under the microscope -...

TRANSCRIPT

UNDER THE MICROSCOPE

OC

T. 2

012

A NATIONAL BANKRUPTCY SERVICES PUBLICATION

Considerations regarding “good faith” and lien

stripping

Progress report on the National Mortgage

Settlement

How the CFPB’s Newly Proposed Rules Will Affect Mortgage Servicers

FORTUNATELY, WE HAVE THE MOST COST EFFECTIVE, COMPLIANT BANKRUPTCY SOLUTIONS FOR KEEPING EVERYTHING IN CHECK.

Since 1987, we’ve focused on helping companies deal with the maze of bankruptcy cases by consistently increasing recovery results, reducing loan losses, and improving the bottom-line performance of their bankruptcy portfolio. Contact NBS and let us help you stay ahead of the game.

NATIONAL BANKRUPTCY SERVICES

9441 LBJ Freeway, Suite 250 Dallas, TX 75243

214.550.4204NBSdefaultservices.com

RESIDENTIAL MORTGAGE LENDERS AUTOMOBILE FINANCE COMPANIES BANKS, CREDIT UNIONS, & FINANCIAL INSTITUTIONS CONSUMER LENDING ORGANIZATIONS PORTFOLIO SERVICERS, OWNERS & INVESTORS

NB

S. H

AN

DL

ING

BA

NK

RU

PTC

Y C

AS

ES

SIN

CE

19

87.

DA

TA

ISS

UE

SPA

GE

1F

OC

US

THE LEDGEROCTOBER 2012

Larry BuckleyCEO [email protected]

Luke MadoleChief Legal Officer [email protected]

Brad CloudCOO [email protected]

Dave [email protected]

Contributing Writers Braden Barnes, Hilary Bonial, Felicia Burda, N. Robert Henry, Elijah Metcalf, Wes Wiley

Magazine Design HW Creative, HWideas.com

THE LEDGER is a National Bankruptcy Services publication. © 2012 National Bankruptcy Services All Rights Reserved

9441 LBJ Freeway, Suite 250 Dallas, TX 75243

NBSDEFAULTSERVICES.COM « APRIL 2012

FORTUNATELY, WE HAVE THE MOST COST EFFECTIVE, COMPLIANT BANKRUPTCY SOLUTIONS FOR KEEPING EVERYTHING IN CHECK.

Since 1987, we’ve focused on helping companies deal with the maze of bankruptcy cases by consistently increasing recovery results, reducing loan losses, and improving the bottom-line performance of their bankruptcy portfolio. Contact NBS and let us help you stay ahead of the game.

NATIONAL BANKRUPTCY SERVICES

9441 LBJ Freeway, Suite 250 Dallas, TX 75243

214.550.4204NBSdefaultservices.com

RESIDENTIAL MORTGAGE LENDERS AUTOMOBILE FINANCE COMPANIES BANKS, CREDIT UNIONS, & FINANCIAL INSTITUTIONS CONSUMER LENDING ORGANIZATIONS PORTFOLIO SERVICERS, OWNERS & INVESTORS

The information in this publication is not a substitute for the advice of an attorney and is not legal advice.

A NATIONAL BANKRUPTCY SERVICES PUBLICATION

IN THIS ISSUE

ISSUES

A review of the reforms outlined in the annual report from the

Financial Stability Oversight Council

2

FOCUS

An interview with Luke Madole, who recently joined NBS as the Chief

Legal Officer.

26

WO

RK

ING

TO

WA

RD

RE

FO

RM

» B

Y F

EL

ICIA

T. B

UR

DA

PA

GE

3D

ATA

ISS

UE

SF

OC

US

DATA

A look at bankruptcy data from across the nation, with detailed

state-by-state breakdowns of filings.

22

TABLE OF CONTENTS

» WORKING TOWARD REFORM

Annual Report of the Financial Stability Oversight Council 2» UNDER THE MICROSCOPE

How the CFPB’s Newly Proposed Rules Will Affect Mortgage Servicers 6» STRIPPING IN GOOD FAITH

In re Lepe: 9th Circuit BAP considers “Good Faith” and Lien Stripping 10» PROGRESS REPORT FROM THE MONITOR OF THE

NATIONAL MORTGAGE SETTLEMENT

Homeowners Seeing Benefits from National Mortgage Settlement? 14» JOSEPH A. SMITH SPEAKS

Monitor’s Remarks at Annual Meeting of NACTT 18» BY THE NUMBERS

Taking a look at the state of bankruptcy 20» HOT SEAT

Luke Madole, Chief Legal Officer, NBS 24» ALWAYS DO THE RIGHT THING

Cheating and Organizational Compliance 26

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

2

THE LEDGER » NBSDEFAULTSERVICES.COM

ANNUAL REPORT OF THE FINANCIAL STABILITY OVERSIGHT COUNCIL

BY FELICIA T. BURDA

According to an article in the evening edition of the Wall Street Journal on September 13, published after this piece was wr i t ten , the Government Accountability Office, the investigative arm of Congress, recently reported that the Financial Stability Oversight Council is lacking in accountability, transparency and collaboration with key financial regulators. This report has spurred Republican criticism and put the Council and Treasury Secretary Timothy Geithner on the defensive, reaffirming their firm commitment to openness and transparency for the relatively new start-up organization. The report also included criticism of the related smaller entity, the Office of Financial Research.

WORKING TOWARD REFORM

NOTE:

WO

RK

ING

TO

WA

RD

RE

FO

RM

» B

Y F

EL

ICIA

T. B

UR

DA

PA

GE

3D

ATA

ISS

UE

SF

OC

US

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

4

One of the many Congressional reactions to the recent housing and financial crisis was enact-ment of the Dodd-Frank Wall Street Reform

and Consumer Protection Act. The Dodd-Frank Act, among other things, established the Financial Stability Oversight Council. The charge of the Council is three fold:• To identify risks to the financial stability of the Unit-

ed States that could arise from the material financial distress or failure, or ongoing activities, of large, interconnected bank holding companies or nonbank financial companies, or that could arise outside the financial services marketplace.

• To promote market discipline, by eliminating expec-tations on the part of shareholders, creditors, and counterparties of such companies that the U.S. gov-ernment will shield them from losses in the event of failure.

• To respond to emerging threats to stability of the U.S. financial system.1

The Council has ten voting members and five nonvot-ing members, consisting of federal financial regulators and state regulators, as well as an independent insur-ance expert appointed by the President and confirmed by the Senate. Voting members include: the Secretary of the Treasury, who also serves as the Chairperson of the Council; the Chairman of the Board of Governors of the Federal Reserve System; the Comptroller of the Cur-rency (OCC); the Director of the Bureau of Consumer Financial Protection (CFPB); the Chairman of the Secu-rities and Exchange Commission (SEC); the Chairperson of the Federal Deposit Insurance Corporation (FDIC); the Chairperson of the Commodity Futures Trading Commission; the Director of the Federal Housing Fi-nance Agency (FHFA); the Chairman of the National Credit Union Administration; and the appointed insur-ance expert. The nonvoting members, serving in an advisory capacity, are: the Director of the Office of Fi-nancial Research; the Director of the Federal Insurance Office; a state insurance commissioner; a state banking supervisor; and a state securities commissioner.

The Dodd-Frank Act requires the Council to issue an annual report, which the voting members approved unanimously on July 18, 2012. The annual report in-

cluded recommendations for housing finance reforms, both with respect to the housing finance system and mortgage servicing standards and servicer compensa-tion.2 This article summarizes those recommendations. Much more detail and analysis behind these recommen-dations, as well as other recommendations, can be found in the over-200 page report.

REFORMS TO THE HOUSING FINANCE SYSTEMNoting that the U.S. housing finance system has re-quired extraordinary support from the federal govern-ment over the past several years, the Council discuss-es some of the progress made in the last year by member agencies to create a framework for housing reform that increases private sector involvement, while still protecting consumers and reducing tax ex-posures. Specifically, the FHFA released a plan in early 2012 for Freddie Mac and Fannie Mae (GSEs) to develop approaches to infrastructure that could sup-port any path toward a broad housing reform. Pursu-ant to such plan, the GSEs’ risk profile would be re-duced and incentives for the private sector would be increased to absorb mortgage credit risk with better pricing and enhanced risk sharing. All the while, the GSEs would still have a role in mitigating credit losses and providing foreclosure alternatives.

The Council notes the progress of the CFPB to imple-ment rules pursuant to the Dodd-Frank Act to ensure that lenders reasonably determine consumers’ ability to re-pay based upon verified information. For more on this, please see N. Rob Henry’s feature article regarding recent rule proposals by the CFPB on page 6.

As well, the Council observes that member agencies have also been working to promote more efficient mar-kets for residential mortgage-backed securities (RMBSs). Specifically, the SEC is considering appropri-ate disclosure rules to provide participants in the pri-vate market with more transparent information regard-ing the underlying assets of RMBSs. Other member agencies have set goals for enhanced clarity and guide-lines regarding asset-backed securities, including the securitization of residential mortgages.

