workshop on joint action 2011 - choisir une...

TRANSCRIPT

WORKSHOP ON JOINT ACTION 2011

FINANCIAL MANAGEMENT ASPECTS

Content of the presentation

1. General information

2. Budgetary aspectsExpenditures & Incomes

3. Financial Viability Information‘Balance sheet’ and ‘Profit & Loss account’

4. Supporting documents to attach yourproposal

5. Useful sources of information

General information

General principles

Co-funding rule: external co-financing from a source other than EC funds is required (own resources or financial contributions from third parties)

Non-profit rule: the grant may not have the purpose or effect of producing a profit for the beneficiary

Non-retroactivity rule: only costs incurred after the starting date stipulated in the grant agreement can be co-funded

Non-cumulative rule: only one grant can be awarded for a specific action carried out by a given beneficiary

Overview of Joint Action mechanism EC Funding of eligible costs: Up to 50% (or up to

70% in case of exceptional utility*)

Type of Organisations: Public bodies and NGOs* (non-profit making, Independence from private sectors)

Type of grants: Multi-beneficiaries

Annexes to the Agreement: Description of the Action (Technical annex); Estimated budget by category (Financial annex)

Duration in months: Up to 36 months

Types of participants

NoNoNoNoNoCollaboratingPartner

NoYesNoNoNoFinancialDonor

NoNoYes

(Invoiced tobeneficiaries)

NoNoSubcontractor

YesYesYesYesNoAssociatedBeneficiary (*)

