willie de beer - esi-africa.com | africa's leading portal for ... de beer.pdfafrican utility...

TRANSCRIPT

African Utility Week 2008, Cape Town, South Africa

Title of presentationDr Willie de Beer

Chief Operations Officer

EDI Holdings

African Utility Week 2008, Cape Town, South Africa

Are the REDs Dead?

African Utility Week 2008, Cape Town, South Africa

• Current Electricity Supply Industry Structure

• Current Situation

• Supply / Demand : In Balance or In Crises?

• Current Electricity Situation from an EDI Perspective

• EDI Maintenance Perspective

• Municipal Case Study : Maintenance and

Refurbishment Requirement

• EDI Maintenance and Refurbishment Requirement

• Technical and Non-Technical Losses

• Conclusion

Presentation Outline

African Utility Week 2008, Cape Town, South Africa

Electricity Supply Chain

Transmission LinesPOWER STATIONS

GENERATION

TRANSMISSION (765/400/275

kV)

TRANSMISSION SUBSTATION

DISTRIBUTION (132/88/66/44/33 kV)

Reticulation HV Lines 22 and 11kV

Reticulation Lines

DISTRIBUTION SUBSTATION

Distribution Lines

ReticulationLV Lines 380/220V

SERVICE CONNECTION

ELECTRICITY DISTRIBUTION INDUSTRY (EDI) FOCUS

African Utility Week 2008, Cape Town, South Africa

• Capacity Shortage

• Longer Term Problem

• Planning reserve margin currently 8–10% against 15%

aspiration (limited opportunity for maintenance)

• A number of generation units are in ‘mid-life’, thus requiring

major planned maintenance and refurbishment

• Current constraints

• Unplanned outages higher than usual

• Generator output reductions (coal quality, handling &

stockpiles)

Source: Eskom

Current situation (…1)

African Utility Week 2008, Cape Town, South Africa

• Plant performance impacted by higher load factor• Immediate Power System Security Problem• Vulnerability increased to unacceptable level – Thursday,

24 January 2008• The highest continuous load shedding of 4000 MW was

required and this compromised system protection• High load shedding due to current constraints• Coal handling problems would continue and possibly

increase with rain forecasts• Customers informed of vulnerability of system and

requested to make their processes safeSource: Eskom

Current situation (…2)

African Utility Week 2008, Cape Town, South Africa

• Current Realities• New build programme delayed• Generation assets stressed (time constraints for

maintenance)• Capacity shortages (under-frequency events,

interruptibility and load-shedding, etc)• Energy shortages more evident• Customers unhappy with industrial customers

(because of interruptibility arrangements)• Stronger economic growth (pressure for increased

supply)• Situation expected to deteriorate over next 8 years

Source: Eskom

Slide 7

Supply/Demand: In balance or In crises

African Utility Week 2008, Cape Town, South Africa

• The electricity distribution industry (EDI) is part of a broader

ESI value chain

• Challenges experienced in generations filter through to

distribution

• Current load-shedding

• These generation capacity problems will disguise

distribution challenges for some time to come

• Every ‘lights off’ moment will most likely be interpreted as

load shedding whilst it could as well be a distribution issue

Current electricity situation from an EDI perspective (…1)

African Utility Week 2008, Cape Town, South Africa

• In 5-7 years time major generation challenges will be

overcome and distribution will be exposed if nothing

happens now:

• Fragmentation and absence of economies of scale

• Maintenance backlogs

• Significant variance in tariff structure

• Inconsistent electrification performance

Current electricity situation from an EDI perspective (…2)