PA

GE

5

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

WO

RK

ING

TO

WA

RD

RE

FO

RM

» B

Y F

EL

ICIA

T. B

UR

DAThe Council recognizes that all these steps are important

in encouraging private capital to incur additional mortgage credit risk. The Council believes, however, that additional certainty is necessary for the future of housing finance infra-structure and policy issues in order to promote even further the return of private capital. The Council notes specifically that no broadly agreed-upon standards regarding the qual-ity and consistency of mortgage underwriting exist. Also, foreclosure practices continue to be non-uniform across the states. Uncertainty remains regarding the liability of a mort-gage securitizer if a loan fails to conform to representations and warranties regarding specific characteristics of the loan.

Noting that the U.S. Treasury and Department of Housing and Urban Development (HUD) continue to evaluate options for the government’s role in a privatized system of housing finance, the Council rec-ommends that work con-tinue to “develop a long-term housing finance reform framework that supports the central role of private capital and the emphasis on consumer and investor protections in any future housing finance system. It is critical for the Council members, HUD, and Congress to continue their work to develop standards and best practices. . . [I]t is critical to address the weaknesses that became evident in the recent housing crisis.”3

MORTGAGE SERVICING STANDARDS AND SERVICER COMPENSATION REFORM“The Council continues to focus on the need for national mortgage servicing standards and servicer compensation reform to strengthen confidence in the mortgage market. The lack of clear servicing standards in the period leading up to the housing crisis led to problems in assisting borrowers to avoid foreclosure, inappropriate servicing practices, and ad-ditional losses for investors.”4

After setting the tone, the Council summarizes progress in this area thus far. Federal prudential banking regulators, HUD, FHFA and the Treasury formed an inter-agency working group to address fair, clear, and uniform national servicing

standards in early 2011. The CFPB joined this working group in July 2011. Well known, there had been an earlier review by the Federal Reserve, OCC, and FDIC of the major servicers that resulted in the consent orders now being implemented. Also in the first half of 2011, FHFA announced its “Servicing Align-ment Initiative” for the GSEs, producing consistent protocols for servicing mortgages from the onset of delinquency. In September 2011 the FHFA’s “Joint Mortgage Servicing Com-pensation Initiative” released a document discussing two alternative compensation structures for servicing single-family mortgages and sought comments. One proposal would establish a reserve account to increase servicing capacity in stressful times. The other would create a new “fee-for-service” structure of compensation. Last but not least, there was the “national mortgage settlement” of February 2012 by which

the federal government and 49 states reached a $25 billion settlement with the five largest mortgage servicers in the United States.

The Council recom-mends that the FHFA, HUD, CFPB and other

agencies “develop comprehensive mortgage servicing stan-dards that require consistent and transparent processes for consumers and promote efficient alternatives to foreclosure where appropriate. In addition, the Council recommends continued efforts to implement compensation structures that align the incentives of mortgage servicing with those of bor-rowers and other participants in the mortgage market.”5

Overall, the Council’s recommendations are very general and not specific, which perhaps is expected since the Coun-cil is relatively new to its responsibilities as an oversight body. It is apparent that there remains much in-depth work and analysis for member and other agencies to consider. Clearly, financial institutions and servicers can expect more regulation and oversight from this avenue, as well as from many others. 1. FSOC 2012 Annual Report, p. i.2. Id., pp. 16-18.3. Id., p. 18.4. Id.5. Id., pp. 18-19.

“It is apparent that there remains much

in-depth work and analysis for member

and other agencies to consider.”

Felicia T. Burda is of counsel to Brice, Vander Linden & Wernick,

P.C. A graduate of Duke University School of Law and DePauw

University, she is a former U.S. Trustee, Deputy Executive Director

of the American Bankruptcy Institute and partner with Troutman

Sanders LLP.

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

6

THE LEDGER » NBSDEFAULTSERVICES.COM

UNDER THE MICROSCOPE

UN

DE

R T

HE

MIC

RO

SC

OP

E »

BY

N. R

OB

ER

T H

EN

RY

PA

GE

7D

ATA

ISS

UE

SF

OC

US

BY N. ROBERT HENRY

How the CFPB’s Newly Proposed Rules Will Affect Mortgage Servicers

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

8

With the number of home fore-closures escalating dramat-ically in the aftermath of the housing bubble burst, the mortgage servicing indus-try has taken heavy criti-

cism based on its relationships with borrowers. In response to public concerns that wrongful actions by mortgage servicers demand greater regulation, on August 10th the Consumer Financial Protection Bureau (CFPB) proposed two sets of new rules de-signed to create increased accountability for mort-gage servicers and protect consumers from surpris-es and costly mistakes by servicers. Under the Dodd-Frank Wall Street Reform and Consumer Pro-tection Act, the CFPB has the authority to attempt to improve the market through rulemaking proposals issued under the Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA).

The first set of proposed rules aims to bring great-er transparency to the mortgage market and to pro-vide consumers with easily understood and timely information regarding their mortgages. These pro-posed rules seek to avoid unexpected expenses through clear monthly mortgage statements, earlier disclosures before interest rate adjustments for most adjustable-rate mortgages, warnings and options to avoid “force-placed” insurance, and timely informa-tion regarding options to avoid foreclosure.

While the Dodd-Frank Act already mandates pe-riodic statements for each billing cycle with rules requiring a breakdown of payments by principal, interest, fees and escrow - as well as statements of due date, amounts, and fee warnings - the proposed rules create greater clarity through sample forms and guidelines. Moreover, small servicers, with 1000 or fewer mortgage loans, may be eligible for

an exemption from certain strict requirements. In changing interest-rate adjustment notices for

adjustable-rate mortgages, servicers would be re-quired to provide adjustable-rate consumers with a 60 to 120 day notice before any adjustment which causes the payment amount to change. For first ad-justments, servicers would have to provide an ear-lier notice 210 to 240 days before the change. Fur-thermore, if a rate adjustment does not result in an increase in the monthly payment, servicers would not be required to provide notice.

Servicers are charged with the responsibility to ensure that mortgagors maintain adequate prop-erty insurance, and in situations where a borrower fails to maintain his or her insurance, servicers have the right to purchase insurance in order to protect the lender’s interest in the property. This “force-placed” insurance is typically more expensive than privately obtained insurance, and as a result, the CFPB is proposing that servicers provide more trans-parent procedures by requiring advanced notice and pricing information prior to implementing force-placed insurance. Additionally, servicers would be required to cease force-placed insurance within 15 days of receiving evidence that the mortgagor has sufficient coverage.

Furthermore, the proposed rules require mort-gage servicers to make good faith efforts to contact delinquent mortgagors and inform them of their op-tions regarding alternatives to foreclosure. For ex-ample, when a borrower is 40 days late, the servicer must provide the borrower written notice containing examples of loss-mitigation options and instruc-tions for receiving more information. Additionally, the required notice would provide the mortgagor in default with further information regarding the fore-closure process.

PA

GE

9

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

“Ultimately, the CFPB’s proposed rules create a

variety of increasingly stringent requirements

and procedures for mortgage servicers.”

N. Robert Henry is an associate attorney at Brice, Vander Linden & Wernick, P.C.

in Dallas with a primary focus on the home equity and foreclosure portfolio. He

is a graduate of The University of Kansas and SMU Dedman School of Law, and

is licensed to practice in Texas.

The second set of proposed rules seeks to implement “com-mon-sense” requirements for handling consumer accounts, accepting accountability for errors, and providing mortgagors with options for alternatives to foreclosure. These are referred to as the “no-runaround” rules.

Addressing potential servicer errors, the proposed rules de-fine specific types of claims that a borrower may assert orally or in writing which servicers would be required to acknowledge within five days and respond to typically within 30-45 days. Servicers would be required to provide borrowers with requests for information or explanations for delay within a similar time period. However, servicers would not be required to delay a scheduled foreclosure sale unless the claim of error stems from the servicer proceeding with a sale during the borrower’s eval-uation of alternatives to foreclosure. Moreover, when a con-sumer notifies the servicer of a potential error, the servicer would be required to acknowledge receiving notification, to conduct a reasonable investigation, and to inform the consum-er regarding the error’s resolution in a timely manner.

Also in accordance with the CFPB’s attempts to “put the service” back in servicer, the proposed rules would require servicers to provide borrowers with direct, easy, and contin-ual access to employees who are dedicated and have the au-thority to provide timely assistance. Under this proposal, employees must be assigned as dedicated contact personnel no more than five days after providing notice of default, and servicers must have established policies and procedures de-veloped to ensure these dedicated employees have access to borrower records and information.

Lastly, and perhaps most burdensome of all, when a mort-gage servicer offers a borrower options to avoid foreclosure, the servicer must promptly review all applications for various reinstatement options. Additionally, servicers would be pro-hibited from initiating a foreclosure sale until review of the borrower’s applications is complete. Under the proposed rules, servicers would be required to evaluate all options, and if a modification is denied, provide the borrower with a mini-mum of 14 days notice to appeal the decision.

In implementing these proposed rules, the CFPB is chan-neling a variety of online mediums to allow the public to share concerns and comment on the proposed rules. The pilot proj-ect Regulation Room (regulationroom.org) serves as a web-based forum where individuals and groups can contribute, discuss, and react to the proposed rules. Following a 60-day period ending October 9, 2012, the CFPB, with the assistance of the Cornell University e-Rulemaking Initiative, will review and analyze public commentary before issuing final rules in January of next year.

