v g ramakrishnan, sr.director, automotive & transportation

TRANSCRIPT

3

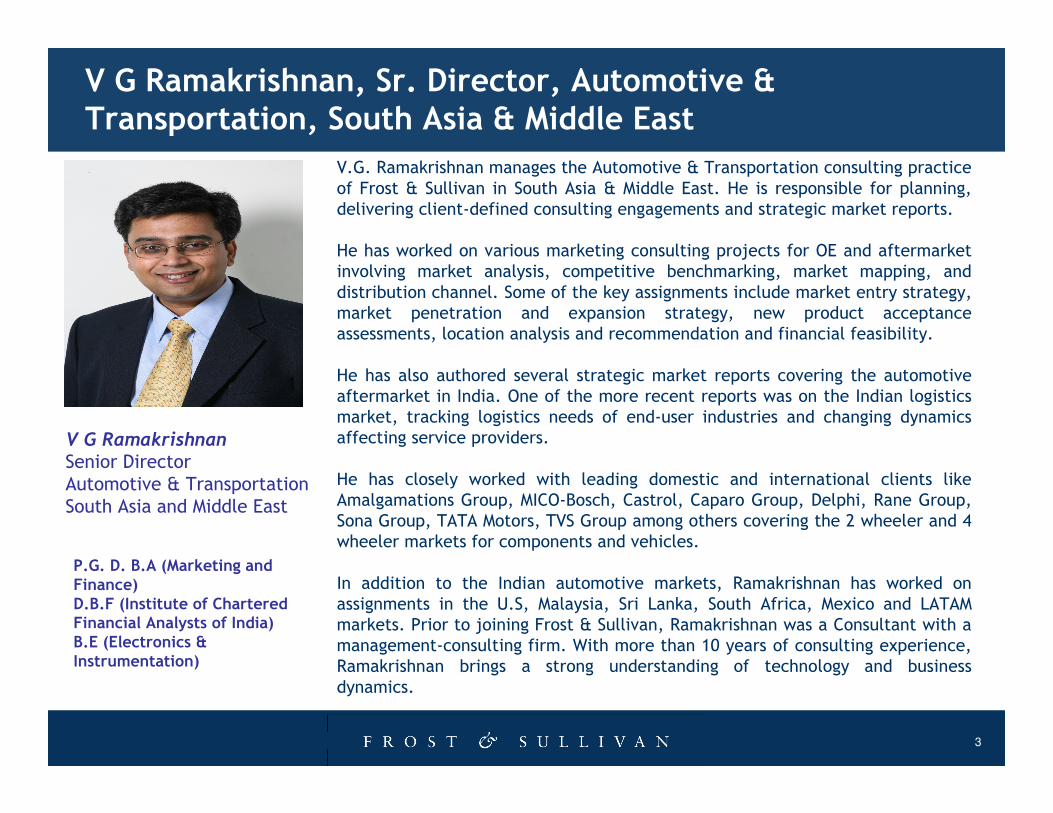

V G Ramakrishnan, Sr. Director, Automotive & Transportation, South Asia & Middle East

V G Ramakrishnan

Senior Director

Automotive & Transportation

South Asia and Middle East

P.G. D. B.A (Marketing and Finance)D.B.F (Institute of Chartered Financial Analysts of India)B.E (Electronics & Instrumentation)

V.G. Ramakrishnan manages the Automotive & Transportation consulting practice

of Frost & Sullivan in South Asia & Middle East. He is responsible for planning,

delivering client-defined consulting engagements and strategic market reports.

He has worked on various marketing consulting projects for OE and aftermarket

involving market analysis, competitive benchmarking, market mapping, and

distribution channel. Some of the key assignments include market entry strategy,

market penetration and expansion strategy, new product acceptance

assessments, location analysis and recommendation and financial feasibility.

He has also authored several strategic market reports covering the automotive

aftermarket in India. One of the more recent reports was on the Indian logistics

market, tracking logistics needs of end-user industries and changing dynamics

affecting service providers.

He has closely worked with leading domestic and international clients like

Amalgamations Group, MICO-Bosch, Castrol, Caparo Group, Delphi, Rane Group,

Sona Group, TATA Motors, TVS Group among others covering the 2 wheeler and 4

wheeler markets for components and vehicles.

