valuation 090904232636-phpapp01

TRANSCRIPT

2www.venturebean.com

FOREWORD

How does one value a company? While at a broad level one may be able to understand why a company may be worth a certain amount to an investor or a buyer, it is not always possible to understand why someone is willing to pay a certain amount for a business.

?? ?

?

3www.venturebean.com

FOREWORD

A business worth a significant amount at a certain point in time may suddenly lose much of its value a very short while later.

This is what happened in many companies commonly referred to as ‘dot-com companies,’ which were valued at amounts which may seem absurd now…. in hindsight.

?? ?

?

4www.venturebean.com

AGENDATopic Slide no.

Background 6

Valuation methods 13

Cost based 16

Book value 18

Goodwill 24

Intangible assets 28

Replacement 31

Liquidation 32

Income based 33

Earnings capitalisation 35

DCF 36

Limitations of DCF 43

Market based 52

5www.venturebean.com

AGENDATopic Slide no.

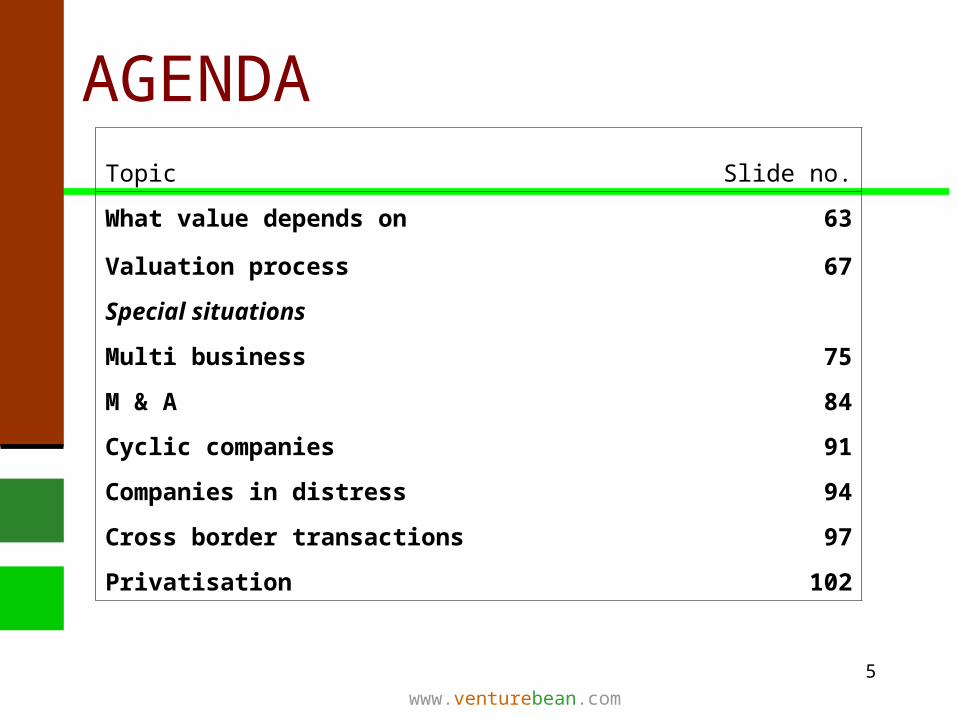

What value depends on 63

Valuation process 67

Special situations

Multi business 75

M & A 84

Cyclic companies 91

Companies in distress 94

Cross border transactions 97

Privatisation 102

6www.venturebean.com

BACKGROUND - FAQs

Why do values of companies change from time to time?

Does value depend on whether one wants to sell a company, to buy a minority stake or to buy the entire company?

Will a strategic investor value a company differently from a financial investor?

How can a company which is continually losing money have any value?

7www.venturebean.com

VALUATION PROCESS

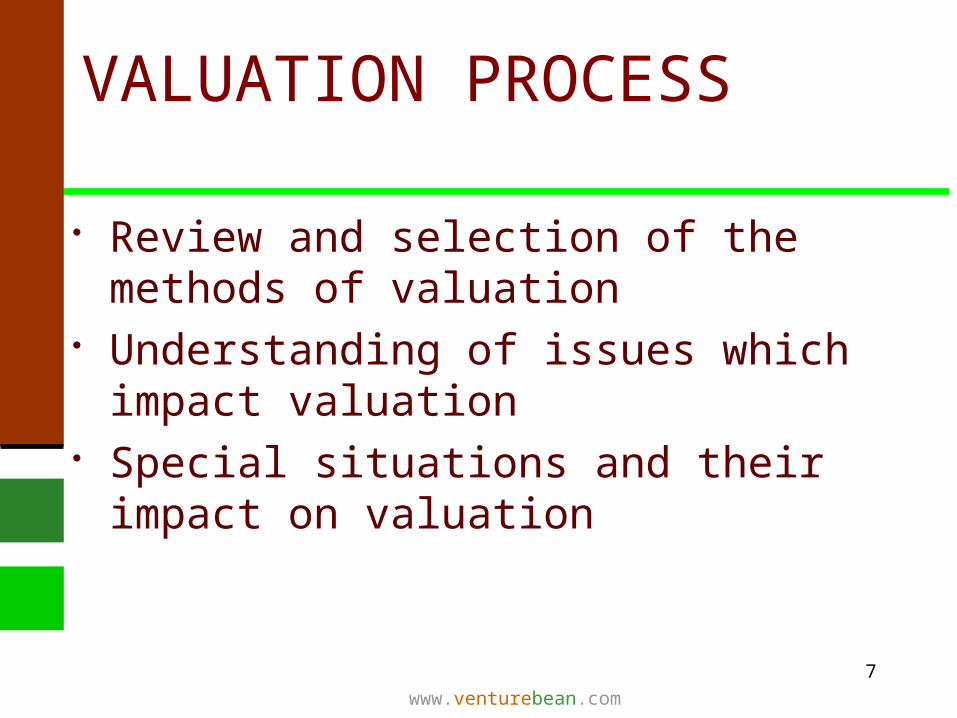

Review and selection of the methods of valuation

Understanding of issues which impact valuation

Special situations and their impact on valuation

8www.venturebean.com

What is value

Cost vs. Market Value

Historical vs. Replacement

Differs depending on need of person doing valuation – buyer, seller, employee, banker, insurance company

9www.venturebean.com

Value to user

Valued because of expected return on investment over some period of time; i.e. valued because of the future expectation

Return may be in cash or in kind

10www.venturebean.com

Complex nature of valuation

Value A + Value B can be

greater or less than

Value (A+B)

11www.venturebean.com

Why Value

When do you think a company is to be valued?

