weo outlook oct 2012

DESCRIPTION

World Economic Outlook, October 2012 (Jaime Custodio Guajardo, Senior Economist, Research Department, International Monetary Fund)TRANSCRIPT

World Economic Outlook

Coping with High Debt and Sluggish Growth

October 2012

Main Message: Action Needed to Put Recovery Back on Track

• The global economy has suffered new setbacks

• The forecasts are down • Risks are up sharply

• AE: policies have progressed but much stronger actions are needed

• EM: complex setting—rebuilding policy room for maneuver versus

supporting growth

New Setbacks to the Global Recovery

Global Manufacturing PMI

(Index; > 50 = expansion; SA)

Source: IMF, Global Data Source.

30

35

40

45

50

55

60

06 07 08 09 10 11 12

World

Advanced

Emerging

3

-80

-60

-40

-20

0

20

40

60

80

05 06 07 08 09 10 11 12

Advanced

Emerging

Merchandise Exports (Percent; 3mma annualized)

Aug. 12 Jul. 12

Increasing strains in the euro area

What Went Wrong?

Large growth impact of fiscal adjustment amid tight financial conditions

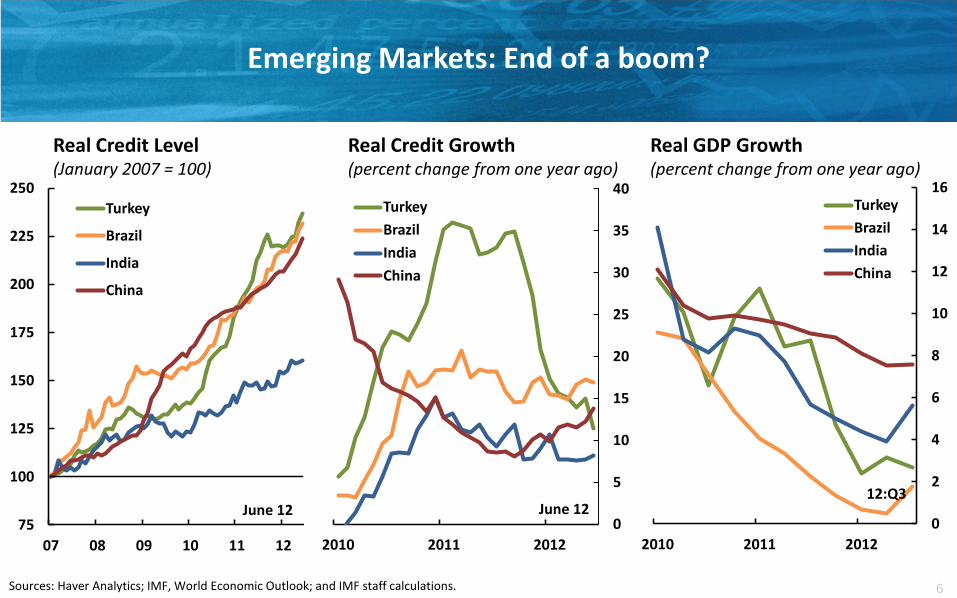

End of the emerging markets boom

4

Euro Area: Growing fragmentation, despite policy responses

5

-12

-10

-8

-6

-4

-2

0

2

4

6

8

2010 2011 2012

Core Periphery Mar. 12

Portfolio and Other Investment Capital Flows, Excluding Central Banks (Cumulative from December 2009, in percent of GDP)

Sources: Haver Analytics; and IMF staff estimates.

Source: Bloomberg, L.P. and IMF staff estimates.

0

100

200

300

400

500

600

700

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12

Italy

Spain

France

Draghi speech Aug. 2nd

2nd LTRO

Sept. 12

10-Year Government Bond Spreads over German Bunds (basis points)

1st LTRO

6

Real GDP Growth (percent change from one year ago)

Emerging Markets: End of a boom?

Sources: Haver Analytics; IMF, World Economic Outlook; and IMF staff calculations.

