trying, but not much progress in 2014 -...

TRANSCRIPT

PREPARED BY NON-US BROKER-DEALER(S):BNP PARIBAS SECURITIES (ASIA) LTD THIS MATERIAL HAS BEEN APPROVED FOR U.S DISTRIBUTION. ANALYST CERTIFICATION ANDIMPORTANTDISCLOSURES CAN BE FOUND AT APPENDIX ON PAGE 39

EQUITIES RESEARCH

CHINA STEEL SECTOR Trying, but not much progress in 2014

n Achieving forced capacity closures will be difficult in 2014, although geared steel mills could be forced out by tight funding after 2015. Currently, mills have to keep generating cash flow to cover interest expenses even if they are loss-making. Given their cash reserves, we think mills can survive for a year-and-a-half to two years. Hebei and Tangshan have announced aggressive capacity closure plans, but they have no clear compensation or labour relocation plans.

n Key differences between the steel and cement segments lie in fragmentation, links with financial systems, the regional nature of the market, economic impact on particular provinces, and product heterogeneity.

n We recommend being long the cement sector and short the steel sector.

Rachel Cheung [email protected]

+852 2825 1824

Our research is available on Thomson One, Bloomberg, TheMarkets.com, Factset and on http://eqresearch.bnpparibas.com/index. Please contact your salesperson for authorisation. Please see the important notice on the inside back cover.

8 JANUARY 2014

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

To find out more about BNP Paribas Equities Research:

Visit : http://eqresearch.bnpparibas.com/ For ipad users : http://appstore.apple.com/BNPP-equities/

2

Trying, but not much progress in 2014

n Forced closures in 2014 are harsh; geared steel mills to be forced out by tight funding in 2015

To curb overcapacity and environmental problems, the State Council and provincial governments

announced capacity closure targets; 60mt in Hebei (40mt in Tangshan) by 2017, 7mt in Jiangsu by

2018, and 15mt of backward capacity by 2015. The government seems more serious than five years

ago, but we are less optimistic than the market and think most of the impact will be back loaded.

Capacity in Hebei will be cut (actual existing capacity is unclear), but new capacity adds in Jiangsu

and Anhui East China mean utilization will not improve. Heavy interest expense will keep steel mills

running, even if loss-making. There is no clear funding source to compensate capacity closures in

Hebei. Based on two years’ of steel trader clean-up (from 3Q11), we think mills’ cash reserves can

support loss-making operations for at least two years with 2013 as the first year of losses for most

steel billet producers. We expect steel mills to struggle in 2014, reaching a critical point in 2015. Our

steel demand growth forecast is 3.5% and supply is 3.4% in 2014 with 78% net utilization at best.

n Fundamental differences between cement and steel determine efficacy of capacity closures

Similar policies to curb overcapacity have been announced in the steel and cement sectors, but the

fundamental differences between them mean the impact for cement is front loaded while steel’s is

back loaded. Thanks to high clinker consolidation, its regional nature, high productivity and more

homogenous products in the cement sector, it is easier for cement leaders to gain market share from

smaller players. Provinces rely less on cement for taxes and revenue since capacity is regionally

diverse. Steel is tradable domestically and internationally. One fundamental difference from the

cement sector is that smaller steel players have better cost control than large SOE steel mills due to

lower environmental concerns, off-spec product quality, and more flexible raw material supply

sources. Steel capacity is clustered in a few provinces and closely linked with local banking/financial

systems via traders. Provinces like Hebei rely heavily on steel businesses for tax revenue and it is

hard to find alternatives to replace this medium term given weak local property market outlook.

n We suggest investors switch from steel to cement

Angang is trading at a 24% P/BV premium to Magang, which we don’t think is sustainable given our

below-market expectations for steel in 2014. As such we downgrade Angang to REDUCE from Hold

and upgrade Magang to HOLD from Reduce. In the cement sector, Given the outperformance of

Angang over Anhui Conch over the past six months and better cement sector fundamentals, we

recommend investors BUY Anhui Conch and REDUCE Angang.

BNPP recommendations

Company BBG code Rating Share price Target price Upside/downside

Anhui Conch Cement 914 HK BUY 26.85 34.20 +27.4%

Maanshan Steel 323 HK HOLD 1.98 2.11 +6.3%

Angang Steel 347 HK REDUCE 5.30 4.65 -12.4%

Sources: Bloomberg; BNP Paribas estimates

8 JANUARY 2014

SECTOR REPORT

CHINA STEEL SECTOR

Rachel Cheung [email protected]

+852 2825 1824

3

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

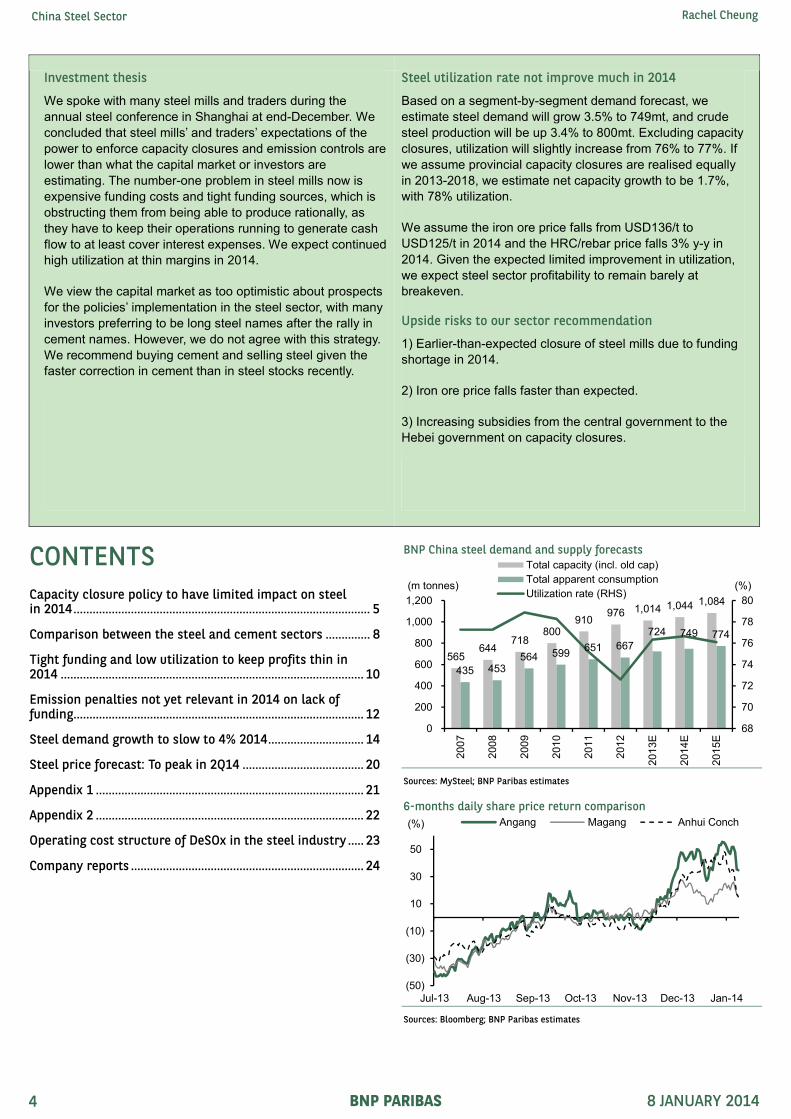

Investment thesis

We spoke with many steel mills and traders during the

annual steel conference in Shanghai at end-December. We

concluded that steel mills’ and traders’ expectations of the

power to enforce capacity closures and emission controls are

lower than what the capital market or investors are

estimating. The number-one problem in steel mills now is

expensive funding costs and tight funding sources, which is

obstructing them from being able to produce rationally, as

they have to keep their operations running to generate cash

flow to at least cover interest expenses. We expect continued

high utilization at thin margins in 2014.

We view the capital market as too optimistic about prospects

for the policies’ implementation in the steel sector, with many

investors preferring to be long steel names after the rally in

cement names. However, we do not agree with this strategy.

We recommend buying cement and selling steel given the

faster correction in cement than in steel stocks recently.

Steel utilization rate not improve much in 2014

Based on a segment-by-segment demand forecast, we

estimate steel demand will grow 3.5% to 749mt, and crude

steel production will be up 3.4% to 800mt. Excluding capacity

closures, utilization will slightly increase from 76% to 77%. If

we assume provincial capacity closures are realised equally

in 2013-2018, we estimate net capacity growth to be 1.7%,

with 78% utilization.

We assume the iron ore price falls from USD136/t to

USD125/t in 2014 and the HRC/rebar price falls 3% y-y in

2014. Given the expected limited improvement in utilization,

we expect steel sector profitability to remain barely at

breakeven.

Upside risks to our sector recommendation

1) Earlier-than-expected closure of steel mills due to funding

shortage in 2014.

2) Iron ore price falls faster than expected.

3) Increasing subsidies from the central government to the

Hebei government on capacity closures.

CONTENTS

Capacity closure policy to have limited impact on steel in 2014 ............................................................................................. 5

Comparison between the steel and cement sectors .............. 8

Tight funding and low utilization to keep profits thin in 2014 ............................................................................................... 10

Emission penalties not yet relevant in 2014 on lack of funding........................................................................................... 12

Steel demand growth to slow to 4% 2014 .............................. 14

Steel price forecast: To peak in 2Q14 ...................................... 20

Appendix 1 .................................................................................... 21

Appendix 2 .................................................................................... 22

Operating cost structure of DeSOx in the steel industry ..... 23

Company reports ......................................................................... 24

BNP China steel demand and supply forecasts

Sources: MySteel; BNP Paribas estimates

6-months daily share price return comparison

Sources: Bloomberg; BNP Paribas estimates

565 644

718 800

910 976 1,014 1,044

1,084

435 453 564 599

651 667

724 749 774

68

70

72

74

76

78

80

0

200

400

600

800

1,000

1,200

2007

2008

2009

2010

2011

2012

2013E

2014E

2015E

(%)(m tonnes)

Total capacity (incl. old cap)

Total apparent consumption

Utilization rate (RHS)

(50)

(30)

(10)

