vietnam beverage industry report 2018 · thuếtrong đócó bia và rượu; ... malt export...

TRANSCRIPT

Content is intentionally removed for demo purposeContent is intentionally removed for demo purpose

VIETNAM BEVERAGE INDUSTRY REPORT 2018

1

Content is intentionally removed for demo purpose

Content

Executive summary 3

1 Business environment 6

1.1 Macroeconomic context 6

1.2 Legal barriers 13

1.3 Free trade agreements 18

2 Industry overview 24

2.1 Global market 24

2.1.1. Beer 25

2.1.2. Wine 36

2.1.3 Soft Drink 45

2.2 Local market 48

2.2.1. Beer 51

2.2.2. Wine 61

2.2.3 Soft Drink 75

2.3 Risk 90

3.2.1 4.1 SWOT analysis 91

2.3.2. Competitiveness analysis 92

2.3.3. Business risk 95

2.4 Planning and development 99

2.5 Prospect and prediction 101

2.5.1. 2.1 Motivational factors 102

2.5.2 Prediction 104

3 Enterprise analysis 112

3.1 Profitability 114

3.2 Operating capability 118

3.3 Financial strength 121

3.4 Return on investment 124

4 Appendix 126

2

Content is intentionally removed for demo purpose

Executive summary

Vietnam beverage industry came into being

years ago but just blossomed for the past

decade.

The local industry is capable of meeting

domestic consumption needs, with less

imports and more exports.

As of soft drinks, the industry has expanded on a

large scale and rapid growth given adequate

domestic supply.

The global beverage market has so far been on a

positive trend but with lots of unexplored

potentials.

2018 witnessed a sharp downturn in the industry

compared to the last year due to production

setbacks.

3

Content is intentionally removed for demo purpose

Executive summary

The wine market is on a small scale with falling

production.

There exists a few large-scale and strong -

branded enterprises in the industry such as

Sabeco, Habeco and Tan Hiep that are capable

of competing with FDI enterprises.

The industry has low debt rate, high liquidity

and high asset performance.

As estimated, the beer, wine and soft drink

segment will revenue 180 billion, 33 billion and

120 billion respectively by 2018.

4

Content is intentionally removed for demo purpose

Abbreviation

MOF Ministry of Finance

CAGR Compounded Annual Growth Rate

FI Foreign Investment

EVFTA EU-Vietnam Bilateral Trade Agreement

FAO Food and Agriculture Organization of the United Nations

FDI Foreign Direct Investment

FTA Free Trade Agreements

VA Value Added

IWSR International Wine & Spirit Research

MFN Most Favoured Nation

OIV International Organisation of Vine and Wine

GDVC General Department of Vietnam Customs

GSO General Statistics Office of Vietnam

SC Special Consumption

TPP Trans-Pacific Agreement TPP

UNFPA United Nations Population Fund

UNWTO World Tourism Organization

USDA U.S. Department of Agriculture

VAT Value Added Tax

VBA Association Beer - Alcohol - Beverage Vietnam

VIRAC VIRAC Joint Stock Company

WTO World Trade Organization

5

Content is intentionally removed for demo purpose

Content

1 Business environment

1.1 Macroeconomic context

1.2 Legal barriers

1.3 Free trade agreements

Content is intentionally removed for demo purpose

6

Source: VIRAC, GSO

1. Business environment

1.1 Macroeconomic context

Source: VIRAC, GSO

Monthly CPI fluctuations, 2014-2018

GDP growth, 2011 - 2018

Content is intentionally removed for demo purpose

7

Source: VIRAC, GSO

Source: VIRAC, GSO

1. Business environment

1.1 Macroeconomic context

CPI by item group, 2018

• The beverage and tobacco industry are among segments having

positive CPI growth in 2018.

• Vietnamese consumer confidence index fell by 1 point percent to 116

points in the third quarter of the year 2018.

Vietnam’s Consumer Confidence Index, Q1/2014 - Q1/2018

Content is intentionally removed for demo purpose

8

Content is intentionally removed for demo purpose

1. Business environment

1.1 Macroeconomic context

9

Source: Synthesized by VIRAC, BCG

• In 2018, the USD/VND exchange rate fluctuated around 22.400.

• 2018’s FDI rose sharply to 35.88 billion dollars, up 47.05% compared to

the same period in 2017.

Thousand

VND

VND/USD exchange rate, 2013-2018 Source: VIRAC, PVN

FDI capital, 2015-2018Billion

USD

Content is intentionally removed for demo purpose

1. Business environment

1.1 Macroeconomic context

10

Source: VIRAC, GDVC

Beverage industry’s shares in GDP, the period 2010-2015

Source: VIRAC, GSO

Billion USD

Commodity import – export, 2006 - 2018

Billion USDThe total im-export value reached 425.12 billion, up 21% corresponding

to 73.74 billion compared to 2017.

Content is intentionally removed for demo purpose

1. Business environment

1.1 Macroeconomic context

11

Beverage consumption is one of the important driving

factors behind consumer goods.

The young population creates a potential market for the

beverage industry.

Source: VIRAC, GSO

Million

people

Total population and working - age population structure, 2010-2018

Beverage and tobacco sectors’ CPI compared to the previous month

T4/2017-2018

Source: VIRAC, GSO

Content is intentionally removed for demo purpose

1. Business environment

1.1 Macroeconomic context

12

Source: VIRAC, Economist Intelligence Unit

Total disposable income, 2010-2020The increasing disposable income has stimulated expenditures on beverage

stuff.

Source: VIRAC, GSO

Billion USD

Vietnam’s retail sales 2011-2018

Content is intentionally removed for demo purpose

Content

I Business environment

1.1 Macroeconomic context

1.2 Legal barriers

1.3 Free trade agreements

13

Content is intentionally removed for demo purpose

14

1. Business environment

1.2. Legal framework

• Quy chuẩn kỹ thuật quốc gia đối với các sản phẩm Đồ uống có cồn (QCVN 6-3:2010/BYT) quy định các chỉ tiêu an toàn thực phẩm và các yêu cầu quản

lý đối với cồn thực phẩm được sử dụng để sản xuất các sản phẩm đồ uống có cồn như Cồn thực phẩm, Bia hơi, Bia hộp, Bia chai, Rượu Vang, Rượu Mạnh,…;

• Quy chuẩn kỹ thuật quốc gia đối với các sản phẩm Đồ uống không cồn (QCVN 6-2:2010/BYT) quy định các chỉ tiêu an toàn thực phẩm và các yêu cầu

quản lý đối với Đồ uống không cồn, bao gồm nước rau quả, nectar rau quả và Đồ uống pha chế sẵn không cồn;

• Quy chuẩn kỹ thuật quốc gia đối với nước khoáng thiên nhiên và nước uống đóng chai (QCVN 6-1: 2010/BYT). Quy chuẩn này quy định các chỉ tiêu

an toàn thực phẩm và các yêu cầu quản lý đối với nước khoáng thiên nhiên đóng chai và nước uống đóng chai được sử dụng với mục đích giải khát. Quy

chuẩn này không áp dụng đối với thực phẩm chức năng. Luật An toàn thực phẩm số 55/2010/QH12, ngày 17/6/2010;

• Luật Chất lượng sản phẩm hàng hóa số 05/2007/QH12 ngày 21/11/2007;

• Nghị định số 38/2012/NĐ-CP của Chính phủ ngày 25/4/2012 quy định chi tiết thi hành một số điều của Luật An toàn thực phẩm;

• Thông tư số 29/2012/TT-BCT của Bộ Công thương quy định cấp, thu hồi Giấy chứng nhận cơ sở đủ điều kiện an toàn thực phẩm thuộc trách nhiệm quản

lý của Bộ Công thương.

• Luật số 55/2014/QH13 – Luật Bảo vệ môi trường quy định về hoạt động bảo vệ môi trường; chính sách, biện pháp và nguồn lực để bảo vệ môi trường;

quyền, nghĩa vụ và trách nhiệm của cơ quan, tổ chức, hộ gia đình và cá nhân trong bảo vệ môi trường;

• Thông tư số 128/2013/TT-BTC ngày 10/9/2013 của Bộ Tài chính quy định về thủ tục hải quan; kiểm tra, giám sát hải quan; thuế xuất khẩu, thuế nhập

khẩu và quản lý thuế đối với hàng hóa xuất khẩu, nhập khẩu;

• Thông tư 164/2013/TT-BTC ngày 15/11/2013 của Bộ Tài chính ban hành Biểu thuế xuất khẩu, biểu thuế nhập khẩu ưu đãi theo danh mục mặt hàng chịu

thuế trong đó có Bia và Rượu;

• Nghị định số 08/2015/NĐ-CP ngày 21/1/2015 của Chính phủ quy định chi tiết và biện pháp thi hành Luật Hải quan về thủ tục hải quan, kiểm tra, giám

sát, kiểm soát hải quan Biểu thuế nhập khẩu Bia, Rượu, Nước Giải Khát;

• Luật số: 27/2008/QH12 – Luật thuế tiêu thụ đặc biệt quy định về đối tượng chịu thuế, đối tượng không chịu thuế, người nộp thuế, căn cứ tính thuế, hoàn

thuế, khấu trừ thuế và giảm thuế tiêu thụ đặc biệt;

• Quyết định số 2219/QĐ-BCT phê duyệt kinh doanh mạng lưới kinh doanh phân phối, bán buôn sản phẩm Rượu trên phạm vi toàn quốc đến năm 2025,

tầm nhìn 2035;

Laws, decrees and regulations of the industry

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Legal framework’s impact on the industry

For state agencies

For businesses in the industry

Beverage export output 2010-2015

Source: VIRAC, GSO

15

1. Business environment

1.2. Legal framework

Thousand tons

Content is intentionally removed for demo purpose

Beer manufacturing enterprises 2010-2017 Profit margin before tax, 2010-2017 Beverage manufacturing growth 2011-2018

Source: VIRAC, GSOSource: VIRAC, GSOSource: VIRAC, GSO

Unit: %

16

1. Business environment

1.2. Legal framework

Content is intentionally removed for demo purpose

17

1. Business environment

1.2. Legal framework

Circulars and decrees of the special consumption tax on alcoholic beverages

SCT on alcoholic beverages are subject to the incremental roadmap as indicated

in Law No. 70/QH13/2014 and will increase gradually to 65% in 3 years’ time,

starting from January 1st, 2017.Commodity Date

Tax rate

(%)

SCT roadmap applicable to liquor and beer since 2017

Source: Synthesized by VIRAC

Content is intentionally removed for demo purpose

18

1. Business environment

1.2. Legal framework

New regulations on liquor imports.

