vincenzo manes letter to the shareholders

TRANSCRIPT

4

letteR to tHe sHAReHoldeRs

Vincenzo manesVice Chairman

Dear Shareholders,

for the fourth year in a row I find myself starting this brief report to you on the state of our Group’s business hav-ing to refer to the enduring crisis which is gripping the Western economies, all the while swinging back and forth between the two shores of the Atlantic without reaching any kind of resolution. By now we’ve used up just about all the figures of speech to express it.Europe, which to date remains KME’s most important market, is presently going through a crucial moment indeed, probably the worst since the end of World War II.“I want to tour Europe…; and yet I realize I am only going to a graveyard, the most precious of graveyards, that’s what it is. Brave are the dead that lie buried there, every tombstone above them speaks of such an ardent life in the past, of a faith so passionate in one’s actions, in one’s truths, struggles, one’s science…”These are the words which Dostoyevsky put into Ivan Karamazov’s mouth about 150 years ago, and this is the risk which a divided Europe runs once again – of becoming, not a graveyard perhaps, but a museum of values, principles and ideas condemned to irrelevance by the ever-evolving global processes.Although 2011 started off with a few positive if contradictory signs, in the second semester markets took a nosedive as the sovereign debt crisis spread from country to country.In this environment, the Western governments and the principal international regulatory institutions have shown all their fragility, as they are unable to respond decisively to international speculative finance, whose behaviour increas-ingly reminds us of the Brechtian stereotype of capitalism.There is no longer any possible doubt that globalization is progressively shifting the axis of the world’s economic activity towards Asia and the BRICS nations. This is an unavoidable shift and cannot be countered with some sort of outdated protectionism: but for this very reason it’s high time for us to drastically overhaul international regulatory mechanisms to restore credible governance of the economic relations across different States and areas of the world.

5

ann

ual

rep

ort

KME Group thus finds itself sailing these treacherous seas, and will have to go on doing so in the foreseeable future.In 2011 the Group continued implementing the programs to reorganize and restructure all its different investment sectors, starting with its KME A.G. copper business – the biggest of its activities – and going on to renewable ener-gies with ErgyCapital SpA, and the services sector with Cobra AT SpA.The exact figures for last year’s activities are detailed in the budget report featured below.Here I would like to underline the timeliness of our actions to increase the Group’s profits, improve operational results and further reduce indebtedness. On the whole, we have retained our financial solidity thanks to a policy of carefully controlling management and costs, but also with strong measures to improve flexibility and our ability to quickly respond to the market’s growing unpredictability.We are firmly convinced that KME’s financial side must at all times be aligned with its strategies for industrial devel-opment. This is why we launched the company’s reorganization. Through the special operations going on at present and consisting of swap offers of KME and Intek shares (and those of subsequent mergers), this overhaul is meant to infuse more dynamism into the Group’s various businesses, on the basis of a coordinated logic aimed at improving the cash flow and increasing value over time.The KME and Intek merger we have in mind will consist of a single holding company benefitting not only from a sig-nificant reduction of costs, but also from important new synergies between the two companies existing presently. The aim here is to guarantee a single-pointed strategic leadership, and ever closer cooperation between the manage-ments of KME’s various investment sectors.In brief, the international situation obliges us to sail on with an ever-wathchful eye, while we remain true to KME’s core values and principles – innovation, sustainability, solidarity. Without them our very idea of doing business would lose all sense.Allow me to point out how important and meaningful the human factor has been to us in the past and even more today. Economic endeavour is made of figures, but above all of people, even though these days people often get sidelined, with the unhappy results we are seeing. For KME Group the human factor is crucial at all times, so let me here acknowledge the dedicated commitment of our entire staff at all levels. From the top management to the fac-tory personnel, all have faced the difficulties and sacrifices forced upon us by the global economic situation with an admirable spirit of sharing and fellowship.As I mentioned at the beginning, we have tricky months ahead of us, and this is because the dangers we face are due for the most part to international conditions we are powerless to influence.But let no-one try to push us into a corner. We have sufficient experience, know-how and far-sightedness to meet the new challenges squarely. Indeed, with the measures we have already put into place to streamline, diversify and internationalize, our Group can look to the coming years with reasonable hopes of success.

6

7

ann

ual

rep

ort

KME is a leading global producer of semifinished and special products, with a central role in the copper value chain. KME’s production range goes to

an extremely wide target of user industries and manufacturing sectors.