In addition to the Indian automotive markets, Ramakrishnan has worked on

assignments in the U.S, Malaysia, Sri Lanka, South Africa, Mexico and LATAM

markets. Prior to joining Frost & Sullivan, Ramakrishnan was a Consultant with a

management-consulting firm. With more than 10 years of consulting experience,

Ramakrishnan brings a strong understanding of technology and business

dynamics.

360 Degree Analysis of the Global Electric

Vehicles Market

Electric Vehicles Market

- Opportunities and Implications

Presented by V G Ramakrishnan

October 23, 2009

2

Electric Vehicles Market Overview, Technology Roadmaps and Infrastructure Trends

Voice Of The Customer – Customer Feedback On EVs

Conclusions And Recommendations

Market Size and Forecasts

Table of Contents

Definitions and History

3

History of Electric Vehicles (1834 – 2009)

Source: Frost & Sullivan

2002: Toyota RAV4-EV retail sales; their estimated 2-year supply sold out in 8 months.

1990: U.S. 1990 Clean Air Act Amendment, the U.S. 1992 Energy Policy Act, and regulations issued by the California Air Resources Board (CARB)., several states have issued Zero Emission Vehicle requirements

1834: Thomas Davenport invents the battery electric car – batteries were not rechargeable

1859: Gaston Plante invented rechargeable lead-acid batteries.

1897: First vehicle with power steering – an EV. Electric self-starters 20 years beforeappearing in gas-powered cars

1902: The Phaeton had a range of 18 miles, a top speed of 14 mph and cost $2,000

1900: All cars produced: 33% steam cars, 33% EV, and 33% gasoline cars

1910: Electric vehicle production peaked

1935: The decline of the electric vehicle was brought about and disappeared by 1935

1921: Federal Highway Act. By 1922, federal match (50%) for highway construction andrepair (for mail delivery).

1990: GM shows their production EV initially named, Impact; later it was re-named the EV-1

1996 - 97: GM begins production of the EV-1 . Toyota Prius hybrid gas-electric vehicle unveiled at the Tokyo Auto Show

1998: The Toyota RAV4 sport

utility, the Honda EV Plus sedan,

and the Chrysler EPIC minivan.

These three vehicles were all

equipped with advanced nickel

metal hydride battery packs

2003: ZEV Mandate weakened to allow ZEV credits for non-ZEV s. Toyota stops production of the RAV4-EV; Honda stops lease renewals of the EV-Plus; GM does the same for the EV-1

1960’s: The first Battronic electric truck was delivered to the Potomac Edison Company in 1964. This truck was capable of speeds of 25 mph, a range of 62 miles and a payload of 2,500 pounds

1894 -

1935

1960 -

2003

2000 : The Honda Insight is the first production vehicle to feature Honda's Integrated Motor Assist system. The first-generation Insight was produced from 2000 to 2006 as a three-door hatchback.

4

Definitions – Battery Electric Vehicles

Battery Electric Vehicles

Electric vehicles use electric motors instead of an internal combustion engine (ICE) to propel a vehicle. The electric power is derived from a battery of one of several chemistries including Lead Acid, Nickle Metal Hydride (NiMH), and Lithium-Ion (Li-ion).

Neighborhood Electric Vehicles (NEVs)

NEV is a US DOT

classification for vehicles

weighing less than 3,000 lbs

(GVW) and top speed of 25

mph. NEVs generally are

restricted to operate on

streets with a speed limit of

35 mph or less.

A city car is a European

classification, for a small

and light vehicle intended for

use in urban areas although

they can operate in mixed

city-highway environment. In

Japan, city cars are called

kei cars.

Extended-Range EVs (eREVs)

A plug-in hybrid electric

vehicle (PHEV) with a IC

engine or other secondary

sources connected to a

generator to supply the

batteries. The drive range

and speeds are comparable

to IC engine vehicles.

High-Performance EVS (HPEVs)

Sporty PHEVs or battery

electric vehicles with top

speeds exceeding 100 mph

and driving range

exceeding 100 miles. The

price of these vehicles is

expected to approach or

exceed $100,000.

GEM e2, e4, e6; REVA G-

Wiz i; ZENN; ZAP etc.