YesYesYesYesYesMainBeneficiary

Contractual relationship

with the European

Commission

FinancialContributionto the grant

Eligible coststo be

co-financedCoreTasksCoordinationTypes of

Participant

Budgetary Aspects

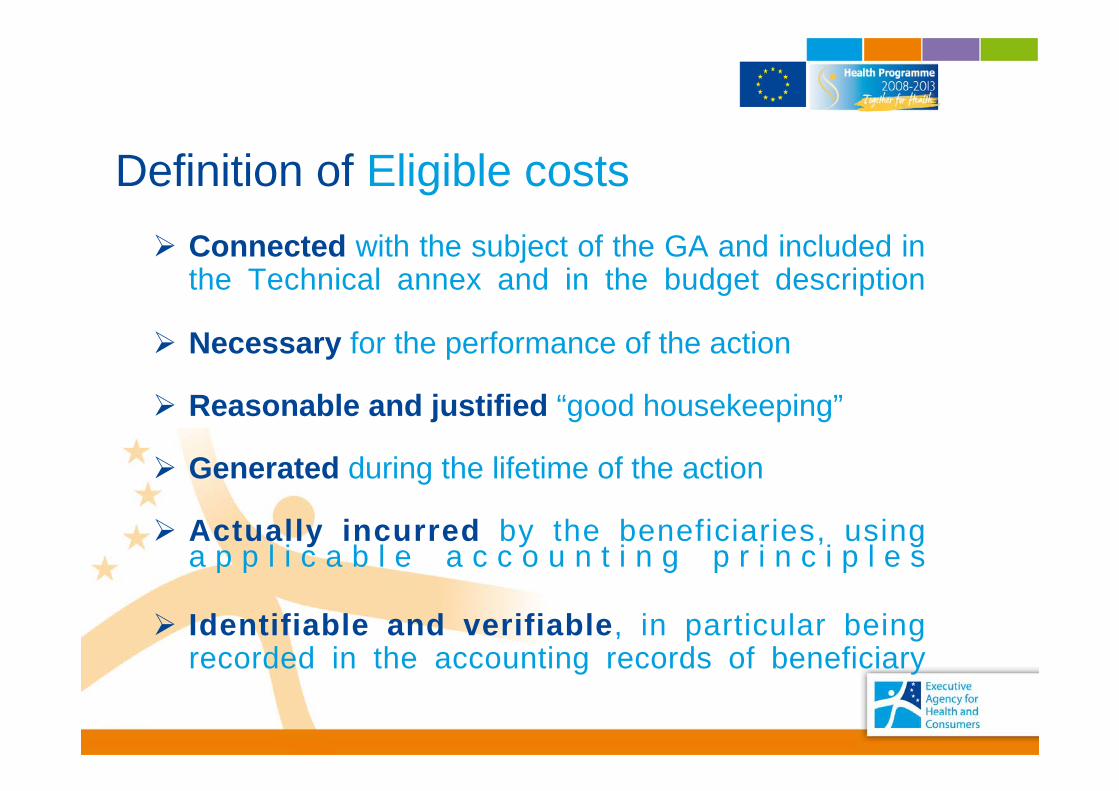

Definition of Eligible costs Connected with the subject of the GA and included in

the Technical annex and in the budget description

Necessary for the performance of the action

Reasonable and justified “good housekeeping”

Generated during the lifetime of the action

Actually incurred by the beneficiaries, using a p p l i c a b l e a c c o u n t i n g p r i n c i p l e s

Identifiable and verifiable, in particular being recorded in the accounting records of beneficiary

Definition of Non-eligible costs Those not compiled in Art. II.14.1

Return on capital

Debt and debt services charges

Provision for losses or potential future liabilities

Interest owed, doubtful debts

Exchange losses

VAT (Unless the beneficiary can prove that is unable to recover it)

Cost declared by a beneficiary and covered by another action funded by a EC grant

Definition of Direct Costs and Indirect Costs

Direct Costs are those costs which are identifiable as specific directly linked to the performance of the action, so they can be charged (if they are eligible to the project). (see cost categories 1 to 6)

Indirect Costs are those costs which are not identifiable as specific costs linked to the performance of the action, but that have been incurred in connection with the eligible direct costs for the action. (see cost categories 7 - Overheads)

