transfer pricing updates and challenges in southern...

TRANSCRIPT

Transfer Pricing Updates and Challenges in Southern China Webinar on 9 October 2013

Presented by : Rhett Liu, PricewaterhouseCoopers, Transfer pricing partner Philip Hung, PricewaterhouseCoopers, Tax Director

Date: 9 October 2013

Disclaimer The materials of this seminar / workshop / conference are intended to provide general

information and guidance on the subject concerned. Examples and other materials in this seminar / workshop / conference are only for illustrative purposes and should not be relied upon for technical answers. The Hong Kong Institute of Certified Public Accountants (The Institute), the speaker(s) and the firm(s) that the speaker(s) is representing take no responsibility for any errors or omissions in, or for the loss incurred by individuals or companies due to the use of, the materials of this seminar / workshop / conference.

No claims, action or legal proceedings in connection with this seminar/workshop/conference brought by any individuals or companies having reference to the materials on this seminar / workshop / conference will be entertained by the Institute, the speaker(s) and the firm(s) that the speaker(s) is representing.

Today’s presenters

Philip Hung Director – Tax Investigation PwC Hong Kong +852 2289 3130 [email protected]

Rhett Liu Partner – Transfer Pricing PwC Hong Kong +852 2289 5619 [email protected]

Section 1

Latest Transfer Pricing Environment in China

TP development trends and focus in China - The SAT’s balanced approach on transfer pricing

Administration

Contemporaneous Transfer Pricing Documentation

Related-party transactions disclosure requirements

Valuation methods

Indirect tax implications

International collaboration

Additional tax liability of RMB 7.2 billion (equivalent to USD 1.1 billion) in 2010, and RMB 20.8 billion (equivalent to USD 3.3 billion) in 2011

Service

APA /BAPA

MAP / competent authority negotiation

Additional TP adjustment of RMB 796 million (equivalent to USD 126 million) in 2010, and RMB 700 million (equivalent to USD 111 million) in 2011

Investigation

Further improve the anti-tax avoidance monitoring system

• Joint audit

• Panel

• Total tax adjustment of

RMB 2.3 billion (equivalent to USD 365 million) in 2010, and RMB 2.4 billion (equivalent to USD 380 million) in 2011

Transfer Pricing Documentation Frequently demanded by tax authorities nowadays

Historical Situation Current Situation

Random selection of taxpayers and a longer time frame.

Tax authorities explicitly request TPD earlier across a larger sample of taxpayers. In some provinces, all taxpayers are selected.

TPD containing general factual details may be accepted in the past.

More disclosure and specific factual details are required in the TPD.

“Wait and See” approach to preparing TPD may have worked for some taxpayers.

Reactive strategy no longer viable. Taxpayers need to be proactive with TPD.

Moderate to high risk of queries from tax authorities .

High risk of queries from tax authorities.

Generalisations on technical aspects of TP analysis may be accepted in the past.

Higher quality of TPD required regarding technical TP analysis. Tax authorities note differences between local CPAs and Big 4.

TPD review process less systematic. Systematic TPD review using balanced scorecard approach.

Self adjustment

Guoshuifa [2012]No.13

Tax authority encourages taxpayer to make self adjustment to rectify TP problem in accordance with China regulation.

Trend

• Formal Audit: Substantial resource and time cost burden to the tax authority • Self adjustment: SAT and municipal level tax authority encourage lower level tax authority to be

more proactive in driving self adjustment scheme

Potentially unfavourable

factor

• Rigid standard: May only consider median value, without taking into account of the specific fact and circumstances of each case

• Local resources: Lower level tax authority may lack experience in dealing with TP dispute • Double taxation: A result of voluntary tax • Formal audit risk: cannot rule out the possibility that an audit will happen in future even

taxpayer had turn itself in making a self adjustment

Legal basis

Guoshuifa [2009]No. 2

Make adjustment to the median value of the benchmarked interquartile range

TP development trends and focus in China – APA

• China has concluded BAPAs with Japan, Korea, USA, Demark and Singapore and has BAPAs in the pipeline with Switzerland and other key regional jurisdictions.

• Now that the APA process is better established, taxpayers and SAT will probably continue to pursue more and more APA applications.

• However, due to the complexities and costs involved in the process change, it will not be too rapid but step-by-step.

• Continued increase in BAPAs while unilateral APAs will slow or even decline.

• PwC has assisted in most of the BAPAs that China has concluded as of 2010 and as of June 2012.

As of 2010 As of June 2012

Total # of BAPAs concluded by China 18 24-29

# of BAPAs assisted by

PwC 12-14 16-20

DTT 2-3 3-4

KPMG 2-3 3-4

EY 0 0

Other 0 1

Note: the total #of BAPAs as of 2010 is officially published; the # as of June 30, 2012 as well as the advisors are PwC estimates and not published. The number assisted by PwC is listed as a range to maintain propriety of the information.

