topic 6 acctg_for_financial_instruments

TRANSCRIPT

TOPIC 6

ACCOUNTING FOR

FINANCIAL INSTRUMENTS

1

Introduction

Accounting standards

1) MFRS 139 Financial Instruments

Recognition and Measurement

2) MFRS 132 Financial Instruments

Presentation

3) MFRS 7 Financial Instruments Disclosures

MFRS 9 Financial Instruments (IFRS 9

issued by IASB in October 2010) (MFRS 139

will be superseded by MFRS 9)

2

Introduction

A financial instrument is any contract that gives

rise to a financial asset of one entity and a

financial liability or equity instrument of another

entity

Financial assets (MFRS 132 para 11)

Financial Liabilities (MFRS 132 para 11)

Financial instruments include primary instruments (such as receivables

payables and equity instruments) and

derivative financial instruments (such as financial

options futures and forwards interest rate swaps

and currency swaps)

3

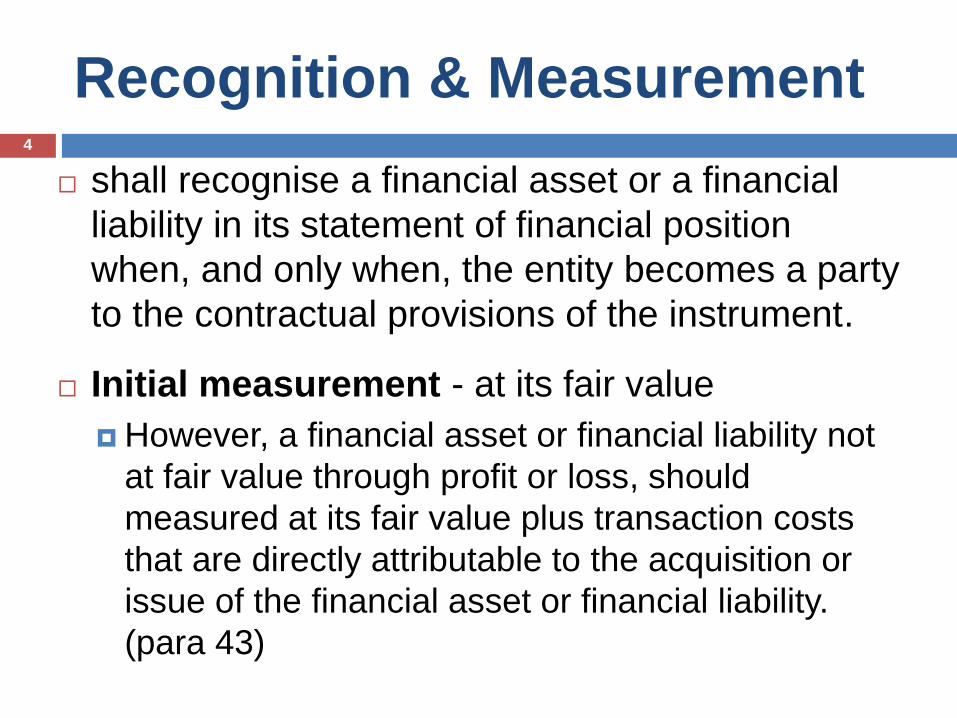

Recognition amp Measurement

shall recognise a financial asset or a financial

liability in its statement of financial position

when and only when the entity becomes a party

to the contractual provisions of the instrument

Initial measurement - at its fair value

However a financial asset or financial liability not

at fair value through profit or loss should

measured at its fair value plus transaction costs

that are directly attributable to the acquisition or

issue of the financial asset or financial liability

(para 43)

