vertical coordination of marketing systems: lessons from

TRANSCRIPT

Abstract

The poultry, egg, and pork industries have taken significant steps to improve the control ofproduction either through contracting and/or vertical integration. These improved controlswere motivated by the emergence of new specialized large-scale production technologiesthat placed a premium on quality control and the efficient use of information. The height-ened speed of production, the perishable nature of products, and significant measuring andsorting costs all increased the difficulty of obtaining accurate economic information andthereby increased the cost of exchange throughout the marketing system. Contracts andvertical coordination provided an efficient means of organizing markets by reducing thesetransaction costs.

Keywords: Vertical coordination, vertical integration, contracts, transaction cost econom-ics, technology, measuring and sorting costs, poultry, pork.

Acknowledgments

I would like to thank Carolyn Dimitri, Jill Hobbs, and Kelly Zering for their extensivecomments. Carolyn provided invaluable comments regarding the organization and contentof the report. I also thank Jim MacDonald, Alden Manchester, and Annette Clauson fortheir helpful comments, John Weber for editorial assistance, and Cynthia Ray for graphicdesign assistance.

Note: Use of brand or firm names in this publication does not imply endorsement by theU.S. Department of Agriculture.

United StatesDepartmentof Agriculture

www.ers.usda.gov

Electronic Report from the Economic Research Service

Vertical Coordination ofMarketing Systems: Lessons From the Poultry, Egg, and Pork Industries

Steve W. Martinez

April 2002

AgriculturalEconomicReport No. 807

Contents

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Evolution of Vertical Coordination in the Poultry, Egg, and Pork Industries . . . . . . . . . . . . 2

Vertical Coordination in the Poultry and Egg Industries . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Vertical Coordination in the Pork Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Incentives for Contracting and Vertical Integration: A Transaction Cost Approach . . . . . . . 6

Asset Specificity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Uncertainty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Measurement Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

The Viability of Spot-Market Transactions in the Poultry, Egg, and Pork Industries . . . . . 10

Physical Specificities and Small-Number Conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Site and Temporal Specificities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Measurement Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Marketing Contracts, Production Contracts, or Vertical Integration? . . . . . . . . . . . . . . . . . 18

Uncertainty and Vertical Acquisitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Vertical Integration in the Turkey and Egg Industries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Marketing Contracts in the Pork Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Beyond Transaction Costs:Benefit Effects From Contracting and Vertical Integration . . . . . . . . . . . . . . . . . . . . . . . . 23

Production Efficiency Gains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Quality and Uniformity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Potential for Further Research on Incorporating Benefit Effects . . . . . . . . . . . . . . . . . . . . . 27

Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Selected References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Appendix A: Vertical Stages of the Poultry and Egg Industries . . . . . . . . . . . . . . . . . . . . . . 37

Appendix B: Geographic Region Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

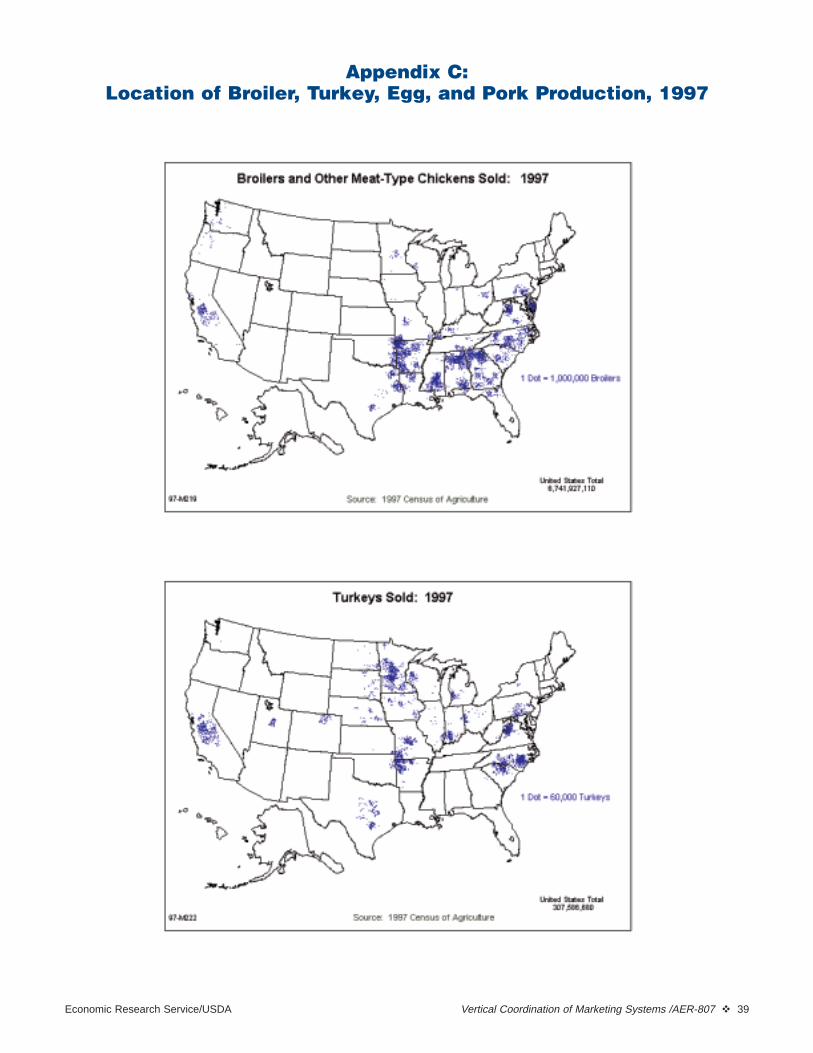

Appendix C: Location of Broiler, Turkey, Egg, and Pork Production, 1997 . . . . . . . . . . . . . 39

Appendix D: Demand Index Calculations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

ii � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

Economic Research Service/USDA Vertical Coordination or Marketing Systems /AER-807 � iii

Summary

The U.S. poultry, egg, and pork industries each have experienced increases in contract-ing and vertical integration. Changes occurred decades ago in the poultry and eggindustries and have occurred more recently in the pork industry. Production contract-ing grew quickly in the broiler industry, and nearly all broilers now are producedunder production contracts between processors and growers. While production con-tracts also became more prevalent in the turkey and egg industries, vertical integrationalso became more common. In the pork industry, marketing contracts became morepopular, although packer ownership of hogs also has risen in more recent years.

In each of the industries, spot markets apparently became a less efficient means ofcoordinating production and processing. This effect may be explained by higher trans-action costs from a variety of sources. First, several developments in each of the indus-tries led to higher costs associated with safeguarding investments. Each of the indus-tries underwent periods in which they adopted new specialized technologies and expe-rienced associated scale economies. These developments led to investments with fewalternative uses and few alternative users, or relationship-specific investments, particu-larly in regions of expanding production. Such investments leave trading partners vul-nerable to opportunistic behavior by other parties seeking a more favorable position inthe relationship.

Other factors also created value in continuing relationships between specific tradingpartners. For example, in the poultry and egg industries, farms and processing unitslocated close to each other. Short distances between trading partners resulted in morerelationship-specific transactions—trading partners separated by longer distanceswould result in higher transportation costs. Also, poultry and eggs are perishable prod-ucts that require timely delivery from the farm to the processing plant. This factormakes producers highly vulnerable to tactics used by processors to delay acceptanceof products to obtain a more favorable deal, as it may be difficult for producers to findalternative processors before the products perish.

Contracting and vertical integration provided a means for reducing transaction costsassociated with relationship-specific transactions, especially in regions of expandingproduction. Contracts could provide some safeguards to protect against opportunisticbehavior, and vertical integration eliminated the exchange relationship altogether.

Contracts and vertical integration also may facilitate reductions in product measuringand sorting costs, leaving more gains from trade to be distributed among producersand consumers. For product attributes that are difficult to measure, gaining additionalcontrol over related production inputs may reduce measuring costs by reducing theneed to measure quality. Similarly, by controlling inputs that result in more uniformproduct attributes, measuring and sorting costs may be reduced because there is noneed to measure every product. Controlling production inputs facilitates branding pro-grams that transfer measuring and sorting costs from consumers to the food supplysystem. The poultry industry has been especially successful with branding programs,and the pork industry is increasing its use of branding strategies.

iv � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

Relationship-specific transactions and uncertain market conditions also may explaindifferences in methods of vertical coordination found in the poultry, egg, and porkmarkets. As transactions become more relationship-specific, vertical integration willbecome more prevalent. Greater uncertainty related to consumer preferences, produc-tion, or income make it more important for firms to find ways to adapt. Consequently,vertical integration and contracts that give the contractor more control over the produc-er or that respond automatically to changing conditions will become more common.

In addition to reducing transaction costs, contracts and vertical integration may influ-ence production decisions that result in more efficient resource allocations. This effectis demonstrated by substantial gains in production efficiency in each of the threeindustries and development of high-quality, consistent consumer products. Consideringboth reductions in transaction costs and benefit effects would provide a more completeframework for analyzing the organization of agricultural markets.

Introduction

Vertical coordination of the broiler, turkey, and eggindustries changed significantly decades ago. In thebroiler industry, production contracts between feedcompanies/contractors and growers accounted for over85 percent of production in 1955, as fewer growersoperated independently. These contracts later evolved,giving more control to the contractors. In the 1960s,relationships between the production and processingstages also changed, as feed companies became moredirectly involved in both broiler production and pro-cessing. In the 1970s, many feed companies exited thebroiler business, leaving processors as the major con-tractors with growers. Since the 1950s, the prevalenceof production contracts in the broiler industry hasbeen stable.

