wipro ltd (wipro) | 317content.icicidirect.com/mailimages/idirect_wipro_q2fy19.pdf · citing the...

TRANSCRIPT

October 25, 2018

ICICI Securities Ltd | Retail Equity Research

Result Update

Growth and margin visibility improving...

Wipro reported Q2FY19 results were above our expectations,

excluding one-offs. In constant currency, global IT services revenues

grew 2.8% sequentially (above our estimate of 1.3% QoQ). Adjusted

for one-off settlement of | 514.1 crore, IT services EBIT margin stood

at 18% in Q2FY19 (vs our expectation of 16.1%).

US$ revenues grew 0.7% QoQ to $2041.2 million. However, adjusting

for divestment of its hosted data centre business, dollar revenue

growth was 1.9% sequentially.

Reported EBIT margin stood at 14.4% (from adjusted margin of

15.6% in Q1FY19). Adjusted EBIT margin improved by 240 bps to

18.0% mainly led by rupee depreciation (+70 bps), automation &

productivity improvement (+90 bps) and cost optimisation of global

subsidiaries (+90 bps).

Improving growth across verticals gives better revenue visibility…

After many quarters of company specific headwinds led by client’s

insolvency and restructuring of business, Wipro reported a strong quarter

with 2.8% revenue growth in constant currency. Four verticals out of

seven grew at 4% and more QoQ in cc terms with BFSI reporting 16%

YoY growth. Healthy performance in BFSI for consecutive seventh quarter

and strong growth in digital business are the highlights for the quarter.

Further, incremental positive commentary for healthcare business and

consumer business segment besides BFSI and communications is a key

positive.

….Order bookings and higher digital contribution are key positive

Citing the outlook for Q3FY19E, Wipro guided that its IT services revenues

would be in the range of $2028-2068 million, translating to 1-3% QoQ

growth. This growth expectation is on the basis of excluding India PSU

and India Government business which contributed $34 million in the

quarter. In addition, two-month consolidation of Alight acquisition (~$25

million) would support the growth in Q3FY19E. Further, improving digital

revenues contribution (accounted for 31.4% of services revenue in

Q2FY19 vs 24.1% in Q2FY18) over the coming years will further drive

growth. Strong order bookings, healthy pipeline, and incremental

positives across verticals are expected to lead to accelerated growth in

the year ahead. This coupled with rupee depreciation, we expect IT

services rupee revenues to increase at a CAGR of 10% over FY18-20E.

Margin improvement to boost profitability…

We believe the company’s margins of 18.0% in current quarter are

sustainable in the coming years mainly led by higher automation (from

3% to 10%), healthy revenue growth and rupee depreciation. As a result,

we upgrade our margin estimates and expect IT services EBIT margin of

16.8%, 17.7% in FY19E, FY20E respectively.

On growth trajectory; maintain BUY…

Wipro reported a strong quarter on all fronts. Further, positive guidance in

the wake of seasonal Q3 along with optimistic commentary across most

verticals with continued strength in BFSI and digital prompt us to be

constructive on Wipro’s growth trajectory. This coupled with

sustainability of higher margins in coming quarters will further boost

profitability. Hence, we maintain our BUY recommendation on the stock

with a revised target price of | 360 per share (15x FY20E EPS).

Rating matrix

Rating : Buy

Target : | 360

Target Period : 12 months

Potential Upside : 14%

What’s Changed?

Target Changed from | 325 to | 360

EPS FY19E Changed from | 18.8 to | 20.1

EPS FY20E Changed from | 21.5 to | 23.8

Rating Unchanged

Quarterly Performance

Q2FY19 Q2FY18 YoY (%) Q1FY19 QoQ (%)

Revenue 14,541 13,424 8.3 13,978 4.0

EBIT 2,062 2,305 (10.5) 2,331 (11.6)

EBIT (%) 14.2 17.2 -299 bps 16.7 -250 bps

PAT 1,889 2,191 (13.8) 2,121 (10.9)

Key Financials

| Crore FY17 FY18 FY19E FY20E

Net Sales 55,040 54,636 60,171 65,306

EBITDA 11,458 10,542 11,763 13,361

Net Profit 8,490 8,008 9,088 10,721

EPS (|) 17.5 16.8 20.1 23.8

Valuation summary

FY17 FY18 FY19E FY20E

P/E 18.2 18.8 15.7 13.3

Target P/E 20.5 21.4 17.8 15.1

EV / EBITDA 10.6 12.1 9.9 8.2

P/BV 2.9 3.1 2.5 2.2

RoNW (%) 16.3 16.6 16.2 16.6

RoCE (%) 16.9 16.9 16.9 17.5

Stock data

Particular Amount

Market Capitalization (| Crore) 142,762.7

Total Debt (| Crore) 13,825.9

Cash and Investments (| Crore) 29,525.1

EV (| Crore) 127,063.5

52 week H/L 339 / 253

Equity capital 904.8

Face value | 2

Price performance (%)