4

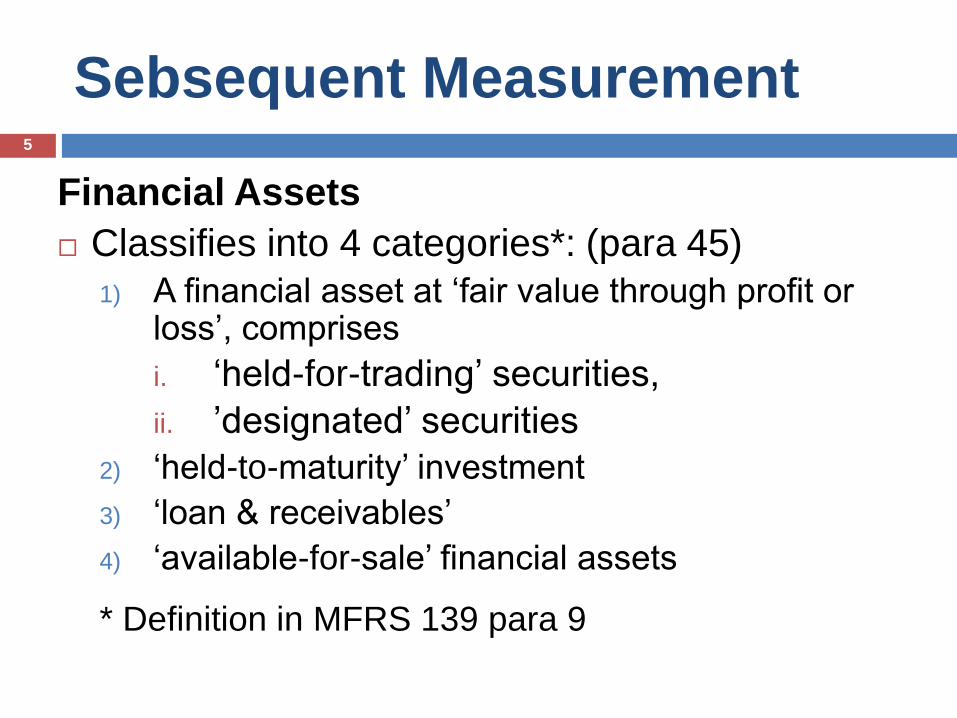

Sebsequent Measurement

Financial Assets

Classifies into 4 categories (para 45)

1) A financial asset at lsquofair value through profit or lossrsquo comprises

i lsquoheld-for-tradingrsquo securities

ii rsquodesignatedrsquo securities

2) lsquoheld-to-maturityrsquo investment

3) lsquoloan amp receivablesrsquo

4) lsquoavailable-for-salersquo financial assets

Definition in MFRS 139 para 9

5

Sebsequent Measurement

Financial Liabilities

Measure either at (para 47)

