tracking the patient engagement movement and its impact on clinical research execution ·...

TRANSCRIPT

Tracking the Patient Engagement Movement and its Impact on Clinical Research Execution

Ken Getz, MBA

Director, Sponsored Programs, Associate Professor

CSDD, Tufts University School of Medicine

Founder and Board Chair, CISCRP

MCC Summit

September 4, 2019

Agenda

• Anticipating a Movement

• Rationale

• Primary Execution Areas

– Key takeaways from selected TCSDD studies

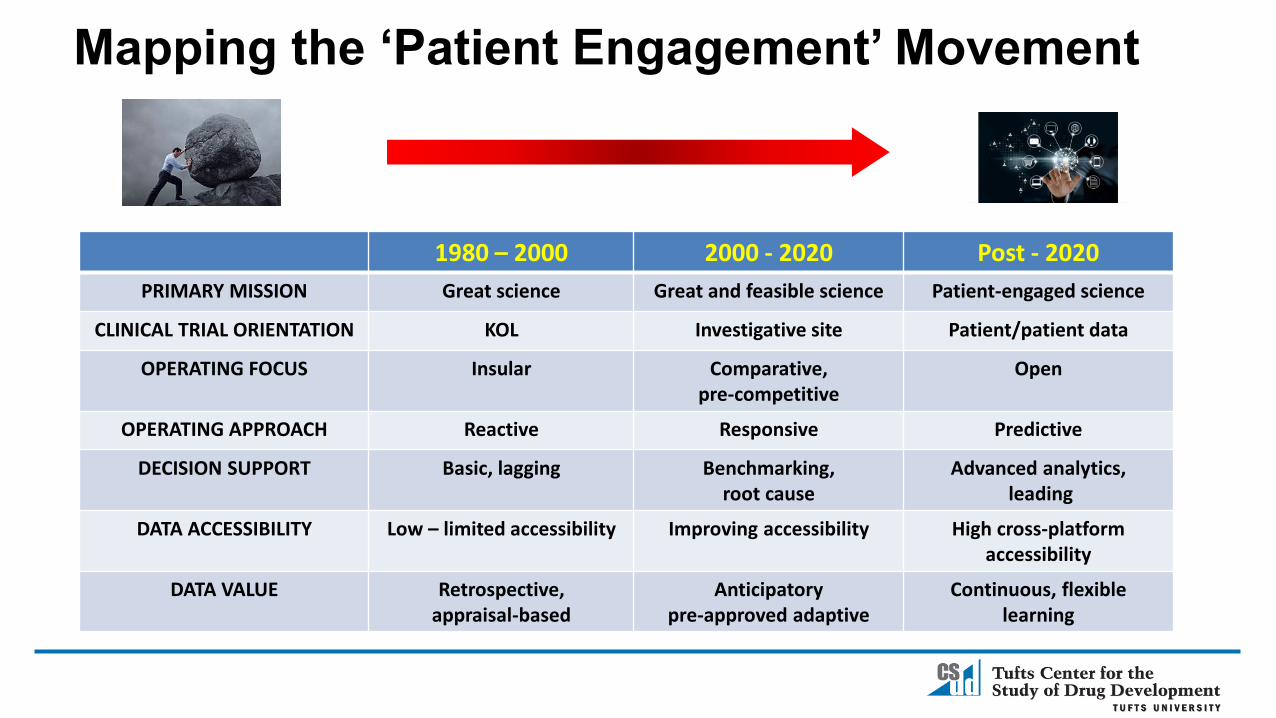

Mapping the ‘Patient Engagement’ Movement

1980 – 2000 2000 - 2020 Post - 2020

PRIMARY MISSION Great science Great and feasible science Patient-engaged science

CLINICAL TRIAL ORIENTATION KOL Investigative site Patient/patient data

OPERATING FOCUS Insular Comparative, pre-competitive

Open

OPERATING APPROACH Reactive Responsive Predictive

DECISION SUPPORT Basic, lagging Benchmarking, root cause

Advanced analytics,leading

DATA ACCESSIBILITY Low – limited accessibility Improving accessibility High cross-platform accessibility

DATA VALUE Retrospective,appraisal-based

Anticipatorypre-approved adaptive

Continuous, flexible learning

A Robust Innovation Engine

4,8855,482

6,4766,531

8,0108,617

9,34910,150

10,75211,166

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Number of New NDA and BLA Approvals

Source: Evaluatepharma; FDA

Total Active Drugs in Global R&D Pipeline

25

19

1115

31

18 18 1621 20

15

24

33

2530

33

15

34

42

2

5

6

6

5

2 4

2

3 6

6

6

6

2

11

12

7

12

17

2000 01 02 03 04 05 06 07 08 09 2010 11 12 13 14 15 16 17 18

NDAs BLAs

Growing Focus on Rare Diseases and Personalized Medicine

Percent of Active R&D

Pipeline

Percent of Total Approvals

2000 9% 11%

2005 11% 20%

2010 18% 29%

2015 24% 34%

2018 31% 58%

Source: Tufts CSDD

Rare Disease Pipeline Activity

Percent of Drugs in the Pipeline that Rely on Biomarker and

Genetic Data

Percentage of All Approved NMEs Classified as

Personalized Medicines

2013 23% 9%

2015 42% 21%

2017 51% 27%

An Overburdened Drug Development Process

• Intensifying protocol complexity

• Fragmented operating processes

• Siloed functions and relationships

• Point-based solutions

• Limited coordination & integration

• Outdated, reactive and tactical practices

• Underutilized assets

Industry Spending on Global R&D

$33.9

$54.6

$94.2

$127.4

$142.2

$159.6

1995 2000 2005 2010 2015 2020P

Source: EvaluatePharma; Tufts CSDD

$ US Billions

Global Spending on Pharma R&D

$1,044

$2,558

2003 2013

$US Millions (2013 dollars)

• 26% Direct Costs• 18% Time-Based• 56% Cost of Failure

Capitalized Cost to Develop a Single Successful Drug

Drug Development Cycle Time(Years from IND Filing to NDA Approval)

