annual report for the construction industry · annual report for the construction industry progress...

TRANSCRIPT

AAllaasskkaa’’ssCCoonnssttrruuccttiioonnSSppeennddiinngg22001100 FFoorreeccaasstt

AnnualAnnual Report Report ffoorr tthheeConstructionConstruction Industry Industry ProgressProgress Fund Fundandand tthheeAssociatedAssociated General General Contractors Contractorsofof Alaska AlaskaBByy Scott Scott GGoollddssmmiitthh and and MMaarryy KKiilllloorriinnIInnssttiittuuttee of of Social Social and and Economic Economic RReesseeaarrcchhUUnniivveerrssiittyy of of Alaska Alaska AAnncchhoorraaggee

2010 Forecast FINAL:Forecast 1/28/10 6:42 PM Page 1

OverviewThe total value of con-

struction spending “on thestreet” in Alaska in 2010 willbe $7.0 billion, down 3%from 2009.1,2,3

Wage and salary employ-ment in the constructionindustry will continue theslow decline which began in2006, but the level remainsabove the long-term averagefor the industry.Excluding the oil and gas

sector—which accounts for43% of the total—construc-tion spending will be $4.0 bil-lion—down 4% from 2009.Private-sector construction

spending will be down only1% from 2009, to $4.4 billion,in spite of the slowdown inthe Alaska economy. Oil and

gas sector spending will beflat. Spending will increasein the utilities and hospitals4

categories but will declinein mining, residential, othercommercial, and the otherrural basic sector categories.Public construction

spending will be down 5%,to $2.6 billion, in spite ofthe infusion of cash from theAmerican Recovery andReinvestment Act (ARRA).Although some categories offederal spending will be high-er, many will be lower andstate spending will also belower because of the lean FY2010 capital budget.Uncertainty in this year’s

forecast comes from severalsources. As we start 2010there is no clear indication

if the national economy isstarting to recover from therecession, and if it does, howstrong that recovery will be.Although Alaska has beeninsulated from the worsteffects of the recession—thecrash in the housing market,high unemployment, andlack of credit—concernsabout the national recoverywill continue to influenceinvestment decisions in thestate, particularly in thecommercial and residentialmarkets. Local governmentcapital spending is alsovulnerable to reductions intax revenues from activities,like tourism, driven by thenational economy.The passage of the American

Recovery and ReinvestmentAct (ARRA) in early 2009has provided an importantboost to construction spend-ing this year. A second stim-ulus may be undertaken laterthis year, but it is too soon tospeculate on how that might

impact construction spend-ing, so we assume no furtherfederal action.The Alaska economy con-

tracted in 2009 for the firsttime in 22 years—but thereduction in employmentwas only about 1%. Forecastsfor Alaska’s economy in 2010vary from further moderatedeclines in employment to aresumption of growth. Thisdifference of opinion under-scores the sense of cautionin the business communityabout the near-termprospects for the economy.As the year begins, petrole-

um and precious metal (goldand silver) prices are strongand rising, and base metalprices (zinc) have reboundedfrom the lows of last year.Petroleum and mining capitalbudgets are particularly sensi-tive to these prices, which arelikely to continue to fluctuatethroughout the year. Weassume these prices remainstrong throughout the year.

Dear Alaska Resident,For the seventh consecutive year, the

Construction Industry Progress Fund (CIPF)and the Associated General Contractorsof Alaska (AGC) are gratified to provide “Alaska’sConstruction Spending Forecast” for your reading and use.

This publication provides an informative review andestimate of construction activity in Alaska for 2010.

Compiled and written by Scott Goldsmith and MaryKillorin of the University of Alaska’s Institute of Social andEconomic Research (ISER), the “Forecast” reviews constructionactivity, projects and spending by both the public and privatesectors for 2010.

The construction industry is Alaska’s third largest industry,paying the state’s second highest wages, employing nearly21,000 workers with a payroll over $1 billion, accounting for20 percent of Alaska’s economy and currently contributingapproximately $7 billion to the state’s economy.

I hope this publication is of value to you. When theconstruction industry is vigorous, so is the state’s economy.