Content is intentionally removed for demo purpose

Content

1 Business environment

1.1 Macroeconomic context

1.2 Legal barriers

1.3 Free trade agreements

19

Content is intentionally removed for demo purpose

• Tariffs:

3.1 WTO — Vietnam joined as the 150th member on November 7th, 2006

• Distribution markets:

• Investment environment:

WTO’s impact on Vietnam’s beverage industry:

Item

Most

Favoured

Nation(%)

Commitments with WTO

Tariff before

membership (%)

Final tariff

(%)

Implementa

tion span

Source: VIRAC, WTO

20

1. Business environment

1.3 Free trade agreements

Content is intentionally removed for demo purpose

• Tariffs:

3.2 EU-Vietnam Bilateral Trade Agreement (EVFTA) was signed on December 2nd, 2015 in Brussels, Belgium.

Entry commitments:Product Commitment

Source: European Commission - Vietnam’s Ministry of

Industry and Trade

21

1. Business environment

1.3 Free trade agreements

• Investment

EVFTA’s impact on Vietnam’s beverage industry:

Content is intentionally removed for demo purpose

3.3 CPTPP - Comprehensive Partnership and Transition Partnership Agreement

Commitments

• Tariff (commercial goods):

• Other commitments

22

1. Business environment

1.3 Free trade agreements

Content is intentionally removed for demo purpose

CPTPP’s impact on Vietnam’s beverage industry:

No. Item Tax - cutting

roadmap

1

2

3

4

5

Vietnam's commitments with CPTPP on import tariffs:

Source: VIRAC, Ministry of Finance

22

1. Business environment

1.3 Free trade agreements

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

3.4 Other trade agreements:

FTA’s impact on Vietnam’s beverage industry:

24

1. Business environment

1.3 Free trade agreements

Content is intentionally removed for demo purpose

Content

2. Industry overview

2.1 Global market

2.2 Local market

2.3 Risk

2.4 Planning and development

2.5 Prospect and prediction

25

Content is intentionally removed for demo purpose

2. Industry overview

2.1 Global market – 2.1.1. Beer

2.1.1 Beer

Input material: Malt, Hops

Regarding malt

26

The UK’s barley price developments 1/2012-2018

Source: VIRAC, Indexmundi

Unit: GBP/tonne

Global barley production and consumption, 10/11-17/18e

Million

tons

Source: VIRAC, USDA

Content is intentionally removed for demo purpose

2. Industry overview

2.1 Global market – 2.1.1. Beer

27

Market shares of 5 largest barley producers 2017/2018

Source: VIRAC, USDA

Barley consumption for malt processing, 10/11-16/17

Million tons

Source: VIRAC, International Grains Council

Content is intentionally removed for demo purpose

2. Industry overview

2.1 Global market – 2.1.1. Beer

28

The UK’s malt price movements, 7/7/2011-2015

Source: VIRAC, Bloomberg

Unit: GBP/tonne

Malt export production in the world and Europe, 2010-

2015

Million tons

Million tons

There is a worldwide decline in malt exports, except for the European region, which

is forecast to be on the upward trend given favorable weather conditions in some

countries in the region: The UK and Spain.

Source: VIRAC, Euromalt, United Nations Trade Statistics

Malt production situations in the world and Europe, 2010-2014

Content is intentionally removed for demo purpose

2. Industry overview

2.1 Global market – 2.1.1. Beer

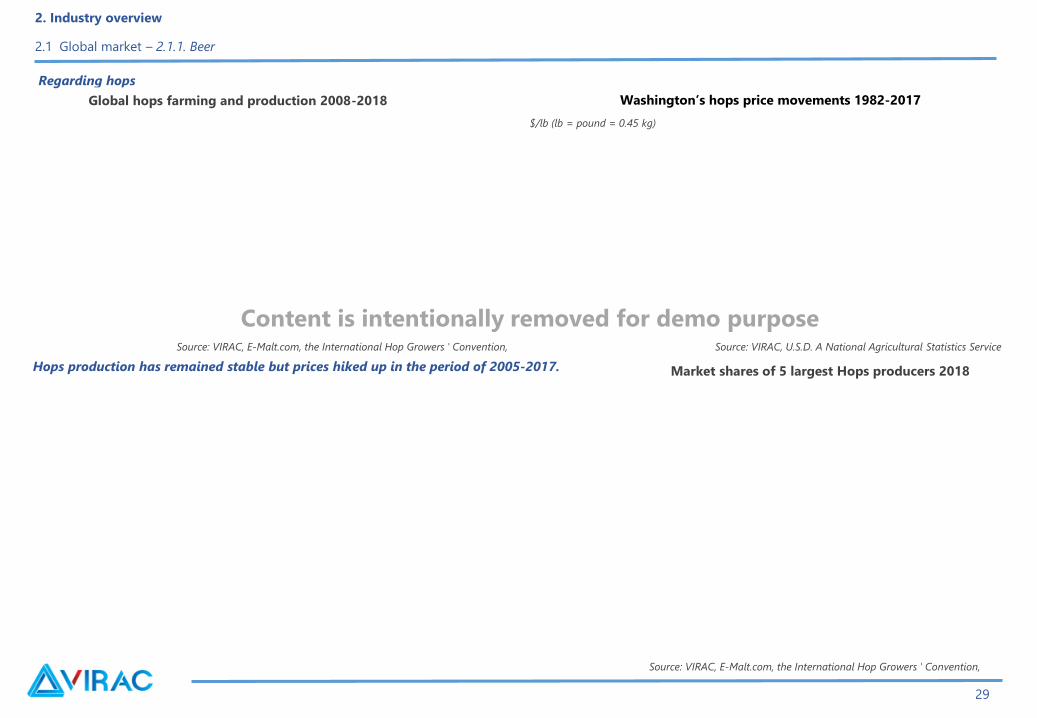

Regarding hops

29

Global hops farming and production 2008-2018

Source: VIRAC, E-Malt.com, the International Hop Growers ' Convention,

Washington’s hops price movements 1982-2017

Source: VIRAC, U.S.D. A National Agricultural Statistics Service

$/lb (lb = pound = 0.45 kg)

Hops production has remained stable but prices hiked up in the period of 2005-2017. Market shares of 5 largest Hops producers 2018

Source: VIRAC, E-Malt.com, the International Hop Growers ' Convention,

Content is intentionally removed for demo purpose

2. Industry overview

2.1 Global market – 2.1.1. Beer

30

Source: VIRAC, Euromalt, United Nations Trade Statistics

Million

tons

Million

USD

Hops export situation, 2011-2017

Market shares of 5 world's largest Hops exporters 2017

Content is intentionally removed for demo purpose

2. Industry overview

2.1 Global market – 2.1.1. Beer

Global beer supply and demand

Global production is of large scale with two major hubs, including Asia and Europe. Irregularities due to prolonged droughts blew a huge hit to malt

production — the main input material. Against this setback, the industry still met the world’s consumption needs.

Global beer consumption and production 2010-2018Beer output and growth rate of 7 regions 2018

Source: Synthesized by VIRAC

31

Billion liter

Source: Synthesized by VIRAC

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

32

Top 10 countries having the highest beer im-export value 2017 Countries with highest beer im-export growth rates 2010-2015

Source: VIRAC, worldsrichestcountries.comSource: VIRAC, Euromalt, United Nations Trade Statistics

2. Industry overview

2.1 Global market – 2.1.1. Beer

Global beer output and exports, 2010-2017

Million

tons

Billion

USD

Content is intentionally removed for demo purpose

The beer market has distinctly divided into two groups: Multinational companies with capital, branding and distribution channel advantages and

indigenous manufacturers with a depth understanding of the local demand.

33

Production market shares of 5 world’s leading enterprises, 2017

Source: VIRAC, VBA

Consumption market shares of 5 world’s leading enterprises,

2017

Source: VIRAC, VBA

2. Industry overview

2.1 Global market – 2.1.1. Beer

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

34

RankLogo Brand Entity Nation

Brand value (million USD) Brand ranking

2018 2017 2018 2017 2018 2017

Source: brandirectory.com

10 highest-value beer brands, 2017-2018

1. Bud Light

2. Industry overview

2.1 Global market – 2.1.1. Beer

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

35

2. Budweiser

3. Heineken

4. Brahma

5. Skol

6. Asahi

2. Industry overview

2.1 Global market – 2.1.1. Beer

Content is intentionally removed for demo purpose

36

7. Corona Extra

8. Guinness

9. Cyrillic

10. Miller Lite

2. Industry overview

2.1 Global market – 2.1.1. Beer

Content is intentionally removed for demo purpose

Wine

37

2. Industry overview

2.1 Global market – 2.1.2. Wine

Top five European countries with the largest wine vineyard area

Source: VIRAC, THE OIV

Top five non- European countries with the largest wine vineyard area

Source: VIRAC, THE OIV

Wine-producing vineyard area, 2005-2017

Source: VIRAC, THE OIV

Content is intentionally removed for demo purpose

38

2. Industry overview

2.1 Global market – 2.1.2. Wine

Unit: million Output

Source: VIRAC, THE

OIV

Grape production in General, 2010-2017eMillion

tons

Source: VIRAC, THE OIV

Total vine production by country in 2017

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

39

2. Industry overview

2.1 Global market – 2.1.2. Wine

Wine production presents lots of discernable fluctuations while the

demand for consumption remained relatively stable during 2005-

2017.

Top five largest wine producers in the world, 2014-2017

Source: VIRAC, THE OIV

Global wine production and consumption, 2005-2017e100 million

litres

Market shares of five largest wine producers, 2017-2017

Source: VIRAC, THE OIV

Source: VIRAC, THE OIV

Content is intentionally removed for demo purpose

40

2. Industry overview

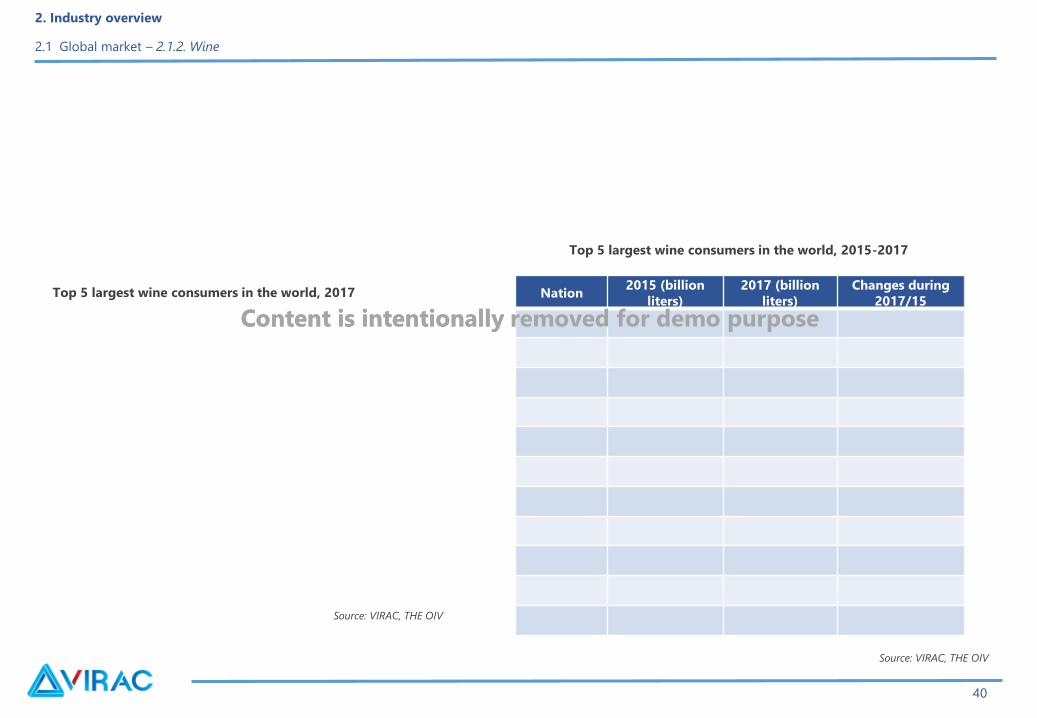

2.1 Global market – 2.1.2. Wine

Nation2015 (billion

liters)

2017 (billion

liters)

Changes during

2017/15

Top 5 largest wine consumers in the world, 2015-2017

Source: VIRAC, THE OIV

Source: VIRAC, THE OIV

Top 5 largest wine consumers in the world, 2017

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Wine exports tend to climb up in value and output with major importers within the EU.

