welfare benefits - puget sound energy health & welfare benefits about your benefits page 4 open...

TRANSCRIPT

PSE Health & Welfare BenefitsEffective January 1, 2015 – December 31, 2015

PSE Health & Welfare Benefits

About Your Benefits Page 4

Open Enrollment Page 7

Mid-Year Changes Page 13

Wellness Page 15

Medical Benefits Page 20

Dental Benefits Page 28

Life, AD&D and LTD Page 30

Flexible Spending Accounts Page 32

How to Enroll Page 36

Legal Notices Page 39

Glossary Page 44

Contacts Page 45

Effective January 1, 2015 – December 31, 2015

2015 BENEFITS GUIDE 3

The PSE 2015 Benefits Guide is your interactive, online overview of your benefit plan coverage. You’ll also find important enrollment information, including how to enroll. (Enrollment instructions are included on page 36.) Your benefits are an important part of your overall compensation. Please take the time to review your options and the cost of coverage, which may change from year to year. You can do this using a new Health Plan Cost Calculator available in the online enrollment system.

Using this guide

Online plan summaries in standardized format

In addition to the plan information in this benefits guide and on PSEWeb, you can also review a Summary of Benefits and Coverage (SBC) for each PSE medical plan.

The federal health care law requires standardized health plan information so that you can better understand and compare plan features.

Access your plan summaries with the links listed below. If you require a paper copy, please contact the Employee Information Center as noted to the left.

2015 Group Health Options Plan SBC

2015 Regence Engage Plan SBC

2015 Regence HSA Plan SBC

2015 Regence PPO Plan SBC

Puget Sound Energy offers a comprehensive, competitive benefits package to help you and your family stay healthy and protect you against financial loss in the event of accident or illness.

2015 Benefits Guide paper copy

The 2015 Benefits Guide is a long document. Please print only the pages you need to save resources and reduce cost. If you require a complete paper copy of the guide, call the HR Employee Information Center (EIC) at 425-462-3389, option 6, or send an email to [email protected].

2015 BENEFITS GUIDE 4

Your benefits include:

• Medical coverage

• Dental coverage

• Life insurance

• Accidental Death & Dismemberment (AD&D) insurance

• Long Term Disability (LTD) insurance

• Flexible spending accounts (FSAs) for health care and dependent care

About your benefitsFlex Credits | Who is eligible to participate | Benefit plan updates

PSE Flex Credits and benefit costs

PSE provides employees with Flex Credits to offset most of the monthly cost of health care. The amount of Flex Credits you receive is based on the medical coverage option you choose:

• Employee Only

• Employee + Family (one or more dependents, including spouse)

• Opt Out Medical

If the cost of the medical plan you choose is less than the Flex Credits provided, the additional credits are available to reduce your cost for other benefits such as dental, AD&D, supplemental life and flexible spending accounts. Unspent Flex Credits are paid to you as taxable income in your paycheck.

If the cost of your benefit elections exceeds the Flex Credits, your share is paid with a pre-tax payroll deduction.

Wellness credits

Employees who earn 1,000 points in the myWellness at PSE program will receive $360 annually ($30/month) to offset the cost of their benefits. Additionally, covered spouses are also eligible to earn wellness credits for a total savings of $720 annually ($60/month). This applies to non-represented and UA–represented employees, at this time. All employees are eligible and encouraged

to participate in the program where they can earn points for gift cards, giveaways and entries into drawings.

Go to myWellness at PSE or see page 15 for details.

Note: The deadline to earn points for 2015 wellness credits has passed. Participant point totals returned to zero on October 6, 2014.

Eligible employees have until September 30, 2015 to earn points for 2016 wellness credits.

If you are considering any of the options below, Open Enrollment is your opportunity to make changes to your 2015 plan coverage. Please read the detailed information about these benefit elections so that you have the best coverage for you and your family.

If you plan to: Go to:

Change medical plans or covered dependents

Page 7

Opt out of medical/dental coverage

Page 7

Add or drop coverage for a domestic partner

Page 10

Add or increase Supplemental Life insurance

Page 30

Enroll in a flexible spending account

Page 32

Joint Health & Welfare Committees

PSE recognizes that a diverse and changing workforce requires many benefit options. The Joint Health & Welfare Committees meet on a regular basis to review health care trends, benefit plan design and claims experience. Decisions about benefits are based on careful analysis of the collected data. PSE offers a variety of plans with different features so that you can select the benefits that best fit your situation.

2015 BENEFITS GUIDE 5

Who is eligible to participate

• Active regular employees working a minimum of 20 hours per week as:

- IBEW-represented employees

- Non-represented employees

- UA-represented employees

• Qualified dependents of eligible employees:

- Legal spouse — opposite or same sex

- Natural, adopted, foster and/or stepchildren under age 26

- Natural, adopted, foster and/or stepchildren age 26 or older who are permanently and totally disabled

- Domestic partners of eligible employees, and their natural, adopted, foster and/or stepchildren under age 26

Dependents

It’s your responsibility to comply with PSE eligibility rules and IRS tax regulations when enrolling dependents in medical and dental plans.

Make sure you log on and confirm your dependents.

Note: Spouses who both work at PSE may not double-cover each other or their dependents. An individual can only be covered once under the PSE plans.

PSE temporary employees, seasonal employees and casual employees are not eligible for benefits while in these categories. Job change to a regular employee category working a minimum of 20 hours per week would qualify for eligibility.

Are you a new employee or newly eligible for benefits?

If you recently enrolled in benefits for 2014 as a new employee (or as newly eligible for benefits), some of your choices will not roll over to 2015. Make sure you enroll for 2015 benefits. It’s your only opportunity, even if the annual Open Enrollment has passed for other employees. Flex Credits and costs are also different for 2015. (The online process prompts you to enroll for 2015 benefits that do not automatically roll over.)

About your benefitsFlex Credits | Who is eligible to participate | Benefit plan updates

2015 BENEFITS GUIDE 6

Federal health care reform and your benefits

PSE employees, like most individuals and families with company-sponsored benefit plans, will see little impact from the Affordable Care Act on their plan cost or benefit plans. Many of the law’s key requirements, such as full coverage for preventive care, have been in place at PSE for a number of years.

PSE benefit plans currently meet, and in most cases, exceed the coverage requirements of the federal law. We will continue to comply with all the requirements of the Affordable Care Act.

The best way for PSE to keep everyone’s healthcare cost down is to support employees in making healthy lifestyle choices. To accomplish this, we will continue to highlight and enhance our wellness program, myWellness at PSE, as part of a comprehensive benefits package.

money for medical expenses you may incur in the future or during retirement.

At this time, only PSE non-represented employees are eligible to participate in the Regence Health Savings Account Plan.

For more information on the HSA plan, go to the HR Benefits page at pse.com/hsaplan.

Reduced rates for life insurance — enrollment opportunities for supplemental life insurance

On January 1, 2015, MetLife will become the new carrier for PSE plans covering life, accidental death & dismemberment (AD&D) and long-term disability (LTD) insurance. As a result, employees who have not signed up for supplemental life insurance have a one-time opportunity to enroll in the coverage for 2015 without a medical review.

If you do not have supplemental life insurance, you may purchase coverage of one times your annual base pay during Open Enrollment.

Employees who already have supplemental life insurance coverage can take advantage of the new lower rates and increase their coverage by one times their annual base pay for 2015 — also without a medical review. This option is available every year at Open Enrollment.

See page 30 for applicable rates.

2015 Benefit Plan Updates: PSE introduces Health Savings Account plan option

If you’re looking for an additional way to save for retirement and set aside before-tax dollars for current and future medical expenses, a health savings account or HSA may be right for you. The newly offered Regence HSA Plan is a qualified high deductible health plan (HDHP), which is paired with a Health Savings Account. If interested, you must choose this option during the upcoming Open Enrollment period.

Contributions to the HSA are made through payroll deductions deposited to an HSA-approved financial institution — in this case, HealthEquity. The funds in this account can be used to pay qualified out-of-pocket expenses. The financial institution also provides savings and investment options, similar to an individual retirement account (IRA) or 401(k) plan.

A health savings account (HSA) is sometimes confused with a flexible spending account (FSA). Both allow you to pay for out-of-pocket medical, dental and vision expenses with tax-free dollars. However, money set aside in an HSA rolls over from year to year, unlike an FSA in which money must be used during the calendar year or forfeited. The money in your HSA belongs to you, even if you switch health plans, retire or leave employment. An HSA allows you to save

About your benefitsFlex Credits | Who is eligible to participate | Benefit plan updates

2015 BENEFITS GUIDE 7

3 easy steps: Opt Out Medical/Opt Out Dental

When you elect Opt Out Medical and/or Opt Out Dental coverage, you can do it online in three easy steps.

1. Elect the Opt Out option on the medical and/or dental page.

2. Complete the Opt Out certification page by filling out the required fields.

3. Read the Confirmation Statement carefully after making your elections. You must elect Opt Out and provide all of the information requested.