Global sales network with offices, agencies and trading companies in 4 continents

2 state-of-the-art research centres: one in italy and one in Germany

Revenue, 3 billion euros

Annual production, 485,000 tons

Headquarters and centre of operations: Florence, italy

founded in 1886 and listed on the milan stock exchange since 1897

Service and technical assistance centres in the world’s principal industrial areas

6.250 employees, more than 11.000 shareholders and 21.000 commercial partners

13 production sites: 12 in europe and one in china

net worth/debt ratio < 50%

8

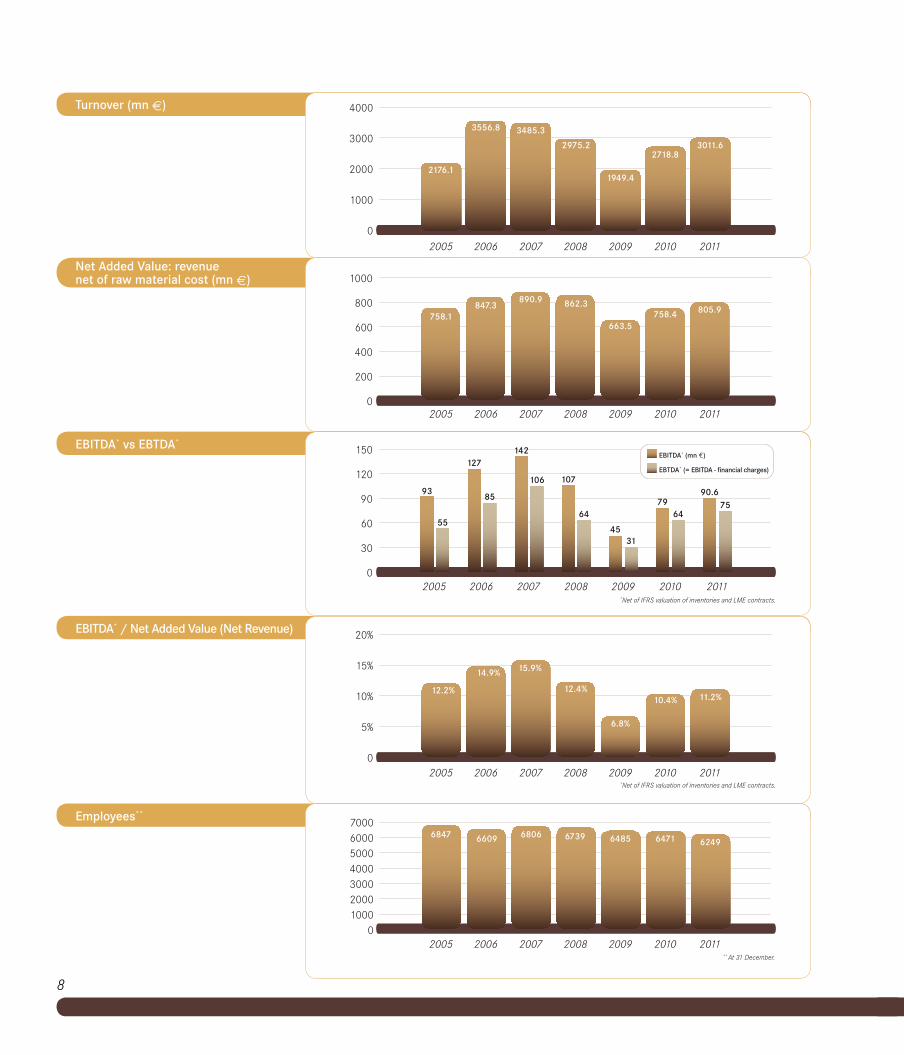

net Added Value: revenue net of raw material cost (mn €)

eBitdA* vs eBtdA*

eBitdA* / net Added Value (net Revenue)

employees**

0

1000

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2000

3000

4000

3556.8 3485.3

2975.2

1949.4

2718.83011.6

2176.1

0

200

400

600

800

1000

758.1847.3

890.9 862.3

663.5758.4 805.9

0

30

60

90

120

150 EBITDA* (mn €)

EBTDA* (= EBITDA - financial charges)

*Net of IFRS valuation of inventories and LME contracts.

*Net of IFRS valuation of inventories and LME contracts.

