what is in store for pe investors in 2017? - tax | advisory systematic analysis ... competitive...

TRANSCRIPT

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 1

What is in store for PE investors in 2017?

April 2017

2 © 2017 Grant Thornton (Vietnam) Limited. All rights reserved.

Grant Thornton is one of the world’s leading organisations of independent assurance, tax and advisory firms. These firms help

dynamic organisations unlock their potential for growth by providing meaningful, forward looking advice.

About GRANT THORNTON INTERNATIONAL

A truly global organisation

$4.8bn revenue in 2016

(USD)

47,000 people in over

140 countries

Global

assurance revenues

$2.025bn

tax Global

revenues

$1.018bn advisory Global

revenues

$1.652bn

other

services

Global

revenues

$94m

3 © 2017 Grant Thornton (Vietnam) Limited. All rights reserved.

About GRANT THORNTON VIETNAM

$5.1* $5.1 MILLION REVENUE

PARTNERS

OFFICES 2

14 PARTNERS

250 PEOPLE

high-quality services

insightful systematic analysis

The only foreign invested firm in Vietnam that holds a Business Valuation

License from the Ministry of Finance.

Grant Thornton is a

LEADING

BUSINESS ADVISER

adding value to

clients performance

Approved by SSC to audit Public Interest Entity in security sector in Vietnam.