6.3 6.8 7.25.9 6.0 6.1 6.3 6.8 6.7 6.8

2.92.6 2

1.4 1.21.75 1.6

1.5 1.4 1.6

87-89 90-92 93-95 96-98 99-01 02-04 05-07 08-10 11-13 14-16

Mean Clinical Time Mean Approval Time

Source: Tufts CSDD

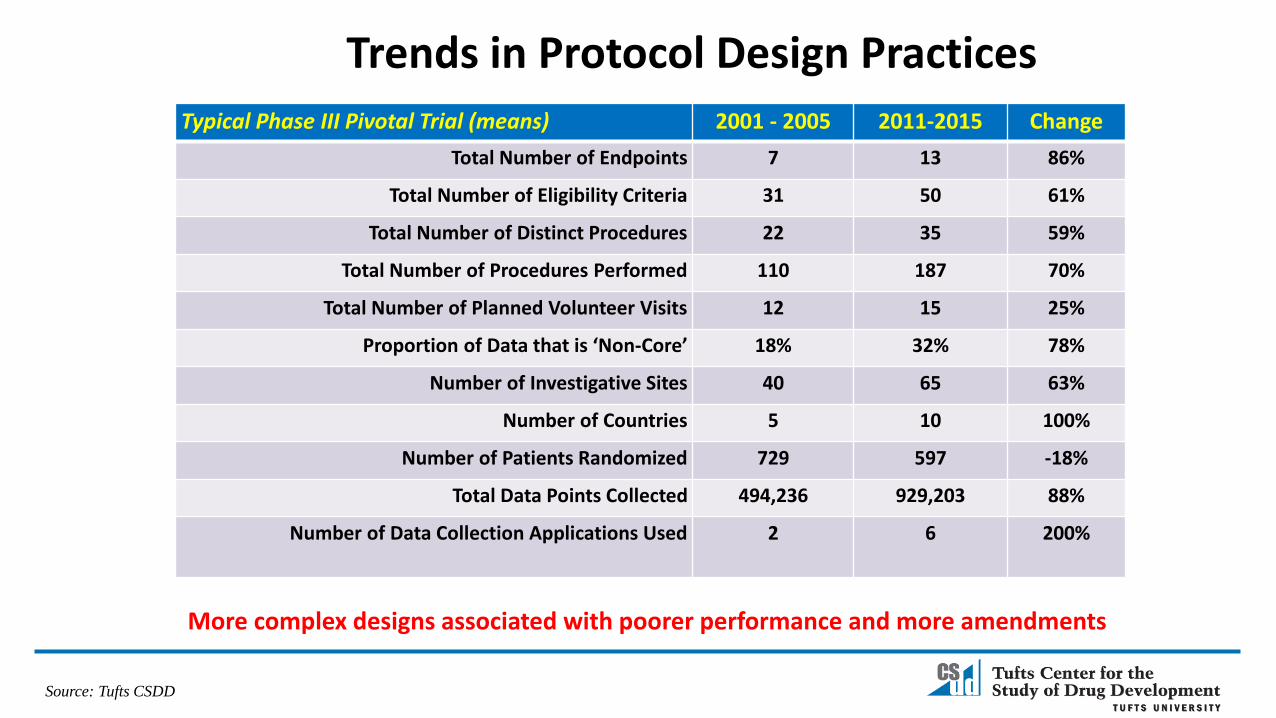

Trends in Protocol Design Practices

Typical Phase III Pivotal Trial (means) 2001 - 2005 2011-2015 Change

Total Number of Endpoints 7 13 86%

Total Number of Eligibility Criteria 31 50 61%

Total Number of Distinct Procedures 22 35 59%

Total Number of Procedures Performed 110 187 70%

Total Number of Planned Volunteer Visits 12 15 25%

Proportion of Data that is ‘Non-Core’ 18% 32% 78%

Number of Investigative Sites 40 65 63%

Number of Countries 5 10 100%

Number of Patients Randomized 729 597 -18%

Total Data Points Collected 494,236 929,203 88%

Number of Data Collection Applications Used 2 6 200%

Source: Tufts CSDD

More complex designs associated with poorer performance and more amendments

Recruitment and Retention Realities

Source: Tufts CSDD, 2015 & 2017

Doubling Planned Timelines

Fail to Enroll a Single

Patient11%

Under Enroll37%

Meet Enrollment

Targets39%

Well Exceed Enrollment

Targets13%

Site Activation and Achievement

Increase in Planned Study Duration to

Reach Target Enrollment

Overall 94%

Cardiovascular 99%

CNS 116%

Endocrine/Metabolic 113%

Oncology 71%

Respiratory 95%

Protocol Amendments

Source: Tufts CSDD, 2016

Percentage of Protocols with

at least one amendment

Mean number of amendments per

protocol

Increase in First Visit

Duration Days(FPFV to LPFV)

Increase in Study Treatment

Duration Days(FPFV to LPLV)

Top Reason for Amending

Direct Cost to

Implement

Phase I 52% 1.8 243 140 New and Modified Safety

Assessment(15.4% of Total)

$98k

Phase II 74% 2.2 197 109 Change in Eligibility Criteria

(17.2%)

$141k

Phase III 69% 2.3 221 239 Change in Eligibility Criteria

(15.2%)

