us restaurants 21 themes for 2021

TRANSCRIPT

US Restaurants21 Themes for 2021

Research Analysts

Lauren Silberman, CFA, CPA

+1 212 325 [email protected]

Douglas Eisman

+1 212 325 [email protected]

19 January 2021

Equity Research US

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

2

Table of ContentsExecutive Summary

21 Themes for 20211. Restaurant Recovery Outlook2. Evolution of the Digital Ecosystem3. Loyalty/Rewards4. Restaurants of the Future5. Delivery6. Off-Premise in Casual Dining7. Ghost Kitchens8. Virtual Brands9. Drive-Thru & Drive-Up Curbside10. Franchisee Economics11. Breakfast Battle12. Chicken Wars13. Value & Innovation On the Menu14. Sustainability15. Plant-Based16. Labor17. Margin Outlook18. Portfolio Optimization19. Unit Growth20. M&A21. Brand Engagement

Company Summaries

3

Executive Summary

4

Coverage & Ratings11 Outperform, 1 Underperform, 5 Neutral

Source: Company data, FactSet, Credit Suisse estimates

Ticker Company CS RatingMarket Cap

($MM)

Current Price

1/15/21

CS Target

Price

Upside/

Downside

NTM

EV/EBITDANTM P/E CS Thesis

CMG Chipotle Outperform $39,218 $1,406 $1,700 20.9% 38.4x 64.8xHigh conviction in 10%+ top-line growth generating margin leverage with attractive flow-through. Strong SSS should support premium multiple, with opportunity for upside on better-

than-expected SSS, margin & unit growth.

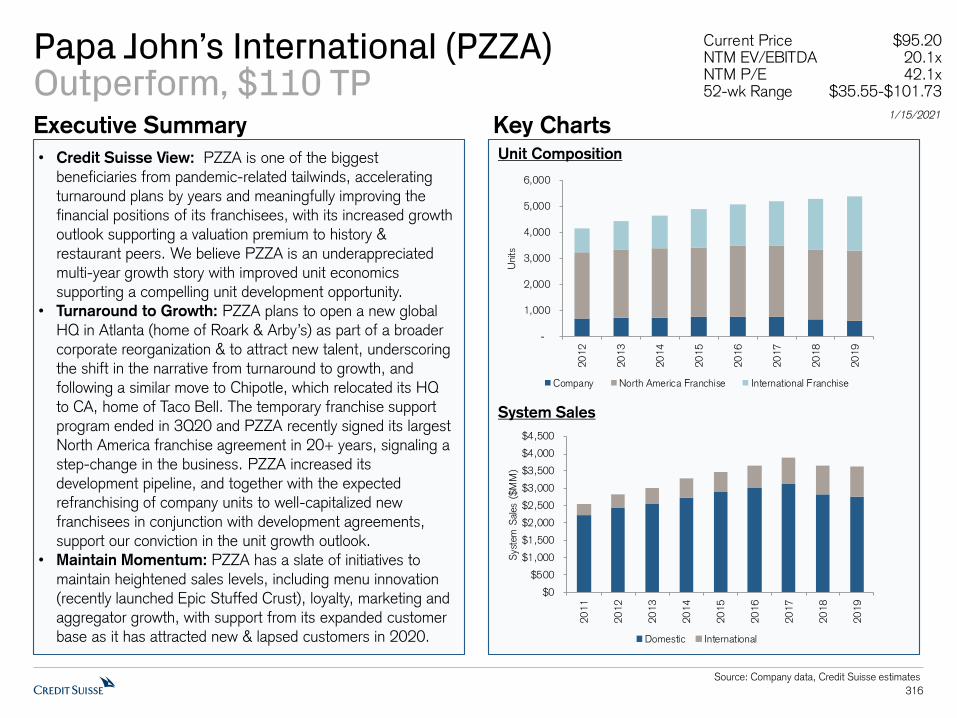

PZZA Papa John's Outperform $3,102 $95 $110 16.5% 20.1x 42.1x

PZZA is shifting its narrative from turnaround to growth, noting pandemic-related tailwinds have accelerated the turnaround plan by a period of years and meaningfully improved the

financial positions of PZZA franchisees. We v iew PZZA as an underappreciated growth multi-year growth story with improved unit economics supporting a compelling development

opportunity. The increased growth outlook supports a valuation premium to history & restaurant peers.

DPZ Domino's Pizza Outperform $15,189 $375 $445 19.4% 21.8x 28.9x

DPZ is one of the best growth stories in restaurants, with high conviction in at least HSD top-line growth supporting global market share gains and among the best returns in the industry.

Third-party delivery concerns appear overblown, noting delivery is a core competency for DPZ, and we're not convinced 3Ps will be able to approach DPZ's execution, value or economics

anytime soon. US SSS outperformance & better-than-expected unit growth support upside to our base case.

DRI Darden Restaurants Outperform $16,595 $121 $141 17.5% 13.4x 23.2xBest-in-class casual dining operator, with industry-leading retention, well-capitalized balance sheet positioning it to invest & leveraging of scale to generate efficiencies support above-

average sales & margin performance. Expect outsized earnings growth in FY22 & return to HSD/LDD earnings algorithm in FY23.

TXRH Texas Roadhouse Outperform $5,682 $81 $90 11.6% 15.4x 30.6xStrong operational execution, compelling value and contribution from off-premise supports recovery trajectory, with favorable steak category dynamics & strong underlying business

supporting unit growth outlook. Market share gains support return to double-digit earnings algorithm in FY22 & premium valuation.

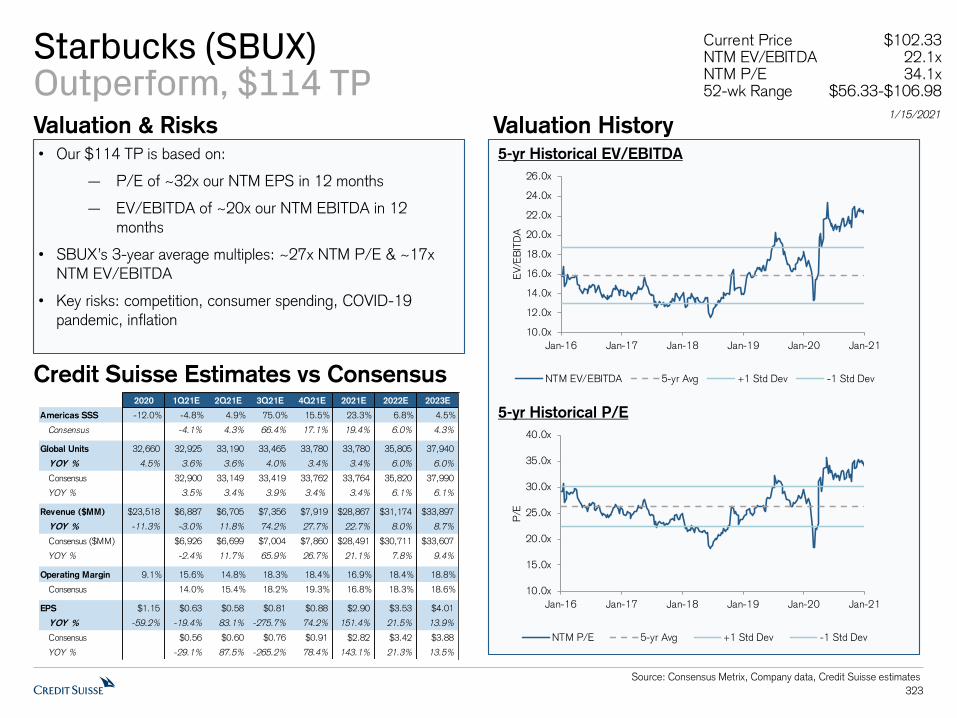

SBUX Starbucks Outperform $120,680 $102 $114 13.2% 22.1x 34.1x

SBUX is one of the highest quality growth companies in restaurants, with 8-10% revenue growth, margin expansion and benefit from repurchases supporting our ~16% EPS growth 3-

yr CAGR. US SSS leverage and strategic optionality (e.g., international licensing) support upside to our base case. A more focused growth strategy & enhanced capital structure support

premium valuation to history.

MCD McDonald's Outperform $157,665 $210 $230 12.0% 18.3x 25.1xWe're bullish on MCD's outlook, with traction against sales initiatives supporting upside to SSS and EPS near & long-term. Healthy global SSS, defensive characteristics, ongoing

transition to ~95% franchise-mix & increased digital focus should prov ide support to valuation.

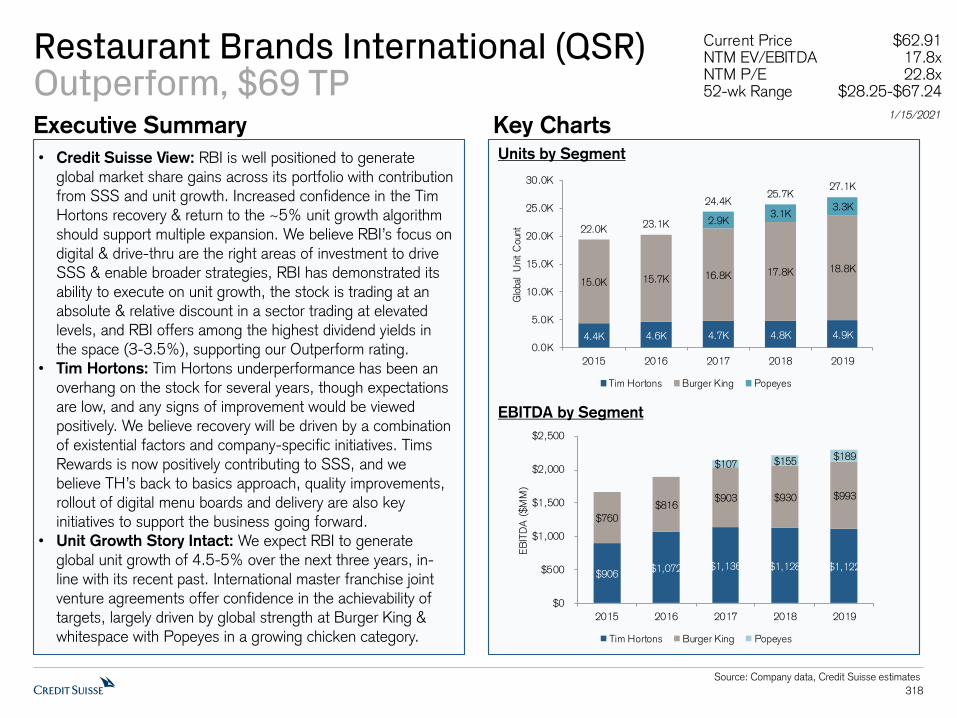

QSRRestaurant Brands

InternationalOutperform $29,446 $63 $69 13.0% 17.8x 22.8x

We believe RBI’s focus on digital & drive-thru are the right areas of investment to drive SSS & enable broader strategies, RBI has demonstrated its ability to execute on unit growth, the

stock is trading at an absolute & relative discount in a sector trading at elevated levels, and RBI offers among the highest div idend yields in the space (3-3.5%), supporting our Outperform

rating

WEN Wendy's Neutral $4,661 $22 $25 16.9% 19.3x 30.0xWhile we like the WEN story and have been impressed with performance, we are cautious on incremental investments required for breakfast and international expansion, as well as the

impact of heightened competition in 2021. We're cautious on a meaningful acceleration in unit growth given recent challenges & lack of international infrastructure.