2005 2006 2007 2008 2009 2010 2011** At 31 December.

0

5%

10%

15%

20%

93

55

127142

107

7990.6

7564

3145

64

106

85

12.2%

14.9% 15.9%

12.4%

6.8%

10.4% 11.2%

01000200030004000500060007000

6847 6609 6806 6739 6485 6471 6249

0

1000

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2000

3000

4000

3556.8 3485.3

2975.2

1949.4

2718.83011.6

2176.1

0

200

400

600

800

1000

758.1847.3

890.9 862.3

663.5758.4 805.9

0

30

60

90

120

150 EBITDA* (mn €)

EBTDA* (= EBITDA - financial charges)

*Net of IFRS valuation of inventories and LME contracts.

*Net of IFRS valuation of inventories and LME contracts.

2005 2006 2007 2008 2009 2010 2011** At 31 December.

0

5%

10%

15%

20%

93

55

127142

107

7990.6

7564

3145

64

106

85

12.2%

14.9% 15.9%

12.4%

6.8%

10.4% 11.2%

01000200030004000500060007000

6847 6609 6806 6739 6485 6471 6249

0

1000

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2000

3000

4000

3556.8 3485.3

2975.2

1949.4

2718.83011.6

2176.1

0

200

400

600

800

1000

758.1847.3

890.9 862.3

663.5758.4 805.9

0

30

60

90

120

150 EBITDA* (mn €)

EBTDA* (= EBITDA - financial charges)

*Net of IFRS valuation of inventories and LME contracts.

*Net of IFRS valuation of inventories and LME contracts.

2005 2006 2007 2008 2009 2010 2011** At 31 December.

0

5%

10%

15%

20%

93

55

127142

107

7990.6

7564

3145

64

106

85

12.2%

14.9% 15.9%

12.4%

6.8%

10.4% 11.2%

01000200030004000500060007000

6847 6609 6806 6739 6485 6471 6249

0

1000

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2000

3000

4000

3556.8 3485.3

2975.2

1949.4

2718.83011.6

2176.1

0

200

400

600

800

1000

758.1847.3

890.9 862.3

663.5758.4 805.9

0

30

60

90

120

150 EBITDA* (mn €)

EBTDA* (= EBITDA - financial charges)

*Net of IFRS valuation of inventories and LME contracts.

*Net of IFRS valuation of inventories and LME contracts.

2005 2006 2007 2008 2009 2010 2011** At 31 December.

0

5%

10%

15%

20%

93

55

127142

107

7990.6

7564

3145

64

106

85

12.2%

14.9% 15.9%

12.4%

6.8%

10.4% 11.2%

01000200030004000500060007000

6847 6609 6806 6739 6485 6471 6249

turnover (mn €)

0

1000

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2000

3000

4000

3556.8 3485.3

2975.2

1949.4

2718.83011.6

2176.1

0

200

400

600

800

1000

758.1847.3

890.9 862.3

663.5758.4 805.9

0

30

60

90

120

150 EBITDA* (mn €)

EBTDA* (= EBITDA - financial charges)

*Net of IFRS valuation of inventories and LME contracts.

*Net of IFRS valuation of inventories and LME contracts.

2005 2006 2007 2008 2009 2010 2011** At 31 December.

0

5%

10%

15%

20%

93

55

127142

107

7990.6

7564

3145

64

106

85

12.2%

14.9% 15.9%

12.4%

6.8%

10.4% 11.2%

01000200030004000500060007000

6847 6609 6806 6739 6485 6471 6249

9

ann

ual

rep

ort

* excluding EU fines payments

* excluding EU fines payments

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

0

100

200

300

400

500

600

495538

458423 452 431

315

0

100

200

300

400

500

600559 534

360

212

287224

0100200300400500600700800

680750

583

344400

358

210

0

50

100

150

200

177%

108%

67%46%

68%50%

85*

198

46%20%*

* excluding EU fines payments

* excluding EU fines payments

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

0

100

200

300

400

500

600

495538

458423 452 431

315

0

100

200

300

400

500

600559 534

360

212

287224

0100200300400500600700800

680750

583

344400

358

210

0

50

100

150

200

177%

108%

67%46%

68%50%

85*

198

46%20%*

* excluding EU fines payments

* excluding EU fines payments

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

0

100

200

300

400

500

600

495538

458423 452 431

315

0

100

200

300

400

500

600559 534

360

212

287224

0100200300400500600700800

680750

583

344400

358

210

0

50

100

150

200

177%

108%

67%46%

68%50%

85*

198

46%20%*

* excluding EU fines payments

* excluding EU fines payments

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

2005 2006 2007 2008 2009 2010 2011

0

100

200

300

400

500

600

495538

458423 452 431

315

0

100

200

300

400

500

600559 534

360

212

287224

0100200300400500600700800

680750

583

344400

358

210

0

50

100

150

200

177%

108%

67%46%

68%50%

85*

198

46%20%*

total equity (mn €)