1) Fair value through profit or loss or

2) Amortised costs using effective interest method

6

Derecognition

Financial Assets

An entity shall derecognise a financial asset

when and only when

(a) the contractual rights to the cash flows from

the financial asset expire or

(b) it transfers the financial asset as set out in

para 18 and 19 and the transfer qualifies for

derecognition in accordance with para 20

7

Derecognition

Financial Liabilities

An entity shall remove a financial liability (or a

part of a financial liability) from its statement of

financial position when and only when it is

extinguished

ie when the obligation specified in the contract is

discharged or cancelled or expires

8

HEDGE ACCOUNTING

9

Hedging

Companies are often exposed to risks of

fluctuations in the prices of currencies

commodities or securities that affect profit or

loss

For example companies with foreign currency

transactions are exposed to risk due to changes

in foreign currency exchange rates

Hedging is a risk management strategy used by

companies to manage risk exposures

10

Hedging

The two most common hedging instruments

used by companies are forward contracts and

option contracts

A forward contract is a contract that enables a

company to lock in the price at which it will buy

or sell a certain asset in the future

An option is a contract that grants the holder of

the option the right but not an obligation to buy

or sell a certain asset at a specified price during

a specified period

11

Hedge Accounting

Hedge accounting involves representation of the

effect of the risk management activities in the

financial statements

Hedge accounting specifies how gains or losses

on hedge instrument are to be accounted

12

Hedge Accounting

Hedge accounting allows profit or loss from

change in fair value of the hedged item and loss

and profit from the hedging instrument to be

offset during the same accounting period ndash thereby

reduces the volatility of profit or loss

Hedged item ndash asset liability firm commitment

forecast transaction or net investment in a foreign

operation that expose to risk of changes in fair

value

Hedge instrument ndash a derivative whose value is

expected to offset change in fair value of a hedged

item

13

Hedge Accounting

Hedge accounting is a special accounting amp is

permited under MFRS 139 if and only if all

the conditions in para 88 are met

Whether or not hedge and whether or not to

apply hedge accounting are two separate

issues

Hedge accounting is not compulsory

14

Hedge Accounting

Hedge Effectiveness

For hedge accounting to be used the hedge

must be expected to be highly effective gains

and losses on the hedging instrument is

expected to be almost fully offset losses and

gains on the item being hedged ndash within a

range of 80 to 125

15

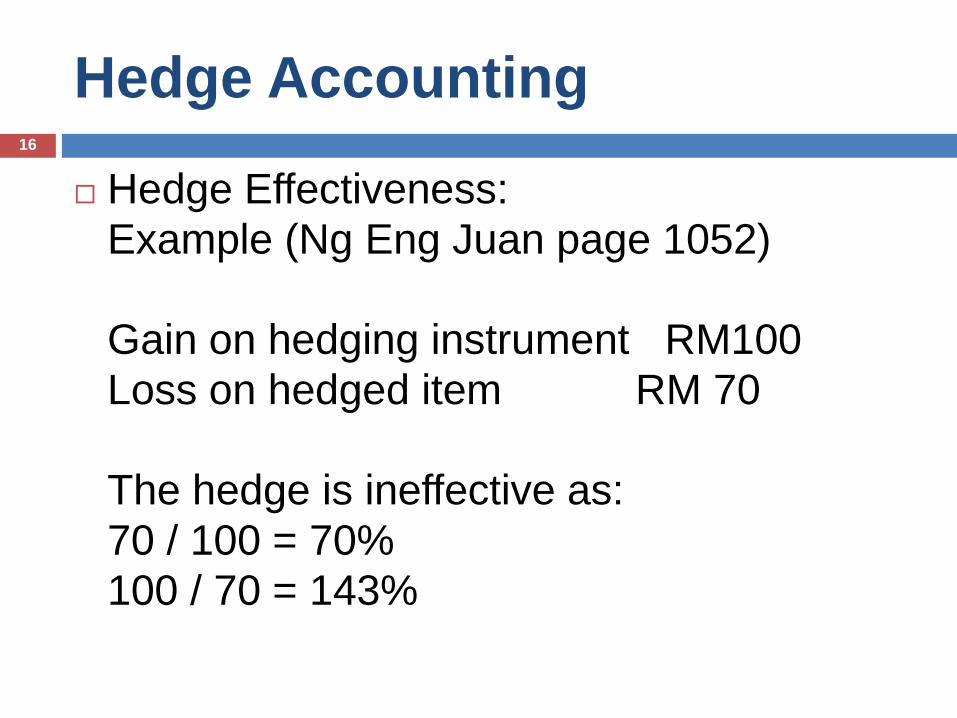

Hedge Accounting

Hedge Effectiveness

Example (Ng Eng Juan page 1052)

Gain on hedging instrument RM100

Loss on hedged item RM 70

The hedge is ineffective as

70 100 = 70

100 70 = 143

16

Hedge Accounting

Hedge Effectiveness

Example (Ng Eng Juan page 1052)

Gain on hedging instrument RM100

Loss on hedged item RM90

The hedge is effective as

90 100 = 90

100 90 = 111

17

Hedge Accounting

Hedging of recognized foreign currency

assetsliabilities and hedging of foreign

currency commitments

The hedge is considered effective if the

currency type currency amount and

settlement date of the hedging instrument

match those of the hedge item

18

Hedge Accounting

Hedging accounting are categorized into 3

types (para 86)

(1) fair value hedge

(2) cash flow hedge

(3) hedge of a net investment in a foreign entity

19

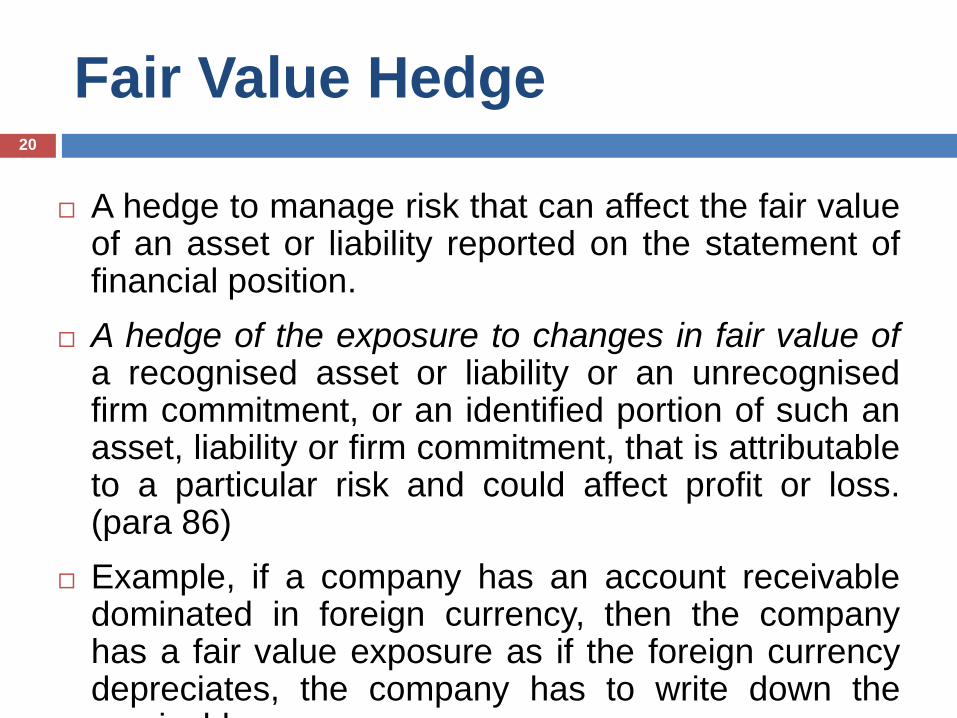

Fair Value Hedge

A hedge to manage risk that can affect the fair valueof an asset or liability reported on the statement offinancial position

