the used car market report 2012 - university of buckingham

TRANSCRIPT

Centre for Automotive Management The University of Buckingham Business School www.buckingham.ac.uk/cam

The Used Car Market Report 2012

A REPORT BY BCA

The Used Car Market – a report by BCA

3

Foreword

We are delighted to bring you this

22nd edition of the BCA Used Car

Market Report.

This year's research looks at the

effect that continuing financial

pressures are having on private

motorists' decisions on buying and

running their car, and the impact of

prolonged, lower new car volumes

on the used car market.

Our editor, Professor Peter N C

Cooke, the Professor of Automotive Management, the Centre for Automotive

Management at The University of Buckingham is a well-known commentator

on the automotive industry.

Professor Cooke spent over 20 years in the motor industry and has taught,

researched and written about the industry at business schools for a similar

period. He has undertaken much work on the fleet, used car and LCV sectors

and edited the BCA Used Car Market Report for several years.

The Buckingham Automotive team has sought to retain the best aspects of

this long-standing report, and has developed new analysis and commentary

on the changing shape of used car market.

Given the uncertainty surrounding the UK’s gloomy economic outlook, and

the implications for the automotive sectors, the BCA Used Car Market Report

2012 is most timely for everyone involved in the used vehicle industry.

Jon Olsen CEO BCA Vehicle Remarketing

The Used Car Market – a report by BCA 4

Contents

Foreword 3

Introduction 6

Overview

Used car market stable The new car market The used car market Consumer perspective

7

789

10

UK Market Review

Used car volumes continue to rise Used:new car ratios Used car market sectors Dealers’ used car volumes Private sector used car sales UK car market value rises Dealer/private sector used car market value Used car selling prices Used car prices at auction Car parc oldest for quarter of a century Cars being scrapped earlier The ‘parc turn’ indicator Car parc ageing rapidly Company car disposals fall

12

1212121315161718181920212223

Consumer Experience

Part One – What Used Car to Buy? What used car to buy next? 'Crunch Factors' Part Two – Where to Buy From? Which used car retailer to buy from? Buying from franchised and non-franchised dealers Three-quarters of motorists buy a used car Seven out 10 families own a car Hatchbacks and saloons most popular Buying used rather than new? Sales of used diesels fall Used car satisfaction rises once more Part Three – Dealer Relations and Buying Intentions Used car customer follow-up Buying a car in the next year? What type of car to buy next? Where to buy the next car? Part Four – Economic Recovery, Running Costs, and Keeping in Touch What car to buy during economic recovery? Reducing personal motoring carbon footprint Offsetting the rising cost of fuel Steps Taken to Cut Car Running Costs Keeping Customers in the Loop A Good Deal is Still the Critical Factor

25

262627282829293031323233353536363738383940414243

The Used Car Market – a report by BCA 5

Contents

Regional Review

'Friends and Family' Holds More Sway This Year Dealer follow-up calls When to buy the next car? Where to buy the next car? What car to buy next? How satisfied are used car owners? Cutting Back on Running Costs

44

44454646474849

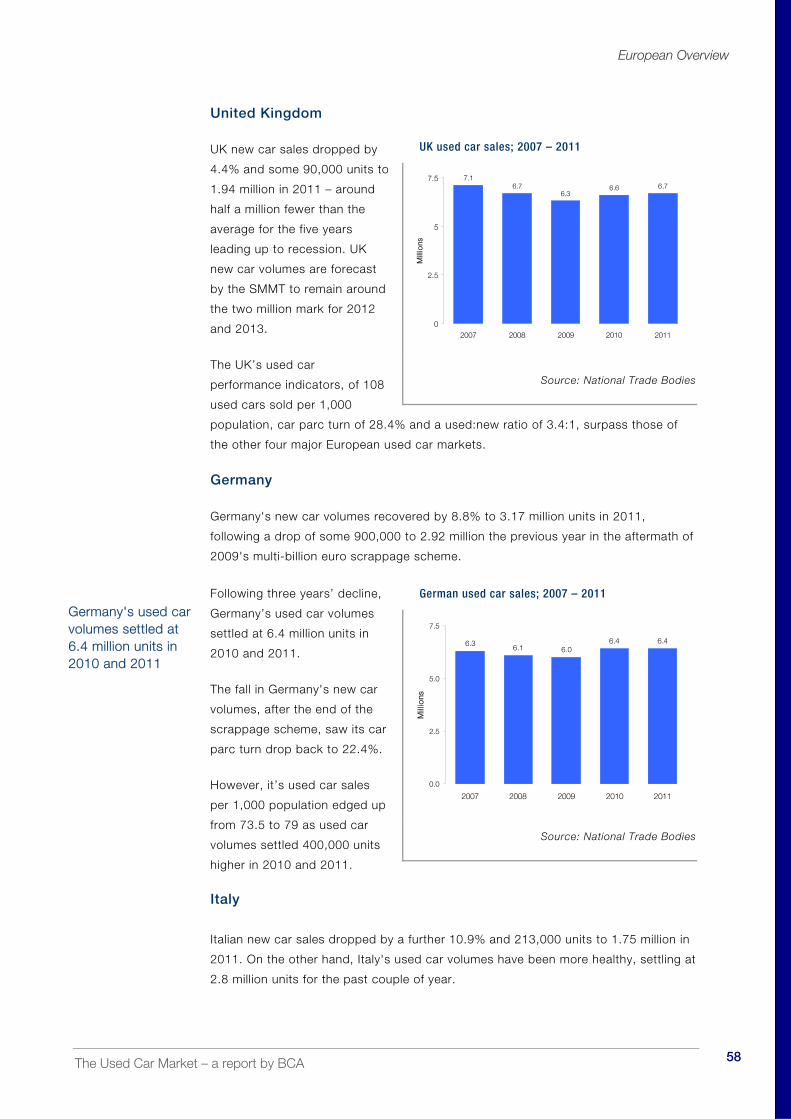

European Overview

New car market EU15 markets New member states Used car volumes Car parc Parc Turn Percentage Used:new volume ratios Used car sales per 1,000 population United Kingdom, Germany. Italy France, Spain

50

50515253545556575859

United Kingdom Economic Situation

The UK Economy – A Macroeconomic Viewpoint Not for the Faint Hearted Mid Year Financial Crisis Do We Have a Plan B? Used Car Market

61

6162646366

Prospects, Buyers and Follow-ups

Tyre-kicking Has Gone Online Social Media Presence A Fickle Mistress Customer Contact – What Is It Really? Car Owners' Preferences What Car To Consider Buying? Strategic Implications

67

67676768697071

LCVs – A Black Hole on the Horizon?

New LCV Sales Plummet Replacing Overage Vehicles The Used LCV Supply Gap Not Yet Critical Emerging Issues for the LCV Industry

72

7273747475

Dealers Need to Face Changes in Consumer Behaviour 76

BCA – Europe's Leading Vehicle Remarketing Company 79

BCA Network 82

Statistical Data 83

Research 97

The Used Car Market – a report by BCA 6

Introduction

The BCA Used Car Market Report 2012 aims to provide the same invaluable insight

into the latest developments in the UK used car industry that each of our previous

editions has done.

The UK Market Review is based on statistical information from national sources. This

is updated and compared with previous years’ data to provide an authoritative

assessment of volume and value trends in the used car market.

The Consumer Perspective section of the report is based on a BMRB International

survey of UK car owners. This contains a review of the key issues that influence used

car buyers when deciding which car to buy, where to buy from and what car owners

expect when buying a used car.

This year, the consumer survey also looked at what type of car motorists might

consider buying as the country's economy struggles to recover, and how high fuel

prices would have to rise before car owners decide to change to a more fuel-efficient

car. Respondents were also asked if they had taken any concerted steps to reduce

their car running costs and how they prefer their used car dealer to keep in contact

with them.

The European section of the Used Car Market Report contains updated trend

information on Europe’s new and used car markets.

Other sections include ‘United Kingdom Economic Situation’ looking at the impact of

the economy on the country's new and used car markets – while 'People, Buyers and

Follow-ups' considers the critical role of communications from used car retailers' and

their customers' point of view.