$535k

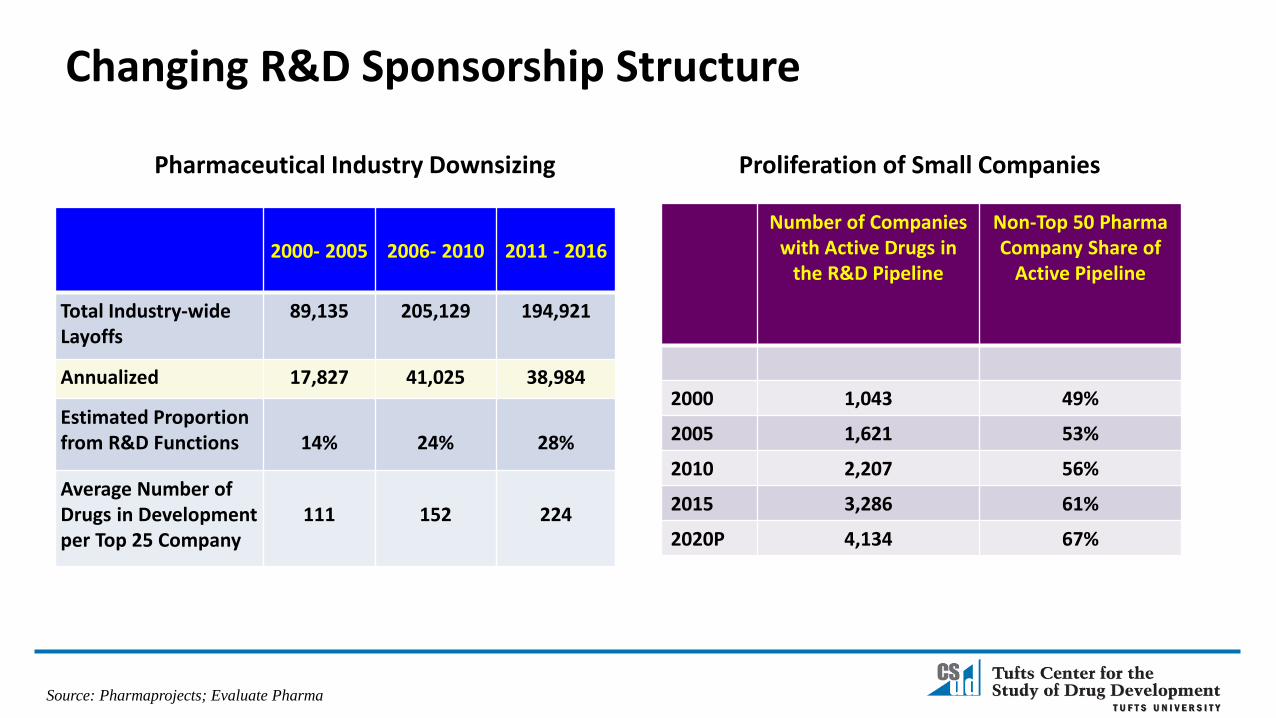

Changing R&D Sponsorship Structure

Source: Pharmaprojects; Evaluate Pharma

Number of Companies with Active Drugs in

the R&D Pipeline

Non-Top 50 Pharma Company Share of

Active Pipeline

2000 1,043 49%

2005 1,621 53%

2010 2,207 56%

2015 3,286 61%

2020P 4,134 67%

2000- 2005 2006- 2010 2011 - 2016

Total Industry-wide Layoffs

89,135 205,129 194,921

Annualized 17,827 41,025 38,984

Estimated Proportion from R&D Functions 14% 24% 28%

Average Number of Drugs in Development per Top 25 Company

111 152 224

Proliferation of Small CompaniesPharmaceutical Industry Downsizing

Distribution of Global R&D Spending(Estimated 3,800 Active Contract Service Providers)

