why do preparers participate in the development of the

TRANSCRIPT

ElsaWachtmeister MartinStrömland BUSN69

1

WhydopreparersparticipateinthedevelopmentoftheaccountingstandardIFRS15?

-Astudyontheaspectsofregion,industry,opinionandargumentation

Authors:

ElsaWachtmeister

MartinStrömland

BUSN69

Supervisor: June2016

KristinaArtsberg MScinAccountingandAuditing

ElsaWachtmeister MartinStrömland BUSN69

2

AbstractTitle WhydopreparersparticipateinthedevelopmentoftheaccountingstandardIFRS15?

–Astudyontheaspectsofregion,industry,opinionandargumentation

SeminarDate 2016-06-01

Course BUSN69DegreeProject–AccountingandAuditing,15ECTScredits

Authors ElsaWachtmeisterMartinStrömland

Supervisor KristinaArtsberg

Keywords IFRS 15, preparer lobbying, due process influence, accounting economic theory,sociologicaltheory

Purpose The aim of this study is to identify to what extent different preparers vary inparticipation among industries and regions and further examine what types ofargumentation that is being used. The purpose is to improve and broaden theunderstandingofwhypreparerschoosetoparticipateinthedueprocessandhowthisrelatestopreviousresearchwiththeintentiontoprovidecontributiontotheresearchlandscape.

Method Aquantitativeresearchstrategywithadeductiveapproachwasapplied.Toexaminethecommentletters,thecontentanalysismethodwasused.Inaddition,statisticalX2-testswasconducted.

Theoreticalperspective Thetheoreticalframeworkwasbasedoneconomictheoryandsociologicaltheoryin

order to identify thepreparers arguments. In addition, previous researchhasbeentakenintoconsiderationwhendiscussingtheresults.

Empiricalfoundation Allof thecomment letters sent frompreparerson thediscussionpaperof thedue

processofIFRS15constitutetheempiricalfoundation.Conclusion Thestudyshowedthattherewerenosignificantdifferencesinopinionwhetherthe

regions or industries agree with one single revenue recognition standard IFRS 15.Furthermore, there were no significant differences between the argumentationamong regions. However, there were significant differences in the use ofargumentationamong the industries. Ingeneral,allof the industrieshadapositiveapproach towards the introduction of one single revenue recognition standard.Regarding the argumentation, the objections of some industries were morecategorised as economic thanothers. Those industries thatwere themost evidentwerethetechnologyandthetelecomindustries.Theindustriesthatarguedmoreinsociologicaltermswerethefinancialindustryaswellasindustrials&transport.

ElsaWachtmeister MartinStrömland BUSN69

3

Acknowledgements

WewouldliketoexpressourgreatestgratitudetooursupervisorKristinaArtsbergforherdevotedguidanceandsupportthroughoutthethesisdevelopmentprocess.WewouldalsoliketoshowourappreciationtoLarsWahlgrenforprovidingassistanceinstatisticalissues.

________________________ ________________________

ElsaWachtmeister MartinStrömland

Lund–June2016

ElsaWachtmeister MartinStrömland BUSN69

4

Tableofcontents1Introduction................................................................................................................................6

1.1Background..................................................................................................................................61.2Problemformulation....................................................................................................................7

1.2.1Researchquestions...............................................................................................................91.2.2Researchhypotheses............................................................................................................91.2.2Purpose...............................................................................................................................10

2Theoreticalframework..............................................................................................................112.1Innovativeprocess(Hussein,1981)............................................................................................112.2Aspectsspecifictotheinnovation(Kelly-Newton,1980)...........................................................11

2.2.1Relativeadvantage.............................................................................................................122.2.2Compatibilitywithnorms...................................................................................................122.2.3Complexityinuse...............................................................................................................122.2.4Trialabilityofthechange....................................................................................................122.2.5Observabilityofperceivedbenefits....................................................................................12

2.3Sociologicalman(Davisetal.,1997).........................................................................................132.4Economicman(Davisetal.,1997).............................................................................................13

2.4.1Positiveaccountingtheory(Watts&Zimmerman(1978,1979&1990)............................142.5Theoreticalframeworksummary...............................................................................................14

3Institutionalcontext..................................................................................................................153.1FinancialAccountingStandardsBoard–FASB...........................................................................153.2InternationalAccountingStandardsBoard–IASB.....................................................................153.3IFRS15........................................................................................................................................153.4ThedueprocessofIASBaccountingstandardsetting...............................................................16

3.4.1TheIASBDiscussionPaper(DP)ofthedueprocessofIFRS15...........................................184Methodology.............................................................................................................................19

4.1Researchstrategyanddesign....................................................................................................194.2Literaturesearch........................................................................................................................194.3Researchmethod–Contentanalysis.........................................................................................20

4.3.1Preparationphase..............................................................................................................204.3.2Organisingphase................................................................................................................214.3.3Reportingphase..................................................................................................................24

4.4Empiricalsample........................................................................................................................254.5Evaluationofmethod.................................................................................................................264.6Ethicalconsiderations................................................................................................................27

5.Empirics....................................................................................................................................285.1Region........................................................................................................................................285.2Industry......................................................................................................................................285.3Preparers’opinionregardingthedevelopmentofIFRS15.........................................................29

5.3.1Whichregionsagreewiththeproposedsinglerevenuestandard?...................................305.3.2Whichindustriesagreewiththeproposedsinglerevenuestandard?...............................30

5.4Typeofargumentationusedbypreparers.................................................................................315.4.1Whattypeofargumentsareusedindifferentregions?....................................................315.4.2Whattypeofargumentsareusedbydifferentindustries?................................................32

5.5Otherfindings............................................................................................................................345.5.1PATcontradictions..............................................................................................................345.5.2ComplexityofcurrentstandardsinUSGAAP.....................................................................355.5.3Notinmybackyard(NIMBY)..............................................................................................36

ElsaWachtmeister MartinStrömland BUSN69

5

6.Discussion................................................................................................................................376.1Discussionoftheresultsoftheregions......................................................................................376.2Discussionoftheresultsoftheindustries..................................................................................386.3Generaldiscussionoftheresults................................................................................................39

7.Conclusion................................................................................................................................417.1Reflectionandfutureresearchsuggestion.................................................................................41

References...................................................................................................................................43

Appendix1–Thecodingmanual..................................................................................................47

Appendix2–X2-testRegionandopinion......................................................................................48

Appendix3–X2-testRegionandargument...................................................................................49Appendix4–X2-testIndustryandargument................................................................................50

Appendix5...................................................................................................................................51ListofpreparersinDP(1/3).............................................................................................................51ListofpreparersinDP(2/3).............................................................................................................52

Appendix6...................................................................................................................................53QuestionsoftheDPinthedueprocessofIFRS15(1/3)..................................................................53QuestionsoftheDPinthedueprocessofIFRS15(2/3)..................................................................54QuestionsoftheDPinthedueprocessofIFRS15(3/3)..................................................................55

ElsaWachtmeister MartinStrömland BUSN69

6

1Introduction1.1Background

Intodaysworld,boardersarebeingmoreblurredasmarketsblendduetoincreasingglobalisationandinternationalisation. This implies thatoccurrences thatbefore couldbeen seenas isolatedevents,nowadaysaffectneighbouringcountriesandmarketsinagreatermanner.Regardingaccounting,thesettingisnodifferent.Associatedwiththeincreasedinternationaltrade,thereisaviewheldbymanythatstandardisationoffinancialreportingenablesinvestorstounderstandandachieveareasonablebasistocomparethefinancialaccountingofcompaniesfromdifferentcountries(Deegan&Unerman,2011). By converging accounting standards, financial reports can become more comparable. Theprocess of convergence is not an easy process, rather coupledwith challenges (Satin&Huffman,2015). Today, there are two main international accounting standard setters, the InternationalAccountingStandardsBoard(IASB)andtheFinancialAccountingStandardsBoard(FASB).FASBoriginsfromtheUnitedStates,withitsregulatoryframeworkGenerallyAcceptedAccountingPrinciples(USGAAP).IASBwithitsequivalentregulatoryframeworkofInternationalFinancialReportingStandards(IFRS) is considered as a wider spread international organization. Since 2002 and the NorwalkAgreementwasenteredbetweenFASBand IASB, the agendaof theboards is dominatedby theireffortstoachievegreaterconvergencebetweenIFRSandUSGAAP(Holzmann&Munter,2015).Onetopic of the convergenceproject is thedevelopmentof a standard regarding revenue recognition(Garmong,2012).Thestandardisdevelopedjointlybythetworegulatorswiththepurposetoclarifytheuseofprincipleswhenrecognisingrevenue(IFRS,2015b).Themaindifferencebetweenthetworegulatoryframeworks IFRSandUSGAAPisthat IFRS isconsideredtobeprinciple-based,whereasFASBisrule-based.FASBaimstoanticipatepotentialproblemsanddeliversolutions,whiletheIASBpresents objectives consisting of principles that enables interpretation (Hlaciuc et al. 2014). Theaccountingstandardsaretogetherthetwomostacknowledgedoffinancialreportingworldwide.

The two accounting standard setting bodies work together with the purpose to increase thecomparability of financial reports (Garmong, 2012). An essential element of a new standarddevelopmentisthesocalleddueprocess,whichrelyonthethreeprinciples;transparency,fullandfairconsultationandaccountability(IFRS,2013).

Differentstakeholderswithvaryingperspectivescanleadtodisagreementsandconflictsofinterestduringthedevelopmentofnewaccountingstandards.Howthesequestionsaretreatedisadelicatebalance of how to handle influence. On one hand, external input is needed in order to createsuccessfulandlegitimateaccountingstandards,ontheotherhanditcouldleadtodoubtfulinfluencedue to lobbying. Additionally, the standards should be based on and alignedwith the conceptualframework.Theconceptualframeworkdescribestheobjectiveandthepurposeoffinancialreporting,itassiststheIASBtodevelopIFRSandarebasedonconsistentconcepts.TheobjectiveoffinancialreportingandthequalitativecharacteristicsoffinancialinformationwasrevisedbytheIASBin2010asaresultoftheconvergenceprojectwithFASB(IFRS,2015a).Thesecorevaluesoftheconceptualframeworkaswellasthedueprocessmightbechallengedduetotheexternalexposure.

