venezuela doc 1.docx

TRANSCRIPT

Hola Dr. Hernández

Le mando algunos datos de Venezuela, por si le sirven, y las fuentes

Euromonitor International

Statistical Summary

2008 2009 2010 2011 2012 2013Inflation (% change) 31.4 27.2 28.2 26.1 21.3 36.6Exchange rate (per US$) 2.14 2.14 2.58 4.29 4.29 6.06Lending rate 22.4 19.9 18.3 17.2 16.4 15.8GDP (% real growth) 5.3 -3.2 -1.5 4.2 5.6 1.3GDP (national currency millions)

677,594.0

707,263.0

1,016,830.0

1,357,487.1

1,640,333.2

2,260,313.5

GDP (US$ millions)

315,953.6

329,787.8

394,348.2

316,482.2

382,424.5

373,033.1

Population, mid-year ('000)

28,288.7

28,749.9 29,208.4 29,663.8 30,115.7 30,563.3

Birth rate (per '000) 21.3 21.0 20.6 20.3 20.0 19.7Death rate (per '000) 5.1 5.1 5.1 5.1 5.2 5.2No. of households ('000) 6,516.3 6,727.0 6,944.6 7,169.0 7,390.9 7,614.0Total exports (US$ millions)

95,021.0

57,603.0 65,745.0 92,811.0 97,340.0 92,317.8

Total 50,971. 39,646. 38,613.0 46,813.0 59,339.0 52,746.7

imports (US$ millions) 0 0Tourism receipts (US$ millions) 1,029.0 990.0 739.0 777.0 1,498.3 2,094.2Tourism spending (US$ millions) 2,040.0 1,835.0 1,809.0 2,400.0 2,721.0 3,648.2Urban population ('000)

24,898.4

25,314.4 25,728.4 26,140.0 26,548.6 26,953.8

Urban population (%) 88.7 88.8 88.8 88.8 88.8 88.8Population aged 0-14 (%) 30.2 29.8 29.5 29.1 28.8 28.5Population aged 15-64 (%) 64.5 64.8 64.9 65.1 65.2 65.3Population aged 65+ (%) 5.3 5.4 5.6 5.8 6.0 6.2Male population (%) 50.2 50.2 50.2 50.2 50.1 50.1Female population (%) 49.8 49.8 49.8 49.8 49.9 49.9Life expectancy male (years) 70.9 71.0 71.2 71.4 71.6 71.7Life expectancy female (years) 76.8 77.0 77.2 77.4 77.5 77.7Infant mortality

10.6 10.6 10.4 10.2 10.0 9.8

(deaths per '000 live births)Adult literacy (%) 95.3 95.5 95.8 96.0 96.2 96.4

Next ›

Imports and ExportsMajor export destinations

2013 Share (%)

Major import sources

2013 Share (%)

North America 39.7 North America 31.4Asia-Pacific 31.9 Latin America 28.9Latin America 12.2 Asia Pacific 19.6Other countries 8.7 Europe 18.5Europe 7.1 Other countries 0.7Africa and the Middle East 0.5 Australasia 0.7

Fuente: Euromonitor International

OPERATING ENVIRONMENT

Venezuelan economy is the least competitive in the regionIn the World Bank’s Ease of Doing Business 2014 report (‘Doing Business 2014’), Venezuela ranked 181st out of 189 countries, slipping one place from 180th out of 185 economies in the 2013 report.Venezuela’s ranking in the Doing Business 2014 report reflects a highly challenging business climate featuring excessive levels of red tape, scarce protection for investors and high barriers to foreign trade. As a result, the country ranked 90th or lower in all 10 categories of Doing Business 2014. Venezuela registered its worst performances in the Doing Business 2014 rankings in the ‘Paying taxes’ and ‘Protecting investors’ categories, where it held the 187th and 182nd places at a global level respectively – ranking amongst the bottom 10 economies in the world in both of these categories.Due to the lack of positive reforms to its business regulations, Venezuela lost places in seven out of the 10 categories of Doing Business 2014 compared to the previous year. Moreover, in some categories like ‘Starting a business’ the country introduced reforms that made doing business more difficult by increasing the companies’ registration fees, resulting in the cost of a business start-up rising to 35.6% of income per capita from 25.7% of income per capita in the previous year. The exception to this trend was the category ‘Getting credit’ where Venezuela improved the depth of credit information by starting to collect companies’ data from financial institutions. As a result, the country gained 24 places to rank 130th at a global level in this category of Doing Business 2014.After contracting for two consecutive years (by 3.2% in 2009 and 1.5% in 2010, both in real terms) owing to the impact of the 2008-2009 global economic crisis, the Venezuelan economy posted positive economic growth of 4.2% and 5.6% in 2011 and 2012 respectively in real terms, due to rising exports