12www.venturebean.com

Why Value To Purchase Sell Transact Take decisions Report

13www.venturebean.com

VALUATION METHODS

14www.venturebean.com

Valuation methods

These can be broadly classified into:

Cost based Income based Market based

15www.venturebean.com

Valuation methods

Different experts have different classifications of the various methods of valuation

Within these methods, there are sub-methods

Sometimes the methods overlap

16www.venturebean.com

1. COST BASED METHODS

17www.venturebean.com

Cost based methods

Book value

Replacement value

Liquidation value

18www.venturebean.com

Book value method

Historical cost valuation All assets are taken at historical book value Value of goodwill* is added to this above

figure to arrive at the valuation

*We will see how goodwill is valued in later slides

19www.venturebean.com

Book value method

Historical cost valuation All assets are taken at historical book

value Value of goodwill is added to this

above figure to arrive at the valuation

Do you think there would be any difficulties in this?

20www.venturebean.com

Book value method

Current cost valuation All assets are taken at current value and summed to

arrive at value This includes tangible assets, intangible assets,

investments, stock, receivables

VALUE = ASSETS - LIABILITIES

21www.venturebean.com

Book value method

Current cost valuation All assets are taken at current value and summed to

arrive at value This includes tangible assets, intangible assets,

investments, stock, receivables

What do you think could be difficulties in this method?

22www.venturebean.com

Book value method

Current cost valuation: Difficulties

Technology valuation – whether off or on balance sheet

Tangible assets – valuation of fixed assets in use may not be a straightforward or easy exercise

Could be subject to measurement error

23www.venturebean.com

Book value method

Current cost valuation: More difficulties

The company is not a simple sum of stand alone elements in the balance sheet

Organisation capital is difficult to capture in a number – this includes– Employees– Customer relationships– Industry standing and network capital– Etc…

24www.venturebean.com

Valuation of goodwill

Based on capital employed and expected profits vs. actual profits

Based on number of years of super profits expected

May be discounted at suitable rate

25www.venturebean.com

Valuation of goodwill

Normal capitalisation method– Normal capital required to get actual return less actual capital

employed Super profit method

– Excess of actual profit over normal profit multiplied by number of years super profits are expected to continue

Annuity method– Discounted super profit at a suitable rate

26www.venturebean.com

Valuation of goodwill

COMPANY A Capital employed: Rs. 45 cr Normal rate of return: 12 % Future maintainable profit: Rs. 5.5 cr

What would be the goodwill under the normal capitalization method?

SOLUTION: (change font colour to see this) = (5.5/.12) – 45 = Rs. 0.83 cr

27www.venturebean.com

Valuation of goodwill

COMPANY B Capital employed: Rs. 50 cr Normal rate of return: 15 % Future maintainable profit: Rs. 8 cr Super profit can be maintained for:3 years

What would be the goodwill under the super profit method?

SOLUTION: (change font colour to see this)

= [8 – (50*.15) ] * 3 = Rs.1.50 cr

28www.venturebean.com

Valuation of IA

The value of the IA is from Economic benefit provided Specific to business or usage Has different aspects

– Accounting value– Economic value– Technical value– Can you think of examples of these

different values?

29www.venturebean.com

Valuation of IA

Depends on objective and can vary widely depending on purpose

For accounting purposes – to show in financial statements

For acquisition/merger/investment For management to understand

value of company for decision making

30www.venturebean.com

IA value in transactions

Often value paid in M&A deals is more than market value/book value. This could be:

Partly due to over bidding due to strategic reason (existing or perceived) and

Partly due to IA of company, not captured in balance sheet

31www.venturebean.com

Replacement value method

Cost of replacing existing business is taken as the value of the business

32www.venturebean.com

Liquidation value method

Value if company is not a going concern

Based on net assets or piecemeal value of net assets

33www.venturebean.com

INCOME BASED METHODS

34www.venturebean.com

Income Based methods

Earnings capitalisation method or profit earning capacity value method

Discounted cash flow method (DCF)

35www.venturebean.com

Earnings capitalisation method

This method is also known as the Profit earnings capacity value (PECV)

Company’s value is determined by capitalising its earnings at a rate considered suitable

Assumption is that the future earnings potential of the company is the underlying value driver of the business

Suitable for fairly established business having predictable revenue and cost models

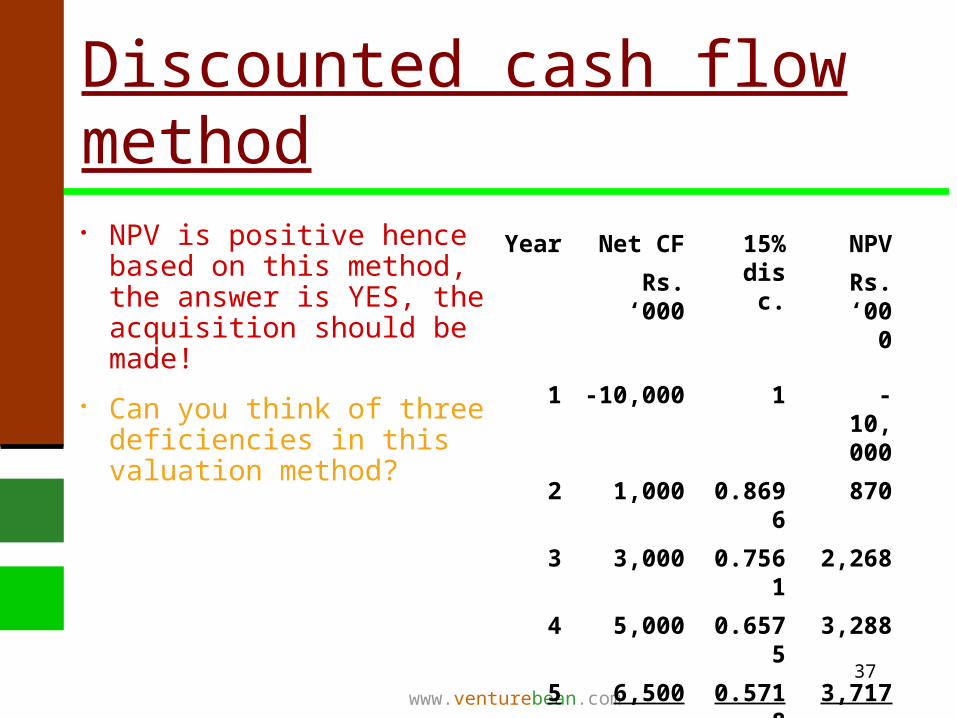

36www.venturebean.com

Discounted cash flow method

Creame Corner wants to acquire Samosa Specials for Rs. 10 million. The net cash flows are in the table below. Creame Corner wants to apply a discount rate of 15%. Should it buy Samosa Specials?