Cheney(2006)presentedtheincreasingnumberofrestatementsthatoccurredintheUS,whichwereexplainedbythemis-recognitionscausedbythemany,andsometimesunclearstandardsofFASB.Therevelations of aggressive earnings accounting, by fraudulently capitalise revenue expenditure ascapitalexpenditureinthecaseofWorldComledtooneoftheworld'slargestcompanybankruptcybecauseofmisleadingaccounting(Unerman&O'Dwyer,2004).Unerman&O'Dwyer(2004)explainedthatintheaftermathoftheWorldComaccountingfailure,manyaccountingregulators,practitionersandpoliticians inEuropeancountriesstated that theaccountingmethod's that led toWorldCom’sfailure would not have been effective in Europe.Moreover, Nobes & Parker (2004) undertook acomparisonofacompany'sresultwhichaccounted inaccordanceto IFRSandUSGAAPandfoundsignificantdifferencesinnetincomeandinshareholderequity.Hence,amoreconvergedandquality

ElsaWachtmeister MartinStrömland BUSN69

7

standardsettingbetweenthetwomainregulatorybodieshasbecomemorerelevantfollowingsuchtypesofaccountingdifferences.

Revenue has an effect on key financial indicators in all financial reporting and it is therefore ofimportancetoachieveacorrectandcomparablerevenuerecognitionaccountingstandard.Itcanbeassumed to be vital to stakeholders in order to understand the value of a company. Hence,collaborationbetweenIASBandFASBwiththepurposetoensurecomparableandqualityaccountingiswelcomed.Thedevelopmentofrevenuerecognitionregulation isconsideredbyNobes&Parker(2012)tobeamajorandcomplexissue.Sincetheprocessstartedin2004,ithastakenseveralyearsoffarreachingconsultationanddeliberationstojointlyissueconvergedaccountingstandardsontherecognitionofrevenuefromcontractswithcustomers. It isknownastheIASB'sstandard; IFRS15-RevenuefromContactswithCustomers.Theprocessconstitutedofover650meetingsandinvolvedparticipationofnumerouskindsofstakeholders,suchas;academics,accountancybodies,auditors&accounting firms, governments, individuals, industry groups, investors, preparers, regulators andstandard-settingbodies (IFRS,2014).The final convergedaccounting standardwas issued in2014,withthegoalofimplementationin2017.Theeffectivedatewaslaterdeferred,whichalsopointsoutthescaleofcomplexityofthestandard(IFRS,2014).WhatfurtherhighlightsthecomplexityofthedevelopmentoftheIFRS15isthefactthatthedueprocess,whichisfurtherexplainedinChapter3,goesbeyondthenormalrequirementsbytheissuingofanadditionalrevisedexposuredraft.Intotalforthewholedueprocess,1500commentletterswerereceivedfromvariousstakeholders.

ThestandardistobeappliedontheannualreportingperiodsaccordingtoIFRSbeginningafterJanuary2018.EntitiesreportingtheirannualreportsaccordingtoUSGAAPwiththeequivalentstandardcalledASC606,willberequiredtobeapplythenewstandardinperiodsbeginningafter15December2017(IFRS,2015c).TheissuanceofIFRS15isanimportantmilestoneinfinancialreporting.CompanieswhoeitherreportinaccordancetoIFRSorUSGAAPwillreportusingtothesameprinciplesregardlessofwhichcapitalmarketthecompanyoperatesin(McConnel,2014).ThepurposeofthedevelopmentofIFRS15isanincreasedalignmentbetweenacompany'srevenueandperformance.

Accountants of financial reports highlights that IFRS 15 will affect some entities with significantchangesfromcurrentstandards.Tocomplywiththestandardwillnotsolelybeconsideredtobeofaccountingcharacter,butalsoofabroaderbusinesschallenge.Thesechallengesincludechangesinprocesses and systems, the control environment, investor relations, tax planning, managementinformationandbusinessoperations.TheaccountingfirmsEY(2014)andKPMG(2014)arguedthatduetonewextensivedisclosurerequirements,anumberofaspectsoftheorganisationwillneedtobeconsidered.Bothoftheaccountingfirmsstressedtheimportanceofhavingaholisticviewwhenimplementing the standard, consideringdifferentaspects inorder toensure that revenue isbeingaccountedforcorrectly.ThereasonforthisisaccordingtoEY(2014)andKPMG(2014)explainedbythe connection between revenue and the valuation of the company,which is seen in various keyfinancialindicators.Sincethestandardhasnotyetbeenimplemented,KPMG(2014)statedthattheimpactofthenewstandardisuncertainregardingwhetherrevenuerecognitionistobeacceleratedordeferred.Thechangesrequiredinordertomeetnewdemandsarethoughexpectedtobecoupledwithcost,atleastinitially.

1.2Problemformulation

Thedevelopmentofsufficientinternationalaccountingstandardsiscoupledwithopportunitiesandchallenges,thebalanceofexternalinfluenceonthestandardsettingprocessshouldbenoted.Thereareseveralpreviousempiricalstudiesofthecommentletterssenttothestandardsetters,whichhavefoundanumberofregularities.Onesignificantpreviousfindingisthatpreparersarepredominantinthedueprocess.

ElsaWachtmeister MartinStrömland BUSN69

8

Forgroupsandindividualswhowantstoaffecttheaccountingstandardsetting,lobbyingthroughthedueprocess isoneapproachtosucceed influence.Sutton(1984)examinedthecharacteristicsofalobbyist, which is argued to be those who expect large financial benefits from the activity. Thepreparersofthefinancialstatementspotentialeconomicbenefitsofsecuringitsfavouredproposalarelikelytobegreaterinabsolutetermsthanfortheuser.Thetypeofindividualororganizationwhoismorelikelytofindlobbyingworthwhilearepreparersoffinancialstatements,largeproducersandundiversifiedproducers.Thereasonwhylargeandundiversifiedproducersareconcernedofindividualstandards is that the effect is often concentrated on certain industries, while users of financialstatementstendtobediversifiedandthereforelessconcernedbytheeffectsofindividualstandards.Sutton(1984)issupportedbyDeakin(1989)andSantos&Santos(2014)researches,whichshowedthatlargeoilcompanies,consideredtobeundiversified,aremorelikelytolobbystandardsettersonaccountingregulationtoobtainstandardsthatmeettheirneeds.Larson(1997)foundsimilarresultsinhisstudyofcorporatelobbyistoftheIASC,wherelobbyingisexertedbyalimitednumberoflargecompanies.AnotherempiricalstudyoncommentlettersisJorissenetal.(2012)researchaboutthelevelofdifferentgroupsactiveparticipation in thedueprocess.Theyalso foundthatparticipatingpreparersintheIASBdueprocessarelargerandmoreprofitablethannon-participatingpreparers.FurtherempiricalresearchonthecorporatelobbyingactivitiesintheconstituentparticipationinonesignificantpartoftheIASB,theInternationalFinancialReportingInterpretationsCommittee(IFRIC)showed that the EU provided a majority of the comment letters, while the US, Canada and thedevelopingcountriesgeneratedfewercomments(Larson,2007).Althoughitshouldbenotedthattheresearchisnotbasedonaconvergenceproject.Atthattime,theUSstillhadinterestintheseissuessince the SEC still required foreign companies listed on US exchanges to reconcile IFRS financialstatementstoUSGAAP.

Zeff (1978) drew attention to the challenges of considering the different interests of differentstakeholdersduringthestandardssettingprocess,bothfromatheoreticalperspectivewithadherencetoprincipleandwhereconsistenceimplementationisheldupassuperior,andapracticalperspectivewhereeconomicconsequencesisconsideredtobemostessential.Theauthorcalledthisadelicatebalanceofaccountingandnon-accountingvariablesthatthestandardsetterischallengedwith.Zeff(1978) highlighted that the American accounting profession and FASB has been exposed of anincreasedexternalinfluenceinthestandardsettingprocess.Zeff(2012citedinNobes&Parker2012)furthertestifiedofhowthesameinfluencehadbeenoccurringtowardsIASB.Thestakeholdershaveemphasized economic consequences,which arguably could result in that these interests could bedetrimental to the interestsofotheraffectedparties. Theauthor stated that accounting standardsettersmusttakethisintoconsiderationwhendealingwithaccountingissues.Furthermore,Bamber&McMeeking(2012)pointedouttheimportanceofthatIASBduringthedueprocessremainshighlyimpartial and independent in their treatment of the comment letters in order to be perceived aslegitimate.Theirempiricalresearchfoundacertainamountofbias inthestatisticalanalysisoftheconsultationresponsestoIFRS7FinancialInstruments-Disclosures.

Watts&Zimmerman(1978)havealsoanalysedtheparticipationofthedueprocess,highlightingthepreparer'spositionoftheeconomiceffectsofproposedstandards.Theyassumethatindividualsacttoinordertomaximizetheirownutility.Hence,theyassumethatmanagementlobbiesonaccountingstandardsbasedonself-interest.

Sutton(1984)researchstatedthatlobbyingandtoexertinfluenceisthemostproductiveinanearlystageofthestandardsettingprocesswhentherulemakersarestillunderconsiderationonhowtomoveforwardtowardsafinalaccountingstandard.Inregardstoatwhatpointpreparerslobbythemost, Sutton’s research is supported by Giner & Arse (2012) study results, which showed thatpreparersaremoreactiveinsendingcommentlettersinthebeginningofthedueprocess.

Stenka&Taylor(2010)investigatedaccountingstandardsettingintheUK.Theresearchwasbasedoncommentletterresponsesondifferentrelatedexposuredraftswheretheydividedthepreparersinto

ElsaWachtmeister MartinStrömland BUSN69

9

twocategories,corporateandnon-corporate.Thestudyresultshowedhowthepreparersarguefortheir interests.Preparersandnonpreparersare foundtouseconceptuallybasedargumentsmoreoften than economic based arguments. However, economic based arguments are solely used bycorporate preparers. Another research which examined preparers and non-preparers positiontowardsnewaccountingstandardsandhowtheyargueincommentletterswasHartwig(2012).Hisstudyfoundthatinregardstotheprohibitionofgoodwillamortization,corporatepreparerssupportnon-amortizationofgoodwilltoahigherextendthannon-preparersduetoeconomicconsequences.Thestudyalsoshowedthatbothcategoriesuseconceptualbasedargumentsinahigherextentthaneconomicconsequencesbasedarguments.

Previousempiricalresearcheshaveemphasisedallthedifferentcommentletters,whicharesentfrompreparers, academics, individuals, accountants, users of financial statement, professional bodies,industryorganisations,standardsetters,regulatorsandconsultantsetcetera.Aspresentedinpreviousstudies,thelargestgroupofstakeholderswhichaimtoinfluencethedueprocessarethepreparersoffinancialstatements.However,therearelimitedresearchesthatfocusonpreparersonly.Chircop&Kiosse (2015)examined the characteristicsof firms that lobbiedon theexposuredraftof IAS19 -Employee benefits, and their position on two important proposals in the ED. Nevertheless, theresearchdoesnottakeanygeographicalaspectsorcomparisonsintotheirconclusions.

