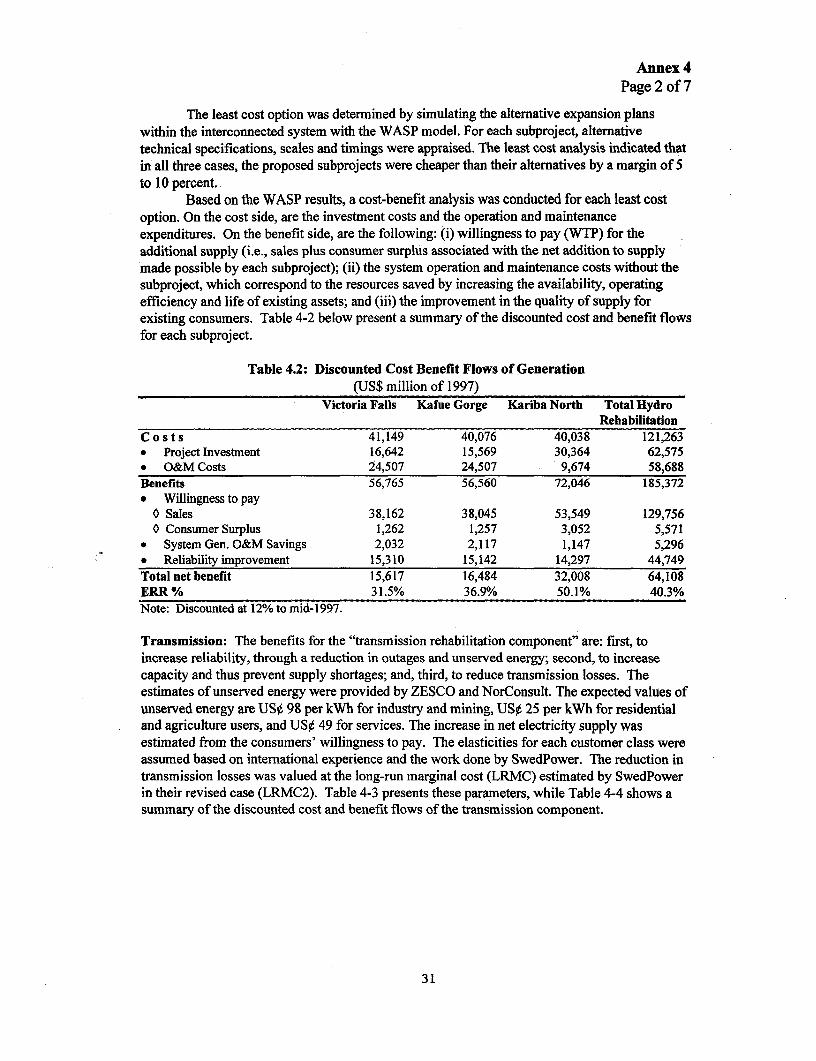

For generation, the least cost options were determined by simulating the alternative interconnected system expansion plans with theWASP IH computer model. In all cases, the discounted system costs with the hydro rehabilitation components were cheaper than itsalternatives by 5 to 10 percent on average.

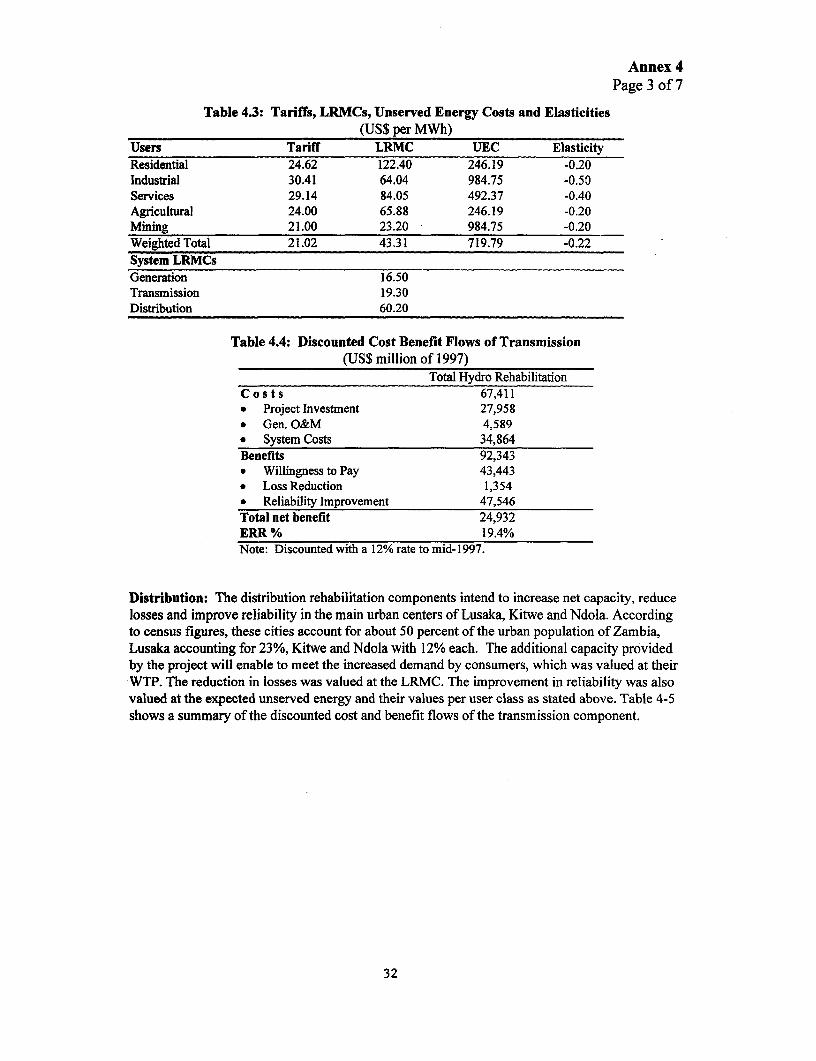

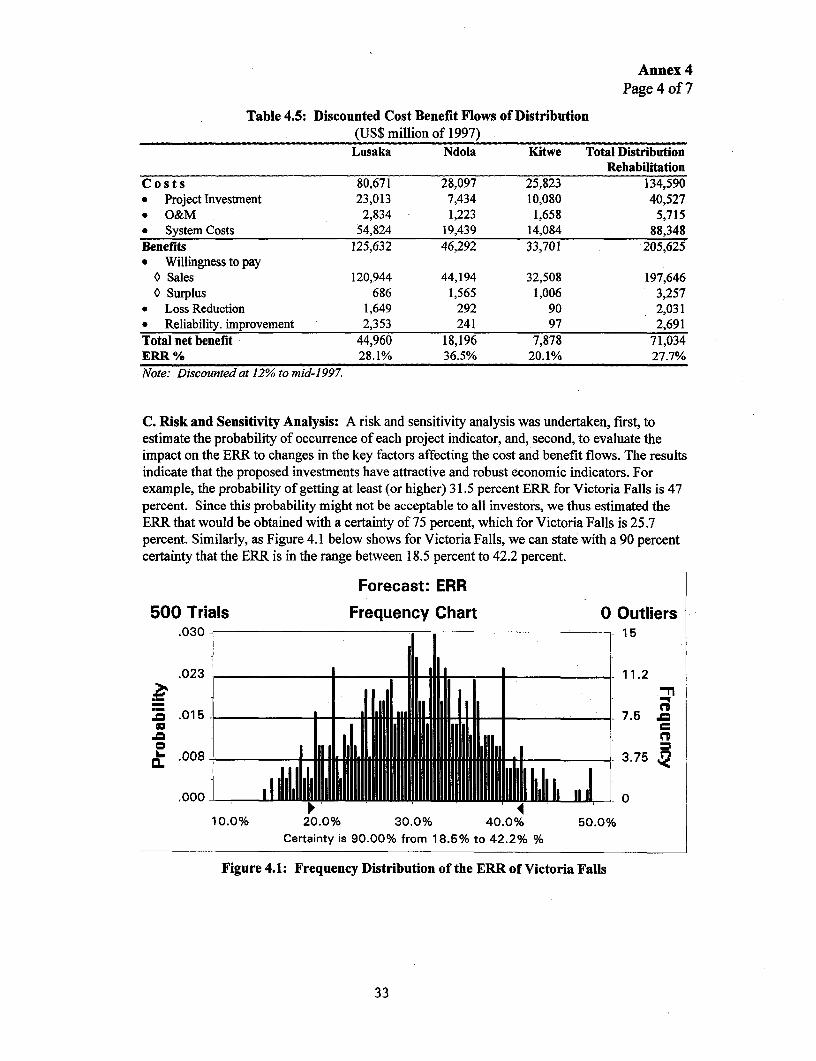

The cost benefit analysis of the total rehabilitation project shows a reasonable economic rate of return (ERR) of 29 percent, with anet present value of USS160 million at 1997 prices with a 12 percent discount rate. This result is compatible with otherrehabilitation projects, which usually have ERRs in the range of 20 percent or higher. For generation, the ERR for Kariba Northhydro station stands out at 50.1 percent. This significant ERR is explained by the poor condition of the plant and the large amountof secondary energy made possible immediately after rehabilitation. The ERR of Victoria Falls is 31.5 percent, while for KafueGorge 36.9 percent. The ERR for the transmission component is estimated at 19.4 percent, while those for the distributioncomponents of Lusaka, Ndola and Kitwe stand at 28.1 percent, 36.5 percent, and 20.1 percent, respectively. Table 1 belowsummarizes the main results of the economic appraisal, while Annex 4 presents the details of the analysis.

'An independent project is defined as that component, which if excluded from the investment program, leaves the NPV of theremaining projects unchanged. This is distinguished from mutually exclusive projects (or project design options) for whichaccepting one necessarily excludes accepting another.

6

Table 1Summary Results of the Economic, Financial and Risk Analysis

Economic FinancialComponent ENPV ERR Probability ERR with FNPV FRR Probability FRR with

IUSS 000 of a 75% US$ 000 of a 75%achievement certainty achievement certainty

GenerationVictoria Falls 15,617 31.5% 47% 25.7% 942 13.0% 33% 10.6%Kafue Gorge 16,484 36.9% 49% 30.6% 1,925 14.3% 48% 12.5%KaribaNorth 32,008 50.1% 50% 44.8% 15,957 29.3% 48% 25.9%

Transmission 24,932 19.4% 54% 16.5% 22,191 18.3% 50% 15.1%Distribution* Lusaka 44,960 28.1% 27% 21.1% 41,409 26.6% 28% 20.2%* Ndola 18,196 36.5% 13% 21.2% 16,009 33.2% 8% 18.2%

Kitwe 7,878 20.1% 190/% 12.9% 6,278 18.4% 16% 11.6%Total Project 160,075 29.0% 38% 27.5% 104,712 21.8% 31% 17.3%

Net present values discounted to 1998 with a 12 percent discount rate.

Risk and Sensitivity Analysis: Projects in Zambia face a considerable degree of risk. Several of the risks are associated with themacroeconomic and political uncertainties facing all developing countries. Others, however, are specific to the nature of thecomponents, including the uncertainties related to the effects of the proposed components on the existing generation, transmissionand distribution systems. A risk analysis was performed to estimate the probability associated with each component outcome. AsTable 1 above indicates, the proposed components are robust and have a small likelihood of being uneconomic. The results suggestthat the probability of achieving the overall project ERR of 29 percent is at least 38 percent. If this probability of achievement isconsidered too low, the analysis estimated the ERR of 27.5 percent with a certainty of 75 percent. The assumptions, rationale andresults of the risk analysis for each component are described in more detail in Annex 4.