1M 3M 6M 12M

TCS (15.4) (6.2) 9.3 43.7

Infosys (9.0) (0.8) 11.8 40.2

Wipro (8.3) 6.7 2.3 2.7

HCL Tech (10.9) (0.5) (8.0) 4.2

Research Analysts

Devang Bhatt

Deepti Tayal

Wipro Ltd (WIPRO) | 317

ICICI Securities Ltd | Retail Equity Research Page 2

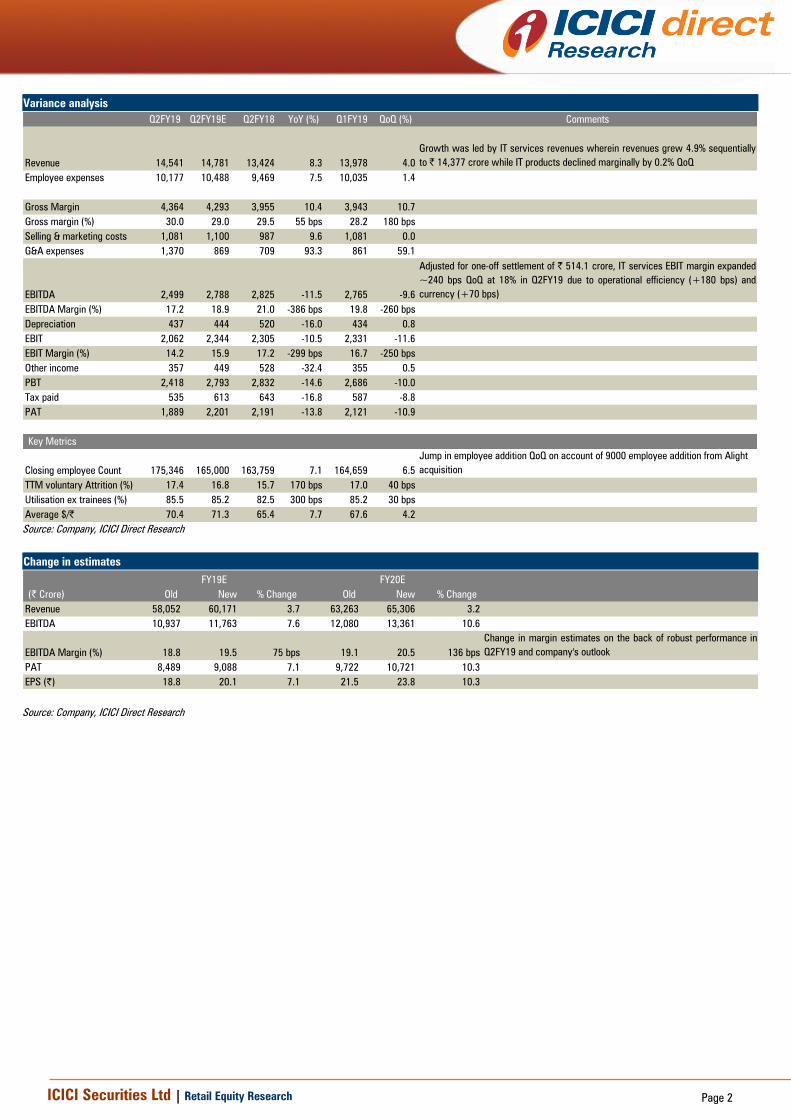

Variance analysis

Q2FY19 Q2FY19E Q2FY18 YoY (%) Q1FY19 QoQ (%) Comments

Revenue 14,541 14,781 13,424 8.3 13,978 4.0

Growth was led by IT services revenues wherein revenues grew 4.9% sequentially

to | 14,377 crore while IT products declined marginally by 0.2% QoQ

Employee expenses 10,177 10,488 9,469 7.5 10,035 1.4

Gross Margin 4,364 4,293 3,955 10.4 3,943 10.7

Gross margin (%) 30.0 29.0 29.5 55 bps 28.2 180 bps

Selling & marketing costs 1,081 1,100 987 9.6 1,081 0.0

G&A expenses 1,370 869 709 93.3 861 59.1

EBITDA 2,499 2,788 2,825 -11.5 2,765 -9.6

Adjusted for one-off settlement of | 514.1 crore, IT services EBIT margin expanded

~240 bps QoQ at 18% in Q2FY19 due to operational efficiency (+180 bps) and

currency (+70 bps)

EBITDA Margin (%) 17.2 18.9 21.0 -386 bps 19.8 -260 bps

Depreciation 437 444 520 -16.0 434 0.8

EBIT 2,062 2,344 2,305 -10.5 2,331 -11.6

EBIT Margin (%) 14.2 15.9 17.2 -299 bps 16.7 -250 bps

Other income 357 449 528 -32.4 355 0.5

PBT 2,418 2,793 2,832 -14.6 2,686 -10.0

Tax paid 535 613 643 -16.8 587 -8.8

PAT 1,889 2,201 2,191 -13.8 2,121 -10.9

Key Metrics

Closing employee Count 175,346 165,000 163,759 7.1 164,659 6.5

Jump in employee addition QoQ on account of 9000 employee addition from Alight

acquisition

TTM voluntary Attrition (%) 17.4 16.8 15.7 170 bps 17.0 40 bps

Utilisation ex trainees (%) 85.5 85.2 82.5 300 bps 85.2 30 bps

Average $/| 70.4 71.3 65.4 7.7 67.6 4.2

Source: Company, ICICI Direct Research

Change in estimates

(| Crore) Old New % Change Old New % Change

Revenue 58,052 60,171 3.7 63,263 65,306 3.2

EBITDA 10,937 11,763 7.6 12,080 13,361 10.6

EBITDA Margin (%) 18.8 19.5 75 bps 19.1 20.5 136 bps

Change in margin estimates on the back of robust performance in

Q2FY19 and company's outlook

PAT 8,489 9,088 7.1 9,722 10,721 10.3

EPS (|) 18.8 20.1 7.1 21.5 23.8 10.3

FY19E FY20E

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 3

Conference call highlights:

Management guidance: Wipro has guided that its Q3FY19E IT

services revenues would be in the range of $2028 -2068 million,

which translates into 1%-3% QoQ growth. This growth expectation

is on the basis of excluding India PSU and India Government

business which translates to global IT services revenue of $2007

million in Q2FY19. However, on reported number basis in Q2FY19

($2041 million), growth guidance for Q3FY19E would translate to (-

0.6%) to 1.3%. Two-month consolidation of Alight acquisition

would support the growth in Q3FY19E

Margins outlook: Adjusting for one-off settlement of | 514.1 crore,

IT services EBIT margins reported strong performance and

expanded 240 bps QoQ to 18.0% (from adjusted margin of 15.6% in

Q1FY19). For FY19E, the management expects IT services EBIT

margins to be in the range of ~18% with Q3FY19E margins to be in

narrow band of Q2FY19

BFSI & Communication momentum: BFSI (30.7% of revenue)

continued its growth trajectory for yet another quarter and grew

4.4% QoQ and 16% YoY (in CC terms). The management reiterated

its positive outlook for BFSI on the back of the segment being an

early adopter of digital and its execution capability of digital

transformation for clients. On the communication segment, after six

quarters of weakness, segment grew 4.2% sequentially in cc terms.

Management cited at increasing traction driven by enterprise core

spend and higher spending on the back of 5G roll out

Healthcare: With 12.8% of revenue, weakness persisted in the

vertical as it declined 3% QoQ in the quarter. Management stated

that headwinds and uncertainty pertains in the segment due to HPS

weakness. By Q3FY19E, it would be clearer of how the segment

pans out in the year ahead. With new leadership in the vertical and

company making investments in the adjacent areas, management

expects healthcare business coming back to industry-level growths

in next two to three quarters

Digital revenues: Digital revenues contribution to revenues

accelerated and accounted for 31.4% of services revenue (vs 24.1%

in Q2FY18) and grew 13% QoQ and 32% YoY in reported terms

Realignment in IT services business: Effective Q3FY19, India PSU

and India government business would be carved out of IT services

segment while enterprise business in India will continue to be part

of IT Services segment. This is done mainly on account of volatile

nature of carved our business and leveraging its portfolio offerings

in terms of areas witnessing good traction

Employee details: The company’s closing employee count was at

175,346 vs. 164,659 in Q1FY19. Jump in employee addition QoQ is

on account of 9000 employee addition from Alight deal. Net

utilisation (ex-trainees) increased 30 bps QoQ to 85.5%. In terms of

attrition rate, voluntary attrition (TTM) increased 40 bps QoQ for

another straight quarter to 17.4%. In terms of visa concerns, HCL

has limited onsite risk as more than 60% of its workforce in US are

locals

ICICI Securities Ltd | Retail Equity Research Page 4

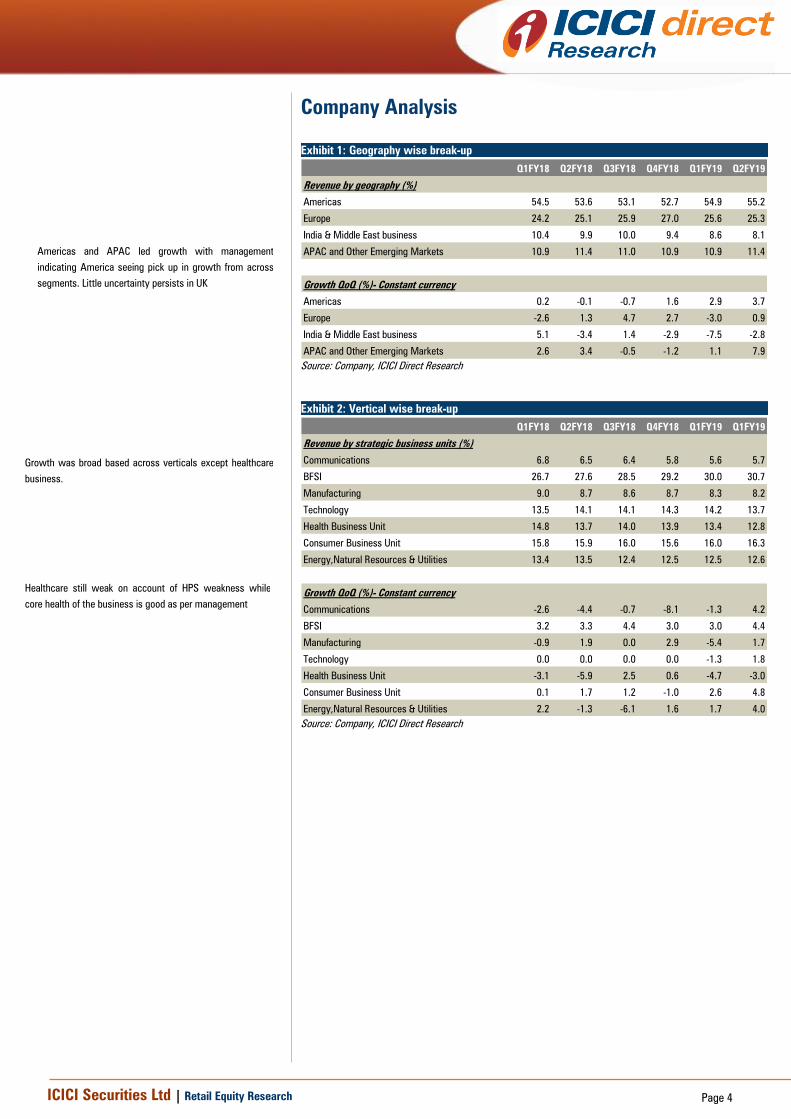

Company Analysis

Exhibit 1: Geography wise break-up

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19

Revenue by geography (%)