Asthepreparerisacentralactorandaninfluentialpartofthedueprocess,wefinditimportanttoinvestigatewhattheopinionsof thepreparersof financialstatementsareandhowtheyargueforthem.Wefindthis informationessentialsincethestandardsetters IASBandFASBdealwithheavyexposuresofdifferentpreparersthatwantsinfluenceinthestandardsettingprocessandfurthermoreremain impartial regardless and take different geographical regions in consideration in order tomaintainitslegitimacyasaccountingstandardsetters.

A new revenue recognition standard has been long waited. The standard of one single revenuestandardforallindustriesisdescribedasacomplexstandardwhichwillhavegreatimpactandleadtosignificantchangesinsomeindustries.Thereisanuncertaintywhetherthestandardwillimpactthepreparersfinancialstatementsinapositiveornegativemanner.Theremaybedifferencesofopinionbetweenthevariousindustriesthestandardwillimpact.Thereforitwouldbeinterestingtoinvestigatewhetherindustrieshavedifferentapproachestowardsthestandardandthetypeofargumentsthatisexpressedtohighlighttheirstandpoint.

DuetothefactthatIFRS15isastandardcreatedjointlybyIASBandFASBasapartoftheconvergenceproject, it is likely thatpreparersdiffer in theiropinions since theirpreviousaccounting standardsregarding revenue recognition have considerably different characteristics. Therefor it would beinteresting to investigatewhether thereare significantdifferences inwhetherpreparersacceptorobjectthenewstandard,andfurtherifandhowopinionsarebeingarguedfor.

1.2.1Researchquestions

- Howarethecommentletterssentbypreparersdistributedamongregionsandindustries?

- Is it possible to see any differences in opinions and arguments used by preparers fromdifferentregionsandindustries?

1.2.2Researchhypotheses

Thefirstresearchquestionisnotsubjecttostatisticaltestsinthisstudy.However,thesecondquestioncanbeansweredthroughoutstatisticalX2-tests.

ElsaWachtmeister MartinStrömland BUSN69

10

Nobes&Parker (2004) andUnerman&O'Dwyer (2004) researches illustratedmajor internationaldifferencesintheadoptionofeitherIFRSorUSGAAPinthefinancialstatements.Hence,theopinionstowardstheconvergenceprojectmightdifferbetweenpreparersfromdifferentregions.Thereof,thefollowinghypothesisistestedforpotentialsignificantdifferences.Ifthetestissignificant,therearedifferencesintheregionsopinion.

1. (H0): There are no differences in regionswhether they agreewith the single

revenuerecognitionstandard.

Zeff (1978)andWatts&Zimmerman(1978,79,90)arguedthatpreparershaveeconomic interests.Hence, some preparers might have more economic based arguments than others. In order toinvestigate the second research question; Is it possible to see any differences in opinions andarguments used by preparers fromdifferent industries and regions?The following hypotheses aretested for potential significant differences. If the tests are significant, there aredifferences in theregionsandindustriesargumentation.

2. (H0):Therearenodifferencesinregionsinhowtheyargue.

3. (H0):Therearenodifferencesinindustriesinhowtheyargue.1

1.2.2Purpose

ThisstudyexaminesthepreparersoffinancialstatementsandtheirparticipationintheinitialphaseofthedueprocessoftheaccountingstandardIFRS15–Revenuefromcontractswithcustomers.Theaimofthisstudyistoidentifytowhatextentdifferentpreparersvaryinparticipationamongindustriesandregionsandfurtherexaminewhattypesofargumentationthatisbeingused.Thepurposeistoimproveandbroadentheunderstandingofwhypreparerschoosetoparticipateinthedueprocessandhowthisrelatestopreviousresearchwiththeintentiontoprovidecontributiontotheresearchlandscape.Inordertounderstandwhypreparers,participateinthedueprocess,weassumethattheargumentsputforwardinthecommentlettersrepresentsthemainreasonsofwhyapreparerchosetoagreeordisagreewiththeproposedstandard.Hence,byansweringtheresearchquestionsthepurposeofthestudywillbeachieved.

1Additionalhypothesesandstatisticaltestscouldnotbeconductedbecauseofmethodologicalconsiderations,seechapter4.3.3.1

ElsaWachtmeister MartinStrömland BUSN69

11

2TheoreticalframeworkInthetheoreticalframeworksection,economicandsociologicaltheoriesthatseekstoexplainwhypreparerswillreactinacertainwaytodifferentaccountingcharacteristicswillbepresented.ThisisdiscussedbyHussein(1981),Kelly-Newton(1980),Davisetal.(1997),andWatts&Zimmerman(1978,1990).ThetheoriesinthischapteriscomplementedbythepreviousresearchpresentedinChapter1.

2.1Innovativeprocess(Hussein,1981)

Hussein presented in his study how the Innovation process is affected by sociological aspects inaddition to traditional economic aspects when setting accounting standards. By addressing theprocessinaquitebroadmanner,Hussein(1981)suitsasanintroductionofthetheoreticalchapter.Among other thoughts, Hussein (1981) identified that stakeholders will interfere with accountingregulation only if management finds a performance gap. Whether or whether not stakeholdersidentifyaperformancegapdependsonifthereisadiscrepancybetweenadesiredandexperiencedlevelofsatisfactionintheaccountinginnovation.

Hussein(1981)developedamodelbasedonZaltmanetal.(1972citedinHussein,1981)intheareaof standard setting accounting norms. Themodel identified a discrepancy between a desired andexperiencedlevelofsatisfactionreferredtoasaperformancegap.Theperformancegapaffectstheregulationprocesswheredifferentactorsandavarietyoffactorshasanimpactonthefinalaccountingsolution.Theresultisbasedonacollectivedecisionbyseveraldifferentactors’participationinthestandardsettingprocess.

Inanearlystage,thestudyshowedtheimportancetoobservethedifferentattitudesofanaccountinginnovation which can result in motivations to consider a change. The actors' perception of theaccountinginnovationisdependentonthecharacteristics,thesameinnovationmaybeperceivedtohave different characteristics and degree of importance by different actors. According to Hussein(1981),therearesixcharacteristicsthataffectstheperceptionofanaccountinginnovation;relativeadvantage,relevance,reliability,compatibility,communicabilityandradicalness.

Aftertheformationofattitudes,thereisaphasewheretheaccountinginnovationmustberegardedas legitimate in order to be accepted. The phase is characterized with implicit bargains betweendifferentgroupswithdifferentinterests’.Husseincalleditimplicitbargainingbecauseofthatsmallergroupsmaynotbeinfluentialenoughalonetoabletoaffecttheaccountinginnovation.Therefore,acompromise is created through implicit bargaining, which means that the relative influence ofdifferentgroupswilldeterminethefinalresult.Differentactorscanalsocreatecoalitionstoincreaseitsrelativeinfluenceintheprocess(Hussein,1981).

2.2Aspectsspecifictotheinnovation(Kelly-Newton,1980)

As a continuation on the theory of Hussein (1982), Kelly-Newton (1980) focuses on the factorsinfluencing managements' reaction to new accounting standards. One of the categories sheconsideredto influencetheacceptanceor therejectionsbycorporatemanagementofaproposedchangeinaccountingpractices istheaspectsspecifictotheinnovation.Theseaspectsare;relativeadvantage,compatibilitywithnorms,complexityinuse,trialabilityofthechange,andobservabilityofperceivedbenefits.Asthecharacteristicsarediscussed,itisofimportancetohaveinmindthatitisthe perception of the attributes that is essential, since these understandings will determine theaccountinginnovations'acceptability.

ElsaWachtmeister MartinStrömland BUSN69

12

2.2.1Relativeadvantage

Therelativeadvantage,orthebenefitsoftheaccountingchangemanagementbelieveswillaccruefromadopting the accountingmethod is primary along the characteristics. The benefits are oftenmeasuredineconomictermsandmayincludeexpectationsofeconomicprofitability,implementationcosts,relatedrisksandtimesavings.Kelly-Newton(1980)referstoWatts&Zimmermans'studiesasexamplesofpositiveaccountingtheory,wheremanagers'goalistomaximizeitsownwealththroughstaypositiveoropposeanaccountinginnovation.Furthermore,theimpactofincreasedaccountingcosts is also central in assessing the relative advantage of an accounting change. These costs caninclude expenses to engage outsiders in the implementation phase and opportunity costs fromdivertingemployeesintoincreasedaccountingtasks.

2.2.2Compatibilitywithnorms

Thesecondcharacteristicwhichinfluencetheadoptionofanaccountinginnovationistheperceivedconsistencyofaproposedchangewithmanagement’snorms,values,attitudes,pastexperiencesandneeds.Thevariableofcompatibilitywithnormsinvolvestheculturalandsociologicalattributesofthebusinesscommunity.Thegreaterthesimilaritywithexistingnorms,thelesschangetheinnovationrepresents. The value schememust be clearly distinguished from the accounting profession. Theaccountingprofessionisuser-orientedconcerningthefinancialstatementreports,stressingdecision-usefulinformationtotheuser.Managementadoptsauserperspectiveonlytotheextentnecessaryformaintainingitsequitymarket.Managementfindsitlessimportantforfinancialstatementstohavequalitiessuchas relevance, timeliness,consistency, lackofbias,uniformityandcomparability.Thebusinesscommunitythusstressesvaluessuchasobjectivity,accuracy,reliabilityandverifiability.

2.2.3Complexityinuse

Theperceiveddifficultyinimplementingandunderstandingtheaccountinginnovationrepresentsthecomplexityfactor.Thisaspectwillbedeterminedbythepreparersexistingtechnicalskills,education,knowledge,priorexperiences,expected learningcurve,availabilitytooutsideconsultantsetcetera.Predictedimplementationcostsarenotdirectlyinvolvedinthisparticularaspectastheyimpacttheperceivedrelativeadvantages,see2.2.1.

2.2.4Trialabilityofthechange

Afourthaspectistrialabilityordivisibility,meaningastowhichextentanaccountinginnovationcanbeimplementedonapartialbasis.Selectiveimplementationmaybeseenasbeneficialifmanagementperceives frompartial adoption, and is thus encouraged to experiment. Furthermore, the gradualapproachreliesononebasicassumption,thesmallertheamountofchange,thegreaterthechanceofacceptancebymanagement.

