university of lusaka school of business studies · university of lusaka school of business studies...

TRANSCRIPT

1

UNIVERSITY OF LUSAKA

SCHOOL OF BUSINESS STUDIES

AFIN 107: COST AND MANAGEMENT ACCOUNTING

2010

Prepared by Christopher Siakakole, ACMA, FZICA.

2

TABLE OF CONTENTS

OVERVIEW / INTRODUCTION 2

UNIT TOPIC PAGE

1 Introduction to Cost and Management Accounting 3

2 Cost Accumulation for Product Costing (Job and Batch Costing) 9

3 Cost Classification and Cost Behaviour 19

4 Materials: Stock Recording and Inventory Control 27

5 Materials – Purchasing, Reception and Storage 29

6 Inventory Control 39

7 Costing of Materials 45

8 Marginal Costing Versus Absorption Costing 55

9 Cost Behaviour and Cost-Volume-Profit (CVP) Analysis 72

10 CVP Analysis Formula and Break-Even Charts 83

11 Relevant Costing and Decision Making 92

12 Short Term Decisions 101

13 Budgeting and Budgetary Control 112

14 Flexible Budgets 122

15 Alternative Budget System 125

16 Standard Costing and Variance Analysis 131

17 Further Variance Analysis 136

18 Absorption Costing, Activity-Based Costing and Marginal Costing 145

19 Process Costing 162

20 Joint Products and By-products 172

21 Service Costing 178

3

INTRODUCTION / OVERVIEW

This module is meant to give information relating to the course in Cost and Management

Accounting. In order to exhibit adequate information to the students, the module has brought on

board all the relevant topics that are contained in a standard Cost and Management Accounting

paper.

In order to enrich the document, it has topics that relate to computations and more importantly

areas that involve aspects of Decision making.

The module goes further to compare the three (3) aspects of Cost Accounting, Financial

Accounting and Management Accounting.

Key topics such as those relating to Budgeting, Break-even Analysis, Decision Making, Variance

Analysis, Activity Based Costing and many others have also been covered.

At the end of each unit, there are some brief review questions to enable students compute and

attempt some of the questions for their learning to become practical.

4

UNIT 1

INTRODUCTION TO COST AND MANAGEMENT ACCOUNTING

LEARNING OUTCOMES

After studying this lecture, students should be able to:

Define Cost Accounting and Management Accounting;

Understand the rage of information provided by the cost accounting system;

Compare and contrast between Cost Accounting, Management Accounting and Financial

Accounting;

Explain the nature and meaning of responsibility accounting and the use of cost centres,

profit centres, and investment centres.

PURPOSE OF MANAGEMENT INFORMATION

The role of managers

Managers within any organization are decision-makers. The have to make decisions bout what

should be done and then issue instructions based on the decisions they have taken. Decisions can

be categorized as planning decisions and control decisions.

Planning decisions - These are decisions relating to what should be done in order to meet

certain objectives. These can be decisions for the long-term or for the short-term. Many

organizations try to work within the framework of an annual plan or budget, but strategic

planning can be for a longer period ahead and much planning is undertaken on a day-to-

day or weekly basis.

Control decisions - These relate to monitoring what is actually happening and if anything

seems to be going wrong deciding what should be done in order to correct the problem.

Control decisions relate to monitoring the direction of performance as budgeted

information is compared against actual performance.

COST AND MANAGEMENT ACCOUNTING

Managers need detailed information about the working of the business to enable them plan,

control and make the relevant decisions. The Cost and management accounting system

provides financial information regarding the financial aspects of business performance

needed by management

MANAGEMENT ACCOUNTING

Management Accounting is the application of the principles of accounting and financial

management in order to create, protect, preserve and increase value so as to deliver that

5

value to the stakeholders of profit and not for profit organizations both public and private

sector environments.

Management Accounting is a wider concept involving professional knowledge and skill in

the preparation and particularly the presentation of information to all levels of management

in the organization structure. The source of such information is the financial and cost

accounts. The information is intended to assist management in its policy and decision-

making , planning and control activities.

COST ACCOUNTING

Cost accounting is the establishment of budgets, standard costs and actual costs of

operations, processes, activities or products and the analysis of variances profitability or

social use of funds to help determine the direction of cost.

Cost accounting involves the application of a comprehensive set of principles, methods and

techniques to the determination and appropriate analysis of costs to suit the various parts of

the organization structure within a business.

Cost accounting and Management accounting are terms which are used interchangeably.

Cost accounting is part of Management accounting. Cost accounting provides a bank of data

for the management accountant to uses. Cost accounting aims at establishing the following:

(a) The cost of goods produced or services provided;

(b) The cost of a department or work station;

(c) What revenues have been;

(d) The profitability of a product, service or department or the organization in total;

(e) Selling prices;

(f) The value of stocks of goods;

(g) Future costs of goods and services; and

(h) Comparison of actual and budgeted costs.

COST ACCOUNTING SYSTEM

A cost accounting system is a system used by an organization in order to gather, store and also

analyze data relating to costs. The purpose of a cost accounting system is to provide

management information about costs and profits.

Cost accounting involves the application of a comprehensive set of principles, methods and

techniques to the determination and appropriate analysis of costs to suit the various parts of the

organization structure within a business.

6

A cost accounting system is often the basis for a management accounting system. The terms

“Cost accounting” and “Management accounting” are often used to mean the same thing though

there are some basic differences.

Benefits of Cost Accounting

The overriding benefit is the provision of information which can be used specifically to:

(a) Disclose profitable and unprofitable activities;

(b) Identify waste and inefficiency;

(c) Analyze movements in profit;

(d) Estimate and fix selling prices;

(e) Valuation of stock;

(f) Develop Budgets and standards to assist planning and control;

(g) Evaluate the cost effects of policy decisions.

FINANCIAL ACCOUNTING AND COST AND MANAGEMENT ACCOUNTING

Financial accounting is the classification and recording of the monetary transactions of an entity

in accordance with established concepts, principles, accounting standards and legal requirements

and their presentation by means of Profit and Loss accounts, Balance Sheet and Cash Flow

Statements, during and at the end of an accounting period.

The financial accounts record transactions between the business and its customers, suppliers,

employees and owners eg. shareholders. The managers of the business must account for the

way in which funds entrusted to them have been used and, therefore, records of assets and

liabilities are required as well as a statement of any increase in the total wealth of the business.

This is done by presenting a Balance sheet and the Profit and Loss Account at least once a year.

Many businesses have a financial accounting system with a nominal ledger, sales ledger and

purchases ledger and books of prime entry for recording transactions that have occurred during a

given period.

7

FINANCIAL ACCOUNTING MANAGEMENT ACCOUNTING

Limited companies are required * There is no legal requirement to prepare

by law to prepare financial accounts. management accounts.

The law and financial reporting * Management accounting formats are

Standards prescribe formats of entirely at the discretion off manage-

Published financial statements. ment.

Most financial accounting * Management accounts incorporate

information is of a monetary both monetary and non-monetary

nature. measures.

Financial accounts present an * Management accounts are both

essentially historic picture of historical record and future planning

past operations.

Financial information is * Management accounting information

Informative on performance. Is futurative for decision making.

Financial accounting information * Management accounting is for internal

is for external use. use.

INTERNAL REPORTING STRUCTURES

When costs are recorded, analyzed and reported, it is important that they are reported to the

managers or departments responsible for the spending. In other words, the reporting of cost

information should ideally be based on a system of responsibility accounting and responsibility

centres.

Responsibility Accounting

This is a system of providing financial information to management where the structure of the

reporting system is based on identifying individual parts of a business which are a responsibility

of a single manager.

Responsibility Centre

A Responsibility centre is an individual part of a business whose manager has personal

responsibility for its performance.

Many businesses are structured into a hierarchy of responsibility centres. These mighft be cost

centres, revenue centres, profit centres and investment centres.

At the lowest level of the hierarchy is the cost centre and at the highest is the investment centre.

8

Cost Centre

A Cost Centre can be defined as a production or service location, function, activity or item of

equipment whose costs may be accumulated and attributed to cost units.