A hedge of the exposure to changes in fair value ofa recognised asset or liability or an unrecognisedfirm commitment or an identified portion of such anasset liability or firm commitment that is attributableto a particular risk and could affect profit or loss(para 86)

Example if a company has an account receivabledominated in foreign currency then the companyhas a fair value exposure as if the foreign currencydepreciates the company has to write down thereceivable

20

Fair Value Hedge

Accounting treatment (para 89)

a) the gain or loss from remeasuring the hedging instrument at fair value (for a derivative hedging instrument) or the foreign currency component of its carrying amount measured in accordance with MFRS 121 (for a non-derivative hedging instrument) shall be recognised in profit or loss and

b) the gain or loss on the hedged item attributable to the hedged risk shall adjust the carrying amount of the hedged item and be recognised in profit or loss

This applies if the hedged item is otherwise measured at cost Recognition of the gain or loss attributable to the hedged risk in profit or loss applies if the hedged item is an available-for-sale financial asset

21

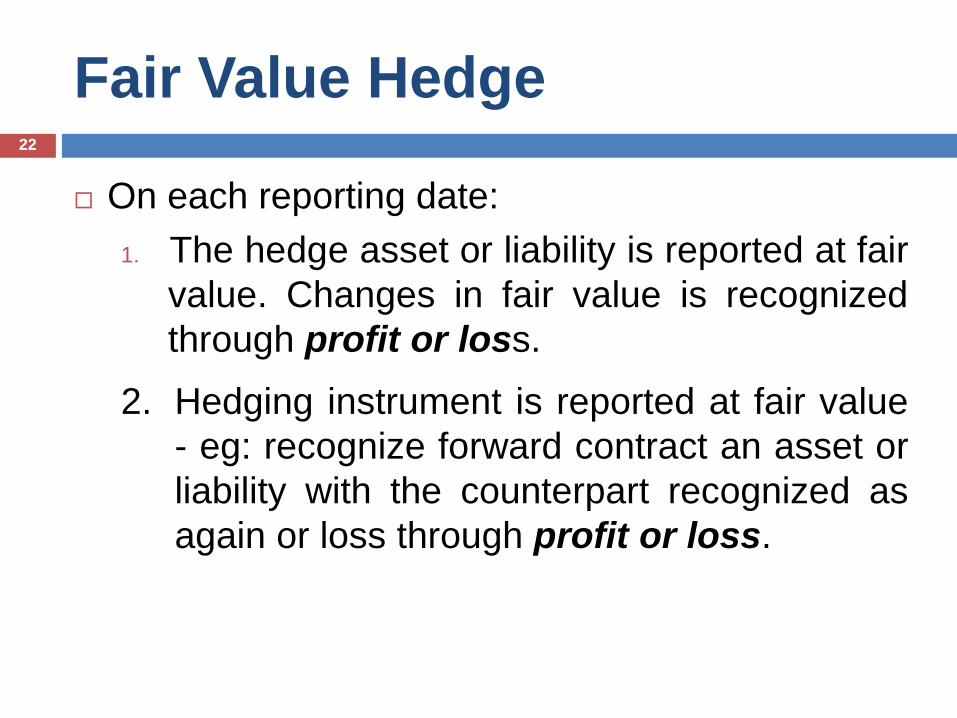

Fair Value Hedge

On each reporting date

1 The hedge asset or liability is reported at fair

