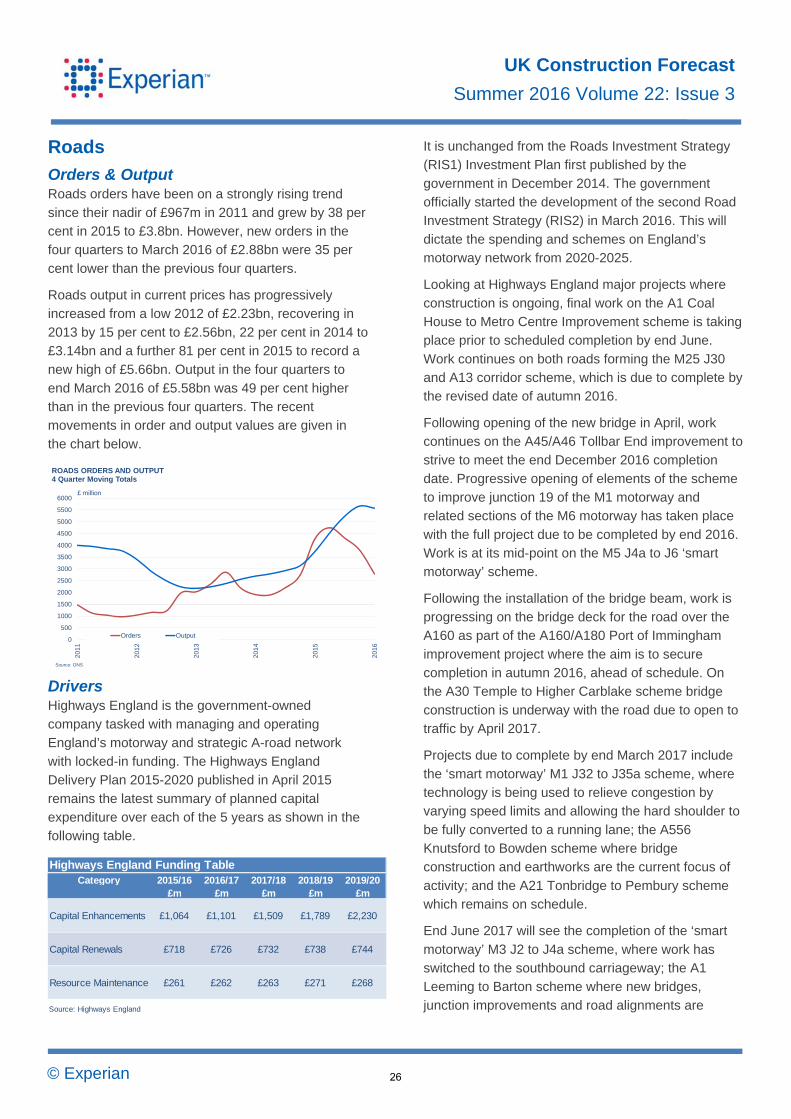

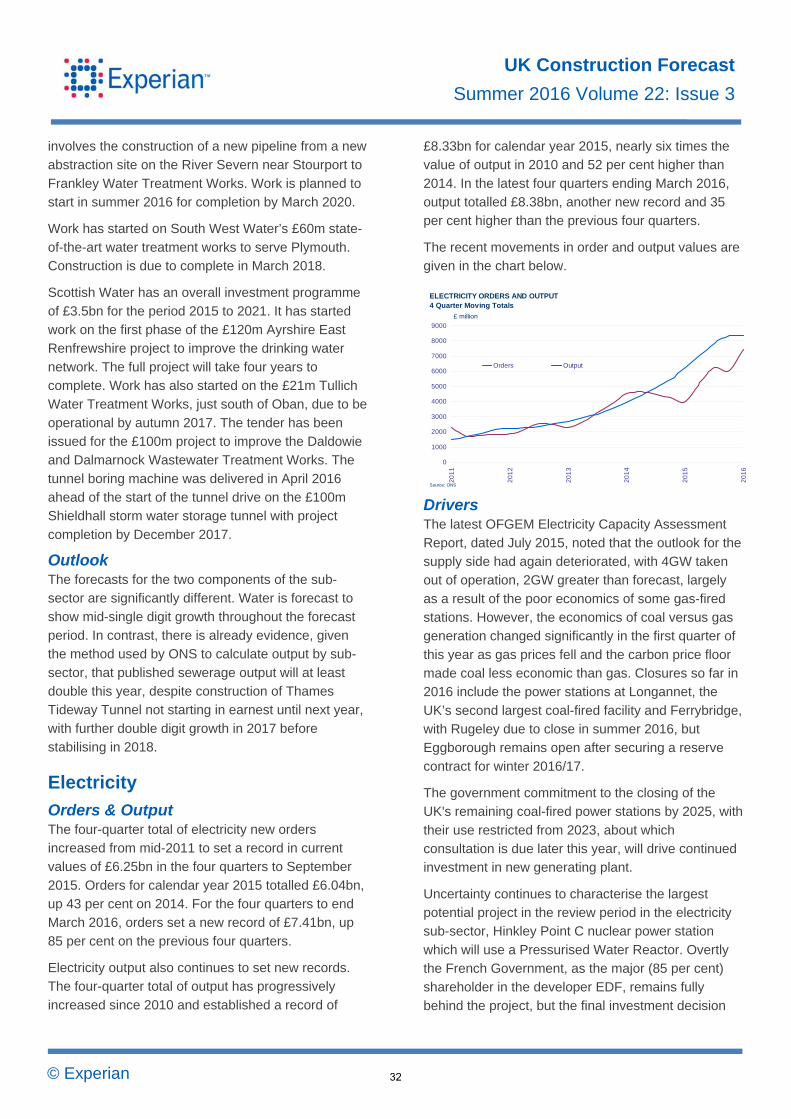

uk construction forecast - · pdf fileuk construction forecast a report by the forecasting...

TRANSCRIPT

UK Construction Forecast A report by the Forecasting Committee for the Construction Industries

Summer 2016 – Volume 22: Issue 3

1

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

A report by the

Forecasting Committee

for the Construction

Industries

This report has been prepared for publication by the Construction Futures team, which is part of Experian’s Economics Unit, with guidance from its Forecasting Committee for the Construction Industries. The members of the committee serve in a personal not a representative capacity. The contribution of the members, and that of the Forecasting Groups (listed in Appendix D), is gratefully acknowledged. Whilst every endeavour has been made to obtain the best available data from appropriate sources, Experian’s Market Insight Division can give no guarantee of accuracy, nor for the applicability of the forecasts for particular decisions. No responsibility is taken for any consequential loss or other effects from these data. Copyright © Experian 2016 ISSN 0308-079X Apart from fair dealing for the purposes of research or private study, or criticism or review, and only as permitted under the Copyright Designs and Patents Act 1998, this publication may only be reproduced, stored or transmitted, in any form or by any means, with the prior permission in writing of the Publishers or in the case of reprographic reproduction in accordance with the terms of the licences issued by the Copyright Licensing Agency in the UK. US copyright law is applicable in the US. Printed by PAPCOM

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

CONTENTS

Page

Executive Summary 1

1. Macroeconomic outlook 7

2. Housing 13

3. Housing repair, maintenance and improvement 18

4. New infrastructure 22

5. Public non-residential construction 38

6. Private industrial construction 44

7. Private commercial construction 48

8. Non-residential repair and maintenance 59

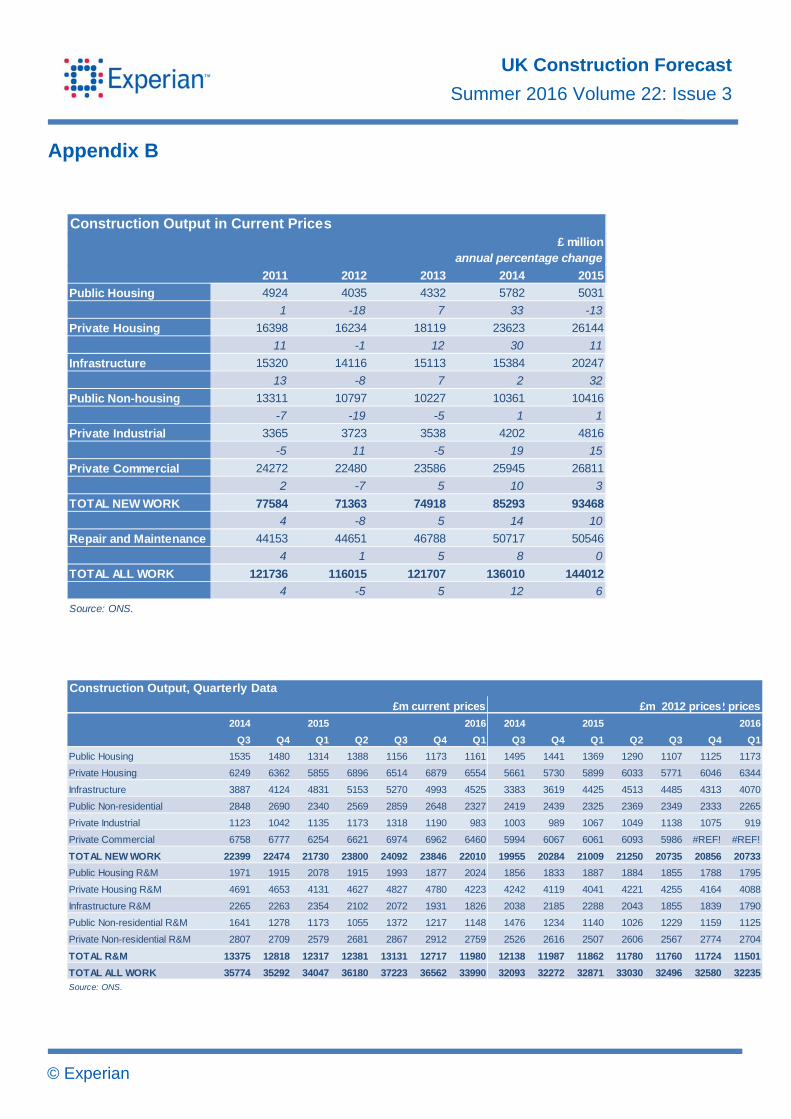

Appendix A: Health and education output Appendix B: Construction output in current prices Appendix C: Definitions: types and examples of construction work Appendix D: Membership of the forecasting committees

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

Executive Summary

Key messages

These forecasts have been assembled prior to the European Union referendum vote on 23rd June. It is too early yet to assess the implications of the vote on either the economy as a whole or construction in particular. However, we have provided an assessment of where we believe the main vulnerabilities lie at the end of this chapter.

Even without the impact of the referendum vote, we believe that the prospects for both the economy and construction have weakened over the three years to 2018 as the global slowdown has impacted growth in the UK.

2016 could be a difficult year for the industry after weak first quarter output results.

Our prognosis for construction is now output growth averaging a little over 1 per cent a year to 2018, with the private housing and commercial sectors the main drivers.

Growth in the infrastructure sector has largely disappeared, affected in large part by the delay in the start of main work on Hinkley Point until 2019. Output, however, will remain close to its current historic high.

Expansion in the repair & maintenance sectors will be very modest as weakness in the public ones largely cancels out growth in the private ones.