and high levels of government expenditure. However, real GDP growth is expected to moderate to 1.3% in 2013 and 3.0% in 2014 due to the effects of the global economic slowdown and the fragile situation of Venezuela’s public finances, which would restrain levels of government spending.High levels of public spending have fed persistent general government net budget deficits during the period 2007-2012 that hiked to 18.9% of total GDP in 2012 (up from 2.8% of total GDP in 2007) and soaring levels of inflation that reached 21.3% in the same year – one of the highest in the world. This has in turn fuelled a rise in public debt levels as a percentage of total GDP to 45.8% in 2012 from 30.8% in 2007. The country’s financial system shows relatively low levels of bank nonperforming loans as a percentage of total gross loans at 1.2% in 2012 (unchanged from 2007), although the banking system remains subject to risks deriving from high levels of state intervention, negative interest rates and strict foreign exchange controls in the country.Business confidence levels have remained depressed after the succession of President Nicolás Maduro (who took office in March 2013) from ex-President Hugo Chávez (who was in power from 1999 to 2013). This is due to the continuity of policies of President Maduro in relation to his predecessor, implementing a socialist economic model and thwarting private sector participation in the economy. This has led to a highly uncertain political, economic and regulatory environment for private companies operating in the country, which has negatively impacted investment and employment levels in Venezuela.The political environment in the country is highly polarised between supporters and opponents of the government, resulting in frequent protests and clashes between the two factions. In addition, insecurity and crime levels in Venezuela continue to be high, as shown by the country’s rate of homicides which stood at 44.4 per 100,000 people in the population in 2012, one of the highest in the world. This is reflected in the ‘Political stability and absence of violence’ index published by the World Bank, where Venezuela held 167th position out of 203 economies in 2012, and second to last amongst Latin American countries – only ahead of Colombia (187th). The ‘Political stability and absence of violence index’ measures the perceptions of the likelihood that the government will be destabilised or overthrown by unconstitutional or violent means.Over the period 2007-2012, the Venezuelan government has continued to increase state intervention in the economy through nationalisations of private companies, price controls and a heavier regulatory burden. Seizures of private capital (including equity, land and inventories) by authorities are common, and the government maintains a confrontational stance towards private businesses, on which it imposes “fair prices” in order to curb “excessive profits”. In the World Bank’s ‘Regulatory quality index’ – which measures the perceptions of the ability of the government to formulate and implement sound policies that permit and promote private sector participation -, Venezuela ranked 192nd out of 202 economies in 2012.Corruption levels in the country are perceived as pervasive especially amongst government officials, security forces and the judiciary. In Transparency International’s Corruption Perceptions Index 2013, Venezuela ranked joint 160th (together with Cambodia and Eritrea) out of 177 countries, comparing unfavourably to Uruguay (joint 19th) and Brazil (joint 72nd).