Audit Tax Advisory Outsourcing

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 4

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved

Agenda

Investment environment

Investment considerations

Investment portfolio

Planning an exit

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 5

INVESTMENT ENVIRONMENT

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 6

Economic outlook over the next 12 months

1 General Statistic Office

78% participants express optimistic view toward Vietnamese

economic situation, yet 2016 marked certain difficulties for

Vietnam’s economy

• In 2016, GDP growth rate achieved 6.21%, exceeding World

Bank’s expectation

• New trade opportunities thanks to Vietnam for being a part of 16

other FTAs with Korea, EU, Russia and ASEAN

• China’s economic slowdown is considered the most negative

factor on Vietnam investment environment

• Despite the expected demise of TPP, it appears not to have

negative impact on the economy

GENERAL OUTLOOK FOR THE VIETNAMESE

ECONOMY OVER THE NEXT 12 MONTHS

55%

78%

40%

20%

5% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2017

Negative

Neutral

Positive

THE IMPACT OF EVENTS HAPPENING IN 2016 TOWARD VIETNAM

INVESTMENT ENVIRONMENT

41%

2%

24%

13%

39%

43%

41%

22%

15%

39%

28%

46%

4%

15%

7%

20%

0% 20% 40% 60% 80% 100%

China economic slowdown

FED increased interest rate

Oil hit multi-year low

US Presidential Election

Most impact Significant impact Less impact Least impact

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 7

Investment outlook

FORECAST LEVEL OF INVESTMENT

ACTIVITY IN VIETNAM

LEVEL OF INVESTMENT

ATTRACTIVENESS, COMPARED

BETWEEN OTHER S.E.A REGION

VIETNAM RANKING IN TERMS OF

INVESTMENT ATTRACTIVENESS

2%

11%

78%

9% Significantly Decrease

Decrease

Stay the same

Increase

6%

22%

70%

2%

Less attractive

Neutral

More attractive

Extremely attractive

2%

2% 20%

41%

28%

7% Other

Laos

Cambodia

Indonesia

Myanmar

Vietnam

Philippines

Level of investment activity in

Vietnam is expected to increase

There was US$15.8 billion newly

registered and additional capital

contributions from existing FDI

enterprises

Vietnam is ranked second as

attractive investment destination

Myanmar is the most promising

investment spot

Vietnam’s investment

environment is considered

“more attractive” due to

highly competitive, abundant

labor, low cost and the

growing middle class and

income

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 8

28%

54%

35%

20%

20%

33%

9%

15%

37%

33%

48%

65%

52%

46%

41%

30%

35%

13%

17%

15%

28%

22%

50%

54%

0% 50% 100%

Constant changes in economic policies on Monetary policies, laws, investment …

Corruption

Government red tape/ processes

Infrastructure

Low labor productivity

Management team's long-term strategies

Negative sentiment about Vietnam from regional/ global investors

Weak macroeconomics

Most critical Critical Less critical

Investment obstacles

INVESTMENT OBSTACLES IN VIETNAM

Corruption is

the most critical

investment

obstacle 87%

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 9

INVESTMENT CONSIDERATIONS

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 10

52%

24%

11%

11%

2%

0% 10% 20% 30% 40% 50% 60%

Others

Corporate divestments

Secondary buyout deals Public market

Private/ family owners

Sources of transactions DO YOU EXPECT TO BE A NET BUYER OR SELLER OF

ASSETS OVER THE NEXT 12 MONTHS? SOURCES OF DEALS IN VIETNAM

52%

Source of deal comes from

“SOE equitisation”

Participants expect to

be net buyers in the

next 12 months 70%

Implementation of Resolution 35/NQ-CP to support enterprises up to 2020

Decision 58 aimed to accelerate the process for SOEs although there are certain difficulties in speeding up

the process as planned

56%

35%

9%

70%

20% 11%

0%

20%

40%

60%

80%

Net Buyer Neutral Net Seller

2016

2017

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 11

Competition on M&A transactions

FROM WHICH SOURCES DO YOU FORESEE THE MOST

COMPETITION FOR DEALS OVER THE NEXT 12 MONTHS?

2%

Domestic Private Equity fund

9%

Foreign/International Private Equity funds

16%

Strategic Partners

Public Markets

49%

Family Offices

Others

Competition for deals

24%

0%

49%

Respondents

claim

“Foreign PE

fund” to be

the most

competitive

source of M&A

activities

M&A activities in Vietnam increased rapidly with significant multimillion

and multibillion deals

The latest notable M&A transaction was in mid-December 2016 between

Fraser & Neave Ltd. (F&N) and Vinamilk

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 12

Healthcare and

Pharmaceuticals

Industry attractiveness INDUSTRY SECTORS IN VIETNAM

16%

9%

27%

24%

53%

38%

24%

24%

7%

33%

49%

22%

38%

31%

24%

29%

29%

31%

31%

29%

38%

29%

24%

24%

31%

24%

29%

22%

33%

20%

11%

27%

24%

27%

7%

16%

18%

31%

22%

18%

16%

4%

27%

2%

4%

16%

4%

22%

13%

4%

7%

11%

7%

29%

7%

2%

7%

7%

36%

13%

4%

9%

4%

0% 20% 40% 60% 80% 100%

Agriculture

Clean-tech

Education

Financial Services

Food and Beverage

Healthcare and …

Hospitality and Leisure

Manufacturing

Oil, Gas and Natural …

Real Estate/ Property

Retails

Software and IT

Transportation and …

Very attractive Somewhat attractive Neutral Somewhat unattractive Very unattractive

49%

Food and beverage

↑3%

38%

↑1%

38%

↑7%

Transportation and

logistics

53%

↑8%

Retail

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 13

Key factors to be considered when investing in

private companies

THE MOST IMPORTANT FACTORS TO CONSIDER

WHEN INVESTING IN VIETNAM

21%

“Transparency in

business activity” is

considered as the most

important issue, with

21%

“Growth story/forecast”

is ranked second by

18% respondents 18%

7%

11%

18%

10% 9%

10%

2%

7%

21%

4%

1% Brands/ Products Cash flow

Growth story/ forecasts Operational/ Cultural fit Strategic fit

Target's management support Tax shields and investment savings Track record Transparency in business activities Speed at which value can be created Others

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 14

Key factors to be considered when investing in

private companies

MOST CONCERNING ISSUES WHEN INVESTING IN VIETNAM

43%

18%

11%

25%

14%

11%

45%

41%

32%

34%

27%

52%

48%

43%

14%

25%

43%

39%

25%

16%

9%

23%

9%

9%

7%

16%

2%

2%

2%

2%

9%

2%

0% 20% 40% 60% 80% 100%

Corporate Governance

Existing shareholders

Finance/ Debt issues

Financial records and reporting

Skills/ Experience of existing management

Sustainability

Transparency

Very concerned Concerned

“Transparency” and

“Corporate Governance”

