how global majors passed through 2020, and themes for 2021

TRANSCRIPT

How global majors passed through 2020, and themes for 2021 and beyond

April 2021

1

Resume

In 2020 global oil & gas majors:

• experienced deterioration of key financial metrics and rating downgrades;

• made significant opex and capex cuts, some slashed dividends;

• sharply increased leverage.

Current challenges include:

• adapting to the global ESG transition;

• upstream underinvestment of Western majors leaves them unprepared for a commodity super-cycle;

• significant balance sheet stresses and adjustments encourage M&A activity.

How global majors passed through 2020

Ho

w g

lob

al m

ajo

rs p

ass

ed

th

rou

gh

20

20

3

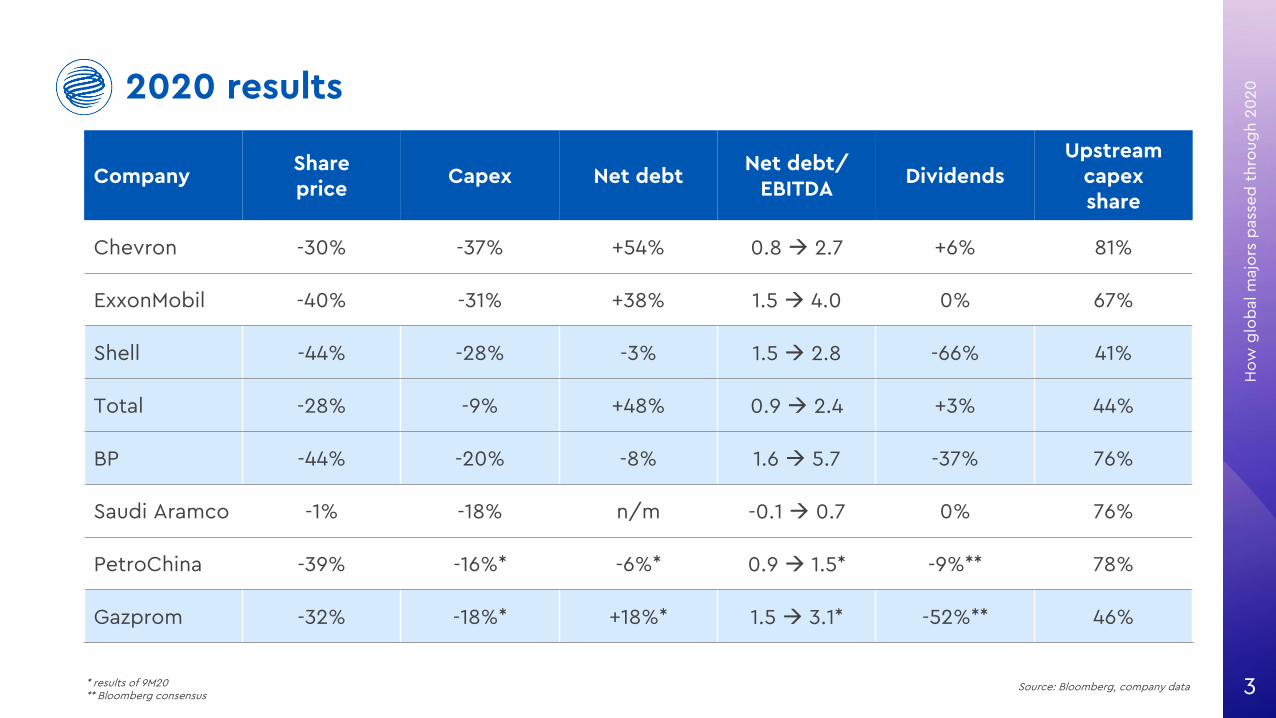

2020 results

Source: Bloomberg, company data