African Utility Week 2008, Cape Town, South Africa

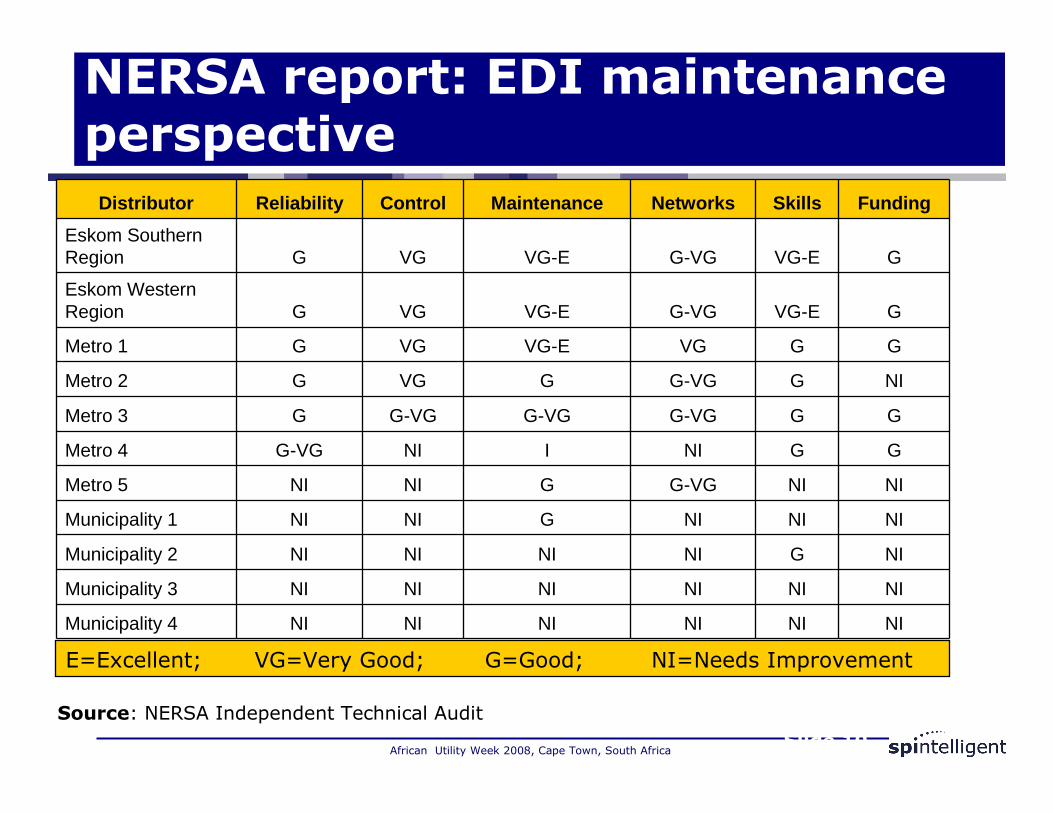

Source: NERSA Independent Technical Audit

E=Excellent; VG=Very Good; G=Good; NI=Needs Improvement

Distributor Reliability Control Maintenance Networks Skills Funding

Eskom Southern Region G VG VG-E G-VG VG-E G

Eskom Western Region G VG VG-E G-VG VG-E G

Metro 1 G VG VG-E VG G G

Metro 2 G VG G G-VG G NI

Metro 3 G G-VG G-VG G-VG G G

Metro 4 G-VG NI I NI G G

Metro 5 NI NI G G-VG NI NI

Municipality 1 NI NI G NI NI NI

Municipality 2 NI NI NI NI G NI

Municipality 3 NI NI NI NI NI NI

Municipality 4 NI NI NI NI NI NI

Slide 10

NERSA report: EDI maintenance perspective

African Utility Week 2008, Cape Town, South AfricaSlide 11

Municipal case study

African Utility Week 2008, Cape Town, South Africa

• The information is based on 2003/2004 as a base year• The combined red and blue bar indicates the total

refurbishment investment backlog• The red bar indicates the current funding allocation • The blue bar reflects the balance of the backlog still to be

addressed• The graph therefore indicates that:• Base year and projected investment suggests an under-investment in

addressing the refurbishment requirement• While it is acknowledged that the ability of the entity to generate revenue

is critical to support financial expenditure, consideration must be given to increase the refurbishment investment

• At the current rate of refurbishment investment, the current entity will not wipe out the current refurbishment backlog in the next 10 years

Municipal case study: narrative

African Utility Week 2008, Cape Town, South Africa

Municipal case study

African Utility Week 2008, Cape Town, South Africa

• The information is based on 2003/2004 as a base year

• The blue bar reflects the total maintenance and

refurbishment requirement per annum for the entity

• The red bar reflects the current maintenance and

refurbishment allocation

• The green bar reflects therefore the additional combined

maintenance and refurbishment requirement18 April 2008

Slide 14

Municipal case study: narrative

African Utility Week 2008, Cape Town, South Africa

• The graph clearly illustrates that the combined maintenance and refurbishment requirement is underfunded, which will results in an increase in maintenance and refurbishment backlog, which will filter through into the network reliability and performance

• The underfunding of the maintenance and refurbishment will result in a further increase in the plant deterioration

• Amongst a number of conclusions that can be derived from the above graph, the most critical one is that the current excessive switching of plant due to load shedding will create an accelerated deterioration of the plant status since it is notmaintained at the desired level.

