used car market report

TRANSCRIPT

2012Used Car Market Report

$25017th Edition

1 2012 Used Car Market Report

1WISEGUY

2 A Note From Sandy Schwartz, Manheim President

3 Year in ReviewThe auto industry performed well in 2011, despite a weak economic backdrop. Further recovery in 2012 is expected, but risks abound.

8 The Remarketing IndustryAuction industry volumes fell in 2011 as the drop in commercial consignments more than offset the in-crease in dealer consignment. Technology advanced rapidly, enabling buyers and sellers to efficiently and effectively participate in live and digital auctions.

12 DealersUsed vehicle retail sales rose more than 5% to 38.8 mil-lion units in 2011. Dealers increasingly turned to online channels to both buy and sell in the wholesale market.

• Q&A with NADA

• Q&A with NIADA

19 RentalNew vehicle sales into rental declined marginally in 2011, but the average fleet size grew significantly. High used vehicle values lowered depreciation expense and boosted industry profits.

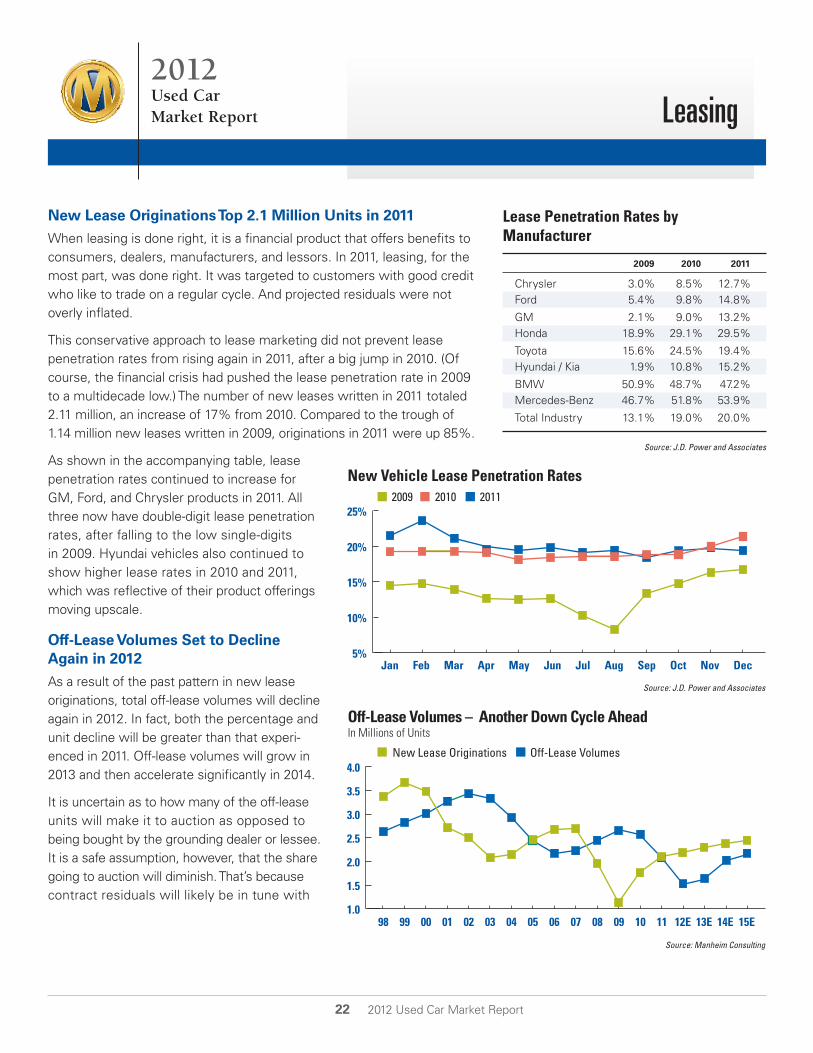

22 LeasingLease originations increased for a third consecutive year while lease maturities declined for a second year. A growing share of off-lease units were acquired by either the lessee or the grounding dealer.

25 RepossessionsRepossessions declined again in 2011 as loan portfolios performed very well. The shortage of fleet and lease units increased buyer interest in repossessions sold at auction.

28 Commercial and Government FleetsCommercial fleet units in service stabilized, but gov-ernment fleets continued to contract due to budget constraints. After experimenting with longer life cycles, many fleet managers returned to remarketing vehicles with closer to historic mileage norms.

31 SalvageMore dealers participated in salvage auctions as buyers and sellers of low-priced vehicles. Repairable units with nonsalvage titles were in high demand.

Remarketing Evolution ContinuesWhile change remained constant for auto dealers in 2011, dealers continued to adapt by embracing new strategies to be more efficient and profitable. These new strategies included the adoption of digital technology in record numbers. Digital and mobile advances have provided dealers with more ways to effectively manage their used vehicle operations than ever before. With change here to stay, dealers now have the tools needed for success right in the palm of their hands.

Webb: “Settle down there boy, we’ll get some tail winds, too.”

manheim.com

2012Used Car Market Report $250

17th Edition

2 2012 Used Car Market Report

2012Used CarMarket Report

Sandy SchwartzPresidentManheim

A Note From Sandy Schwartz,Manheim President

The wholesale automotive industry has probably never experienced a year like 2011. This 17th edition of Manheim’s Used Car Market Report analyzes the events that made the year so challenging and exciting, including the supply and demand for used vehicles, digital and mobile technol-ogy advances, changes in how customers want to conduct business, and how the business of remarketing continues to evolve.

Manheim and our customers adjusted to a cyclical drop in vehicle supply and the realization that working smarter and more effectively will be critically important going forward.

After reviewing our future direction and listening to our customers, we aligned our physical and digital assets with our personnel and services, and accelerated our invest-ment in technology.

Even with fewer vehicles entering the wholesale market-place over the past few years – a condition that will likely continue – we believe that physical auctions will play an important role within the wholesale industry for many years to come. But, even as we improve the live auction experience, we have embraced the changes made possible by technology to support our digital auction channels and online services.

Through all of the changes in remarketing during the past decade, the one constant has been the reliability of the auction process in live and digital channels in determining the market value of any vehicle on any day.

Today, our customers purchase approximately 25 percent of the vehicles remarketed through a Manheim digital chan-nel. But as we continue to roll out new mobile applications and online services, and dealers gain confidence in buying and selling vehicles online, we believe that number will rise quickly above 50 percent. At Manheim, our goal is not to dictate where buyers and sellers connect, but rather to ensure that they can quickly and confidently transact in any manner that is convenient for them, whether that is by smartphone, tablet, PC, or bidding in a lane.

In 2011, we conducted a series of successful pilot tests of our newest and most exciting service, Simulcast Everywhere. Simulcast was launched nearly 10 years ago and was an immediate success because it enabled online bidders to participate in live auctions on their personal computers. Simulcast Everywhere goes a step further by bringing the auctioneer and live auction to the seller’s location. Simulcast Everywhere enables sellers to remarket vehicles faster, and that allows dealers to search larger inventories and bid on more vehicles earlier in the remar-keting cycle. It is an innovation that enables all of us – dealers, commercial consignors, and Manheim – to work more effectively.

I look forward to seeing you in 2012, sharing our plans, and hearing your ideas about how we can help you succeed. The foundation of our success depends on providing you with the highest level of service.

Sincerely,

Sandy Schwartz President

3 2012 Used Car Market Report

2012Used CarMarket Report Year in Review and Outlook

Tom WebbChief EconomistManheim Consulting

Follow Tom Webb on his blog and on Twitter: Blog: http://manheimconsulting.typepad.com/Twitter: @TomWebb_Manheim

Amid a weak economic backdrop, auto manufacturers, rental car companies, lenders, and – most importantly – dealers increased revenues and earnings in 2011. This was achieved even as businesses, financial mar-kets, and consumers wrestled with the uncertainty created by the European sovereign debt issue and the inability of U.S. policymakers to provide an environ-ment conducive to long-term planning or investing. And, of course, it was the auto industry that naturally bore the brunt of the tremendous supply disruptions resulting from Japan’s earthquake and tsunami.

The auto industry’s revenue growth in 2011 was, in large part, a simple bounce-back from deep recession lows, but the improvement in profitability was the result of business restructurings, productivity gains, effective use of new technolo-gies, and – in the case of dealers – good old-fashioned customer service and selling. To achieve similar gains in 2012, the industry will need to be blessed with an economic recovery that has solidified to withstand inevitable outside pressures. How likely is that scenario? Let’s consider that question before looking at industry-specific trends and projections.

Uncertainty Swirled, but Consumers Spent

Heightened uncertainty makes it difficult for economic forecasters, but, more importantly, it restrains businesses and can stop a weak recovery in its tracks. And, in 2011, uncertainty reigned. As evidence, consider this:

• When we wrote this section for the 2011 Used Car Market Report, Congress and the president were in the throes of debate regarding a continuing budget resolution and whether or not all the Bush-era tax cuts should be extended.