Fall in value of sterling could boost exports, at least in the short term

Private housing output should benefit from the Starter Homes Initiative

Thames Tideway to start this year and HS2 in 2018

Forecast highlights

Boom in universities construction slackens off, but still a couple of big projects to come through in London and Glasgow

The office development cycle may be peaking in London but the regional centres are still in the early part of their upswing

Forecast highlights

Impact of referendum result currently unquantifiable but almost certain to be negative

Hinkley Point now delayed until at least 2019

Retail construction continues to struggle in a very competitive environment

Forecast highlights

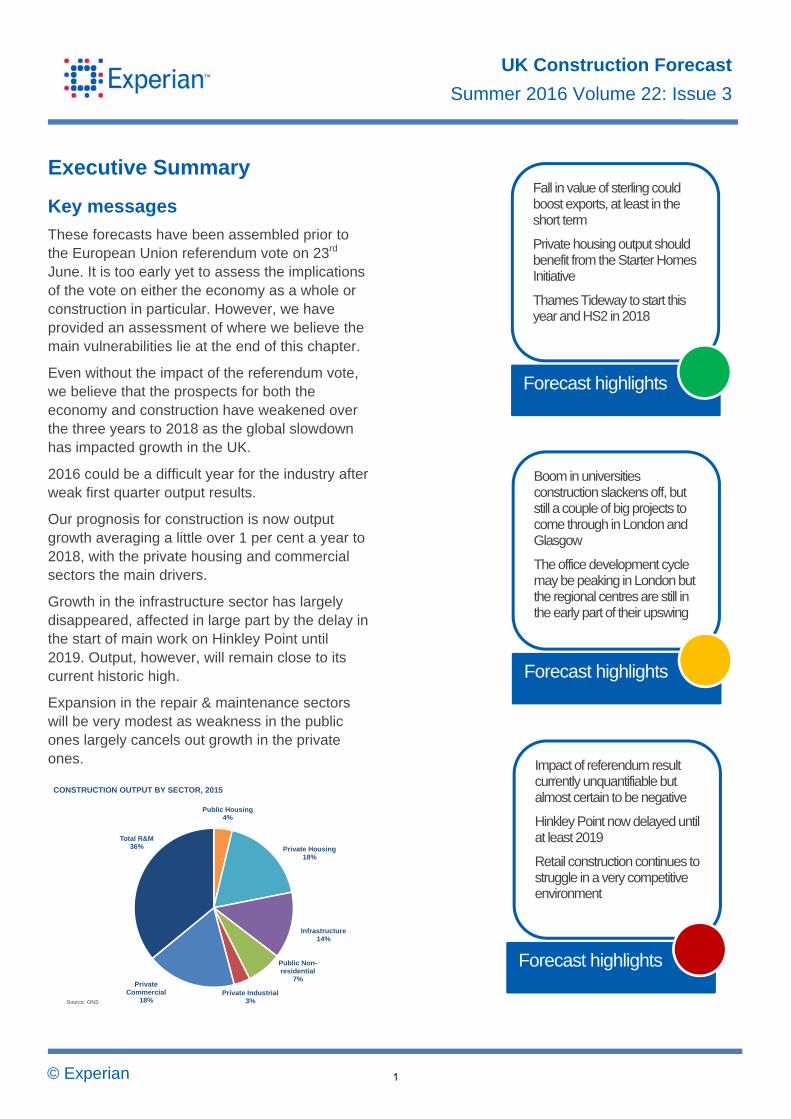

Public Housing4%

Private Housing18%

Infrastructure14%

Public Non-residential

7%

Private Industrial3%

Private Commercial

18%

Total R&M36%

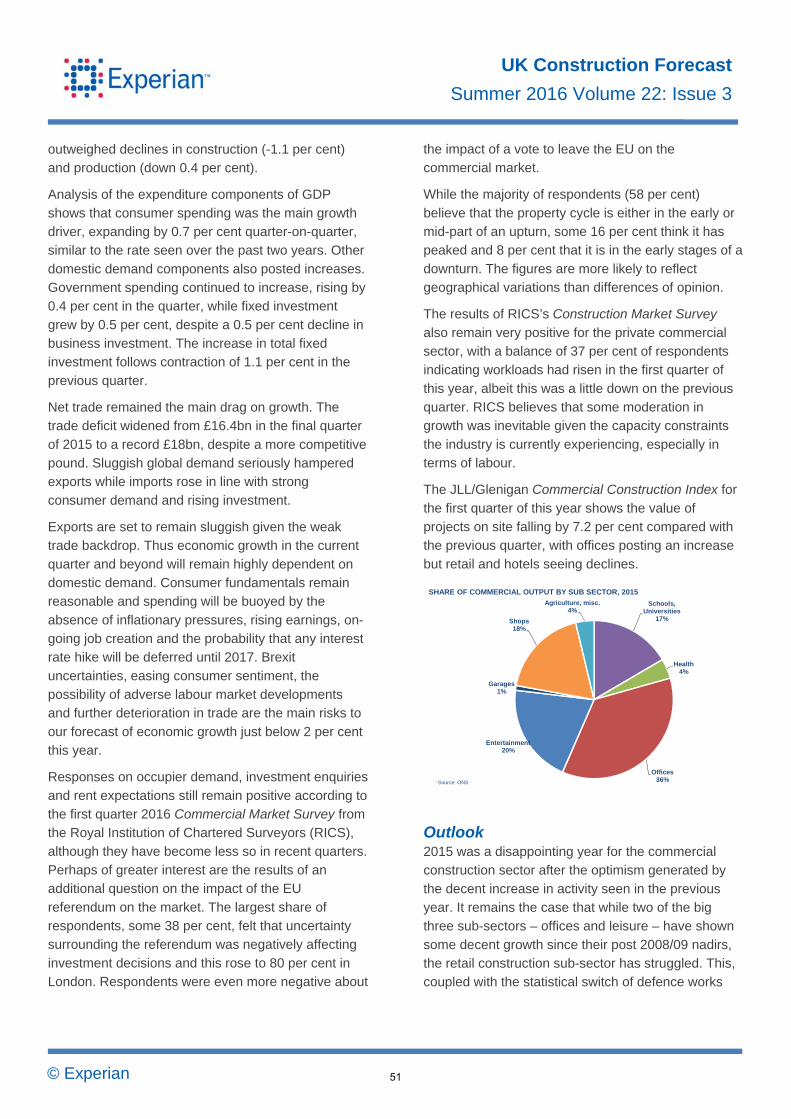

CONSTRUCTION OUTPUT BY SECTOR, 2015

Source: ONS

1

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

The outturn for 2015

After some slight revision, the UK economy grew by 2.3 per cent last year, some way down on its 2014

outturn of 2.9 per cent but still the second best result since 2007.

Household expenditure rose by 2.7 per cent in real

terms and total investment was up by over 4 per cent. Household expenditure growth was driven by a better performance from average earnings coupled with

historically very low inflation and interest rates which meant that consumers saw some real increase in disposable incomes during the course of the year.

Construction output grew by 3.4 per cent in real terms in 2015 according to the Office for National Statistics. However, as mentioned in previous reports we believe

that due to a statistical discontinuity growth last year was overstated and was nearer to 2 per cent.

This statistical discontinuity was centred on the

infrastructure sector and means that the growth of nearly 30 per cent shown in the official data was probably half that. However, this still made the sector

the star performer last year, with strong rises in the electricity and roads sub-sectors.

Public housing output was hit by the almost inevitable

hiatus in investment between the end of one Affordable Housing Programme and the start of another, while growth in private housing had to come

down from the very high level seen in 2014. Total housing starts in Great Britain reached 167,600 last year, a relatively modest 5 per cent increase on 2014

but their highest level since 2007.

Activity in the public non-residential sector continues to be constrained by tight controls on public

expenditure and output subsided for the fifth consecutive year on the back of declines in university, leisure and miscellaneous work.

The industrial construction sector experienced good growth of around 10 per cent in real terms in 2015 buoyed by a second year of strong performance in the

warehouse sub-sector as the return of speculative logistics and distribution building gathered pace.

In contrast 2015 was a disappointing year for the

commercial construction sector after the optimism generated by the decent increase in activity seen in

the previous year. It remains the case that while two of the big three sub-sectors – offices and leisure – have shown some decent growth since their post

2008/09 nadirs, the retail construction sub-sector has struggled against a backdrop of poor performance by the major food retailers, high high street vacancy rates

and continuing growth in online shopping.

The surprise in the repair and maintenance (R&M) sectors was the poor performance of the private

housing element, where output was static despite a good year for average earnings growth and disposable incomes, which tend to drive activity in the

sector.

The outlook to 2018

Towards the end of 2015 and into the first part of this

year there have been signs of a slowdown in the global economy and some leading indicators have been weak.

The Markit/CIPS Purchasing Managers Indices have generally been heading in a downward direction in recent months and in April the manufacturing one fell

below the no change mark of 50, although it did pick up to marginally above it in May.

Growth in retail sales volumes has been relatively

weak, expansion in employment has slowed markedly, and average earnings growth has stuttered. The economic waters were undoubtedly being

muddied by business uncertainty relating to the EU referendum, and the uncertainty is set to continue through at least two years of negotiations as a result

of the vote on 23rd June.

Not surprisingly GDP growth in the first quarter of this year was down on the previous one at 0.4 per cent

and there is reason to believe that it could slip still further in the second quarter.

GDP growth this year and next is expected to be

below 2 per cent annually and will continue to be heavily dependent on domestic demand, which could prove to be fragile in the light of recent events.

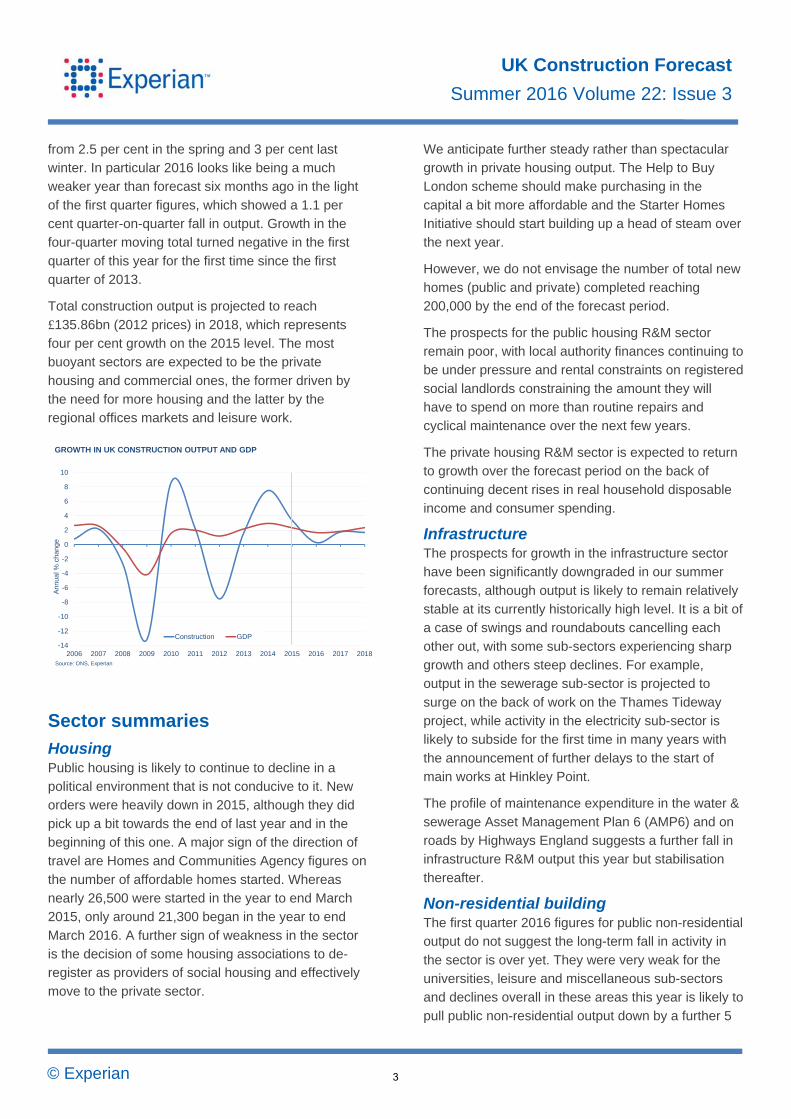

Even without factoring in the referendum result our prognosis for growth in the construction industry has weakened significantly over the next three years, to