0

2

4

6

8

10

12

14

16

2010 2011 2012

Turkey

Brazil

India

China

75

100

125

150

175

200

225

250

07 08 09 10 11 12

Turkey

Brazil

India

China

Real Credit Level (January 2007 = 100)

0

5

10

15

20

25

30

35

40

2010 2011 2012

Turkey

Brazil

India

China

Real Credit Growth (percent change from one year ago)

June 12 June 12 12:Q3

7

Tight financial conditions and fiscal policies in AE

-40

-20

0

20

40

60

80

100

2007 2008 2009 2010 2011 2012

U.S.

Euro area

Japan

U.K.

12:Q2

Lending Conditions (Net percentage of domestic respondents tightening standards for loans)

Sources: Lending surveys by the Bank of England, European Central Bank, Bank of Japan, and the U.S. Federal Reserve for households and corporations; and IMF staff estimates.

-3

-2,5

-2

-1,5

-1

-0,5

0

0,5

1

1,5

2009 10 11 12 13

Advanced economies

Emerging and developing economies

Fiscal Consolidation (Change in structural balance as percent of GDP)

Key

Assumptions

•Strong euro-area policies improve financial conditions in 2013H2

•US policymakers avoid fiscal cliff, raise debt ceiling

Outlook: Weak and Uncertain

Outlook •Recovery gradually strengthens

•Downside risks are large

7

World

U.S. Euro Area Japan Brazil India China Russia

2012

(September 2012) 3.3 2.2 -0.4 2.2 1.5 4.9 7.8 3.7

2012

(Revision from Jul 2012) -0.2 0.1 -0.1 -0.2 -1.0 -1.3 -0.2 -0.3

2012

(Revision from Apr 2012) -0.2 0.1 -0.1 0.2 -1.5 -2.0 -0.4 -0.3

2013

(September 2012) 3.6 2.1 0.2 1.2 4.0 6.0 8.2 3.8

2013

(Revision from Jul 2012) -0.3 -0.1 -0.5 -0.3 -0.7 -0.6 -0.2 -0.1

2013

(Revision from Apr 2012) -0.5 -0.3 -0.7 -0.5 -0.1 -1.3 -0.6 -0.1

The outlook has deteriorated since April

WEO Real GDP Growth Projections (percent change from a year earlier)

Source: IMF, World Economic Outlook. 9

-1

0

1

2

3

4

5

6

7

2009 2010 2011 2012 2013

90 percent confidence interval

90 percent confidence interval (April 2012 WEO)

90 percent confidence interval (Sept 2011 WEO)

Baseline

Downside risks are large: 1 in 6 chance of serious global slowdown (global growth < 2 percent)

Prospects for World GDP Growth (percent change)

Downside: 1. More stress in euro area 2. US fiscal cliff, debt ceiling 3. Higher oil prices 4. Medium-term risks: high AE debt; lower EM growth

Key Risks: Escalating euro crisis and U.S. fiscal cliff

Source: IMF staff estimates

Euro Area Downside Scenario (Output loss, percent deviation from baseline in 2013)

-7

-6

-5

-4

-3

-2

-1

0

Note: This scenario assumes that sovereign and corporate spreads rise, credit contracts, and periphery governments are forced to front-load fiscal consolidation.

•Removing

immediate

risks

•Euro Area: Restoring confidence

•United States: Avoiding the fiscal cliff, raise debt ceiling

What Is To Be Done?