value Changes in fair value is recognized

through profit or loss

2 Hedging instrument is reported at fair value

- eg recognize forward contract an asset or

liability with the counterpart recognized as

again or loss through profit or loss

22

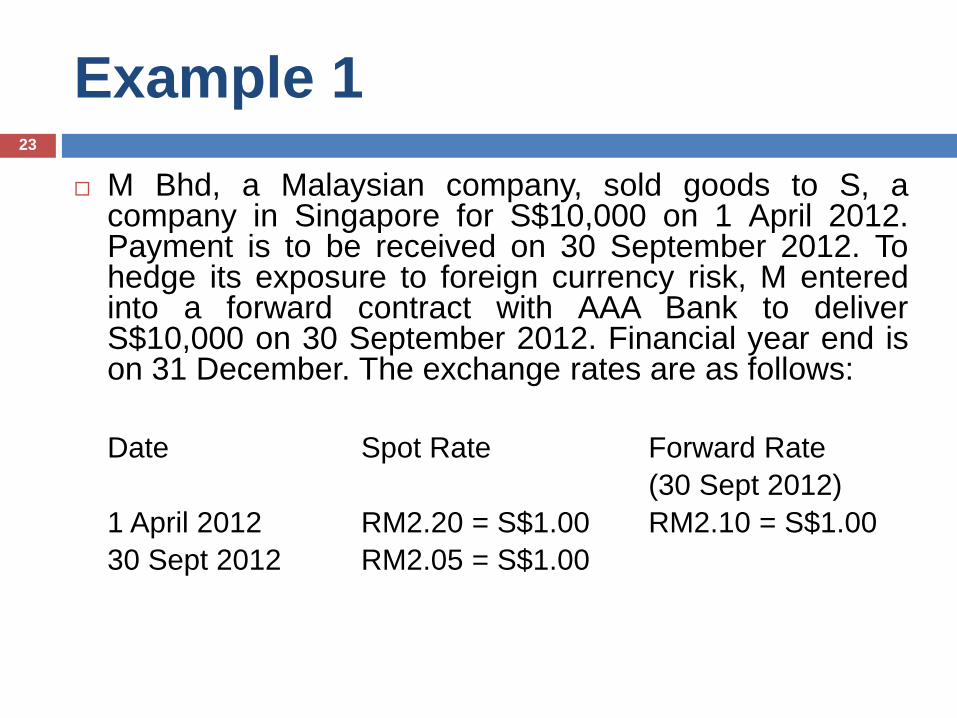

Example 1

M Bhd a Malaysian company sold goods to S acompany in Singapore for S$10000 on 1 April 2012Payment is to be received on 30 September 2012 Tohedge its exposure to foreign currency risk M enteredinto a forward contract with AAA Bank to deliverS$10000 on 30 September 2012 Financial year end ison 31 December The exchange rates are as follows

Date Spot Rate Forward Rate

(30 Sept 2012)

1 April 2012 RM220 = S$100 RM210 = S$100

30 Sept 2012 RM205 = S$100

23

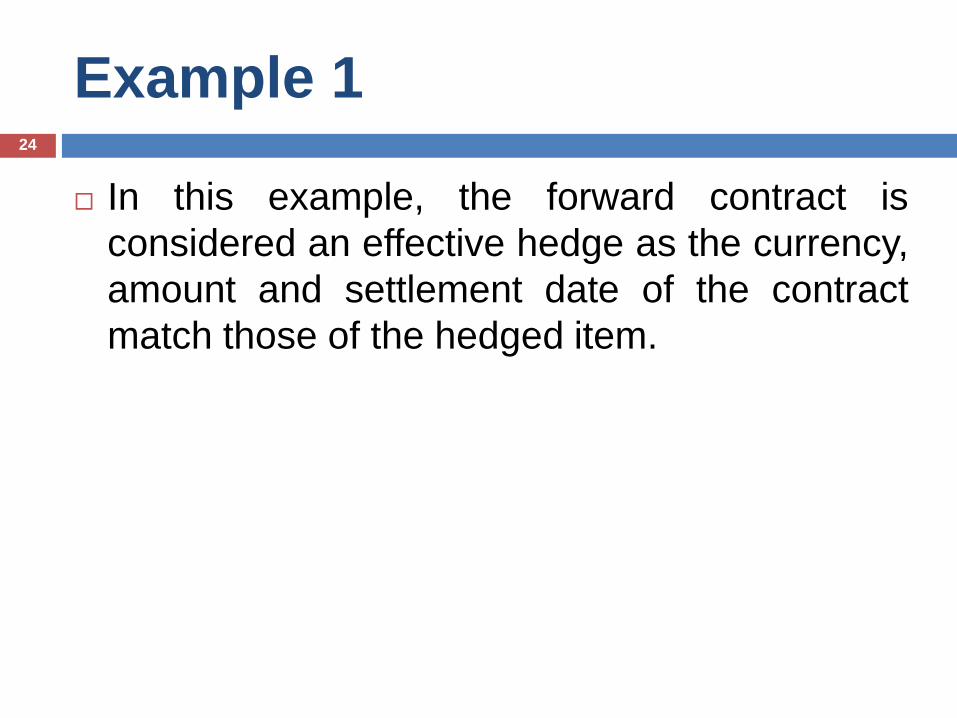

Example 1

In this example the forward contract is

considered an effective hedge as the currency

amount and settlement date of the contract

match those of the hedged item

24

Example 1

Solution

1 April 2012

Accounts receivable (S$) 22000

Sales

22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

25

Example 1

30 Sept 2012

Foreign exchange loss 1500

Accounts receivable (S$) 1500

(To adjust the value of receivable to the new spot rate of RM205 10000 x (RM220 ndash RM205) = 1500)

