western european urban rail market for rolling stock systems

TRANSCRIPT

Strategic Analysis of Growth Opportunities in the Western

European Urban Rail Market for Rolling Stock Systems Strong Orders in Light Rail and Automated People Mover Systems is Driving Growth

M77E-18

May 2013

2 M77E-18

Shyam Raman Research Analyst-Rail

Automotive & Transportation

+1-4164952686

Contact the Research Team

Lead Analyst

3 M77E-18

Contents

Section Slide Numbers

Executive Summary 4

Research Scope, Objectives, Background and Methodology 15

Definitions and Segmentation 22

Overview of Trends in the Urban Rail Market 27

Mega Trends and Industry Convergence Implications 43

Urban Rail Market

• External Challenges: Drivers and Restraints 57

Light Rail Rolling Stock 66

• Forecast and Trends 78

• Market Share and Competitive Analysis 87

Metro Rail Rolling Stock 96

• Forecast and Trends 104

• Market Share and Competitive Analysis 112

Automated People Mover (APM)Systems 121

• Forecast and Trends 128

• Market Share and Competitive Analysis 132

Conclusions 138

Appendix 145

4 M77E-18

Executive Summary

5 M77E-18

Executive Summary—Key Findings Automated people movers (APMs) are the fastest growing urban rail segment while light rail has the majority of

infrastructure projects.

Source: Frost & Sullivan analysis.

After a decade of flurried development, growth in light rail systems are stabilizing as most

municipalities have installed light rails.

Though the number of light rail projects is decreasing as compared to the previous decade, light

rail still has the maximum number of greenfield projects.

1

2 APMs represent the fastest growing segment and will have increased their presence by more than

three times in 2021.

3 A total of 406 urban areas have urban rail in active service in countries considered in this study.

The size of the urban rail network expanded by 2,843 km between 2003 and 2012. Metro rail has

higher opportunities in track upgrades, extensions, and signaling systems.

4 63.4 percent of all urban rail projects installed in the last 10 years were light rail systems. A total of

46 new light rail systems have been developed over the last 20 years (1993‒2012) while 30 new

systems are expected to come up in the next 10 years (2013‒2022).

5

European metro rail systems are more active in purchasing new rolling stock as compared to light

rail. No metro fleet operator currently operating has any fleet that is more than 35 years old (on an

average). Italy, France, and the United Kingdom are expected to place rolling stock orders to

replace 1,268 metro rolling stock by 2015.

6 Alstom, Siemens, and Bombardier face threats from Ansaldo, CAF, and Vossloh, which are

significantly increasing their market presence with strong orders for rolling stock.

6 M77E-18

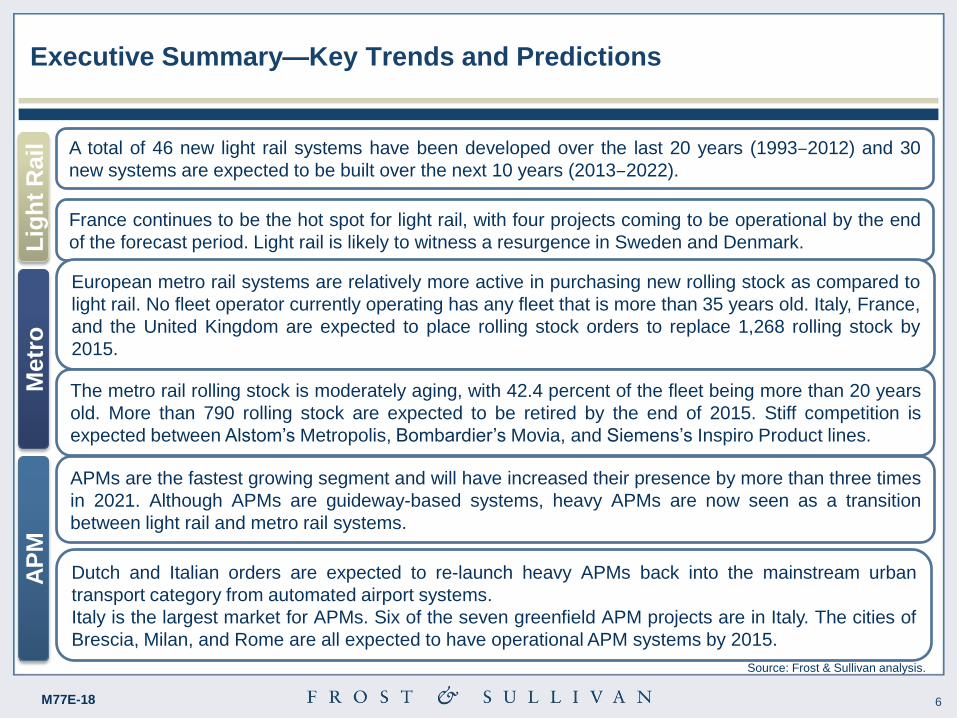

Executive Summary—Key Trends and Predictions

A total of 46 new light rail systems have been developed over the last 20 years (1993‒2012) and 30

new systems are expected to be built over the next 10 years (2013‒2022).