Number of APAs Signed by Year

Year Unilateral APAs Bilateral APAs Multilateral APAs Total

2010 4 4 0 8

2011 8 4 0 12

2012 3 9 0 12

TP methods applied in APAs signed between 2005-2012

Comparable uncontrolled Price Method

Resale Price method

Cost Plus method

TNMM – Full Cost Mark-up

TNMM– Return on Capital Employed

TNMM – Return on Sales

TNMM – Berry Ratio

Profit Split method

Other

4 1 17 31 1 32 0 3 4

APA in China

• Concluded bilateral APAs with Japan, Korea, USA, Demark and Singapore and has bilateral APAs in the pipeline with Switzerland and other key regional jurisdictions.

• SAT may pursue APAs with additional trading partners or for diverse new types of transactions – shifting from manufacturing and buy-sell to intangible asset transfers and services.

• Latest issued APA Report on Aug 2013

Signed bilateral APAs by regions of counterparty *

* As of December 31, 2012 Source: China Advanced Pricing Arrangement Annual Report 2012

2005-2010 Number of APA signed* Case

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011 2012

Unilateral APA

Bilateral APA

69%

17%

14%

Asia

Euro

North

TP investigation trends in China The SAT plans to further improve the anti-tax avoidance monitoring system through:

Emphasis on the equal importance of administration, service and investigation, creating anti-avoidance prevention and control system

Expanding focus into:

Enterprises – extending to domestic enterprises , especially going-out enterprises

Industries – extending to financial services, trading, and other services industries

Transactions – extending to transfers of equities or intangibles and financial arrangements between related parties

Locations – extending to Central and Western China; and

Measures – extending to cost sharing agreements, controlled foreign companies, thin capitalization, and general anti-avoidance

Improving human resources and accumulating expertise

Promote the use of analytical methods and establish a panel of economic experts

Develop regional industry expertise

Increasing international activities

192

152

167

178

207

175

¥987

¥1240

¥2090 ¥2307

¥2400

¥4585

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012

TP Investigation in China (2007-2012)

Case closed

Total Adjustments (RMB million)

Section 2

Latest Transfer Pricing Environment in Hong Kong

Transfer pricing trends in Hong Kong

DIPN 48 (APA) issued on

29 March 2012

Treaty network continues to expand

IRD increasing

resources – staff and training

Increase in queries on intercompany

transactions

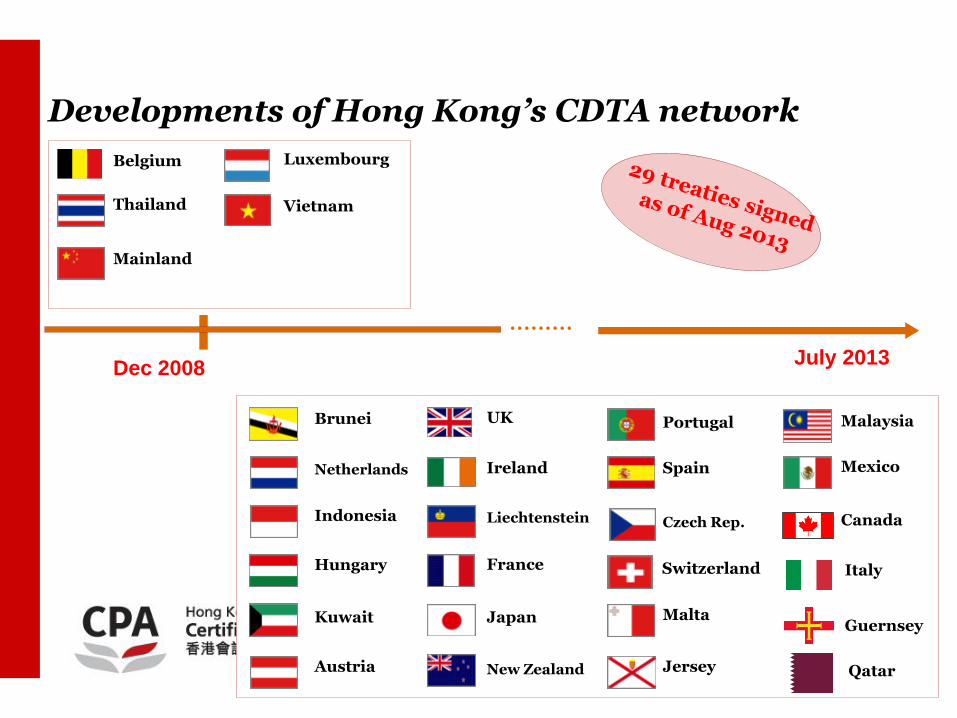

Developments of Hong Kong’s CDTA network

Dec 2008 July 2013

………

Belgium

Thailand

Mainland

Luxembourg

Vietnam

Brunei

Netherlands

Indonesia

Hungary

Kuwait

Austria

UK

Ireland

Liechtenstein

France

Japan

New Zealand

Switzerland

Portugal

Spain

Czech Rep.