• When we were writing the midyear update, the U.S. debt ceiling debate was in full force. That led to a downgrade in the U.S. credit rating and the formation of a congressional “super committee” that failed to reach a resolution.

• And, as we wrote this review, policymakers wrangled over the future of the payroll tax cut before offering up a two-month extension.

All of these were cases of kicking the can down the road. And some of the kicks were awfully puny!

But, despite the self-imposed headwinds, the recovery became more self-reinforcing and more balanced in 2011. The economy showed several fits and starts during the course of the year, but that was often due to outside shocks such as the supply disruptions resulting from Japan’s earthquake or the host of domestic weather events ranging from floods and fires to hurricanes and tornadoes.

4 2012 Used Car Market Report

Year in Review and Outlook

Through it all, consumer spending supplied a steady underlying support to the economy. After falling by a record 7% in 2009, total retail sales rose 6.4% in 2010 and another 7.7% in 2011. This occurred despite low consumer confidence and weak income growth. In fact, in 2011, the disconnect between consumer spending and consumer confidence took on historic proportions.

A popular explanation for that disconnect is that high-income households, which account for the bulk of retail sales, kept on spending and thus, further increased their share of total purchases in 2011. That’s a factor, but there were two other causes that were more impor-tant. First, the retail sales tally is indifferent as to whether the purchase is made with a pay-check, a welfare check, or food stamps. In the latter two cases (which accounted for a grow-ing share of purchases in 2011), the buyer is not exuding confidence. Second, there is more inflation contained in the total retail sales num-ber than many realize. Total inflation remained subdued in 2011, but several important neces-sities had rapidly rising prices. For example, the cost of food consumed at home rose by 6% in 2011 and gasoline prices were up 33%. When inflation causes higher spending on necessities, the increase in retail sales should not be regarded as a sign of con-sumer confidence.

To enable their spending, consumers had to draw down their savings rate. After averaging more than 5% in 2010, the savings rate fell to 3.5% by the end of 2011. Like higher spending levels, the decline in savings rate was likely more a reflection of need, rather than of increased consumer confidence. And, of course, the lower savings rate means that further gains in retail sales will require growing personal income or stronger household balance sheets.

Review

1fromReviewppt

complete

2fromReviewppt

complete

Annual Net Change in Nonfarm PayrollsIn Millions

Source: Conference Board and Dept. of Commerce

0

20

40

60

80

100

120

140

-15%

-10%

-5%

0%

5%

10%

15%

Jan95

Jan97

Jan11

Jan99

Jan01

Jan03

Jan05

Jan09

Jan07

3fromReviewppt

complete

Retail Sales versus Consumer Confidence Consumer Confidence Retail Sales Year-Over-Year Percent ChangeCONSUMERCONFIDENCE

RETAILSALES

Source: Bureau of Labor Statistics

U.S. Personal Savings Rate3-Month Moving Average

Source: U.S. Dept of Commerce

0%

1%

2%

3%

4%

5%

6%

7%

1101 02 03 04 05 06 07 08 09 10-6-5-4-3-2-10123

Jan00

Jan01

Jan02

Jan03

Jan05

Jan04

Jan07

Jan08

Jan10

Jan11

Jan09

Jan06

Review

1fromReviewppt

complete

2fromReviewppt

complete

Annual Net Change in Nonfarm PayrollsIn Millions

Source: Conference Board and Dept. of Commerce

0

20

40

60

80

100

120

140

-15%

-10%

-5%

0%

5%

10%

15%

Jan95

Jan97

Jan11

Jan99

Jan01

Jan03

Jan05

Jan09

Jan07

3fromReviewppt

complete

Retail Sales versus Consumer Confidence Consumer Confidence Retail Sales Year-Over-Year Percent ChangeCONSUMERCONFIDENCE

RETAILSALES

Source: Bureau of Labor Statistics

U.S. Personal Savings Rate3-Month Moving Average

Source: U.S. Dept of Commerce

0%

1%

2%

3%

4%

5%

6%

7%

1101 02 03 04 05 06 07 08 09 10-6-5-4-3-2-10123

Jan00

Jan01

Jan02

Jan03

Jan05

Jan04

Jan07

Jan08

Jan10

Jan11

Jan09

Jan06

4fromReviewppt

complete

5fromReviewppt

complete

6fromReviewppt

complete

Total U.S. Nonfarm PayrollsIn Millions

Source: Bureau of Labor Statistics

125.0

127.5

130.0

132.5

135.0

137.5

140.0

Dec99

Dec01

Dec11

Dec03

Dec09

Dec07

Dec05

Initial Jobless Claims Four-Week Moving AverageIn Thousands

Source: Bureau of Labor Statistics

200

300

400

500

600

700

Dec99

Dec02

Dec01

Dec11

Dec03

Dec04

Dec05

Dec07

Dec08

Dec10

Dec00

Dec09

Dec06

Household Net Worth In Trillions

Source: Federal Reserve Board

1Q71

1Q76

1Q86

1Q81

1Q11

1Q91

1Q96

1Q06

1Q01

$0$10$20$30$40$50$60$70$80

5 2012 Used Car Market Report

Year in Review and Outlook

Employment

The income statement of consumers is dictated overwhelmingly by labor market conditions. Employment grew by an average of 137,000 per month in 2011, a significant improvement from 2010’s average of 78,000 per month and, of course, much better than the large losses recorded in 2008 and 2009. If employment gains in 2012 exceed 173,000 per month (not a totally unreasonable forecast), it would be the fastest annual growth rate since 2006. Such growth would, however, make only a small dent in the 6.1 million employment deficit that we currently suffer relative to the previous peak. And, as can be seen in the accompanying chart, total employment in December 2011 was virtually same as it was in May 2001, a time when the U.S. population was smaller by 32 million people.

Nevertheless, as we have said in the past, analysts should focus on the doughnut (employment), not the hole (unemployment). Payrolls are grow-ing, and they will continue to grow. Initial jobless claims have also fallen significantly. That should raise the job security and confidence of those already employed.

Home Values Continue to Fall, but at a Slower Rate

The typical family’s net worth resides predominantly in their home. Thus, the collapse in the housing market pushed household net worth down by an astonishing $11.6 trillion between the second quarter of 2007 and sec-ond quarter of 2010. Net worth has since grown, but primarily because of the writing-off of debt through foreclosures and bankruptcies. And total household net worth is still $9.4 trillion below its previous peak.

As 2011 ended, the Case-Shiller Price Index showed home values continu-ing to hit new post-bubble lows. The year-over-year decline was 3.4%, which pushed prices 32% below their 2006 peak. We are optimistic that home prices will find a bottom in 2012. Lower home values, record low mortgage rates, and a healthy rental market have already enticed inves-tors back into the market. An improvement in owner-occupied purchases will come as underwriting standards become more consistent and as the shadow inventory created by existing and pending foreclosures winds down.

Nevertheless, it is clear that the collapse in housing will have a multi-gen-erational impact. Each year an increasing share of potential home buyers will consist of individuals who never experienced the free ride of rapidly rising home values, but instead know only the downside of short sales, foreclo-sures, and underwater mortgages. Thus, another housing bubble will not appear for many decades, if ever. And, in addition to feeding on itself, the housing bubble provided a tremendous amount of liquidity that, through home equity loans and cash-out refinancings, found its way into the new and used vehicle sales market.

4fromReviewppt

complete

5fromReviewppt

complete

6fromReviewppt

complete

Total U.S. Nonfarm PayrollsIn Millions

Source: Bureau of Labor Statistics

125.0

127.5

130.0

132.5

135.0

137.5

140.0

Dec99

Dec01

Dec11

Dec03

Dec09

Dec07

Dec05

Initial Jobless Claims Four-Week Moving AverageIn Thousands

Source: Bureau of Labor Statistics

200

300

400

500

600

700

Dec99

Dec02

Dec01

Dec11

Dec03

Dec04

Dec05

Dec07

Dec08

Dec10

Dec00

Dec09

Dec06

Household Net Worth In Trillions

Source: Federal Reserve Board

1Q71

1Q76

1Q86

1Q81

1Q11

1Q91

1Q96

1Q06

1Q01

$0$10$20$30$40$50$60$70$80

New Car and Light-Duty Truck SalesSeasonally Adjusted Annual Rate – 3-Month Moving Average Millions of Units