10

30

50

Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14

(%) Angang Magang Anhui Conch

4

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

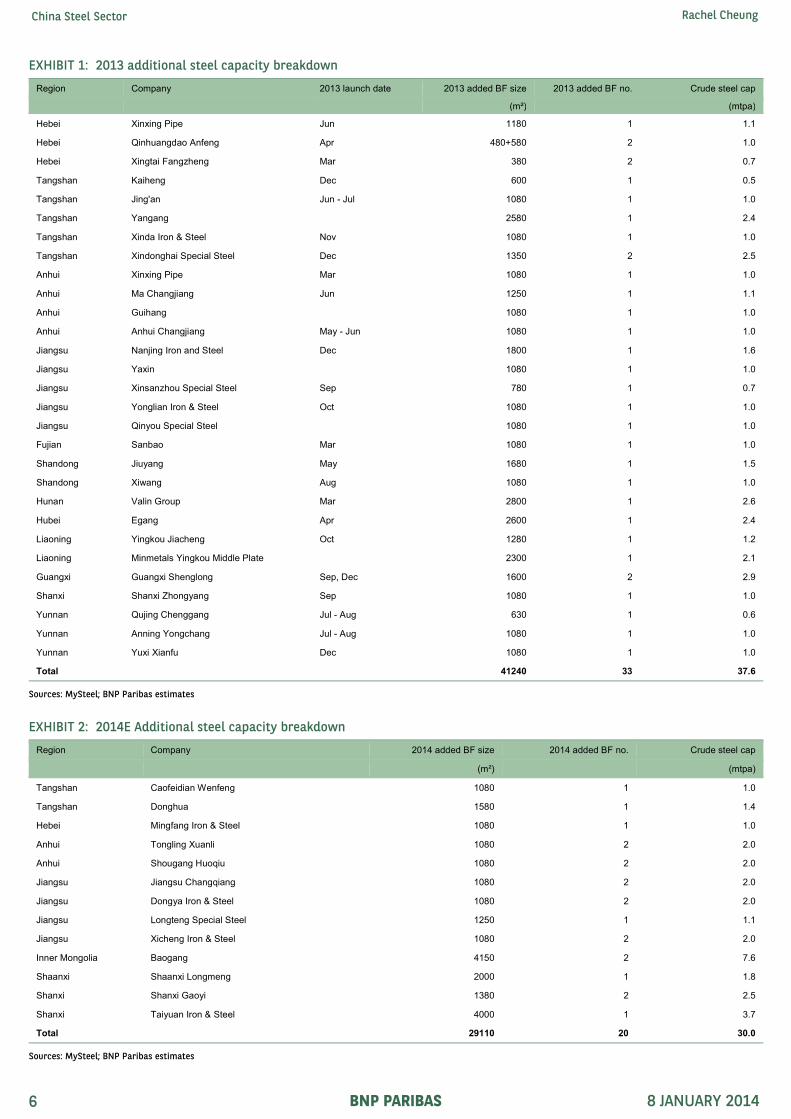

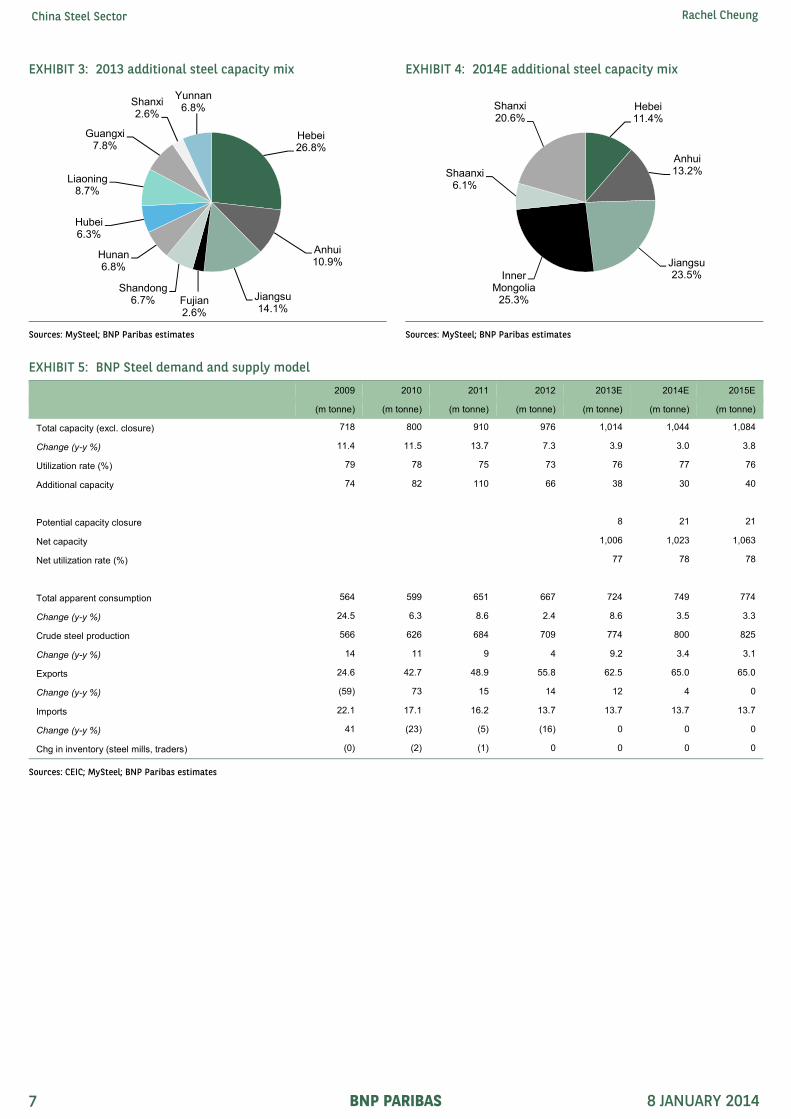

Capacity closure policy to have limited impact on steel in 2014

We have recently seen a lot of capacity closure announcements from the State

Council, and local and provincial governments, especially Hebei province.

§ The State Council announced its backward steel capacity closure target of 15mt

by 2015 (1.5% of total capacity).

§ The Hebei government aims to close 60mt (6% of total capacity or 25% of Hebei

capacity) by 2017, with 15mt in 2014. The local government cut 8.3mt in 2013

(mostly non-operational blast furnaces).

§ The Jiangsu government has unveiled a plan to cut 7mt of steelmaking capacity

(0.7% of total capacity) in 2014-18.

§ We expect more local governments to follow the leads of Hebei and Jiangsu.

§ There have been frequent electricity suspensions in Hebei and Shandong to cub

air pollution during periods of continuous smog.

However, after attending the annual steel conference and speaking with many steel

traders and steel mills, we do not believe the capacity closures will be significant

enough to support overall sector profitability or utilization, because:

§ Backward steel capacity closure of 15mt is mostly non-operational or with very

low utilization.

§ We see the most aggressive capacity cut target (60mt) in Hebei, of which

Tangshan city accounts for 40mt. However, we have to bear in mind: 1) the most

serious overcapacity problem is found in Hebei, especially Tangshan. Most the

steel billet producers in Tangshan were loss-making in 2013. Hebei’s total steel

capacity is around 230-250mt, while Tangshan has 150mt capacity; 2) The Hebei

Provincial government understood that most of the steel mills are loss-making at

the cash level in 2013. Tight funding conditions will squeeze small and

problematic steel mills to inevitably close after two years of cash losses. The

government can wait for problematic mills to close by themselves with no need to

force closures, thereby saving the need for compensation, and the aggressive

capacity closure only applies to Hebei province while other provinces are adding

capacity to take the market share from Hebei in 2014, so overall overcapacity will

still not improve significantly in 2014 (i.e. Jiangsu is only closing 7mt by 2018,

while adding 12mt in 2013-2014) (Exhibit 1-4).

§ Frequent electricity suspensions will hinder only the steel processing/rolling

plants, but will have a limited impact on blast furnace operation. It is very costly to

re-heat a blast furnace (around RMB15m-20m to re-heat, not to mention that the

coking plant may break after suspension), so steel mills prefer not to stop their

blast furnaces at all. Therefore, we note that steel mill inventory continue to rise

despite the electricity suspension (Exhibit 12).

Even if we include all the announced capacity closures in our capacity forecast, the

steel utilization rate is still low at around 77-78%, not much different from the gross

utilization of 76-77% in 2014E (Exhibit 5), due to the continuous substantial capacity

additions.

5

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

EXHIBIT 1: 2013 additional steel capacity breakdown

Region Company 2013 launch date 2013 added BF size 2013 added BF no. Crude steel cap

(m²)

(mtpa)

Hebei Xinxing Pipe Jun 1180 1 1.1

Hebei Qinhuangdao Anfeng Apr 480+580 2 1.0

Hebei Xingtai Fangzheng Mar 380 2 0.7

Tangshan Kaiheng Dec 600 1 0.5

Tangshan Jing'an Jun - Jul 1080 1 1.0

Tangshan Yangang

2580 1 2.4

Tangshan Xinda Iron & Steel Nov 1080 1 1.0

Tangshan Xindonghai Special Steel Dec 1350 2 2.5

Anhui Xinxing Pipe Mar 1080 1 1.0

Anhui Ma Changjiang Jun 1250 1 1.1

Anhui Guihang

1080 1 1.0

Anhui Anhui Changjiang May - Jun 1080 1 1.0

Jiangsu Nanjing Iron and Steel Dec 1800 1 1.6

Jiangsu Yaxin

1080 1 1.0

Jiangsu Xinsanzhou Special Steel Sep 780 1 0.7

Jiangsu Yonglian Iron & Steel Oct 1080 1 1.0

Jiangsu Qinyou Special Steel

1080 1 1.0

Fujian Sanbao Mar 1080 1 1.0

Shandong Jiuyang May 1680 1 1.5

Shandong Xiwang Aug 1080 1 1.0

Hunan Valin Group Mar 2800 1 2.6

Hubei Egang Apr 2600 1 2.4

Liaoning Yingkou Jiacheng Oct 1280 1 1.2

Liaoning Minmetals Yingkou Middle Plate

2300 1 2.1

Guangxi Guangxi Shenglong Sep, Dec 1600 2 2.9

Shanxi Shanxi Zhongyang Sep 1080 1 1.0

Yunnan Qujing Chenggang Jul - Aug 630 1 0.6

Yunnan Anning Yongchang Jul - Aug 1080 1 1.0

Yunnan Yuxi Xianfu Dec 1080 1 1.0

Total 41240 33 37.6

Sources: MySteel; BNP Paribas estimates

EXHIBIT 2: 2014E Additional steel capacity breakdown

Region Company 2014 added BF size 2014 added BF no. Crude steel cap

(m²)

(mtpa)

Tangshan Caofeidian Wenfeng 1080 1 1.0

Tangshan Donghua 1580 1 1.4

Hebei Mingfang Iron & Steel 1080 1 1.0

Anhui Tongling Xuanli 1080 2 2.0

Anhui Shougang Huoqiu 1080 2 2.0

Jiangsu Jiangsu Changqiang 1080 2 2.0

Jiangsu Dongya Iron & Steel 1080 2 2.0

Jiangsu Longteng Special Steel 1250 1 1.1

Jiangsu Xicheng Iron & Steel 1080 2 2.0

Inner Mongolia Baogang 4150 2 7.6

Shaanxi Shaanxi Longmeng 2000 1 1.8

Shanxi Shanxi Gaoyi 1380 2 2.5

Shanxi Taiyuan Iron & Steel 4000 1 3.7

Total 29110 20 30.0

Sources: MySteel; BNP Paribas estimates

6

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

EXHIBIT 3: 2013 additional steel capacity mix EXHIBIT 4: 2014E additional steel capacity mix

Sources: MySteel; BNP Paribas estimates Sources: MySteel; BNP Paribas estimates

EXHIBIT 5: BNP Steel demand and supply model

2009 2010 2011 2012 2013E 2014E 2015E

(m tonne) (m tonne) (m tonne) (m tonne) (m tonne) (m tonne) (m tonne)