just over 1 per cent a year on average in the summer,

2

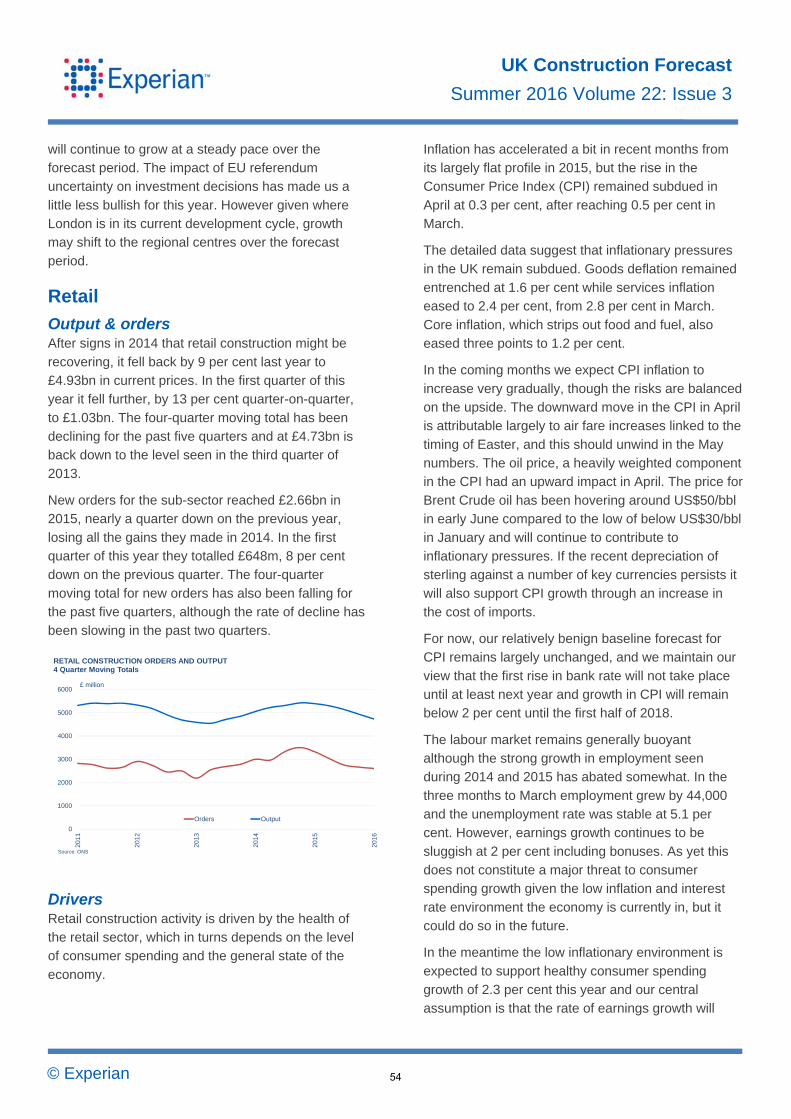

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

from 2.5 per cent in the spring and 3 per cent last winter. In particular 2016 looks like being a much weaker year than forecast six months ago in the light

of the first quarter figures, which showed a 1.1 per cent quarter-on-quarter fall in output. Growth in the four-quarter moving total turned negative in the first

quarter of this year for the first time since the first quarter of 2013.

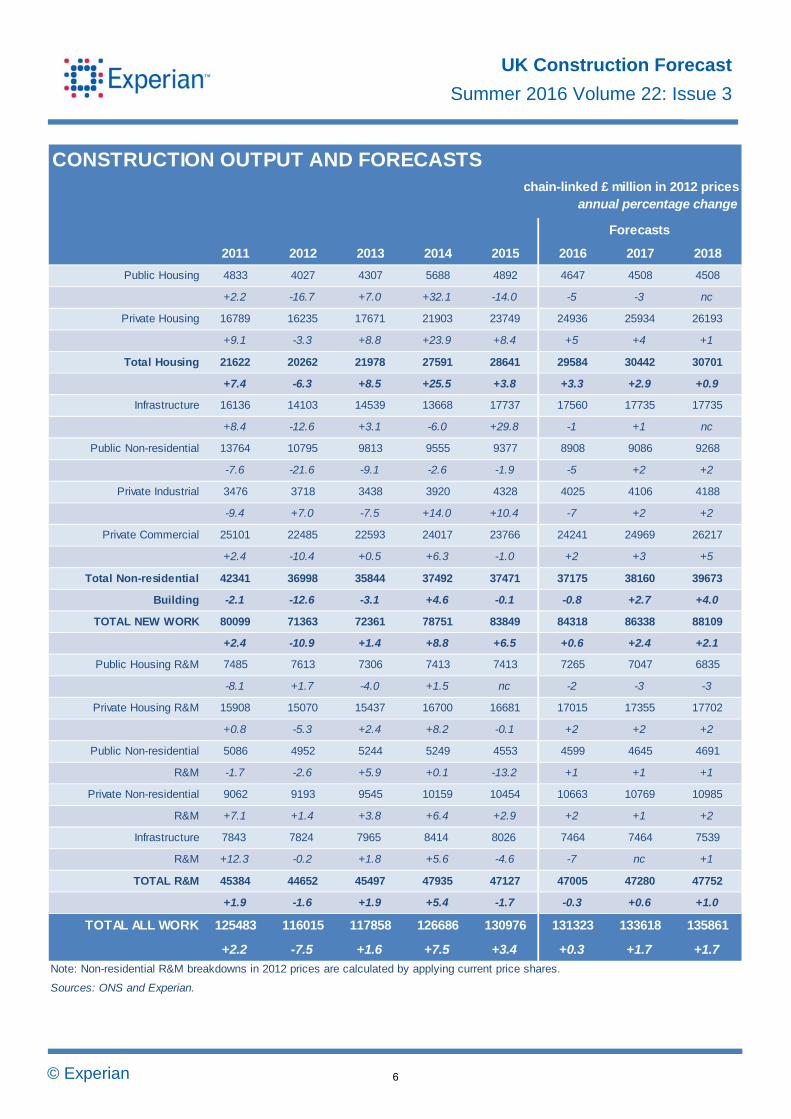

Total construction output is projected to reach

£135.86bn (2012 prices) in 2018, which represents four per cent growth on the 2015 level. The most buoyant sectors are expected to be the private

housing and commercial ones, the former driven by the need for more housing and the latter by the regional offices markets and leisure work.

Sector summaries

Housing Public housing is likely to continue to decline in a political environment that is not conducive to it. New orders were heavily down in 2015, although they did

pick up a bit towards the end of last year and in the beginning of this one. A major sign of the direction of travel are Homes and Communities Agency figures on

the number of affordable homes started. Whereas nearly 26,500 were started in the year to end March 2015, only around 21,300 began in the year to end

March 2016. A further sign of weakness in the sector is the decision of some housing associations to de-register as providers of social housing and effectively

move to the private sector.

We anticipate further steady rather than spectacular growth in private housing output. The Help to Buy London scheme should make purchasing in the

capital a bit more affordable and the Starter Homes Initiative should start building up a head of steam over the next year.

However, we do not envisage the number of total new homes (public and private) completed reaching 200,000 by the end of the forecast period.

The prospects for the public housing R&M sector remain poor, with local authority finances continuing to be under pressure and rental constraints on registered

social landlords constraining the amount they will have to spend on more than routine repairs and cyclical maintenance over the next few years.

The private housing R&M sector is expected to return to growth over the forecast period on the back of continuing decent rises in real household disposable

income and consumer spending.

Infrastructure The prospects for growth in the infrastructure sector have been significantly downgraded in our summer

forecasts, although output is likely to remain relatively stable at its currently historically high level. It is a bit of a case of swings and roundabouts cancelling each

other out, with some sub-sectors experiencing sharp growth and others steep declines. For example, output in the sewerage sub-sector is projected to

surge on the back of work on the Thames Tideway project, while activity in the electricity sub-sector is likely to subside for the first time in many years with

the announcement of further delays to the start of main works at Hinkley Point.

The profile of maintenance expenditure in the water &

sewerage Asset Management Plan 6 (AMP6) and on roads by Highways England suggests a further fall in infrastructure R&M output this year but stabilisation

thereafter.

Non-residential building The first quarter 2016 figures for public non-residential output do not suggest the long-term fall in activity in

the sector is over yet. They were very weak for the universities, leisure and miscellaneous sub-sectors and declines overall in these areas this year is likely to

pull public non-residential output down by a further 5

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Ann

ual %

cha

nge

GROWTH IN UK CONSTRUCTION OUTPUT AND GDP

Construction GDP

Source: ONS, Experian

3

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

per cent. Modest growth is projected for the following two years, driven largely by education and health, the former seeing some expansion on the back of the

commitment to create 600,000 new school places over the next five years, and a couple of large long-term university expansion programmes.

After two years of strong growth, output in the warehouse sector is likely to fall sharply this year and with factory construction remaining flat, total industrial

construction activity is expected to fall. Modest growth is projected for the next two years, largely driven by domestic demand.

The office sub-sector will remain the most buoyant one in commercial construction over the forecast period, continuing the trend of the recent past.

However, the focus of growth in the sub-sector may shift a little from London to the main regional centres. The leisure sub-sector is also expected to experience

good growth, assuming that the £2bn Paramount Park scheme goes ahead. At the other end of the scale, retail construction is likely to subside still further in the

short term, before activity stabilises as the prospects for the big food retailers in particular improve a little.

Some marginal increases in public non-residential

R&M could be seen over the forecast period on the back of rises in allocations under the schools basic needs and school conditions budget.

Private non-residential R&M is expected to do a little better than the public sector, on the back of further progress on the energy efficiency/renewables

agendas of some of the major property holders and on needs of retailers to attract footfall in a very competitive environment.

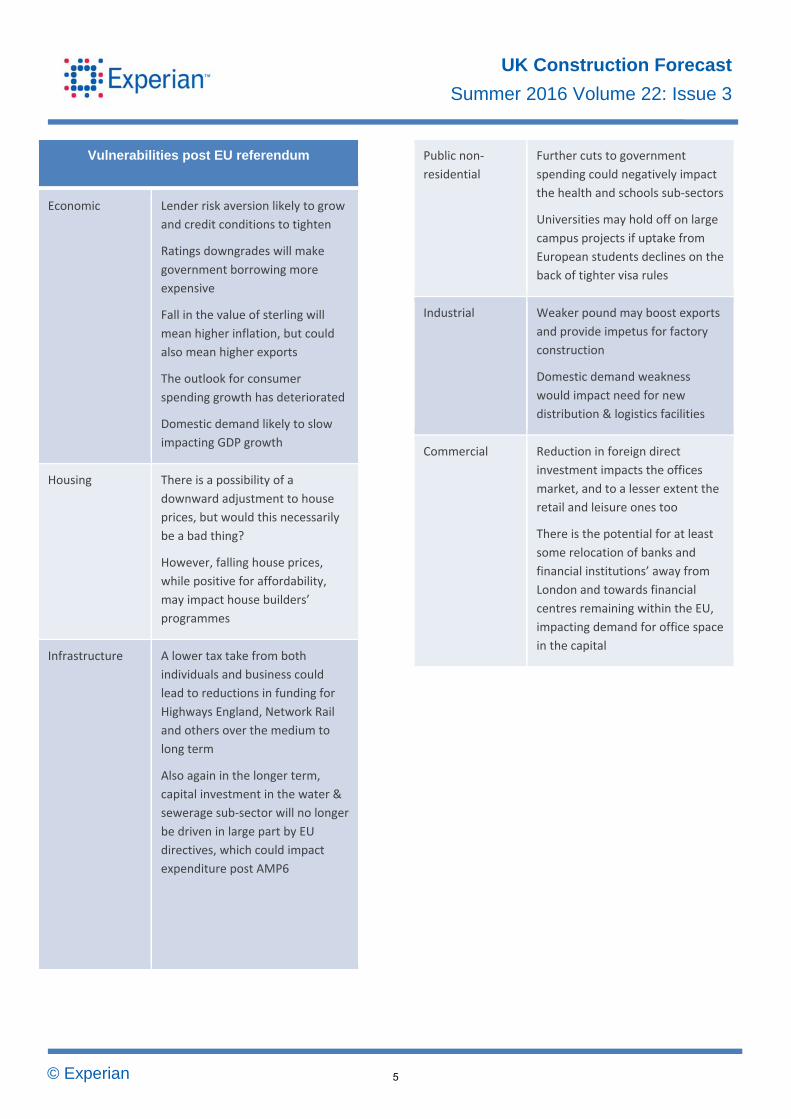

The EU referendum and forecast timings

Our forecasting committees met in May and early

June when our central assumption was the maintenance of the status quo, that is, no change in our relationship with the European Union.