In the turkey and egg industries, contracting developedat a slower rate than in the broiler industry, but verticalintegration was more common. In vertically integratedoperations, a single firm conducts production and pro-cessing. Initially, feed dealers entered production con-tracts with egg and turkey producers. In 1955, 21 per-cent of turkeys were produced under production con-tracts, and 4 percent were produced in vertically inte-grated operations. By 1977, production contractsaccounted for 52 percent of production, and verticalintegration had increased to 28 percent of production.In 1955, only 2 percent of table eggs were producedunder production contracts or vertically integratedoperations. By 1977, production contracts and vertical-ly integrated operations accounted for 44 and 37 per-cent of table egg production, respectively. Over thisperiod, production contracts in the egg and turkeyindustries evolved to transfer more price and produc-tion risk from growers to contractors, and processorsassumed the role of contractor. Today, production con-tracts, together with vertical integration, account forover 90 percent of production in each of the threeindustries.

Coordinating arrangements in the turkey and eggindustries have received less scrutiny than arrange-ments in the broiler industry, perhaps due to the small-er size and level of growth of the turkey and eggindustries. In 1999, broilers represented 68 percent ofthe estimated farm value of U.S. poultry and egg sales,compared with 19 percent for eggs and 13 percent forturkeys (USDA[c]). However, despite these differ-ences, a comparison of the structural changes in eachof the three industries may provide useful insights intoother agricultural industries that are undergoingchanges in vertical coordination.

More recently, the U.S. pork industry also has under-gone significant changes in vertical coordination, ascontracting has surged. From 1993 to 2001, hogs soldthrough contractual arrangements increased in share oftotal hogs sold from 10 to 72 percent. Consequently,sales and purchases through the traditional spot, oropen, markets have dwindled to 28 percent.

This report examines possible motives for changes invertical coordination of the poultry, egg, and porkindustries. In the broiler industry, production contractsand vertical integration facilitated rapid growth of theindustry through gains in production efficiency andresponse to consumer preferences for convenient,nutritious products (Martinez, 1999). To what extentis the broiler industry unique in its motives for con-tracting and vertical integration? What are the com-mon characteristics of the poultry, egg, and porkindustries that explain such a large degree of contract-ing and vertical integration? Why are there differencesin the use of contracting and vertical integration in theotherwise similar poultry and egg industries? Whatinsights do such comparisons bring to industries thatare currently undergoing dramatic structural changes,such as the pork industry? This report attempts toanswer these questions by extending concepts fromtransaction cost economics.

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 1

Evolution of VerticalCoordination in the Poultry,

Egg, and Pork Industries

Vertical coordination refers to the synchronization ofsuccessive stages of production and marketing, withrespect to quantity, quality, and timing of productflows. Methods of vertical coordination include openproduction (also referred to as open, or spot, market),contract production, and vertical integration. In openproduction, a firm does not commit to selling its out-put before completing production. Cash (or spot)prices coordinate resource transfer across the stages ofproduction. Contract production is the production ofgoods and services for future delivery. Before complet-ing production, a producer commits to deliver a partic-ular good to a particular buyer. Contract productioninvolves more interaction between buyers and sellersthan open production. Production contracts vary incontrol allocated and risk transferred across stages. Inmarket-specific production contracts, the contractorand producer may negotiate delivery schedule, pricingmethod, and product characteristics. The contractorusually provides a market for the goods but engages infew of the producer’s decisions.1 In resource-providingcontracts, the contractor provides a market for thegoods, engages in many of the producer’s decisions,and retains ownership of important production inputs.While this classification scheme is not unique, it pro-vides a general framework for contract terminology(Martinez and Reed).2

In vertical integration, a single firm controls two ormore successive stages of vertical coordination. In ver-tically integrated firms, management directives dictatethe transfer of resources across stages.

Movement along the continuum of vertical coordina-tion from open-market production to vertical integra-tion represents the degree to which control of produc-tion has shifted to the contractor or integrator as morefunctions are transferred from the producer (fig. 1).

While market-specific production contracts, oftenreferred to as marketing contracts, provide contractorswith more control than open-market coordination, thecontrol transferred across stages is usually minimal.

Vertical Coordination in the Poultry and Egg IndustriesIn the mid-1900s, poultry and egg firms specialized incertain activities, and spot markets were the dominantmeans of vertical coordination (app. A). Feed was pro-duced in commercial feed mills. Poultry and eggs weresold to slaughter plants and egg-handling facilities thatperformed many of the marketing functions. By themid-1950s, however, vertical coordination of theseactivities through contracts and vertical integration hadbecome increasingly common.

Broilers3

Production contracts, whereby the contractor andgrower (or a smaller producer) each provide significantinputs into the production process, have been the dom-inant means of coordinating broiler production sincethe mid-1950s (fig. 2).4 Initially, feed companies con-tracted with broiler growers, spurred by a potentiallylarge and stable market for their feed. As broiler pro-duction grew in the South, production contractsevolved to give the contractor more control over pro-duction and shift more price and production risk fromgrowers to contractors.

In the 1960s, feed-company contractors becameinvolved in broiler processing by acquiring or con-structing processing plants. Contractors, such as

2 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

1The contractor in an exchange relationship is the firm that con-trols several stages of production and marketing through con-tracts. In this report, the term “integrator” is reserved for a firmthat controls several stages through vertical integration. 2In their ground-breaking 1963 study, Mighell and Jones alsoinclude production-management contracts in their categorizationof production contracts. These contracts are similar to market-specific contracts but give contractors more direct involvement inproduction decisions.

3See Martinez (1999) for more details regarding developments inbroiler contracting and vertical integration. 4Continuous time series data sets that document methods of verti-cal coordination are generally not available. National surveys andindividual State studies provide some indications of these devel-opments at particular points in time.

Figure 1

Methods of vertical coordination along the spectrum of control

Control offered to contractor or integrator Least Most

Verticalintegration

Source: Mighell and Jones.

Openproduction

Market-specific contract

(or marketing contract)

Resource-providing contract

(or production contract)

Ralston-Purina, Allied Mills, Central Soya, Cargill,and ConAgra, controlled broiler production capacityfrom feed mills to processing and marketing.

In the early 1970s, broiler price swings caused manyfeed companies to reduce their investments in thepoultry business (Strausberg). Processors, such asTyson Foods and Hudson Foods, then took over therole of contractor. Today, nearly all broiler productionand processing is coordinated through production con-tracts between growers and processors. Contract termstypically specify that the processors will provide thebaby chicks, feed, and management and veterinary ser-vices. The growers provide the labor and chickenhouses and receive a payment per pound of live broil-ers produced, based on a grower’s performance relativeto other growers.

Turkeys

Before 1950, turkey growers operated independently,obtaining financing from traditional sources (localbanks, production credit associations) to pay for feed,poults, and supplies (Roy, 1972). However, in the1950s, the industry experienced financial setbacks, andthese traditional sources became more reluctant to

finance turkey growing. Consequently, hatcheries pro-vided poult financing, and feed companies providedboth feed and poult financing as a means to expandfeed production. These financial arrangements eventu-ally evolved into production contracts that shifted riskfrom grower to contractor.5 By 1961, feed companiesaccounted for 65 percent of total turkey productionunder contract (Gallimore). To coordinate productionand processing, many feed companies also ownedhatcheries and acquired processing facilities. As theturkey industry developed throughout the 1960s,processors became increasingly involved in turkey pro-duction decisions (Manchester). Processors began rais-ing their own turkeys or contracting to better scheduleproduction and ensure supplies.6 By 1977, as feweroutlets existed for independent growers, the share ofturkeys sold on the U.S. spot market fell to only 10percent of turkeys produced.

Today, production contracts account for about 56 per-cent of turkey production and vertical integrationaccounts for about 32 percent. Production contracts inthe turkey industry are similar to resource-providingproduction contracts in the broiler industry: the growerprovides the buildings, equipment, and labor, and theprocessor provides poults, feed, veterinary services,and managerial assistance. Most growers receive a feeper bird or per pound that may include performanceincentives for feed conversion and reduced turkey mor-tality rates (Lasley, Henson, and Jones). Vertically inte-grated operations, in which the processor owns all pro-duction facilities and hires labor to care for the birds,are more prevalent in the turkey industry than in thebroiler industry.

EggsIn the egg industry, significant increases in contractingby feed companies and processors began in the late1950s. As in the broiler industry, contracts in the eggindustry evolved to give the contractor more controlover production and reduce growers’ price and produc-tion risks. Grower returns became less dependent onmarket prices, as flat-fee payments (for example, perbird, per dozen eggs) or payments related to produc-

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 3

1955 65 75 77 94 1955 65 75 77 94 1955 65 75 77 940

20

40

60

80

100

Production contracts

Marketing contracts

Vertical integration

Figure 2

Poultry and eggs produced under contracts andvertical integration

Percent

Broilers Turkeys Eggs

Note: According to Roy (1963), independent broiler production accounted for 95 percent of total production in 1950.Sources: Rogers (1979); Manchester.

5Similar to the broiler industry, turkey production contractsevolved from financing arrangements, in which the contractorsometimes participated in the management decisions, to risk-shar-ing arrangements (Gallimore and Vertrees). 6According to Gallimore and Irvin, unlike the broiler industry,processors, rather than feed companies, were “the major coordi-nators in the turkey industry.”