Ultimately, the CFPB’s proposed rules create a variety of increasingly stringent requirements and procedures for mort-gage servicers. Although the CFPB hopes the new rules lessen the challenges faced by delinquent borrowers working with servicers, it remains unclear how the CFPB intends to enforce its proposed rules. Either way, all mortgagor servicers, large and small alike, should make serious efforts to develop im-proved practices designed to ensure clear, accurate and time-ly correspondence with borrowers so as to avoid potential conflicts during the mortgage-servicing process.

UN

DE

R T

HE

MIC

RO

SC

OP

E »

BY

N. R

OB

ER

T H

EN

RY

PA

GE

10

THE LEDGER » NBSDEFAULTSERVICES.COM

ST

RIP

PIN

G IN

GO

OD

FA

ITH

» B

Y B

RA

DE

N B

AR

NE

SPA

GE

11

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

PA

GE

11

DA

TA

ISS

UE

SF

OC

US

STRIPPING IN GOOD FAITH

IN RE LEPE: 9TH CIRCUIT BAP CONSIDERS “GOOD FAITH” AND LIEN STRIPPING

BY B R ADEN BAR N ES

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

12

Issues related to lien stripping of junior mortgages in the chapter 13 context are prevalent and heavily litigated in today’s environment. Is such lien stripping allowed as a matter of law? If so, is it allowed under the particu-

lar circumstances of the case before the court? Is the debtor acting in good faith?

In In re Lepe,¹ the debtor sought relief under chapter 13 and, among other things, sought to “strip” the secured second lien on his house and treat the claim as unsecured. The debtor’s liabilities exceeded his assets substantially, but his monthly income exceeded his monthly expenses at the time of peti-tion. No creditors, including the second lien holder, objected to the original plan. The chapter 13 trustee did object, how-ever, asserting that the debtor did not file the plan and peti-tion in “good faith” as set forth in § 1325(a)(3) and (a)(7) of the Bankruptcy Code.² At the time of filing the petition, Lepe only had $549 of unsecured debt, so the trustee reasoned that positive monthly cash flow and minimal unsecured debt meant that Lepe’s sole intent in filing chapter 13 was to strip the second lien and nothing more, resulting in an abuse of bankruptcy laws.

Lepe subsequently filed an amended plan increasing pro-posed payments to the trustee. In theory, this would place the unsecured second lien holder in a better financial position, assuming the debtor adhered to the plan. The trustee also ob-jected to the amended plan and asserted the previous argu-ments in support (there was also discussion by the trustee of a related chapter 13 case filed by the debtor’s girlfriend, but for the purposes of this article, focus will remain on the debtor only). At the confirmation hearing the bankruptcy court con-sidered relevant factors, including that (a) payments to unse-cured creditors were “not insignificant,” (b) the argument of not having very much unsecured debt is not controlling in determining the eligibility for chapter 13, and (c) the second lien holder did not object. The bankruptcy court noted that the decision was “a very close call,” but in the end, confirmed the amended plan. The chapter 13 trustee appealed to the Ninth Circuit Bankruptcy Appellate Panel (BAP).

The BAP considered the trustee’s arguments and felt that the position taken relied too heavily on a very limited stance. The BAP relied on In re Goeb,³ an older case that looked at good faith. The court in Goeb noted that good faith was not formally defined and should be looked at in an equitable manner. Also, it established that in the Ninth Circuit, when determining good faith with respect to a chapter 13 plan, a court cannot look to a single factor or purpose of the plan and dismiss all other reasons. When determining good and bad faith motives, the Ninth Circuit looks to the “totality of the circumstances” in each case presented. The BAP noted fac-tors used in In re Warren4 that help implement the totality of circumstances approach when deciding if a chapter 13 debt-

or has acted in good faith, and the factors should be looked at on a case-by-case basis.

Relevant factors may include:• The amount of the proposed payments and the amount of

any surplus of debtor’s income after paying expenses;• The debtor’s employment history, ability to earn, and like-

lihood of future increases in income;• The probable or expected duration of the plan;• The accuracy of the plan’s statements of the debts, expenses

and percentage of repayment of unsecured debt, and wheth-er any inaccuracies are an attempt to mislead the court;

• The extent of any preferential treatment between classes of creditors;

• The extent to which secured claims are modified;• The type of debt sought to be discharged, and whether any

such debt is nondischargeable in chapter 7;• The existence of special circumstances such as inordinate

medical expenses;• The frequency with which the debtor has sought bank-

ruptcy relief;• The motivation and sincerity of the debtor in seeking chapter

13 relief; and• The burden which the plan’s administration would place

upon the trustee. The trustee’s narrow scope basically took the position that if

the debtor had monthly income it would be considered bad faith to seek to strip a second lien. The trustee cited several cases not permitting a debtor to strip the junior lien in support of his posi-tion, but the BAP did not find anything controlling because they all dealt with attorney fees and not junior creditors.

In the end, the BAP reiterated many of the key points of the lower court, including the amount being paid to unsecured creditors not being insignificant and the fact that the lien holder in question failed to object to the plan. The BAP con-cluded that Lepe’s amended plan fell within the confines of what the Bankruptcy Code allows and the lien stripping pro-vision of the plan did not prove a lack of good faith on Lepe’s behalf when everything was considered as a whole compared to any one element.

While I am not going to pass judgment on the BAP’s deci-sion or the trustee’s stance, I do think there are some under-lying issues prevalent in these types of situations that go beyond the text of the case. For this discussion, I would like to refer to the case of In re Dang,5 as recently written about by other BVW counsel in National Bankruptcy Service’s August electronic newsletter, Proceedings. In Dang, the court was presented with a chapter 20 case (a chapter 7 followed by a chapter 13) where the debtor sought to strip a wholly unse-cured junior lien even though chapter 13 discharge was not possible due to multiple filing eligibility factors. Good faith was not an issue in Dang as it was in Lepe because the parties

PA

GE

13

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

ST

RIP

PIN

G IN

GO

OD

FA

ITH

» B

Y B

RA

DE

N B

AR

NE

S

stipulated to good faith, but the facts of Dang begged the question of good faith. The Dang court ruled in favor of the debtor and allowed the lien stripping.

The question of good or bath faith many times walks a very thin line, and the ultimate determination is fact specific with-out controlling guidelines - or logical sequences - of “if this then that.” One does not even have to go to the level of good or bad faith to present intriguing questions that may be per-fectly legal, but leave a bad taste in one’s mouth when as-serted. In Lepe, if a hard stance in the trustee’s corner was taken, it could be analogized, at least distantly, to the loss mitigation sphere before HAMP-style modifications, and to the current foreclosure world in regard to the hot topic issue of “strategic default.” When cash flow modifications ruled the day, and financial planners and finance students were the only ones worrying about NPV and the like, it was com-mon for a workout plan to account for all relevant expenses of a borrower - including the newly modified mortgage pay-ment - and target a residual amount of monthly income to be retained by the borrower. While this residual amount could vary depending on the current guidelines a servicer was sub-ject to, it is logical to assume that the amount could be simi-lar to what the debtor in this case retained after all monthly expenses and debts were paid.

Another example of current trends outside of the bank-ruptcy world is that of strategic default. With strategic default, a borrower is “under water,” and although he has more than enough income to support the mortgage payment, he chooses to default and usually let the home go to foreclosure for finan-cial reasons. Both the factors of having enough to meet the

monthly obligations and the fact that more is owed on the property than the property is worth are present here just like in Lepe. Certainly, different rules apply to bankruptcy than to loss mitigation and foreclosure, but it is not uncommon for a bankruptcy court to justify the stripping of a subsequent lien, and as part of the justification, reference the fact that the lienholder in question would not be any better off outside of bankruptcy if the property were sold at foreclosure sale with-out even enough funds to satisfy the first lien, much less the second or third. Going back to the Dang court’s decision, it could make creditors uneasy worrying that if they are deemed wholly unsecured in a chapter 20 situation, the chapter 13 portion might be used only as a tool to strip their priority even though it was known from the outset that discharge was nev-er the end result sought by the debtor.

It is possible that situations could arise such that, regard-less of what creditors do, they will ultimately end up behind the eight ball. However, subsequent lienholders should make sure that they feel comfortable with the valuation in a lien stripping scenario; if there is any doubt, they should object to any motion to value they find contrary. According to the Ninth Circuit BAP, we know that many factors are considered when determining good faith. If there appear to be several negative factors related to a debtor’s “good faith,” then a creditor should review and dispute legitimate acts supporting that doubt before the court.

1. In re Lepe, BAP No. EC-11-1349-PaDMk (BAP. Ninth Circuit, May 9, 2012). 2. 11 U.S.C. § 1325(a)(3) and (a)(7). 3. In re Goeb, 675 F.2d 1386 (9th Cir. 1982). 4. In re Warren, 89 B.R. 87, 93 (9th Cir. BAP 1987) 5. In re Dang, Case No. 3:11-bk-2970-PMG (Bankr. M.D. Fla. March 12, 2012).