However this has proved not to be the case and on 23rd June the United Kingdom electorate voted narrowly to set in motion the UK’s exit from the EU.

Our economics team will be assessing the implications of this decision over the next few weeks as the dust settles on the early turmoil it has caused

and the respective negotiating positions of the UK government and those leading the EU side become clearer.

We will therefore hopefully be in a position to assess at least some of the implications for construction in our Autumn Update and Winter Forecast. In the

meantime, we have highlighted in the following table where we see the major vulnerabilities to the construction sector lying.

-15

-10

-5

0

5

10

15

PublicHousing

PrivateHousing

Infrastructure Public Non-residential

PrivateIndustrial

PrivateCommercial

Total R&M AllConstruction

GROWTH IN CONSTRUCTION OUTPUT BY SECTOR, 2016 TO 2018

% change

Source: Experian

4

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

Vulnerabilities post EU referendum

Economic Lender risk aversion likely to grow

and credit conditions to tighten

Ratings downgrades will make

government borrowing more

expensive

Fall in the value of sterling will

mean higher inflation, but could

also mean higher exports

The outlook for consumer

spending growth has deteriorated

Domestic demand likely to slow

impacting GDP growth

Housing There is a possibility of a

downward adjustment to house

prices, but would this necessarily

be a bad thing?

However, falling house prices,

while positive for affordability,

may impact house builders’

programmes

Infrastructure A lower tax take from both

individuals and business could

lead to reductions in funding for

Highways England, Network Rail

and others over the medium to

long term

Also again in the longer term,

capital investment in the water &

sewerage sub‐sector will no longer

be driven in large part by EU

directives, which could impact

expenditure post AMP6

Public non‐

residential

Further cuts to government

spending could negatively impact

the health and schools sub‐sectors

Universities may hold off on large

campus projects if uptake from

European students declines on the

back of tighter visa rules

Industrial Weaker pound may boost exports

and provide impetus for factory

construction

Domestic demand weakness

would impact need for new

distribution & logistics facilities

Commercial Reduction in foreign direct

investment impacts the offices

market, and to a lesser extent the

retail and leisure ones too

There is the potential for at least

some relocation of banks and

financial institutions’ away from

London and towards financial

centres remaining within the EU,

impacting demand for office space

in the capital

5

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

CONSTRUCTION OUTPUT AND FORECASTSchain-linked £ million in 2012 prices

annual percentage change

2011 2012 2013 2014 2015 2016 2017 2018

Public Housing 4833 4027 4307 5688 4892 4647 4508 4508

+2.2 -16.7 +7.0 +32.1 -14.0 -5 -3 nc

Private Housing 16789 16235 17671 21903 23749 24936 25934 26193

+9.1 -3.3 +8.8 +23.9 +8.4 +5 +4 +1

Total Housing 21622 20262 21978 27591 28641 29584 30442 30701

+7.4 -6.3 +8.5 +25.5 +3.8 +3.3 +2.9 +0.9

Infrastructure 16136 14103 14539 13668 17737 17560 17735 17735

+8.4 -12.6 +3.1 -6.0 +29.8 -1 +1 nc

Public Non-residential 13764 10795 9813 9555 9377 8908 9086 9268

-7.6 -21.6 -9.1 -2.6 -1.9 -5 +2 +2

Private Industrial 3476 3718 3438 3920 4328 4025 4106 4188

-9.4 +7.0 -7.5 +14.0 +10.4 -7 +2 +2

Private Commercial 25101 22485 22593 24017 23766 24241 24969 26217

+2.4 -10.4 +0.5 +6.3 -1.0 +2 +3 +5

Total Non-residential 42341 36998 35844 37492 37471 37175 38160 39673

Building -2.1 -12.6 -3.1 +4.6 -0.1 -0.8 +2.7 +4.0

TOTAL NEW WORK 80099 71363 72361 78751 83849 84318 86338 88109

+2.4 -10.9 +1.4 +8.8 +6.5 +0.6 +2.4 +2.1

Public Housing R&M 7485 7613 7306 7413 7413 7265 7047 6835

-8.1 +1.7 -4.0 +1.5 nc -2 -3 -3

Private Housing R&M 15908 15070 15437 16700 16681 17015 17355 17702

+0.8 -5.3 +2.4 +8.2 -0.1 +2 +2 +2

Public Non-residential 5086 4952 5244 5249 4553 4599 4645 4691

R&M -1.7 -2.6 +5.9 +0.1 -13.2 +1 +1 +1

Private Non-residential 9062 9193 9545 10159 10454 10663 10769 10985

R&M +7.1 +1.4 +3.8 +6.4 +2.9 +2 +1 +2

Infrastructure 7843 7824 7965 8414 8026 7464 7464 7539

R&M +12.3 -0.2 +1.8 +5.6 -4.6 -7 nc +1

TOTAL R&M 45384 44652 45497 47935 47127 47005 47280 47752

+1.9 -1.6 +1.9 +5.4 -1.7 -0.3 +0.6 +1.0

TOTAL ALL WORK 125483 116015 117858 126686 130976 131323 133618 135861

+2.2 -7.5 +1.6 +7.5 +3.4 +0.3 +1.7 +1.7

Note: Non-residential R&M breakdowns in 2012 prices are calculated by applying current price shares.

Sources: ONS and Experian.

Forecasts

6

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

1 The Macroeconomic Outlook

Global background

Output and trade The softness of the global economy continues to create widespread concern. Trade - formerly a key driver of global growth – remains extremely sluggish

depressing output growth in most economies. In some cases –e.g. the US, China and India – domestic demand is underpinning expansion, but growth rates

are generally disappointing. Where domestic demand is weak, in Japan and the Eurozone for example, GDP growth is lacklustre and provides little opportunity for

trading partners to boost exports.

Among the slow-growing economies, Japan remains firmly in the doldrums with GDP growth forecast at just

0.5 per cent this year and next, with little hope of a significant improvement thereafter. Conditions are stronger in the Eurozone where consumer spending is

expected to reach 1.7 per cent in 2016 and remain near that rate in 2017 and 2018, underpinning GDP growth at near 1.6 per cent in 2016 and 2017,

perhaps rising to 2 per cent by 2018. Growth at this pace seems insufficient on the evidence of recent trade data to prevent net trade remaining a severe

drag on UK growth prospects but the position should gradually improve once Eurozone growth matches or surpasses the UK rate.

In the US, the underlying performance remains solid, supported by buoyant consumer spending which in April was the strongest for six years. GDP growth is

forecast at 2 per cent this year and is likely to be between 2.3 and 2.5 per cent in 2017 and 2018.

Key Global Risks

Geopolitical Political tensions and unresolved

crises (notably in the Middle East)

have produced the largest number

of refugees globally for 60 years.

This is de‐stabilising and increases

the risk of loss of confidence,

political over‐reaction and the

emergence of unstable regimes.

Terrorist attacks Additional threats to morale stem

from terrorism which can de‐

stabilise government and hamper

economic progress.

2007/08 Legacy Several advanced economies and

some emerging markets are still

dealing with the legacy of the

2007/08 financial crisis. High

private and/or public debt will

continue to pose a threat to

economic growth prospects and

financial stability.

Brexit While primarily affecting the UK,

the outcome of the referendum

has profound implications for the

whole of the EU. The ‘leave ‘vote

could result in EU‐wide instability.

2014 2015 2016 2017 2018

GDP 2.9 2.3 1.7 1.8 2.3

Household consumption 2.5 2.7 2.4 2.3 2.2

Government consumption 2.5 1.5 0.7 -1.1 -0.3

Gross fixed investment 7.3 4.1 0.8 2.8 3.6

Bank Rate (average for year) 0.5 0.5 0.5 0.6 1.1

CPI (annual) 1.4 0.1 0.7 1.4 2.0Source: ONS, Experian.

KEY UK MACROECONOMIC INDICATORS

annual percentage change (unless otherwise stated)

ForecastsActual

7

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

Growth in much of Asia is faltering in the face of a weak trade backdrop but remains buoyant by Western standards. China is shifting to a consumption-based

growth model and despite widespread worries about a sharp slowdown, the country’s GDP growth is still expected to reach 6.5 per cent in 2016 and remain

comfortably above 6 per cent in the following two years. Even stronger rates of growth, over 7.5 per cent per annum, are generally forecast for India in

2016-18. Other developing countries in the region (Indonesia, Malaysia, Philippines) are also expected to remain on a robust growth path.

The global economy is expected to see growth accelerate from a modest 3.2 per cent in 2016 to 3.8 per cent in 2017 and 4 per cent in 2018. This will help

world trade volumes pick up from the depressed level of recent years providing better opportunities for UK export sales. But much will depend on the strength

and sustainability of a Eurozone recovery; on the outcome of the Brexit vote; and on trade negotiations in the event of the UK leaving the EU.

The UK economy

Upswing continues but at a slower pace The UK economy is still expanding but at a slower pace than in recent years as EU referendum

uncertainties hit business investment, net trade has become a major drag on growth and consumer spending, while still buoyant, is easing. Consumer

fundamentals are less positive than in recent years and Brexit uncertainties have undermined confidence.

GDP growth slowed to 0.4 per cent quarter-on-quarter

in the first quarter of 2016, from 0.6 per cent in the previous three months. Two of the four main industrial groupings showed growth - services output rose by

0.6 per cent marking the 13th consecutive quarter of steady growth continuing to underpin overall expansion. Within the sector, distribution, hotels &

catering output increased by a robust 1.1 per cent, with wholesale and retail trade making a prominent contribution. The service sector’s performance

outweighed estimated declines in construction (-1.1 per cent) and production (down 0.4 per cent). Within production, manufacturing showed a decline of 0.4 per

cent taking the cumulative decline in the year to the first quarter of 2016 to 1.3 per cent, highlighting the

challenging global trade backdrop for exporters over the past year. However, output data for April was unexpectedly buoyant, rising by 2.3 per cent, the

fastest since 2012. It remains to be seen whether this is a blip or the beginning of better times for the sector.

Among the expenditure components of GDP

consumer spending was the main growth driver in the first quarter of the year, expanding by 0.7 per cent quarter-on-quarter, similar to the quarterly rate seen

over the past two years. Other domestic demand components also posted increases. Government spending continued to increase, rising by 0.4 per cent

in the quarter, while fixed investment grew by 0.5 per cent, despite a 0.5 per cent decline in business investment. The increase in total fixed investment

follows contraction of 1.1 per cent in the previous quarter.

Net trade remained the main drag on growth. The

trade deficit widened from £16.4bn in the final quarter of 2015 to a record £18bn, despite a more competitive pound. Sluggish global demand seriously hampered

exports while imports rose in line with strong consumer demand and rising investment. As with manufacturing output, data for April showed a

welcome upturn, with exports rising at their strongest pace since 2003.

Despite the improved manufacturing and trade

figures, early indications for the second quarter of 2016 are generally weak, pointing to even slower expansion than in the first quarter. The Markit/CIPS

Purchasing Managers’ index for the service sector, which accounts for some 75 per cent of growth, picked up slightly in May but remains subdued while

the manufacturing and construction PMIs are only just in expansionary territory. Taken together, these indicators point to sluggish growth in the second

quarter of 2016.