CompanyShare price

Capex Net debtNet debt/

EBITDADividends

Upstream capex share

Chevron -30% -37% +54% 0.8 2.7 +6% 81%

ExxonMobil -40% -31% +38% 1.5 4.0 0% 67%

Shell -44% -28% -3% 1.5 2.8 -66% 41%

Total -28% -9% +48% 0.9 2.4 +3% 44%

BP -44% -20% -8% 1.6 5.7 -37% 76%

Saudi Aramco -1% -18% n/m -0.1 0.7 0% 76%

PetroChina -39% -16%* -6%* 0.9 1.5* -9%** 78%

Gazprom -32% -18%* +18%* 1.5 3.1* -52%** 46%

* results of 9M20** Bloomberg consensus

Ho

w g

lob

al m

ajo

rs p

ass

ed

th

rou

gh

20

20

4

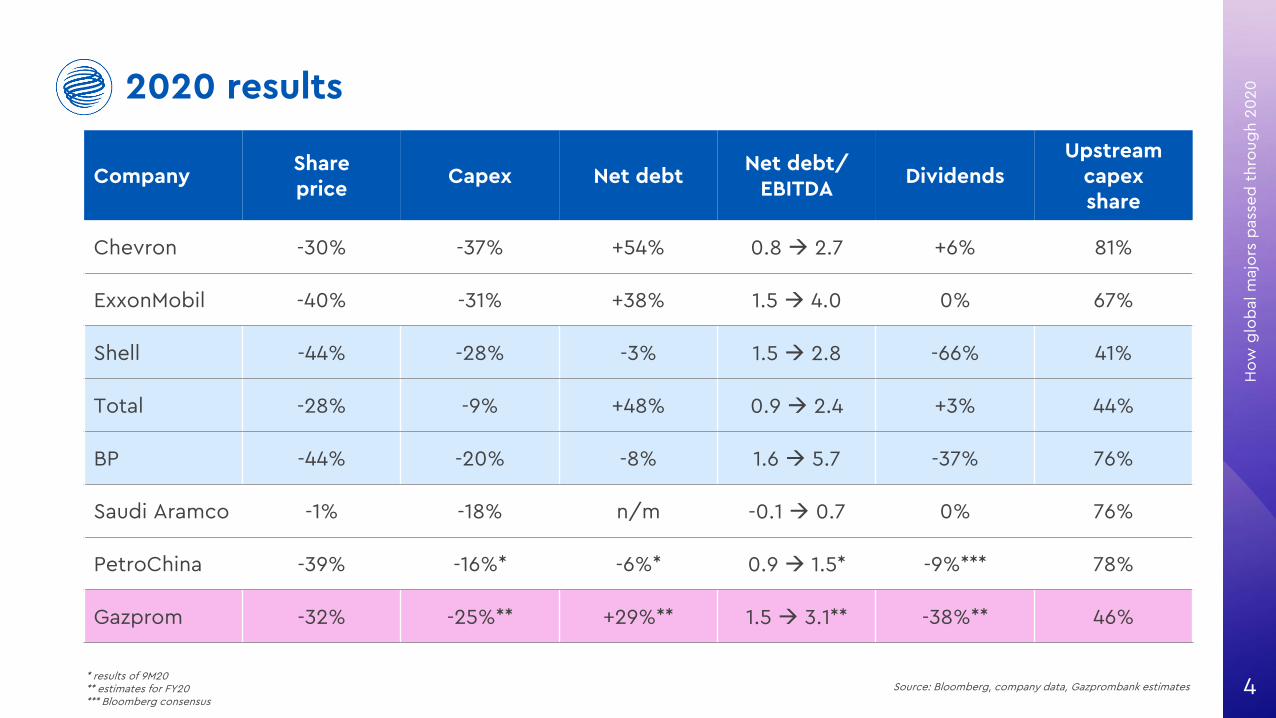

2020 results

Source: Bloomberg, company data, Gazprombank estimates

CompanyShare price

Capex Net debtNet debt/

EBITDADividends

Upstream capex share

Chevron -30% -37% +54% 0.8 2.7 +6% 81%

ExxonMobil -40% -31% +38% 1.5 4.0 0% 67%

Shell -44% -28% -3% 1.5 2.8 -66% 41%