debt / equity ratio

net working capital (mn €)

net financial position (mn €)

10

KME Group is a holding company with investments in three principal sectors: copper, renewable energies and services.

oVeRView of tHe GRoup’s coRpoRAte stRuctuRe

KME Group SpA

KME AGKME Recycle SpA

ErgyCapital SpA Cobra AT SpA Titoli e disponibilità

KME Partecipazioni

RENEWABLE ENERGIES

COPPER

100% 100%

100%52%52%

SERVICES OTHER ACTIVITIESNote:

Percentages of voting shares

Listed company

51.5%

3.3%

2.0%

1.8%

41.3%FREE FLOATQUATTRODUEDUE B.V.*

KME GROUP SpA***

BAGGI SISINI FRANCESCO**

DIMENSIONAL FUND ADVISORS LP

* indirectly owned through subsidiaries Quattrotretre SpA (29.66%) and Intek S.p.A. (11.67%)

** as a subject indirectly controlling Arbus Srl, a direct shareholder of KME Group

*** own shares

11

ann

ual

rep

ort

compAnY Bodies

Board of Directors

Chairman Salvatore Orlando

Deputy Chairman Vincenzo Manes B

Deputy Chairwoman Diva Moriani B

General Manager Riccardo Garrè B,E

General Manager Italo Romano B

Vincenzo Cannatelli Mario d’Urso A,C,D

Marcello Gallo Giuseppe Lignana A,C,D

Board Secretary Gian Carlo Losi Alberto Pecci A,D

Alberto Pirelli A,C

A. Independent director, B. Executive director, C. Member of the Remuneration Committee (Alberto Pirelli, Chairman), D. Member of the Internal Control Committee (Mario d’Urso, Chairman), E. The Director Domenico Cova resigned on 22 March 2011; the Board of Directors co-opted Riccardo Garrè on the same date and appointed him General Manager.

Board of Statutory Auditors

Chairman Marco Lombardi

Statutory Auditors Pasquale Pace Vincenzo Pilla

Alternate Auditors Lorenzo Boni Angelo Garcea

Manager in charge of financial reporting

Marco Miniati

Independent auditors

KPMG S.p.A.

General representative of savings shareholders

Romano Bellezza

13

ann

ual

rep

ort

KME Group S.p.A. has been listed on the Stock Exchange since 1897. During the year ended 31 December, 2011, KME Group shares registered the following performance:•Kme Group’s ordinary shares reached a high of Euros 0.381 in February, and a low of Euros 0.246 in September;•Kme Group’s savings shares reached a high of Euros 0.720 in March, and a low of Euros 0.479 in December;

Investor Relations Tel: 055-4411454 / Fax: 055-4411681Email: [email protected]: www.kme.com

Share Capital (Amounts in Euro)

No. of ordinary shares (1) 447,347,650

No. of savings shares 43,699,416

Share capital 297,040,568.04 (1) - Including the ordinary shares issued on exercise of the KME Group warrants option, completed in December 2001.

Capitalisation(in Euros – Capitalisation at end 2011)

Capitalisation of ordinary shares 136,888,381

Capitalisation of savings shares 20,932,020

capitalisation 157,820,401

infoRmAtion foR inVestoRs

Quotes 2011

50

75

100

125

150KME Group ord. KME Group risp. FTSE Italia All Share

January 2011 June 2011 December 2011

14

Kme woRldwide

1 Firenze - Italy Head Office + National Branch Office

2 Fornaci di Barga - ItalyManufacturing plantR&D centre

3 Serravalle Scrivia - Italy4 Milano - Italy5 Osimo - Italy6 Courbevoie - France7 Givet - France8 Niederbruck - France9 Boisthorel - France10 Sérifontaine - France11 Besançon - France12 Osnabrück - Germany

