welcome to financial freedom “ there is probably no area where we have a greater opportunity to...

TRANSCRIPT

Welcome to Financial Freedom

“There is probably no area where we have a greater opportunity to make a mess of our lives than in this area of our finances. …….If we do

not get control of our money according to God’s principles, we will never manage our

time and talents well for God’s purpose.”

Objective – Provide Tools For:

• Establishing personal goals

• Understanding what we are spending

• Developing a Spending Plan & Debt Reduction Plan

• Controlling expenses

Cultural Myths

• Things bring happiness.• We can have everything we want, and we

shouldn’t have to wait for what we want.• Debt is expected and unavoidable.• Our self-worth is directly connected to our

possessions and what we do.• A little more money will solve all our problems.• Life should be easy and fair.

The Steward’s Mindset

• God created everything – Genesis 1:1 …God created the heavens and the earth

• God owns everything – Psalm 50:12…the world is Mine and all it contains

• We are managers of what He has given us – Genesis 1:26-30….Let’s make man in Our image…and let them rule over …all the earth…

Five Areas Of Our Financial Lives

• Earning

• Giving

• Saving

• Debt payment

• Spending

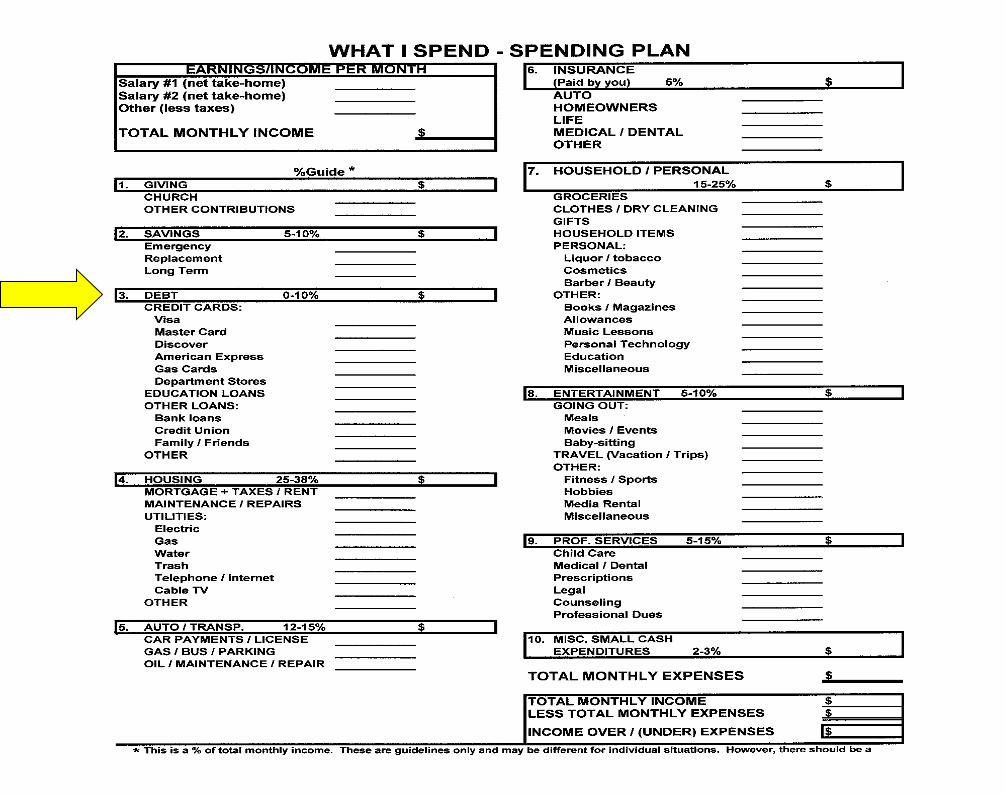

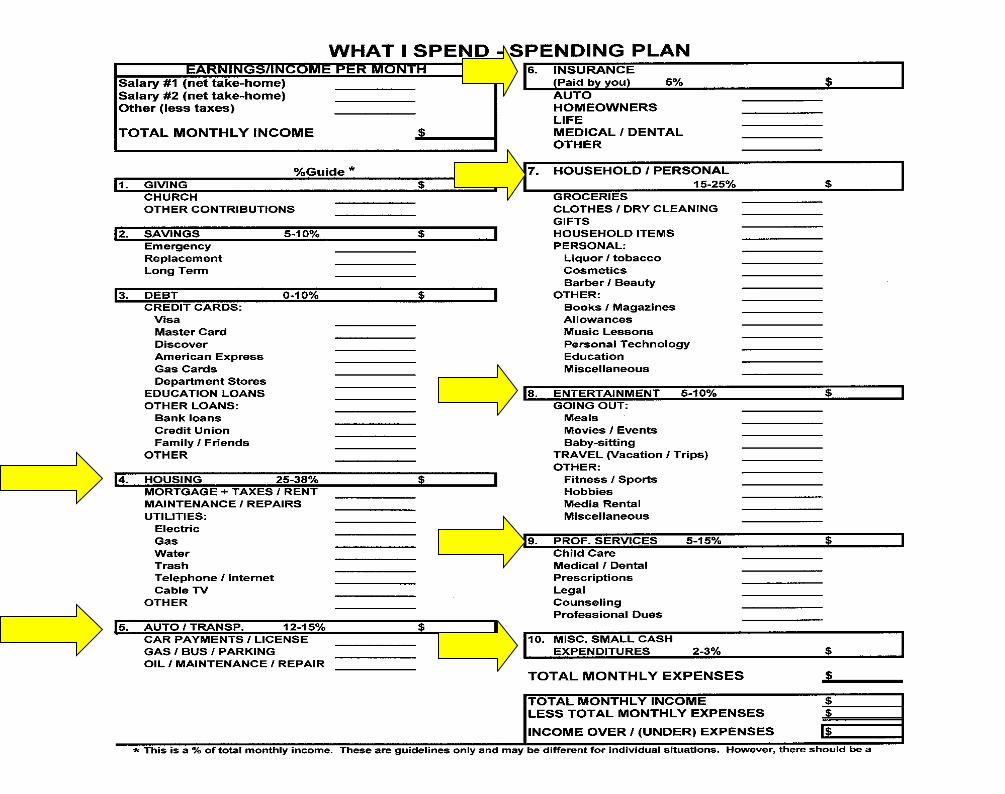

A Budget Is:

• The tool that enables us to control our money so that it doesn’t end up controlling us.

• A Spending Plan for how we will allocate our financial resources.

• The Spending Plan is the way to reach our financial goals.

The Benefits of a Spending Plan

• Gives us FACTS

• Avoids WASTE

• Keeps our VALUES and priorities in check and should reflect our financial goals

• Leads to FINANCIAL FREEDOM

The Culture Says:

• “Our value is measured by our position, achievement and our paycheck.”

• “A little more money will solve all our problems.”

Earnings - The Bible Says

• Be enthusiastic & serve God.

Colossians 3:23-24

• Provide for those dependent on us.

1 Timothy 5:8

• Be grateful.