France continues to be the hot spot for light rail, with four projects coming to be operational by the end

of the forecast period. Light rail is likely to witness a resurgence in Sweden and Denmark.

APMs are the fastest growing segment and will have increased their presence by more than three times

in 2021. Although APMs are guideway-based systems, heavy APMs are now seen as a transition

between light rail and metro rail systems.

Dutch and Italian orders are expected to re-launch heavy APMs back into the mainstream urban

transport category from automated airport systems.

Italy is the largest market for APMs. Six of the seven greenfield APM projects are in Italy. The cities of

Brescia, Milan, and Rome are all expected to have operational APM systems by 2015.

European metro rail systems are relatively more active in purchasing new rolling stock as compared to

light rail. No fleet operator currently operating has any fleet that is more than 35 years old. Italy, France,

and the United Kingdom are expected to place rolling stock orders to replace 1,268 rolling stock by

2015.

The metro rail rolling stock is moderately aging, with 42.4 percent of the fleet being more than 20 years

old. More than 790 rolling stock are expected to be retired by the end of 2015. Stiff competition is

expected between Alstom’s Metropolis, Bombardier’s Movia, and Siemens’s Inspiro Product lines.

Lig

ht

Rail

M

etr

o

AP

M

Source: Frost & Sullivan analysis.

7 M77E-18

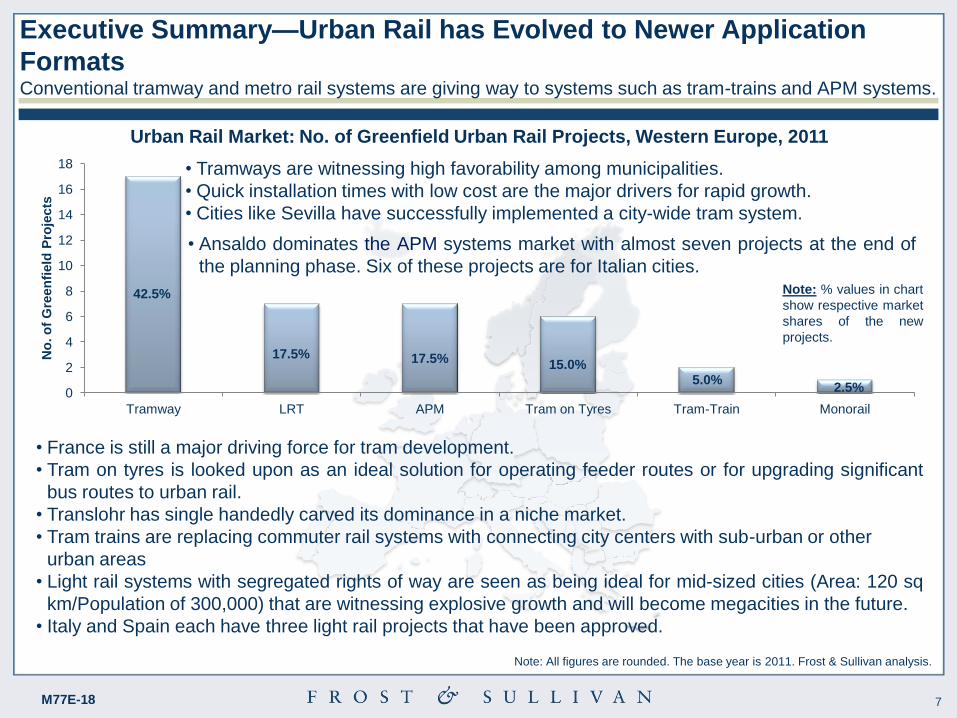

Executive Summary—Urban Rail has Evolved to Newer Application

Formats Conventional tramway and metro rail systems are giving way to systems such as tram-trains and APM systems.

Urban Rail Market: No. of Greenfield Urban Rail Projects, Western Europe, 2011

• France is still a major driving force for tram development.