Braden Barnes serves as Assistant General Counsel for

National Bankruptcy Services, LLC and is of counsel with

Brice, Vander Linden & Wernick, P.C. in Dallas. Licensed to

practice in Texas, he received a finance degree from Texas

Christian University and law degree from the University of

Tulsa College of Law.

SIDEBARThe Lepe and Dang cases discussed here did not address the underlying statutory authority for such lien stripping,

which was already established in the jurisdictions involved (the Ninth and Eleventh Circuits), but instead looked at

whether certain factual situations raising additional statutory sections regarding good faith and discharge prohibit

otherwise authorized lien stripping. In both instances, the courts allowed the lien stripping. In a recent case published

after this article was drafted, the Tenth Circuit Court of Appeals addressed the underlying statutory authority for

stripping junior liens in chapter 13. In Wooley v. Citibank (In re Woolsey), Case No. 11-4014 (Sept. 4, 2012), the court

held in favor of the lender, not allowing the lien stripping. This ruling, however, does not bring much comfort to sec-

ond lien holders. The debtors in this case limited their argument to one particular section of the Bankruptcy Code.

The court made it clear that it likely would have allowed the lien stripping if the debtors had pursued an alternative

argument under a different statutory code section, but in this case, the debtors expressly informed the court upon

its inquiry that they did not want it to consider the alternative argument.

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

14

THE LEDGER » NBSDEFAULTSERVICES.COM

HOMEOWNERS SEEING BENEFITS FROM NATIONAL MORTGAGE SETTLEMENT?

BY FELICIA T. BURDA

PROGRESS REPORT FROM THE MONITOR OF THE NATIONAL MORTGAGE SETTLEMENT

PR

OG

RE

SS

RE

PO

RT

FR

OM

TH

E M

ON

ITO

R O

F T

HE

NA

TIO

NA

L M

OR

TG

AG

E S

ET

TL

EM

EN

T »

BY

FE

LIC

IA T

. BU

RD

AD

ATA

FO

CU

SPA

GE

15

ISS

UE

S

On August 29, the monitor of the na-tional mortgage servicing settlement, Joseph A. Smith, issued his first re-port, one not required by the terms of

the Settlement. The Monitor states that this prog-ress report is “intended to inform the public about the nature of the Settlement, the steps that have been taken to implement it and the results to date.”1

SUMMARY OF SETTLEMENTThe Settlement went into effect on April 5 by virtue of five separate consent judgments en-tered by the U.S. District Court for the District of Columbia, settling claims of improper mortgage servicing practices by five major servicers, as listed in Hilary Bonial’s article on page 18 (Servicers). The governmental entities that are party to the Settlement are the U.S. Department of Housing and Urban Development (HUD), the U.S. Department of Justice (DOJ), the attorneys general from 49 states and the District of Columbia, various state mortgage regulatory agencies and other government parties such as the Consumer Financial Protection Bureau and the U.S. De-partment of Treasury.

The government parties agreed to release their claims against the Servicers, and in exchange the Servicers agreed to: (i) make direct payments of approximately $5 billion to governments; (ii) provide various forms of consumer relief to distressed borrowers, such an principal forgiveness and refinanc-ing (Consumer Relief); (iii) adopt more than 300 servicing standards to change their practices in dealing with borrowers (Servic-ing Standards); and (iv) provide various pro-tections specific to those serving in the military. Pursuant to the terms of the Settle-ment, the Monitor is responsible for certify-ing the execution of the Consumer Relief and overseeing implementation of the Servic-ing Standards.

There is a monitoring committee to oversee the Monitor, comprised of representatives from HUD, DOJ and 15 states. The Monitor operates under an approved budget paid out of the Servicers’ cor-porate funds, and has negotiated work plans with the Servicers which describe in detail the procedures to measure their performance. Cur-rently, the monitoring committee has these agreed-upon work plans under review.

ORGANIZATIONAL STRUCTUREThe Monitor has retained BDO Consulting, a division of BDO USA, LLP, as the primary firm assisting him in enforcement of the Settle-ment. He invited 46 firms to submit proposals, and received 23 for review. BDO, which as-sisted the Monitor in negotiating the work plans, will ensure both quality control and that the review of the Servicers is consistent. They will also review and confirm the Con-sumer Relief. With BDO’s assistance, the Monitor has retained a secondary firm for each Servicer to assist in reviewing that Ser-vicer’s performance under the Settlement. In addition, each Servicer has an internal review group consisting of employees and/or inde-pendent contractors responsible for perform-ing compliance reviews.

Although not required by the Settlement, the Monitor has created the Office of Mortgage Settlement Oversight (OMSO), a not-for-profit organization providing administrative sup-port, transparency, and independence. He also has retained various other legal, accounting, and communication professionals.

CONSUMER RELIEFThe Servicers have each agreed to provide specific amounts of relief to distressed bor-rowers during a three-year period. Such relief may include first and second-lien modifica-tions, enhanced borrower transitional funds, facilitation of short sales, deficiency waivers, forbearance for unemployed borrowers, anti-

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

16

blight activities, benefits for service members, and refinanc-ing programs. Generally, but not without limit, the Settle-ment gives the Servicers flexibility to apply different kinds of relief as they deem appropriate to meet their obligations.

The first quarterly report of Consumer Relief by the Ser-vicers is due to the states on November 14th of this year. The Servicers will also report to the Monitor on a quarterly basis regarding their progress toward meeting their payment ob-ligations, as well as statistical data on their overall perfor-mance in servicing.

The Settlement details how crediting toward the obliga-tions works – some activity is credited dollar for dollar, such as principal forgiveness when a Servicer owns and services the loan, and some is credited five cents on the dollar, such as certain forbearance activity. Providing incentive for dem-onstrating substantial progress quickly, the Servicers will receive 25 percent “bonus” credit for certain activities, such as principal reductions, which take place from March 2012 to February 2013. If a Servicer does not meet its total commit-ment within three years, it faces a penalty of at least 125% of the unmet commitment.

The Servicers have voluntarily provided the Monitor with in-formation regarding Consumer Relief to borrowers from March 1 to June 30, totaling $10.561 billion. They report the following:• 137,846 borrowers have received some type of Consumer Relief

totaling $10.56 billion, an average of $76,615 per borrower;• 7,093 borrowers have received a first-lien modification and

$749.4 million in principal forgiveness, averaging $105,650 per borrower;

• An additional 5,500 borrowers have received forgiveness related to pre-March forbearance of $348.9 million, an av-erage of $63,445 per borrower;

• 4,213 borrowers have received second-lien modifica-tions or extinguishments of $231.4 million, averaging $54,930 per borrower;

• Servicers have refinanced 22,073 homes for a total unpaid principal balance of $4.9 billion, with an estimated average monthly interest savings of $388 per borrower;

• 74,615 borrowers have completed a short sale or tendered a deed in lieu of foreclosure, in both cases the Servicers waiving any unpaid principal balance, approximating about $8.67 billion or $116,200 per borrower;

• Through other Consumer Relief programs, about 24,353

borrowers have received relief of $458.8 million or $18,840 per borrower; and

• Servicers have offered 32,104 borrowers first-lien modification trials, totaling $3.9 billion in potential relief, with 28,047 in active trial modifications, totaling $3 billion in potential relief.

SERVICING STANDARDSThe Servicers agreed to meet certain milestones regarding the 304 Servicing Standards required by the Settlement as of June 4, July 5 and October 2, 2012. As of July 5, there were 56 Servicing Standards that all Servicers indicate had been implemented; four Servicers report having implemented more than half the Servicing Standards for a total range of implementation of 35 to 72 percent. Some of the Servicing Standards reportedly in place are:• Integrity of Documents: Documents filed in bankruptcy

and foreclosure proceedings are based upon affiants’ per-sonal knowledge, in compliance with state law, complete, signed and dated, and true and substantiated.

• Single Point of Contact: Each potentially eligible borrower has an accessible and reliable contact who, among other things: (i) contacts the borrower to explain the program; (ii) obtains information and the documents for the pro-gram; (iii) helps the borrower clear any processing require-ments; and (iv) communicates the Servicer’s decision in writing to the borrower.

• Customer Service: Various standards of customer service are in place regarding communications, staffing, experi-ence, and training requirements.

• Loss Mitigation: Servicers report designing proprietary first-lien loan modification programs, not levying fees for first and second-lien applications for modification, and performing independent evaluations of initial denials of first-lien modifications.

• Servicemember Protection: Servicers are complying with the Servicemembers Civil Relief Act, and have engaged independent consultants to review foreclosures involving servicemembers.

• Anti-Blight: Servicers report implementation of policies to ensure no blighting of real estate owned by the Servicers.

• Tenant Rights: Servicers report compliance with federal and state laws regarding rights of tenants living in fore-closed properties.

PA

GE

17

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

PR

OG

RE

SS

RE

PO

RT

FR

OM

TH

E M

ON

ITO

R O

F T

HE

NA

TIO

NA

L M

OR

TG

AG

E S

ET

TL

EM

EN

T »

BY

FE

LIC

IA T

. BU

RD

A

METRICSAs discussed in Hilary Bonial’s article on page 18, the Monitor must use a series of defined metrics to assess the Servicers’ adherence to the Servicing Standards. The metrics do not re-late to each and every one of the 304 Servicing Standards, but the Monitor has authority to add metrics to cover standards that do not map to the metrics. Whenever a Servicer imple-ments a standard that maps to a metric, the Monitor will evaluate that metric during the next quarter. In the first quar-ter of 2013, the Monitor will evaluate Servicers’ performance during the third and fourth quarters of 2012 against 29 met-rics, with various metrics applied to particular Servicers for particular quarters.