National Branch OfficeManufacturing plantR&D centre

13 Berlino - Germany14 Greven - Germany15 Menden - Germany16 Stolberg - Germany17 Barcellona - Spain

National Branch Office Manufacturing plantSales office

18 Kirkby - UK

19 Worcester - UKNational Branch OfficeSales office

20 Porto - Portugal21 Vienna - Austria22 Tiburg - The Netherlands23 Diegem - Belgium 24 Kladno - Czech Republic25 Praga - Czech Republic26 Odense - Denmark27 Stoccolma - Sweden28 Jönköping - Sweden29 Turku - Finland30 Budapest - Hungary31 Kety - Poland

32 Wroclaw - Poland33 Zurigo - Switzerland34 Ginevra - Switzerland35 Istanbul - Turkey36 Twer - Russian Fed.37 San Pietroburgo - Russian Fed.38 Magnitogorsk - Russian Fed.39 Dalian - China40 Shanghai - Cina41 Santiago - Cile42 Singapore - Singapore43 Chicago - USA44 Santa Catarina - Mexico45 Bangalore - India46 Wollongong - Australia

15

ann

ual

rep

ort

16

ceo’s RepoRt on tHe Business YeAR of 2011

riccardo GarrèChief Executive Officer

2011 was a difficult year for all the economies of the West, and in particular for those in Europe. Although market trends seemed at first to follow the pattern of the second semester of the previous year, they quickly entered uncertain and soon after that negative territory; in the second half the downward curve strengthened and eventually slumped into a full-fledged recession.Thus KME A.G. found itself looking at a gloomy scenario, where the demand of copper and copper alloy semis contracted right from the beginning of the second quarter, and contracted even more throughout the second semester. The biggest difficulties were seen to hit the industries that supply the building sector, which suffered both from the economic trends in this area and from the high prices for raw materials. However, other industrial activities were also affected.We confronted the situation with decisive action on the organizational front, and also in terms of price policy and cost optimization at all levels. The result was 10.8% growth in the gross turnover (+ 6.3% of the raw ingredi-ent’s net value) in spite of the drop in volume, and an operational result that rose 14.6%, all of which enabled us to minimize the negative repercussions of the world crisis.What was our strategic vision? KME A.G. has remained strongly anchored to its value system and to its well-known competence in the copper sector, and has opted to increasingly position itself in the more advanced sectors of the global economy, bringing together innovation, technological excellence and sustainability, and thus boosting the overall value of its product range. In the building sector, KME tried to respond to the unfavourable economic conditions by bringing to the market complete design solutions which are not only of high architectural value but also vehicle a particularly effective message in terms of environmental sustainability and human health. Going in this same direction is the production of rolled “ecological copper”: these products are entirely obtained from recycled scrap metal, and save energy in the production phase as well as optimizing the costs of the raw material.The same holds true for the products with the KME Plus® trademark, which are installed mainly in hospitals and clinics, schools, gymnasiums and public transportation. KME Plus® products with the “Antimicrobial copper” trademark and the “cu+” logo, are made of finished and semifinished copper and copper alloy products with a proven antimicrobial value, manufactured by companies following strict regulations and conforming to techni-cal specifications based on a registration procedure.

17

ann

ual

rep

ort

KME has also boosted its strategic position in the high-tech sector of the building industry. We have consolidat-ed our joint venture with the Zahner Group and completed building projects which include roofing and façade cladding and are highly innovative both technologically and architecturally. Also, KME unveiled a wide range of interior design solutions last year at Milan’s “Fuori Salone” fair, and is again this year showcasing the same solutions in a brand-new showroom it has recently inaugurated in Milan, one of the world’s capitals of design. KME also continued its drive towards innovative sectors in the field of renewable energies, with products which harmonize sustainability and added value and go into the making of solar heat and solar cell systems, and are used for wind energy and electric mobility.To make the best of the market opportunities KME gained through the above initiatives, we have also continued consolidating our structural and organizational base. While actively implementing our OpEx programs to boost excellence in all phases of the corporate operations, we have at the same time persevered in our efforts to set up KME Recycle, a multinational network for treating and marketing scrap metal, for we have no doubt that this sector of the metals industry will become more and more important in the future.Finally, we identified a clear strategic path of global development which aims at increasingly asserting KME as a major player in the new expanding economies, either singly or in partnership with others. Pride of place goes to China, where KME is present in the engineering products sector with Dahlian Dashan, already a leader in its field.The economic forecast for 2012 shows with brutal clarity that difficult months lie ahead, what with Europe in a de-facto recession, the US ecomony making a weak and uncertain comeback, and the BRIC countries also experiencing something of a slowdown.In this overall context, KME will continue engineering innovative products and technologies, further streamline its corporate structure and work on cost-cutting policies, and formulate an appropriate growth plan to look beyond the present crisis.