Important: Remember that if you elected to opt out for 2014, that election does not roll over to 2015. You must elect to opt out each calendar year and provide updated certification online that you have other employer group coverage.

Open Enrollment begins October 17 and ends October 31, 2014

Open Enrollment is your annual opportunity to:

• Review your benefit plan choices and costs.

• Change your enrollment decisions for the next year, including your medical, dental, AD&D, life insurance and flexible spending accounts.

• Change who is covered under your plan. (They must be eligible for enrollment.)

• Change premium payment election for LTD — taxable or nontaxable.

• Elect:

1. Opt Out Medical.

2. Opt Out Dental.

3. Flexible spending accounts.

If you are enrolled for 2014 benefits, your coverage for the three items listed above ends December 31 and does not roll over to 2015.

Check your beneficiaries for life and other benefit plans

You can review and update your beneficiaries at any time during the year. However, Open Enrollment is a good time to check your designations to make sure they reflect your current situation and wishes. Review and make beneficiary updates for your pension plan at Milliman Benefits Service Center and for your 401(k) plan at T. Rowe Price. Life and Accidental Death & Dismemberment insurance beneficiaries can be updated on the benefits enrollment site.

Open enrollmentOpt Out medical/dental | Open Enrollment checklist | Employees on a leave of absence | Domestic partner enrollment | Understanding imputed income | Frequently asked questions

2015 BENEFITS GUIDE 8

To access the online benefits enrollment site, go to page 36.

The benefit elections you make will remain in effect from January 1 to December 31, 2015.

No changes are permitted and no exceptions are made unless you have a mid-year status change, and you enroll within the enrollment period. (For details, see Mid-Year Benefit Elections on page 13.)

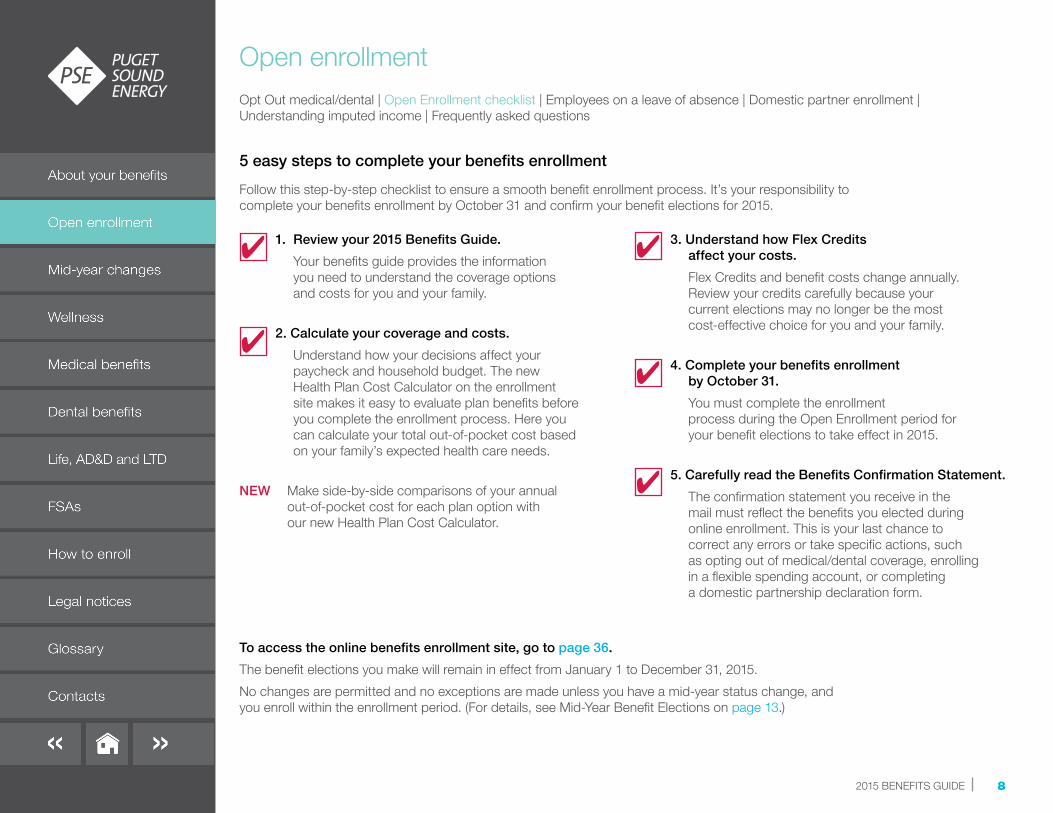

5 easy steps to complete your benefits enrollment

Follow this step-by-step checklist to ensure a smooth benefit enrollment process. It’s your responsibility to complete your benefits enrollment by October 31 and confirm your benefit elections for 2015.

1. Review your 2015 Benefits Guide.

Your benefits guide provides the information you need to understand the coverage options and costs for you and your family.

2. Calculate your coverage and costs.

Understand how your decisions affect your paycheck and household budget. The new Health Plan Cost Calculator on the enrollment site makes it easy to evaluate plan benefits before you complete the enrollment process. Here you can calculate your total out-of-pocket cost based on your family’s expected health care needs.

NEW Make side-by-side comparisons of your annual out-of-pocket cost for each plan option with our new Health Plan Cost Calculator.

3. Understand how Flex Credits affect your costs.

Flex Credits and benefit costs change annually. Review your credits carefully because your current elections may no longer be the most cost-effective choice for you and your family.

4. Complete your benefits enrollment by October 31.

You must complete the enrollment process during the Open Enrollment period for your benefit elections to take effect in 2015.

5. Carefully read the Benefits Confirmation Statement.

The confirmation statement you receive in the mail must reflect the benefits you elected during online enrollment. This is your last chance to correct any errors or take specific actions, such as opting out of medical/dental coverage, enrolling in a flexible spending account, or completing a domestic partnership declaration form.

Open enrollmentOpt Out medical/dental | Open Enrollment checklist | Employees on a leave of absence | Domestic partner enrollment | Understanding imputed income | Frequently asked questions

2015 BENEFITS GUIDE 9

Employees on leave must re-enroll

The health and welfare benefits plan covers employees during most leaves of absence. If you’re on a leave of absence, you are required to complete the Open Enrollment process.

If, while you are on leave, you increase your level of Supplemental Life insurance or change your LTD taxation election, your choices will not take effect until you return to work and meet the carrier requirement to be an active employee. Increasing by more than one level of Supplemental Life coverage requires an Evidence of Insurability approval from the carrier before the new benefit elections take effect.

For more information about issues affecting employees on leave, go to pseweb/employeetools/hr/la/.

For more information on Supplemental Life insurance and the one-time opportunity to increase your coverage without a medical review, see page 30.

Long Term Disability taxation options

During the Open Enrollment period you may elect to receive your LTD monthly payments as taxable or nontaxable income. See page 31 for details.

Open enrollmentOpt Out medical/dental | Open Enrollment checklist | Employees on a leave of absence | Domestic partner enrollment | Understanding imputed income | Frequently asked questions

2015 BENEFITS GUIDE 10

Enrolling domestic partners and their dependents for the first time

If you are enrolling your domestic partner or your domestic partner’s children for the first time, you must complete a PSE Declaration of Domestic Partnership form and return it to PSE Benefits (PSE-10N) by October 31, the last day of the Open Enrollment period.

If your domestic partner or his/her children are currently enrolled, you are not required to complete a new declaration form during the Open Enrollment period. The medical/dental coverage will roll over from year to year.

If you wish to cancel your domestic partner’s coverage or his/her children’s, you must enroll online during the Open Enrollment period and elect to drop their 2015 coverage elections.

If your enrolled domestic partner ceases to be your domestic partner, he or she is no longer eligible for medical/dental coverage. You must promptly notify PSE if such an event occurs.

A domestic partner must be enrolled in the medical/dental plan in order to enroll the domestic partner’s children.

Did you know?

If a valid PSE Declaration of Domestic Partnership form is on file, the domestic partner of an employee who dies while receiving Long Term Disability payments may receive a lump-sum payment. See page 31 for details.

Understanding imputed income

PSE provides family Flex Credits to all employees who include their domestic partner (same or opposite sex) as part of their benefit plan coverage.

The PSE-covered monthly cost paid for eligible domestic partners must be counted as “imputed” or taxable income because the IRS does not recognize domestic partners as “dependents.”

Dependent children of a domestic partner are also nonqualified tax dependents. You will be responsible for paying imputed income based on the value of providing medical or dental coverage.

NOTE: Health care expenses for a domestic partner are not reimbursable under a health care flexible spending account or a health savings account.

Open enrollmentOpt Out medical/dental | Open Enrollment checklist | Employees on a leave of absence | Domestic partner enrollment | Understanding imputed income | Frequently asked questions

2015 BENEFITS GUIDE 11

Frequently asked questions

Do I have to re-enroll for 2015 benefits if I am making no changes?