Forward contract 500

Gain on forward contract 500

[To record the forward contract as an asset at its fair value of RM500 (10000 x (RM210 ndash RM205)]

26

Example 1

30 Sept 2012

Foreign currency (S$) 20500

Accounts receivable (S$)20500

(To record receipt of S$10000 from S at spot rate ofRM205)

Cash 21000

Foreign currency (S$) 20500

Forward contract 500

(To record settlement of contract ndash receipt of RM21000in exchange for S$10000)

27

Cash Flow Hedge

A hedge to manage risk that can affect the amount of

cash flow to be realized in the future

a hedge of the exposure to variability in cash flows that

1) is attributable to a particular risk associated with a

recognised asset or liability (such as all or some

future interest payments on variable rate debt) or a

highly probable forecast transaction and

2) could affect profit or loss

On each reporting date

Hedging instrument is reported at fair value - egrecognize forward contract an asset or liability with thecounterpart recognized as a cash flow hedge reserve(other comprehensive income)

28

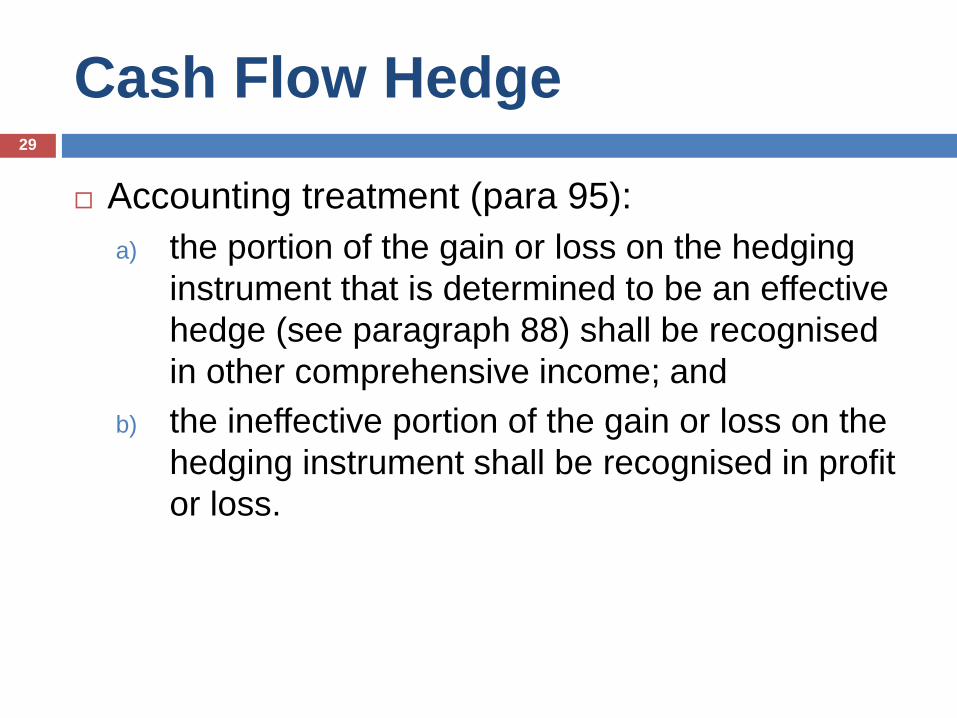

Cash Flow Hedge

Accounting treatment (para 95)

a) the portion of the gain or loss on the hedging

instrument that is determined to be an effective

hedge (see paragraph 88) shall be recognised

in other comprehensive income and

b) the ineffective portion of the gain or loss on the

hedging instrument shall be recognised in profit

or loss

29

Hedges of a net investment

Hedges of a net investment in a foreign operation (ie

the amount of the reporting entityrsquos interest in the net

assets of that operation) including a hedge of a

monetary item that is accounted for as part of the net

investment (see MFRS 121)

shall be accounted for similarly to cash flow hedges (para 102)

a) the portion of the gain or loss on the hedging instrument that is determined to be an effective hedge (see paragraph 88) shall be recognised in other comprehensive income and

b) the ineffective portion shall be recognised in profit or loss

30

Example 2

M Bhd a Malaysian company sold goods to S acompany in Singapore for S$10000 on 1 December2012 Payment is to be received on 1 March 2013 Tohedge its exposure to foreign currency risk M enteredinto a forward contract with AAA Bank to deliverS$10000 on 1 March 2013 Financial year end is on 31December The exchange rates are as follows

