towers watson fossil fuels study

TRANSCRIPT

Fossil Fuels Exploring the stranded assets debate

Governments around the world agreed in 2010 to limit global warming to below 2°C relative to pre-industrial1 levels in order to prevent dangerous climate change. In order to achieve this, only a limited amount of carbon dioxide can be emitted globally until 2050. Some argue this means only one-fifth of proven fossil fuel reserves can be burnt, rendering those reserves left in the ground uneconomical to exploit, hence the term ‘stranded assets’. This disparity does not appear to be fully factored in by markets and thus current valuations of fossil fuel companies may be incorrect. Testing whether the market is fairly priced is never an exact science but the magnitude of this disparity would suggest the risk of mispricing of fossil fuel assets does exist.

In order to assess whether the stranded asset argument is real and/or material to an investor it is important to understand the macro factors that may influence possible future scenarios. Such factors include policy, science, technology and social momentum. An informed view of the interaction of these factors should allow investors to explore the distribution of risk in a balanced and holistic manner. In particular an understanding is required of the unfolding situation regarding the extent and manner in which carbon constraints will be applied. It follows to consider the impact of these constraints on the economics of the fossil fuel industry. We advocate assessing the potential impacts throughout the energy supply chain, and across a broad spectrum of asset classes.

Should we continue to invest in fossil fuels? Are fossil fuel related investments compatible with our long-term investment horizon? Will fossil fuels become economically stranded and as such are they mispriced?These are the questions we hear institutional investors asking. This paper aims to help investors begin to assess the issues and provides a framework for developing an appropriate response.

2 towerswatson.com

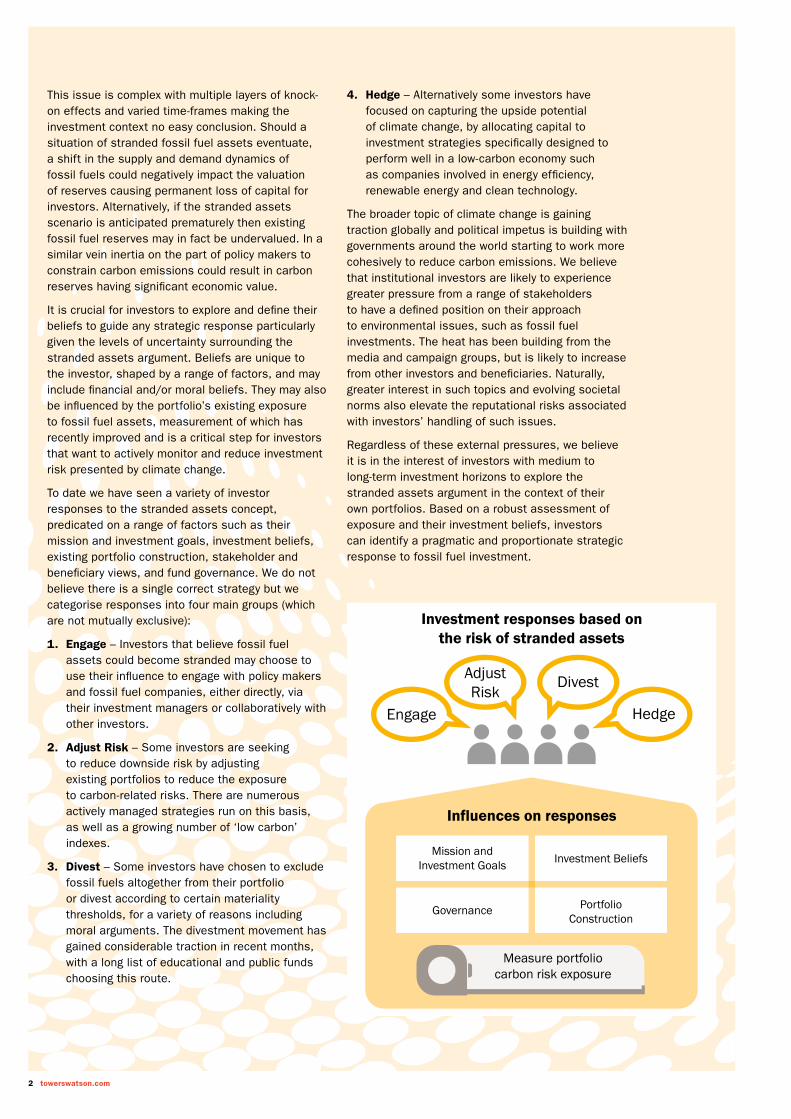

This issue is complex with multiple layers of knock-on effects and varied time-frames making the investment context no easy conclusion. Should a situation of stranded fossil fuel assets eventuate, a shift in the supply and demand dynamics of fossil fuels could negatively impact the valuation of reserves causing permanent loss of capital for investors. Alternatively, if the stranded assets scenario is anticipated prematurely then existing fossil fuel reserves may in fact be undervalued. In a similar vein inertia on the part of policy makers to constrain carbon emissions could result in carbon reserves having significant economic value.

It is crucial for investors to explore and define their beliefs to guide any strategic response particularly given the levels of uncertainty surrounding the stranded assets argument. Beliefs are unique to the investor, shaped by a range of factors, and may include financial and/or moral beliefs. They may also be influenced by the portfolio’s existing exposure to fossil fuel assets, measurement of which has recently improved and is a critical step for investors that want to actively monitor and reduce investment risk presented by climate change.

To date we have seen a variety of investor responses to the stranded assets concept, predicated on a range of factors such as their mission and investment goals, investment beliefs, existing portfolio construction, stakeholder and beneficiary views, and fund governance. We do not believe there is a single correct strategy but we categorise responses into four main groups (which are not mutually exclusive):

1. Engage – Investors that believe fossil fuel assets could become stranded may choose to use their influence to engage with policy makers and fossil fuel companies, either directly, via their investment managers or collaboratively with other investors.

2. Adjust Risk – Some investors are seeking to reduce downside risk by adjusting existing portfolios to reduce the exposure to carbon-related risks. There are numerous actively managed strategies run on this basis, as well as a growing number of ‘low carbon’ indexes.

3. Divest – Some investors have chosen to exclude fossil fuels altogether from their portfolio or divest according to certain materiality thresholds, for a variety of reasons including moral arguments. The divestment movement has gained considerable traction in recent months, with a long list of educational and public funds choosing this route.

4. Hedge – Alternatively some investors have focused on capturing the upside potential of climate change, by allocating capital to investment strategies specifically designed to perform well in a low-carbon economy such as companies involved in energy efficiency, renewable energy and clean technology.