Roger HickelCIPF Chairman

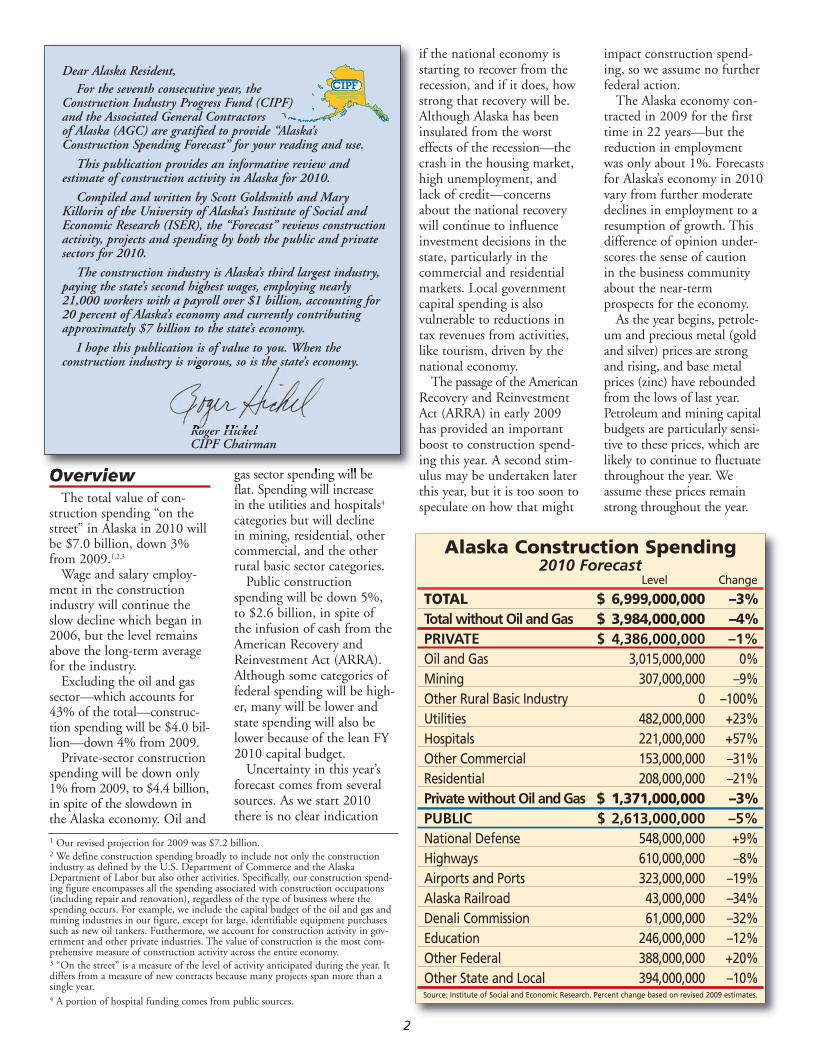

Alaska Construction Spending2010 Forecast

Level Change

TOTAL $ 6,999,000,000 –3%Total without Oil and Gas $ 3,984,000,000 –4%PRIVATE $ 4,386,000,000 –1%Oil and Gas 3,015,000,000 0%Mining 307,000,000 %–9%Other Rural Basic Industry 0 –100%Utilities 482,000,000 +23%Hospitals 221,000,000 +57%Other Commercial 153,000,000 –31%Residential 208,000,000 –21%Private without Oil and Gas $ 1,371,000,000 –3%PUBLIC $ 2,613,000,000 –5%National Defense 548,000,000 +9%Highways 610,000,000 –8%Airports and Ports 323,000,000 –19%Alaska Railroad 43,000,000 –34%Denali Commission 61,000,000 –32%Education 246,000,000 –12%Other Federal 388,000,000 +20%Other State and Local 394,000,000 –10%Source: Institute of Social and Economic Research. Percent change based on revised 2009 estimates.

2

1 Our revised projection for 2009 was $7.2 billion.2 We define construction spending broadly to include not only the constructionindustry as defined by the U.S. Department of Commerce and the AlaskaDepartment of Labor but also other activities. Specifically, our construction spend-ing figure encompasses all the spending associated with construction occupations(including repair and renovation), regardless of the type of business where thespending occurs. For example, we include the capital budget of the oil and gas andmining industries in our figure, except for large, identifiable equipment purchasessuch as new oil tankers. Furthermore, we account for construction activity in gov-ernment and other private industries. The value of construction is the most com-prehensive measure of construction activity across the entire economy.3 “On the street” is a measure of the level of activity anticipated during the year. Itdiffers from a measure of new contracts because many projects span more than asingle year.4 A portion of hospital funding comes from public sources.