Date Spot Rate ForwardRate

(1 March 2013)

1 Dec 2012 RM220 = S$100 RM210 =S$100

31 Dec 2012 RM215 = S$100 RM200 = S$100

1 March 2013 RM185 = S$100

31

Fair Value Hedge

1 Dec 2012

Accounts receivable (S$) 22000

Sales 22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

32

Fair Value Hedge

31 Dec 2012

Foreign exchange loss 500

Accounts receivable (S$) 500

(To adjust the value of receivable to the new spot rate

10000 x RM220 ndash RM215)

Forward contract 980

Gain on forward contract 980

[To record forward contract as an asset at its fair value

10000 x (210 ndash 200) = 1000 Present value = 1000 x

0980 = 980 Assume M has an incremental borrowing rate

of 12 per year (1 per month)]

33

Fair Value Hedge

1 March 2013

Foreign exchange loss 3000

Accounts receivable (S$)3000

(To adjust the value of receivable to the new spotrate - 10000 x RM215 ndash RM185)

Forward contract 1520

Gain on forward contract 1520

[To adjust the value of forward contract to its currentfair value of RM2500 (10000 x (210 ndash 185)RM2500 ndash RM980 = RM1520]

34

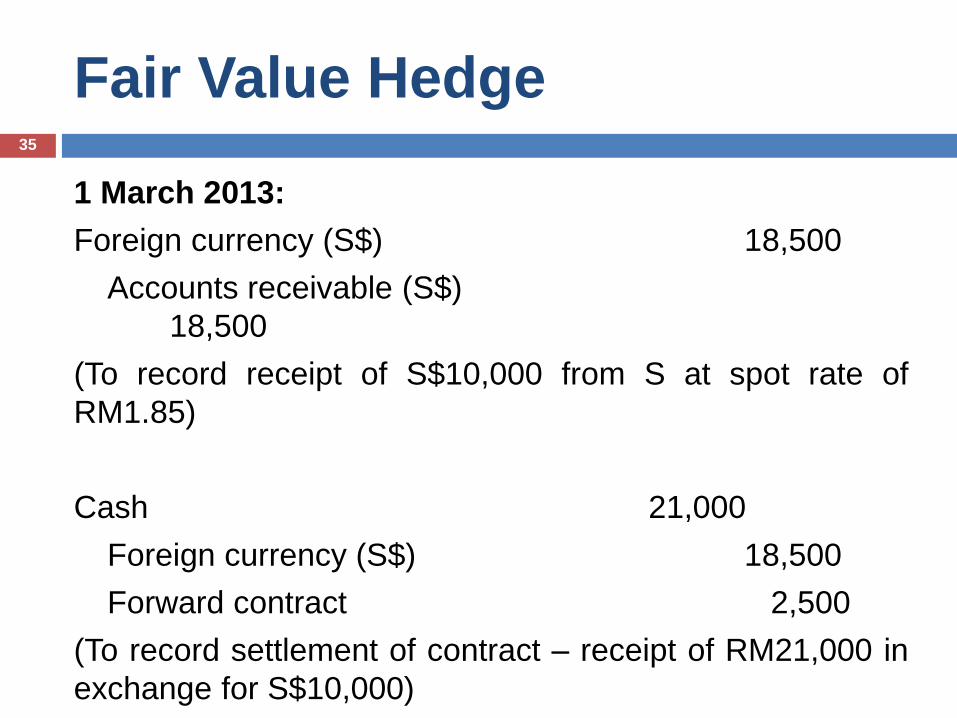

Fair Value Hedge

1 March 2013

Foreign currency (S$) 18500

Accounts receivable (S$)

18500

(To record receipt of S$10000 from S at spot rate of

RM185)

Cash 21000

Foreign currency (S$) 18500

Forward contract 2500

(To record settlement of contract ndash receipt of RM21000 in

exchange for S$10000)

35

Cash Flow Hedge

1 Dec 2012

Accounts receivable (S$) 22000

Sales 22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

36

Cash Flow Hedge

31 Dec 2012

Foreign exchange loss 500

Accounts receivable (S$) 500

(To adjust the value of receivable to the new spot rate

10000 x RM220 ndash RM215)

Forward contract 1000

Cash flow hedge reserve

(Other comprehensive income) 1000

[To record forward contract as an asset at its fair value

10000 x (210 ndash 200) = 1000 Present value = 1000 x

0980 = 980 Assume M has an incremental borrowing rate

of 12 per year (1 per month]

37

Cash Flow Hedge

31 Dec 2012

Cash flow hedge reserve

(Other comprehensive income) 500

Gain on forward contract 500

(To offset the foreign exchange loss)