A Cost Centre is a small part of a business in respect of which costs may be determined and

when related to cost units. Terminology varies from organization to organization, but the small

part of a business could be a whole department or merely a sub-division of a department. A

number of departments together would comprise a function. Thus a cost centre could be a

location, function or item of equipment or a group or combination of any of these.

Revenue Centre

A Revenue centre is part of the organization that earns sales revenue, its manager is responsible

for the revenue earned but not for the cost of the operation.

Profit Centre

A profit Centre is a part of the business for which both the costs and revenues earned are

identified. The Manager is responsible for both costs and revenues.

Investment Centre

An Investment Centre is a profit centre with additional responsibilities for capital employed and

possibly investment decisions. Managers of investment centres are responsible not for decisions

affecting costs and revenues only but also investment decisions.

CATEGORY OF COSTS

Costs are incurred in business on the following:

Direct materials;

Direct labour;

Direct expenses;

Production overheads;

Administrative overheads;

General overheads.

When costs are incurred, they are generally allocated to cost centres. Cost centres are simply

collection points for costs for further analysis.

Cost Units

Once costs have been traced to cost centres, they can further analyzed in order to establish cost

per unit. -`

9

A Cost Unit is a unit of production or unit of activity in relation to which cost is measured. The

cost unit is a basic control unit for costing purposes.

A cost unit is a unit of product or service in relation to which costs are ascertained.

The physical measure of product or service for which costs can be determined, is a cost unit. In

a printing firm for example, the cost unit would be the specific customer order. For a paint

manufacturer, the unit would be a litre of paint, to the milk supplier, it would be a litre of milk

etc.

Cost units are measured for several reasons:

To establish how much it has cost to produce an item or perform an activity;

To measure profit or loss on an item;

To value closing stocks;

To compare costs with budgeted costs.

Cost object

A Cost object is any activity for which a separate measurement of costs is desired.

KEY TERMS

Responsibility Accounting – A system of providing financial information to management, where

the structure of the reporting system is based on identifying individual parts of a business which

are the responsibility of a single manager.

Responsibility Centre – An individual part of a business whose manager has personal

responsibility for its performance.

Cost Centre – A location, function, activity or item of equipment for which costs are

accumulated and attributed to cost units.

Profit Centre – A part of the business or which both the costs incurred and revenues earned are

identified.

Investment Centre – A profit centre which is also responsible for capital investment.

REVIEW QUESTIONS

1 What is the purpose of management information?

2 Explain the term Cost unit;

3 Explain the term Cost centre;

4 Explain the term Profit centre;

5 Explain the term Investment centre;

10

UNIT 2

COST ACCUMULATION FOR PRODUCT COSTING

JOB AND BATCH COSTING

LEARNING OBJECTIVES:

After studying this topic, students should be able to:

Compare and contrast between: Job costing, Batch costing and Contract costing;

Undertake computation and analysis of information relevant to job, batch and contract

costing;

Prepare Ledger accounts for job and batch costing systems;

Prepare Ledger accounts for contract costing systems.

INTRODUCTION

Every organization will normally have its own costing systems with characteristics that are

unique to each particular given system. The costing system would have the same basic

characteristics as those of other comparable organizations in similar activities.

Specific order costing methods are appropriate for organizations which produce cost units which

are separately identifiable from one another. For example, job costing , batch costing and

contract costing are all types of specific order costing that students need to understand.

JOB COSTING

Job costing actually applies in environments where work is undertaken according to specific

orders from customers in order to meet their own special requirements. Normally each order is

for a short duration, probably within one month. For example, a customer may request the

manufacture of a single machine to meet the customer‟s own specification. Other examples, say

from service organizations, might be the need for the repair of a vehicle or the preparation of a

set of accounts for a client.

In this respect, the job costing method can also be applied to help monitor the costs of the

internal work done for the benefit of the internal organization itself. For example, job cost sheets

can actually be used in order to collect the costs of property repairs carried out by the

organization‟s own employees or they may be used in the costing of internal capital expenditure

jobs and other services.

JOB COST SHEETS AND DATABASES

The main feature of a job costing system is the use of a job cost sheet or a job card which is a

detailed record used in order to collect the costs of each job. Normally this would be a file in a

11

computerized system but the essential feature is that each job would be given a specific number

which identifies it from all the other jobs. In this respect, costs would be allocated to this

number as they are being incurred on behalf of that specific job. Since the sales value of each

job can also be separately identified, it is then possible also to determine the profit or loss on

each specific job undertaken.

The job cost sheet would therefore record details of the job as it proceeds. Therefore, the items

recorded would include the following:

Job number;

Description of the job; specifications, etc;

Customer details;

Estimated cost, analyzed by cost element;

Selling price, and also the Estimated profit;

Promised delivery date;

Actual costs incurred to date, analyzed by cost element;

Actual delivery date, once the job is completed;

Sales details; eg. Delivery note number, invoice number etc.

For example, a job cost sheet may be prepared for a plumbing job. This job would have been

carried out on the customer‟s own premises. The job cost sheet has a separate section to record

the details of each cost element. There is also a summary section where the actual costs incurred

are compared with the original estimates. This comparison helps managers to control costs and

also to refine their estimating process.

COLLECTING THE DIRECT COSTS OF EACH JOB

Costs relevant to job costing are in a number of categories including the ones summarized below:

(a) DIRECT LABOUR

The correct analysis of labour costs and their attribution to specific jobs depends upon the

existence of an efficient time recording and analysis system. For example, daily or

weekly time sheets may be used to record how each employee‟s time is spent on the job,

using job numbers where appropriate in order to indicate the time spent on each job. In

this respect, the wages cost can also then be charged to specific job numbers or to

overhead costs, if the employee was actually engaged on indirect tasks.

(b) DIRECT MATERIAL

All documentation used to record movements of material within the organization should

actually indicate the job number to which it relates. For example, a Material Requisition

note, which is a formal request for items to be issued from the stores, should at least have

12

a space to record the number of the job for which the material is being requisitioned. In

case any of this material is returned to the stores, them the Material Returned Note should

indicate the original job number which is to be credited with the cost of the returned

material.

Sometimes items of material might be purchased specifically for an individual job,

without the material first being delivered to the general stores and then requisitioned from

the stores for the appropriate job. In this type of situation, the job number must be

recorded on the supplier‟s invoice or on the relevant cash records. This type of recording

will help ensure that the correct job is charged with the cost of the material purchased.

(c) DIRECT EXPENSES

Although direct expenses are not as common as direct material and direct labour costs, it

is still important to analyze them and ensure that they are charged against the correct job

number.

For example, if a machine is hired to complete a particular job, this is a direct expense of

the job. In this respect, the supplier‟s invoice should be coded in order to ensure that the

expense is charged to the appropriate job. On the other hand, if cash is paid, then the

cash book analysis should show the job number which is to be charged with the

appropriate cost.

ATTRIBUTING OVERHEAD COSTS TO JOBS

Overhead costs related to jobs may be divided into categories of Production overheads and also

Non-production overheads.

(a) PRODUCTION OVERHEADS

The successful attribution of production overhead costs to cost units depends on the

existence of well-defined cost centres and appropriate absorption bases for the overhead

costs of each cost centre.

It may be possible to record accurately the units of the absorption base which are

applicable to each job. For example, if machine hours are to be used as the absorption

base, then the number of machine hours spent on each job must be recorded on the job

cost sheet. The relevant cost centre absorption rate can then be applied in order to

produce a fair overhead charge for that specific job.

For example, if the production overhead section of a given job cost sheet shows that the

absorption rate is at K5 000 per labour hour. The labour analysis shows that 9 hours were

13

worked on this particular job, therefore the amount of production overhead absorbed by

this job will be K45 000.

(b) NON-PRODUCTION OVERHEADS

The level of accuracy achieved in attributing costs such as selling, distribution and

administration overheads to jobs will depend on the level of cost analysis which an

organization applies.

Many organizations simply use a predetermined percentage in order to absorb such costs,

based on estimated levels of activity for the forthcoming period.