CAKE The Cheesecake Factory Neutral $1,803 $41 $44 6.7% 10.5x 27.1x

CAKE’s mall-based exposure remains an overhang on the stock and investor sentiment, especially amidst recent challenges accelerating changes in customer behavior and portfolio

optimization across retailers. We're cautious on the unit growth outlook given scarce site selection for Cheesecake Factory restaurants & execution risk for growth of recently acquired

concepts. At current valuation, we rate shares Neutral.

BLMN Bloomin' Brands Neutral $1,836 $21 $21 1.7% 8.1x 19.3xWe like BLMN's focus on off-premise & digital, supporting more resilient sales trends, though slower recovery of its upscale brands, international exposure and high leverage is likely to

weigh on valuation & sentiment.

YUM Yum! Brands Neutral $32,481 $107 $103 -1.6% 19.5x 26.5xSolid asset-light business with a strong unit growth outlook and diversified portfolio across brands and geographies. But greater v isibility into the return to the long-term 4% unit growth

algorithm is likely necessary to improve sentiment.

SHAK Shake Shack Neutral $3,890 $111 $102 -8.3% 57.6x

While we have confidence in the LT unit growth potential, SHAK faces outsized near-term risk from the impact of COVID-19 with its exposure to high-traffic, tourist areas, which will

weigh on margins. SHAK is diversifying its asset base with a range of new formats and additions to the existing system, positioning the company to increase its addressable market & long-

term unit potential. But at current valuation, we remain Neutral

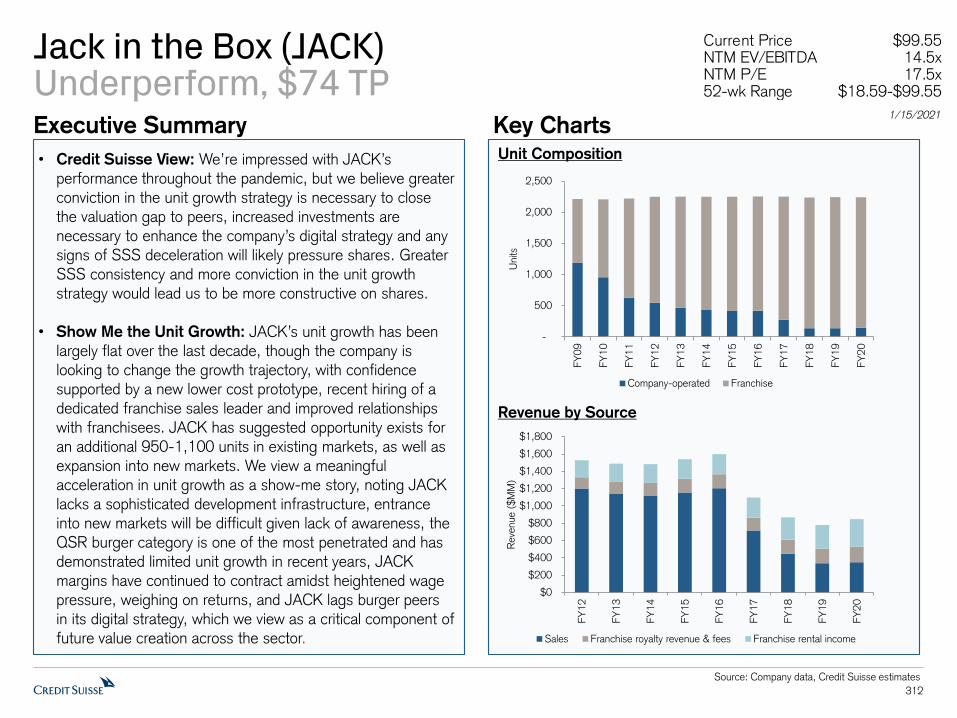

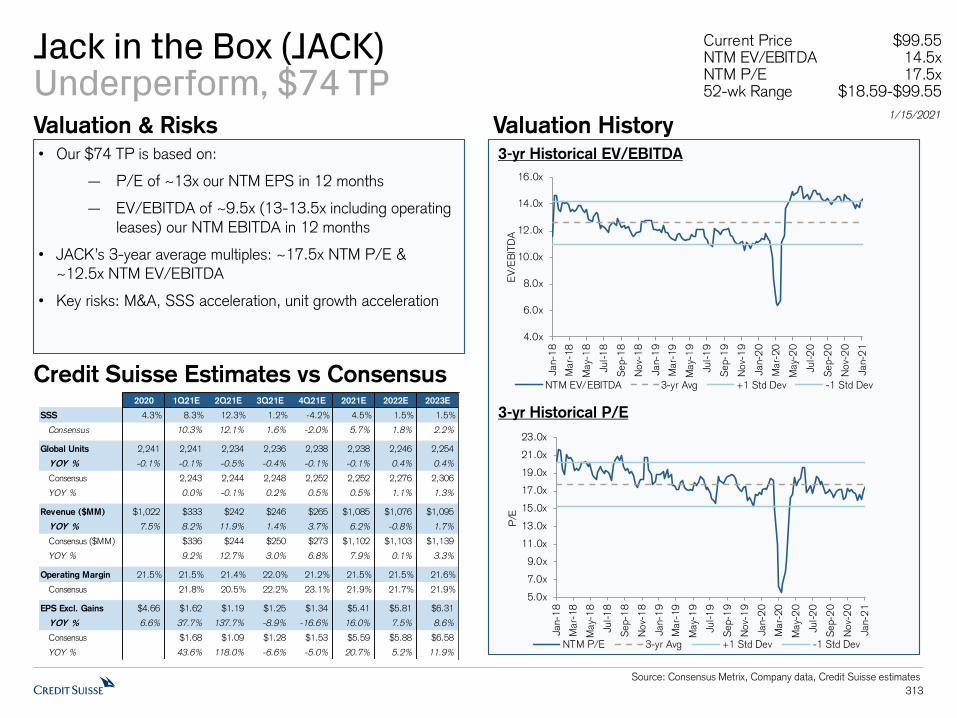

JACK Jack in the Box Underperform $2,224 $100 $74 -24.1% 14.5x 17.5xWhile we've been impressed by JACK's performance over the last several quarters, greater conviction in the consistency of SSS and the unit growth strategy is necessary to close the

value gap to peers, increased investments are likely necessary to enhance the company's digital strategy and any signs of SSS deceleration will likely pressure shares.

US Restaurants Coverage

Ticker Company CS RatingMarket Cap

($MM)Current Price

CS Target

Price

Upside/

Downside

NTM

EV/EBITDANTM P/E CS Thesis

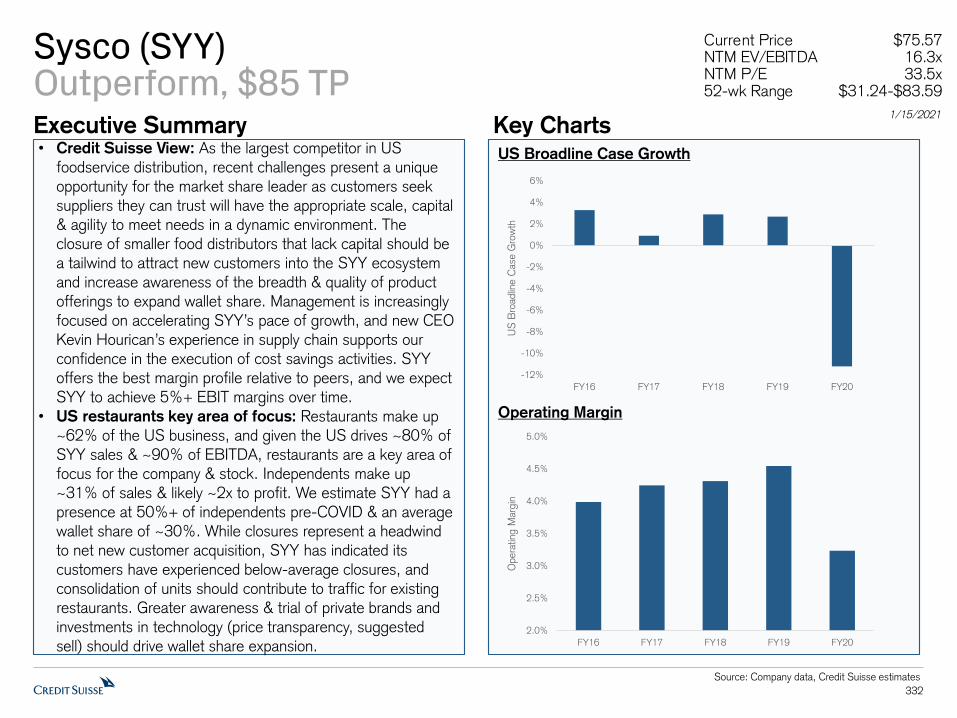

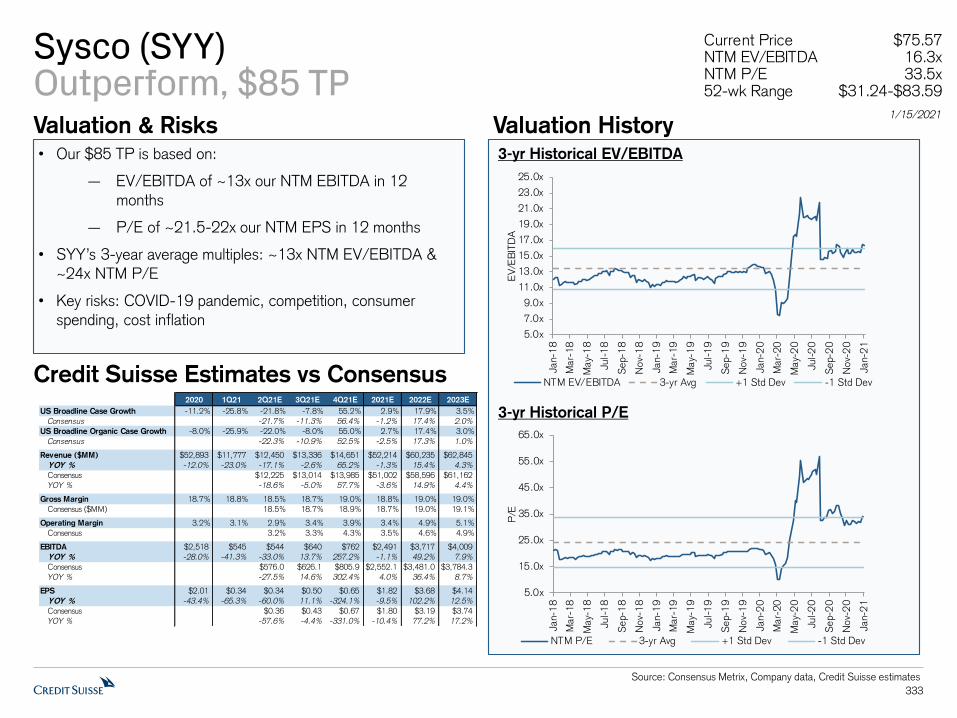

SYY Sysco Outperform $39,918 $76 $85 14.8% 16.3x 33.5xRecent challenges present a unique opportunity for the market share leader as customers seek suppliers they can trust will have the appropriate scale, capital and agility to meet needs in a

dynamic environment. SYY offers the best margin profile relative to peers and we expect SYY to continue to leverage its scale to achieve 5%+ EBIT margins over time.