The broader topic of climate change is gaining traction globally and political impetus is building with governments around the world starting to work more cohesively to reduce carbon emissions. We believe that institutional investors are likely to experience greater pressure from a range of stakeholders to have a defined position on their approach to environmental issues, such as fossil fuel investments. The heat has been building from the media and campaign groups, but is likely to increase from other investors and beneficiaries. Naturally, greater interest in such topics and evolving societal norms also elevate the reputational risks associated with investors’ handling of such issues.

Regardless of these external pressures, we believe it is in the interest of investors with medium to long-term investment horizons to explore the stranded assets argument in the context of their own portfolios. Based on a robust assessment of exposure and their investment beliefs, investors can identify a pragmatic and proportionate strategic response to fossil fuel investment.

Mission andInvestment Goals Investment Beliefs

PortfolioConstruction

Governance

HedgeEngage

DivestAdjust Risk

Investment responses based onthe risk of stranded assets

Influences on responses

Measure portfolio carbon risk exposure

Fossil Fuels – Exploring the stranded assets debate 3

Until relatively recently, the issue of climate change has largely been the domain of policy makers and civil society, with much attention focused on attempts to reach a globally binding treaty to reduce greenhouse gas emissions. However, stimulated by new research and fossil fuel divestment campaigns, the investment industry is now being challenged on the potential risks to long-term returns from fossil fuel investments, which some argue could, in part, become economically ‘stranded assets’. Indeed, in Towers Watson’s 2013 Secular Outlook report2 we noted that investors should acknowledge the potential financial impacts of climate change, including volatile, non-linear and unpredictable adjustments to fossil fuel asset valuations, and seek to position portfolios accordingly.

The UN Framework Convention on Climate Change reached agreement in 2010 that future global warming should be limited to below 2°C relative to pre-industrial levels1 in order to prevent dangerous anthropogenic interference with the climate system. To put this in perspective, the Earth warmed 0.85°C between 1880 and 2012, according to the Intergovernmental Panel on Climate Change (IPCC)3.

In order to keep below the 2°C target, only a limited amount of carbon dioxide can be emitted globally between 2000 and 2050; in effect, there is a fixed carbon budget. Research from a leading think-tank, the Carbon Tracker Initiative (CTI)4, concludes that only one-fifth of proven fossil fuel reserves can be burnt by 2050 to keep below the 2°C target. If a portion of proven reserves cannot be exploited they may become economically stranded as carbon emissions continue to be cut and the world transitions to a low-carbon economy. According to CTI, there are more fossil fuels listed on the world’s capital markets than we are able to burn if we are to prevent dangerous and irreversible climate change. This is the crux of the stranded assets argument; this disparity does not appear to be fully priced in by the markets and thus current valuations of fossil fuel related companies may be incorrect. Testing whether the market is priced fairly is never an exact science but the magnitude of this disparity would suggest the risk of mispricing of fossil fuel assets exists.

While natural gas and renewable energies will undoubtedly play a more significant role in meeting our future energy needs, we will still rely on coal and oil as overall energy demand continues to rise. According to the International Energy Agency (IEA), world primary energy demand will be 37% higher in 2040 than now. However, in the IEA’s central scenario, demand for coal and oil will plateau by 2040, at which point world energy supply will be divided into four almost equal parts: low-carbon sources (nuclear and renewables), oil, natural gas and coal5.

In parallel to the stranded assets debate, a fossil fuel divestment campaign built on environmental concerns has resulted in numerous educational and public funds selling fossil fuel assets. The confluence of the stranded assets debate and the divestment movement has stimulated growing curiosity within the investment community about the potential risks associated with fossil fuel investments, and in particular the risk that they may be mispriced in light of the stranded assets argument.

The intention of this paper is not to prove or disprove the stranded assets argument; rather we consider the potential investment implications and suggest a framework to help institutional investors explore, and potentially respond to, questions around investments in fossil fuels.

Introduction Total carbon emmissions if current reserves of

fossil fuels are burned

UN carbon budget 2000 – 2050

Carbon already emitted between 2000 and 2011

4 towerswatson.com

Institutional investors may question whether the risk of stranded assets is real and/or material to their portfolio, and if so when and how that risk will manifest. To explore this question it can be useful to consider the various factors which might influence future scenarios. An informed view of the macro drivers should allow investors to assess the distribution of risk in a balanced and holistic manner. In particular, an assessment needs to be made regarding the extent to which carbon constraints will be applied, and the impact of these constraints on the economics of the fossil fuels industry. Below, we show some illustrative (not exhaustive) influencing factors and possible future scenarios, as a representation of various views across the industry.

Investment Relevance

• Regulations restricting greenhouse gas emissions• Policy to support renewable energy industry

Policy and regulation

• Disruptive technological advances in energy efficiency or renewables• Quality of responses from fossil fuel companies – for example, advances in carbon capture

Technology

• Further scientific evidence or extreme weather shifts prompting more immediate reaction from policy makers, consumers and/or investors

Science

• Fossil fuel divestment campaigns• Changes in human behaviours and demands on their governments • Politics of higher energy costs

Social momentum

Influencing Factors

Potential scenarios

A shift in the supply and demand dynamics of fossil fuels could render those assets uneconomical and impact the valuation of reserves. This could cause a permanent loss of capital for investors.

Stranded fossil fuel assets

Above scenario may take longer to be realised or may be mitigated by technological advances in carbon capture. This could mean that reserves are in fact under valued.

Premature anticipation of a stranded asset scenario

Inertia on the part of policy makers to curtail carbon emissions could result in carbon reserves having significant economic value.

No co-ordinated carbon constraints

Fossil fuel divestment campaigns could stigmatise fossil fuel companies and failure by certain industries or companies to respond effectively could be detrimental to corporate reputation and undermine their social licence to operate.

Licence to operate undermined

Fossil Fuels – Exploring the stranded assets debate 5

Investment Relevance

EquityPublic Equity: The intrinsic value of an equity asset is determined by the net present value of future cash flows and as a general rule ongoing uncertainty over those future cash flows can result in lower net present values.

In the case of fossil fuel stocks in a lower emission scenario investors should consider the implications of lower demand and prices for fossil fuels. Reserves, capital expenditure plans and production costs are key inputs in forecasting cash flows. The potential scenarios highlighted previously could affect the operating cash flows of resource companies. The key is to assess how, when and to what extent cash flows are likely to be affected and whether management has the ability to respond to these factors to protect shareholder value.