Smart EV, Th!nk City, BMW

Mini and others

Chevy Volt, Toyota Prius

PHEV, Chrysler Sedan and

others

Tesla, Fiskers - Karma,

Venturi - Fetish, Lightning

GT

City Electric Vehicles

(CEVs)

5

Current Electric Vehicle Market Structure : Provides Opportunity to Enter New Fields

Could work to improve charging time and safety

Infrastructure

supplier

Key Responsibility:

Development of Charging

Infrastructure

Key Responsibility:

Promotion of EV use

UtilitiesIntegrators

(Project Better

Place)

OEMs

System/Battery Manufacturers

GovernmentCharging Station

Manufacturers

Integrators to create partnerships with Utilities, OEMs

and Government

Subsidies for

EV purchase

and

investment in

R&D to reduce

emissions

Lower fuel

dependency by

expanding the

use of

renewable

energy sources

Supplies

infrastructure to

distribute their

energy

Cooperation to simultaneously promote EV use and electricity as a fuel

Development of

performing

batteries

6

Hours to Charge

37%

47%

0%

20%

40%

60%

80%

100%

120%

1 2 3 4 5 6 7 8 9 10 11 12 or

moreHours to Charge

37%

47%

0%

20%

40%

60%

80%

100%

120%

1 2 3 4 5 6 7 8 9 10 11 12 or

more

“My wish list for EV

specification..”

UK Consumer

Miles

Pric

e (£

)

To

p S

pe

ed

Time (Hr)

Technology and Infrastructure development to be tuned towards consumers needs and driving habits

50.20%

0%

20%

40%

60%

80%

100%

101+91 -100

81 -90

71 -80

61 -70

51 -60

41-50

< 40

50.20%

0%

20%

40%

60%

80%

100%

101+91 -100

81 -90

71 -80

61 -70

51 -60

41-50

< 40

82.00%

76.70%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

>251 226 -250

176 -200

126 -150

76 -100

51 -75

26 -50

Up to25

12 ormore

82.00%

76.70%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

>251 226 -250

176 -200

126 -150

76 -100

51 -75

26 -50

Up to25

12 ormore

Price

62.50%

44.20%

0%

20%

40%

60%

80%

100%

120%

2000 4001 to

6000

8001 to

10000

12001 to

14000

16001 to

18000

More

than

20001

• Ideal hours to charge that will result in maximum uptake of potential EV customers in UK

• Ideal speed characteristics that will result in maximum uptake of potential EV customers in UK

• Ideal distance characteristics that will result in maximum uptake of potential EV customers in UK

• Ideal price range that will result in maximum uptake of potential EV customers in UK

Miles/hr

Miles Source: Frost & Sullivan

7

EV Customer Segmentation and Targeting Uses Out of Box Thinking and Will be Depended Upon Usage Characteristics and Specific EV Factors

Weekend

vacation /

leisure driving

11%

Retail

Shopping

8%

Visiting

friends or

family

Supermarket

Shopping

15%

Commuting to

and from work

26%

Evening

entertainment

5%

Recreational

activities

5%Taking and

picking kids

up from

school

7%

To use while

at work such

as visiting

clients

7%

Others

1%

London Private Users: Main use of Private Car, 2008

Requirement for EV ����

Others

Evening Entertainment

Recreational activities

Taking and picking kids

up from school

To use while at work

Retail shopping

Weekend vacation /

leisure driving

Visiting friends or family

Supermarket shopping

Commuting to and from

work

Average trips

over 100 miles

Average hours

parked at location

Average miles

per trip

EV FactorsCar use

HighLow

• Innercity commuters (travelling within the M25) represent almost 60% of consumers that use a vehicle to travel to work

8

Key Challenges in Electric Vehicle Market Development

Well To Wheel

ViableBusiness

ModelStandardization

Battery Technology

Charging Infrastructure

ElectricVehicle

Eco System

9

• Improved range extension will see charging points extend beyond city limits to urban and sub-urban areas with emphasis

on both normal and fast charging stations

50+

25

10

Normal Charging Spots

Fast Charging Spots

Mile Post

Commercial Facilities

• E.g., Dept. Stores, hotels,

malls

• Special parking lot for EV

next to handicap

provision

• Free charge (1-2 hrs)

using AC outlet

Pub. & Pvt. Parking Place

• Special EV parking space

• Free charging from charging outlet

Home

• Normal charging by nigh time

discounted electricity

• Special charging plug at home

Car Dealers, Public

Building

• Current strategic

locations for fast

charging

• 15 min. charge to yield

60 miles range

PRESENT DEVELOPMENTS WITH RESPECT TO ELECTRIC CHARGING STATIONS (2008 - 2011), EUROPE

Current EV Range (60-80 Miles On Full Charge) Limits Developments Of Infrastructure To City Limits.