GOVERNMENT REGULATION AND TRADING ACROSS BORDERS

Government policies are unfavourable towards foreign investmentDuring the period 2007-2012, Venezuela’s climate for foreign direct investment (FDI) became extremely challenging owing to government policies to increase control over the economy. The current investment regulatory framework imposes restrictions on foreign investment in sectors including hydrocarbons, banking, mining and media, although in practice private investment across all economic sectors is exposed to risks of nationalisation, price controls and state intervention. In addition, stringent foreign exchange controls imposed by the government make it highly difficult to repatriate capital, dividends and profits, while public procurement processes favour state-owned companies or private companies associated with the government.As a consequence of the government’s stance towards private investment, FDI inflows into Venezuela have averaged 0.5% of total GDP over 2007-2012 (0.8% in 2012 alone), one of the lowest in the region. After recording negative FDI inflows (or repatriation of investment by foreign companies) of BsF4.7 billion (US$2.2 billion) in 2009 due to the impact of the global economic crisis, Venezuela registered positive FDI inflows over 2010-2012 that reached BsF13.8 billion (US$3.2 billion) in 2012. On the other hand, FDI outflows (or investment abroad by Venezuelan companies) during the period 2007-2012 have been negligible, averaging just 0.3% of total GDP.The country has an overall poor infrastructure network as a consequence of chronic underinvestment on infrastructure by the government. In the World Economic Forum’s Global Competitiveness Report 2013, Venezuela ranked 137th out of 148 economies in the ‘Quality of infrastructure’ sub-category. Its

lowest rankings for infrastructure components were in the sub-categories ‘Quality of electricity supply’ (the cause of frequent blackouts in the country) and ‘Port infrastructure’, where it held the 142nd and 141st places respectively at a global level, while the best performance was in the ‘Available airline seat km/week’ sub-category, where it ranked 55th.Venezuela has been a member of the World Trade Organization (WTO) since 1995 and it joined the Mercosur trade bloc (which includes partners Brazil, Argentina, Uruguay and Paraguay) in July 2012, after which it will have a period of four years to implement Mercosur’s common tariffs. For imports from countries outside Mercosur, Venezuela applies tariffs generally of up to 40.0%. In addition, imports into the country are taxed VAT at 12.0% (with the exception of some products like foodstuffs, medicines and certain personal care products). Venezuela imposes numerous non-tariff barriers to imports including permits, certificates and licences from one or several government bodies, as well as inefficient and expensive port operations in the state-owned port system. One of the major barriers to import into the country is the tight foreign exchange controls in place since 2003, which leave importers with scarce access to foreign currency in a government-controlled foreign exchange market, which also gives preference to state-owned and associated companies.Exporting a container from Venezuela takes on average 8.0 documents, and in the case of importing 9.0 documents, according to Doing Business 2014. The average time required for exporting from Venezuela is 56.0 days, while importing takes 82.0 days, compared to the regional averages of 17.0 days for exports and 19.0 days for imports. The cost to export from Venezuela is US$3,490 per container while the import cost is US$3,695, considerably higher than the Latin American & Caribbean averages of US$1,283 and US$1,676 respectively.

TAX ENVIRONMENT

Tax system does not favour business activityVenezuela has an overly complex tax system with high total tax rates that are not conducive to business activity. The standard top corporate income tax rate stands at 34.0% in 2013, although in the case of oil companies this can be as high as 50.0%. The VAT rate stands at 12.0% in the same year, with several VAT-exempt products including certain foodstuffs, medicines, books and exports. In addition, companies operating in the country are subject to multiple fees and contributions including: a 2.0% payroll tax (on top of the employers’ social security contributions); a tax on economic activities (generally up to 18.0% on sales, depending on economic activity and district); a contribution for science and technology (up to 2.0% of gross income, for companies with annual sales over BsF76,000 or US$17,674); and a contribution for development of sports and physical education (1.0% of annual profits, for companies with annual net profits over BsF15,200 or US$3,585).According to Doing Business 2014, Venezuela’s total tax rate as a percentage of total profits reaches 61.7% of total profits (compared to the regional average of 47.3% of total profits), as a result of the country’s numerous taxes and contributions. Venezuela’s total tax rate includes labour taxes and contributions for an equivalent of 18.0% of total profits, higher than the Latin American & Caribbean average of 14.7% of total profits, according to the same source.It takes on average 792 hours per year for a company to prepare, file, pay or withhold its taxes and contributions in Venezuela, according to Doing Business 2014. This figure is amongst the highest in the world, highlighting the country’s complicated tax system especially in relation to VAT and social security contribution payments.Despite the country’s high total tax rates, Venezuela’s tax burden as a percentage of total GDP stood at 16.3% in 2012, which is relatively low by regional standards. This is the result of inefficiencies in the tax collection system, corruption in the country’s tax agency, and widespread tax evasion in Venezuela. The latter is fuelled by the large informal sector existent in the country.