Two year outlook Growth prospects in the next two years remain heavily dependent on the continued buoyancy of domestic

spending given that the weak global backdrop implies challenging times for exporters. Within domestic demand, the onus is firmly on consumer spending as

the constraints on government spending persist and

8

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

business investment is subject to EU referendum uncertainties.

We expect resilience in consumer spending to persist

in the next few quarters but forecast more moderate gains than in the past two years as conditions become less favourable. Output growth is slowing,

employment creation is moderating, unemployment has virtually stabilised and earnings growth is still stuck at a weak 2 per cent year-on-year. Meanwhile

inflation is likely to pick up gradually in the remaining months of this year and into 2017.

All these developments have been factored into our

forecasts of consumer spending growth for some time so our latest forecast of expansion in household spending is substantially unchanged at 2.4 per cent

for this year. With official interest rates unlikely to begin rising until the first quarter of 2017, most households will not feel a significant impact until late

2017. This means that despite rising inflation and ongoing fiscal austerity household spending can continue to advance at a solid pace, 2.3 per cent, in

2017.

Difficult conditions for exporters mean that trade weakness is likely to continue. At the same time,

government spending will still be constrained by fiscal tightness. But the expected resilience of consumers will underpin GDP growth near 2 per cent a year in

2016-18.

There are tentative signs that conditions in the Eurozone are improving. Any sustained improvement

should mean that net trade will become less of a drag on GDP expansion in the UK, and might even make a positive contribution earlier than expected in the base

case. This gives an upside risk to our central forecast of GDP growth for the next few years.

Consumer spending and investment Real incomes rose by 3.3 per cent in 2015, the

strongest outcome since 2001. This underpinned a boom period for consumers with spending growing by a total of 5.2 per cent in 2014 and 2015.

While this boom is over, household spending is still growing at a solid pace benefiting from modest employment creation, low inflation and wage growth

around 2 per cent a year. Real incomes growth is expected to reach 2.6 per cent this year and 2.4 per

cent in 2017 and 2018. Despite weaker consumer confidence than in recent years, we still expect consumer spending growth to reach 2.4 per cent this

year followed by similar rates of growth in 2017 and 2018.

Fixed investment picked up markedly in 2013-15 but

has faltered this year depressed by Brexit fears and weak house building. Investment in the remainder of 2016 and in 2017-18 will be supported by the

resilience of consumer spending and the low cost of finance, but is subject to huge uncertainty ahead of the EU referendum outcome. In our central case we

expect investment growth to average 2.9 per cent in the three years 2016-18.

Public finances Efforts to reduce the public sector deficit are

progressing but at a slower pace than planned. Net borrowing has been significantly reduced, from 9 per cent of GDP in 2010 to 4.4 per cent in 2015, but

remains substantial at £76bn in 2015/16 against the target of £72bn. A deficit of this magnitude means that borrowing as a percentage of GDP is still rising

steadily and last year reached almost 90 per cent of GDP compared with 74 per cent in 2010.

The financial year 2016/17 got off to a poor start for the chancellor as he plans to reduce borrowing to £56.5bn this financial year and run a budget surplus

by the end of the decade. Government borrowing in April was £8.2bn, well above expectations despite a rise in income tax, stamp duty, national insurance and

VAT receipts. The government borrowed £9.7bn in May, slightly above expectations. The disappointing outcome for the first two months of the financial year

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

An

nu

al %

ch

ang

e

CONSTRUCTION OUTPUT VS CONSUMER SPENDING AND INVESTMENT

Construction output

Consumer spending

Investment

Source : ONS, Experian

9

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

suggests that the chancellor will struggle to reduce borrowing this year to the extent set out in the budget.

Labour market moderating The labour market continues to make progress

despite a marked easing of output growth in recent months. The key points comparing the three months to March 2016 with the previous three months are:

• Employment rose by 44,000. The number of employees was up 27,000, accompanied by a rise of 20,000 in self-employment;

• The number of full-time employees was up 47,000, while the number working part time fell by 3,000;

• Unemployment decreased by 2,000 to 1.69 million;

• The unemployment rate remained at 5.1 per cent.

• Average weekly earnings including bonuses rose by 2per cent compared with a year earlier. Pay

excluding bonuses was 2.1 per cent higher.

On balance the latest figures are mildly encouraging given prevailing Brexit uncertainties and weak output

growth. While they indicate a cooling off from the period of vigorous employment growth and steadily falling unemployment seen in 2014 and 2015 when

the economy was growing strongly, this phase could not be expected to continue indefinitely.

The persistence of sluggish earnings growth, up only

2 per cent, does not yet constitute a major threat to consumer spending on which the UK economy is heavily reliant. The still benign rate of inflation

provides scope for strong gains in real disposable income providing a solid foundation for consumer spending growth.

Inflation to pick up but remain very low this year The Consumer Prices Index (CPI) rose by 0.3 per cent in the year to April, down from 0.5 per cent in the year to March.

The main downward contribution came from transport where prices fell by 0.1 per cent between March and April this year compared with a rise of 1.1 per cent

between the same two months a year earlier. By far the largest effect came from air transport. The timing of Easter this year caused a large increase in fares

between February and March and a subsequent fall in

April. These downward effects were partially offset by an upward contribution from motor fuels.

The latest data suggest that inflationary pressures in

the UK remain subdued. Goods deflation remained entrenched at 1.6 per cent while services inflation eased to 2.4 cent from 2.8 per cent in March. Core

inflation, which strips out food and fuel, also eased three percentage points to 1.2 per cent.

In the coming months we expect CPI inflation to

increase very gradually, though the risks are balanced on the upside. The price for Brent Crude oil is now approaching US$50/bbl compared to the low of below

US$30/bbl in January and will continue to contribute to inflationary pressures. The depreciation of sterling in the last few months of 2015 will also support CPI

growth through an increase in the cost of imports.

Interest rates – no move expected until the first quarter of 2017 Weaker economic growth, low inflation and modest rises in wage costs point to no early rise in official

rates. The latest published vote of the Monetary Policy Committee at their May meeting was unanimous to maintain Bank Rate at 0.5 per cent. We expect the

first rise, a 25 basis point increase taking Bank Rate to 0.75 per cent, to take place in the first quarter of 2017.

When Bank Rate does begin to rise, we expect it to do so far more gradually than in previous cycles given the persistence of headwinds together with the legacy

of the financial crisis. Our specific forecast is for 25 basis point increases every other quarter, taking the rate to 1.7 per cent by the first quarter of 2019.

Sterling still vulnerable Sterling has fallen sharply against the euro and the looming Brexit threat suggests no early recovery. The pound is vulnerable to a ‘leave’ vote on 23 June. In

our base case, sterling is likely to settle in the range Euro1.24-1.28/£ in the next few months. Against the dollar we expect the pound to trade in a range

between $1.42-1.47/£ in the near term.

Growth moderating and risks persist The economy has enjoyed a strong recovery, robust job creation and falling inflation in recent years. We expect progress to be sustained but at a more

10

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

moderate pace. Downside risks to this slower growth scenario are:

The most significant risk is dependence for overall

growth on consumer demand. If consumer spending falters, for example through weak earnings growth or significant loss of confidence in economic prospects,

our central forecast of growth at near 2 per cent a year in 2016-18 would be threatened. But there is a modest upside risk that UK growth will be better than

in the central case if the recent modest Eurozone recovery is sustained and provides an unexpectedly strong boost to exports.

Uncertainty regarding the UK’s future in the EU could continue to depress investment and lead to further sterling depreciation. This is a major risk to our

forecast of GDP growth at 1.7% this year.

Output gains are still driven by rising employment with little improvement in productivity, making it difficult for

significant earnings growth to occur. If pay growth subsides or even fails to accelerate, then our forecast of household consumption growth will need to be

downgraded.

The weakness in the global trade and financial backdrop is a key risk. A further marked decline in world trade would result in even weaker export

growth. Sterling’s decline against the euro will do little to offset the impact of weak demand.

Fiscal policy will remain tight. At the same time

monetary policy, which has been extremely accommodative during the great recession and its aftermath, is set to tighten gradually from 2017. There

is a risk that the economy may not be strong enough to cope with this dual policy constraint. A particular threat to heavily-indebted households comes from the

prospect of a rise in interest rates before real incomes are increasing at a healthy pace.

While risks are still skewed to the downside, there are

two upside risks. The removal of Brexit uncertainties could result in a rebound in fixed investment in the second half of the year. And if the unexpectedly

strong April export numbers prove to be the turning point for net trade and manufacturing, there would be a boost to growth prospects.,

11

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

% change year-on-year in real terms unless otherwise stated

2014 2015 2016 2017 2018

OUTPUT AND UNEMPLOYMENT

GDP 2.9 2.3 1.7 1.8 2.3

Manufacturing output 2.1 -0.4 -1.1 0.5 1.6

Unemployment rate (ILO - %) 6.2 5.4 5.0 4.9 4.9

HOUSEHOLDS (incl. NPISH)

Consumption 2.5 2.7 2.4 2.3 2.2

Real household disposable income 0.7 3.3 2.6 2.4 2.4

Savings ratio (%) 5.4 4.2 4.1 4.3 4.6 Total household income (current prices) 2.6 2.6 3.7 3.9 4.3

GROSS CAPITAL FORMATION

Gross fixed investment 7.3 4.1 0.8 2.8 3.6

General government 5.8 1.5 -0.1 0.5 0.0

Business investment 4.7 5.2 -0.6 2.9 3.1

Private sector dwellings 14.0 3.5 4.1 4.2 6.5

Public sector dwellings 5.5 18.2 -4.6 0.5 0.0

OTHER EXPENDITURE

Government consumption 2.5 1.5 0.7 -1.1 -0.3

Exports (G & S) 1.2 5.1 1.6 4.2 4.5

Imports (G & S) 2.4 6.3 3.8 3.5 3.1

WORLD VARIABLES

Volume of world trade 3.6 3.9 4.8 4.9 5.3

World GDP 3.4 3.2 3.8 4.0 4.2

Eurozone GDP 0.9 1.5 1.7 1.8 2.0

*Brent crude oil price ($ per barrel) 97.8 53.6 38.3 48.5 59.4

INTEREST AND EXCHANGE RATES (year averages)

Sterling - US Dollar exchange rate 0.61 0.65 0.69 0.65 0.65

Sterling - Euro exchange rate 0.81 0.73 0.80 0.76 0.77

Bank Rate (%) 0.5 0.5 0.5 0.6 1.1

- quarter 4 average 0.5 0.5 0.5 0.8 1.3

Govt 10yr bond yield (%) 2.5 1.8 1.7 2.0 2.6

COSTS AND PRICES

Retail Price Index (Q4) 1.9 1.0 2.6 3.2 3.3

CPI (annual) 1.4 0.1 0.7 1.4 2.0

House prices (year-on-year - DCLG measure) 10.0 6.7 6.7 3.6 3.1

Source: ONS, Experian.

MACROECONOMIC FORECASTS

Forecasts

12

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

2 New Housing

Summary A number of private housing market indicators – output, gross mortgage lending and property transactions all point towards a flurry of activity in the run up to April. This is most likely due to the changes that came into force in April which saw purchasers of second homes and buy-to-let landlords paying a 3 per cent surcharge on each Stamp Duty band.

Currently there is a lull after the pre-Stamp Duty rush. Monthly property transactions figures have gone from 153,300 in March to just 89,700 in May.

Overall, moderate growth has been predicted for private housing output over the next three years. By 2018, the sector should be at an all-time high. Help to Buy London, the latest government initiative that was implemented in February should provide an upside risk to the forecasts. There is a significant downside risk that the negotiations of the UK’s exit from the EU will lead to a prolonged period of uncertainty, reducing consumer confidence and overall spending in the economy.