Year Net CF 15% disc.Rs. ‘000

1 -10,000 1

2 1,000 0.8696

3 3,000 0.7561

4 5,000 0.6575

5 6,500 0.5718

37www.venturebean.com

Discounted cash flow method NPV is positive hence

based on this method, the answer is YES, the acquisition should be made!

Can you think of three deficiencies in this valuation method?

Year Net CF 15% disc.

NPV

Rs. ‘000 Rs. ‘000

1 -10,000 1 -10,000

2 1,000 0.8696 870

3 3,000 0.7561 2,268

4 5,000 0.6575 3,288

5 6,500 0.5718 3,717

5,500 142

38www.venturebean.com

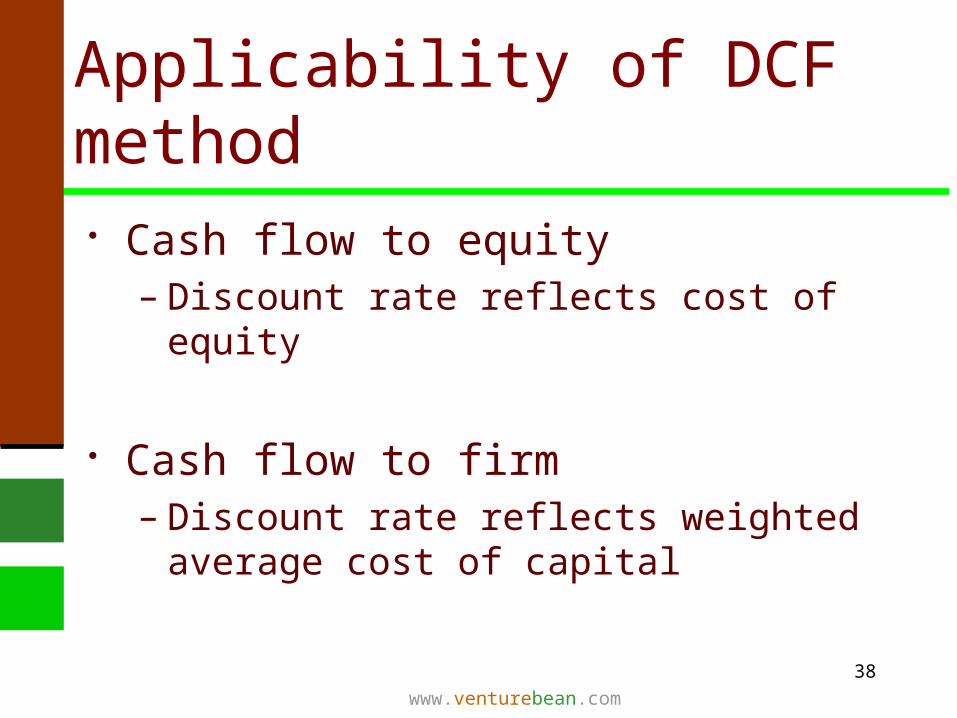

Applicability of DCF method

Cash flow to equity– Discount rate reflects cost of equity

Cash flow to firm– Discount rate reflects weighted

average cost of capital

39www.venturebean.com

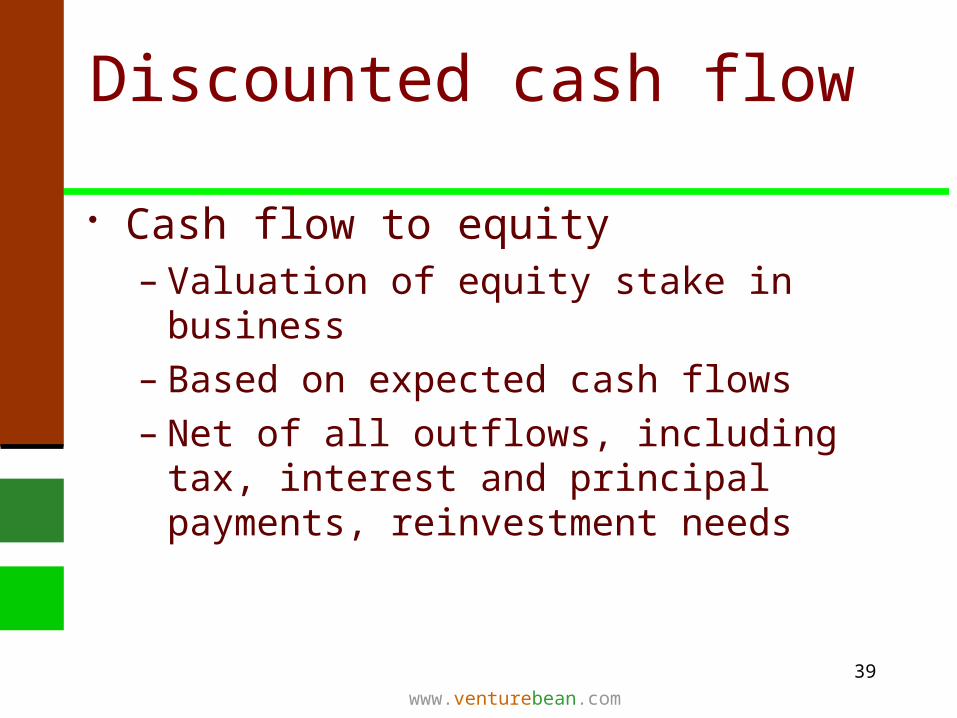

Discounted cash flow

Cash flow to equity– Valuation of equity stake in business– Based on expected cash flows – Net of all outflows, including tax,