LABOUR MARKET AND POPULATION SKILL SET

Extremely rigid labour market reduces competitivenessBacked by government literacy programmes, Venezuela’s adult literacy rates have risen over the long term to reach 96.2% of adult population aged 15+ in 2012 (up from 84.0% in 1980). In 2012, 15.6% of the total Venezuelan population aged 15+ had a higher education degree, higher than the Latin American average of 12.7%. Nevertheless, the quality of the country’s educational system is perceived as poor, as reflected by Venezuela’s ranking in the ‘Quality of the educational system’ sub-category of the Global Competitiveness Report 2013, where Venezuela held 128th position at a global level.Government spending on education as a percentage of total GDP in Venezuela has risen from 6.4% in 2007 to 8.0% in 2012 – one of the highest in the region. However, this spending makes relatively little emphasis on the higher education segment, which is facing increasing funding demands owing to the rising number of higher education students (including universities) in the country which reached a historical high of 2.7 million in 2012, up from 1.7 million in 2007.Venezuela’s constraints to private sector growth have weighed on job creation by private businesses, leading to an oversupply of graduates that cannot be absorbed by subdued demand from the labour market. The excess of professionals is most evident in popular careers like Social Sciences, Business and Law and Education. Notwithstanding the abundance of labour, the country suffers from skills shortages owing to the deficient quality of the country’s educational system, which creates a vast pool of semi- and low-skilled labour but relatively few highly-qualified professionals. Skills shortages are particularly critical in areas like engineering and finance, and are exacerbated by strong levels of brain drain due to qualified Venezuelans emigrating to look for opportunities elsewhere due to political and economic instability existent in the country.

Source: Euromonitor International from UNESCO/national statistics/ International Labour Organisation (ILO)/OECD/Trade Sources

Venezuela’s unemployment rate as a percentage of economically active population rose from 7.4% in 2008 to 8.5% in 2010 due to the impact of the global economic crisis, although it has somewhat eased since then to reach 7.8% in 2012. The decline has been the result of the country’s economic growth, rising public sector employment and a decline of the labour force participation rate (due to discouraged jobseekers leaving the labour force). Between 2007 and 2012, Venezuela’s youth