Americas 54.5 53.6 53.1 52.7 54.9 55.2

Europe 24.2 25.1 25.9 27.0 25.6 25.3

India & Middle East business 10.4 9.9 10.0 9.4 8.6 8.1

APAC and Other Emerging Markets 10.9 11.4 11.0 10.9 10.9 11.4

Growth QoQ (%)- Constant currency

Americas 0.2 -0.1 -0.7 1.6 2.9 3.7

Europe -2.6 1.3 4.7 2.7 -3.0 0.9

India & Middle East business 5.1 -3.4 1.4 -2.9 -7.5 -2.8

APAC and Other Emerging Markets 2.6 3.4 -0.5 -1.2 1.1 7.9

Source: Company, ICICI Direct Research

Exhibit 2: Vertical wise break-up

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q1FY19

Revenue by strategic business units (%)

Communications 6.8 6.5 6.4 5.8 5.6 5.7

BFSI 26.7 27.6 28.5 29.2 30.0 30.7

Manufacturing 9.0 8.7 8.6 8.7 8.3 8.2

Technology 13.5 14.1 14.1 14.3 14.2 13.7

Health Business Unit 14.8 13.7 14.0 13.9 13.4 12.8

Consumer Business Unit 15.8 15.9 16.0 15.6 16.0 16.3

Energy,Natural Resources & Utilities 13.4 13.5 12.4 12.5 12.5 12.6

Growth QoQ (%)- Constant currency

Communications -2.6 -4.4 -0.7 -8.1 -1.3 4.2

BFSI 3.2 3.3 4.4 3.0 3.0 4.4

Manufacturing -0.9 1.9 0.0 2.9 -5.4 1.7

Technology 0.0 0.0 0.0 0.0 -1.3 1.8

Health Business Unit -3.1 -5.9 2.5 0.6 -4.7 -3.0

Consumer Business Unit 0.1 1.7 1.2 -1.0 2.6 4.8

Energy,Natural Resources & Utilities 2.2 -1.3 -6.1 1.6 1.7 4.0

Source: Company, ICICI Direct Research

Americas and APAC led growth with management

indicating America seeing pick up in growth from across

segments. Little uncertainty persists in UK

Growth was broad based across verticals except healthcare

business.

Healthcare still weak on account of HPS weakness while

core health of the business is good as per management

ICICI Securities Ltd | Retail Equity Research Page 5

Exhibit 3: Service line wise break-up

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q1FY19

Revenue by service lines (%)

Cloud Infrastructure Services 28.1 28.4 28.2 28.8 27.4 26.5

Data, Analytics & AI 7.1 7.1 7.0 7.0 7.1 7.8

Digital operations and Platforms 12.0 12.1 12.6 12.1 12.1 12.7

Industrial & Engineering Services 7.0 6.9 6.9 7.3 7.3 7.3

Modern Application Services 45.8 45.5 45.3 44.8 46.1 45.7

Growth QoQ (%)- Constant currency

Cloud Infrastructure Services 0.2 1.5 0.4 3.4 -4.6 2.6

Data, Analytics & AI 3.6 -1.3 -0.4 1.7 1.5 11.1

Digital operations and Platforms -1.6 1.7 4.7 -2.5 -0.6 6.2

Industrial & Engineering Services -1.8 1.2 -0.3 7.4 -1.1 1.9

Modern Application Services 0.6 -0.8 0.6 -0.3 3.3 1.0

Source: Company, ICICI Direct Research

Exhibit 4: Client & human resource metrics

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q1FY19

Client metrics

$1 mn Clients 624 627 635 631 624 612

$10 mn Clients 163 170 167 171 173 180

$50 mn Clients 36 39 41 39 40 39

$75 mn Clients 18 16 17 20 19 19

$100 mn Clients 9 9 9 8 8 9

Headcount, Utilization & Attrition

Closing employee count 166790 163759 162553 163827 164659 175346

Net Utilization (Excluding trainees) 82.1 82.5 81.9 83.4 85.2 85.5

Voluntary Attrition LTM 15.9 15.7 15.9 16.6 17.0 17.4

Source: Company, ICICI Direct Research

Growth was broad based among service lines.

Management indicated that pipeline looking strong for

cloud migration

Net utilisation (ex-trainees) expanded 30 bps QoQ to

85.5%, multi quarter high

In terms of client engagements, clients contributing

>$100 million category increased by one to 9

ICICI Securities Ltd | Retail Equity Research Page 6

Financial story in charts

Exhibit 5: Digital contribution trend

19.6

21.7 22.1 22.524.1

25.026.7

28.0

31.4

11.29.9

4.6

2.7

9.4

3.7

9.4

3.1

13.0

0.0

10.0

20.0

30.0

40.0

Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19

%

Digital as a % of revenue Growth, QoQ

Source: Company, ICICI Direct Research

Exhibit 6: Dollar revenues may grow at 4.9% CAGR in FY18-20E

70

82

73

46

19

31

19

16

19

03

19

55

20

62

20

27

20

41

82

63

88

61

77

04

19

71

20

14

20

13

80

60

7.6

5.8

1.4

2.5

7.27.0

3.7

4.6

3.5

3.94.9

2.15.1

5.5

4.6

2.8

1000

4000

7000

10000

FY

15

FY

16

Q1

FY

17

Q2

FY

17

Q3

FY

17

Q4

FY

17

FY

17

Q1

FY

18

Q2

FY

18

Q3

FY

18

Q4

FY

18

FY

18

Q1

FY

19

Q2

FY

19

FY

19

E

FY

20

E

$ m

illion

0

10

20

%

Dollar revenue Growth, YoY

[

Source: Company, ICICI Direct Research

Digital revenues now account for 31.4% of services

revenue (vs 24.1% in Q2FY18) and grew strongly by

13% sequentially and 32% YoY

ICICI Securities Ltd | Retail Equity Research Page 7

Exhibit 7: Barring one-off, IT services margin expanded 240 bps to 18%

22.1

20.5

17.8 17.818.3

17.617.9

16.817.3

14.814.4

15.8

17.5

14.4

16.8

17.7

12

15

18

21

24

FY

15

FY

16

Q1

FY

17

Q2

FY

17

Q3

FY

17

Q4

FY

17

FY

17

Q1

FY

18

Q2

FY

18

Q3

FY

18

Q4

FY

18

FY

18

Q1

FY

19

Q2

FY

19

FY

19

E

FY

20

E

%EBIT margin (IT services)