are continuously chosen

as top two fears for PE

investors in Vietnam

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 15

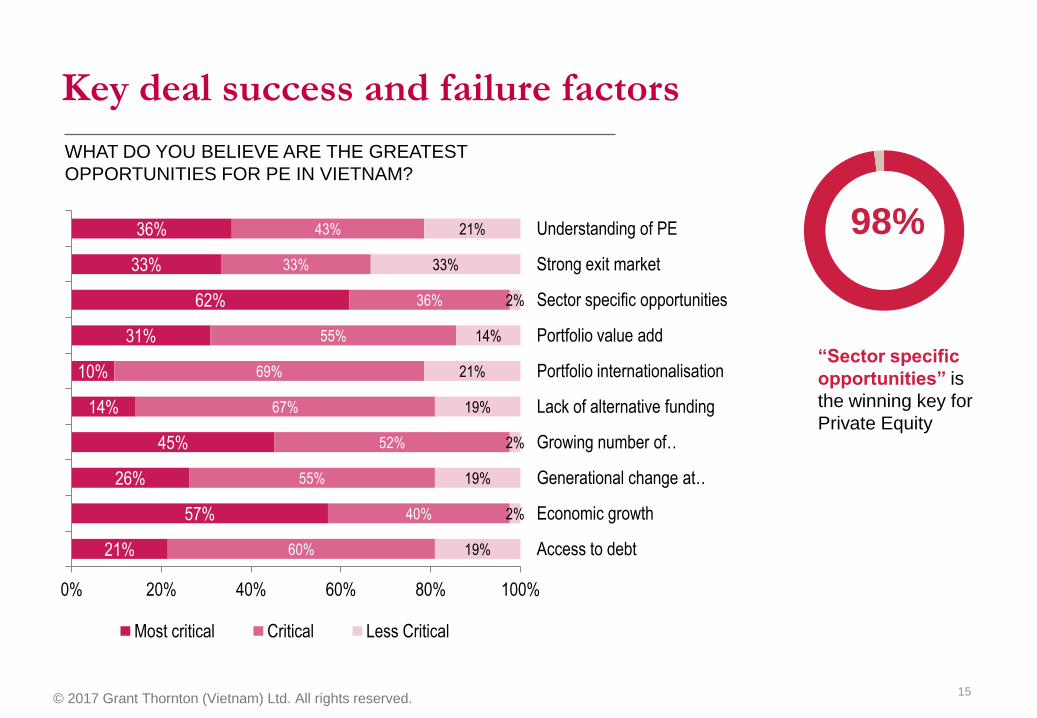

Key deal success and failure factors

WHAT DO YOU BELIEVE ARE THE GREATEST

OPPORTUNITIES FOR PE IN VIETNAM?

21%

57%

26%

45%

14%

10%

31%

62%

33%

36%

60%

40%

55%

52%

67%

69%

55%

36%

33%

43%

19%

2%

19%

2%

19%

21%

14%

2%

33%

21%

0% 20% 40% 60% 80% 100%

Access to debt

Economic growth

Generational change at …

Growing number of …

Lack of alternative funding

Portfolio internationalisation

Portfolio value add

Sector specific opportunities

Strong exit market

Understanding of PE

Most critical Critical Less Critical

98%

“Sector specific

opportunities” is

the winning key for

Private Equity

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 16

Key deal success and failure factors FACTORS CAUSING DEAL FAILURE

“Resistance to sharing

deal risk” and “Difference

in valuation expectations”