Direct Costs - 6 cost categories

1

2

3

4

5

6

Staff

Travel Costs and subsistence allowances

Equipment

Consumables and supplies linked to the project

Subcontracting costs

Other costs

7 Overheads

Indirect Cost – 1 cost category

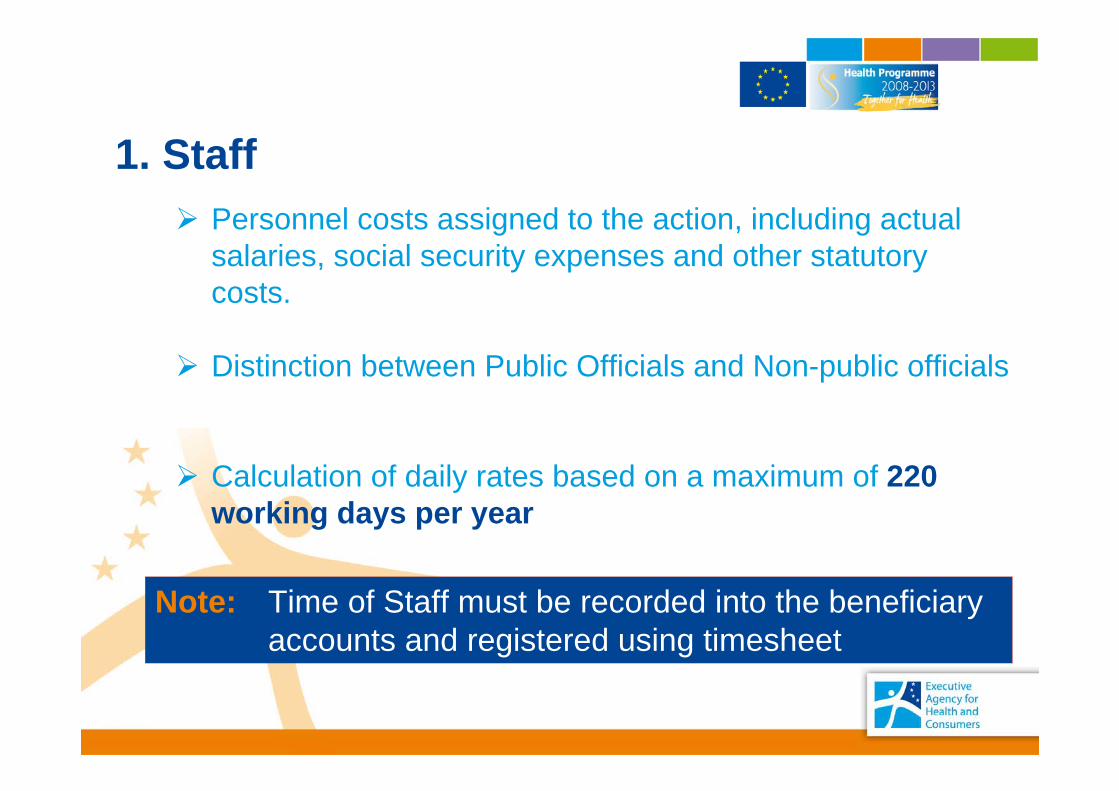

1. Staff Personnel costs assigned to the action, including actual

salaries, social security expenses and other statutory costs.

Distinction between Public Officials and Non-public officials

Calculation of daily rates based on a maximum of 220 working days per year

Note: Time of Staff must be recorded into the beneficiary accounts and registered using timesheet

Definition of Public officials

An official of a public body who is directly remunerated by the budget of the State or a local authority and his/her work concerns the implementation of tasks typically devolved to public institutions.

By extension, it does concern all public officials who work in international organisations.

Note: Cost of Public officials must also satisfy the cumulativeand general criteria laid down in Article II.14.1 of thegrant agreement defining the eligible costs.

Encoding of StaffExample for a joint action of 36 month-duration

Public Officials

Example

Encoding of StaffExample for a joint action of 36 month-duration

Non Public Officials

Example

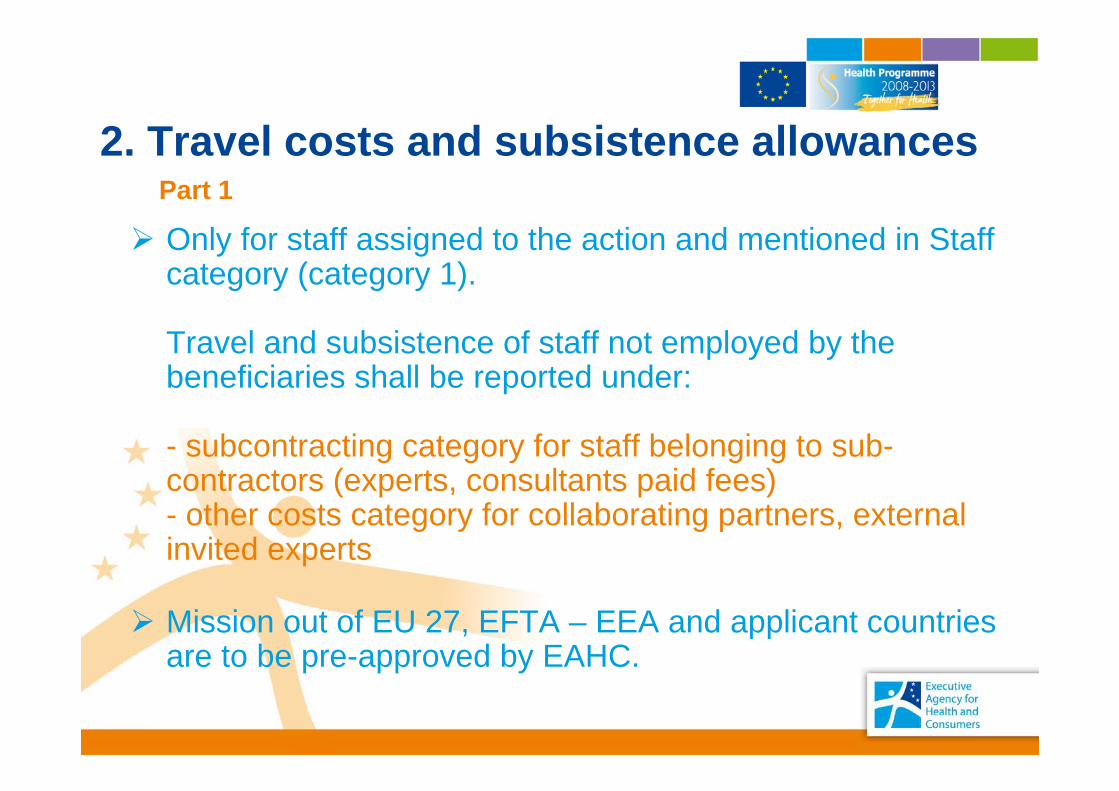

Only for staff assigned to the action and mentioned in Staff category (category 1).