As an example, a coal company may be able to adapt to a certain level of government intervention in the form of a carbon tax. A combination of cost reductions, an increase in volumes and passing a portion of the cost on to consumers may allow a coal company to offset the additional cost from taxes. Thus analysts might only expect a short-term adjustment in earnings for that company. However a series of government interventions that were considered severely restrictive to a coal company might have more far reaching effects including:

1. The ability of the company to offset those increased costs may be limited resulting in reduced earnings, and

2. The reduced cash flow and profitability of the company might impact the ability of the company to attract equity or debt financing.

In turn the cost of capital applied to the company by the market may rise which would lead to a reduced net present value of future cash flows and could permanently depress the valuation of the stock.

There is a view that a stranded assets situation would not necessarily be a bad outcome in the medium term for investments in certain fossil fuel companies: a company which is not ploughing returns back into new capital expenditure projects, as they continuously move up the production cost curve, will be free to distribute returns back to shareholders in the form of dividends. While the longevity of the company’s mining activities may be curtailed, the return to shareholders while those viable reserve assets are run down may be attractive. Such was the basis for a resolution put forward by shareholders at a recent Exxon AGM6. Thus, understanding expected future cash flows and the associated timing is important in this analysis.

Industry analysis is also important. As another example, understanding the players in the resource industry is relevant in assessing supply scenarios as national resource companies may respond quite differently to listed companies. The former has arguably a wider stakeholder group and consequently different motivations for continuing operations.

Many corporates already provide carbon footprint reports both voluntarily and under various regional regulations. Some companies employ internal carbon pricing metrics when pricing new projects even though there may not be an explicit price on carbon emissions in the region of operation. Engagement with companies by institutional investors to understand how management anticipates industry changes should leave the investor better informed of the potential risks faced.

Current divestment by institutional investors from fossil fuels is unlikely to have a material impact on overall equity valuations because the size of the outflows is not significant relative to the market capitalisation of the industry. Coal companies are most likely to suffer the direct effects from the divestment campaign but pure coal companies represent a small fraction of the market capitalisation of fossil fuel

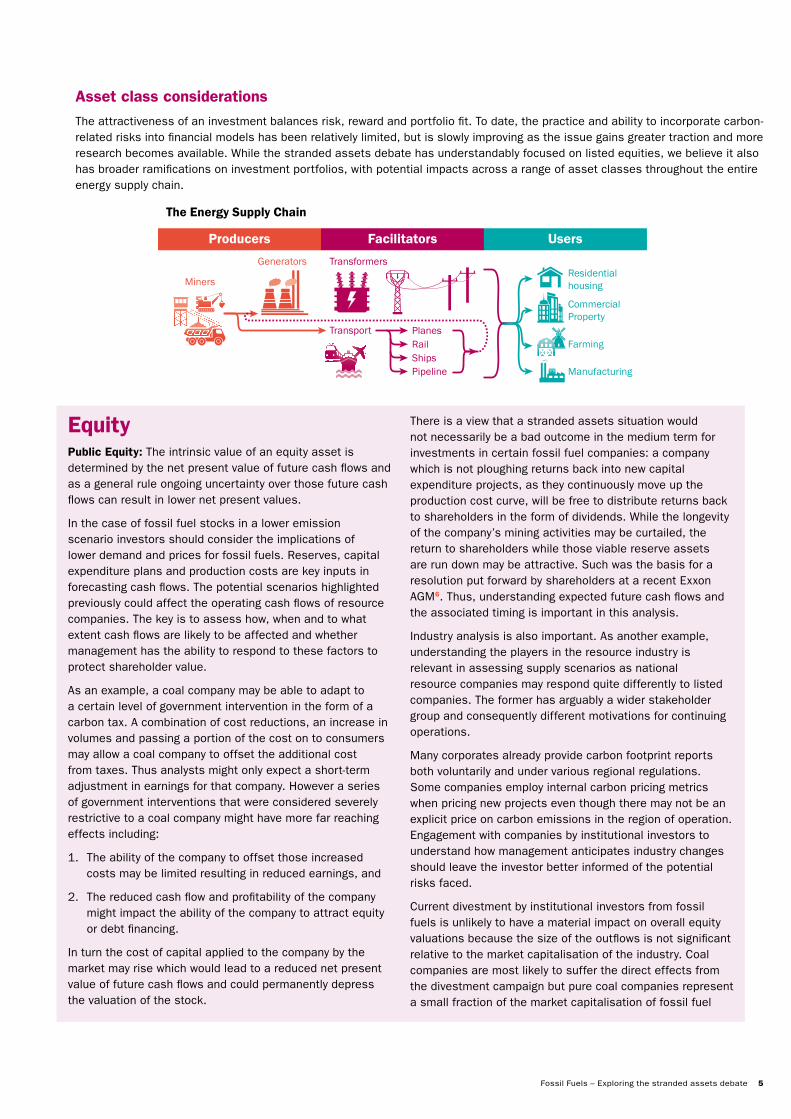

The Energy Supply Chain

UsersFacilitatorsProducers

Manufacturing

Farming

Commercial Property

Residential housing

PipelineShipsRailPlanesTransport

TransformersGenerators

Miners

Asset class considerations The attractiveness of an investment balances risk, reward and portfolio fit. To date, the practice and ability to incorporate carbon-related risks into financial models has been relatively limited, but is slowly improving as the issue gains greater traction and more research becomes available. While the stranded assets debate has understandably focused on listed equities, we believe it also has broader ramifications on investment portfolios, with potential impacts across a range of asset classes throughout the entire energy supply chain.

6 towerswatson.com

CreditCorporate Credit: The majority of research assessing the risk of stranded assets to equity assets would also be relevant for corporate credit. Crucially an assessment of whether the credit spread is a fair reflection of the risk posed by stranded assets is required. There is an increasing ability to screen or tilt positions across a bond portfolio according to certain criteria and an increasing number of thematic indexes that might fulfil an investor’s desired response to stranded assets. Time horizon is also an important consideration for credit given the finite life of the security. For example, if the maturity of a bond is short enough so that the bond is repaid in full before the asset becomes stranded then the risk is effectively mitigated, although the path to maturity could be volatile if credit spreads widen. It might be useful to think about dynamically playing exposure to an entity via different mixes of debt and equity depending on the unfolding environment. However, taking credit risk relating to this topic is challenging given it is a common factor risk which is not always easy to diversify away so one may argue that taking credit risk makes more sense in other heterogeneous sectors.

Sovereign Credit: Government bonds potentially require a better understanding of the regulatory environment within the relevant country with respect to climate change. Arguably the policy adopted by a country may have a smaller

effect on that country’s bond valuations than the activities of a company may have on that company’s corporate credit valuations. However the interaction between domestic public policy/commitments and global policy is an area investors who are concerned about this topic may want to monitor with respect to government bond valuations. It also brings to the surface an interesting question around who pays – taxpayers or investors as this could have a material impact on sovereign debt values depending on the policy response.