41

2. Industry overview

2.1 Global market – 2.1.2. Wine

Source: VIRAC OIV, GTA

Source: VIRAC, THE OIV

Nation

Wine export output,

2012-2017

(billion liters)

Export value

(billion EUR)

2015 2017 2015 2017

Wine export value and output 2000-2017e Largest wine exporters

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purposeContent is intentionally removed for demo purpose

42

2. Industry overview

2.1 Global market – 2.1.2. Wine

Largest wine importers

Nation

Import output, 2012-

2017

(billion liters)

Import value

(billion EUR)

2015 2017 2015 2017

Source: VIRAC OIV, GTA

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

43

2. Industry overview

2.1 Global market – 2.1.2. Wine

Rượu Mạnh

Rượu Rạnh là chất cồn được chưng cất và có thể được làm từ bất kì chất hữu cơ nào có thể lên men để tạo ra cồn. Hầu hết các Đồ uống có cồn được làm ra từ

quá trình lên men trái cây hay ngũ cốc. Chất cồn được chiết ra từ chất lỏng được lên men bằng cách đun sôi và cô đọng phần chất cồn bốc hơi. Sau đó người ta

đưa chất lỏng vào thùng gỗ sồi để ủ (đối với Whisky hoặc Cognac) hay đóng chai luôn (đối với Vodka, Gin,…). Do đó khi đề cập đến Rượu Mạnh nói chung không

có một nguyên liệu đầu vào đặc trưng như đối với Rượu Vang (sản xuất bởi Nho).

product

• Brandy: Chỉ chung các loại Rượu Mạnh chưng cất từ Rượu Vang (Nho) hay từ trái cây đã lên men. Thường thì Brandy phải qua hai lần chưng cất để đạt tỷ lệ

cồn 70–80% rồi mới ủ cho rượu dịu bớt trong các thùng gỗ sồi nhờ quá trình oxy hóa, sau đó pha thêm nước cất để đạt được độ cồn khoảng 40%. Cũng có khi

Brandy được pha thêm caramen (đường ngào) để có màu đẹp. Brandy có hai dòng chính là Cognac và Armagnac. Các nhãn hiệu nổi tiếng của dòng Rượu

Brandy: Hennessy, Remy Martin, Martel, Otard, Courvoisier, Camus, Hines.

• Whiskey: Whisky là sản phẩm chưng cất từ những hạt lúa đại mạch, lúa mạch đen bắp và các loại ngũ cốc có hạt nhỏ khác. Trước năm 1820, tất cả các loại

whisky đều được làm ra từ mạch nha của lúa đại mạch (nên còn có tên là Whisky đại mạch). Việc chưng cất loại whisky từ lúa đại mạch pha trộn với bắp xuất

hiện vào năm 1830, sau khi bằng sáng chế được cung cấp. Từ đó người ta mới phát hiện ra rằng Whisky pha trộn có mùi êm dịu hơn. Nhưng whisky tuyệt đối

không sử dụng nguyên liệu khoai tây, trái cây hay bất cứ loại thực phẩm nào khác, ngoài những thứ đã kể trên. Có 4 nhà sản xuất trên thế giới nổi tiếng nhất

hiện nay):

- Scotch Whisky, Malt whisky: đi từ hạt lúa mạch được sơ chế thành hạt mạch nha; Blend whisky: được pha từ nhiều loại ngũ cốc (đa dạng sản phẩm); Những sản

phẩm trên chủ yếu được chưng cất bằng nồi 2 lần.

- Canadian Whisky: Thời gian ủ ít nhất là 3 năm và được chưng cất bằng cột với các thành phần chính: Rye (Lúa mạch đen), Lúa mạch (barley), Lúa mì (wheat),

Ngô.

- American Whisky: Sản phẩm cũng khá đa dạng trong cách kết hợp các nguyên liệu chính từ ngũ cốc với những nồng độ khác nhau và đặc biệt chưng cất bằng

cột. Ví dụ: American Bourbon whisky với 51% ngô + 49% ngũ cốc khác; Rye whisky với 51% rye + 49% ngũ cốc khác.

- Irish Whisky: Thời gian ủ ít nhất 5 năm, và cũng từ những nguyên liệu chủ yếu từ ngũ cốc và lúa mạch nhưng đặc biệt là không có mùi khói, chưng cất 3 lần

bằng nồi.

• Vodka là loại Rượu Mạnh không màu làm từ bất cứ chất liệu nào. Lúc mới chưng cất Vodka đạt đến 95 độ cồn, sau giảm dần còn 40–50 độ. Vodka không nhất

thiết phải qua khâu ủ, nhưng cần xử lý nhằm loại bỏ hương vị và màu sắc để trở thành trong suốt, không mùi (chủ yếu sử dụng than hoạt tính để khử chất

độc). Đây là loại rượu dễ bay hơi có thể pha chế với nhiều loại trái cây và các hỗn hợp Đồ uống khác. Có hai loại Vodka: Clear Vodka (sản xuất theo kiểu thông

thường không màu); Flavour Vodka (sử dụng hương vị, nguyên liệu làm thơm Vodka).

• Gin là loại Rượu được chưng cất từ các loại hạt (bắp, lúa mạch, lúa mì, lúa mạch đen) trộn với hương liệu thảo mộc như hạnh nhân, quế, hạt côca, gừng, vỏ

chanh, cam,… Về mặt kỹ thuật, Gin có thể được coi là các loại Rượu mùi nếu được cho thêm đường. Độ cồn trong Rượu Gin thường là 34–47%.

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

44

2. Industry overview

2.1 Global market – 2.1.2. Wine

The consumption demand for malt wine is on the rise alongside a slight increase in export values.

Largest malt wine importers 2017

Source: VIRAC, UN COMTRADE statistics

Malt wine consumption 2009-2017

Billion USD

Content is intentionally removed for demo purpose

45

2. Industry overview

2.1 Global market – 2.1.2. Wine

RankChan

geType of wine

Total

point

Total brand

point

Brand

quantity of

top 10

Most prevalent liquor types in the world 2017

Source: VIRAC, drinkspowerbrands.com

Rank Type of wineTotal brand

pointChange

World-class alcohol brands 2017

Source: VIRAC, drinkspowerbrands.com

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

46

2. Industry overview

2.1 Global market – 2.1.2. Wine

Rank Change Type of wine Total point ChangeTotal brand

pointChange

Brand quantity

of top 10Change

World’s largest wine traders and producers 2015

Source: VIRAC, drinkspowerbrands.com

Rank Change Type of wine Total point ChangeTotal brand

pointChange

Brand quantity

of top 10Change

-

World - famous wine exporters 2015

Source: VIRAC, drinkspowerbrands.com

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

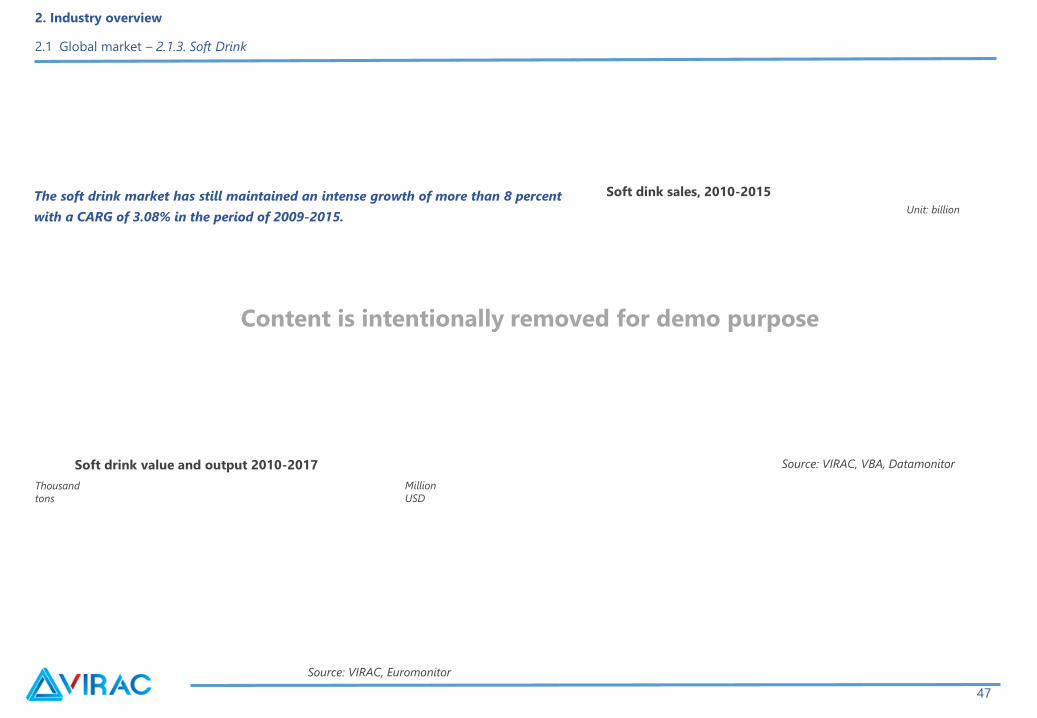

The soft drink market has still maintained an intense growth of more than 8 percent

with a CARG of 3.08% in the period of 2009-2015.

47

2. Industry overview

2.1 Global market – 2.1.3. Soft Drink

Soft dink sales, 2010-2015

Source: VIRAC, VBA, Datamonitor

Unit: billion

Soft drink value and output 2010-2017

Thousand

tons

Million

USD

Source: VIRAC, Euromonitor

Content is intentionally removed for demo purpose

Fizzy drinks are still the most preferred but the demand for

consumption is shifting to bottled water and fruit juice.

48

2. Industry overview

2.1 Global market – 2.1.3. Soft Drink

Sales of soft drink lines 2015

Source: VIRAC, VBA

RankLogo Brand Entity

Brand value (million USD)Change

Brand

ranking2017 2018 2017 2018

10 highest-value soft drink brands, 2017-2018

Source: brandfinance

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

49

2. Industry overview

2.1 Global market – 2.1.3. Soft Drink

Coca-Cola and Pepsico has taken the lead in the industry, contributing 8 out of 10 largest - value brands. Coca-Cola is dubbed as the most expensive

global brand, reaching 31.89 billion, up 6% compared to 2017.

Fizzy soft drink supplemental and sports drink Fruit juice Bottled water

Source: VIRAC, Bloomberg Intelligent, VBA

Content is intentionally removed for demo purpose

Content

2. Industry overview

2.1 Global market

2.2 Local market

2.3 Risk

2.4 Planning and development

2.5 Prospect and prediction

50

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

The drinks industry has a large scale and high growth potential. Production is gradually meeting the demand, with increasing exports and falling

imports.

51

2. Industry overview

2.2 Local market

Local soft drink im-export import, 2010-2017e

Thousand

tons

Source: VIRAC, UN COMTRADE

statistics

Local soft drink production and consumption, 2010-2018

Billion

liter

Source: VIRAC, GDVC

Billion

VND

Content is intentionally removed for demo purpose

Segment structure and shifting during 2010-2018 recorded no significant change. Beer and soft drinks were still dominant while the wine segment only

made up the small share.

52

2. Industry overview

2.2 Local market

Production structure by segment 2010-2018

Source: VIRAC, GDVC

Content is intentionally removed for demo purpose

Source: Synthesized by VIRAC

The beer value chain

Agriculture Malt

Brewing

Agency Consumer

Packaging

53

2. Industry overview

2.2 Local market – 2.2.1. Beer

2.2.1. Beer

Content is intentionally removed for demo purpose

Vietnam’s major malt export areas, 2017e

Malt and hops import 2010-2017

Source: VIRAC, Euromalt, United Nations Trade Statistics

The beer industry depend its input material on imports, mainly for malt.

Source: VIRAC, Euromalt, United Nations Trade

Statistics

54

2. Industry overview

2.2 Local market – 2.2.1. Beer

Input material

Thousand kg

Malt import situations, 2010-2017

Source: VIRAC, Euromalt, United Nations Trade Statistics

Million

tons

Europe

Content is intentionally removed for demo purpose

55

2. Industry overview

2.2 Local market – 2.2.1. Beer

Vietnam’s hops supply structure 2017

Source: VIRAC, Euromalt, United Nations Trade

Statistics

Thousand kg

Source: VIRAC, Euromalt, United Nations Trade

Statistics

Hops import to Vietnam, 2010-2017e

Content is intentionally removed for demo purpose

56

2. Industry overview

2.2 Local market – 2.2.1. Beer

Production-consumption

The domestic beer industry is in surplus due to production beyond

consumption demand. However, there is much space for growth, particularly

the high-end beer segment.