2010 Forecast FINAL:Forecast 1/28/10 6:42 PM Page 2

The progress of a number oflarge projects this year hingeson companies getting thenecessary permits and avoidinglitigation. An example is theplan by Shell Oil to drill in theBeaufort and Chukchi seas.In these cases our forecast isconservative. We assumedelays will postpone some ofthis spending. If these projectsall move forward withoutdelay, actual spending willexceed our forecast.In spite of the uncertainty

associated with the economythis year, there is little down-side risk to the forecast.Private construction spend-ing will be dominated by apetroleum industry thatinvests strategically and isnot overly influenced by thecurrent recession. Publicconstruction spending willbe driven by money hittingthe street from the ARRA.Public construction spending

estimates are perennially com-plicated by consistent delays inpassage of the budget for thefederal fiscal year (Octoberthrough September).As in past years, some firms

are reluctant to reveal theirinvestment plans, because theydon’t want to alert competitors,and some have not completedtheir 2010 planning. Largeprojects often span two ormore years, so estimating cashon the street in any year isalways difficult—because theconstruction “pipeline” neverflows in a completely predictablefashion. Tracing the path of

federal spending coming toAlaska without double countingis also a challenge.We are confident in the

overall pattern of the fore-cast—but as always, we canexpect some surprises as theyear progresses.

PRIVATELYFINANCEDCONSTRUCTION5

The private sector willspend $4.4 billion on con-struction-related activities inAlaska in 2010. That is 63%of total construction spend-ing, and a decrease of 1%compared with 2009.

Oil and Gas:$3.015 MillionOil and gas industry

spending, which will accountfor 43% of all constructionspending in 2010, is expect-ed to be about the same aslast year. Spending will belower on the North Slope,but higher in Cook Inlet andin petroleum manufacturing.None of the three major

producers on the NorthSlope—British Petroleum(BP), Conoco Phillips, andExxon—will be exploring,and their spending will be

down this year. BP will con-centrate on bringing theLiberty field into production,developing existing reserves,and maintaining infrastruc-ture. Conoco Phillips willalso concentrate on develop-ing existing reserves, since its

Alpine West prospect contin-ues to be delayed. Exxon willconcentrate on drilling atPoint Thomson.Three other companies—

ENI, Pioneer, and Shell—willhave large North Slope budg-ets this year. ENI will resume

Anchorage International Airport Covered Walkway

Dowling Road Extension, Anchorage

3

5 We try to include in this category allspending that is financed primarilyfrom private sources. Although this isrelatively straightforward for oil andgas, mining, fishing, timber, manufac-turing, and tourism, it is not so easyfor hospitals, utilities, and other com-mercial construction. We includespending from all sources in our hospi-tal and utilities categories. However, insome years most hospital spending isfinanced by the federal government,and the state provides some of thefunding for electric utility investment.Construction activity reported by localgovernments as residential or commer-cial often includes projects financed inwhole or in part by public sources.

2010 Forecast FINAL:Forecast 1/28/10 6:42 PM Page 3

work to bring the Nikaitchuqfield into production, andPioneer will continue thedevelopment of the Oooguruk

field. Shell has plans to drilloffshore in the Beaufort andChukchi seas, although ithas yet to receive a final air

discharge permit from theEnvironmental ProtectionAgency, and its Beaufort planfaces a legal challenge.Two small companies—

Brooks Range Petroleum andSavant—are planning to drillexploratory wells.In Cook Inlet, Marathon,

Chevron, and Conoco Phillipswill all be active, as well asArmstrong Petroleum, whichhas just signed a contract withEnstar to supply gas. Also, weassume that Escopeta will besuccessful in bringing a jackuprig to Cook Inlet to drill dur-ing the summer.Plans for a gas storage

facility in Cook Inlet, to dealwith the challenge of havingenough gas to meet demandin Southcentral during thehigh-demand winter months,are moving forward rapidly.The hope is that storage willbe in place by the time theLNG export license expiresin 2011, since that facilitycurrently functions to meetthe winter peak demand forgas in Cook Inlet. Finally,refinery upgrades are plannedat the Tesoro refinery inNikiski (benzene unit) andwill continue at the Petrostarrefinery in Valdez (ultra-low-sulfur diesel).

Mining:$307 MillionSpending by the mining

industry—on exploration,6

development, and upgradingexisting mines—will be down9% this year. The recordhigh price of gold and therecovery of base metal pricesare not enough to offset thecompletion of a number oflarge projects last year.With the exception of

Pogo, the other three world-scale metal mines will havesignificant developmentbudgets this year. The RedDog mine is working tomove operations to the adja-cent Aqqaluk site by 2011,although it could be delayeddue to a court challenge ofits water discharge permit.Because of the high gold

and base metal prices, thereare plans to reopen severalsmaller mines includingRock Creek, Lucky Shot,and Galore Creek.Donlin Creek and the

Pebble prospect have bothmoved past the explorationphase and are being analyzedfor development, so theirconstruction budgets thisyear are quite modest.