EXAMPLE

A company uses a predetermined percentage of production cost to absorb distribution

costs into the total cost of its jobs. Based on historical records and an estimate of activity

and expenditure levels in the forthcoming period, they have produced the following

estimates:

Estimated distribution costs to be incurred K133 000

Estimated production costs to be incurred on all jobs K1 900 000

Therefore, predetermined overhead absorption rate for distribution costs will be:

Estimated distribution costs x 100

Estimated production costs on all jobs

K133 000 x 100 = 7% of production costs

K1 900 000

The plumbing company that has produced the job cost sheet uses a predetermined percentage of

5 % of total production cost to absorb administration overhead into job costs.

The use of predetermined rates will normally lead to the problems of under or over absorption of

overhead costs. In this respect the rates should therefore be carefully monitored throughout the

period to ensure that they do not require adjusting to more accurate levels in order to reflect

recent trends in costs and activity relating to that job.

14

QUESTION

Jere Ltd manufactures precision tools to its customers‟ own specifications. The manufacturing

operations are divided into three cost centres, namely: A, B and C.

An extract from the company‟s budget for the forthcoming period shows the following data:

Cost Centre Budgeted Production Basis of Production overhead

Overhead Absorption

K

A 38 500 22 000 machine hours

B 75 088 19 760 machine hours

C 40 964 41 800 machine hours

Job number 075 was manufactured during the period and its job cost sheet reveals the following

information relating to the job:

Direct material requisitioned K6 780.10

Direct material returned to stores K39.60

Direct labour recorded against job number 075:

Cost centre A: 146 hours at K4.80 per hour

Cost centre B: 39 hours at K5.70 per hour

Cost centre C: 279 hours at K6.10 per hour

Special machine hired for this job: hire cost K59.00

Machine hours recorded against job number 075:

Cost centre A: 411 hours

Cost centre B: 657 hours

Price quoted and charged to customer, including delivery K17 200

Jere Ltd absorbs non-production overhead using the following predetermined overhead

absorption rates:

Administration and general overhead 10% of production cost

Selling and distribution overhead 12% of selling price

15

REQUIRED

You are required:

(a) to present an analysis of the total cost and

(b) To prepare a cost and profit analysis attributable to job number 075.

PREPARING LEDGER ACCOUNTS FOR JOB COSTING SYSTEMS

In job costing systems, a separate work in progress account is maintained for each job, as well as

a summary work in progress control account for all jobs worked on in a given period.

QUESTION 1

Jasoni Ltd operates a job costing system. All jobs are carried out on Jasoni‟s own premises and

then delivered to customers as soon as they are completed.

Direct employees are paid K10 per hour and production overhead is absorbed into job costs

using a predetermined absorption rate of K24 per hour. General overhead is charged to the

income statement on completed jobs using a rate of 12 per cent of total production cost.

Details of work done during the latest period are as follows:

Work in progress at the beginning of the period:

Job number 308 was in progress at the beginning of the period.

Job number 308:

Cost incurred up to beginning of the period:

K

Direct material 1 790

Direct labour 960

Production overhead absorbed 2 304

Production cost incurred up to beginning of period 5 054

Activity during the period:

Job numbers 309 and 310 were commenced during the period. The following details are

available concerning all work done this period.

Job number: 308 309 310

Direct materials issued from stores K169 K2 153 K452

Excess materials returned to stores - K23 -

Direct labour hours worked 82 53 28

Status of job at end of period Completed Completed In progress

Invoice value K9 900 K6 870 -

16

Cost of material transferred from job 309 to job 310 K43

Production overhead cost incurred on credit K4 590

General overhead cost incurred on credit K1 312

REQUIRED

(a) Prepare the ledger account for the period for each job, showing the production cost of

sales transferred on completed jobs.

(b) Prepare the following accounts for the period:

(i) Work in progress control;

(ii) Production overhead control;

(iii) General overhead control;

(iv) Overhead under or over absorbed control; and

(v) Income statement.

(c) Calculate the profit on each of the completed jobs.

QUESTION 2

The data below relates to a single accounting period in a jobbing engineering works by China

Ltd.

Extracts from Job Cost Cards

Opening Charged during Closing

WIP Period WIP

K k k

Materials 10 620 32 840 12 630

Labour 15 250 53 260 16 170

Production overheads 10 830 33 520 9 260

The financial accountant supplied the following information relating to the same period:

K

Materials purchased 39 150

Selling & Administration overheads 12 780

Production overheads 30 620

Sales 146 330

The opening stock of material was K9 200. All completed jobs are invoiced immediately to

customers and you are advised that the Cost Department recover selling and administrative

overheads at the rate of 10% of the cost of completed jobs.

17

REQUIRED

Using the above information, you are required:

(a) To write up all the Cost ledger accounts; and

(b) To prepare a Costing Profit and Loss Account for the period,

assuming that the firm operates an interlocking system with separate financial and cost

accounts.

BATCH COSTING

This is a form of costing which applies where a quantity of identical articles are manufactured as

a batch. The most common forms of batch are:

(a) Where a customer orders a quantity of identical items, or

(b) Where an internal manufacturing order is raised for a batch of identical parts, sub-

assemblies or products to replenish stocks.

In general however, the procedures for costing batches are similar to costing jobs. In this case

the batch would be treated as a job during manufacture and the costs collected for that job. On

completion of the batch, the cost per unit can be calculated by dividing the total batch cost by the

number of good units produced.

Batch costing is common in the engineering component industry, footwear and also clothing

manufacture and other similar industries.

The following question shows a typical cost build-up for a batch of similar parts and it actually

illustrates typical job costing procedures and the subsequent calculation of the unit cost and the

appropriate profit.

QUESTION

A company, Moono Ltd manufactures small assemblies to order and has the following budgeted

overheads for the year, based on normal activity levels.

Department Budgeted Overheads Overhead Absorption Base

K

Blanking 18 000 1 500 labour hours

Machining 43 000 2 500 machine hours

Welding 20 000 1 800 labour hours

18

Assembly 15 000 1 000 labour hours

Selling and Administration overheads are 20% of factory cost.

An order for 250 assemblies type X 128, made as Batch 5931, incurred the following costs:

Materials: K3 107

Labour: 128 hours Blanking shop at K10 per hour

452 hours Machining shop at K11 per hour

90 hours Welding shop at K10 per hour

175 hours Assembly shop at K9 per hour.

K525 was paid for the hire of a special X-ray equipment for testing the welds. The time booking

in the machine shop was 643 machine hours.

REQUIRED

Calculate the total cost of the batch, the unit cost and also the profit per assembly if the selling

price was K150 per assembly.

USING ACTIVITY BASED COSTING FOR JOB/BATCH COSTING

Overheads can be charged to jobs or batches by using either traditional labour or machine hour

absorption rates or by using various cost drivers in the Activity Based Costing systems. If all

jobs or batches were much the same and placed similar loads on support activities, there would

be little difference in the costs calculated by either method. Such uniformity is unlikely and jobs

and batches do vary in the loads they place on production facilities and support activities.

As a consequence of this, costs calculated by traditional methods and ABC system are actually

likely to be different. The general effect is that more complex/diverse/small quantity production

will tend to be costed higher using the ABC as compared to traditionally calculated costs.

QUESTION

The following details have been recorded for four (4) batches made in a given period.

Batch A B C D

Output in units 250 60 200 120

Cost per batch K K K K

Direct Material 1 650 750 2 100 900

Direct Labour 9 200 1 520 6 880 2 400

Labour hours per batch 1 150 190 860 300

The total production overhead for the period has been analyzed as follows:

19

K

Machine related costs 14 600

Materials handling & dispatch 6 800

Stores 8 250

Inspection/Quality control 5 850

Set- up 6 200

Engineering support 8 300

50 000

Cost drivers have been identified for the cost pools as follows:

Cost pool Cost driver

Machine costs Machine hours

Materials handling Materials movements

Stores Requisitions raised

Inspection Number of inspections

Set-up No. of set-ups

Engineering support Engineering hours

The following cost driver volumes were recorded for the batches:

Batch A B C D Total

Machine hours per batch 520 255 610 325 1 710

Material movements 180 70 205 40 495

Requisitions 40 21 43 26 130

Inspections 18 8 13 8 47

Set-ups 12 7 16 8 43

Engineering hours 65 38 52 35 190

REQUIRED

From the above details, prepare the following:

(a) The batch and unit costs using the traditional costing based on a labour hour overhead

absorption rate.