Deuteronomy 8:17-18

Earnings: Salaries # 1 (Net Take-home Pay) Is

The amount of the paycheck after all taxes and deductions.

Earnings: Variable Incomes

Take a CONSERVATIVE estimate of our after-tax annual income—based on our income of the past few years—and divide by twelve.

Example:$30,000/12 = $2,500 per month

Earnings: Two-Income Strategy

• Income #1: Basic Lifestyle Expenses– Giving– Savings– Housing– Food – Clothing– Transportation– Basic household– Debt payment

Earnings: Two Incomes

• Income #2: Extras

– Additional giving– Additional savings– Accelerated debt repayment– Other non-essentials

• Entertainment• Gifts• Vacation

Earnings: Questions

• What happens to raises, bonuses, overtime pay, income from an extra job, or money received as gifts?

Three Cultural Myths About Giving

• “Give if it benefits us.”

• “Give if there is anything left over.”

• “Give out of a sense of duty.”

God Wants Us to Give:

• As a response to God’s goodness – James 1:17

• To focus on God as our source of security – Matt. 6:19-21

• To break the hold of money

For Those Not Giving:

• Begin by giving something.

• “Each of you must give as you have made up your mind, not reluctantly or under compulsion, for God loves a cheerful giver.” 2 Cor. 9:7 (NIV)

Saving - Two Cultural Myths:

• “If we have it, spend it; and if we don’t have it, spend it anyway.”

• “It is futile to save.”

Saving: The Bible Says:

• It is wise to save. – Proverbs 21:20

• It is sinful to hoard.– Eccl. 5:10

Savings Is:

• Money we keep

• Future spending

Compound Interest Example

• $100 @ 6% = $6.00 interest

• $106 @ 6% = $6.36 interest

The extra $0.36 is compound interest.

Setting Goals

• Financial Goals will help us decide how much to save each month

• Review goals often for motivation

• Prioritize goals

• Be realistic and make goals achievable

• Goals should reflect our values

• Goals must be quantified

Three Kinds of Savings

• Emergency savings

• Savings for major purchases

• Long-term savings

Key Question:

If giving is so right and saving is so wise, why are they so hard to do?