Total capacity (excl. closure) 718 800 910 976 1,014 1,044 1,084

Change (y-y %) 11.4 11.5 13.7 7.3 3.9 3.0 3.8

Utilization rate (%) 79 78 75 73 76 77 76

Additional capacity 74 82 110 66 38 30 40

Potential capacity closure 8 21 21

Net capacity 1,006 1,023 1,063

Net utilization rate (%) 77 78 78

Total apparent consumption 564 599 651 667 724 749 774

Change (y-y %) 24.5 6.3 8.6 2.4 8.6 3.5 3.3

Crude steel production 566 626 684 709 774 800 825

Change (y-y %) 14 11 9 4 9.2 3.4 3.1

Exports 24.6 42.7 48.9 55.8 62.5 65.0 65.0

Change (y-y %) (59) 73 15 14 12 4 0

Imports 22.1 17.1 16.2 13.7 13.7 13.7 13.7

Change (y-y %) 41 (23) (5) (16) 0 0 0

Chg in inventory (steel mills, traders) (0) (2) (1) 0 0 0 0

Sources: CEIC; MySteel; BNP Paribas estimates

Hebei 26.8%

Anhui10.9%

Jiangsu14.1%

Fujian2.6%

Shandong 6.7%

Hunan 6.8%

Hubei 6.3%

Liaoning 8.7%

Guangxi 7.8%

Shanxi 2.6%

Yunnan6.8% Hebei

11.4%

Anhui13.2%

Jiangsu23.5%Inner

Mongolia 25.3%

Shaanxi 6.1%

Shanxi20.6%

7

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

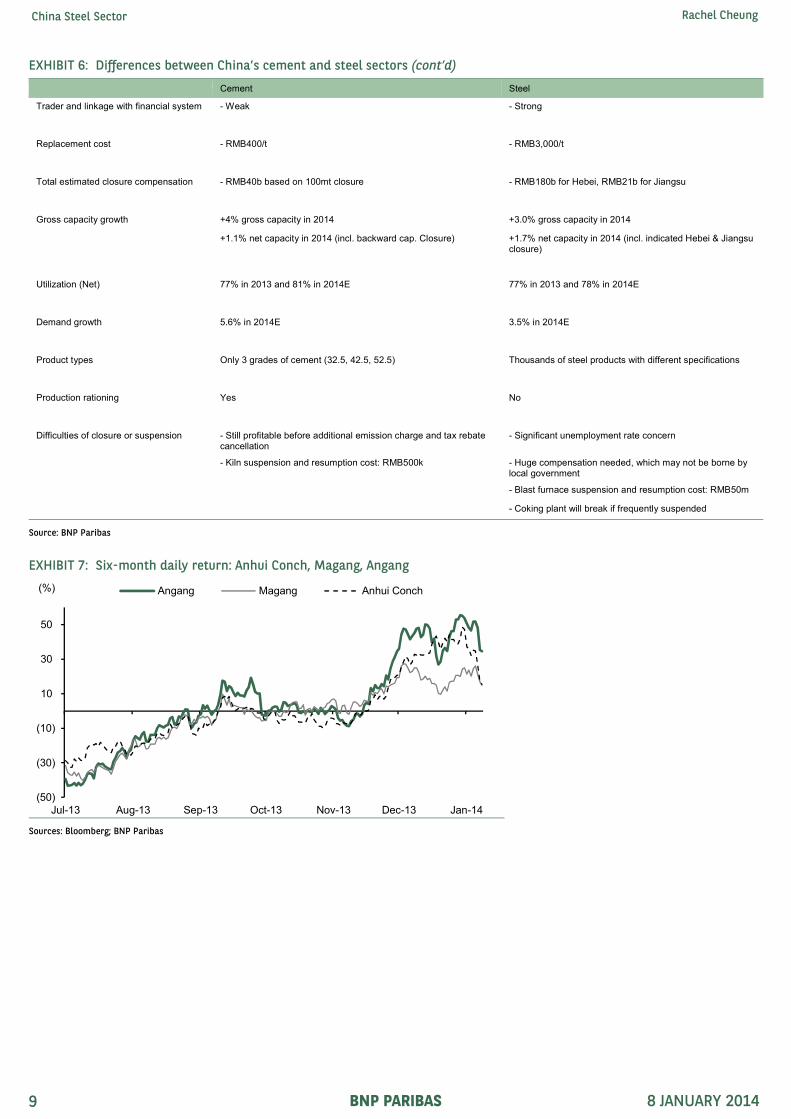

Comparison between the steel and cement sectors

The cement and steel sectors are two overcapacity sectors that the central

government would like to focus on improving in its 12th Five Year Plan. Although

similar policies have been announced, we think there are fundamental differences

between the steel and cement sectors.

Thanks to high clinker consolidation, the regional nature of the cement sector, high

productivity, and more homogenous products, we believe it is easier to implement

capacity controls in the cement sector and allow cement leaders to take market

share from smaller players. Since cement capacity is spread widely between

provinces in China, each province relies less on the cement sector for its fiscal

revenue or taxes.

We found there are still many hurdles for the government in closing capacity in the

steel sector. Steel is not spread regionally (as cement is) and steel products are

tradable domestically and internationally. We expect steel capacity to grow outside

Hebei, while Hebei is keen on closing capacity. One of the fundamental differences

from the cement sector is that smaller steel players have better cost control than

large SOE steel mills due to lower environmental concerns, off-spec product quality,

and more flexible raw material supply sources. Steel capacity is not only clustered in

a few provinces, but is also linked closely with local banking/financial systems

through traders. Provinces such as like Hebei rely heavily on steel businesses for tax

revenue and we believe it is hard to find alternative non-steel businesses to replace

their contribution in the medium term, given the weak local property market outlook.

Given the outperformance of Angang over Anhui Conch over the past six months and

better fundamentals of the cement sector over the steel sector, we recommend

investors to BUY Anhui Conch and REDUCE Angang (Exhibit 7).

EXHIBIT 6: Differences between China’s cement and steel sectors

Cement Steel

Policies - Straight new capacity approval, replacement with less or equal volume

- Straight new capacity approval, replacement with less or equal volume

- Close 5% backward capacity (100mt) by 2015 - Close 1.5% backward capacity (15mt) by 2015

- Latest tight emission standard announced 27 Dec 2013 - Latest emission standard announced June 2012

- Cancel PC32.5 grade cement from mid-2014 - Hebei to close 60mt steel cap. by 2017

- Tangshan to close 40mt steel cap. by 2017

- Jiangsu to close 7mt steel cap. by 2018

Net profit margin 6.83% [Based on Dcement survey] 0.55% [based on CISA survey]

Electricity suspension impact - Kilns and grinding stations - Rolling/processing facilities

Top 3 provinces’ share 21% 44%

Top 10 capacity concentrate 54% 35%

Annual Labour productivity 2,317t/person 100t/person

No. of impacted employees - 86k people impacted if 10% closure (i.e. 5% small NSP + 5% backward)

- 600k people impacted in Hebei, 70k in Jiangsu

Cost structure Large players lower operating cost Small players lower operating cost

Gearing ratio 57% 123%

(Continued on next page)

8

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

EXHIBIT 6: Differences between China’s cement and steel sectors (cont’d)

Cement Steel

Trader and linkage with financial system - Weak - Strong

Replacement cost - RMB400/t - RMB3,000/t

Total estimated closure compensation - RMB40b based on 100mt closure - RMB180b for Hebei, RMB21b for Jiangsu

Gross capacity growth +4% gross capacity in 2014 +3.0% gross capacity in 2014

+1.1% net capacity in 2014 (incl. backward cap. Closure) +1.7% net capacity in 2014 (incl. indicated Hebei & Jiangsu closure)

Utilization (Net) 77% in 2013 and 81% in 2014E 77% in 2013 and 78% in 2014E

Demand growth 5.6% in 2014E 3.5% in 2014E

Product types Only 3 grades of cement (32.5, 42.5, 52.5) Thousands of steel products with different specifications

Production rationing Yes No

Difficulties of closure or suspension - Still profitable before additional emission charge and tax rebate cancellation

- Significant unemployment rate concern

- Kiln suspension and resumption cost: RMB500k - Huge compensation needed, which may not be borne by local government

- Blast furnace suspension and resumption cost: RMB50m

- Coking plant will break if frequently suspended

Source: BNP Paribas

EXHIBIT 7: Six-month daily return: Anhui Conch, Magang, Angang

Sources: Bloomberg; BNP Paribas

(50)

(30)

(10)

10

30

50

Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14

(%) Angang Magang Anhui Conch

9

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Tight funding and low utilization to keep profits thin in 2014

Back in 2011, tight funding was the key reason dragging down the China steel price.

The price drop in 2012 was due to a slowdown in steel demand drivers (i.e., property,

railways, shipbuilding). The increase in the interest rate and tight funding dragged

the steel price down again in 2013.

An increasing number of steel traders have been forced into bankruptcy since 3Q11,

increasing bad loan provisions to banks from 2011 to early 2013. Given their bad

experiences with the steel sector as well as the discouraging message from the

government about overcapacity in the steel sector, many banks are reluctant to lend

to steel-related companies, including steel mills. Due to the heavy capital needs of

steel projects, both private and SOE steel company projects under construction are

heavily geared, which means they suffer from financial risk in a tight funding

environment. The profitable and positive outlook is encouraging cement leaders to

continue M&A to increase market concentration.

After two years of steel trader clean-up with tight funding, most of the speculators

have been closed. Based on our communication with steel traders and mills at the

annual steel conference in Shanghai, we found that the traditionally superior position

of steel mills over steel traders is declining. Many steel traders are not willing to be

direct distributors for steel mills, helping to bear the steel mills’ inventories, which is

causing steel mills’ inventories to inevitably increase while steel traders’ inventories

remain at low levels. In addition, some steel traders, for the first time, have asked

steel mills to sell on bank-draft, instead of the traditional full-cash, basis. Low steel

capacity concentration reduces the bargaining power of overseas iron ore suppliers,

so China steel leaders would prefer to acquire overseas iron ore assets rather than

acquiring loss-making steel mills domestically.

The increasing finance cost burden is forcing steel mills to continue operating at high

utilizations to maintain cash flow even with high inventories and low margins

(Exhibits 8-13). Tangshan steel billet producers have turned from moderately

profitable to loss-making since the beginning of 2013. We believe steel mills normally

have healthy balance sheets, so we think problematic steel mills’ financial reserves

can keep them running for at least another 1-1.5 years, based on reference to the

clean-up period of the steel traders.

EXHIBIT 8: Steel price vs. M2 EXHIBIT 9: Steel price vs. SHIBOR

Sources: CEIC; MySteel; BNP Paribas Sources: MySteel; Bloomberg; BNP Paribas

10

12

14

16

18

20

22

24

26

28

30

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

(%)(RMB/tonne)

Rebar steel price M2 yoy growth (RHS)

0

2

4

6

8

10

12

3,000

3,200

3,400

3,600

3,800

4,000

4,200

4,400

4,600

4,800

5,000

2008-09-28

2009-02-25

2009-07-17

2009-12-09

2010-05-05

2010-09-21

2011-02-18

2011-07-12

2011-12-02

2012-04-26

2012-09-14

2013-02-07

2013-07-04

2013-11-26

(%)(RMB/tonne)

SHIBOR - 1 week (LHS)

HRB400: 20mm price - Shanghai (RHS)

10

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

EXHIBIT 10: Key steel mills’ profit margin EXHIBIT 11: Tangshan billet producers’ profit & loss

Sources: MySteel; BNP Paribas Sources: MySteel; BNP Paribas

EXHIBIT 12: Steel mill inventory EXHIBIT 13: Steel trader inventory

Sources: MySteel; BNP Paribas Sources: MySteel; BNP Paribas

(25)

(20)

(15)

(10)

(5)

0

5

10

15

(1,400)

(1,200)

(1,000)

(800)

(600)

(400)

(200)

0

200

400

600

800

1,000

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

(%)(RMB/tonne) Profit per tonne Profit margin (RHS)

(500)

(400)

(300)

(200)

(100)

0

100

200

300

400

0

1,000

2,000

3,000

4,000

5,000

Apr-11

Jun-11

Aug-11

Oct-11

Dec-11

Feb-12

Apr-12

Jun-12

Aug-12

Oct-12

Dec-12

Feb-13

Apr-13

Jun-13

Aug-13

Oct-13

Dec-13

(RMB/tonne) (RMB/tonne)Tangshan billet profit/(loss) (RHS)

Tangshan billet ex-factory price

Tangshan billet unit cost

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Apr-06

Sep-06

Feb-07

Jul-07

Dec-07

May-08

Oct-08

Mar-09

Aug-09

Jan-10

Jun-10

Nov-10

Apr-11

Sep-11

Feb-12

Jul-12

Dec-12

May-13

Oct-13

('000 tonnes)

0

5,000

10,000

15,000

20,000

25,000

Apr-06

Oct-06

Apr-07

Oct-07

Apr-08

Oct-08

Apr-09

Oct-09

Apr-10

Oct-10

Apr-11

Oct-11

Apr-12

Oct-12

Apr-13

Oct-13

('000 tonnes)

Average since 2006

11

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Emission penalties not yet relevant in 2014 on lack of funding

The Ministry of Environmental Protection (MEP) announced the latest emission

standards for the steel sector in June 2012, effective in January 2015 (Exhibit 14).

Among all the emissions, we think we should focus on DeSOx and water treatment

for steel mills due to their heavy capex (RMB30m-120m per line) and substantial unit

operating cost increase (RMB 30-107/t).

EXHIBIT 14: Steel emission standards table

Unit Current standard

----------------- Standard to be effective from 2015 -----------------

For existing capacity For new capacity In key regions

SOx mg/m³ 600 200 200 180

NOx mg/m³ 500 300 300 300

PM mg/m³ 80 50 50 40

Sources: MEP; BNP Paribas

2013 research on Chinese steel mills’ environmental protection costs, published by

the China Metallurgical Industry Planning and Research Institute, suggested that for

integrated iron and steel works to meet the latest emission standards, the average

expense on environmental protection is around RMB100-107/t on a crude steel

basis. Of this cost, RMB20-26/t is for water treatment and RMB80/t is spent on flue

gas treatment: a RMB69/t additional electricity cost and RMB11/t DeSOx.

