value vs growth & active vs passive. growth stocks growth: high p/e ratio (high mv/bv) low or no...

TRANSCRIPT

Value vs Growth &

Active vs Passive

Growth StocksGrowth:

High P/E Ratio (high MV/BV)Low or no dividend yieldHigh ROAHigh Expected growth rate in EPS Better yet, the high growth rate in EPS is accelerating!

Key to Active Growth Strategy

Identify high growth firms who will continue to exhibit exceptional earnings momentum. Goal is to outsmart othersFocus is on EPS growth Alternatively, try to exploit that others have irrational behavior

Value Stocks Value:

Low P/E Ratio (MV/BV) stocks (Think ratio will increase)

Price is “cheap” by some measure of comparisonLow growth rate in EPSLow ROAHigh dividend yield (or no dividend yield if really in trouble)

Key to Success (Value)

Which firms have sound businesses that can be acquired cheaply?Focus on P/E or ME/BEOn December 16, 2005, the U.S. S&P/Citigroup Value Series became Standard and Poor’s official style series, replacing the S&P/Barra indices.

Which Does Better??

Value stocks produce higher average returns than growth, with a lower standard deviation. However, not consistently!

Size-Style GridClassify mgr by size & value vs growth:

Lg Cap Value Lg Cap Growth

Sm Cap Value Sm Cap Growth

Size-Style GridThe size-style grid is used as a risk-adjustment model. Logic?

Abnormal Return = RP,t – R Benchmark,t

where the “Benchmark” portfolio is an index matched on Size and the Value-Growth Dimension.

ACTIVE EQUITY MANAGEMENT

Goal: Earn a portfolio return net of

transaction costs and expenses that exceeds the return of a passive benchmark portfolio (most often an index) on a risk-adjusted basis.

Challenges (Active) 1. Costs & Fees

Transaction Costs and fees range from 1% - 2% of assets under management on average. (hurdle)

Challenges (Active) 2. Appropriate Evaluation of Performance

Difficulty differentiating Luck from Skill

Appropriate Risk-Adjustment Model? (CAPM vs Fama-French Factor Model vs Other Models)

Themes of Active Mgmt

1. Asset Allocation: Shift between stocks, bonds & T

bills

Themes of Active Mgmt2. Sector Rotation Strategy

Overweighting Industries or Sectors (Based on Fundamental or Technical Analysis)

Overweight certain attributes:

Growth vs Value; Small vs Lg Cap

Themes of Active Mgmt

3. Individual Stock Selection

Examine individual issues to find over and undervalued stocks.

Terminology

Screening: Screen for stocks with certain

attributes (Small cap, P/E in lower 1/3,

Operating income increasing last two qtrs etc. )

Backtesting

Test to see if trading rules would have worked using historical data. Subject to data mining criticisms as you can always find some patterns. It does not mean that they will persist in the future.

Terminology

Quadratic Programming: Efficient frontier optimization using Markowitz’s formula.

Hedge Funds (Long/Short Strategy)

Long-Short Approach: buy some and short others. Called “hedge funds”

Create a Market Neutral Portfolio or net long or net short portfolio.

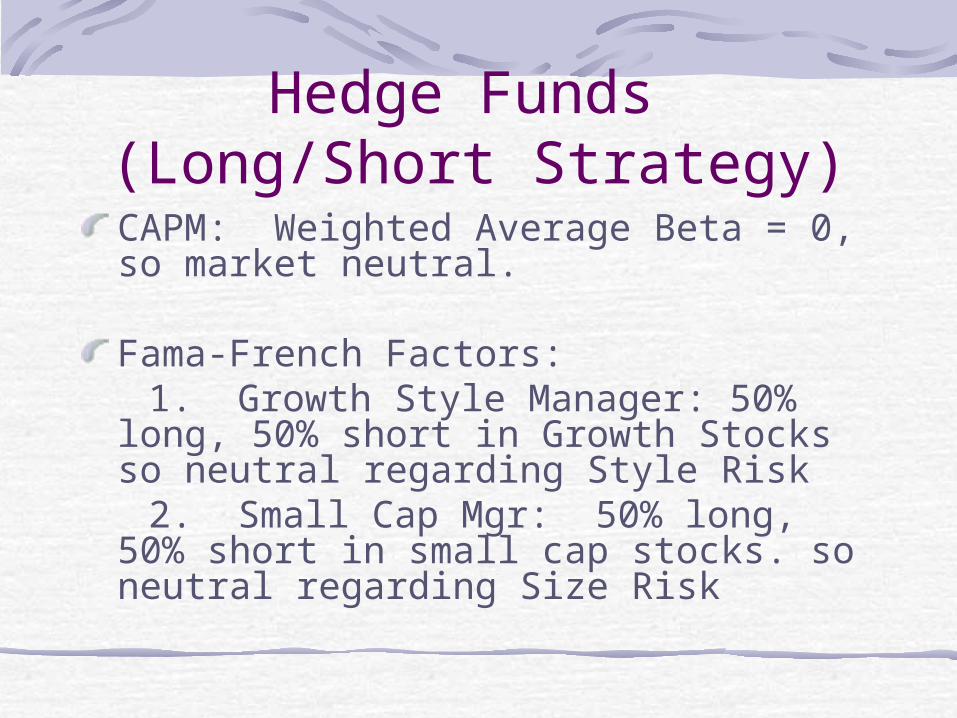

Hedge Funds (Long/Short Strategy)

CAPM: Weighted Average Beta = 0, so market neutral.