Case-Shiller Composite Home Price Index�Seasonally Adjusted 7

fromReviewppt

complete

8fromReviewppt

Source: Case-Shiller

50

100

150

200

250

Jan87

Jan11

Jan91

Jan99

Jan03

Jan07

Jan95

Source: Automotive News

5

10

15

20

Jan87

Jan89

Jan11

Jan91

Jan93

Jan97

Jan99

Jan03

Jan05

Jan01

Jan09

Jan07

Jan95

Ratio of Used Vehicles Retailed�to New Vehicles Retailed

9fromReviewppt

Source: Automotive News and CNW Marketing Research

2.00

2.25

2.50

2.75

3.00

3.25

3.50

87 1191 99 03 079579 83

Review

1fromReviewppt

complete

2fromReviewppt

complete

Annual Net Change in Nonfarm PayrollsIn Millions

Source: Conference Board and Dept. of Commerce

0

20

40

60

80

100

120

140

-15%

-10%

-5%

0%

5%

10%

15%

Jan95

Jan97

Jan11

Jan99

Jan01

Jan03

Jan05

Jan09

Jan07

3fromReviewppt

complete

Retail Sales versus Consumer Confidence Consumer Confidence Retail Sales Year-Over-Year Percent ChangeCONSUMERCONFIDENCE

RETAILSALES

Source: Bureau of Labor Statistics

U.S. Personal Savings Rate3-Month Moving Average

Source: U.S. Dept of Commerce

0%

1%

2%

3%

4%

5%

6%

7%

1101 02 03 04 05 06 07 08 09 10-6-5-4-3-2-10123

Jan00

Jan01

Jan02

Jan03

Jan05

Jan04

Jan07

Jan08

Jan10

Jan11

Jan09

Jan06

6 2012 Used Car Market Report

Year in Review and Outlook

New and Used Vehicle Sales

New car and light-duty truck sales totaled 12.8 million in 2011, an increase of 10% from 2010. This fell short of our forecast of 13.1 million for the year, but that was due to lost sales resulting from inventory shortages in the aftermath of the Japan earthquake. In the first four months of 2011, new vehicles sold at a 13.1 million annualized rate. In the final four months, the pace was 13.3 million. It was the 11.9 million sales pace in the middle four months of the year that dampened the annual total.

Importantly, the increase in new vehicle sales in 2011 was not driven by sales into fleet (retail deliveries rose 12%, while fleet sales were up only 3%) or by heavy incentives (in fact, industry-wide incentive spending was down for the year and net new vehicle transaction prices were up substantially for the second consecutive year).

New vehicle sales should continue to improve in 2012 (we’re looking for 13.6 million), but long-term expectations should be kept in check. Slower household formation rates, reduced miles of travel, lower scrappage rates, and demographic shifts all suggest that the underlying rate of demand for new vehicles is in the 15 million to 15.5 million range, not the 17 million annual sales rate that was achieved during the seven-year period between 1999 and 2005.

Used vehicle retail sales were 38.8 million in 2011, the strongest level in four years. The percentage gain in used vehicle sales in 2011 (+5%) was only half that of new vehicles, but used vehicle sales did not fall as steeply during the recession. And, in fact, the ratio of used vehicles retailed to new vehicles sold remained high at more than 3-to-1 for the third consecutive year.

New Car and Light-Duty Truck SalesSeasonally Adjusted Annual Rate – 3-Month Moving Average Millions of Units

Case-Shiller Composite Home Price Index�Seasonally Adjusted 7

fromReviewppt

complete

8fromReviewppt

Source: Case-Shiller

50

100

150

200

250

Jan87

Jan11

Jan91

Jan99

Jan03

Jan07

Jan95

Source: Automotive News

5

10

15

20

Jan87

Jan89

Jan11

Jan91

Jan93

Jan97

Jan99

Jan03

Jan05

Jan01

Jan09

Jan07

Jan95

Ratio of Used Vehicles Retailed�to New Vehicles Retailed

9fromReviewppt

Source: Automotive News and CNW Marketing Research

2.00

2.25

2.50

2.75

3.00

3.25

3.50

87 1191 99 03 079579 83

New Car and Light-Duty Truck SalesSeasonally Adjusted Annual Rate – 3-Month Moving Average Millions of Units

Case-Shiller Composite Home Price Index�Seasonally Adjusted 7

fromReviewppt

complete

8fromReviewppt

Source: Case-Shiller

50

100

150

200

250

Jan87

Jan11

Jan91

Jan99

Jan03

Jan07

Jan95

Source: Automotive News

5

10

15

20

Jan87

Jan89

Jan11

Jan91

Jan93

Jan97

Jan99

Jan03

Jan05

Jan01

Jan09

Jan07

Jan95

Ratio of Used Vehicles Retailed�to New Vehicles Retailed

9fromReviewppt

Source: Automotive News and CNW Marketing Research

2.00

2.25

2.50

2.75

3.00

3.25

3.50

87 1191 99 03 079579 83

4fromReviewppt

complete

5fromReviewppt

complete

6fromReviewppt

complete

Total U.S. Nonfarm PayrollsIn Millions

Source: Bureau of Labor Statistics

125.0

127.5

130.0

132.5

135.0

137.5

140.0

Dec99

Dec01

Dec11

Dec03

Dec09

Dec07

Dec05

Initial Jobless Claims Four-Week Moving AverageIn Thousands

Source: Bureau of Labor Statistics

200

300

400

500

600

700

Dec99

Dec02

Dec01

Dec11

Dec03

Dec04

Dec05

Dec07

Dec08

Dec10

Dec00

Dec09

Dec06

Household Net Worth In Trillions

Source: Federal Reserve Board

1Q71

1Q76

1Q86

1Q81

1Q11

1Q91

1Q96

1Q06

1Q01

$0$10$20$30$40$50$60$70$80

7 2012 Used Car Market Report

Year in Review and Outlook

Manufacturer certified pre-owned (CPO) sales totaled more than 1.7 million in 2011, a record high. Fifteen brands, 10 of which were Asian, had best-ever CPO sales. Many of these brands have long-established CPO programs that emphasize dealer train-ing and often offer low-rate financing for certified vehicles.

Likewise, used vehicles retailed by the seven publicly-traded dealership groups also reached a new high in 2011, at just under 1 million units. On a same-store basis, these dealership groups have had nine consecutive quarters of increasing retail used unit volumes. There has been some erosion in margins on these sales, but faster turns, slower depreciation, and low interest rates have reduced holding costs and led to record profits.

The Year Ahead: Continued Recovery, but with Tempered Expectations

Despite the previously mentioned uncertainty and the shocks that will surely arise (from both here and abroad), we can more confidently pre-dict this year, than we could last year, that the U.S. economy will grow and that new and used vehicle sales will rise. That’s because even an anemic recovery (like we had in 2011) gener-ates momentum. And, although the recovery will now enter its third year, there is tremen-dous slack in the economy and unprecedented pent-up demand. Continued job growth will unleash that demand. Additionally, commercial businesses and financial institutions are generating strong cash flows and building reserves. That will enable them to with-stand temporary shocks. So, unlike 2008, they won’t be contributing to turmoil and volatility in the market, they will be calming it.

So, why do we temper our outlook and what are the risks that the economy will reverse course? The biggest dampening effect will continue to be consumer deleveraging. The downturn in home values has left a hole in household balance sheets that will take years to repair. And, although the housing industry will likely find a bottom in 2012, there is no way that it will make the same contribution to overall growth that it once did. Likewise, austerity and job cuts at the state and local levels (a loss of 625,000 jobs over the past three years) are winding down, but that will not suddenly change into new spending and hiring. Meanwhile, the amount of federal fiscal stimulus will be less in 2012 and monetary policy has little room left to be more accommodating.

As to the risk of the economy slipping into another recession, we noted last year that the European sovereign debt issue was the number one threat. That picture has not gotten any prettier, and a plan to deal with it has yet to be formulated, much less implemented. For Europe, the problem has gotten worse and dire consequences are inevitable, but the risk of contagion aborting the U.S. recovery has diminished. U.S. banks and other financial institutions are much better prepared than they were a year ago to withstand the possible fallout.

This year, our chief threat is once again ourselves. Although our debt and deficit issues need not – and cannot – be solved in the short term, there is a limited window of opportunity to rationally address the issue. Failure to do so will simply make the necessary hard choices harder and the easy alternatives all the more harmful in the long run.

Percent Change Used Units Retailed – Same Store BasisPublicly-Traded Dealership GroupsWeighted Average for KMX*, AN, PAG, SAH, GPI, ABG and LAD

11fromReviewppt

2004

*KMX shifted forward one month to correspond with calendar quarter Source: Company filings

-25%-20%-15%-10%

-5%0%5%

10%15%20%

2005 2006 2007 2008 2009 2010 2011

10fromReviewppt

fromemail:

The 2011 CPO sales is 1.67 million. Please drop off the oldest year when you add 2011.

1.73 per ppt

complete Source: Automotive News

11E01 02 03 04 05 06 07 08 09 10

Certified Pre-Owned (CPO) Sales In Millions

0.0

0.5

1.0

1.5

2.0

8 2012 Used Car Market Report

2012Used CarMarket Report The Remarketing Industry

The shortage and aging of vehicles in the wholesale market dominated the headlines in 2011 and influenced the actions of buyers and sellers. Fortunately, the adaptation of digital technology to every aspect of selling and buying vehicles enabled industry participants to manage their businesses in real time under challenging circumstances.