Private Credit: The approach to private credit can be similar to that for public credit markets and equity markets, without the liquidity. With that said, private credit investments can include more esoteric investments such as shipping and aircraft leases, which come with their own challenges but understanding the business model exposure at the asset level is the first step in the process. There may also be opportunities in private credit if we see banks reducing their willingness to provide financing to certain mining businesses or pressure on mining businesses leads to non-performing loans. This in itself could create a supply/demand imbalance which would see the cost of debt rise for these groups. In turn such a situation could provide an opportunity for non-bank lenders to enter the market and fill the void of banks – not unlike what we have seen with the significant regulation which has structurally impacted the banking industry.

companies7. Indeed even a larger divestment movement would potentially only have short-term impacts on equity valuations, as divestment is unlikely to affect the operating cash flows of the targeted companies and there is likely to be a neutral or contrarian investor happy to acquire the divested stock at a temporarily depressed price. Another consequence of divestment could be an increased cost of capital at the margin for companies targeted for divestment. However again there are likely to be other investors willing to provide funding.

An investor could use the inherent nature of the asset class (liquidity in the case of equities) to help formulate an appropriate response to this topic. The liquidity of listed equities versus private markets would arguably make it easier in equity allocations to respond to changes in scenarios and tilt dynamically according to updated risk assessments.

Private Equity: This can be assessed in a similar fashion to public equities without the associated short-term noise of public equity markets. The illiquidity of the asset class means that more conviction will be required to take a position designed to exploit the stranded asset theme, regardless of what the investor believes. For an investor that believes renewable energy will be a much greater part of the world’s future energy mix, private equity is ripe for investment opportunities related to the topic with a plethora of clean-tech focused private equity funds available for investment. However private equity investing requires a greater governance budget as well as potentially high fees and may not be the most appropriate solution for every investor. Investors also need to be aware of the potential risks of being first mover investors in new technologies.

Fossil Fuels – Exploring the stranded assets debate 7

Diversifying StrategiesFor the purposes of this paper we have focused on the key diversifying asset classes which form an integral part of many institutional investment portfolios around the world, namely real estate, infrastructure and hedge funds. Diversifying strategies tend to be more concentrated in terms of asset level exposure – for example, an infrastructure or real estate fund may only have ten assets whereas equity portfolios can have many more positions. Valuation risk needs to be considered for diversifying strategies in a similar manner to equity and credit.

Infrastructure: Assets such as railways and ports involved in the transportation of commodities, could potentially face significant valuation headwinds if certain commodities become stranded assets. Infrastructure assets are underpinned by long-term growth assumptions. Given the current prices being paid for large ‘trophy’ assets, particularly in countries like Australia, it would appear that many of these assumptions are quite aggressive. One must question the longer term use of these assets if a stranded assets scenario were to play out or further government intervention were to be implemented (for example, recent Chinese restrictions on the importation of metallurgical coal8). Institutional investors should also question whether the management teams of these assets have the appropriate skills to convert assets to alternative uses in a timely manner should the risk of stranded assets materialise (for example, converting a coal port to a container port).

There are also opportunities in infrastructure such as renewable energy which can act as a natural hedge to other exposures in the portfolio. The viability of renewable energy projects is predicated on investment and this investment can be used to further develop the technology supporting these projects resulting in a rapidly changing environment in the way in which energy is produced, stored and used. For example, since the Chinese moved into the market for solar energy, the price of small scale solar projects has almost halved9. This also highlights the early mover risk with renewables and broader technological advancement – even

if the technology is widely accepted, rapidly falling prices and technological piggy-backers may result in sub-optimal returns for first movers.

Hedge Funds: By their very nature hedge funds present an opportunity to take advantage of the stranded assets theme. Equity and credit strategies with a particular focus on momentum and directional trading could target pure play coal companies should they come under further scrutiny from the market. Activist equity strategies could also be used to engage more closely with company management on the topic, while macro or trend following strategies could be used to exploit government policy changes. The re-insurance sector could also be an interesting asset class both from a risk and opportunity perspective if there is further scientific evidence linking the impact of weather patterns to climate change. This could have lasting impacts on the catastrophe bond market and the broader re-insurance market.

Real Estate: Property is also exposed to the financial risks associated with carbon exposure although it tends to be through energy consumption within buildings rather than direct emissions. Buildings are the single largest contributor to the world’s greenhouse gas emissions, using 40% of global energy and generating up to 40% of carbon emissions10. The advantages of reduced energy consumption and greener policies are well recognised for property assets. There are widely accepted reporting standards for energy and water efficiency ratings in the real estate industry (for example, GRESB, NABERS, ABGR and Green ratings) and in some regions incentives exist to promote energy efficient buildings. The benefit of greater energy efficiency is lower operating costs which can make the building more attractive to potential tenants. Additionally future rental growth, lower depreciation and the green policies in place by many corporates contribute to the attractiveness of energy efficient buildings. Older property assets, which continue to be large consumers of energy, are potentially at risk if higher energy prices emerge as a result of carbon taxes or a reduced availability of economically cheap sources of energy such as fossil fuels.