$38.3$60.4 $71.6 $68.6 $65.7

$10.4

$24.3

$43.1 $59.7$78.6

$5.9

$9.5

$12.7$13.7

$15.3

2000 2005 2010 2015 2020P

Internal Staff and Infrastructure CRO Services Investigative Site Services

Source: EvaluatePharma; CenterWatch; William Blair & Wells Fargo Securities

$ US Billions

2008 2009 2010 2011 2012 2013 2014 2015

Multi-year filers First time filers

The Global Community of FDA-Regulated Investigators

Source: Tufts CSDD

33,920

24,805

29,670

27,60428,521 28,872

30,069

32,816

Average Annual Volume

Number of Unique

Investigators

Percent of Total

Proportion Based

OutsideNorth

America

TurnoverRate*

1 Clinical Trial 21,708 64% 53% 49%

2-3 CTs 8,480 25% 39% 20%

4-6 CTs 2,374 7% 20% 5%

7+ CTs 1,358 4% 7% 1%

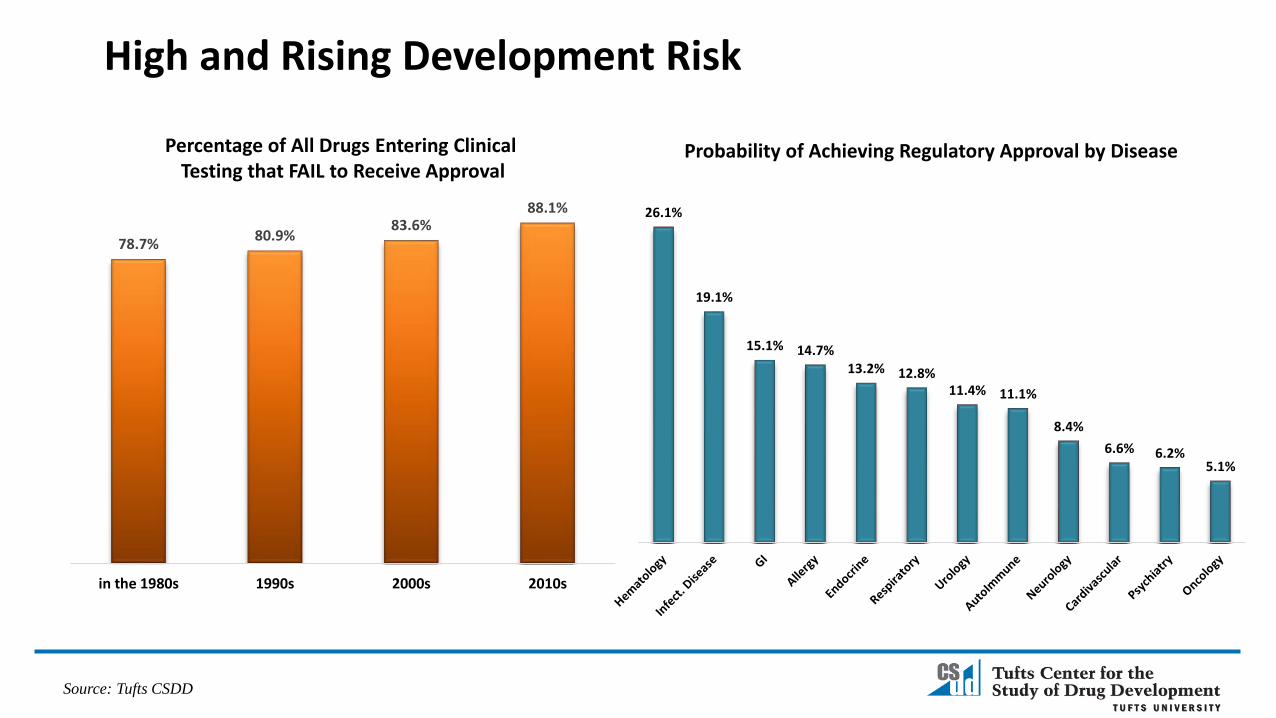

High and Rising Development Risk

Source: Tufts CSDD

Percentage of All Drugs Entering Clinical Testing that FAIL to Receive Approval

78.7%80.9%

83.6%88.1%

in the 1980s 1990s 2000s 2010s

26.1%

19.1%

15.1% 14.7%13.2% 12.8%

11.4% 11.1%

8.4%

6.6% 6.2%5.1%

Probability of Achieving Regulatory Approval by Disease

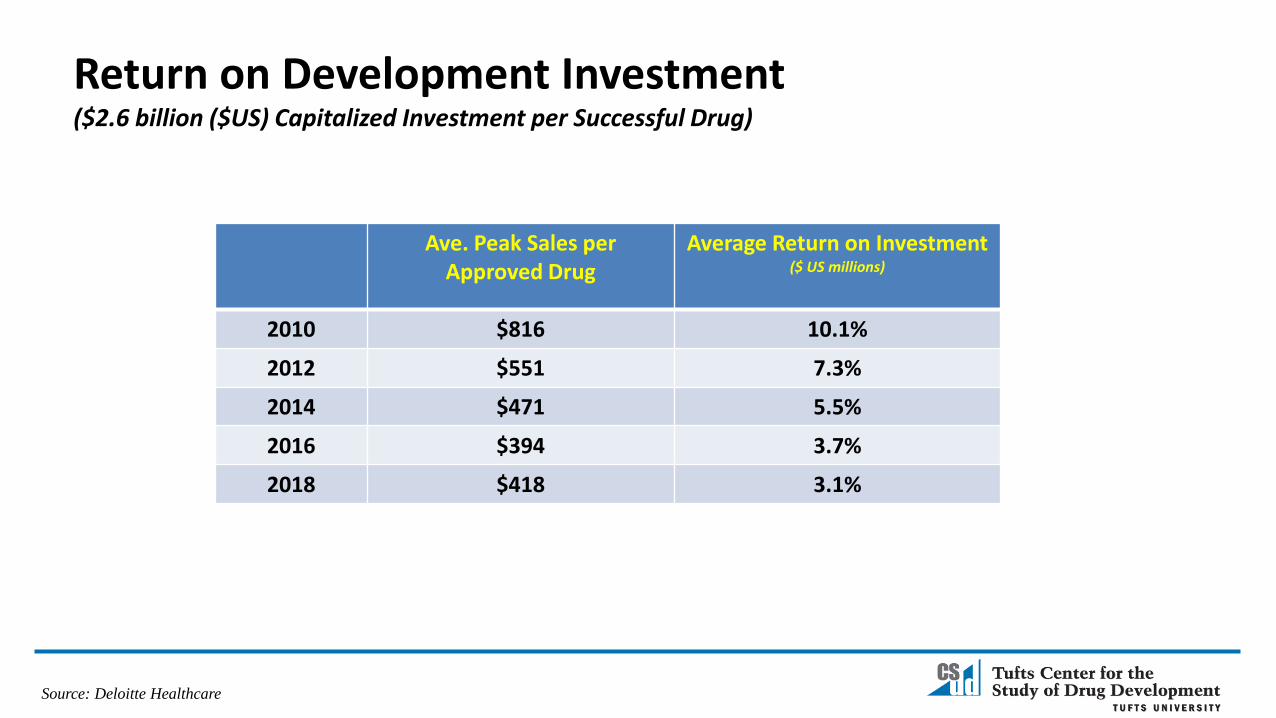

Return on Development Investment($2.6 billion ($US) Capitalized Investment per Successful Drug)

Ave. Peak Sales per Approved Drug

Average Return on Investment($ US millions)

2010 $816 10.1%

2012 $551 7.3%

2014 $471 5.5%

2016 $394 3.7%

2018 $418 3.1%

Source: Deloitte Healthcare

Source: Tufts CSDD;

A Closer Look at Rare Disease Drug Development

Average Direct Cost (Phase III)

IND Filing to FDA

Submission

FDA Submission to Approval

Rare Diseases

$103 MM (US)

131 months 10 months

All Indication

s

$193 MM (US)

78 months 14 months

81%

56%

14%

57%

36%

21%

Screen FailureRates

RandomizationFailure Rates

Drop Out Rates

Rare Diseases Non-Rare Diseases

Mapping the ‘Patient Engagement’ Movement

1980 – 2000 2000 - 2020 Post - 2020

PRIMARY MISSION Great science Great and feasible science Patient-engaged science

CLINICAL TRIAL ORIENTATION KOL Investigative site Patient/patient data

OPERATING FOCUS Insular Comparative, pre-competitive

Open

OPERATING APPROACH Reactive Responsive Predictive

DECISION SUPPORT Basic, lagging Benchmarking, root cause

Advanced analytics,leading

DATA ACCESSIBILITY Low – limited accessibility Improving accessibility High cross-platform accessibility

DATA VALUE Retrospective,appraisal-based

Anticipatorypre-approved adaptive

Continuous, flexible learning

Leveraging Data and Analytics

• Flexible, open, integrated models oriented around patients and patient data

• Can accommodate process customization

• Efficiency and cost reduction through more sophisticated use of data and analytics to optimize decision support and leverage global talent

Primary Execution Areas – Impacted by Patient Engagement

• Protocol design and feasibility

• Data management and coordination

• Site identification and study start-up

• New models and approaches to improve study volunteer experience and recruitment/retention performance

• Vendor management practices

20

Top Sponsor Engagement Objectives and Initiatives(Implemented/Piloted/Planned)

Source: Tufts CSDD, 2017 (N=38 sponsor and CRO companies)

77%

70%

47%

40%37%

34%

Patient AdvisoryBoards

ProfessionalAdvisory Panels

CT ResultsSummaries

Home NursingNetworks

WearableDevices

ConciergeServices

Percent of Companies Patient Centric Programs

Phase II – III enrollment timelines 40% Faster

Likelihood of reaching market launch 21% Higher

Percentage accepted by formularies (EU, US, Japan)

10 Point increase

Source: Levitan et al. TIRS 2018; 52(2): 220-229.