The outlook for public housing output is still gloomy with local authority budget constraints and rent reductions taking their toll on the sector. Last year one of the biggest registered social landlords, Genesis Housing Association announced that it would stop building social housing due to the difficult operating environment and instead provide homes for the private sector. It remains to be seen whether these tough conditions lead to many more housing associations deciding to de-register as social housing

providers and start behaving like private house builders.

Public Housing

Output & orders After reaching a new high in 2014, last year public housing output went down by 14 per cent to £4.89bn

in 2012 prices. However, in the first quarter of 2016 it rose by 4 per cent to £1.17bn compared with three months earlier. In contrast, on a four-quarter moving

total basis, output decreased for the fourth successive quarter between January and March 2016.

Public housing orders dropped for the second year

running in 2015, by 28 per cent to £1.32bn. In the first three months of 2016, orders increased by 6 per cent to £438m compared with the previous quarter. On a

four-quarter moving total basis, orders went up for the second successive quarter in the first quarter of this year.

Starts & completions The Welsh government discontinued publication of housing starts data broken down by tenure in April 2011 due to concerns over the accuracy of the split

between public and private. Due to the relatively small number of public housing starts in Wales, in terms of analysis, we include these in the private housing

sector.

In 2015, the number of English and Scottish public housing starts declined by 5 per cent to 28,344 units

compared with the previous year. While English starts

2011 2012 2013 2014 2015 2016 2017 2018

Private Housebuilding

£ million (2012 prices) 16789 16235 17671 21903 23749 24936 25934 26193

Annual % Change 9.1 -3.3 8.8 23.9 8.4 5.0 4.0 1.0

Public Housebuilding

£ million (2012 prices) 4833 4027 4307 5688 4892 4647 4508 4508

Annual % Change 2.2 -16.7 7.0 32.1 -14.0 -5.0 -3.0 0.0

All Housing

£ million (2012 prices) 21622 20262 21978 27591 28641 29584 30442 30701

Annual % Change 7.4 -6.3 8.5 25.5 3.8 3.3 2.9 0.9

Source: ONS and Experian.

ForecastHousing Construction Output

13

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

decreased by 3 per cent to 24,520 units, the Scottish ones dropped by 14 per cent, to 3,824 units.

English public housing starts have been released for the first quarter of this year. At 5,590, they were down by 7 per cent compared with three months earlier and

declined by 19 per cent compared with the corresponding period in the preceding year.

Last year, GB public housing completions grew by 23

per cent, to 36,203 units, compared with the corresponding period in the preceding year. Wales saw the greatest rise of 55 per cent to 1,187 units

whilst completions in England (31,220 units) and Scotland (3,796 units) rose by 24 per cent and 13 per cent respectively.

During the first quarter of this year English completions fell by 20 per cent to 5,630 compared with three months earlier, and Welsh ones declined by

40 per cent to 192 units.

Drivers For the 2016-2021 Shared Ownership and Affordable Homes Programme (SOAHP) the announcement of

initial allocations will be made in early/mid-December. However, as mentioned previously, around 90 per cent of the capital funding will be spread over the final

three years of the programme. The vast majority of homes being built under the SOAHP will be for shared ownership. As these homes will eventually be owned

by individuals they should be classed under the private housing sector.

Genesis Housing Association announced last year

that due to the tough conditions the sector is going through, it was no longer going to build social housing and instead only build properties for rent at full market

rates, for shared ownership, or for sale. Since the beginning of 2016, there have been three voluntary de-registrations of registered social landlords. It may

be the case that as poor conditions in the sector continue, the number of voluntary de-registrations increases in the months ahead.

Whilst social rents in England are to decline by 1 per cent per annum, the opposite is true for Wales. Between 2014 and 2019 the Welsh Government

stated that there would be a rise in social rents for registered social landlords, linked to September’s Consumer Price Index in the previous year. However,

2011 2434 -21.3 4833 2.2

2012 2257 -7.3 4027 -16.7

2013 3656 62.0 4307 7.0

2014 1820 -50.2 5688 32.1

2015 1315 -27.7 4892 -14.0

2014 Q3 389 -62.8 1495 37.9

Q4 318 -67.0 1441 17.2

2015 Q1 303 -42.9 1369 2.3

Q2 328 -43.6 1290 -8.8

Q3 272 -30.1 1107 -26.0

Q4 413 29.9 1125 -21.9

2016 Q1 438 44.6 1173 -14.3

Source: ONS.

% change y-on-y

% change y-on-y

Orders Output

£ million (2005 prices)

£ million (2012 prices)

Public Housing Orders And Output

2011 2012 2013 2014 2015 2016 2017 2018

Private Housing

Starts 103.2 96.4 115.5 129.1 139.3 148 158 160

Completions 100.5 103.7 102.3 110.3 127.6 143 153 158

Social Housing

Starts 29.9 24.4 28.7 29.7 28.3 25 24 24

Completions 34.3 32.2 27.8 29.3 36.2 33 27 28

Total

Starts 133.0 120.8 144.2 158.8 167.6 173 182 184

Completions 134.9 136.0 130.0 139.6 163.8 176 180 186

Note: starts and completions forecasts are rounded to the nearest thousand.

Welsh housing starts no longer split betw een private and public thus are allocated to the private sector as the largest element

Starter homes are classed as private homes.

Source: CLG and Experian.

Forecasts Housing Starts and Completions 000s

14

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

the Welsh Government has recently reviewed this policy and on the back of this, the Minster for Communities and Tackling Poverty has agreed to

maintain the current social housing rents policy for 2016/17. At present it is unclear whether this policy in will change from its current form in 2017/2018 and

2018/19.

As part of the North Halifax Transformation Project, Wates has won a contract to build 500 homes on

Calderdale council and Pennine Housing Association sites. A number of homes are to be provided for older or disabled individuals which meet their care and

support needs.

Leeds & Yorkshire Housing Association has appointed United Living Group to provide 23 new affordable rent

apartments on the outskirts of Leeds city centre. Demolition work began in December last year.

As part of a housing scheme in Stockton-On-Tees,

around 70 to 100 affordable units have been planned with work expected to commence this year.

Outlook Given the uptick in public housing output and orders in

the first quarter of 2016, we now expect a smaller fall in the sector’s output for this year. The forecasts for the following two years are unchanged and by 2018

output is predicted to be around 79 per cent of its 2014 peak.

Private Housing

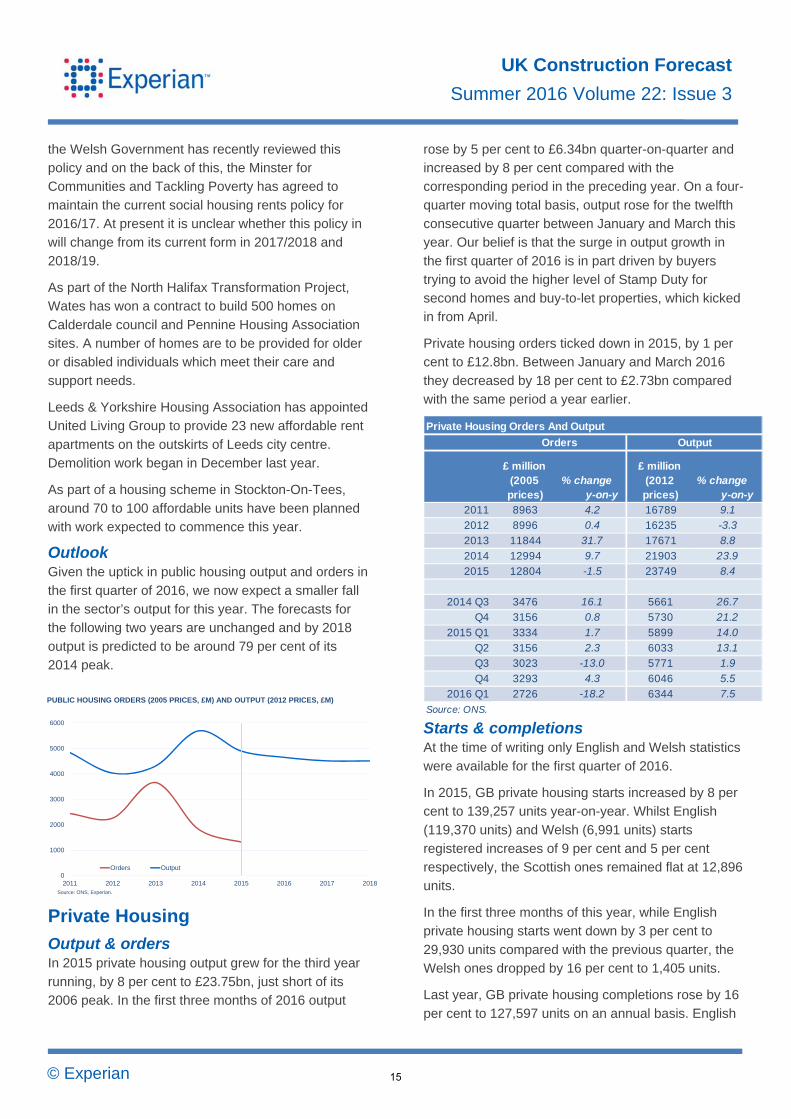

Output & orders In 2015 private housing output grew for the third year

running, by 8 per cent to £23.75bn, just short of its 2006 peak. In the first three months of 2016 output

rose by 5 per cent to £6.34bn quarter-on-quarter and increased by 8 per cent compared with the corresponding period in the preceding year. On a four-

quarter moving total basis, output rose for the twelfth consecutive quarter between January and March this year. Our belief is that the surge in output growth in

the first quarter of 2016 is in part driven by buyers trying to avoid the higher level of Stamp Duty for second homes and buy-to-let properties, which kicked

in from April.

Private housing orders ticked down in 2015, by 1 per cent to £12.8bn. Between January and March 2016

they decreased by 18 per cent to £2.73bn compared with the same period a year earlier.

Starts & completions At the time of writing only English and Welsh statistics

were available for the first quarter of 2016.

In 2015, GB private housing starts increased by 8 per cent to 139,257 units year-on-year. Whilst English

(119,370 units) and Welsh (6,991 units) starts registered increases of 9 per cent and 5 per cent respectively, the Scottish ones remained flat at 12,896

units.

In the first three months of this year, while English private housing starts went down by 3 per cent to

29,930 units compared with the previous quarter, the Welsh ones dropped by 16 per cent to 1,405 units.

Last year, GB private housing completions rose by 16

per cent to 127,597 units on an annual basis. English

2011 8963 4.2 16789 9.1

2012 8996 0.4 16235 -3.3

2013 11844 31.7 17671 8.8

2014 12994 9.7 21903 23.9

2015 12804 -1.5 23749 8.4

2014 Q3 3476 16.1 5661 26.7

Q4 3156 0.8 5730 21.2

2015 Q1 3334 1.7 5899 14.0

Q2 3156 2.3 6033 13.1

Q3 3023 -13.0 5771 1.9

Q4 3293 4.3 6046 5.5

2016 Q1 2726 -18.2 6344 7.5

Source: ONS.

Orders

% change y-on-y

Private Housing Orders And Output

£ million (2005 prices)

£ million (2012 prices)

Output

% change y-on-y

0

1000

2000

3000

4000

5000

6000

2011 2012 2013 2014 2015 2016 2017 2018

Orders Output

PUBLIC HOUSING ORDERS (2005 PRICES, £M) AND OUTPUT (2012 PRICES, £M)

Source: ONS, Experian.

15

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

completions registered a jump of 19 per cent to 110,050 units whereas lower growth of 4 per cent was recorded for the Welsh ones (5,630 units). In contrast,

Scottish completions edged down by 2 per cent to 11,917 units.

Between January and March 2016 while English

private completions declined by 7 per cent to 27,320 quarter-on-quarter, the Welsh ones dropped by 31 per cent to 1,135 units.