Source: Company, ICICI Direct Research

Exhibit 8: PAT may grow at 15.7% CAGR in FY18-20E

86538886

2052 2067 2168 2261

8490

2076 21911937 1803

8008

21211889

9088

10721

1000

4000

7000

10000

FY

15

FY

16

Q1

FY

17

Q2

FY

17

Q3

FY

17

Q4

FY

17

FY

17

Q1

FY

18

Q2

FY

18

Q3

FY

18

Q4

FY

18

FY

18

Q1

FY

19

Q2

FY

19

FY

19

E

FY

20

E

| c

rore

PAT

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 8

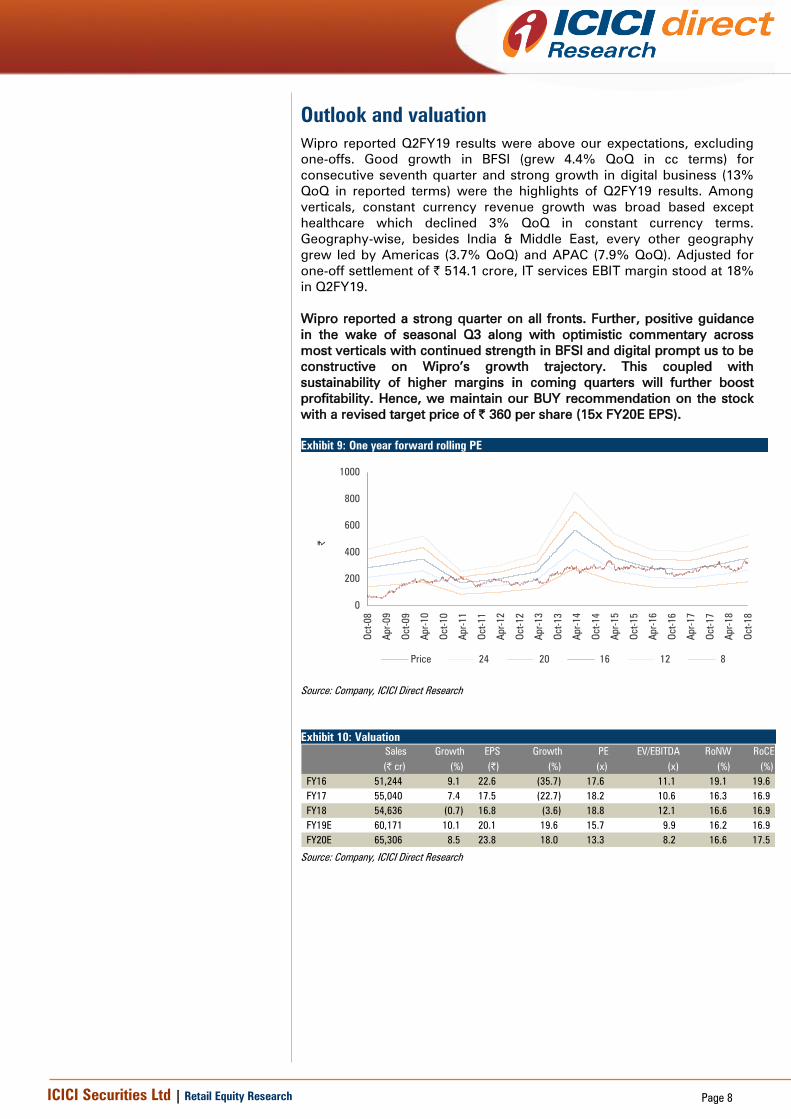

Outlook and valuation

Wipro reported Q2FY19 results were above our expectations, excluding

one-offs. Good growth in BFSI (grew 4.4% QoQ in cc terms) for

consecutive seventh quarter and strong growth in digital business (13%

QoQ in reported terms) were the highlights of Q2FY19 results. Among

verticals, constant currency revenue growth was broad based except

healthcare which declined 3% QoQ in constant currency terms.

Geography-wise, besides India & Middle East, every other geography

grew led by Americas (3.7% QoQ) and APAC (7.9% QoQ). Adjusted for

one-off settlement of | 514.1 crore, IT services EBIT margin stood at 18%

in Q2FY19.

Wipro reported a strong quarter on all fronts. Further, positive guidance

in the wake of seasonal Q3 along with optimistic commentary across

most verticals with continued strength in BFSI and digital prompt us to be

constructive on Wipro’s growth trajectory. This coupled with

sustainability of higher margins in coming quarters will further boost

profitability. Hence, we maintain our BUY recommendation on the stock

with a revised target price of | 360 per share (15x FY20E EPS).