ann

ual

rep

ort

20

pRoducts

ROLLED PRODUCTS

Ribbons, plates and discs are used in the electrical, electronic and mechanical industries, coin minting and production of decorative objects and gifts. Specific divisions produce high-performance alloy ribbons for connectors and the car industry, and ribbons for solar collectors.

INDUSTRIAL TUBES

KME has a high quality range of copper tubes designed to meet the requirements for specific industrial applications: air-conditioning and cooling systems, construction of boilers, high-frequency coaxial cables, connectors and fittings, thermal solar systems…

ROLLED PRODUCTS FOR BUILDING

KME’s traditional line of TECU® surfaces for façade cladding, roofing and rainwater drainage systems, is now enriched with the “Kme design” collection of surfaces for exterior/interior decoration.

21

ann

ual

rep

ort

TUBES FOR PLUMBING AND HEATING SYSTEMS

Bare or sheathed tubes are ideal for drinking water and heating systems, conveying gasoil, natural gas and LPG, applications in the medical and food industries, and to create healthy and natural air conditioning systems.

RODS

High quality copper and brass rods, plain and profiled, are utilized to produce taps, valves and fittings, precision mechanical components, car components, electronic and electrical apparatuses, locks, profiles for door and window frames and architectural applications.

SPECIAL PRODUCTS

A series of high-tech products: tubes for naval engineering, tube bundles, mineral insulated tubes, special extruded and drawn products, cupronickel cladding for offshore platforms and detailed solutions for the steel and metallurgical industries.