Other BasicIndustries inRural Alaska:$0 MillionInvestments in facilities to

support tourism, the seafoodindustry, timber processing,and other natural resourceindustries often occur inrural parts of the state,“hidden” from view. Theonly major project in thiscategory is the continueddevelopment of the dockand cold storage complexat Dutch Harbor, but it iscurrently on hold withno expenditures expectedthis year.

Gravina Island Road Development, Ketchikan

Clark Middle School, Anchorage

4

6 Excluding exploration and develop-ment costs associated with environ-mental studies, community outreachand engineering.

PHOTO

COURT

ESY K

IEW

IT PACIFIC

COM

PANY

2010 Forecast FINAL:Forecast 1/28/10 6:42 PM Page 4

Utilities:$482 MillionSpending in this category

will be up 23% this year,primarily because of the con-struction of the new gas-firedelectric generation facility byChugach Electric Associationand Anchorage MunicipalLight and Power. The FireIsland wind farm project isalso moving forward.The budgets for the major

telecommunications firmswill be lower this year, andno significant gas utility proj-ects are planned. The firstphase of a project to providehigh bandwidth Internet serv-ice to rural Western Alaskawill get underway this year.There will be numerous

smaller electric generationfacilities—mostly wind andhydroelectric—constructedthroughout the state usingfunding from the staterenewable energy programappropriation.

Hospitals:$221 MillionHospital spending will be

considerably higher than itwas last year, with new facili-ties at the Providence com-

plex in Anchorage again lead-ing the way. Construction ofthe new hospital at Nome isthe other large project thatwill begin this year. In addi-tion, the first phase of con-struction of the new hospitalin Barrow will also get started.

Other PrivateCommercial:$153 MillionPrivate commercial con-

struction spending consistsof a wide range of buildingtypes, including retail, office,medical, hotel, and ware-house space.7 The level ofspending from year to yearcan be influenced by a fewlarge projects—which is onereason we project spendingwill be down this year.Several large projects inAnchorage were finishedin 2009 and very littleis planned for this year.The absence of large proj-

ects reflects both the slow-down in the overall economyand the uncertainty regardingfuture prospects in generaland specifically for the con-struction of a gas pipeline.Investors in new commercialfacilities have adopted a wait-and-see attitude regarding

both, and consequently weforecast the level of privatelyfunded commercial activityacross the state to be downconsiderably from last year.

Residential:$208 Million Although Alaska has been

largely insulated from thenational housing marketcrash—both in terms ofprices and foreclosures—residential constructionwill decline again this year,continuing a trend thatbegan in 2007. The declineis the result of the fall inemployment and uncertaintyabout the future growth ofthe Alaska economy.

Weeks Field Estates Phase I, Fairbanks

5

7 Our commercial construction figureis not comparable to the publishedvalue of commercial building permitsreported by Anchorage and other com-munities. Municipal reports of thevalue of construction permits mayinclude government-funded construc-tion, which we capture elsewhere inthis report. We have also excluded hos-pitals and utilities from commercialconstruction to provide more detailabout the composition of privatespending (even though some hospitaland utility spending is funded frompublic sources).

Goose Creek Correctional Center, Mat-Su

2010 Forecast FINAL:Forecast 1/28/10 6:42 PM Page 5

PUBLICLYFINANCEDCONSTRUCTIONPublicly financed construc-

tion8 spending in 2010 isexpected to be $2.6 billion,5% lower than last year, inspite of the stimulus to capitalspending provided by theAmerican Recovery andReinvestment Act of 2009.Historically, the majority of

funding for public construc-tion has come from the feder-al government, and much ofit flows through state govern-ment as grants, thus showingup in the state budget. Oncein the state budget, these fed-eral funds are often combinedwith state appropriations.Federal funds also flow

directly to non-profit organi-zations, like the Alaska Nativehealth organizations, and to amodest extent directly to localgovernments. Federal agencies,both military and civilian, alsohave their own capital budgets.Non-federal funds for state

capital spending have histori-cally come primarily from thestate General Fund and bondsales. With the growth in

complexity of the state budg-et, an increasing share ofstate-financed construction iscoming out of other funds.An important source of

local government spending isgrants from the state. For thelarger communities, currentrevenues and bond proceedsalso contribute to construc-tion spending.Finally, state and local

enterprises like the state air-ports and local wastewaterand sewer utilities generatefunds for capital expendituresfrom current revenues and thesale of revenue bonds.There are numerous ways

to categorize public construc-tion spending. We presentthem by function.