PSE recommends that you go online to view your options and understand the implications of your decisions because PSE Flex Credits and the cost of your benefit plan change each year. Open Enrollment is your only opportunity to do so before the new benefits and costs become effective for the calendar year.

You may decide to elect different benefits based on Flex Credits and changes in benefit plan costs.

Additionally, you must re-enroll each Open Enrollment period if you want to:

1. Change plans or covered dependents.

2. Elect or re-elect Opt Out Medical or Opt Out Dental.

3. Enroll or re-enroll in a flexible spending account for health care or dependent care.

How do I find benefit plan costs and the amount of my Flex Credits?

The cost of each benefits plan and your Flex Credits are displayed when you sign in to the online benefits enrollment system. Flex Credits vary depending on whether you elect to cover yourself, yourself and your family, or opt out of medical coverage altogether. Flex Credits also vary depending on your employee group — non-represented, IBEW-represented or UA-represented. Please note that wellness credits are not displayed in the online benefits enrollment system.

If I want to choose Opt Out Medical or Opt Out Dental, what do I do?

You can do it in three easy steps as described on page 6. You must complete the enrollment process to opt out of medical and/or dental.

Important: If you do not enroll online and provide all the information requested within the Open Enrollment period, you will be enrolled in:

Regence Engage Medical — Employee Only coverage

Delta Dental Basic Option — Employee Only coverage

There are no exceptions. You will be enrolled in these benefits for the entire calendar year.

Open enrollmentOpt Out medical/dental | Open Enrollment checklist | Employees on a leave of absence | Domestic partner enrollment | Understanding imputed income | Frequently asked questions

2015 BENEFITS GUIDE 12

Do I need to have a medical review to add or increase my Supplemental Life insurance? During most Open Enrollment periods, you must complete a medical review or Evidence of Insurability (EOI) form. However, if you have opted out of Supplemental Life insurance in the past, you have a one-time opportunity to add this coverage without a medical review with our new plan administrator MetLife. If you have existing coverage, you can take advantage of the new lower rates and increase your coverage by one times your annual base pay without a medical review. This option is available every year at Open Enrollment.

I am currently on leave. How do I enroll for benefits?Read your 2015 Benefits Guide. Enroll online or through the Benefit Service Call Center at 1-800-531-1328. The same enrollment rules apply to employees on leave. Your elections become effective on January 1, 2015.

If you elect to increase your current level of Supplemental Life coverage, your new elections will not become effective until you have returned to work per the carrier requirements. If the election you choose requires Evidence of Insurability, approval from the carrier is necessary before the new elections take effect.

Additionally, a change in the taxation of your LTD benefit will not take effect until you return to work as scheduled.

When will I get a Benefits Confirmation Statement?A Confirmation Statement with your elections will be mailed to your home address approximately one week after the close of Open Enrollment. You can also print a copy of your Confirmation Statement directly from the confirmation page of the online enrollment system. However, because of the special enrollment rules involved in opting out of medical/dental or enrolling a domestic partner, the final confirmation is the version you receive in the mail. A grace period for corrections will be stated on the confirmation if you find any errors in your enrollment.

How does the preventive care benefit for the medical plans work?Employees have 100 percent routine preventive care coverage (not for diagnostic tests) for all medical plans. There is no maximum limit, deductible or coinsurance payment. Covered services include routine pediatric exams and adult physical exams; immunizations and flu shots; routine screening colonoscopies and mammography; and women’s preventive care, including some contraceptives and screenings.

For specific questions, call your plans’ customer service number in the Contacts section.

Will I receive a new medical plan ID?Only employees who are making a change in their medical plan coverage will receive a new medical plan ID card,

except Group Health members in Eastern Washington, who have a new group number in 2015 and will receive new ID cards.

New medical plan ID cards will be delivered to your home before January 1. Please make sure your health care provider records your new card.

Will I receive a dental plan ID card?

No. Delta Dental does not issue ID cards. When visiting the dentist, you will only need to provide your name, date of birth and dental plan number (174), along with your Social Security number or the member ID number located on all Delta Dental correspondence. If you would like to print a copy of your card, go to deltadentalwa.com.

Can I get information on 2015 plan benefits from Regence, Group Health or Delta Dental?Yes. Go to Benefits from the HR home page on PSEWeb. From the Benefits menu, you can review the medical plan comparison and the dental plan comparison charts or review your benefit booklets. If you have more detailed questions about what is or is not covered, please call the carrier or access your coverage information by logging on to your plan’s secure member website.

Do I need to re-enroll my dependents for medical and/or dental coverage for 2015?If your dependent is currently enrolled, he or she will continue to be enrolled.

Open enrollmentOpt Out medical/dental | Open Enrollment checklist | Employees on a leave of absence | Domestic partner enrollment | Understanding imputed income | Frequently asked questions

2015 BENEFITS GUIDE 13

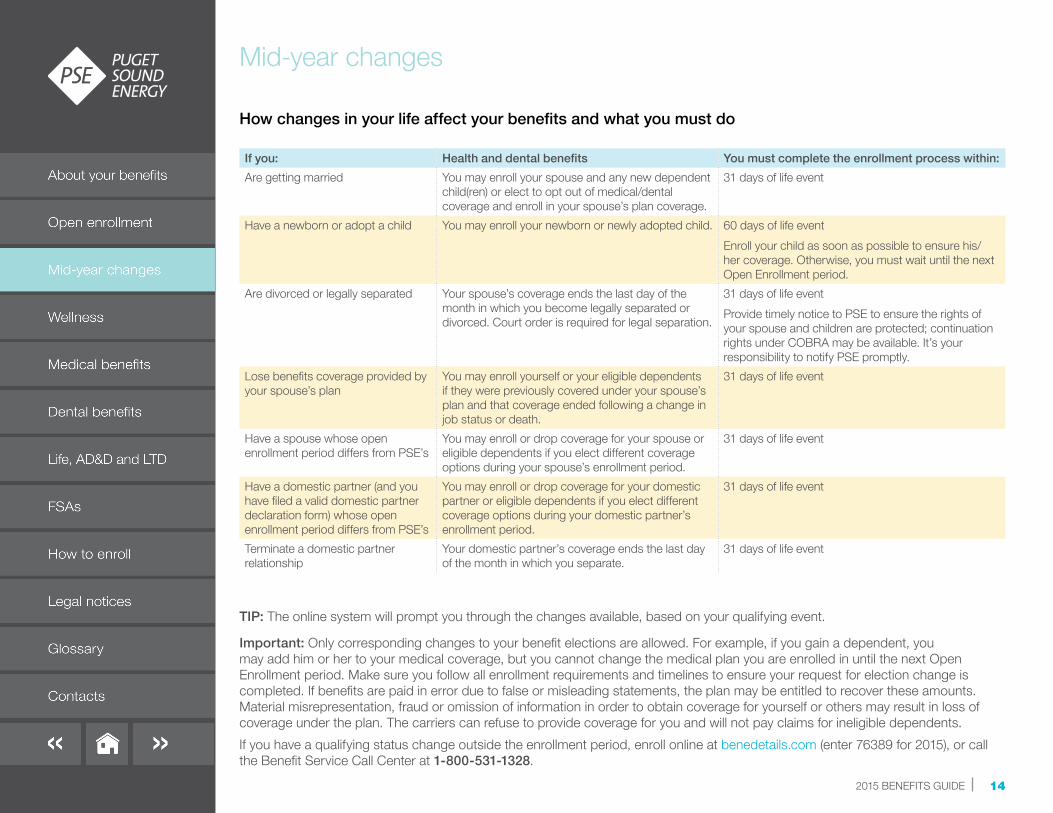

31 days to make qualifying changes — mid-year benefit elections

Most benefit plan changes for next year can only be made during the fall Open Enrollment period. However, you may change your benefit plan coverage in 2015 if you or a family member experiences a “qualifying” life event, such as:

• Marriage, divorce or legal separation.

• Birth or adoption of a child.

• Newly acquired legal guardianship of a dependent child.

• Loss of benefits coverage under your spouse’s plan after a job change or death.

• Change in your spouse’s coverage during his or her open enrollment period.

You must make the benefit change within 31 days of the qualifying event — 60 days to add coverage for newborns or adopted children.

To make a mid-year change, re-enroll online or call the Benefit Service Call Center at 1-800-531-1328. A Mid-Year Status Change form must be completed for legal separation, adoption or legal guardianship.

Qualifying mid-year changes are determined in a uniform and consistent manner for all employees enrolled in a benefits plan. PSE allows qualified changes — though employers are not required to — if the change meets IRS requirements, and online election and other requirements, if applicable, are completed within the designated periods mentioned above.

Mid-year changes

What you must do: divorce or legal separation

It is your responsibility to notify PSE within 31 days if your marital status changes. That’s because your spouse is no longer eligible for coverage under PSE medical/dental plans following a divorce or court-certified separation. However, a divorce or legal separation triggers eligibility for benefits continuation (COBRA) for your spouse and/or children covered under your medical/dental plan.