Total -28% -9% +48% 0.9 2.4 +3% 44%

BP -44% -20% -8% 1.6 5.7 -37% 76%

Saudi Aramco -1% -18% n/m -0.1 0.7 0% 76%

PetroChina -39% -16%* -6%* 0.9 1.5* -9%*** 78%

Gazprom -32% -25%** +29%** 1.5 3.1** -38%** 46%

* results of 9M20** estimates for FY20*** Bloomberg consensus

Ho

w g

lob

al m

ajo

rs p

ass

ed

th

rou

gh

20

20

5

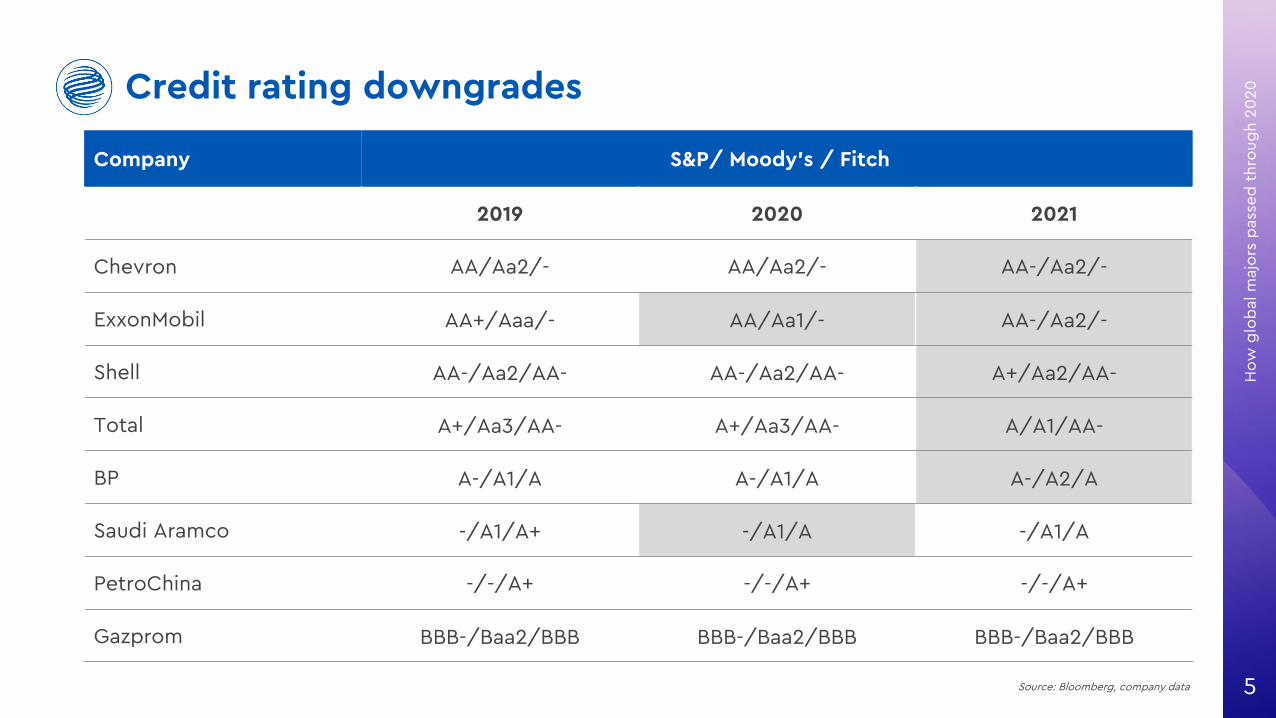

Credit rating downgrades

Source: Bloomberg, company data

Company S&P/ Moody’s / Fitch

2019 2020 2021

Chevron AA/Aa2/- AA/Aa2/- AA-/Aa2/-

ExxonMobil AA+/Aaa/- AA/Aa1/- AA-/Aa2/-

Shell AA-/Aa2/AA- AA-/Aa2/AA- A+/Aa2/AA-

Total A+/Aa3/AA- A+/Aa3/AA- A/A1/AA-

BP A-/A1/A A-/A1/A A-/A2/A

Saudi Aramco -/A1/A+ -/A1/A -/A1/A

PetroChina -/-/A+ -/-/A+ -/-/A+

Gazprom BBB-/Baa2/BBB BBB-/Baa2/BBB BBB-/Baa2/BBB

Ho

w g

lob

al m

ajo