National Defense:$548 MillionSpending for national

defense will be up 9% fromlast year. Military spending isdivided into three basic cate-gories—MILCON (MilitaryConstruction), civil works,and environmental remedia-tion, including FUDS(Formerly Used DefenseSites). The missile defensesystem at Fort Greely isbudgeted outside these basiccategories, and this year theARRA is an important sourceof funding augmenting all thebasic categories.The number of active duty

military assigned to the statecontinues to grow and require

new facilities, construction ofwhich falls under the MILCONprogram. The largest share ofnew construction this year isscheduled to occur at EielsonAir Force Base and FortWainwright in Interior Alaska.The Corps of Engineers

provides funds for civil workssuch as flood control andenvironmental remediation.We include these corps activitiesin the national defense total,although they primarily benefitcommunities rather than thenational defense mission.

Transportation—Highways:$610 MillionSpending for highways and

roads will be 8% lower thanlast year, primarily due to thesmall size of the state capitalbudget in FY 2010. But a largeportion of the proceeds of therecent state transportationbond issue will be available.

A large share of transporta-tion funds comes as a formulagrant from the federal govern-ment. That program has notyet been reauthorized and iscurrently operating on amonth-to-month basis, withallocations to the states at70% of the former formularate. Consequently the stateis receiving less than in yearspast. However, this loss iscurrently being offset by asignificant amount of fundingfrom the ARRA.Locally funded highway

projects will be funded at alevel similar to past years.

Transportation—Airports, Portsand Harbors:$323 MillionSpending for airports,

ports, and harbors will belower than in past yearsbecause of the absence offunding of projects in the FY2010 state capital budget and

Sand Lake Water and Sewer Upgrades, Anchorage

6

Trading Bay Subsea Diffuser

8 This category includes all spendingfinanced by federal, state, and localgovernment sources, except hospitalsand electric utilities. Public dollarsoften fund the investments of privateand non-profit organizations. Thisspending is included here. Fundingfor some projects comes from multiplepublic sources, or from a combinationof public and private sources. We tryto account for these multiple fundingsources in this analysis.

PHOTO

COURT

ESY A

MER

ICAN M

ARINE

CORP

ORA

TION

2010 Forecast FINAL:Forecast 1/28/10 6:42 PM Page 6

the completion of significantupgrades at both theAnchorage and Fairbanksinternational airports lastyear. Federal funding in theform of grants from theFederal AviationAdministration will be aboutthe same as in past years.Spending for publicly

funded port and harborupgrades will be about thesame as last year, unless thePort of Anchorage receives alarge grant under ARRA—inwhich case the port will beable to move its developmentschedule forward.

Alaska Railroad:$43 MillionThe capital construction

program for modernizingand upgrading the AlaskaRailroad will continue thisyear at a slower pace than lastyear. Project funding comesfrom a variety of federalsources as well as retainedearnings. The focus of theprogram continues to betrack rehabilitation, sidingextensions and upgrades,bridge replacement andupgrades, passenger equip-ment, and a collision-avoid-ance system. It is possiblethat work could begin on theTanana River bridge as partof the rail extension to Fort

Greely, if funding can beidentified in the Departmentof Defense budget.

DenaliCommission:$61 MillionThe Denali Commission,

created by former U.S.Senator Ted Stevens to moreefficiently direct federal capi-tal spending to rural infra-structure needs, will spendaround $61 million for con-struction—down consider-ably from last year.The commission supports

a broad range of projects,including transportation,health, and energy-relatedinfrastructure, with fundsprovided by other federalagencies. The loss in fundinghas primarily impacted ener-gy and health facilities.

Education:$246 MillionEducation project funding

will be down 12% from lastyear. Spending will be up forprimary and secondaryschool construction andupgrades, which are financedby a combination of directstate appropriations for therural school districts anddebt finance for the urbandistricts. The state continues

to reimburse urban districtsfor most of the interest onschool bonds.University of Alaska con-

struction will be down due tothe completion of a numberof large buildings. Severalbuildings are in various stagesof planning, but none areready for construction this year.