2.2.5Observabilityofperceivedbenefits

Finally,thedegreeofvisibleresultsfromadoptingtheaccountingchangeandhowitiscommunicatedtomanagementisanaspectoftheaccountinginnovation.Ifpositivebenefitsareclearlystatedintheaccounting proposal, it enhances the accounting innovations acceptability with management. Ingeneral,managementplace lowervalue in controversialdisclosuresbuthighervalueonbasicandcommonly disclosed information items. The observability of perceived benefits can be improvedthroughappropriateuseofstrategy.Persuasionprogramscanheightenthevisibilityoftheadvantages

ElsaWachtmeister MartinStrömland BUSN69

13

tothepreparersoftheaccountingchange.Educationstrategieswhichmayinvolveexperimentationofthenewaccountingmethodcanreduceinitialresistancebymanagement.

2.3Sociologicalman(Davisetal.,1997)

Davisetal.(1997),statedthatthestewardshiptheoryissprungoutofsociologicalandpsychologicalapproaches of governance. Since the theories of Kelly-Newton (1980) involved aspects bothconsideredtobeeconomicandsociological,acontinuationonthesociologicalframeworkissuitable.Davisetal.brieflydescribedthetheoryasawaytohighlighthow“stewardsaremotivatedtoactinthebestinterestoftheirprincipals”(1997,p.24).SomecharacteristicswillbefurtherexaminedwithinspirationofDavis et al. (1997) framework, focusingonmotivation, identification and theuseofpowerastheycanbeseentobepsychologicalmechanismsaffectinghowtheagentisassumedtoact.

When investigating what tends to motivate individuals that is more aligned with the theories ofstewardshipgovernance, the intrinsicvaluesareofutmost importance. Intrinsicvaluescanbe thepossibilitytogrow,achievegoalsandbeabletoself-actualise.Eventhoughtheintrinsicvaluesaredifficulttoquantify,thesevaluesarekeysofmotivation.Asteward’sgoal istobealignedwiththeorganisation,sincegoalcongruencyistobenefittheorganisation.ThevaluesmotivatingastewardareexplainedtobeofhighorderputintocontextinMaslow’shierarchyofneeds(1970citedinDavisetal.,1997).

The observation of how an individual’s identification with an organisation can lead to positiveoutcomesisnotexceptional.Davisetal.(1997)statedhowidentificationenablesindividualstostriveforaltruisticbehaviourandcontinuousimprovement,thusit'snotbeingrewardedinfinancialterms.Continuousimprovementsarethoughcoupledwiththeself-actualisationwhichinitselfisrewarding.

Withgovernancecomespower.Davisetal.(1997)usedthesimplifiedtypologyofGibsonetal.(1991cited inDavis et al., 1997) dividingpower into the categories of institutional andpersonal power.Stewardshipischaracterisedbypersonalpower.Personalpowerisnotinheritedinthestructureofanorganisationasan institutionalpower,nor is it legitimateby law,butby interpersonalexperiencecreatedandtendedforovertime.Personalpowerisinthissensethemainsourceofinfluenceinanorganisationpermeatedbystewardshipvalues.

2.4Economicman(Davisetal.,1997)

Davisetal.(1997)presentedhowthetraditionalviewofeconomicgovernanceandagencytheoryisaffiliatedwiththeassumptionsofindividualistic,opportunisticandself-servingbehaviours.Inotherwords,it iscalled:theassumptionsofhomoeconomicus.Moreover,theeconomicmanconstitutesthebaseofagencytheory,assumingtheagenttobeanactorcharacterisedasarationalandself-maximising individual. Theeconomicman is thereforassumed toact in self interestwhenmakingdecisions.Thesamepsychologicalmechanismsaspresentedinthechapterofsociologicalmanaretobetreatedinthelightoftheeconomicman.Thesearemotivation,identificationandtheuseofpower.Additionally,Watts&Zimmermans'theoryofpositiveaccountingispresented.

Davisetal.(1997)explainedtheeconomicmantobemotivatedbylowordereconomicneeds.Theauthors draw parallels to Maslow (1970), who describes lower order needs as physiological andsecurityneeds. Theauthorsproposed that individualswithextrinsicmotivations tend to inhigherdegreebeactinginselfinterest,andisfurthercharacterisedinaccordancetoeconomicman(Davisetal.,1997).

ElsaWachtmeister MartinStrömland BUSN69

14

Kelman andMael& Ashforth, (1958, 1992 cited in Davis et al., 1997) define towhich extent themanagerisidentifyingitselfwithanorganisationaswhen“acceptingtheorganisation’smission,goalandobjectives”(1997,p.29).Individualsthatarenotacceptingandidentifyingthemselveswiththeorganisationareproposedtobemorelikelytoactinlinewiththeeconomicman.Furthermore,Davisetal.(1997)statedthatanindividualwhodoesnotidentifywiththeorganisationcouldactuallybeharmfulduetotheriskofnotacceptingresponsibilityandnotactintheorganisation'sbestinterest.

Davisetal.(1997)statedthatinstitutionalpoweriscommonintheuseofcontrollinganagentastheagent isassumedtoactself-servingandoropportunistic.Theuseof legitimatepoweroftentakesformasrulesandregulationandcouldforexamplebecoerciveor legitimate,oftenhierarchalandcentralised.

2.4.1Positiveaccountingtheory(Watts&Zimmerman(1978,1979&1990)

Watts & Zimmerman (1978, 1979, 1990) are the founders of positive accounting theory. Positivetheories try to explain andpredictwhich accounting policies firmswill choose andhow firmswillrespond to newly proposed accounting standards. The theory recognized that economicconsequencesintakenintoconsiderationwhencompaniesmakesitsdecisionofaccountingpolicies.This is an explanationwhymanagerswant flexibility in choosing accountingpolicies,whichbringsforward theproblemofopportunisticbehaviour.Thisoccurswhenmanagementacts in theirownpersonalinterests.Positiveaccountingtheoryhasthreehypothesesfromwhichitisorganized(Watts&Zimmerman,1990).Thefirsttwofollowinghypothesesaremostrelevantforthethesis.

Thebonusplanhypothesisrelatedtofirmswithbonusplansforthemanagers.Theywillbemorelikelytochooseaccountingpoliciesthatshiftreportedearningsfromfutureperiodstothecurrentperiodtoreceivehigherbonuses.

Thedebt/equityhypothesispredictedthatthehigherthedept/equityratiois,thelikelihoodincreasesthatmanagementmoveearningsfromthefuturetocurrentperiod.Itisthenlesslikelytodisruptdebtcovenantsandmanagementhasreduceditsconstraintsinrunningthefirm.

Politicalcosttheorypredictedthatitismorelikelyforthemanagementtomovecurrentearningstothefuturetopreventthegreaterthepoliticalcostsfacedbythefirm.Increasedpoliticalpressurecanderivefromhighprofitabilityandresultinhighertaxesorregulations,especiallyforlargercompanieswhichisoftenheldtohigherreportingstandards.

2.5Theoreticalframeworksummary

Thetheoriespresentedisabasisfortheunderstandingofthecharacteristicsoftheinnovationprocessaswellasthemanagerialtraits.Thetheoriesarethebaseofthecategorisationoftheregionsandindustriesopinionandargumentation.ArgumentationthatcanberelatedtoDavisetal.(1997),Watts&Zimmerman(1978,1979,1990)andKelly-Newton's(1980)firsttopic,relativeadvantages,whicharecategorised as economic arguments. Argumentation that can be related to Kelly-Newton (1980)headlines about compatibility with norms, complexity in use and trialability of the change arecategorised as sociological arguments. Further explanation of our categorisation is explained inchapter4.3.2.3.

ElsaWachtmeister MartinStrömland BUSN69

15

3InstitutionalcontextIn this chapter, overall information is provided about themain actors that develops internationalaccountingstandards.Moreover,generalinformationaboutIFRS15andtheprocessofthestandarddevelopmentwillbepresented.

3.1FinancialAccountingStandardsBoard–FASB

FASBisestablishingstandardsforfinancialaccountingthatgovernthepreparationoffinancialreportsbynongovernmentalentitiesintheUS.ThestandardsarerecognizedasrespectedbytheSecuritiesandExchangeCommission(SEC)andtheAmericanInstituteofCertifiedPublicAccountants(AICPA).

Themission of FASB is to create and improve financial accounting standards reports that providedecision-useful information to investors and other users of the financial reports. The mission isaccomplishedoveranindependentandcomprehensiveprocessthatencouragesbroadparticipationthatobjectivelyconsidersallstakeholdersview(FASB,n.d.).

3.2InternationalAccountingStandardsBoard–IASB

IASB is a non-profit public interest organisation which mission is to develop IFRS that bringsaccountability,transparencyandefficiencytotheworld'sfinancialmarkets.Theorganisation'sworkservesthepublic interest in theglobaleconomyby fosteringgrowth, trustand long-termfinancialstability.

IFRSbringstransparencybyimprovinginternationalqualityandcomparabilityoffinancialinformation,supportinginvestorsandotherparticipantstomakeinformedeconomicdecisions.

IFRS strengthens accountability by reducing the information gap between companies and theirinvestors.Thestandardsaimtoprovidethenecessaryinformationtoholdmanagementintoaccount.Also,IFRSaimtocontributetotheglobaleconomicefficiencybyhelpinginvestorsaroundtheworldtoidentifyrisksandopportunities.Theuseofasingletrustedaccountingstandardlowersthecostofcapitalandinternationalreportingcostsforbusinesses(IFRS,n.d.,e).

In2002,theEuropeanParliamentdecidedthataccordingtoECnr.1606/2002art.4,listedcompaniesof every member state of the European Union should apply from January 2005 its consolidatedfinancialstatementsaccordingtoIFRS(EuropeanParliament,2002).Altogether,120countriesaroundtheworldhaverequiredorpermittedtheuseofIFRS(IFRS,2015f).

IFRSaredevelopedthroughaninternationalconsultationprocess,whichinvolvesstakeholdersfromaroundtheworldwhichiscalledthedueprocess.

3.3IFRS15

ThegoalofthejointlyconductedrevenueprojectbyIASBandFASBwastoclarifyandtheprinciplesofrecognisingrevenuefromcontractswithcustomers.ThefinalissuedversionofIFRS15appliestoallcontractsexceptforfinancialinstruments,insurancecontractsandleases2.

2Inthediscussionpaper,financialinstruments,insurancecontractsandleaseshadnotyetbeenexcludedfromthescope.

ElsaWachtmeister MartinStrömland BUSN69

16

Themainobjectivesoftheprojectweretoprovideclearprinciplesforrevenuerecognitioninarobustframework to remove weaknesses and inconsistencies in existing revenue recognition standards.Furthermore,toprovideasinglerevenuerecognitionmodelinordertoincreasecomparabilityoverarangeofcompanies,industriesandgeographicalregions.