The report also looks briefly at the used LCV market and the key issues driving this

key automotive sector. The used LCV sector will be examined in more detail in the

forthcoming ‘Used LCV Market Report 2013'.

BCA is pleased to provide this 2012 edition of its Used Car Market Report to all those

associated with the UK automotive industry.

The Used Car Market – a report by BCA 7

Overview

Used car market stable

The severe 2008/2009 economic downturn pushed combined new and used car

volumes below the nine million mark to 8.8 million units in 2008, dipping to 8.3 million

the following year.

Thereafter, combined sales settled at 8.6 million units in 2010 and 2011 as stronger

used car volumes offset the impact of the weaker new car market.

Market volumes new vs. used; 2002 – 2011

2.02.12.42.32.42.62.62.6

2.0 1.9

6.36.7

7.17.47.3

6.87.2

6.6 6.6 6.7

9.79.8

9.29.7

9.4 9.5

8.88.3

8.6 8.6

1

2

3

4

5

6

7

8

9

10

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Mill

ions

New Used Total

Source: SMMT/BMRB

Following an 11-year spell comfortably over two million units, new car sales fell to

1.99 million in 2009 – falling back to 1.94 million units in 2011 after a brief recovery

to 2.03 million in 2010.

The UK accounted for 15.2% of Western Europe's new car market in 2011,

compared with 15.6% the previous year – and holds third place in the European new

car sales league ahead of Italy (1.75 million) by 193,000 units.

UK used car volumes dropped during the recession to 6.3 million units in 2009.

Despite a weak and uncertain economy used car volumes rose to 6.6 million in 2010,

edging up to 6.7 million units in 2011.

Overview

The Used Car Market – a report by BCA 8

The new car market

Following six years over the £30 billion mark, the value of the UK new car market

dipped to £28 billion in 2008 and 2009 as new car volumes fell steeply during

recession.

The new car market value recovered to £28.7 billion in 2010 and reached £29 billion

the following year, despite a 90,000 drop in new car volumes in 2011.

New car market volume and value; 2002 – 2011

1.9 1.9

2.1

1.7

2.42.4

2.6 2.6 2.6

2.3

32.4

33.5

32.4 32.2 32.433.0

28.1 28.028.7 29.0

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Mill

ions

20

25

30

35

£ b

illion

Volume Value Scrappage deals

0.30.1

Source: SMMT//BMRB

Despite the boost from 285,000 scrappage deals, new car registrations fell steeply to

1.99 million units in 2009, and have failed to improve significantly since. 2011 saw

new car volumes slip 4.4% to 1.94 million compared with 2010's figure of 2.03 million

units.

Private sector new car sales dropped 14.1% and 134,911units to 823,094 in 2011.

New car sales to the 25-plus fleet sector broke through the one million mark once

more last year, rising 4.7% to 1.02 million units, pushing this sector's new car market

share up to an all-time high of 52.5%.

As high prices of fuel, food, household essentials and high unemployment continue to

erode car buyers' confidence and spending power, new car volumes remain relatively

weak in 2012 – edging up 2.7% on 2011's low base to 1.06 million for the first six

months of the year – still some 15% below 2007's pre-recession level.

However, the SMMT believes the new car market is stabilising, with the 12-month

running total of 1.97 million units, at the end of June 2012, some 30,000 above

2011's full year figure. It predicts the UK's new car market will rise 1.6% to 1.97

million in 2012 – and by a further 1.0% to 1.99 million units in 2013.

Overview

The Used Car Market – a report by BCA 9

The used car market

UK used car sales topped seven million for four out of five years from 2003, falling

back to 6.3 million units in 2009 as recession hit the used car market hard. While

hopes of an economic recovery saw used car volumes rise to 6.6 million in 2010,

growth slowed to 6.7 million units in 2011 as the economy headed towards a double-

dip recession. UK used car market values edged upwards in 2011 to a new high of

£35.7 billion.

Used car market volume and value; 2002 – 2011

6.7

6.3

7.1

7.47.3

6.8

7.2

6.6 6.66.7

28.1

32.0

30.0

32.3

33.933.3

32.4

34.235.0

35.7

4

5

6

7

8

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Mill

ions

20

25

30

35

40

£ billion

Volume Value

Source: BMRB

Stronger supply and sales of 6-8 year-old cars saw used car market volumes grow by

118,000 units to 6.69 million in 2011, as weaker supply from lower new car sales

continued to hamper sales of younger used vehicles.

Dealers' and private sector used car volumes both grew in 2011 – the former's up 2%

to 3.74 million and the latter's 7% higher at 2.63 million units.

Sales of cars in the 0-2 year age group dropped 9.5% to 642,000 units in 2011 –

this segment's share of the market down to 9.6% from 10.8% the previous year.

Sales of 3-5 year-old cars fell by 6.2% to 1.73 million units, their used car market

share slipping 2.2% to 25.8%.

The 6-8 year age group's sales volumes continued to rise in 2011, up 7.4% and

124,000 to 1.79 million units, their share of the market 1.4 points higher at

26.8% – boosted by high volumes of new cars sold in the first half of the 2000s.

Sales of 9 years-plus cars grew for the second year running, rising by 7.5% to

2.53 million and 37.8% of the used car market.

Overview

The Used Car Market – a report by BCA 10

Consumer perspective

Twenty-four per cent of this year's consumer survey's respondents had bought a car

over the past two years, three-quarters of them choosing to buy a used car instead of

a new vehicle.

'Views of friends and family' (24%) edged 'personal experience of make and

model' (21%) into second place amongst the issues motorists consider when

thinking about what used car they might buy next. ‘Independent Internet sites'

were a factor with 16% of used cars buyers, while 'used car sites/showrooms'

(12%) and 'dealers' websites' (10%) are also significant factors.

'Price' (41%), 'low mileage' (31%) and 'make and model', cited by 30% of car

owners, are 'crunch factors' in deciding which particular used car to buy –

although 'engine size' (18%) and 'body type' (17%) are also key factors.

Affordability tops motorists' priorities when deciding which used car retailer to

buy a car from. 'I got a good deal on the car' was the number one issue for a

third of survey respondents, followed by 'the right car at the best possible price'

for three out of 10 used car buyers. A fifth of used car owners look to 'trade in'

their existing car and prefer to do business with a 'local dealer'.

Diesel-engined cars’ used car market share dipped to 33% in 2012 from 34% in

2011 and 36% in 2010 – as fewer fleet vehicles from 2009's low new car

volumes reached the marketplace and private used car buyers looked towards

smaller, petrol-driven models.

Owners' satisfaction with their used car rose two points to 95% this year – 67%

of them saying they were 'very satisfied', while 28% were 'quite satisfied' with

their latest used vehicle.

This year's report shows a marked drop in the number of car owners who believe

they will 'certainly' or 'quite likely' buy a used car in the next 12 months – down

3% to 11% in 2012 from 14% the previous year. The number of motorists who

believe there is a '50:50 chance' they will buy a car in the next year edged up

one point to 9%.

Three-quarters of car owners plan to replace their car with a used one next time

they make a change. However, there has been a swing of 4% towards diesel this

time – 30% of prospective used car buyers saying they intend to go in this

direction – a long way short of diesels' current 50% share of the new car market.

The number of car owners saying they will deal with a franchised dealer next time

rose by 5% to 50% in this year's survey, half of them trading in their old car.

Thirty per cent of motorists plan buying privately or from a friend, while 13% are

considering doing business with a non-franchised used car retailer.

Overview

The Used Car Market – a report by BCA 11

Faced with a gloomy economic outlook, nine out of 10 motorists intend to

replace their car with a different type of vehicle next time. Top of their shopping

list are 'a car with better fuel consumption', 'lower road tax', 'a smaller car',

'best purchase price' and 'lower CO2' – all things that used car buyers have a

great degree of control over.

'Walking more often' and 'cutting the number of journeys' top the list of

measures motorists have in mind to cut their personal CO2 – with other steps

such as 'driving more slowly', 'reducing annual mileage', 'buying a car with lower

emissions' and 'buying a smaller car' also in the frame.