FROM THE MARKET PLACEBy virtue of the website the Monitor has developed (www.mort-gageoversight.com), he has received almost 1,300 submissions from consumers in the 49 involved states and the District of Columbia, which he claims adds a richness and depth to the data he gathers. Through a separate portal on the site, he has received 118 submissions from professionals assisting home-owners, such as attorneys, bankruptcy trustees, housing coun-selors, realtors, and staff from Attorneys General offices.

ANALYSIS AND COMMENTARYIt is notable that the bulk of the relief reported thus far is with respect to shorts sales and deeds in lieu of foreclosure – almost 75,000 borrowers, well more than half, and $8.67 billion of the $10.5 billion in relief. The Servicers reported relief through modifications and principal forgiveness, which would actually keep people in their homes, at a much more disappointing rate – about 7,000 borrowers and $749.4 million in relief. As pointed out in a New York Times article, a short sale is one of the simpler forms of relief; a loan mod-ification requires engagement of the borrowers, paperwork, and a successful three-month trial period.2 Apparently, Bank of America, the Servicer having the highest obliga-tions pursuant to the Settlement, did not report any princi-pal reductions during the period. A spokesman for Bank of America, however, stated that from July 1 to August 21, the bank has granted $600 million in principal reductions and tripled the number of households in the three-month trial period for a modification.3

Adam J. Levitin, a professor of law at Georgetown Law Center in Washington, D.C. and a recent appointee to the Consumer Advisory Board for the CFPB, drafted a fairly critical commen-tary regarding the Monitor’s preliminary report.4 He notes first that the Monitor includes virtually no analysis, but he also rec-ognizes that more time and results are needed for an in-depth examination. He points out that helping 137,000 borrowers is not a lot, even compared to the “sad standard” of HAMP. Levi-tin estimates that only one to two percent of the underwater population has received help so far under the Settlement, stat-ing that many of these borrowers would have received relief without the Settlement and that the Servicers purposefully slowed down and stock piled loss-mitigation activities prior to its implementation. Regarding the short sales, Levitin says they must be happening with a non-representative group because the average size of the short-sale loss is $116,000 – nearly as large as the average mortgage loan. Last, he notes that nearly half of the relief has gone to borrowers in California.5 While his commentary is somewhat depressing (one blogger replies, “Thanks for that incredibly uplifting and spirit raising review there, Professor Sunshine . . . ;)”), Professor Levitin is well re-spected and active in the field. Future articles in NBS publica-tions will examine his recent papers on the reasons the housing industry was vulnerable to a bubble, and the loan cost increas-es that would allegedly occur if bankruptcy judges were al-lowed to modify loans in chapter 13 cases.

It is important to remember that the Monitor has not yet veri-fied the information in his preliminary report. He is just “report-ing” what the Servicers have reported to him. Also, the crediting formulas under the Settlement have not been applied. Short sales do not receive dollar for dollar credit, so the $10.56 billion figure will be significantly reduced in the final count. However, the fact that the Monitor issued this non-mandatory report is admirable and does lend transparency to the process. NBS will include analysis of his first official report due to be filed in early 2013 with the U.S. District Court for the District of Columbia. 1. The Report, p. 1.

2. http://www.nytimes.com/2012/08/30/business/monitor-reports-progress-on-

homeowner-aid.html

3. Id.

4. http://www.creditslips.org/creditslips/2012/08/national-mortgage-servicing-

Settlement-progress-report-little-to-show-and-little-expected.html?utm_

source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+creditslips%

2Ffeed+%28Credit+Slips%29

5. Id.

Felicia T. Burda is of counsel to Brice,

Vander Linden & Wernick, P.C. A graduate

of Duke University School of Law and

DePauw University, she is a former U.S.

Trustee, Deputy Executive Director of

the American Bankruptcy Institute, and

partner with Troutman Sanders LLP.

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

18

On February 9, 2012 the attorneys general of 49 states1 and the District of Columbia, the federal government, and five banks and mortgage servicers (Ally/GMAC, Bank of America, Citi, JPMorgan Chase and Wells Fargo) reached agreement on a mortgage settlement that will create new servicing standards, provide loan modification relief to distressed homeowners and provide funding for state and federal governments. On March 12, 2012, the participants in the 49-state mortgage settlement appointed attorney Joseph A. Smith, Jr. as the Monitor who will oversee implementation of the agreement. Smith’s appointment is for a three-and-a-half year term. He spoke at the recent an-nual meeting of the National Association of Chapter 13 Trustees in New Orleans; the following is a summary of the discussion.

The Office of Mortgage Settlement Oversight has been charged with auditing and compiling metrics derived from approximate-

ly 290 servicing standards enunciated within the settlement. Currently, only 29 auditable metrics have been developed, but it is expected that more will be derived following the evolution of the initial review of the current servicing landscape. The 29 met-rics are being described as the “basic points of the servicing standards” contained in the settlement. Their derivation came first by defining the operable standards within the settlement itself. Most reviewers have identified 285 to 290 standards, of which 29 can be measured within a metric-reporting process. Of the 29, five are normative metrics; for example, does a procedure exist? The remaining 24 are measured metrics that will require an audit of eligible accounts to determine compliance.

Out of the approximately 290 standards, 29 have some relation to the bankruptcy process. Of the 29 metrics currently developed, eight have some relation to the bankruptcy

JOSEPH A. SMITH SPEAKSRemarks at Annual Meeting of NACTT

By Hilary Bonial

PA

GE

19

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

1. Oklahoma is the only state which did not join the settlement.

process. The eight bankruptcy metrics are as follow:1. Whether foreclosure sales were in vio-

lation of the stay;2. Integrity of proofs of claim;3. Integrity of motions for relief from stay;4. Reasonableness of fees and costs

charged to accounts;5. Reconciliation of waived fees;6. Management of third party vendors;7. Compliance with single point of con-

tact requirement;8. Timeliness of responses to complaints.

In response to questions from the au-dience, Mr. Smith discussed his under-standing of the metric regarding the integrity of proofs of claim. The Office will be reviewing proofs of claim to de-termine if the following documents are attached and consistent with the infor-mation on the claim itself:• Pre-petition payment history;• Current copy of the note showing en-

dorsement to current holder or in blank;• Recorded deed of trust / mortgage;• Full chain of assignments;• Correct calculation of arrearage,

post-petition due date, and date of last payment;

• Disclosure of the current correct in-terest rate;

• Phone and e-mail contact information for the single point of contact;

• Statement of standing.Mr. Smith also addressed the Office’s

review of servicers’ management of third-

party vendors. The Office will be review-ing the policies and procedures of the vendor, the standards provided by the servicer, and the underlying agreements and statements of work that establish the servicer/vendor relationship.

The Office will also be looking for pat-terns of non-compliance within the rec-onciliation of fees charged to the bor-rowers. Were the fees disclosed? Were they allowed or denied by the court? If denied, were they properly and timely categorized by the servicer?

As to motions for relief from stay, the microscope will be focused on the re-quirement to review the payment his-tory 48 hours prior to the hearing.

How will the Office discover viola-tions? Mr. Smith emphasized that trust-ees and debtors’ attorneys will be able to assist in discovery of non-compli-ance. The website, www.mortgageover-sight.com, includes an area for trustees and attorneys to submit individual is-sues for review.

The settlement requires formal re-ports to be filed with the U.S. District Court for the District of Columbia. The first report, covering July through De-cember 2012, is expected to be filed on February 14, 2013.

National Bankruptcy Services will continue to provide additional informa-tion as it becomes available. If you have any questions, please feel free to contact the author.

“Out of the

approximately 290

standards, 29 have

some relation to the

bankruptcy process. Of

the 29 metrics currently

developed, eight have

some relation to the

bankruptcy process.”

Hilary B. Bonial serves as General Counsel

for National Bankruptcy Services, LLC.

and is of counsel for Brice, Vander

Linden & Wernick, P.C. She is certified by

the American Board of Certification in

Consumer Bankruptcy.

JO

SE

PH

A. S

MIT

H S

PE

AK

S »

HIL

AR

Y B

. BO

NIA

L

PA

GE

20

THE LEDGER » NBSDEFAULTSERVICES.COM

DATA

< 100

200-300

100-200

>300

D.C.

