up from sin: a portfolio approach to financial salvation randall dodd, financial policy forum shari...

TRANSCRIPT

Up From Sin: A Portfolio Approach to Financial

Salvation

Randall Dodd, Financial Policy Forum Shari Spiegel, Initiative for Policy

Dialogue (IPD), Columbia University

U.N. Financing for DevelopmentWorld Economic Forum

June 22, 2005

IDENTIFYING FINANCING PROBLEM AND POLICY REMEDY

PROBLEM1. Developing countries face too much foreign exchange risk from foreign

debt denominated in US dollar and other major currencies• Most financial crisis linked to currency devaluation

2. Original Sin: developing countries cannot borrow abroad in their own currency – or so we thought

3. Foreign investors unwilling to hold exchange rate risk on highly volatile developing country currencies

4. Hedging local currency risk through use of derivatives prohibitively expensive

SOLUTION1. Invest in local currencies through diversified portfolio2. Diversification is effective because of low degree of correlation between

rates of return on local currency assets3. Diversification – the only real free lunch in financial economics – allows

investors to earn high returns on portfolio whose variance is low due to low and sometimes negative correlation

4. Promote the use of such investment strategies by international investors and international financial institutions. Support the development of local currency and Treasury security markets by developing country governments.

Emerging Market Local Currency Debt Portfolio

The historical risk profile of an Equally Weighted Emerging Market Local Currency Debt (EMLCD) portfolio (WITH MAJOR CURRENCY RISK HEDGED) provides better risk adjusted returns, with a Sharpe Ratio of .9

*Returns are from January 1994 to January 2004.

¹EMLCD: data based on equal country weightings. Except for countries with liquidity restrictions, which were limited to 1% weightings.

Major currency (USD/EURO, YEN/USD) risk is hedged.

Annualized Return and Risk since January 1993*

EMLCD Universe¹

JP Morgan Emerging MarketBond Index (EMBI)

MSCI Emerging MarketEquity Free Index

-5

0

5

10

15

20

Annual Return (%)

Annual Volatility (%)

5 10 15 20 25 30

Local Currency Debt – A Good Diversifier

The portfolio has very little correlation with other financial assets.

*Correlations of monthly returns for the period 1/93 - 9/01

U.S. High Grade: Lehman Brothers Aggregate Index

U.S. High Yield: Lehman Bros. B-Rated High Yield Index

U.S. Equity: Standard & Poors 500 Index

WGBI (US$ hgd): Salomon Bros. NonUS World Gov’t Bond Index (Hedged)

Brady Bonds: Salomon Brady Bond Index

Emerging Equity: MSCI Emerging Market Free IndexEMLCD: data compiled from study based on equal country weightings. Except for countries with liquidity restrictions, which were limited to 1% weightings. Major currency (USD/EURO, YEN/USD) risk is hedged.