Source: Frost & Sullivan

10

Over 1500 charging stations globally –OEM leading the initiative

SpainUnited States

Monaco

China

Japan

The U.K.

1. Number of charging stations - /above 500

2. Key participants -

Coulomb Tech, Eaton, EVOasis and others

Germany France

1.Number of charging stations –approximately 380

2. Key participants -

Park & Charge

1. Number of charging stations -

approximately 260

2. Key participants -

DBT, STGE,Circuritor /and others

1. Number of charging stations –approximately 190

2. Key participants -Elektromotive and Park & Power

1. Number of charging stations - less than 10

2. Key participants - NA

1. Number of charging stations - above 75

2. Key participants - NA

1. Number of charging stations - above 100

2. Key participants - NA

1. Number of charging stations –approximately 176

2. Key participants - NA

Norway

1. Number of charging stations –approximately 40

2. Key participants - NA

Portugal

1. Number of charging stations –approximately 20

2. Key participants - EDP

Italy

1. Number of charging stations –approximately 121

2. Key participants -

ACI Informatica

Australia

1. Number of charging stations -approximately20

2. Key participants - NA

SwitzerlandAustria

1. Number of charging stations –approximately 80

2. Key /participants -

Park & Charge

1. Number of charging stations -approximately 200

2. Key participants -

Park & Charge

Demark

1. Number of charging stations –approximately 40

2. Key participants - NA

Sweden

1. Number of charging stations –approximately 150

2. Key participants - NA

Source: Frost & Sullivan

11

Charging Stations Evolution Will Focus On Charging Time, Space Optimisation, Service Integration And Multi-functionality

Source: Frost & Sullivan

Slow charging - onboard

Mode of Charging Fast charging – mostly off board

Battery Swapping

Type of Charging Station

2005 2010 2015

Bollard / Ground Fixed

Wall mounted / Pole mounted

Dedicated charging station with lounge

Open to public / Free of charge

Subscription models

Roaming / reciprocal sharing and utility reconciliation

Smart Card (Oyster) Type

Battery chemistry sensing

Vehicle diagnosis and data collection

Solar panels for energy generation

Entertainment added services

Socket Type

Retractable arm

Automatic / Inductive

Charging Mechanism

Billing System

Extended Functionality

12

50+

Highway - Motels / Dining

• High potential of fast charging

stations seen to extend range of

EV’s

• Battery Swapping stations likely

to gain ground as well

Long Duration Stay

• Multiplexes, railway stations are

strategic spots where consumer

“Park & Pickup” intervals are

ideal for 80% charge

• Conventional charging stations

preferred over fast charging

Corporate Offices / Independent Houses

10

Short-Medium Duration Stay

• Dining & Restaurants, Golf courses,

movie theatres

• Fast charging stations attractive

• EV Range extension will see the rise of urban/sub-urban consumers using EV

• Fast charging stations seen across strategic locations on highways like motels, dining centres etc

Normal Charging Spots

Fast Charging Spots

Mile Post

Future Developments With Respect To Electric Charging Stations (2010-2015) : Target Focus on Parking Slots With Over 30 Minute Journey Stops

Source: Frost & Sullivan

13

Smart House with EV car generator

Smart Grid Control Centre

Wind Power

Solar Power

Energy Storage

Hospital

Pre

20

08

Time Frame

Utility Power Generation InfrastructureTopics

Low

High

20

08 -

201

5

Implications on Utilities

Conventional Grid and Infrastructure

Houses

Power Station

Office Building

Factory

Transformation of` Conventional Grid ����Energy Internet

• Centralised power stations

• Centralised power generation resulting in substantial power and transmission losses

• Several small generating facilities –wind, solar

• Offices, hospitals selling excess energy back to grid

• EV as generators when not in use

• Increased efficiencies and reduced operational cost and environmental affects

EV Support Capability

ROI Opportunities

Own Generation

UTILITY• Consumers – Utility Bills• Partnership with renewable

energy generators• Charging Stations• Parking Space• Govt - Carbon Trading• Venture Capital• Garage and Stores SupportEXTERNAL• Battery Manufacturers• Telecom Providers• Smart Card • Banks, insurance etc.• Green Collared Jobs• Recycling• Battery Servicing - Swapping