Drivers

Demand factors Like the private housing output statistics, various other

housing market indicators are also suggesting strong expansion pre-April to avoid paying higher levels of Stamp Duty.

For example, between January and March 2016 HMRC’s seasonally adjusted (SA) property transactions (368,930) were up by 15 per cent

compared with the final quarter of 2015 and increased by 30 per cent year-on-year. In March they reached 153,300, the highest on record and 42 per cent up on

February’s figure. However, since then the number of monthly property transactions has declined dramatically, averaging around 89,000 in April and

May.

The Council of Mortgage Lenders’ (CML) gross mortgage lending statistics show that lending was

strong in March as it soared by 46 per cent to £26.18bn compared with February. However, it fell by a third to £17.6bn in April, although it did pick a little to

£18.2bn in May. This further supports the assertion that there was a big surge in housing market activity pre the changes to Stamp Duty and as a result the

second quarter of this year will have been much quieter.

Both the Office for National Statistics (ONS) and

Nationwide’s SA annual house price data suggest that monthly house prices rose at an increasing rate just before the Stamp Duty changes came into effect, but

have slowed since then. Markit, who have taken over the production of the Halifax House Price Index have released house price inflation data for May.

Unfortunately, the statistics only go back to May 2015 therefore analysis of SA annual house price trends prior to May is no longer possible. However on a

monthly percentage change basis, in March prices rose by 2.2 per cent, up from a decline of 1.5 per cent in February and there has been little movement in

prices post March.

Based on the ONS mixed-adjusted index, Experian is estimating a UK house price increase of around 6.7

per cent for 2016. This rate is expected to slow in following two years.

In February the Help to Buy London (HtBL) scheme

was introduced which will allow buyers with a 5 per cent deposit to access a loan worth up to 40 per cent of the property. The loan will be interest free for five

years. There is potential for this scheme to provide an upside risk to the forecasts. However the downside is that it may push up further the already very high

prices in the capital making it even harder for those towards the bottom end of the income scale to get on to the property ladder. Under HtBL, buyers will only be

able to afford new build homes in the outer London boroughs, but this is where prices have been rising the fastest; prices in Waltham Forest grew by 25 per

cent in the year to April while in Newham they increased by 21 per cent.

The latest data from the Financial Services Authority

(FSA) shows that in the first quarter of 2016 around 68.3 per cent of gross mortgage lending was for loans with a loan-to-value (LTV) of less than 75 per cent, up

from 65.9 per cent three months earlier, whilst around 28.9 per cent of gross lending was for loans with an LTV of between 75 per cent and 90 per cent. Around

2.5 per cent of lending was for loans with an LTV of between 90 and 95 per cent, down from 3.3 per cent in the previous quarter.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

200

8 Q

1Q

2Q

3Q

42

009

Q1

Q2

Q3

Q4

201

0 Q

1Q

2Q

3Q

42

011

Q1

Q2

Q3

Q4

201

2 Q

1Q

2Q

3Q

42

013

Q1

Q2

Q3

Q4

201

4 Q

1Q

2Q

3Q

420

15Q

1Q

2Q

3Q

420

16Q

1

LOAN-TO-VALUE RATIOS AS A PERCENTAGE OF GROSS MORTGAGE LENDING

>95%

>90% <=95%

>75% <=90%

<= 75%

Source: FCA/CML.

16

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

Earlier this year, high street bank Barclays announced that house buyers do not need to put a deposit down when purchasing a home using its 100 per cent

mortgage. But there’s a catch – a helper (usually parents) is required. Helpers need to contribute 10 per cent of the house purchase price and this money will

be invested into a savings account linked to the mortgage. The money will be returned back to the helper after three years, with interest, provided the

house buyer has kept up with mortgage repayments.

Getting a helper on board does not mean house buyers automatically qualify for the 100 per cent

mortgage. Both will still need to go through the new affordability tests that have been brought in by the Mortgage Market Review.

Supply factors According to the Royal Institution of Chartered

Surveyors’ Residential Market Survey, in May the net balance for new instructions remained in negative territory for the third successive month. The -30

reading was the worst one since the series began in April 1999. It is feasible that this negative score was primarily the result of EU referendum uncertainties.

The supply of properties available for sale also fell across all regions and devolved nations apart from Wales, which saw a rise in instructions.

In contrast the results of the Home Builders Federation’s (HBF) survey were somewhat more upbeat. A positive balance of nearly 22 per cent of

respondents reported net reservations up in March on a year ago, although the balance on site visitors was marginally negative. However, the use of sales

incentives has started to rise a little, although the vast majority of respondents reported no change. Some 70 per cent of respondents to the March survey expect

their level of sales in 2016 to be higher than the previous year.

The HBF survey also reveals that the percentage of

respondents reporting planning delays as a major constraint on activity decreased to 60 per cent in March, from 65 per cent three months earlier. The

proportion indicating that labour availability was restricting activity also declined (38 per cent vs. 41 per cent) whilst at 24 per cent labour costs also became

less of a concern. In contrast, those stating land

prices as a limitation on activity rose from 15 per cent to 20 per cent.

As part of the £300m Leeds Kirkstall Forge scheme

around 1,500 residential properties are to be built alongside new office, retail and leisure buildings. Work is expected to start this year and complete by 2020.

Work should also begin this year on a large-scale housing development near Ransome Road in Northampton. The 770 unit development is expected

to cost £120m and work should be completed in late 2019.

In King’s Lynn, Norfolk, there are plans for 600 new

homes. Work on the £80m project is set to commence in the second half of 2016 with completion in 2019.

Enabling works on the £850m new St James Quarter

in Edinburgh started in January, with main construction expected to begin some time in the spring and complete in 2020. The development is now

planned to contain around 250 new homes.

One of the most active developers in Wales at present is the Conygar Investment Company plc, which is

currently taking forward three marina projects, at Fishguard, Holyhead and Pembroke Dock, all with large residential elements, totalling 937 apartments. It

also has plans for a 900 residential unit scheme in Haverfordwest.

Outlook Growth in private housing output is likely to be

marginally slower in 2018 compared to our forecasts in the Spring Update. However, our overall projections of moderate expansion over the next three years

remain. This is despite the presence of pent-up demand in the market as the housing affordability issue continues to act as a drag on the sector.

0

5000

10000

15000

20000

25000

30000

2011 2012 2013 2014 2015 2016 2017 2018

Orders Output

PRIVATE HOUSING ORDERS (2005 PRICES, £M) AND OUTPUT (2012 PRICES, £M)

Source: ONS, Experian.

17

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

2011 2012 2013 2014 2015 2016 2017 2018

Private Housing

£ million (2012 prices) 15908 15070 15437 16700 16681 17015 17355 17702

Annual % Change 0.8 -5.3 2.4 8.2 -0.1 2.0 2.0 2.0

Public Housing

£ million (2012 prices) 7485 7613 7306 7413 7413 7265 7047 6835

Annual % Change -8.1 1.7 -4.0 1.5 0.0 -2.0 -3.0 -3.0

All Housing

£ million (2012 prices) 23393 22683 22743 24113 24094 24279 24402 24537

Annual % Change -2.2 -3.0 0.3 6.0 -0.1 0.8 0.5 0.6

Source: ONS and Experian.

ForecastsHousing Repair, Maintenance & Improvement

3 Housing Repair, Maintenance & Improvement

Summary

A bleak outlook has been forecast for the public

housing repair, maintenance and improvement (RM&I) output as fiscal austerity continues to hold back the sector.

That said, there will still be low value RM&I projects that will be carried out by social landlords over the forecast period but due to their small nature, it won’t

be enough to drive expansion in the sector.

In the coming months we expect Consumer Price Index (CPI) inflation to increase slowly, though remain

below 1 per cent by the end of the year. The oil price has picked up since January, and the depreciation of sterling will also support a rise in CPI inflation through

an increase in the cost of imports.

Private housing RM&I output experienced no growth last year, which was something of the surprise given

robust growth in household consumption of 2.7 per cent, usually one of the main drivers of the sector. In the three years to 2018 modest expansion is predicted

for the sector as consumer spending and real household disposable incomes experience decent growth.

Public Housing Repair, Maintenance and Improvement

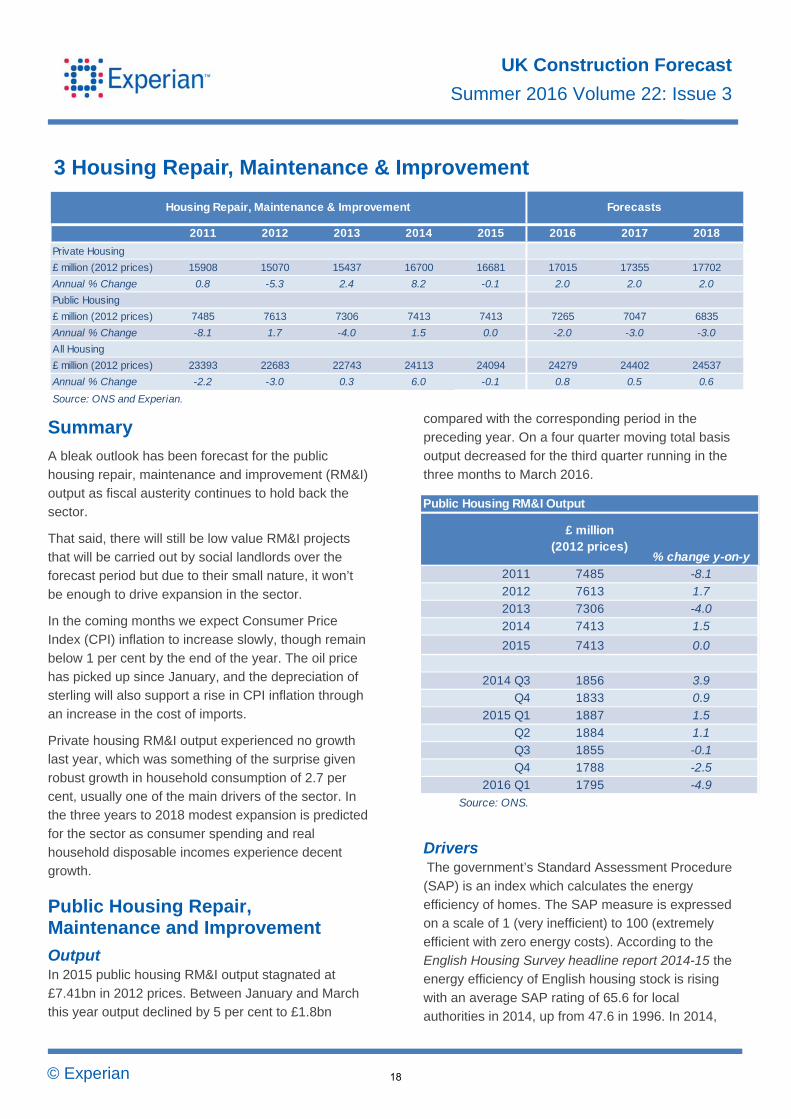

Output In 2015 public housing RM&I output stagnated at

£7.41bn in 2012 prices. Between January and March this year output declined by 5 per cent to £1.8bn

compared with the corresponding period in the preceding year. On a four quarter moving total basis

output decreased for the third quarter running in the three months to March 2016.

Drivers The government’s Standard Assessment Procedure

(SAP) is an index which calculates the energy efficiency of homes. The SAP measure is expressed on a scale of 1 (very inefficient) to 100 (extremely

efficient with zero energy costs). According to the English Housing Survey headline report 2014-15 the energy efficiency of English housing stock is rising

with an average SAP rating of 65.6 for local authorities in 2014, up from 47.6 in 1996. In 2014,

% change y-on-y

2011 7485 -8.1

2012 7613 1.7

2013 7306 -4.0

2014 7413 1.5

2015 7413 0.0

2014 Q3 1856 3.9

Q4 1833 0.9

2015 Q1 1887 1.5

Q2 1884 1.1

Q3 1855 -0.1

Q4 1788 -2.5

2016 Q1 1795 -4.9

Source: ONS.