Thecurrentrevenuerecognitionstandards inUSGAAPhasbroadconceptsofrevenuerecognitionwhichnumerousindustryandtransactionspecificrequirementsexiststohandlewithdifferenttypesofcontracts.IFRSconsistsoffewerstandards,howevertheycanbedifficulttoapplyincomplicatedtransactionsduetolimitedrulesandguidelines(IFRS,n.d.,m).

IFRS15replacesallpreviouslyissuedstandardsandinterpretationsrelatingtorevenuerecognition,whichincludeIAS11–ConstructioncontractsandIAS18–Revenueamongotherrelevantstandards(Anjou,2014). IAS11andIAS18havebeentheapplicableregulationsince1995(DeloitteIASplus,n.d.,a)(DeloitteIASplus,n.d.,b).

Thestandardwillapplytoannualperiodsbeginningonorafter1January2018forcompaniesapplyingwithIFRS.ForUSGAAP,theeffectivedatestartsthe15December2017.EarlyadoptionisacceptableinIFRSbutnotforpublicentitiesreportingunderUSGAAP.(IFRS,2015c)Entitieswillshiftfollowingeitherafullretrospectiveapproachoramodifiedretrospectiveapproach(EY,2014).

Thestandard’sprincipleswillbeappliedbyusingafivestepmodel,seeFigure3.3.Theentitieswillhavetoexercisejudgementwhenconsideringthetermsofthecontractandallrelevantcircumstancesandfacts.Therequirementswillhavetobeappliesconsistentlytocontractswithcomparablefeaturesandinsimilarcircumstances(EY,2014).

Figure3.3–Fivestepmodel(EY,2014).

3.4ThedueprocessofIASBaccountingstandardsetting

Inorder tobe able to reach IASB's objectiveof developinghighquality accounting standards, theorganisationstartsfirststagewithananalysisofwhatisofvaluetotheusersoffinancialstatements.Highqualityinformationistheprimarygoal,whichaswellisakeyaspectofotherstakeholders,suchas preparers.When initiating the standard setting process and setting the agenda, the followingaspectsareconsidered;therelevancetousers,whetherexistingguidanceisavailable,thepossibilityof increasing convergence, thequality of standard to bedeveloped, and finally; possible resourceconstraints(IFRS,n.d.,g).SeeFigure3.4forvisualisationofthedueprocess.

Step1•Identifythecontract

Step2•Identify

performanceobligations

Step3•Detirminethetransactionprice

Step4•Allocatethe

transactionprice

Step5•Recognise revenue

ElsaWachtmeister MartinStrömland BUSN69

17

Inthesecondstage,whenfurtherplanningtheproject,theIASBconsiderwhetherthestandardsettingprocessistobeconductedaloneorwiththehelpofanotherstandardsettingbody.InthecaseofIFRS15, thestandard isdeveloped jointlywithFASB.During thecaseofplanning,possibleconsultativegroupsarecreatedtoassisttheproject(IFRS,n.d.,h).

The third stage is not a mandatory process, although a discussion paper is often published. Thepurpose of the discussion paper is to collect solicit opinions at an early stage. In the case of thedevelopmentof IFRS15, adiscussionpaperwaspubliclypublished in2008containingpreliminaryviewsofthenewstandard(IFRS,n.d.,i).

Infourthstage,anexposuredraftispublished.Thiscontainsaconcretestandardproposalandhandlesearlier research made by staff and further comments obtained internally from IASB consultativegroups(IFRS,n.d.,j).

In stage five, a consideration whether a second exposure draft, a so called, re-exposure draft isneeded.Thedecisionofwhetherornottore-publishadraftistakenonanIASB-meetingandifchosen,thedueprocessisthesameasbefore.Ifandwhenthestandardhasbeenre-published,theresultisputtogetherinordertocreatethefinaldraft.Usually,itisreviewedexternallybytheInterpretationCommittee(IFRIC)(IFRS,n.d.,k).

Asinstagesix,thestandardhasbeenissuedandnewobjectivescanarise.IASBfacilitateeducationandhandlespossibleeventualities.IASBalsoconductstudiesintheeffectsduetotheimplementationofanewstandardandhowitmighthaveaffectedtheinformationenvironmentanditsquality(IFRS,n.d.,l).

InthedueprocessofIFRS15,thepossibilitytosendcommentlettersweregivenat4times.Thefirstpossibility was given in the discussion paper. Further, there were two exposure drafts open forcomments on the standard specifications. In addition, because of the complex and extensiveimplementationconsequencesofthestandard,anexposuredraftoftheeffectivedateofIFRS15wasissued.Hence,thestandarddevelopmentofIFRS15hasbeenmoreextensivethanthedueprocessdescribedabove.

Figure3.4–Thedueprocess(IFRS,2015d)

1.Settingtheagenda 2. Planningtheproject

3.DevelopingandpublishingtheDiscussionPaper,includingpublic

consultation

4.DevelopingandpublishingtheExposureDraft,includingpublic

consultation

5.DevelopingandpublishingtheStandard

6. ProceduresafteranIFRSisissued

ElsaWachtmeister MartinStrömland BUSN69

18

3.4.1TheIASBDiscussionPaper(DP)ofthedueprocessofIFRS15

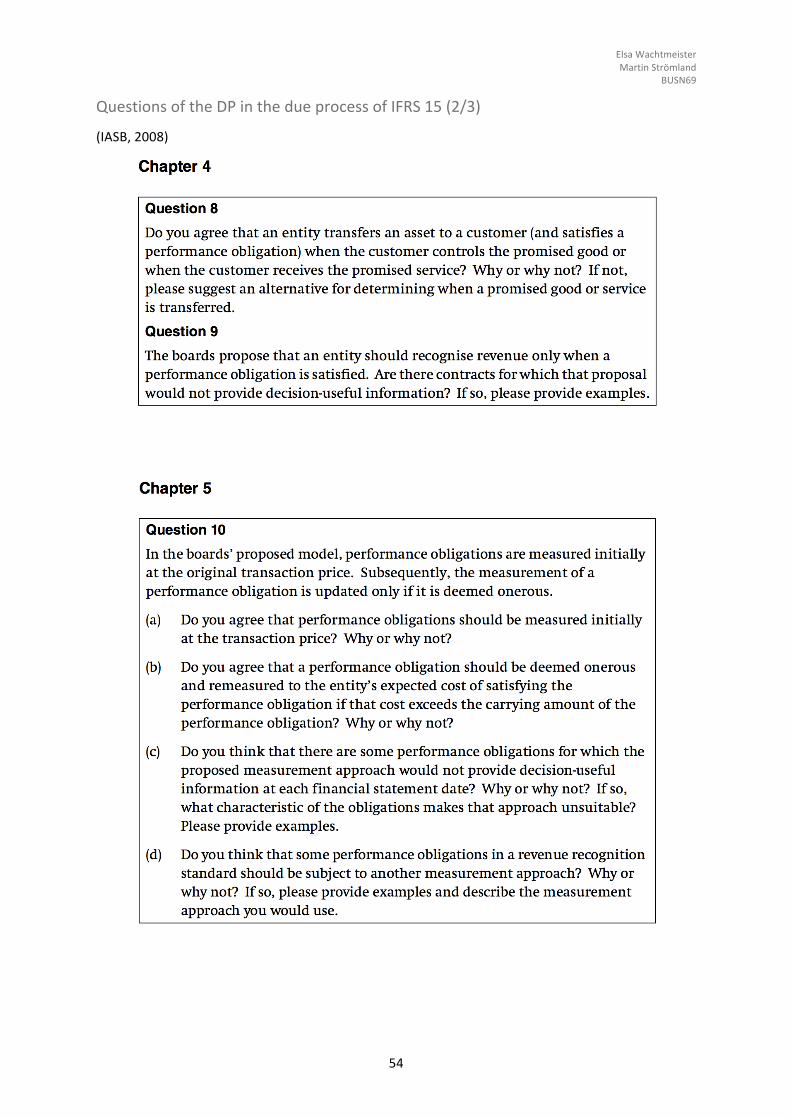

InDecember2008, the firstdiscussionpaperregarding IFRS15waspublished.Thepurposeof thepublication was to create a basis for discussion and enabling every stakeholder which believesthemselves to experience any affects of the new revenue standard to be able to influence thedevelopment.Thediscussionpaperconsistsoffivechapterswhichtogetherholdsatotalofthirteenquestions(IASB,2008).AllofthequestionsarepresentedinAppendix6.

ElsaWachtmeister MartinStrömland BUSN69

19

4Methodology4.1Researchstrategyanddesign

Thepurposeofthethesisistoidentifytowhatextentdifferentpreparersvaryinparticipationamongindustries and regions and further examine what types of argumentation that is being used. AsintroducedinChapter1,IFRS15isaninterestingstandardtofocusonsinceitisacurrentsubjectintheareaofaccountingandastandardthathasrecentlybeendeveloped.InMay2014thestandardwas finally issued. The thesis is basedonquantitative research tobroaden theperspectiveof thepreparer's role in the standard setting process. This has been achieved by collecting informationqualitativelyincommentletters.

Thehypothesesbasedonthethesisresearchquestionsarededucedfromtheoryandissubsequentlytested.Itisoneofthemaincharacteristicsofaquantitativeresearch(Bryman&Bell,2007).Althoughthethesisisbasedonadeductiveapproach,westillhadaninductiveapproachwherewetriedtoseekotherobservationswhichwerenotbasedonparticulartheory.Thequantitativeresearchhasbeenfocusingononeexposuredraftof thediscussionpaperof IFRS15.Thechoiceof investigatingoneparticular standard could be seen as a limitation, since alternative standard developments werediscarded.

Theresearchwasbasedonacomparativedesign.Wecomparedpreparersfromdifferentindustriesandregionsandtheirrespectivelyopinionsandargumentations.Thedatawascollectedbytheuseofacross-sectionaldesign,seeAppendix1.Thecross-sectionaldesign involvedthecollectionofdatafrommorethanonecaseatacertaintimeinordertocomeupwithasetofquantitativedatarelatingto two or more variables. These were further examined in order to detect patterns of differentrelationships (Bryman&Bell,2007).Wehavecollectedthedatabyexaminingpreparerscommentlettersfromthediscussionpaperandfurthersearchedfordifferencesandrelationshipsbetweentheiropinionandargumentation.

4.2Literaturesearch

Whentheresearchquestionhadstartedtotakeform,oursearchforexistingliteraturebegan.It isaccordingtoBryman&Bell(2007)ofimportancetoinvestigatewhatsubjectsandwhatperspectivesthat has been examined in previous research. Ourmain source of literaturewas the database ofreferencesLUBSearchwhichhasbeencomplementedbythedatabaseofGoogleScholar.LUBSearchis LundUniversity's libraries shared referencedatabasewhichprovidesabroad rangeof research,includingregardingthefieldofaccounting.