interest and principal payments, reinvestment needs

40www.venturebean.com

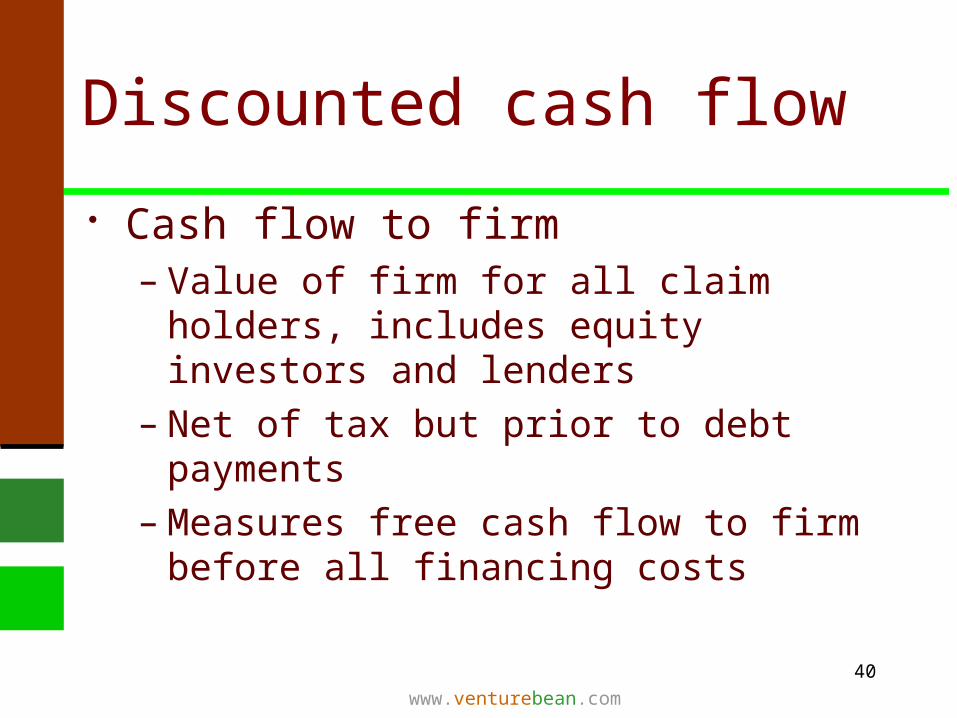

Discounted cash flow

Cash flow to firm– Value of firm for all claim holders,

includes equity investors and lenders– Net of tax but prior to debt payments– Measures free cash flow to firm

before all financing costs

41www.venturebean.com

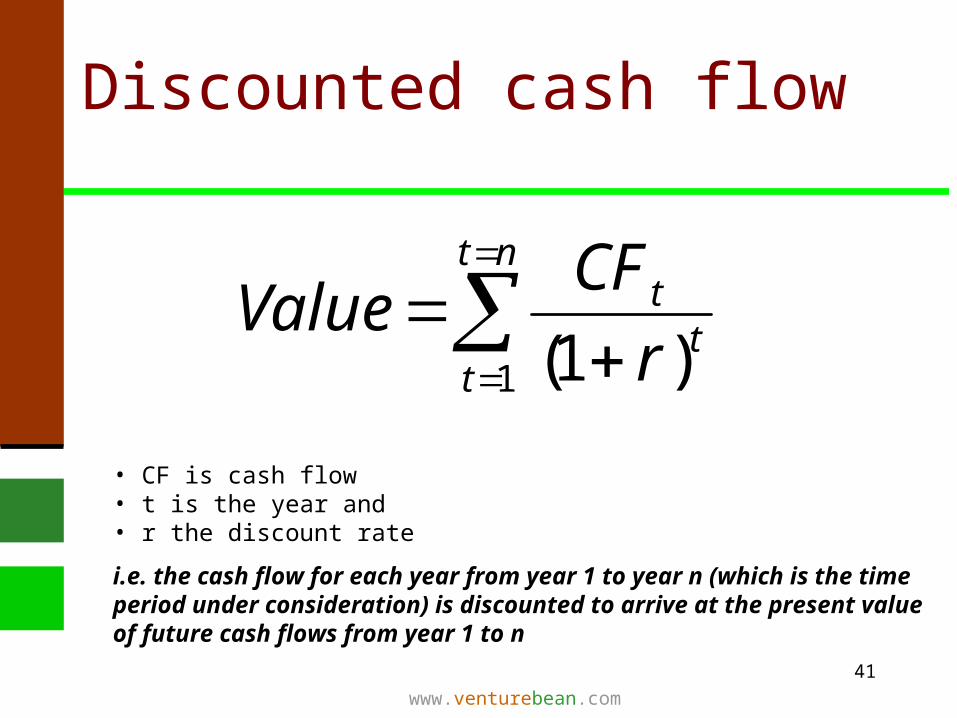

Discounted cash flow

nt

tt

t

r

CFValue

1 )1(

• CF is cash flow • t is the year and • r the discount rate

i.e. the cash flow for each year from year 1 to year n (which is the timeperiod under consideration) is discounted to arrive at the present valueof future cash flows from year 1 to n

42www.venturebean.com

Applicability

Discounted cash flow is based on expected cash flow and discount rates

Sometimes it is difficult to get a reliable estimate for the future and the valuation model may need modification