(b) The batch and unit costs using the Activity Based Costing (ABC).

(c) Compare the costs in (a) and those in (b).

(d) Comment on the likely position if the firm uses the Cost-plus pricing.

20

SUMMARY POINTS

(a) Job costing is employed where work is done to customer‟s requirements, eg. In a factory

or workshop;

(b) For job costing to be effective, there must be a good system of production control, works

documentation, material and labour booking;

(c) All costs incurred must be charged to the job, usually on to a job cost card.

(d) The job cost cards in total form the firm‟s work-in-progress.

(e) The detail entries to the job cards would be debited in total to the work-in-progress

account.

(f) Prime costs are gathered from labour and material bookings on the shop floor and, in the

case of expenses, from invoice or cash book analysis. Overheads can be charged to jobs

either by the traditional methods using labour or machine hour absorption rates or by

various cost driver rates using the ABC method. At present, overhead attribution by

labour or machine hour rates is more common but this may change in the future if the use

of ABC becomes more widespread.

(g) Batch costing is very similar to job costing and is used where a batch of identical units

are manufactured. Costs are gathered as for job costing and when the batch is completed,

the total cost is divided by the number of good units made in order to establish the unit

cost.

21

UNIT 3

COST CLASSIFICATION AND COST BEHAVIOUR

Cost Accounting

Financial, cost and management accounting

The financial accounts records transactions between the business and its customers,

suppliers employees and owners. The managers of the business must account for the way

in which funds entrusted to them have been utilized and therefore, the records of assets

and liabilities are required as well as a statement of any increase in the total wealth of the

business. This is done by presenting a balance sheet and a profit and loss account

annually.

Cost accounting

Cost accounting involves the application of a comprehensive set of principles, methods

and techniques to the determination and appropriate analysis of costs to suit the various

parts of the organization structure within a business.

Management accounting

Management accounting is a wider concept involving professional knowledge and skill in

the preparation and particularly the presentation of information to all levels of

management in the organization structure. The source of such information is the

financial accounts and cost accounts. The information is intended to assist management

in its policy and decision-making, planning and control activities.

Cost ascertainment

Cost accounting systems are primarily designed to ascertain costs: costs of operating

identifiable sections of the business and the cost of output products of units or service.

The system thus represents a data bank which can be referred to and adapted to suit the

needs of people throughout the organization.

In developing a system, guidelines should be recognized so that the basic objective is not

ignored:

(a) Utility of information – procedures involved in cost accounting should be

examined to confirm that the information provided is of specific, ie. it is

uneconomic to carry out analysis and presentation on the basis that „it may be

useful to someone at some time‟.

22

(b) Accuracy and experience – the cost of obtaining a high degree of accuracy must

be measured against the purpose of the exercise.

(c) Actual cost – The concept is entirely theoretical, since in ascertaining the cost of a

cost centre or cost unit, many estimates will be made based upon experienced

judgement.

(d) Normality – Costs will be used for a variety of purposes et. Settling selling prices

or choosing between alternative production methods. Unless a distinction is made

between normal and abnormal costs, the information may be misleading.

Benefits of cost accounting

(a) Disclose profitable and unprofitable activities;

(b) Identify waste and inefficiency;

(c) Analyse movements in profit;

(d) Estimate and fix selling prices;

(e) Value stocks

(f) Develop budgets and standards to assist planning and control;

(g) Evaluate the cost effects of policy decisions.

Analysis of Costs

Cost units

A cost unit is a unit of product or service in relation to which costs are ascertained. Such

a unit could be measured in form of a litre, metre, kg, tonne etc.

The ascertainment of the cost per cost unit is important for the following reasons:

(a) Making decisions about pricing, acceptance of orders and so on‟

(b) Measuring changes in costs and relative levels of efficiency;

(c) Inventory valuation for financial reporting;

(d) Planning future costs (budgeting and standard costs).

In this respect the process of ascertaining unit costs involves analysis, classification and

grouping of costs.

Cost classification

Classification is a means of analyzing costs into logical groups so that they may be

summarized into meaningful information for management.

23

Elements of cost

The initial classification of costs is according to the elements upon which expenditure is

incurred:

(a) Materials

(b) Labour

(c) Services

Within cost elements, costs can be further classified according to the nature of

expenditure. This is the usual analysis in a financial accounting system eg. raw materials,

consumable stores, wages, salaries, rent, rates and depreciation etc.

Direct and Indirect costs

Direct cost – A direct cost is expenditure which can be economically identified with a

specific saleable cost unit.

Prime cost – Prime cost is the aggregate of direct materials, direct labour and direct

expenses.

Indirect costs – Indirect costs or overheads are expenditure on labour, materials or

services which cannot be economically identified with a specific saleable cost unit.

Direct materials }

Direct labour } Prime cost

Direct expenses } }

} Total cost

Indirect materials } }

Indirect labour } Overhead

Indirect expenses }

In order to ascertain the total cost of a cost unit, indirect costs are allocated to cost centres

and cost centre costs are shared over (absorbed by) cost units.

Functional analysis of cost

Overheads are usually categorized into the principal activity groups:

(a) Manufacturing

(b) Administration

(c) Selling

(d) Distribution

(e) Research

24

In this respect prime costs are usually regarded as being solely related to manufacturing

and so are not classified.

Manufacturing and service industries

Whereas manufacturing industries are concerned with converting raw materials into a

product, service industries do not have a manufactured output, their output consists of

services to a customer.

Cost centres

A cost centre is a production or service location, function, activity or item of equipment

whose costs may be attributed to cost units.

A cost centre is a small part of a business in respect of which costs may be determined

and then related to cost units. A number of departments together would comprise a

function. Thus “a cost centre could be a location, function or item of equipment or a

group or combination of any of these”

COST BEHAVIOUR

Total cost

It has been noted that production cost comprises three elements, namely: materials,

labour and expenses. It can also be noted that production cost includes both fixed costs

and variable costs. It is important to consider the way costs behave in response to

changes in production volume.

Cost behaviour is the way in which costs of output are affected by fluctuations in the

level of activity.

Example

Production

500 units 1 000 units

K K

Sales at K3 per unit 1 500 3 000

Total costs 1 000 1 500

Profit 500 1 500

Average cost per unit K2.00 K1.50

Average unit profit K1.00 K1.50

Total costs have increase by only 50% although production has doubled. This is because

some costs will not rise in relation to the increase in the volume.

25

Example

Suppose the product is widgets and the only costs are as follows:

(a) Rental of a fully equipped factory, at K500 000 per annum;

(b) Raw materials at K1.00 per widget.

Show the manner in which these costs can be shown.

Solution

The way these two types of costs react to producing varying numbers of widgets is as

follows:

(a) Factory rental – a fixed cost

Although production rises, the same rent is payable.

(diagram 1) Showing relationship between total fixed cost and output

Fixed costs, within certain output and turnover limits tend to be unaffected by

fluctuations in the levels of activity.

(diagram 2) Average fixed cost per unit graph

As output increases, unit fixed costs decline.

(b) Raw materials – a variable cost

Every widget has a raw material cost of K1.00, therefore, the cost varies directly

with the level of production.

Variable costs – Variable costs are the costs which tend to vary with the level of

activity.

(diagram 3) Graph showing relationship between total variable cost and output

In the case of variable costs unit cost remains constant irrespective of the level of

output (provided that there are no discounts for bulk purchase).

26

Contribution

If the two types of cost are segregated, the operating statement can be presented in

a different way, as shown below.

Production of widgets

1 unit 500 units 1 000 units

K K K

Sales 3 1 500 3 000

Less: Variable costs (rm) 1 500 1 000

Contribution 2 1 000 2 000

Fixed costs – factory rent 500 500 500

Profit/(loss) (498) 500 1 5 00

The revised presentation is based on the concept that each unit sold contributes a

selling price less the variable cost per unit. Total contribution provides a fund to

cover fixed costs and net profit.