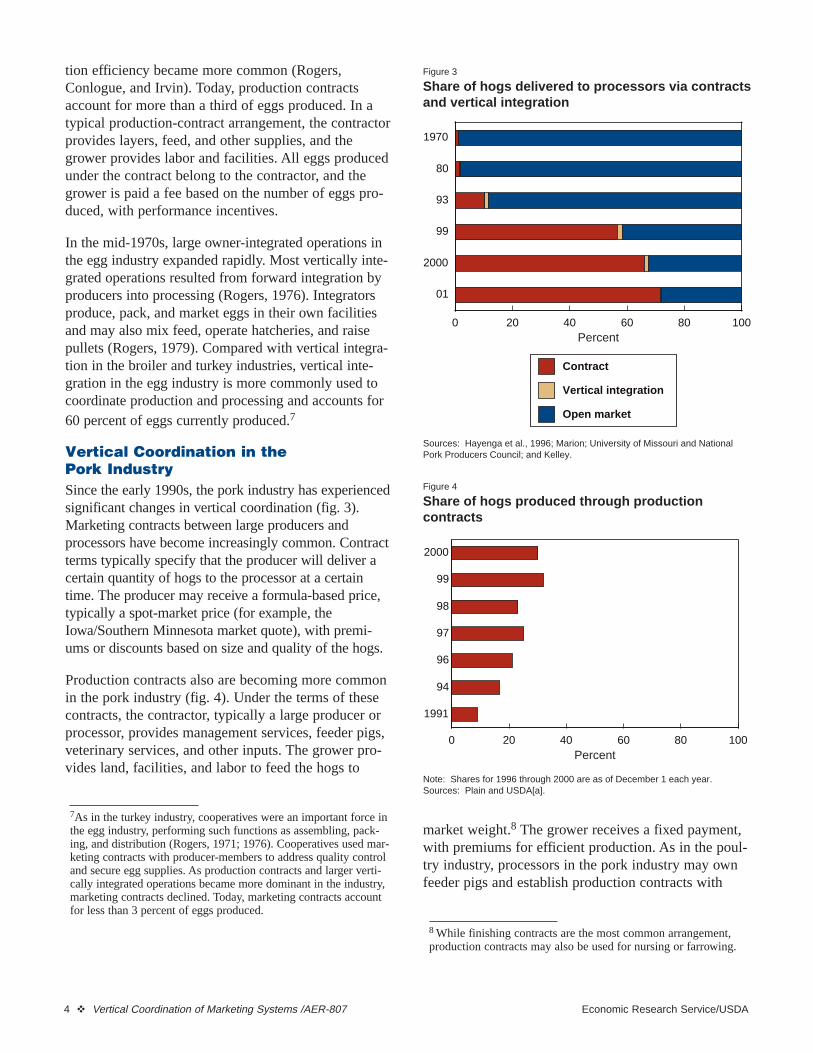

tion efficiency became more common (Rogers,Conlogue, and Irvin). Today, production contractsaccount for more than a third of eggs produced. In atypical production-contract arrangement, the contractorprovides layers, feed, and other supplies, and thegrower provides labor and facilities. All eggs producedunder the contract belong to the contractor, and thegrower is paid a fee based on the number of eggs pro-duced, with performance incentives.

In the mid-1970s, large owner-integrated operations inthe egg industry expanded rapidly. Most vertically inte-grated operations resulted from forward integration byproducers into processing (Rogers, 1976). Integratorsproduce, pack, and market eggs in their own facilitiesand may also mix feed, operate hatcheries, and raisepullets (Rogers, 1979). Compared with vertical integra-tion in the broiler and turkey industries, vertical inte-gration in the egg industry is more commonly used tocoordinate production and processing and accounts for60 percent of eggs currently produced.7

Vertical Coordination in the Pork IndustrySince the early 1990s, the pork industry has experiencedsignificant changes in vertical coordination (fig. 3).Marketing contracts between large producers andprocessors have become increasingly common. Contractterms typically specify that the producer will deliver acertain quantity of hogs to the processor at a certaintime. The producer may receive a formula-based price,typically a spot-market price (for example, theIowa/Southern Minnesota market quote), with premi-ums or discounts based on size and quality of the hogs.

Production contracts also are becoming more commonin the pork industry (fig. 4). Under the terms of thesecontracts, the contractor, typically a large producer orprocessor, provides management services, feeder pigs,veterinary services, and other inputs. The grower pro-vides land, facilities, and labor to feed the hogs to

market weight.8 The grower receives a fixed payment,with premiums for efficient production. As in the poul-try industry, processors in the pork industry may ownfeeder pigs and establish production contracts with

4 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

Figure 3

Share of hogs delivered to processors via contractsand vertical integration

Percent

Sources: Hayenga et al., 1996; Marion; University of Missouri and National Pork Producers Council; and Kelley.

01

2000

99

93

80

1970

0 20 40 60 80 100

Contract

Vertical integration

Open market

Figure 4

Share of hogs produced through production contracts

Percent

Note: Shares for 1996 through 2000 are as of December 1 each year.Sources: Plain and USDA[a].

1991

94

96

97

98

99

2000

0 20 40 60 80 100

7As in the turkey industry, cooperatives were an important force inthe egg industry, performing such functions as assembling, pack-ing, and distribution (Rogers, 1971; 1976). Cooperatives used mar-keting contracts with producer-members to address quality controland secure egg supplies. As production contracts and larger verti-cally integrated operations became more dominant in the industry,marketing contracts declined. Today, marketing contracts accountfor less than 3 percent of eggs produced.

8 While finishing contracts are the most common arrangement,production contracts may also be used for nursing or farrowing.

growers to feed the hogs to market weight. Packer-owned hogs increased from 6.4 percent of U.S. hogproduction in 1994 to 24 percent in 2000, reflectingSmithfield Foods’ (the Nation’s largest hog producerand processor) recent purchases of two leading hogproducers (Messenger, April 2000). Most of these hogsare priced using formula-based marketing contractswith the production unit (Grimes and Meyer).9

Hog producers and processors may enter into both pro-duction and marketing contracts. For example,Prestage Farms, the Nation’s fourth-largest hog pro-ducer, produces its hogs under production contractswith growers. Prestage then sells the hogs toSmithfield Foods, using marketing contracts at market-indexed prices.

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 5

9Grimes and Meyer categorize these contracts as formula-basedmarketing contracts. In our classification scheme, these contractsare best described as production contracts because the processorowns significant production inputs.

6 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

Incentives for Contracting and Vertical Integration:

A Transaction Cost Approach

To explain alternative forms of vertical coordination inthe poultry, egg, and pork industries, one must rely onthe existence of market failures (Milgrom andRoberts). In the traditional neoclassical paradigm,coordination through spot markets can reconcile theindividual objectives of many consumers, direct manyvaluable and limited resources to production, andmotivate firms to produce the right products. Theresulting allocation of goods is efficient given the fol-lowing assumptions:

• Each producer knows prices and production technol-ogy and maximizes profits.

• Consumers know prices and preferences and maxi-mize utility given income.

• Prices adjust to equate supply and demand for eachgood.

Under these assumptions, prices allocate resources totheir most valued use, and consumers prefer no otherallocations given available resources and technology.In reality, however, firms have concerns about theirability to buy and sell the quantities they want at givenprices. Buyers and sellers may not know the exactspecifications of goods that they demand or supply.Buyers face costs associated with searching for ade-quate suppliers offering the most favorable prices, andsellers face costs associated with communicating theavailability of products with specific attributes.

This report applies the transaction cost economics(TCE) paradigm, which relies on the existence oftransaction costs.10 Transaction costs are costs associ-ated with reaching and enforcing agreements and havebeen equated to “the costs of running the economicsystem” (Masten, 1996; Williamson, 1996).Transaction costs include those costs associated withplanning, adapting, and monitoring economic activi-ties. While these functions are not directly productive,

they are required to coordinate the activities of buyersand sellers.

TCE analysis suggests that the main purpose andeffect of contracts and vertical integration is to reducetransaction costs. Transaction costs associated withspot-market coordination include buyer costs ofsearching for suppliers offering preferred quality fea-tures at favorable prices and seller costs of determiningprices and buyer preferences. Buyers and sellers canreduce some of these costs by entering into a contractarrangement before production is completed, but theycan still encounter other types of costs. Ex ante (priorto reaching an agreement) contracting costs are costsassociated with drafting, negotiating, and safeguardingagreements. Ex post (following an agreement) costsare costs associated with enforcing agreements andmay require measuring damages or injury to a contractparty, enacting penalties, and compensating an injuredparty (North). Vertical integration may reduce costs ofcontracting and spot-market trading but may alsointroduce new types of transaction costs, includingcosts related to communicating information within afirm (Putterman and Kroszner). Firms choose amethod of vertical coordination based on a comparisonof the net effect on transaction costs.

Asset SpecificityTransaction costs and the choice of vertical coordina-tion method depend on characteristics of the transac-tion. The TCE paradigm places an emphasis on thedegree of asset specificity in an exchange relationship,or the degree to which assets are specifically designedor located for a particular use or user. Once specificassets are locked into a relationship, they can be rede-ployed only at a great loss in productive value, whichresults in sizable quasi-rents.11 Because relationship-specific assets have much lower value in other uses byother users, they reduce the number of potential trad-ing partners. Hence, the investing party will be subjectto holdup, or exploitative, self-interested actions (alsoreferred to as opportunistic behavior) by the otherparty to appropriate the quasi-rents and generateabove-normal returns.

A decline in the number of buyers and sellers also canlead to small-number bargaining problems (Frank andHenderson). Coupled with specialized assets, small-

10Other explanations for alternative methods of vertical coordina-tion include (i) to increase profits in noncompetitive markets(Royer), (ii) to price discriminate and create barriers to entry(Stigler), (iii) to shift price and production risk to firms that canmanage risk more efficiently (Knoeber and Thurman; Martin,1997), (iv) to ensure input supplies (Carlton), and (v) to sustain astrategic competitive advantage (Westgren).

11The difference between the value of an asset in its best use andin its next-best use is referred to as “quasi-rent.”

number bargaining increases the potential for oppor-tunistic behavior because alternative exchanges cannotbe easily arranged. Asset specificity and small-numberconditions, however, create value in enduringexchange relationships.