• Tram on tyres is looked upon as an ideal solution for operating feeder routes or for upgrading significant

bus routes to urban rail.

• Translohr has single handedly carved its dominance in a niche market.

• Tram trains are replacing commuter rail systems with connecting city centers with sub-urban or other

urban areas

• Light rail systems with segregated rights of way are seen as being ideal for mid-sized cities (Area: 120 sq

km/Population of 300,000) that are witnessing explosive growth and will become megacities in the future.

• Italy and Spain each have three light rail projects that have been approved.

0

2

4

6

8

10

12

14

16

18

Tramway LRT APM Tram on Tyres Tram-Train Monorail

No

. o

f G

reen

field

Pro

jects

42.5%

17.5% 17.5% 15.0% 5.0%

2.5%

• Tramways are witnessing high favorability among municipalities.

• Quick installation times with low cost are the major drivers for rapid growth.

• Cities like Sevilla have successfully implemented a city-wide tram system.

• Ansaldo dominates the APM systems market with almost seven projects at the end of

the planning phase. Six of these projects are for Italian cities. Note: % values in chart

show respective market

shares of the new

projects.

Note: All figures are rounded. The base year is 2011. Frost & Sullivan analysis.

8 M77E-18

• After a decade of flurried development, growth in light

rail systems is stabilizing as most municipalities have

installed light rails.

• Further expansion depends on passenger adoption

and demand.

• By 2021, France, Italy, and Spain will have a total of

41 greenfield light rail systems constructed since

2000. (93.2 percent of the total market).

Executive Summary—Light Rail is the Top Urban Rail Choice Although the number of light rail projects has reduced as compared to the previous decade, the maximum

number of greenfield projects are still light rail projects. APM systems constitute the second fastest growing

market.

0

5

10

15

20

25

30

35

40

1980–1989 1990–1999 2000–2009 2010–2019

No

. o

f G

ree

nfi

eld

Pro

jec

ts

APM Light Rail Metro Monorail PRT

“Metro and its costs are unjustified and unwarranted unless you are talking about city sizes

comparable to London, Paris, and Berlin. When we upgrade, we will choose an APM

systems/light metro solution and complement it with new tram/Bus Rapid Transit (BRT) lines.”

– EU Operator & City Council

Urban Rail Market: Trend of Greenfield Urban Rail Projects, Western Europe, 1980‒2019

• APMs represent the fastest growing segment

and will have increased their presence by more

than three times in 2021.

Though the number of projects is

decreasing as compared to the

previous decade, light rail still has the

maximum number of greenfield

projects.

Source: Frost & Sullivan analysis.

9 M77E-18

Executive Summary—Urban Rail Technology Roadmap Energy efficiency is a top priority in urban rail systems. Automatic driverless operation and maximized power

regeneration are the key technology targets.

Urban Rail Market: Metro Rail Technology Roadmap, Western Europe, 2011‒2021

Co

ntr

ol &

Sig

nalli

ng

T

ractio

n

Ro

llin

g S

tock

2011 2013 2017 2021

Communications-Based Train Control + Global

Positioning System Radio infrastructure in wayside

GPS-based control of traffic signals

Aluminium and stainless steel bodies.

Composites to reduce weight

Broadband wireless connectivity to control

centre. Real-time CCTV and monitoring

Electro-pneumatic friction brakes blended with electric regenerative braking. Anti-skid

valves. Brushless 3 phase induction motors. VVVF control

AC Induction Motors

Catenary-free, induction-based

power transmission

Automatic coupler Completely bi-directional trams

Super-capacitors enabled pantograph-less inter-stop tram propulsion

(for example, the Alstom STEEM project)

IGBT Control

Permanent magnet motors

PWM Rectifiers

Lead Acid Batteries Lithium Ion/Sodium Halide/Super-capacitor

Line of sight for trams

Source: Frost & Sullivan analysis.

10 M77E-18

Executive Summary—Forecast of Light Rail Rolling Stock Deliveries France continues to be the hot spot for light rail rolling stock, with four projects likely to be completed by the end

of the forecast period. Light rail systems are likely to witness a resurgence in Sweden and Denmark.