8 towerswatson.com

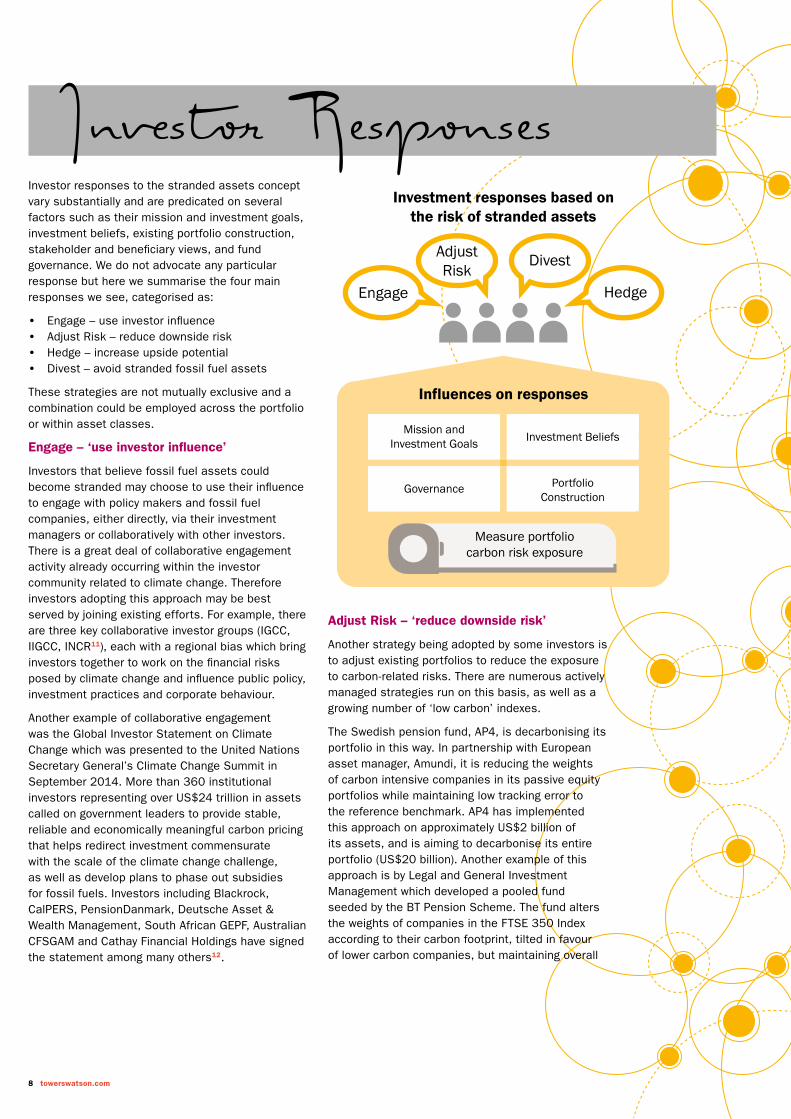

Investor responses to the stranded assets concept vary substantially and are predicated on several factors such as their mission and investment goals, investment beliefs, existing portfolio construction, stakeholder and beneficiary views, and fund governance. We do not advocate any particular response but here we summarise the four main responses we see, categorised as:

• Engage – use investor influence • Adjust Risk – reduce downside risk • Hedge – increase upside potential • Divest – avoid stranded fossil fuel assets

These strategies are not mutually exclusive and a combination could be employed across the portfolio or within asset classes.

Engage – ‘use investor influence’

Investors that believe fossil fuel assets could become stranded may choose to use their influence to engage with policy makers and fossil fuel companies, either directly, via their investment managers or collaboratively with other investors. There is a great deal of collaborative engagement activity already occurring within the investor community related to climate change. Therefore investors adopting this approach may be best served by joining existing efforts. For example, there are three key collaborative investor groups (IGCC, IIGCC, INCR11), each with a regional bias which bring investors together to work on the financial risks posed by climate change and influence public policy, investment practices and corporate behaviour.

Another example of collaborative engagement was the Global Investor Statement on Climate Change which was presented to the United Nations Secretary General’s Climate Change Summit in September 2014. More than 360 institutional investors representing over US$24 trillion in assets called on government leaders to provide stable, reliable and economically meaningful carbon pricing that helps redirect investment commensurate with the scale of the climate change challenge, as well as develop plans to phase out subsidies for fossil fuels. Investors including Blackrock, CalPERS, PensionDanmark, Deutsche Asset & Wealth Management, South African GEPF, Australian CFSGAM and Cathay Financial Holdings have signed the statement among many others12.

Adjust Risk – ‘reduce downside risk’

Another strategy being adopted by some investors is to adjust existing portfolios to reduce the exposure to carbon-related risks. There are numerous actively managed strategies run on this basis, as well as a growing number of ‘low carbon’ indexes.

The Swedish pension fund, AP4, is decarbonising its portfolio in this way. In partnership with European asset manager, Amundi, it is reducing the weights of carbon intensive companies in its passive equity portfolios while maintaining low tracking error to the reference benchmark. AP4 has implemented this approach on approximately US$2 billion of its assets, and is aiming to decarbonise its entire portfolio (US$20 billion). Another example of this approach is by Legal and General Investment Management which developed a pooled fund seeded by the BT Pension Scheme. The fund alters the weights of companies in the FTSE 350 Index according to their carbon footprint, tilted in favour of lower carbon companies, but maintaining overall

Investor Responses

Mission andInvestment Goals Investment Beliefs

PortfolioConstruction

Governance

HedgeEngage

DivestAdjust Risk

Investment responses based onthe risk of stranded assets

Influences on responses

Measure portfolio carbon risk exposure

Fossil Fuels – Exploring the stranded assets debate 9

sector weightings as for the FTSE 350 Index13. In a similar vein the MSCI Global Low Carbon Target Indexes overweight companies with low carbon emissions (relative to revenues) and low potential carbon emissions (per dollar of market capitalisation). The indexes are designed to achieve a 30 basis point per annum ex ante tracking error target while minimising the carbon exposure relative to their parent indexes14.

Hedge – ‘increase upside potential’

Alternatively some investors have placed more emphasis on positioning portfolios to capture the upside potential of climate change, as opposed to managing for downside risks. These investors have allocated capital to investment strategies specifically designed to perform well in a low-carbon economy such as companies involved in energy efficiency, renewable energy and clean technology. If such companies thrive in a low carbon environment they could provide some degree of offset, or hedge, against climate-related risk on more conventional portfolios which are exposed to fossil fuels. There are a numerous such investment strategies, across a range of asset classes, including both active and passive approaches.

Examples of funds taking this approach include Local Government Super (Australia), which invests approximately 8% of its assets in low carbon investments. These include equities with low carbon activities, property, private equity and green bonds. Meanwhile the UK Environment Agency Pension Fund is aiming to have 25% of its portfolio invested in companies and assets that make a positive contribution to a low carbon and climate resilient economy by 201513.

For passive investors there are a number of indexes which provide exposure to specific market segments. The FTSE Environmental Markets Index series measures the performance of global companies whose core business is in the development and deployment of environmental technologies, including renewable and alternative energy, energy efficiency, water technology and waste and pollution control15. Other examples include S&P’s Global Eco Index which comprises 40 of the largest publicly traded companies in clean energy, environmental services and water16 and the MSCI Global Climate Index which is an equal weighted index of 100 developed market companies that are leaders in renewable energy, future fuels, clean technology and efficiency14.

Divest – ‘avoid fossil fuel assets’

Some investors have chosen to exclude fossil fuels altogether from their portfolio, for a variety of reasons including moral arguments. Regardless of the motivation, the divestment movement has gained considerable traction in recent months, in part stimulated by the 350.org campaign focused on educational and public institutional investors. In practice divestment may be confined to the avoidance of coal companies, or may involve a broader interpretation which excludes all fossil fuel companies.