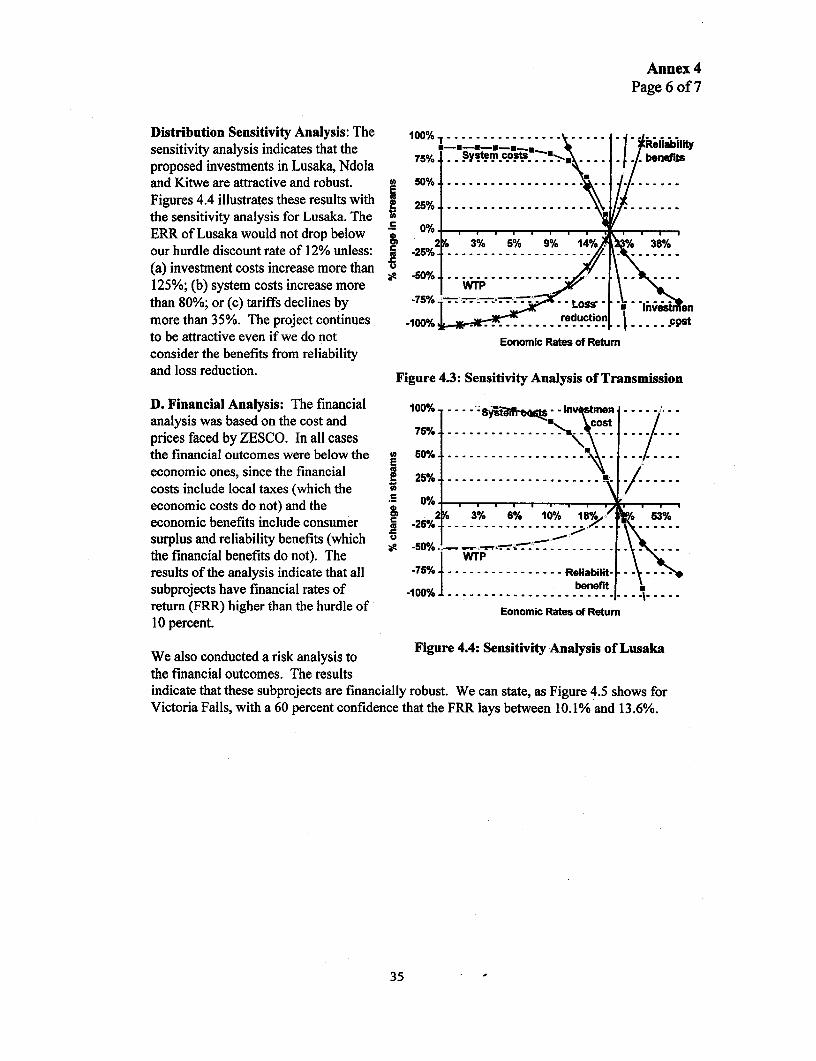

A sensitivity analysis was undertaken to test the robustness of the ERRs of each project component to changes in key cost and benefitvariables which are subject to risk and uncertainty. The results also confirm that the proposed investments have attractive and robusteconomic indicators, as only with very large increases in costs or substantial decreases in benefits, would the ERRs fall below theopportunity cost of capital of about 12 percent. For instance, the investment costs for the Victoria Falls component would have toincrease by more than 40 percent, for its ERR to drop below 12 percent. Tariffs are the single most important variable affecting theeconomics of the project. If tariffs decline more than 25 percent in real terms, the ERRs of several components would suffer.Therefore, it is critical that the agreed tariff implementation schedule is maintained with as little deviation as possible. A summaryof the changes in the cost and benefit streams of each component that would be required for the ERRs to fall below the 12 percentbenchmark rate is presented in Annex 4.

Table 2Summary Results of the Sensitivity Analysis:

Percentage (%)l Increases in Costs or Reduction in Benefits for a 12 Percent ERRComnponent Project Investment & Systemn WTP Resource Savings Reliability

Op. Costs Costs Improvement

GenerationVictoria Falls 38 59 -40 -55 -102Kafue Gorge 41 63 -42 -58 -109Kariba North 80 85 -57 -83 -85

Transmission 77 72 -56 -1841 -52Distribution

Lusaka 127 82 -37 -2727 -1911Ndola 210 94 -40 -6234 -7544K.itwe 67 56 -24 -8727 8164

7

Financial Analysis: The financial analysis of the components also shows that they have financial rates of return (FRR) higherthan the benchmark 10 percent financial rate. The overall FRR of the project is 21.8 percent, with a net present value of US$105million. The FRRs in generation are: Kariba North hydro station, 29.3 percent; Victoria Falls, 13 percent; and Kafue Gorge, 14.3percent. The FRR for the transmission component is 15.1 percent. The FRRs for the distribution components for Lusaka, Ndolaand Kitwe are 26.6 percent, 33.2 percent, and 18.4 percent, respectively.

The risk analysis of the financial outcomes also confirms that the components profiles are robust against the risks that may affecttheir implementation and operation. As Table 1 above shows, with a 75 percent certainty, all the FRRs of the project componentsare higher than the 10 percent financial benchmark rate. Annex 4 provides the results for the other components.

Distribution Analysis: The distribution analysis of the project flows shows that the income and fiscal distributional impacts of theoverall project are positive. The distribution coefficient of the project (net benefits to unskilled labor and poor residential users as aproportion of the project's net benefits) amounts to 9 percent, while the fiscal coefficient (net fiscal revenue as a proportion ofproject's total net benefits) is 35 percent. The risk analysis suggests that with a 75 percent certainty, the likely distributioncoefficients would decline to 7 percent and 26 percent, respectively.