Types of asset specificity include physical, site, andtemporal. Physical specificity is derived from the phys-ical features of an asset. For example, special-purposeequipment and specialized investments required forscale economies are physical specificities (Williamson,1979). The buyer of the finished product can appropri-ate quasi-rents that are generated from these invest-ments by offering a price lower than the originallyagreed-upon price. As long as the offer price exceedsthe value of the asset in its next-best use, the producerhas few options but to accept the offer. Site specificityoccurs when buyers and sellers locate facilities close toeach other to reduce transportation costs. Becauserelocation costs are high, site specificities lock partiesinto an exchange relationship for the useful life of theasset. For example, a producer may be decidingwhether to locate a farm operation close to a processor.The quasi-rents generated are the difference betweenthe negotiated price and the price available from thenext-closest processor, less transportation costs. Onceagain, the buyer can appropriate these rents by offeringa lower price than originally agreed. Temporal speci-ficity refers to the timing of delivery and its effect onproduct value. For example, temporal specificities mayarise because a producer of a perishable product has

difficulties finding alternative processors on shortnotice. The buyer may appropriate the quasi-rents bythreatening to delay acceptance of the product.Temporal specificities are less severe in “thick” mar-kets where large numbers of buyers and sellersenhance competition (Pirrong).

A party that invests in specific assets will choose alter-natives to spot-market coordination that provide safe-guards against opportunistic behavior and reduceresource expenditures on haggling and bargaining overprice. In a contract relationship, one party may agreeon investments to be made and quantities to be deliv-ered. The other party may agree on prices to pay basedon various contingencies that arise over time. Privateactions for breach of contract and public laws protect-ing contract parties help enforce contracts and protectcontract parties. As assets become more specialized, theinvesting party will expend more resources to specifymore contract contingencies because there are greaterbenefits from “holding up” the asset owner. In addition,parties may not always honor contracts, and theseactions may result in costs associated with investigatingcontract violations and court litigation. Consequently,vertical integration, which eliminates the exchangerelationship, becomes more prevalent as asset specifici-ty and the potential benefits to reneging on contractsincrease (Klein, Crawford, and Alchian) (see box onrelationship between asset specificity, transaction costs,and methods of vertical coordination).

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 7

Methods of vertical coordination are chosen to min-imize transaction costs. In the figure, k is the level ofasset specificity, M(k) is transaction costs associatedwith spot-market coordination, C(k) is costs associ-ated with contracting, and V(k) is costs associatedwith vertical integration. Each method of verticalcoordination is expressed as a function of assetspecificity. For low levels of asset specificity (k<k1),

transaction costs of spot-market coordination areminimal. As asset specificity increases to intermedi-ate levels (k1<k<k2), contract arrangements mini-

mize transaction costs. For transactions character-ized by high levels of asset specificity (k>k2), verti-

cal integration becomes the cost-minimizing methodof vertical coordination.

Transaction costs

0 k1 k2Assetspecificity

M(k) C(k)V(k)

Relationship between asset specificity, transaction costs, and methods of vertical coordination

Source: Williamson, 1991.

UncertaintyIn addition to varying by asset specificity, transactionsmay vary by degree of uncertainty, which arises fromthree basic sources (Williamson, 1996; 1985;Koopmans). First, uncertainties arise due to technolog-ical changes, unpredictable changes in consumer pref-erences, and random acts of nature. Second, uncertain-ties may arise from lack of timely communication orthe inability to determine simultaneous decisions andplans made by others, such as investment decisionsand purchasing plans of consumers. Third, uncertain-ties may arise due to strategic behavior regardingnondisclosure, disguise, or distortions of information(also referred to as “behavioral uncertainty”).

Greater uncertainty, coupled with asset specificity,increases the importance of organizing relationship-specific transactions in ways that avoid costly hagglingby adapting to market conditions. Bounded rationality,which makes it impossible, or very costly, to specifyall possible contingencies or appropriate adaptations inadvance, makes it necessary for parties to adapt or“work things out” (Williamson, 1985).12 That is,bounded rationality makes it costly to write a completecontract. Therefore, contracting parties are susceptibleto opportunistic behavior as contracts are renegotiatedin response to changing market conditions. Monitoringof performance and verification of breach of contractalso become more difficult as uncertainty increases. Incases where the degree of asset specificity is low,uncertainty is expected to have no effect on verticalcoordination because little value is placed in an ongo-ing relationship. The need to adapt to market condi-tions is lessened because alternative exchanges can bequickly arranged in light of unexpected events.

Given investments in specific assets, parties mayrespond to increasing uncertainty in two ways. First,parties may engage in contracts that may become morerelational in nature. That is, instead of laying out spe-cific details, contracts will specify the process throughwhich future terms of trade will be determined.Contract terms will be specified that provide incentivesfor rent-increasing adaptations to changing marketconditions, while limiting opportunism and the needfor costly arbitration (Masten, 1996). For example,instead of negotiating a specific contract price, parties

may agree to adjust the contract price based on a mar-ket-determined index. This arrangement reduces incen-tives to gain advantage by obtaining special informa-tion on future prices. In addition, if a negotiated con-tract price differs substantially from the market price,the disadvantaged party may be reluctant to continuethe agreement. The party may then engage in subtle,costly behavior, such as requiring strict adherence tothe rules, purposefully delaying deliveries, or interpret-ing the contract literally.13 Market-based contractprices, which narrow the gap between contract priceand market price, reduce these types of inefficientbehavior.

Contracting parties may also respond to increasinguncertainty by progressing from marketing contracts tovertical integration in the spectrum of control (fig. 1)(Frank and Henderson). When the level of uncertaintybecomes particularly high, ceteris paribus, verticalintegration is expected to become more prevalent.14

While contracting relies on the ability to anticipatepotential problems, vertical integration requires nocontract revisions and serves to facilitate adaptation tochanging circumstances as they unfold (Masten, 1996).Vertically integrated firms can more readily adapt tochanging conditions because opportunistic behavior isless likely within such a firm, disputes can be settledby top management, convergent expectations can facil-itate planning, and access to relevant information canreduce haggling (Dietrich).

Measurement CostsTransaction costs can also result from informationasymmetry among trading partners regarding productvalue and producer effort. Some important attributes ofa traded good may not be directly observable to thebuyer, seller, or both. Consequently, parties may bene-fit by engaging in costly searching and sorting toobtain information about the attribute of the good. Forexample, a producer may sell low- and high-qualityproducts at the same price, and the purchaser mayexpend resources to search for undervalued goods andreject those that are overpriced. Contracts that includecompensation for efficient producer performance mayrequire parties to measure appropriate indicators ofproduction efficiency. Social waste occurs when mea-

8 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

12Bounded rationality refers to limits on people’s knowledge,foresight, skill, time, and ability to articulate knowledge in a waythat can be understood by others.

13According to Goldberg and Erickson, literal interpretation isoften referred to as “working to the rules.”14 The term “ceteris paribus” is used in economics to indicate thatall variables except those specified are assumed not to change.

surement by buyers to determine the true value of agood simply redistributes wealth from sellers to buyers(Leffler, Rucker, and Munn). Expanding time andeffort in haggling and delaying agreements to influ-ence the terms of exchange is also inefficient(Milgrom and Roberts).

Vertical coordination arrangements can reduce transac-tion costs related to inefficient measuring and sorting,and leave more gains from exchange to be distributedamong contracting parties. If measuring output qualitywere cost free, spot-market production would provide

effective price incentives for performance. On theother hand, if measuring output quality were costly,parties would be encouraged to shirk, cheat, andengage in other types of opportunistic behavior. Tolimit such behavior, markets may be reorganized sothat accurate measurements require less effort and cost(Milgrom and Roberts). For example, in contracts inwhich output is difficult to measure and inputs serve asan adequate proxy for output value, buyers may enterinto contract arrangements that enable them to monitorproduction inputs.

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 9

The Viability of Spot-MarketTransactions in the Poultry,

Egg, and Pork Industries

This report examines the role of contracting or verticalintegration in reducing transaction costs in the poultry,egg, and pork industries and relates transaction charac-teristics to vertical coordination methods over periodsof significant change in vertical coordination. Assetspecificity and measurement costs are examined aspossible sources of transaction costs that reduce theefficiency of spot-market trading.15

Physical Specificities and Small-Number ConditionsFirms that specialize in certain types of output or dif-ferentiated products, or those with highly technicalproduction processes, may require investments in spe-cialized assets.16 Investments in assets that have fewalternative uses, coupled with fewer outlets or inputsuppliers, determine the relationship-specific nature ofthe transaction. In the broiler, turkey, egg, and hogmarkets, investments in relationship-specific assetssuggest a role for contracts and vertical integration,particularly in geographic regions undergoing industryexpansion.

Broilers and turkeysFollowing World War II, the poultry industry experi-enced rapid changes in technology, which inducedmore specialized production facilities, processingplants, and breeding stock designed for the productionof chickens for meat or for eggs. In the broiler indus-try, most growers invested heavily in chicken housing.As noted by Breimyer, “As a broiler house cannot beconverted readily to uses other than poultry, the finan-cial obligation imposes a tight restraint on a grower’sfreedom of action.” Similarly, the U.S. Department of

Agriculture, Packers and Stockyards Administrationfound that “limited alternative uses for existing invest-ments in broiler enterprises and limited off-farmemployment, principally in the South, have kept manyfarmers in broiler production in spite of excess capaci-ty and generally low returns.”

Investments in specialized broiler production and pro-cessing assets affected the relationship-specific natureof transactions by limiting alternative uses and usersof such investments. While broiler houses may be spe-cific in a production sense (that is, specialized tobroiler production), they may not represent relation-ship-specific investments unless there also are fewbuyers.17 Scale economies associated with specializedtechnology adoption resulted in fewer and largerfirms, especially in expanding regions of the South.18

According to Reimund, Martin, and Moore, techno-logical innovations could be adapted more readily inareas with relatively little output because existing cap-ital investments and production methods had lessinfluence in these areas.