Fama-French Factors: 1. Growth Style Manager: 50% long,

50% short in Growth Stocks so neutral regarding Style Risk

2. Small Cap Mgr: 50% long, 50% short in small cap stocks. so neutral regarding Size Risk

Passive Equity Management

Logic: Market is fairly efficient. Too difficult to overcome 1 - 2% costs of running an active equity portfolio.

Don’t try to beat the market, just equal it and keep expenses to a bare minimum.

Passive FeaturesPortfolio is built without using technical or fundamental analysis.

Buy & Hold: The securities are purchased and then held with only occasional re-balancing (reinvest dividends, a change in the index etc..)

Index Funds

Passive portfolios that track an index and sell shares to investors are called Index Funds.

(Ex: Vanguard 500 Index which tracks the S&P 500.)

Index Funds

Manager Performance: Judged by how well he/she tracks the index and by the costs generated to do so.

Index Fund Types

1. Full Replication: Buy all stocks in the index in proportion to their weights in the index.

Index Fund Types2. Sampling: Buy the stocks with larger

index weights & hold a representative sample of the others.

Benefit Relative Full Replication: Lower commissions (less stocks to purchase and to reinvest dividends).Drawback Relative Full Replication: Will be Tracking Error

R-Squared = (r i,j)2

The correlation coefficient between the portfolio and the benchmark index squared! Tells us what fraction of the movement in the portfolio is due to the benchmark portfolio.

R-Squared = (rport, benchmark)2

R-Squared = (r i,j)2

Helps to identify an active portfolio’s style on the grid. Find the index that has the highest correlation coefficient (or the highest R-squared.)Tells us something about the level of diversification of an active portfolio manager.One measure of whether an index fund manager is tracking the underlying index.

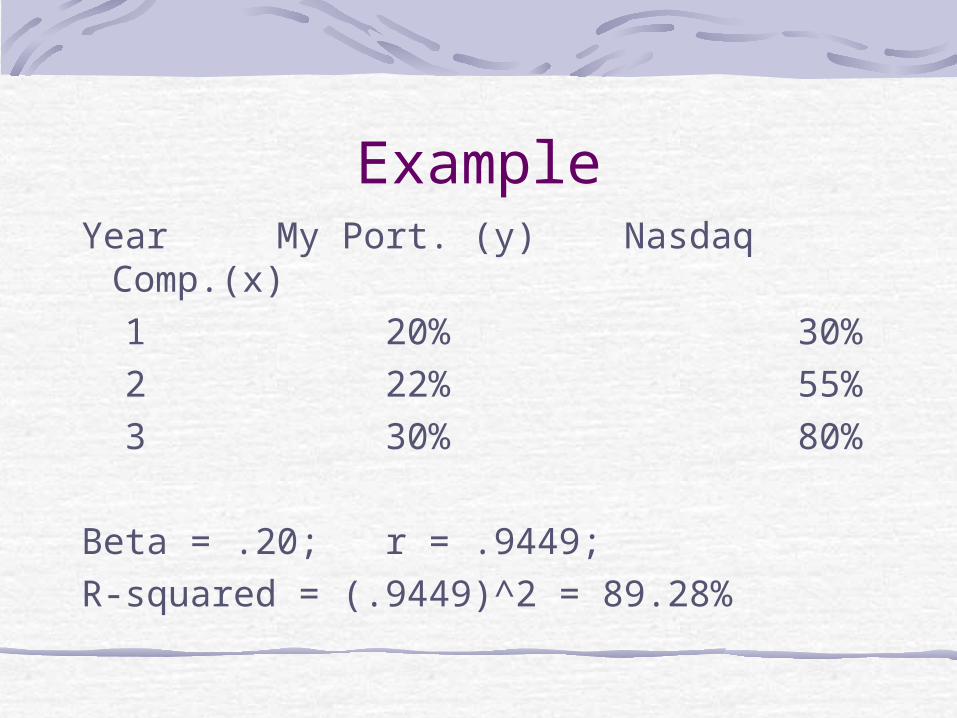

ExampleYear My Port. (y) Nasdaq Comp.(x)

1 20% 30% 2 22% 55% 3 30% 80% Beta = .20; r = .9449; R-squared = (.9449)^2 = 89.28%

Evaluating Index Fund Manager Performance

1. R-Squared: Measures how closely the fund is moving with the benchmark index.

This measures tracking, but not

costs!

Exchange Traded FundsAn alternative to buying shares in an Index Fund.Depositary receipts with underlying stocks in an index held in deposit by the financial institution that issued certificates. Shares are traded like a stock but represent a claim on the portfolio.

Exchange Traded FundsExample SPDRs: Depositary receipts on the S&P 500.Buy like a share of stock no fund marketing fees (means lower expenses).No cash on hand to handle fund flows. Trade when market open not just at market close price. Can be shorted or purchased with margin.

Investor Types Efficient Market Proponent

Fundamental Analyst

Technical Analyst