18 April 2008

Slide 15

Municipal case study: narrative

African Utility Week 2008, Cape Town, South Africa

EDI refurbishment requirement

African Utility Week 2008, Cape Town, South Africa

• The information is based on 2003/2004 as a base year• The combined red and blue bar indicates the total

refurbishment investment backlog for the industry• The red bar indicates the current funding allocation • The blue bar then reflects the balance of the backlog still to

be addressed• The graph therefore indicates that:

• Base year and projected investment suggests an under-investment in addressing the refurbishment requirement

• At the current rate of refurbishment investment, the industry will not wipe out the current refurbishment backlog in the next 10 years

EDI refurbishment requirement: narrative

African Utility Week 2008, Cape Town, South AfricaSlide 18

EDI combined maintenance and refurbishment requirement

African Utility Week 2008, Cape Town, South Africa

• The information is based on 2003/2004 as a base year

• The dark blue bar reflects the current projected investment

• The red bar reflects the required combined refurbishment

and maintenance requirement

• The green bar reflects the total additional requirement

excluding the current investment

• The purple, light blue and orange is a breakdown of the

combined maintenance and refurbishment requirement as

reflected in the green bar

EDI combined maintenance and refurbishment requirement

African Utility Week 2008, Cape Town, South Africa

In addition to the lack of investment in generating capacity, the South African electricity distribution network is (according to industry experts) also in a state of critical under-investment. Eskom is responsible for 95% of generation and 100% of transmission. Distribution, however, is owned about 50-50 between Eskom itself and the “munics” (municipality-owned distribution companies). As a rule of thumb, distribution companies should be investing at a rate of about 10% of asset value per year. However, for a number of reasons beyond the scope of this report, investment rates in many (especially non-Eskom) distribution companies are as low as 1-2% per year. Thus, while much of the focus has been on generating capacity, a major threat to efficient energy supply is distribution.

UBS investment research –March 2008

African Utility Week 2008, Cape Town, South AfricaSlide 21

Technical and non-technical losses per RED

African Utility Week 2008, Cape Town, South Africa

• Losses in a utility are categorised into technical and non-technical losses.

• Technical losses: Network related losses associated with the flow of current through the conductors

• Non-technical losses: Losses normally associated with administrative processes, non-payment, incorrect billing, energy theft e.g. meter tampering

• The norm based on international research, suggest that 7% combined technical and non-technical losses is achievable

• Based on the high losses experienced in the SA industry and considering the international trends, it is regarded as realistic to do an improvement of 2% per annum

• Based on the above, the graph suggests an improvement plan over a 5 year period which will bring each of the REDs within the recommended norm of 7%

Technical and non-technical losses per RED: narrative

African Utility Week 2008, Cape Town, South Africa

Assumptions:

1.Losses are reduced from 16.64% average to a norm of 7%.2.Total Potential Savings = 6,842 GWh

Source: EDI Holdings Industry Model based on 2003/2004 figures

POTENTIAL SAVINGS GWh

Base Year Yr 1 Yr 2 Yr 3 Yr 4

Loss 11,970 10,340 8,711 7,081 6,022Potential Savings 1,629 1,629 1,629 1,059 896

Potential savings in GWh

African Utility Week 2008, Cape Town, South Africa

• Technical Losses

• Network configuration - strengthening

• Power Factor Correction

• Load balancing

• Effective maintenance

• Load flow and network capacity management

• Typical constraints:

• Large investment required

• System constraints

Slide 24

Typical strategies to reduce losses

African Utility Week 2008, Cape Town, South Africa

• Non-Technical Losses

• Metering Error Management

• Metering Audits

• Electricity theft management

• Sales report management

• Inspections

• Investment in technology, e.g. split metering

• Billing process and system improvement

• Credit control management

Typical strategies to reduce losses

African Utility Week 2008, Cape Town, South Africa

RED 1

RED 4

RED 2

RED 3

RED 6

RED 5

Provincial Boundaries

Cape Town Metro Nelson Mandela

Bay Metro

eThekwini Metro

Ekurhuleni Metro

City of Tshwane MetroCity of

Johannesburg Metro

6 wall-to-wall REDs

African Utility Week 2008, Cape Town, South Africa

CREATING SHAREHOLDERAND CUSTOMER VALUE

EFFIENCY AND CONTINIOUS BUSINESS IMPROVEMENT

REVENUE

OPERATING & CAPITAL EXPENDITURE

RED FINANCIALRED FINANCIAL

SUSTAINABILITYSUSTAINABILITY

Business model: RED sustainability

African Utility Week 2008, Cape Town, South Africa

• Promote RED sustainability

• Balance between revenue realisation and continuous

business efficiency improvement

• Close to the customer

• Decentralised focus

• Effective shareholder and stakeholder management

• Focus on, interalia:

• Technical losses

• Non-technical losses

• Effective asset management

• Staff development and skills retention

Business model: Brief summary

African Utility Week 2008, Cape Town, South Africa

• Service Provider to Service Authority (Municipalities)

• SDA as contemplated in MSA 2000 Section 81

• Distinct wires and retail focus

• Pursue appropriate best practices

• Benchmarking

• Integrated inter RED network management approach:

• Managing distribution grid integrity

• Enhance customer interface opportunities

Business model: Brief summary

African Utility Week 2008, Cape Town, South Africa

EDI Holdings Direct & Oversee EDI Restructuring

EDI Holdings Direct & Oversee EDI Restructuring

REDs x 6REDs x 6

Wires

RetailRetailShared ServicesShared Services

Industry AssociationIndustry Association

EDI interim state

African Utility Week 2008, Cape Town, South Africa

EDI Holdings Direct & Oversee EDI Restructuring

EDI Holdings Direct & Oversee EDI Restructuring

REDs x 6REDs x 6

Wires

Retail Companies x n

Retail Companies x n

Shared ServicesShared Services

Industry AssociationIndustry Association

Potential EDI future state

African Utility Week 2008, Cape Town, South Africa

2003 to 2004 2005 to 2006 2007 to Date

o EDI Holdings establishedo Eskom Distribution ringfenced

within Eskom Holdingso Boundaries for the six REDs

definedo Eskom and SALGA signed the

accession to the co-operative agreement

o EDI Holdings developed various tools to reduce cost and to facilitate the restructuring process

o Eskom Distribution (7 Regions) aligned with the boundaries of the six REDs

o RED project governance structures implemented

o Transitional Labour Relation Structure (TLRS) established

o Metros and numerous municipalities started the MSA Sect 78 process and business ringfencing

o NERSA approved (April 2006) through the MYPD R1.2bn over a 3 year period to assist in funding some of the EDI restructuring costs

o 25th October 2006 Cabinet reconfirmed support to the creation of six wall to wall REDs as Public Entities

o RED 1 was established (June 2005)as a Municipal Entity wholly owned by the City of Cape Town & liquidated by City of Cape Town during 2007

o Municipal electricity business asset transfer enabling mechanism approved by National Treasury

o Eskom Distribution 95% ringfenced

o Boundary energy metering installed as per the six RED footprint

o 120 Municipalities (ITD) signed the accession to the co-operative agreement

o 3 Metro’s & 13 municipalities completed Section 78 process

o 4 Metro’s & 13 municipalities ringfenced

o All Six RED establishment governance structures and stakeholder engagement structures established and operational

o Extensive progress towards a system solution for the future REDs

o Funding and support mechanisms in place to support readiness activities

Progress towards sustainable REDs

African Utility Week 2008, Cape Town, South Africa

Conclusion

• Never before has the environment for the establishment of

the REDs looked so promising

• The constraints that were protracting the process are well on

their way to being resolved

• The immediate focus for 2008/9 financial year will be:

• Finalising the implementation strategy

• Concluding the Deal (both design and negotiation)

• Advocating for the EDI restructuring enabling legislation and

policies to ensure rapid implementation;

• Development of a systems solutions for the industry;

Conclusion

African Utility Week 2008, Cape Town, South Africa

Conclusion

• Enhancing current asset owner readiness to transfer to the REDs

• Continued stakeholder engagement to ensure that the restructuring process is accelerated

• The current electricity challenges calls for an integrated and holistic approach to the solution from all industry players, business and citizens of this country

• A restructured Electricity Distribution Industry can only contribute to a sustainable industry:

• Support the economic growth required• Create investor confidence• Meet customer expectations

Conclusion