unemployment rates have remained about twice as high as overall unemployment rates, reaching 16.4% of economically active population aged 15-24 in 2012, reflecting the excess of graduates in the labour force as well as employers’ preference for experienced personnel.In 2012, Venezuela’s female employment rate stood at 50.0% of the female population of working age (15-64), up from 49.2% in 2007. This is markedly lower than the male employment rate which reached 77.5% of male population of working age in 2012, down from 78.3% in 2007. The difference between female and male employment rates is the consequence of traditional lack of work opportunities for Venezuelan women, and of cultural characteristics of the Venezuelan society where single-income households have been predominant. Nonetheless, the gap is expected to narrow over the long term driven by rising rates of educational attainment amongst Venezuelan women and cultural shifts in the Venezuelan society (where households with two breadwinners are becoming increasingly common).The Community, Education, Health, Social, Personal Services, Public Administration and Defence sector is Venezuela’s largest employment generator, accounting for 31.5% of the total employed population in 2012 (up from 30.4% in 2007) and reflecting the large size of the country’s public sector and massive amounts of government spending. This sector also experienced the largest rise in the share of employment across all industries over 2007-2012, as job losses in the private sector were partly offset by employment gains in the public sector. On the other hand, the Manufacturing sector registered the biggest decline in employment during the same period, with its share of total employment decreasing from 12.3% in 2007 to 11.1% in 2012, owing to the effects of the global economic crisis 2008-2009 and the real appreciation of Venezuela’s domestic currency (due to rapidly rising levels of inflation), which adversely impacted the country’s exports of manufactured products.Venezuela’s labour market is extremely rigid in terms of wage determination, work hours and hiring and firing practices – it is not possible under Venezuelan labour law to make an employee redundant. In 2012, the government approved a new Law of Labour and Workers significantly expanding workers’ rights and benefits, banning outsourcing and reducing the length of the legal work week (from 44.0 to 40.0 hours). Current labour regulations allow the hiring of workers on probationary periods, although the maximum length of such contracts was reduced to one month from three months by the new 2012 labour law.The minimum wage per month in Venezuela stood at BsF2,048 (US$477) in 2012, one of the highest in Latin America, after having increased by 233% in nominal terms over 2007-2012 (although in real terms the rise was only 1.7% during this period due to rampant levels of inflation). The country’s labour productivity levels (measured as GDP per person employed) rose by 50.8% in US$ terms over the period 2007-2012 to reach US$28,420 by the end of this period. These are amongst the highest in the region, though they are more the consequence of higher prices of crude oil during this period (which supported a rise in exports), considerable government spending and an overvalued domestic currency, which boosted Venezuela’s GDP in US$ terms over 2007-2012.

Risks and Vulnerabilities: VenezuelaCountry Briefing | 27 Mar 2013

MAJOR COMPONENTS OF THE ECONOMY

Oil sector remains key driver of economic growthVenezuela’s lucrative oil sector continues to be the main engine of the economy, and attracts the majority of government funding and foreign direct investment (FDI). High global prices for oil have driven the development of the oil sector, with Europe Brent crude oil trading at above US$100 per barrel for most of 2012. However, political intervention in the economy has continued to undermine the business environment, with the World Bank’s 2013 Ease of Doing Business Index ranking Venezuela at 180th out of 185 economies, below Guinea-Bissau and above the Democratic Republic of Congo.In 2012, the mining and quarrying sector comprised 25.7% of total Gross Value Added (GVA), making it the dominant economic sector. However, growing dependence on the oil sector has led to the contraction of the non-oil sector, exacerbated by frequent state nationalisations of key industries and the imposition of price and supply controls. This has reduced incentives to invest in the non-oil sector and left the economy vulnerable to a sharp downturn in global oil prices. The importance of the oil sector is shown by the fact that the second-largest sector, manufacturing comprised 13.3% of total GVA in 2012.Even despite current high global oil prices, Venezuela’s economy is suffering. GDP grew by 5.6% year-on-year (y-o-y) in real terms in 2012 and by a real 4.2% in 2011. This was an improvement on the real contractions of 1.5% and 3.2% in 2010 and 2009 respectively, but remains well below the high real growth rates of more than 7.0% of much of the 2000s. However, this does not represent a major economic recovery but more the huge increase in public spending approved by President Hugo Chávez in the run-up to presidential and legislative elections in October 2012. With the elections over, spending is likely to fall in 2013, with real GDP growth forecast at only 1.3%. The stuttering economy is also weighing on GDP per capita, which fell to BsF45,930 (US$10,708) in 2011, down from BsF35,011 (US$13,578) in 2010, before rebounding to BsF58,658 (US$13,675) in 2012.