Local beer production and consumption, 2010 – 2018

Source: VIRAC, GSO

Billion

liter

Thousand

billion VND

Source: VIRAC, GSO

Content is intentionally removed for demo purpose

57

2. Industry overview

2.2 Local market – 2.2.1. Beer

Inventories

Million USD

Beer inventories, 2011-2018

Source: VIRAC, GSO

Beer inventory structure, 2011-2018

Source: VIRAC, GSO

Content is intentionally removed for demo purpose

The beer market has a discernable concentration with more than 90% of the value belong to such giant corporations as: Sabeco, Habeco, Heineken,

Carlsberg, Tiger.

58

2. Industry overview

2.2 Local market – 2.2.1. Beer

Internal competition

Domestic consumption market shares, 2017

Source: VIRAC Source: VIRAC

Top 10 Vietnam’s beer brands, 2017

Content is intentionally removed for demo purpose

59

2. Industry overview

2.2 Local market – 2.2.1. Beer

In 2017, Sabeco vẫn duy trì vị trí dẫn đầu dù thị phần giảm nhẹ từ 41.6% năm 2015 xuống 40.9%.

Sabeco là hãng bia nổi tiếng nhất và là doanh nghiệp đang được tất cả các hãng bia khác quan tâm, trong năm qua, thương vụ thoái vốn nhà nước tại Sabeco trị

giá gần 5 tỉ USD. Công ty TNHH Vietnam Beverage – nhà đầu tư Thái lan, đã trả mức giá 320,000 đồng/cổ phiếu – chưa từng có trong lịch sử để chiếm 53.59% cổ

phần tại Sabeco. Hiện tại, Sabeco đang sở hữu 24 nhà máy bia đang hoạt động. Năm 2018, Sabeco tiêu thụ 1.727 tỷ lít bia và kỳ vọng lên mức 1.85 tỷ lít trong

năm 2018. Sabeco trở thành "gã khổng lồ" trên thị trường nhờ việc thành lập và hợp nhất nhiều nhà máy bia, đặc biệt là ở phía Nam. Mạng lưới nhà máy rộng lớn

là lợi thế cạnh tranh giúp Sabeco phân phối hiệu quả hơn các đối thủ. Sabeco có 2 thương hiệu bia mang tính biểu tượng và có truyền thống tại Việt Nam là "Bia

Sài Gòn" và "333". Ngoài ra, Sabeco đang đẩy mạnh các thương hiệu Saigon Special (hay còn được gọi là Sài Gòn lùn do mẫu thiết kế chai thấp).

Không những thế, Sabeco đang giành giật thị phần của Habeco ở miền bắc. Tính riêng tại khu vực miền bắc, thị phần Sabeco tăng từ 10% năm 20014 lên 15.5%

trong năm 2017. Trong top 10 thương hiệu Bia có đến 3 nhãn hiệu thuộc sở hữu của Sabeco và đều chiếm thị phần cao: Saigon Export (16.5%), 333’

Export (13.2%) và Saigon lager (10.4%). 2 thương hiệu mang tính biểu tượng và có truyền thống tại Việt Nam là Bia Sài Gòn và 333.

Kể từ năm 2015, VBL đã vượt Habeco, vươn lên vị trí thứ 2 về thị phần tiêu thụ và đạt 23% trong năm 2017.

VBL với sản phẩm chính là Heineken hiện đang thống lĩnh phân khúc cao cấp, ngoài ra còn có các thương hiệu Tiger, Larue, Desperados, Affligem và Strongbow…

Trong phân khúc này, riêng VBL đã chiếm khoảng 67% thị phần, trong đó 40% thuộc về thương hiệu Tiger và 27% thuộc về thương hiệu Heineken. Saigon Special

của Sabeco có thị phần 28% ở phân khúc này. VBL hiện sở hữu 5 nhà máy tại Việt Nam, trong đó 3 nhà máy tại miền Nam và 2 nhà máy tại miền Trung, đây là 2

thị trường trọng điểm của công ty.

VBL đầu tư mạnh cho tiếp thị, quảng cáo với sự tham gia của nhiều người nổi tiếng, có những vị trí đắc địa hưởng lợi từ việc tâm lý tiêu dùng của người dân trong

nước chuyển hướng ưa chuộng các dòng sản phẩm thương hiệu nước ngoài. Trong khi đó, Sabeco và Habeco có dấu hiệu giảm thị phần do gặp khó khăn trong

việc phát triển địa điểm bán hàng. Với bối cảnh cạnh tranh ngày càng gay gắt, mọi địa điểm bán hàng tại các thành phố lớn như Hà Nội, Hồ Chí Minh cũng như

tỉnh lẻ như Hải Dương, Thái Nguyên đều bị giành giật quyết liệt. Do vậy, hai doanh nghiệp này gần như độc quyền chỉ ở phân khúc bình dân – sản phẩm tạo ra

giá trị thấp, các sản phẩm cao cấp gần như không cạnh tranh được với VBL.

Habeco chiếm 16.2% thị trường

Habeco nắm hơn 50% thị phần ở miền Bắc và chiếm 16.2% thị trường, xếp thứ 3 trong năm 2017 . Tương tự như Bia Sài Gòn của Sabeco, thì Bia Hà Nội của

Habeco cũng có tính biểu tượng ở miền bắc.Ngoài bia chai và bia lon, Habeco cũng sản xuất dòng bia hơi riêng, nổi bật nhất là "Bia hơi Hà Nội". Bia hơi chiếm

15-16% tổng sản lượng của Habeco. Dòng bia bình dân và sản phẩm Bia Hà Nội chiếm phần lớn sản lượng của Habeco, trong khi thương hiệu cao cấp là Trúc

Bạch không đạt được nhiều thành công. Habeco có 15 nhà máy bia chủ yếu ở miền bắc.

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Other beer labels

Masan Brewery

Sapporo

AB InBev

60

2. Industry overview

2.2 Local market – 2.2.1. Beer

Content is intentionally removed for demo purpose

61

2. Industry overview

2.2 Local market – 2.2.1. Beer

Vietnamese beer is gradually penetrating the world market, with increasing

exports and falling imports, which contributes to boosting the production.

Source: VIRAC, GDVC

Largest beer suppliers for Vietnam 2018

Thousand

tons

Million

USD

Source: VIRAC, Euromalt, United Nations Trade Statistics

Beer import – export, 2010 –2018

Beer consumption market largest Vietnam

2018

Source: VIRAC, GDVC

Content is intentionally removed for demo purpose

62

2. Industry overview

2.2 Local market – 2.2.1. Beer

Export markets outside the territory of Vietnam Beer is Southeast Asia (Singapore, Laos and the Philippines)

Kim ngạch xuất khẩu Bia sang Lào ngày một tăng (chiếm 3.3%), thị trường Lào cũng là một thị trường đầy tiềm năng mà các doanh nghiệp sản xuất Bia Việt Nam

còn chưa khai thác hết. Những ưu điểm lớn của thị trường Lào: vị trí địa lý, khí hậu tương đương Việt Nam, số lượng dân số nam chiếm đa số, kinh tế Lào đang

từng bước phát triển và đây là cùng được coi là một đất nước lễ hội (một năm có 4 lần đón Tết).

Australia là nước nhập khẩu Bia từ Việt Nam lớn thứ 4. Trong những năm gần đây kim ngạch xuất khẩu Bia từ thị trường Việt Nam sang Australia tăng trưởng

khá tốt do giá Bia nhập khẩu từ Việt Nam rẻ so với các nước khác, trong khi chất lượng khá tốt lại quy tụ nhiều hãng bia nổi tiếng tham gia sản xuất. Một nguyên

ngân khác là do chính sách khuyến khích xuất khẩu của Nhà nước.

Trong top 10 doanh nghiệp xuất khẩu bia nhiều nhất, có đến 7 doanh nghiệp có vốn đầu tư của nước ngoài như: Công ty TNHH Sabmiller Việt Nam, Công ty

TNHH Nhà Máy Bia Heineken Hà Nội, Công ty TNHH Bia San Miguel Việt Nam,... Tỷ trọng xuất khẩu của 7 doanh nghiệp này chiếm 32% lượng bia xuất khẩu của

Việt Nam. Mặc dù các doanh nghiệp sản xuất bia trong nước chỉ có 3 đại diện là: Tổng Công ty CP Bia Rượu Nước Giải Khát Sài Gòn, Công ty CP Tập Đoàn

Hương Sen và Công ty CP Đầu Tư Phát Triển Công Nghệ Bia Rượu Nước Giải Khát Hà Nội nhưng tỷ trọng xuất khẩu bia của các công ty này cao hơn các doanh

nghiệp FDI và chiếm 32% thị phần bia xuất khẩu cả nước.

In 2018, 3 main supplyment of Vietnam's Beer is...Mexico (17%), Hà Lan (16%) và Thái Lan (13%). Mexico và Hà Lan là 2 thị trường thống trị bia thế giới

với những công ty bia được ưa chuộng hàng đầu thế giới nói chung và Việt Nam nói riêng là: AB Inbev, Corona Extra thuộc Hà Lan và Mexico.

Thái Lan đứng thứ 3 trong top các quốc gia xuất khẩu Bia sang Việt Nam, Bia Thái Lan được người tiêu dùng Việt ưa chuộng bởi giá chỉ cao hơn sản phẩm Việt

từ 10 - 20% nhưng lại rẻ hơn nhiều so với hàng hóa có xuất xứ từ châu Âu mà chất lượng lại không thua kém nhiều. Dòng Bia Thái được ưa chuộng nhất là Bia

Con Voi của ThaiBev. ThaiBev là doanh nghiệp có cùng chủ sở hữu với tập đoàn TCC Holdings – tập đoàn đã mua lại chuỗi siêu thị Metro. Do vậy, các thương

hiệu Bia Thái thông qua các chuỗi bán lẻ dễ dàng tiếp cận người tiêu dùng trong nước.

Content is intentionally removed for demo purpose

63

2. Industry overview

2.2 Local market – 2.2.1. Beer

Payment methods of beer export enterprises 2018

Beer export delivery conditions 2018

Source: VIRAC, GDVC

Purchasing method:

Content is intentionally removed for demo purpose

64

2. Industry overview

2.2 Local market – 2.2.1. Beer

10 Vietnam’s biggest beer exporters 2018 10 Vietnam’s biggest beer importers 2018

Source: VIRAC, GDVC

Main Vietnam beer import partners, 2018 Main beer export partners to Vietnam, 2018

Source: VIRAC, GDVCSource: VIRAC, GDVC

Source: VIRAC, GDVC

Content is intentionally removed for demo purpose

65

2. Industry overview

2.2 Local market – 2.2.1. Beer

Distribution system

Beer consumption by distribution channels, 2011-2017

Source: VIRAC, Euromonitor

End-user beer price structure

Source: VIRAC, Euromonitor

Content is intentionally removed for demo purpose

Agriculture Vine

FermentationPressing, filtering

and smoothingPackagingWine brewing

Squeezed grape

juiceMixing

Consumer

Agency

Source: Synthesized by VIRAC

66

The wine value chain

Regarding wine

2. Industry overview

2.2 Local market – 2.2.2. Wine

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Source: Synthesized by VIRAC

Regarding malt wine

AgricultureGrapes, cereals,

sugar cane

Fermentation Distillation PackagingWine brewing Mixing

Consumer

Agency

67

2. Industry overview

2.2 Local market – 2.2.2. Wine

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Input material

68

2. Industry overview

2.2 Local market – 2.2.2. Wine

Rice and other cereals

Vine

Content is intentionally removed for demo purpose

69

2. Industry overview

2.2 Local market – 2.2.2. Wine

Content is intentionally removed for demo purpose

Production-consumption

The wine market is on a small scale with falling consumption.