Exhibit 9: One year forward rolling PE

0

200

400

600

800

1000

Oct-0

8

Ap

r-0

9

Oct-0

9

Ap

r-1

0

Oct-1

0

Ap

r-1

1

Oct-1

1

Ap

r-1

2

Oct-1

2

Ap

r-1

3

Oct-1

3

Ap

r-1

4

Oct-1

4

Ap

r-1

5

Oct-1

5

Ap

r-1

6

Oct-1

6

Ap

r-1

7

Oct-1

7

Ap

r-1

8

Oct-1

8

|

Price 24 20 16 12 8

Source: Company, ICICI Direct Research

Exhibit 10: Valuation

Sales Growth EPS Growth PE EV/EBITDA RoNW RoCE

(| cr) (%) (|) (%) (x) (x) (%) (%)

FY16 51,244 9.1 22.6 (35.7) 17.6 11.1 19.1 19.6

FY17 55,040 7.4 17.5 (22.7) 18.2 10.6 16.3 16.9

FY18 54,636 (0.7) 16.8 (3.6) 18.8 12.1 16.6 16.9

FY19E 60,171 10.1 20.1 19.6 15.7 9.9 16.2 16.9

FY20E 65,306 8.5 23.8 18.0 13.3 8.2 16.6 17.5

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 9

Recommendation History vs. Consensus

0

200

400

600

800

1,000

Oct-

18

Sep-

18

Jul-

18

Jun-

18

Apr-

18

Feb-

18

Jan-

18

Nov-

17

Oct-

17

Aug-

17

Jul-

17

May-

17

Apr-

17

Feb-

17

Jan-

17

Nov-

16

Sep-

16

Aug-

16

Jun-

16

May-

16

Mar-

16

Feb-

16

Dec-

15

Nov-

15

Sep-

15

(|

)

0.0

20.0

40.0

60.0

80.0

100.0

(%

)

Price Idirect target Consensus Target Mean % Consensus with SELL

Source: Bloomberg, Company, ICICI Direct Research

Key events

Date Event

Sep-17

Wipro wins a five year IT applications management contract from Outokumpu, global leader in stainless steel. Wipro would provide applications management services

for Outokumpu SAP landscape along with legacy applications support

Sep-17 Wipro bags a seven year contract from European energy company, innogy SE to manage the data centre and cloud services

Sep-17

Wipro enters into a partnership with CloudGenix, a leading provider of Software defined Wide Area Networking (SD-WAN) products. Under the partnership, Wipro

would offer its customers end to end managed WAN services.

Oct-17

Wipro Digital signs a definitive agreement to acquire Cooper, design and business strategy consultancy. Wipro Digital is the digital business unit of Wipro. Acquisition

is expected to be closed in Q3FY18.

Mar-18 Wipro announces it would pay $8.8 million for a 33% stake in application security company Denim Group, to boost its cybersecurity offerings to clients

Apr-18

Wipro sells 63% of its stake in Wipro Airport IT to Antariksh Softtech for a consideration of ₹ 3.15 crore. Wipro Airport IT Services is a joint venture between Wipro

(74%) and Delhi International Airport Limited (DIAL) (26%).

Jun-18

Wipro selected by Nokia to accelerate its supply chain digital transformation. Wipro would help design, digitalise and run Nokia's sales order management operations

from multiple centres, globally. Financial details of the deal were undisclosed

Aug-18

Wipro has entered into a settlement of the lawsuit filed by National Grid US for $75 million (~| 500 crore). The lawsuit was filed by National Grid US in 2017 seeking

damages amounting to US$ 140 million plus additional costs related to an ERP implementation project.

Aug-18

Wipro has been awarded a multi-year business process services contract from Denmark based Falck, a leading international supplier of ambulance services, employee

health care and roadside assistance. Falck is active in 35 countries and has over 37,000 employees. As part of the contract, Wipro will help transform Falck’s finance

operations through its enterprise operations transformation model

Source: Company, ICICI Direct Research

Top 10 Shareholders Shareholding Pattern

Rank Name Latest Filing Date % O/S Position (m) Change (m)

1 Premji (Azim Hasham) 30-Jun-18 60.5% 2,722.8 0.0

2 Azim Premji Trust 30-Jun-18 13.7% 618.5 0.0

3 Life Insurance Corporation of India 30-Jun-18 3.1% 138.7 0.0

4 ICICI Prudential Asset Management Co. Ltd. 30-Jun-18 2.0% 90.0 7.6

5 Stewart Investors 20-Dec-17 1.3% 57.8 -4.0

6 BlackRock Institutional Trust Company, N.A. 30-Sep-18 0.9% 42.0 0.8

7 The Vanguard Group, Inc. 30-Sep-18 0.5% 24.1 -0.1

8 Norges Bank Investment Management (NBIM) 31-Dec-17 0.4% 19.5 4.2

9 Dimensional Fund Advisors, L.P. 30-Sep-18 0.4% 17.7 0.0

10 SBI Funds Management Pvt. Ltd. 30-Sep-18 0.4% 16.4 -0.9

(in %) Mar-18 Jun-18 Sep-18

Promoter 74.32 74.31 74.31

Public 25.17 25.19 25.21

Others 0.51 0.49 0.48

Total 100.00 100.00 100.00

Source: Reuters, ICICI Direct Research

Recent Activity

Investor name Value Shares Investor name Value Shares

ICICI Prudential Asset Management Co. Ltd. 28.9m 7.6m T. Rowe Price International (UK) Ltd. -41.1m -9.2m

Mirae Asset Global Investments (India) Pvt. Ltd. 7.4m 1.7m T. Rowe Price Hong Kong Limited -20.8m -4.7m

Reliance Nippon Life Asset Management Limited 5.9m 1.3m Kotak Mahindra Asset Management Company Ltd. -11.7m -2.8m

UTI Asset Management Co. Ltd. 4.7m 1.0m SBI Funds Management Pvt. Ltd. -4.2m -0.9m

BlackRock Institutional Trust Company, N.A. 3.6m 0.8m IDFC Asset Management Company Private Limited -3.9m -0.9m

Buys Sells

Source: Reuters, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 10

.