EXHIBIT 15: Total unit environmental cost for steel mills

Unit

Unit price

Consumption per ton of crude steel

Cost per ton of crude steel

Remarks

(RMB)

Electricity used in flue gas treatment

kWh 0.65 106.7 69 Majority is electricity

DeSOx for sintering flue gas

ton of sintered ore

8 1.35 11 Fully DeSOx

Subtotal 80

Sewage in steel making

m^3 0.5~0.7 20 10~14

General sewage treatment

m^3 3 2.5~3 7.5~9 Equipped with deep treatment facilities

Coking sewage treatment

m^3 12 0.2~0.3 2.4~3.6 Equipped with deep treatment facilities

Subtotal 19.9~26.6

Total 99.9-106.6

Sources: China Metallurgical Industry Planning and Research Institute

Status of DeSOx equipment installation and operation in China’s steel industry

DeSOx treatment has not been widely employed in China’s steel industry so far. By

the end of 2012, DeSOx equipment had been installed on 389 sets of sintering

machines in China, amounting to around 32% of China’s 1,200 total sintering

machines and around 50% of China total if measured in m2.

Even for the 389 sets of sintering machines with DeSOx equipment, that equipment

is not running 24/7. Big SOE mills perform better on keeping DeSOx equipment

running; while private SMEs are neither willing nor motivated to run DeSOx treatment

all the time, given that the occasional fines on illegal emissions are less than 10

times the daily DeSOx operating expense (for a 360m2 sintering machine). An early

2013 investigation in north China by the MEP reveals that nearly 70% of steel mills

failed to meet emission standards. The grand average of SOx removal efficiency in

China’s steel sector was only 38.6% in June 2013 (as opposed to >=80% designed

efficiency), according to an MEP official. The efficiency for 2011 was 47.3%. More

sintering machines are equipped with DeSOx, while average removal efficiency

declines, indicating a worsening trend in DeSOx operation sectorwide.

The MIIT announced a first and second list of steel mills that meet 2012 Iron and

Steel Industry Standard Conditions in April and December 2013. Total crude steel

12

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

capacity of 160 steel mills in these two lists is estimated to be around 640mtpa,

which is about 64% of the 2012 China total. The third list is to be published in 1H14.

The three lists are to include 80-90% of China’s total crude steel capacity, and only

steel mills named in the lists will be eligible for future support policies, according to

the MIIT. A punitive electricity price will be applied to the other steel mills who fail to

appear in the lists.

Given the large percentage electricity takes of steel mills’ environmental protection

costs, a punitive electricity price appears to be quite a big negative for mills not in the

lists if the standards are to be strictly enforced. However, we do not think the timeline

for the implementation of punitive electricity price is clear yet. In addition, most

Chinese steel mills are struggling at breakeven level and face tight funding pressure.

It’s difficult for them to finance DeSOx equipment installation and operation. At the

same time, funding costs keep increasing. Mills are poorly positioned to follow the

stringent emission standards, unless subsidies are to be provided. Although

governments wish to enforce standards for air quality and on overcapacity concerns,

we do not see enough funding from the government for redundancy settlements and

closure compensation in the near term, as explained below. As a result, we do not

see any substantial change in the 2014 outlook.

Enforcement difficulties

We see the hurdles for significant capacity closures as being a lack of clarity on

compensation plans and sources, as well as the unemployment issue. Average steel

labour productivity is 100t per year. Therefore, closing 60mt of steel capacity in

Hebei implies 600,000 workers, or 6% of Hebei’s total workforce, will be affected.

Based on the assumption of a RMB3,000/t replacement cost for steel mills, the

Tangshan government needs total theoretical compensation of RMB120b to close

40mt by 2017. With only an RMB50b central government subsidy for steel capacity

closures for Beijing-Tianjin-Hebei, we find it difficult to see the Tangshan or Hebei

government financing the compensation gap, not to mention the problems of the

associated bad bank loans. Steel traders and mills in Hebei see limited alternatives

for the transfer of the steel sector, given a bearish regional property market and other

non-steel commodities businesses.

In conclusion, we do not expect significant forced closures of steel capacity in the

short term, unless the local government lays out solid plans for compensation and

the source of its funding.

13

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Steel demand growth to slow to 4% 2014

Proactive fiscal policy and Neutral monetary policy in 2014

Based on our economist Chen Xingdong’s report China Perspectives 2014:

Addressing 12 questions (3 January), we expect a proactive fiscal policy and a

neutral monetary policy in 2014. The CEWM maintained the macro policy lines for

2014. Under the reform perspectives, both Xi Jinping and Li Keqiang set the basic

lines: macro policy must remain relatively stable, micro policy must be active and

flexible, and social policy is to provide bottom-line support. As such, fiscal policy

remains proactive. Proactive fiscal policy would mean enlarging the budget deficit;

under strict controls the central government might allow local governments to raise

debt capital through legal and transparent ways. The central government would

continue undertaking structural tax cutting through conversion of business taxes to

VAT in service sectors. For detailed fiscal policy, we should wait for the national fiscal

and financial meeting, which usually follows the CEWM. Through the terms of the so-

called ‘‘prudent’’ monetary policy, policy is neither expansionary nor contractionary,

but the government declines to use the term ‘‘neutral’’. In our observations, the

government and PBOC intend to exercise a policy of neutral-tilted tightening. We

expect the PBOC will fail to meet its controlling target of broad money supply M2 at

13% in 2013 as M2 at November was still a high 14.2%. We believe the central bank

will still set 13% M2 growth as the controlling target in 2014. On the other hand, we

believe lessons have been learnt from 2008-09 and that it is understood that the

China economy is overleveraged. The leverage ratio measured by broad money, M2,

against GDP has exceeded 200%, a rare case globally. The PBOC is under

tremendous pressure to deleverage the economy, although it might take a long time.

Therefore, we expect the ‘‘prudent’’ monetary policy in 2014 to be a passive one, i.e.,

a follower, or accommodative to growth. Liquidity management by monitoring the

weighted interest rate in the interbank market and referring to the changes in bond

yield curves would likely be the key policy focus.

EXHIBIT 16: BNP China macro forecast v. street

---------------------- 2013E ---------------------- ---------------------- 2014E ----------------------

BNPP Street BNPP Street

GDP (y-y %) 7.7 7.7 7.3 7.5

Industrial output (y-y %) 9.7 9.6 9.1 9.4

Retail sales (y-y %) 13.0 12.9 13.2 13.8

FAI (y-y %) 19.8 19.9 17.2 19.3

Exports (y-y %) 7.2 7.7 7.5 8.6

Imports (y-y %) 6.9 7.4 6.8 8.6

Trade balance (USD b) 254.1 254.0 286.8 276.0

Current account to GDP (%) 2.6 2.4 2.4 2.3

M2 (y-y %) 13.4 13.8 12.8 12.9

1-yr deposit rate (EOP, %) 3.00 - 3.00 -

1-yr lending rate, (EOP, %) 6.00 6.00 6.00 6.00

RRR for major banks (%) 20.0 - 19.0 -

RMB/USD (EOP) 6.05 - 5.89 -

Budget balance/GDP (%) (2.1) (1.8) (2.1) (1.8)

CPI (y-y %) 2.6 2.7 2.8 3.1

PPI (y-y%) (2.0) (1.7) 0.5 0.8

Sources: Concensis Economics; BNP Paribas

Steel demand growth to slow from 9% in 2013 to 4% in 2014

We forecast China’s crude steel apparent consumption will grow 8.6% to 724mt in

2013 and 3.5% to 749mt in 2014, with production to slow from 9.2% in 2013 to 3.4%

in 2014.

14

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

EXHIBIT 17: Steel demand breakdown in 2014E EXHIBIT 18: Steel demand by segment changes

Sources: Mysteel; BNP Paribas estimates Sources: Mysteel; BNP Paribas estimates

Property (27% of steel demand): Constraints kick in, sales growth has peaked

We forecast steel demand growth in the property segment to slow from 10% in 2013

to 2.8% in 2014. Based on our property team’s report Constraints kick in, sales

growth has peaked (6 December, 2013), growth in floor space sold will slow from

20% in 2013 to 5-10% in 2014E. Key issues in the 2014 property market are:

§ Landbank replenishment will be the biggest constraint on growth. Our property

team has analysed the past landbank replenishment behaviour for each

developer and projected proportions of landbank to contracted sales growth. The

results point to landbank replenishment as the biggest constraint against

sustained 30%-plus annual growth for most developers over the next few years.

§ Balance sheet & funding constraints. The developers who have been more active

in raising funds in the offshore market are those who have been more aggressive

in their landbanking. With QE tapering starting in 2014, the ability to raise funds

via the offshore channel could be constrained. This would further affect the pace

of landbanking in 2014 and beyond. Despite the good sales in 2013, net gearing

positions of most developers have not significantly improved. This should limit

their ability to further gear up to buy land.

§ Saleable resource constraint in 2014. Macro data-wise, floor space starts have

not been able to catch up with the rapid pace of sales growth since July 2012

(Exhibit 19).

§ More tightening before any loosening: 1) Plans are to reduce local governments’

reliance on land sales for financing; 2) Given the pace of property price increases

is continuing to accelerate in Tier 1 & 2 cities, local governments could tighten the

enforcement of existing policies, such as HPR, before their eventual relaxation.

Railway2.5% Highway

2.7%

Property25.7%

Machinery16.9%

Environmental & utility14.8%

Urban transit2.3%

Auto7.2%

White goods1.6%

Shipbuilding2.4%

Energy5.2%

Mines5.3%

Others13.6%

(4)(2)02468101214

Railw

ay

Highway

Property

Machinery

Environmental & utility

Urban transit

Auto

White goods

Shipbuilding

Energy

Mines

(y-y %)

15

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

EXHIBIT 19: YTD monthly nationwide area starts vs. area sold y-y % change

Sources: NBS; BNP Paribas

EXHIBIT 20: Steel demand in the property segment

Property 2010 2011 2012 2013E 2014E 2015E

Total property

Total steel consumption- property (k tonnes) 131,659 154,674 170,097 187,266 192,541 196,724

Change (y-y %) 15.0 17.5 10.0 10.1 2.8 2.2

% of total steel consumption 22.0 23.8 25.5 25.9 25.6 25.3

Private commodity prop. consumption as % of total property demand 48 46 44 50 53 54

Public prop. steel consumption % of total property demand 9 14 18 13 10 10

Commercial prop. consumption as % of total property demand 42 40 38 37 37 36

Steel needed per real estate C&I FAI (k/RMB b) 38.97 35.79 34.25 32.74 30.52 28.56

Total property FAI (RMB b) 4,827 6,174 7,096 8,171 9,011 9,840

Change (y-y %) 33.2 27.9 14.9 15.2 10.3 9.2

Investment in property (C&I) (RMB b) 3,379 4,322 4,967 5,720 6,308 6,888

Commodity buildings (private)

Total steel consumption - private commodity (k tonnes) 63,558 71,521 74,884 94,354 102,044 107,146

Change (y-y %) 17.6 12.5 4.7 26.0 8.1 5.0

Investment in non-social housing property (RMB b) 4,278 5,244 5,833 7,166 8,209 9,092

Change (y-y %)

11.2 22.9 14.6 10.8

Floor space sold - Commodity (m sq. m) (private) 1,043 1,099 1,086 1,303 1,368 1,437

Change (y-y %) 10.1 5.4 (1.2) 20.0 5.0 5.0

Average area per flat - commodity (sq.m) 90 90 90 90 90 90

Steel needed (tonne per sq. m) 0.061 0.065 0.069 0.072 0.075 0.075

Social Housing

Total steel consumption - public housing (k tonnes) 12,421 21,514 29,875 24,307 19,833 18,914

Change (y-y %) 2 73 39 (19) (18) (5)

Government target of unit starts (m) 5.9 36

Units to be started (m) 5.9 10.4 8.0 6.5 6.0 5.1

Investment in social housing (RMB b) 549 930 1263 1005 802 748

Change (y-y %) 207 69 36 (20) (20) (7)

Floor space completed (m sq.m) 198 335 456 362 289 270

Change (y-y %) 0 69 36 (20) (20) (7)

Average house size (sq.m) 60 60 60 60 60 60

Steel needed (t/sq. m) 0.063 0.064 0.066 0.067 0.069 0.070

Sources: MySteel; BNP Paribas estimates

(40)

(20)

0

20

40

60

80

100

120

Mar-99

Oct-99

May-00

Dec-00

Jul-01

Feb-02

Sep-02

Apr-03

Nov-03

Jun-04

Jan-05

Aug-05

Mar-06

Oct-06

May-07

Dec-07

Jul-08

Feb-09

Sep-09

Apr-10

Nov-10

Jun-11

Jan-12

Aug-12

Mar-13

Oct-13

(y-y %) YTD floor space sold YTD floor space started

20.8

10.5

16

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Auto segment (7% of steel demand): Growth still on track

Based on our auto team’s report China Auto: 2014 – Growth still on track (6

December, 2013), our house forecast is for passenger vehicle sales to grow 15.7% in

2013 and 14.4% in 2014 due to consumption upgrades and rising penetration in tier-

2 and tier-3 cities. This implies 7.5% steel demand growth in the auto segment in

2014.