Over half of this year's respondents (53%), believe the higher price of fuel will

eventually push them into 'buying a more fuel efficient vehicle' or 'change their

driving habits' – or both

Car owners show a clear preference for receiving the least invasive type of

communication from the dealer they bought their used car from; ones they can

read and absorb when it suits them and not the sender. Email leads the field in

this respect, cited by a fifth of survey respondents as their preferred means of

contact, followed by letters/mailing then websites.

Evolution or revolution?

The Overview points to an automotive industry in evolution, some would claim closer

to revolution on a number of fronts;

The second recession in under four years, and the prospect of an agonisingly

slow economic recovery is reflected in prolonged low new car market volumes –

'starving' the used car market of younger, lower mileage units – with no prospect

of a significant upturn in sight.

Younger used car availability will become much tighter before it improves, with

the pent-up demand for younger and middle-aged used cars increasingly difficult

to satisfy for some considerable time to come.

Diverging private sector and business new car buyer patterns mean the mix of

cars that will ultimately enter the used car market will differ significantly from the

historic stock profile with associated revenue and profit implications.

New and used car markets appear to have become increasingly price sensitive in

recession which, in turn, will put increased pressure on 'value for money' - and

dealer margins.

Perhaps dealers may have to rethink car buyers' affordability in terms of selling

new or used cars, and consider the product offering more in terms of monthly

payments than a one-off capital price?

The Used Car Market – a report by BCA 12

UK Market Review

Used car volumes continue to rise

2011 saw car buyers'

confidence and incomes

eroded by a powerful mix of

high inflation, escalating fuel

costs, rising unemployment

and an economy heading

towards a double-dip

recession.

This saw new car sales fall

4.4% to 1.94 million last

year – around a half a

million units lower than pre-

recession market volumes.

A rise of 1.8% in used car volumes to 6.7 million units and flat used car selling prices

saw the used car market value edge up £0.7 billion to a new high of £35.7 billion last

year.

Used:new car ratios

The ratio of used car sales to new car sales rose

for the second year running in 2011 to 3.4:1, as

used car volumes increased to 6.7 million and

new car volumes dropped 90,000 to 1.94 million

units.

Used car market sectors

Rising sales of 6-8 year-old

cars helped used car

volumes rise by 1.8% and

118,000 units to 6.7 million

as sales of cars in the 0-2

and 3-5 year age groups

slipped further in 2011.

Dealers' and the private

sector's used car sales both

grew in 2011 – dealers'

volumes up 2% to 3.74

million and private sales 7%

higher at 2.63 million units.

Car volume trends; 2007 – 2011

2.42.1 2.0 2.0 2.0

7.16.7

6.36.6 6.7

0

1

2

3

4

5

6

7

8

2007 2008 2009 2010 2011

Mill

ions

New Used

Source: SMMT/BMRB

Used:new car ratios; 2007 – 2011

2007 3.0:1

2008 3.2:1

2009 3.2:1

2010 3.3:1

2011 3.4:1

SMMT/BMRB

Volume of used car sales by source; 2007 – 2011

0.4

2.7

4.0

7.1

0.4

2.7

3.6

6.7

0.6

2.2

3.5

6.3

0.5

2.4

3.7

6.6

0.3

2.6

3.7

6.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Mill

ions

2007 2008 2009 2010 2011

Other/Auction Private Dealers Total

Source: BMRB

The used car market edged up to a new high of £35.7 billion

UK Market Review

The Used Car Market – a report by BCA 13

Looking at the age profile of used cars sold in 2011 shows the market continues to

change:

Sales of cars in the 0-2 year age group fell for the third year running in 2011, by

9.5% to 642,000 units, pushing this segment's share of the used car market

down to 9.6% from 10.8% the previous year.

Sales of 3-5 year-old cars also dropped last year, by 6.2% to 1.73 million units,

their used car market share slipping 2.2% to 25.8%.

Used car market volume by age of car; 2007 – 2011

642710

989 978

762

1725

1840188418821949

1632 15831481

1793

1669

2489

2208 2174

25292352

500

1000

1500

2000

2500

3000

2007 2008 2009 2010 2011

Tho

usan

ds

0-2 3-5 6-8 9+ yrs

Source: BMRB

Sales of cars in the 6-8 year age group continued to rise in 2011 by 7.4% and

124,000 units to 1.79 million, driving this sector's market share up 1.4 points to

26.8% – as record high volumes of new cars sold in the first half of the 2000s

bolstered supply in this segment of the used car market.

9 years-plus used car volumes grew for the second year, rising 7.5% to 2.53

million and 37.8% of the used car market.

Dealers’ used car volumes

Stronger sales of 6-8 year-old cars helped used car retailers' volumes grow 2% to

3.74 million units in 2011, their share of the market remaining at 55.9% (see overleaf).

Dealers' sales in the 0-2 year age group slipped by 1.5% to 535,000 units, but

their share of this segment rose to 83.3% in 2011.

Dealers' 3-5 year-old used car volumes rose by 1.8% and 23,000 to 1.33 million

units, their share of this sector reaching a three-year high of 76.8%.

Sales of cars in the 6-8 year age group continued to rise in 2011

UK Market Review

The Used Car Market – a report by BCA 14

Dealers’ used car volumes and market share; 2002 – 2011

3.57

3.87

3.66

3.874.01 3.97

3.613.53

3.673.74

55.955.856.0

54.3

56.3

54.8

53.353.653.654.3

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

% M

arket share

40

45

50

55

60

Mill

ions

Millions Market share

Source: BMRB

While dealers' sales of cars in the 6-8 year age group rose for the second year in

2011, their share of this segment slipped 0.9% to 62.8% as retailers faced fierce

competition in this buoyant sector of the market.

Dealers’ used car volume by age of car; 2007 – 2011

663

856

854

543 535

15421462

13581302 1325

1063 11261034

780

965

759 755

473513

606

0

200

400

600

800

1000

1200

1400

1600

1800

2007 2008 2009 2010 2011

Tho

usan

ds

0-2 3-5 6-8 9+yrs

Source: BMRB

Used car retailers' share of the 9 years-plus group fell to 29.9% in 2011, their

volumes dropping 0.5% to 755,000 as a growing number of buyers turned to

private sources for cheaper cars.

UK Market Review

The Used Car Market – a report by BCA 15

Dealers' used car sales

continued to edge towards

older cars. As new car

volumes feeding the market

settled around two million

units for the fourth

successive year in 2011,

retailers were forced to look

to older units for adequate

used car supply.

Sales of 0-2 year-old cars

now account for just 14% of

dealers' used car volumes,

while sales of cars in the 6-8

year group account for 30% of their used car business compared with 24% five years

earlier.

Private sector used car sales

Higher volumes in the 6-8 year group (+15.9%) pushed the private sector's used car

volumes up 7% to 2.63 million units in 2011 – its share of the used car market rising

1.9 points to 39.3%.

Private to private used car volumes by age of car; 2007 – 2011

609399 65 47

281278317

326313

598708

348

513442

16441774

15061594

1703

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2007 2008 2009 2010 2011

Tho

usan

ds

0-2 3-5 6-8 9+yrs

Source: BMRB

The private sector's sales of 0-2 year-old cars dropped by 33,000 units to

60,000 units in 2011, its share of this segment dipping to 9.4%.

Volume share of dealers’ used car sales, by age of car 2011

6-8 years30%

3-5 years36%

0-2 years14%

9+years20%

Source: BMRB

Retailers were forced to look to older units for adequate used car supply

UK Market Review

The Used Car Market – a report by BCA 16

While private-to-private sales of 3-5 year-old cars rose by 3,000 to 281,000 units

last year, their share of the sector slipped from 11.3% to 10.7% year on year, as

dealers fought hard for supply in a sector weakened by ongoing low new car

volumes.

The private sector’s sales of cars in the 6-8 year age group rose 15.9% and

70,000 to 513,000 units, taking 28.6%of this segment compared with 26.5% the

previous year.