Shift from “Dumb Grid” to “Smart Grid” set the earliest precedence on developments towards the EV support infrastructure

40 %

development

80 %

development

• Limited to Grid and Utility industry

14

IN-BUILT SOLAR PANELS

• Generating proprietary electricity

•Will get energy from Utilities through groundwork

INTERACTIVE LCD DISPLAY

•Payment option - either manually through Debit/Credit Card or automatically through RFID

•Club with parking charges

•Opportunity to place orders in nearby coffee centres, restaurants or internet bays

•Vehicle Diagnostic Interface

CHARGING TYPE OPTIONS

•Compartments to provide charging capabilities for up to 4 vehicles at a time

•Option to provide both on-board and off-Board charging

DESIGN BLEND WITH ENVIRONMENT

• Charging posts are specifically designed to blend with a specific cities environment theme

EXTENDED FUNCTIONALITY

• Battery chemistry sensing

• Content delivery for on-board systems like MP3 stereos, TiVO systems and back-seat entertainment

• Gaming Options – coin fed for additional revenue generation

• Vehicle Tracking System GARAGE SERVICES

• Future functionality of automotive diagnostics

• Communicate any or all (by law) or requested (by mfg) access to in-car diagnostic or fault tolerance modules in real time to a shared database

• Use unique IP address to store repair data for future access and compliance tracking

MANUFACTURER FOCUSED SERVICES

• Provide billing, roaming, and geo-location reporting and audit trails for reciprocal sharing and utility reconciliation

• Scaleable solution for charge-point installation upgrades

• Employ wireless networking capability and multi-carrier redundancy

Design and Functionality Evolution of Charging Stations (Global), 2009-2015

Diagnostic & Billing Services, Tie-ups With Key Entertainment Industry Services Will Attract Potential Investors To Expand Charging Stations Functionality

Oyster Type Charging Stations

15

Electric Vehicle Technology Roadmap (Global), 2008-2015 - Iron phosphate and Manganese based Li-ion batteries are preferred

Electric Vehicle Market: Technology Roadmap for Electric Vehicles (Global), 2005-2015

Source: Frost & Sullivan

Lead acid

Nickel Metal Hydride

Ba

tteri

es

Sodium Nickel Chloride

Phosphate based

Manganese based

Titanate based

2005 2010 2015 2020

Silica based

Lithium Ion

Zinc Air

Permanent Magnet

Ele

ctr

ic M

oto

rs

Asynchronous

Switch Reluctance

In wheel motors

Motor Power- Up to 70 kW 70 kW – 250 kW

16

Electric Vehicle Technology Roadmap (Global), 2008-2015 - Charging times to drop from 6-8 hours currently to <30 minutes by 2015

Electric Vehicle Market: Technology and Product Roadmap for Electric Vehicles (Global), 2005-2015

So

urc

e:

Fro

st

& S

ulliv

an

Driving Distance/charge-up to 55 Miles

Charge Time – 6 to 8 hrs

Slow charging - onboard

Infr

as

tru

ctu

rep

erf

orm

an

ce Up to 125 Miles

Battery Capacity – up to 16kWh

Motor Power- Up to 70 kW

Fast charging – mostly off board

Battery Swapping

190 + Miles

< 1 hour < 15 minutes

Up to 50 kWh 75 kWh +

70 kW – 250 kW

ELECTRIC RANGE

BATTERY CAPACITY

MOTOR POWER

Up to 40 miles Up to 100 miles

7kWh – 15kWh 16kWh – 25kWh

50kW – 70kW 70kW – 140kW

CHARGING TIME 2 – 6 hrs 15 mins – 2 hrs

Market for Extended-Range Electric Vehicles: Technology Roadmap for Plug in Hybrid Electric Vehicles

Source: Frost & Sullivan

2005 2010 2015 2020

17

Steering

Electric Vehicle Market: List of New and Evolving Technologies

Electric Vehicles Component and Systems to see a shift from the conventional type; brings about electrification in integrated systems