“With patient engagement, ENPV increases can exceed 500-fold the investment equivalent to accelerating a phase III product launch by 20-24 months.”

Source: The Economist Intelligence Unit, 2018

Current and Projected Sources of Clinical Research Data

Current Projected in 3 Years

Electronic and Paper Case Report Forms 100% 100%

Local and Central Labs 60% 65%

Smart Phones 45% 92%

Electronic Clinical Outcomes Assessments 21% 93%

Electronic Health and Medical Records 20% 67%

eSource 38% 84%

Mobile Health and Wearable Devices 29% 76%

Social Media 6% 27%

Source: Tufts Center for the Study of Drug Development, 2018; N=257 pharmaceutical, biotech and contract research companies

Use of Real World Data

Large Companies

Small/Mid-Sized

Companies

Have a centralized function 69% 58%

Ave. Number of FTEs 89 13

Ave. Number of contract FTEs 10 13

Expected FTE increase by 2020 35% 20%

29%

29%

38%

46%

50%

63%

75%

Better signal detection for riskmanagement

Assist site identification

Support portfolio managementdecisions

Faster completion of post-marketing requirements

Assist patient identification

Richer effectiveness data

Product positioning

Source: Tufts CSDD, 2017; N=57 pharmaceutical and biotechnology companies

Reported Primary Uses

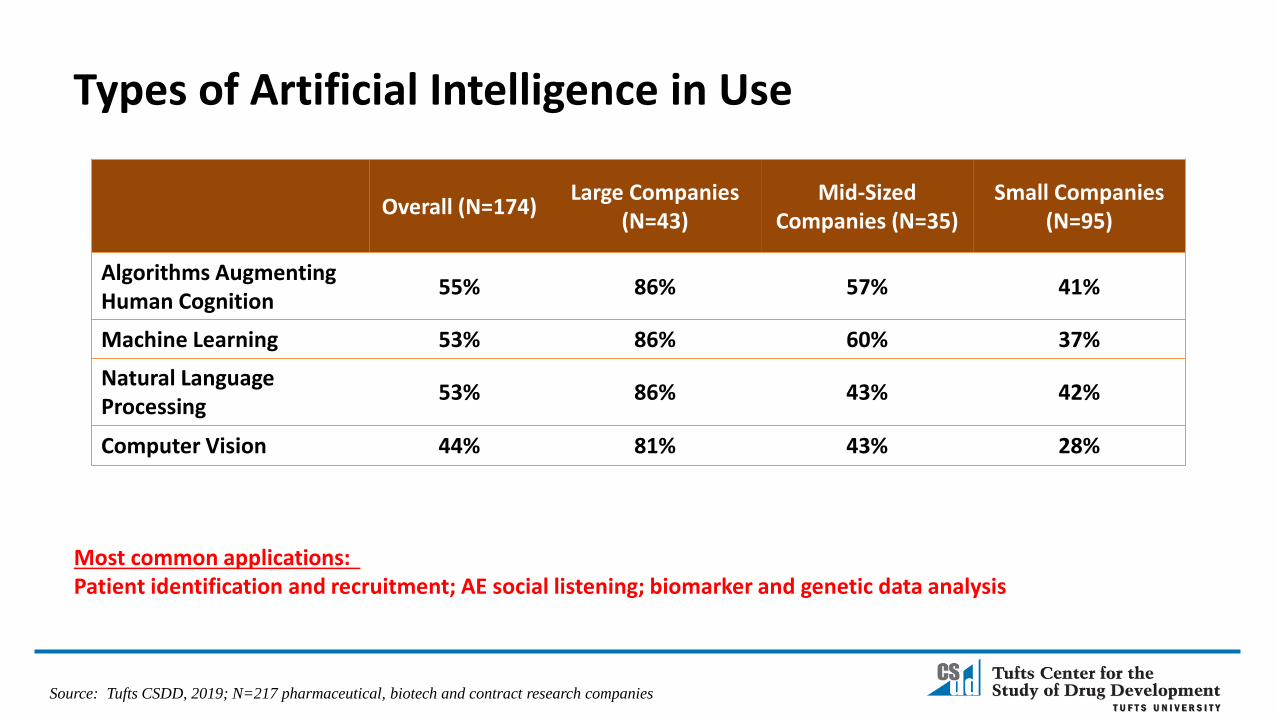

Types of Artificial Intelligence in Use

Overall (N=174)Large Companies

(N=43)Mid-Sized

Companies (N=35)Small Companies

(N=95)

Algorithms Augmenting Human Cognition

55% 86% 57% 41%

Machine Learning 53% 86% 60% 37%

Natural Language Processing

53% 86% 43% 42%

Computer Vision 44% 81% 43% 28%

Source: Tufts CSDD, 2019; N=217 pharmaceutical, biotech and contract research companies

Most common applications: Patient identification and recruitment; AE social listening; biomarker and genetic data analysis

Start-up and Data Management Cycle Times

Typical Phase III Pivotal Trial (means) 2001-2005 2011-2015

Study Start-Up

Total Cycle Time from Site Identification to FPI 25.6 weeks(CoV .63)

29.1 weeks(CoV .76)

Data Management

Time to Build Study Database 65.7 days(CoV .41)

68.3 days(CoV .48)

Time from Patient Visit to Data Entry 6.9 days(CoV .66)

8.1 days(CoV .89)

LPLV to Data Base Lock 33.4 days(CoV .75)

36.1 days(CoV .93)

Source: Tufts CSDD, 2018

111

139

266

245

263254

278269 274

2001 2003 2005 2007 2009 2011 2013 2015 2017

Complaints for Site Non-Compliance and Fraud

Source: FDA CDER Office of Compliance

Health Providers as Engagement Enablers

• 68% of patients rate their HCP as the top preferred source for information about clinical research

• 88% of patients feel it would be ‘very’ and ‘somewhat valuable’ for clinical research options to be presented during regular office visits

• 71% of patients say that they would speak with their physician or nurse prior to deciding to participate