EXHIBIT 21: Steel demand in the auto segment

Auto 2010 2011 2012 2013E 2014E 2015E

Total steel consumption - Autos (k tonnes) 42,000 43,200 46,200 49,900 53,660 60,368

Change (y-y %) 22.1 2.9 6.9 8.0 7.5 12.5

Steel needed per unit (t/unit) 2.3 2.3 2.4 2.2 2.1 2.1

% of total steel consumption 7.01 6.64 6.93 6.90 7.17 7.80

Auto production (k units) 18,243 18,432 19,261 22,285 25,494 28,681

Change (y-y %) 32.5 1.0 4.5 15.7 14.4 12.5

Sources: MySteel; BNP Paribas estimates

White goods (1.6% of steel demand): Moderate white goods demand growth of 2%

After the end of the white goods subsidy in June 2013, white goods demand faced a

short-term growth catalyst. In the medium term, we believe the following factors can

support continuous growth of white goods demand:

§ Increasing residential income and urbanization;

§ Upgrades to more environmentally friendly and high-quality goods;

§ Demand tends to be more stable after wider application in public services (i.e.

more public areas with installed air con);

§ Continuous growth in white goods exports.

Based on a 2% white goods demand growth assumption in 2014, we forecast steel

demand to drop 1% y-y in 2014 (vs. +3.5% y-y in 2013E).

EXHIBIT 22: Steel demand in the white goods segment

White goods 2010 2011 2012E 2013E 2014E 2015E

Total steel consumption - Shipping (k tonnes) 9,000 11,300 11,500 11,900 11,774 11,649

Change (y-y %) 11.1 25.6 1.8 3.5 (1.1) (1.1)

Steel needed per FAI (t/k unit) 35.5 37.7 40.0 37.9 36.73 35.6

% of total steel consumption 1.50 1.74 1.73 1.64 1.57 1.51

White goods production (m units) 254 299 287 314 321 327

Change (y-y %) 28.5 18.1 -4.0 9.3 2.0 2.0

Sources: MySteel; BNP Paribas estimates

Machinery segment (18% of steel demand): Relying on replacement and upgrades

Under the stable-growth macro target announced by the central government, we do

not expect significant new demand in machinery. China has a huge reserve of

operating power machinery, cars, construction machinery, etc., which can sustain the

demand for machinery replacement. According to MySteel, when GDP grows at 7-

8%, machinery demand growth is 10-15%. However, we conservatively put it at 8%

y-y for 2014 in our assumptions, as we believe policies to curb overcapacity may

further hinder machinery demand, implying 3.4% steel demand growth in the

machinery segment in 2014.

17

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

EXHIBIT 23: Steel demand in the machinery segment

Machinery 2010 2011 2012 2013E 2014E 2015E

Total steel consumption – Machinery (k tonnes) 106,100 114,800 117,500 122,500 126,670 129,904

Change (y-y %) 34 25 9.2 4.3 3.4 2.6

Steel needed per C&I FAI - Road (kt/ RMB b)

% of total steel consumption 17.71 17.64 17.63 18.38 17.50 17.35

Machinery gross output (RMB b) 13,510 16,887 18,441 20,285 21,908 23,222

Change (y-y %) 34 25 9.2 10.0 8.0 6.0

Sources: MySteel; BNP Paribas estimates

Shipbuilding segment (3% of steel demand): Better than 2013

We expect average the shipping rate in 2014 to be higher than 2013, which will

cause a recovery in the shipbuilding sector. After years of decline in the bulk and oil

shipping business, we expect 2014 to start to recover. Following the increasing price

of vessels in 2014, the oversupply situation should improve. We conservatively

forecast shipbuilding demand to grow 10% and cause a 7.2% increase in steel

demand in the segment.

EXHIBIT 24: Steel demand in the shipbuilding segment

Shipbuilding 2010 2011 2012 2013E 2014E 2015E

Total steel consumption - Shipping (k tonnes) 23,400 22,600 20,100 16,700 17,900 18,489

Change (y-y %) 61.4 (3.4) (11.1) (16.9) 7.2 3.3

Steel needed per FAI (kt/10k DWT) 1.1 2.1 2.1 3.2 3.1 3.1

% of total steel consumption 3.91 3.47 3.02 2.31 2.39 2.39

Shipping demand (10k DWT) (Under construction - completed + started orders) 20,553 10,948 6,459 5,167 5,684 6,025

Change (y-y %) 8.7 (46.7) (41.0) (20) 10 6

Sources: MySteel; BNP Paribas estimates

Infrastructure

Infrastructure construction growth slowed in 2012, partly due to inadequate funding,

especially for high-speed railways. We conservatively expect infrastructure projects

started in 2H13 to continue in 1H14. We forecast infrastructure FAI growth to slow

from 23% y-y in 2013 to 16% y-y in 2014.

Investment in environment management and municipal infrastructure (15% of steel demand)

Given greater environmental concerns and urbanization, investment in environment

management and municipal infrastructure will likely continue to see the fastest

growth among all infrastructure segments, with 18% growth in 2013. We expect the

trend to continue in 2014 with 16% growth.

EXHIBIT 25: China construction and installation FAI growth

Sources: CEI; BNP Paribas

0

10

20

30

40

50

60

Jan-04

Jun-04

Nov-04

Apr-05

Sep-05

Feb-06

Jul-06

Dec-06

May-07

Oct-07

Mar-08

Aug-08

Jan-09

Jun-09

Nov-09

Apr-10

Sep-10

Feb-11

Jul-11

Dec-11

May-12

Oct-12

Mar-13

Aug-13

(%) CN: FAI: YoY: ytd: Construction and Installation

18

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Railway (2.5% of steel demand) – slow in railway construction

Based on the most up-to-date government target of 123,000km total railway by 2015,

we forecast 7,500km to be completed in each of 2014 and 2015. Although the length

completed should be more than the 6,200km we expect in 2013, we expect railway

investment to rely more on equipment purchase and installation in 2014 and 2015 as

most of the planned construction works have been completed this year (total railway

FAI growth of 10% y-y vs. railway construction FAI 2% y-y in 2013E). We forecast

steel demand from the railway segment to decline 2% in 2014.

EXHIBIT 26: Steel demand in the railway segment

Railway 2010 2011 2012 2013E 2014E 2015E

Total steel consumption - Railway (kt) 28,386 18,762 19,462 19,245 18,838 17,649

Change (y-y %) 13.6 (33.9) 3.7 (1.1) (2.1) (6.3)

Steel needed per railway FAI (kt/RMB b) 33.68 32.00 31.04 30.11 29.21 28.33

% of total steel consumption 4.74 2.88 2.92 2.66 2.52 2.28

Steel needed per railway C&I FAI (kt/RMB b) 56.8 48.7 47.3 45.8 44.5 43.2

FAI - Railway (RMB b) 843 586 627 691 645 623

Change (y-y %) 19.6 (30.4) 6.9 10.2 (6.7) (3.4)

FAI ratio per mile (RMB b/mile) 231.1 144.6 96.5 92.5 92.5 92.5

Total mileage - Railways ('000 km) 91.2 95.2 101.7 108.0 115.5 123.0

Change (y-y %) 6.6 4.4 6.8 6.2 6.9 6.5

Net increased mileage 3.6 4.1 6.5 6.3 7.5 7.5

FAI ratio per mile (RMB b/mile) 137 95 63 67 56 55

C&I FAI 500 385 412 420 423 409

Change (y-y %) 17.5 (23.0) 6.9 2.0 0.9 (3.4)

Sources: MySteel; BNP Paribas estimates

Highways (3% of steel demand): High growth not sustainable

We forecast highway cement demand based on the 12th Five-Year Plan target to

reach 4,500k km, implying completion of 100k km each year during 2013-15.

However, due to high growth of 19% road FAI in 2013, we conservatively forecast

road FAI to stay flat in 2014, implying steel demand in the highway segment declines

3% for 2014.

EXHIBIT 27: Steel demand in the highway segment

Highway 2010 2011 2012 2013E 2014E 2015E

Total steel consumption - Roads 19,174 20,000 17,834 20,519 19,868 19,984

Change (y-y %) 14.9 4.3 (10.8) 15.1 (3.2) 0.6

Steel needed per FAI - Road (kt/RMB b) 15.62 14.84 14.40 13.97 13.55 13.14

% of total steel consumption 3.20 3.07 2.68 3.08 2.98 3.00

FAI - Road (RMB b) 1,227 1,347 1,436 1,704 1,701 1,764

Change (y-y %) 20.9 9.8 6.6 18.6 (0.2) 3.7

Total mileage - Roads ('000 km) 4,008 4,106 4,205 4,310 4,410 4,510

Change (y-y %) 3.8 2.4 2.4 2.5 2.3 2.3

FAI ratio per mile (RMB b/mile) 8.33 13.73 14.41 14.99 15.71 16.34

Expressways 74 85

1st Grade 64

2nd Grade 309

3rd Grade 388

4th Grade 2,470

Net increased mileage ('000 km) 147.4 98.2 98.5 105.0 100.0 100.0

Sources: MySteel; BNP Paribas estimates

19

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Steel price forecast: To peak in 2Q14

Against a background of capacity pressure and slow demand growth in 2014

lowering the iron ore price, we expect the China steel price to drop 3% y-y in 2014

with limited volatility. We expect the steel price to peak in 2Q14 due to: 1) carried

forward construction projects; 2) less tight funding right after CNY.

Key reasons for our 3% price decline forecast in 2014 are:

§ Tight funding in 2014, especially biased against the steel sector, a limited steel

price hike;

§ Steel utilization remaining low, which hinders price hikes;

§ Increasing international iron ore supply, negative to the steel price;

§ Implementation of tighter emission controls and low steel trader inventories will

moderately improve the overcapacity issue.