Other Federal:$388 MillionThe categories already

discussed—national defense,transportation, education andthe Denali Commission —together make up the largestand most visible part of

federal construction spendingin Alaska. We forecast anadditional $388 millionof federally funded capitalspending in Alaska for othertypes of projects—20%higher than last year.9

Excluding transportation,the largest program fundedby federal grants to state gov-ernment is the Village SafeWater program of rural sani-tation. These funds comefrom a number of agencies,including the EnvironmentalProtection Agency and theIndian Health Service.Funding from these agencieshas fallen, but this initiativewill again contribute $100million to state constructionspending because of stimulusfunds from ARRA.The federal government

also provides grants andother construction fundingto Alaska tribes, non-profitorganizations, and local gov-ernments across the state.The most important recipi-ents of these grants areAlaska Native non-profitcorporations, housingauthorities, and health-careproviders. The largest of

Anchorage Museum At Rasmuson Center Expansion

Minnesota Drive Resurfacing, Anchorage

7

9 It is difficult to track all the federaldollars that find their way into con-struction spending in the state becausethere are so many pathways, and theychange every year. The possibility ofdouble counting funds as they passfrom agency to agency, or become partof a larger project, also creates difficul-ties for the analyst.

2010 Forecast FINAL:Forecast 1/28/10 6:42 PM Page 7

these programs is the NativeAmerican Housing SelfDetermination Act (NAHS-DA), which provides fundsfor housing construction inNative communities throughmany Native housing author-ities statewide. These pro-grams will be significantlyaugmented this year byARRA funds.We expect the level of

direct construction spendingby other federal departmentsto be about the same as in2009. This includes spendingby the Department of theInterior (National ParkService, U.S. Fish andWildlife Service, and Bureauof Land Management), thePostal Service, theDepartment of Agriculture,and the National Oceanicand AtmosphericAdministration (NOAA).

Other Stateand Local:$394 MillionState and local government

capital spending, excludingtransportation, education,and energy (electric utilities)will be about 10% lowerthan last year due to thesmaller state capital budgetof FY 2010 and constraintson local government budgetsfrom the downturn in theeconomy. The largest stateproject will be continuationof construction of the newGoose Creek prison in theMat-Su Borough. Other important categories

of state capital spending are anumber of smaller projectsfunded by the cruise ship taxand small projects funded bythe state weatherization andrebate programs. Spending on

weatherization could be high-er if federal ARRA weather-ization funds are leveraged inan AHFC bond package.Local government capital

spending, from general fundsas well as enterprise funds,will be about the same as lastyear, as no significant newprojects are anticipated. Buttighter finances will be offsetby ARRA funds.

WHAT’S DRIVINGSPENDING?Construction activity—

measured by total spending,jobs, payroll, or gross product—has experienced stronggrowth for more than adecade, driven largely bygrowing federal capital grantsto Alaska, large federal agencycapital budgets, oil and gasspending, and more recently,large state capital budgets.These large external sources

of construction funds not onlyfuel public spending and oilpatch spending but also give ageneral boost to the economy—and thus add to the aggre-gate demand for new residen-tial, commercial, and privateinfrastructure spending.

CONSTRUCTIONIN THE OVERALLECONOMYConstruction spending is

one of the important con-tributors to overall economicactivity in Alaska. Annualwage and salary employment

in the construction industryin 2009 was about 16.6thousand workers, withaverage annual earnings of$60 thousand per worker.Missing from this total arethe “hidden” constructionworkers employed in otherindustries like oil and gas,mining, and government(force account workers). Inaddition, this total does notaccount for the large numberof construction workers whoare self-employed—estimatedto be about 9,000 in 2009.Construction spending

generates activity in a num-ber of industries that supplyinputs to the constructionprocess. These “backwardlinkages” include, for exam-ple, sand and gravel purchas-es (mining), equipment pur-chase and leasing (wholesaletrade), design and adminis-tration (business services),and construction finance andmanagement (finance).The payrolls and profits

from this construction activi-ty support businesses in everycommunity in the state. Asthis income is spent and cir-culates through localeconomies, it generates jobsin businesses as diverse asrestaurants, dentists’ offices,and furniture stores.

Cover:UAA ConocoPhilips IntegratedScience Building Photo by Chris Arend

All other photos by Danny DanielsPhotography except as otherwise credited

North Slope Ice Road

PHOTO

COURT

ESY C

RUZ

CONST

RUCTION

2010 Forecast FINAL:Forecast 1/28/10 6:42 PM Page 8

Hicks Creek Glenn Highway Road Improvement

The 2010 Forecast is generously underwritten by Northrim Bank