2011 2021

Urban Rail Market: Total Expected Deliveries of Light Rail Rolling Stock, Western Europe, 2011–2021

21.5%

57.8%

11.5% 4.5%

1.8% 2.9%

23.9%

51.5%

12.0%

6.5% 2.2%

3.2%

0.6% 16.5%

2.9%

0.7%

2.3% 5.7%

4.1% 2.8% 0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Denmark France Germany Italy Spain Sweden UK

Exp

ecte

d D

eliv

eri

es o

f L

igh

t R

ail R

ollin

g

Sto

ck

Expected Deliveries of Light Rail Rolling Stock, 2011-2021

Denmark France Germany Italy Spain Sweden The United Kingdom

The 12 km long Swedish Aarhus

light rail project will link two

existing rail lines north and south

of the city, enabling the creation of

a 103 km tram train network.

• Tramways in the cities of Tours and Besançon are expected to commence operations by 2015. Lines

3b,5,6,7 and 8 (planned total of 48.3 km served by 107 train-sets) of the Tramway in Île-de-France are

likely to be completed by 2015.

• The highest number of deliveries is expected to take place in France followed by Germany and Spain.

• Denmark and Sweden are expected to invest in new light rail infrastructure towards the mid-term of the

forecast period.

Note: % values in the bars on the left and right side show the market share.

Note: % values in the center chart show a CAGR

(2011-2021) of rolling stock deliveries for each

country

CAGR

1.8%

Note: All figures are rounded. The base year is 2011. Frost & Sullivan analysis.

11 M77E-18

Executive Summary—Forecast of Metro Rail Rolling Stock Deliveries The highest number of deliveries is expected to be in France followed by the United Kingdom and Spain.

Germany is expected to experience growth towards the mid-term of the forecast period.

2011 2021

Urban Rail Market: Total Expected Deliveries of Metro Rail Rolling Stock, Western Europe, 2011–2021

7..%

16.8%

3.4%

27.6%

18.8%

5.8%

20.6%

6.8%

17.1%

3.4%

28.7%

18.5%

5.9%

19.6%

CAGR

1.3%

0.7%

1.7%

1.1%

1.5% 0.7%

1.5%

1.4%

0

200

400

600

800

1,000

1,200

1,400

Denmark France Germany Italy Spain Sweden The United Kingdom

Exp

ecte

d D

eliv

eri

es o

f M

etr

o R

ail R

ollin

g

Sto

ck

Expected Deliveries of Metro Rail Rolling Stock,2011-2021

Denmark France Germany Italy Spain Sweden The United Kingdom

Germany: The Kleinprofil G and A3L92 rolling stock series from Berlin U-Bahn are expected to be replaced

by the end of the forecast period.

Spain: The forecast period is expected to witness the completion of several urban rail projects sanctioned in

the late 2000s. For example, Line 3 of Metro Bilbao, Lines 9 and 10 of Barcelona Metro, and Malaga Metro.

France and the United Kingdom: The forecast period is expected to witness the retirement and

replacement of the 1973 Stock used in the London Underground Piccadilly Line (528 units) and the Z5300

and MS61 series (717 units) from the Paris RER.

Note: % values in the center chart show

CAGR (2011‒2021) of rolling stock

deliveries for each country

Note: % values in the bars on the left and right side show the market share. Note: All figures are rounded. The base year is 2011. Frost & Sullivan analysis.