Contribution

Contribution is the sales value less variable cost of sales.

Thus: Sales – variable cost = Contribution

Contribution – Fixed costs = Net profit

As output increases, total unit costs gravitate towards the unit variable cost:

Semi-fixed or step costs

Some costs rise in a series of steps. Large steps (renting a second factory) or

small steps (renting a typewriter) may occur.

(a) If the steps are large, the concept of the relevant range of activity usually

applies ie. only occasionally is a new factory considered and therefore one can

assume the cost to be fixed for the relevant range.

(b) If the steps are small, they may be ignored ie. the cost may be treated as a

variable cost.

27

Semi-variable costs (also referred to as semi-fixed costs)

Semi-variable costs

Semi-variable costs are costs which exhibit the characteristics of both variable

and fixed costs, in that while they increase with output they never fall to zero,

even at zero output

28

UNIT 4

MATERIALS: STOCK RECORDING AND INVENTORY CONTROL

Objective

After studying this module, students will:

Understand the objectives and principles of stock recording;

Have been introduced to Inventory Control;

Distinguish between Perpetual inventory and periodic inventory;

Acquire concepts relating to inventory control and management.

STOCK RECORDING

The Inventory or Stock Control system is in the firm, a basic prerequisite that stock movements

(issues and receipts) are accurately recorded. In addition, the stock record typically shows

various control levels which relate to the Inventory Control system.

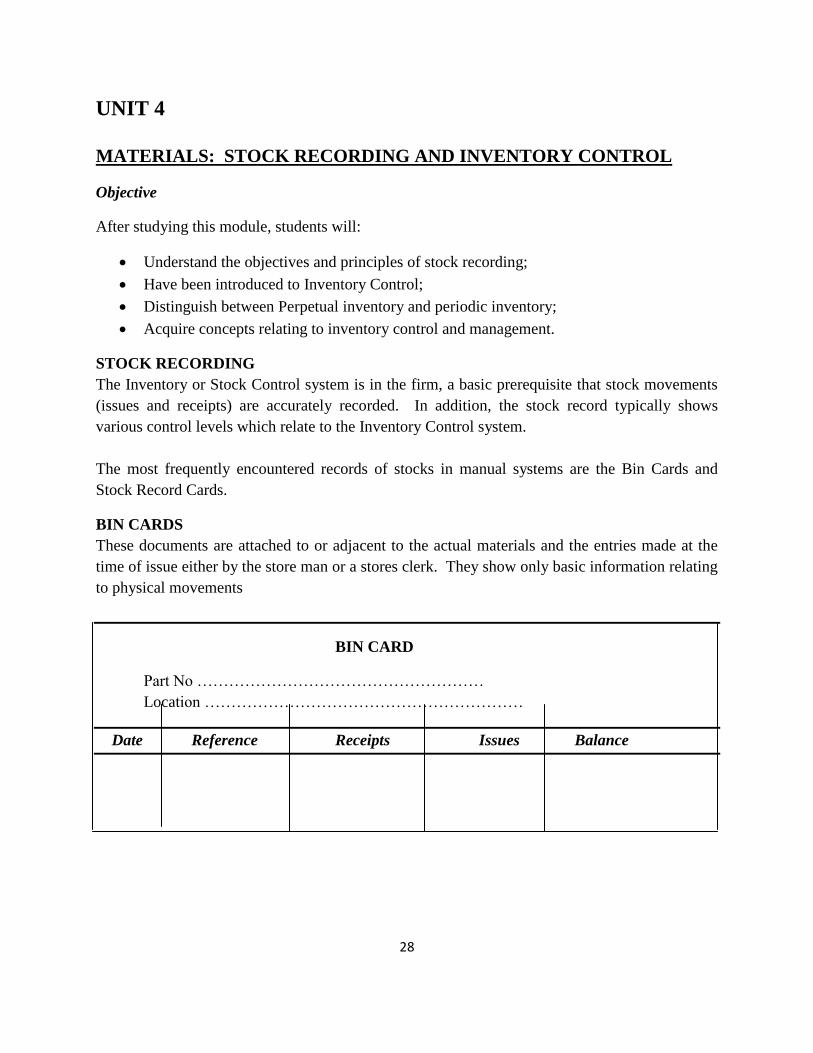

The most frequently encountered records of stocks in manual systems are the Bin Cards and

Stock Record Cards.

BIN CARDS

These documents are attached to or adjacent to the actual materials and the entries made at the

time of issue either by the store man or a stores clerk. They show only basic information relating

to physical movements

BIN CARD

Part No ………………………………………………

Location ……………………………………………………

Date Reference Receipts Issues Balance

29

Notes:

(a) The reference column would be used for inserting the GRN or Material Requisition

number;

(b) The use of Bin cards is declining partly because of the difficulty of keeping them up to

date and partly because of the increasing integration of stock recording and inventory

control procedures, frequently using computers.

PERPETUAL INVENTORY SYSTEM

This system simply means that each issue of receipt the balance is calculated. The total of the

balances represent the stock on hand and the system avoids the necessity for wholesale, periodic

stocktaking. Instead, a continuous stocktaking system must be operated to ensure that the

records accurately reflect actual stocks.

If the records are to be relied upon at all times, stock discrepancies must be investigated

immediately and appropriate corrections made either to the system or to the record or both.

Typical causes of discrepancies between actual stocks and recorded stocks are the following:

(a) Errors caused by incorrect recording and calculation;

(b) Incorrect coding causing the wrong part to be issued and/or wrong card to be altered;

(c) Under or over issues not noted;

(d) Parts and materials returned to the stores and not documented;

(e) Shrinkage, pilferage, evaporation, losses due to breaking bulk, etc;

(f) Loss or non-use of GRNs, material requisitions and other appropriate documentation.

Review questions:

1 Explain the term perpetual inventory

2 What is the use of the document Bin card?

3 Explain the difference between the terms: „stealing‟ and „pilfering‟ in as far as stock

management and control is concerned.

4 Distinguish between an Internal Requisition and an Order form.

30

UNIT 5

MATERIALS – PURCHASING, RECEPTION AND STORAGE

Objectives

After studying this unit, students should be able to:

Understand the principles of materials control;

Be able to describe the main purchasing procedures;

Know the elements of storekeeping and stocktaking;

Understand the advantages and disadvantages of centralized stores; and

Be able to describe the main features of JIT purchasing and JIT production.

THE ESSENTIALS OF MATERIALS CONTROL

The essentials of materials control prior to actual use in production can be summarized as

follows:

(a) Materials of the appropriate quality and specification should be purchased only when

required and appropriately authorized;

(b) The suppliers of materials chosen should represent an appropriate balance between

quality, price and delivery;

(c) Materials should be properly received and inspected;

(d) Appropriate storage facilities should be provided and stock levels physically checked on

a regular basis;

(e) Direct materials used in production should be charged to production on an appropriate

and consistent pricing basis;

(f) Indirect materials used in production and non production departments should be

appropriately charged to the correct cost centre and included in the overheads of the cost

centre;

(g) The documentation, accounting systems and controls at each stage should be well

designed and effective;

(h) Stocktaking must be well organized to ensure that stock quantities on hand are available

when required.

PURCHASING

Due to the large proportion of a firm‟s costs are represented by bought in materials and services,

the purchasing function is of great importance and has become highly specialized.

The responsibility of the purchasing function includes price, quality and delivery all of which are

crucial factors. Late or non-delivery, poor and substandard materials, incorrect specifications,

etc are all likely to have at least as great an impact on profitability as paying an unnecessary high

price.

31

The avoidance of production delays, excessive scrap caused by incorrect materials and the

avoidance of excessive stocks are among the aims of an efficient purchasing function.

Frequently the purchasing function of a group or of a firm with numerous branches is

centralized.

This has many advantages including: larger quantity discounts, uniform standards, possibility of

more continuous supplies in difficult times, etc but there may be disadvantages such as longer

response times; some lack of flexibility in catering for specialized needs and general remoteness

from the scene of operations.

Diagram on: Purchase Requisition Form

PURCHASE REQUISITION

Dept/Job no. Reg No…………………..