ann

ual

rep

ort

24

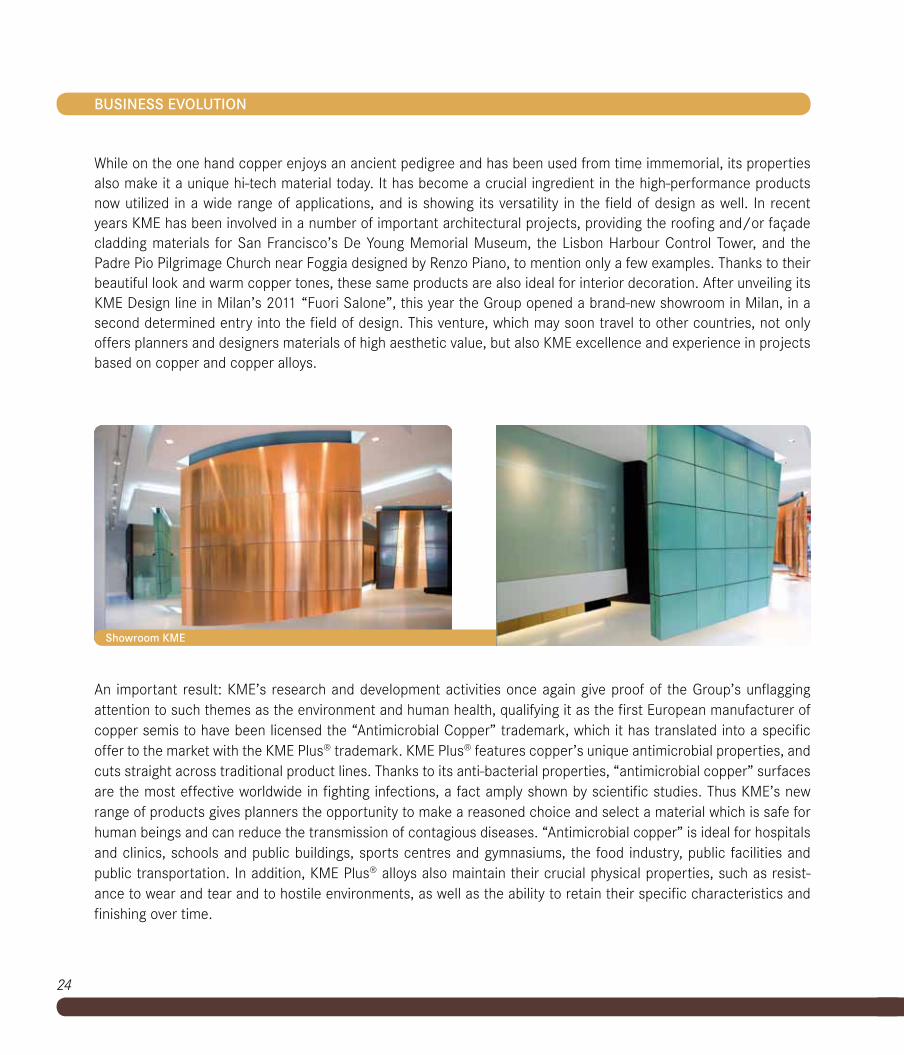

While on the one hand copper enjoys an ancient pedigree and has been used from time immemorial, its properties also make it a unique hi-tech material today. It has become a crucial ingredient in the high-performance products now utilized in a wide range of applications, and is showing its versatility in the field of design as well. In recent years KME has been involved in a number of important architectural projects, providing the roofing and/or façade cladding materials for San Francisco’s De Young Memorial Museum, the Lisbon Harbour Control Tower, and the Padre Pio Pilgrimage Church near Foggia designed by Renzo Piano, to mention only a few examples. Thanks to their beautiful look and warm copper tones, these same products are also ideal for interior decoration. After unveiling its KME Design line in Milan’s 2011 “Fuori Salone”, this year the Group opened a brand-new showroom in Milan, in a second determined entry into the field of design. This venture, which may soon travel to other countries, not only offers planners and designers materials of high aesthetic value, but also KME excellence and experience in projects based on copper and copper alloys.

Business eVolution

An important result: KME’s research and development activities once again give proof of the Group’s unflagging attention to such themes as the environment and human health, qualifying it as the first European manufacturer of copper semis to have been licensed the “Antimicrobial Copper” trademark, which it has translated into a specific offer to the market with the KME Plus® trademark. KME Plus® features copper’s unique antimicrobial properties, and cuts straight across traditional product lines. Thanks to its anti-bacterial properties, “antimicrobial copper” surfaces are the most effective worldwide in fighting infections, a fact amply shown by scientific studies. Thus KME’s new range of products gives planners the opportunity to make a reasoned choice and select a material which is safe for human beings and can reduce the transmission of contagious diseases. “Antimicrobial copper” is ideal for hospitals and clinics, schools and public buildings, sports centres and gymnasiums, the food industry, public facilities and public transportation. In addition, KME Plus® alloys also maintain their crucial physical properties, such as resist-ance to wear and tear and to hostile environments, as well as the ability to retain their specific characteristics and finishing over time.

showroom Kme

25

ann

ual

rep

ort

Fully conscious of the key role which recycled materials play in preserving the environment and its resources, KME has always utilized scrap metal as widely as possible in its production proc-esses. Today the very high level of metal refinement attained by the Group’s manufacturing plants effectively annuls any qualitative difference between primary and recycled copper, thus helping not only to guard resources, but also to reduce energy consumption compared to the overall process of mining the metal, smelting and transporting it to the manufacturing plants. It is a fact that melting scrap metal requires far less energy than it does to extract the raw ore and then produce cathode-grade metal from it. According to the Bureau of International Recycling, recycling copper saves 85% of the energy needed to produce the primary metal. In this way CO2 emissions are also re-duced by about 36%.

Copper is indefinitely and to-tally recyclable, and always per-forms at its very best. Today, KME brings to the market cop-per products for building and architecture manufactured ex-clusively with 100% recycled

production phase

Kme plus® Alloys

scrap

products for architecture and building

26

special products

materials which have exactly the same physical and chemical properties as the primary metal, are used for the same applications and yield the same results. For this reason, KME recycled copper prod-ucts have a crucial competitive edge over others when it comes to building projects based on bio building and bio architecture criteria, now more and more widespread in the public building sector. Only KME today can offer copper products for architec-ture and building made with 100% recycled material.