12 M77E-18

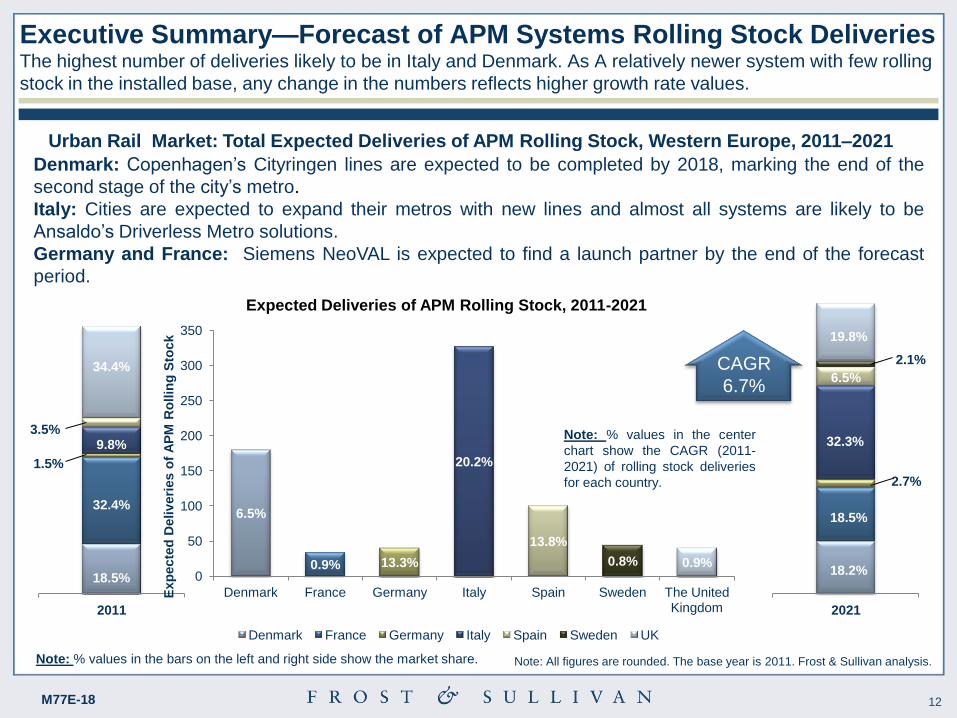

Executive Summary—Forecast of APM Systems Rolling Stock Deliveries The highest number of deliveries likely to be in Italy and Denmark. As A relatively newer system with few rolling

stock in the installed base, any change in the numbers reflects higher growth rate values.

2011 2021

Urban Rail Market: Total Expected Deliveries of APM Rolling Stock, Western Europe, 2011–2021

CAGR

6.7%

6.5%

0.9% 13.3%

20.2%

13.8%

0.8% 0.9% 0

50

100

150

200

250

300

350

Denmark France Germany Italy Spain Sweden The United Kingdom

Exp

ecte

d D

eliv

eri

es o

f A

PM

Ro

llin

g S

tock

Expected Deliveries of APM Rolling Stock, 2011-2021

Denmark France Germany Italy Spain Sweden UK

18.5%

3.5%

32.4%

9.8%

34.4%

18.2%

19.8%

2.1%

18.5%

Denmark: Copenhagen’s Cityringen lines are expected to be completed by 2018, marking the end of the

second stage of the city’s metro.

Italy: Cities are expected to expand their metros with new lines and almost all systems are likely to be

Ansaldo’s Driverless Metro solutions.

Germany and France: Siemens NeoVAL is expected to find a launch partner by the end of the forecast

period.

Note: % values in the center

chart show the CAGR (2011-

2021) of rolling stock deliveries

for each country.

Note: % values in the bars on the left and right side show the market share.

1.5%

2.7%

32.3%

6.5%

Note: All figures are rounded. The base year is 2011. Frost & Sullivan analysis.

13 M77E-18

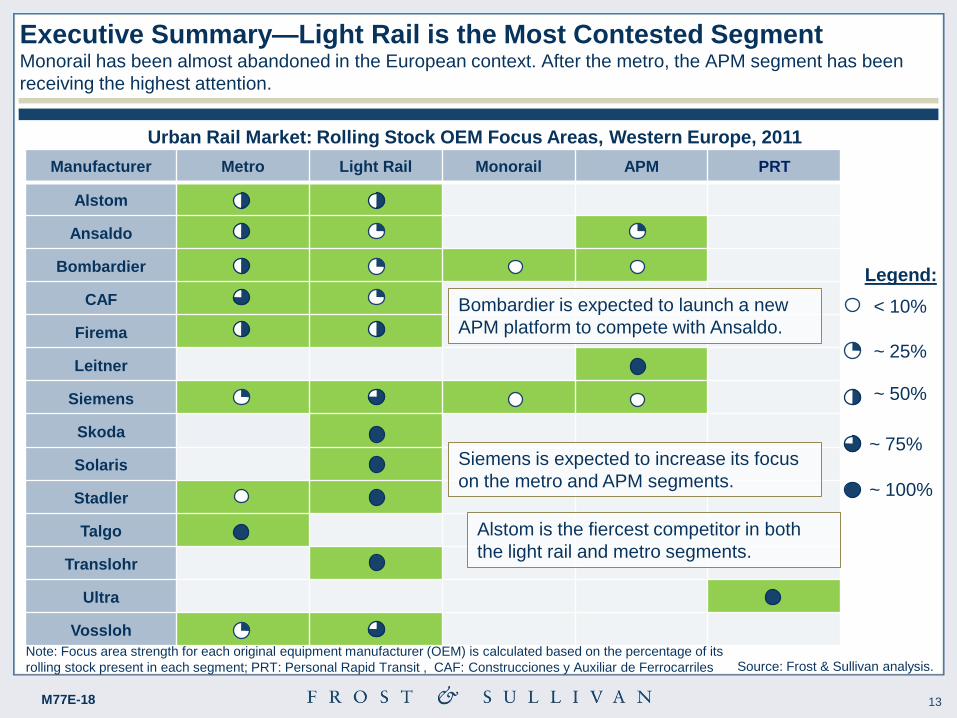

Executive Summary—Light Rail is the Most Contested Segment Monorail has been almost abandoned in the European context. After the metro, the APM segment has been

receiving the highest attention.