Suggested supplier:

Requested by:

Latest Date Required:

Quantity Code No. Description Estimated costs

Units K

Authorized Signature:

PURCHASING PROCEDURES

The purchasing procedure follows the following sequence of steps:

Search for possible and suitable suppliers by using the various sources of information;

Request for tenders from the possible suppliers;

32

Receive the various quotations from the suppliers;

Select the suitable supplier and

Submit the Purchase Order from the chosen supplier.

Diagram on: Purchase Order Form

PURCHASE ORDER

Purchase Order Ref:

To: Address of please deliver to the above address

supplier Ordered by………………..

Passed + checked by………………..

Total order value K…………………..

Qty Description Code Unit price Total

K K

Total cost

Signature ……………..

RECEPTION AND INSPECTION PROCEDURES

The procedure for receiving the ordered goods is as follows:

Receipt of goods in the Materials Reception;

Quantities received are checked and the Goods Received Note is raised by the receiving

firm;

Details of the Goods Received Note are checked against the Purchase Order to ensure

that they are in agreement in as far as quality, quantity and size are concerned;

On satisfaction of the above, the goods are taken into the Stores and the GRN and or

Inspection Note is then signed for approval

33

Diagram on Goods Received Note (GRN)

GOODS RECEIVED NOTE

Date:………………… Time:………………….

Our order No……………..

Supplier and supplier’s advice note No………….

Qty Code No. Description

Condition Goods Received…………………………………………

Name of Receiver……………………………………………………

Signature…………………………………………………..

STORE KEEPING

Storekeeping is an important function and can make a substantial contribution to efficient

operations. Storekeeping includes the following activities:

(a) Efficient and speedy issue of required materials, tools etc;

(b) Receipt of parts and materials from the Goods Reception (ie. External items) and from

Production (ie, internal items);

(c) Organizing storage in logical sequences, thus ensuring items can be found speedily, that

all items can be precisely identified and storage space is used effectively;

(d) Organizing Stock Checks either on a continuous or a periodic basis so as to be able to

provide accurate stock figures when required;

(e) Protecting items in the Stores from damage and deterioration;

(f) Securing the stores from theft, fire and pilfering.

34

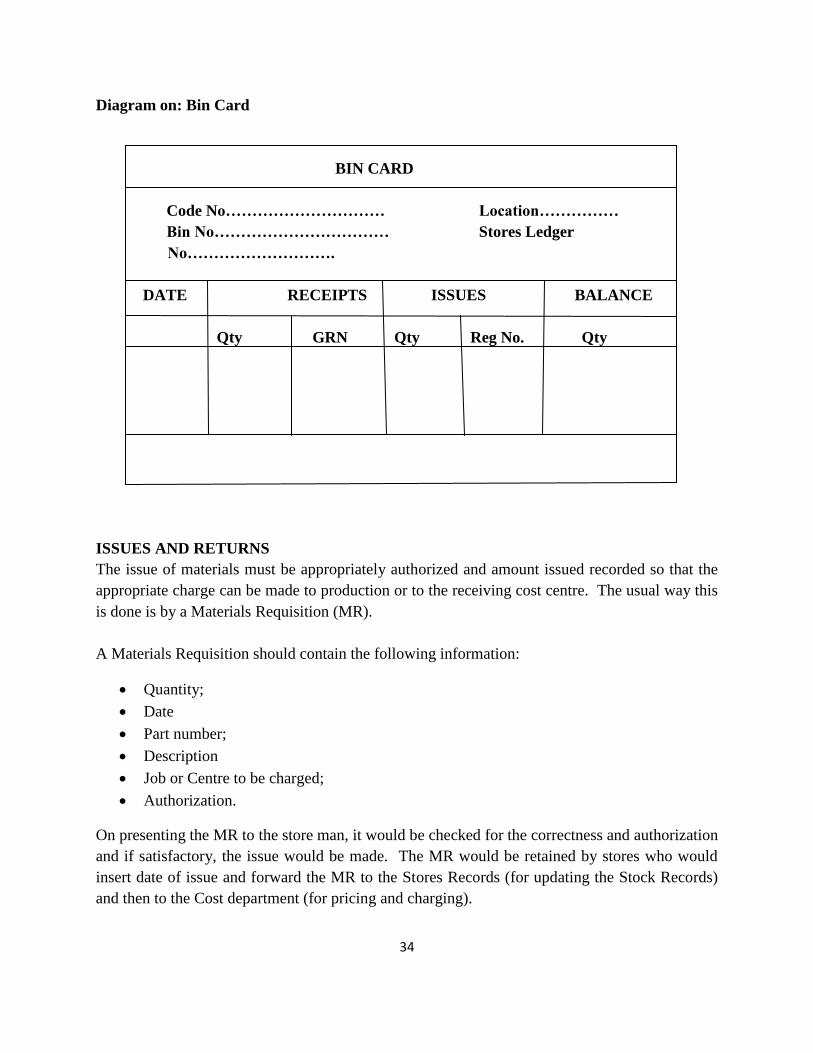

Diagram on: Bin Card

BIN CARD

Code No………………………… Location……………

Bin No…………………………… Stores Ledger

No……………………….

DATE RECEIPTS ISSUES BALANCE

Qty GRN Qty Reg No. Qty

ISSUES AND RETURNS

The issue of materials must be appropriately authorized and amount issued recorded so that the

appropriate charge can be made to production or to the receiving cost centre. The usual way this

is done is by a Materials Requisition (MR).

A Materials Requisition should contain the following information:

Quantity;

Date

Part number;

Description

Job or Centre to be charged;

Authorization.

On presenting the MR to the store man, it would be checked for the correctness and authorization

and if satisfactory, the issue would be made. The MR would be retained by stores who would

insert date of issue and forward the MR to the Stores Records (for updating the Stock Records)

and then to the Cost department (for pricing and charging).

35

The store man must ensure that the MR is amended when the issue cannot be made exactly as the

original request, eg. where only a part issue is made or an alternative material is acceptable when

that originally requested is unavailable.

The procedure for goods returned to store is similar to that outlined above except that the

document involved is termed a Material Return Note, and of course, the goods are taken into the

stores rather then issued.

STORAGE – STOCKTAKING

There are two approaches stocktaking: namely, Periodic stocktaking and also Continuous

stocktaking.

Periodic stocktaking

The objective of periodic stocktaking is to find out the physical quantities of materials of all

types (raw materials, finished goods, WIP etc) at a given date.

This is a substantial task even in a modest organization and becomes a difficult if not impossible

task in a large firm. The following factors need to be considered in as far as stock taking is

concerned:

(a) Adequate numbers of staff should be available who should receive clear and precise

instructions on the procedures;

(b) Ideally the stock take should be done at a weekend or overnight so as not to interfere with

production;

(c) The stock take should be organized into clearly defined physical areas and the checkers

should count or estimate all materials in the area;

(d) Adequate technical assistance should be available to identify materials, part numbers etc.

Far greater errors are possible because of wrong classification than wrong counting;

(e) Greater care should be taken to ensure that only valid stock items are included and that all

valid items are checked;

(f) The completed stock sheets should have random, independent checks to verify their

correctness;

(g) The quantities of each type of material should be checked against the stock record to

expose any gross errors which may be due to stock taking errors or faults or errors in the

recording system. Small discrepancies are inevitable;

(h) The pricing and extension of the Stock Sheets, where done manually, should be closely

controlled. Frequently the pricing and value calculations are done by computer, the only

action necessary being to input quantities and stock and part numbers.

36

Diagram on: Stores Ledger Card

STORES LEDGER CARD

Materials………………………………… Maximum Qty………………

Code……………………………… Minimum Qty……………….

DATE RECEIPTS ISSUES BALANCE

Qty Unit price AmountQty Unit price Amount Qty Amount

K K K K K

Continuous Stocktaking

In order to avoid some of the disruptions caused by periodic stocktaking and to be able to use

better trained staff, many organizations operate a system whereby a proportion of stock is

checked daily so that over the year all stock is checked at least once and many items, particularly

the major value or fast moving items, would be checked several times. Where continuous

stocktaking is adopted, it is invariably carried out by staff independent from the storekeepers.