Travel and subsistence of staff not employed by the beneficiaries shall be reported under:

- subcontracting category for staff belonging to sub-contractors (experts, consultants paid fees)- other costs category for collaborating partners, external invited experts

Mission out of EU 27, EFTA – EEA and applicant countries are to be pre-approved by EAHC.

2. Travel costs and subsistence allowancesPart 1

The internal rules of the partners have precedence in matter of travel costs and subsistence allowances. In absence of such rules EC rules must be applied :

- use of the more economic and direct way- at least 100 km from normal place of work- rail first class- plane economic and cheaper (e.g. APEX)- car on the equivalence of rail first class

2. Travel costs and subsistence allowancesPart 2

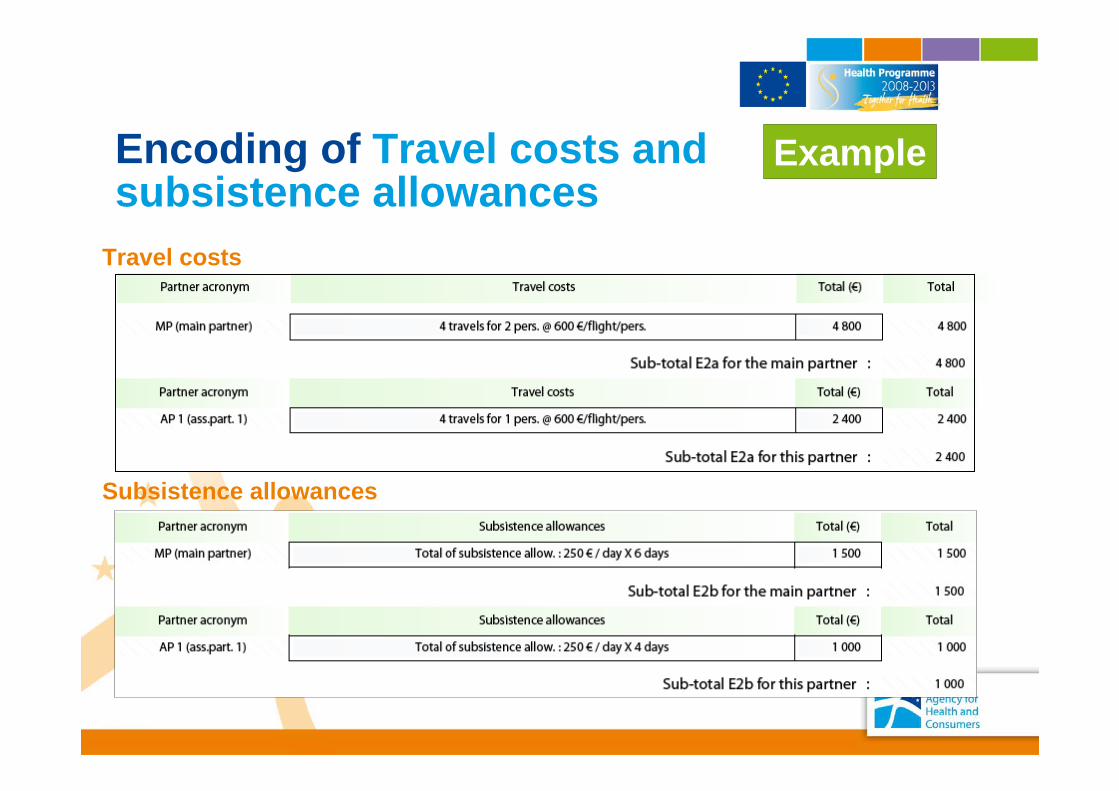

Encoding of Travel costs and subsistence allowances

Travel costs

Subsistence allowances

Example

Only the portion of the equipment’s depreciation corresponding to the duration of the project and the rate of actual use for the purposes of the project (% allocation to the project) may be taken into account by the EAHC