•Adjusting

policies

•AE: Managing medium-term fiscal adjustment

•EM&DC: Managing risks vs rebuilding policy space

•Developing Countries: Dealing with commodity price shock

Periphery

•Fiscal adjustment

•Bank recapitalization/resolution

•Structural reforms

Restoring Confidence in the Euro Area

EA partners

•Support adjustment through EFSF/ESM

•Help recapitalize banks

•Advance euro area fiscal and banking union

ECB

•Help ease financial conditions in periphery—latest action

fully delivers on this front; ball is now in other courts

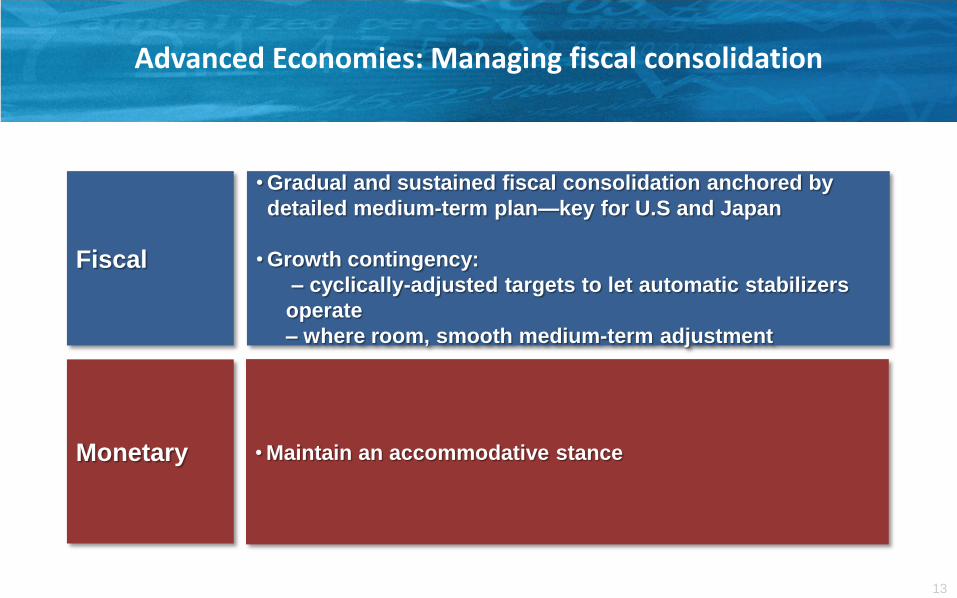

Fiscal

•Gradual and sustained fiscal consolidation anchored by

detailed medium-term plan—key for U.S and Japan

•Growth contingency:

– cyclically-adjusted targets to let automatic stabilizers

operate

– where room, smooth medium-term adjustment

Advanced Economies: Managing fiscal consolidation

Monetary •Maintain an accommodative stance

13

0

20

40

60

80

100

120

140

160

180

200

220

240

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Reducing public debt is a marathon, not a sprint

After Crossing the 100 Percent Threshold (Percent of GDP, advanced economies)

Median 10th/90th percentile 25th/75th percentile

Years Source: IMF staff calculations.

Downside

risks

•Ease monetary policy further, strengthen macro-prudential measures

•Allow fiscal stabilizers to work

• If needed and consistent with stronger medium-term growth,

deploy fiscal stimulus (e.g. China)

EMDEs: Complex setting—need to calibrate macro stance given potential for real and financial vulnerabilities