Failure to notify PSE may cost you money in the following ways:

• You will not receive a refund of paycheck deductions from your divorced spouse retroactively.

• PSE may recover from you any costs incurred from providing late COBRA notice to your ex-spouse.

• Imputed (taxable) income will be added to your gross income for any months the divorced spouse was covered because PSE was not notified that he or she was no longer eligible for benefits.

2015 BENEFITS GUIDE 14

Important: Only corresponding changes to your benefit elections are allowed. For example, if you gain a dependent, you may add him or her to your medical coverage, but you cannot change the medical plan you are enrolled in until the next Open Enrollment period. Make sure you follow all enrollment requirements and timelines to ensure your request for election change is completed. If benefits are paid in error due to false or misleading statements, the plan may be entitled to recover these amounts. Material misrepresentation, fraud or omission of information in order to obtain coverage for yourself or others may result in loss of coverage under the plan. The carriers can refuse to provide coverage for you and will not pay claims for ineligible dependents.

If you have a qualifying status change outside the enrollment period, enroll online at benedetails.com (enter 76389 for 2015), or call the Benefit Service Call Center at 1-800-531-1328.

How changes in your life affect your benefits and what you must do

TIP: The online system will prompt you through the changes available, based on your qualifying event.

Mid-year changes

If you: Health and dental benefits You must complete the enrollment process within:

Are getting married You may enroll your spouse and any new dependent child(ren) or elect to opt out of medical/dental coverage and enroll in your spouse’s plan coverage.

31 days of life event

Have a newborn or adopt a child You may enroll your newborn or newly adopted child. 60 days of life event

Enroll your child as soon as possible to ensure his/her coverage. Otherwise, you must wait until the next Open Enrollment period.

Are divorced or legally separated Your spouse’s coverage ends the last day of the month in which you become legally separated or divorced. Court order is required for legal separation.

31 days of life event

Provide timely notice to PSE to ensure the rights of your spouse and children are protected; continuation rights under COBRA may be available. It’s your responsibility to notify PSE promptly.

Lose benefits coverage provided by your spouse’s plan

You may enroll yourself or your eligible dependents if they were previously covered under your spouse’s plan and that coverage ended following a change in job status or death.

31 days of life event

Have a spouse whose open enrollment period differs from PSE’s

You may enroll or drop coverage for your spouse or eligible dependents if you elect different coverage options during your spouse’s enrollment period.

31 days of life event

Have a domestic partner (and you have filed a valid domestic partner declaration form) whose open enrollment period differs from PSE’s

You may enroll or drop coverage for your domestic partner or eligible dependents if you elect different coverage options during your domestic partner’s enrollment period.

31 days of life event

Terminate a domestic partner relationship

Your domestic partner’s coverage ends the last day of the month in which you separate.

31 days of life event

2015 BENEFITS GUIDE 15

myWellness at PSE

In 2013, myWellness at PSE was launched to consolidate wellness resources under one program that rewards employees for making healthy choices with the support of an informative and engaging website. PSE teamed up with Limeade, a local wellness company that provides a broad range of offerings that cover physical, emotional and financial fitness — all designed to help you and family members reach goals for healthy living. All employees are eligible and encouraged to participate either as an individual, through group activities or working with an individual health coach.

Get started today!

Go to mywellnessatpse.limeade.com and access the tools you need to build an active, engaged and healthful future.

Rewarding you for making healthy choices

All employees and their covered spouse/domestic partner are eligible and encouraged to participate in myWellness at PSE. Once you create your account, you can start earning points for gift cards, giveaways and entries into drawings. Use the free confidential assessment to gauge your well-being and establish goals. Then, you can participate as an individual or in group activities, or work with a wellness coach to reach those goals. Here’s how to earn points and 2016 wellness credits between now and September 30, 2015.*

Level 1 – Plugged In

Earn 1,000 points and receive a water bottle and wellness credits worth $360 annually ($30/month) toward the cost of your benefits. Covered spouses/domestic partners are eligible to earn an additional $360 for a total of $720 ($60/month) in savings.

Level 2 – Fired Up

Earn 2,000 points and receive a $25 Amazon gift card and be eligible to win a free Fitbit wellness device.

Level 3 – Energized

Earn 3,000 points and receive the Energized Award and be eligible to win the grand prize valued at $700 to $1,000.

About wellness credits: These credits can be applied to the cost of your benefits such as medical, dental and flexible spending accounts. However, you may also receive taxable income, as you would with unused Flex Credits. See page 4.

*Wellness credits apply only to non-represented and UA-represented employees and their covered spouses/domestic partners at this time.

WellnessmyWellness at PSE | Resources for all PSE employees | Group Health resources | Regence resources

2015 BENEFITS GUIDE 16

Additional healthy living resources for all PSE employees

Preventive careRoutine screenings, at no out-of-pocket cost to you, include physicals, gynecological exams, immunizations, life-saving cancer screenings such as colonoscopies, and other important routine tests. Preventive care is available through your Group Health and Regence plans.

Flu shotsThe cost of flu shots is covered at 100 percent through your Group Health and Regence plans. Vaccinations are available at your local pharmacy or physician’s office.

Smoking cessation The nationally recognized Quit for Life™ program offers free 12-month telephone support to help you become tobacco-free at your pace. Our health plans cover prescribed smoking cessation drugs at little or no cost. The program is available through Regence at 1-866-784-8454 and Group Health at quitnow.net/ghc or 1-800-462-5327.

Dental benefits centerMySmile® is Delta Dental’s patient portal to your personal dental benefits, where you can review coverage, find a dentist, check claims status, view demos and much more: deltadentalwa.com.

Onsite fitness and companywide teamsMany PSE facilities have onsite exercise equipment, feature wellness activities such as group walks, and recruit participants for companywide sports leagues including golf, soccer and softball.

Safety information and eventsPSEWeb safety pages include stretch videos, office ergonomics, safety meeting information and much more to support a safety-first mindset. PSE Safety Days build on this information with educational speakers, company resources and hands-on learning opportunities.

Safety equipment discounts and resourcesSafety is a top priority. PSE partners with select vendors to make personal protective equipment affordable and accessible. Employees may purchase qualifying work boots from any vendor and PSE contributes up to $75 toward the cost. Red Wing provides a 17 percent discount for employees using their PSE ID.

PSE contributes up to $300 toward the cost of qualifying prescription safety glasses. SafeVision provides discounted pricing, but employees may purchase qualifying eyewear from any

vendor. Hearing resources, including clinics and test schedules, are also available for employees exposed to higher-than-average noise levels.

For more information on the full range of PSE safety resources, go to pseweb/organizations/corpsafety/.

WellnessmyWellness at PSE | Resources for all PSE employees | Group Health resources | Regence resources

2015 BENEFITS GUIDE 17

Employee Assistance Program (EAP)

This program helps employees with everything from finding home repairs services to finding care providers for family members, as well as legal consultations, counseling services and financial advising. Services are confidential and most offerings are free. Behavioral health services are available to help with mental health and substance abuse issues with no charge for up to three sessions.

The EAP is a free employee resource, providing referrals and online tools for you and your household family members. Find out more at liveandworkwell.com (access code 5271), or call 1-800-358-8515 to speak with an EAP professional.

Financial Fitness

Revisiting your blueprint to retirement every three to five years is a smart thing to do. Investments rise and fall, as do income and expenses. Refocusing your goals helps to ensure your changing financial resources will sustain you into the future.

T. Rowe Price can help you update your plan with advice, online calculators and other financial tools focused on budgeting, saving for college, tax planning and more.

Employees who have a PSE Retirement Plan (or pension) can complete their financial picture with Milliman’s Personal Retirement Planner at yourpensionsite.com. This financial planner shows how your Social Security, PSE retirement and PSE 401(k) plan benefits work together, allowing you to review different scenarios based on your target retirement age, current savings and future contributions.

Washington Health Alliance

PSE is a participating employer in the Washington Health Alliance, a nonprofit organization dedicated to improving the region’s health care delivery with scorecards on health care quality, up-to-date resources for consumers and much more. Check out the Alliance’s Own Your Health, which include videos and tips on health topics, such as how to choose and partner with your primary care provider for better health. Go to oyh.wacommunitycheckup.org.

WellnessmyWellness at PSE | Resources for all PSE employees | Group Health resources | Regence resources

2015 BENEFITS GUIDE 18

Healthy living resources from Group Health

Group Health provides free wellness support services to help its members improve health and well-being. Find out more at member.ghc.org or 1-888-901-4636.

Health ProfileIn addition to the well-being assessment on myWellness at PSE, Group Health has a unique, confidential assessment that is tied in with your care team and medical record. If you receive primary care at a Group Health Medical Center, some information will conveniently be auto-populated from your medical record. Your doctor can use this tool to better help you address health risks or concerns.

Complementary Choices The Complementary Choices program offers non-covered alternative care services at a discount. These services include acupuncture, naturopathy, chiropractic care and massage therapy.