70

2. Industry overview

2.2 Local market – 2.2.2. Wine

Million

litres

Domestic liquor production and consumption 2010-2018

Source: VIRAC, GDVC

Content is intentionally removed for demo purpose

Consumer trends shifted from ordinary wines to vine and high-end ones. The local vine market has a great potential for growth while the malt wine

segment is gloomy, with a shortage of high-quality products.

71

2. Industry overview

2.2 Local market – 2.2.2. Wine

Billion

VND

Million

litres

Wine inventories, 2010-2018

Source: VIRAC, GSO

Sales of vine and malt wines 2010 - 2018

Source: VIRAC, GSO

Content is intentionally removed for demo purpose

72

2. Industry overview

2.2 Local market – 2.2.2. Wine

Internal competition

As of the malt wine segment, Halico occupies the largest consumption share with 2 prevalent brands, including Hanoi Vodka and Hanoi New Rice.

Malt wine consumption of production enterprises, 2017

Source: VIRAC

Malt wine consumption market share, 2017

Source: VIRAC

Avinaa

Content is intentionally removed for demo purpose

73

2. Industry overview

2.2 Local market – 2.2.2. Wine

The local vine wine market is distinctly and Thang Long wine contributes a large share to the market. In addition, local enterprises produce only low-

cost wine lines.

Source: VIRAC

Vine wine consumption of production enterprises, 2017 Vine wine consumption market share by output, 2017

Source: VIRAC

Content is intentionally removed for demo purpose

Import – export

Domestic wine is exported in small and low-value quantities, while high-end

imports are worth 30 times higher.

74

2. Industry overview

2.2 Local market – 2.2.2. Wine

Million

USD

Thousand

tons

Source: VIRAC, United Nations Trade Statistics, GDVC

Thousand

tons

Million

USD

Source: VIRAC, United Nations Trade Statistics, GDVC

Vine wine import and export 2010-2018

Alcohol import and export 2010-2018

Content is intentionally removed for demo purpose

75

2. Industry overview

2.2 Local market – 2.2.2. Wine

Million

USD

Thousand

tons

Source: VIRAC, United Nations Trade Statistics, GDVC

Major wine suppliers to Vietnam, 2018

Source: VIRAC, United Nations Trade Statistics, GDVC

Malt wine import and export 2010-2018

Content is intentionally removed for demo purpose

76

2. Industry overview

2.2 Local market – 2.2.2. Wine

In 2018, wine imports from Laos also rose sharply to due the fact that

glutinous rice wine and white wine with an alcoholic concentration of

under 39% are much favored.

Vietnam’s major wine exports 2018

Source: VIRAC, United Nations Trade Statistics, GDVC

Content is intentionally removed for demo purpose

77

2. Industry overview

2.2 Local market – 2.2.2. Wine

Asia has maintained a key malt wine supplier and consumer of Vietnam

Vietnam’s larges malt wine suppliers 2018

Source: VIRAC, GDVC

Vietnam’s larges malt wine consumers 2018

Source: VIRAC, GDVC

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

78

2. Industry overview

2.2 Local market – 2.2.2. Wine

Source: VIRAC, GDVC

10 Vietnam’s biggest malt wine importers 20107e 10 Vietnam’s biggest malt wine exporters 20107e

Top 10 Vietnam’s malt wine importers 2018Top 10 malt wine exporters to Vietnam 2018

Source: VIRAC, GDVC

Source: VIRAC, GDVCSource: VIRAC, GDVC

Content is intentionally removed for demo purpose

79

2. Industry overview

2.2 Local market – 2.2.2. Wine

Source: VIRAC, GDVC

Top 10 Vietnam’s largest malt wine exporting enterprises 2018 Top 10 Vietnam’s largest malt wine importing enterprises 2018

Top 10 largest malt wine exporters to Vietnam 2018 Top 10 Vietnam’s largest malt wine importers 2018

Source: VIRAC, GDVC

Source: VIRAC, GDVCSource: VIRAC, GDVC

Content is intentionally removed for demo purpose

The soft drink industry

Source: Synthesized by VIRAC

Pure water/mineral water

Mineral water

sourcesFiltration Cooling Bacterial filtration Bottling

AgencyConsumer

Synthesized

by VIRAC

Industrial

water

Soft

drink

LiddingHeat

treatmentBottling Agency

Consume

r

Cooling

CO2

loading

Fizzy soft drink

Source: Synthesized by VIRAC

80

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Content is intentionally removed for demo purpose

Fruit juice

Source: Synthesized by VIRAC

Agriculture Fruit

PressingManual

filtrationFruit gel Purifying

Crystal

filtrationProcessing

Agency

Filling

Consumer

.

81

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Content is intentionally removed for demo purpose

Input material

Sugar

Mineral water

Green tea leaves

82

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Content is intentionally removed for demo purpose

Fruit

Flavorings

83

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Content is intentionally removed for demo purpose

84

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Content is intentionally removed for demo purpose

Production - consumption

The soft drink market runs on a large scale and high growth rate that gradually

meets the local consumption.

85

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Domestic soft drink production and consumption

2010-2018

Billion

liter

Thousand billion

VND

Source: VIRAC, GSO

Soft drink consumption structure (by volume) 2018

Source: VIRAC, GSO

Content is intentionally removed for demo purpose

The soft drink market has a high level of inventories compared to beer and wine, increasing sharply in the period of 2015-2018

86

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Inventories

Unit: million liters

2010 2018

Source: VIRAC, GSO

Inventory structure by product lines 2010-2018

Soft drink inventories 2010 – 2018

Source: VIRAC, GSO

Content is intentionally removed for demo purpose

The soft drink market has a high concentration level and great growth potentials which are very much attractive to investors. The domestic enterprises

remain weak with inadequate production capacity compared to foreign businesses.

Total soft drink enterprises 2010-2018

Source: VIRAC, TCKT

87

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Internal competition

Content is intentionally removed for demo purposeContent is intentionally removed for demo purpose

88

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Vietnam’s soft drink market shares, 2018

Source: VIRAC

Soft drink line market shares, 2018

Source: VIRAC

Content is intentionally removed for demo purpose

89

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Exports have exceeded imports but with lower values.

Import – export

Source: VIRAC, United Nations Trade Statistics, GDVC

Thousand tons Thousand kg

Soft drink export and import, 2010-2018

Content is intentionally removed for demo purpose

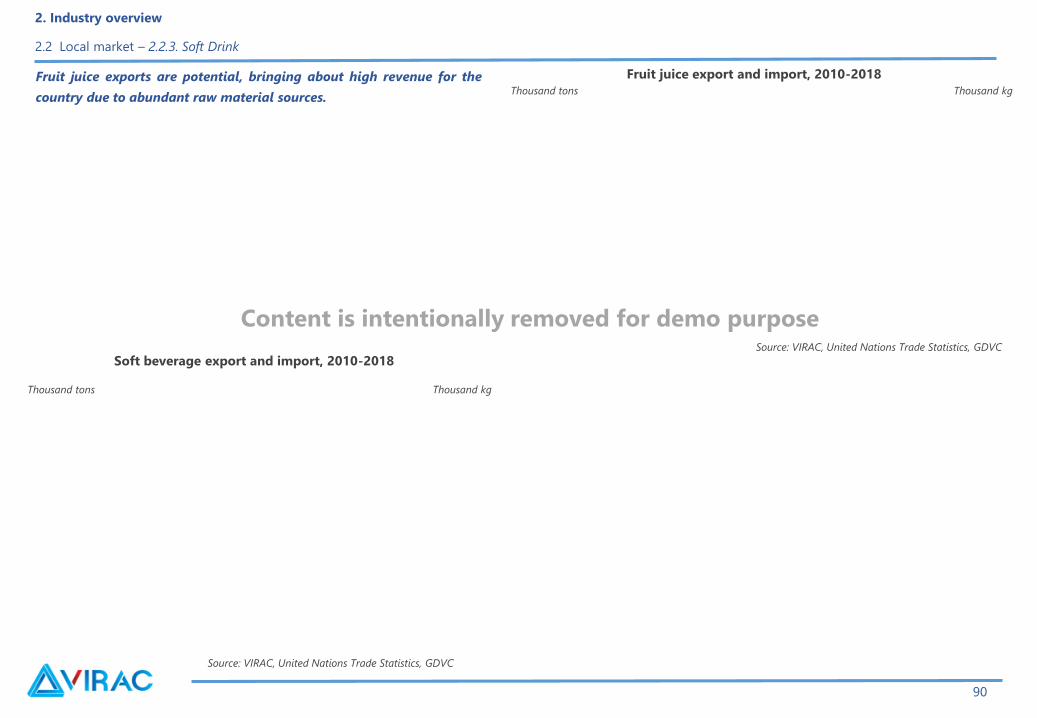

Fruit juice exports are potential, bringing about high revenue for the

country due to abundant raw material sources.

Source: VIRAC, United Nations Trade Statistics, GDVC

Thousand tons Thousand kg

90

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Source: VIRAC, United Nations Trade Statistics, GDVC

Thousand tons Thousand kg

Fruit juice export and import, 2010-2018

Soft beverage export and import, 2010-2018

Content is intentionally removed for demo purpose

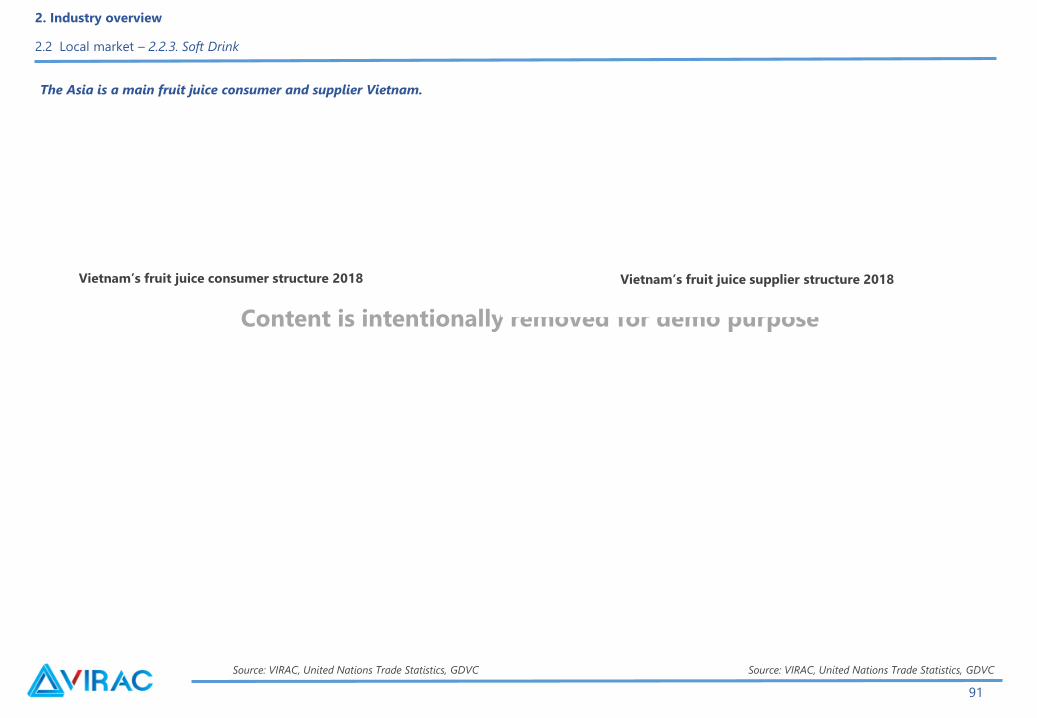

Source: VIRAC, United Nations Trade Statistics, GDVC

The Asia is a main fruit juice consumer and supplier Vietnam.