Thesearchinginthedatabasesstartedwiththeuseofgeneralaccountingtermsregardingaccountingstandardssettingsuchas;standardsetting,standardsettingprocess,dueprocessandlobbying.Whenthescopefurtherwasnarrowed,keywordssuchas;corporatelobbying,preparerlobbying,decisionprocess, lobbying in thedueprocess, IFRS15etceterawereused.Furthermore,while investigatingearlierempiricalstudiesof thesubject,keywordssuchas;empiricalstudiesdueprocess,corporatelobbyingempiricalstudyandpreparerlobbyingempiricalstudy.Themajorityofthetheorieswhichthestudyreliesonwerealsofoundinthedatabases,usingkeywordssuchaseconomicman,sociologicalman,innovationprocessandpositiveaccountingtheory.Thesekeywordsprovideduswithaninitialinsightofthepreviousresearchbutalsowithadditionalreferences.Wealsotookvaluableadvicefromour supervisor regarding additional relevant literature in order to broaden our perspective ofaccountingtheory.

ElsaWachtmeister MartinStrömland BUSN69

20

4.3Researchmethod–Contentanalysis

When aiming to understand, analyse and draw conclusion from the primary source of commentletters,contentanalysisapproachwaschosenasasuitablemethod.Contentanalysisisanappropriatemethodwhensystematicallyandinareplicablemanneranalysedocumentsandtextsthatseekstoqualifyandquantifycontentbycategoriesthathasbeendesignedinadvance.Thepositiveaspectsofacontentanalysisarethatitisanopenresearchmethodthatmakesiteasytodescribethesamplepopulationandthedesignofthecodingmanual,whichmakesfuturestudiessimplertoreplicateandfollowup(Bryman&Bell,2007).Krippendorff(2013)arguedthatthetraitofcontentanalysisasbeingreplicableincreasesthechancesofareliablestudy.Thelimitationsofthecontentanalysisarethatitrelies on the quality of the documents which it is based on. One should assess the documentsaccordingtoScott(1990,citedinBryman&Bell,2007)onthefollowingthreecriteria:authenticity,thatthedocumentiswhatitispurportstobe,credibility;whethertherearereasonstobelievethatthe documents have been or are distorted, representativeness; whether or not the documentsexaminedarerepresentativeofallpossiblerelevantdocuments.AlltheoriginalcommentletterssentarepubliclypublishedontheIASBandtheFASBwebpages.Furthermore,thecommentletterscontactpersonisclearlystatedineachofthedocuments.Hence,thethreecriteriawereconsideredtobemetandthecommentletterswereconsideredtobeahighqualitysourceofdocumentsanalysedinthecontentanalysis.

Thisstudywasconductedwithadeductiveandaninductiveapproach.Ittookpreviousresearchintoconsiderationwhenformulatingmethodandpurposebutwestill triedtohaveacuriousapproachandsearchfornewfindings.Thedeductiveapproachrepresentsthemostcommonperceptionoftherelationship between theory and practice (Bryman & Bell, 2007). Other authors have a differentopinion.Polit&Beck(2004citedinElo&Kyngäs,2008)statedthatthemethodofcontentanalysisisto bemoredifficult than amoreordinary quantitativemethod since it is less standardised. Elo&Kyngässtatedthatoneof themainchallenges lies inchoosinghowtoconstruct theframeworkofanalysis since it is very flexible, meaning that there is "no simple 'right' way" (2008, p. 113) ofconductingsuchastudy.Wethereforealsoappliedaninductiveapproachinordertoseekiftherewereanynewobservedpatternsinargumentationsandopinionsofthepreparerscommentletters.

ThecontentanalysiscanbeconductedthroughaprocessaccordingtothedescriptionofElo&Kyngäs(2008),seeFigure4.3.

Figure4.3–Theprocessofthecontentanalysis(Simplified)(Elo&Kyngäs,2008)

4.3.1Preparationphase

Theprocessstartswiththepreparationphasewherethematerialisbeingreviewedandthekeyfigureis to classify larger amounts of information into more manageable content categories. Withbackground of our research question, we categorised basic information of region and industry.Moreover, the primary focus lied in the opinions and the types of argumentation communicatedthrough the comment letters. When we investigated the characteristics of actors that chose toinfluence the standard setting process and further understand their standpoint, various research

1. Preparationphase 2.Organisingphase 3. Reportingphase

ElsaWachtmeister MartinStrömland BUSN69

21

methodscouldhavebeenused.Inordertoachieveasimplifiedunderstandingandtogetanoverviewof the due process, a useful basis was to read comment letter summaries published by IFRS. AcommentlettersummaryisconsideredtobeasecondarydatasourcesinceitisananalysisconductedbythestaffofIFRSoftheprimarysourceoftheoriginalcommentletters(Bryman&Bell,2007).Thiswastherefornotusedasthemainsourceofinformation,merelyasanintroductionofthesubject.

4.3.2Organisingphase

4.3.2.1Codingschedule

Tobeabletoextractdesiredinformationoftheempiricalmaterial,thenextstepwastoorganisethecontent analysis. By constraining the structure of the coding schedule, the research structurefacilitatedtheinformationthatwasdesired,leavingoutanswerstoquestionsthatwerenotofinterestofourparticularstudy(Elo&Kyngäs,2008).Thiswasachievedbyfocusingontherespondents'region,industry,whethertheyagreeordisagreewiththepropositionandifandhowitisbeingarguedfor.

The structure of the coding process is visualized in Figure 4.3.2.1. The codingmanual is found inAppendix1,whereamoredetailedstructureandcategorizationisfound.

Whenwecategorisedtheoriginofthepreparer,majorregionswereused inorderto improvethecomparability.Bymajorregions,wedividedthoseinNorthAmerica,Europe,AsiaandAfrica.Somecountrieshadveryfew,ifanyrespondents,andwerethereforcompoundedintolargerregions.Sincethe revenue recognition standard affect various type of preparers, it was difficult to take everyperspectiveintoconsiderationandwerethereforcompoundedintoindustries,seecategorisationofregionandindustryinAppendix5.TheindustrycategorisationwasinspiredbythesamecategorisationasIFRSuseswhenpresentingcommentlettersummaries(IFRS,2011).

Figure4.3.2.1–Thecodingschedule

Commentletterby preparer

Geographicalregion Industry

Position onthequestionof asinglerevenuestandard?

Position

Agree withEDQ1

Supportingarguments

Economicarguments

Botheconomicandsociological

arguments

Sociologicalarguments

Nosupportingarguments

DoesnotagreewithEDQ1

Supportingarguments

Economicarguments

Botheconomicandsociological

arguments

Sociologicalarguments

Nosupportingarguments

Noposition

ElsaWachtmeister MartinStrömland BUSN69

22

4.3.2.2 Categorisation whether the respondents agree or not agree with the one single revenuerecognitionstandard

Whencodingthecommentletters,wewantedtoinvestigatewhethertheprepareracceptsoropposeswiththeonesinglerevenuerecognitionstandard.Question1oftheDiscussionPaper(IASB,2008)sentoutinthedueprocessaimstoinvestigatethismatter.Thequestionis:

“Doyouagreewiththeboards’proposaltobaseasinglerevenuerecognitionprincipleonchangesinanentity’scontractassetorcontract liability?Whyorwhynot?Ifnot,howwould you address the inconsistency in existing standards that arises from havingdifferentrevenuerecognitionprinciples?”IASB(2008,p.14)

The decision to categorise whether the preparer agree or disagree with the one single revenuerecognitionstandardwasnotalwaysasimpletask.Somerespondentsansweredwithclaritywhichmadethecategorisationeasy.Apositiveapproachcouldbecodedbyaquotesuchas:

“We fully support the boards’ intention to develop a single principle for revenuerecognitionandhenceeliminatetheinconsistenciesbetweencurrentIAS11ConstructionContractsandIAS18Revenue.”-DeutscheTelekomAG(2009,p.2)

Anevidentnegativeresponsecouldbe:

“No.Historically,revenuesarerecognizedwhentheyarerealizedorrealizable,andareearned(whengoodsand/orservicesaretransferredorrendered.).Underthematchingprinciple expenses are recognized when goods and/ or services are transferred orrendered and offset against revenues generated from those expenses. Applying theboards’proposedmodelwouldviolatetheseprinciples,causingmismatchingofcostsvs.revenuesforlong-termcontracts.“-DeeBrownInc.(2009,p.1)

Sometimes the responseswhether theprepareragreeordisagreeneededdeeperdeliberations. Itcouldsometimesbetimeconsumingforustoconcludeawellthoughtcategorization.Anexampleofamoreproblematiccommentlettertodeciphercouldbe:

“TheSwatchGroupwelcomestheworkoftheboardstoissueacomprehensivediscussionpaperthataddressespossibleshortcomingsofIAS11andIAS18.Suchastandardshouldincrease the transparency of the recognition of revenue for the users and result inrequirements that are practicable for the preparers.We therefore view the discussionpaper as a positive first step. Nevertheless, after having analysed the impact of thediscussion paper on the financial statements of Swatch Group, we established thefollowingconcerns:”-TheSwatchGroupLtd(2009,p.2)

Afterdeliberationwe chose tobelieve this answer corresponds to anegative attitude to thenewstandard proposal and therefore categorised as "do not agree". We found too many negativeargumentsinthecommentlettertobelievethecompanyactuallyisinfavouroftheonesinglerevenuerecognitionstandard.

ElsaWachtmeister MartinStrömland BUSN69

23

4.3.2.3Examplephrasesofeconomic&sociologicalarguments

To categorise the argumentationsof the respondentsby their standpoint, the argumentationwasbasedon chosen theories inChapter2 (Kelly-Newton, 1980;Hussein, 1981;Watts&Zimmerman,1978,1990andDavisetal.1997)whichprovideduswithaframeworkofwhypreparersreacttonewtypesofaccountinginnovations,eitherbasedoneconomic,sociologicalorbothtypesofarguments.Inaddition,weaimedforaninductiveapproachandidentifiednewtypesofargumentationpatternswhichhavebeennotedinthecodingunderOtherthoughts,seeAppendix1.

Examplequoteswhichwecategorisedassociologicalargumentsarerelatedtothepreparersnorms,complexityinapplyingthenewstandardandresistancetobeinthescopeofthenewstandard.