43www.venturebean.com

Limitations

Companies in difficulty– Negative earnings– May expect to lose money for some

time in future– Possibility of bankruptcy– May have to consider cash flows after

they turn negative or use alternate means

44www.venturebean.com

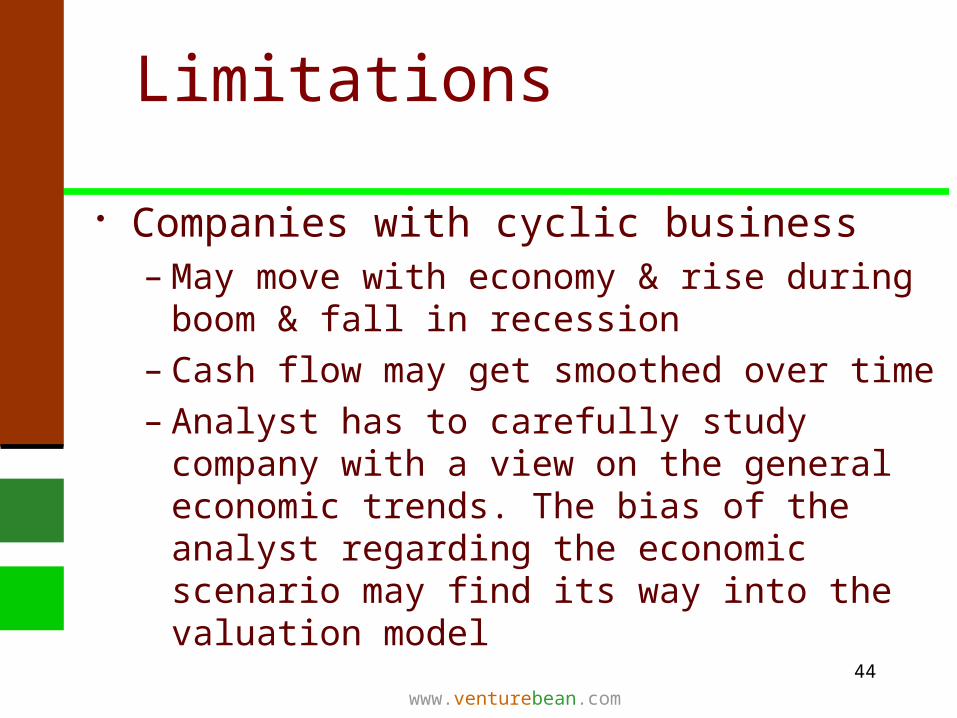

Limitations

Companies with cyclic business– May move with economy & rise during

boom & fall in recession– Cash flow may get smoothed over time– Analyst has to carefully study company

with a view on the general economic trends. The bias of the analyst regarding the economic scenario may find its way into the valuation model

45www.venturebean.com

Limitations

Unutilised assets of business– Cash flow reflects assets utilised by

company– Unutilised and underutilised assets may

not get reflected in the valuation model– This may be overcome by adding value

of unutilised assets to cash flow. The value again may be on assumption of asset utilisation or market value or a combination of these

46www.venturebean.com

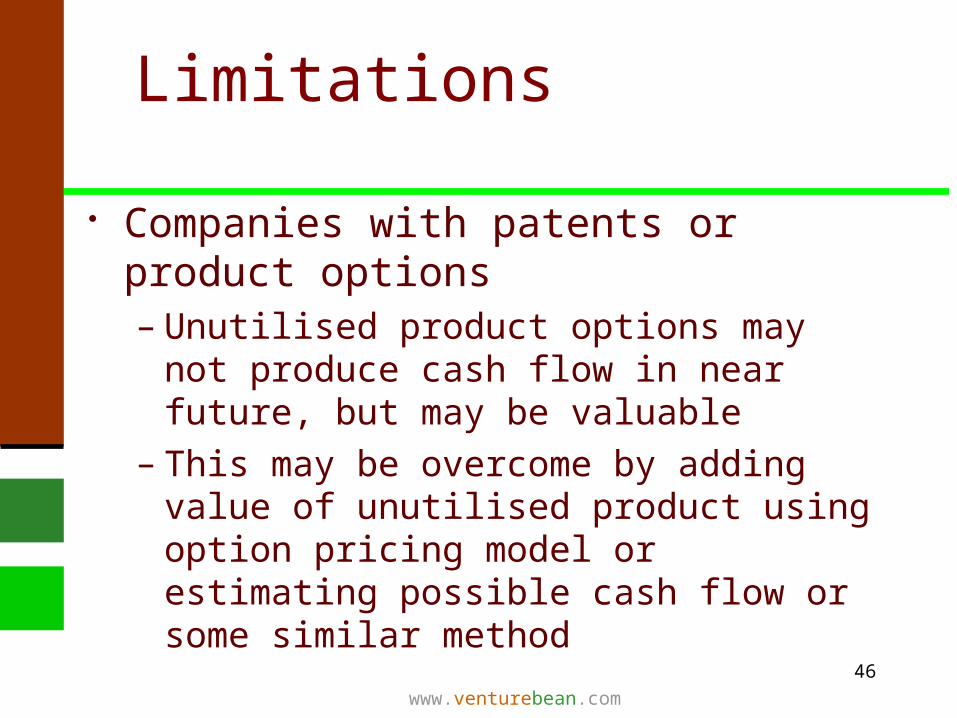

Limitations

Companies with patents or product options– Unutilised product options may not

produce cash flow in near future, but may be valuable

– This may be overcome by adding value of unutilised product using option pricing model or estimating possible cash flow or some similar method

47www.venturebean.com

Limitations

Companies in process of restructuring– May be selling or acquiring assets– May be restructuring capital or

changing ownership structure– Difficult to understand impact on cash

flow

48www.venturebean.com

Limitations

Companies in process of restructuring– Firm will be more risky, how can this

be captured?– Historical data will not be of much

help– Analysis should carefully try to

consider impact of such change

49www.venturebean.com

Limitations

Companies in process of M&A– Estimation of synergy benefit in terms

of cash flow may be difficult– Additional capex may be calculated

based on inadequate information or limited data

– Difficult to capture effect of change in management directly in cash flow

– Analyst should try to study impact of M&A with due care

50www.venturebean.com

Limitations

Companies in process of M&A Historically, many M&As have not

done as well as expected. Many times this has been attributed to valuation being too high. To minimise this risk of over valuation, a proper due diligence review (DDR) exercise is to be done, with one of the mandates for this being careful review of the value drivers and the business proposition.