NATIONAL AVERAGE (-13.4%)128.8

StateFilings Per

CapitaPercent Change1

Nevada 7.69 -3.41

Georgia 7.10 -0.82

California 6.2 -0.71

Tennessee 6.19 -1.67

Alabama 5.47 -1.69

Michigan 5.23 -1.47

Illinois 5.02 -1.23

Utah 4.92 -1.53

Arizona 4.73 -1.58

Kentucky 4.57 -1.03

StateFilings Per

CapitaPercent Change1

Alaska 1.10 -0.48

District of Columbia 1.40 -0.74

South Dakota 1.45 -0.99

Vermont 1.51 -1.11

South Carolina 1.54 -0.50

North Dakota 1.71 -0.76

New York 1.78 -1.06

Wyoming 1.81 -0.98

Montana 1.92 -1.11

Iowa 1.95 -1.26

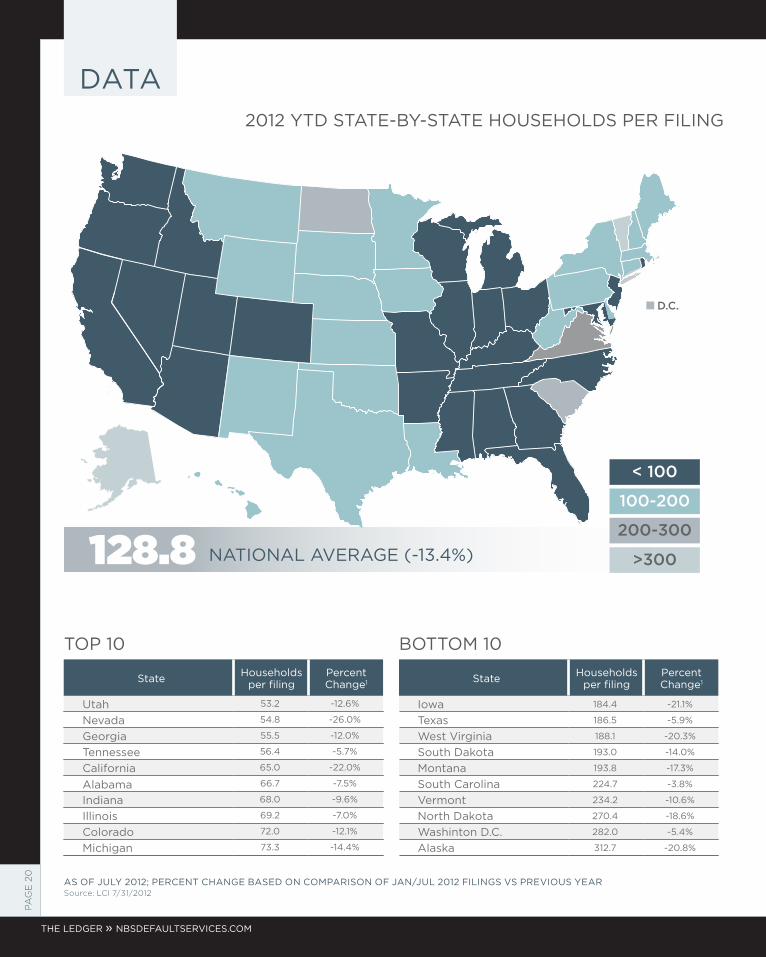

DATA

StateHouseholds

per filingPercent Change1

Utah 53.2 -12.6%

Nevada 54.8 -26.0%

Georgia 55.5 -12.0%

Tennessee 56.4 -5.7%

California 65.0 -22.0%

Alabama 66.7 -7.5%

Indiana 68.0 -9.6%

Illinois 69.2 -7.0%

Colorado 72.0 -12.1%

Michigan 73.3 -14.4%

StateHouseholds

per filingPercent Change1

Iowa 184.4 -21.1%

Texas 186.5 -5.9%

West Virginia 188.1 -20.3%

South Dakota 193.0 -14.0%

Montana 193.8 -17.3%

South Carolina 224.7 -3.8%

Vermont 234.2 -10.6%

North Dakota 270.4 -18.6%

Washinton D.C. 282.0 -5.4%

Alaska 312.7 -20.8%

AS OF JULY 2012; PERCENT CHANGE BASED ON COMPARISON OF JAN/JUL 2012 FILINGS VS PREVIOUS YEARSource: LCI 7/31/2012

2012 YTD STATE-BY-STATE HOUSEHOLDS PER FILING

TOP 10 BOTTOM 10

PA

GE

21

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

STATE-BY-STATE TOTAL 2012 YTD BANKRUPTCY FILINGSAND PERCENTAGES OF CHAPTER 7 VS. CHAPTER 13

State Total 2012 Chapter 7 Filings Chapter 13 Filings

Alabama 15,881 39.9% 59.9%

Alaska 475 83.6% 16.2%

Arizona 16,755 86.0% 13.4%

Arkansas 7,327 54.3% 45.5%

California 111,423 75.0% 24.6%

Colorado 15,874 83.3% 16.6%

Connecticut 4,973 87.2% 12.3%

Washington DC 522 86.0% 12.8%

Delaware 1,856 71.4% 28.5%

Florida 46,993 72.4% 27.3%

Georgia 36,628 50.3% 49.5%

Hawaii 1,547 76.1% 23.7%

Idaho 3,815 89.2% 10.5%

Illinois 40,043 72.6% 27.3%

Indiana 21,187 73.8% 26.1%

Iowa 3,871 91.1% 8.7%

Kansas 5,254 66.7% 33.1%

Kentucky 11,730 73.7% 26.2%

Louisiana 9,142 35.8% 64.0%

Maine 1,815 86.2% 13.3%

Maryland 13,945 80.8% 18.9%

Massachusetts 10,257 72.9% 26.5%

Michigan 30,277 83.8% 16.0%

Minnesota 10,346 83.4% 16.5%

Mississippi 7,109 53.9% 45.9%

Missouri 15,148 73.2% 26.7%

Montana 1,212 82.8% 16.8%

Nebraska 3,310 72.4% 27.4%

Nevada 10,533 80.3% 18.7%

New Hampshire 2,408 76.0% 24.0%

New Jersey 18,757 78.7% 21.1%

New Mexico 2,846 91.3% 8.3%

New York 24,635 84.8% 15.0%

North Carolina 12,474 45.2% 54.3%

North Dakota 605 90.1% 9.8%

Ohio 29,653 77.1% 22.8%

Oklahoma 6,906 83.9% 16.0%

Oregon 9,220 79.0% 20.9%

Pennsylvania 17,038 69.2% 30.6%

Rhode Island 2,491 84.9% 15.0%

South Carolina 4,572 45.5% 54.2%

South Dakota 964 90.5% 9.3%

Tennessee 25,254 47.5% 52.2%

Texas 27,326 44.6% 55.1%

Utah 9,649 67.7% 32.1%

Vermont 640 79.2% 20.6%

Virginia 17,680 65.8% 34.1%

Washington 16,433 80.5% 19.2%

West Virginia 2,301 87.2% 12.6%

Wisconsin 15,682 77.1% 22.7%

Wyoming 746 85.8% 13.5%

TOTAL 707,528 70.6% 29.1%

2012 YTD as of July 31, 2012.

PA

GE

22

THE LEDGER » NBSDEFAULTSERVICES.COM

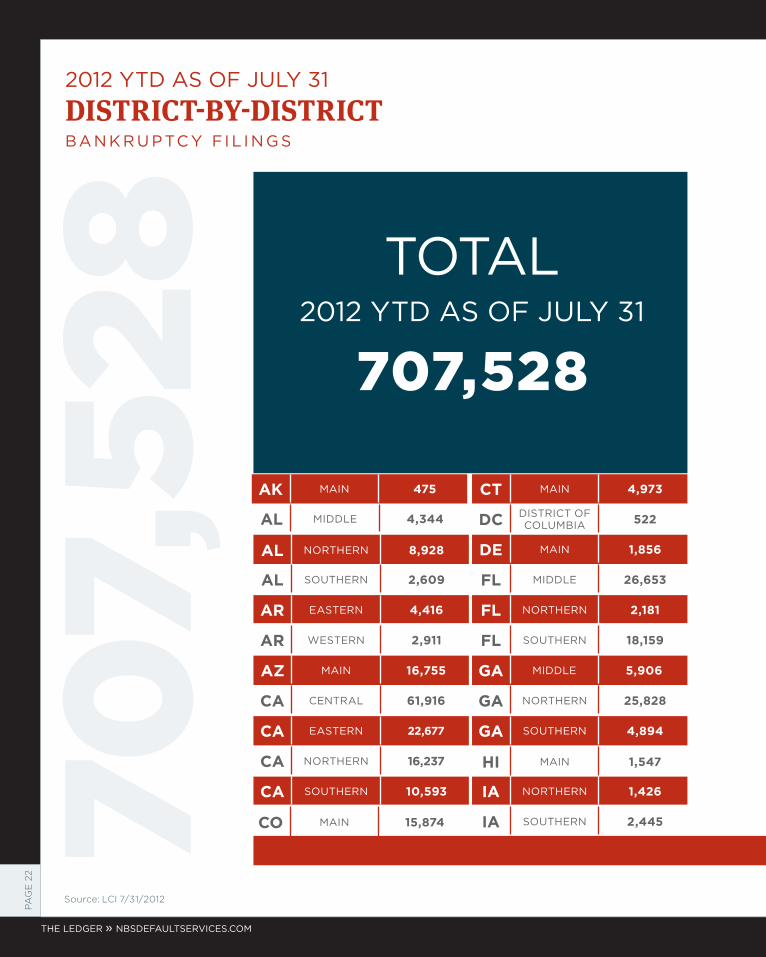

70

7,5

28 TOTAL

2012 YTD AS OF JULY 31

2012 YTD AS OF JULY 31

DISTRICT-BY-DISTRICTBAN K R U PTC Y F I L I N G S

707,528

Source: LCI 7/31/2012

AK MAIN 475 CT MAIN 4,973

AL MIDDLE 4,344 DC DISTRICT OF COLUMBIA 522

AL NORTHERN 8,928 DE MAIN 1,856

AL SOUTHERN 2,609 FL MIDDLE 26,653

AR EASTERN 4,416 FL NORTHERN 2,181

AR WESTERN 2,911 FL SOUTHERN 18,159

AZ MAIN 16,755 GA MIDDLE 5,906

CA CENTRAL 61,916 GA NORTHERN 25,828

CA EASTERN 22,677 GA SOUTHERN 4,894

CA NORTHERN 16,237 HI MAIN 1,547

CA SOUTHERN 10,593 IA NORTHERN 1,426

CO MAIN 15,874 IA SOUTHERN 2,445

PA

GE

23

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

ID MAIN 3,815 MT MAIN 1,212 PA WESTERN 5,528

IL CENTRAL 4,620 NC EASTERN 5,379 RI MAIN 2,491

IL NORTHERN 32,758 NC WESTERNA 3,803 SC MAIN 4,572

IL SOUTHERN 2,665 NC MIDDLE 3,292 SD MAIN 964

IN NORTHERN 8,586 ND MAIN 605 TN EASTERN 8,320

IN SOUTHERN 12,601 NE MAIN 3,310 TN MIDDLE 6,910

KS MAIN 5,254 NH MAIN 2,408 TN WESTERN 10,024

LA WESTERN 5,818 NV MAIN 10,533 TX EASTERN 3,507

LA EASTERN 2,219 NY NORTHERN 4,845 TX NORTHERN 10,189

KY EASTERN 5,586 NJ MAIN 18,757 TX SOUTHERN 7,420

KY WESTERN 6,144 NM MAIN 2,846 TX WESTERN 6,210

LA MIDDLE 1,105 NY SOUTHERN 5,983 UT MAIN 9,649

MA MAIN 10,257 NY WESTERN 3,634 VA EASTERN 13,487

MD MAIN 13,945 NY EASTERN 10,173 VA WESTERN 4,193

ME MAIN 1,815 OH NORTHERN 15,463 VT MAIN 640

MI EASTERN 22,923 OH SOUTHERN 14,190 WA EASTERN 3,345

MI WESTERN 7,354 OK EASTERN 1,082 WA WESTERN 13,088

MN MAIN 10,346 OK NORTHERN 2,072 WI EASTERN 11,354

MO EASTERN 8,299 OK WESTERN 3,752 WI WESTERN 4,328

MO WESTERN 6,849 OR MAIN 9,220 WV NORTHERN 1,026

MS SOUTHERN 4,016 PA EASTERN 7,141 WV SOUTHERN 1,275

MS NORTHERN 3,093 PA MIDDLE 4,369 WY MAIN 746

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

24

Luke Madole joins the company as a Vice President and Shareholder of Brice, Vander Linden & Wernick, P.C. and Chief Legal Of-ficer of National Bankruptcy Services, LLC. Luke’s outstanding credentials, back-ground and experience as one of Dallas’ premiere litigation trial attorneys will pro-vide immeasurable value to the company and its clients.

THE LEDGER: Tell us a little about yourself.

LM: I am Dallas born and bred. My moth-er’s parents moved to Dallas in the 1920s.