As well as producing semifinished products, KME leads globally in engineering special high-tech prod-ucts for the steel industry and the naval and off-shore industries, where KME excellence has been consistently proved over time. To defend and boost its position in these sectors, the group has opened sales offices and servicing centres in various con-tinents, including Asia, Australia and the Americas. With increasing efficiency it supports its clients in their respective industrial areas – some of the planet’s largest. In addition, KME’s “Engineered Products” Division has for the past 8 years enjoyed an important vantage point in the Chinese steel and metal industry market, which is constantly expand-ing. Thanks to its solid experience and specialized

know-how, KME is increasing its production, turnover and profits year after year.

KME has launched a diversification process in the field of renewable energies with Kme Solar Italy. This company installs solar cell systems, which in themselves represent a natural evolution of our products, since into their mak-ing go copper tubes and copper alloy connections. Most importantly, KME Solar Italy can benefit from the parent company’s technical and sales know-how in developing this new business sector, offering a unique and complete range of energy-saving solutions including, solar cell, solar heat, geothermal and low-temperature radiant systems. In its determination to follow the path towards sustainable business activities, KME has been devoting much time and attention to health and safety on the job, and to environmental issues as well. In this field, it has reached highly significant results after setting up and implementing a “plan for excellence” in terms of environmental health and workplace safety, which featured in this Report last year. Working together also with the local labour unions, KME Group launched training and prevention programs, involving KME staff in all of our Italian, German, French, Spanish and U.K. offices, so as to promote responsible and efficient management of workplace safety and environmental

opening factory in dalian

27

ann

ual

rep

ort

questions. The certifications which KME plants obtained as a result are tangible proof of the Group’s dedicated commitment in this field, and how it meets the requirements of increasingly demanding and responsible clients. All in all, the Group’s indus-trial plants have to date been awarded six ISO 14001:2004 envi-ronmental certifications, and five OHSAS 18001 certifications, for workers’ health and workplace safety management.The success of KME’s activities in this field is principally dem-onstrated by the 30% reduction of sick leave hours due to ac-cidents on the job last year. This allows us to realistically aim at becoming a “zero accident” industrial concern. Today we mark this first important step on the path which KME has initiated in recent years to promote sustainability, a concept which is also based on our culture of safety, appropriate behaviour, organiza-tional and management models, prevention and examples that inspire.

management convention 5-7 september 2011

ann

ual

rep

ort

30

In 2011, Dynamo camp cel-ebrated its first five years of activity, and achieved excep-tional results. Almost 900 children were welcomed to the Camp during the last sea-son, thanks to the help of 500 volunteers who took part in the project with enthusiasm, professionalism and a strong sense of fellowship.

solidARitY

This achievement makes us at KME very proud, for we have from the very beginning been strongly committed to supporting this recreational therapy village for children suffering from severe or chronic illnesses, which goes by the name of Dynamo Camp and is located in KME’s newly renovated ex-production plant at Limestre, in the mountains near Pistoia.Last year’s traditional end-of-season Open Day celebrations lasted right through the weekend and played host to about 7,000 visitors. The success of this event, by no means a minor one, served to underline what is being achieved at Camp Dynamo. To make it happen once again this year were about one hundred staff from KME, who freely volun-teered to do the set-up and take care of the entire facility while the event was underway. KME’s commitment here is in fact not only financial, but also a managerial one, given that its staff freely contributes part of its time and know-how so that the Camp Dynamo project can benefit from a big company’s experience in business management and organizational methods. And, by the way, the Group’s direct involvement in this initiative has now also gone beyond

dynamo Academy

osnabrück september 2011

31

ann

ual

rep

ort

the Italian borders. Last autumn, KME organized an “Open Doors” day in its German production plant at Osnabrück, inviting the citizenry to an event where they could get to know, appreciate and support the Camp’s activities, which in the past three years has also been hosting German chil-dren. This event took place last year, on 25 September, and at-tracted more than 20,000 people in the space of only 8 hours, even eliciting donations in support of Dynamo Camp Association.

Thanks to KME’s substantial contribution over time, and lately from other business companies as well, Dynamo Camp has become an important landmark in the context of corporate solidarity initiatives both in Italy and abroad.

For its part, Dynamo Sanctuary – the wildlife area which is affiliated to the WWF and surrounds the village on KME land – has also con-tinued to grow with new “ecological tourism” programs and organic livestock breeding and agriculture. These initiatives, in addition to those undertaken by the Dynamo Academy, define the activity of a full-fledged “social enterprise”.

dynamo camp