Private-to-private 9 years-plus used car volumes grew by 130,000 units to 1.77

million last year, their market share edging up to 70.2% from 69.9%.

The unpredictable supply of quality, 0-5 year-old cars saw used car retailers focusing

more on vehicles in the 6-8 year age group, where there is currently a stronger supply

from the high new car volumes in the early 2000s.

Last year a struggling economy heading for a double-dip recession, falling family

incomes, high unemployment and stubbornly high inflation, saw consumer confidence

hit hard and more used car buyers turn to older, cheaper used cars.

UK car market value rises

The total value of the UK's new

and used car markets rose by £1

billion to £64.7 billion in 2011, as

higher used car volumes offset a

drop in new car sales – some way

short, though, of the pre-recession

high of £66.3 billion reached in

2007.

While new car volumes fell by 4.4%

last year, a move towards larger

cars and prestige marques (SMMT registration data) saw the value of the new car

market edge up £0.3 billion to £29 billion.

Higher used car volumes made up for flat average used car selling prices – reflecting

an ageing mix of used car sales. This helped push the value of the used car market

up £0.7 billion to a new high of £35.7 billion last year – £6.7 billion higher than the

new car market value.

New and used car market values; 2007 – 2011

£ billions 2007 2008 2009 2010 2011

New 33.0 28.1 28.0 28.7 29.0

Used 33.3 32.4 34.2 35.0 35.7

Total 66.3 60.5 62.2 63.7 64.7

Used % * 50.2 53.6 55.0 54.9 55.2

* as % of total market value

Source: BMRB

The value of new and used car markets rose to £64.7 billion in 2011

UK Market Review

The Used Car Market – a report by BCA 17

Dealers/private sector used car market value

Dealers' used car market value edged up £0.3 billion to £26.8 billion in 2011, higher

used car volumes counteracting lower selling prices from the ageing used car sales

profile. The private sector's market value also increased, by £0.6 billion to £7.4 billion

last year, a combination of higher volumes and selling prices.

Value of used car sales by source; 2007 – 2011

1.7 1.4 1.7 1.53.4

7.05.9 5.66.8 7.4

25.724.0

25.226.5 26.8

33.3 32.434.2 35.0 35.7

0

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011

£ B

illio

ns

Other/Auction Private Dealers Total

Source: BMRB

Share of used car market value; 2002 – 2011

76.374.274.7 75.3 75.5 75.175.673.774.077.0

21.3 19.5 18.2 17.8 17.6 17.721.6

16.419.3 20.7

0

10

20

30

40

50

60

70

80

90

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

%

Franchised/non-franchised Private to private

Source: BMRB

Franchised and non-franchised used car dealers retained their three-quarters share

(75.1%) of used car market value in 2011; the private sector's share rising to 20.7%,

as fewer used car buyers resorted to auction or other sources last year.

UK Market Review

The Used Car Market – a report by BCA 18

Used car selling prices

Overall average used car selling prices remained flat at £5,336 in 2011, compared

with £5,332 the previous year, Dealers’ average used car selling prices slipped from

£7,295 to £7,169, while the private sector's average used car prices edged up £66 to

£2,815.

The chart below shows the relationship between dealers' used car selling prices and

the Retail Price Index (RPI) over a 20-year period. While the two indices have followed

much the same trend over this time span, dealers' selling prices tend to be lower

than RPI during periods of economic downturn and credit restrictions.

Average dealers' used car selling prices; 1998 - 2011

164.8162.1

223.9

199.2

147.3142.8

139.5134.8

131.6129.6

124.9

118.0

107.8

152.4154.7

159.3

174.6169.6

179.6185.3

193.3

203.9

213.7

203.6

186.0

148.4

138.6

117.4 103.7

120.9

120.6

121.3

132.8

101.4

162.4158.1

164.5163.0166.7

174.1177.5

178.3178.0183.6

202.9

207.2

100

110

120

130

140

150

160

170

180

190

200

210

220

230

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

RPI Dealers' used car selling price

Source: BCA

The gap between selling prices is currently wider than any point since 1990. Is this a

sign of the length and depth of the current recession, price sensitivity or a shift

towards older used cars?

Given the forecasts of at least a further 18 months of economic woes, it could be

some time before the two indices converge once more – although this will be helped

by the significant fall in the RPI index, which dropped from 5.5% to 2.8% over the

past 18 months, and is expected to fall further.

Used car prices at auction

Average used car prices at auction fell steeply during recession to £4,836 at the end

of 2008. They made a strong recovery during 2009 and 2010 reaching £6,451 in

December 2011 – a rise of £1,515 over the three year period.

Average used car selling prices remained flat at £5,336

UK Market Review

The Used Car Market – a report by BCA 19

Average used car prices at auction; 2009 – 2012

£5,9

38

£5,7

92£5

,792 £5

,905

£5,9

74£5

,985

£5,7

52£5

,626 £5

,790

£5,6

62£5

,633

£5,8

88£6

,252

£5,9

63

£6,2

01£6

,451

£6,0

40£6

,244

£5,9

74

£5,5

99£6

,098

£5,9

64

£5,9

05

£5,7

84£5

,802

£5,6

56£5

,871

£5,7

91£5,9

59£5

,939

£6,1

88£5

,903£6

,021£6

,217

£6,2

23

£6,0

28£5

,850

£5,1

36£5

,571

£5,5

82£5

,641 £5

,773

£4,000

£4,500

£5,000

£5,500

£6,000

£6,500

£7,000

Jan-09

Mar May July Sept Nov Jan10

Mar May July Sept Nov Jan-11

Mar May July Sept Nov Jan-12

Mar May

Source: BCA

Apart from a seasonal blip in April, auction prices remain firm in 2012; fleet and lease

values reaching a record high of £8,042 in June this year – even though the average

fleet car sold had recorded 3,000 miles more than those coming to market 18 months

earlier. Good quality vehicles remain in short supply in the fleet sector and buyers

continue to focus on quality and value, while competition for the best vehicles is

fierce.

The rise in average values at the 'value-for-money' end of the market reflects the

squeeze on household budgets and the increased demands from motorists for

affordable transport.

However, the supply side of the auction market cannot be overlooked. There have, at

times, been supply constraints of the best, retail quality cars which, in a competitive

remarketing environment, are contributing to the general strength in auction values.

Cars in parc oldest for quarter of a century

The UK car parc rose steadily for decades to 30.2 million in 2007, settling around

that level since as new car market volumes fell to two million units in 2009 and have

failed to recover from that point.

The average age of cars in the parc, which had fallen to a 14-year low of 6.69 years

in 2004, has climbed to 7.44 over the past six years – the highest figure for over a

quarter of a century (see overleaf). The average age of cars in the parc will reach new

heights over the next few years as the bulge of new cars sold in the early 2000s head

for the 10-years plus mark – and will only decrease when new car volumes

substantially exceed two million units for several years.

Fleet and lease auction values reached a record high of £7,934

UK Market Review

The Used Car Market – a report by BCA 20

UK car parc – average age of car; 2002 – 2011

30.430.330.130.330.229.0 29.4 29.8 29.9

28.5

7.25

7.06

6.88

6.706.78

6.69 6.786.79

6.93

7.44

10.0

15.0

20.0

25.0

30.0

35.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Mill

ions

5.00

5.50

6.00

6.50

7.00

7.50

Averag

e age

Millions Average age

Source: SMMT

Cars being scrapped earlier

The number of

cars running until

the 12-year mark

rose to 75.3% at

the end of 2011,

from 71.7% the

previous year, as

most of the

400,000 ten-years-

plus units, traded

in under the

scrappage scheme

in 2009/2010,

were replaced by

younger cars.

Cars continue to

be scrapped

earlier; only 36.1% of them on the country's roads at the 15-year point compared

with 40% ten years earlier.

UK car parc survival rate; 2011 vs. 2002

30

40

50

60

70

80

90

100

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Years

Sur

viva

l rat

e %

2011 2002

Source: SMMT Cars continue to be scrapped earlier

UK Market Review

The Used Car Market – a report by BCA 21

The ‘parc turn’ indicator

The ‘parc turn’

indicator, which

expresses annual

new and used car

volumes as a

percentage of the

UK car parc, is a

useful way of

monitoring car

sales trends.