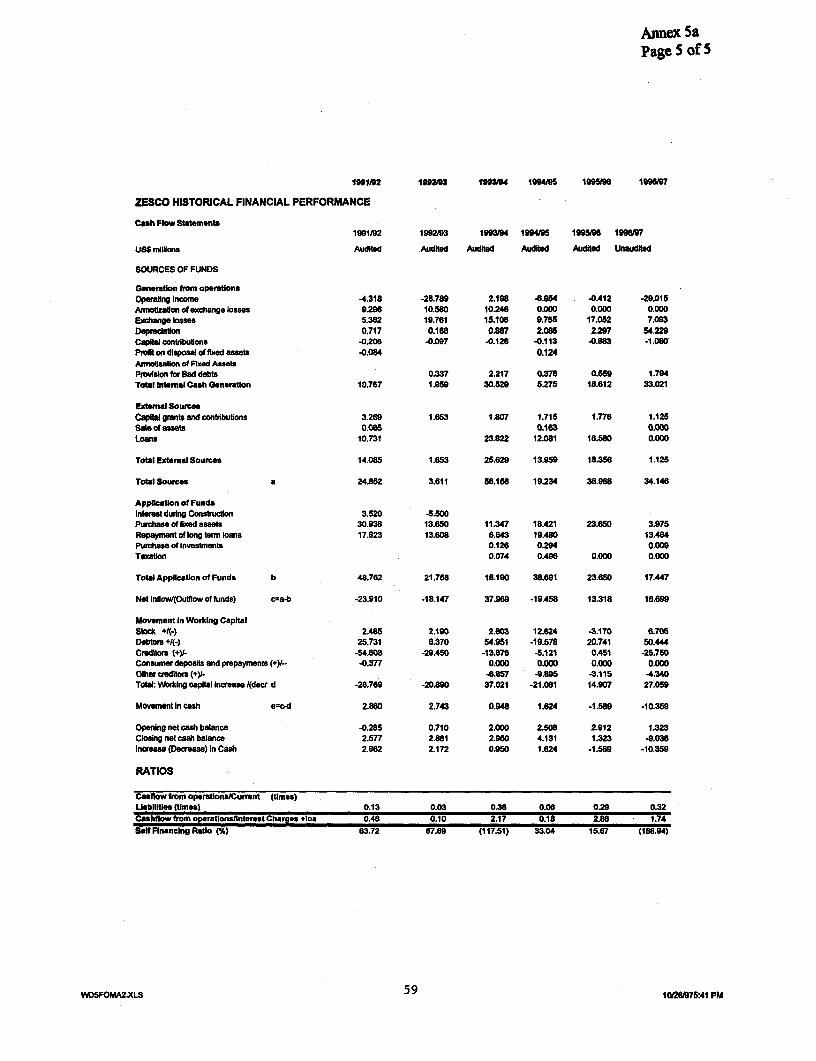

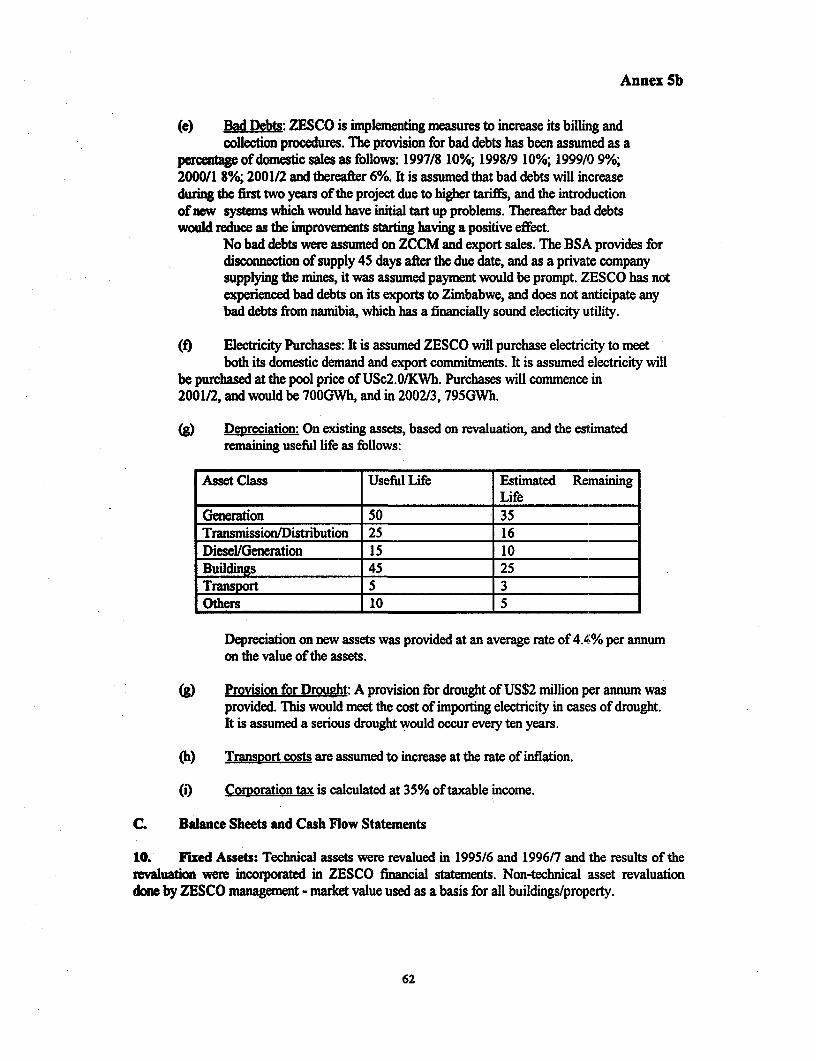

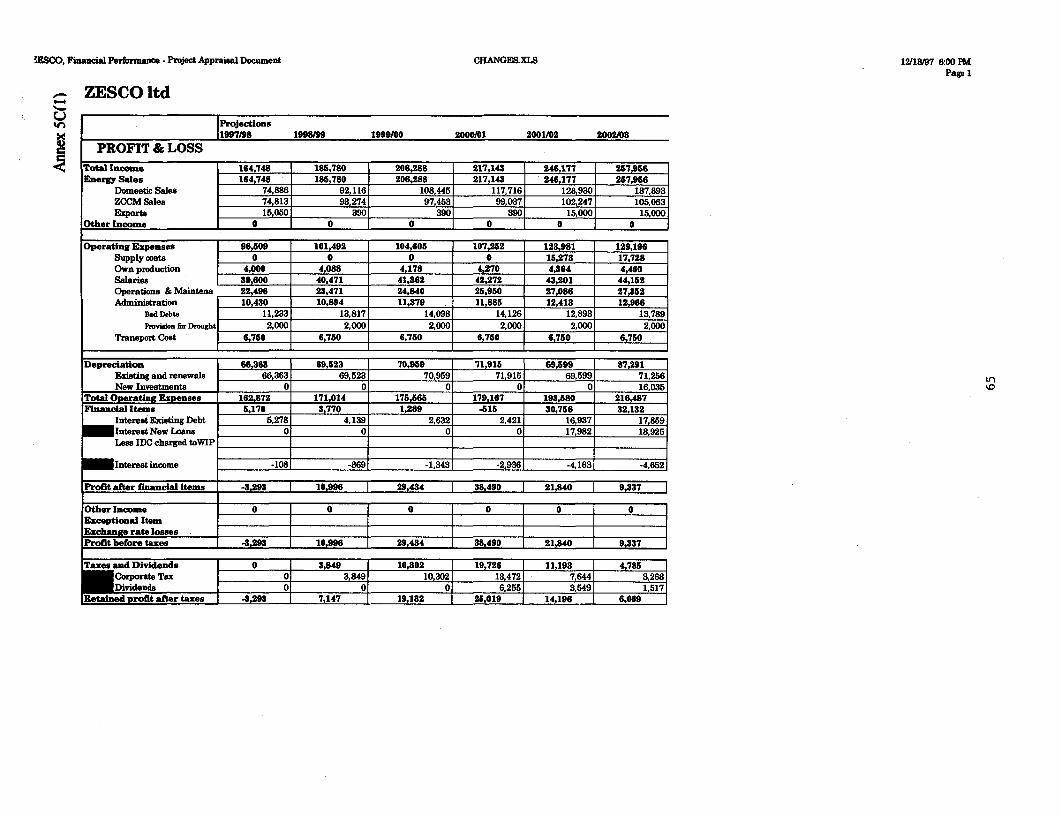

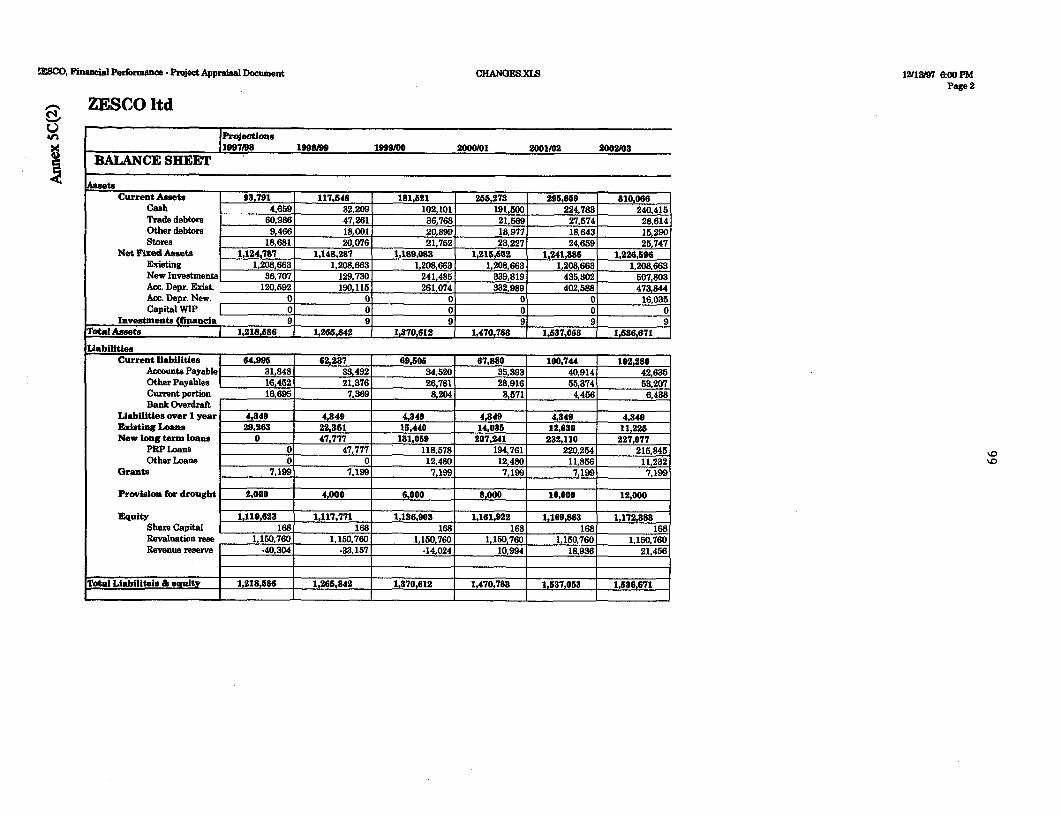

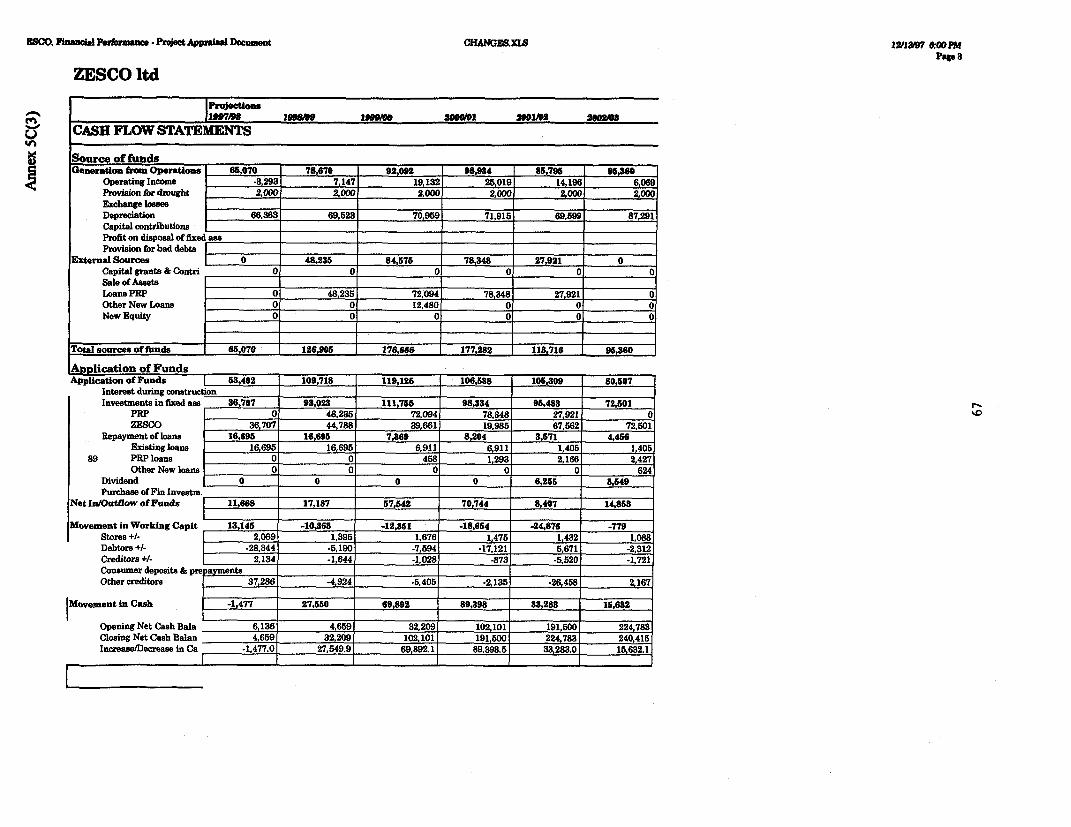

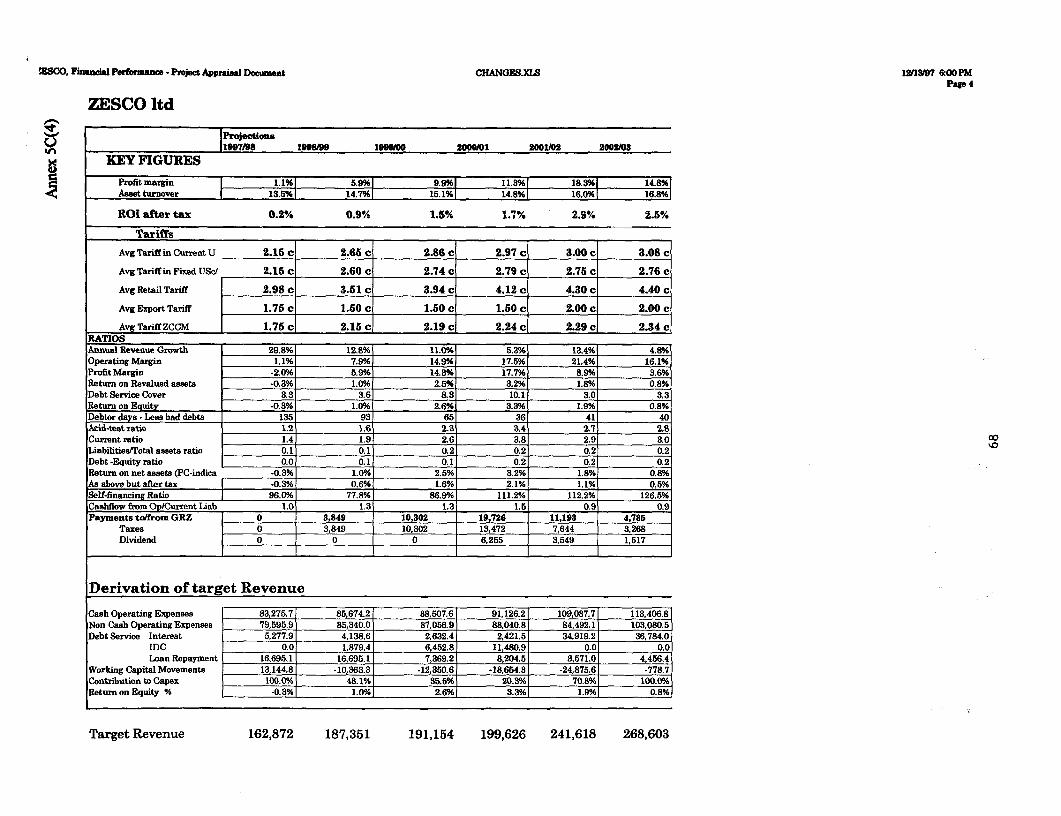

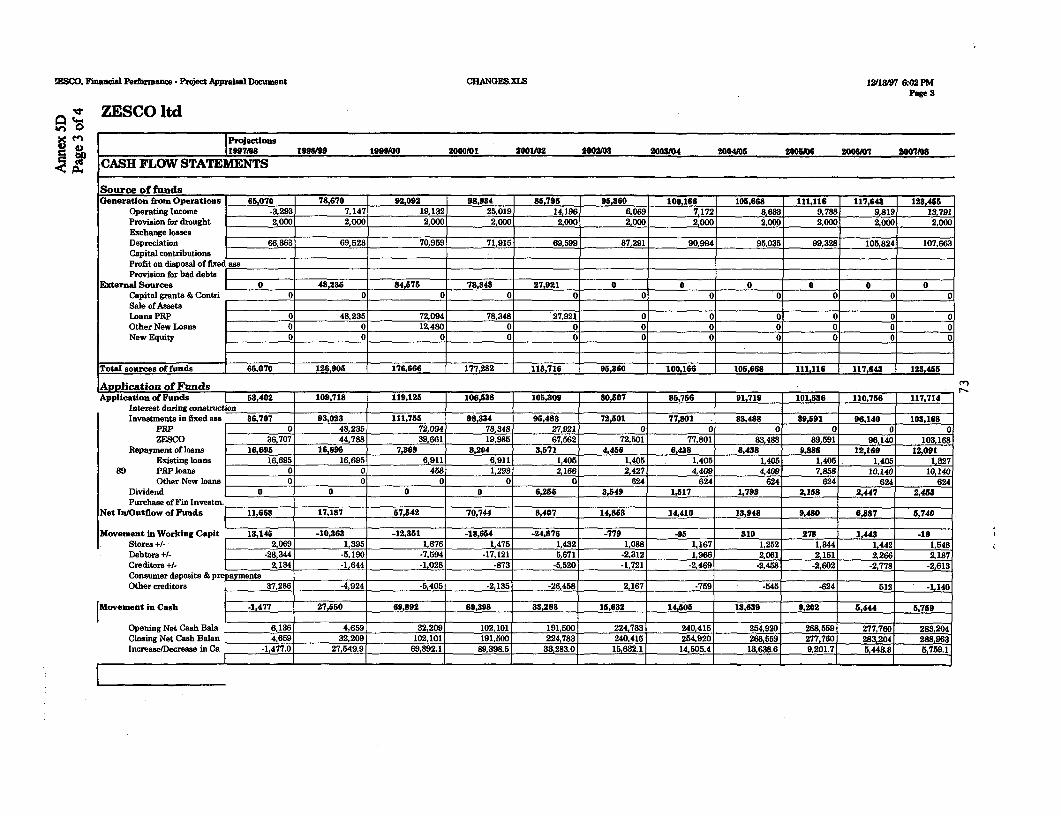

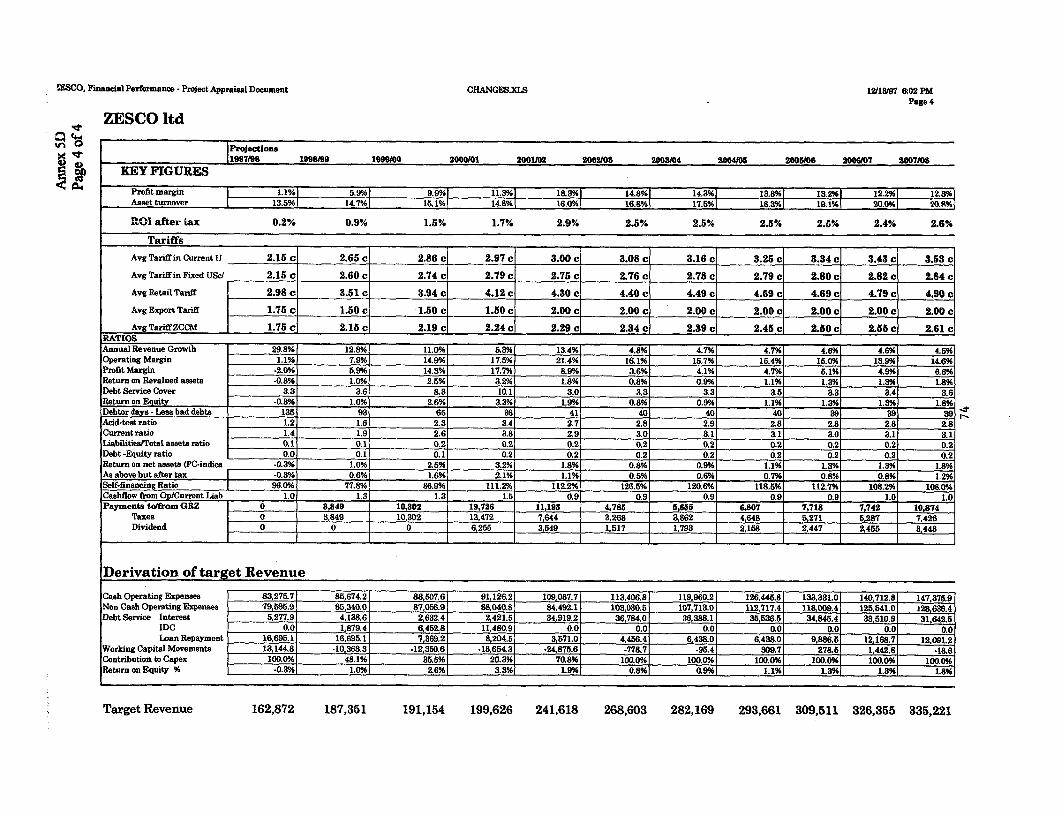

14. Financial Assessment of ZESCO (see Annex 5.)Detailed analysis of ZESCO's past and current financial performance, tariff issues and future financial projections are included inAnnex 5.

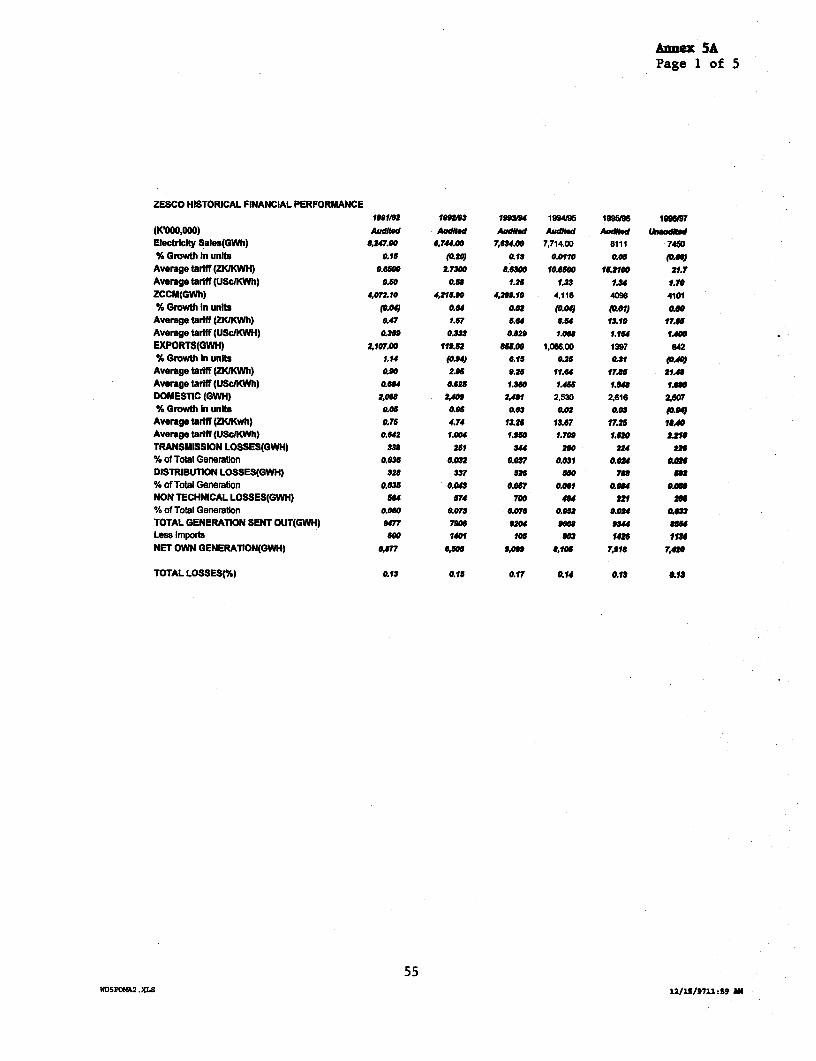

ZESCO's Past and Current Financial Performance. ZESCO's financial performance during the period 1991/2-1996/7 wasunsatisfactory (Table 1, Annex 5).