• 83% of patients consider their physician’s recommendation a top factor influencing their decision to participate

• 91% of patients agree that having clinical study procedures conducted during regular doctor visits would be more convenient

• 93% of patients report feeling ‘Very’ and ‘Somewhat Comfortable’ having their medical health records routinely used to identify appropriate studies

Source: CISCRP 2017 Perceptions & Insights Study; N=12,427; ONC/AHA 2017

1.6% 3.6%

16.9%

34.4%43.4%

11.8%15.5%

39.1%

48.7%

52.1%

2008 2010 2012 2014 2016

Comprehensive Functionality

Basic Functionality

EHR Adoption

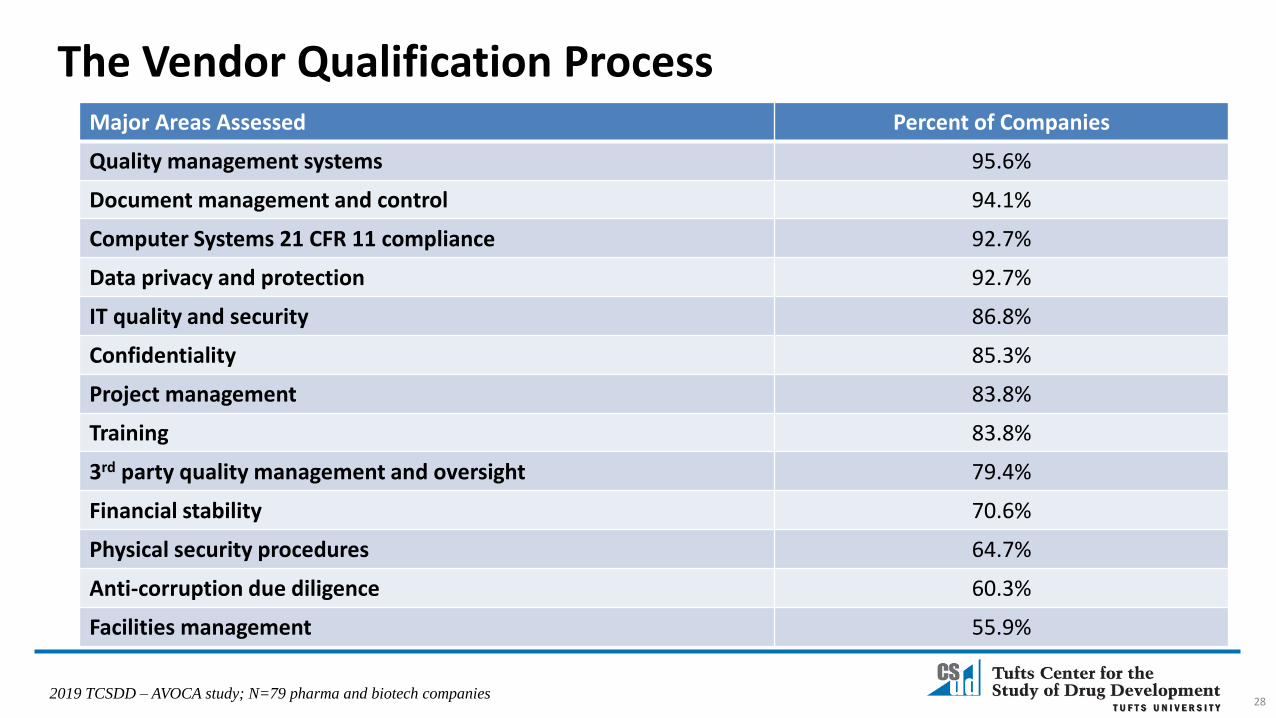

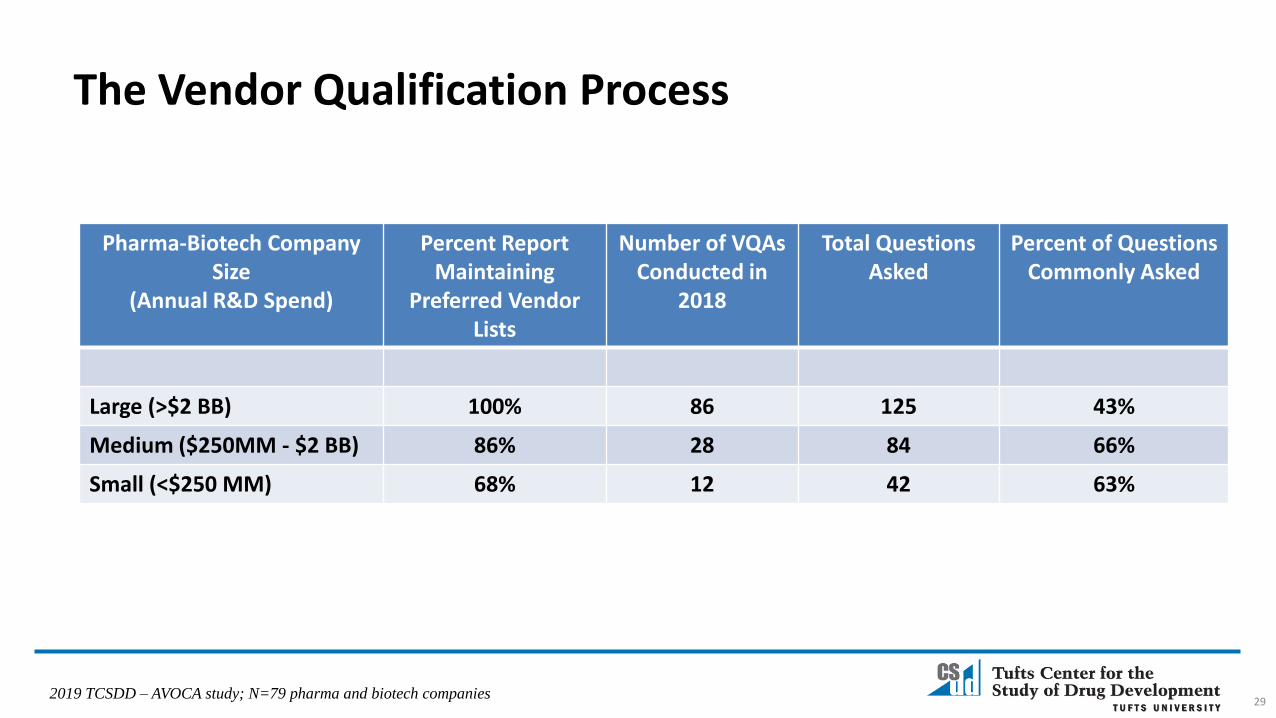

The Vendor Qualification Process

28

Major Areas Assessed Percent of Companies

Quality management systems 95.6%

Document management and control 94.1%

Computer Systems 21 CFR 11 compliance 92.7%

Data privacy and protection 92.7%

IT quality and security 86.8%

Confidentiality 85.3%

Project management 83.8%

Training 83.8%