The extent of technology adoption and associated scaleeconomies in the South is indicated by changes in thesize and number of U.S. broiler firms as the share ofproduction in the South increased (fig. 5) (app. B). In1964, 201 processing firms operated 320 plants thatslaughtered 6.7 billion pounds of broilers. By 1984,134 firms operated 238 plants that slaughtered 17.8billion pounds. Larger plants became more prevalent inthe South as broiler slaughter capacity became moreconcentrated in this region. In 1984, pounds slaugh-tered per plant in the South averaged 99 millionpounds, compared with the U.S. average of 73 millionpounds. On the production side, from 1959 to 1982,the number of farms selling broilers fell from 42,185to 30,100. Over the same period, the share of U.S.broiler sales by large broiler farms (100,000 or morebirds) increased from 29 to 89 percent (Lasley et al.).

Similarly, in the turkey industry, investments in spe-cialized assets had a significant effect, especially in theSouth. As confinement and semi-confinement produc-tion operations replaced range rearing, increasinglyspecialized production stages created demand for

10 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

15Efficiency of alternative organizational arrangements is typical-ly related to observable characteristics of the transaction becausetransaction costs are difficult to measure directly (Joskow).Hence, transaction-cost economics requires detailed informationon organizational form and attributes of transactions (Williamsonand Masten). 16Proxies for physical asset specificity used in the empirical liter-ature include fixed assets to shipments, fixed assets to number ofemployees, advertising (representing intangible assets, such asbrand name and reputation) to shipments, expenditures onresearch, ratio of research and development expenditures to sales,and the difference between acquisition price and salvage value(Mahoney; Frank and Henderson; MacDonald; Shelanski andKlein; Sporleder; Caves and Bradburd).

17I thank Jill Hobbs for emphasizing this point.18In addition to the relationship-specific nature of these invest-ments, larger operations are associated with larger quasi-rentsand, hence, greater benefits from holdup by the other party(Pirrong).

feeds, equipment, and other products and servicesdesigned for each stage (Rogers, 1979; Small). By themid-1980s, large and specialized turkey processingplants replaced plants that slaughtered both broilersand turkeys during the broiler slack season, a commonpractice in the 1960s (Gallimore and Irvin; Lasley,Henson, and Jones). Regional variations in the adop-tion of new, specialized production technology werereflected by the rapid decline in number and growth insize of turkey production and processing operations(figs. 6, 7, and 8).

Table eggsIn the table egg industry, specialized productionreplaced the general farm flock due to improvementsin breeding, feeding, disease control, management, andmarketing. For example, as in the broiler industry, pul-let growing in the table egg industry was dominated byspecialized, large-scale operations using mass-produc-tion techniques (Roy, 1972). Technological innovationsin the 1950s and 1960s, including automated eggwashers, blood spot detectors, and automated egg car-toners, encouraged large-scale production and mecha-nized handling and distribution of a large number of

eggs.19 Large-scale enterprises could implement new,highly mechanized technology more advantageouslythan smaller operations, which encouraged further

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 11

19Modern “in-line” operations that mechanically gather, clean,grade, and package the eggs require large capital investments forenvironmentally controlled housing and computer technology tocontrol egg flow, quality control, and packaging. Typically, eggson commercial egg-laying farms are never touched until they arehandled by the food service operator or consumer (United EggProducers).

Figure 5

Geographic patterns of poultry and egg production

Total U.S. production

Source: Lasley.

Broilers Turkeys Eggs

1950 70 80 1950 70 80 1950 70 800

20

40

60

80

100

South

West

North Central

Northeast

Figure 6

Decrease in number of turkey farms (1959-78) andprocessing plants (1962-81)

Percent

Source: Lasley, Henson, and Jones.

Northeast EastNorth

Central

WestNorth

Central

SouthAtlantic

SouthCentral

West UnitedStates

-120

-100

-80

-60

-40

-20

0

Farms Processing plants

Figure 7

Increase in average number of turkeys per farm,1959-78

Percent (thousands)

Source: Lasley, Henson, and Jones.

Northeast EastNorth

Central

WestNorth

Central

SouthAtlantic

SouthCentral

West0

2

4

6

8

10

12

14

growth in specialized egg production units (NationalCommission on Food Marketing; Strausberg).

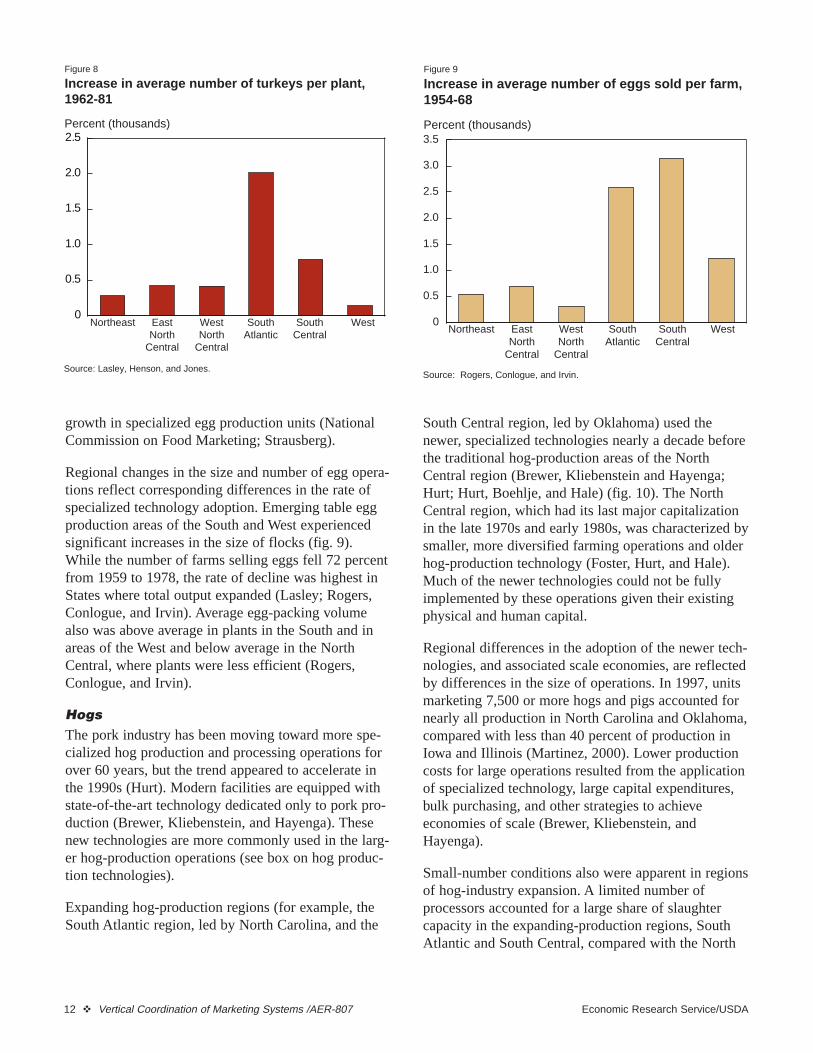

Regional changes in the size and number of egg opera-tions reflect corresponding differences in the rate ofspecialized technology adoption. Emerging table eggproduction areas of the South and West experiencedsignificant increases in the size of flocks (fig. 9).While the number of farms selling eggs fell 72 percentfrom 1959 to 1978, the rate of decline was highest inStates where total output expanded (Lasley; Rogers,Conlogue, and Irvin). Average egg-packing volumealso was above average in plants in the South and inareas of the West and below average in the NorthCentral, where plants were less efficient (Rogers,Conlogue, and Irvin).

HogsThe pork industry has been moving toward more spe-cialized hog production and processing operations forover 60 years, but the trend appeared to accelerate inthe 1990s (Hurt). Modern facilities are equipped withstate-of-the-art technology dedicated only to pork pro-duction (Brewer, Kliebenstein, and Hayenga). Thesenew technologies are more commonly used in the larg-er hog-production operations (see box on hog produc-tion technologies).

Expanding hog-production regions (for example, theSouth Atlantic region, led by North Carolina, and the

South Central region, led by Oklahoma) used thenewer, specialized technologies nearly a decade beforethe traditional hog-production areas of the NorthCentral region (Brewer, Kliebenstein and Hayenga;Hurt; Hurt, Boehlje, and Hale) (fig. 10). The NorthCentral region, which had its last major capitalizationin the late 1970s and early 1980s, was characterized bysmaller, more diversified farming operations and olderhog-production technology (Foster, Hurt, and Hale).Much of the newer technologies could not be fullyimplemented by these operations given their existingphysical and human capital.

Regional differences in the adoption of the newer tech-nologies, and associated scale economies, are reflectedby differences in the size of operations. In 1997, unitsmarketing 7,500 or more hogs and pigs accounted fornearly all production in North Carolina and Oklahoma,compared with less than 40 percent of production inIowa and Illinois (Martinez, 2000). Lower productioncosts for large operations resulted from the applicationof specialized technology, large capital expenditures,bulk purchasing, and other strategies to achieveeconomies of scale (Brewer, Kliebenstein, andHayenga).

Small-number conditions also were apparent in regionsof hog-industry expansion. A limited number ofprocessors accounted for a large share of slaughtercapacity in the expanding-production regions, SouthAtlantic and South Central, compared with the North

12 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

Figure 8

Increase in average number of turkeys per plant,1962-81

Percent (thousands)

Source: Lasley, Henson, and Jones.

Northeast EastNorth

Central

WestNorth

Central

SouthAtlantic

SouthCentral

West0

0.5

1.0

1.5

2.0

2.5

Figure 9

Increase in average number of eggs sold per farm,1954-68

Percent (thousands)

Source: Rogers, Conlogue, and Irvin.