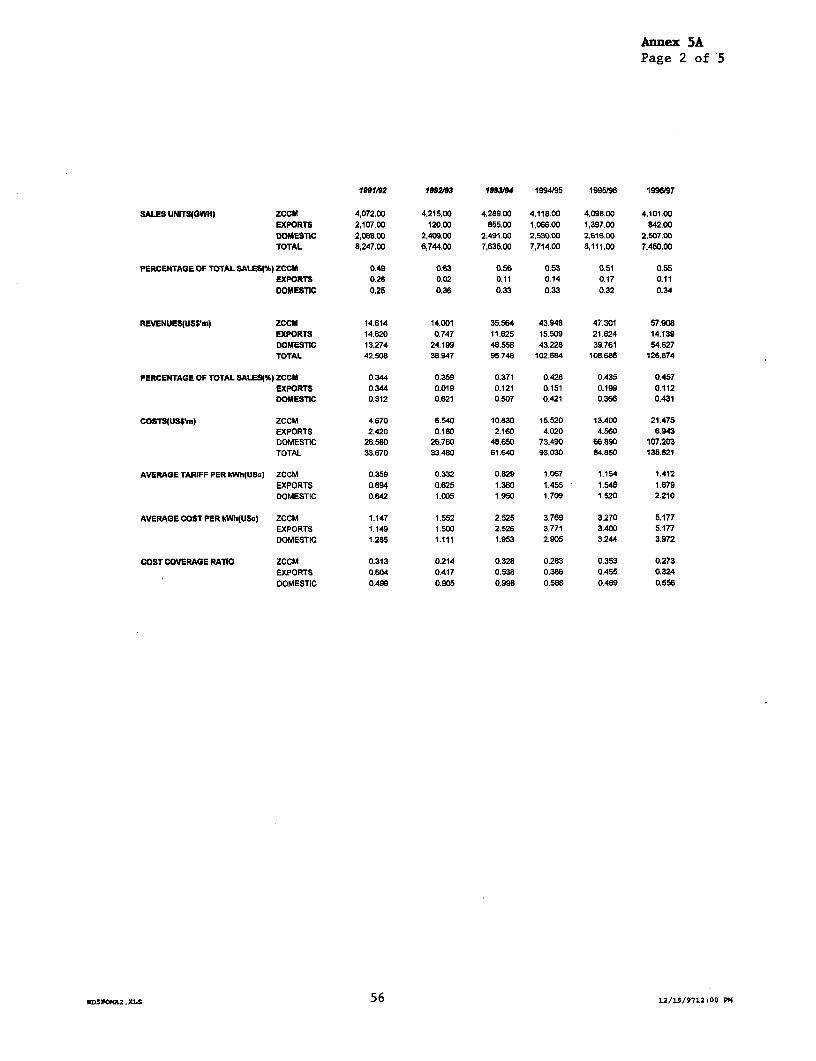

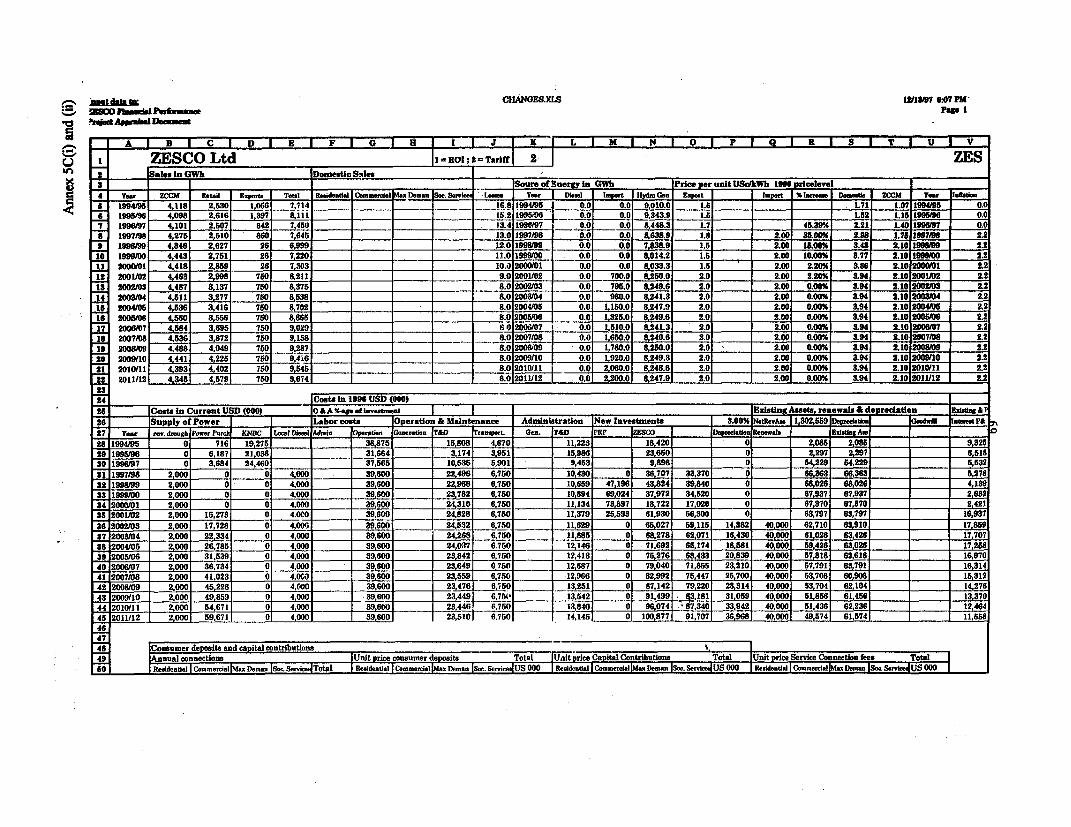

Sales 199112 199213 199314 199415 199516 199617ZCCM Sales (GWh) 4072 4216 4289 4118 4098 4101Exports(GWH) 2107 120 855 1066 1397 842Oomestik(GWH) 2068 2409 2491 2530 2616 2507Total 8,247.10 6,744.45 7,635.10 7,714.00 8,111.00 7,450.RevenueZCCM Sales (USS million) 14.61 14.00 35.56 43.95 47.30 57.91ExpoWUS$) 14.62 0.75 11,62 15.51 21.62 14.14Domestic(US$) 13.27 24.20 48.56 43.23 39.76 54.63TotalUSS) 42.51 38.95 95,75 102.68 108.69 126.67ProfitabilityTotal Operating Revenue 45.07 41.87 96.61 105.16 110.48 131.23Operating Margin 14.79 8.38 34.97 12.13 25.63 (16.39)Profi/Loss before Taxation (4.32 (28.79 2.20 (6.95) (6.62) (29.01')