Workshops for chronic conditionsIf you have a chronic condition like diabetes, high blood pressure, asthma or congestive heart failure, Group Health offers six-week workshops online or in-person to help you learn how to manage your condition and improve your quality of life. Call or go online for information on Living Well with Chronic Conditions or Living Well with Diabetes.

Group Health Fitness NetworkGroup Health sponsors cycling, running and other fitness events throughout the year to promote an active and engaged lifestyle. Services through the website include information on upcoming fitness events, partner sites, event updates and registration deadlines. grouphealthfitnessnetwork.com

GlobalFitA gym is a great place to get inspired, stay focused and break a sweat. Group Health partners with GlobalFit to give you low rates on neighborhood and chain fitness centers, home exercise equipment, and meal programs for improved weight management. Go to globalfit.com and enter Group Health in the search box to indicate your eligibility and to register.

Consulting Nurse helplineThe Consulting Nurse helpline, which includes a consulting physician, is available 24/7 if you have a non–life-threatening illness, injury or just want some medical advice. This resource is a great way to stay well and reduce unnecessary health care cost. Call 1-800-297-6877.

myGroupHealth Web servicesAccess healthy living services and information at ghc.org. Refill prescriptions, check your benefits coverage and look up reliable health information and classes. If you receive care at a Group Health Medical Center, you can also email your doctor, make appointments and view test results.

WellnessmyWellness at PSE | Resources for all PSE employees | Group Health resources | Regence resources

2015 BENEFITS GUIDE 19

Healthy living resources from Regence

Regence provides a range of wellness services to promote and sustain good health for its members. Find out more at regence.com or 1-866-240-9580.

Regence Advantages

Beat the high cost of health care with reduced fees from a number of nationally recognized health-related programs such as Jenny Craig and member-only discounts on hearing aids, LASIK eye surgery and other health care needs.

Special Beginnings®

This program is designed to help moms-to-be and provides phone support from a nurse case manager every trimester, access to an around-the-clock nurse line, and educational materials that support a healthy and joyful pregnancy. Call 1-888-JOY-BABY (569-2229).

Nurse Advice Line

With the Regence Nurse Advice Line, you can talk to a registered nurse — any time of the day or night — and get fast, reliable and confidential answers. The registered nurse will assess your condition and advise you on whether a trip to a doctor or clinic is necessary. Call 1-800-267-6729.

Redesigned regence.com

With a fresh new look and more robust content, regence.com is replacing myRegence.com with improved features and streamlined access.

A newly created member dashboard provides an overview of key information, including a summary of benefit maximums, how much has been used and what’s remaining.

The new site includes an enhanced treatment cost estimator that calculates your out-of-pocket costs for a particular service based on your health plan’s deductible and coinsurance amounts.

The newly enhanced regence.com website provides more visibility for the health tools and information you value most. Visit regence.com today.

WellnessmyWellness at PSE | Resources for all PSE employees | Group Health resources | Regence resources

2015 BENEFITS GUIDE 20

Medical benefits overview

Your choices for medical coverage are:

1. Regence

• PPO Plan

• Engage Plan

• Health Savings Account (HSA) Plan

2. Group Health

• Options Plan

3. Opt Out Medical

• Opt Out certification is required when enrolling online. See page 7 for details.

Reminder: January 1 begins a new calendar-year period for the calculation of all plan deductibles, out-of-pocket maximums and plan limits.

Medical plan ID cards

Your ID cards are mailed directly from your carrier to your home, prior to January 1, 2015. If you enroll at another time (for example, as a new hire), your card will be mailed to your home within 10 business days.

If you are currently enrolled and make no changes, keep your ID card — a new card will not be mailed to you for 2015. Group Health members in Eastern Washington have a new group number in 2015 and will receive new ID cards. Be sure to provide your new ID card to your providers at your next visit.

Regence and Group Health medical plan booklets online

Enjoy the convenience of having the e-version of your plan summary as close as your desktop. Quickly search and find important information to make the best health care decisions for you and your family.

For your online copy, log on to your plan’s member site, or go to Benefits from the HR home page on PSEWeb and select your plan from the right margin.

New online tool simplifies comparing health plan costs

Our new Health Plan Cost Calculator on the benefits enrollment site makes it easy to generate side-by-side comparisons of your annual out-of-pocket cost for different plan options. Here you can view what you would pay in monthly payroll deductions, deductibles, copays and all other costs associated with your family’s expected health care needs. Make the most of this online tool to identify cost-effective plan coverage for you and your family.

Medical benefitsMedical benefits overview | Medical plan comparison | Group Health Options Plan | Regence PPO, Engage and HSA Plans

2015 BENEFITS GUIDE 21

Some quick tips on what you can do to reduce health care costs

You reduce health care costs if you:

• Purchase generic drugs.

• Contact your plan’s 24-hour nurse hotline for after-hours service to get advice on appropriate treatment.

• Visit an urgent care facility instead of the emergency room for non-emergency care.

• Get routine preventive care screenings

You increase health care costs if you:

• Use brand-name drugs when generics are available.

• Visit the emergency room for after-hours services and care.

• Wait until you are sick to see a health care provider.

How to save time and money

Urgent care vs. emergency care

The overuse of emergency care for non-emergency medical conditions is a major contributor to health care cost. A visit to the emergency room can cost up to five times more than a trip to an urgent care center.

Symptoms appropriate for an emergency room include chest pain, confusion, high fever, seizures, severe burns, loss of consciousness, uncontrolled bleeding or poison ingestion. Call 9-1-1.

Injuries or illnesses that don’t appear to pose a serious health risk — colds, flu, insect bites, sprains, strains and nausea — are appropriate for urgent care or your primary care physician. When used for non–life-threatening conditions, urgent care often provides a more appropriate and less expensive level of care with costs similar to an office visit. And, it’s usually faster.

If you’re unsure which is the appropriate choice for you, contact the 24-hour nurse advice line. These professionals can help you evaluate your symptoms and determine what to do next.

• For Regence Nurse Advice Line, call 1-800-267-6729.

• For Group Health Consulting Nurse, with access to a physician, call 1-800-297-6877.

Quick Tip: Make a plan in advance so that you know where to go when you require care outside of office hours. Contact your primary care provider or go online to locate an emergency room or urgent care center near you.

Group Health members can access this information, and much more, with the Group Health mobile app for smartphones.

Reducing costs with “formulary” drugs

Every medical plan has a drug formulary: a list of generic and brand-name drugs developed by a panel of doctors and pharmacists to ensure that the most appropriate and cost-effective medication is used to treat your health condition.

If you are prescribed a drug that is not on your plan formulary, talk to your doctor about an alternative. Medications not included on the health plan’s formulary will cost you more.

Medical benefitsMedical benefits overview | Medical plan comparison | Group Health Options Plan | Regence PPO, Engage and HSA Plans

2015 BENEFITS GUIDE 22

Medical benefitsMedical benefits overview | Medical plan comparison | Group Health Options Plan | Regence PPO, Engage and HSA Plans

Comparison of Medical Plans: Effective January 1, 2015 – December 31, 2015Group Health Options Plan Regence Pro Regence Engage Regence HSA

(Non-Represented employees only)In-network Out-of-network

Deductible — Calendar Year

No annual deductible $400 per person

$1,200 per family

$300 per person

$900 per family

$1,200 per person

$2,400 per family

$1,500 for Employee Only coverage. $3,000 for Employee+Family coverage (Family deductible must be met before plan pays benefits.)

Copays/Coinsurance

In-Network: $20 copay usually required per professional service. After copay, most services are covered in full unless specifically stated otherwise.

Out-of-Network: After the deductible, the plan pays 80% of Usual, Customary and Reasonable (UCR) to the out-of-pocket maximum, then 100% for the remainder of the calendar year.

After the deductible, the plan pays: In-Network (Category 1 Preferred): 80% up to out-of-pocket maximum, then 100% for the remainder of the calendar year.

Out-of-Network (Category 2 & 3 Participating and Non-Participating): 50% up to out-of-pocket maximum, then 100% for the remainder of the calendar year.

Category 1, 2 & 3 providers: After the deductible, the plan pays 80% up to out-of-pocket maximum, then 100% for the remainder of the calendar year.

After the deductible, the plan pays: In-Network (Category 1 Preferred): 80% up to out-of-pocket maximum, then 100% for the remainder of the calendar year.

Out-of-Network (Category 2 & 3 Participating and Non-Participating): 50% up to out-of-pocket maximum, then 100% for the remainder of the calendar year.

Out-of-pocket maximum including deductible amounts — calendar year

In-Network:

$2,000 per person $4,000 per family Combined for In & Out-of-Network

Out-of-Network:

2,400 per person $5,200 per family Combined for In & Out-of-Network

$1,300 per person $2,600 per family

$2,200 per person $4,400 per family

$4,500 for Employee Only coverage $9,000 for Employee+Family coverage

Accessing care & services

Choose a personal physician from any of Group Health’s 25 medical centers or a Group Health-contracted physician.

Select from physicians at Group Health medical centers statewide or contracted physicians statewide; and access specialists at Group Health medical centers by self-referring.