PFGC Performance Food Group Outperform $6,711 $51 $56 9.4% 15.8x 35.7xPFGC is a compelling growth story well positioned to capture market share in a fragmented industry, with the company's lower independent restaurant mix and regional presence

supporting our confidence in the significant runway for growth on both the top & bottom lines, with sizable market share and margin opportunities supporting mid-teens EPS growth.

USFD US Foods Outperform $7,975 $36 $40 12.2% 13.4x 29.6xSales improvements among existing customers and the acquisition of new customers should support a full sales recapture over time, while an ongoing focus to increase private label mix &

effectively manage costs should contribute to operating margin expansion, supporting mid-teens EPS growth and helping to close the valuation gap to SYY.

Food Distribution

5

Restaurants Coverage Summary

Source: Company data, FactSet, Credit Suisse estimates

Current Mkt Ent. EV/EBITDA P/E Net Short

CS CS Price Cap Value 3-yr 3-yr Div. Debt/ Int. as %

Ticker Company Rating PT 1/15/21 ($BN) ($BN) Avg Avg Yield EBITDA of Float

Quick Service Restaurants

DPZ Domino's Pizza O $445 $375 $15.2 $18.5 21.8x 20.7x 28.9x 28.3x 0.8% 4.3x 3%

JACK Jack in the Box U $74 $100 $2.2 $3.5 14.5x 12.6x 17.5x 17.8x 0.4% 4.0x 10%

LOCO El Pollo Loco - - $20 $0.7 $0.8 15.9x 11.3x 24.3x 18.2x 0.0% 1.3x 12%

MCD McDonald's O $230 $210 $157.7 $190.9 18.3x 16.9x 25.1x 23.7x 2.4% 3.0x 1%

PZZA Papa John's International O $110 $95 $3.1 $3.7 20.1x 16.8x 42.1x 34.6x 1.0% 2.8x 13%

QSR Restaurant Brands International O $69 $63 $29.5 $40.4 17.8x 17.0x 22.8x 21.8x 3.3% 4.8x 2%

SBUX Starbucks Corporation O $114 $102 $120.7 $132.5 22.1x 16.9x 34.1x 26.8x 1.8% 1.8x 1%

WEN The Wendy's N $25 $22 $4.7 $7.0 19.3x 16.8x 30.0x 29.4x 1.4% 4.6x 4%

YUM Yum! Brands N $103 $107 $32.5 $42.6 19.5x 18.6x 26.5x 24.9x 1.7% 4.6x 2%

Average 18.8x 16.4x 27.9x 25.0x 3.5x

Fast Casual Restaurants

CMG Chipotle Mexican Grill O $1,700 $1,406 $39.2 $39.2 38.4x 27.0x 64.8x 50.4x 0.0% -0.8x 3%

NDLS Noodles & Company - - $9 $0.4 $0.4 15.7x 14.2x 33.5x 68.7x 0.0% 1.0x 5%

PBPB Potbelly Corporation - - $5 $0.1 $0.11 30.8x 18.8x 0.0% -1.1x 5%

SHAK Shake Shack N $102 $111 $3.9 $4.0 57.6x 29.7x 0.0% -2.4x 15%

WING Wingstop - - $145 $4.3 $4.8 53.0x 43.2x 102.1x 86.4x 0.4% 4.9x 8%

Average 41.2x 29.0x 66.8x 56.1x 0.3x

Casual Dining Restaurants

BJRI BJ's Restaurants - - $47 $1.0 $1.1 17.3x 11.0x 0.0% 0.5x 9%

BLMN Bloomin' Brands N $21 $21 $1.8 $2.9 8.1x 7.4x 19.3x 11.3x 3.8% 2.8x 16%

CAKE Cheesecake Factory N $44 $41 $1.8 $2.3 10.5x 9.3x 27.1x 0.5x 0.0% 2.2x 27%

CBRL Cracker Barrel Old Country Store - - $141 $3.3 $3.9 13.9x 11.0x 22.2x 17.9x 0.0% 1.6x 6%

CHUY Chuy's Holdings - - $33 $0.6 $0.6 12.8x 9.7x 30.9x 17.8x 0.0% -1.4x 7%

DIN Dine Brands Global - - $70 $1.1 $2.5 12.1x 11.4x 13.4x 12.1x 0.0% 5.7x 6%

DRI Darden Restaurants O $141 $121 $16.6 $16.1 13.4x 11.5x 23.2x 19.3x 1.1% 0.1x 3%

EAT Brinker International - - $59 $2.8 $3.8 9.7x 8.0x 17.3x 12.0x 0.0% 2.8x 11%

PLAY Dave & Buster's Entertainment - - $34 $1.6 $2.2 33.7x 13.7x 7.7x 0.0% 5.9x 24%

RRGB Red Robin Gourmet Burgers - - $25 $0.4 $0.6 17.0x 10.8x 17.2x 0.0% 2.8x 14%

RUTH Ruth's Hospitality Group - - $19 $0.6 $0.7 20.0x 12.7x 36.2x 22.0x 0.0% 0.9x 9%

TXRH Texas Roadhouse O $90 $81 $5.7 $5.5 15.4x 13.3x 30.6x 28.2x 0.0% -0.4x 6%

Average 15.3x 10.8x 24.5x 15.1x 1.9x

Food Distribution

SYY Sysco O $85 $76 $39.9 $47.0 16.3x 13.3x 33.5x 24.1x 2.3% 2.8x 1%

USFD US Foods O $40 $36 $8.0 $12.9 13.4x 10.2x 29.6x 17.4x 0.0% 4.4x 2%

PFGC Performance Food Group O $56 $51 $6.7 $9.0 15.8x 11.4x 35.7x 22.6x 0.0% 3.2x 2%

Average 15.2x 11.6x 32.9x 21.3x 3.4x

NTM NTM

6

Appetite for restaurantsPositive on near-term & long-term fundamentals

Near-term

Restaurant industry should benefit from reopening and increased consumer mobility, noting industry

participants have suggested the potential for heightened sales given pent-up demand for dining

Reduced competition supports unprecedented opportunity for market share gains among existing

restaurants

Improved margin outlook, as commentary from both publics & privates suggest improved margin

profiles in a post-COVID era

Long-term

Structural factors have supported food away from home stomach share gains over the last several

decades, such as an increase in women in the workforce, a shift in the generational timeline (people

are getting married, having children & buying homes later in life) and increased demand for

experiences over goods

Acceleration of digital strategies to drive value creation

– Opportunity for further market share gains as restaurants are better equipped to capture

customer data and incentivize behavior, including driving increased frequency and spend

– Opportunity to increase addressable markets with new formats

– Opportunity to improve margins through efficiency gains & productivity enhancements

7

Looking back on 2020Unprecedented challenges & actions

The restaurant sector faced unprecedented challenges in 2020, as restaurants were forced to

shutter on-premise dining, reconfigure operations to shift off-premise and make significant

investments to meet enhanced standards

– Restaurants was among the hardest hit sectors as an industry built around people, connections

and in-person experiences

Select acts of kindness and leadership:

Texas Roadhouse founder & CEO gave up his compensation in 2020 & contributed $5MM to

support team members; a total of 13 executives voluntarily gave up portions of their compensation

Yum! Brands CEO David Gibbs voluntarily elected to forgo his salary for the balance of 2020 to

assist with funding one-time $1,000 bonuses to team members in company-operated stores and to

the Yum! Brands Foundation Global Employee Medical Relief Fund

McDonald’s CEO Chris Kempczinski offered a 50% reduction in his base salary, and other

executives took a 25% reduction in their base salaries (4/15-9/30)

Darden CEO Gene Lee gave up his salary (3/23-5/31), and other executives also temporarily

reduced their salaries by 50% (4/13-5/31)

The Cheesecake Factory CEO David Overton, along with other executives, took a 20% reduction in

salaries

8

Looking back on 2020Unprecedented challenges & actions

Select enhanced pay & benefits: Starbucks paid employees an additional $3 per hour of service pay (end of March through May)

McDonald’s gave employees at corporate stores bonuses (May)

Yum! Brands gave its restaurant general managers at company-owned restaurants $1,000 bonuses

(end of March)

Shake Shack instituted a 10% premium pay policy (end of April through mid-August) and paid

hourly employees a holiday bonus of $250-400 (December)

Chipotle boosted hourly pay by 10% (mid-March through early June) and honored bonuses

Wendy’s offered free meals to team members, emergency paid sick leave, restaurant recognition

pay (10% increase in hourly pay in April) and protected general manager bonuses

Domino’s paid bonuses to eligible company-owned store and supply chain hourly team members

Papa John’s paid bonuses to eligible company-owned store and supply chain hourly team members

We also note franchisees across brands implemented their own assistance programs, including

premium pay and bonuses to employees

9

Looking back on 2020Unprecedented challenges & actions

Select franchisee assistance programs:

McDonald’s offered franchisees the option to defer rent & service fees for March & April in most

markets globally, and provided specific organizations with additional assistance where necessary

Yum! Brands offered assistance to franchisees who needed access to more capital and were in

good standing, including grace periods for certain near-term payments; the company also deferred

2020 capital obligations for remodels & new unit development for US franchisees

Restaurant Brands International advanced cash payments and rebates to franchisees in markets

globally, including ~$70MM in North America; the company temporarily converted its rent structure

where it has property control to 100% variable rent (from fixed plus variable rent) and deferred rent

payments for up to 45 days; RBI also temporarily paused capital expenditure requirements

Wendy’s extended payment terms for royalties & marketing funds by 45 days for three months,

deferred base rent payments on properties owned by Wendy’s & leased to franchisees by 50% for

three months and extended its Image Activation & restaurant development requirements by one

year; Wendy’s also suspended franchisee marketing fund contributions toward breakfast in 2020

Jack in the Box reduced April marketing fees to 4% of sales (from 5%) & postponed collection,

deferred the collection of ~40% of April franchisee rental payments and delayed FY20 franchise

development agreements by at least six months & other required capital investments

10

Looking back on 2020Performance across our coverage varied

QSR/fast casual stocks outperformed the market, up 24% on average in 2020, with the global

QSR franchisors underperforming the group, while high-growth and company-owned business

models skewed to the US outperformed

– CMG was the best performing restaurant stock (+66%), followed by SHAK (+42%), DNKN

(+41%; note: DNKN was acquired by Inspire Brands), PZZA (+34.5%) and DPZ (+30.5%)