ZESCO incurred losses in every year but one during that period. Moreover, these losses are understated as depreciation was basedon the historical cost of assets and the expenditure on maintenance in these years was limited by the availability of funds. The majorcauses of ZESCO's poor financial performance were: (a) Government control of tariffs, set at levels which did not cover costs (seebelow); (b) devaluation of the Kwacha, and as ZESCO's foreign debt and 80 percent of its operating costs are dollar based, thishad a substantial impact; (c) high levels of arrears (see below); and (d) revaluation of Assets led to considerably higherdepreciation charge in FY96. (However, this has also had positive effects on capital structure, as discusssed below.) GRZ andZESCO have recently made several important changes that have already begun to improve ZESCO's financial performance incertain areas, and if maintained will impact well upon ZESCO's future financial position. Changes in tariff setting processaccompanied by appropriate tariff adjustments will have a tremendous impact. In May 1996, a Performance Contract was signedbetween the Govermment and ZESCO. The latter has also introduced operational efficiencies, including the rationalization of itslabor force. Despite these positive changes, in 1996/7 due to a higher depreciation charge on account of revalued assets, ZESCOfailed to cover its operating costs -- recording an operating loss of US$16.3 million, and a total loss of US$29.01 million before tax.On the positive side, stabilization in exchange rates resulted in much lower foreign exchange losses than in previous years (1996/7,US$7 million as compared to 1995/6, US$25 million). The revaluation of fixed assets added US$1,150 million to equity as arevaluation reserve, strengthening ZESCO's equity base and capital structure -- in 1996/7, the debt to equity ratio was only 6percent The 1992 decision to have the ZCCM tariff quoted and paid in US dollars resulted in increased revenues during the periodof major devaluation froml991/2 to 1995/6. As a result of real tariff increases, sales revenues increased during the period 1994/5-1996/97 by 23 percent in dollar terms, from US$103 million to $127 million, an average annual increase of 11.5 percent.

8

ZESCO's Tariff. Before 1991, ZESCO was required to obtain government approval for all tariff increases: it developed tariffrecomnmendations and the Government generally approved less than applied for after a lengthy process. Consequently tariffs didnot cover costs, and tariff increases were below the rate of inflation. In 1991, ZESCO was given the autonomy to review tariffs asneeded. Domestic tariffs increased in dollar terms from USc 1.7/kWh in 1994/5 to USc 2.21/kWh in 1996/7, an average annualincrease of 10 percent. The ZCCM tariff increased from USc 1.067/KWh in 1994/5 to USc 1.4/KWh in 1996/7. Negotiations fortariff increases with ZCCM have always posed a problem as also its late settlement of debt causing significant negative impact onZESCO's cashflow. As a part of the tariff restructuring process, ZESCO has commissioned a Tariff Study, financed by the SwedishInternational Development Agency (SIDA) which will be used as the basis for establishing an appropriate tariff structure. ZESCOhas agreed to implement the reconunendations of the Tariff Study with regards to tariff structure by April 1, 1998. The levels oftariff increase required to achieve the financial objectives are provided in Annex 5.

Historical Tariffs 1991/2 1992/3 1993/4 1994/5 1995/6 1996/7Implied Average Tariff 0.515 0.578 1.254 1.331 1.340 1.70(UScents/kWh)Implied ZCCM Tariff 0.359 0.332 0.829 1.067 1.154 1.40(UScents/kWh)Implied Domestic Tariff 0.642 1.005 1.949 1.709 1.520 2.21(USc/kWh) .Implied Export Tariff 0.694 0.625 1.360 1.455 1.548 1.68(UScents/kWh)

Main Issues.

(a) ZESCO remains exposed to foreign exchange fluctuations and inflation, and will need to manage these variables to avoidnegative results on its financial performance. An agreement has been reached that ZESCO would apply an automatic tariffadjustment mechanism to take account of movements in both local and international exchange rates and inflation. The adjustmentwill be premised on tracking the impact of the above variables on ZESCO's operating costs, and subsequently translating these intoan adjustment factor for tariffs. The adjustment would occur quarterly and will not require Ministry approval. Agreement was alsoreached that the ZCCM tariff would continue to be quoted in US dollars.

(b) Arrears. Cashflow was ZESCO's critical problem during the period 1994/5 to 1996/7. Both the current and quick ratios werebelow one. Collections from ZCCM, Government and other parastatals was a major problem. The position worsened in 1996/7with 218 days of debt outstanding. As a result during this period, ZESCO's overdraft increased from US$1.4 million to US$15million. Strong efforts need to be made for recovery of arrears, and disconnection policy needs to be enforced vigorously. Anagreement has been reached between the Ministry of Finance and ZESCO that a clearing house mechanism would be established toclear outstanding arrears among parastatals and government departments, and ensure that dues owing to ZESCO will not exceedtwo months' billing. It was also agreed that ZESCO would submit semi-annual reports on December 1 and June 1 of each year onits billings and collections. ZESCO would reduce its outstanding balance of electricity sales debts equivalent to 120 days in1998/99, 90 days in 1999/2000, and 60 days thereafter. As of April 1, 1998, ZESCO will levy a late payment charge of 10 percenton bills unpaid on the due date. ZESCO agreed to enforce its disconnection policy which includes disconnecting customers withbills outstanding for 60 days after the due date. Under the project, agreement was reached that ZESCO would maintain a quickratio of one, and a current ratio of 1.5.

(c) Demand and Sales. Of ZESCO's three main customer categories, ZCCM, domestic and exports, ZCCM is the most significant,constituting 54 percent of its energy sales and 46 percent of its revenue in 1996/. ZCCM's relative importance to sales revenue(which increased from 43 percent in 1994/5 to 46 percent in 1996/7) is larger than its importance in volume of sales which havestabilized around 4,100 GWh per annum. As a percentage of ZESCO's sales, ZCCM's share increased modestly from 53 percentin 1994/5 to 54 percent in 1996/7. Although domestic sales increased by 3 percent per annum from 1994/5 to 1996/7 and ZCCMsales stabilized, overall sales decreased from 7717 GWh in 1994/5 to 7707 GWh in 1996/7 due to the loss of about half of the exportmarket (to Zimbabwe). Exports decreased from 1,397 GWh in 1995/6 to 860 GWh in 1996/7, and it is expected that the wholeexport market will be lost in 1997/8 for a few years. The financial projections are sensitive to demand and ZESCO's ability toexpand its domestic market.

(d) Privatization of ZCCM. GRZ is in the process of privatizing ZCCM. A fifteen year bulk sales agreement (BSA) between thenew owner of ZCCM's Power Division (Copperbelt Energy Consortium) and ZESCO has been reached.

9

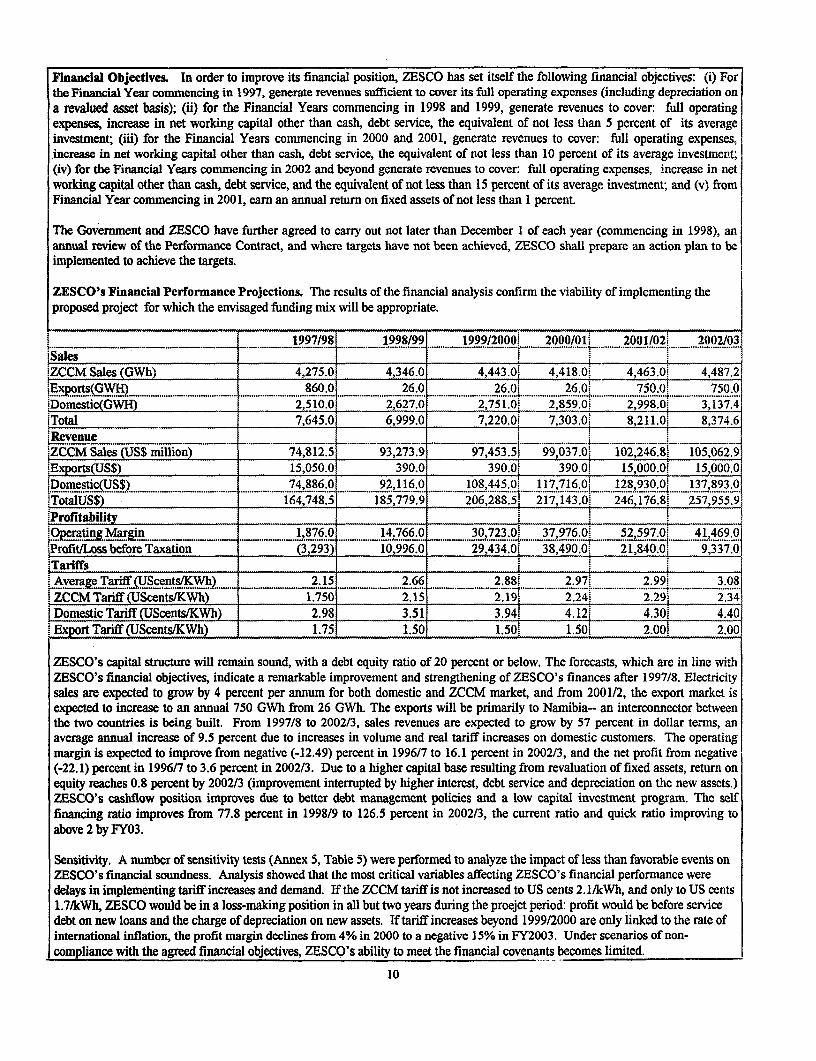

Financial Objectives. In order to improve its financial position, ZESCO has set itself the following financial objectives: (i) Forthe Financial Year commencing in 1997, generate revenues sufficient to cover its full operating expenses (including depreciation ona revalued asset basis); (ii) for the Financial Years commencing in 1998 and 1999, generate revenues to cover: full operatingexpenses, increase in net working capital other than cash, debt service, the equivalent of not less than 5 percent of its averageinvestment; (iii) for the Financial Years commencing in 2000 and 2001, generate revenues to cover: full operating expenses,increase in net working capital other than cash, debt service, the equivalent of not less than 10 percent of its average investment;(iv) for the Financial Years commencing in 2002 and beyond generate revenues to cover: full operating expenses, increase in networking capital other than cash, debt service, and the equivalent of not less than 15 percent of its average investment; and (v) fromFinancial Year commencing in 2001, earn an annual return on fixed assets of not less than 1 percent.

The Government and ZESCO have further agreed to carry out not later than December 1 of each year (commencing in 1998), anannual review of the Performance Contract, and where targets have not been achieved, ZESCO shall prepare an action plan to beimplemented to achieve the targets.

ZESCO's Financial Performance Projections. The results of the financial analysis confirm the viability of implementing theproposed project for which the envisaged funding mix will be appropriate.