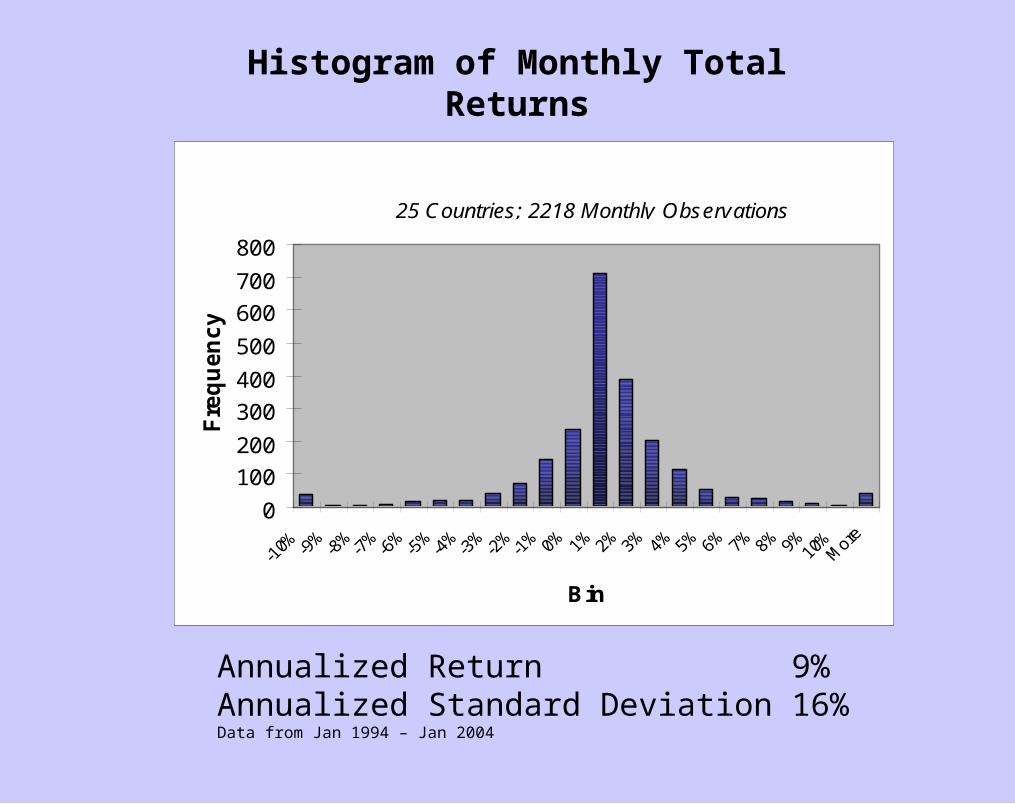

Histogram of Monthly Total Returns

0

100

200

300

400

500

600

700

800

Bin

Frequency

25 Countries; 2218 Monthly Observations

Annualized Return 9%Annualized Standard Deviation 16%Data from Jan 1994 – Jan 2004

Histogram of Portfolio Returns (Equally Weighted Countries)

0

2

4

6

8

10

12

14

-4.7

5%

-4.2

5%

-3.7

5%

-3.2

5%

-2.7

5%

-2.2

5%

-1.7

5%

-1.2

5%

-0.7

5%

-0.2

5%0.

25%0.

75%1.

25%1.

75%2.

25%2.

75%3.

25%3.

75%4.

25%4.

75%M

ore

Frequency

112 Monthly Observations

Annualized Return: 9%Annualized Standard Deviation: 5.3%Worst Monthly Case: -4.3%Data from Jan 1994 – Jan 2004

POLICY ISSUES

For Developing Countries

BENEFITS of Portfolio Approach1. Reduce foreign currency exposure2. Develop and deepen local financial markets

• Countries can initiate local market improvements and/or issue internationally

• Price discovery – create a yield curve for pricing future events• Liquidity• Auctions can replace underwriting costs

3. Simple, flexible and cheap4. Seigniorage – more local currency transactions generate more use of currency

and in turn more seigniorage

COSTS 1. Higher nominal interest rates than dollar debt2. Exposure to capital flight

LIMITATIONS1. Maturity

For Investors

BENEFITS of Portfolio Approach1. High Sharpe ratio – risk adjusted rate of return2. Investment returns that are uncorrelated with developed country returns

COSTS 1. High transactions costs 2. High initial investment needed to overcome high fixed transaction costs3. High minimum investment needed to achieve sufficient diversification

POLICY ISSUES

REMEDY THROUGH ABS STRUCTURE

BENEFITS of Asset Back Security Structure1. Gains from specialization in managing transactions costs2. Lower minimum investment thresholds for diversification3. Lower transactions costs 4. More liquid5. Longer-term commitment

COSTS 1. Underwriting (instead of auction)2. Contribute less to development and deepening of local financial markets

POLICY ISSUES

UNANSWERED QUESTIONS

1. What is the best index associated for local currency assets?2. How to handle partial diversification for regional investment or as

temporary process in the building of a fully diversified portfolio?3. What is the best structure for a new issue? Should it include tranches for

risk?

POLICY ISSUES

Up From Sin: A Portfolio Approach to Financial

Salvation

Randall Dodd, Financial Policy Forum Shari Spiegel, Initiative for Policy

Dialogue (IPD), Columbia University

U.N. Financing for DevelopmentWorld Economic Forum

June 22, 2005