My father, a lawyer, moved to Dallas in 1939 to work in the legal department of the Magnolia Petroleum Company. His office was in the downtown Magnolia Building. As children, he would take us all the way to the top so we could see the “Flying Red Horse” (which still rotated in those days) up close. My wife, Susan ( a lawyer’s daughter), is also from Dallas. We were high school classmates, married after first year of law school, have three grown chil-dren and one daughter-in-law.

THE LEDGER: Prior to joining NBS/BVW, in what areas of practice did you specialize?

Born and raised in Dallas, Texas, Mr. Madole is a graduate of The University of Texas at

Austin School of Law. After law school, Mr. Madole returned to Dallas as a trial lawyer

with Carrington, Coleman, Sloman & Blumenthal, Bird & Reneker, P.C. and as an Assistant

Dallas County Criminal District Attorney Mr. Madole has tried over 80 jury cases, over 160

non-jury cases, and has been involved in 14+ reported appellate opinions. His courtroom

work germane to the unique businesses of BVW and NBS includes the representation of

debtors, mortgage insurers, creditors, tenants, landowners, lawyers, contractors, Fannie

Mae and others. From 2001-2012, Mr. Madole worked as outside counsel for BVW and

NBS in court-related matters. He is a member of the State Bar of Texas and numerous

other professional associations, is AV rated by the Martindale Hubbell Law Directory, and

has been a ‘Texas Super Lawyer’ since 2004.

NBS Welcomes Luke Madole AN INTERVIEW WITH THE NEW CHIEF LEGAL OFFICER

INTERVIEWER: WES WILEY

PA

GE

25

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

HO

T S

EA

T »

LU

KE

MA

DO

LE

LM: Trial work, primarily in commercial matters. I also served four-plus years as a Dallas County prosecutor.

THE LEDGER: Which area of practice in-trigued you the most and why?

LM: I like the interplay of trials. Many be-lieve lawyers are able to manipulate juries and juries often misfire. You’ll never con-vince me of either. I’ve yet to see a jury that was not conscientious. Jurors realize they are deciding something of importance, and they take that responsibility seriously. Ju-rors look for the lawyers, the witnesses and the evidence they can rely on to resolve com-peting versions of what happened in times past. The collective wisdom and common sense of 12 people drawn from all walks of life has never ceased to impress me, even when my side lost. There are a few jury mis-fires, but not many. And even then, the re-sponsibility for most jury misfires comes from non-jury participants. Some misfires result from a judge’s refusal to enforce the rules of evidence/procedure, turning the jury into an unguided missile loaded with

inflammatory evidence that should never have been admitted. They get called “run-away juries,” but the real cause of the misfire lies elsewhere. Most of the relatively few misfires involve a client and/or lawyer who was foolish enough to think a jury could be over-swayed by a lawyer’s cleverness or by sympathetic circumstances. When those disbeliefs result in a failure to bring forth the reliable evidence and arguments earnest juries look for, the result can look outland-ish. It wasn’t outlandish - it fit what the jury actually saw and heard. But the clients and/or lawyers who misjudged the timber of the jury blame the jury, not themselves, for the “Not Guilty” or no liability or high damage award given in the verdict. Trial by jury has intrigued me the most and continues to draw my unstinting admiration.

THE LEDGER: What were some of the rea-sons you decided to join NBS/BVW?

LM: I have represented BVW & NBS for ten-plus years as outside counsel. During the mortgage crisis, I have been all around the country with BVW and/or NBS personnel in

“hot” situations. I’m sure, from the inside, one can see the warts along with the beauty spots. I can, however, attest that from the outside, and from listening to insufficient explanations to judges of what have been the practices of other default services pro-viders, that BVW and NBS can take pride in their efforts and record. Perfect? No. Aiming at delivering valuable services at junctures of complex compliance requirement as the law and clients expect? Yes.

THE LEDGER: Tell our readers a little more about your responsibilities with NBS/BVW.

LM: Primarily risk management. I have repre-sented lawyers over the years in alleged mal-practice and other contexts. I’m familiar with the administrative issues NBS encounters.

THE LEDGER: What are some of the chal-lenges you see in the future for creditors within the default space?

LM: Co-ordination of the multiplying com-pliance requirements from consent orders, new laws and additional regulations.

NBS Welcomes Luke Madole

THE LEDGER » NBSDEFAULTSERVICES.COM

PA

GE

26

ALWAYS DO THE RIGHT THINGCHEATING AND ORGANIZATIONAL COMPLIANCE

BY ELIJAH METCALF

PA

GE

27

NBSDEFAULTSERVICES.COM « OCTOBER 2012

DA

TA

ISS

UE

SF

OC

US

I was listening to the radio in my car recently and hap-pened upon a show dedicated to broadcasting excerpts from various TED Talk speeches and interviews. For those not familiar with TED, the acronym stands for

Technology, Entertainment, Design, and this non-profit orga-nization has held conferences since 1984 cultivating “Ideas Worth Spreading.” I listened to a speech prepared by Dan Ariely, the James B. Duke professor of psychology and behav-ior at Duke University. His speech was focused on a study he had conducted on cheating while at MIT. In particular, he studied the prevalence of cheating within a given environ-ment and the factors that would increase and decrease the instances of cheating by participants. I was immediately in-terested in the implications for organizational compliance.