The overall ‘parc

turn’ slipped from

28.4% in 2010 to

28.3% in 2011, 5.5

points below

2003's figure when

new and used car sales were both at a peak. This was due to flat new and used car

volumes of 8.6 million and the car parc rising 0.1 million to 30.4 million units.

The new car parc turn fell to 6.3% in 2011 from 6.6% the previous year, reflecting a

drop of 4.4% and 90,000 units in new car volumes.

In contrast, an

increase of 1.8%

(118,000 units) in

used car sales saw

the used car parc

turn rise marginally

to 22%.

Franchised and

non-franchised

dealers' slice of the

used car parc turn

edged up to 12.2%

last year, while the

private-to-private

sector's share rose

0.5 points to 8.6%.

Car parc turn; 2002 – 2011

23.522.1

20.921.8 22.0

24.824.523.2

24.823.1

6.36.66.66.97.97.78.08.89.09.1

28.328.427.629.0

31.532.3

33.832.0 32.532.5

0

5

10

15

20

25

30

35

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

%

Used % parc New % parc Total

Source: SMMT/BMRB

Dealer vs. private sector used car parc turn; 2002 – 2011

13.2

11.911.6

12.1 12.2

13.7

13.112.6

13.5

12.5

8.68.1

7.3

8.98.9

9.710.1

9.6

10.3

9.5

5.0

7.5

10.0

12.5

15.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

%

Dealer % of parc Private % of parc

Source: SMMT/BMRB

The overall 'parc turn' slipped from 28.4% in 2010 to 28.3% in 2011

UK Market Review

The Used Car Market – a report by BCA 22

Car parc ageing rapidly

While the car parc is destined to settle around the 30 million mark for at least the

next three years, the average age of cars on the country's roads has increased

rapidly. This will continue to do so as current new car volumes flat line around two

million units and cars from record new car sales in the early 2000s are approaching

the 10-years plus mark.

The used car

supply chain is

essentially a

funnel; new cars

feed into the top of

the funnel and flow

down to ultimately

become used cars,

changing hands

four times on

average before

they are scrapped

(source SMMT).

It's stating the

obvious, if the flow of new cars slows down markedly for some considerable time,

this has a dramatic impact on the supply of younger used cars available to be sold.

The effect of the last four years' low new car volumes, and similar low forecasts, is

shown in the following chart which illustrates the striking change in the volumes of

cars in the various age group segments.

UK car parc segments; 2000 – 2015

4.344.07

3.893.853.823.883.984.38

4.584.624.865.055.155.09

4.754.42

5.74

5.795.866.056.19

6.546.847.01

7.297.557.567.28

6.856.57

6.436.25

5.87

6.226.566.856.81

7.087.317.31

7.056.65

6.396.266.085.79

5.535.29

14.9514.6714.24

13.6513.55

12.80

11.9511.60

11.2611.0610.9410.7810.9011.0311.0911.22

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

Millio

ns o

f ca

rs

0-2 years 3-5 years 6-8 years 9+ years

Source: SMMT/Buckingham

UK new car sales; 2000 – 2015

0.28

0.11

2.34

2.22 2.20

1.94

1.921.71

2.13

2.40

2.57

2.442.46

2.56 2.58

2.10

1.952.00

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Mill

ions

of

cars

New car sales Scrappage deals New car sales forecast

2.031.99

Source: SMMT/Buckingham

Used cars change hands four times on average before they are scrapped

UK Market Review

The Used Car Market – a report by BCA 23

The report has shown that franchised and non-franchised used car retailers depend

on 0-5 year-old cars for 50% of their business and on cars in the 6-8 year age group

for a further 30% of their sales.

The chart shows there were 1.9 million fewer 0-5 year-old cars in the parc at the end

of 2011 compared with the pre-recession level at the end of 2007 – and 240,000

fewer units in the 6-8 year age group. The problem is, that while the supply of 0-5

year-old cars will remain relatively flat over the next three years, the stock of cars in

the 6-8 year group will drop by a further 900,000 units – adding up to three million

fewer 0-8 year old 'used cars in stock' than pre-recession times.

Taking a conservative used car 'parc turn' of 20%, this amounts to the loss of around

600,000 used cars sales per year in this critical age group, until substantially more

new cars are fed into the used car supply chain over several years.

Company car disposals to fall

While there have been reports of a growing shortage of good quality, first-time used

cars reaching the market, the full impact of the sharp fall and prolonged, low new car

volumes is yet to fully hit the used car market – as most of the new cars from the low

new car volume period are still with their first owners.

Disposals of 3-5 year-old fleet and business cars, which many retailers rely on for a

steady supply of used cars, illustrates this pattern of events.

Company car

disposals (used car

supply) in this

critical age group

held up well until

the end of 2011,

fuelled by record

high new fleet and

business sales

averaging 1.34

million units for five

years leading up to

2007.

From 2012,

company car

disposals in the 3-5 year age group will increasingly reflect much lower fleet and

business new car volumes, which fell steeply by some 350,000 to 980,000 units in

2009 and have recovered little since.

Fleet and business car disposals 3-5 year age group; 2006 – 2015

495,200

473,700

520,400 517,800503,500

495,000

415,300 408,600

432,200

451,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: SMMT/Buckingham

The full impact of the sharp fall and prolonged low new car volumes is yet to fully hit the used car market

UK Market Review

The Used Car Market – a report by BCA 24

This will see company car disposals in this key age sector drop substantially over the

next two to three years, some 100,000 units lower than the peak of 520,000 reached

in 2008 – until such time as new fleet and business car volumes stage a marked

recovery.

Should the economy begin to show signs of recovery and/or car owners can't hold on

to their old car any longer, the growing shortage of younger used cars will become

more apparent as consumer demand rises.

Some initial conclusions

The UK Market Review portrays an industry in the midst of a long-term economic

downturn, with the impact of a lengthy period of low new car volumes flushing

through the used car supply chain. The impending and prolonged shortage of

younger used cars coming to market will take something like a decade to pass

through the system.

The following points might be considered:

Perhaps the strongest single message from this section of the report is the steep

climb in the average age of cars in the UK car parc. It has reached the highest

point for at least a quarter of a century at 7.44 years – up from 6.69 in 2004.

Could the average age of cars in the parc surpass eight years before it turns

around?

The used car market accounts for more than 55% of the value of car sales in the

United Kingdom and is £6.7billion greater than the new car market.

A change in buying patterns away from new cars to used cars as private buyers

seek to retain a ‘younger car’, but avoiding the greater expense of buying a new

one.

An increase in private-to-private sales suggests some sellers are seeking to cut

out the middleman or can no longer afford a younger vehicle.

The implications from the UK Market Review are significant in terms of franchised

dealer operations with less focus on new car sales and greater profit opportunities

from their used car activities. There is also a strong likelihood of reduced service

opportunities as the car parc continues to age, given that motorists tend to switch to

non-franchised outlets for maintenance when their car's warranty finishes.

The average age of cars has reached the highest point for a quarter of a century at 7.44 years

The Used Car Market – a report by BCA 25

The Consumer Perspective

The Consumer Perspective section of the BCA Used Car Market Report looks at the

pattern of car ownership in the UK and the key issues that motorists take into

account when deciding what used car to buy and where to buy from.

BCA commissioned BMRB International to carry out face-to-face interviews with

4,000 car owners in the UK to identify their preferences and experiences in buying

and owning a used car – what persuaded them to buy their latest used car, what

influenced their choice of seller, what type of car they might buy next time they make

a change, where they might buy it, and when.

This year, the consumer research also looked at what type of car motorists might

look for during the current economic uncertainty, and how high the price of fuel

would need to be before they would think about buying a more fuel-efficient car

and/or changing their pattern of driving. Car owners were also asked if they had

taken any concerted steps to reduce their car running costs and how they prefer the

dealer they bought their car from to keep in touch with them.

Fieldwork for the BMRB consumer research took place during late March 2012.