Supply Shortages Shrink Sales at NAAA Member Auctions

A significant reduction in commercial consignment volumes more than offset the increase in dealer consignment in 2011. Preliminary numbers suggest that the number of vehicles remarketed through the member auctions of the National Auto Auction Association (NAAA) declined by about 8% in 2011 to less than 7.8 million units. This marked the fourth consecutive year of lower volume.

With residuals strong and volumes declining, grounding dealers bought a growing share of off-lease vehicles. Likewise, strong demand for late-model vehicles enabled the rental industry to sell more vehicles directly to local dealers, and allowed commercial fleets to sell more units directly to company employees.

Auctions remarketed fewer late-model used vehicles as the changing mix of sellers shifted auction volume toward older units. Dealer consignment sales increased by more than 10%, while rental, off-lease and other commercial seller volumes fell more than 20% in 2011. Dealer consignment accounted for 55% of total NAAA volume, compared to 45% in 2010 and less than 40% in 2009.

While timing and channel selection decisions impact the age mix of wholesale supply, so too do past new vehicle sales. Between 2004 and 2007, 66.6 million new vehicles were sold, so vehicles of these model years are disproportionately represented in the vehicle population compared to the low supply of 2008 through 2011 model year vehicles.

The Manheim Used Vehicle Value Index Posts an Annual Gain of 3.7%

The Manheim Used Vehicle Value Index topped out in May at 127.8 and remained at historically high levels adjusted for mileage and seasonality through year-end. For the year, the Index averaged 124.9, up from 120.5 in 2010, for a gain of 3.7%. Even older high-mileage vehicles often commanded prices that were thousands of dollars higher than a year earlier. As a result, deal-ers specializing in under-$5,000 units often turned to salvage and government auctions to find inventory.

Small and midsized cars had substantially higher prices in 2011 than in 2010. All other market segments showed flat pricing or, in some cases, declines. The spike in wholesale values for fuel-efficient vehicles corresponded with the run-up in gas prices, but it was driven more by the supply disruption in new vehicle inventory (due to the Japan earthquake) than by pump prices.

3

Quarterly Call

Manheim Used Vehicle Value IndexJanuary 1995 = 100

Source: Manheim Consulting

059695 97 99 0098 01 02 03 0604 07 08 09 10 1195

100

105

110

115

125

120

complete

from Quarterly Call pdfpg 3

5complete

from Quarterly Call pdf pg 5

7complete

from Quarterly Call pdf pg 7

Used Vehicle Price Trends – Selective Market ClassesJanuary 1997 = 100 Compact Cars Midsize Cars Luxury Cars Pickups SUV/CUV

70

80

90

110

100

120

130

140

Jan07

Jul07

Jan08

Jul08

Jan09

Jul09

Jan10

Jul10

Jan11

Jul11

Source: Manheim Consulting

Source: National Auto Auction Association and CNW Market Research

99 00 01 02 03 04 05 06 07 08 09 10 11-12.5%

-10.0%

-5.0%

0%

5.0%

7.5%

-7.5%

2.5%

-2.5%

Percent Change in Auction Volume,Used Retail Sales and Manheim Index Auction Volume Used Retail Sales Manheim Index

9 2012 Used Car Market Report

Manufacturer Incentives Impact Wholesale Values of Luxury Cars and Pickup Trucks

Prices of luxury vehicles and pickup trucks underperformed the overall market in the sec-ond half of the year due to higher manufacturer incentives on comparable new vehicles. Year-end sales campaigns among luxury brands, especially German makes, were more gener-ous than those of recent years. Pickup truck inventory was relatively high throughout the year, so manufacturers stimulated demand with cash rebates and financing incentives.

Auction Volumes to Hold Steady in 2012

With new vehicle sales rising again in 2012, dealer consignment volumes should grow for the fourth consecutive year. The number of commercial fleet units and repossessions sold at auction should remain steady. There will, however, be another significant reduction in off-lease volumes in 2012. The net result will be relatively stable total auction volumes for the year, but with big shifts in the makes, ages, mileage, and price points of vehicles being sold.

Technology Transforms the Wholesale Marketplace

A decade ago, the Internet gave rise to digital upstream auction channels where the strong relationships between related buyers and sellers overcame the inherent risk in buying vehicles without personally inspecting them. Auto companies and their franchised dealers, as well as corpora-tions and their employees, were ideally paired to transact online since buyers knew the product and they counted on the seller to stand behind the vehicle. In this unique slice of the wholesale marketplace, vehicles could be remarketed using stock photographs and simple condition reports (CRs).

Although the technology also made it possible for unrelated buyers and sellers to transact with each other, few did so because they lacked the information needed to make informed judgments. And, with ample choice in live auction channels, buyers did not see the advantage of bidding online.

The promise of a 24/7 open auction environment that met all of the conditions needed by sellers and buyers began to take shape over the past decade as technology advanced and auction companies established processes to make the digital mar-ketplace more effective. For example, Manheim white papers and case studies demonstrated to sellers the need to price vehicles close to market values in order to generate active bidding. The accuracy and consistency of electronic CRs were improved to overcome any buyer hesitation. Arbitration policies were modified to reflect the transportation time and cost involved in remote buying and selling. And, dealer training programs, such as Manheim’s Wholesale Institute, were launched to teach dealers the best uses of the technology and how to develop effective strategies for online selling and buying.

The Remarketing Industry

3

Quarterly Call

Manheim Used Vehicle Value IndexJanuary 1995 = 100

Source: Manheim Consulting

059695 97 99 0098 01 02 03 0604 07 08 09 10 1195

100

105

110

115

125

120

complete

from Quarterly Call pdfpg 3

5complete

from Quarterly Call pdf pg 5

7complete

from Quarterly Call pdf pg 7

Used Vehicle Price Trends – Selective Market ClassesJanuary 1997 = 100 Compact Cars Midsize Cars Luxury Cars Pickups SUV/CUV

70

80

90

110

100

120

130

140

Jan07

Jul07

Jan08

Jul08

Jan09

Jul09

Jan10

Jul10

Jan11

Jul11

Source: Manheim Consulting

Source: National Auto Auction Association and CNW Market Research

99 00 01 02 03 04 05 06 07 08 09 10 11-12.5%

-10.0%

-5.0%

0%

5.0%

7.5%

-7.5%

2.5%

-2.5%

Percent Change in Auction Volume,Used Retail Sales and Manheim Index Auction Volume Used Retail Sales Manheim Index

3

Quarterly Call

Manheim Used Vehicle Value IndexJanuary 1995 = 100

Source: Manheim Consulting

059695 97 99 0098 01 02 03 0604 07 08 09 10 1195

100

105

110

115

125

120

complete

from Quarterly Call pdfpg 3

5complete

from Quarterly Call pdf pg 5

7complete

from Quarterly Call pdf pg 7

Used Vehicle Price Trends – Selective Market ClassesJanuary 1997 = 100 Compact Cars Midsize Cars Luxury Cars Pickups SUV/CUV

70

80

90

110

100

120

130

140

Jan07

Jul07

Jan08

Jul08

Jan09

Jul09

Jan10

Jul10

Jan11

Jul11

Source: Manheim Consulting

Source: National Auto Auction Association and CNW Market Research

99 00 01 02 03 04 05 06 07 08 09 10 11-12.5%

-10.0%

-5.0%

0%

5.0%

7.5%

-7.5%

2.5%

-2.5%

Percent Change in Auction Volume,Used Retail Sales and Manheim Index Auction Volume Used Retail Sales Manheim Index

10 2012 Used Car Market Report

The Remarketing Industry

In 2011, online bidders accounted for 25% of all Manheim sales. Additionally, the majority of dealers and commercial sellers connect through Manheim.com daily to manage their accounts, search inventory, post vehicles for sale, and arrange for other services that promote suc-cessful outcomes in digital channels. A true 24/7 marketplace, which freed dealers and commercial sellers from their desktop computers, was then enabled by the advent of smartphones.

Other milestones and achievements that brought us to a fully digital marketplace include:

• High-speed broadband service, which enabled dealers to bid in Simulcast auctions. With Simulcast, dealers had the familiarity of the live auction, heard the call of the auctioneer, and could inspect vehicles prior to sale. Dealers then saved time by bidding through their computers.

• OVE.com was launched as a 24/7 digital channel in 2006. Over time, the functionality embedded in OVE.com expanded. Today buyers on OVE.com can place proxy bids, purchase vehicles at Buy It Now prices, and interact directly with sellers. Sellers can accept “if” bids, contact bidders, monitor bidding activity, change reserve prices, and manage their inventory between live and digital channels.

• Data captured in online channels was increasingly used to help buyers and sellers improve their remarketing performance.

• Manheim.com became the single portal through which customers accessed all their remarketing needs – such as live and digital auctions, account management, inventory searches, bid placement, and interac-tions with one another.

• The smartphone and iPad provided the technological leap that made 24/7 digital wholesale markets possible. Dealers were no longer dependent on a personal computer. As more mobile applications were launched, buyers and sellers accessed Manheim and all of its services to fulfill the promise of the Anytime+Anywhere marketplace.