Cultural Order for Using Money

• Lifestyle (Spending)

• Debt

• Saving

• Giving

God-Honoring Order For Using Money

• Giving

• Saving

• Lifestyle is based on what is left

Transitional Order For Using Money

• Give. . . SOMETHING

• Save. . . a LITTLE

• Debt. . . MAXIMIZE repayment of consumer debt

• FRUGAL Lifestyle

Facts:

33% of Americans don’t have a CC

36% pay balance in full every month

31% carry a balance

Debt - Cultural Myth: “Debt is Expected and Unavoidable”

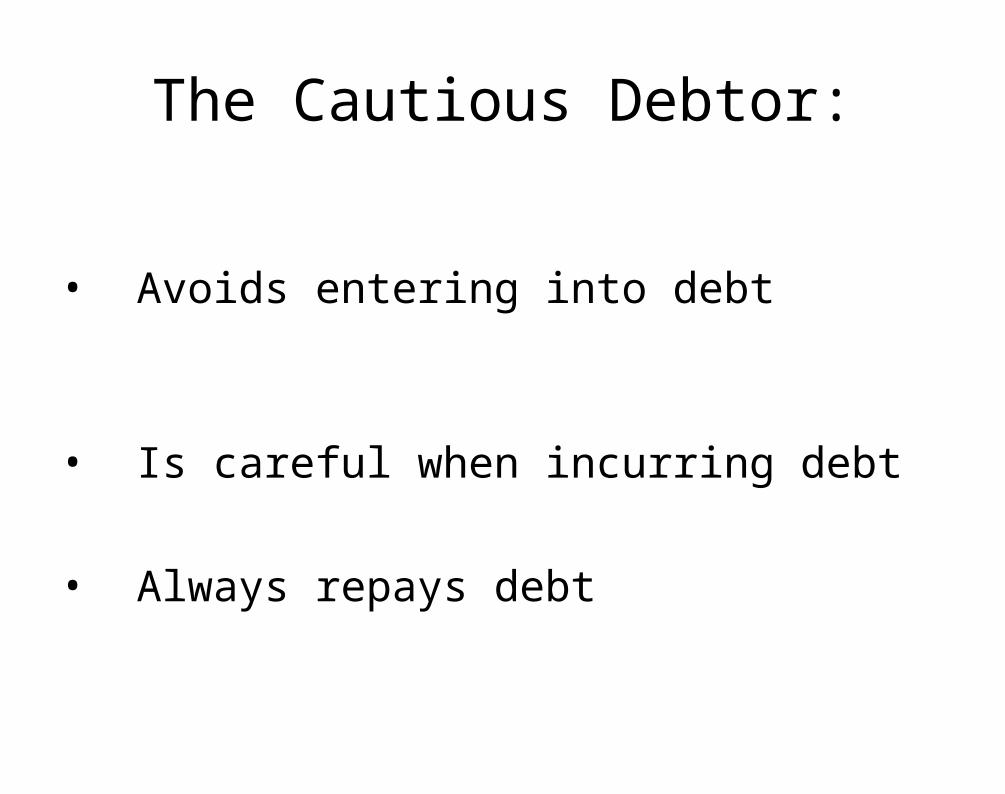

The Cautious Debtor:

• Avoids entering into debt

• Is careful when incurring debt

• Always repays debt

Biblical Guidelines:

• Repay debt – Psalm 37:21 “The wicked does not repay….”

• Avoid debt – Proverbs 22:7 “….The borrower becomes the lender’s slave.”

Three Spiritual Dangers of Debt:

• Presumes on the future – James 4:14 “….you do not know what your life will be like tomorrow….”

• Denies God the opportunity to teach us or provide for us.

• Promotes envy and greed – Luke 12:15 “…be on guard against every form of greed…”

Five Kinds of Debt:

• Auto

• Home

• Education

• Business

• Credit card

Credit Card Studies:

– The amount families spent with a credit card rose between 20% and 30% compared to paying cash

– Average on groceries - $32.96 using cash vs. $43.49 with credit

– Average spent on non-essentials at grocery $9.08 with cash vs. $18.72 with credit