Examplequotesregardingthattheaccountinginnovationcontrarytonorms:

"Inrelationtoourindustry,webelievethatcurrentstandardsinSOP81-1,SAB101andSAB 104 provide decision-useful information to the users of financial statements forengineeringandconstructionindustry,butwhicharenotevidentintheproposedmodel.”-URS(2009,p.8)

"Inthiscaserevenueisdelayedtotheendoftheproject.Inthiscaserevenuewillnotbeagoodmeasureoftheworkthatthesupplierhasbeendoingandtheuserofthefinancialstatementswouldgainanincompletepictureofthecompanyactivities."-Fujitsu(2009,p.2)

Examplequotesregardingargumentsforthecomplexityinapplyingthestandard:

"The application of the proposed revenue allocation model as it relates to... may bedifficult to implement... the proposals in the discussion paper need to be explainedfurther..."-Telstra(2009,p.1)

“Developing a single revenue recognition model is difficult due to the complexity ofrevenuetransactionswithvaryingcontractualrightsand...."-IntelCorporation(2009,p.1)

Examplequotesregardingargumentsforbeingscopedoutofthestandard:

"Wewouldotherwisebeinfavourofallowingforanexceptiontothegeneralprinciplesforthesespecificsituations"

-SyngentaInternationalAG(2009,p.2)

“Webelieveallfinancial instrumentsshouldbescopedoutoftheproposedmodel/newrevenue recognition standard as the nature of financial instrument contracts arefundamentallydifferentfromthecontractdescribedintheDP…”-DeutscheBankAG(2009,p.1)

Examplequoteswethathavebeencategorisedaseconomicargumentsarerelatedtowhethertheaccounting innovationwill result in financialburdenfor thepreparer,or if thepreparerargues forflexibilityintheapplicationoftheaccountingstandard.

"ThenecessitytoimplementnewITsystemsandtherecognitionofassetsandliabilitiesonacontract-by-contractbasiswouldsignificantlyincreasethelevelofinternalcontrolsnecessarytoensurecompliancewiththeproposedmodelinourfinancialstatements.Weacknowledgethattheseadditionalcostsareonlyindirectlylinkedtotheproposedmodelbutwebelievethattheyshouldbetakenintoaccountinanycost/benefit-analysisoftheproposedmodel."-DeutscheTelekomAG(2009,p.6)

ElsaWachtmeister MartinStrömland BUSN69

24

"anyrevenuerecognitionconceptneedstobeflexible"-SiemensAG(2009,p.1)

InFigure4.3.2.3, inthecontextofcodingacommentletter,wehavehighlightedquoteswhicharealignedwitheconomicandsociologicalarguments.

Figure4.3.2.3–Exampleofconductedcoding

4.3.3Reportingphase

Whenthedatahasbeencollected,thereportingprocessstarts.Inordertodososuccessfullythedatahastobesimplified,analysedandputintocategories(Elo&Kyngäs,2008).Inthisstudy,thepreparerrespondentswerecategorisedintogroupsasgeographicalregion,industry,opinionandwhattypeofargumentationcommunicated.Furthermore,thedatawasusedtocreatevarioustablesandpiechartsin Excel and X2-tests that was conducted in SPSS in order to present the information in anunderstandableandoverallmanner.

4.3.3.1TheX2-method

TheX2-method testsweremade inorder to complement thevarious tablesandpie chartson thedifferencesbetweenregionsandindustriesintheiropinionsandarguments.AX2-testisastatisticaltestonappliedsetofcategoricaldatatoestimatethepossibilitythatanyobserveddifferencebetweenthe sets occurred by chance. By observing our tables, it might look like there are differences inopinions and arguments between regions and industries.Hence, in order to confirmwhether ourresultsarestatisticallysignificantorbasedonchancewaspossiblebymakingX2-tests.Thetestmethodinvolves a comparison between the observed class frequencies with corresponding expectedfrequencies,whicharecalculatedontheassumptionthatthenullhypothesis(H0)youwanttotryis

ElsaWachtmeister MartinStrömland BUSN69

25

correct(Körner,1985).TheX2-testsanswerwhethertheresultswehaveinthesamplevaluationdiffersfromthevaluationofthenullhypothesis.Itisestimatedbythep-value.Thesignificancelevelisatap-valueat0,05,meaningthatifthecorrelationsshowap-value≤0,05,werejectthenullhypothesis.Ifthecorrelationshowsap-value>0,05,thenullhypothesiscannotberejectedandthatthereisnostatisticsignificance(Körner&Wahlgren,2015).

InordertoperformtheX2-testswehadtomakesomelimitations.Inordertoperformanadequateapproximation, itusually setsasageneral rule that all expected frequenciesmustbeat least five(Körner,1985).Inothercases,amergeroftwoormoreclassescantakeplaceinordertomeetthecondition.Inourrathersmallsampleof81commentletterswehadtomakesomemergesinordertoperformtheX2-tests.When testing if therewasacorrelationbetweenhow industriesargueswitheconomic, both economic & sociological and sociological arguments, wemerged solely economicarguments with economic & sociological arguments to raise the frequency of the group to thedesirableminimum.Inaddition,the"nonarguments"wereexcluded.Wedidnotbelievethiswouldmake poorer results, because it is relevant to distinguish between those industries who argueeconomicandthosewhodonot.

We also had to exclude preparers from Africa and Asia from the statistical testing because theycontributedwithmuchlesscommentlettersthanNorthAmericaandEurope.Itwouldhavebeentoosmall frequencies and subsequently contributed to a misleading result. Moreover, the industrieswhich sent a small number of comment letters; consumer goods, consulting, Medical & pharmachemicalsandenergy&utilities,hadtobeexcludedinordertoconductaX2-test.

Thenullhypothesiscannotberejectedifthetestfunctionvalue,X2-sum,fallsbelowacertaincriticalvalue.Theapproximationrequiresthattheexpectedfrequenciesarenotoverlytoosmall.Thegeneralrulesarethatnoexpectedfrequencyistobelessthan1,andthatmaximumof20%oftheexpectedfrequenciesistobelessthan5(Körner&Wahlgren,2015).

4.4Empiricalsample

Whenwemadethedecisiontomakeacontentanalysisonthecommentlettersentbypreparers,wehadtomakeachoicewhichstageinthedueprocessweshouldfocuson.ThedueprocessofIFRS15havefourdifferentstageswherethepossibilitytosendcomment letterweregiven. Inthe lightofwhatSutton(1984)stated,whichisfurtherstrengthenbyGiner&Arse(2012),isthatpreparerstendto try to affectpolicymakers in early stages in theaccounting standard settingprocess since it isassumedtohavegreateraffectduetothatdifferentalternativesarestillunderconsideration.IntheprocessofsettingthestandardofIFRS15,thediscussionpaperisthefirstdocumentwhichisbeingopen for comments. Hence, we chose to investigate the comment letters to that document.Furthermore,weconsideredthedocumentofthediscussionpapertocontainquestionsconcerningthe main principles and objectives of the new revenue recognition standard rather in the latterdocumentsinthestandardsettingprocess,suchastheexposuredraftswheremorespecifictechnicaldetailsarepresent.

Based on the questions in the discussion paper, we observed the preparers opinion and theirargumentswhethertheyacceptoropposestheproposedstandard.Someofthepreparerrespondentshavefollowedeachandeveryquestionofthediscussionpaper,andansweredtoitsspecificissue,butthemajorityhavewrittenageneralanswerwithoutaclearstructure.TheanswertoQuestion1 isalmostalwaysincludedwithinthegeneralsectionorunderQuestion2.Question2referstowhetherthestandardwillprovidedecision-useful information,wheremanypreparersarguesprosandconsabouttheimplementationofthestandard,seeAppendix6.Therefore,wewereoftenrequiredtoreadthe whole comment letter since the opinions and arguments towards Question 1 could existthroughoutthedocument.

ElsaWachtmeister MartinStrömland BUSN69

26

Outof a total of 211 respondentsof thediscussionpaper, 81of themwere sent frompreparers,constitutingthelargestgroupofrespondentsatapercentageof38%.Allofthe211originalcommentletters are published on IASB's and FASB's webpages, where the preparers were identified anddownloaded.

Whenweidentifiedthetestingsampleselectionwehadtomakesomelimitationstogetasareliableandrepresentablepictureoftheproportionofthepreparersaspossible.Thisstudyfocusonsinglepreparers, meaning that trade associations representing dozens or hundreds of companies wereexcludedfromthetestingsample.Webelievedthecommentlettersfromtradeassociationscouldnotbecoupledtoalloftheindividualcompanies'specificopinionsandarguments.Thesamedecisionwasmaderegardingcommentletterssentfromasmalleramountofcompanies,whichwedecidedtobeamaximumof5units,wherearepresentativefromonlyonecompanyrefersto"onthecompany’sbehalf..."andonlythatcompanyrepresentativesignatureispresent.However,ifasmalleramountofcompanieshadwrittenacommentletterjointly,referringto"we"andthepresenceofsignaturesbyrepresentatives fromallof thecompaniesexisted,weacceptedthecomment lettertooursamplereferringtheopinionsandargumentstoeachindividualcompany.

4.5Evaluationofmethod

Replicability, reliability and validity is usual aspects and important subjects in an assessment of abusinessresearch.

Reliabilityisdefinedastowhethertheinvestigationresultwouldbethesameifthestudywouldbeconductedagainoriftheresultisbasedonrandomoroccasionalconditions.AsBryman&Bell(2007)state,itisalmostimpossibletoconductacontentanalysisthatiscompletelyfreefrominterpretationandhavingasubjectiveapproachfromtheencoders'side.Wehaveinourstudyputalotofefforttoget familiarwith the comment letters thatwe laterworked onwhen conducting the analysis. Byreadingseveralcommentletterstogetherbeforewestartedthecoding,webelievedthatwetothegreatest extent as possible designed a coding manual that could provide us a generalizableimplementation.Sincewedoaquantitativeanalysisbasedonqualitativedata,wehaveconductedthecodingofeverycommentlettertogethertoincreasethereliability.Bymanuallyconductingthecoding,Krippendorff(2013)explainshowhumanscananalysecontentinawaythatcomputersfinddifficult,creatingabetterunderstandingofthematerial.Thisiswhywecodedmanually,inordertoensurethateverycommentlettergotthesameprocess.Further,alloftheimportantquestionsthatoccurredduringtheworkprocessweresolvedtogetherafterdiscussingthemandreachinga jointconclusion.

Bryman& Bell (2007), describes replicability as the possibility to reproduce or repeat a study. Asmentioned,contentanalysisisaveryopenresearchmethodwherethesampleselectionandcodingisdescribedconcretely.Sincethedocuments,thecommentlettersareavailableatIASB'sandFASB’swebsites; there are no obstacles to repeat our study. We have aimed to be as descriptive andtransparentof the conductedmethod throughout thewhole chapter to increase thepossibility tomakeareplicablestudy.Thisisaprerequisitetoaccessthepossibilitytoreplicateacomparativeandcross-sectionaldesignstudy(Bryman&Bell,2007).