The Consumer Experience section is split into four parts;

What Used Car to Buy? – looks at the issues which influence used car buyers’

decision on what car to consider buying and the crunch factors when deciding which

particular used car to buy.

Where to Buy From? – this part of the report considers what factors influence car

owners when choosing which dealer to buy their used car from, and what matters

most when buying from a franchised or non-franchised used car retailer. It also looks

at the pattern of car ownership in the country, why motorists buy a used car instead

of a new one, the type of used car they decided to buy – and how satisfied they are

with their purchase.

Dealer Relations and Buying Intentions – looks at used car retailers’ ongoing

relationship with their customers, when motorists might next be in the market for

another car, what type of car they plan to buy next and where they might buy from.

Fuel Prices, Economic Uncertainty and Car Running Costs – assesses what type

of car motorists might buy next time in the face of financial pressures and ongoing

economic uncertainty, and how they might combat the rising cost of fuel. It also looks

at what steps car owners have already taken to cut their motoring costs and what

they are prepared to do to cut their personal carbon footprint.

Car owners were asked if they had taken steps to reduce their car running costs

The Consumer Perspective

The Used Car Market – a report by BCA 26

Part One – What Used Car to Buy?

What used car to buy next?

For the first time, 'views of friends and family', cited by 24% of car owners in this

year's survey, edged 'personal experience of make and model' (21%) into second

place when motorists thought about what used car they might buy next.

Influences on type of used car considered

2

4

4

4

6

6

8

8

8

10

12

15

21

24

16

Social media

Car TV shows

Dealer advice

Specialist motor mags

Car TV ads

General car mags

Newspaper adverts

Cars on street

Consumer reports

Dealer websites

Used car physical sites

Test drive

Independent Internet sites

Personal experience

Family & friends %

Source: BMRB

The influence of ‘independent Internet sites' increased from 12% to 16% of used cars

buyers this year, while 'used car sites/showrooms' (12%) and 'dealers' websites'

(10%) also had a part to play helping some used car shoppers decide which used car

to look for.

As in previous surveys, used car buyers are much less likely to be influenced by

'general car magazines', 'car TV adverts', 'dealer advice' or 'car TV shows', whilst

very few car owners felt 'social media' (Facebook or Twitter) could help their used car

buying deliberations.

Women (28%) depend more on the 'views of friends or family' than men (20%), who

rely on a blend of 'personal experience of make and model' (21%) and 'independent

car Internet sites' (16%) to settle on what car they might buy next.

While 'independent dealer websites' are important to a fifth of car buyers in the 25-34

year age group, they are not on 65 years-plus motorists' radar (5%). 'Consumer

reports' are of more interest to wealthier car owners and owners of cars in the

£15,000 plus band, who are also influenced more than others by a blend of 'personal

experience', 'test drive', 'used car showrooms/sites' and 'dealer advice'.

The influence of 'independent Internet sites' increased this year

The Consumer Perspective

The Used Car Market – a report by BCA 27

'Crunch factors'

'Price' (41%), 'low mileage' (31%) and 'make and model', mentioned by 30% of

respondents, are firmly established as 'crunch factors' in deciding which particular

used car to buy – although 'engine size' (18%) and 'body type' (17%) can make the

difference on some occasions.

Critical factors in choosing a used car

41

31 30

1817

1412

108 8 7

3

0

5

10

15

20

25

30

35

40

45

%

Price

Low m

ileag

e

Mak

e/m

odel

Engine

size

Body t

ype

Age

Fuel

optio

n

Insur

ance

Specific

ation

Safety

Colour

Enviro

nmen

tal

Source: BMRB

Men and women have much the same views on the top-three 'crunch factors',

although 'age of vehicle' has more influence with women (18%) than men (11%).

However, the opposite is true for 'body type', cited as a factor by 19% of men but

just 14% of women.

While 'price' outstrips all other considerations for 56% of 17-24 year-olds and 50% of

low-income used car buyers, it only matters to three out of 10 older and wealthier car

owners who are more interested in the 'age of vehicle' and 'specification'.

‘Price’, which remains a top priority for half of motorists who bought a car for less

than £3,000, only makes a difference to a fifth of car buyers with cars in the £10,000

to £15,000 band and a quarter of those with cars priced over that mark. Owners of

cars costing more than £10,000 were more influenced by a mix of 'low mileage',

'make and model of vehicle', 'body type', 'age of vehicle and 'fuel option' that best

met their expectations.

Men and women have much the same views on the top-three 'crunch factors'

The Consumer Perspective

The Used Car Market – a report by BCA 28

Part Two – Where to Buy From?

Which used car retailer to deal with?

Affordability tops motorists' priorities when deciding which used car retailer to buy a

car from. 'I got a good deal on the car' topped the shopping list for a third of survey

respondents, followed by 'the right car at the best possible price', which was in the

frame for three out of 10 of last year's used car buyers. A fifth of used car owners

look to 'trade in' their existing car and prefer to do business with a 'local dealer'.

Factors influencing choice of dealer

1

2

2

3

3

4

7

7

9

10

11

12

13

14

19

19

29

33

Dealer contact

Showroom facilities

Internet/onlline

Read about dealer

Low finance

Quick delivery

Easy negotiation

Aftersales

Recommended

Bought before

Wide choice

Friendly,helpful

Warranty

Reliable, trustworthy

Local

Trade-in

Right car, price

Good deal %

Source: BMRB

Dealer experience is also a prominent aspect of the buying process, in the form of

'the dealer appeared reliable and trustworthy' (14%) and 'staff are friendly, helpful

and professional', mentioned by 12% of used car owners.

There is little difference in men's and women's buying priorities in this year's survey.

Getting 'the right car at the best possible price' far outweighs all other considerations

for young used car buyers, who also rely more heavily on the 'dealer appeared

reliable and trustworthy' (32%).

The chief concern for two out of five wealthier car buyers is the 'dealer appeared

reliable and trustworthy', which is of little interest to low-income motorists (5%) who

are more focused on buying from a 'local and convenient' used car retailer (36%).

While 'the right car at the best possible price' tops the list for people buying cars

costing up to £10,000, other factors are more influential over that price level – 'trade

in', 'local dealer', 'friendly, helpful staff, 'dealer was recommended' and 'lack of sales

pressure' can sometimes play a key role in clinching the deal on higher value cars.

Dealer experience is a prominent aspect of the buying process

The Consumer Perspective

The Used Car Market – a report by BCA 29

Buying from franchised and non-franchised dealers

Used car buyers are quite clear what they want from franchised dealers selling the

same make of car – two out of five expect a 'good deal on the car', 28% want the

'right car at the best possible price' and 25% 'look to trade in their old car'.

A little further down the list, some car owners head to a franchised dealer because of

their 'friendly, helpful and professional staff' (17%), or they have 'bought a car from

them before (16%).

Factors influencing choice of dealer

8

7

4

4

3

30

28

17

19

9

16

7

6

10

7

2

10

2

3

16

15

15

11

11

17

18

39

28

25

7

Got a good deal

Right car right price

Trade-in

Local

Friendly, helpful

Bought before

Reliable/trustworthy

Warranty

Lack of pressure

Range of choice

Aftersales

Quick delivery

Recommendation

Showroom facilities

Low finance

%

Franchised dealer same make

Used car retailer

Source: BMRB

Three out of 10 car owners who chose to buy from a non-franchised used car retailer

did so because 'they got a good deal on the car' and/or the dealer had 'the right car

at the best possible price', cited by 28% of this group this year. Dealing with 'friendly,

helpful and professional staff', or having 'bought a car from them before', is much

less of an concern for non-franchised used car retailers' customers than those who

had bought from a franchised point.

Three-quarters of motorists buy a used car

Twenty-four per cent of this year's consumer survey's respondents had bought a car

over the past two years, three-quarters of them choosing to buy a used car instead of

a new vehicle (see overleaf).

More men (26%) than women (23%) had bought a car in the past 24 months, 72% of

men and 77% of women opting to buy a used car rather than a new one.