1997/98 1998/99 1999/2000 2000/01 2001/02 2002/03.Sales , ._ _

.ZCCM Sales (GWh) 4,275.0 4,346.0 4,443.0. 4,418.0 4 463 0 4,487.2.Exports(.GWHj ._ . . .. . _ .............. ... .. .. 860.0 .26.0 .26.0 26.0 750.0 750.0~~~~~~~~.. ..... .... . . .... ... ... ... ... .. ..... ..... 2 2.( ..... .=............... ------............................... .. ----Domestic(GH)2,510.0 2,627.0 2,751.01 2,859.01 2,998.O0 3,137.4:Total 7,645.0 6,999.0 7,220.0 7 303.0. 8 211.0 8,374.6Revenue

_ ~. _ ............... _ ._ ........... _ ........ ..... ._ ._ ._ ._.........._._...._... _ ....... ...... _.._._......... . . _._...,._..._._._..._ _ _.__... . ..... _

;ZCCM Sales (US$ million) 74,812.5 93,273.9 97,453.5' 99,037.0i 102,246.8 105,062.9.Exports(US$) 15,050.0 390.0 390.0, 390 0 1500.00 15,000.0,Domestic(US$L -.- -74,886.0 92,116.0 108,445.0, 117,716.0. 128 930.0 137,893.0t _ _~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~... ... _._.______Z_ .......... .......... ........ _ ..... ........ ...... .._ ..... ..... ._ .... ....'Tota1US$) 164,748.5 185,779.9 2217,143.0 246=176.8 257,955.9Profitability |

1,876.0 14.766.0 30,723.0, 37 976.0- 525 41,469.0sProftlLoss before Taxation (3,293) 10,996.0 29,434.0 38,490.0. 21840.0 9,337.0Tariffs l _ ,_j _ I

E Average Tariff (UScents/KWh) 2.15 2.66 2.881 2.97. 2.99! 3.08,~~~~~~~~~~~~~~ ... .. ...... . .... .... . ...... . . ....... ... .... ..... ...... . ..... ------ ........ . ......... ....... .......ZCCM Tariff (UScentslKWh) 1.750 2.15 2.195 2.241 2.291 2.34Domestic Tariff (UScents/KWh) 2.98 3.51 3.941 4.121' 4.30: 4.40Export Tariff (UScents/KWh) 1.75 1.50 1.50! 1.501' 2.00i 2.00

ZESCO's capital structure will remain sound, with a debt equity ratio of 20 percent or below. The forecasts, which are in line withZESCO's financial objectives, indicate a remarkable improvement and strengthening of ZESCO's finances after 1997/8. Electricitysales are expected to grow by 4 percent per annum for both domestic and ZCCM market, and from 2001/2, the export market isexpected to increase to an annual 750 GWh from 26 GWh. The exports will be primarily to Namibia-- an interconnector betweenthe two countries is being built. From 1997/8 to 2002/3, sales revenues are expected to grow by 57 percent in dollar terms, anaverage annual increase of 9.5 percent due to increases in volume and real tariff increases on domestic customers. The operatingmargin is expected to improve from negative (-12.49) percent in 1996/7 to 16.1 percent in 2002/3, and the net profit from negative(-22.1) percent in 1996/7 to 3.6 percent in 2002/3. Due to a higher capital base resulting from revaluation of fixed assets, return onequity reaches 0.8 percent by 2002/3 (improvement interrupted by higher interest, debt service and depreciation on the new assets.)ZESCO's cashflow position improves due to better debt management policies and a low capital investment program. The selffinancing ratio improves from 77.8 percent in 1998/9 to 126.5 percent in 2002/3, the current ratio and quick ratio improving toabove 2 by FY03.

Sensitivity. A number of sensitivity tests (Annex 5, Table 5) were performed to analyze the impact of less than favorable events onZESCO's financial soundness. Analysis showed that the most critical variables affecting ZESCO's financial performance weredelays in implementing tariff increases and demand. If the ZCCM tariff is not increased to US cents 2. 1/kWh, and only to US cents1.7/kWh, ZESCO would be in a loss-making position in all but two years during the proejct period: profit would be before servicedebt on new loans and the charge of depreciation on new assets. If tariff increases beyond 1999/2000 are only linked to the rate ofinternational inflation, the profit margin declines from 4% in 2000 to a negative 15% in FY2003. Under scenarios of non-compliance with the agreed financial objectives, ZESCO's ability to meet the financial covenants becomes limited.

10

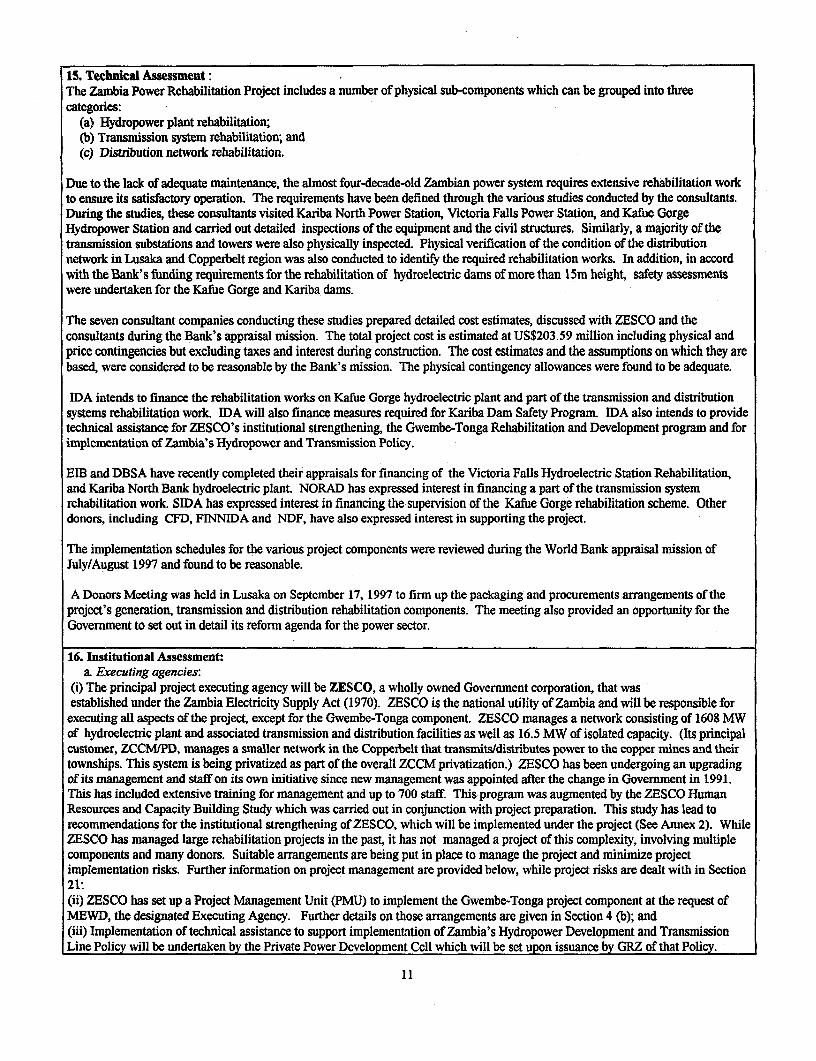

15. Technical Assessment:The Zambia Power Rehabilitation Project includes a number of physical sub-components which can be grouped into threecategories:

(a) Hydropower plant rehabilitation;(b) Transmission system rehabilitation; and(c) Distribution network rehabilitation.

Due to the lack of adequate maintenance, the almost four-decade-old Zambian power system requires extensive rehabilitation workto ensure its satisfactory operation. The requirements have been defined through the various studies conducted by the consultants.During the studies, these consultants visited Kariba North Power Station, Victoria Falls Power Station, and Kafue GorgeHydropower Station and carried out detailed inspections of the equipment and the civil structures. Similarly, a majority of thetransmission substations and towers were also physically inspected. Physical verification of the condition of the distributionnetwork in Lusaka and Coppeibelt region was also conducted to identify the required rehabilitation works. In addition, in accordwith the Bank's funding requirements for the rehabilitation of hydroelectric dams of more than l5m height, safety assessmentswere undertaken for the Kafue Gorge and Kariba dams.

The seven consultant companies conducting these studies prepared detailed cost estimates, discussed with ZESCO and theconsultants during the Bank's appraisal mission. The total project cost is estimated at US$203.59 million including physical andprice contingencies but excluding taxes and interest during construction. The cost estimates and the assumptions on which they arebased, were considered to be reasonable by the Bank's mission. The physical contingency allowances were found to be adequate.

IDA intends to finance the rehabilitation works on Kafue Gorge hydroelectric plant and part of the transmission and distributionsystems rehabilitation work. IDA will also finance measures required for Kariba Dam Safety Program. IDA also intends to providetechnical assistance for ZESCO's institutional strengthening, the Gwembe-Tonga Rehabilitation and Development program and forimplementation of Zambia's Hydropower and Transmission Policy.

EIB and DBSA have recently completed their appraisals for financing of the Victoria Falls Hydroelectric Station Rehabilitation,and Kariba North Bank hydroelectric plant. NORAD has expressed interest in financing a part of the transmission systemrehabilitation work. SIDA has expressed interest in financing the supervision of the Kafue Gorge rehabilitation scheme. Otherdonors, including CFD, FINNIDA and NDF, have also expressed interest in supporting the project.

The implementation schedules for the various project components were reviewed during the World Bank appraisal mission ofJuly/August 1997 and found to be reasonable.

A Donors Meeting was held in Lusaka on September 17, 1997 to firm up the packaging and procurements arrangements of theproject's generation, transmission and distribution rehabilitation components. The meeting also provided an opportunity for theGovernment to set out in detail its reform agenda for the power sector.

16. Institutional Assessment:a Executing agencies:

(i) The principal project executing agency will be ZESCO, a wholly owned Government corporation, that wasestablished under the Zambia Electricity Supply Act (1970). ZESCO is the national utility of Zambia and will be responsible forexecuting all aspects of the project, except for the Gwembe-Tonga component. ZESCO manages a network consisting of 1608 MWof hydroelectric plant and associated transmission and distribution facilities as well as 16.5 MW of isolated capacity. (Its principalcustomer, ZCCM/PD, manages a smaller network in the Copperbelt that transmits/distributes power to the copper mines and theirtownships. This system is being privatized as part of the overall ZCCM privatization.) ZESCO has been undergoing an upgradingof its management and staff on its own initiative since new management was appointed after the change in Government in 1991.This has included extensive training for management and up to 700 staff. This program was augmented by the ZESCO HumanResources and Capacity Building Study which was carried out in conjunction with project preparation. This study has lead torecommendations for the institutional strengthening of ZESCO, which will be implemented under the project (See Annex 2). WhileZESCO has managed large rehabilitation projects in the past, it has not managed a project of this complexity, involving multiplecomponents and many donors. Suitable arrangements are being put in place to manage the project and minimize projectimplementation risks. Further information on project management are provided below, while project risks are dealt with in Section21:(ii) ZESCO has set up a Project Management Unit (PMU) to implement the Gwembe-Tonga project component at the request ofMEWD, the designated Executing Agency. Further details on those arrangements are given in Section 4 (b); and(iii) Implementation of technical assistance to support implementation of Zambia's Hydropower Development and TransmissionLine Policy will be undertaken by the Private Power Development Cell which will be set upon issuance by GRZ of that Policy.

11

b. Project management: Because of the Project's complexity and magnitude, it has been agreed with ZESCO that it should beimplemented under a special Project Implementation Unit (PIU) headed by a Project Director (PD) reporting directly to theManaging Director (MD). A group of engineers will assist the PD to: (i) monitor the cost and schedule of the project components;(ii) handle procurement and contractual matters; and (iii) advise the PD, in a timely manner, on any cost or schedule overruns. ThePD will implement the project through Project Managers (PMs), who will manage the project on a day-to-day basis with theassistance of engineering/management consultants, as appropriate. One consultant will be appointed to supervise each projectcomponent. Each PM will have a project engineer, stationed in the field, and be required to maintain an appropriate level ofcoordination during project implementation. A Steering Committee, chaired by the MD, will be established to ensure coordinationamong the various ZESCO Directorates and the orderly transfer of the completed project components to the appropriate ZESCODirectorate. An expatriate advisor will be appointed to assist the PD in project implementation. ZESCO has prepared a ProjectImplementation Plan (PIP).17. Social Assessment:The social component of the Project aims to improve the conditions of people unsuccessfully resettled in the first Kariba project.The Bank and the University of Zambia's Institute of Economic and Social Research (INESOR) signed the contract for a study andaction plan for rehabilitation of Kariba-affected peoples in January 1997. That study, "The Rehabilitation and DevelopmentStrategy for the Peoples Affected by the Construction of the Kariba Dam (Gwembe-Tonga)," produced a report (September 1997),incorprating a Rehabilitation and Development program and cost estimate (see Annex 12). The current cost estimate for theRehabilitation and Development Program is US$15.13 million of which ongoing IDA projects, DBSA funding and the RE Fund(Section 8) will be tapped to assure that all the project sub-components are fully financed.