shared the top two key deal

breakers

79%

43%

21%

33%

55%

12%

48%

29%

26%

33%

33%

31%

24%

43%

29%

50%

31%

17%

17%

12%

5%

24%

12%

14%

12%

5%

10%

2%

2%

7%

10%

5%

17%

2%

19%

21%

14%

14%

2%

2%

14%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Changing the deal

Cultural gap

Delays to the completion of deals and legal restrictions on deal structures

Difference in Valuation expectation

Lack of conviction to close

Non-disclosure of material items at the appropriate time

Resistance to sharing deal risk

Unexpected departure of key employees during the due diligence

Most critical Critical Neutral Less critical Least critical

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 17

INVESTMENT PORTFOLIO

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 18

55%

The required rate of return for PE investment portfolio

THE REQUIRED RATE OF RETURN FOR PE

INVESTMENT PORTFOLIO

Higher required rate of returns to compensate

for higher risks

Required rate of return for investment “Above

22%” in 2017 is nearly double than that of 2016

33%

5%

40%

21%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2017

Above 22%

Below 15%

From 15%-18%

From 18%-22%

IMPORTANT DRIVERS OF VALUE

14%

31% 55%

Financial Engineering

M&A growth

Market growth

Performance Improvement

Others

55% participants

choose “Performance

improvement” to be

the key value growth

driver

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 19

Hands-on involvement with portfolio companies

PARTICULAR AREAS FOR HANDS-ON INVOLVE MENT WITH

PORTFOLIO COMPANIES

1%

3%

6%

7%

10%

10%

13%

13%

17%

20%

0% 5% 10% 15% 20% 25%

Other

Operational Input

Managing Banking …

Innovation

Sector Knowledge

Cost Control

Access to Capital

Strategic Input

Financial planning

Governance

20%

“Corporate

Governance” is

flagged as the

most important

area of hands-on

17%

“Financial

planning” is

considered the

second most important area

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 20

PLANNING AN EXIT

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 21

Access to finance

THE AVAILABILITY OF DEBT FINANCE FOR

PRIVATE EQUITY INVESTMENT WITHIN

VIETNAM

THE COST OF DEBT OVER THE NEXT 12

MONTHS

19%

21% 55%

5% Decrease significantly

Decrease slightly

Stable

Increase slightly

Increase significantly

Debt finance in Vietnam is

considered difficult to obtain by

47% PE survey participants

Interest rates will increase slightly

Lending rates were kept stable, decreasing 0.5-1%

compared to the beginning of 2016

In 2017, the State Bank of Vietnam is expected to:

• Keep lending rates steady

• Boost the economy

• Control inflation under the target of 5%

12%

7%

38%

40%

38%

33%

12%

17% 2%

0% 20% 40% 60% 80% 100%

2016

2017

Very Difficult to Obtain

Somewhat Difficult to obtain Neither Easy nor Difficult to obtain

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 22

Exit multiples

EXIT MULTIPLES FOR INVESTMENT IN VIETNAM FORECAST EXIT MULTIPLES

Increase

Stay the same

Decrease

19%

76%

5%

76% participants expect that the exit multiples is

going to be steady for the next 12 months

6%

15%

63%

10%

6%

2%

29%

45%

19%

2%

2%

<3X EBITDA

3X to 5X EBITDA

5X to 10X EBITDA

10X to 15X EBITDA

>15X EBITDA

15X to 20X EBITDA

>20X EBITDA

2017 2016

45% participants forecast their exit multiples at

5X-10X EBITDA

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 23

Exit strategies

THE MOST ATTRACTIVE OR ACHIEVABLE EXIT

STRATEGY FOR PRIVATE EQUITY INVESTMENT

FORECAST LEVEL OF EXIT ACTIVITY OVER THE

NEXT 12 MONTHS

36%

“IPO" is cited the most selected

exit strategy for PE investors Level of exit

activities is

expected to stay

the same in the

next 12 months

62%

When certain restrictions on foreign

ownership in listed entities have been

removed, public markets are

increasingly more of an option for an

exit strategy

8% 7%

62% 62%

31% 31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2017

Increase

Stay the same

Decrease

23%

36%

40%

33%

2% 6%

7%

0% 20% 40% 60% 80% 100%

2016

2017

IPO Trade sale MBO

Refinancing Others

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 24

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved.

ABOUT THE SURVEY

PRIVATE EQUITY SURVEY PARTICIPANTS IN MARCH 2017

17%

8%

33% 6%

25%

12%

Advisory/ Legal Firm Institutional/ Corporate Investor

Investment Fund/ Fund Manager Private Investor

Security Firms Others

© 2017 Grant Thornton (Vietnam) Ltd. All rights reserved. 25

What is in store for PE investors in 2017?

April 2017

THANK YOU