Financial summary

Profit and loss statement | Crore

FY17 FY18 FY19E FY20E

Total Revenues 55,040 54,636 60,171 65,306

Growth (%) 7.4 (0.7) 10.1 8.5

COGS 39,154 38,558 41,738 45,305

Other Expenditure 5,214 5,537 6,703 6,672

EBITDA 11,458 10,542 11,763 13,361

Growth (%) 2.6 (8.0) 11.6 13.6

Depreciation 2,070 2,112 1,805 1,959

Other Income 2,242 2,400 2,294 2,941

Exchange difference 28 - - -

Net interest expense (594) (583) (636) (636)

Pft. from associates - 1 (3) (3)

PBT 11,036 10,247 11,613 13,704

Growth (%) (3.8) (7.1) 13.3 18.0

Tax 2,521 2,239 2,555 3,015

PAT before Minority int, 8,514 8,008 9,058 10,689

Minority int. 25 0 (30) (32)

PAT 8,490 8,008 9,088 10,721

EPS 17.5 16.8 20.1 23.8

EPS (Growth %) (22.7) (3.6) 19.6 18.0

Source: Company, ICICI Direct Research

Cash flow statement | Crore

FY17 FY18 FY19E FY20E

PAT before minority int. 8,514 8,008 9,058 10,689

Depreciation 2,311 2,112 1,805 1,959

(inc)/dec in Current Assets 1,269 (717) 688 (1,802)

(inc)/dec in current Liabilities (815) 623 1,500 1,900

Taxes paid (2,548) (2,811) (2,555) (3,015)

CF from operations 9,277 8,423 11,396 10,445

Other Investments (10,014) 5,628 2,294 5,234

(Purchase)/Sale of Fixed Assets (1,965) (2,070) 85 (2,482)

CF from investing Activities (11,628) 3,558 2,379 459

Inc / (Dec) in Equity Capital - 2 - -

Inc / (Dec) in sec.loan Funds 1,312 (1,098) - -

Dividend & Divendend tax (1,073) (854) (1,999) (4,779)

CF from Financial Activities (2,275) (12,998) (1,999) (2,780)

Exchange rate differences (141) 38 - -

Opening cash balance 9,905 5,271 4,493 16,268

Closing cash 5,271 4,493 16,268 24,392

Source: Company, ICICI Direct Research

Balance sheet | Crore

FY17 FY18 FY19E FY20E

Liabilities

Equity 486 905 905 905

Reserves & Surplus 51,544 47,389 55,114 63,690

Networth 52,030 48,294 56,019 64,595

Minority Interest 239 241 211 179

Debt - long term 1,961 4,527 4,527 4,527

Debt - short term 12,280 9,299 10,269 11,146

Deffered Tax Liability 661 306 306 306

Other liabilities & provisions 1,505 1,346 1,354 1,354

Source of funds 68,677 64,012 72,686 82,107

Assets

Goodwill 12,580 11,758 11,758 11,758

Intangible Assets 1,592 1,811 1,679 1,716

PPE 6,979 6,444 4,687 5,172

O.non current assets 3,201 4,102 4,102 4,102

Investments 710 887 884 881

Debtors 9,884 10,544 11,547 12,608

Cash & Cash equivalents 5,271 4,493 16,268 24,392

Investments - short term 30,178 25,033 25,033 25,033

O.current assets 8,957 10,992 9,300 10,041

Trade Payable 6,549 6,813 7,595 8,293

OCL & Provisions 4,126 5,239 4,978 5,303

Application of funds 68,677 64,012 72,686 82,107

Source: Company, ICICI Direct Research

Key ratios

FY17 FY18 FY19E FY20E

Per share data (|)

EPS 17.5 16.8 20.1 23.8

BV 107.0 101.5 124.1 143.1

DPS 2.0 2.0 2.0 2.0

Operating Ratios

EBIT Margin 17.1 15.4 16.5 17.5

PAT Margin 15.4 14.7 15.1 16.4

Debtor days 66 70 70 70

Creditor days 43 46 46 46

Return Ratios (%)

RoE 16.3 16.6 16.2 16.6

RoCE 16.9 16.9 16.9 17.5

RoIC 28.3 24.4 31.7 34.9

Valuation Ratios (x)