rs p

ass

ed

th

rou

gh

20

20

6

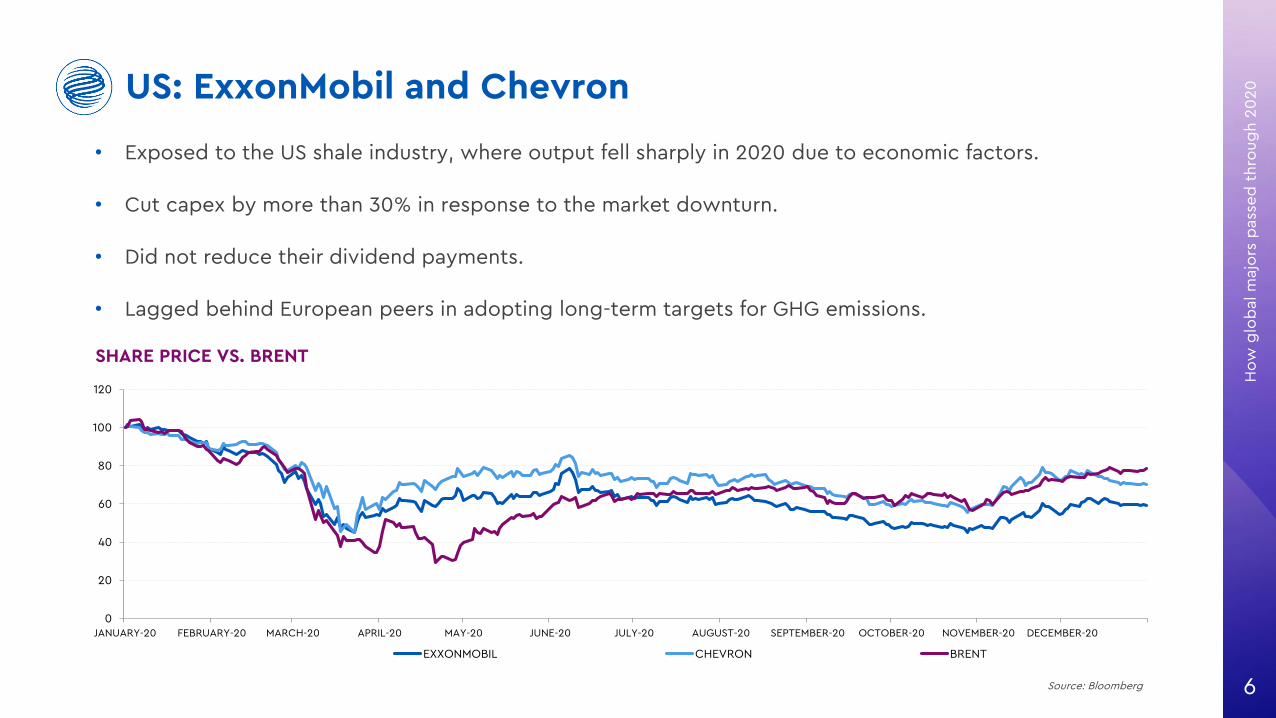

US: ExxonMobil and Chevron

Source: Bloomberg

SHARE PRICE VS. BRENT

• Exposed to the US shale industry, where output fell sharply in 2020 due to economic factors.

• Cut capex by more than 30% in response to the market downturn.

• Did not reduce their dividend payments.

• Lagged behind European peers in adopting long-term targets for GHG emissions.

0

20

40

60

80

100

120

JANUARY-20 FEBRUARY-20 MARCH-20 APRIL-20 MAY-20 JUNE-20 JULY-20 AUGUST-20 SEPTEMBER-20 OCTOBER-20 NOVEMBER-20 DECEMBER-20

EXXONMOBIL CHEVRON BRENT

Ho

w g

lob

al m

ajo

rs p

ass

ed

th

rou

gh

20

20

7

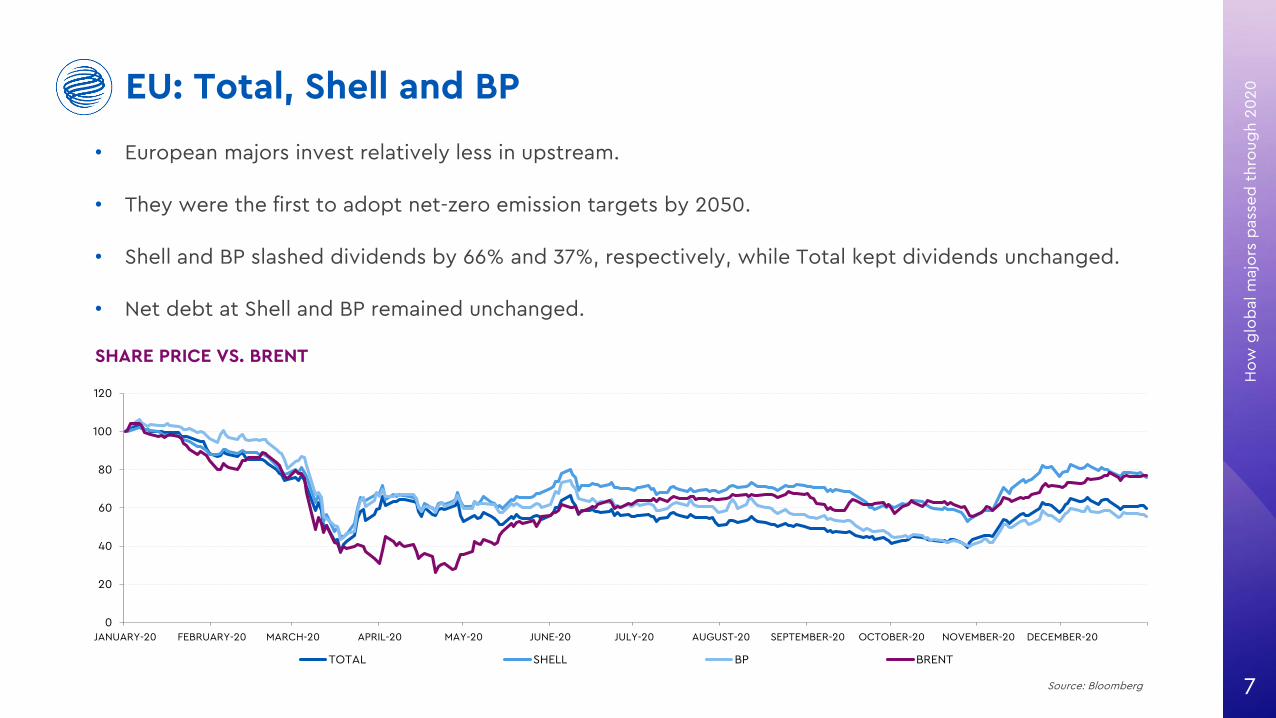

EU: Total, Shell and BP

SHARE PRICE VS. BRENT

• European majors invest relatively less in upstream.