Between 2007 and 2012, Agriculture, Hunting, Forestry and Fishing formed the fastest growing sector of the economy, growing by 7.5% on average annually in real terms. This reflected the sharp run-up in incomes and consumer prices, fuelled by high levels of government spending and surging oil revenues. The second fastest growing sector was Hotels and Restaurants, growing at an annual average rate of 6.0% in real terms in the same period. The services sector is likely to suffer from slower forecast growth in 2013, especially as political uncertainty will weigh on consumer confidence.Perhaps counter-intuitively, the mining and quarrying sector posted poor growth between 2007 and 2012, growing by an annual average of 0.5% in real terms. High oil revenues, driven by global oil prices, act to mask the deteriorating state of the domestic hydrocarbons sector, which suffers from persistent under-investment and inefficiency at state-run oil firm PDVSA. These factors will continue to hinder the mining and quarrying sector growth in the medium term, particularly with post-election government spending forecast to decelerate in 2013.The manufacturing sector also performed poorly between 2007 and 2012, growing by an annual average rate of 0.7% in real terms. This is also a result of under-investment; nationalisations in sectors such as the steel industry have deterred investment and reduced efficiency.

SOCIO-POLITICAL RISK

Political tensions deter investmentSocio-political tensions are extremely high in Venezuela, particularly following President Chávez’s death on 5th March 2013. As Mr Chávez has been Venezuela’s dominant political figure since he first won the presidency in 1998, his death could undermine stability. Elections must now be held within 30 days. A disputed result could spark violent demonstrations and clashes between supporters and opponents of Mr Chávez’s designated successor, Vice-President Nicolás Maduro. The World Bank’s Political Stability and Absence of Violence Index ranked Venezuela at -1.3 in 2011 (latest available data), with -2.5 being the most negative.Under Mr Chávez, corruption has become entrenched, particularly in the hydrocarbons sector but generally throughout the Venezuelan business environment. In Transparency International’s Corruption Perceptions Index 2011, Venezuela was ranked 165th out of 176 countries, making it one of the least attractive locations in the world. High levels of corruption, alongside the government’s ongoing nationalisation process, have acted as a strong disincentive to investment. While foreign investors are still willing to invest in the hydrocarbons sector, owing to the high rates of return, investment in the non-oil sector has fallen sharply. In particular, Venezuela’s decision in January 2012 to withdraw from the International Centre for the Settlement of Investment Disputes (ICSID) has unnerved investors, who now have little recourse for arbitration in the event of an investment dispute.Unemployment is falling yet the economy is slowing and the non-oil sector declines, reaching 7.8% of the economically active population in 2012, although it is worth noting that this is a reduction from 10.0% in 2006. In particular, the youth unemployment rate is high, standing at 16.4% in 2012. This is partly due to the decline in the non-oil sector but particularly to a reduction in the need for skilled labour. Although Venezuela’s education standards are high relative to the region, the slowing economy has made it difficult for recent graduates to find employment. Employers are unwilling to lose experienced staff, particularly in the hydrocarbons sector, where there is a shortage of trained technical staff and so are less willing to take on new graduates.

Despite high levels of social spending under the Chávez government designed to alleviate poverty, income inequality has risen in Venezuela between 2007 and 2012. In 2012, the Gini index (with zero corresponding to perfectly equal and 100 corresponding to perfectly unequal) stood at 42.5, up from

41.0 in 2007. In part, this is the result of the economic slowdown since 2009, but in larger part it reflects the concentration of the economy and particularly the lucrative oil sector in the hands of a small elite group, who reap most of the benefits.Such inequality continues to fuel social tensions, with Mr Chávez’s core constituency being among the working classes and rural poor. He and his government are highly popular and he easily won re-election in October 2012, meaning that his successor is likely to perform well in the fresh 2013 elections. However, his authoritarian style of government has undermined democratic institutions and there are grave concerns about the independence of institutions, such as the judiciary, the central bank and the electoral council. There is a vocal opposition media, although the state media is able to call on far more financial resources and airtime.