Malta

Jersey

Malaysia

Mexico

Canada

Italy

Guernsey

Qatar

Statistics results of the field audit & investigations in Hong Kong

14

Results 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

No. of cases completed

1,873 1,875 1,864 1,862 1,803 1,805 1,804 1,802

Understated earnings and profits (HK$ million)

10,934.9 10,474.8 12,133.2 9,084.7 12,192.8 19,470.1 34,083.4 16,348.0

Average understatement per case (HK$ million)

5.8 5.6 6.5 4.9

6.8 10.8 18.9 9.1

Back tax and penalties assessed (HK$ million)

2,118.3 2,196.2 2,528.5 2,181.2 2,590.4 3,827.4 6,003.0 3,447.7

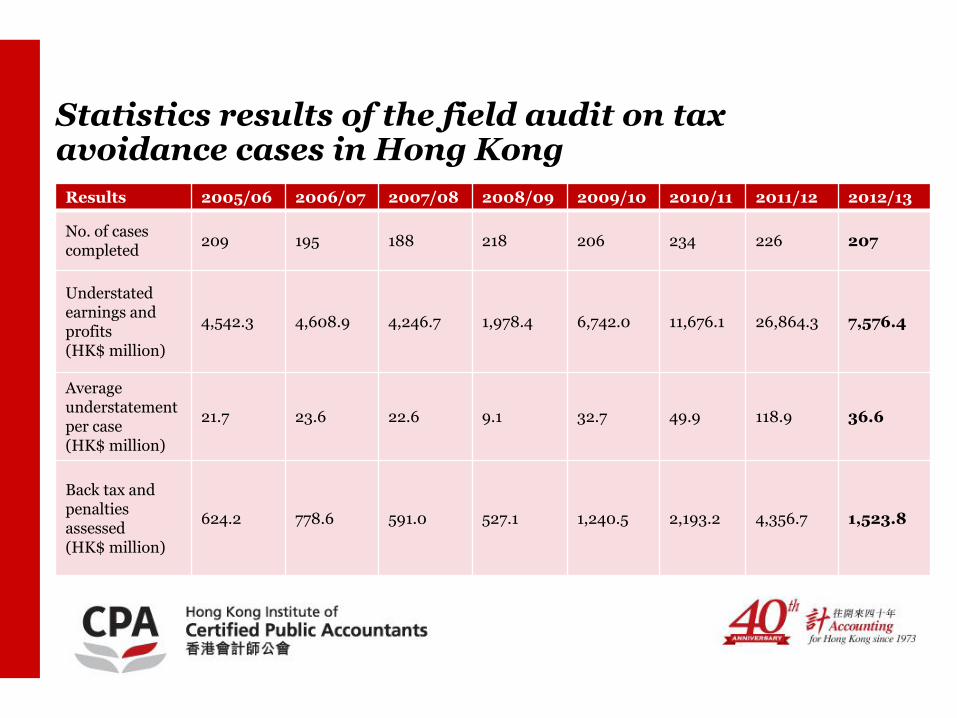

Statistics results of the field audit on tax avoidance cases in Hong Kong

Results 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

No. of cases completed

209 195 188 218 206 234 226 207

Understated earnings and profits (HK$ million)

4,542.3 4,608.9 4,246.7 1,978.4 6,742.0 11,676.1 26,864.3 7,576.4

Average understatement per case (HK$ million)

21.7 23.6 22.6 9.1 32.7 49.9 118.9 36.6

Back tax and penalties assessed (HK$ million)

624.2 778.6 591.0 527.1 1,240.5 2,193.2 4,356.7 1,523.8

Examples of situations that may be queried by IRD or overseas tax authorities

Pays royalties overseas but has A&P activity in HK or

“HK brand”

No intercompany agreements / No TP

documentation

Significant services fees or royalty fees

Procurement Hub in HK Retail and technology company (intangibles, BEPS, LSAs in China)

Group structures resulting in double non-taxation (i.e.

