winter past, winter future role of lng in new england prepared for: new hampshire energy summit...

TRANSCRIPT

Winter Past, Winter Future Role of LNG in New England

Prepared for:

New Hampshire Energy Summit

Concord, NH

October 5, 2015

1

Joe DaltonDirector, Government AffairsGDF SUEZ Gas North America, Inc.

GDF SUEZ ENERGY INTERNATIONAL - OVERVIEW – SEPTEMBER 2013

GDF SUEZ - Overview

GDF SUEZ is a Global LNG portfolio player 3rd largest importer of LNG in the world

Involved in Liquefaction in the USA

Global portfolio of LNG supply

Operate 17 LNG carriers including 2 SRV’s

No. 1 Independent Power Producer in the world

13,000 MW USA

115.3 GW Worldwide

22

3

Think Energy began serving MAresidential customers in early 2015.

4

The Everett LNG Import Terminal is the longest-operating in the U.S., and the only continuously operating one.

Opened in 1971 as a peak shaving facility to help meet New England’s relatively small natural gas demand.

Today it is an essential part of the region’s energy supply mix.

Trucking capacity: 100 million cubic feet/day

Vaporization capacity: 715 million cubic feet/day – sustainable 435 million cubic feet/day – Non-Mystic

(Algonquin, Tennessee, LDCs) 1 billion cubic feet/day – maximum installed

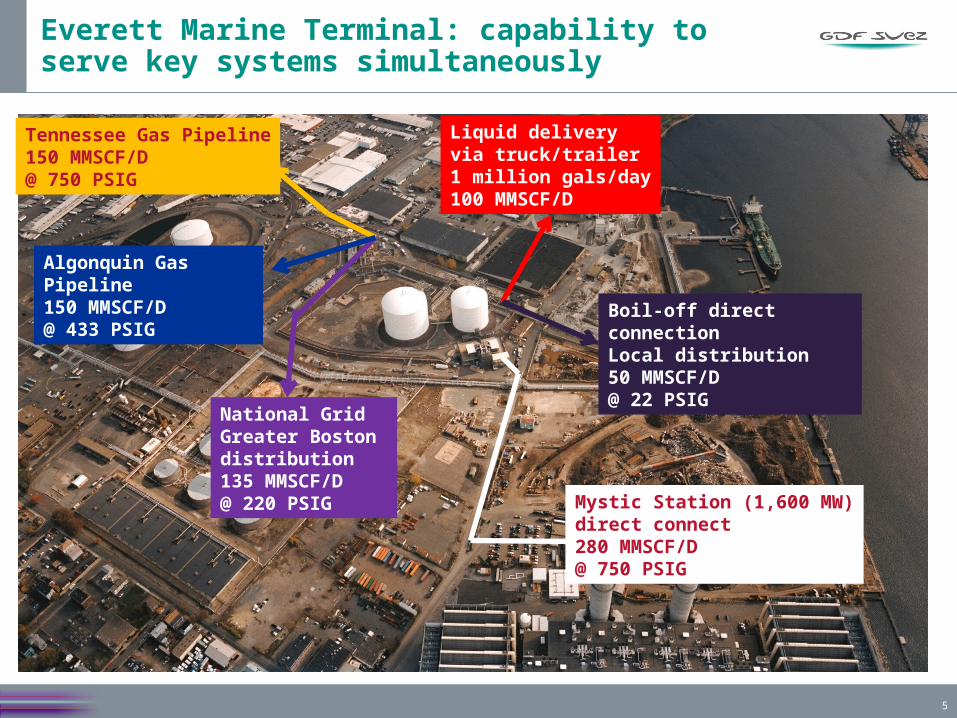

The Everett LNG Import Terminal

5

Everett Marine Terminal: capability to serve key systems simultaneously

Liquid deliveryvia truck/trailer1 million gals/day100 MMSCF/D

Mystic Station (1,600 MW)direct connect280 MMSCF/D@ 750 PSIG

Boil-off direct connectionLocal distribution50 MMSCF/D@ 22 PSIG

National GridGreater Boston distribution135 MMSCF/D@ 220 PSIG

Tennessee Gas Pipeline150 MMSCF/D@ 750 PSIG

Algonquin Gas Pipeline150 MMSCF/D@ 433 PSIG

The Everett Terminal directly connects into:

Algonquin PipelineTennessee Gas Pipeline

National Grid local distribution systemMystic Power Station

The Everett Terminal supplies LNG via truck to nearly all of the 46 customer-owned LNG storage tanks in region. (LNG is how natural gas is stored in New England.) Today, LNG from Everett and these facilities can meet as much 40% of the natural gas demand on peak days. Total LNG storage in New England is 20 Bcf.