Northeast EastNorth

Central

WestNorth

Central

SouthAtlantic

SouthCentral

West0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 13

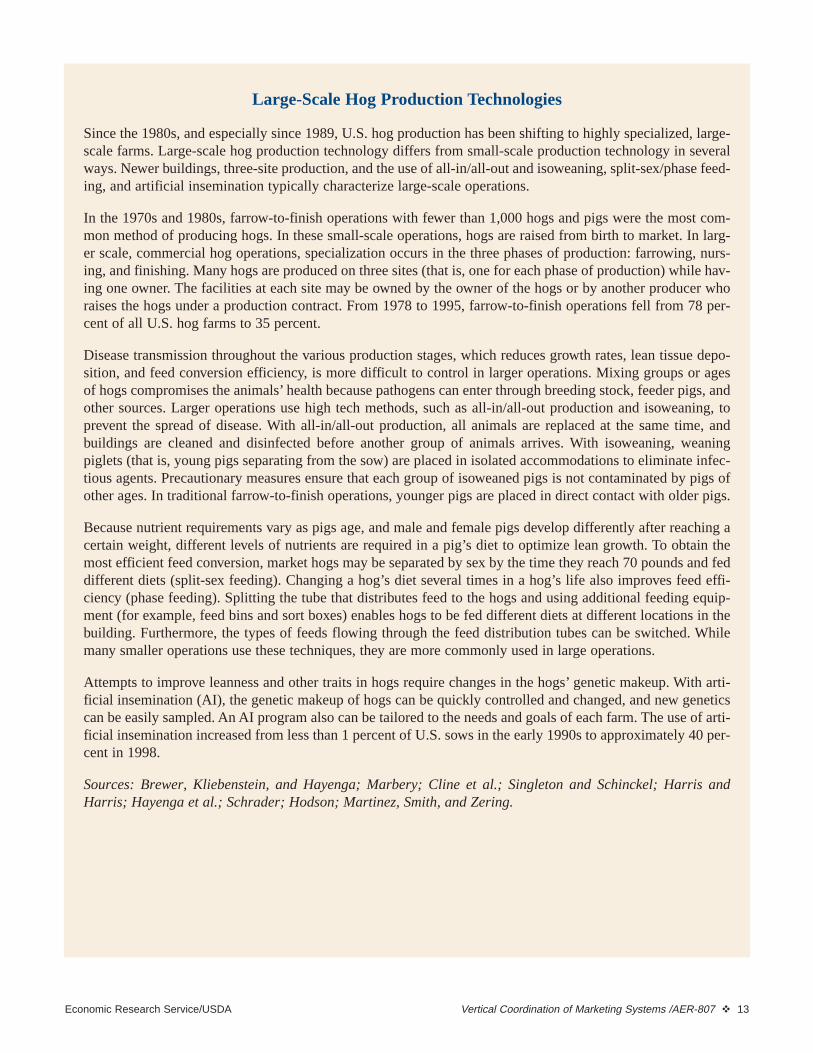

Large-Scale Hog Production Technologies

Since the 1980s, and especially since 1989, U.S. hog production has been shifting to highly specialized, large-scale farms. Large-scale hog production technology differs from small-scale production technology in severalways. Newer buildings, three-site production, and the use of all-in/all-out and isoweaning, split-sex/phase feed-ing, and artificial insemination typically characterize large-scale operations.

In the 1970s and 1980s, farrow-to-finish operations with fewer than 1,000 hogs and pigs were the most com-mon method of producing hogs. In these small-scale operations, hogs are raised from birth to market. In larg-er scale, commercial hog operations, specialization occurs in the three phases of production: farrowing, nurs-ing, and finishing. Many hogs are produced on three sites (that is, one for each phase of production) while hav-ing one owner. The facilities at each site may be owned by the owner of the hogs or by another producer whoraises the hogs under a production contract. From 1978 to 1995, farrow-to-finish operations fell from 78 per-cent of all U.S. hog farms to 35 percent.

Disease transmission throughout the various production stages, which reduces growth rates, lean tissue depo-sition, and feed conversion efficiency, is more difficult to control in larger operations. Mixing groups or agesof hogs compromises the animals’ health because pathogens can enter through breeding stock, feeder pigs, andother sources. Larger operations use high tech methods, such as all-in/all-out production and isoweaning, toprevent the spread of disease. With all-in/all-out production, all animals are replaced at the same time, andbuildings are cleaned and disinfected before another group of animals arrives. With isoweaning, weaningpiglets (that is, young pigs separating from the sow) are placed in isolated accommodations to eliminate infec-tious agents. Precautionary measures ensure that each group of isoweaned pigs is not contaminated by pigs ofother ages. In traditional farrow-to-finish operations, younger pigs are placed in direct contact with older pigs.

Because nutrient requirements vary as pigs age, and male and female pigs develop differently after reaching acertain weight, different levels of nutrients are required in a pig’s diet to optimize lean growth. To obtain themost efficient feed conversion, market hogs may be separated by sex by the time they reach 70 pounds and feddifferent diets (split-sex feeding). Changing a hog’s diet several times in a hog’s life also improves feed effi-ciency (phase feeding). Splitting the tube that distributes feed to the hogs and using additional feeding equip-ment (for example, feed bins and sort boxes) enables hogs to be fed different diets at different locations in thebuilding. Furthermore, the types of feeds flowing through the feed distribution tubes can be switched. Whilemany smaller operations use these techniques, they are more commonly used in large operations.

Attempts to improve leanness and other traits in hogs require changes in the hogs’ genetic makeup. With arti-ficial insemination (AI), the genetic makeup of hogs can be quickly controlled and changed, and new geneticscan be easily sampled. An AI program also can be tailored to the needs and goals of each farm. The use of arti-ficial insemination increased from less than 1 percent of U.S. sows in the early 1990s to approximately 40 per-cent in 1998.

Sources: Brewer, Kliebenstein, and Hayenga; Marbery; Cline et al.; Singleton and Schinckel; Harris andHarris; Hayenga et al.; Schrader; Hodson; Martinez, Smith, and Zering.

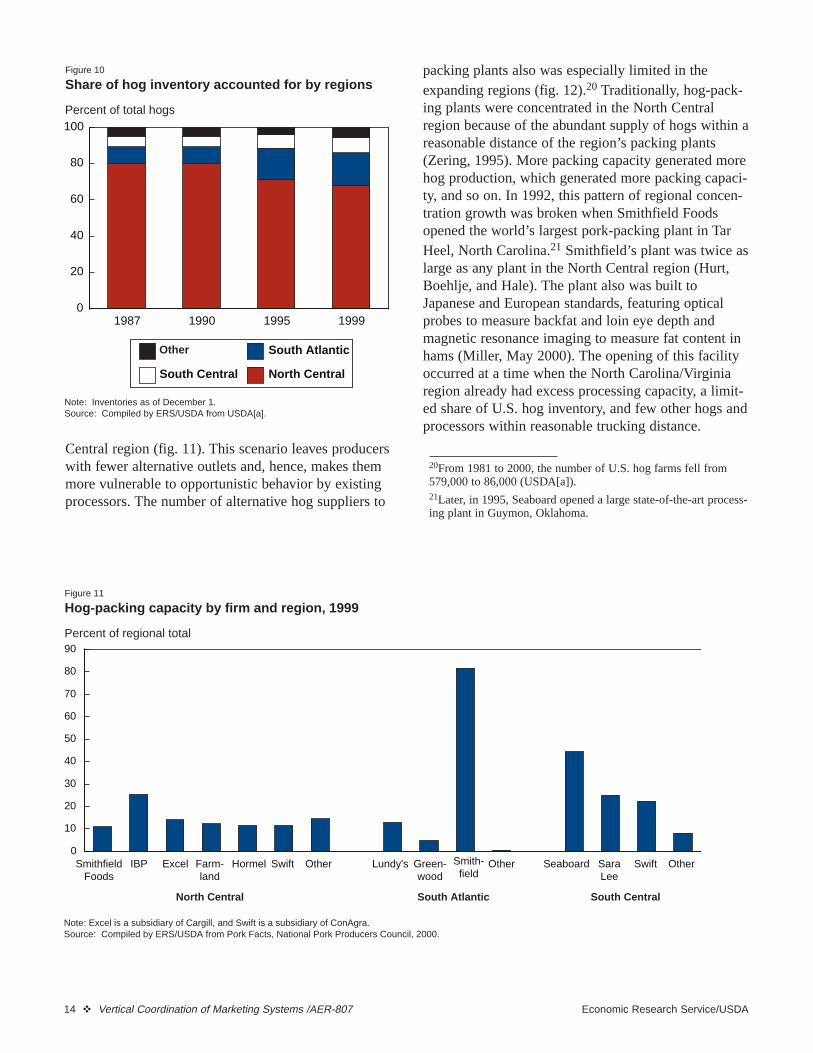

Central region (fig. 11). This scenario leaves producerswith fewer alternative outlets and, hence, makes themmore vulnerable to opportunistic behavior by existingprocessors. The number of alternative hog suppliers to

packing plants also was especially limited in theexpanding regions (fig. 12).20 Traditionally, hog-pack-ing plants were concentrated in the North Centralregion because of the abundant supply of hogs within areasonable distance of the region’s packing plants(Zering, 1995). More packing capacity generated morehog production, which generated more packing capaci-ty, and so on. In 1992, this pattern of regional concen-tration growth was broken when Smithfield Foodsopened the world’s largest pork-packing plant in TarHeel, North Carolina.21 Smithfield’s plant was twice aslarge as any plant in the North Central region (Hurt,Boehlje, and Hale). The plant also was built toJapanese and European standards, featuring opticalprobes to measure backfat and loin eye depth andmagnetic resonance imaging to measure fat content inhams (Miller, May 2000). The opening of this facilityoccurred at a time when the North Carolina/Virginiaregion already had excess processing capacity, a limit-ed share of U.S. hog inventory, and few other hogs andprocessors within reasonable trucking distance.