51www.venturebean.com

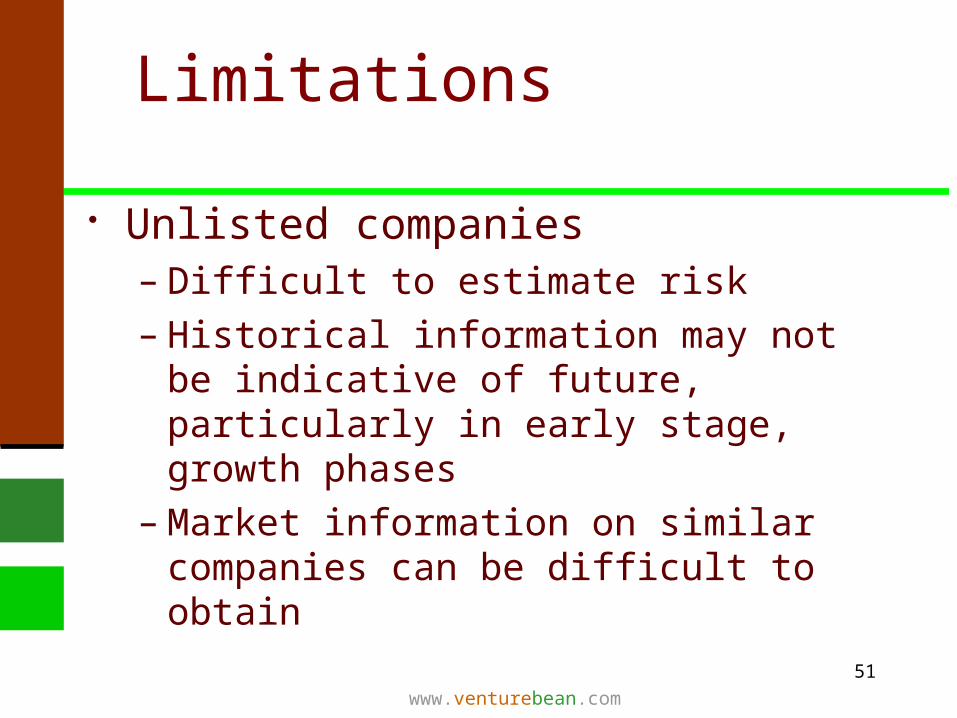

Limitations

Unlisted companies– Difficult to estimate risk– Historical information may not be

indicative of future, particularly in early stage, growth phases

– Market information on similar companies can be difficult to obtain

52www.venturebean.com

MARKET BASED METHOD

53www.venturebean.com

Market based method

Also known as relative method Assumption is that other firms in

industry are comparable to firm being valued

Standard parameters used like earnings, profit, book value

Adjustments made for variances from standard firms, these can be negative or positive

54www.venturebean.com

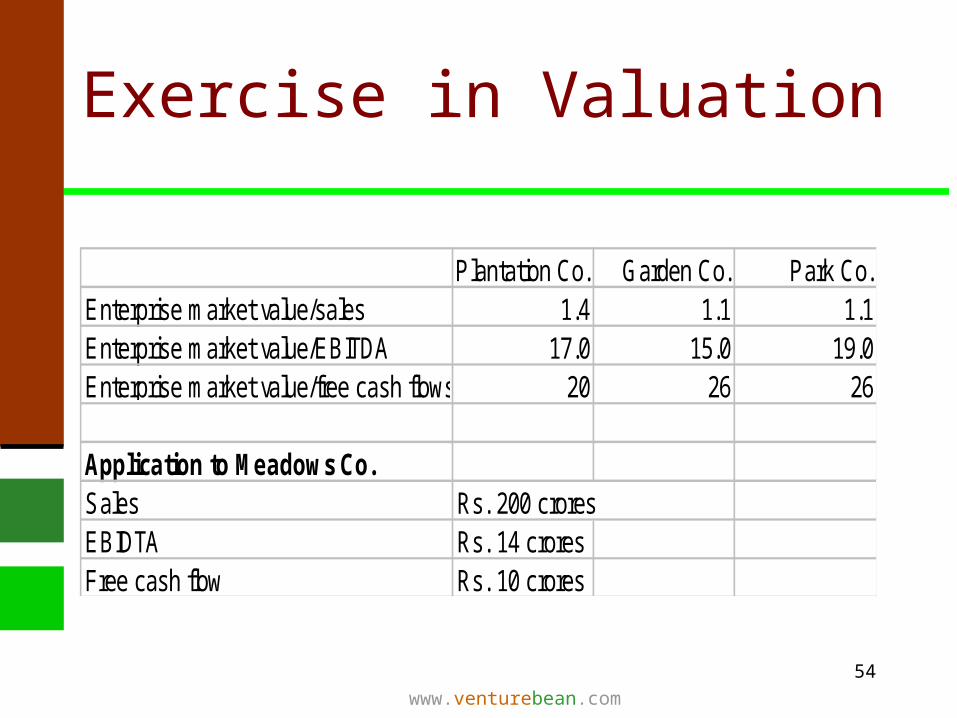

Exercise in Valuation

Plantation Co. Garden Co. Park Co.Enterprise market value/sales 1.4 1.1 1.1Enterprise market value/EBITDA 17.0 15.0 19.0Enterprise market value/free cash flows 20 26 26

Application to Meadows Co.Sales Rs. 200 croresEBIDTA Rs. 14 croresFree cash flow Rs. 10 crores

55www.venturebean.com

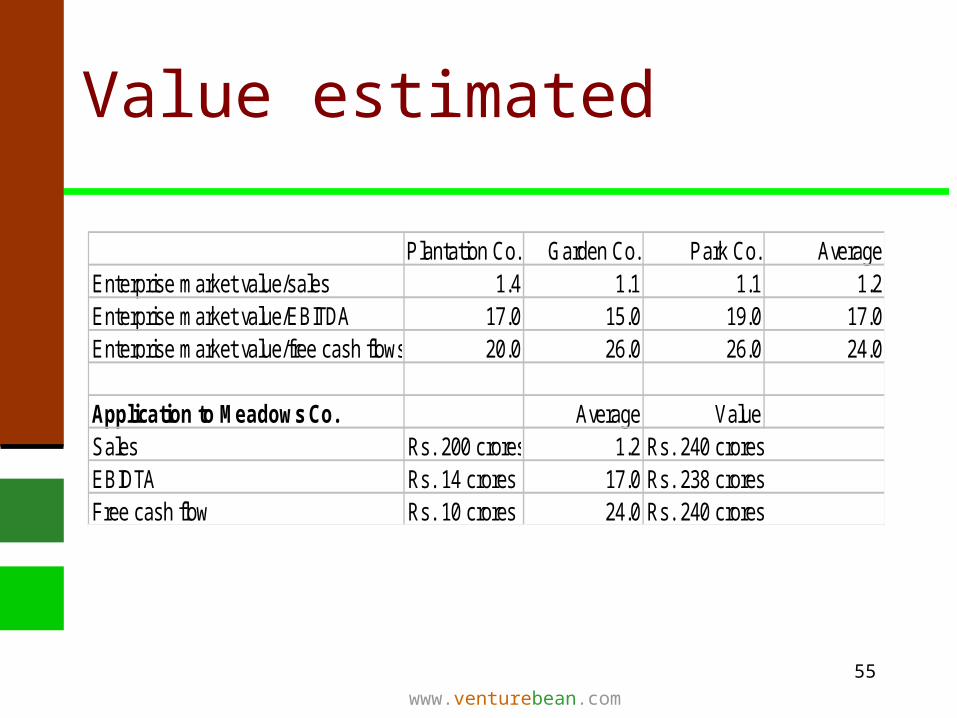

Value estimated

Plantation Co. Garden Co. Park Co. AverageEnterprise market value/sales 1.4 1.1 1.1 1.2Enterprise market value/EBITDA 17.0 15.0 19.0 17.0Enterprise market value/free cash flows 20.0 26.0 26.0 24.0

Application to Meadows Co. Average ValueSales Rs. 200 crores 1.2 Rs. 240 croresEBIDTA Rs. 14 crores 17.0 Rs. 238 croresFree cash flow Rs. 10 crores 24.0 Rs. 240 crores

56www.venturebean.com

Exercise in Valuation

Papers Co Docs Co. Prints Co.Enterprise market value/sales 2.6 1.9 0.9Enterprise market value/EBITDA 10.0 21.0 4.0Enterprise market value/free cash flows 21.0 30.0 24.0

Application to PenPencil Co.Sales Rs. 300 croresEBIDTA Rs. 15 croresFree cash flow Rs. 7.5 crores

57www.venturebean.com

Value estimated ?