EXHIBIT 28: BNP Steel price forecasts

(RMB/tonne) 2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015E

HRC price 3,981 4,294 4,961 3,677 4,174 4,596 3,990 3,686 3,595 3,416

Re-bar price 2,934 3,560 4,528 3,513 4,083 4,705 3,916 3,550 3,442 3,236

HRC (y-y %) (6) 8 16 (26) 14 10 (13) (8) (2.5) (5)

Rebar (y-y %) (10) 21 27 (22) 16 15 (17) (9) (3.0) (6)

(RMB/tonne) 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13E 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

HRC price 4,251 4,203 3,660 3,883 4,077 3,600 3,595 3,501 3,554 3,784 3,557 3,486

Re-bar price 4,248 4,112 3,640 3,706 3,777 3,477 3,504 3,483 3,483 3,657 3,365 3,264

HRC (q-q %) (2) (1) (13) 6 5 (12) (0) (3) 2 7 (6) (2)

Re-bar (q-q %) (5) (3) (11) 2 2 (8) 1 (1) 0 5 (8) (3)

(USD/tonne) 2013 2014 2015

Iron ore price 136 125 110

Sources: CEIC; MySteel; Bloomberg; BNP Paribas estimates

20

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Appendix 1

EXHIBIT 29: China steel prices EXHIBIT 30: Coking Coal price

Sources: Bloomberg; BNP Paribas estimates Sources: Wind; BNP Paribas estimates

EXHIBIT 31: 10-day China crude steel daily production EXHIBIT 32: China rebar price vs. imported iron ore price

Sources: www.96369.net; BNP Paribas estimates Sources: MySteel; BNP Paribas estimates

EXHIBIT 33: Large mill cash margin vs. utilization EXHIBIT 34: Utilization react to small mills’ profit/loss

Sources: Bloomberg; BNP Paribas estimates Sources: MySteel; BNP Paribas estimates

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Jan-06

Jun-06

Nov-06

Apr-07

Sep-07

Feb-08

Jul-08

Dec-08

May-09

Oct-09

Mar-10

Aug-10

Jan-11

Jun-11

Nov-11

Apr-12

Sep-12

Feb-13

Jul-13

Dec-13

(RMB/tonne) China HRC 3mm spot

China CRC 1mm spot

China Steel Rebar 25mm spot

950

1,050

1,150

1,250

1,350

1,450

1,550

1,650

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

Jan-11

Apr-11

Jul-11

Oct-11

Jan-12

Apr-12

Jul-12

Oct-12

Jan-13

Apr-13

Jul-13

Oct-13

(RMB/tonne)

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

Jan-11

Apr-11

Jul-11

Oct-11

Jan-12

Apr-12

Jul-12

Oct-12

Jan-13

Apr-13

Jul-13

Oct-13

(m tonnes)

50

250

450

650

850

1,050

1,250

1,450

1,650

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000Mar-05

Oct-05

May-06

Dec-06

Jul-07

Feb-08

Sep-08

Apr-09

Nov-09

Jun-10

Jan-11

Aug-11

Mar-12

Oct-12

May-13

Dec-13

(RMB/tonne)(RMB/tonne) China - SH Rebar price (LHS)

China iron ore px (Major ports) (RHS)

(500)

(400)

(300)

(200)

(100)

0

100

200

% 80

% 85

% 90

% 95

% 100

Jun-12

Aug-12

Oct-12

Dec-12

Feb-13

Apr-13

Jun-13

Aug-13

Oct-13

Dec-13

(RMB/tonne)(%)

Big steel rebar cash margin (spot) (RHS)

Tangshan utilization rate

(200)

(100)

0

100

200

300

400

500

600

% 80

% 85

% 90

% 95

% 100

Jun-12

Jul-12

Aug-12

Sep-12

Oct-12

Nov-12

Dec-12

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

(RMB/tonne)(%)

Small mill rebar cash margin (spot) (RHS)

Tangshan utilization rate

84%

99% 97%

91%

21

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Appendix 2

DeSOx technology comparison

Emissions generated during the sintering process contribute 60-70% to total SOx

emissions in steelmaking. DeSOx technologies applied in sintering flue gas

treatment can be classified into three categories based on desulfurizer: 1) the wet

method; 2) the semi-dry method; 3) the dry method.

EXHIBIT 35: DeSOx technology comparison

Semi-dry Dry Wet

Example CFB Active coke absorption

Limestone-gypsum, ammonia FDG

SOx removal efficiency >=90% 80~90% >=95%

Corrosion slight no serious

Waste water treatment no no yes

Total investment (RMB m) 72 80 120

Operating cost (RMB/tonne of sintered ore) 3-5 7-8 5-10

Suitable for flue gas amount small-mid small-mid large

Suitable for SO2 density low-mid low-mid mid-high

Sources: Company data; BNP Paribas estimates

The wet method is the more traditional and mature technology, as compared with dry

and semi-dry. Its DeSOx efficiency is the highest of the three. Limestone-gypsum

and ammonia FGD are two common wet methods. Revenue from the sale of

ammonium sulphate, a by-product of ammonia FDG, can help reduce DeSOx cost;

while gypsum, a by-product of limestone-gypsum, is already oversupplied in China.

Main drawbacks of the wet method are: 1) the corrosion it brings, 2) it is difficult to

upgrade/transform if DeNOx equipment is needed in the future, and 3) the sewage

generated is difficult to treat.

The dry method is a more recent development than the wet method, with a more

difficult process and more complex equipment. The major advantage of a dry method

(like active coke absorption) is that it can remove not only SOx, but also NOx and

dioxins. But active coke absorption is usually more expensive than wet methods.

The Circulating Fluidized Bed (CFB) method is one of the semi-dry methods.

EXHIBIT 36: CFB vs. ammonia-ammonium sulphate

CFB Ammonia-ammonium sulphate

Land size small Large

SOx removal efficiency 90%~99.7% 90-95%

Sewage no Yes, but recycled, no external discharge

Corrosion no Serious on equipment

Absorbent consumption 2.1t/h 1.22t/h

Water consumption 36t/h 23t/h

Annual operating & maintenance cost (RMB m) 800 1000

Total investment (for 100 sqm) (RMB m) 34 38

Sources: Sichuan Industrial Research Institute of Environmental Monitoring, BNP Paribas estimates

So far, no method dominates in the sector. All methods, if applied for suitable

machine size and feed flue gas density, can lower SOx emissions to meet the current

200mg/m3 standard in theory. But in practice, poorly designed or installed equipment,

or improper operation may lead to lower-than-designed efficiency.

22

China Steel Sector Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Operating cost structure of DeSOx in the steel industry

EXHIBIT 37: Operating cost structure of limestone-gypsum

Limestone-gypsum Annual consumption Unit cost Annual cost Cost

(RMB) (RMB m/year) (RMB/tonne of sintered ore)

Operating cost

CaO 16100t 275 4.51 1.45

Sewage treatment 80000t 2.5 0.20 0.064

Electricity 29704000 0.52 15.45 4.966

Water 640000 2 1.28 0.412

Salary 0.66 0.211

Equipment maintenance 0.97 0.313

Revenue from by-product (0.91) (0.293)

Total DeSOx cost 22.16 7.123

Source: BNP Paribas estimates

EXHIBIT 38: Operating cost structure of ammonia FGD

Ammonia FGD Annual ----- Unit cost ----- ---- Annual cost ---- ------------ Cost ------------

Operating cost consumption Liquid

ammonia Aqueous ammonia

Liquid ammonia

Aqueous ammonia

Liquid ammonia

Aqueous ammonia

(RMB/tonne or kwh) (RMB m /year) (RMB/tonne of sintered ore)

Liquid ammonia, Aqueous ammonia

8kt/40kt 2750 400 22.0 16.00 7.07 5.14

Vapor 46kt 65 65 3.0 3.0 0.963 0.963

Electricity 17.2m*kwh 0.52 0.52 89.1 8.9 2.87 2.87

Water 640kt 2 2 1.28 1.28 0.412 0.412

Salary 0.66 0.66 0.211 0.211

Equipment maintenance

0.83 0.83 0.265 0.265

Revenue from by-product

(18.0) (18.0) (5.8) (5.8)

Total DeSOx cost 18.7 12.7 5.99 4.06

Source: BNP Paribas estimates

EXHIBIT 39: Operating cost structure of active coke absorption

Active coke absorption annual operating cost

(RMB m)

Consumables 22.2

Electricity 15.34

Salary 3.0

Maintenance 4.1

Depreciation

other 2.0

Total operating cost 48.7

operating cost/t of sintered ore (RMB) 9.75

Source: BNP Paribas estimates

The unit incremental cost of DeSOx ranges between RMB12-15/t of sintered ore

between the various methods, and 1.275t of sintered ore is needed to produce 1t of

crude steel. So, a RMB15-20/t DeSOx cost would be added for crude steel

production to meet the current (June 2012) emissions standards.

23

Not worth the high premium

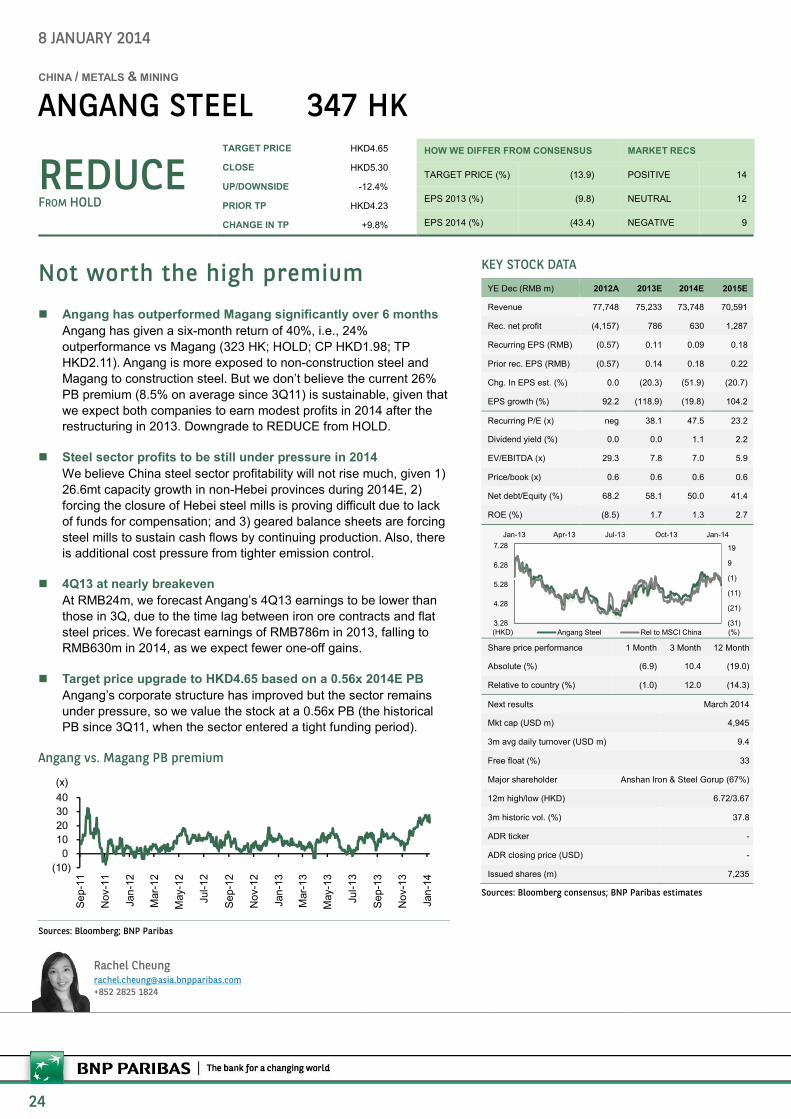

n Angang has outperformed Magang significantly over 6 months

Angang has given a six-month return of 40%, i.e., 24%

outperformance vs Magang (323 HK; HOLD; CP HKD1.98; TP

HKD2.11). Angang is more exposed to non-construction steel and

Magang to construction steel. But we don’t believe the current 26%

PB premium (8.5% on average since 3Q11) is sustainable, given that

we expect both companies to earn modest profits in 2014 after the

restructuring in 2013. Downgrade to REDUCE from HOLD.

n Steel sector profits to be still under pressure in 2014

We believe China steel sector profitability will not rise much, given 1)

26.6mt capacity growth in non-Hebei provinces during 2014E, 2)

forcing the closure of Hebei steel mills is proving difficult due to lack

of funds for compensation; and 3) geared balance sheets are forcing

steel mills to sustain cash flows by continuing production. Also, there

is additional cost pressure from tighter emission control.

n 4Q13 at nearly breakeven

At RMB24m, we forecast Angang’s 4Q13 earnings to be lower than

those in 3Q, due to the time lag between iron ore contracts and flat

steel prices. We forecast earnings of RMB786m in 2013, falling to

RMB630m in 2014, as we expect fewer one-off gains.

n Target price upgrade to HKD4.65 based on a 0.56x 2014E PB

Angang’s corporate structure has improved but the sector remains

under pressure, so we value the stock at a 0.56x PB (the historical

PB since 3Q11, when the sector entered a tight funding period).