Manufacturer Metro Light Rail Monorail APM PRT

Alstom

Ansaldo

Bombardier

CAF

Firema

Leitner

Siemens

Skoda

Solaris

Stadler

Talgo

Translohr

Ultra

Vossloh

Urban Rail Market: Rolling Stock OEM Focus Areas, Western Europe, 2011

Note: Focus area strength for each original equipment manufacturer (OEM) is calculated based on the percentage of its

rolling stock present in each segment; PRT: Personal Rapid Transit , CAF: Construcciones y Auxiliar de Ferrocarriles

< 10%

~ 25%

~ 50%

~ 100%

~ 75%

Legend:

Siemens is expected to increase its focus

on the metro and APM segments.

Bombardier is expected to launch a new

APM platform to compete with Ansaldo.

Alstom is the fiercest competitor in both

the light rail and metro segments.

Source: Frost & Sullivan analysis.

14 M77E-18

Executive Summary—Light Rail Rolling Stock Segment Witnesses

Higher Interest Levels CAF, Alstom, Ansaldo, and Translohr are likely to be the top performers in rolling stock deliveries up till 2015.

Metro

APM

Light Rail

2012 2013 2014 2015

CAF

Urbos 2

CAF

Urbos 3

CAF

A35

Alstom Citadis

Siemens NF8U

Stadler

Variotram

SSB DT8:12

Bombardier

Flexity 2

Translohr STE6 CAF

Urbos 2

CAF

Urbos 3

Alstom/Bombardier

HHA Type DT5

Ansaldo Breda

Driverless Metro

Ansaldo to supply railcars to

Copenhagen’s Metro lines M3 and M4

to carry 240,000 passengers daily

CAF is Alstom’s new threat: Entering

three new markets: France, Sweden,

and the United Kingdom, with a 29.5

share of all the light rail orders.

Translohr STE3

By 2014, Lines T5 and T6 in Paris will

be served by 213 Translohr Railcars.

Translohr has a 12.4 percent share of all

light rail orders.

Urban Rail Market: Overview of Rolling Stock Orders, Western Europe, 2012‒2015

Image source: Alstom, Ansaldo, Bombardier, CAF, Siemens, Stadler, Solaris, Translohr. Source: Frost & Sullivan analysis.

SolarisTramino

15 M77E-18

Research Scope, Objectives, Background, and

Methodology

16 M77E-18

Research Scope France, Germany, Italy, Spain and the United Kingdom are regarded as the key centers of urban rail

development, often setting standards for the urban rail market.

Urban Rail Rolling Stock: Light rail systems, metro rail systems, and

APMs (Guide way based train system) Topics Covered

2012 to 2021 Forecast Period

2011 to 2021 Study Period

2011 Base Year

Denmark, France, Germany, Italy, Spain, Sweden, and the United

Kingdom

Geographical Scope

49.2% 48.2%

2.1% 0.5% 0.0% 0.0%

20.0%

40.0%

60.0%

Metro Light Rail APM Monorail Personal Rapid Transit

Ro

llin

g S

toc

k in

Ac

tive

S

erv

ice

Monorail and PRT systems are

not covered in this study

Urban Rail Market: Percent of Rolling Stock in Service, Western Europe, 2011

Note: All figures are rounded. The base year is 2011 Note: All figures are rounded. The base year is 2011. Frost & Sullivan analysis.