Papers Co Docs Co. Prints Co. AverageEnterprise market value/sales 2.6 1.9 0.9 1.8Enterprise market value/EBITDA 10.0 21.0 4.0 11.7Enterprise market value/free cash flows 21.0 30.0 24.0 25.0

Application to PenPencil Co. Average ValueSales Rs. 300 crores 1.8 Rs. 540 croresEBIDTA Rs. 15 crores 11.7 Rs. 175.5 croresFree cash flow Rs. 7.5 crores 25.0 Rs. 187.5 crores

Since multiples differ, this cannot be used as a dependable guide for valuation

58www.venturebean.com

Relative Valuation

Using fundamentals– Valuation related to fundamentals of

business being valued

Using comparables– Valuation is estimated by comparing

business with a comparable fit

59www.venturebean.com

Relative Valuation

Using fundamentals for multiples to be estimated for valuation– Relates multiples to fundamentals of

business being valued, eg earnings, profits

– Similar to cash flow model, same information is required

– Shows relationships between multiples and firm characteristics

60www.venturebean.com

Relative Valuation

Using Comparables for estimation of firm value– Review of comparable firms to

estimate value– Definition of comparable can be

difficult– May range from simple to complex

analysis

61www.venturebean.com

Applicability

Simple and easy to use Useful when data of comparable

firms and assets are available

62www.venturebean.com

Limitation

Easy to misuse Selection of comparable can be

subjective Errors in comparable firms get

factored into valuation model

63www.venturebean.com

VALUATION: What it depends on

64www.venturebean.com

Valuation depends on

Management team Historical performance Future projections Project, product, USP Industry scenario Country scenario Market, opportunity, growth

expected, barriers to competition

65www.venturebean.com

Valuation depends on

Nature of transaction Whether 1st round or later round Whether family and friends or other parties Amount of money required Stage of company - early stage, mezzanine

stage (pre-IPO), later stage (IPO)

66www.venturebean.com

Valuation depends on

Strategic requirements and need for transaction

Demand / supply position Flavour of the season

Initial ballpark valuation can alsobe a deal issue

67www.venturebean.com

VALUATION: Process

68www.venturebean.com

Process of valuation

Consider Net assets tangible and intangible Financial data Historical information Company info Industry info Economic environment

69www.venturebean.com

Process of valuation

Include elements of cash, costs, revenues, markets

Plan long term not short haul Use more than one model Discount for risks, assign probabilities Arrive at range

A valuation range is preferable to a single number

70www.venturebean.com

Process of valuation

Finally after arriving at the value rangeraise some fundamental questions

Does the value reflect the past performance and the expected future?

Does the value reflect the USP as compared to competition?

Does the value reflect the quality of the management?

71www.venturebean.com

Process of valuation

The last mile…

Does the valuation reflect the picture you have of the business?

Would you be willing to pay this price?

72www.venturebean.com

Valuation: for investment

Valuation is perception in the eye of the beholder

It is subject to negotiation

InvestorInvestorValue

CompanyCompanyValue

73www.venturebean.com

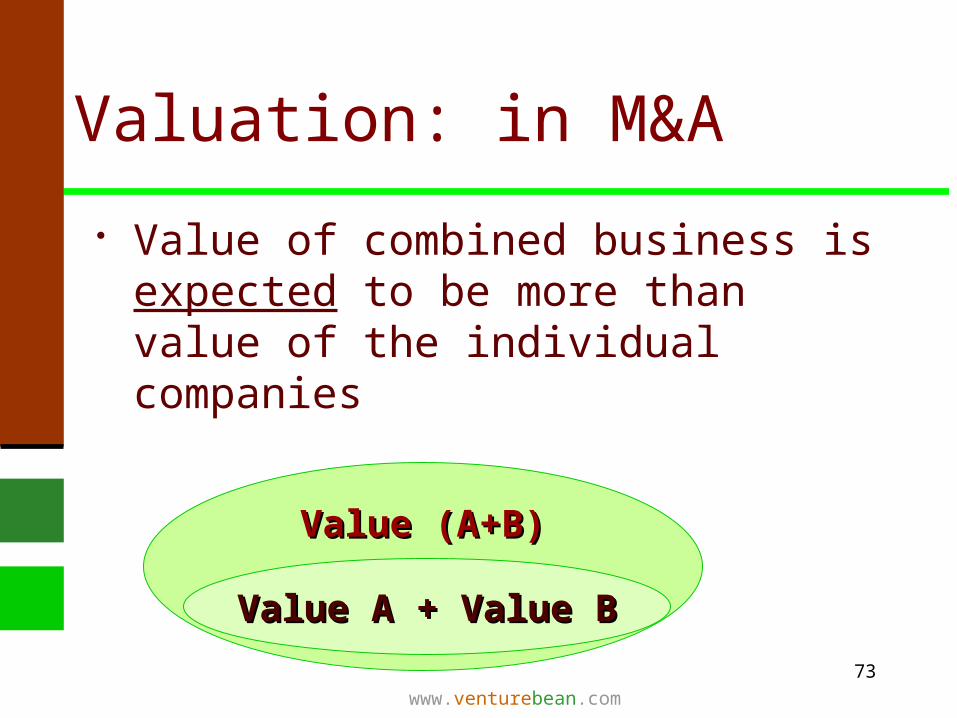

Valuation: in M&A

Value of combined business is expected to be more than value of the individual companies

Value (A+B)Value (A+B)