Professor Ariely’s experiment brought to light startling revelations on cheating. In the context of the experiment, “cheating” meant lying about the number of math problems a participant answered correctly in order to receive more money from the observers. Applying the concept to organi-zational compliance, I defined cheating as knowingly oper-ating outside of reasonably expected ethical behavior. For example, this definition could apply to employees cutting corners and not adhering to known policy, whether regard-ing an internal procedure or a government regulation. Pro-fessor Ariely’s study found that when given the opportunity, cheating was widespread, but not severe. This goes against the “few bad apples” theory of cheating - that misdeeds are more likely to be perpetrated by a limited number of malcon-tents, while the surrounding population is filled with mod-el corporate citizens. In fact, however,, the study found that instead of a few people who cheat a lot, the reality is that “a lot of people …cheat a little bit.”1 According to Ariely, “But because it’s so prevalent, it basically creates much larger financial devastation.”2

This concept of “a lot of people cheating a little bit” poses a frighteningly complex puzzle to solve in terms of organiza-tional compliance. One can envision a scenario in which mul-tiple employees, cheating just a little, are all responsible for

critical compliance missteps without ever intending harm, or even fully realizing the consequences of their actions. The “cheaters” in this case might include star performers, subject matter experts, and even members of various levels of man-agement. And with numerous companies within an industry, all filled with employees cutting the corners of compliance, it would only be a matter of time before a scandal surfaces and the call for tighter regulation rings forth. Admittedly, this may be a worst-case scenario, but it has proved an unfortunate reality in today’s world of twenty-four hour news cycles and citizen journalism. The results of such scandals, including Enron and the recent foreclosure crisis, have led to exactly the “financial devastation” Ariely’s study foreshadowed. And the regulatory reaction has included the Sarbanes-Oxley Act and the national servicing standards.

No company or industry should wait for government regula-tion to drive its compliance-related internal policies and pro-cedures. It is to the advantage of every company to embrace self-regulation as the cornerstone of its corporate compliance activities. Through self-regulation, management is able to de-fine compliance not only to mitigate risk, but also add value. For example, by formalizing operational processes into docu-mented procedures, necessary and critical knowledge can be codified. Thus, when an employee who has assumed subject matter expert status decides to retire, that important knowl-edge is not lost. Instead, crucial information is retained within the organization and used to benefit all future employees. The documented procedures can then be included within the com-pany’s training program, to be disseminated as needed. More-over, by setting a schedule to regularly review and revise the procedures and the training documentation, a company can ensure that new employees are provided with the most up-to-date information, allowing them to learn how to perform their job expediently and effectively.

The above is just one example to illustrate ways in which compliance can add value to an organization. The main point is that compliance should be used to mitigate real and actual risk as determined by the company’s management, just as an

Elijah Metcalf is the Internal Audit

Manager at National Bankruptcy

Services, LLC and currently oversees

client audit coordination. He holds

an MBA from the University of Texas

at Dallas with a concentration in

Internal Audit.

ALW

AY

S D

O T

HE

RIG

HT

TH

ING

» E

LIJ

AH

ME

TC

AL

F

THE LEDGER » NBSDEFAULTSERVICES.COM

DA

TA

ISS

UE

SPA

GE

28

FO

CU

S

audit should be leveraged to provide independent and objective oversight for the purpose of assuring that proper controls are in place and working effectively. When compliance measures are dictated and determined by government enforced regula-tion, a greater separation between the perceived risk being mitigated and the true risk threatening the company is likely to exist. For example, when outside regulators are trying to assess whether mortgage lenders and servicers are properly verifying the performance of their vendors, proof of the verifica-tion can take priority over the existence and efficacy of the verification. In this climate of heightened government over-sight, greater focus and resources are often needed to prove that risks are mitigated instead of adequate-ly assuring that the relevant risks are in fact mitigated appropriately. This can lead to compliance and audit efforts becoming inefficient, leading to a poor reputation and limited acceptance within a com-pany. My opinion is not at all meant to discredit government-mandated regulation. I am merely making the point that the management of a company understands its business far better than any politician ever could, and that legislators would have no need to enforce com-pliance on a business or an industry if proper self-regulation were in place.

With this in mind, in determining the right approach to take when tackling compliance, I return to Dan Ariely’s study on cheating to provide advice. He found that the possibility of increased profit did not encourage greater cheating, nor did decreasing the likelihood of being caught. “Again, a lot of people cheated by just by a little bit, and they were insensitive to these economic incentives.”1 However, one experiment completely eliminated all instances of cheating:

“The moment people thought about trying to recall The Ten Commandments, they stopped cheating. In fact, even when we gave self-declared atheists the task of swearing on the Bible and we give them a chance to cheat, they don’t cheat at all. Now, Ten Commandments is something that is hard to bring into the education system, so we said, ‘Why don’t we get people to sign the honor code?’ So, we got people to sign, ‘I understand that this short survey falls under the MIT Honor Code.’ Then they

shredded it. ‘No cheating whatsoever.’ And this is particularly interesting, because MIT doesn’t have an honor code.”1

This experiment found that reminding participants of moral-ity had a direct effect on the likelihood of cheating. In theory, a company could use this finding as inspiration to circulate regular compliance reminders for employees. The above quote suggests that neither the scripture nor the fictitious MIT honor code were the motivators of the change in behavior. Rather, it appears that the participants’ self-judgment, brought about by the subtle reminder of morality, instigated the adjustment. One might conclude, therefore, that it is not enough to have employ-

ees sign an honor code once upon the commencement of their em-ployment with a company. Instead, each employee should routinely be made aware of his obligation to be an exemplary member of staff, and be encouraged to examine whether or not he is behaving ethically in his work performance.

A final note on compliance: it is generally true that people adapt to their surroundings. If an organization believes in compliance, embraces compliance, and promotes compliance from the top-down, it will spread throughout the organization. Employees are likely to set their ethical behavior to be in line with that of their col-leagues. Indeed, Ariely’s study found that participants were more inclined to cheat if they believed cheating was com-mitted by people they considered to be in their clique.1 From that, one could draw the conclusion that an organization should reward employees who display ethical behavior to improve overall compliance. Conversely, employees who will not capitulate to compliance initiatives should be dis-ciplined and, if sufficiently obstinate, terminated to foster the ideal company culture. Compliance efforts should be devoted to ensuring that each individual at the company is doing things right and doing the right things. 1. http://www.ted.com/talks/dan_ariely_on_our_buggy_moral_code.html

(Transcript provided within the video player)

2. http://www.npr.org/2012/04/27/150818706/why-do-we-cheat (Transcript link:

http://www.npr.org/templates/transcript/transcript.php?storyId=150818706 )

Works Referenced

http://blogs.hbr.org/cs/2008/01/how_honest_people_cheat.html

“THIS CONCEPT OF ‘A LOT OF

PEOPLE CHEATING A LITTLE

BIT’ POSES A FRIGHTENINGLY

COMPLEX PUZZLE TO SOLVE IN

TERMS OF ORGANIZATIONAL

COMPLIANCE.”

ALW

AY

S D

O T

HE

RIG

HT

TH

ING

» E

LIJ

AH

ME

TC

AL

F

NBS TRADESHOW PRESENCENational Bankruptcy Services continues to take

an active role at many of the industry’s top events.

Most recently, NBS participated at the Debt

Connection Symposium (DCS) in September in

Las Vegas, NV.

Look for NBS next at these conferences:

• REperform; October 3-5; Dallas, TX; Panel discussion on Oct. 3 at 3 P.M.

• Auto Finance Summit (AFS); October 22-24; Las Vegas, NV; Booth #107

NBS NEWS DESK

OUR MISSION IS SIMPLE. We strive to improve the

bottom line performance of our clients’ bankruptcy portfolios

through careful, efficient, and client-specific management of

each individual case.

NBS provides nationwide bankruptcy management services

to the following types of organizations:

* Residential Mortgage Lenders

* Automobile Finance Companies

* Banks and Financial Institutions

* Consumer Lending Organizations

* Portfolio Servicers, Owners, and Investors

NBS is a leader in bankruptcy servicing for the consumer

finance industry. NBS is a subsidiary of Advent International.

ABOUT NBS

BANKRUPTCY SYMPOSIUM SERIES NBS will be hosting our next Bankruptcy

Symposium in Las Vegas on Monday, October

22, prior to the AFS conference. We’ll spend the

afternoon discussing the latest statistics, trends,

and rule changes affecting bankruptcy in the auto

sector and cap it off with a night out on the town.

Please request an invitation by sending an email to

Wes Wiley at [email protected].

RSVP OF FRIDAY, OCTOBER 17

WWW. N B S D E FAU LTS E RV I C E S .CO M

NBS RECENTLY INTRODUCED PROCEEDINGS A PERIODIC PERSPECTIVE ON BANKRUPTCY SERVICING

Developed and published by a panel of NBS bankruptcy

experts, Proceedings features an assortment of quick-

hitting articles spotlighting the current events affecting

bankruptcy servicing. The September edition features ar-

ticles on the decrease in delinquency rates and a progress

report from the Monitor of National Mortgage Settlement.

Please be our guest and review this and other editions

of Proceedings by visiting the Perspective web page at

NBSdefaultservices.com.

To learn more about NBS and our free portfolio help

assessment offer, please visit our website and watch our

brief introduction video.

If you’d like to receive future editions of The Ledger, our periodic online newsletter, Proceedings, and other NBS updates, please submit your email address to the Newsletter Signup field on our home page

TH

E L

ED

GE

RA

PR

IL 2

012

TH

E L

ED

GE

RO

CT. 2

012