Source: Euromonitor International from World BankNotes: Political stability and absence of violence ranking is obtained from political stability and absence of violence index reflecting a better score in a higher position. Political stability and absence of violence index measures the perceptions of the likelihood that the government will be destabilised or overthrown by unconstitutional or violent means, including domestic violence and terrorism

EXTERNAL SECTOR

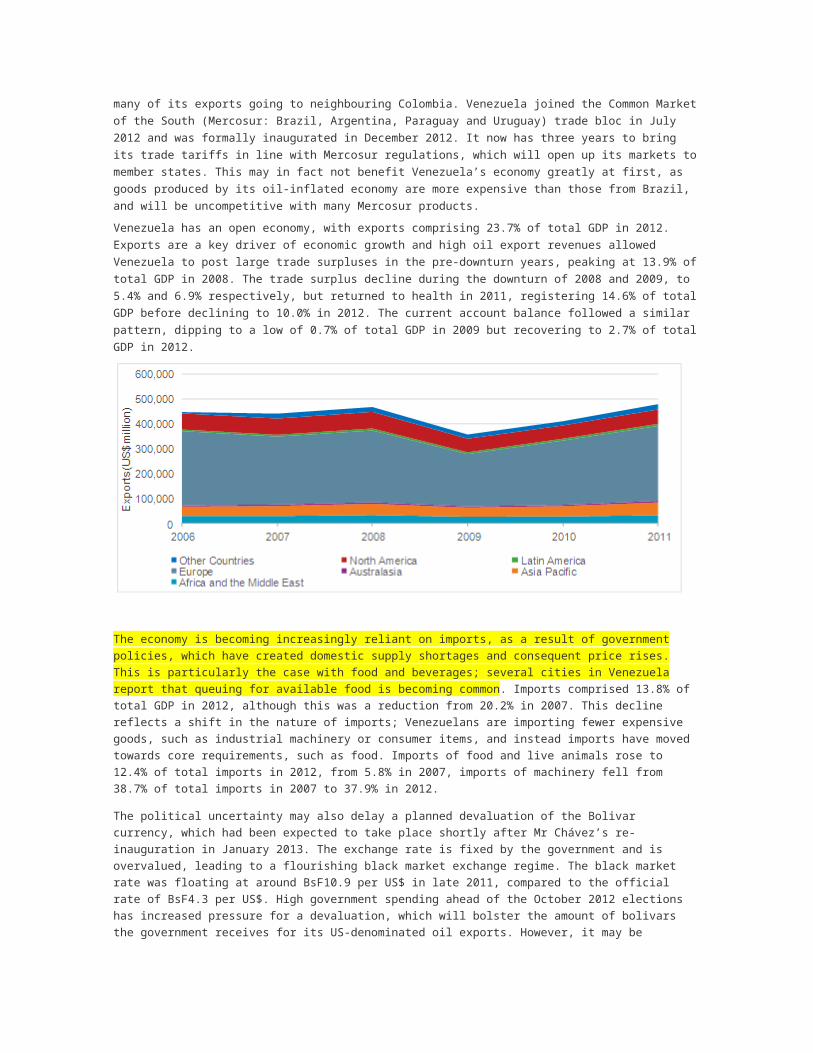

Oil exports drive economic fortunesVenezuela is one of the world’s largest oil exporters, ranked 9th in the world in 2012, and its oil exports determine the overall trend of its economy. The USA is Venezuela’s largest export partner, with exports to the USA comprising 48.0% of Venezuela’s total exports in 2012. This is despite

Venezuela’s hostile rhetoric towards the USA and it is worth noting that despite President Chávez’s frequent threats to shut off the taps to the USA, he has never done so. Indeed, such an action would be highly damaging to Venezuela’s economy, as it would substantially damage export revenues; for this reason, Venezuela is highly unlikely to reduce oil exports to the USA.This dependence on oil exports leaves Venezuela vulnerable to any downturn in oil prices, although it has been fortunate in the last decade to enjoy sustained high oil prices. Apart from oil, Venezuela’s exports are agricultural and manufacturing, with many of its exports going to neighbouring Colombia. Venezuela joined the Common Market of the South (Mercosur: Brazil, Argentina, Paraguay and Uruguay) trade bloc in July 2012 and was formally inaugurated in December 2012. It now has three years to bring its trade tariffs in line with Mercosur regulations, which will open up its markets to member states. This may in fact not benefit Venezuela’s economy greatly at first, as goods produced by its oil-inflated economy are more expensive than those from Brazil, and will be uncompetitive with many Mercosur products.Venezuela has an open economy, with exports comprising 23.7% of total GDP in 2012. Exports are a key driver of economic growth and high oil export revenues allowed Venezuela to post large trade surpluses in the pre-downturn years, peaking at 13.9% of total GDP in 2008. The trade surplus decline during the downturn of 2008 and 2009, to 5.4% and 6.9% respectively, but returned to health in 2011, registering 14.6% of total GDP before declining to 10.0% in 2012. The current account balance followed a similar pattern, dipping to a low of 0.7% of total GDP in 2009 but recovering to 2.7% of total GDP in 2012.