Note:

Continuous stocktaking is absolutely essential when an organization uses what is known as the

Perpetual Inventory System. This is a stock recording system whereby the stock balance is

shown on the record after every stock movement, either issue or receipt. With this system, the

balances on the stock record represent the stock on hand and balances would be used in monthly

and annual accounts as the closing stock. Continuous stocktaking is necessary to ensure that the

perpetual inventory system is functioning correctly and that minor stock discrepancies are

corrected.

STORAGE – CENTRALIZATION Vs DECENTRALIZATION

There is no conclusive answer as to whether there should be a centralized stores or several stores

situated in branches or departments. Each system has its advantages and disadvantages as

indicated below.

37

Advantages of Centralization

(a) Lower stock on average;

(b) Less risk of duplication;

(c) Higher quality staff may be usefully employed to specialize in various aspects of

storekeeping;

(d) Closer control is possible on a central site;

(e) Possibly more security from pilferage;

(f) Some aspects of paperwork may be reduced, eg. purchase requisitions;

(g) Stocktaking is facilitated;

(h) Likelihood that more advanced equipment will be viable, eg. materials handling, visual

displays.

Disadvantages of Centralization

(a) Less convenient for outlying branches/departments;

(b) Possible loss of local knowledge;

(c) Longer delays possible in obtaining materials;

(d) Greater internal/external transport costs in fetching and carrying materials.

JUST-IN-TIME (JIT) SYSTEMS

JIT systems were developed in Japan, and are considered as one of the main contributions to

some manufacturing successes.

The aim of JIT systems is to produce the required items, of high quality, exactly at the time when

such items are required. JIT systems are characterized by the pursuit of excellence at all stages

with a climate of continuous improvement.

A Just In Time environment is characterized by the following features:

A move towards zero inventory;

Elimination of non-value added activities;

An emphasis on perfect quality, ie zero defects;

Short set-ups;

A mover towards a batch size of on;

100% on-time deliveries;

A constant drive for improvement;

Demand-pull manufacture.

It is this latter characteristic which gives rise to the name of Just-in-Time. Production only takes

place when there is actual customer demand for the product so JIT works on a pull-through basis

which means that products are not made to go into stock. Contrast this with the traditional

38

manufacturing approach of production-push where products are made in large batches and move

into stores for stock keeping.

Definition

Just-In-Time (JIT) – System whose objective is to produce or to procure products or components

as they are required by a customer or for use, rather than for stock. JIT pull system which

responds to demand, in contrast to a push system in which stock act as buffers between the

different elements of the system such as purchasing, production and sales.

JIT PURCHASING

This seeks to match the usage of materials with the delivery of materials from external suppliers.

This means that material stocks can be kept at near zero levels.

For JIT purchasing to work requires the following:

Confidence that suppliers will deliver exactly on time;

That suppliers will deliver materials of 100% quality so that there will be no rejects,

returns and consequent production delays.

The reliability of suppliers of suppliers is all-important and JIT purchasing means that the

company must build up close working relationships with their suppliers. This is usually

achieved by doing more business with fewer suppliers and placing long term purchasing orders

in order that the supplier has assured sales and can plan to meet the demand.

JIT PRODUCTION

JIT production works on a demand-pull basis and seeks to eliminate all waste and activities

which does not add value to the product being produced. As an example, consider the lead times

associated with making and selling a product. These include the following:

Inspection time;

Transport time;

Queuing time;

Storage time;

Processing time

Of these, only processing time adds value to the product whereas all the others add cost, but not

value. The ideal for JIT systems is to convert materials to finished products with a lead time

equal to processing time so eliminating all activities which do not add value. A way of

emphasizing the importance of reducing throughput time if to express the above lead times as

follows:

THROUGHPUT TIME = VALUE ADDED TIME + NON VALUE ADDED TIME

39

BENEFITS AND PROBLEMS FROM USING JIT

Successful users of JIT systems are making substantial savings. These arise from numerous

areas including the following:

(a) Lower investment required in all forms of inventory;

(b) Space savings from the reduction in inventory and improved layouts;

(c) Greater customer satisfaction resulting from higher quality better deliveries and greater

product variety;

(d) The buffers provided by traditional inventories masked other areas of waste and

inefficiency. Examples include co-ordination and work flow problems, bottlenecks,

supplier unreliability and so on. Elimination of these problems improves performance

drastically;

(e) The flexibility of JIT and the ability to supply small batches enables companies to

respond more quickly to market changes and to be able to satisfy market niches.

As would be expected, there are often problems in implementing JIT systems. JIT does not

necessarily reduce inventories in total. One firm may reduce their inventory but this is often at

the expense of others in the supply chain. Component and material suppliers need to keep stocks

in case of rush orders because there are usually penalty clauses in the event of later delivery.

REVIEW QUESTIONS

1 Invariably goods, services and the supply of materials are obtained by the use of a

Purchase Order. Design the layout of a Purchase Order, showing what essential

information the order should contain.

2 Give six (6) advantages of continuous stocktaking.

3 Give five (5) reasons why stocktaking errors occur.

4 Give five (5) differences between JIT Purchasing and the conventional purchasing.

5 Distinguish between centralized storages system and the departmental storage system.

40

UNIT 6

INVENTORY CONTROL

Learning objectives

After covering this module, students should be able to:

Define the Economic order quantity model;

Define Reorder Level

Define Lead time

Compute and explain the meaning of Economic Order Quantity (EOQ).

Identify the different types of stock related costs and control such costs.

Inventory control can be defined as the system used in a firm to control the firm‟s investment in

stock. This includes; the recording and monitoring of stock levels, forecasting future demands

and deciding when and how many to order.

The overall objective of inventory control is to minimize, in total, the costs associated with stock.

These costs can be categorized into three groups, namely:

Carrying costs

(a) Interest on capital invested in stocks;

(b) Storage charges (rent, lighting, heating, refrigeration and air conditioning);

(c) Stores staffing, equipment, maintenance and running costs;

(d) Material handling costs;

(e) Audit, stocktaking, stock recording costs;

(f) Insurance and security;

(g) Deterioration and obsolescence;

(h) Pilferage, evaporation and vermin damage.

Costs of obtaining Stock (Ordering costs)

(a) Clerical and administrative costs of Purchasing, Accounting and Goods Reception;

(b) Transport costs;

(c) Where goods are manufactured internally, the set-up and tooling costs associated with

each production run plus the planning, production control costs associated with the

internal order.

Stock out Costs (Costs of being without Stock)

(a) Lost contribution through the lost sale caused by stock out;

(b) Loss of future sales because customers may go elsewhere;

(c) Costs of production stoppages caused by stock outs of WIP and raw materials;

41

(d) Extra costs associated with urgent, often small quantity, replenishment orders.

Some of the above items may be difficult to quantify, particularly stock out costs, but

nevertheless may be of considerable importance. The avoidance of stock out costs is the basic

reason why stocks are held in the first place.

INVENTORY (STOCK) CONTROL TERMINOLOGY

Some common inventory control items are defined below as follows:

(a) Lead or procurement time – The period of time between ordering (externally or

internally) and replenishment, ie when the goods are available for use.

(b) Economic Order Quantity (EOQ) or Economic Batch Quantity (EBQ) – this is a

calculated reorder quantity which minimizes the balance of cost between carrying costs

and ordering costs.

(c) Buffer Stock or Minimum Stock or Safety Stock – A stock allowance to cover errors in

forecasting the lead time or the demand during the lead time.

(d) Maximum Stock Level – A stock level calculated as the maximum desirable which is

used as an indicator to management to show when stocks have risen too high.

(e) Reorder Level – The level of stock (usually free stock) at which a further replenishment

order should be placed. The reorder level is dependent on the lead time and the rate of

demand during the lead time.

(f) Reorder Quantity – The quantity of the replenishment order – frequently, but not always,

the EOQ.