Public Housing RM&I Output

£ million (2012 prices)

18

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

housing associations had a mean SAP rating of 67.1, up from 52.6 in 1996. Overall, the social housing sector was more energy efficient than the private one.

This is probably due to wider use of wall insulation in social housing as well as differing dwelling types, e.g. there is a higher proportion of flats in the social

housing sector which will have less exposed surface areas through which heat can be lost compared with detached or semi-detached houses. The assumption

is that work will continue to be undertaken to improve SAP ratings.

The domestic renewable heat incentive scheme which

is administered by Office of Gas and Electricity Markets (OFGEM) E-Serve was launched in April 2014. The aim is to promote the use of renewable

heat and households that install these measures receive tariff payments over a seven year period. Between April 2014 and May 2016 a total of 52,504

applications were made for the scheme, of which 49,083 were accredited i.e. an installation has gone through the required checks by OFGEM E-Serve and

was ready to start receiving payment. Approximately 24 per cent (11,709) of accreditations were for social landlords. Of these around 83 per cent were for air

source heat pumps.

Earlier this year Birmingham City Council announced a £59m investment in its residential stock. Kitchens

and bathrooms will be replaced, heating systems will be upgraded and new windows and roofs will also be installed on around 5,800 properties.

Refurbishment work has started on various council housing sites across Sheffield. Main improvements to properties include new windows, doors, flooring,

bathrooms and kitchens. There will also be upgrades of plumbing systems.

Outlook Our forecasts for public housing RM&I output have

been downgraded from the winter and spring in the light of the first quarter figures and deterioration in the economic scenario. Funding for major renovation

schemes is likely to be at a premium given on-going budget constraints not just for local authorities but other social housing providers.

Private Housing Repair, Maintenance & Improvement

Output At £16.68bn private housing RM&I output was largely

flat in 2015. In the first quarter of this year, it edged up by 1 per cent to £4.09bn compared with the same period a year earlier. On a four quarter moving total

basis, output went up for the fourth successive quarter between January and March 2016.

Drivers One of the key drivers of the private housing RM&I market is the health of the economy and, more specifically, household finances. When people are

more secure in their jobs and disposable incomes are

6400

6600

6800

7000

7200

7400

7600

7800

2011 2012 2013 2014 2015 2016 2017 2018

PUBLIC HOUSING REPAIR, MAINTENANCE & IMPROVEMENT OUTPUT (2012 PRICES, £M)

Source: ONS.

£ million (2012 prices)

% change y-on-y

2011 15908 0.8

2012 15070 -5.3

2013 15437 2.4

2014 16700 8.2

2015 16681 -0.1

2014 Q3 4242 7.4

Q4 4119 3.8

2015 Q1 4041 -3.9

Q2 4221 2.1

Q3 4255 0.3

Q4 4164 1.1

2016 Q1 4088 1.2

Source: ONS.

Private Housing RM&I Output

19

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

rising, they are more likely to invest in non-essential improvement work to their homes, such as a new bathroom or kitchen, but when there are concerns

over unemployment and incomes are being squeezed, this non-essential work is likely to be put off.

However, there is also a body of essential repair and

maintenance work that must be undertaken in order to keep a dwelling habitable, and this cannot be put off indefinitely.

The Consumer Prices Index (CPI) rose by 0.3 per cent in the year to May, unchanged from April. Other than a spike in the CPI in March, due largely to the

timing of Easter, inflation has been at 0.3 per cent for every month so far this year. Given the absence of any large movements in the latest numbers, our

benign baseline forecast for CPI remains largely unchanged. We expect CPI inflation to increase gradually as the oil price recovers and the large falls

in the food component of CPI over the past couple of years bottom out. Over the next three years consumer spending is likely to rise by an annual average of 2.3

per cent.

The chart below plots quarterly changes based on four-quarter moving totals for real household

disposable incomes (RHDI), consumer spending and private housing RM&I output.

While RHDI and consumer spending are thought to be

the most relevant variables influencing housing RM&I expenditure, RM&I spending may not always follow the trends of the former two variables as there are

other factors at work in the sector.

Under the domestic renewable heat incentive scheme of the 49,083 accreditations between April 2014 and

May 2016, just over three quarters were for owner occupiers and private landlords. Owner occupiers accounted for the largest share at 73 per cent whilst

private landlords accounted for just 3 per cent of total accreditations.

As mentioned before there will be no more Green

Deal loans or cashback funding. Customers who have cashback vouchers or are already paying loans will be unaffected. Bearing this in mind, in May a total of

657,681 Green Deal assessments had been undertaken, with the May figure of 5,362 assessments down by 6 per cent on the previous month. There

were 14,029 households that had Green Deal Plans and of these, 164 were at the pending stage, where the plan has been signed and installation was in

progress, and 13,146 were at the live stage, where all measures had been installed. Since the beginning of the Green Deal scheme a total of 20,676 measures

have been installed.

In contrast, as expected significantly more installations were recorded under the ECO scheme

with around 1,832,500 measures installed between January 2013 and April 2016. In April the number of ECO measures installed was down by 8 per cent to

39,049 compared with the previous month.

Between October and December last year, according to data from the Bank of England, housing equity

withdrawal remained negative for the 31th consecutive quarter as homeowners continued to pay down mortgages with the value of funds being injected

at £9.45bn in the quarter. This figure was 2 per cent lower compared with the previous quarter and down 32 per cent year-on-year. One of the main methods of

funding substantial RM&I work is through housing equity withdrawal thus the negative trend is likely to have impacted on major RM&I works.

It is worth noting that some RM&I work may be undertaken by firms not classified in the construction sector, such as manufacturers of kitchen and

bathroom equipment using their own workforce, and thus it would not show up in construction statistics.

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

-1%

-1%

0%

1%

1%

2%

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

Qau

rter

ly %

cha

nge

in t

he fo

ur q

uart

er m

ovin

g to

tal

Real household disposable income (lhs)Consumer spending (lhs)Private housing RM&I output (rhs)

PRIVATE HOUSING REPAIR, MAINTENANCE & IMPROVEMENT OUTPUT VS. REAL HOUSEHOLD DISPOSABLE INCOME VS. CONSUMER SPENDING

Source: ONS.

20

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

Outlook Our spring private housing RM&I output forecasts have been retained, with relatively modest growth at around 2 per cent a year, roughly in line with

consumer spending growth, the most likely scenario. By the end of the forecast period output is projected to be around 86 per cent of its 2002 peak.

8000

9000

10000

11000

12000

13000

14000

15000

16000

17000

18000

19000

2011 2012 2013 2014 2015 2016 2017 2018Source: ONS.

PRIVATE HOUSING REPAIR, MAINTENANCE & IMPROVEMENT OUTPUT (2012 PRICES, £M)

21

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

4 New Infrastructure

Summary

In 2015 the Office for National Statistics (ONS)

published two significant revisions to construction output data. A large firm from the services sector was reclassified to construction. Data were only revised

from March 2015 and thus are no longer comparable with earlier data. The estimated impact was about 12 per cent of reported output for 2015.

ONS also made changes to the treatment of outliers in the output data. Changes were made at that stage only to the output series for 2014 and 2015. Published

output in the nine months to September 2015 was revised up by £615m, but decreased by £343m for 2014. This added about a further 4 per cent to the

output increase in 2015 over 2014. New orders data have not been impacted by either of these changes.

Since its peak in 2011, infrastructure output has been

somewhat volatile but the general trend was downward to end 2014. However, 2015 set a new annual record at £17.7bn in 2012 chain linked prices,

29.8 per cent higher than 2014. For the four quarters ending March 2016 output totalled £17.4bn, an 18 per cent increase over the preceding four quarters.

In the context of performance over the last three years, current price output in the water sub-sector remains low in historical terms, but sewerage has

recovered from the trough experienced in 2014. The patterns of decline established in the gas, air & communications and rail sub-sectors have persisted.

Output in the electricity and roads sub-sectors has continued to grow strongly through 2015. Infrastructure new orders progressively increased

from the recent low point in the first quarter of 2014 through the recent high points in the second and third quarters of 2015. Orders have weakened since then

but the four-quarter total to March 2016 was still 36 per cent higher than the previous four quarters.

Following the strong growth in output in 2015 output is forecast to stall, with 2016 recording a fall of 1

percent, before recovering by a similar 1 per cent in 2017 and then stabilising in 2018. The strongest drivers of output through the review period are

sewerage and roads. Sewerage is the major contributor to growth in 2016, predicated on the method used by ONS to calculate output by orders for

the sub-sector despite Thames Tideway Tunnel construction not starting in earnest until 2017. The increase in output from major roads schemes also

drives growth in 2017 as well as 2018. The forecasts now assume the start of main works on Hinkley C nuclear power station is delayed beyond 2018.

The March 2016 National Infrastructure Plan shows an Infrastructure pipeline, excluding social infrastructure, of £425bn in 2014/15 prices. This

excludes areas of expenditure which are devolved to the Welsh Assembly and the Scottish Parliament. Of this total £240bn of projects will be delivered by

2020/21. Spending progressively falls from £52bn in 2016/17 to £41bn in 2020/21. 60 per cent of the projects and programmes are either in construction or

part of an active programme. In the period to 2020/21 the two largest sectors, energy (£117.4bn, 49 per cent) and transport (£88.4bn, 37 per cent), account for

87 per cent of the pipeline’s total value, but not all of this expenditure will be measured as infrastructure construction output. £100bn of this spend will be

entirely publicly funded, 50 per cent entirely private investment and the balance a mix of public and private sources. In percentage terms, the main

changes in the pipeline since the July 2015 report are a reduction in the spend on water and waste offset by additional flood spend. The Government has set up

two new bodies, the Infrastructure and Projects Authority and an independent National Infrastructure Commission, to ensure the right infrastructure projects

are identified and delivered successfully.

2010 2011 2012 2013 2014 2015 2016 2017 2018

£ million (2012 prices) 14887 16136 14103 14539 13668 17737 17560 17735 17735

Annual % Change 27.5 8.4 -12.6 3.1 -6.0 29.8 -1 1 0

Source: ONS and Experian.

New Infrastructure Construction Output Forecasts

22

© Experian

UK Construction Forecast

Summer 2016 Volume 22: Issue 3

Mix of Infrastructure Output by Sub-Sector 2012 to 2015

18%23% 35%

41%

16% 17%

20%

28%32% 31%

23%

14%

15% 10% 6% 3%

5%3% 3%

5%

4% 4%5%

5%11% 11% 8% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015

Gas, Air &CommsHarbours

Railways

Roads

Electricity

Sewerage

Water

Source: ONS

Sector Overview

Output & Orders Infrastructure output in 2015 established a new record

of £17.7bn, up 29.8 per cent on 2014 in chain-linked 2012 prices, following a 6 per cent decrease in 2014 from 2013. Output grew progressively from the

second quarter of 2014 to peak at £4.51bn in the third quarter of 2015, but has since fallen back progressively to £4.07bn in the first quarter of 2016. In

the four quarters to March 2016 output was £17.4bn, 18 per cent higher than the previous four quarters.

The following table shows the value of contractors’

orders and output in constant prices since 2011.

Following an excellent year in 2012, when new orders

totalled £10.1bn in 2005 prices, boosted by a 10-year water and sewerage framework contract, new infrastructure orders in 2013 fell back to £8.4bn, a

16.8 per cent decrease. Orders fell by a further 14.3 per cent in 2014 to £7.2bn, a similar level to 2011 before picking up by 50.3 per cent to set a new record

of £10.9bn in 2015. In the four quarters to March 2016 orders totalled £11.3bn, 36 per cent on previous four quarters.