• They were the first to adopt net-zero emission targets by 2050.

• Shell and BP slashed dividends by 66% and 37%, respectively, while Total kept dividends unchanged.

• Net debt at Shell and BP remained unchanged.

Source: Bloomberg

0

20

40

60

80

100

120

JANUARY-20 FEBRUARY-20 MARCH-20 APRIL-20 MAY-20 JUNE-20 JULY-20 AUGUST-20 SEPTEMBER-20 OCTOBER-20 NOVEMBER-20 DECEMBER-20

TOTAL SHELL BP BRENT

Ho

w g

lob

al m

ajo

rs p

ass

ed

th

rou

gh

20

20

8

EM: Saudi Aramco and PetroChina

• National oil producers in emerging markets continue to invest actively in upstream.

• Saudi Aramco has free float of 1.5%, among the lowest globally. This helped its share price performance.

• Saudi Aramco’s earnings slumped 44%, but the company maintained stable quarterly dividend payments.

• PetroChina paid a dividend while reporting negative free cash flow.

Source: Bloomberg

0

20

40

60

80

100

120

JANUARY-20 FEBRUARY-20 MARCH-20 APRIL-20 MAY-20 JUNE-20 JULY-20 AUGUST-20 SEPTEMBER-20 OCTOBER-20 NOVEMBER-20 DECEMBER-20

SAUDI ARAMCO PETROCHINA BRENT

SHARE PRICE VS. BRENT

Ho

w g

lob

al m

ajo

rs p

ass

ed

th

rou

gh

20

20

9

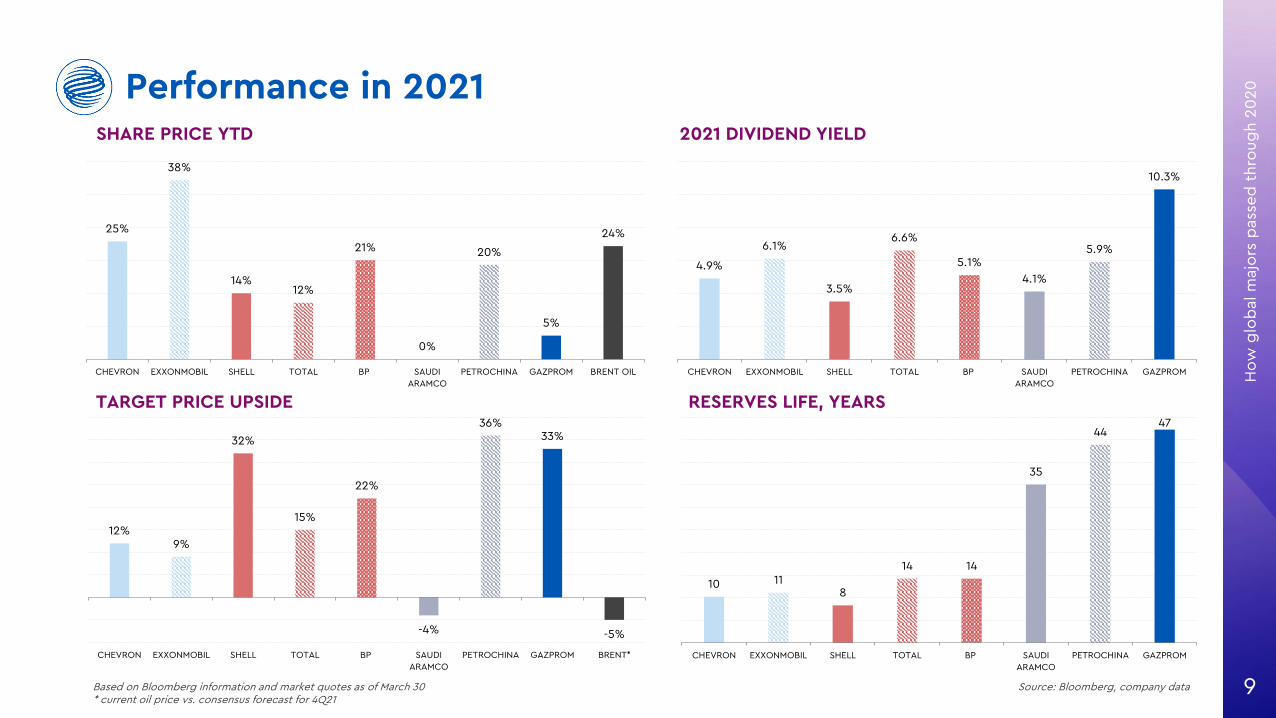

Performance in 2021

Source: Bloomberg, company dataBased on Bloomberg information and market quotes as of March 30* current oil price vs. consensus forecast for 4Q21