You can change doctors any time.

Care and services may be received from any licensed provider.

You have access to First Choice Health network and First Health network providers for less out-of-pocket costs; network discounts mean your portion of the bill is at a reduced cost.

If you use a provider who is not a First Choice or First Health provider, you may be responsible for any billed charges above the allowed amounts.

You can switch between in-network and out-of-network providers any time.

Care and services received from a Preferred provider or facility will generally be provided at a higher benefit level and reduce your out-of-pocket costs.

Category 1 & 2 (Preferred & Participating) providers: You will not be billed for balances beyond any deductible and/or coinsurance (balance billing).

Category 3 (Non-Participating) providers do not have a contract with Regence and can balance bill above the Regence allowed amount.

Care and services may be received from any licensed provider. If you use a Preferred or Participating provider you may have less out-of-pocket expense.

Category 1 & 2 (Preferred & Participating) providers: You will not be billed for balances beyond any deductible and/or coinsurance (balance billing).

Category 3 (Non-Participating) providers do not have a contract with Regence and can balance bill above the Regence allowed amount.

Care and services received from a Preferred provider or facility will generally be provided at a higher benefit level and reduce your out-of-pocket costs.

Category 1 & 2 (Preferred & Participating) providers: You will not be billed for balances beyond any deductible and/or coinsurance (balance billing).

Category 3 (Non-Participating) providers do not have a contract with Regence and can balance bill above the Regence allowed amount.

Service area Service area includes portions of Western, Central and Eastern Washington and Northern Idaho.

Service area is worldwide. First Choice Health network is available in WA, AK, ID, MT and OR. First Health network is available in all other states.

Service area is worldwide. Services received outside of Regence BlueShield service area are available through the BlueCard program.

Service area is worldwide. Services received outside of Regence BlueShield service area are available through the BlueCard program.

Service area is worldwide. Services received outside of Regence BlueShield service area are available through the BlueCard program.

This summary of your medical benefits is for your information only. It is not intended as a complete description of the benefits. Although we’ve made every effort to ensure this comparison is accurate, provisions of the official plan documents and contracts will govern in case of conflict. In addition, this comparison does not constitute an employment contract or a guarantee to continue employment for any period of time. This program is subject to review and (subject to the provisions of any applicable collective bargaining agreement) may be modified or terminated in whole or in part at any time for any reason.

2015 BENEFITS GUIDE 23

Comparison of Medical Plans: Effective January 1, 2015 – December 31, 2015Group Health Options Plan Regence Pro Regence Engage Regence HSA (Non-Represented

employees only)In-network Out-of-network

Prescription Drugs Certain medications require pre-authorization.

Group Health: Go to ghc.org. Click on Members, then Pharmacy Services, and search their Drug Formulary to check if a medication requires pre-authorization. Or call GHC Pharmacy Help desk at 1-800-245-7979.

Regence: Go to regencerx.com Select Learn About Medications, then on Alternatives or Prior Auth/ Medication Quantities for list of specific drugs with preauthorization requirements under Regence BlueShield (WA).

Pharmacy: 30-day supply $4 copay – Value Based medication $8 copay – Formulary Generic $25 copay – Formulary Brand $50 copay – Non-Formulary Generic and Brand.

Pharmacy: 30-day supply $13 copay – Formulary Generic $30 copay – Formulary Brand $55 copay – Non-Formulary Generic and Brand.

Participating Pharmacy: 30-day supply $0 copay – Value Based medication $5 copay – Formulary Generic $25 copay – Formulary Brand $50 copay – Non-Formulary Brand

Participating Pharmacy: 30-day supply $0 copay – Value Based medication $5 copay – Formulary Generic $25 copay – Formulary Brand $50 copay – Non-Formulary Brand

Participating Pharmacy: 30-day supply $0 copay – Value Based medication Ded+20% – Formulary Generic Ded+20% – Formulary Brand Ded+20% – Non-Formulary Brand

Non-participating Pharmacies: Covered at Out-of-Network benefit level or not covered.

Non-participating Pharmacies: Covered at same copays, but may be required to pay in full and submit for reimbursement. May also be responsible for excess charges by non-participating pharmacies above covered expenses.

Non-participating Pharmacies: Covered at same copays, but may be required to pay in full and submit for reimbursement. May also be responsible for excess charges by non-participating pharmacies above covered expenses.

Non-participating Pharmacies: Covered at same cost shares, but may be required to pay in full and submit for reimbursement. May also be responsible for excess charges by non-participating pharmacies above covered expenses.

Mail Order: 30-day supply $0 copay – Value Based medication All others – $5 discount per 30 days

Mail Order: Not covered If filled at GHO pharmacies or In- Network, covered through the Group Health mail order program

Mail Order: 90-day supply $0 copay – Value Based medication $10 copay – Formulary Generic $50 copay – Formulary Brand $100 copay – Non-Formulary Brand

Mail Order: 90-day supply $0 copay – Value Based medication $10 copay – Formulary Generic $50 copay – Formulary Brand $100 copay – Non-Formulary Brand

Mail Order: 90-day supply $0 copay – Value Based medication Ded+20% – Formulary Generic Ded+20% – Formulary Brand Ded+20% – Non-Formulary Brand

Preventive Care / Routine Services, i.e. well baby care, routine physical exams & screenings

100%

Covered in accordance with the well care schedule established by Group Health and the Patient Protection and Affordable Care Act of 2010. The well care schedule is available in Group Health medical centers, at ghc.org, or upon request from Customer Service.

Commercial Drivers License (CDL) exam for the Subscriber is covered once every 24 months, in-network only.

100%, Deductible waived

Covered in accordance with the well care schedule established by Group Health and the Patient Protection and Affordable Care Act of 2010. The well care schedule is available in Group Health medical centers, at ghc.org, or upon request from Customer Service.

In-Network: 100%, Deductible waived

Out-of-Network: 100%, Deductible waived Covered services are in accordance with age limits and frequency guidelines according to, and as recommended by, the United States Preventive Service Task Force (USPSTF), the Health Resources and Services Administration (HRSA), or the Advisory Committee on Immunization Practices of the Centers for Disease Control and Prevention (CDC). For a list of services, visit regence.com or contact Customer Service.

If a condition of employment, Department of Transportation annual physicals are covered.

100%, Deductible waived

Covered services are in accordance with age limits and frequency guidelines according to, and as recommended by, the United States Preventive Service Task Force (USPSTF), the Health Resources and Services Administration (HRSA), or the Advisory Committee on Immunization Practices of the Centers for Disease Control and Prevention (CDC). For a list of services, visit regence.com or contact Customer Service.

If a condition of employment, Department of Transportation annual physicals are covered.

In-Network: 100%, Deductible waived Out-of-Network: 100%, Deductible waived

Covered services are in accordance with age limits and frequency guidelines according to, and as recommended by, the United States Preventive Service Task Force (USPSTF), the Health Resources and Services Administration (HRSA), or the Advisory Committee on Immunization Practices of the Centers for Disease Control and Prevention (CDC). For a list of

services, visit regence.com or contact Customer Service.

If a condition of employment, Department of Transportation annual physicals are covered.

This summary of your medical benefits is for your information only. It is not intended as a complete description of the benefits. Although we’ve made every effort to ensure this comparison is accurate, provisions of the official plan documents and contracts will govern in case of conflict. In addition, this comparison does not constitute an employment contract or a guarantee to continue employment for any period of time. This program is subject to review and (subject to the provisions of any applicable collective bargaining agreement) may be modified or terminated in whole or in part at any time for any reason.

Medical benefitsMedical benefits overview | Medical plan comparison | Group Health Options Plan | Regence PPO, Engage and HSA Plans

2015 BENEFITS GUIDE 24

Group Health Options Plan

The Group Health Options Plan gives you access to the Group Health Cooperative provider network, as well as community physicians who contract with Group Health. Most in-network services are covered at only a $20 copay. Additionally, you can choose out-of-network care through the First Choice Health network or First Health network at a discount, or see any licensed provider anywhere. If you’re considering the Group Health Options Plan, find helpful information on how it works at ghc.org/pse.

With in-network care

You can choose from hundreds of personal physicians from any of Group Health’s 25 statewide medical centers or a Group Health–contracted physician. You can also refer yourself to hundreds of specialists at Group Health Medical Centers — and change doctors at any time.

You’ll also benefit from:

• Lower costs than going out-of-network.

• Online explanation of benefits, certificate of coverage and a library of 5,000 health topics.

These convenient services are available to all plan participants who use a Group Health Medical Center:

• Use of the Group Health mobile app services.

• Secure email access to your doctor.

• Access to your online medical record and test results (and your child’s through age 12) and after-visit summaries.

• Enhanced 24-hour Consulting Nurse helpline with access to your personal medical records.

• Online appointment scheduling.

• Lab, pharmacy and X-ray services located on-site at most Group Health Medical Centers.

Preventive care is covered in full with no copay for in- or out-of-network care.