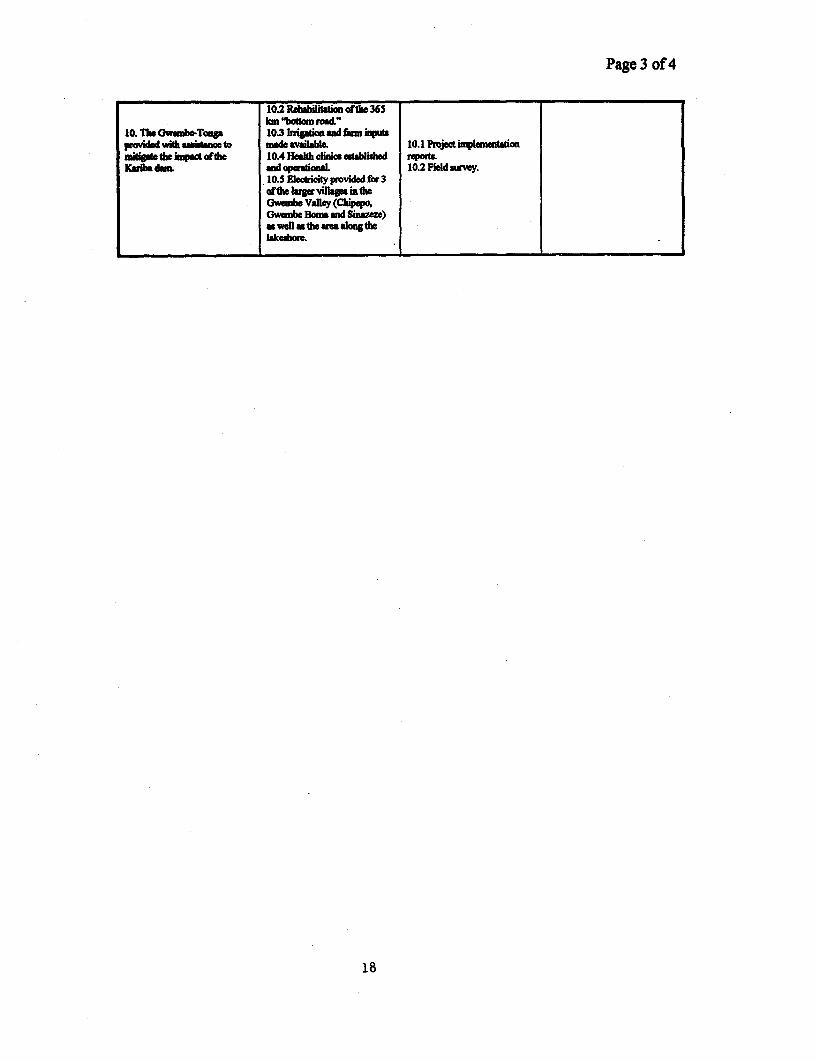

The Rehabilitation and Development Program includes inter alia: (a) the rehabilitation of 365 km of a key road ("the BottomRoad") that connects the three districts that have received the resettled people; (b) water resources development combiningimproved water supply and improving cropping patterns along the margins of the reservoir that are timed to coincide with thepatterns of reservoir drawdown and refilling; (c) improvement of land use through strengthened agricultural extension facilities,including a pilot agriculture scheme. In addition, a fund is to be created to support micro-projects dealing with land use; (d)Upgrading of health facilities and services; and (e) electrification of three of the large villages (Chipepo, CGwembe Boma andSinazeze), as well as the area around the reservoir.

Strengthening the Social Affairs professional staff in ZESCO's recently formed Environment and Social Affairs Unit (ESU) is alsoincluded in the proposed Project (Section 18).

18 Environmental Assessment:A Sectoral Environmental Scoping study for Zambia's power sector, including the proposed Project, was completed in 1995. Themajor recommendations of the Study were to: (a) establish an Environmental and Social Affairs Unit (ESU) in ZESCO; (b)develop a rehabilitation plan for the Kariba Gwembe-Tonga (see Section 17); (c) develop a waste management plan, including forPCBs; (d) undertake sub-basin-wide environmental and social assessments for upcoming hydropower projects; and (e) encouragecommitment to the ESU by ZESCO's Board and senior management. These recommendations will be addressed under the proposedproject.

The major environmental issue identified in project preparation was the treatment of wastes and harmful substances in some of theexisting hydropower plants and transmission lines. An assessment of waste was included in each of the separate rehabilitationcomponents of the Project and their management will be addressed during implementation. A study financed by CIDA will developa comprehensive program for management/disposal of PCBs, and will be coordinated with the Enviromnental Council of Zambia(ECZ) and ZESCO. ZESCO has agreed to implement the study's recommendations.

Strengthening the recently formed ESU, which is responsible for planning and implementation of enviromnental and socio-economic programs associated with ZESCO projects, is a key component in the Project, as is ESU completion of initial training andwork programs. In addition, the ESU will initiate a monitoring and audit program, with monthly reporting requirements. Theprogram will track project progress in relation to the implementation of environmental and socio-economic activities.

Victoria Falls Hydro Station Rehabilitation Environmental Assessment (EA). The EA on Victoria Falls, a World Heritage site dueto its unique geology, was completed in March 1997 in conjunction with the preparation of the rehabilitation study of the VictoriaFalls hydro station. The EA found no additional impacts associated with the Project. However, the EA found that operation of thestation has had negative impacts, including land degradation, PCB contamination, water management issues and associateddegeneration of tourism and aesthetic loss. To address these issues, the proposed Project includes environmental component forVictoria Falls which will enhance the ecology and aesthetic value of the site (see section 22). Zambia is a riparian on the Zambeziriver. While the proposed Victoria Falls Rehabilitation component does not alter the flow regime of the Zambezi and does notrequire notification, GRZ has agreed to notify the Government of Zimbabwe at the request of EIB.

12

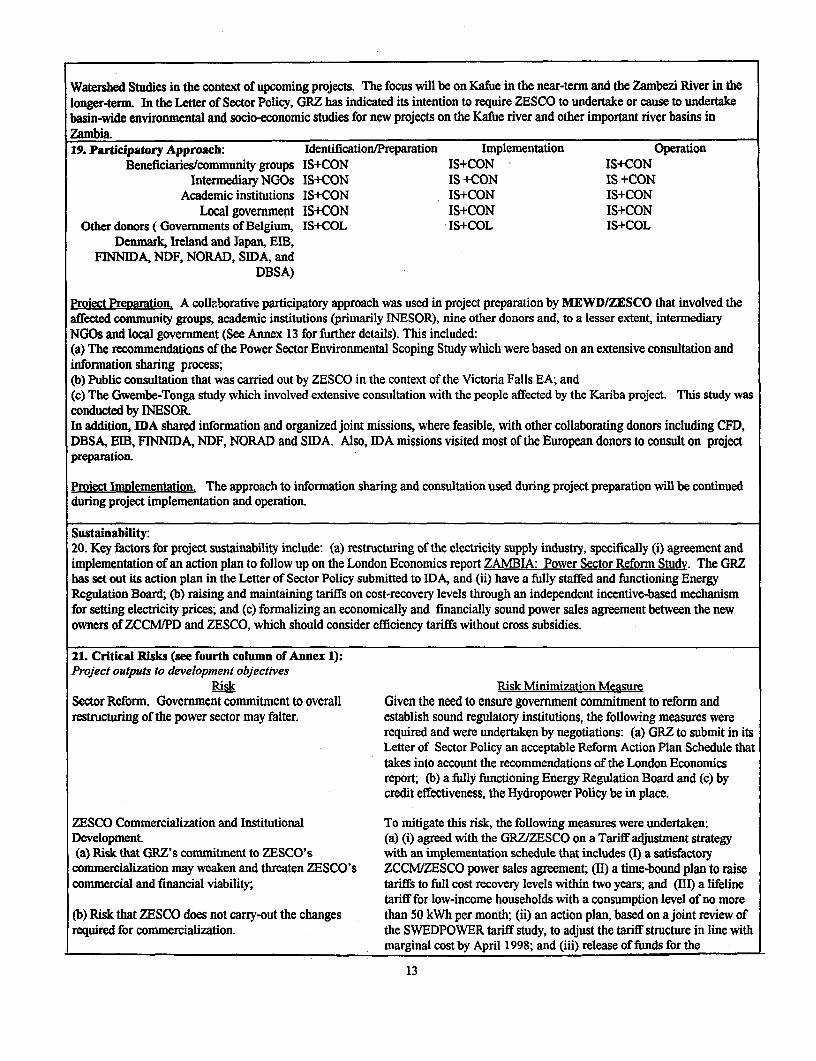

Watershed Studies in the context of upcoming projects. The focus will be on Kafue in the near-term and the Zambezi River in thelonger-term. In the Letter of Sector Policy, GRZ has indicated its intention to require ZESCO to undertake or cause to undertakebasin-wide environmental and socio-economic studies for new projects on the Kafue river and other important river basins inZambia.19. Participatory Approach: Identification/Preparation Implementation Operation

Beneficiaries/community groups IS+CON IS+CON - IS+CONIntermediary NGOs IS+CON IS +CON IS +CON

Academic institutions IS+CON IS+CON IS+CONLocal government IS+CON IS+CON IS+CON

Other donors ( Govermnents of Belgium, IS+COL IS+COL IS+COLDenmark, Ireland and Japan, EIB,

FlNNlDA, NDF, NORAD, SIDA, andDBSA)

Project Preparation. A collaborative participatory approach was used in project preparation by MEWD/ZESCO that involved theaffected community groups, academic institutions (primarily INESOR), nine other donors and, to a lesser extent, intermediaryNGOs and local government (See Annex 13 for further details). This included:(a) The recommendations of the Power Sector Environmental Scoping Study which were based on an extensive consultation andinformation sharing process;lb) Public consultation that was carried out by ZESCO in the context of the Victoria Falls EA; and(c) The Gwembe-Tonga study which involved extensive consultation with the people affected by the Kariba project. This study wasconducted by INESORIn addition, IDA shared information and organized joint missions, where feasible, with other collaborating donors including CFD,DBSA, EIB, FINNIDA, NDF, NORAD and SIDA. Also, IDA missions visited most of the European donors to consult on projectpreparation.

Project Implementation. The approach to information sharing and consultation used during project preparation will be continuedduring project implementation and operation.

Sustainability:20. Key factors for project sustainability include: (a) restructuring of the electricity supply industry, specifically (i) agreement andimplementation of an action plan to follow up on the London Economics report ZAMBIA: Power Sector Reform Studv. The GRZhas set out its action plan in the Letter of Sector Policy submitted to IDA, and (ii) have a fully staffed and functioning EnergyRegulation Board; (b) raising and maintaining tariffs on cost-recovery levels through an independent incentive-based mechanismfor setting electricity prices; and (c) formalizing an economically and financially sound power sales agreement between the newowners of ZCCM/PD and ZESCO, which should consider efficiency tariffs without cross subsidies.

21. Critical Risks (see fourth column of Annex 1):Project outputs to development objectives

Risk Risk Minimization MeasureSector Reform. Government commitment to overall Given the need to ensure govermment commitment to refonn andrestructuring of the power sector may falter. establish sound regulatory institutions, the following measures were

required and were undertaken by negotiations: (a) GRZ to submit in itsLetter of Sector Policy an acceptable Reform Action Plan Schedule thattakes into account the recommendations of the London Economicsreport; (b) a fully functioning Energy Regulation Board and (c) bycredit effectiveness, the Hydropower Policy be in place.

ZESCO Commercialization and Institutional To mitigate this risk, the following measures were undertaken:Development. (a) (i) agreed with the GRZ/ZESCO on a Tariff adjustment strategy(a) Risk that GRZ's commitment to ZESCO's with an implementation schedule that includes (I) a satisfactory

commercialization may weaken and threaten ZESCO's ZCCMIZESCO power sales agreement; (II) a time-bound plan to raisecommercial and financial viability; tariffs to full cost recovery levels within two years; and (III) a lifeline

tariff for low-income households with a consumption level of no more(b) Risk that ZESCO does not carry-out the changes than 50 kWh per month; (ii) an action plan, based on a joint review ofrequired for commercialization. the SWEDPOWER tariff study, to adjust the tariff structure in line with

marginal cost by April 1998; and (iii) release of funds for the

13

transmission component, financed by IDA, will be linked to satisfactoryproject performance by the GRZ/ZESCO over its first two years. Inaddition, (iv) the Borrower shall establish a mechanism, acceptable toIDA, to clear outstanding arrears bi-monthly among parastatals andGovermnent Departments.

(b) (v) ZESCO will implement its manpower rationalization programand recommended company change processes; and (vi) ZESCO willcarry out a review of its performance contract with GRZ on an annualbasis and where targets have not been achieved, shall prepare fordiscussion with IDA and for implementation, an action plan to achievetargets.

Project components to outputsRisk Risk Minimization Measure

Delays in project implementation due to Beneficiary's Implementation of the project through a reduced number of contracts,inexperience, large number of components, complexity and provision of technical assistance in project implementationand multiple funding sources. (including the hiring of competent supervisory consultants) will

mitigate the risk. Careful planning and coordination between co-financing agencies will also be required.