Angang vs. Magang PB premium

Sources: Bloomberg; BNP Paribas

(10)

0

10

20

30

40

Se

p-1

1

Nov-1

1

Jan

-12

Mar-

12

May-1

2

Jul-1

2

Se

p-1

2

Nov-1

2

Jan

-13

Mar-

13

May-1

3

Jul-1

3

Se

p-1

3

Nov-1

3

Jan

-14

(x)

8 JANUARY 2014

CHANGE IN RECOMMENDATION 6CHINA / METALS & MINING

ANGANG STEEL 347 HK

REDUCE FROM HOLD

TARGET PRICE HKD4.65

CLOSE HKD5.30

UP/DOWNSIDE -12.4%

PRIOR TP HKD4.23

CHANGE IN TP +9.8%

HOW WE DIFFER FROM CONSENSUS MARKET RECS

TARGET PRICE (%) (13.9) POSITIVE 14

EPS 2013 (%) (9.8) NEUTRAL 12

EPS 2014 (%) (43.4) NEGATIVE 9

Rachel Cheung [email protected]

+852 2825 1824

KEY STOCK DATA

YE Dec (RMB m) 2012A 2013E 2014E 2015E

Revenue 77,748 75,233 73,748 70,591

Rec. net profit (4,157) 786 630 1,287

Recurring EPS (RMB) (0.57) 0.11 0.09 0.18

Prior rec. EPS (RMB) (0.57) 0.14 0.18 0.22

Chg. In EPS est. (%) 0.0 (20.3) (51.9) (20.7)

EPS growth (%) 92.2 (118.9) (19.8) 104.2

Recurring P/E (x) neg 38.1 47.5 23.2

Dividend yield (%) 0.0 0.0 1.1 2.2

EV/EBITDA (x) 29.3 7.8 7.0 5.9

Price/book (x) 0.6 0.6 0.6 0.6

Net debt/Equity (%) 68.2 58.1 50.0 41.4

ROE (%) (8.5) 1.7 1.3 2.7

Share price performance 1 Month 3 Month 12 Month

Absolute (%) (6.9) 10.4 (19.0)

Relative to country (%) (1.0) 12.0 (14.3)

Next results March 2014

Mkt cap (USD m) 4,945

3m avg daily turnover (USD m) 9.4

Free float (%) 33

Major shareholder Anshan Iron & Steel Gorup (67%)

12m high/low (HKD) 6.72/3.67

3m historic vol. (%) 37.8

ADR ticker -

ADR closing price (USD) -

Issued shares (m) 7,235

Sources: Bloomberg consensus; BNP Paribas estimates

(31)

(21)

(11)

(1)

9

19

3.28

4.28

5.28

6.28

7.28

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14

(%)(HKD) Angang Steel Rel to MSCI China

24

Angang Steel 347 HK Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Investment thesis

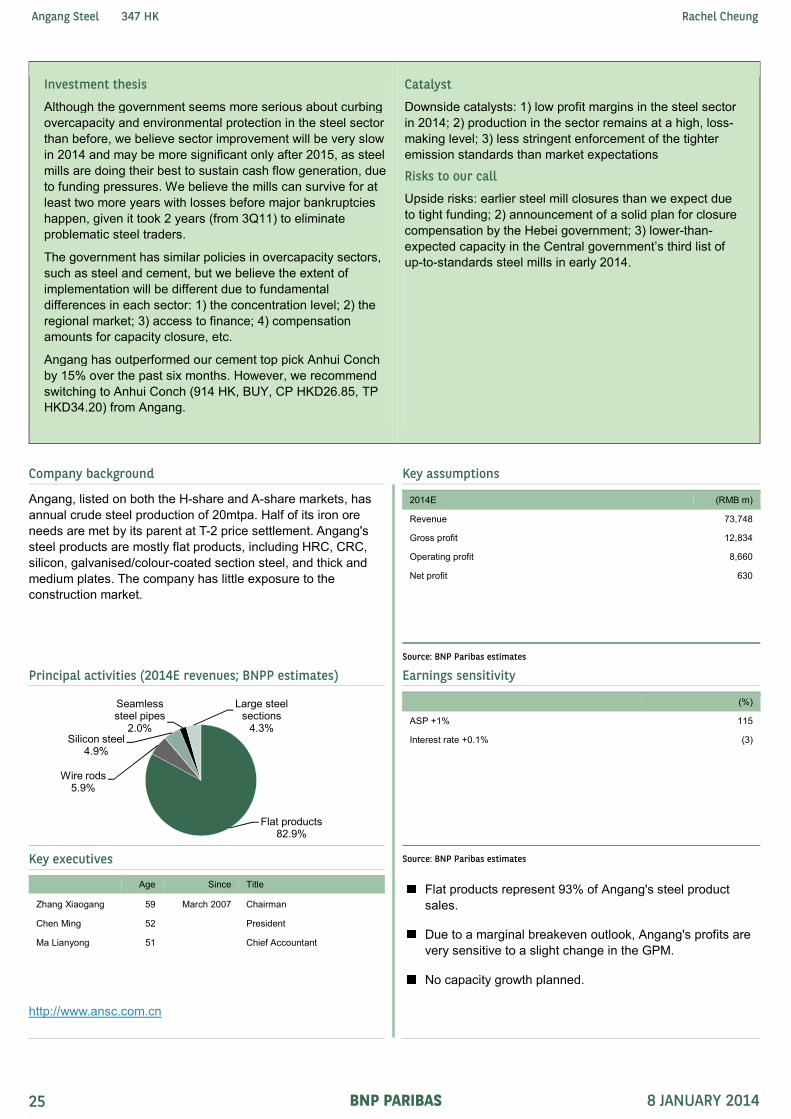

Although the government seems more serious about curbing

overcapacity and environmental protection in the steel sector

than before, we believe sector improvement will be very slow

in 2014 and may be more significant only after 2015, as steel

mills are doing their best to sustain cash flow generation, due

to funding pressures. We believe the mills can survive for at

least two more years with losses before major bankruptcies

happen, given it took 2 years (from 3Q11) to eliminate

problematic steel traders.

The government has similar policies in overcapacity sectors,

such as steel and cement, but we believe the extent of

implementation will be different due to fundamental

differences in each sector: 1) the concentration level; 2) the

regional market; 3) access to finance; 4) compensation

amounts for capacity closure, etc.

Angang has outperformed our cement top pick Anhui Conch

by 15% over the past six months. However, we recommend

switching to Anhui Conch (914 HK, BUY, CP HKD26.85, TP

HKD34.20) from Angang.

Catalyst

Downside catalysts: 1) low profit margins in the steel sector

in 2014; 2) production in the sector remains at a high, loss-

making level; 3) less stringent enforcement of the tighter

emission standards than market expectations

Risks to our call

Upside risks: earlier steel mill closures than we expect due

to tight funding; 2) announcement of a solid plan for closure

compensation by the Hebei government; 3) lower-than-

expected capacity in the Central government’s third list of

up-to-standards steel mills in early 2014.

Company background Key assumptions

Angang, listed on both the H-share and A-share markets, has

annual crude steel production of 20mtpa. Half of its iron ore

needs are met by its parent at T-2 price settlement. Angang's

steel products are mostly flat products, including HRC, CRC,

silicon, galvanised/colour-coated section steel, and thick and

medium plates. The company has little exposure to the

construction market.

2014E (RMB m)

Revenue 73,748

Gross profit 12,834

Operating profit 8,660

Net profit 630

Source: BNP Paribas estimates

Principal activities (2014E revenues; BNPP estimates) Earnings sensitivity

(%)

ASP +1% 115

Interest rate +0.1% (3)

Key executives Source: BNP Paribas estimates

Age Since Title

Zhang Xiaogang 59 March 2007 Chairman

Chen Ming 52 President

Ma Lianyong 51 Chief Accountant

http://www.ansc.com.cn

Flat products represent 93% of Angang's steel product

sales.

Due to a marginal breakeven outlook, Angang's profits are

very sensitive to a slight change in the GPM.

No capacity growth planned.

Flat products82.9%

Wire rods5.9%

Silicon steel4.9%

Seamless steel pipes

2.0%

Large steel sections

4.3%

25

Angang Steel 347 HK Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

EXHIBIT 1: Angang – changes to key assumptions (2014E)

2014E assumption change New Old Change

(RMB m) (RMB m) (%)

Revenue 73,748 71,469 3.2

COGS (excl depreciation) (60,913) (56,859) 7.1

Gross profit 12,834 14,610 (12.2)

SG&A (4,174) (4,135) 0.9

Operating EBITDA 8,660 10,475 (17.3)

Profit before tax 809 1,704 (52.5)

Minority tax (27) 8 -

Net profit 630 1,311 (51.9)

Source: BNP Paribas estimates

Valuation

EXHIBIT 2: Angang PB band

Sources: Bloomberg; BNP Paribas estimates

EXHIBIT 3: Target price calculation

Unit

BVPS 2014E RMB 6.64

Average P/B since September 2011 x 0.56

Target price in RMB RMB 3.72

Target price in HKD HKD 4.65

Source: BNP Paribas estimates

0.0

0.5

1.0

1.5

2.0

2.5

Feb-09 Aug-09 Feb-10 Aug-10 Feb-11 Aug-11 Feb-12 Aug-12 Feb-13 Aug-13

(x)

+1SD

Avg

-1SD

26

Angang Steel 347 HK Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Financial statements Angang Steel

Profit and Loss (RMB m) Year Ending Dec 2011A 2012A 2013E 2014E 2015E

Revenue 90,207 77,748 75,233 73,748 70,591

Cost of sales ex depreciation (82,549) (69,789) (61,256) (60,913) (56,905)

Gross profit ex depreciation 7,658 7,959 13,977 12,834 13,686

Other operating income 201 (1,625) 0 0 0

Operating costs (3,306) (4,545) (4,847) (4,174) (3,996)

Operating EBITDA 4,553 1,789 9,130 8,660 9,690

Depreciation (6,778) (5,841) (6,065) (6,290) (6,514)

Goodwill amortisation 0 0 0 0 0

Operating EBIT (2,225) (4,052) 3,065 2,370 3,176

Net financing costs (1,470) (1,846) (1,200) (1,161) (1,124)

Associates 391 402 (1,220) (400) (400)

Recurring non operating income 0 0 80 0 0

Non recurring items 0 0 0 0 0

Profit before tax (3,304) (5,496) 725 809 1,652

Tax 955 1,116 47 (151) (309)

Profit after tax (2,349) (4,380) 772 657 1,343

Minority interests 186 223 14 (27) (56)

Preferred dividends 0 0 0 0 0

Other items 0 0 0 0 0

Reported net profit (2,163) (4,157) 786 630 1,287

Non recurring items & goodwill (net) 0 0 0 0 0

Recurring net profit (2,163) (4,157) 786 630 1,287

Per share (RMB)

Recurring EPS * (0.30) (0.57) 0.11 0.09 0.18

Reported EPS (0.30) (0.57) 0.11 0.09 0.18

DPS 0.00 0.00 0.00 0.04 0.09

Growth

Revenue (%) (2.2) (13.8) (3.2) (2.0) (4.3)

Operating EBITDA (%) (58.3) (60.7) 410.4 (5.1) 11.9

Operating EBIT (%) (168.8) 82.1 (175.6) (22.7) 34.0

Recurring EPS (%) (205.3) 92.2 (118.9) (19.8) 104.2

Reported EPS (%) (205.3) 92.2 (118.9) (19.8) 104.2

Operating performance

Gross margin inc depreciation (%) 1.0 2.7 10.5 8.9 10.2

Operating EBITDA margin (%) 5.0 2.3 12.1 11.7 13.7

Operating EBIT margin (%) (2.5) (5.2) 4.1 3.2 4.5

Net margin (%) (2.4) (5.3) 1.0 0.9 1.8

Effective tax rate (%) - - (6.4) 18.7 18.7

Dividend payout on recurring profit (%) - - 0.0 50.0 50.0

Interest cover (x) (1.2) (2.0) 1.6 1.7 2.5

Inventory days 60.5 65.1 62.4 61.1 63.4

Debtor days 23.1 37.1 39.6 34.9 35.3

Creditor days 42.6 52.6 57.5 54.4 56.5

Operating ROIC (%) (2.0) (4.4) 4.9 3.1 4.3

ROIC (%) (1.5) (3.5) 2.6 2.1 3.1

ROE (%) (4.1) (8.5) 1.7 1.3 2.7

ROA (%) (1.2) (2.8) 2.1 1.6 2.3

*Pre exceptional, pre-goodwill and fully diluted

Revenue By Division (RMB m) 2011A 2012A 2013E 2014E 2015E

Flat products 72,397 63,153 60,235 59,824 57,238

Wire rods 4,393 3,960 4,252 4,222 4,025

Silicon Steel 5,729 3,451 3,583 3,556 3,393

Seamless steel pipes 1,780 1,157 1,444 1,410 1,345

Large steel sections 1,956 2,238 3,087 3,158 3,014

Others 3,951 3,789 1,577 1,577 1,577

Sources: Angang Steel; BNP Paribas estimates

27

Angang Steel 347 HK Rachel Cheung

BNP PARIBAS 8 JANUARY 2014

Financial statements Angang Steel

Cash Flow (RMB m) Year Ending Dec 2011A 2012A 2013E 2014E 2015E

Recurring net profit (2,163) (4,157) 786 630 1,287

Depreciation 6,778 5,841 6,065 6,290 6,514

Associates & minorities (577) (625) 1,206 427 456

Other non-cash items 50 (3,491) (3,491) (3,491) (3,491)