Power Train Interiors & Acoustics

OthersPower Systems Chassis

Active Front Steering

Steer By Wire

Braking

HBS+EVP

Brake by Wire/ EMB

Engine

Electric Motors – PMM/

Induction/ SR/ In-wheel, Hub

Motors

E-Engine

Gearbox

Integrated transmission

with differential

In-wheel motors w/o

transmission

Batteries

Lithium Ion + Lead Acid for SLI (Optional)

P-Electronics

Stepped DC/DC, DC/AC

Converters, Inverters

Advanced BMS

16-32-bitµ-controllers,

IGBTs, MOSFETs

Charging unit/equipment

Harness

12V/ 300-440V

CAN/TT-CAN/Flex Ray

Cockpit

Battery SOC, Temperature

Indicator

Charging Systems Indicator-Locators\

Motor Vehicle Speed,

Distance Calculator

NVH

High Frequency Isolators

Sound Generators

E-Systems

eHVAC Systems (Electric

Compressors)

Electric Water Pump

Emerging Technologies

Evolving Technologies

Legend:

Range ExtenderModule

Others

Electric Axle and E-AWD

Electric Corner Module

Integrated Battery

Modules

18

Predominantly –the TN 400/230 V Network Systems

Predominantly – the TN 240/120 V Network Systems

TN 240/120V TN 400/230V

TT 400/230V TN/TT 400/230V

NA

230 V

TN 240/120V TN 400/230V

TT 400/230V TN/TT 400/230V

NA

230 V

One of the major challenges is standardisation: Example of energy distribution systems with it's different voltages and safety concepts around the world

Key Western European regions- implementing TT 400/230 V

Current Standards

Energy Transfer System for EV J2293

EV Inductive Coupled ChargingJ1773

EV Conductive Charge CouplerJ1772

ImplementationArea of applicationStandardRegion

Plugs, socket-outlets and couplers for industrial purposes

60309

Electric Vehicle Conductive Charging System

61851

ImplementationArea of applicationStandardRegion

To have a dedicated plug for EV that ensures user safety and could support faster chargingMain EV plug

To provide a wider range of services and make them available for all users regardless of their EV modelCommunication Systems

To ensure viability of battery swapping stations as well as interoperability with all EV modelsBattery swapping standard

Priority in timeImportanceIssue

Unaddressed issues

�Cost reduction through compatible systems

�Safety

�Interoperability of systems

DRIVERS:

Standardization of Electric Vehicle Infrastructure

19

Business Models Analysis : Future Leasing Models To Sell 75% Of EVs; The Rest 25% Sold Traditionally

~ €900- €1500€500- €800Up to €300Up to €150MONTHLY

LEASE

Free car50% car priceNANASUBSIDY

7 years4 yearsNANACONTRACT

Flat: 30,000km/yearFlat: 25,000km/yearFlat: Max 2000km/monthMonthly BillENERGY

Maintenance Package+ 100% Discount

Maintenance Package+ Discount

Energy Package+ Insurance+ Maintenance

Partial battery lease + Electricity

COVER

Full SubsidyPart SubsidyMaintenance PackageEnergy PackageTYPE

Business Model 4Business Model 3Business Model 2Business Model 1

Flexible Contract

Pay as you goMax number of milesUnlimited MilesFlexible Mileage

The customer opts for the number of years and flexible mileage- customized lease

Other Possible Leasing modelsSource: Better Place, Frost & Sullivan

20

• Investment:

• Groundwork

• Installation

• Connection

• Subscription

• Unit Margin

• £ 2,000

• £ 2,500 / postDigging of holes, trenches, laying cable ducting,

installation of ground kit, reinstating of surface

• £ 200 / postConnection and commissioning of the Charging Point

• £ 600 / postSite survey, drawings as necessary, electrical feeder

pillar and installation of feeder pillar

• Capital

Expenditure

• £ 150 / agreed area** / yearConnection & commissioning of the Charging Point

Cost of Manufacturing =

{833 (a) + 2083 (b) +

1250 (c) + 3750 (d)}

Business Opportunities

• 20% on manufacturing cost

• Potential to increase installation across strategic locations- Rail, Golf Course, Shopping Complex

• Opportunity to partner VM’s to expand proprietary solutions across key geographical markets• Opportunity to liaise and partner with government and related organizations, VC and large corporate firms in their green credential pursuit

Co

mp

eti

tio

nP

rod

uct

Desig

nIn

du

str

ies

• SGTE Power (Fr)

• DBT (Fr)

• Transtex (Fr)

• Elektromotive (UK)

• Ciant (Fr)

• Spie-Trindel (Fr)

Initial Short - Term

• Charging Station

Manufacturers

• Utility Companies

a) b)

c) d)

Wall Mounted

Parking Posts

Oyster Type Charging Stations

Bu

sin

ess M

od

el

COST Long - Term

• Aftermarket division of

VM’s

• Government Org.