Common software (ex. Microsoft Office, Excel, Word,) should be covered by the flat-rate in “E7. Overheads”

The internal rules of the partners have precedence in matter of depreciation of equipment, if not the EC rules apply (hardware – 36 months, furniture – 60 months)

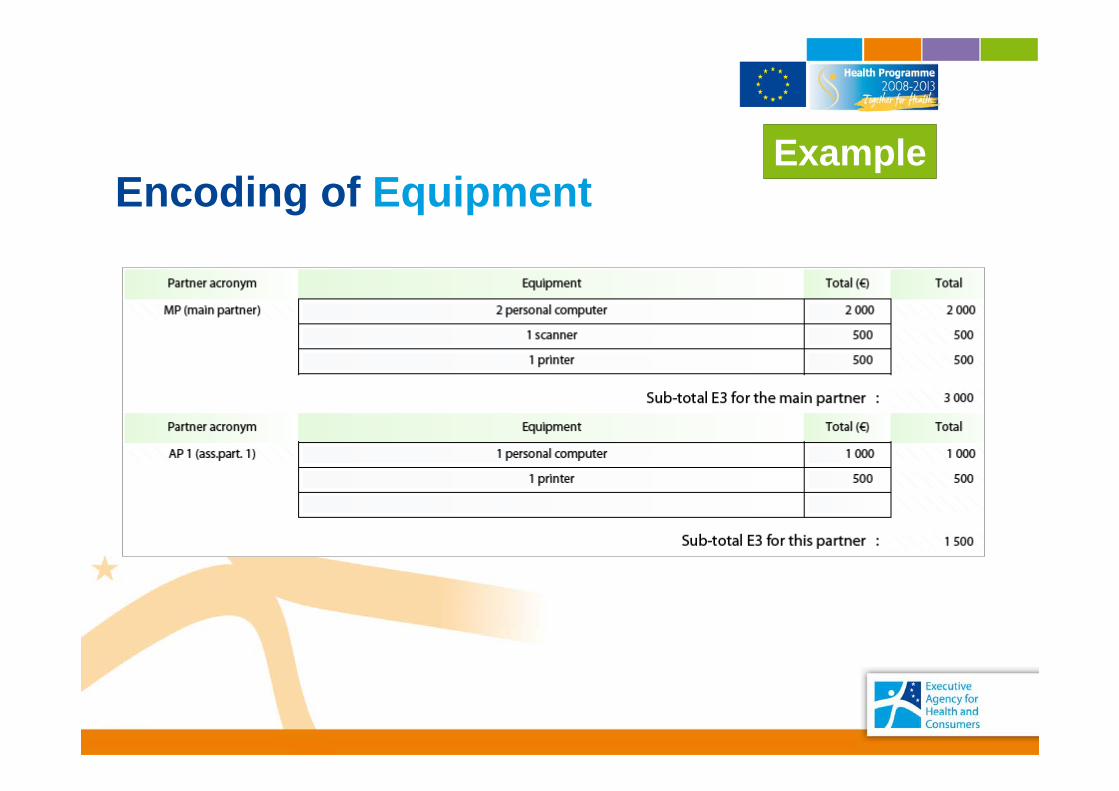

3. Equipment

Encoding of EquipmentExample

These costs should normally appear in “E7. Overheads”.

Nevertheless, provided that they are identifiable as specific costs directly linked to performance of the joint action and booked into the partners’ accounting system, they can appear under this category.

4. Consumables and supplies linked to the joint action

Encoding of Consumables and supplies linked to the joint action

Example

Contracts awarded to cover the execution of a limited part of the joint action (40% of the eligible cost as a general rule).