SHARE PRICE YTD

TARGET PRICE UPSIDE

2021 DIVIDEND YIELD

RESERVES LIFE, YEARS

25%

38%

14%12%

21%

0%

20%

5%

24%

CHEVRON EXXONMOBIL SHELL TOTAL BP SAUDI

ARAMCO

PETROCHINA GAZPROM BRENT OIL

12%9%

32%

15%

22%

-4%

36%33%

-5%

CHEVRON EXXONMOBIL SHELL TOTAL BP SAUDI

ARAMCO

PETROCHINA GAZPROM BRENT*

4.9%

6.1%

3.5%

6.6%

5.1%

4.1%

5.9%

10.3%

CHEVRON EXXONMOBIL SHELL TOTAL BP SAUDI

ARAMCO

PETROCHINA GAZPROM

10 118

14 14

35

4447

CHEVRON EXXONMOBIL SHELL TOTAL BP SAUDI

ARAMCO

PETROCHINA GAZPROM

Themes for 2021 and beyond

Th

em

es

for

20

21

an

d b

eyo

nd

11

Oil majors devise long-term plans to improve ESG metrics

• The Paris Agreement and numerous investor groups call on the sector to address climate change concerns.

• Large pension funds have announced that they will only hold stocks in those energy companies which invest in renewable technologies.

• Energy transition is gaining traction.

• European majors such as BP, Shell, Total and Equinor have committed to net-zero emissions by 2050.

• US oil and gas companies lag behind European peers.

• ExxonMobil adopted long-term targets for GHG emissions in December 2020, becoming the last US major to bow to shareholder pressure.

Th

em

es

for

20

21

an

d b

eyo

nd

12

Clean energy without fossil fuels? Not so soon

• Only renewable sources allow to produce clean pollution-free energy.

• In the EU, the share of renewables in energy consumption increased continuously between 2004 and 2019, from 10% to 20%.

• The Europe 2030 target for renewables is 32%, which still leaves ample room for oil and gas supplies.

• Interest in hydrogen is rising. Europe is lobbying to invest carbon emission fees into hydrogen.

• However, hydrogen’s advantage over LNG/natural gas is not obvious.

• Massive investment in new economy infrastructure requires uninterrupted oil and gas supplies.

Th

em

es

for

20

21

an

d b

eyo

nd

13

Lower capex leaves the market exposed to supply deficit

• Global majors have optimized upstream portfolios to turn in faster cash generation. This has been accomplished at the expense of exploration.

• In the medium term, the upstream will remain a core segment for majors and require more capex.

• BP announced no exploration in new countries and a 40% reduction of hydrocarbon output by 2030.

• Capex in green energy will take a significant share of investment programs.

• Europe’s dependence on external gas supplies is a risk. Recent example: S. Arabia cancelling LNG plans.