42

CALCULATING CONTROL LEVELS

The common methods of calculating the major control levels include the following:

Reorder Level;

Minimum Level;

Maximum Level

Number of Orders = D/EOQ

Average inventory = EOQ/2

Total Carrying Cost = Average inventory *Carrying cost

Total Ordering Cost = Number of Orders *Ordering Cost

Total Inventory Cost = Total carrying Cost + Total Ordering Cost

QUESTION

The following information was collected from the books of Chalo Ltd who maintain storage

facilities for storage control purchases:

Average usage 100 units per day

Minimum usage 60 units per day

Maximum usage 130 units per day

Lead time 20 – 26 days

EOQ (previously calculated) 4 000 units

REQUIRED

From the above details, calculate the following:

(a) Reorder level;

(b) Minimum stock level;

(c) Maximum stock level

Notes:

(a) These are the normal control levels encountered in basic inventory control systems.

Each time an entry is made, a comparison would be made between actual stock and the

control level;

(b) Reorder level is a definite action level; maximum and minimum levels are levels at which

management would be warned that a potential danger may occur.

(c) The minimum level is set so that management are warned when usage is above average

and buffer stock is being used. There may be no danger, but the situation needs

watching.

(d) The maximum level is set so that management will be warned when demand is the

minimum anticipated and consequently stock may rise above maximum intended.

43

(e) The calculation of control levels is done relatively infrequently in manual systems, but in

a computer based system calculations would take place automatically to reflect current

and forecast future conditions.

THE ECONOMIC ORDER QUANTITY (EOQ) MODEL

The EOQ is a calculated order quantity which minimizes the balance of cost between ordering

and carrying costs.

In order to calculate a basic EOQ, certain assumptions are necessary and these include the

following:

(a) That there is a known, constant stock holding cost;

(b) That there is a known, constant ordering cost;

(c) That rates of demand are known;

(d) That there is a known, constant price per unit;

(e) That replenishment is made instantaneously, ie the whole batch is delivered at once.

The above assumptions are wide ranging and it is unlikely that all could be made in practice.

Nevertheless, the EOQ calculation is a useful starting point in establishing an appropriate reorder

quantity.

The EOQ formula is given below and its derivation given in Quantitative techniques.

EOQ =

Where: Co = Ordering cost per order

D = Demand per annum

Cc = Carrying cost per item per annum

QUESTION

The following information was collected from a manufacturing organization. The forecasted

demand is 1 000 units per month, the ordering cost is at K350 per order. The units cost at K8

each and it is estimated that the carrying costs are 15% per annum.

REQUIRED

From the above details, calculate the Economic Order Quantity for this manufacturing

organization.

Notes:

44

(a) It will be seen that it is necessary to bring the factors involved to the correct time scale;

(b) The EOQ formula give above is for replenishment in one batch. Where replenishment

takes place gradually, for example where the items are manufactured internally and

placed into stock as they are made, the formula changes slightly as follows:

EOQ (with gradual replenishment) =

Where: R = Replenishment rate per annum

SUMMARY

(a) The two most common stock records found in traditional systems are the Bin card and

the Stock Record Card (or its computer equivalent);

(b) The Bin card, where used, shows Issues, Receipts and Physical Balance;

(c) As well as physical information the Stock Record Card shows the Free Stock balance and

the major control levels; Reorder level Maximum level, and Minimum stock level;

(d) The perpetual inventory system means that after each stock movement, the balance on

hand is calculated. To ensure that the records keep in line with actual stocks, continuous

stocktaking is carried out;

(e) Inventory control is the system used in a firm to control the investment in stocks and has

the overall objective of minimizing in total the three costs associated with stocks:

carrying costs, ordering costs and stock out costs;

(f) Reorder level is an action point, maximum and minimum stock levels are management

indicators;

(g) The EOQ is a calculated order quantity to help minimize the balance of ordering and

carrying costs.

POINTS TO NOTE

(a) Keeping stock records aligned with actual stocks is a major practical problem which is

rarely solved completely successfully;

(b) The inventory control system described above is the Reorder Level System, sometimes

known as the Two Bin System;

(c) An alternative control system is known as the Periodic Review System where all stock

levels are reviewed at fixed intervals and replenishment orders issued. These orders

would be based on estimated usage, lead time etc and would not be the EOQ used in the

Reorder Level System;

45

(d) The newer approaches to production, such as the JIT, challenge the philosophy behind

the traditional EOQ model. JIT systems seek to eliminate stocks entirely and where

possible, move towards a batch size of one.

This applies especially to Work in Progress stocks. In effect the JIT philosophy does not

accept that ordering cost and holding costs are fixed. JIT systems continually seek to

reduce both costs. In particular because of the close links with suppliers, ordering costs

reduce dramatically and thus the EOQ and total annual costs are reduced.

When ordering costs are low and holding costs are high the resulting EOQ drives firms to

consider adopting the JIT systems.

REVIEW QUESTIONS

1 An investigation into stores procedures and record keeping showed that for Part

No. Y292 the physical stock differed from the Bin Card and also from the Record

Card kept in the works office which did not agree with the Bin Card.

Give reasons for the differences.

2 What is the relationship between Perpetual Inventory Systems and Continuous

Stocktaking?

3 Calculate the Economic Order Quantity when demand is 25 per working day,

ordering costs are K150.00 per order, the items do cost K3.00 each and carrying

costs are at 12% per year. There are 250 working days in a year.

46

UNIT 7

COSTING OF MATERIALS

Learning Outcomes:

After covering this lecture, students should be able to:

Explain the distinction between direct and indirect material costs;

Describe the documentation used for recording material costs;

Calculate the cost of materials used and the value of closing stocks using the FIFO, LIFO

and the Weighted Average Cost methods of stock pricing;

Account for materials costs in the stores account in the cost ledger; and

Calculate material input requirements and control measures where wastage occurs.

DIRECT AND INDIRECT MATERIALS

In cost accounting, materials are commonly classified as either direct materials or indirect

materials.

Direct materials – These are the materials that can be directly attributed to a unit of production,

or a specific job, or a service provided directly to a customer.

In a manufacturing business, direct materials are therefore the raw materials and components that

are directly input into the products that the organization makes . For example, the various

components that make up an aeroplane are the direct materials of the aeroplane.

Indirect materials - These are the other materials that cannot be directly attributed to a unit of

production.

An example of indirect materials might be the oil used for the lubrication of production

machinery. This is a material that is used in the production process but it cannot be directly

attributed to each unit of finished product.

In a manufacturing business, the cost of direct materials can be charged directly to the production

department that uses the materials. In a jobbing business or a contracting business, direct

materials costs are charged directly to the job or contract for which they are used.

The costs of indirect materials are charged to the cost centre that requisitions them from the

stores department and then uses them.

47

PROCEDURES AND DOCUMENTATION FOR MATERIALS

The stores department is responsible for the receipt, storage and issue of materials and

components to the using units/departments.

Receipts of materials into the store – When materials are received from suppliers, they

are normally delivered to the stores department. The stores personnel must then check

that the goods delivered are the ones that have been ordered, in the correct quantity, of

the correct quality and in good condition.

Storage - Once the materials have been received, they must be stored until required by

the user departments.

Issue of materials from store – When cost centres require materials, they submit a

requisition for the materials to the stores department.

Recording Receipts and Issues - Receipts of materials into store and issues of materials

must be controlled and recorded. Generally the responsibility for recording receipts and

issues of materials is divided between the stores department and also the costing

department.

Each of these departments could maintain its own separate stock records, although there

should ideally be one integrated stock control system. The store department should

monitor the quantities of materials received and also issued and ensure the safety and

security of the physical stocks. The costing department is responsible for recording the

cost of materials received into stores and for putting a value to the cost of direct and

indirect materials issued from stores.

PROCEDURES AND DOCUMENTATION FOR RECEIPTS OF MATERIALS

It is useful to have an overview of the departments that are involved in the purchasing and stores

procedures:

Stores Department – Notifies the purchasing department of the need to buy materials, using a

Purchase Requisition or Stock Order form.

Purchasing Department – Orders goods for external supplier using the Purchase Order.

External Supplier – Delivers goods to the stores department. The goods are accompanied by a

Delivery Note. The external supplier also sends a Purchase Invoice to the accounts department,

asking for payment for the goods supplied.

48