Core elements of the joint action cannot be subcontracted.

The technical and financial management of the joint action is the legal responsibility of the main partner. (no transfer to a third party or associated partner).

Tasks subcontracted must be set out in Annex I and the corresponding costs presented in Annex II of the Grant Agreement

5. SubcontractingPart 1

Public beneficiaries must refer to National rules in matter of award of contracts

NGOs beneficiaries shall seek competitive tenders from potential tender subcontractors. The subcontract shall be awarded to the bid offering best value for money. In doing so beneficiary shall observe the principles of transparencyand equal treatment of potential subcontractors and shall take care to avoid any conflict of interests.

Minimum of bids to be consulted (recommendation)- more than 5 bids…….....................x > 60.000 €- at least 5 bids…………25.000 € < x < 60.000 €- at least 3 bids…………..5.000 € < x < 25.000 €- one bid……………….....................x < 5.000 €

x = estimated value of subcontract

5. SubcontractingPart 2

Encoding of Subcontracting Example

Other exceptional additional costs not falling within any of the five other cost categories (1 to 5) may be charged, provided that they :- are directly related to the joint action- can be clearly identified and justified by the accounting rules and principles of the partners- satisfy the criteria of direct eligible costs.

Examples of other costs: dissemination of information, specific evaluation of the joint action, financial audits, financial guarantee, translations, reproduction, travels costs and subsistence allowances for collaborating partners or for external invited experts.

6. Other costs

Encoding of Other costs Example

Costs which are not identifiable as specific costs directly linked to performance of the action which can be booked to it direct, but which can be identified and justified by the beneficiary using his accounting system as having been incurred in connection with the eligible direct costs for the action

No justifying accounting documents needed

A maximum of 7% of the total eligible direct costs

7. Overheads (indirect costs)Part 1

Overheads comprise costs connected with infrastructures and the general operation of the organisation.

Examples of other costs : hiring, depreciation of buildings and plant, water/gas/electricity, maintenance, insurance, supplies and petty office equipment, communication, postage, administrative and financial management, human resources, training, legal advice, IT, etc.

7. Overheads (indirect costs)Part 2

Encoding of Overheads Example

Overview of Expenditures Example

Incomes : 5 categories 1. Co-funding request from the Community budget: Financial

contribution granted by European Union.

2. Contribution pertaining to public officials: Amount automatically copied from “Costs pertaining to public officials” – No input required.

3. Applicant financial contribution: Own financial contribution provided by main or each associated applicants.

4. Income generated by the project: Revenues linked to and generated by the action itself such as admission fee to a conference, sale of publications, etc.

5. Other external resources of the project: Other grants allocated either at international level, European level, national level, regional level or local level and/or financial transfers received from donors/sponsor.

Encoding of Incomes and Checks

Example

Check if balance iszero !

Total Expenditures= Total Incomes

Check if EC contribution in % is correct !

Check if EC contribution in Eur is correct !

Input required

Financial viability information

Financial viability information Only required for NGOs main applicant.

Information to be encoded in the application form:- Accountancy information- Balance sheet of the two last accounting years (*)- Profit and loss account (*)

(*) NGOs using a cash accounting system and newly created entities are exempted to encode this information in the application form.

Supporting documents to be attached to the proposal:- Copy of balance sheet of the two last accounting years- Copy of profit and loss account

For NGOs using a cash accounting system and newly created entities a copy of statutory accounts is sufficient.

ExampleEncoding of Accountancy information

To be ticked if applicable !

ExampleEncoding of Balance sheetfor the last 2 financial years

Assets

Liabilities

Check if Assetsand Liabilities do balance for each

year!