HK offshore)

Low tax jurisdictions / HK has profits but no clear

reason for HK entity or lack of substance for HK entity

Potential reference to China practice

• Loss • Profit fluctuation • Transaction with tax

haven company…

Tax Investigations and Field Audit in Hong Kong - Key TP Investigation focus

TP related issues are likely to be challenged by the IRD under the anti-avoidance provisions

Economic substance

Sound transfer pricing policy

Documentation evidence

TP could be regarded as a tool for tax avoidance or evasion instead of a bona fide business issue in the commercial world

Methodology as settlement basis

Contract processing case

Continuous loss for HK subsidiary of MNC

Hong Kong launched APA in April 2012

DIPN 45

Increased resources DIPN 48

April 2009

December 2009

2012 IRD

DIPN 46

June 2010

DIPN 47

Latest APA development in Hong Kong – Programme Highlights

On 29 March 2012,the Inland Revenue Department (“IRD”) took an important step forward by formalizing the Advance Pricing Arrangement (“APA”) programme in Hong Kong and issued Departmental Interpretation and Practice Notes Number 48 – Advance Pricing Arrangement (DIPN48).

APA is appropriate for:

Relatively large, complex or controversial related party transactions

Related party transactions in countries that frequently challenge transfer pricing

Requiring particularly high levels of certainty, for example business restructuring, IPO or M&A related situations.

Noteworthy aspects of guidance on the APA framework:

The APA programme is open to all resident and non-resident enterprises with a permanent establishment in Hong Kong that are subject to profits tax and have related party transactions pertinent to Hong Kong.

The APA will not agree precisely the actual profit but stipulate the methodology to determine the transfer pricing

Process: Pre-filing – Formal application – Analysis and evaluation – Negotiation and agreement – Drafting, execution and monitoring

Once concluded, the APA would be in effect for a period of generally 3 to 5 years

Latest APA development in Hong Kong - Programme Highlights (Continued)

Eligibility thresholds

HK$80m p.a. sale and purchase of goods transactions;

HK$40m p.a. services transactions; or

HK$20m p.a. intangible property transactions.

Collateral issues – material issues in addition to the intercompany transactions

Processing time – tentative timeframe for concluding APA is 18 months from acceptance of formal application

Voluntary disclosure – penalty reduction available if APA application submitted before audit or queries

Renewal – seek renewal at least six months before expiration of APA

Rollback – application of APA transfer pricing methodology to prior years at taxpayer’s request or initiated by IRD

Section 3

Hot Topic in China / Hong Kong Transfer pricing

Location specific advantages Why does it matter?

Tax authorities cite location specific advantages (“LSAs”) as a reason for China to retain the extraordinary high profits earned by entities with operations in China.

Manufacturing

Retail and Consumer Products

Location savings Market premium

Location factors allowing products to be produced faster, cheaper, better

Location factors allowing products to be sold for a higher price

Applies to all industries Particularly relevant to retail business and high value/luxury consumer goods

China

• Published in Oct 2012 in the United Nations’ Practical Manual on Transfer Pricing for Developing Countries (“UN TP Manual”)

• Presents SAT’s views and practices on TP issues in China as a developing country

• Issues not addressed in the OECD TP Guidelines:

- lack of reliable comparables,

- local specific advantages,

- alternative methods to traditional transactional or profits-based approaches to fit China’s unique economic and geographic factors.

OECD

• Location saving is a comparability factor

• No need to be paid for since it cannot be owned, controlled or transferred, but it may affect the arm’s length price for other transactions

• Use of local market comparables

• If no comparable, adopt the 4-step approach:

Whether location savings exist The amount of any location savings Whether they are passed on to

independent customers or suppliers How any net location savings not passed

on to customers and suppliers should be allocated

China vs OECD views - Tug of war between emerging and developed economies

A China case regarding market premium –Automotive OEM in Southern China

JV’s profit before royalty payment

Routine profit

Foreign partner’s non-routine profit

JV’s non-routine profit

The value of intangibles reflect JV’s non-routine profits

JV pays royalty to foreign investor

Routine profit

Foreign partner’s non-routine profit

1. Non-routine profit for intangibles owned by JV 2. LSA (e.g. location savings, market premium Consumer preference to foreign brands in general, barriers to entry, and others

A Hong Kong case regarding sourcing operation - Sourcing centre

Tax position

• Sourcing operation

• Continuous loss

HK group company

HK Ex-HK

Sale of goods

Commission $$$

(Sourcing of goods)

Agency agreement

Overseas group company

Suppliers / Manufacturers

Should a sourcing centre for the group substantiate loss?

IRD considered transfer pricing as a settlement basis

Q&A Session

Please drop questions into the question box.

Thank you!

The information contained in this presentation is of a general nature only. It is not meant to be comprehensive and does not constitute legal or tax advice. PricewaterhouseCoopers Ltd ("PwC") has no obligation to update the information as law and practice change. The application and impact of laws can vary widely based on the specific facts involved. No reader should act or refrain from acting on the basis of any material contained in this presentation without obtaining advice specific to their circumstances from their usual PwC client service team or their other advisers. The materials contained in this presentation were assembled in March 2012 and were based on the law enforceable and information available at that time. © 2013 PricewaterhouseCoopers Ltd. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Ltd which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

Please fill in the evaluation form.