P/E 18.2 18.8 15.7 13.3

EV / EBITDA 10.6 12.1 9.9 8.2

EV / Net Sales 2.2 2.3 1.9 1.7

Market Cap / Sales 2.6 2.6 2.4 2.2

Price to Book Value 2.9 3.1 2.5 2.2

Solvency Ratios

Debt/EBITDA 1.2 1.3 1.3 1.2

Debt / Equity 0.3 0.3 0.3 0.2

Current Ratio 1.8 1.8 1.7 1.7

Quick Ratio 1.8 1.8 1.7 1.7

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 11

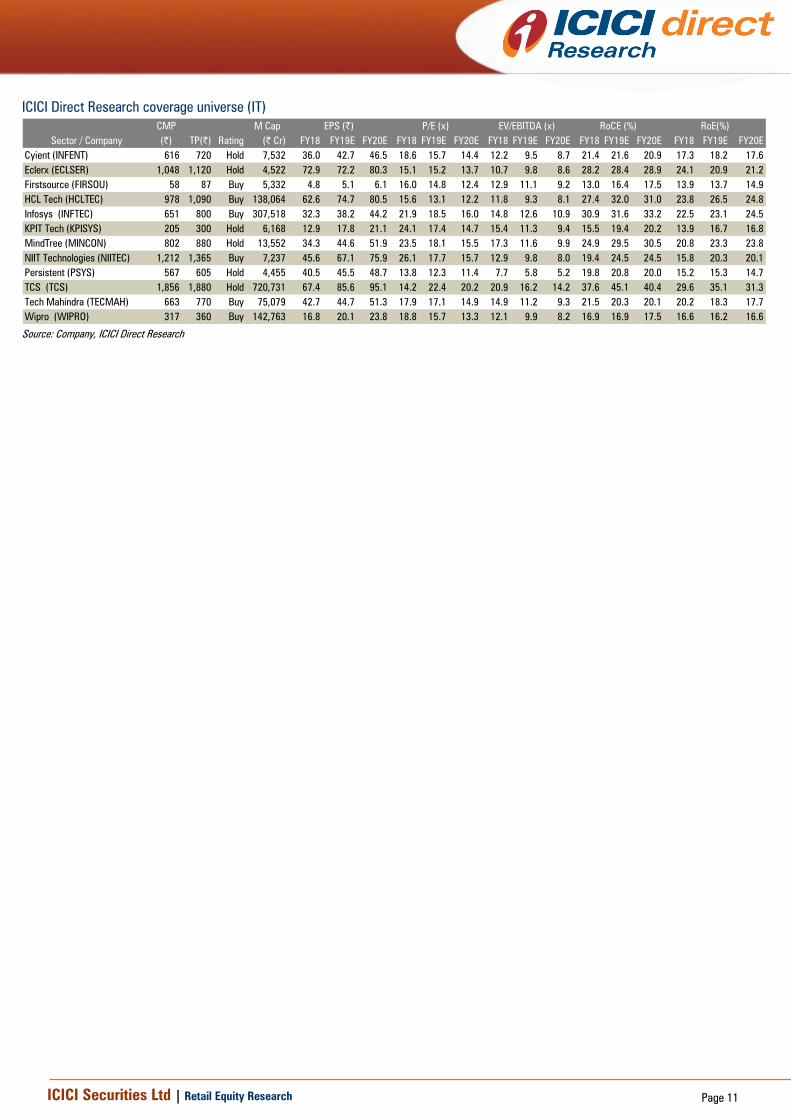

ICICI Direct Research coverage universe (IT)

CMP M Cap

(|) TP(|) Rating (| Cr) FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E

Cyient (INFENT) 616 720 Hold 7,532 36.0 42.7 46.5 18.6 15.7 14.4 12.2 9.5 8.7 21.4 21.6 20.9 17.3 18.2 17.6

Eclerx (ECLSER) 1,048 1,120 Hold 4,522 72.9 72.2 80.3 15.1 15.2 13.7 10.7 9.8 8.6 28.2 28.4 28.9 24.1 20.9 21.2

Firstsource (FIRSOU) 58 87 Buy 5,332 4.8 5.1 6.1 16.0 14.8 12.4 12.9 11.1 9.2 13.0 16.4 17.5 13.9 13.7 14.9

HCL Tech (HCLTEC) 978 1,090 Buy 138,064 62.6 74.7 80.5 15.6 13.1 12.2 11.8 9.3 8.1 27.4 32.0 31.0 23.8 26.5 24.8

Infosys (INFTEC) 651 800 Buy 307,518 32.3 38.2 44.2 21.9 18.5 16.0 14.8 12.6 10.9 30.9 31.6 33.2 22.5 23.1 24.5

KPIT Tech (KPISYS) 205 300 Hold 6,168 12.9 17.8 21.1 24.1 17.4 14.7 15.4 11.3 9.4 15.5 19.4 20.2 13.9 16.7 16.8

MindTree (MINCON) 802 880 Hold 13,552 34.3 44.6 51.9 23.5 18.1 15.5 17.3 11.6 9.9 24.9 29.5 30.5 20.8 23.3 23.8

NIIT Technologies (NIITEC) 1,212 1,365 Buy 7,237 45.6 67.1 75.9 26.1 17.7 15.7 12.9 9.8 8.0 19.4 24.5 24.5 15.8 20.3 20.1

Persistent (PSYS) 567 605 Hold 4,455 40.5 45.5 48.7 13.8 12.3 11.4 7.7 5.8 5.2 19.8 20.8 20.0 15.2 15.3 14.7

TCS (TCS) 1,856 1,880 Hold 720,731 67.4 85.6 95.1 14.2 22.4 20.2 20.9 16.2 14.2 37.6 45.1 40.4 29.6 35.1 31.3

Tech Mahindra (TECMAH) 663 770 Buy 75,079 42.7 44.7 51.3 17.9 17.1 14.9 14.9 11.2 9.3 21.5 20.3 20.1 20.2 18.3 17.7

Wipro (WIPRO) 317 360 Buy 142,763 16.8 20.1 23.8 18.8 15.7 13.3 12.1 9.9 8.2 16.9 16.9 17.5 16.6 16.2 16.6

EV/EBITDA (x)P/E (x)

Sector / Company

RoE(%)RoCE (%)EPS (|)

Source: Company, ICICI Direct Research

ICICI Securities Ltd | Retail Equity Research Page 12

RATING RATIONALE

ICICI Direct Research endeavours to provide objective opinions and recommendations. ICICI Direct Research

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and

the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 13

ANALYST CERTIFICATION

We /I, Devang Bhatt, PGDBM, Deepti Tayal, MBA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect

our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities Limited Sebi Registration is INZ000183631 for stock broker. ICICI Securities is a wholly-owned

subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture

capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Devang Bhatt, PGDBM, Deepti Tayal, MBA, Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve

months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Devang Bhatt, PGDBM, Deepti Tayal, MBA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.