• Venture Capitalists

• Italian and French

manufacturers

Business Model Analysis : Charging Station Manufacturers Have A High ROI Potential

• Varies by solution

21

Market Expansion Strategy- Better Place Business Model –Better Place

Israel:�Geography�Oil Dependency �Investments and Subsidies

Denmark:� Renewable energy- 60%

�Subsidies

Australia:� Investment Partners�Subsidies

California:� Home & Green mindset�Government investment

Battery Swap Station

Battery Suppliers

Leasing Network

Infrastructure Contractors/

Suppliers

Private Customers

Business Fleets

Electric Utilities

Charging Stations

Services & Subscriptions

Electric Recharge Grid Operator

Revenues from Services

Revenues from Products

Service ModelProduct Model

Better Place- Map of Battery Swap Network in California

100 mile radius

Battery Swap Station

Battery swap stations are located edge of the cities and freeways connecting i m p o r t a n t c i t i e s

� Better Place to build 500,000 recharge stations and network of swap centers in three stages

� Govt. to support of infrastructure and cars- 78% tax on cars replaced by 10% for first 4 years

� Beta country- Investment about $200M. Farthest drive is 250 miles.

� Better Place rises $160 for infrastructure and operations in Denmark.

� Partnered with DONG which has a 60% renewable grid: 18% coming from wind; to double soon.

� Potential scenario- With 0% tax $60,000 car can be bought at $20,000.

� Two strong partners: AGLEnergy provide energy from renewable sources (wind and others). Macquarie provide financial advice and raise $1Billion(AUD) to build initial network.

� Tremendous support from federal government with $500M Green Car Innovation Fund.

Isra

el

Den

mark

Au

str

alia

Business Model- Better Place- Cash rich start up, along with its partners have already raised over $1 Billion on EV infrastructure

Potential Future Markets

So

urc

e:

Fro

st

& S

ull

iva

n

22

Global Electric Vehicle Unit Forecast by Scenarios- Oil price uncertainties, government support and technology breakthroughs are clear drivers of EVs

Scenario Analysis of Global Electric Vehicle Market, 2008-2015

Source: Frost & Sullivan

4%

7%

12%

2020(% of total car sales)

520,953

1,212,140

2,163,150

2015

394,605273,224168,96572,89525,8847,5505,103Conservative

778,577462,281251,329109,52138,2458,4115,103Frost & Sullivan

1,389,180863,160574,435273,11694,47517,4755,103Optimistic

2014201320122011201020092008Scenario Analysis

(Unit Shipment)

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2008 2009 2010 2011 2012 2013 2014 2015

Un

it S

hip

men

ts (

Mil

lio

ns)

Optimistic Scenario F&S Scenario Conservative Sceanrio

23

0

100

200

300

400

500

600

Asia Pacific Europe North America Others

Thousands

CEV eREV NEV/QC HPEV

60%

28%

12%73%

24%

2%

1%

56%

42%

1%

1%

Global Electric Vehicle Market: Breakdown By Region (Estimates), 2015

1.21 Million

65%

31%

3%

1%

20092015

8,411

3%

14%

63%

21%

68%

3%29%

1%

• Japan and China are the key markets for APAC=> likely 80% market share. China expects major share from the local OEMs andppotential for strong growth in India

•eREV and PHEVs likely to account major share in the North American market driven by the virtue of demographics and customer driving

characteristics => GM & Chrysler key OEMs. On the other hand, CEVs suit the demographics for the Europe.

EV Breakdown by Region- eREVs popular segment in NA accounting 42% share and

CEVs to account for 73% in Europe

24

Customers, Manufacturers and Regulators at X roads

25

Electric

Vehicles

Discussion Points- Applicability to INDIA and Key Lessons

What type of infrastructure do we need to create? Pilot Projects/ Standards

Customer Education and Awareness

Regulatory Framework and Government

support

Innovative business models- Value chain

creation, value added services

Is there a electric vehicle market in

India?

26

Thank You