With out-of-network care

You can choose from the First Choice Health network (fchn.com) in Washington, Oregon, Idaho, Montana, and Alaska; First Health (firsthealth.com) and its affiliates in any other state; or any licensed provider. You receive care at a reduced cost at your out-of-network benefit level for your portion of the medical bill if you use a provider who is part of the First Choice Health network or First Health network. Otherwise, you can receive care from any licensed provider at your out-of-network benefit level.

You’ll also be able to:

• Visit a Group Health Medical Center, when needed, or refer yourself to hundreds of specialists at Group Health Medical Centers.

• Switch between in-network and out-of-network providers at any time.

• Access some online services such as explanation of benefits and certificate of coverage.

• Use the 24-hour Consulting Nurse helpline and online library of 5,000 health topics.

For more information, go to ghc.org and select MyGroupHealth for Members. You can link to online provider directories and find information for pharmacy services and other available health care services.

Remember: Using out-of-network providers results in greater costs to you. If you have services that would not be covered in-network, they will not be covered out-of-network.

Medical benefitsMedical benefits overview | Medical plan comparison | Group Health Options Plan | Regence PPO, Engage and HSA Plans

2015 BENEFITS GUIDE 25

Prescriptions and your Group Health Options Plan

You can have your prescriptions filled at any pharmacy listed in your provider directory or at ghc.org. Prescriptions written by an out-of-network provider can be filled at any MedCare National Network Pharmacy, managed through MedImpact, at the out-of-network benefit level. They can also be filled at any Group Health pharmacy or through the Group Health mail-order service at the in-network benefit level if the prescription is on the Group Health formulary. Applicable cost shares will apply.

Value Based Pharmacy Program — helping you manage maintenance medications

Group Health has a Value Based Pharmacy Program to help plan participants significantly reduce the cost of copays for maintenance medications. The program is designed to help employees manage chronic health conditions, encourage self-care, and promote the use of preventive screening services.

30-day supply copay — in-network

$50 Nonformulary generic and

brand-name drugs copay

$25 Brand-name drugs copay

$8 Generic drugs copay

$4 Value-based drugs, in-network copay

The Group Health Mail Order Program is a great way to save money on your maintenance medications. Value-based medications have no charge for a 30-day supply. (For other in-network prescriptions, you receive a $5 discount per 30-day supply.)

For a complete list of value-based medications, go to Benefits from the HR home page on PSEWeb and select Group Health Value Based Medication List.

Four easy ways to order refills for home delivery:

1. Online — Register with MyGroupHealth. When this one-time process is completed, log in to the online pharmacy anytime with your member ID number and password.

2. Phone — Call the pharmacy line to refill a prescription and request home delivery. The telephone number is 1-800-245-7979.

3. Fax — Complete and fax a mail-order request form — available at Group Health Medical Centers and under Pharmacy Services on ghc.org.

4. Mail — Complete and mail a mail-order request form — available at Group Health Medical Centers and under Pharmacy Services on ghc.org.

For more information, go online to ghc.org or call Customer Service at 1-888-901-4636.

If you have questions about specific medications, call the Group Health Pharmacy Help Desk at 1-800-245-7979.

Medical benefitsMedical benefits overview | Medical plan comparison | Group Health Options Plan | Regence PPO, Engage and HSA Plans

2015 BENEFITS GUIDE 26

Regence PPO, Engage and HSA plans

What’s the most cost-effective plan for you?

Regence provides two plan options for all PSE employees — Preferred Provider (PPO) and Engage. Non-represented employees may also choose the Health Savings Account (HSA) plan. Understanding the key differences between the plans could help you and your family make the most cost-effective choice.

Provider coverage: The PPO and HSA plans cover preferred providers at 80 percent, while other participating or noncontracted providers are covered at 50 percent. The Engage plan covers any licensed provider at 80 percent.

Annual deductible: The PPO plan has a $300 individual deductible as compared to $1,200 for the Engage plan and $1,500 for the HSA plan. If you include family members on the HSA plan, the family deductible of $3,000 must be met before the plan begins to pay benefits.

Annual out-of-pocket maximum: The PPO plan has an individual total out-of-pocket maximum of $1,300 per calendar year as compared to $2,200 for the Engage plan and $4,500 for the HSA plan. (Your deductible and copays count toward your out-of-pocket maximum for all plans.)

Plan cost: The PPO plan is significantly more expensive — more than 40 percent higher than the Engage plan coverage. Review your plan cost carefully, using the online enrollment system tools.

At this time, non-represented employees are eligible for the HSA plan. For more information about the HSA plan, visit pse.com/hsaplan.

Open Enrollment is a good time to sit down and review your annual health care costs and better understand which benefit plan provides the best coverage for your projected health care expenses.

Redesigned regence.com enhances online experience

Inspired by member feedback, Regence has redesigned its website for an enriched online experience. At regence.com, plan participants can now access their personal data all in one place and experience a host of new features:

• A member dashboard that provides an overview of key information including a summary of benefit maximums, how much has been used and what’s remaining.

• Claims, coverage and electronic Explanation of Benefits (EOB) that are simplified and streamlined.

• A treatment cost estimator to help members compare cost of services by different providers.

Take a test drive at regence.com today and explore the tools, tips and data you value most when making decisions about your health and your family’s.

Medical benefitsMedical benefits overview | Medical plan comparison | Group Health Options Plan | Regence PPO, Engage and HSA Plans

2015 BENEFITS GUIDE 27

Value-based drug coverage

No copay is required for certain maintenance medications that help with asthma, diabetes, high-blood pressure, high cholesterol, nicotine dependence and other chronic conditions. You may be able to prevent specific illnesses, symptoms and improve your overall health with maintenance medications.

To find out if the formulary or generic medication you require has no copay, go to Benefits/Medical Benefits/Regence prescriptions from the HR home page on PSEWeb and select the Regence Rx Value Based Medication list.

Regence prescriptions

The Regence benefit plans’ prescription medications are defined by four tiers.

The four-tier approach encourages you and your doctor to try lower-cost medications before moving to higher-priced alternatives.

Rx: Regence PPO and Engage plans

$50 Nonformulary brand-name copay

$25 Formulary brand-name copay

$5 Generic drug copay

$0 Value-based drug, copay

Regence members have coverage for all four categories. What you pay (your copay) depends on which medication (or tier) you and your doctor choose.

You can help lower costs for yourself and for the PSE medical plan by making good choices about your prescription drugs.

• Use generics when available.

• Shop around for pharmacies charging less for the same drug.

The cost of prescription medications is not the copay or even the $50 that you pay at the pharmacy. The actual cost should be printed on your receipt — if not, ask your pharmacist.

Prior authorization required for some medicationsMedications requiring prior authorization generally are in one of these categories:

• Used for conditions excluded from the plan, such as obesity or cosmetic improvements.

• Have safety issues or a high potential for inappropriate use.

• Have a clinical alternative that is a much lower-priced medication.

For maintenance medications, order online and save

If you plan to use mail order and do not have a sufficient supply on hand to last you until your mail order arrives (allow two to three weeks), ask your doctor for two prescriptions — one for the local pharmacy and the other for mail order.

For more information, go online to regence.com or call customer service at 1-866-240-9580.

Medical benefitsMedical benefits overview | Medical plan comparison | Group Health Options Plan | Regence PPO, Engage and HSA Plans

2015 BENEFITS GUIDE 28

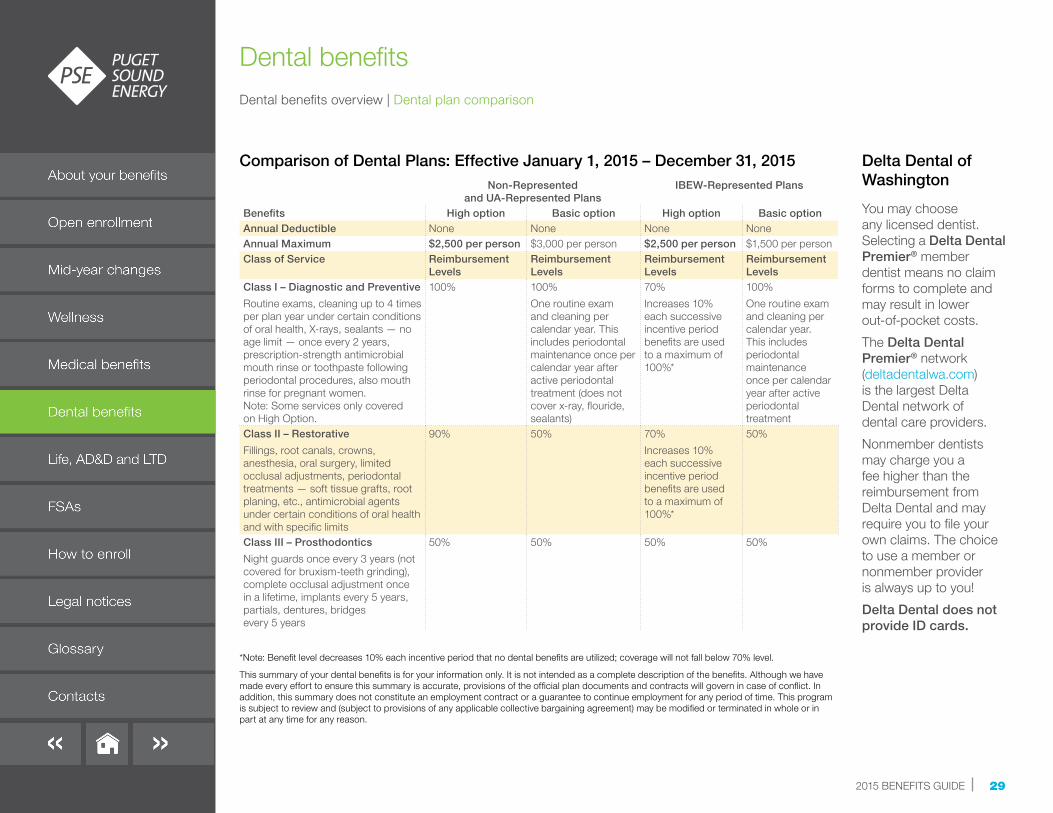

Dental benefits overview

Choose from the following three options:

1. Basic Option

• Covers one exam and one cleaning per plan year.