Recurring cash flow 4,088 (2,432) 4,566 3,857 4,766

Change in working capital 218 3,155 1,207 401 9

Capex - maintenance (5,495) (2,918) (3,600) (3,600) (3,600)

Capex - new investment 0 0 0 0 0

Free cash flow to equity (1,189) (2,195) 2,173 658 1,175

Net acquisitions & disposals 0 0 0 0 0

Dividends paid (1,085) 0 0 0 (315)

Non recurring cash flows (1,206) 1,486 2,237 3,016 2,987

Net cash flow (3,480) (709) 4,410 3,673 3,847

Equity finance 0 51 0 0 0

Debt finance 2,170 366 (3,652) 900 200

Movement in cash (1,310) (292) 758 4,573 4,047

Per share (RMB)

Recurring cash flow per share 0.57 (0.34) 0.63 0.53 0.66

FCF to equity per share (0.16) (0.30) 0.30 0.09 0.16

Balance Sheet (RMB m) Year Ending Dec 2011A 2012A 2013E 2014E 2015E

Working capital assets 28,001 24,940 21,749 21,319 20,407

Working capital liabilities (17,970) (18,064) (16,080) (16,051) (15,148)

Net working capital 10,031 6,876 5,669 5,268 5,259

Tangible fixed assets 69,655 60,993 58,528 55,838 52,923

Operating invested capital 79,686 67,869 64,196 61,105 58,182

Goodwill 0 0 0 0 0

Other intangible assets 3 6,677 6,677 6,677 6,677

Investments 2,125 2,740 2,788 2,836 2,884

Other assets 2,790 3,838 3,838 3,838 3,838

Invested capital 84,604 81,124 77,499 74,456 71,581

Cash & equivalents (2,341) (2,049) (2,807) (7,381) (11,428)

Short term debt 20,831 25,891 25,891 26,791 26,991

Long term debt * 13,821 9,053 5,401 5,401 5,401

Net debt 32,311 32,895 28,485 24,811 20,964

Deferred tax 0 0 0 0 0

Other liabilities 0 0 0 0 0

Total equity 50,739 46,598 47,384 48,014 48,986

Minority interests 1,554 1,631 1,631 1,631 1,631

Invested capital 84,604 81,124 77,499 74,456 71,581

* includes convertibles and preferred stock which is being treated as debt

Per share (RMB)

Book value per share 7.01 6.44 6.55 6.64 6.77

Tangible book value per share 7.01 5.52 5.63 5.71 5.85

Financial strength

Net debt/equity (%) 61.8 68.2 58.1 50.0 41.4

Net debt/total assets (%) 30.8 32.5 29.6 25.3 21.4

Current ratio (x) 0.8 0.6 0.6 0.7 0.8

CF interest cover (x) 0.2 (0.2) 2.8 1.6 2.0

Valuation 2011A 2012A 2013E 2014E 2015E

Recurring P/E (x) * neg neg 38.1 47.5 23.2

Recurring P/E @ target price (x) * neg neg 33.4 41.6 20.4

Reported P/E (x) neg neg 38.1 47.5 23.2

Dividend yield (%) 0.0 0.0 0.0 1.1 2.2

P/CF (x) 7.3 (12.3) 6.6 7.8 6.3

P/FCF (x) (25.2) (13.6) 13.8 45.5 25.5

Price/book (x) 0.6 0.6 0.6 0.6 0.6

Price/tangible book (x) 0.6 0.7 0.7 0.7 0.7

EV/EBITDA (x) ** 12.5 29.3 7.8 7.0 5.9

EV/EBITDA @ target price (x) ** 11.8 27.6 7.3 6.6 5.5

EV/invested capital (x) 0.8 0.8 0.8 0.8 0.7

* Pre exceptional, pre-goodwill and fully diluted ** EBITDA includes associate income and recurring non-operating income

Sources: Angang Steel; BNP Paribas estimates

28

Looks fairly valued at 0.5x PB

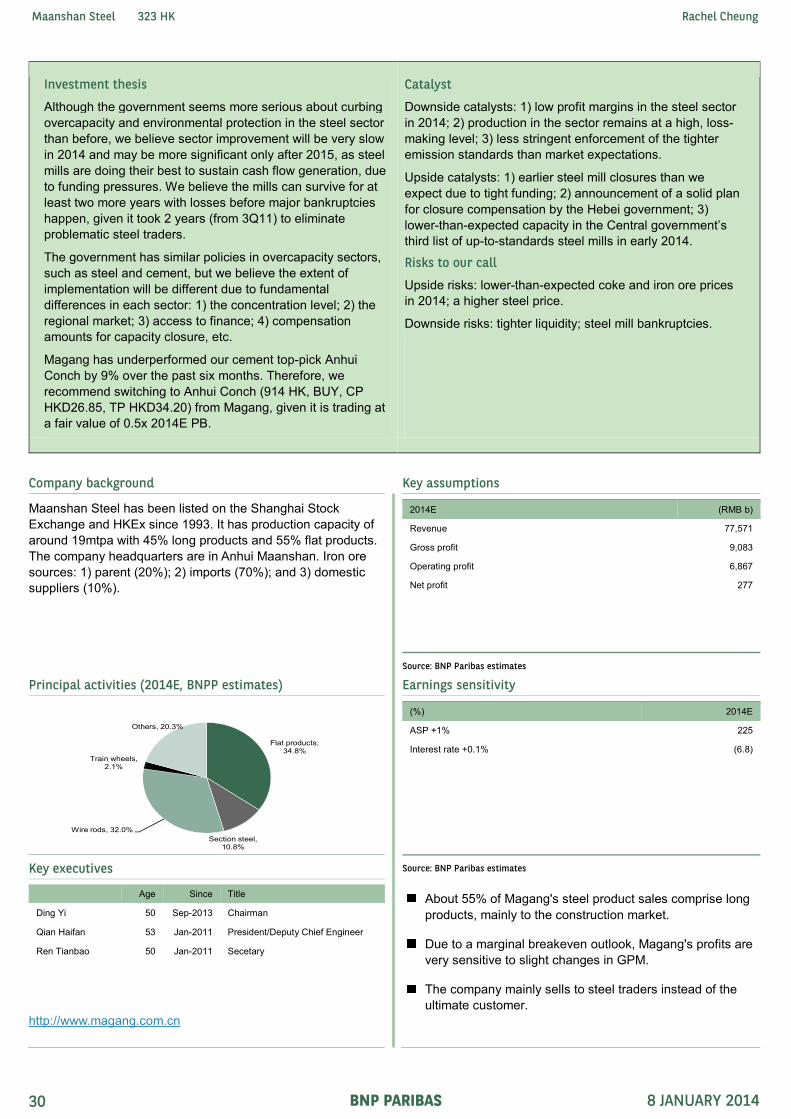

n Magang’s 2014E 0.5x PB seems fair We upgrade Magang from REDUCE to HOLD, purely based on its

fair valuation. Given the improved corporate structure after disposal

of non-steel assets to its parent in 2013, we value Magang at a 0.55x

PB (the historical PB since 3Q11, when the sector entered a tight

funding period) with a TP of HKD2.11 (HKD1.36 earlier).

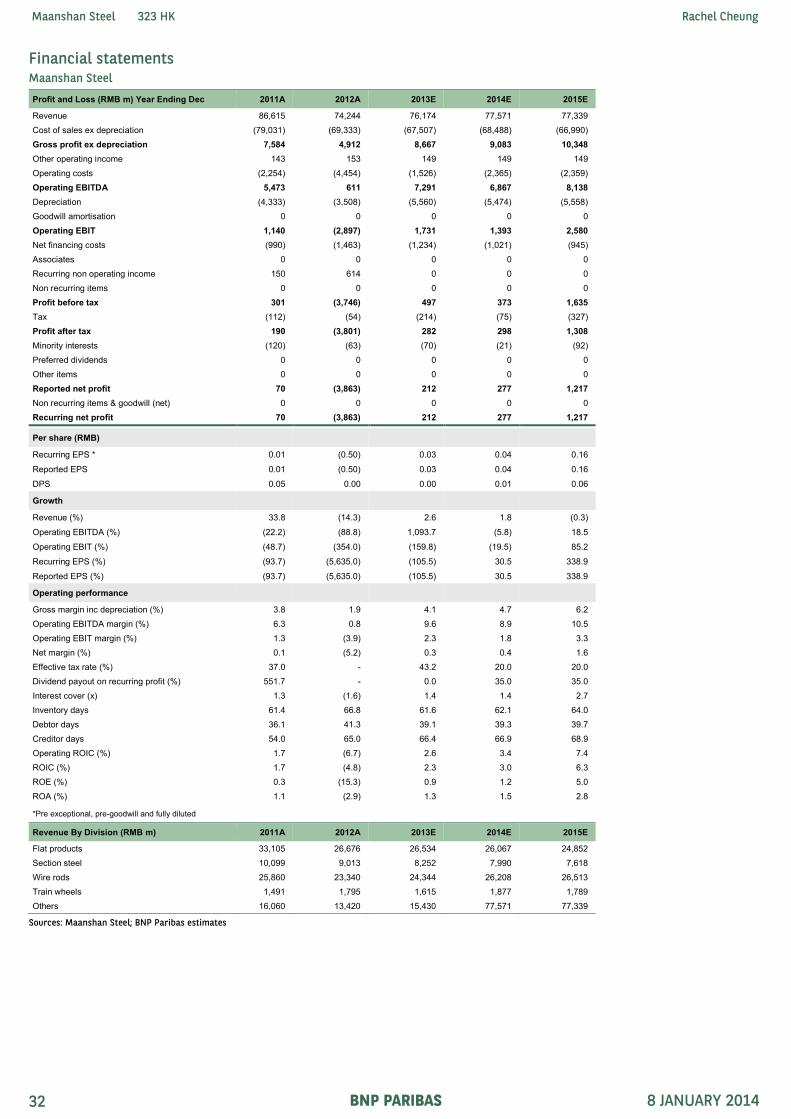

n Steel sector profits to be still under pressure in 2014 We believe China steel sector profitability will not rise much, given 1)

26.6mt capacity growth in non-Hebei provinces during 2014E, 2)

forcing the closure of Hebei steel mills is proving difficult due to lack

of funds for compensation; and 3) geared balance sheets are forcing

steel mills to sustain cash flows by continuing production. Also, there

is additional cost pressure from tighter emission control.

n 4Q13 profit thanks to the realisation of disposal gains Management indicates non-steel asset disposal gains realised in

4Q13 were RMB918m. Thus, we forecast earnings of RMB501m in

4Q13 and RMB212m in 2013E.

n Profits in 2014 despite no one-off gains We assume the iron ore price will decline 8.5% to USD125/t in 2014

and Magang’s ASP will fall just 0.5% with limited capacity growth.

Despite no one-off gains, we still estimate NP of RMB277m in 2014.

Angang vs. Magang PB premium – average since Sep-11: 8.5%

Sources: Bloomberg; BNP Paribas

(10)

0

10

20

30

40

Sep-11

Nov-11

Jan-12

Mar-12

May-12

Jul-12

Sep-12