17 M77E-18

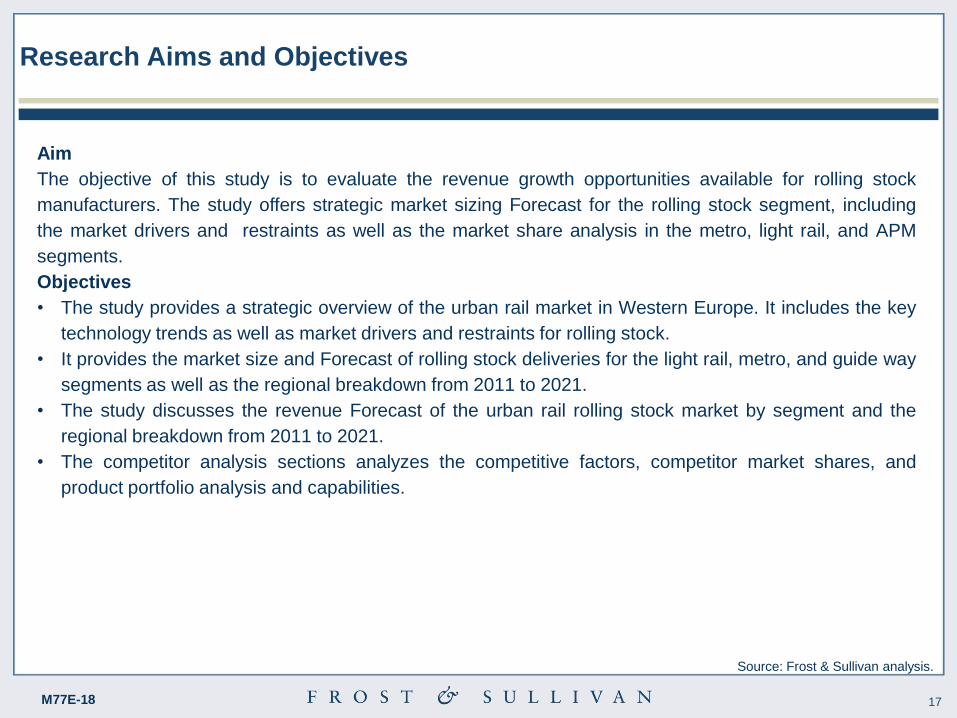

Research Aims and Objectives

Aim

The objective of this study is to evaluate the revenue growth opportunities available for rolling stock

manufacturers. The study offers strategic market sizing Forecast for the rolling stock segment, including

the market drivers and restraints as well as the market share analysis in the metro, light rail, and APM

segments.

Objectives

• The study provides a strategic overview of the urban rail market in Western Europe. It includes the key

technology trends as well as market drivers and restraints for rolling stock.

• It provides the market size and Forecast of rolling stock deliveries for the light rail, metro, and guide way

segments as well as the regional breakdown from 2011 to 2021.

• The study discusses the revenue Forecast of the urban rail rolling stock market by segment and the

regional breakdown from 2011 to 2021.

• The competitor analysis sections analyzes the competitive factors, competitor market shares, and

product portfolio analysis and capabilities.

Source: Frost & Sullivan analysis.

18 M77E-18

Key Questions This Study Will Answer

Who are the leading rolling stock suppliers in the metro, light rail, and guide way segments in

Denmark, France, Germany, Italy, Spain, the United Kingdom, and Sweden?

What are the new opportunities in rolling stock for urban rail?

Which way is the urban rail signalling technology headed? Will radio-based signalling witness a rapid

uptake in the urban rail environment? If so, in which environment and segment will it witness the

uptake?

What is the market share of the rolling stock in urban rail applications? Who is the market leader in

each rolling stock segment in each country?

What is the business environment of the Western European urban rail market? What are its market

dynamics, and its impact on mobility and urbanization?

Urban Rail Market: Key Questions This Study Will Answer, Western Europe, 2011

Source: Frost & Sullivan analysis.

19 M77E-18

Year Research

Study Title Title

2012 M77D-18 Strategic Insight on Global Rail Market Global

2011 M4DD-18 Strategic Analysis of the Global High Speed Rail Market Global

2011 M64A-18 North American Locomotive Market: A strategic Analysis of Powertrain Technologies and Auxiliary Systems

Considered by OEMs for EPA Emission Compliance North America

2011 M6DB-18 Strategic Analysis of Alternative Powertrain Technologies in the European Diesel Locomotive and Railcar

Market Europe

2011 N92D-18 An Executive Analysis on Passenger Rail Rolling Stock and Seating Systems Market in the U.S. USA

2011 P488-18 Green Technologies and Developments in Rail Transportation APAC

2010 M649-18 European Rail Catenary Systems – Executive Analysis of Copper Requirement for Electrification across

Strategic European Markets Europe

2009 M3F5-18 Strategic Analysis of the European Rail Electrification Market Europe

2009 M1B6-18 Strategic Analysis of the European Light Rail and Underground Market - Part 2: Market Engineering

Measurements Europe

2009 P2A3-18 Strategic Analysis of the Growth Opportunities in the Indian Rail Industry India

2009 M363-18 Strategic Opportunity Analysis of the Russian Rail Market: Implication for the Global Supply Chain Russia

2008 P391-18 360 Degree CEO Perspective on Green Transportation: Focus on Rail, Automotive and Procurement Global

Research Background

This research study strengthens our coverage of the rail industry.