14 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

Figure 10

Share of hog inventory accounted for by regions

Percent of total hogs

Note: Inventories as of December 1.Source: Compiled by ERS/USDA from USDA[a].

1987 1990 1995 19990

20

40

60

80

100

North Central

South Atlantic

South Central

Other

Figure 11

Hog-packing capacity by firm and region, 1999

Percent of regional total

Note: Excel is a subsidiary of Cargill, and Swift is a subsidiary of ConAgra. Source: Compiled by ERS/USDA from Pork Facts, National Pork Producers Council, 2000.

SmithfieldFoods

IBP Excel Farm-land

Hormel Swift Other Lundy's Green-wood

Other Seaboard SaraLee

Swift Other0

10

20

30

40

50

60

70

80

90

Smith-field

North Central South Atlantic South Central

20From 1981 to 2000, the number of U.S. hog farms fell from579,000 to 86,000 (USDA[a]).21Later, in 1995, Seaboard opened a large state-of-the-art process-ing plant in Guymon, Oklahoma.

Changing methods of vertical coordinationin regions of industry expansion22

In light of investments made in new specialized assetsand small-number conditions in expanding poultry,egg, and hog markets, transaction-cost considerationssuggest that the spot market was an inefficient meansof vertical coordination in regions of industry expan-sion. At the same time, contracting in the broiler andturkey industries became more prevalent in the South.Similarly, table egg contracting increased in the Southas well (table 1). In the late 1950s, egg productioncontracts existed mostly in the Southern States, wherecontracting and large-scale flocks were commonbecause of the region’s sizeable broiler industry. Bythe mid-1960s, egg production contracts had spread tothe West, where contract systems and large, verticallyintegrated egg complexes that require huge invest-ments developed together.

In the pork industry, expanding production in nontradi-tional regions also was accompanied by marketingcontracts and packer-owned hogs produced under pro-duction contracts. A 1994 survey of large hog produc-ers found that large producers in the North Centralregion marketed 26 percent of hogs through the spotmarket and 63 percent using marketing contracts. In

areas outside the North Central region, the differencewas greater; 14 percent of hogs were sold through spotmarkets, and 81 percent were sold through marketingcontracts. For example, Smithfield Foods, which hasmost of its slaughter plant capacity in the SouthAtlantic region, obtains 50 percent of its slaughterrequirements from company-owned hogs, and an addi-tional 14 percent are obtained from marketing con-tracts (Smithfield Foods, 10K, filed July 28, 2000).Seaboard Farms has most of its slaughter capacity inthe South Central region and owns about 75 percent ofthe hogs that it slaughters (Marbery). On the otherhand, in 1999, IBP, which has slaughter plants in theNorth Central region and is the Nation’s second-largestpork processor, did not own sows (Freese). The com-pany’s main supply of hogs is purchased daily by IBPbuyers, a few days before processing (IBP, 10K, filedMarch 23, 2000).23

Investments in specialized genetics for producing porkwith unique quality attributes also have increased. Forexample, in the early 1990s, Smithfield Foods intro-duced Lean Generation Pork in response to diet andhealth concerns related to fat content of foods. LeanGeneration Pork is produced from National PigDevelopment (NPD) hogs, the leanest hogs in U.S.large-scale production. In this case, specialized genet-ics represents a relationship-specific asset, regardlessof small-number conditions, because it is tied to a spe-cific brand. Smithfield obtained uniform genetics forthe pork through a partnership with a leading hog pro-ducer, Carroll Foods, involving long-term marketingagreements and joint ownership of hog-productionoperations.

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 15

Figure 12

Number of U.S. hog and pig operations, December 1, 1999

Operations (thousands)

Source: Compiled by ERS/USDA from USDA[a].

North Central South Atlantic South Central0

10

20

30

40

50

60

70

22In this section, information on regional differences in methodsof vertical coordination is obtained from Roy (1963; 1972);Gallimore; Rogers, Conlogue, and Irvin.; Rogers (1979); andLawrence et al.

23 In each of the next 5 years, IBP is committed to purchasingabout 21 percent of its annual hog production capacity, usingmarketing contracts with payments based on market-derivedprices (IBP, 8-K, filed November 7, 2000).

Table 1—Table egg production and contracting inthe South

State Change in Production underproduction, 1959-65 contract, 1964

PercentAlabama 71 45Georgia 72 33Arkansas 159 50Source: Gallimore and Vertrees.

Site and Temporal Specificities24

Limited procurement distances also created relation-ship-specific transactions in the poultry and egg indus-tries. Parties can move chickens only about 30 milesand still remain profitable because live birds loseweight if transported over lengthy distances.Consequently, as advances in distribution technologymade it more efficient to transport processed poultryproducts, site specificities were created when largeprocessing plants moved closer to the flocks.Production density was more critical than optimal pro-cessing plant size in determining the competitive posi-tion of processors. As processors sought high-produc-tion density to reduce the span of their broiler supplysources, many contract growers had essentially noalternative trading partners. Vertically integrated opera-tions, in which the integrator owns both the productionand processing facilities, were more common withlarger-than-average broiler houses located closer to theprocessing plants.

Timing factors create temporal specificities in the poul-try, egg, and pork markets.25 Poultry and eggs are con-sidered to be perishable products. Poultry requires awithdrawal period, whereby growers withdraw feedbefore the birds are processed to limit intestinal con-tents and protect against fecal contamination of poultrycarcasses. Processing delays can result in deteriorationof the birds’ intestines, which increases susceptibility torupture and contamination. Furthermore, the pressurerequired to remove the crop in older birds can rupturethe crop, spill its contents, and lead to salmonella cont-amination, which suggests that poultry must be sent tothe processor within a narrow age range.26 In addition,large investments by poultry processing plants in thelate 1950s, in response to mandatory inspectionrequirements, increased the importance of timely birdsupplies. Table eggs undergo weight loss and albumendeterioration immediately after lay, so eggs must reachthe supermarkets within a few days of leaving the lay-ing house to ensure a fresh and safe product.

In the pork industry, timely delivery of hogs to theprocessing plant affects processing costs. Modern porkprocessing plants are designed to operate efficiently ata particular utilization level, and operating costs riserapidly at other levels of production.

Measurement CostsWhile consumers gain by understanding the value of agood, measuring the good at the point of sale may becostly to the consumer. Some meat attributes, such astaste and product safety, are costly to verify before themeat is consumed. In addition, consumers incur a costsorting through heterogeneous packages of equal priceto affect the distribution of gains but do not alter theoverall quality of the products. As household leisuretime becomes more valuable, such sorting becomeseven more costly.

Many product attributes that can influence consumers’eating experiences depend on the characteristics ofanimals supplied for processing. These characteristicsmay be difficult to measure when the animals are sold,but production inputs, such as genetics, feed and nutri-tion, and management practices, may affect certainproduct attributes. For example, the pale, soft, exuda-tive (PSE) condition in hogs, which is associated withtough, dry, and lean pork, is difficult to measure whenhogs are sold but is highly heritable (K.E. Smith).Measuring pathogen content also may be difficult.Furthermore, it is costly to measure and sort animalsof varying size, shapes, and quality within and acrossflocks and herds.

Contracts and vertical integration, together with brand-ing of retail meat products, can reduce total measure-ment costs within the food system. Branded productstend to reduce consumer concerns about purchasing adeficient product. Such a product could tarnish thebrand name and saddle the producer with potentiallycritical losses. For this reason, the quality of brandedproducts is expected to be less variable. Quality assur-ances inherent in branded products are especiallyimportant for those product attributes that are difficultfor the consumer to measure at the point of purchase.Instead of consumers incurring the cost of attributemeasurement at the time of purchase, processors canmeasure product characteristics more cheaply furtherupstream, or earlier in the process.27 For those quality

16 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

24This section is based on information contained in Henry,Chappell, and Seagraves; Rogers (1976); Marion and Arthur; Roy(1972); Pork ’99 Staff; Byrd; Martinez (1999); Van Leusen andCeton; and United Egg Producers. 25Rapid structural changes in the production of poultry, eggs,and pork that resulted in thin markets, particularly in regions ofindustry expansion, may have increased the severity of temporalspecificities.26The crop stores undigested feed and is removed at processing.

27“Upstream” refers to stages of the marketing system closest tothe beginning of the production process. “Downstream” refers tothose stages closest to the consumer. Value is added as productmoves downstream through successive stages to consumers.

attributes of a live animal or carcass that are costly tomeasure, processors can reduce measurement costs bycontrolling farm inputs through contracts or verticalintegration.28 Substituting measurement by consumerswith earlier, less costly measurement further upstreamreduces total measurement costs in the food system,leaving more gains to be distributed among buyers andsellers.29 As sellers bear some of the cost of buyer pre-sale measurement, sellers would also benefit (Barzel).

Branding has been an integral part of the poultryindustry for over 20 years. For example, Tyson Foods,the Nation’s leading broiler producer, maintains astrong national brand. Tyson’s broiler contracts specifythat growers use only company-supplied birds, whichcome from genetic stock supplied by Tyson’s breedingstock company, Cobb-Vantress. Tyson invests in breed-ing stock research and development to produce birdswith the most desirable natural characteristics. In theturkey industry, Jennie-O Foods, the world’s leadingturkey processor, emphasizes branded, packaged con-sumer items, such as the company’s rotisserie turkey.The company owns turkey production facilities andsupplements output from these operations with grower

contracts that specify the breed to be used, in additionto weight and pricing formula (Hormel Foods, 10-K,January 23, 1998).