Casual dining companies underperformed in 2020, though TXRH outperformed the market and

peers (+39%)

The food distributors meaningfully underperformed, with all three stocks down for the year

Source: FactSet, Credit Suisse

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

QS

R

WE

N

YU

M

MC

D

JA

CK

SB

UX

DP

Z

PZ

ZA

DN

KN

SH

AK

CM

G

TX

RH

DR

I

CA

KE

BLM

N

PF

GC

SY

Y

US

FD

S&

P 5

00

QSR/Fast Casual Casual Dining Food Distribution

% R

etu

rn

11

Looking forward to 2021Tale of two halves, with uncertainty still on the menu

The first half of 2021 will in part look similar to what we experienced in 2020, albeit with a greater

degree of hope as the vaccine rolls out more broadly across the general population

– We expect restaurants to remain in a planning and implementation phase, strategizing on how to

most effectively capitalize on a post-COVID environment, from heightened customer demand for

social gatherings to greater real estate availability

– Near-term trajectory of reopening remains a focus after a majority of US states reversed

reopening plans amidst a resurgence of COVID-19 cases in the late fall/early winter

We believe the general consensus is that a vaccine will be available to a majority of Americans by

mid-2021 (Credit Suisse biotech team forecasts herd immunity in the US by 4Q21), suggesting a

return to a more normalized life beginning in the second half of 2021

– But herein lies a host of other uncertainties, including the pace of recovery, level of demand for

eating out, permanency of recent changes in customer behavior and where it settles in a post-

COVID environment, state of the economy, employment & business closures, as well as potential

changes with the incoming Biden administration

The impact of the economy on the industry has received less focus than expected, in part due to

the uncertainty of what the environment looks like in a post-COVID world, as well as the offsetting

dynamics from reduced restaurant supply amidst heightened closures, expectation for outsized

demand for restaurants & experiences and benefit from additional stimulus, which seems likely now

that the Democrats control all three branches of government

12

Looking forward to 2021Finding certainty in an uncertain environment

As industry participants and investors grapple with what the restaurant industry looks like in a post-

COVID world, we expect the industry to look largely similar to pre-COVID

– We do not expect any drastic, lasting changes to customer behavior or food stomach share shift

– We do expect an increased focus on digital ecosystems, personalization and enhancing

convenience – but this is more of an acceleration of trends, rather than any new trends

1) We believe relationships are best developed and enhanced in-person – technology is not yet at a

point where virtual interactions can substitute in-person experiences

2) We believe brand matters – customers are not necessarily loyal to a product, but rather loyal to a

brand; products and menu items can be commoditized over time, but experiences cannot be

replicated

– Brands like Starbucks, Chick-fil-A and Taco Bell have tribe-like followings – not necessarily

because of the food/drinks they are offering, but because they have curated experiences that

make their customers want to be part of the brand

Starbucks has consistently highlighted the importance of elevating the customer experience

by elevating its employee experience as the #1 driver of SSS

13

Looking forward to 2021Finding certainty in an uncertain environment

3) Food away from home share has structurally increased over the last several decades – driven by an

increase in women in the workforce, a shift in the generational timeline (people are getting married,

having children & buying homes later in life) and increased demand for experiences over goods

– The trajectory of the recovery as states reopen offers confidence in the resiliency of restaurant

demand, as limited service restaurant SSS have largely recovered to positive and full service

restaurants have noted demand has exceeded capacity

4) The restaurant industry is resilient – 1 in 2 Americans have worked at a restaurant at some point in

their lives and 1 in 3 Americans have had their first job at a restaurant

– The quick shift to off-premise only operations in an industry built for on-premise operations and

dining underscores the adaptability of the industry

– The restaurant industry has low barriers to entry and skills are transferable across languages,

countries and generations

5) Big companies are likely to get even bigger – they have the capital and resources to withstand a

challenging and dynamic operating environment and invest to help offset headwinds; the worse it is

in the broader restaurant industry, the better it is for large restaurant companies as supply contracts

– That said, there are implications for employment, as the restaurant industry represents 10% of

jobs and is a critical component of the value chain – based on the National Restaurant

Association, every $1 spent in restaurants contributes ~$1.60-1.90 to the economy

14

Looking forward to 2021Value Creation in Restaurants

We view technology as a key driver in the elements of value creation, unlocking opportunities to:

Leverage the box (increase in-store sales) – demand for convenience

– Unlock incremental sales through digital channels (mobile order & pay, delivery, loyalty, digital

drive-thru lanes, curbside pickup)

– Increase throughput & capacity

– Leverage customer data to incentivize behavior

Expand the global footprint – increase real estate site potential

– New formats increase addressable market

– Increase number of access points

Improve margins – generate leverage & cost saves

– Increased capacity/throughput to drive margin leverage (not constrained to three meals; reduce

processing time/speed of service)

– Cost savings (e.g., labor scheduling, inventory management, automate tasks)

15

Looking forward to 2021High Conviction Outperform

QSR & Fast Casual

Chipotle (CMG) - $1,700 Target Price

Leverage the box – implementing sales initiatives that resonate with consumers (digital, delivery,

menu innovation, marketing, operations)

Expand the global footprint – improving returns; expansion of new formats (Chipotlanes, digital-only)

Improve margins – SSS leverage and cost savings opportunities ($100K in AUVs = 100bps

restaurant margin)

Papa John’s (PZZA) - $110 Target Price

Leverage the box – implementing sales initiatives to maintain and grow sales (menu innovation,

marketing, operations, digital, delivery)

Expand the global footprint – improving returns following strong sales and in-store operational

enhancements; recruit well-capitalized franchisees into system (including refranchising opportunities)

Improve margins – SSS leverage, cost savings opportunities (corporate stores & supply chain) and

refranchising efforts

16

Looking forward to 2021High Conviction Outperform

Casual Dining

Darden (DRI) - $141 Target Price

Leverage the box – implementing sales initiatives that resonate with consumers (operations, menu

innovation, off-premise, value, marketing, digital)

Expand the global footprint – improving returns; opportunities in smaller markets

Improve margins – SSS leverage, productivity enhancements and cost savings opportunities

(simplification of menu, processes and procedures)

Food Distribution

Sysco (SYY) - $85 Target Price

Leverage multiple levers to drive organic case growth – improved restaurant traffic, acquisition of

new business and expansion of wallet share

Expand inorganic case growth – increased focus on M&A opportunities to supplement organic case

growth strategies, including expansion into new markets and categories (supporting growth of new

business and wallet share)

Improve margins – sales leverage and cost savings opportunities (already announced $350MM

structural cost savings in FY21, with more opportunities in FY22)

17

21 Themes for 2021

18

Restaurant Recovery Outlook

19

State of the industryAppetite for restaurants

The trajectory of the sales recovery has been better than initially feared as restaurants have proven

to be more resilient in an environment without dine-in as they have transitioned to off-premise

While a resurgence of virus cases has reversed reopening plans in many states, restaurants are

operationally better positioned than at the initial outbreak in mid-March and there appears to be

greater consumer trust in restaurants (as well as at-home fatigue)

Near-term, we believe trends are unlikely to meaningfully improve until states resume reopening

plans and weather is more favorable, though the rollout of several vaccines and expectations for

widespread availability by mid-2021 offer hope for a sustainable recovery (Credit Suisse biotech

team forecasts herd immunity in the US by 4Q21) – we expect 2022 AUVs to be above 2019

levels across our coverage

Over the near, medium and long-term, existing restaurants should benefit from a reduction in

industry supply – current forecasts suggest ~10-20% of restaurants have closed/will close

We expect the focus in 2021 will be on reemergence and how companies can capitalize on the

opportunities ahead with a reduction in industry supply and more favorable real estate environment

to accelerate market share gains

We view large chains as fundamentally better positioned than independents given their access to

resources & capital and more established off-premise & digital infrastructures, with a prolonged

reopening potentially leading to an even more favorable backdrop long-term

20

State of the industryTrajectory of recovery

Restaurant industry SSS have continued to improve across all segments since mid-March lows,

though the disparity in performance remains wide between limited service and full service restaurants

Restaurant SSS were down ~50% in April, improved to down 7-8% in September & October, though

began to reverse in November amidst more prohibitive on-premise dining restrictions and an increase

in COVID-19 cases; QSR SSS have remained strong, while full service trends decelerated exiting

2020

Source: Black Box, Bloomberg, MillerPulse, Credit Suisse

QSR SSS & Casual Dining SSS (MillerPulse)Restaurant Industry SSS (Black Box)

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

Jan-2

0

Feb-2

0

Mar-

20

Apr-

20

May-

20

Jun-2

0

Jul-2

0

Aug-2

0

Sep-2

0

Oct

-20

Nov-

20

Dec-

20

Rest

aura

nt

Indust

ry S

SS

QSR SSS Casual Dining SSS

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

Jan-2

0

Feb-2

0

Mar-

20

Apr-

20

May-

20

Jun-2

0

Jul-2

0

Aug-2

0

Sep-2

0

Oct

-20

Nov-

20

Dec-

20

Rest

aura

nt

Indust

ry S

SS

Traffic Average Check SSS

21

State of the industryTrajectory of recovery

Based on data from Technomic, US restaurant industry sales growth declined ~21% in 2020,

representing nearly ~$125BN, including ~$22BN from the limited service segment and ~$101BN

from the full service segment, or six years of restaurant sales growth (average ~4% per year)

Technomic estimates the restaurant industry will grow ~16% in 2021, gaining ~$73BN in sales,

including ~$20BN in limited service and ~$53BN in full service

Technomic estimates imply the restaurant industry will recapture ~91% of 2019 sales in 2021, with

limited service to recover ~99% of sales and full service to recover ~80-85% of sales

Source: Technomic, Credit Suisse

Restaurant Industry Sales GrowthRestaurant Industry Sales

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

Sale

s G

row

th

$0

$100

$200

$300

$400

$500

$600

$700

200

7

200

8

2009

201

0

201

1

201

2

2013

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

Sale

s ($

BN

)

QSR Fast Casual Casual Dining Midscale Fine Dining

22

State of the industryTrajectory of recovery

Based on data from Technomic, limited service restaurant sales growth declined ~7.5% in 2020,

including QSR sales growth of down ~6.5% and fast casual sales growth of down 11-11.5%

Technomic estimates the limited service restaurant segment will grow ~7% in 2021, including QSR

sales growth of 6.5-7% and fast casual sales growth of 8.5-9%

Technomic estimates imply the limited service restaurant segment will generate ~$301BN of sales in

2021, recovering 99% of 2019 sales, with QSR sales to fully recover to ~$243BN and fast casual

sales to recover to ~$57.5BN, down ~3.5% from 2019 levels

Source: Technomic, Credit Suisse

2020/2021 Limited Service Restaurant Sales vs 2019 LevelsLimited Service Restaurant Sales

$303BN$281BN

$301BN

$0BN

$50BN

$100BN

$150BN

$200BN

$250BN

$300BN

$350BN

$400BN

2019 2020 2021

Sale

s ($

BN

)