Dealing with 'friendly, helpful staff' is less of a concern for non-franchised retailers' customers

The Consumer Perspective

The Used Car Market – a report by BCA 30

Cars bought over past two years – by age group

2426

23

16

2832

27

16

28

7477

80

87

81

7072

6064

0

10

20

30

40

50

60

70

80

90

All ages Men Women 17-24 25-34 35-44 45-54 55-64 65+

Age

%

% bought car in last two years % of these bought used

Source: BMRB

Motorists in the 35-44 year age group were the top buyers of cars on this occasion; a

third of them buying a car during the past two years, compared with just 16% of 17-

24 year-olds and 65 years-plus car owners. Nearly nine out of ten 25-35 year-olds

(87%), and 81% of those in the 35-44 age group, chose to buy a used car, in

contrast to just 60% of older motorists.

While three out of 10 wealthier car owners had bought a car in the previous two

years, just one in 10 low-income families followed suit, 67% of the former opting for a

used car compared to 85% of the latter.

Seven out of 10 families own a car

Similar to last year, seven out of 10 families (72%) own at least one car (see overleaf)

– 5% fewer, though, than two years ago, as the effects of the second recession in

four years, high inflation and rising fuel and maintenance costs has badly eroded car

owners' disposable incomes.

Households of car owners in the 35-54 age group have the most cars in their

families, 83% of them have at least one car, 30% of them owning two cars. The

lowest car ownership is found in 65 years plus and low-income households, where

just 62% of the former and 37% of the latter run a car.

A third of wealthier families own two cars, 9% of them in the three-car family bracket

– mostly those in the 45-54 year age group with a high percentage of used cars

costing more than £10,000.

Motorists in the 35-44 year age group were the top buyers of cars

The Consumer Perspective

The Used Car Market – a report by BCA 31

Four years of economic

downturn and financial

hardship has seen the

number of families

without a car rise five

points to 28% over the

past two years. Two-

car households

dropped 3% to 22%,

and the number of

three-car families fell

from 8% to 5% of

households during the

same period.

Hatchbacks and saloons most popular

Hatchbacks (47%) and

saloons (22%) remain

motorists' most popular

used cars, taking the

same share of the

market as last year.

Apart from MPVs,

which saw their share

rise from 6% to 10% in

2012, demand for other

variants was stable

year on year.

Women (52%) favour

hatchbacks more than

men (43%), who have more appetite for MPVs/People Carriers (12%) than women, at

7%. While a fifth of motorists in the 35-44 year group opt for an MPV, mostly in the

£10,000-£15,000 band, estate cars find favour with 55-64 year-olds, and saloons are

preferred by three out of 10 older motorists.

Estates and MPVs are twice as popular in the £10,000 to £15,000 price band, while

Sports Cars/Coupe and Prestige variants are favoured most by used car buyers

spending £20,000 plus.

Cars in the household

Two22%

Three or more4%

One45%

None28%

Source: BMRB

Type of used car bought

Hatchback47%

Saloon22%

Prestige1%

Micro/City2%

MPV10%

Sports/Coupe4%Off-road

4%

Other3%

Estate7%

Source: BMRB

Four years of economic downturn has seen the number of families without a car rise four points to 28%

The Consumer Perspective

The Used Car Market – a report by BCA 32

Buying used rather than new

Reasons for buying

a used car rather a

new one are firmly

established. A third

of car owners said

'I couldn't afford a

new car', a fifth

believe 'used cars

offer better value

for money', and

14% of motorists

are convinced

'there is lower

depreciation with

used cars'.

While a quarter of

men and a fifth of women said 'used cars offer better value for money', more women

(38%) than men (30%) said 'they couldn't afford a new car'.

Two-fifths of car owners between 17 and 34 years of age and low-income motorists

bought a used car because 'they were unable to afford a new one', in contrast to just

one fifth of older and wealthier motorists who found themselves in a similar position.

55-64 year-olds believe more strongly than other groups that 'used cars provide

better value for money' (28%) and 'there is lower depreciation with used cars' (23%).

While ‘I couldn’t afford a new car’ is the major influence in buying a used car costing

up to £5,000, it is of little concern for car owners who paid £10,000 to £15,000 for

their last used car (8%) – and those who bought more expensive vehicles (12%).

Sales of used diesels stall

Diesel-engined cars’ used car market share dipped to 33% this year from 34% in

2011 and 36% in 2010 – as fewer fleet vehicles from 2009's low new car volumes,

reached the marketplace and more private used car buyers looked towards smaller,

petrol-driven models.

Diesel new car volumes climbed four percentage points to 50.6% of the new car

market in 2011; rising 4.8% to 981,594 units, driven by higher sales (4.7%) to fleet

operators and a 14% drop in private sector new car volumes.

Fleet operators dominate the diesel new car market. Diesels accounted for close to

two-thirds (63.2%) of new cars sold to the 25-plus fleet sector in 2011 (644,230

units), compared with just 36.6% of private new car volumes – 337,364 units.

Buying new or used?

4

6

11

14

21

34

More choice

Needed quickly

Always buy used

Depreciation

Better value

Couldn't afford new %

Source: BMRB

Diesel-engined cars' used car market share dipped to 33% this year

The Consumer Perspective

The Used Car Market – a report by BCA 33

Motorists in the 35-44 year age group are the biggest diesel buyers, 41% of them

choosing a diesel-engined used car last time, as did 35% of wealthier used car

buyers. Diesels remain a less attractive proposition for 65 year-plus (24%) and low-

income (21%) used car owners many of whom prefer a smaller, petrol vehicle.

The high fleet and

premium sectors'

diesel new car

content can be

seen in the

£10,000 to

£15,000 used car

band – where two

thirds of vehicles

bought run on

diesel, as do seven

out of 10 used

cars priced

between £15,000

and £20,000.

Although 'better fuel consumption' still tops the reasons for buying a diesel used car,

the number of car owners citing this dropped to 57% compared with 68% in last

year's consumer survey – as petrol-engined cars become more frugal on the fuel

front and the significant diesel/petrol price gap remains. A quarter of used car buyers

believe a diesel is a 'more reliable engine', while nearly a fifth are confident this type

of used car 'maintains its value better'.

Used car satisfaction rises once more

Used car owners'

satisfaction with their

used car rose two

points to 95% this year

– 67% of them saying

they were 'very

satisfied' and 28%

'quite satisfied'.

The number of 17-24

year-old used car

owners, 'very satisfied'

with their car, jumped

10% to a high of 68%

this year, with a further

21% 'quite satisfied'.

Reasons for buying diesel

57

24

18

8 86

0

10

20

30

40

50

60%

Fuelconsumption

More reliableengine

Maintainsvalue

Engine lastslonger

High mileage Environment

Source: BMRB

Used car satisfaction

Quite dissatisfied2%

Neither2%

Quite satisfied28%

Very dissatisfied 1%

Very satisfied67%

Source: BMRB

Used car owners' satisfaction with their used car rose two points to 95%

The Consumer Perspective

The Used Car Market – a report by BCA 34

Used car satisfaction within all other age groups is well over the 90% mark, topped

by 55-64 year-olds and 65 plus motorists at 98% and 97% respectively – with

wealthiest used car buyers the most satisfied contingent at 99%. Although 92% of

low-income used car owner declared they were 'satisfied with their car, just 55%

claimed to be 'very satisfied' compared with the average of 67% – suggesting many

in this group run older vehicles.

The number of car owners ‘satisfied’ with their used car also rises in line with

purchase price – reaching 96% for cars costing between £5,000 and £10,000, 97%

between the £10,000 and £15,000 mark – and 100% for cars priced over £20,000.

The Consumer Perspective

The Used Car Market – a report by BCA 35

Part Three – Dealer Relations and Buying Intentions

Used car customer follow up

The BCA consumer survey asks used car owners if the dealer they bought their car

from, keeps in touch to see if they are satisfied with their vehicle, are interested in

servicing their car, or might be thinking of buying another car. This year's results

show that just 52% car owners had heard from their selling dealer since they bought

their car, compared to 56% in last year's survey.

Overall, the

percentage of

used car

customers

contacted by

dealers to find out

if they 'were

satisfied with their

car' or were

interested in

'having it serviced'

both fell to their

lowest point in the

survey's history.