Validityistoassesswhetherthechosenmethodactuallyprovidesavalidgroundtodrawarelevantconclusion.Twovariouskindsofvalidityareinternalandexternalvalidity.Internalvalidityisbasedoncausality,meaningthatwhichisintendedtobemeasuredisactuallymeasured(Bryman&Bell,2007).The study investigated the opinions and arguments used by preparers fromdifferent regions andindustrialsectors.Thiswasfeasiblebyreviewingtheiraccessibleoriginalcommentletters,whichasmentioned in Chapter 4.3 is perceived as a reliable, since is it a primary source and can arguablyincrease the research’s internal validity. Sending comment letters is a way for the preparers to

ElsaWachtmeister MartinStrömland BUSN69

27

influencetheaccountingstandardsetting.Hence,manyofthepreparersopinionsandargumentsareoftenclearlystatedinorderforthepreparertobeunderstoodandevaluatedbythestandardsetter.Ifnot,wehavehadguidelineswhichareaddressedinChapters4.3.2.2&4.3.2.3inordertocollectconsistent information in thecodingprocess. Inaddition,wehavegonethroughseveralcommentletterstwiceinordertoensureconsistency.Nevertheless,researchesbasedonacomparativedesignusuallyhaslowinternalvalidity.Basedonthecollectedinformationandresults,itishardtoexplainthereasonsfortheoutcome(Bryman&Bell,2007).However,thestudywasbasedontheassumptionthatthedifferenttypesofargumentationrepresentsthereasonwhyapreparerwanttoparticipateinthedueprocess.Wethinkitisavalidassumption,sincewedonotbelieveapreparerwithoutanyobjectionswithsubsequentargumentationwouldparticipateatall.

Externalvalidityisbasedontheextenttowhichthestudycanbegeneralisedbeyondthespecificstudycontext.Sincewedidnotmakearandomselectionofthepopulation,theexternalvalidityisdoubtful(Bryman&Bell,2007).Thus,thestudyresultscannotbeperceivedasgeneral.Nevertheless,ourstudyisbasedonthecommentlettersonthediscussionpaperdocumentofthedueprocessofIFRS15,andourpurposeistocontributetotheresearchlandscapefocusingontheprepareraspectofaccountingstandardsetting.Hence,ourstudyontherecentlypublishedandlongwaitedstandardofIFRS15canbroadentheunderstandingofwhypreparerschoosetoparticipateinthedueprocess.

4.6Ethicalconsiderations

Ethicalconsiderationshavebeentakenintoaccountduringthewholeworkprocess.Ethicalprincipleshavebeenbrokendowntofourmainareas(Diener&Crandall,1978citedinBryman&Bell,2007)thesearewhether there is;harm to theparticipant,a lackof consent, an invasionofprivacyor ifdeceptionisinvolvedintheresearch.Thedocuments,thecommentletters,thathasbeenexaminedinordertoconductthecontentanalysisarepubliclypublishedonIFRSwebpageandareonlywithheldfromthepublicand thewebsite if theremightbeanyharmfor thesubmittingparty (IFRS,2013).Hence,thismeanswedidnothavetodealwiththeissueofdataanonymityandconfidentialitywhichaccordingtoBryman&Bell(2007)raisesparticularproblemsformanymethodsofqualitativestudies.Thepreparerswhichsentcommentlettersareawarethatthecommentlettersarepublishedpublicly,whichmadenolackofconsentinusingthecommentlettersasempiricaldata.Deceptionmeansthatthe researchers present their research to something other than it is (Bryman & Bell, 2007). Ourambitionhasbeentobeasconsistentandunbiasedaspossiblewhilereadingandinterpretingthecontentofthecommentletters,aimingforhighlevelofobjectivity.Nevertheless,weacknowledgetherewereprobablysomeextentofsubjectiveapproacheswhichmightaffecttheconclusions.

ElsaWachtmeister MartinStrömland BUSN69

28

5.EmpiricsThischapterdescribestheresultsofthestudyofthecommentlettersonthefirstdiscussionpaperinthedueprocessofIFRS15.Asthecodingmanualinthemethodologychapterexplains,andasseeninAppendix1,thecodingprocesshasprovidedthethesiswithinformationregardingnumerousaspects.Thesewillbefurtherpresentedintheorderofthecodingmanual.

5.1Region

Thecountriesarecategorisedaccordingtoregion,theresultis;37preparersfromNorthAmerica,33from Europe, 9 fromAsia and 2 fromAfrica. North America and Europe is almost singlehandedlyrepresentinghalfofthetotalcommentletters,resultinginAsiaandAfricaasundisputedlyminorities.Givingatotalof81commentlettersprovidedbypreparers.

Figure5.1

5.2Industry

Theresultshowsthatrespondentsfromsomeindustriesaremoreactiveintheprocessofdevelopingthe accounting standard. As the most frequent participating preparers, construction, technology,financials and utilities & transport industries appear as themost active. Even if preparers in theconsumergoods-andconsulting industriesareseentoberelatively lessactive,oneshouldbare inmindthatthere isat leastsomeactivity,thereare industrieswhichdonotparticipateatall inthisprocess.

46%

41%

11%

2%

Regionalcommentletterfrequency

NorthAmerica(37)

Europe(33)

Asia(9)

Africa(2)

ElsaWachtmeister MartinStrömland BUSN69

29

Figure5.2

5.3Preparers’opinionregardingthedevelopmentofIFRS15

Asforwhetherthepreparerofthecommentletterhasaclearopinionregardingwhethertheyagreeordisagreewiththedraftedproposalsofthediscussionpaper,theconductedcontentanalysisfindseverysinglepreparertohaveaposition.Onthequestionofwhethertheprepareragreeswiththeproposalofasinglerevenuestandard,thecontentanalysisshowsthat55preparers(68%)agreesand26(32%)donotagree.AllofthepreparersopinionareaccountedforinFigure5.3.

Figure5.3

21%

2%

2%4%

18%15%

4%

20%

14%

Industrycommentletterfrequency

Construction(17)

Consultingfirm(2)

Consumergoods(2)

Energy&utilities(3)

Financials(15)

Industrialsandtransport(12)

Medical&pharmachemicals(3)

Technology(16)

Telecom(11)

68%

32%

Overallagreementwithsinglerevenuestandard

Yes No

ElsaWachtmeister MartinStrömland BUSN69

30

5.3.1Whichregionsagreewiththeproposedsinglerevenuestandard?

Table5.3.1showshowdifferentregionsagreeordonotagreewiththenewsinglerevenuestandard.Alloftheregionsareinmajoritypositivetothenewstandard.Lookingatthepercentage,Asia(78%)andAfrica(100%)aremostpositive,butshouldberecognizedassmallergroupsofrespondents.NorthAmerica(70%)andEurope(61%),whichtogetheranswer86%ofthetotalpreparersarepositivebutwithaslightlymoreevendistributionofopinions.

Agreeordisagreewithasinglerevenuestandard?Regions Yes No Total %Yes %No

NorthAmerica 26 11 37 70% 30%Europe 20 13 33 61% 39%Asia 7 2 9 78% 22%Africa 2 0 2 100% 0%

Allregions 55 26 81 68% 32%

Table5.3.1

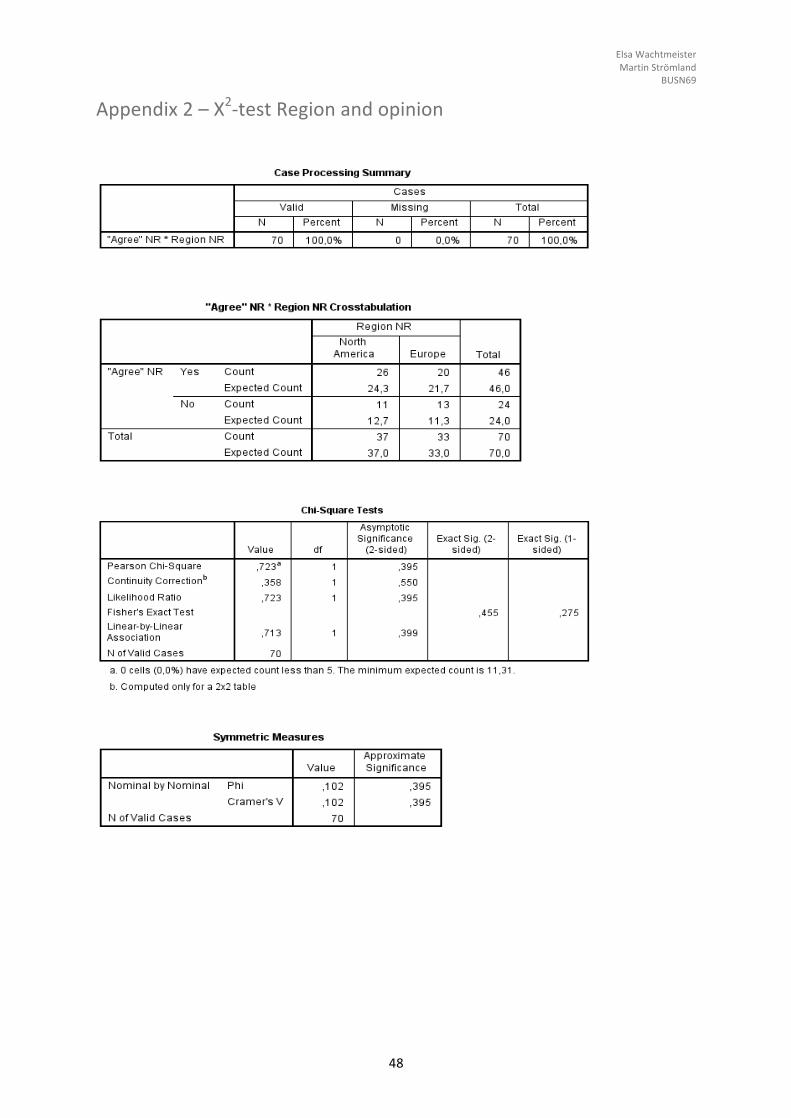

TheobservationsinTable5.3.1.1aretestedwithaX2-test.Thetestshowsnosignificanceatap-valueat0,395(Appendix2).

(H0): There are no differences in regions whether they agree with the single revenuerecognitionstandard.

We can therefore not reject (H0), there are no statistically significant differences among regionswhethertheyagreewiththesinglerevenuestandard.

X2-test-Agreeordisagreewithasinglerevenuestandard?Regions Yes No Total %Yes %No

NorthAmerica 26 11 37 70% 30%Europe 20 13 33 61% 39%

Allregions 46 24 70 66% 34%