QSR Fast Casual

-6.4%

-11.3%

-7.4%

-0.1%

-3.6%

-0.8%

-12%

-10%

-8%

-6%

-4%

-2%

0%

QSR Fast Casual Limited Service (Total)

2020/2

021 S

ale

s vs

2019 S

ale

s

2020 vs 2019 2021 vs 2019

Limited Service Restaurants

23

State of the industryTrajectory of recovery

Based on data from Technomic, full service restaurant sales growth declined ~37% in 2020,

including casual dining down ~32.5% and midscale/fine dining down ~48.5%

Technomic estimates the full service restaurant segment will grow ~31% in 2021, including casual

dining sales growth of 26.5% and midscale/fine dining growth of 45%

Technomic estimates imply the full service restaurant segment will generate ~$226BN of sales in

2021, recovering 80-85% of 2019 sales, with casual dining sales to recover to ~$168BN, down

~14.5% relative to 2019, and midscale/fine dining to recover to ~$58BN, down ~25% from 2019

Source: Technomic, Credit Suisse

2020/2021 Full Service Restaurant Sales vs 2019 LevelsFull Service Restaurant Sales

$275BN

$173BN

$226BN

$0BN

$50BN

$100BN

$150BN

$200BN

$250BN

$300BN

$350BN

$400BN

2019 2020 2021

Sale

s ($

BN

)

Casual Dining Midscale Fine Dining

-32.5%

-46.5%

-51.5%

-37.0%

-14.6%

-24.3%-26.6%

-17.6%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Casual Dining Midscale Fine Dining Full Service (Total)

202

0/2

02

1 S

ale

s vs

201

9 S

ale

s

2020 vs 2019 2021 vs 2019

Full Service Restaurants

24

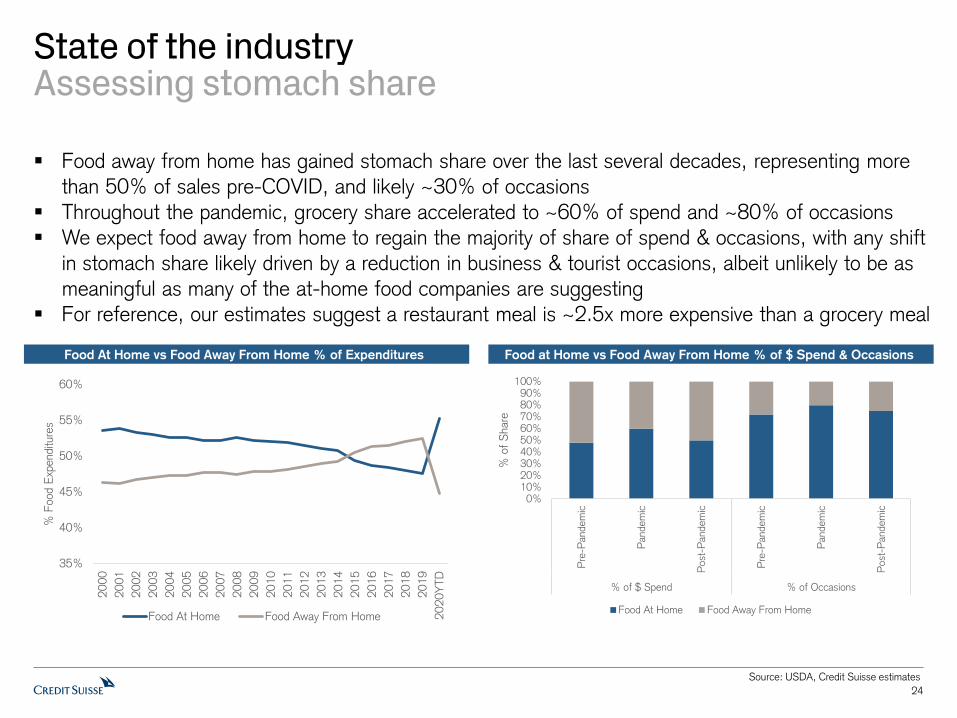

State of the industryAssessing stomach share

Food away from home has gained stomach share over the last several decades, representing more

than 50% of sales pre-COVID, and likely ~30% of occasions

Throughout the pandemic, grocery share accelerated to ~60% of spend and ~80% of occasions

We expect food away from home to regain the majority of share of spend & occasions, with any shift

in stomach share likely driven by a reduction in business & tourist occasions, albeit unlikely to be as

meaningful as many of the at-home food companies are suggesting

For reference, our estimates suggest a restaurant meal is ~2.5x more expensive than a grocery meal

Source: USDA, Credit Suisse estimates

Food at Home vs Food Away From Home % of $ Spend & OccasionsFood At Home vs Food Away From Home % of Expenditures

35%

40%

45%

50%

55%

60%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20Y

TD

% F

ood E

xpenditu

res

Food At Home Food Away From Home

0%10%20%30%40%50%60%70%80%90%

100%

Pre

-Pandem

ic

Pandem

ic

Post

-Pandem

ic

Pre

-Pandem

ic

Pandem

ic

Post

-Pandem

ic

% of $ Spend % of Occasions

% o

f S

hare

Food At Home Food Away From Home

25

State of the industryDimensionalizing trends

Segment: QSRs have outperformed full service restaurants given their channel mix (65-70% drive-thru historically & limited dine-in), value appeal and level of convenience

Channel: 1) dine-in: trends have been challenged given dine-in capacity restrictions; many limited service restaurants have been slow to reopen; 2) drive-thru: QSRs have benefitted with the channel

representing ~90% of sales, up from 65-70% historically, and prompting the rollout of curbside; 3)

digital: digital channels have increased in mix across all restaurants for both pickup & delivery

Daypart: Breakfast & late night have demonstrated the slowest recovery given a reduction in commuter traffic & social gatherings

Traffic/Average Check: Traffic has been down & average check has been up more significantly for QSRs as occasions shift to larger family meals; average check has been down for full service

restaurants given reduced beverage attachment associated with off-premise

Occasion: Restaurants have lost the single diner transaction at a higher rate given less commuter traffic, and a factor driving larger average checks as customers consolidate occasions and purchase

more family meals; the coffee/breakfast category has faced an outsized impact from the shift

Geography: Geography has been a differentiating factor for restaurant performance throughout the pandemic, as those with longer lockdowns and greater exposure to urban areas have experienced

more significant declines; the Northeast & California have been the weakest regions, while the

Southeast has consistently been the strongest region

26

Full service restaurants facing operational, financial & consumer challenges in new world

Full service restaurants have fared worse than limited service restaurants in an environment

requiring increased social distancing and increasing shift toward off-premise given:

1) Capacity restrictions and social distancing requirements limit throughput

2) Increasing shift toward off-premise channels, with many full service restaurants not positioned

for multi-channel business, leading to reduced throughput and potential changes in employee

pay (reduced % tipped workers)

3) Average checks/profitability impacted given a reduction in high-margin beverage/alcohol

attachment of off-premise (with off-premise to be a bigger part of the sales mix)

4) Incremental costs as restaurants invest to enhance safety protocols for team members and

customers, including personal protective equipment, increasing sanitization/cleaning, shift

toward more disposable tableware & menus

5) Increasing investments required for digital ecosystems, with expectation for acceleration in

cashless payment adoption, noting full service restaurants and independents in particular have

invested less in technology & digital ecosystems

6) To the extent restaurants closed temporarily, it takes time and resources to re-ramp and make

necessary modifications to operations and layouts

27

Finding the silver lining for casual diningAccelerated efforts to innovate

Casual dining represents 70%+ of full service restaurant sales, the largest subsegment, though still

relatively fragmented, with ~30%+ of sales operated by large chains, relative to 80%+ among

chains within limited service restaurants

While there are clearly challenges in casual dining as a result of COVID, we believe it has also been

a catalyst to drive much needed innovation given years of complacency and share loss to limited

service restaurants

– Off-premise – off-premise has been touted as a key initiative for casual dining chains in recent

years, and efforts have been accelerated to recover sales with a multi-channel approach

– Digital – digital innovation has been relatively limited, though such will likely be prioritized as

consumers accelerate digital adoption & seek out limited interaction, and restaurants are forced

to manage under heightened scrutiny & look for opportunities to capture occasions across

channels, with interaction outside of the restaurants’ four walls increasingly important

Greater off-premise mix also supports greater digital adoption (off-premise has higher mix of

digital than on-premise)

– Value-proposition – many casual dining chains skew toward middle income consumers with a

segment of consumers prioritizing value; given a challenging economic environment, value

proposition will be important

28

Fine dining faces most significant challengesHigh ticket, high alcohol, high business & travel exposure

Fine dining represents ~11% of full service restaurant sales, and the most fragmented subsegment,

with ~12% of sales operated by large chains, relative to 30%+ in midscale and casual dining

We view fine dining as most at risk from recent COVID-19 challenges given:

– High average ticket & most discretionary in restaurants – likely to face the most significant

headwinds in an economic downturn

– High alcohol mix – relative profitability of on-premise and off-premise checks more pronounced

– High business and traveler mix – there has been a significant reduction in discretionary spending

among corporates and reduction in travel (with uncertainty regarding timing of a recovery)

– Greater exposure to urban markets – fine dining restaurants tend to be concentrated in high

traffic urban regions

– Limited off-premise mix historically (if at all) – infrastructure, operations & food offerings are not

well suited for multi-channel approach

– Hospitality and experience key to value proposition – modifications to high-touch, personalized

experiences likely to weigh on relative value of occasion

29

Chains better positioned than independentsWell capitalized, trusted & established infrastructures

We believe large chains are better positioned than independents given:

– Most large chains have remained open throughout the pandemic, which has largely allowed them

to maintain their staff, and we expect them to be better positioned to ramp up operations as

traffic returns

– Greater access to resources and capital, noting large public chains enhanced their cash positions

through debt and equity raises to position them to weather the challenges

– More established off-premise infrastructures, as many large chains have made investments in

the back-of-house & front-of-house to enhance operations for off-premise and digital

transactions (e.g., to-go stations, enhanced layouts, online ordering platforms)

– More established digital ecosystems, including online ordering, investments in waitlist

management, investments in table top tablets, more favorable terms with third-party providers

– Greater negotiating power with suppliers, landlords and lenders

– Likely more explicit guidelines as chains share consistent operational procedures over a large

base of restaurants

– Greater concentration in QSR, fast casual & casual dining segments, which will fare better than

fine dining

30

Source: The National Restaurant Association, OpenTable, Independent Restaurant Coalition, Technomic, CNBC, The New York Times, Credit Suisse

COVID-19 to leave a lasting impact on the future of restaurant industry supply

Based on industry resources, commentary and estimates, we believe 10-20% of restaurants could

close permanently, including 25% of full service restaurants, as a result of headwinds from COVID-

19, though such could be even higher should the duration of social distancing guidelines, lingering

concerns of health/safety and negative economic impact be even worse

– The National Restaurant Association estimates 17% of restaurants have already closed (12/20)

– OpenTable has indicated 32% of independent full service restaurants in the US have closed, an

increase from an initial estimate of 25% (12/20)

– Technomic estimates ~11% of restaurants closed in 2020, including ~11% of full service

restaurants & ~7% of limited service restaurants (majority to come from independents) (11/20)

– The Independent Restaurant Coalition (IRC) suggested the possibility that 85% of independents

could close if not provided additional government funding (6/20)

– Founder and former Chairman & CEO of Starbucks Howard Schultz suggested 30%+ of

independents could close without additional government intervention (per CNBC 4/20)

Restaurateur David Chang communicated similar sentiment, suggesting government

intervention would be necessary and likely needed higher up the chain (real estate investors)

to help alleviate pressure, as well support for hospitality employees

Restaurateur Danny Meyer has discussed deep challenges facing the restaurant industry,

with rent and labor costs too high, employee wages too low and insufficient restaurant

margins, calling for a systemic change across the industry

31

Source: CNBC, Credit Suisse

A second wave of closuresOver the next 12-24 months

While estimates regarding the number of restaurants that will not reopen is grim, risk still exists for

the restaurants that are able to open

– Initial pent-up demand not sustainable, particularly as stimulus wears off, consumers spend

recent savings and the impact on the economy is better understood

– Ongoing uncertainty regarding the pace of recovery to prior sales levels, especially amidst

capacity constraints and a challenging economic environment

– Profitability of new transactions are lower

Off-premise – generally lower profitability than in-store given less beverage attachment,

incremental packaging costs and incremental delivery costs (if applicable)

On-premise – incremental costs associated with new safety standards (PPE including

sanitization, masks, gloves, disposable tableware & menus, etc.)