Overall project risk ratingRisk

Sector reforms will not be sustained Release of fimds by IDA for the project's transmission component(about US$20 million) will be linked to satisfactory project performanceover its first two years. Performance indicators will be based on ZESCOcompliance with financial and institutional covenants.

22. Possible Controversial Aspects:Some Zambian tour operators would like to see Victoria Falls Power Station closed, as they believe it negatively alters the dry

season flow of the Falls lowering the aesthetic/tourist value of the Falls. However, the diversion of water in the dry season to theZimbabwe side of the Falls is largely due to geologic conditions. During the EA done to evaluate the problem there was extensiveconsultation with tour operators. Based on this consultation, the EA identified a series of actions to reduce any negative impact ofthe power station and its operation on the environment and aesthetics and, further, to take actions to enhance the Falls aesthetic andtourist appeal. These actions, which are part of the proposed Project under the rehabilitation of Victoria Falls, include: (i)developing a waste management and site restoration program to mitigate ZESCO's historic impact on the National Park area; (ii)relocating the majority of staff housing from the Falls to Livingstone and convert the Falls housing to tourist accommodation; (iii)relocating the intake siphon discharge and reconstruct the original steps to the Falls base; (iv) developing the 1938 power stationinto a museum and interpretive center, (v) developing and implementing a water management plan which optimizes powergeneration, aesthetic beauty for Victoria Falls and public safety; and (vi) initiating a monitoring and audit program to track projectprogress and implementation.

Block 4: Main Loan Conditions23. Effectiveness ConditionsPrior to effectiveness the following actions will have been undertaken:(a) the ZESCO Subsidiary Loan Agreement (SLA) will have been duly authorized or ratified by the Borrower and ZESCO and willbe legally binding upon the Borrower and ZESCO according to its terms;(b) the (cofinanciers) Loan Agreements for NORAD and SIDA would have been duly executed and all conditions precedent to theeffectiveness of the Loan Agreements fulfilled, other than those related to the effectiveness of the DCA;(c) the Project Agreement would have been duly authorized or ratified by ZESCO and be legally binding upon the Borroweraccording to its terms;(d) ZESCO will have hired engineering consultants to assist in the implementation of the following principal project components: (i)

rehabilitation of the Victoria Falls hydroelectric station; (ii) rehabilitation of the Kafue Gorge hydroelectric station; (iii) rehabilita-tion of the Kariba North Bank hydroelectric station; (iv) Kariba Dam safety activities; and (v) the transmission systemrehabilitation;

(e) ZESCO will have adopted a Project Implementation Plan satisfactory to IDA; and(f) GRZ will have promulgated its Hydropower Development and Transmission Line Policy.

14

24. Coditions of Disbursement* Releas of funds by IDA for the project's transmission component (about USS20 million) will be linked to satisfactory project

prfoanance over its first two years; and* Rdease of funds by IDA for the project's Gwembe-Tonga component wil be subject to conclusion of implementation

arran nts, satiaory to IDA.

25. CovenantsIn addition to the standard covenants covering auditing and record-keeping, the Project will use the following covenants:* The Borrower shall apply an automatic adjustment mechanism of tariffs acceptable to 1DA.* The Borrower shaU establish a mechanism, acceptable to IDA, to clear outstanding arrears monthly among parastatals and

Government Departments, and ensure that its dues to ZESCO would not exceed two months billing.* ZESCO shall carry out, with the participation of the Borrower, not later than December 1 of each year, an annual review of the

Perbrmance Contract under terms of reference satisfactory to IDA, and prepare an action plan to achieve the targets, if notachieved.

* ZESCO shall meet the following financial objectives: (i) for fiscal year commencing April 1, 1997, the borrower shall generatervenues to cover full operating expenses (including depreciation on a revalued asset basis); (ii) for fiscal years commencingApril 1, 1998 and 1999, generate revenues to cover full operating expenses (including depreciation on a revalued asset basis), networking capital increases other than cash, debt service and 5 percent of the average of its investment; (iii) for fiscal yearscommencing April 1, 2000 and 2001, generate revenues to cover full operating expenses (including depreciation on a revaluedasset basis ), net working capital increases other than cash, debt service and the equivalent of not less than 10% of the average ofits investment; and (iv) for fiscal year commencing April 1, 2002, generate revenues to cover full operating expenses (includingdepreciation on a revalued asset basis), net working capital other than cash, debt service and the equivalent of not less than 15%of the avcrage of its investment In addition, beginning in fiscal year April 1, 2000, ZESCO shall earn a return on equity of notless than II/a. Accordingly, ZESCO shall implement a tariff increase on April 1, 1998, to meet its FY98 financial objectives.

* The Borrower and the Association shall jointly review semiannually the adequacy of electricity tariffs.* The Borrower shaU submit by May 1 in each year commencing in 1998 ZESCO's draft rolling five year investment program and

ZESCO shaU adopt a power investment program for such Financial Year which shaU be satisfactory to IDA. Thereafter, ZESCOshall not carry out any power investment in excess of US$5 million which is not for the program.

* ZESCO shall, twice yearly, furnish to the Association the status of its billings and collections as of September 30 and March 31each year and will not alow its outstanding customer accounts to exceed 120 days of revenue in fiscal year commencing in 1998,90 days of revenue in fiscal year commencing in 1999, and 60 days in all succeeding financial years. ZESCO shall, according toagreed targets in the Project Agreement, reduce non-technical losses.

* ZESCO shall revalue its fixed assets annually in accordance with indices acceptable to IDA.* ZESCO shall implement by July 1, 1998 the agreed manpower rationalization plan.. ZESCO shall implement the agreed recommendations of the PCB Study, and the execution of interim protective measures by

June 30, 1998.* ZESCO will put in place guidelines for environmental review of projects and determine the types of projects which require ESU

approval or clearance by June 30, 1998.* ZESCO shall implement its disconnection policy. As of April 1, 1998, ZESCO will levy a late payment charge of 10 percent on

bills unpaid on the due date and will disconnect customers with bills outstanding for 60 days after the due date.

Block 5: Compliance with Bank Policies[x ] This project complies with all applicable Bank policies.[1 [The foUowing exceptions to Bank policies are recommended for approval: None. The project complies with all other

applicable Bank policies.]

Task Manager: Donal O'tVarBocar Tha-m Cu ry halliso omerant

15

Annex 1Page 1 of 4

Zambia: Power Rehabilitation ProjectProject Design Summary

Narratve Summary Verifiable Indicators Means of Verification Assumptions/Risks

CAS OBJECrmVE: Increased Annual real GDP per capita National statistics.eeomic rowth gowth

Development Objecdive: Impact Outcomes:1. Stable macro economy.

EffEimi reliable and 1. Energy and power supply is 1. Electricity demand forecastfincally viable power sysem meeting 100% of expected and ZESCO's generation 2. Continued deregulatoryedablisbed and meeting power domestic demand at efficient records. policies.d_mnd at leaodat. prices by 2001.

2. ZESCO's operational 3. Other infiastructure services2. Lncreased electricity records. are improved as well.coverage.

3. ZESCO's records. 4. Other conditions for growth3. Average system losses are created.reduced to 14% by 2000. 4. Consumer surveys.

5. Adequate mobilization of4. ZESCO's annual O&M cosL 5. Project Managemnent resources.

Records.5. ERR for components at start, 6. Adequate tariff increasesmid-term and at the end of 6. ZESCO's records & implemented.project intemational cost data.

6. Cost of supply. 7. ZESCO's financialstatements.

7. ZESCO's annual ROR onrevalued assets and selffinancing ratio. _

Outpdas: Proes Indicators:

1. Power sector reformed 1.1 Action plan implemented 1.1 Monitoring & supervision 1.1 Continued Governmentfor power sector restructuring of TA and policy dialogue. commitment to reform.1.2 Energy Regulation Board 1.2. ERB allowed to operateoperational (ERB). independently.1.3 Policy framework for 1.3. ERB staff adoptprivate sector participation in professionally sound practices.generation and transmission 1.4. NORAD and other donorsestablished. This includes providing additional technicalestablishing a Private Power assistance as agreed.Development Cell (PPDC) or 1.5 PPDC allowed to operateequivalent organization, effectively.1.4 Electricity tariff adjusted 1.6. Government providingbased on economic and adequate budget allocations.

2. ZESCO instional financial requirements. 2.1 Project implementationdevelopment incl. commercial documents. 2.1. Government commitmentoperation, and utility & to commercialization includingfinncial management 2.1 Company change program agreement set out in the

inplemented. Performance Contract with2.2 Manpower restructuring ZESCO.plan inplemented. 2.2 ZESCO management2.3 Staff appraisal scheme conumitmentimplemented. 2.3 NORAD and other donors2.4 Health awareness program provide additional technicaland life insurance scheme assistance as agreed.

3. Financial Sustainability of implemented. 3.1 ZESCO's audited fmancialZESCO. staternents. 3.1 ZCCM tariff negotiated at

3.2 ZESCO's management level to cover cost and give3.1 Tariffwhich cover costs accounts. return on equity.for all consumer categories, and 3.3 Auditors management 3.2 Price elasticity is low.gives a return on equity. letters. 3.3 Commitment by GOZ and3.2 Quick ratio of 1 or more. 3.4 Progress reports. ZESCO.3.3 Implementation and 3.4 Effective implementationconsistent application of of financial management andformula for automatic accounting systems.adjustment oftariffs. 3.5 Effective operation of

16

Page 2 of 4

3.4 Reduction of system losses. clearing mechanism for3.5 Collecions improving from Govemment debt coniset21 days to 60 days. application offoemula for3.6 Timely producion of automatic a4jutment oftarifs.montly management accounta. 3.6 QuaUified and competnt3.7 Establishmnt of cost staffin Finance De _tnt.centres for geeration,disribution and traision.3.8 Payment of dividends.

4. 1 Projec management unit 4. ZESCO commitnetestablishe4.2 Expeft hired to help with 4.1 Projed implementation

4. Project managanat project implementation, document.cpacity is ineaed

5.1 The ESU is caryring out 5.1. Maagemet committedtomonitoring ofthe sound environmental policieLenvironmental mitigation plan 5.1 Supervision mission & 5.2 Staff adapt professionally

5. The pefmane of ofthe project satisfictorily. environental reports produced sound practices.ZESCO's envionmental and by ZESCO.soca affais uit (ESU) incrying out envionental 6.1 Generation and

_ssesmta is inproved 6.1 # of substations refurbished transmission rehabilitated asper year. wel.6.2 # ofsubstations 6.1 Site visits & project

6. The distribution systems in constructed. implementation repots 5.2 The whole network isTuaka, Kitwe, Ndola 6.3 - kms of conductors maintained and operated inrehabilitated. reinforced. accordance with good industry

6.4-bks offaulty or practice.overloaded cables replaced.6.5 # oftrinsformers inIstalled.6.6 SCADA systemrefurbished.

7.1 30,000 meters installed by 7.1 Consumer acceptance.2001. 7.2 Tampering of meters6.2 No of load and power factor eliminated.indicators installed by 2001. 7.1 Site visits & project

7. Repcement and installation implementation records.of consumer mnets and power S. 16,000 km of transmissionfadtor indicators. lines rehabilitated by 2001. S. 1 Generation and distrbution

8.2 # ofsubstations rehabilitated as well.rehabilitated by 2001. 8.2 Adequate and timely

S. Transmission sytetm 8.3 PLC and radio link 8. 1 Site visits & project maintenance of the wholerehabilitated established. inplementation records. system.

9.1 9.1 Transmission andVictoria Falls: distribution rehabilitated as- civil stuctwures maintained well.- electro mechanical equipment 9.2 Adequate hydrology.

9. 3 hydro power plants refurbished. 9.1 Site visits & project 9.3 ZESCO provides adequatereshbilted (Victoria Falls, - protection and staff safety implementation records. funds for O&M expenditure.Kariba North, Kafiue Gorge). equipment rehabilitated.

- environmental action plan 9.4 Consumer demand exist.implemented.

Kariba North:- civil structures rehablitated.- electro mechanical equipmentrefurbished.

. protection and staffsafetyequipment rehabilitated.

Kafue Gorge:* civil structures rehabilitated- electromechanical equipmnetrehabilitated.

- staff safety equipmentrehabilitated.

10.1 Safe drinking wateravailable. 10.1 GwembaTonga

17

Page 3 of 4

10.2 Rbabdbaitaion of th 365km "botm road."