Leading egg companies also emphasize branding. Cal-Maine Foods, the Nation’s largest egg company, pro-duces branded egg products for health-conscious con-sumers under the Egg·Land’s Best and Farmhouselabels. Egg·Land’s Best eggs (with “EB” stamped oneach egg) come from hens that are fed all-natural, veg-etarian diets, with no animal by-products, and containless saturated fats than regular eggs. Farmhouse eggsare produced from free-range hens that feed on naturalgrains. Attributes of these branded products, whichdepend on special feeds and production practices,would be difficult to measure by consumers andprocessors in a spot market.

As in the poultry industry, contracts and vertical inte-gration in the pork industry may lower measurementcosts and facilitate branding programs for fresh pork(chops, tenderloins, ribs, and roasts). Companies thathave recently introduced branded fresh pork productsinclude Hormel Foods and Seaboard. Hormel obtains50 percent of its hog supplies from 5- to 10-year mar-keting contracts (Egerstrom). These contracts specifythat producers use Hormel-approved facilities andgenetics that can produce lean, uniform-sorted hogs.Seaboard controls genetics and nutrition for its PrairieFresh label through integrated, environmentally con-trolled operations. The Pig Improvement Co. providesthe genetic base for producing uniform products withfewer PSE-related meat attributes, resulting in lessmoisture loss and juicier meat after cooking (Marbery,June 5, 2000).

Economic Research Service/USDA Vertical Coordination of Marketing Systems /AER-807 � 17

28Furthermore, tournament production contracts used in the broil-er industry also reduce measurement costs by basing grower pay-ments on a grower’s performance relative to other growers (atournament). This feature reduces measurement costs because rel-ative performance is cheaper to measure than absolute perfor-mance associated with weight and other factors, such as feed effi-ciency and mortality rates (Knoeber).29The opposite is true for consumer warranties. According toBarzel, warranty contracts on finished products, such as house-hold appliances and other durables, reduce measuring costsbecause it is cheaper for consumers to determine output quality asthe product is used than for manufacturers to test every product.

Marketing Contracts,Production Contracts, or

Vertical Integration?

While characteristics of poultry, egg, and pork markettransactions and associated transaction costs suggestthat spot-market trading will be inefficient, the signifi-cance of alternative vertical coordination arrangementsvaries across industries. Vertical integration of the pro-duction and processing stages is more prevalent in theturkey and egg industries, while marketing contractsare more common in the pork industry. Reasons forthese differences are explored in the following section.

Uncertainty and Vertical Acquisitions

In markets with significant asset specificity, increasinglevels of uncertainty are expected to lead to methodsof coordination that transfer more control over func-tions to the integrator. During periods of extensivechanges in structure and vertical coordination in thepoultry and egg industries, uncertainty originated froma variety of sources.30 Disease and heavy mortalityrates were found among birds (Black). Significanttechnological advances were made within a short peri-od of time (technological uncertainty) (Tobin andArthur; Martinez, 1999).31 Poor coordination of salesbetween producers and buyers led to wide marketswings. Sharp industry losses in 1959 and 1961, char-acterized by overproduction and depressed live-bird

prices, led many hatching-egg producers, hatcheries,and feed companies to exit the broiler and turkeyindustries. Extensive changes in competitive condi-tions, mergers, and acquisitions at all stages in the1960s (National Commission on Food Marketing) andrapid inflation fueled by OPEC (Organization of thePetroleum Exporting Countries) in the early 1970s cre-ated further uncertainties.

In the late 1950s and early 1960s, uncertainty in thebroiler industry led management centers to becomeinvolved in stages further downstream in the verticalchain (Tobin and Arthur). At the time, rapidly increas-ing broiler sales complicated coordination of verticalstages. Advances in technology at all stages led toexcess production and depressed prices. Greaterdemand for research and new product developmentincreased demand for capital through periods of erraticprice movement. Retailers who offered chicken breastsand thighs at one price and drumsticks at another com-plicated inventory control (Strausberg). Lack of com-munication with buyers of dressed broilers andoveremphasis on broiler shortages and surplus led tothe demise of open markets further upstream. Feedcompanies began to deal directly with wholesalers orretailers by acquiring or merging with processors andby building their own processing facilities. Conse-quently, production-related decisionmaking wasenhanced by the retailers’ superior knowledge of con-sumer preferences and buying habits.

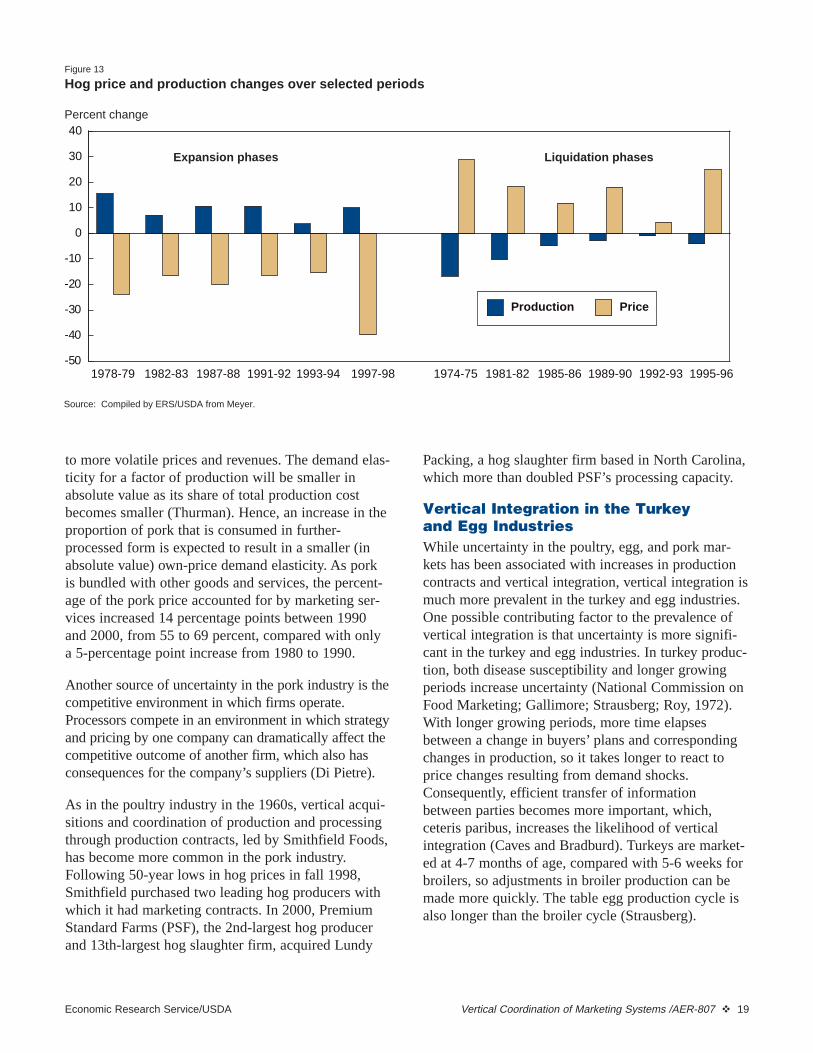

In the pork industry, sources of uncertainty includegovernment regulations (for example, environmentalregulations, family farm ordinances) and hog prices(table 2). In recent years, hog prices have becomemore sensitive to changes in hog production (fig. 13).Hog demand has become more inelastic, which has led

18 � Vertical Coordination of Marketing Systems /AER-807 Economic Research Service/USDA

30Proxies for technological uncertainty in the empirical literatureinclude years to technological obsolescence, frequency of changesin product specification, and probability of technologicalimprovements (Mahoney).31In the United States, shell egg production accounts for over 70percent of total table egg production.

Table 2—Types of uncertainty faced by selected pork companies

Firm Type

Hormel Hog prices and availability, government regulations, consumer acceptance of products, and interest rate debt.

Smithfield Foods Availability and prices of live hogs and raw materials, product pricing, competitive environmentand market conditions, and failure or inability to comply with government regulations, includingenvironmental and health regulations.

Seaboard Farms Hog and raw material prices, third-party hogs, and pork prices.

Farmland Industries Federal, State, and local environmental laws and regulations, disease, genetic changes, market prices for hogs, strength of competition, and regulatory delays that affect growth strategies, joint ventures, and operational alliances. Note: Includes uncertainty that may causea company’s actual results to differ substantially from forward-looking statements.

Sources: Smithfield Foods, Form 10Q, March 14, 2000; Hormel, Form 10-K405, January 28, 2000; Farmland Industries, Form 10-Q, January 14, 2000 and Form S-1, January 19, 2000; and Seaboard Farms, Form 10-Q, April 28, 2000. Filings with the Securities and Exchange Commission.

to more volatile prices and revenues. The demand elas-ticity for a factor of production will be smaller inabsolute value as its share of total production costbecomes smaller (Thurman). Hence, an increase in theproportion of pork that is consumed in further-processed form is expected to result in a smaller (inabsolute value) own-price demand elasticity. As porkis bundled with other goods and services, the percent-age of the pork price accounted for by marketing ser-vices increased 14 percentage points between 1990and 2000, from 55 to 69 percent, compared with onlya 5-percentage point increase from 1980 to 1990.

Another source of uncertainty in the pork industry is thecompetitive environment in which firms operate.Processors compete in an environment in which strategyand pricing by one company can dramatically affect thecompetitive outcome of another firm, which also hasconsequences for the company’s suppliers (Di Pietre).

As in the poultry industry in the 1960s, vertical acqui-sitions and coordination of production and processingthrough production contracts, led by Smithfield Foods,has become more common in the pork industry.Following 50-year lows in hog prices in fall 1998,Smithfield purchased two leading hog producers withwhich it had marketing contracts. In 2000, PremiumStandard Farms (PSF), the 2nd-largest hog producerand 13th-largest hog slaughter firm, acquired Lundy

Packing, a hog slaughter firm based in North Carolina,which more than doubled PSF’s processing capacity.