The list of institutional investors that have committed to divest fossil fuel assets is growing; some examples include Stanford University (US), the University of Glasgow (UK), Oxford City Council (UK), City of Moreland (Australia)17 and the Rockefeller Foundation. The latter announced in September 2014 that it is working to exclude coal and tar sands from its portfolio immediately and will then determine an appropriate strategy for further divestment of other fossil fuels over the next few years18. By contrast, in 2014 the Norwegian Government Pension Fund reviewed its approach to fossil fuel investments and concluded that a blanket exclusion of fossil fuels was not appropriate but that its guidelines should be amended to allow companies to be removed from the investment universe on a case-by-case basis where there is ‘unacceptable’ risk that a company’s actions are ‘severely harmful’ to the climate19.

To facilitate divestment, index providers have created fossil-fuel-free indexes. Examples include the MSCI ACWI ex Fossil Fuels Index which eliminates 100% of carbon reserves exposure by excluding companies that own oil, gas and coal reserves, while the MSCI ACWI ex Coal Index excludes companies that own coal reserves14. Meanwhile the FTSE Developed ex Fossil Fuels Index Series is a market capitalisation-weighted index which excludes companies that explore, own, and directly extract carbon reserves20.

Investors considering a divestment approach should be mindful of several issues. For example, is divestment in the best interests of the Fund’s stakeholders? Have fiduciaries sought to understand the views of members? If divestment is pursued, what exactly will be excluded; coal only or all fossil fuels? By its very nature, a portfolio which excludes fossil fuels will differ from its conventional reference benchmark and as such is likely to possess different risk-return characteristics. Investors should also consider the costs associated with excluding fossil fuels which may include transition costs, or higher manager fees.

10 towerswatson.com

We believe that institutional investors will experience greater pressure in the future from a range of stakeholders to set out their approach to environmental issues, such as climate change. These demands are likely to come from the media and campaign groups, but also increasingly from beneficiaries as social interest in the topic builds.

Naturally, greater interest in such topics also elevates the reputational risks associated with investors’ handling of such issues. This is particularly so where investors are required to be more transparent; in Australia for example there are moves towards disclosure of underlying holdings by superannuation funds which would enable greater scrutiny from stakeholders.

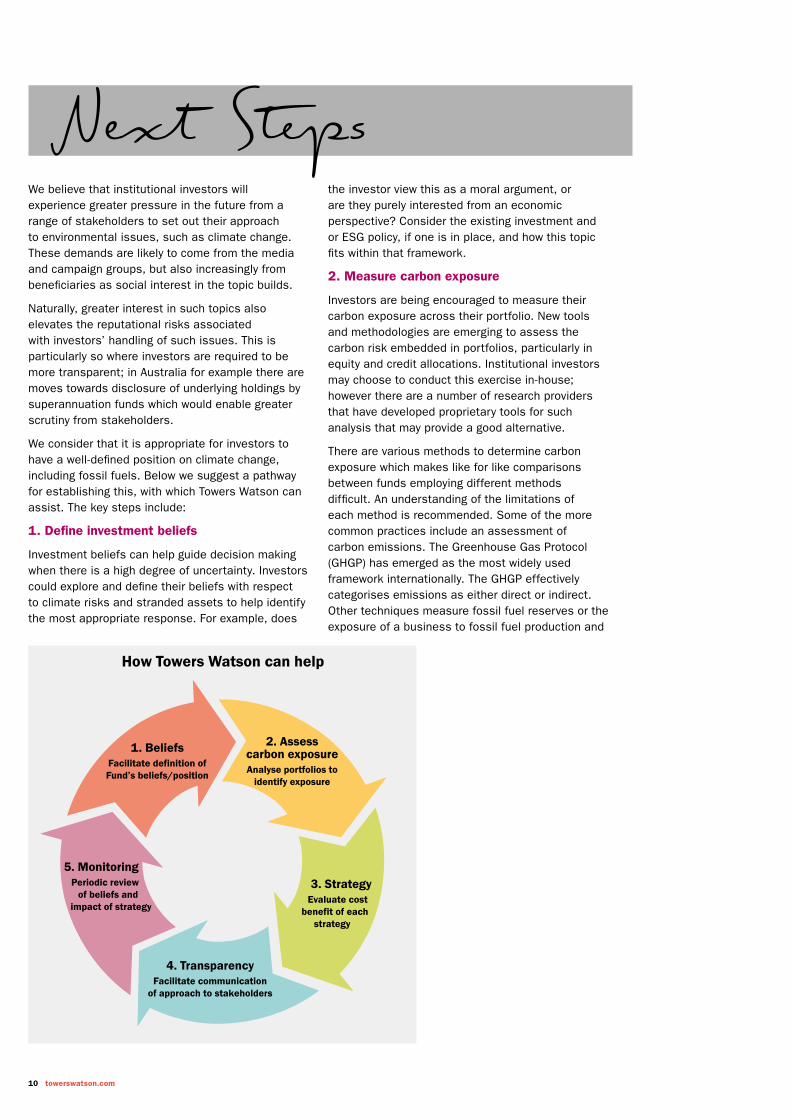

We consider that it is appropriate for investors to have a well-defined position on climate change, including fossil fuels. Below we suggest a pathway for establishing this, with which Towers Watson can assist. The key steps include:

1. Define investment beliefs

Investment beliefs can help guide decision making when there is a high degree of uncertainty. Investors could explore and define their beliefs with respect to climate risks and stranded assets to help identify the most appropriate response. For example, does

the investor view this as a moral argument, or are they purely interested from an economic perspective? Consider the existing investment and or ESG policy, if one is in place, and how this topic fits within that framework.

2. Measure carbon exposure

Investors are being encouraged to measure their carbon exposure across their portfolio. New tools and methodologies are emerging to assess the carbon risk embedded in portfolios, particularly in equity and credit allocations. Institutional investors may choose to conduct this exercise in-house; however there are a number of research providers that have developed proprietary tools for such analysis that may provide a good alternative.

There are various methods to determine carbon exposure which makes like for like comparisons between funds employing different methods difficult. An understanding of the limitations of each method is recommended. Some of the more common practices include an assessment of carbon emissions. The Greenhouse Gas Protocol (GHGP) has emerged as the most widely used framework internationally. The GHGP effectively categorises emissions as either direct or indirect. Other techniques measure fossil fuel reserves or the exposure of a business to fossil fuel production and

Next Steps

1. BeliefsFacilitate definition of Fund’s beliefs/position

2. Assesscarbon exposureAnalyse portfolios to

identify exposure

3. StrategyEvaluate cost

benefit of each strategy

4. TransparencyFacilitate communication

of approach to stakeholders

5. MonitoringPeriodic review

of beliefs and impact of strategy

How Towers Watson can help

Fossil Fuels – Exploring the stranded assets debate 11

attempt to make a judgement on the materiality of those exposures according to revenues/market cap measures or other.