Th

em

es

for

20

21

an

d b

eyo

nd

14

Expecting active M&A and restructuring period ahead

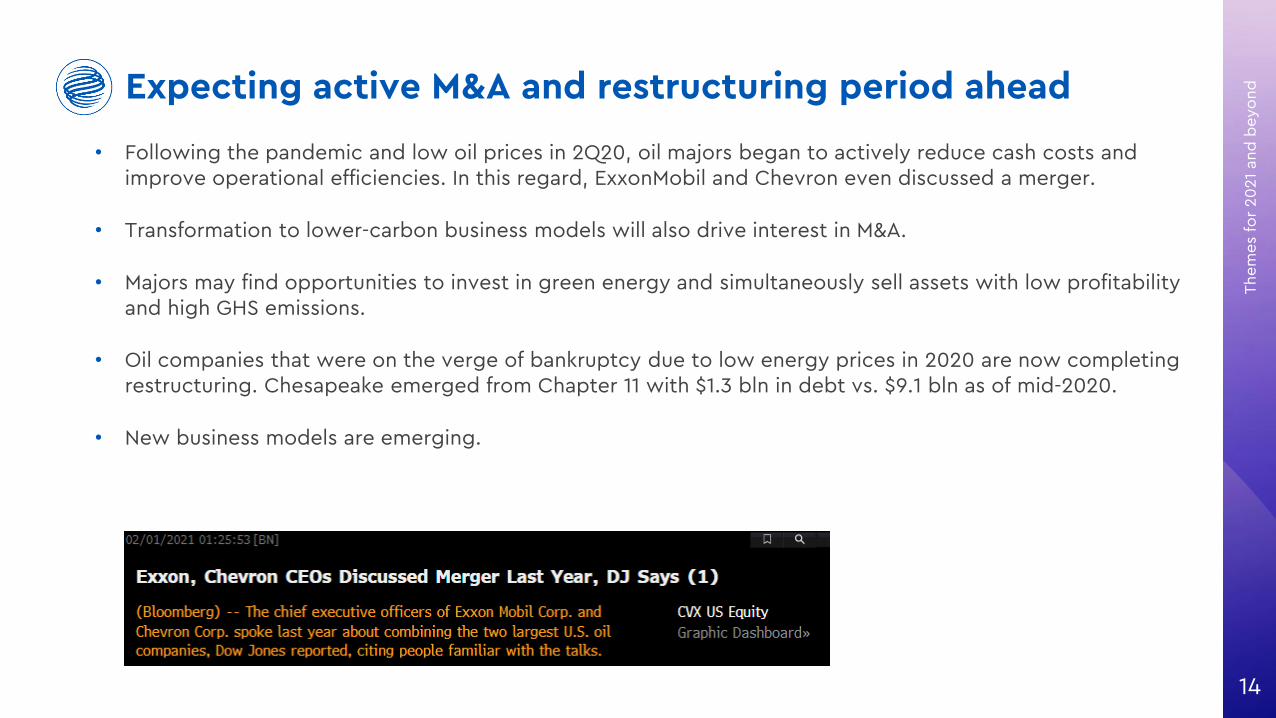

• Following the pandemic and low oil prices in 2Q20, oil majors began to actively reduce cash costs and improve operational efficiencies. In this regard, ExxonMobil and Chevron even discussed a merger.

• Transformation to lower-carbon business models will also drive interest in M&A.

• Majors may find opportunities to invest in green energy and simultaneously sell assets with low profitability and high GHS emissions.

• Oil companies that were on the verge of bankruptcy due to low energy prices in 2020 are now completing restructuring. Chesapeake emerged from Chapter 11 with $1.3 bln in debt vs. $9.1 bln as of mid-2020.

• New business models are emerging.

Th

em

es

for

20

21

an

d b

eyo

nd

15

How this commodity super-cycle is different

• Some analysts argue that a new commodity super-cycle has begun.

• Post-pandemic recovery, massive stimulus spending, rising inflation, Chinese economic growth and a deteriorating US dollar are seen as drivers for a bull market in commodities.

• Prices of silver, copper, platinum and other commodities are at their highest levels in years.

• Oil prices have also recovered from multi-year lows.

• Current underinvestment in upstream may significantly limit future supplies.

• Unprecedented monetary easing smooths the cycle.

• Explosive growth of the new economy requires heavy investments.

Th

em

es

for

20

21

an

d b

eyo

nd

16

Drivers of value in O&G

• DM majors: saving on upstream investments will enhance financial performance.

• EM producers: can gain market share in the long term, as drilling is profitable at current oil prices.

• Majors again can select value-enhancing capital allocations among dividends, capex and debt repayment.

• Europe’s gas storage levels dropped to 30% of capacity and must be topped up.

• ESG and de-carbonization strategies.

• Developing new economy infrastructure will drive energy demand.

• Investors are shifting attention to hydrogen as a cleaner fuel alternative.

• Expected rise in electricity demand will support power generation businesses.

HQ: 16/1 Nametkina St., Moscow 117420, Russia. Office: 7 Koroviy val St.

Research Department

+7 (495) 983 18 00

EQUITY SALES

+7 (495) 988 24 10

FIXED INCOME SALES

+7 (495) 980 41 82

Copyright © 2003-2021. Gazprombank (Joint Stock Company). All rights reserved

This material has been prepared by Research Department of Gazprombank (Joint Stock Company), incorporated in Moscow, Russia and licensed by the CentralBank of Russian Federation. Where this document refers to “you” it refers to you or your organisation. It is an investment recommendation and has beenprepared pursuant to the provisions of Markets in Financial Instruments Directive 2014/65/EU (MIFID II) and Market Abuse Regulation 2014/596/EU as well asGazprombank policies, procedures and internal rules of conduct for managing conflicts of interest.

This material contains an independent explanation of the matters contained within and must not be relied upon as investment advice. It does not take intoaccount whether an investment, course of action, or associated risks are suitable for the recipient. This material is not intended to provide personal investmentadvice and it does not take into account the specific investment objectives, financial situation and the particular needs of any specific person who may receivethis report. Recipients should seek independent professional financial advice regarding the legal, financial, tax and regulatory consequences of any transactionas well as the suitability and/or appropriateness of making an investment or implementing any investment strategies discussed in this document and shouldunderstand that statements regarding future prospects may not be realised. Any information and opinions contained in the report are published for theassistance of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient, are subject tochange without notice and not intended to provide the sole basis of any evaluation of the instruments discussed herein.

This investment recommendation is based on information obtained from public sources believed by Gazprombank (Joint Stock Company) (hereinafter referredto as “Gazprombank” or “we”) to be reliable, but we do not represent it as accurate or complete, and it should not be relied on as such. With the exception ofinformation directly pertaining to Gazprombank, Gazprombank shall not be liable for the accuracy or completeness of any information shown herein.