Importance of LNG in Greater Boston & New England

Winter 14/15

7

Source: ISO-NE presentation, March 4, 2015, **excludes approx. 5 Bcf/d to Mystic & LDCs

Winter 14/15 - continued

8

Source: SNL, “In New England power market, small changes lead to big price differences,” by Mark Hand, March 2, 2015

Total Distrigas sendout up from 9.3 Bcf/d in Jan/Feb 2014 to 15.6 Bcf/d in Jan/Feb 2015

67% increase

According to ISO-NE COO ReportsDec 14 – Feb 15 costs compared

to Dec 13 – Feb 14

Down over $2 BILLION

GDF SUEZ ENERGY INTERNATIONAL - OVERVIEW – SEPTEMBER 2013

Recent Report on Winter Alternatives

9

GDF SUEZ ENERGY INTERNATIONAL - OVERVIEW – SEPTEMBER 2013

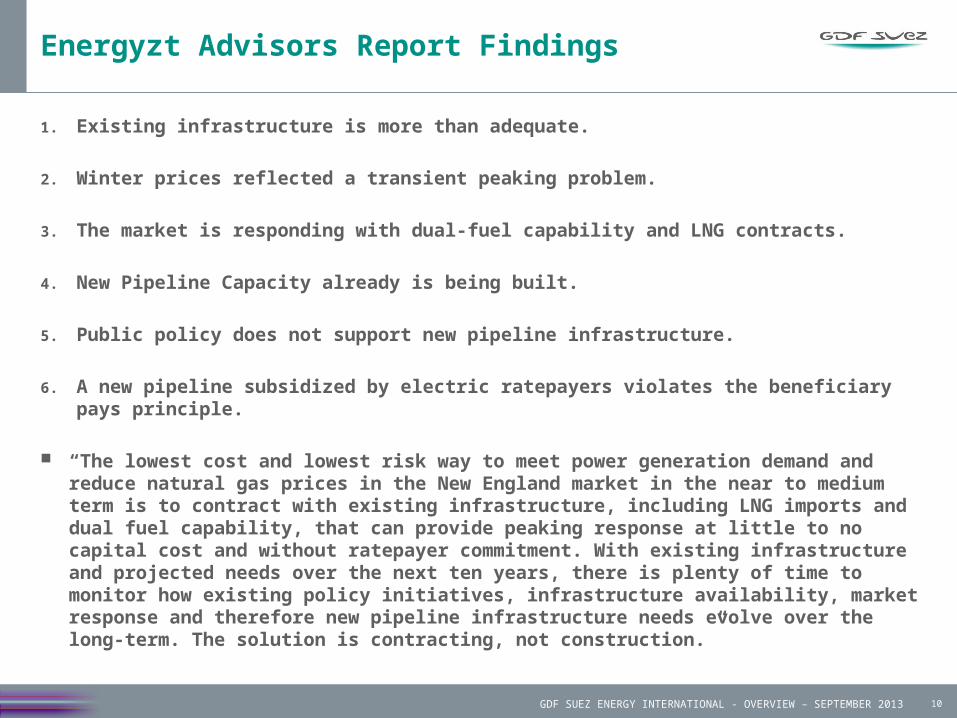

Energyzt Advisors Report Findings

1. Existing infrastructure is more than adequate.

2. Winter prices reflected a transient peaking problem.

3. The market is responding with dual-fuel capability and LNG contracts.

4. New Pipeline Capacity already is being built.

5. Public policy does not support new pipeline infrastructure.

6. A new pipeline subsidized by electric ratepayers violates the beneficiary pays principle.

“The lowest cost and lowest risk way to meet power generation demand and reduce natural gas prices in the New England market in the near to medium term is to contract with existing infrastructure, including LNG imports and dual fuel capability, that can provide peaking response at little to no capital cost and without ratepayer commitment. With existing infrastructure and projected needs over the next ten years, there is plenty of time to monitor how existing policy initiatives, infrastructure availability, market response and therefore new pipeline infrastructure needs evolve over the long-term. The solution is contracting, not construction.”

10