In a normal operating environment, 60% of restaurants fail within their first year and 80% of

restaurants close within five years, underscoring the challenges of the industry Pre-COVID, full service industry unit growth had been negative over the last two years amidst

significant cost pressures weighing on profitability despite a relatively strong consumer backdrop

32

Source: CNBC, Bureau of Labor Statistics, Credit Suisse

When one restaurant closes, another one opensRestaurant resiliency and low barriers to entry

The restaurant industry has low barriers to entry, with 67%+ of all restaurants independently owned

and operated (and 92% within the full service segment)

– With the rise of ghost kitchens & virtual brands, the barrier to entry and risk to entry are even

lower, with low cost, turnkey solutions available to test concepts and gauge demand

The restaurant industry is a critical component of the US economy, employing nearly 10% of the

American workforce

– 1 in 3 Americans have had their first job at a restaurant

– 1 in 2 Americans have worked at a restaurant at some point in their lives

Given the low barriers to entry and opportunity for ownership across people of all skill sets, the

restaurant industry has historically been very resilient

– Restaurant employment dropped by ~50% in April 2020, though the industry has brought back

~60% of the ~6.1MM jobs lost between February and April, recovering to down ~20% through

December 2020

That said, December marked the second sequential monthly decline in employment

While we do not expect all restaurants to survive, and industry supply consolidation should be

beneficial for the long-term health of the sector, we still expect to see new restaurants to open

going forward that will capitalize on consumer trends

33

Source: Credit Suisse estimates

Off-premise to remain at sustainably higher levelLimited service restaurants

We estimate drive-thru and digital channels now represent ~90% of QSR sales, up from 65-70%

pre-COVID and digital channels comprise ~50% of fast casual sales, up from ~20% pre-COVID

We expect drive-thru and digital sales to remain at a sustainably higher level, accelerating the shift

to off-premise that existed even pre-COVID, and noting digital channels are generally stickier given

the increased level of convenience

Drive-Thru

65-70%

Sales MixDrive-Thru

Mobile Order

Delivery Digital ~20%

Sales Mix

Digital

Pre-COVID Post-COVID Pre-COVID Post-COVID

QSR Fast Casual

34

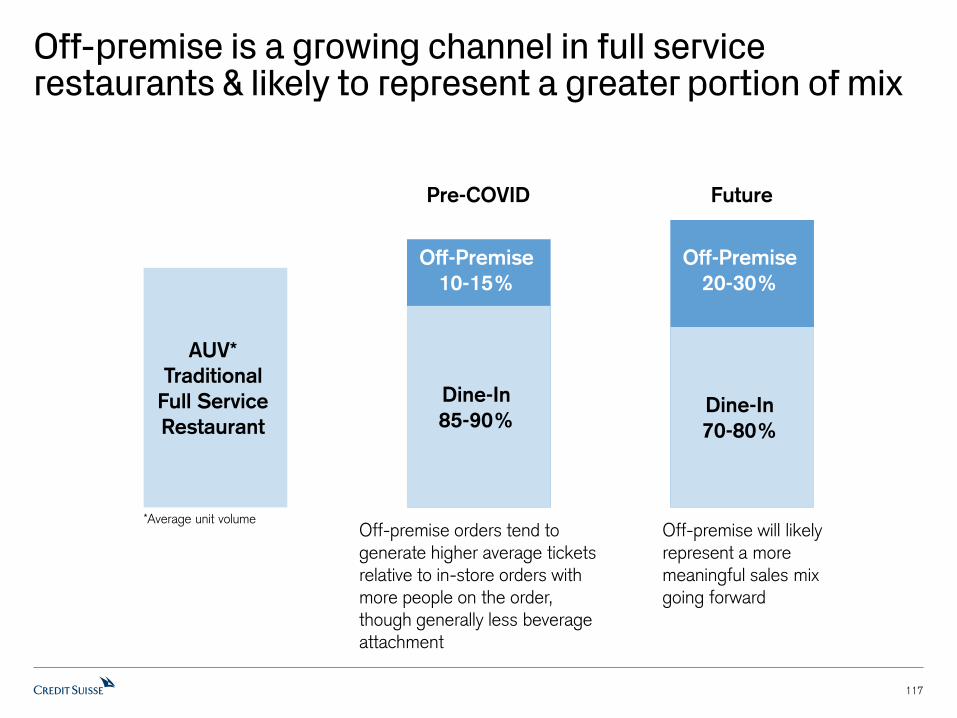

Off-premise to remain at sustainably higher levelFull service restaurants

Off-Premise

10-15%

Dine-In

85-90%

Off-Premise

20-30%

Dine-In

70-80%

Even as restaurants have reopened dining rooms, off-premise sales have remained at elevated

levels, with off-premise sales volumes running ~1.5-3x pre-COVID levels as restaurants appear to

be maintaining ~50% of peak off-premise sales on average

We expect off-premise sales volumes to remain at a sustainably higher level going forward given

changes in customer behavior, enhanced execution and greater customer awareness

Pre-COVID Post-COVID

Casual Dining

Off-Premise Sales Maintained as Dine-in Opened

0% 20% 40% 60% 80% 100%

Texas Roadhouse (TXRH)

Outback (BLMN)

LongHorn (DRI)

Chuy's (CHUY)

Olive Garden (DRI)

Carrabba's (BLMN)

Red Robin (RRGB)

BJ's (BJRI)

Cheesecake Factory (CAKE)

% of Peak Off-Premise Sales

Source: Company data, Credit Suisse estimates

Post-COVID Return to Prior Sales Levels ($000s)

Scenario 1 Scenario 2 Scenario 3 Scenario 4

Off-Premise AWS $38.5 $28.8 $19.2 $9.6

% COVID Off-Premise 100% 75% 50% 25%

On-Premise AWS $38.5 $48.1 $57.7 $67.3

% Pre-COVID On-Premise 57% 71% 85% 99%

Post-COVID AWS Shift $29.2 $19.6 $10.0 $0.4

% of Total AWS 38.0% 25.5% 13.0% 0.5%

On-Premise Mix 50% 63% 75% 88%

Off-Premise Mix 50% 38% 25% 13%

35

Source: Company data, Credit Suisse estimates

Reduced capacity to weigh on near-term dine-in salesExpectations for gradual recovery to on-premise dining & increase in off-premise In our base case assumption, we expect full service restaurants will maintain 50% of peak

off-premise sales volumes generated when operating as off-premise only, which implies restaurants

will need to recover 85% of prior on-premise capacity to return to pre-COVID sales levels

– Implies off-premise mix increases to 25% from our assumed ~12% pre-COVID

Assuming restaurants sustainably retain 50% of off-premise sales volumes generated when operating as

off-premise only, 85% of prior on-premise capacity will need to recover to return to pre-COVID sales volumes

Assumptions

Pre-COVID ($000s)

Annualized AUV $4,000

Average Weekly Sales $76.9

On-Premise $67.7 88%

Off-Premise $9.2 12%

COVID Off-Premise Only ($000s)

Annualized AUV ($000s) $2,000

% Prior Year Sales Levels 50%

Average Weekly Sales $38.5

On-Premise $0.0 0%

Off-Premise $38.5 100%

36

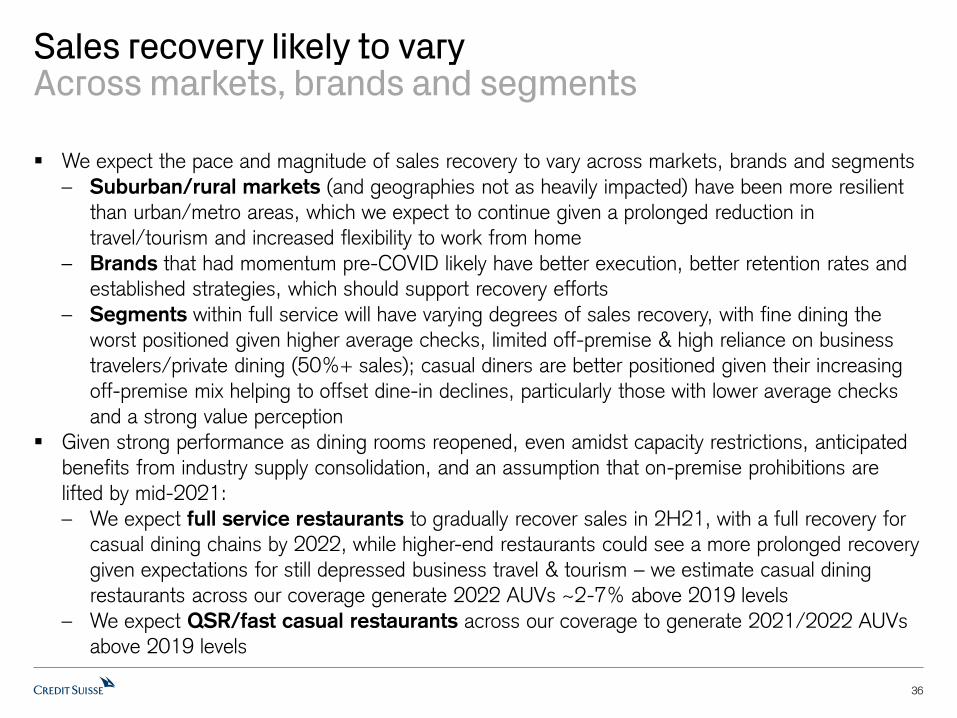

Sales recovery likely to varyAcross markets, brands and segments

We expect the pace and magnitude of sales recovery to vary across markets, brands and segments

– Suburban/rural markets (and geographies not as heavily impacted) have been more resilient than urban/metro areas, which we expect to continue given a prolonged reduction in

travel/tourism and increased flexibility to work from home

– Brands that had momentum pre-COVID likely have better execution, better retention rates and established strategies, which should support recovery efforts