Check if figures are consistent with supporting documents

attached to the proposal.And

ExampleEncoding of Profit and loss account

Important documents to attach to your proposition

Legal documents to providefrom applicant

Copy of the organization’s statutes / articles

Copy of the official registration certificate (for Public bodies, copy of the decree on their creation)

Declarations of Honour Original of the Declaration of Honour,

duly signed and stamped, is required from the main applicant

Original or copy (fax or scan) of the Declaration of Honour, duly signed and stamped, is required from the associated applicants

Missing originals will be required if the proposition is selected for funding)

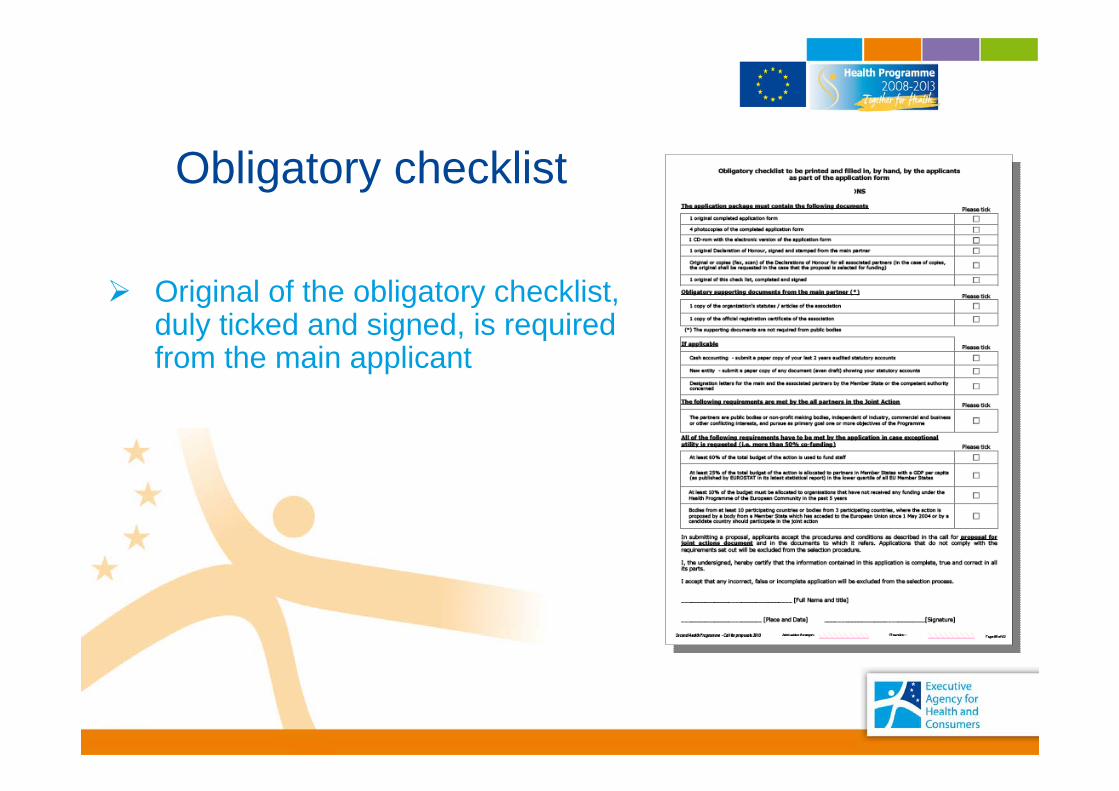

Obligatory checklist

Original of the obligatory checklist, duly ticked and signed, is required from the main applicant

Useful sources of information

And

Documentation helping in preparation of the proposition

Useful sources of information Websites

Executive AgencyEAHC Website

http://ec.europa.eu/eahc/index.html

Public Health Portalhttp://ec.europa.eu/health-eu/

European CommissionDG SANCO Web Site

http://ec.europa.eu/health/index_en.htm

Guide for applicants

http://ec.europa.eu/eahc/health/actions.html

To be read before starting to fill in the application form !!!

Conclusion

Conclusion – Main reminders when preparing the proposals

Original of the obligatory checklist, duly ticked and signed, is provided ?

Global Budget is balanced ? Expenditures = Incomes

Balance Sheet is balanced ? Assets = Liabilities

Figures of ‘Balance Sheet’ and in ‘Profit & LossAccount ’ encoded in the Viability Check annex are consistent with supporting documents ?

Thank you for your attention –any questions?