The economy is becoming increasingly reliant on imports, as a result of government policies, which have created domestic supply shortages and consequent price rises. This is particularly the case with food and beverages; several cities in Venezuela report that queuing for available food is becoming common. Imports comprised 13.8% of total GDP in 2012, although this was a reduction from 20.2% in 2007. This decline reflects a shift in the nature of imports; Venezuelans are importing fewer expensive goods, such as industrial machinery or consumer items, and instead imports have moved towards core requirements, such as food. Imports of food and live animals rose to 12.4% of total imports in 2012, from 5.8% in 2007, imports of machinery fell from 38.7% of total imports in 2007 to 37.9% in 2012.

The political uncertainty may also delay a planned devaluation of the Bolivar currency, which had been expected to take place shortly after Mr Chávez’s re-inauguration in January 2013. The exchange rate is fixed by the government and is overvalued, leading to a flourishing black market exchange regime. The black market rate was floating at around BsF10.9 per US$ in late 2011, compared to the official rate of BsF4.3 per US$. High government spending ahead of the October 2012 elections has increased pressure for a devaluation, which will bolster the amount of bolivars the government receives for its US-denominated oil exports. However, it may be unwilling to introduce a major devaluation at a time when the political leadership remains so uncertain.

To maintain the exchange rate, as well as high levels of government spending, the government has been running down its foreign exchange reserves. These fell to US$2.8 billion in 2012, from a high of US$32.6 billion in 2008, demonstrating the impact of the 2008-2009 economic slowdown on reserves. The government has failed to translate the benefits of high oil revenues into foreign exchange reserves, which will reduce its ability for fiscal manoeuvre during a potentially difficult political transition.

GOVERNMENT FINANCE

Government finances increasingly precariousThe government’s financial position is highly dependent on oil revenues, which funds high levels of social spending. At the same time, the government is increasing borrowing to fund this spending, which has resulted in a slow but steady build-up of debt. This accelerated during the economic downturn of 2008-2009, with the budget deficit spiking to 8.1% of total GDP in 2009, from 2.6% of total GDP the previous year. This moderated to 5.4% before rising again to 7.4% in 2011 and 2012 respectively, which is high for such a resource-rich country. This level of deficit is sustainable given current oil revenues, but would become less so if global oil prices dipped.Moreover, the government has failed to reap the benefits of its decade-long oil bonanza in the form of savings, or a fiscal sustainability fund. Instead, revenues are immediately dispersed in the form of social spending, leaving the government with no cushion to counter any potential economic shocks. Borrowing and spending might have been expected to decline in 2013, following Mr Chávez’s re-election and a consequent reduced need to garner public support. However, political instability and the prospect of fresh elections following Mr Chávez’s death may keep spending high and push the budget deficit up further.As part of the government’s social spending policy, pension payments have been increased. With Venezuela’s ageing population, this is storing up a pensions crisis in the long term. However, far more risky is the government’s high-spending and no-savings fiscal policy, which is likely to bring about a fiscal crisis far earlier. This is likely to take place in conjunction with a political crisis, with any change of government likely to provoke a reassessment of expenditure and borrowing commitments.

Chart 6 Public Debt vs. General Government Budget Deficit in Venezuela: 2007-2012

Chart 6 Public Debt vs. General Government Budget Deficit in Venezuela: 2007-2012