– McDonald’s - $4.50 cash vs. $7.00 credit

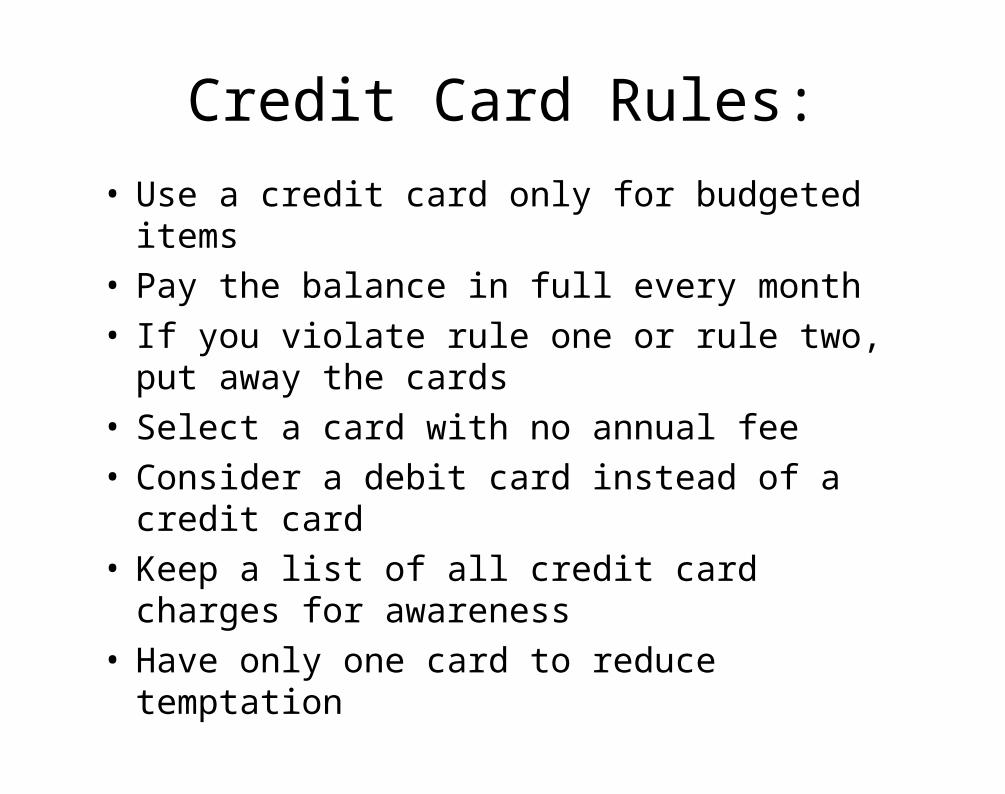

Credit Card Rules:

• Use a credit card only for budgeted items• Pay the balance in full every month• If you violate rule one or rule two, put away the

cards• Select a card with no annual fee• Consider a debit card instead of a credit card• Keep a list of all credit card charges for

awareness• Have only one card to reduce temptation

Debt Example

You owe $9,000 @ 13%(Minimum payment = 4.5% of the balance starting at $405/mo.)

You Pay Total Paid Time

$Minimum/month $11,817 11.1 years$405/month $10,352 2.2 years$405 + $100/month $10,054 1.7 years

Principles for Accelerating Debt Repayment:

• Pay off the smallest debt first.

• As each debt is repaid, roll the amount you were paying to the next largest debt.

• Incur no new debt!

Debt Reduction Plan

Item Amount Owed

Interest Minimum Monthly Payment

Additional Payment

$150

Payment Plan and Pay-Off Dates

3 Months

6 Months

15 Months

22 Months

26 Months

Sears $372 18.0 $15 $165 Paid!

Doctor $550 0 $20 $20 $185 Paid!

Visa $1,980 19.0 $40 $40 $40 $225 Paid!

Master $2,369 16.9 $50 $50 $50 $50 $275 Paid!

Auto $7,200 6.9 $259 $259 $259 $259 $259 $534 Paid!