Aggregating exposures at an individual allocation level can give a view of the total portfolio exposure. This could be based on greenhouse gas emissions or another measurement. Another approach from a total portfolio view would be to depict the spectrum of exposures represented across the portfolio varying according to the intensity of the exposure. The aim should be for the investor to find a comfortable balance across that spectrum that they feel reflects the organisation’s beliefs. The spread should mirror the assessment of the risks to the portfolio. The ability to handle those investments from a governance perspective should also be taken into consideration in this exercise.

The Portfolio Decarbonisation Coalition (PDC) is a multi-stakeholder initiative encouraging institutional investors to assess and subsequently decarbonise their portfolios. One of their main goals is to make ‘carbon exposure footprinting’ common practice. PDC was co-founded by the UN Environment Programme Finance Initiative (UNEP FI), the fourth national pension fund of Sweden (AP4), Amundi Asset Management and CDP (formerly known as the Carbon Disclosure Project). The initiative aims to drive down carbon emissions by mobilising a critical mass of institutional investors to measure and publicly disclose their carbon exposure and gradually decarbonise their portfolios.

We have seen financial regulators apply stress tests to the banking sector in order to understand the resilience of the banks. It is important to note that these tests are not determined by how likely the regulators consider the scenarios to be but rather to understand the areas of vulnerability. Institutional investors could take the same approach. Using a variety of scenarios an asset owner could consider how the portfolio would be positioned from a risk perspective in those situations. Using managers to explain how companies in the portfolio are set up to deal with the internalisation of environmental costs for example could be helpful.

A number of frameworks have been developed to allow fossil fuel companies to report their carbon emissions using quantitative and qualitative information21. Quantitative information includes emissions by value chain stage, assumed emissions based on current production and reserves, and contribution of clean energy technologies. Qualitative information includes the analysis of climate change policies, the demand outlook and requires the consideration of the physical effects of climate change on the business’ operations. The information provided can help investors understand the underlying risks involved in investee companies.

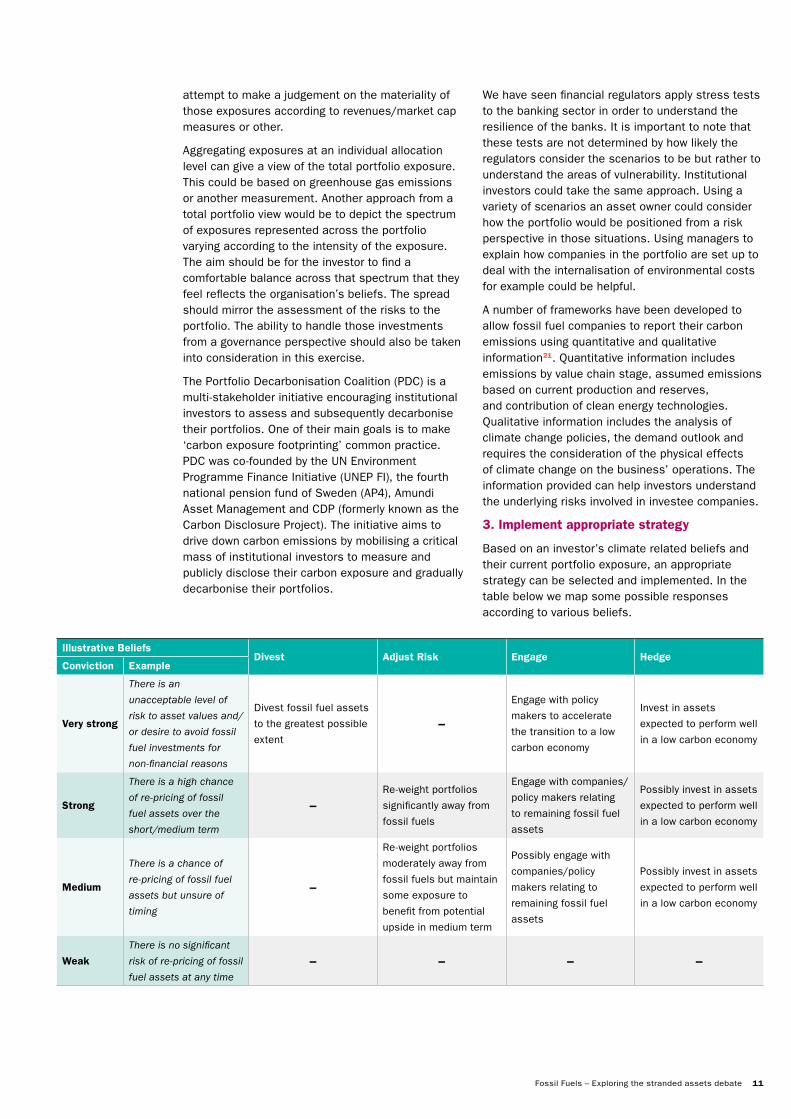

3. Implement appropriate strategy

Based on an investor’s climate related beliefs and their current portfolio exposure, an appropriate strategy can be selected and implemented. In the table below we map some possible responses according to various beliefs.

Illustrative BeliefsDivest Adjust Risk Engage Hedge

Conviction Example

Very strong

There is an

unacceptable level of

risk to asset values and/

or desire to avoid fossil

fuel investments for

non-financial reasons

Divest fossil fuel assets

to the greatest possible

extent–

Engage with policy

makers to accelerate

the transition to a low

carbon economy

Invest in assets

expected to perform well

in a low carbon economy

Strong

There is a high chance

of re-pricing of fossil

fuel assets over the

short/medium term

–Re-weight portfolios

significantly away from

fossil fuels

Engage with companies/

policy makers relating

to remaining fossil fuel

assets

Possibly invest in assets

expected to perform well

in a low carbon economy

Medium

There is a chance of

re-pricing of fossil fuel

assets but unsure of

timing

–

Re-weight portfolios

moderately away from

fossil fuels but maintain

some exposure to

benefit from potential

upside in medium term

Possibly engage with

companies/policy

makers relating to

remaining fossil fuel

assets

Possibly invest in assets

expected to perform well

in a low carbon economy

Weak

There is no significant

risk of re-pricing of fossil

fuel assets at any time– – – –

12 towerswatson.com

4. Be transparent

We see increasing levels of transparency relating to investors’ position on fossil fuels, which in part is stimulated by engagement initiatives such as the Asset Owners Disclosure Project (AODP)22. The AODP focuses on improving disclosure and conducts a survey of the world’s largest 1,000 asset owners (pension, superannuation, insurance and sovereign wealth funds) with respect to their management of climate risks, the results of which are published in the AODP Global Climate Index. The UK Environment Agency Pension Fund currently occupies first place in the index; it has been conducting annual carbon footprints for several years and its overall footprint has reduced by 39% since 200823. Recently it commissioned Trucost to assess the embedded carbon emissions in the fossil fuel assets held in the equity portfolio to identify the potential for stranded assets24.