'Satisfaction' calls

dropped 3% to

27% while

'servicing' was 4% lower at 31%.

Franchised dealers selling the same make of used car have a much better record on

customer contact than their non-franchised counterparts; 73% kept in touch with

their used car buyers compared with 40% of independent dealers, 57% versus 18%

on servicing' and 13% versus just 4% to see if the owner might be 'interested in

buying another car'.

17-24 year-old car owners and low-income motorists are least likely to hear from the

retailer they bought their car from – three out of five saying they had heard nothing

since they took delivery of their vehicle. Used car buyers in the 55 years plus group

and wealthier motorists are most likely to be approached about 'servicing their car' or

if they 'might be interested in buying another vehicle' – the latter aspect unheard of

by low-income car owners.

Eighty-five per cent of owners of cars costing between £10,000 and £15,000 had

heard from their supplying dealer, three out of five about 'servicing' and a fifth on the

topic of 'changing their car'.

Dealer contact with used car customers

31

1

73

57

13

4

1818

40

4

0

10

20

30

40

50

60

70

80

Contact Servicing car Satisfied with car Change car Sell tofriend/family

%

Franchised dealer same make Non-franchised dealer

Source: BMRB

The percentage of used car customers contacted by dealers to find out if they were satisfied fell to its lowest point

The Consumer Perspective

The Used Car Market – a report by BCA 36

Buying a car in the next year?

Car owners are

clearly not immune

from the impact of

the long-running

spell of financial

pressures,

recession or

gloomy economic

outlook. This

year's consumer

research shows a

significant drop in

the number of car

owners who think

they will 'certainly'

or 'quite likely' buy a car in the next 12 months – down 3% to 11% in 2012 from 14%

last year. The number of motorists who believe there is a '50:50 chance' they will buy

a car in the next year edged up one point to 9%.

Men are more likely to buy a car in the next 12 months than women, 13% of the

former feel they will 'certainly' or 'quite likely' do so, compared with just 10% of

women. Sixteen per cent of 35-44 year-olds feel they might buy a used car in the

next year in contrast to just 3% of 65 years-plus motorists – while a fifth of car

owners who bought a used car in the £10,000 to £20,000 band, and 35% of those

with cars in the £20,000 group, feel they might follow suit.

What type of car to buy next?

Three-quarters of

car owners intend

to replace their car

with a used one

when they make a

change. However,

there has been a

swing of 4%

towards diesel this

time – 30% of

prospective used

car buyers saying

they plan to go in

this direction next

time – a long way

short though of

diesels' current 50% plus share of the new car market.

Likelihood of buying a car in the next year

3

8 9

26

20

30

3

0

5

10

15

20

25

30

%

Certainlywill

Quitelikely

50:50chance

Unlikely Certainlynot

Won'tbuy again

Don'tknow

Source: BMRB

Next car bought will be

12

1

1

3

3

4

7

27

40

Don't Know

Used car alternative

Used car hybrid

Nearly new petrol

Nearly new diesel

New car diesel

New car petrol

Used car diesel

Used car petrol %

Source: BMRB

Three-quarters of car owners intend to replace their car with a used one

The Consumer Perspective

The Used Car Market – a report by BCA 37

While four out of five car owners in the 25-34 age group plan to buy a used car next

time they replace their car, a third looking for a diesel, only 62% of older motorists

are planning a similar move, just 17% heading in the diesel direction. The biggest

potential buyers of a used car are those who spent £5,000- £10,000 last time (92%),

and owners of used cars that cost between £15,000 and £20,000 (88%).

Where to buy the next car?

While some car owners might consider more than one option, the number of

respondents saying they will deal with a franchised dealer next time rose by 5% to

50% in this year's survey, half of them planning to trade in their old car. Other

potential used car sources remain unchanged; 30% of motorists have in mind buying

privately or from a friend, while a further 13% are considering doing business with a

non-franchised used car retailer.

Nearly three out of

five car owners

over the age of 35

say a franchised

dealer will be their

first port of call

when they get

round to buying a

used car to replace

their current

vehicle – which

rises to seven out

of 10 in the case of

better-off used car

buyers.

Two out of five 17-

24 year-olds and

low-income car buyers say they will buy privately or from a member of their family

next time, as will half of buyers of cars in the £1,000 to £3,000 band. On the other

hand, three out of five owners of cars costing between £10,000 and £15,000 are

intent on doing business with a franchised dealer.

Where next car will be bought

13

7

6

5

4

3

12

22

50

Don't know

Other

Auction

Car supermarket

Family friend

Internet trader

Used car dealer

Private

Franchised dealer %

Source: BMRB

The number of respondents saying they will deal with a franchised dealer next time rose by 5%

The Consumer Perspective

The Used Car Market – a report by BCA 38

Part Four – Economic Recovery, Running Costs and

Keeping in Touch with Customers,

What car to buy during an economic recovery?

The economy is in the midst of a double-dip recession, prices of essential goods and

fuel have spiralled in recent years, and unemployment is uncomfortably high. The

Governor of the Bank of England, Mervyn King, predicts it could take five more years

for a full economic recovery – three years longer than he originally expected.

Faced with this gloomy outlook, what type of car might car owners consider buying to

help them offset financial pressures? The answer? The 'status quo' is under severe

threat.

Buying a car during slow economic recovery

2

2

3

5

8

9

9

12

13

14

14

20

27

Bigger car

New instead of used

Low interest loan

Lower depreciation

Best part-exchange price

Same type of car

Used instead of new

Lower maintenance

Lower CO2

Best purchase price

Smaller car

Lower road tax

Better fuel consumption %

Source: BMRB International

Just 9% of car owners say they will 'buy the same car again', down from 14% last

year and 20% who expressed this view in 2010. Simple arithmetic, therefore,

suggests that nine out of 10 motorists intend to replace their car with a different type

of vehicle next time.

Top of the shopping list are 'a car with better fuel consumption', 'lower road tax', 'a

smaller car' 'best purchase price' and 'lower CO2' – all things that used car buyers

have a great deal of control over. Significant progress on all or most of these

measures could produce dramatic savings.

.

Just 9% of car owners say they will 'buy the same car again'

The Consumer Perspective

The Used Car Market – a report by BCA 39

There remains little difference between men and women, and across the age and

social groups, on what steps motorists might take to protect their motoring needs

and withstand the 'slings and arrows' of the country's economy

Men (29%) appear more intent than women (24%) on changing to a 'car with better

fuel consumption', a step too far, though, for the vast majority of younger car owners,

just 16% of whom said this is tolerable. On the price front, people with cars in the

£10,000 to £15,000 group, are more resolved than others to cut costs when they

replace their car. A third of them are considering a move to 'a car with better fuel

consumption' and/or one with 'a lower road tax', while a quarter are thinking about

'buying a used car rather a new one' and/or negotiating 'the best possible price'.

Reducing personal motoring carbon footprint

The number of cars owners prepared to take steps to cut their personal carbon

footprint rose to 94% this time. Support for such measures is wide spread with the

exception of 65 years-plus (76%) and low-income respondents (72%).

Steps to reduce personal motoring carbon footprint

16

6

6

9

9

10

13

14

15

15

15

15

16

16

21

29

No action

Drive off-peak times

Work from home

Cycle more often

Car share

Switch off air conditioning

Use public transport more

Accelerate less quickly

Avoid heavy braking

Avoid short trips

Buy smaller car

Car with lower emissions

Reduce annual mileage

Drive more slowly

Cut journeys

Walk more often %

Source: BMRB

'Walking more often' and 'cutting the number of journeys', favoured by 29% and 21%

of car owners respectively, top the list of measures motorists have in mind to cut

their personal CO2 – with other steps such as 'driving more slowly', 'reducing annual

mileage', 'buying a car with lower emissions' and 'buying a smaller car' also in the

frame.

Men appear more intent than women on changing to a 'car with better fuel consumption'

The Consumer Perspective

The Used Car Market – a report by BCA 40

Women (33%) are more likely to 'walk more often' than men at 24%. However, when