• As dealers shifted from desktops to mobile devices, Manheim Mobile piloted Simulcast Everywhere in 2011. This new service enabled real-time bidding in live auctions that could be conducted anywhere the vehicles were located – dealer-ships, car rental lots, or marshaling yards.

Today, virtually all franchised dealers and most independent dealers have bid on vehicles via Simulcast or OVE.com. Manheim Consulting research shows that once dealers have had a successful experience buying a vehicle online, they then fill an increasing percentage of their inventory needs through digital channels.

Manheim Digital Statistics for 2011

• In 2011, an average of 118,000 customers logged in each month to Manheim websites and apps, representing an 11% increase over 2010.

• The total number of OVE.com consignors was up 25% from 2010 due to an increase in dealer sellers. The number of vehicles offered by dealer sellers was up 22% over 2010.

• Manheim received more than 4 million visits to its Mobile website, iPhone app, and Android app in 2011. The iPhone and iPad accounted for 64% of mobile visits, and Android devices accounted for 32% of mobile visits.

• A quarter of all Manheim sales came from Simulcast or OVE.com in 2011, compared to 21% in 2010.

11 2012 Used Car Market Report

The Remarketing Industry

Functionality and Use of Manheim Mobile Grows

The revolution in mobile device functionality has transformed when, and where, buyers and sellers conduct business. Mobile devices are quickly displacing desktop computers as the dominant means of interaction in the wholesale market. Manheim Mobile, which was launched in the first quarter of 2010, recorded nearly 300% more visits in 2011 than the previ-ous year. Today, mobile applications enable buyers and sellers to do anything through a mobile device that they can do in person or over a desktop computer. Services range from researching price and vehicle information to account management and placing bids. Dealers are no longer limited to business hours to manage their inventory and bid on vehicles. And sellers can continuously monitor bidding activity, which enables them to make price adjustments or respond to bidder questions in real time.

Successful Selling in Digital Channels Requires Giving Buyers More and Better Information

Commercial sellers have learned that to effectively sell to an unrelated party, they need to provide enough information to generate bids at the fair value for the vehicle. That’s why most commercial consignors provide multiple photographs and full CRs. Dealers, as more recent sellers on OVE.com, provide condition information on just over one-third of their listings, and in some cases, it is a seller’s disclosure rather than a third-party inspection and report.

Studies by Manheim Consulting have repeatedly demonstrated that listings with electronic CRs and photographs attract more bidders and generate higher retention than those without.

Effective Online Selling Also Requires Reasonable Reserve Prices

Bidders will bypass listings when reserve prices are far from market value. In 2011, more than 55% of all listings were “market priced;” but only 35% of dealer listings were in that sweet spot. As dealers refine their digital remarketing strategies, the percentage of OVE.com dealer listings with comprehensive CRs, and appropriate Buy Now prices will continue to increase, just as it has throughout the last two years. Buy Now transactions account for about 63% on OVE.com, and that percentage is increasing as more dealers carry limited inventory and need specific vehicles for customer orders or stock.

Simulcast Everywhere Optimizes the Experience for Buyers and Sellers

Simulcast has been around for nearly a decade and is now an essential tool for most used car managers. Simulcast allows dealers to remotely buy vehicles and to get a sense of the overall market as each vehicle arrives at the block. Simulcast ensures that the number of bidders is not limited to those standing in the lane that day. From the dealers’ perspective, Simulcast expanded the inventory they could bid on and allowed them to manage their time more effectively.

The next step for Simulcast was to make it portable for the seller and the buyer. There is no inherent requirement that Simulcast sales be limited to auction lanes and accessed only through desktop computers. In fact, Manheim specialty equipment and heavy truck auctions have been successfully Simulcasted from marinas, RV lots, and other locations for several years.

In 2011, Manheim pilot-tested Simulcast Everywhere, a new service that brings the auction to the seller’s location and enables buyers to bid in real time through a mobile device. Vehicles are staged sequentially with a live auctioneer conduct-ing each sale. Dealers are able to search pre-sale lists and view seller disclosures before the auction.

With Simulcast Everywhere, sellers will not have to move vehicles to an auction, but will still be able to generate the excitement of a live sale. Buyers will be able to search and buy vehicles in all channels through computers and mobile devices.

12 2012 Used Car Market Report

2012Used CarMarket Report

Used vehicle sales by franchised and independent dealers rose in 2011 as the economy continued its slow recovery and as the availability of retail financing increased, especially for subprime shoppers. Wholesale supplies remained tight, however, so finding enough of the right vehicles was tough and acquisition costs were significantly higher.

The shortage of used vehicles in the wholesale market was driven by lower off-lease and repossession volumes. Dealer consignment volumes rose significantly in 2011. Nevertheless, even the older, less expensive vehicles that typically come from dealer consignment were in short supply relative to demand. With demand for used vehicles high across the board, wholesale prices continued to rise in 2011, reaching a peak in May and then remaining at historically high levels at year-end.

New and Used Vehicle Sales Rise in 2011

New vehicle sales rose 10% in 2011 to 12.8 million units. Although sales were the highest since 2008, the total was still three million units below what analysts regard as “normal.” Between 2008 and 2011, only 48 million new vehicles were sold, compared to 67 million in the prior four years. This low level of new vehicle sales will create a deficit in the supply of vehicles from these model years for years to come.

Used vehicle sales in 2011 totaled 38.8 million, up 5.2% from 2010, approximately half the rate of increase for new vehicles. New and used vehicle demand responds to the same economic factors; however, used vehicle sales are much less volatile.

Dealers Increase Their Share of the Used Vehicle Market

In 2011, used vehicle sales by franchised dealers increased 8% to slightly more than 13.8 million units and sales by independent dealers increased by 5.6% to just under 13.8 million. Private party sales (11.2 million) rose only 1% from 2010. With vehicle owners finding dealers willing to pay top dollar for their car or truck and also finding credit readily avail-able through them, dealers gained share in the used vehicle market at the expense of private party transactions.

Certified Pre-Owned (CPO) Vehicle Sales Rise 6.4% in 2011

Franchised dealers sold more than 1.7 million CPO vehicles in 2011, up 6.4% from 2010 despite the tight supply of late-model vehicles. CPO programs enable customers to purchase a used vehicle with superior warranty protec-tion and often with better financing terms.

Dealers

Dealers

1

2

3

needs data

61 817166 76 86 91 0196 1106

Source: Automotive News

468

101214161820

New Car and Light-Duty Truck SalesMillions of Units

Dealers Post Largest Used Unit Sales Gain Since 1993Annual Percent Change in Used Unit Sales by Dealers

Source: CNW Marketing Research

-10%-8%-6%-4%-2%0%2%4%6%8%

10%

0590 9291 9695 97 99 0098 01 02 03 060493 94 07 08 1009

2011 is a Manheim Consulting estimate based onboth internal and industry sources.

Source: National Auto Auction Association Surveys, 2001-2010

01 1002 03 04 05 06 07 08 09 11E0%

10%

20%

30%

40%

50%

60%

Dealer-Consignment Sales as Percentage of Total Auction Volume

needs data

39.4040.0140.5046.3051.6050.9050.0042.0039.3045.4055.50

from Quarterly Call pdf pg 15

15

Used Vehicle Sales Inherently More Stable Than New Vehicle Sales New Vehicle Sales Used Vehicle Sales

Source: Automotive News & CNW Marketing Research

-25%-20%-15%-10%

-5%0%5%

10%15%20%

77 79 81 83 0585 87 89 91 95 97 99 01 0393 07 09 11

13 2012 Used Car Market Report

In 2011, vehicle manufacturers increased their support of pre-owned vehicles with greater marketing and with more low-rate, low-down payment, loans.

CPO certification favors late model off-lease, executive and program vehicles remarketed in closed upstream channels. In addition, in 2011, grounding dealers bought a high percentage of the off-lease units returned to their stores. For some brands, more than 50% of the end-of-term units were bought by the grounding dealer and more than 80% were bought within upstream channels by franchised dealers. This left a very limited supply for remarketing through open auctions where independent dealers are active buyers.

Wholesaling Percentages Decline at Franchised Dealerships

In 2011, franchised dealers held onto a higher percentage of their trade-ins, including off-brand units, if they were consis-tent with the dealer’s target customer. Internet marketing sites such as AutoTrader.com have enabled franchised dealers to better merchandise their own and off-brand used vehicles online since visitors search by make and model rather than a specific dealership.

While most franchised dealers still wholesale trade-ins that are not consistent with their image and clientele, many of these dealers have also begun to sell older, less-expensive, units on their existing lots or at separate locations. In addition, many dealers have recently leaned towards retailing an aged used vehicle at a wholesale-like price, rather than actually wholesaling it. This offers the opportunity to generate F&I income, allows salespeople at least some commission, creates potential service revenue, and possibly garners a lifetime customer. Of course, it also runs the risk of lowering gross mar-gins throughout the department.