Source: Frost & Sullivan analysis.

20 M77E-18

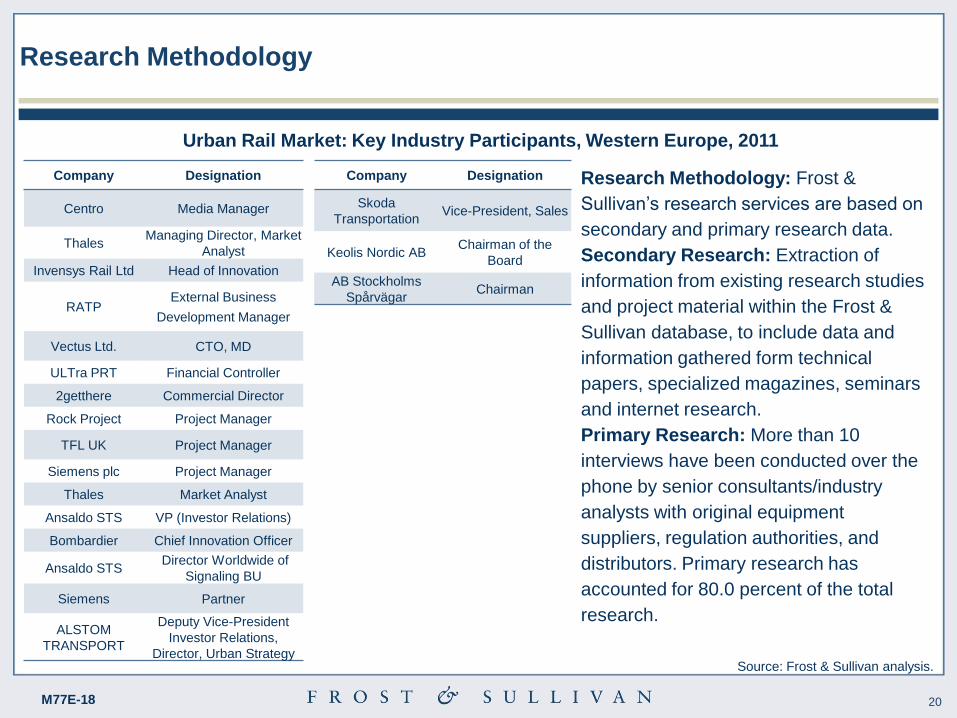

Company Designation

Centro Media Manager

Thales Managing Director, Market

Analyst

Invensys Rail Ltd Head of Innovation

RATP External Business

Development Manager

Vectus Ltd. CTO, MD

ULTra PRT Financial Controller

2getthere Commercial Director

Rock Project Project Manager

TFL UK Project Manager

Siemens plc Project Manager

Thales Market Analyst

Ansaldo STS VP (Investor Relations)

Bombardier Chief Innovation Officer

Ansaldo STS Director Worldwide of

Signaling BU

Siemens Partner

ALSTOM

TRANSPORT

Deputy Vice-President

Investor Relations,

Director, Urban Strategy

Research Methodology: Frost &

Sullivan’s research services are based on

secondary and primary research data.

Secondary Research: Extraction of

information from existing research studies

and project material within the Frost &

Sullivan database, to include data and

information gathered form technical

papers, specialized magazines, seminars

and internet research.

Primary Research: More than 10

interviews have been conducted over the

phone by senior consultants/industry

analysts with original equipment

suppliers, regulation authorities, and

distributors. Primary research has

accounted for 80.0 percent of the total

research.

Research Methodology

Company Designation

Skoda

Transportation Vice-President, Sales

Keolis Nordic AB Chairman of the

Board

AB Stockholms

Spårvägar Chairman

Urban Rail Market: Key Industry Participants, Western Europe, 2011

Source: Frost & Sullivan analysis.

21 M77E-18

Key OEM/Participant Groups Compared in this Study

Group OEMs/Divisions

Alstom Alstom Transportation

Bombardier Bombardier Transportation

Siemens Siemens Mobility

Thales Thales Transportation

Invensys Invensys Rail

Finmeccanica Ansaldo STS, Ansaldo Breda

Group OEMs/Divisions

Vossloh Vossloh Kiepe

CAF CAF

Stadler Stadler

The OEM groups and companies compared in this study are as follows:

Source: Frost & Sullivan analysis.