3rd party quality management and oversight 79.4%

Financial stability 70.6%

Physical security procedures 64.7%

Anti-corruption due diligence 60.3%

Facilities management 55.9%

2019 TCSDD – AVOCA study; N=79 pharma and biotech companies

Pharma-Biotech Company Size

(Annual R&D Spend)

Percent Report Maintaining

Preferred Vendor Lists

Number of VQAs Conducted in

2018

Total QuestionsAsked

Percent of Questions Commonly Asked

Large (>$2 BB) 100% 86 125 43%

Medium ($250MM - $2 BB) 86% 28 84 66%

Small (<$250 MM) 68% 12 42 63%

29

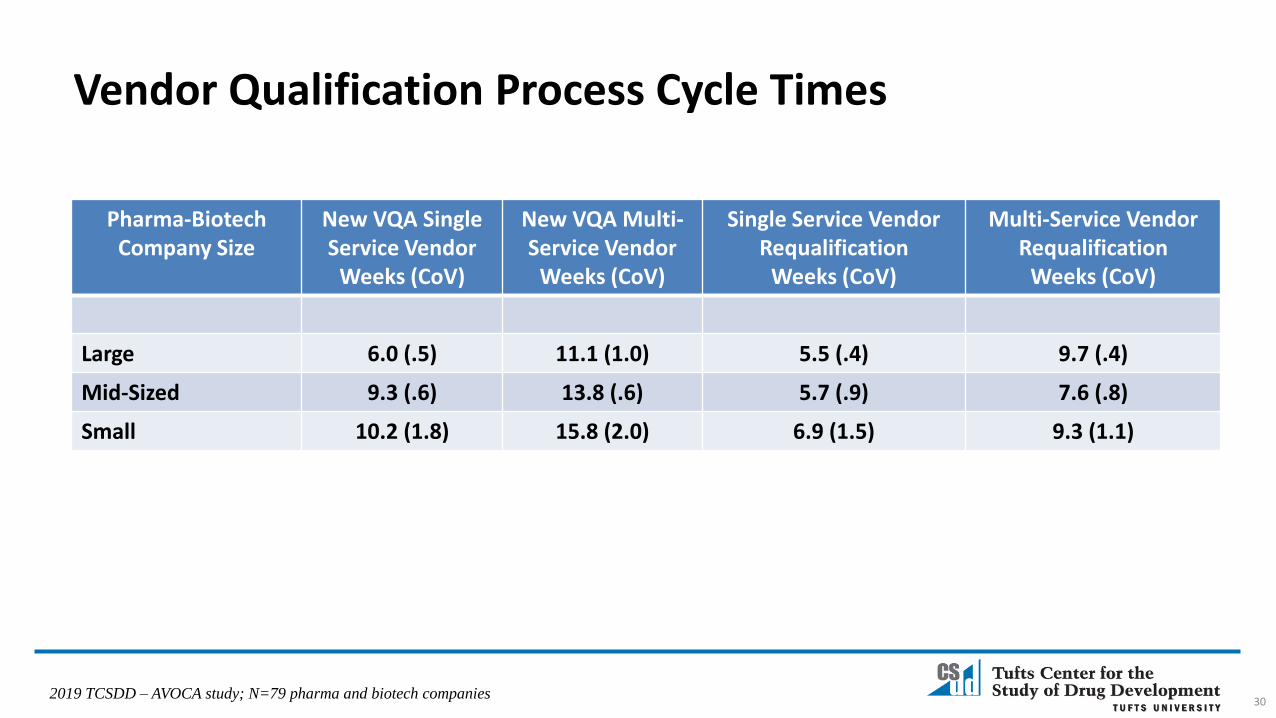

The Vendor Qualification Process

2019 TCSDD – AVOCA study; N=79 pharma and biotech companies

Pharma-Biotech Company Size

New VQA Single Service Vendor

Weeks (CoV)

New VQA Multi-Service Vendor

Weeks (CoV)

Single Service Vendor Requalification

Weeks (CoV)

Multi-Service VendorRequalification

Weeks (CoV)

Large 6.0 (.5) 11.1 (1.0) 5.5 (.4) 9.7 (.4)

Mid-Sized 9.3 (.6) 13.8 (.6) 5.7 (.9) 7.6 (.8)

Small 10.2 (1.8) 15.8 (2.0) 6.9 (1.5) 9.3 (1.1)