Dealers Devote More Effort to Finding the Right Inventory

The most common complaint from both franchised and independent dealers was the increased effort they had to put into inventory acquisition. Dealers scanned pre-sale lists, mined online listings, and attended or participated in multiple live and digital auctions each week. While auctions rolled out more tools and services to make it easier for dealers to search, evaluate, and bid on vehicles Anytime+Anywhere, there is no denying that reduced wholesale supplies challenged dealers.

Franchised dealers used a variety of marketing strategies to simultaneously prompt the sale of a new vehicle and provide the dealer with a sellable used unit. Existing customers received direct mail solicitations offering to buy their vehicle at cur-rent high market prices. Similarly, dealership service personnel encouraged customers in for repair to have their vehicle appraised. The value often exceeded the owner’s expectation and led to a new vehicle sale.

Independent Dealers Increasingly Adopt Online Channels

Independent dealers had to adapt both their sourcing strategies and sometimes their business model to an environment of high prices and tight supply. This meant tapping more local and regional sources and venturing farther away to buy vehicles. Besides traditional whole car auctions, salvage and repo auctions attracted dealers looking for lower-priced units.

In 2011, dealers attended more physical auctions and searched for, bid on, and bought more vehicles in digital auctions. The need to shop efficiently and to see more inventory, as well as the convenience of logging on through a mobile device, increased the independent dealer’s use of digital channels in 2011. Dealers simply don’t want to be away from their stores more than one day a week, so digital channels and services have become essential to the conduct of their business.

Dealers

Used Vehicle

2

3

Source: Automotive News

1101 02 03 04 05 06 07 08 09 10

Certified Pre-Owned (CPO) Sales In Millions

0.0

0.5

1.0

1.5

2.0

Manheim Used Vehicle Value IndexJanuary 1995 =100

Source: Manheim Consulting

059695 97 99 0098 01 02 03 0604 07 08 09 10 11 1295

100

105

110

115

125

120

complete

from Quarterly Call pdfpg 3

14 2012 Used Car Market Report

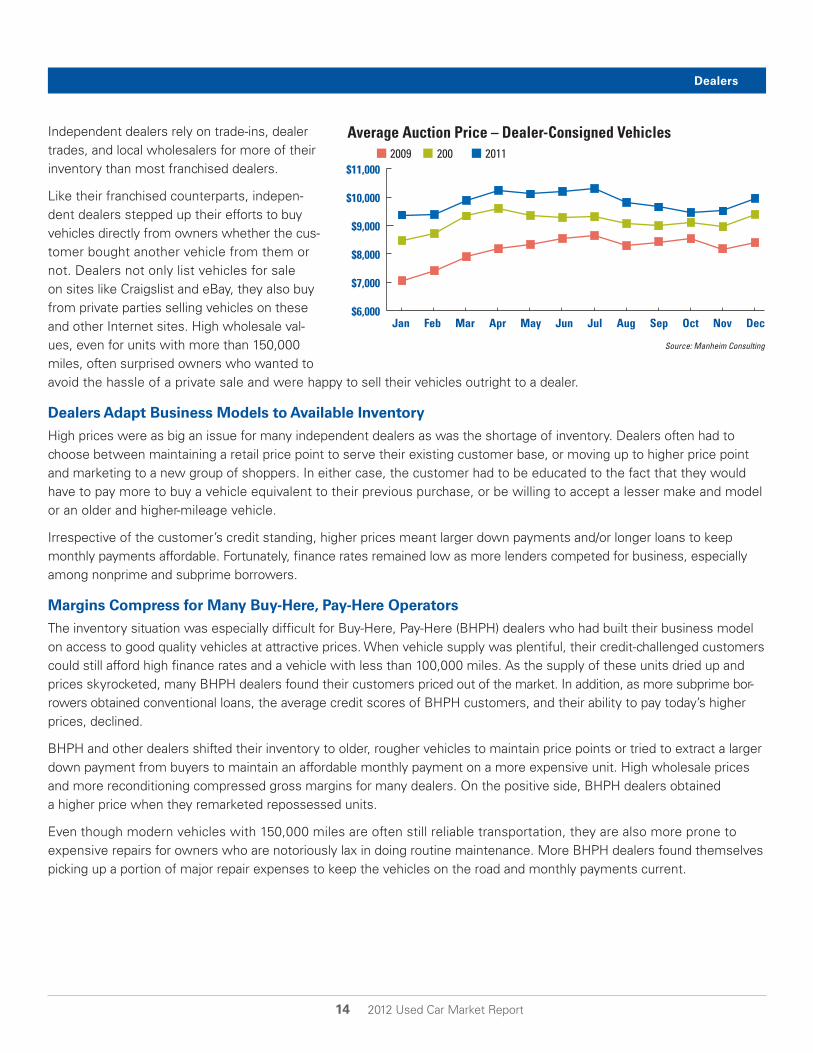

Independent dealers rely on trade-ins, dealer trades, and local wholesalers for more of their inventory than most franchised dealers.

Like their franchised counterparts, indepen-dent dealers stepped up their efforts to buy vehicles directly from owners whether the cus-tomer bought another vehicle from them or not. Dealers not only list vehicles for sale on sites like Craigslist and eBay, they also buy from private parties selling vehicles on these and other Internet sites. High wholesale val-ues, even for units with more than 150,000 miles, often surprised owners who wanted to avoid the hassle of a private sale and were happy to sell their vehicles outright to a dealer.

Dealers Adapt Business Models to Available Inventory

High prices were as big an issue for many independent dealers as was the shortage of inventory. Dealers often had to choose between maintaining a retail price point to serve their existing customer base, or moving up to higher price point and marketing to a new group of shoppers. In either case, the customer had to be educated to the fact that they would have to pay more to buy a vehicle equivalent to their previous purchase, or be willing to accept a lesser make and model or an older and higher-mileage vehicle.

Irrespective of the customer’s credit standing, higher prices meant larger down payments and/or longer loans to keep monthly payments affordable. Fortunately, finance rates remained low as more lenders competed for business, especially among nonprime and subprime borrowers.

Margins Compress for Many Buy-Here, Pay-Here Operators

The inventory situation was especially difficult for Buy-Here, Pay-Here (BHPH) dealers who had built their business model on access to good quality vehicles at attractive prices. When vehicle supply was plentiful, their credit-challenged customers could still afford high finance rates and a vehicle with less than 100,000 miles. As the supply of these units dried up and prices skyrocketed, many BHPH dealers found their customers priced out of the market. In addition, as more subprime bor-rowers obtained conventional loans, the average credit scores of BHPH customers, and their ability to pay today’s higher prices, declined.

BHPH and other dealers shifted their inventory to older, rougher vehicles to maintain price points or tried to extract a larger down payment from buyers to maintain an affordable monthly payment on a more expensive unit. High wholesale prices and more reconditioning compressed gross margins for many dealers. On the positive side, BHPH dealers obtained a higher price when they remarketed repossessed units.

Even though modern vehicles with 150,000 miles are often still reliable transportation, they are also more prone to expensive repairs for owners who are notoriously lax in doing routine maintenance. More BHPH dealers found themselves picking up a portion of major repair expenses to keep the vehicles on the road and monthly payments current.

Dealers

4

5

needs data

6

needs data

Average Auction Price – Dealer-Consigned Vehicles 2009 200 2011

Source: Manheim Consulting

Jan Feb Mar Apr May Jun Jul Sep Oct Nov DecAug$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

15 2012 Used Car Market Report

Independent Dealers Still Limited in Floorplan Lines

Independent dealers have always faced more challenges in terms of floor-plan credit. Prior to the recession, however, dealers with good credit could often borrow from small local and regional banks against their inventory or get a personal line of credit. But many of these sources dried up during the credit crisis, so independent dealers either used their own funds to purchase vehicles or relied on lenders such as Manheim Financial Services (MAFS). In 2011, the number of dealers served by MAFS increased by more than 17% and available credit lines rose by nearly 13%.

Even as lenders like MAFS stepped up their commitments to indepen-dent dealers, the rapid increase in vehicle prices often meant that dealers had to stock fewer units and try to turn them faster to reach their sales goals. The best scenario for the independent dealer was to acquire a vehi-cle and immediately retail it based upon a firm customer order. Using features like Retail View on OVE.com, more dealers showed online vehi-cles to prospective buyers, negotiated a price, and then bought the vehicle online at the “Buy It Now” price.

Inventory Management Systems Link Dealers Directly to Auction Inventory

Inventory management systems that evaluate local sales and price trends and recommend stocking selections are proven tools that maxi-mize inventory turns. In 2011, vAuto launched a new service, Provision, that blends the resources of AutoTrader and Manheim to provide a comprehen-sive inventory solution that addresses the key questions of what cars to stock, what to pay, and where to find them. Provision, and other IMS systems, combine market data and technology to optimize each dealer’s inventory mix and facilitate the vehicle search and bidding process.