• Provides comprehensive coverage (fillings and crowns).

• Does not cover additional diagnostic or preventive care (X-rays, fluoride or sealants).

2. High Option

• Provides comprehensive coverage (fillings and crowns).

• Provides for preventive and diagnostic care (cleanings and X-rays) twice per plan year.

3. Opt Out Dental

• Opt Out certification is required when enrolling online. See page 7 for details.

Did you know?

Some services covered at 90 percent in the PSE High Option plan are covered at 80 percent or less under most other employer’s dental plans. The maximum annual coverage is also generous. PSE does not restrict your choice of providers to a preferred network — you have a very wide range of providers from which to choose. However, if you visit a Delta Dental Premier® dentist, your out-of-pocket expense will be lower.

Dental benefitsDental benefits overview | Dental plan comparison

Quick Tip: Pay for noncovered services with tax-free dollars in your health care FSA or HSA.

2015 BENEFITS GUIDE 29

Delta Dental of Washington

You may choose any licensed dentist. Selecting a Delta Dental Premier® member dentist means no claim forms to complete and may result in lower out-of-pocket costs.

The Delta Dental Premier® network (deltadentalwa.com) is the largest Delta Dental network of dental care providers.

Nonmember dentists may charge you a fee higher than the reimbursement from Delta Dental and may require you to file your own claims. The choice to use a member or nonmember provider is always up to you!

Delta Dental does not provide ID cards.

*Note: Benefit level decreases 10% each incentive period that no dental benefits are utilized; coverage will not fall below 70% level.

This summary of your dental benefits is for your information only. It is not intended as a complete description of the benefits. Although we have made every effort to ensure this summary is accurate, provisions of the official plan documents and contracts will govern in case of conflict. In addition, this summary does not constitute an employment contract or a guarantee to continue employment for any period of time. This program is subject to review and (subject to provisions of any applicable collective bargaining agreement) may be modified or terminated in whole or in part at any time for any reason.

Dental benefitsDental benefits overview | Dental plan comparison

Comparison of Dental Plans: Effective January 1, 2015 – December 31, 2015Non-Represented

and UA-Represented PlansIBEW-Represented Plans

Benefits High option Basic option High option Basic optionAnnual Deductible None None None NoneAnnual Maximum $2,500 per person $3,000 per person $2,500 per person $1,500 per personClass of Service Reimbursement

LevelsReimbursement Levels

Reimbursement Levels

Reimbursement Levels

Class I – Diagnostic and Preventive

Routine exams, cleaning up to 4 times per plan year under certain conditions of oral health, X-rays, sealants — no age limit — once every 2 years, prescription-strength antimicrobial mouth rinse or toothpaste following periodontal procedures, also mouth rinse for pregnant women. Note: Some services only covered on High Option.

100% 100%

One routine exam and cleaning per calendar year. This includes periodontal maintenance once per calendar year after active periodontal treatment (does not cover x-ray, flouride, sealants)

70%

Increases 10% each successive incentive period benefits are used to a maximum of 100%*

100%

One routine exam and cleaning per calendar year. This includes periodontal maintenance once per calendar year after active periodontal treatment

Class II – Restorative

Fillings, root canals, crowns, anesthesia, oral surgery, limited occlusal adjustments, periodontal treatments — soft tissue grafts, root planing, etc., antimicrobial agents under certain conditions of oral health and with specific limits

90% 50% 70%

Increases 10% each successive incentive period benefits are used to a maximum of 100%*

50%

Class III – Prosthodontics

Night guards once every 3 years (not covered for bruxism-teeth grinding), complete occlusal adjustment once in a lifetime, implants every 5 years, partials, dentures, bridges every 5 years

50% 50% 50% 50%

2015 BENEFITS GUIDE 30

Basic Life insurance

PSE covers 100 percent of the cost of Basic Life insurance for all employees. The life insurance plan pays a benefit to your beneficiary for the coverage amount if you die while you are insured. MetLife is the insurance carrier for life and AD&D plans as of January 1, 2015.

Accidental Death & Dismemberment (AD&D) insurance (optional)

This insurance provides coverage for loss of life, loss of limb or loss of use following an accident.

• The benefit is paid to the accident survivor if the loss meets the carrier payment criteria.

• You may elect coverage of $50,000 up to $250,000, available as Employee Only or Employee + Family coverage.

• Elections cannot exceed 10 times your annual base pay.

• Eligible dependents include your spouse/domestic partner and unmarried dependent children under 26.

Supplemental Life insurance (optional)

This coverage is in addition to your Basic Life coverage amount. You may choose additional coverage amounts of one, two, three or four times your annual base pay, up to the plan limits.

One-time opportunity to add coverage during this Open Enrollment

If you are not currently enrolled for Supplemental Life insurance and you choose coverage during Open Enrollment, you are usually required to complete a medical review and Evidence of Insurability (EOI) form. However, with this year’s change to MetLife, you have a one-time opportunity to add this coverage without a medical review during this year’s Open Enrollment period, if you are not currently enrolled.

If you have existing coverage, you can take advantage of the lower rates through MetLife, the new plan administrator, and increase coverage by one times your annual base pay without a medical review.

Select the level of coverage appropriate for your needs. If any portion of the requested amount is subject to approval first, you will receive an EOI form directly from MetLife.

Keeping your supplemental life

If you leave PSE, you have the option of continuing your Supplemental Life insurance by completing a portability form and submitting payment according to the carrier requirements within 31 days from the day your coverage terminates.

Enrolling as a new hire

If you enroll in Supplemental Life insurance within the first 31 days of eligibility, you do not need to provide an EOI. You may enroll for up to four times your annual base salary.

Important: The IRS tax code requires PSE to charge you imputed income for life insurance in excess of $50,000.

Life, AD&D and LTD InsuranceLife, AD&D insurance | Long-term disability

Supplemental Life insurance rates (per $1,000 of coverage)

Example: For a 50-year old employee earning $50,000 per year: $.25 x $50,000/1,000 = $12.50 per month. $12.50 x 12 = $150 (your annual cost)

Age band Rate< 30 0.06

30 – 34 0.0835 – 39 0.10

40 – 44 0.1045 – 49 0.1650 – 54 0.2555 – 59 0.4460 – 64 0.6665 – 69 1.27

> 70 2.06

2015 BENEFITS GUIDE 31

Life, AD&D and LTD InsuranceLife, AD&D insurance | Long-term disability

Long Term Disability

PSE covers 100 percent of the cost of your Long Term Disability premium. MetLife is the insurance carrier for the Long Term Disability plan as of January 1, 2015.

Should you become disabled, you have the option of receiving the LTD monthly payment as taxable or nontaxable income. When you enroll online, this payroll designation will be available to you. You may only change this option, which becomes effective January 1, at annual Open Enrollment.

Your premium election for LTD may be made with pre-tax or post-tax dollars: You decide.

• Pre-tax premium election: You are not taxed on the value of the LTD premium paid by PSE. If you have an approved disability in the future, your monthly benefit payments are reduced by applicable federal income taxes.

• Post-tax premium election: You are taxed now on the value of the LTD premium paid by PSE. If you have an approved disability in the future, your monthly benefit payments are not reduced because you already paid federal income taxes. (You will see Imputed HC Cost on your paychecks.)

Your coverage

The plan pays up to 65 percent of your base monthly pay if you become disabled from a covered injury, illness or pregnancy.

Survivor benefit

If an employee dies while receiving Long Term Disability benefit payments from PSE, the surviving domestic partner may receive a one-time lump-sum payment just like a legal spouse would according to the contract. The employee must have a valid domestic partner declaration on file with PSE at the time of death and be receiving a monthly LTD benefit.