– Segments within full service will have varying degrees of sales recovery, with fine dining the worst positioned given higher average checks, limited off-premise & high reliance on business

travelers/private dining (50%+ sales); casual diners are better positioned given their increasing

off-premise mix helping to offset dine-in declines, particularly those with lower average checks

and a strong value perception

Given strong performance as dining rooms reopened, even amidst capacity restrictions, anticipated

benefits from industry supply consolidation, and an assumption that on-premise prohibitions are

lifted by mid-2021:

– We expect full service restaurants to gradually recover sales in 2H21, with a full recovery for casual dining chains by 2022, while higher-end restaurants could see a more prolonged recovery

given expectations for still depressed business travel & tourism – we estimate casual dining

restaurants across our coverage generate 2022 AUVs ~2-7% above 2019 levels

– We expect QSR/fast casual restaurants across our coverage to generate 2021/2022 AUVs above 2019 levels

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

SS

S

Casual Dining Steakhouse (Casual Dining) Fine Dining

37

Source: Company data, Credit Suisse estimates

Dining during economic downturnsEconomic challenges likely to weigh on recovery

Full service restaurant sales are more of a consumer discretionary occasion, weighing on sales

trends during economic downturns – in 2008/2009, SSS across public full service restaurant

chains were negative for nine consecutive quarters, averaging down ~4% across 2.5 years and

down ~7% at the height of the recession from 4Q08-3Q09

– Higher-end full service restaurants performed even worse, while more value-oriented players,

family dining and bar & grill concepts appeared to be more resilient

Public Full Service Restaurant Industry SSSPublic Restaurant Industry SSS

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

SS

S

FSR SSS LSR SSS

38

Source: Technomic, Credit Suisse estimates

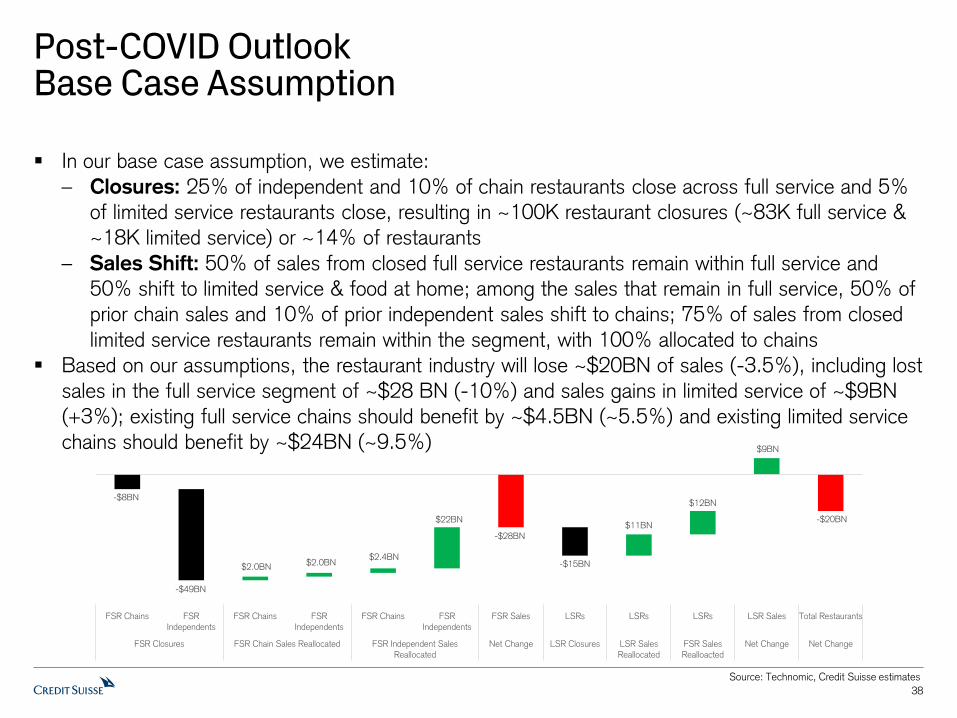

Post-COVID OutlookBase Case Assumption

In our base case assumption, we estimate:

– Closures: 25% of independent and 10% of chain restaurants close across full service and 5% of limited service restaurants close, resulting in ~100K restaurant closures (~83K full service &

~18K limited service) or ~14% of restaurants

– Sales Shift: 50% of sales from closed full service restaurants remain within full service and 50% shift to limited service & food at home; among the sales that remain in full service, 50% of

prior chain sales and 10% of prior independent sales shift to chains; 75% of sales from closed

limited service restaurants remain within the segment, with 100% allocated to chains

Based on our assumptions, the restaurant industry will lose ~$20BN of sales (-3.5%), including lost

sales in the full service segment of ~$28 BN (-10%) and sales gains in limited service of ~$9BN

(+3%); existing full service chains should benefit by ~$4.5BN (~5.5%) and existing limited service

chains should benefit by ~$24BN (~9.5%)

-$8BN

$2.0BN$2.0BN

$2.4BN

$22BN

-$28BN

$9BN

-$20BN

-$49BN

-$15BN

$11BN

$12BN

FSR Chains FSR

Independents

FSR Chains FSR

Independents

FSR Chains FSR

Independents

FSR Sales LSRs LSRs LSRs LSR Sales Total Restaurants

FSR Closures FSR Chain Sales Reallocated FSR Independent Sales

Reallocated

Net Change LSR Closures LSR Sales

Reallocated

FSR Sales

Realloacted

Net Change Net Change

39

Post-COVID OutlookBlue Sky Scenario

In our blue sky scenario, we estimate:

– Closures: 15% of independent & 5% of chain restaurants close across full service and 5% of limited service restaurants close, resulting in ~67K restaurant closures (~50K full service &

~18K limited service) or ~10% of restaurants

– Sales Shift: 75% of sales from closed restaurants remain within the full service segment and 25% shift to limited service & food at home; among the sales that remain in the segment, 50%

of prior chain sales and 10% of prior independent sales shift to chains; 75% of sales from

closed limited service restaurants remain within the segment, with 100% allocated to chains

Based on our assumptions, the restaurant industry will lose ~$8BN of sales (-1.5%), including lost

sales in the full service segment of ~$8.3BN (-3%); existing full service chains should benefit by

~$3.7BN (~4.5%) and existing limited service chains should benefit by ~$15BN (~6%)

Source: Technomic, Credit Suisse estimates

-$4BN

-$29BN

$1.5BN$1.5BN

$2.2BN

$20BN

-$8BN

-$15BN

$11BN$4BN

-$0.1BN

-$8BN

FSR Chains FSR

Independents

FSR Chains FSR

Independents

FSR Chains FSR

Independents

FSR Sales LSRs LSRs LSRs LSR Sales Total Restaurants

FSR Closures FSR Chain Sales Reallocated FSR Independent Sales

Reallocated

Net Change LSR Closures LSR Sales

Reallocated

FSR Sales

Realloacted

Net Change Net Change

40

Post-COVID OutlookGrey Sky Scenario

In our grey sky scenario, we estimate:

– Closures: 35% of independent & 10% of chain restaurants close across full service and 25% of independent & 5% of chain restaurants across limited service, resulting in ~164K restaurant

closures (~115K full service & ~48K limited service) or ~23% of restaurants

– Sales Shift: 50% of sales from closed restaurants remain within the full service segment and 50% shift to limited service & food at home; among the sales that remain in the segment, 50%

of prior chain sales and 10% of prior independent sales shift to chains; 75% of sales from

closed limited service restaurants remain within the segment, with 100% allocated to chains

Based on our assumptions, the restaurant industry will lose ~$28BN of sales (-5%), including lost

sales in full service of ~$38BN (-14%) and sales gains in limited service of ~$10BN (+3.5%);

existing full service chains should benefit by ~$5.4BN (~7%) and existing limited service chains

should benefit by ~$35BN (~14%)

Source: Technomic, Credit Suisse estimates

-$8BN

-$38BN

-$28BN

-$68BN

$2.0BN $2.0BN $3.4BN

$31BN

-$26BN

$19BN

$17BN

$10BN

FSR Chains FSR

Independents

FSR Chains FSR

Independents

FSR Chains FSR

Independents

FSR Sales LSRs LSRs LSRs LSR Sales Total Restaurants

FSR Closures FSR Chain Sales Reallocated FSR Independent Sales

Reallocated

Net Change LSR Closures LSR Sales

Reallocated

FSR Sales

Realloacted

Net Change Net Change

41

Evolution of the Digital Ecosystem

42

Enhancing the digital ecosystemIntegrating technology across all facets of organization

While restaurants have increasingly invested in technological ecosystems, we believe there will be

an acceleration in the implementation of technology across all facets of the organization and the

end-to-end customer experience as restaurants seek to:

Leverage the box (increase in-store sales)

– Unlock incremental sales through digital channels (mobile order & pay, delivery, loyalty, digital

drive-thru lanes, curbside pickup)

– Increase throughput & capacity

– Leverage customer data to incentivize behavior

Expand the global footprint

– New formats increase addressable market

– Increase number of access points

Improve margins

– Increased capacity/throughput to drive margin leverage (not constrained to three meals; reduce

processing time/speed of service)

– Cost savings (e.g., labor scheduling, inventory management, automate tasks)

The second derivative of digitalFrom implementation to integration & execution

Companies across all restaurant segments have increased investments to expand digital

ecosystems, though efforts have largely been concentrated on customer facing initiatives (e.g.,

mobile order & pay and delivery), with less regard to execution or long-term implications

– Primary focus has been unlocking opportunities to leverage the box (increase in-store sales)

largely by enhancing apps to add mobile order & pay capabilities and partnering with third-party

delivery platforms

More recently, we have seen companies establishing holistic infrastructures and strategies that

permeate throughout the organization as the restaurant and technology worlds learn to coexist –

challenging given a historically antiquated industry with low profit margins

Going forward, we expect the focus will shift to what we view as the second derivative of digital

– integrating technology to unlock value across all facets of the business including: 1) customer

facing initiatives to strategically increase digital utilization, capture customer data and secure more

loyalty, and 2) back of house opportunities to enhance margins amidst increasing cost pressures

43

Leverage the box (increase in-store sales)Increase digital utilization

Digital utilization (mobile order & delivery) remains relatively limited across the industry (<10% of

sales), though companies are seeking greater digital adoption given benefits of customer data, a

stickier digital customer, higher average checks, higher frequency and more profitable orders

– While the majority of digital growth has been delivery more recently, we expect a greater focus

on pushing in-store digital adoption (primarily mobile order & pay), as digital pickup orders are

the most profitable transactions (reduces transaction time, less labor required, less wear & tear),

and companies capture valuable customer data

Increase awareness

Separate sections/signage for digital transactions, social media posts & limited time campaigns to

encourage digital downloads

Loyalty/rewards programs

Addition of loyalty/rewards programs as an incentive to accelerate mobile order adoption, noting

companies with the highest mobile order utilization have strong rewards platforms, offering

opportunities to capture data to incentivize behavior and increase customer loyalty

44

Leverage the box (increase in-store sales)Execution over implementation

Now that restaurants have added customer facing capabilities (digital app, mobile order & pay,

delivery), we believe the focus shifts to optimize digital channels within restaurants to enhance the

in-store and digital customer experience

Modify store layouts

Add separate sections dedicated to digital and out-of-restaurant orders to reduce friction

Employee operations

Assign employees dedicated to digital orders (especially during peak hours)

Invest in technology to provide tools for best execution (upgrade POS systems, digital scanners,

digitized labels, etc.)