Provision, and other IMS systems, link dealers directly to Manheim and other online inventory sources so they can search for specific models, see run lists, and create proxy bids or “click to purchase” and buy the unit immediately. Inventory management systems save dealers time in searching multiple inventory lists for the right vehicles for their stores.

Interest in Dealer Consignment Grows

Because dealer vehicles vary greatly in terms of the total volume per dealer as well as the age, condition and make of those vehicles, the remarketing process at dealerships has often been more opportunistic than structured. Small dealers will often sell vehicles locally to another dealer or to a wholesaler to get cash immediately. Some large dealers favor sealed-bid auctions once a week or month, even though this is time consuming, adds administrative costs, and ties up cash until the cars are sold.

Dealers

Value of Condition Reports: Dealer Consignments

Manheim Consulting reviewed live and Simulcast auction data from dealer con-signment sales from January through November of 2011. During this time period, only 9% of dealer-consigned units were sold with condition reports (CRs), compared to 97% of vehicles in commercial sales. The 9% of dealer units sold with a CR in 2011 actually represented a 36% increase vs. last year. The increase in dealer units being offered at the auction with a CR drove Simulcast activity up substantially in 2011.

The study shows that vehicles with CRs had fewer arbitration claims and attracted more online bidders, which resulted in a higher online sales per-centage – 48% of vehicles sold with a CR in the $30,000-and-up price range were directly impacted by a Simulcast buyer. These vehicles also experienced a retention lift, especially those in the $10,000-to-$25,000 price range.

View the complete case study by visiting www.manheim.com/consulting and search under the “Presentations” tab.

16 2012 Used Car Market Report

Participation in the dealer lanes at auction and retention have both been rising as the supply of cars and trucks in fleet/ lease lanes declined. The combination of more buyers for dealer consignments and recognition that even small changes can influence returns has altered how many dealers remarket their unwanted units, choosing auctions over other channels.

Manheim now Simulcasts all dealer lane sales, and that has brought more remote buyers into these sales. But to appeal to online bidders, dealers have to provide the same condition information routinely available on fleet and off-lease vehicles. Dealer units with condition reports receive more online bids than vehicles remarketed only with seller disclosures.

Dealers Ask for More Remarketing Training

The shift from selling the majority of their vehicles in a live auction to offering their inventory 24/7 sequentially in multiple digital as well as live auctions can be a daunting task for dealers. Dealers, even large regional and national chains, often rely upon local store management to handle the wholesaling of unwanted units. Developing the sophistication and comfort with remarketing through multiple channels takes time and experience. Just as it has taken years to reach the point where the majority of dealers have bid on and bought a vehicle through a digital channel, building up the expertise at the dealer level to do the same when remarketing a vehicle takes time.

At the request of dealers, The Wholesale Institute has expanded its syllabus to include remarketing training for both in-lane and digital channels. This, and other efforts by auction staff, is encouraging dealers to set reserve prices consistent with market values, to represent vehicles in the lanes, to include a “Buy It Now” or “Make an Offer” options available in digital listings, and to provide prospective bidders with photos and condition reports (CRs). Dealers are also encouraged to list their vehicles in pre-sale inventory where they can be shown with both the lane assignment and approximate run time so that bidders can participate via Simulcast.

Manheim Consulting Evaluates Dealer Remarketing Performance

In an effort to assist dealers in optimizing their remarketing strategies, Manheim Consulting periodically evaluates individual dealer performance by comparing actual prices obtained against auction values of comparable vehicles in the same peri-ods. By letting the numbers speak for themselves, the analyses enable dealers to optimize remarketing by type of vehicle and channel.

Dealers have expressed satisfaction with the performance reports provided to them and, in an indication of how they are being used inter-nally, made specific requests for additional data to help them make smarter decisions.

The Manheim Consulting staff has now produced hundreds of reports for individual dealers. Overall, the conclusions support more proactive involvement by dealers in remarketing their vehicles. With overall dealer-ship profits under continuous pressure, dealers cannot ignore the potential to improve returns on wholesale units by applying the same techniques used by large consignors. The acceptance of business intelli-gence and technologies in dealership operations evolved slowly through 2005. Since then, driven by both need and improved functionality, these tools have become essential in maintaining financial performance.

Dealers

Dealers

1

2

3

needs data

61 817166 76 86 91 0196 1106

Source: Automotive News

468

101214161820

New Car and Light-Duty Truck SalesMillions of Units

Dealers Post Largest Used Unit Sales Gain Since 1993Annual Percent Change in Used Unit Sales by Dealers

Source: CNW Marketing Research

-10%-8%-6%-4%-2%0%2%4%6%8%

10%

0590 9291 9695 97 99 0098 01 02 03 060493 94 07 08 1009

2011 is a Manheim Consulting estimate based onboth internal and industry sources.

Source: National Auto Auction Association Surveys, 2001-2010

01 1002 03 04 05 06 07 08 09 11E0%

10%

20%

30%

40%

50%

60%

Dealer-Consignment Sales as Percentage of Total Auction Volume

needs data

39.4040.0140.5046.3051.6050.9050.0042.0039.3045.4055.50

17 2012 Used Car Market Report

2012Used CarMarket Report

Q&A With NADA Chairman William P. Underriner

National Automobile Dealers Association (NADA)

William P. Underriner, president and co-owner of Underriner Motors in Billings, Mont., is chairman of the National Automobile Dealers Association and represents Montana’s franchised new-car dealers on the association’s board of directors.

In the automobile business since 1984, Underriner took over the family business in 2001. He currently owns Honda, Hyundai, Buick, and Volvo franchises in Billings. Previously, he served three terms as treasurer of NADA and on the association’s Executive, Industry Relations, Dealership Operations, and Membership committees. He has also served as chairman of the association’s Finance and Convention committees. Underriner has held a variety of offices with the Montana Automobile Dealers Association, including chairman of the board.

Franchised dealers focused on their used car operations during the period of low new vehicle sales. Do you believe they will continue to emphasize used cars in the future?

Franchised dealers will continue to focus more of their resources on used cars in 2012. Many consumers are still uncertain about the current economy and are opting to buy lower-priced vehicles. Dealers are the best at adapting to changes in their local markets. Depending on a dealer’s circumstance, this retailing out of lower-priced trade-ins can make good business sense.

Auto companies are emphasizing their certified pre-owned (CPO) programs. Do consumers understand the value in the CPO designation compared to non-CPO units?

CPO vehicles have seen a surge in popularity. These vehicles offer customers a compromise between buying new and pre-owned and are in high demand. CPO vehicles do hold more value due to the mechanical inspection and additional warranty usually offered on these vehicles. CPO vehicles create more service business for the dealer besides what is in the certification process itself.

Franchised dealers retailed more of their off-brand trades in 2011. Does this represent profit opportunity for the fran-chised dealer or just a reflection of the current market?

Maintaining used vehicle inventory has been a challenge all year for all dealers. This constrained supply makes keeping off-brand vehicles a great strategy, but dealers still need the auction channel because they still need to wholesale units that are too far out of their target market.

In 2011, franchised dealers actively sought customers’ vehicles they would like to stock. Do you see them con-tinuing to try to acquire inventory directly?

We have seen franchised dealers buying used cars directly from their service customers. This makes sense because these vehicles have usually been properly serviced and cared for and dealers know the vehicles. These solicitations give the dealer a chance to acquire a good quality used vehicle and also the chance to sell a new vehicle.

Are all dealers spending more time and effort to find the used vehicles they need?

Yes, dealers are spending more time sourcing used car inventory. But using digital tools, searching online inventory, and attending live auctions allow us to see more inventory. This is a more effi-cient and better use of time and resources.

Can you give us your perspective on how digital technol-ogy has changed both acquiring used car inventory and remarketing of used cars by franchised dealers?

The digital market has made buying and selling used cars easier and more efficient. It also provides the ability to buy beyond our local market. Digital technology has changed the entire industry, and this trend will continue. Dealers must be proactive instead of reactive. Online vehicle condition reports are much more accurate today than when online buying first began, and this greatly reduces the risk to the buyer. This doesn’t mean dealers have given up on brick-and-mortar auctions. Auctions are like attending a sporting event. You can watch the event live rather than from your chair at home in front of the TV.

What kind of expertise does today’s used car manager need?

Dealer principals and general managers have had to take a more active role in used car management and operations. In this new economy, most dealers have operated with a smaller, more effi-cient staff, thereby creating the need for both dealer principals and general managers to be actively involved in the used car department. Used car managers must have knowledge of the market as well as current economic trends and vehicle valuations. NADA, along with partners such as Manheim, has developed an online solution, AppraisalPRO, which displays market data and is simple to use. It includes the next step forward for dealers – a mobile application with a VIN scanner.