Baseline

scenario

•Pause monetary policy tightening or modestly ease

•Continue to rebuild fiscal position, especially India and Russia

15

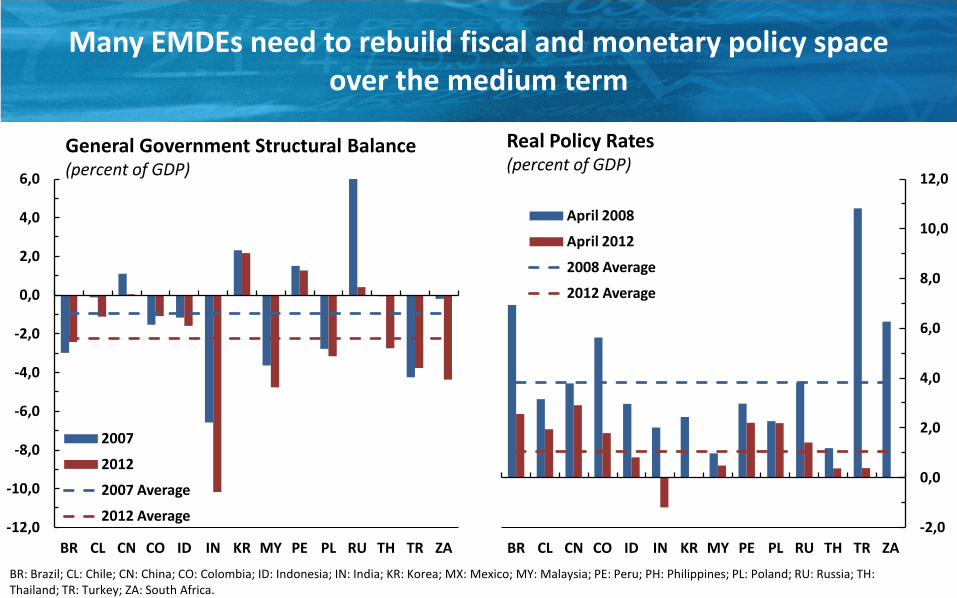

Many EMDEs need to rebuild fiscal and monetary policy space over the medium term

General Government Structural Balance (percent of GDP)

Real Policy Rates (percent of GDP)

-12,0

-10,0

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

BR CL CN CO ID IN KR MY PE PL RU TH TR ZA

2007

2012

2007 Average

2012 Average -2,0

0,0

2,0

4,0

6,0

8,0

10,0

12,0

BR CL CN CO ID IN KR MY PE PL RU TH TR ZA

April 2008

April 2012

2008 Average

2012 Average

BR: Brazil; CL: Chile; CN: China; CO: Colombia; ID: Indonesia; IN: India; KR: Korea; MX: Mexico; MY: Malaysia; PE: Peru; PH: Philippines; PL: Poland; RU: Russia; TH: Thailand; TR: Turkey; ZA: South Africa.

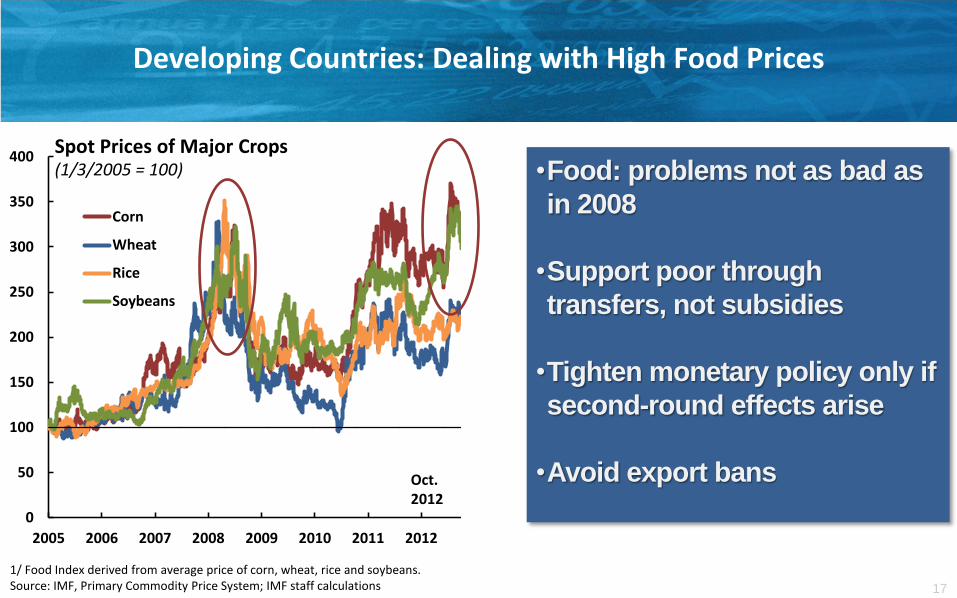

0

50

100

150

200

250

300

350

400

2005 2006 2007 2008 2009 2010 2011 2012

Corn

Wheat

Rice

Soybeans

•Food: problems not as bad as

in 2008

•Support poor through

transfers, not subsidies

•Tighten monetary policy only if

second-round effects arise

•Avoid export bans

Developing Countries: Dealing with High Food Prices

17

Spot Prices of Major Crops (1/3/2005 = 100)

1/ Food Index derived from average price of corn, wheat, rice and soybeans. Source: IMF, Primary Commodity Price System; IMF staff calculations

Oct. 2012

World Economic Outlook

October 2012