Packaging & menu development

Invest in packaging better suited for longer travel times/more transportable & multiple handlers

Modify and reduce menu size availability for specific channels to limit complexity and optimize the

out-of-restaurant experience

45

Leverage the box (increase in-store sales)Integration of digital channels

We expect restaurants will look to upgrade digital assets for more seamless integration across all

digital channels

Integrate third-party delivery within broader ecosystems

Mitigate the “multiple-tablet” problem in what appears to be a non-exclusive world of delivery with

multiple partnerships, which should help improve accuracy and limit lost orders

Integrate delivery within apps

Limit the customer shift to third-party aggregators

Get access to customer data from delivery channels

Introduce and integrate AI

Leverage decision logic technology to learn about customers, gather data and use data to

incentivize behavior

46

47

Leverage the box (increase in-store sales)Contactless order & pay

We expect restaurants will look for opportunities to implement contactless end-to-end processes,

including digital menus, ordering solutions and payment solutions, to limit interaction and ease

transaction friction

Full service restaurants generally point to payment as a key point of friction, with digital payment

solutions an opportunity to enhance the end-to-end experience

Menus

QR codes to be scanned on tables for customers to access menus on phones

In-restaurant tablets with digitized menus

Ordering solutions

In-restaurant tablets and digital apps with features to access menus and order in-restaurant or

mobile order ahead (including opportunities for upsell and add-on)

Payment solutions

In-restaurant tablets and digital apps with features to pay at table and with order ahead

Digital order notifications

Implementation of web/app messaging and notification systems to allow guests to inform

restaurants when they arrive, and restaurants can inform guests when orders are ready for pickup

48

Leverage the box (increase in-store sales)Modify operations for off-premise mix shift

We expect off-premise sales volumes will remain elevated as execution improves, marketing around

off-premise increases and customer awareness of off-premise has grown

Restaurant layouts

Add separate sections in restaurant and kitchens dedicated to off-premise orders to reduce friction

– Reduce distance food travels from kitchen to customer to enhance wait & service times

Add separate drive-thru lanes & parking spots to facilitate off-premise operations & the multi-

channel experience

Employee operations

Assign employees dedicated to off-premise orders (especially during peak hours)

Invest in technology to provide tools for best execution (upgrade POS systems, digital scanners,

digitized labels, etc.)

Packaging and menu development

Invest in packaging better suited for longer travel times/more transportable and multiple handlers

Modify & reduce menu availability for specific channels to limit complexity & optimize the experience

Enhanced features/channel availability

Expand available channels to include mobile/web order & pay, curbside pickup, third-party delivery

49

Leverage the box (increase in-store sales)Enhance procedures to ease concerns & attract dine-in

We expect customers will be less willing to wait for tables in large crowds (and degree of use of

communal bars is uncertain), and assume they will also seek out restaurants they trust are enforcing

enhanced safety procedures for employees and customers

Reservations and table management notifications

Implementation of web/app reservation and notification systems to inform guests of table availability

and when they are ready (can also integrate access to menus, order & payment solutions, etc., for

end-to-end contactless experiences)

Contactless order & pay

Access to menus and expanded availability of contactless order & pay with in-restaurant tablets and

phones (scan QR code, use near-field communication (NPC), go to a URL, download/use app) to

limit person-to-person contact and shared surfaces (e.g., menus)

Enhanced safety procedures

Increased sanitization (cleaning products, masks, gloves, sanitary wipes), temperature checks,

employee questionnaires/certifications, disposable menus/tableware

50

Leverage the box (increase in-store sales)Build relationships outside of restaurants’ four walls

As restaurants increasingly invest in digital platforms and technology infrastructures, we expect

them to better leverage CRM tools and look to establish loyalty, engage with customers to increase

frequency and encourage the use of multiple channels (especially if more of the at-the-table

transaction occurs digitally)

Customer relationship management (CRM)

Enhance personalization through implementation of guest engagement platform, including direct

booking capabilities, personalized guest profiles, targeted promotions, etc.

Loyalty/rewards programs

Addition of loyalty/rewards programs as an incentive to accelerate digital adoption, with greater

utilization supporting more opportunities to capture customer data to be used for personalization &

segmentation to incentivize behavior & increase customer loyalty

Guest engagement platforms and loyalty programs could be even more powerful for companies with

multiple concepts and locations as restaurants seek to capture different customer occasions and

increase frequency/loyalty through personalization

Expand the global footprintNew and enhanced formats

We expect restaurants will design new formats to mitigate friction of multiple channels, encourage

higher digital utilization and take advantage of the increasing shift to off-premise channels

Digital-forward restaurants

Likely smaller stores in dense locations, with limited seating and primarily focused on off-premise

and leveraging digital channels

Delivery/carryout focused restaurants

Limited menus, smaller formats, reduced seating

Enhancements through remodels

Add elements to encourage greater digital utilization (e.g., kiosks, in-store pickup shelves, pickup

windows, mobile-only drive-thrus)

Modify back of house to limit friction, including considerations of secondary production lines and

split kitchens (if possible)

51

Expand the global footprintVirtual, host and ghost kitchens

We expect more restaurants will explore opportunities to increase in-store capacity, particularly if

there are reduced capacity requirements near-term, or explore the potential for turnkey solutions to

test new markets (particularly if the off-premise mix is expected to be high)

Virtual Kitchens/Brands

Offer opportunity to increase in-restaurant capacity as existing restaurant launches separate virtual

brand available only on third-party platforms, likely during off-peak times (potentially expand into

additional dayparts)

Host Kitchens

Offer opportunity to increase in-restaurant capacity as existing restaurant provides kitchen to be

used by external operator (available on third-party platforms) during off-peak times as an alternative

to ghost kitchen for external operator

Ghost Kitchens

Offer opportunity to increase the number of access points, enter new markets and mitigate

disruption from operating multiple channels (mobile order, delivery, catering) within restaurants

52

Improve marginsBack of house opportunities

We expect a much greater focus on unlocking back of house opportunities by integrating technology

to optimize operations and realize cost savings, moving beyond customer facing initiatives to reduce

non-value add tasks, simplify roles, reallocate resources and better leverage data across the system

Optimize resources & reduce administrative tasks

Implement labor deployment software, automated scheduling, inventory management tools, digitized

invoices, track food waste, predictive analytics

Equipment

Digitize elements of the transaction (e.g., labels, upgrade digital assets, third-party delivery

integration)

Decision logic technology

If kitchen slower, can suggest menu items that won’t compound the problem

53

Improve marginsVoice technology

We view voice as the next wave of technology, with customer facing applicability already in the

marketplace and capabilities being implemented for back of house operations, helping to offset

increasing workforce challenges and regulatory pressures unlikely to subside

Voice order taking

Implement voice technology at the drive-thru

– McDonald’s is already in test following its acquisition of AI platform, Apprente, with deployment a

key milestone in the future of voice – 1) train customers on mainstream applicability and 2)

accelerate advancements for other companies to follow

Implement technology to accept voice orders over the phone

Voice inventory management

Eliminate some of the manual work required by writing and keying in inventory checks

54

55

Improve marginsIntegrate technology to increase productivity

We expect a much greater focus on unlocking productivity opportunities by integrating technology

to optimize operations and realization of cost savings to reduce non-value add tasks, simplify roles,

reallocate resources and better leverage data across the system

Digital contactless order & pay capabilities

Digital contactless order & pay capabilities to reduce staff resources & potentially increase table turns

Optimize resources and reduce administrative tasks

Implement labor deployment software, automated scheduling, inventory management tools, digitized

invoices, track food waste, predictive analytics

Equipment

Digitize elements of transaction (e.g., labels, upgrade digital assets, third-party delivery integration)

Leverage equipment/robots to eliminate/reduce manual tasks

Decision logic technology

Predictive analytics (e.g., if kitchen slower, suggest menu items that won’t compound the problem)

Voice technology

Implement technology to accept phone voice orders & eliminate manual tasks (e.g., inventory)

Technology comes at a costCorporate Level

Technology is a perpetual cost restaurants must incur to maintain their digital ecosystems

– As customer expectations evolve and the industry faces increasing pressures, investing in

technology is critical to enhance four wall economics through top-line leverage and cost savings

Select companies are making big investments in outside firms as they seek to gain a competitive

advantage against peers (accelerate digital innovation, access to talent, etc.)

56

February 2018: $200MM in Grubhub

July 2018: Acquires license for CardFree to accelerate digital development

December 2018: Acquires QuikOrder for $77MM

February 2019: $25MM digital investment, including $15MM for Accenture partnership

March 2019: $100MM investment in Venture Fund that invests in food & retail startups

March 2019: $300MM to acquire Dynamic Yield startup & $5MM investment in Plexure

September 2019: Acquires Apprente voice tech startup; launches McD Tech Labs

March 2020: Acquires Heartstyles, a leadership development program

Technology comes at a costRestaurant Level

Infrastructure, Equipment & Software – Back of house/front of house technology and equipment, maintenance fees, support, etc. (annual & one time fees)

Technology/Digital Transaction Fees – Franchisees generally pay fees on every digital order

Credit Card Processing Fees – Digital orders generally transacted with credit/debit cards

Mobile offers and loyalty programs – Many restaurant companies offer mobile/online-specific deals to encourage utilization and loyalty programs, with restaurants incurring the cost of discounts

Delivery Fees – Incremental costs: 1) commission and delivery costs for third-party delivery (average ~15-30% of average ticket); 2) proprietary delivery infrastructure (if applicable)

Customer Level Delivery Fees – Customers pay higher prices for delivery through 1) delivery fees, 2) service fees

and 3) inflated menu prices

– Near-term, we expect customers will bear a disproportionate amount of the costs as: 1) third-

party aggregators are fighting for share and seem to be more willing to negotiate with

restaurants to accept lower rates, while shifting costs to customers through delivery & service

fees; 2) increased regulations on third-party fees in many jurisdictions limit what aggregators can

charge restaurants (for now, temporary); and 3) restaurants have flexibility in pricing menus on

third-party platforms, with most charging higher delivery menu prices relative to in-store

57

58

Inflection in digital trends and accelerating adoptionExpect increased investments and focus going forward

Customer facing technology is largely unsophisticated across full service, lagging behind upgrades

made by QSR & fast casual peers which have accelerated investments in technology in recent years

Going forward, we expect an increase in digital adoption and utilization for both off-premise and

on-premise transactions, driven by customer demand and changing restaurant operations

Sustainably higher off-premise sales mix to support increased digital utilization: – Greater awareness of digital ordering, with recent advertising focused on digital off-premise

availability