18 2012 Used Car Market Report

2012Used CarMarket Report

Q&A With NIADA President Don Fincher

National Independent Automobile Dealers Association (NIADA)

Don Fincher became president of NIADA in 2011. Don has spent his entire working life in the auto retail industry, starting out at the age of 15 in his father’s store. After 18 years, Fincher took over one of his father’s stores and has operated that Buy Here, Pay Here store in Texas ever since. He has been active in NIADA and previously served as president of the Houston and Texas IADAs.

How would you describe business conditions for indepen-dent used vehicle dealers in 2011?

In general, demand for used vehicles improved and people wanted to replace their older cars with something better. There is always a base demand for used vehicles, but in 2011 we saw more cus-tomers coming in to replace their older vehicles. With retail credit more available, we see demand for used cars and trucks continuing to improve. The limiting factors for many customers are today’s high used car prices.

Many independent dealers relied on credit lines from local lenders in the past, but this changed after the credit crisis. How are used car dealers financing their busi-nesses today?

Many large operators have been able to attract private capital to replace the bank lines they previously relied on, but smaller, family-owned dealerships are often limited to their own capital or lines provided by auctions or specialty lenders. This can be a challenge for dealers who want to expand their inventory or grow their business.

How does the small used vehicle dealer stay profitable in this environment?

Used car dealers have always been resilient and kept costs, espe-cially overhead, down while managing inventory. But many successful dealers are niche sellers, and that often gives the small dealer a better chance to compete against larger, less focused operations. There are very successful smaller dealers who stock mainly pickup trucks and sport utility vehicles or mid-size trucks for commercial use. Some dealers make a very good return buying repairable units from salvage auctions. They suc-ceed with a small, but focused, inventory and provide good customer service.

The shortage of used vehicles pushed prices to record levels in 2011. What has that meant for used vehicle dealers?

High used car prices have made it more difficult for dealers to stock as many vehicles as they did in the past, so they have to be sure they carry the right models. Many dealers are now selling older, higher mileage vehicles. I know many dealers who used to pass on vehicles with more than 150,000 miles on them who now bid on them at the auctions. We’re learning that a high-mile-age car or truck can be mechanically sound and has a lot of life left in it. Our customers are also being educated to the value of these vehicles.

I don’t see the shortage abating soon. It will get better as new vehicle demand increases and more trade-ins come back to the auctions, but we are always going to have a shortage of 2008 through 2011 models.

Have dealers altered their sourcing strategies given the current shortage?

Dealers, myself included, still rely on auctions for much of their inventory. But market conditions have encouraged us to tap other potential sources, including buying some inventory directly from owners. Even small dealers advertise locally that they will make an offer on your car or truck.

Do you see NIADA members buying more of their inven-tory in digital auctions?

Yes, I do. I’m one of those people who spent his life in the lanes bidding on units that I inspected. It’s hard to transition to the digi-tal world, but I’ve gone through the training, and I know that I have to be active in both live and digital auctions.

Auctions have done a great job making the online experience work. With arbitration and inspection standards and more vehicles with condition reports, it is easier to buy with confidence.

19 2012 Used Car Market Report

2012Used CarMarket Report

Rental

Rental Industry Revenues Rise

The rental industry generated record revenues of $22.4 billion in 2011, up from $20.6 billion in 2010. A slow recovery in business and leisure travel resulted in more rental volume, but a sharp increase in the size of the rental fleet resulted in more competition and lower rates. Vehicles in service grew sharply due to a shift in mix between local and daily rental. In 2011, the rental industry purchased slightly fewer (1.40 million versus 1.41 million) new vehicles than in 2010, so the increase in fleet size reflected longer lengths of service.

Risk Vehicles Reduce Seasonal Swings in Fleet Size

Although risk vehicles enable rental companies to operate a mixed-brand fleet and negotiate purchases by make and model, they also prevent com-panies from adjusting fleet size to seasonal variations in demand. Rental demand peaks during the summer vacation period, with smaller peaks during spring breaks and from Thanksgiving through the New Year. When program vehicles dominated rental fleets, automakers shipped vehicles to rental companies in the spring and repurchased them in the fall. Thus, it was easier to downsize fleets in the early fall and add units in anticipa-tion of summer rentals. With risk vehicles now accounting for more than 70% of the fleet at most rental companies, there is less seasonal variation in overall fleet size and therefore more rate competition during slow travel months.

Cost Avoidance Influences Vehicle Service Life

Achieving favorable operating economics, depreciation in particular, dictates careful selection of vehicles equipped with features that support higher residual values. It also requires service lives that are often more than one year and sometimes as long as 18 months and 45,000 miles or more. Rental companies, like their commercial fleet counterparts, try to remove vehicles from service before they require another tire change or costly repair.

Rental

Rental

1

2

3

needs data

U.S. Car Rental Market Revenue In Billions

Source: Auto Rental News 2012 Fact Book

01 02 03 04 05 06 07 08 10 1109$0

$5

$10

$15

$20

$25

System Revenue Passenger Enplanements In Thousands of Scheduled Passengers

2009 2010 2011

45,000

50,000

55,000

60,000

65,000

70,000

75,000

Jan Feb Mar Apr May Jun Jul Sep Oct Nov DecAug

Source: Bureau of Transportation Statistics U.S. Department of Transportation

New Vehicle Sales Into Rental and�Rental Fleet Size In Millions

New Purchases Average Fleet Size

Source: Bobit Business Media

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

99 0100 0302 04 08 10 110605 0907

18.2016.4316.4617.6418.9120.4121.4921.4920.0520.5922.40

1.570698 1.7333911.686076 1.8290001.675712 1.7380001.711582 1.6430001.772285 1.6170001.936146 1.6650002.079675 1.7140462.054373 1.7680001.897486 1.8614611.503734 1.8130001.128426 1.6370001.412070 1.6290001.399353 1.760761

Rental

1

2

3

needs data

U.S. Car Rental Market Revenue In Billions

Source: Auto Rental News 2012 Fact Book

01 02 03 04 05 06 07 08 10 1109$0

$5

$10

$15

$20

$25

System Revenue Passenger Enplanements In Thousands of Scheduled Passengers

2009 2010 2011

45,000

50,000

55,000

60,000

65,000

70,000

75,000

Jan Feb Mar Apr May Jun Jul Sep Oct Nov DecAug

Source: Bureau of Transportation Statistics U.S. Department of Transportation

New Vehicle Sales Into Rental and�Rental Fleet Size In Millions

New Purchases Average Fleet Size

Source: Bobit Business Media

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

99 0100 0302 04 08 10 110605 0907

18.2016.4316.4617.6418.9120.4121.4921.4920.0520.5922.40

1.570698 1.7333911.686076 1.8290001.675712 1.7380001.711582 1.6430001.772285 1.6170001.936146 1.6650002.079675 1.7140462.054373 1.7680001.897486 1.8614611.503734 1.8130001.128426 1.6370001.412070 1.6290001.399353 1.760761

Rental

1

2

3

needs data

U.S. Car Rental Market Revenue In Billions

Source: Auto Rental News 2012 Fact Book

01 02 03 04 05 06 07 08 10 1109$0

$5

$10

$15

$20

$25

System Revenue Passenger Enplanements In Thousands of Scheduled Passengers

2009 2010 2011

45,000

50,000

55,000

60,000

65,000

70,000

75,000

Jan Feb Mar Apr May Jun Jul Sep Oct Nov DecAug

Source: Bureau of Transportation Statistics U.S. Department of Transportation

New Vehicle Sales Into Rental and�Rental Fleet Size In Millions

New Purchases Average Fleet Size

Source: Bobit Business Media

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

99 0100 0302 04 08 10 110605 0907

18.2016.4316.4617.6418.9120.4121.4921.4920.0520.5922.40

1.570698 1.7333911.686076 1.8290001.675712 1.7380001.711582 1.6430001.772285 1.6170001.936146 1.6650002.079675 1.7140462.054373 1.7680001.897486 1.8614611.503734 1.8130001.128426 1.6370001.412070 1.6290001.399353 1.760761

20 2012 Used Car Market Report

Rental

Small rental operators, especially those that are located off-airport, buy used vehicles for their fleets. Lack of supply, however, limited these purchases in 2011. In addition, in the second quarter, major rental companies also turned to used vehicles when confronted by cancellations and delivery delays. Rental companies see used vehicles as a potential source of seasonal supply and have experimented with sourcing and integrating used vehicles into fleets for a service life of three to five months. But currently, the supply of quality late-model vehicles is not adequate to make this a significant source.

Rental Companies Strive to Reduce Days to Sale

Rental companies are focused on reducing fixed costs, recovering the cost of customer damage to vehicles, raising employee productivity, and applying life cycle cost management across the fleet. Remarketing strategies are still evolving within the industry as companies embrace digital technology to expose their inventory to more buyers – often even before vehicles come out of service. The profitability of a rental company is highly dependent, not just on the price paid for each vehicle, but equally important, on the value obtained when the unit is taken out of service. Remarketing channels that reduce days to sale and avoid expenses, transportation in particular, are favored by this industry. In other words, digital channels are important.