Vietnam’s fruit juice consumer structure 2018 Vietnam’s fruit juice supplier structure 2018

Source: VIRAC, United Nations Trade Statistics, GDVC

91

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Content is intentionally removed for demo purpose

Similar to the fruit juice segment, Vietnam’s soft drink also deals with the Asia as a major im-exporter.

Vietnam’s soft drink consumer structure 2018 Vietnam’s soft drink supplier structure 2018

Source: VIRAC, Euromalt, United Nations Trade Statistics

92

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Source: VIRAC, United Nations Trade Statistics

Content is intentionally removed for demo purpose

93

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Source: VIRAC, GDVC

10 Vietnam’s biggest soft drink importing enterprises 2018 10 Vietnam’s biggest soft drink exporting enterprises 2018

Top largest fresh drink exporters Vietnam 2018 Top Vietnam’s largest fresh drink importers 2018

Source: VIRAC, GDVC

Source: VIRAC, GDVCSource: VIRAC, GDVC

Content is intentionally removed for demo purpose

94

2. Industry overview

2.2 Local market – 2.2.3. Soft Drink

Source: VIRAC, GDVC

10 Vietnam’s biggest fruit juice exporting enterprises 2018

Top 10 fruit juice exporters to Vietnam 2018

10 Vietnam’s biggest fruit juice importing enterprises 2018

Source: VIRAC, GDVC

Source: VIRAC, GDVC

Source: VIRAC, GDVC

Top 10 fruit juice importers to Vietnam 2018

Content is intentionally removed for demo purpose

Content

2. Industry overview

2.1 Global market

2.2 Local market

2.3 Risk

2.4 Planning and development

2.5 Prospect and prediction

95

Content is intentionally removed for demo purpose

2. Industry overview

2.3 Risks - 2.3.1 SWOT analysis

Strength: Weakness:

Opportunities: Challenges:

96

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

0

1

2

3

4

5

Source: Synthesized by

VIRAC

-1

1

3

5 Customer power

Source: Synthesized by

VIRAC

97

2. Industry overview

2.3 Risks -2.3.2 Competitiveness analysis (5-forces)

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Supplier power

0

1

2

3

4

5

Source: Synthesized by

VIRAC

0

1

2

3

4

5

Nguồn: VIRAC tổng hợp

Potential competitors

98

2. Industry overview

2.3 Risks -2.3.2 Competitiveness analysis (5-forces)

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Subsitute product risks

0

1

2

3

4

5

Source: Synthesized by

VIRAC

012345

Internal competition

Source: Synthesized by

VIRAC

99

2. Industry overview

2.3 Risks -2.3.2 Competitiveness analysis (5-forces)

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

3.1 Production risks

• Input material risks:

• Food safety risks:

100

2. Industry overview

2.3 Risks - 2.3.3 Operating risks

Content is intentionally removed for demo purpose

• Production policy risks:

• Supply chain risks:

• Consumption policy risks:

101

2. Industry overview

2.3 Risks - 2.3.3 Operating risks

Content is intentionally removed for demo purpose

• Competitiveness risks:

• Consumer taste risks:

102

2. Industry overview

2.3 Risks - 2.3.3 Operating risks

Content is intentionally removed for demo purpose

• Media communication risks:

• M&A risks:

103

2. Industry overview

2.3 Risks - 2.3.3 Operating risks

Content is intentionally removed for demo purpose

Content

2. Industry overview

2.1 Global market

2.2 Local market

2.3 Risk

2.4 Planning and development

2.5 Prospect and prediction

104

Content is intentionally removed for demo purpose

Target Beer Wine Soft Drink

Product planning:

Region

Production capacity by

region (million litres)

Capital

investment

2011-2015

(billion VND)2015 2025

Production area planning and

capital investment

Source: VIRAC

Source: VIRAC

105

2. Industry overview

2.4 Planning and development

Content is intentionally removed for demo purpose

Content

2. Industry overview

2.1 Global market

2.2 Local market

2.3 Risk

2.4 Planning and development

2.5 Prospect and prediction

106

Content is intentionally removed for demo purpose

Population:

Income:

Lifestyle and consumer habits:

107

2. Industry overview

2.5 Prospect and prediction -2.5.1 Motivations

Content is intentionally removed for demo purpose

FTAs’ positive impacts

Other factors

108

2. Industry overview

2.5 Prospect and prediction -2.5.1 Motivations

Content is intentionally removed for demo purpose

Source: VIRAC, VBA

109

2. Industry overview

2.5 Prospect and prediction - 2.5.2 Prediction

Sub-sector

Annual forecast (billion VND)Average growth rate (%)

2018f 2019f 2020f

Sub-sectoral consumption price forecast (including both domestic and imported products), 2018-2020

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Product development trend

Beer:

No. Entity Project

Total

invest

ment

Impleme

ntation

span

Capacity (

million

tons/year)

Phas

e I

Phase

II

1

2

3

4

5

6

7

Built and inaugurated beer factories, 2015-2019

Source: Synthesized by VIRAC

110

2. Industry overview

2.5 Prospect and prediction - 2.5.2 Prediction

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Liquor:

Soft Drink:

111

2. Industry overview

2.5 Prospect and prediction - 2.5.2 Prediction

Content is intentionally removed for demo purposeNo. Entity Project

Total

investmentImplementation span

Capacity ( million

tons/year)

Phase IPhase

II

Built and inaugurated soft drink plants, 2015-2018

Source: Synthesized by VIRAC

112

2. Industry overview

2.5 Prospect and prediction - 2.5.2 Prediction

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Relevant sector development trends

Tourism:

113

2. Industry overview

2.5 Prospect and prediction - 2.5.2 Prediction

Content is intentionally removed for demo purpose

114

2. Industry overview

2.5 Prospect and prediction - 2.5.2 Prediction

• Đối tượng sử dụng dịch vụ du lịch sẽ ngày càng đa dạng.

Về khả năng chi tiêu: du lịch đang ngày càng phổ biến, không chỉ những người giàu có từ các nước phát triển mới đi du lịch mà tất cả các tầng lớp khác, từ nhiều

quốc gia khác nhau cũng tham gia ngày càng đông đảo;

Về độ tuổi: người già, người mới nghỉ hưu đi du lịch ngày càng nhiều nên cần có những chương trình đặc biệt phục vụ nhu cầu về nghỉ dưỡng cho đối tượng khách

này;

Về nhân thân: số người độc thân đi du lịch ngày càng tăng;

Về giới tính: Những thay đổi về vai trò và trách nhiệm trong gia đình khiến khách là phụ nữ ngày càng tăng, yêu cầu các cơ sở có những cải tiến, bổ sung các trang

thiết bị, vật dụng và các dịch vụ, lịch trình phù hợp với nhu cầu của nữ thương nhân.

Về loại hình: ngày càng nhiều những nhóm gia đình đăng ký đi du lịch với sự tham gia của đầy đủ các thành viên của cả ba thế hệ trong gia đình, đặc biệt các dịp lễ,

cuối tuần và kỳ nghỉ hè của trẻ em.

• Xu hướng ngày càng tăng nhu cầu cho khách lựa chọn chương trình du lịch có sự kết hợp giữa các loại hình du lịch.

Sự kết hợp hình thức du lịch có thể bao gồm nghỉ biển kết hợp với hội nghị, du lịch khen thưởng kết hợp thăm dò thị trường, du lịch nghỉ dưỡng ngắn ngày kết hợp

với casino,...đòi hỏi các cơ sở đa dạng hoá các sản phẩm như tạo chương trình nghỉ ngơi tham quan di tích lịch sử kết hợp thăm trang trại trồng rau, chè và cây ăn

quả, tổ chức các hoạt động giải trí trên biển.

• Khách hàng có xu hướng muốn chọn tour du lịch tự thiết kế, đặt chỗ qua mạng; tự lựa chọn dịch vụ, không đi theo hình thức trọn gói.

Du lịch mang tính cá nhân nhiều nhất là dịch vụ ăn uống. Vì vậy các doanh nghiệp lữ hành, vận chuyển, khách sạn thường kết hợp tổ chức các chương trình chỉ

cung ứng một phần dịch vụ du lịch như hãng Hàng không quốc gia Việt Nam (Vietnam Airlines) đã tổ chức khá thành công gói sản phẩm Free and Easy chỉ gồm vé

máy bay, dịch vụ đón tiễn sân bay và 3 đêm khách sạn. Nếu có nhu cầu, khách có thể tiếp tục mua tour lẻ và các dịch vụ khác tại điểm đến. Như vậy, để hỗ trợ thúc

đẩy xu hướng này, cần hỗ trợ nâng cao năng lực tiếp cận thị trường của các doanh nghiệp, cơ quan xúc tiến du lịch bằng các công cụ cập nhật theo đời sống hiện

đại như các mạng di động, mạng xã hội như Facebook, Twitter…

Content is intentionally removed for demo purpose

Retailing sector:

11/1/2011 11/1/2012. 11/1/2014 11/1/2015

100%-FDI enterprises’ market penetration roadmap

Source: Synthesized by VIRAC

115

2. Industry overview

2.5 Prospect and prediction - 2.5.2 Prediction

Content is intentionally removed for demo purpose

No. FDI enterprise Total investment Plan/activitty

1

2

3

4

Source: Synthesized by VIRAC

FDI enterprises’ retailing projects and plans have been launched in Vietnam

116

2. Industry overview

2.5 Prospect and prediction - 2.5.2 Prediction

Content is intentionally removed for demo purpose

Content is intentionally removed for demo purpose

Content

117

3 Enterprise analysis

3.1 Profitability

3.2 Operating capability

3.3 Financial strength

3.4 Return on investment

Content is intentionally removed for demo purpose

3. Enterprise analysis

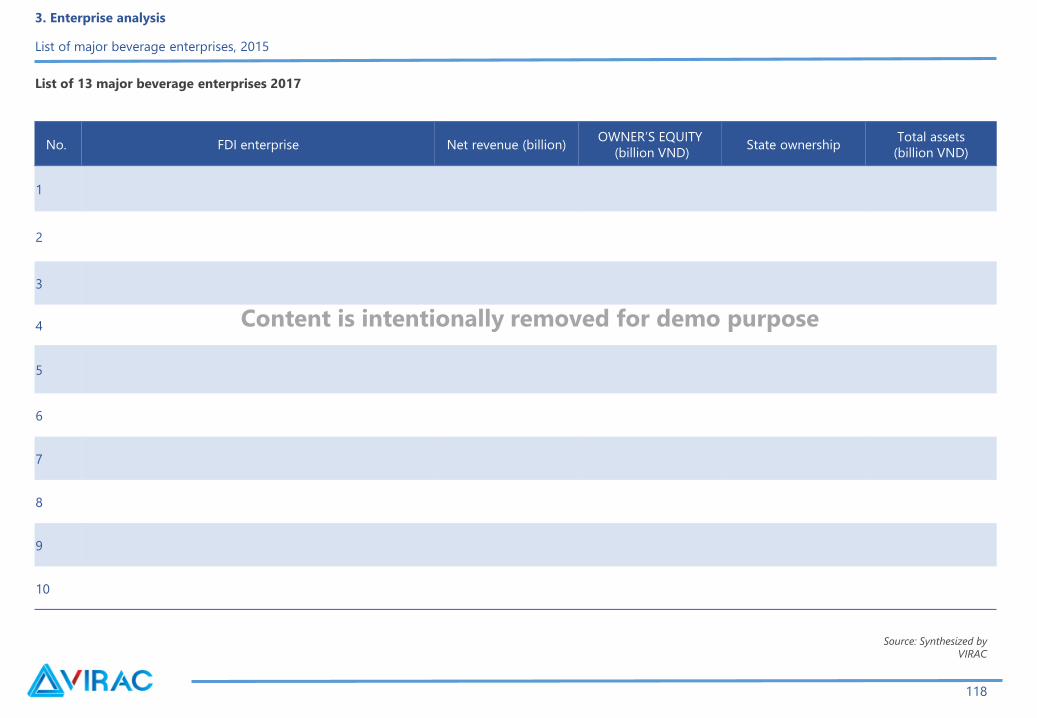

List of major beverage enterprises, 2015

No. FDI enterprise Net revenue (billion)OWNER’S EQUITY

(billion VND)State ownership

Total assets

(billion VND)