Total $12,471 $384 $534 $534 $534 $534 $534 0

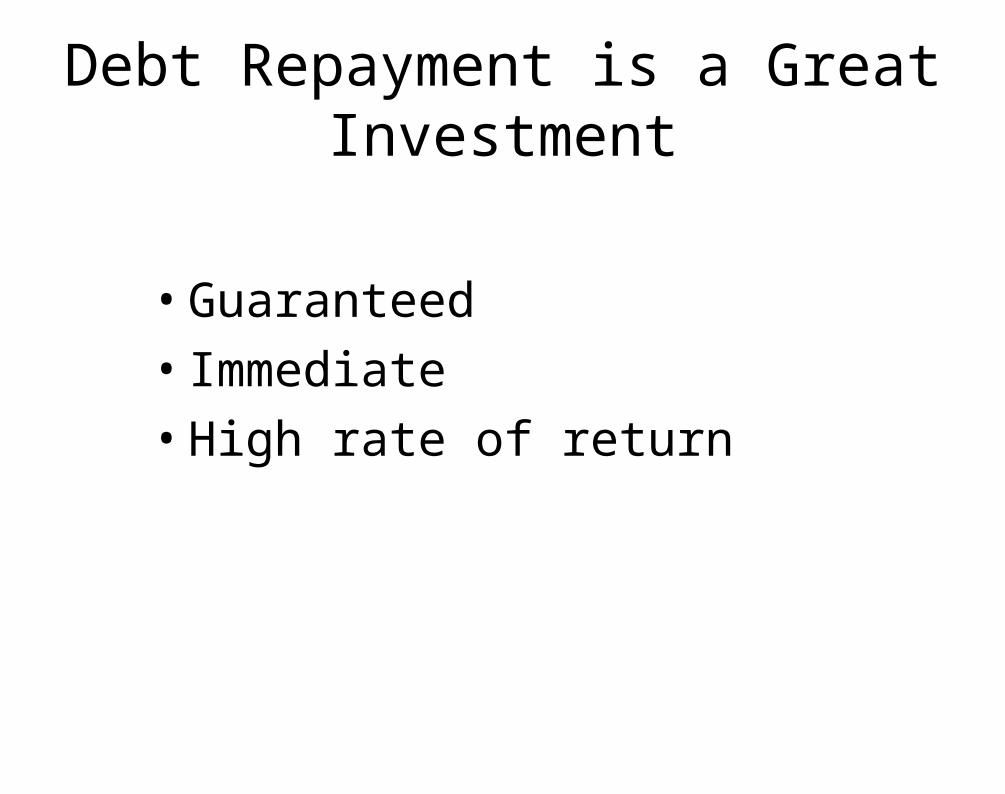

Debt Repayment is a Great Investment

• Guaranteed

• Immediate

• High rate of return

Spending - Four Myths:

• “Things bring happiness.”• “Our possessions define who we are.”• “The more we have, the more we should

spend.”• “Spending is a competition.”

Spending - Three Biblical Principles:

• Beware of idols – Dt 5:7-8; Rom 1:25

• Guard against greed and seek moderation – Lk 12:15; Prv 30:8

• Be content – Phil 4:12

Key Question:

Are we willing to be content with our true needs vs. what the culture says we need?

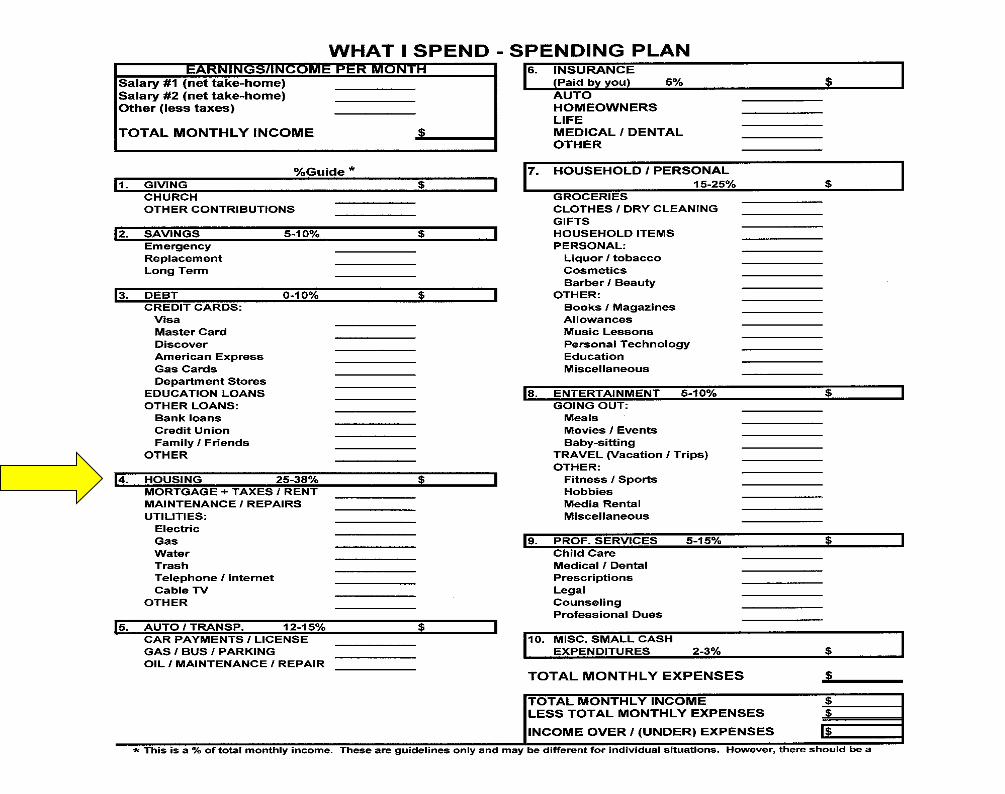

Spending: Mortgage/Taxes/Rent:

• Consider the issue of renting vs. owning

• Thinking of prepaying mortgage?

• Beware of basing a mortgage on two incomes

• Exercise caution toward equity loans

• Consider an extended household

HOUSING: COST OF BAD CREDIT ON $100,000 30-YR MORTGAGE

• A credit score of 520 will cost you $110,325 more in interest than someone with a 720 credit score.