We certify in this investment recommendation that (i) the views expressed in this investment recommendation accurately reflect our personal views about thesubject company or companies and its or their securities, and (ii) no part of the analyst’s remuneration was, is or will be, directly or indirectly, related to thespecific recommendations or views expressed in this investment recommendation, and all opinions should not be regarded as Gazprombank’s position. Allopinions and estimates are given as of the date hereof and are subject to change without notice. All opinions herein represent solely analysts’ personal opinionregarding the events and situations described and analyzed in this investment recommendation and may differ from or be contrary to the opinions expressedby business and investments divisions of due to using different approach or assumptions in making conclusions by them.

Investment recommendations may contain forecasts, projections and/or price targets that constitute the current judgment of the author as of the date of therelevant communication.

Gazprombank shall be under no obligation to update, amend this investment recommendation or otherwise notify anyone of any such changes. The financialinstruments mentioned herein may be unsuitable for certain categories of investors. This investment recommendation is for Professional Clients.

This investment recommendation should not be the only basis used when adopting an investment decision. Investors should make investment decisions at theirown discretion, inviting independent legal, financial, tax or any other consultants, if necessary, for their specific interests and objectives. Investors should notethat financial instruments and other investments denominated in foreign currencies are subject to exchange rate fluctuations, which may adversely affect thevalue of the investment or financial instrument.

Gazprombank and the individuals (excluding any financial analysts or other personnel involved in the production of investment recommendation) associatedtherewith may (in various capacities) have positions or deal in transactions or securities (or related derivatives) identical or similar to those described herein.Gazprombank and/or its affiliates may also be holding securities of the issuers it writes on.

Gazprombank and/or its affiliate(s) may make a market and/or provide liquidity in the instruments within the Investment recommendation.

Gazprombank respects the confidentiality of information it receives about its clients and complies with all applicable laws with respect to the handling of thatinformation. Gazprombank has enacted effective internal procedures in respect of informational barriers (including the establishment of “Chinese walls”) whichare designed to restrict information flows between different areas of the Gazprombank. For more information, please, use the link:https://www.gazprombank.ru.

Employees are paid in part based on the profitability of Gazprombank and its affiliates, which includes investment banking revenues.

To the fullest extent permitted by law, Gazprombank accepts no liability and will not be liable for any loss, damage or expense arising directly andindirectly(including, but not limited to, special, incidental, consequential, punitive or exemplary damages or any loss, damage or expense arising from, but notlimited to, any defect, error, imperfection, fault, mistake or inaccuracy contained herein or any associated services, or due to any unavailability of thiscommunication or any contents or associated services) from the use of any information contained on this website, including any information which mayconstitute an investment recommendation/research.

Any information contained herein or in the appendices hereto shall not be construed as an offer or a solicitation of an offer to buy or sell or subscribe for anysecurities or financial instruments or as any investment advertisement, unless otherwise expressly stated herein or in the appendices hereto. Past performance isnot a guide to future performance. Estimates of future performance are based on assumptions that may not be realized.

Disclosures of conflicts of interest, if any, can be found in the Disclosures section.

Further information on the securities referred to in this investment recommendation can be obtained from Gazprombank upon request.

Redistribution or reproduction of this investment recommendation, wholly or in part, is prohibited without prior written permission from Gazprombank.

Recipients should consider whether a particular Investment Recommendation/Investment Research qualifies an inducement under MiFID II. If you are required orotherwise wish to pay for this research, we will enter into a separate written agreement which shall set out the terms on which research is provided to you,including the charges payable by you for receiving such material.

For residents of Hong Kong: Research which relates to “securities” (as defined in the Securities and Futures Ordinance (Cap. 571 of the Laws of Hong Kong)) isissued in Hong Kong by, or on behalf of, GPB Financial Services Hong Kong Limited (GPBFSHK), which takes responsibility for that content. Information in thisinvestment research shall not be construed to imply any relationship, advisory or otherwise, between GPBFSHK and the recipient or user of the investmentresearch unless expressly agreed by GPBFSHK. GPBFSHK is not acting nor should it be deemed to be acting, as a “fiduciary” or as an “investment manager” or“investment advisor” to any recipient or user of this information unless expressly agreed by GPBFSHK. GPBFSHK is regulated by Hong Kong Securities andFutures Commission. Please contact [Mr. Shaun Ansell (+852 2867 1883) or Mr. Joseph Chu (+852 2867 1812)] at GPBFSHK if you have any queries on or anymatters arising from or in connection with this investment research.

For GPB - Financial Services Ltd: The content of this investment research has been prepared within the meaning of MiFID II. The information contained herein isprovided for information purposes only and it is not a marketing communication, investment advice or personal recommendation within the meaning of MiFID II.The information must not be used or considered as an offer or solicitation of an offer to sell or buy or subscribe for any securities or financial instruments. GPB-Financial Services Ltd is regulated by the Cyprus Securities and Exchange Commission under license number 113/10.