Another example of an investor promoting greater disclosure is The Pensions Trust in the UK which requires its hedge fund managers to report quarterly on the Fund’s underlying exposure to companies in six of the most carbon intensive sectors. This information helps the Trust to monitor its exposure to climate risk and participate in relevant engagement activity13.

While we welcome greater transparency the timing of communications and the extent of transparency should be considered carefully. Any communication of a commitment should reflect the ability of the asset owner to implement the policy in practice. The reputational risk associated with failing to adhere to one’s own policy on fossil fuels should not be underestimated.

5. Monitor and review

Any response adopted should incorporate a regular review process to monitor the progress and status of the chosen strategy. We would suggest:

1. Reviewing the thesis for the response adopted and ensuring that conviction in that belief remains;

2. Comparing the performance of the portfolio against expectations and objectives; and

3. Considering valuation metrics relevant to assets in the portfolio that are particularly exposed to the stranded assets theme to assess whether particular opportunities have become attractive/unattractive over time.

Further InformationIf you would like to discuss any of the areas covered in more detail, please contact your usual Towers Watson consultant.

Fossil Fuels – Exploring the stranded assets debate 13

References1 UN Framework Convention on Climate Change

(UNFCCC), The Cancun Agreement 2010.

2 Global Investment Committee, Secular Outlook 2013, Assimilating Thematic Thinking, Towers Watson.

3 Observations: Atmosphere and Surface, 2013. Available at: http://www.climatechange2013.org/report/full-report/

4 Carbon Tracker Initiative (CTI) is a not for profit financial think-tank aimed at enabling a climate secure global energy market by aligning capital market actions with climate reality. The CTI team comprises financial, energy and legal experts with a ground breaking approach to limiting future greenhouse gas emissions. CTI provides information, research and events to educate and empower all the key decision makers and groups.

5 World Energy Outlook 2014, International Energy Agency, 2014. http://www.iea.org/newsroomandevents/pressreleases/2014/november/signs-of-stress-must-not-be-ignored-iea-warns-in-its-new-world-energy-outlook.html/

6 2015 Shareholder Resolution Exxon Mobil, Arjuna Capital and As you Sow at the request of Capital Distribution/Carbon Asset Risk, 2014. Available at: http://www.asyousow.org/companies/exxon-mobil/

7 Stranded assets and the fossil fuel divestment campaign: what does divestment mean for the valuation of fossil fuel assets?, University of Oxford Smith School of Enterprise and the Environment Stranded Assets Programme, 2014.

8 “Coking coal - also known as metallurgical coal - is mainly used in steel production”, http://www.worldcoal.org/coal/uses-of-coal/

9 “China-US deal is a tipping point for carbon policy”, The Australian Financial Review, Friday 12 November 2014.

10 The Business Case for Green Building, Green Building Council of Australia, 2013. Available at: http://www.gbca.org.au/resources/gbca-publications/green-building-evolution-2013/

11 The Investor Group on Climate Change (IGCC) brings together investors from Australia and New Zealand; the Institutional Investors Group on Climate Change (IIGCC) is a forum of predominantly European investors with over 90 members with €7.5trillion in assets; and the Investor Network on Climate Risk (INCR) is mainly a North American focused network of institutional investors with over 100 members with over $13 trillion in assets.

12 http://investorsonclimatechange.org/

13 Financial Institutions Taking Action on Climate Change, IIGCC, INCR, IGCC, AIGCC, UNEP FI and PRI, 2014. Available at: http://www.investorsonclimatechange.org/

14 http://www.msci.com/products/indexes/esg/environmental/

15 http://www.ftse.com/products/indices/env-markets

16 http://eu.spindices.com/index-family/environmental-social-governance/green-investing/

17 http://gofossilfree.org/commitments/

18 http://www.rbf.org/content/divestment-statement/

19 http://www.ipe.com/10005429.article?utm_source=Newsletter&utm_medium=Email&utm_campaign=IPE_Daily/

20 FTSE Developed ex Fossil Fuel Index Series, FTSE, 2014. Available at: http://www.ftse.com/products/indices/dev-ex-fossil-fuels/

21 Global Climate Disclosure Framework for Oil & Gas Companies, IIGC, Ceres and IGCC, 2010. Available at: http://www.igcc.org.au/page-1357360/

22 http://aodproject.net/

23 Strategy to address climate risk, The Environment Agency Pension Fund, 2014. Available at: http://www.eapf.org.uk/

24 Stranded Assets: fossil fuels, Trucost, 2014. Available at: http://www.trucost.com/published-research/128/strandedassets/environmentagency/

towerswatson.com

/company/towerswatson @towerswatson /towerswatson

This document was prepared for general information purposes only and should not be considered a substitute for specific professional advice. In particular, its contents are not intended by Towers Watson to be construed as the provision of investment, legal, accounting, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. As such, this document should not be relied upon for investment or other financial decisions and no such decisions should be taken on the basis of its contents without seeking specific advice. This document is based on information available to Towers Watson at the date of issue, and takes no account of subsequent developments after that date. In addition, past performance is not indicative of future results. In producing this document Towers Watson has relied upon the accuracy and completeness of certain data and information obtained from third parties. This document may not be reproducedor distributed to any other party, whether in whole or in part, without Towers Watson’s prior written permission, except as may be required by law. In the absence of its express written permission to the contrary, Towers Watson and its affiliates and their respective directors, officers and employees accept no responsibility and will not be liable for any consequences howsoever arising from any use of or reliance on the contents of this document including any opinions expressed herein.

Copyright © 2015 Towers Watson. All rights reserved.TW-EU-2015-44266. July 2015.

About Towers WatsonTowers Watson is a leading global professional services company that helps organisations improve performance through effective people, risk and financial management. With 16,000 associates around the world, we offer consulting, technology and solutions in the areas of benefits, talent management, rewards, and risk and capital management. Learn more at towerswatson.com

Towers Watson71 High HolbornLondonWC1V 6TP