• Or, $307.00 per month over the 30 years

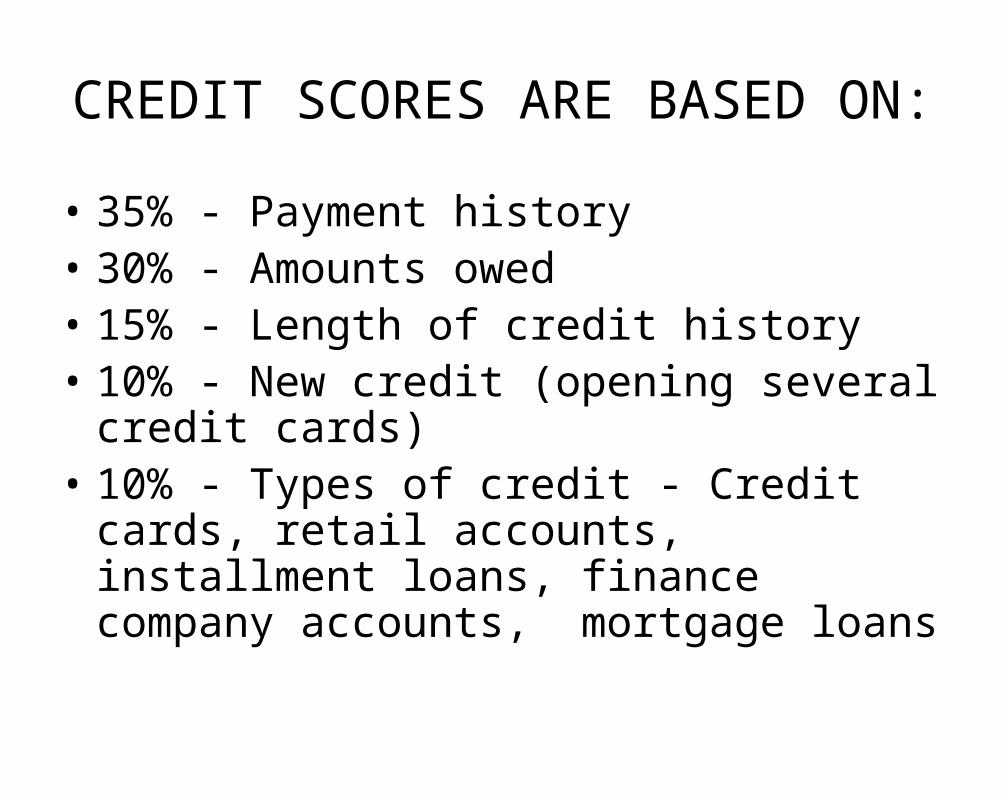

CREDIT SCORES ARE BASED ON:

• 35% - Payment history• 30% - Amounts owed• 15% - Length of credit history• 10% - New credit (opening several credit

cards) • 10% - Types of credit - Credit cards, retail

accounts, installment loans, finance company accounts, mortgage loans

CHECKING YOUR CREDIT REPORT

• Free credit report from Equifax, Experian, or TransUnion

• One report/year/bureau

• Suggest one report every four months alternating bureaus

• Online at www.annualcreditreport.com

• Or 1-877-322-8228

Housing: Maintenance and Repairs:

Become a Mr. or Ms. “Fix-it”

Housing: Utilities

• Control the thermostat. Lowering the thermostat by one degree in winter = 3 to 5% reduction in energy cost.

• Use phones wisely.

• Evaluate options for internet and cable services.