1

2

3

4

5

6

7

8

9

10

List of 13 major beverage enterprises 2017

Source: Synthesized by

VIRAC

118

Content is intentionally removed for demo purpose

Content

119

3 Enterprise analysis

3.1 Profitability

3.2 Operating capability

3.3 Financial strength

3.4 Return on investment

Content is intentionally removed for demo purpose

120

3. Enterprise analysis

3.1 Profitability

Billion

VND

Source: Synthesized by

VIRAC

Rate of turnover, 2015-2016

Content is intentionally removed for demo purpose

121

3. Enterprise analysis

3.1 Profitability

Content is intentionally removed for demo purpose

122

3. Enterprise analysis

3.1 Profitability

Billion

VND

Gross profit and gross profit margin, 2016

Source: Synthesized by

VIRAC

Content is intentionally removed for demo purpose

Content

123

3 Enterprise analysis

3.1 Profitability

3.2 Operating capability

3.3 Financial strength

3.4 Return on investment

Content is intentionally removed for demo purpose

124

3. Enterprise analysis

3.2 Operating capability

Turnover of receivables 2016

Unit: times

Source: Synthesized by VIRAC

Source: Synthesized by VIRAC

Corporate inventory turnover 2016

Content is intentionally removed for demo purpose

125

3. Enterprise analysis

3.2 Operating capability

Asset performance, 2016

Unit: times

Source: Synthesized by VIRAC

Content is intentionally removed for demo purpose

Content

126

3 Enterprise analysis

3.1 Profitability

3.2 Operating capability

3.3 Financial strength

3.4 Return on investment

Content is intentionally removed for demo purpose

127

3. Enterprise analysis

3.3 Financial strength

Tan Hiep Phat and Vang Thang Long have debt/equity as well as debt/total assets many times higher than the industry average.

Solvency capacity, 2016

Source: Synthesized by

VIRAC

Content is intentionally removed for demo purpose

128

3. Enterprise analysis

3.3 Financial strength

Payment capacity, 2016

Source: Synthesized by VIRAC

Content is intentionally removed for demo purpose

Content

129

3 Enterprise analysis

3.1 Profitability

3.2 Operating capability

3.3 Financial strength

3.4 Gross profit margin 2015

Content is intentionally removed for demo purpose

130

3. Enterprise analysis

3.4 Gross profit margin

Source: Synthesized by VIRAC

ROA and ROE 2015-2016

Content is intentionally removed for demo purpose

Content

131

4 Appendix

Financial Statements

Content is intentionally removed for demo purpose

BALANCE SHEET

Unit: billion 2016 2015

A. SHORT-TERM ASSETS

I. Cash and cash equivalents

II. Short-term financial investments

III. Short-term receivables

1. Short-term receivables from customers

IV. Inventories

B. LONG-TERM ASSETS

I. Long-term receivables

II. Fixed assets

1. Tangible fixed assets

2. Intangible fixed assets

TOTAL ASSETS

A. LIABILITIES

I. Short-term liabilities

1. Short-term liabilities and loans

2. Taxes and amounts payable to the state

II. Long-term liabilities

1. Long-term liabilities and loans

2. Long-term provisions

B. OWNER’S EQUITY

TOTAL LIABILITIES AND OWNER’S EQUITY

REPORT ON BUSINESS RESULTS

Unit: billion 2016 2015

Net revenue from sales and services

Costs of goods sold

Gross revenues from sales and services

Financial income

Financial cost

Interest expenses

Cost of sales

Enterprise administration expenses

Net profits from operating activities

Total net profit before tax

Current corporate income tax expense

Deferred corporate income tax expense

Profit after tax

CASH FLOW STATEMENT

Unit: billion 2016 2015

I. Cash flows from operating activities

Fixed assets

Unrealized foreign exchange gain/loss

Net cash flows from operating activities

II. Cash flows from investing activities

Other long-term assets

Net cash flows from investing activities

III. Cash flows from financial activities

Net cash flows from financial activities

Effect of exchange rate fluctuations

Net cash flows during the fiscal year

4. Appendix

Financial statements- Saigon Beer-Alcohol-Beverage Joint Stock Corporation (Sabeco)

Content is intentionally removed for demo purpose

132

Content is intentionally removed for demo purpose

CASH FLOW STATEMENT

Unit: billion 2016 2015

I. Cash flows from operating activities

Fixed assets

Unrealized foreign exchange gain/loss

Net cash flows from operating activities

II. Cash flows from investing activities

Other long-term assets

Net cash flows from investing activities

III. Cash flows from financial activities

Net cash flows from financial activities

Effect of exchange rate fluctuations

Net cash flows during the fiscal year

BALANCE SHEET

Unit: billion 2016 2015

A. SHORT-TERM ASSETS

I. Cash and cash equivalents

II. Short-term financial investments

III. Short-term receivables

1. Short-term receivables from customers

IV. Inventories

B. LONG-TERM ASSETS

I. Long-term receivables

II. Fixed assets

1. Tangible fixed assets

2. Intangible fixed assets

TOTAL ASSETS

A. LIABILITIES

I. Short-term liabilities

1. Short-term liabilities and loans

2. Taxes and amounts payable to the state

II. Long-term liabilities

1. Long-term liabilities and loans

2. Long-term provisions

B. OWNER’S EQUITY

TOTAL LIABILITIES AND OWNER’S EQUITY

REPORT ON BUSINESS RESULTS

Unit: billion 2016 2015

Net revenue from sales and services

Costs of goods sold

Gross revenues from sales and services

Financial income

Financial cost

Interest expenses

Cost of sales

Enterprise administration expenses

Net profits from operating activities

Total net profit before tax

Current corporate income tax expense

Deferred corporate income tax expense

Profit after tax

4. Appendix

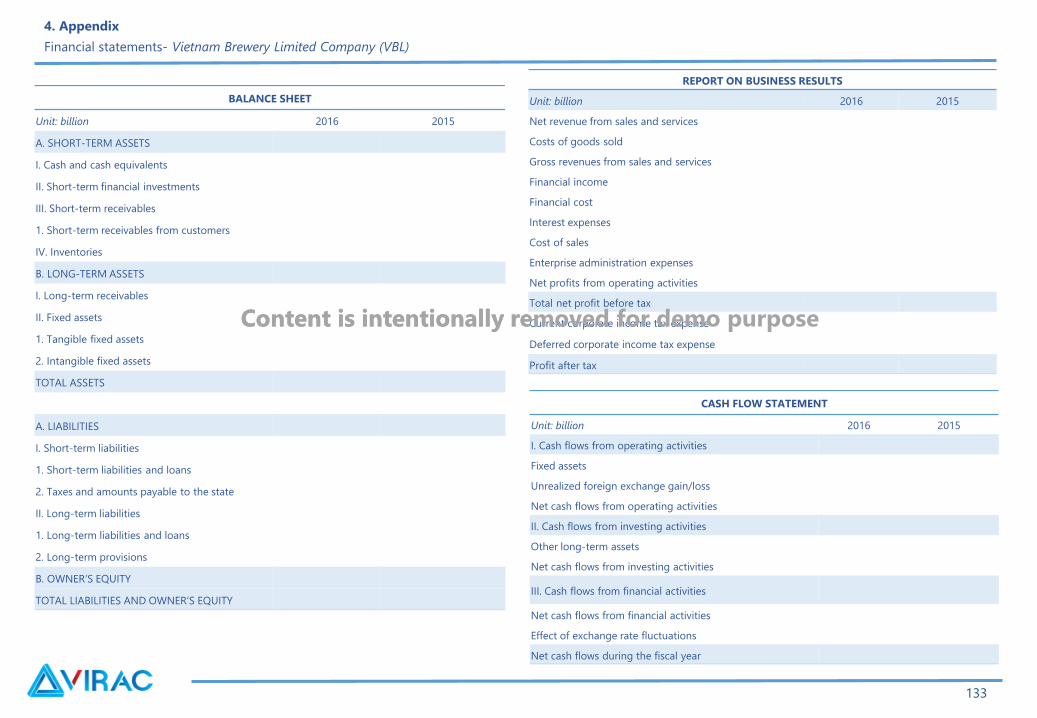

Financial statements- Vietnam Brewery Limited Company (VBL)

Content is intentionally removed for demo purpose

133

Content is intentionally removed for demo purpose

BALANCE SHEET

Unit: billion 2016 2015

A. SHORT-TERM ASSETS

I. Cash and cash equivalents

II. Short-term financial investments

III. Short-term receivables

1. Short-term receivables from customers

IV. Inventories

B. LONG-TERM ASSETS

I. Long-term receivables

II. Fixed assets

1. Tangible fixed assets

2. Intangible fixed assets

TOTAL ASSETS

A. LIABILITIES

I. Short-term liabilities

1. Short-term liabilities and loans

2. Taxes and amounts payable to the state

II. Long-term liabilities

1. Long-term liabilities and loans

2. Long-term provisions

B. OWNER’S EQUITY

TOTAL LIABILITIES AND OWNER’S EQUITY

REPORT ON BUSINESS RESULTS

Unit: billion 2016 2015

Net revenue from sales and services

Costs of goods sold

Gross revenues from sales and services

Financial income

Financial cost

Interest expenses

Cost of sales

Enterprise administration expenses

Net profits from operating activities

Total net profit before tax

Current corporate income tax expense

Deferred corporate income tax expense

Profit after tax

CASH FLOW STATEMENT

Unit: billion 2016 2015

I. Cash flows from operating activities

Fixed assets

Unrealized foreign exchange gain/loss

Net cash flows from operating activities

II. Cash flows from investing activities

Other long-term assets

Net cash flows from investing activities

III. Cash flows from financial activities

Net cash flows from financial activities

Effect of exchange rate fluctuations

Net cash flows during the fiscal year

4. Appendix

Financial statements- Hanoi Beer-Alcohol-Beverage Joint Stock Corporation (Habeco)