30

Vendor Qualification Process Cycle Times

2019 TCSDD – AVOCA study; N=79 pharma and biotech companies

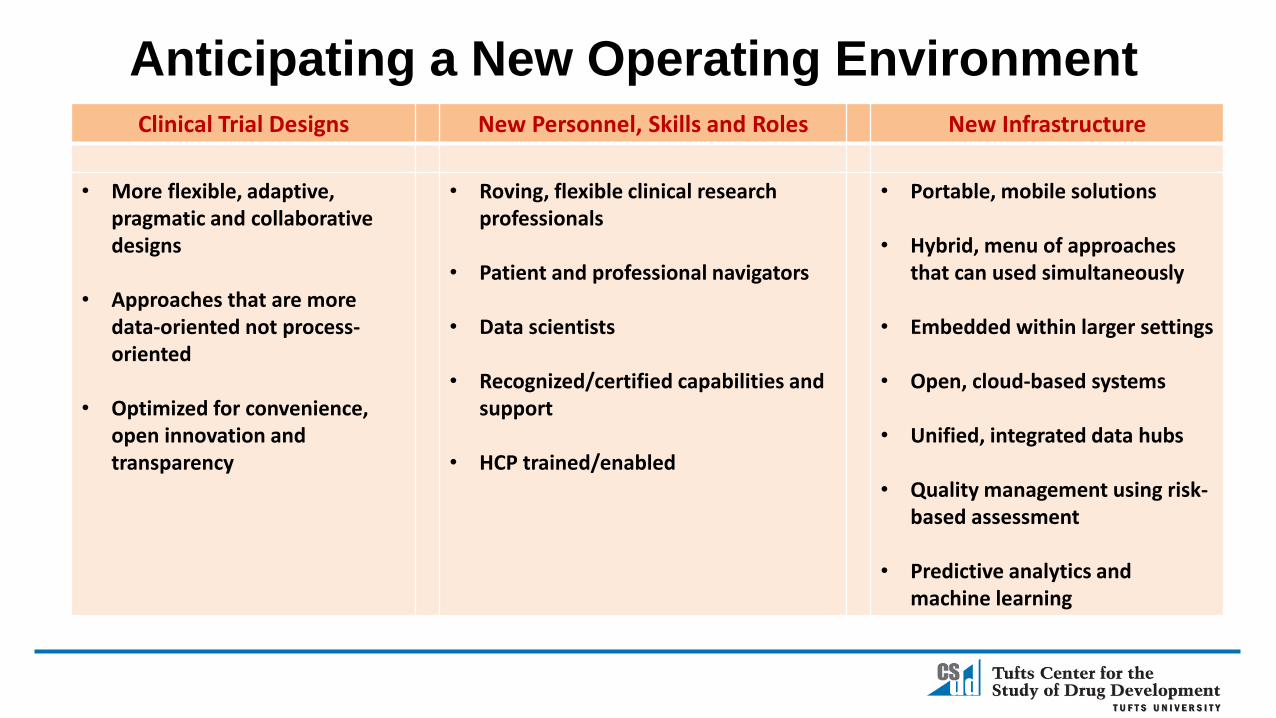

Clinical Trial Designs New Personnel, Skills and Roles New Infrastructure

• More flexible, adaptive, pragmatic and collaborative designs

• Approaches that are more data-oriented not process-oriented

• Optimized for convenience, open innovation and transparency

• Roving, flexible clinical research professionals

• Patient and professional navigators

• Data scientists

• Recognized/certified capabilities and support

• HCP trained/enabled

• Portable, mobile solutions

• Hybrid, menu of approaches that can used simultaneously

• Embedded within larger settings

• Open, cloud-based systems

• Unified, integrated data hubs

• Quality management using risk-based assessment

• Predictive analytics and machine learning

Anticipating a New Operating Environment

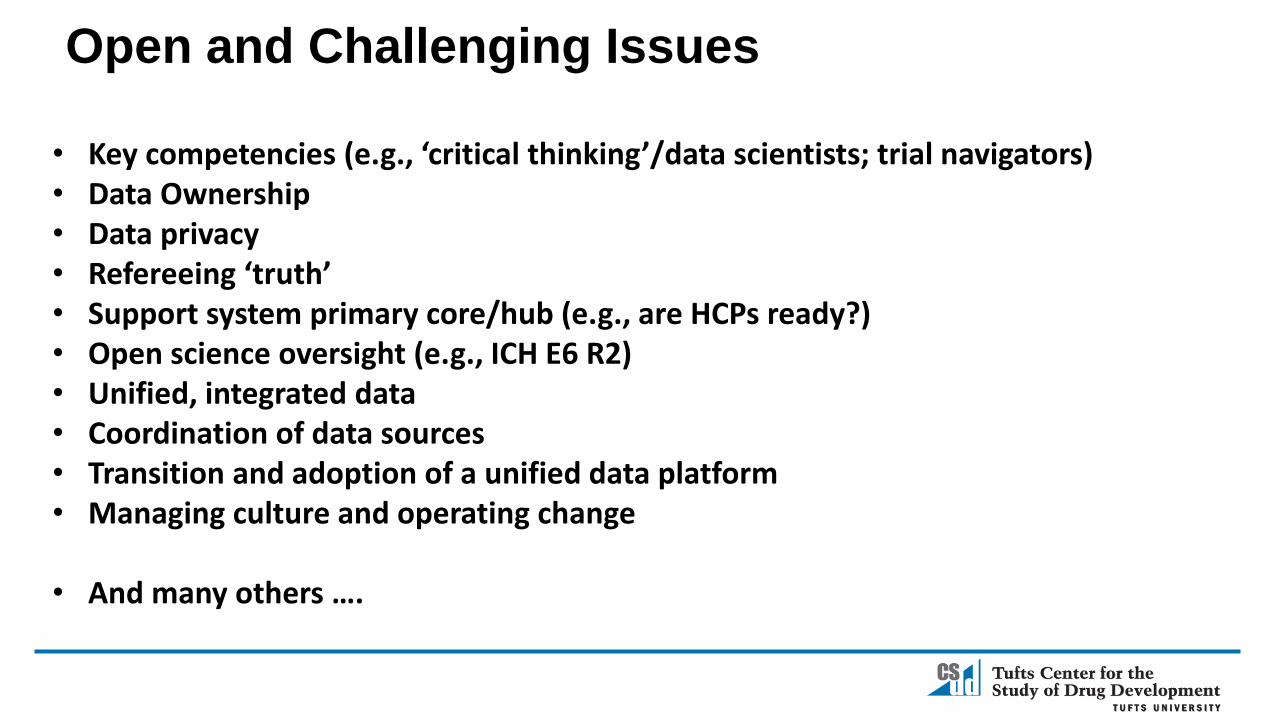

• Key competencies (e.g., ‘critical thinking’/data scientists; trial navigators)• Data Ownership• Data privacy• Refereeing ‘truth’• Support system primary core/hub (e.g., are HCPs ready?)• Open science oversight (e.g., ICH E6 R2)• Unified, integrated data• Coordination of data sources• Transition and adoption of a unified data platform• Managing culture and operating change

• And many others ….

Open and Challenging Issues

Ken Getz

Founder and Board Chair, CISCRP

Director, Sponsored Programs

Associate Professor

CSDD, Tufts University School of Medicine

617-636-3487, [email protected]