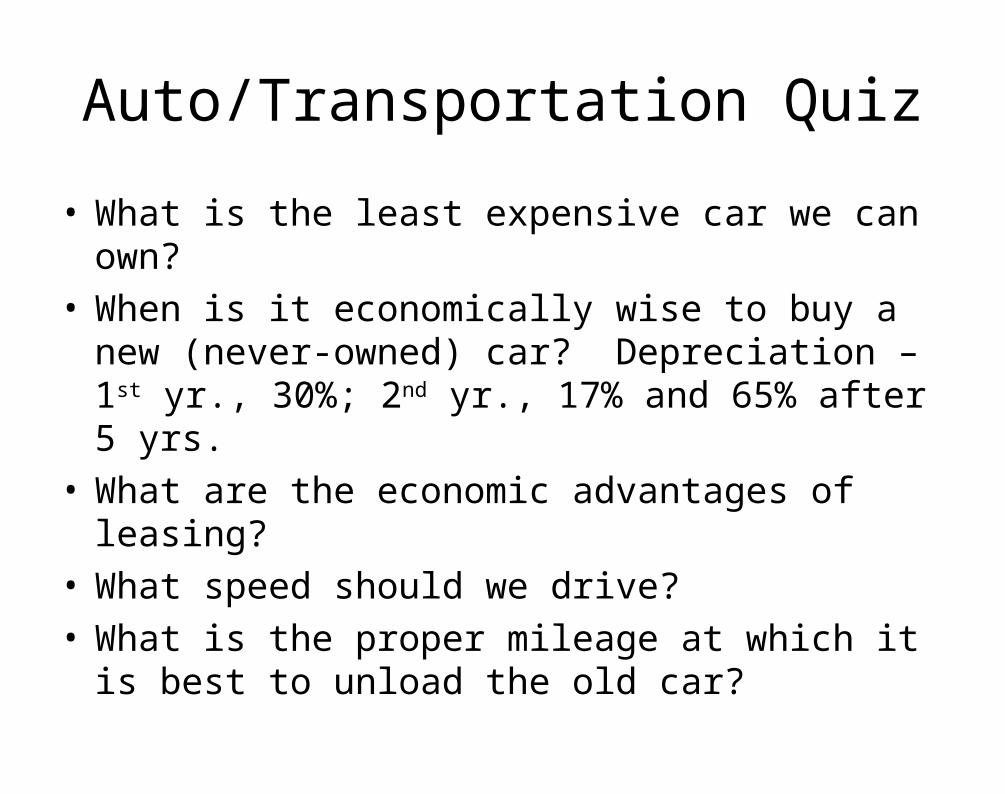

Auto/Transportation Quiz

• What is the least expensive car we can own?• When is it economically wise to buy a new (never-

owned) car? Depreciation – 1st yr., 30%; 2nd yr., 17% and 65% after 5 yrs.

• What are the economic advantages of leasing?• What speed should we drive?• What is the proper mileage at which it is best to

unload the old car?

Auto Statistics:

• Average Reliability– Life = 15 years– Mileage = 150,000

• Average Trade-in – Time = 4 years– Mileage = 55,000

Pay Cash for the Next Car!

.

Auto Insurance Tips:

• Choose the highest deductible you can afford. $1,000 deductible costs less than $500 deductible.

• Shop for it.• Combine policies.• Look for other discounts.• Consider eliminating collision coverage

on an older car.

Consider Other Insurance*

• Health• Life (renewable term)• Home or renter’s • Disability• Umbrella liability• Long-term healthcare (as you approach 60s)

* For more on insurance, take the course “Raising Your Financial IQ”

Household/Personal

• Groceries

• Clothing

• Gifts – 44% of families don’t plan gifts

• Household items

• Books and magazines

Entertainment

• Going Out – Meals, Movies/Events, Baby-sitting

• Travel – Vacations/Trips

• Other – Fitness/Sports, Hobbies, Media Rental

Professional Services

• Child Care– Evaluate the financial costs (taxes, gas, clothes,

more meals out) and relational costs (stress, less time together, less time with children, fatigue) of two working parents.

• Other– Use good judgment– Seek referrals– Evaluate progress

Three Possible Outcomes

• Scenario 1: Income exceeds expenses

• Scenario 2: Income equals expenses

• Scenario 3: Expenses exceed income

Three Ways to Adjust Our Spending Plan

• Increase income

• Sell assets

• Reduce expenses (recommended)

Reducing Expenses

• Do I have optional expenses I can eliminate?• Do I have variable expenses I can further

control and reduce?• Can I eliminate any assumptions about my

“FIXED” expenses?• Spending fast/procrastinate.• Calculate the hours worked to make the

purchase.

Key Questions:

How serious am I?

What are my options and the consequences of each option?

What are the consequences of continuing to do what I am currently doing?

Benefits of Record Keeping:

• Gives accurate data

• Improves communication

• Allows for mid-course corrections

• Provides accountability

Three Record-Keeping Systems:

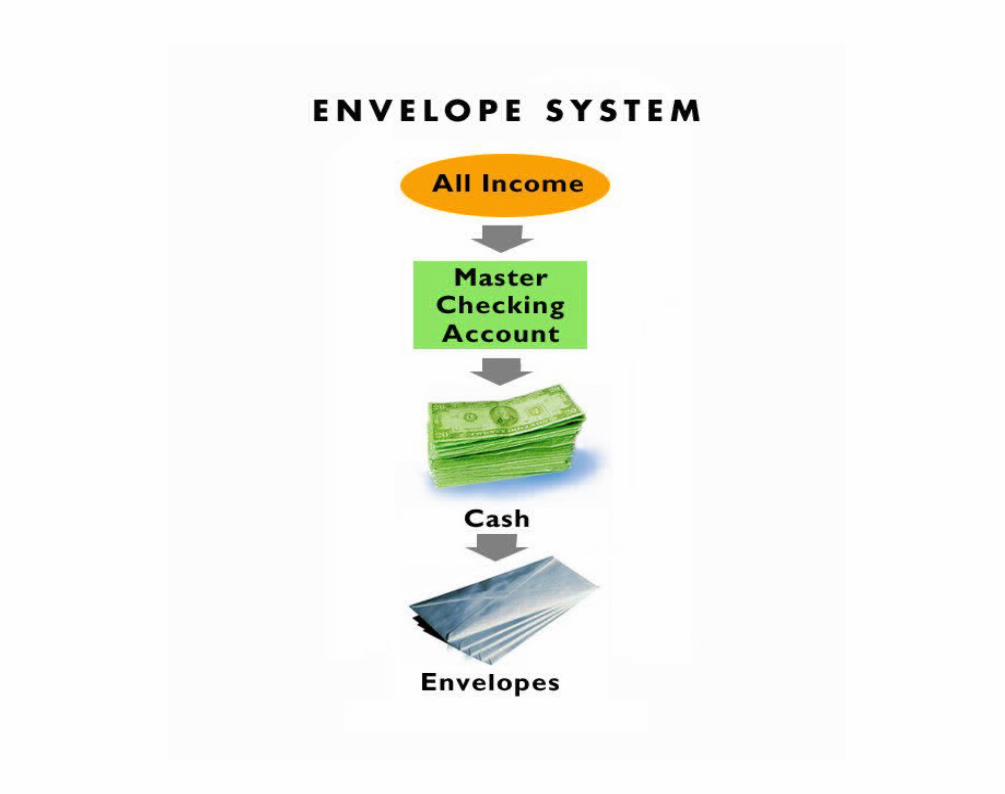

• Envelope

• Written record

• Electronic– Quicken or Excel– Mint.com– Mvelopes.com - $7.00/month

Envelope System

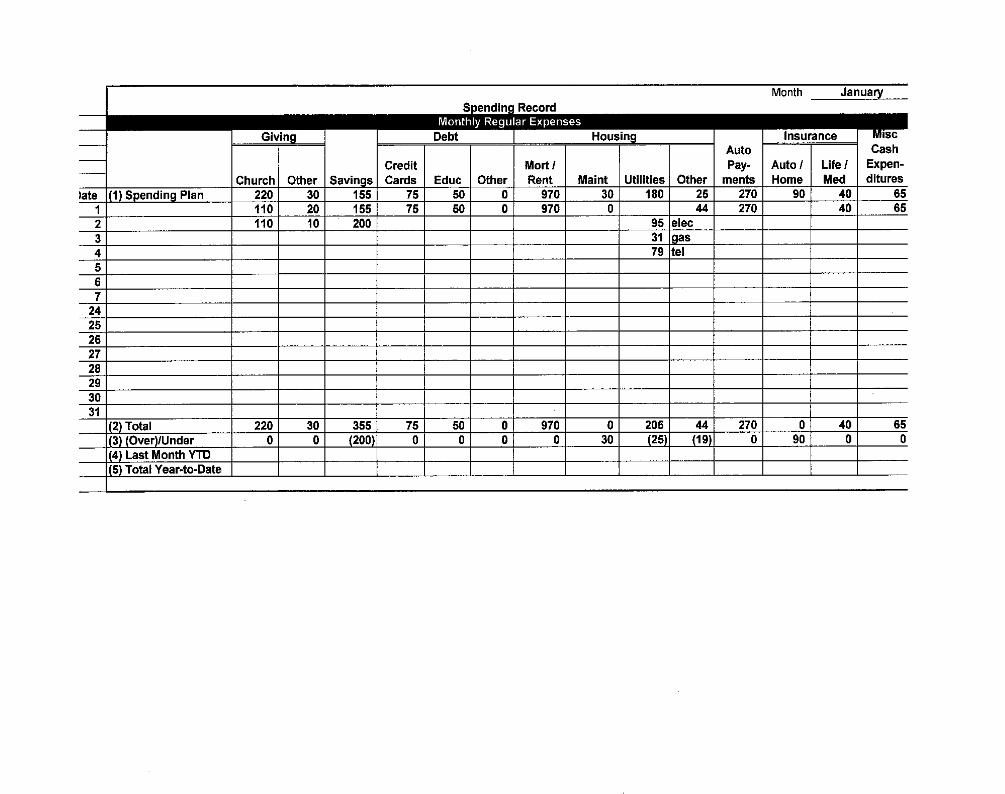

Hints to Make Record Keeping Easier:

• Keep the Spending Record where you will see it daily – make it a priority

• Round off to the nearest dollar

• Combine categories

• Estimate when you forget to record

• Use even billing for utilities & insurance

• Have a miscellaneous cash envelope or column for item 10 on the spending plan.

Electronic System(Quicken or Excel)

There are some cautions involved with starting here.

- Is the computer readily accessible?

- Will you do the updates on a regular basis?

Inertia/procrastination

Discipline

Spouses not in agreement

No emergency fund to draw on

Some Obstacles to Budgeting

The Steward’s Mindset

• God created everything – Genesis 1:1

• God owns everything – Psalm 50:12

• We are managers of what He has given us – Genesis 1:26-30

God is Able

• Philippians 4:13 says, “I can do all things through Him who strengthens me.”