Content is intentionally removed for demo purpose

134

Content is intentionally removed for demo purpose

BALANCE SHEET

Unit: billion 2016 2015

A. SHORT-TERM ASSETS

I. Cash and cash equivalents

II. Short-term financial investments

III. Short-term receivables

1. Short-term receivables from customers

IV. Inventories

B. LONG-TERM ASSETS

I. Long-term receivables

II. Fixed assets

1. Tangible fixed assets

2. Intangible fixed assets

TOTAL ASSETS

A. LIABILITIES

I. Short-term liabilities

1. Short-term liabilities and loans

2. Taxes and amounts payable to the state

II. Long-term liabilities

1. Long-term liabilities and loans

2. Long-term provisions

B. OWNER’S EQUITY

TOTAL LIABILITIES AND OWNER’S EQUITY

REPORT ON BUSINESS RESULTS

Unit: million 2016 2015

Net revenue from sales and services

Costs of goods sold

Gross revenues from sales and services

Financial income

Financial cost

Interest expenses

Cost of sales

Enterprise administration expenses

Net profits from operating activities

Total net profit before tax

Current corporate income tax expense

Deferred corporate income tax expense

Profit after tax

CASH FLOW STATEMENT

Unit: billion 2016 2015

I. Cash flows from operating activities

Fixed assets

Unrealized foreign exchange gain/loss

Net cash flows from operating activities

II. Cash flows from investing activities

Other long-term assets

Net cash flows from investing activities

III. Cash flows from financial activities

Net cash flows from financial activities

Effect of exchange rate fluctuations

Net cash flows during the fiscal year

4. Appendix

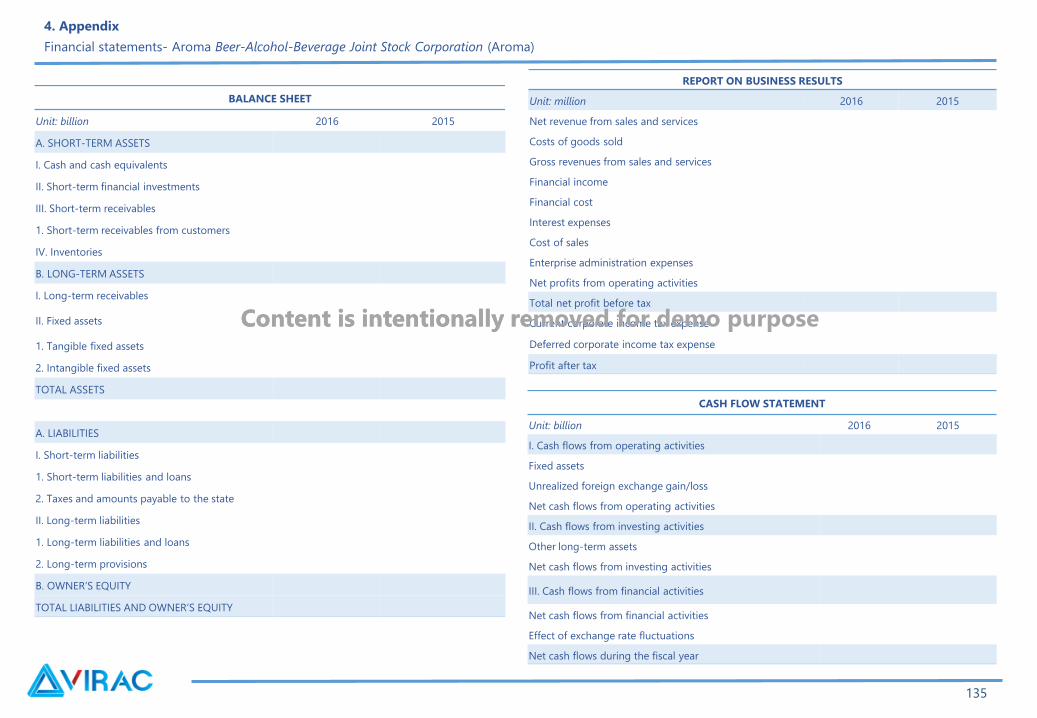

Financial statements- Aroma Beer-Alcohol-Beverage Joint Stock Corporation (Aroma)

Content is intentionally removed for demo purpose

135

Content is intentionally removed for demo purpose

BALANCE SHEET

Unit: billion 2016 2015

A. SHORT-TERM ASSETS

I. Cash and cash equivalents

II. Short-term financial investments

III. Short-term receivables

1. Short-term receivables from customers

IV. Inventories

B. LONG-TERM ASSETS

I. Long-term receivables

II. Fixed assets

1. Tangible fixed assets

2. Intangible fixed assets

TOTAL ASSETS

A. LIABILITIES

I. Short-term liabilities

1. Short-term liabilities and loans

2. Taxes and amounts payable to the state

II. Long-term liabilities

1. Long-term liabilities and loans

2. Long-term provisions

B. OWNER’S EQUITY

TOTAL LIABILITIES AND OWNER’S EQUITY

REPORT ON BUSINESS RESULTS

Unit: billion 2016 2015

Net revenue from sales and services

Costs of goods sold

Gross revenues from sales and services

Financial income

Financial cost

Interest expenses

Cost of sales

Enterprise administration expenses

Net profits from operating activities

Total net profit before tax

Current corporate income tax expense

Deferred corporate income tax expense

Profit after tax

CASH FLOW STATEMENT

Unit: billion 2016 2015

I. Cash flows from operating activities

Fixed assets

Unrealized foreign exchange gain/loss

Net cash flows from operating activities

II. Cash flows from investing activities

Other long-term assets

Net cash flows from investing activities

III. Cash flows from financial activities

Net cash flows from financial activities

Effect of exchange rate fluctuations

Net cash flows during the fiscal year

4. Appendix

Financial statements- Thang Long Wine Joint Stock Company

Content is intentionally removed for demo purpose

136

Content is intentionally removed for demo purpose

BALANCE SHEET

Unit: billion 2016 2015

A. SHORT-TERM ASSETS

I. Cash and cash equivalents

II. Short-term financial investments

III. Short-term receivables

1. Short-term receivables from customers

IV. Inventories

B. LONG-TERM ASSETS

I. Long-term receivables

II. Fixed assets

1. Tangible fixed assets

2. Intangible fixed assets

TOTAL ASSETS

A. LIABILITIES

I. Short-term liabilities

1. Short-term liabilities and loans

2. Taxes and amounts payable to the state

II. Long-term liabilities

1. Long-term liabilities and loans

2. Long-term provisions

B. OWNER’S EQUITY

TOTAL LIABILITIES AND OWNER’S EQUITY

REPORT ON BUSINESS RESULTS

Unit: billion 2016 2015

Net revenue from sales and services

Costs of goods sold

Gross revenues from sales and services

Financial income

Financial cost

Interest expenses

Cost of sales

Enterprise administration expenses

Net profits from operating activities

Total net profit before tax

Current corporate income tax expense

Deferred corporate income tax expense

Profit after tax

CASH FLOW STATEMENT

Unit: billion 2016 2015

I. Cash flows from operating activities

Fixed assets

Unrealized foreign exchange gain/loss

Net cash flows from operating activities

II. Cash flows from investing activities

Other long-term assets

Net cash flows from investing activities

III. Cash flows from financial activities

Net cash flows from financial activities

Effect of exchange rate fluctuations

Net cash flows during the fiscal year

4. Appendix

Financial report- Ladofood Company Ltd.

Content is intentionally removed for demo purpose

137

Content is intentionally removed for demo purpose

BALANCE SHEET

Unit: billion 2016 2015

A. SHORT-TERM ASSETS

I. Cash and cash equivalents

II. Short-term financial investments

III. Short-term receivables

1. Short-term receivables from customers

IV. Inventories

B. LONG-TERM ASSETS

I. Long-term receivables

II. Fixed assets

1. Tangible fixed assets

2. Intangible fixed assets

TOTAL ASSETS

A. LIABILITIES

I. Short-term liabilities

1. Short-term liabilities and loans

2. Taxes and amounts payable to the state

II. Long-term liabilities

1. Long-term liabilities and loans

2. Long-term provisions

B. OWNER’S EQUITY

TOTAL LIABILITIES AND OWNER’S EQUITY

REPORT ON BUSINESS RESULTS

Unit: billion 2016 2015

Net revenue from sales and services

Costs of goods sold

Gross revenues from sales and services

Financial income

Financial cost

Interest expenses

Cost of sales

Enterprise administration expenses

Net profits from operating activities

Total net profit before tax

Current corporate income tax expense

Deferred corporate income tax expense

Profit after tax

CASH FLOW STATEMENT

Unit: billion 2016 2015

I. Cash flows from operating activities

Fixed assets

Unrealized foreign exchange gain/loss

Net cash flows from operating activities

II. Cash flows from investing activities

Other long-term assets

Net cash flows from investing activities

III. Cash flows from financial activities

Net cash flows from financial activities

Effect of exchange rate fluctuations

Net cash flows during the fiscal year

4. Appendix

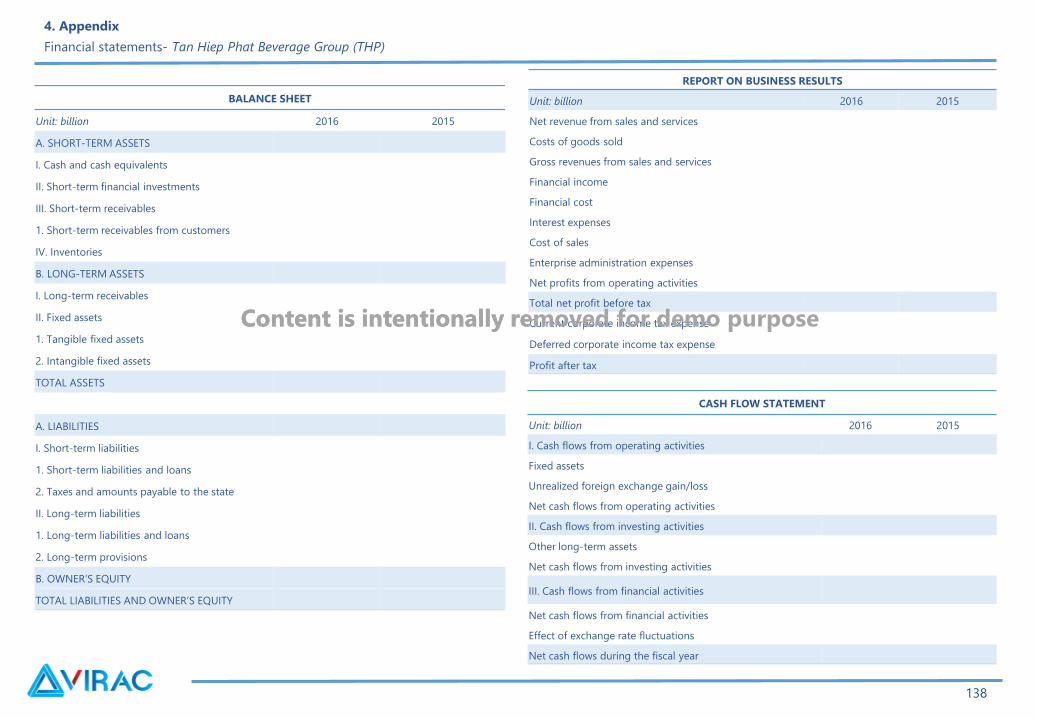

Financial statements- Tan Hiep Phat Beverage Group (THP)

Content is intentionally removed for demo purpose

138

Content is intentionally removed for demo purpose

BALANCE SHEET

Unit: billion 2016 2015

A. SHORT-TERM ASSETS

I. Cash and cash equivalents

II. Short-term financial investments

III. Short-term receivables

1. Short-term receivables from customers

IV. Inventories

B. LONG-TERM ASSETS

I. Long-term receivables

II. Fixed assets

1. Tangible fixed assets

2. Intangible fixed assets

TOTAL ASSETS

A. LIABILITIES

I. Short-term liabilities

1. Short-term liabilities and loans

2. Taxes and amounts payable to the state

II. Long-term liabilities

1. Long-term liabilities and loans

2. Long-term provisions

B. OWNER’S EQUITY

TOTAL LIABILITIES AND OWNER’S EQUITY

REPORT ON BUSINESS RESULTS

Unit: billion 2016 2015

Net revenue from sales and services

Costs of goods sold

Gross revenues from sales and services

Financial income

Financial cost

Interest expenses

Cost of sales

Enterprise administration expenses

Net profits from operating activities

Total net profit before tax

Current corporate income tax expense

Deferred corporate income tax expense

Profit after tax

CASH FLOW STATEMENT

Unit: billion 2016 2015

I. Cash flows from operating activities

Fixed assets

Unrealized foreign exchange gain/loss

Net cash flows from operating activities

II. Cash flows from investing activities

Other long-term assets

Net cash flows from investing activities

III. Cash flows from financial activities

Net cash flows from financial activities

Effect of exchange rate fluctuations

Net cash flows during the fiscal year

4. Appendix

Financial statements- URC Vietnam Co., Ltd

Content is intentionally removed for demo purpose

139

Content is intentionally removed for demo purpose

BALANCE SHEET

Unit: billion 2016 2015