Value A + Value BValue A + Value B

74www.venturebean.com

APPLICATION OF VALUATION MODELS

In special cases

75www.venturebean.com

Multi business models

The entire business is valued as a sum of the parts

Valuation depends on successful management of different units

Strategic decisions usually occur at each business unit level

To understand the company one needs to first understand the opportunities and threats faced by each business unit

76www.venturebean.com

Multi business models

Valuation of company that is based on valuation of individual business units provides deeper insight

Valuation of individual business units also helps understand whether the company is more valuable as a whole or in parts and to understand where the value is (eg. in some units or in the company as a whole)

77www.venturebean.com

Multi business models

Particularly useful in restructuring and reworking business and financial strategy of the business going ahead

Helps understand and get a better picture of costs of the corporate office and understand allocation of these costs and whether these can be reduced

78www.venturebean.com

Multi business models

Identifying business units can be complex

Cash flows projection can be complex and interdependent on different units

Allocation of corporate office costs and other company costs/benefits may be difficult

79www.venturebean.com

Multi business models

A business unit is identified as one which can be split off as a stand alone unit or sold to another enterprise– Units are to be logically separable– They should not have depend

production/sales/distribution etc.– Some joint products may fall under one unit, if

there is interdependency which calls for this– If there is limited interdependency, this may

be viewed by considering transfer pricing and whether transactions could be considered ‘arms length’

80www.venturebean.com

Multi business models

Allocation of corporate costs including some or all of these:– Salary and other costs of key

management – Board costs– Corporate administration costs– Costs of listing as a public company– Advertising and marketing costs

81www.venturebean.com

Multi business models

Allocation methods are to be carefully thought through and could be a combination of different methods for different costs, including– Based on time spent (time sheets)– Advertising based on revenue

82www.venturebean.com

Multi business models

Benefits are also to be incorporated, including– Saving on operational costs– Information/communications– Tax benefits / shields (ie one loss producing

unit would provide a shield to another profit making one – important when one is considering a split up / hive off of some units)

– Intangible benefits – can these be quantified? (Eg key person in management team / Board)

83www.venturebean.com

Multi business models

Difficulties and concerns– Partial holdings in units (taken as a

percentage of ownership of business unit value)

– Double counting may occur– Allocation may pose difficulties– Interdependency may not be easy to

separate – Intangibles cannot be easily quantified– Transfer pricing to be viewed in the

regulatory context

84www.venturebean.com

Mergers/Acquisitions

These have become very important as companies try to grow inorganically or network to exploit possible synergies

Most senior executives may be involved in such transactions– Directly or indirectly– In the buy side or target side

85www.venturebean.com

Mergers/Acquisitions

Rationale for the proposed transaction is to be understood

Synergy – Revenues– Costs– Intangibles

Control/ dominance in market Under valuation perceived

(LBOs/LBIs)

86www.venturebean.com

Mergers/Acquisitions

Studies show that generally acquired company shareholders gain

Reasons for failure– Poor post acquisition management– Over payment for target

87www.venturebean.com

Mergers/Acquisitions

Research has suggested that the following factors have resulted in positive deals– Bigger value creation overall– Lower premiums paid– Better run by acquirers

88www.venturebean.com

Mergers/Acquisitions

Overpayment could be because of a combination of these factors:

Market potential - overoptimistic appraisal

Synergy – overestimated Due diligence – inadequate Bidding – excessive

89www.venturebean.com

Mergers/Acquisitions

Synergy– Operational (vertical and horizontal

M&A eg backward integration, captive customer)

– Functional (Production, sales)– Benefits (tax, control etc.) and impact

on cash flow to be quantified (eg. increased sales, reduced wages) keeping timing in mind

90www.venturebean.com

Mergers/Acquisitions

LBOs/LBIs Initially high leverage May be followed by rapid reduction

in debt This impacts business risk which

will change

91www.venturebean.com

Cyclic companies

Fluctuation in earnings over different periods in time

One approach taken is that if done correctly, DCF evens out fluctuations /volatility in the long term because all value is reduced to a single period

However position of current year in cycle, needs to be factored in as it is considered as base year

92www.venturebean.com

Cyclic companies

Growth rates in different years need to be adjusted based on expected cycles

There may be difficulty in estimating cycles accurately

If future differs from past, this would impact forecasts and therefore impact valuation

93www.venturebean.com

Cyclic companies

It is important to have different possible scenarios and arrive at a range of values should be arrived

This is useful as managers can implement decisions based on the valuation depending on the stage of the cycle the company is in (eg. for buyback, issue of shares, raising of debt funds)

94www.venturebean.com

Companies in distress

May have one or all these problems Negative cash flow Unable to pay back debt Liquidity crunch

95www.venturebean.com

Companies in distress

Valuing the company based on expectation of turnaround

Assume the company will be healthy soon and look at future based on a healthier past

Analyse based on future expected transaction in which cash flow is identifiable

96www.venturebean.com

Companies in distress

Liquidation value Sum of parts based on individual

identification of units – Consider different alternate scenarios

of units in different combinations– Consider all assets tangible and

intangible Cap at possible realisable value

97www.venturebean.com

Cross border transactions

There are special issues in such cases, including

Foreign exchange fluctuations Difference in regulations

(statutory, accounting) Estimating cost of capital Country risks Inter country transactions

98www.venturebean.com

Cross border transactions

Analyse past performance Translate Fx into host country

financials, based on accounting standards

Include any tax implication (eg subsidiary may pay dividend tax only if this is paid out)

Arrive at FCF and convert to domestic currency

99www.venturebean.com

Cross border transactions

Consider impact of restrictions on transfer of currency

In place of FCF, multiples may also be used

100www.venturebean.com

Cross border transactions

View impact of accounting regulations on financials– Provisions (pension)– Goodwill (amortised or against equity)– Revaluation of assets– Deferred taxes – Fx translations– Non operating assets– Tax

101www.venturebean.com

Cross border transactions

Cost of capital– Market risk premium difficult to

estimate, sometimes proxies are used– Risks in changing regulations – Political risks– Illiquid capital markets– Restrictions on cash flows

102www.venturebean.com

Privatisation

Listed companies have the following which may lead to increased costs

Increase in information to be provided per listing requirements

Separation of ownership and management (good/bad?)

Focus on stock prices at the cost of fundamental growth, in many cases

103www.venturebean.com

Privatisation

Implication of privatisation Reduced access to finance Reduced visibility of company (impact

on brand) Reduced requirement for

compliance/governance

Impacts to be factored in for valuation, to the extent possible