Discount expense 333

Cash flow hedge reserve

(Other comprehensive income) 333

(To record discount expense 10000 x (220 spot rate on 1 Dec

minus 210 forward rate on 1 Dec x 13 - using straight line

method)

the cost of extending credit to S as S$ sold at discount in the 3

month forward market

38

Cash Flow Hedge

1 March 2013

Foreign exchange loss 3000

Accounts receivable (S$) 3000

(To adjust the value of receivable to the new spot rate ndash10000 x RM215 ndash RM1855)

Forward contract 1520

Cash flow hedge reserve

(Other comprehensive income) 1520

[To adjust the value of forward contract to its current fairvalue of RM2500 (10000 x (210 ndash 185) RM2500 ndashRM980 = RM1520]

39

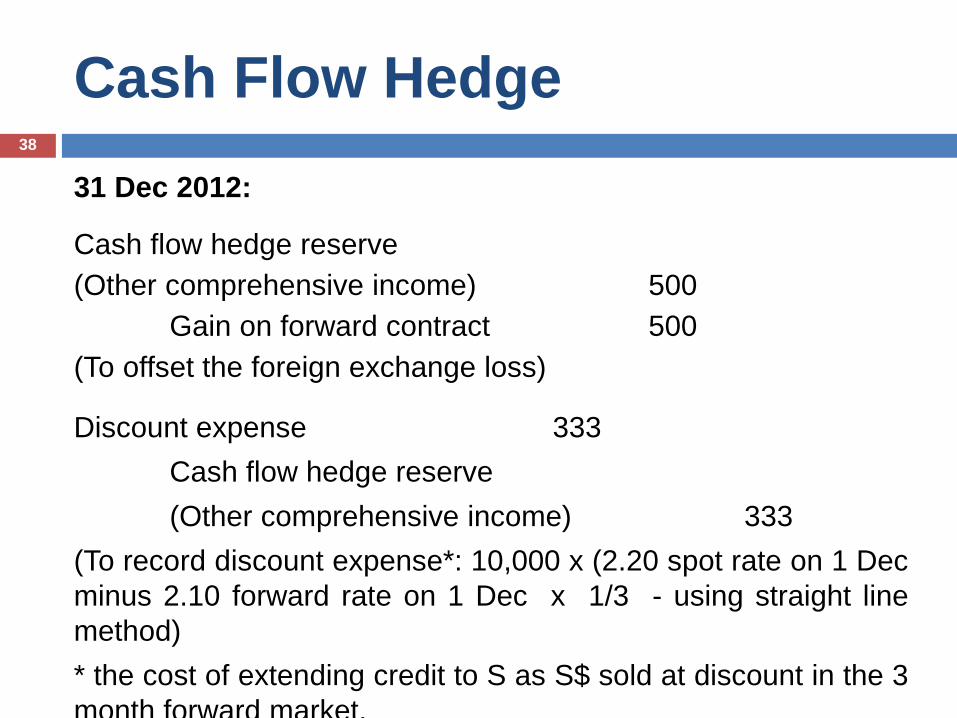

Cash Flow Hedge

1 March 2013

Cash flow hedge reserve

(Other comprehensive income) 3000

Gain on forward contract3000

(To offset the foreign exchange loss)

Discount expense 667

Cash flow hedge reserve

(Other comprehensive income) 667

(To record discount expense ndash the cost of extending creditto S 10000 x (220 spot rate on 1 Dec minus 210 forwardrate on 1 Dec) x 23 ndash using straight line method)

40

Cash Flow Hedge

1 March 2013

Foreign currency (S$) 18500

Accounts receivable (S$)18500

(To record receipt of S$10000 from S at spot rate ofRM185)

Cash 21000

Foreign currency (S$) 18500

Forward contract 2500

(To record settlement of contract ndash receipt of RM21000in exchange for S$10000)

41

Example 3 ndash Hedge of Probable

Forecast Transaction (Future

Sale)(refer page 1087 of Ng Eng Juan (2012) Q5)

On 1 April 20X8 ABC has 10 metric tons of tin

inventory carried at cost of RM22000 per metric

ton (total cost = RM220000)

Intends to sell the tin inventory on 30 June 20X8

On 1 April ABC enters into a futures contract to

sell 10 metric tons of tins at RM30000 per

metric ton on 30 June 20X8

42

Example 3

Date Spot price Futures price

(30 June 20X8)

1 April 20X8 RM29000 RM30000

30 April 20X8 RM31000 RM32000

31 May 20X8 RM33300 RM34500

30 June 20X8 RM35000

43

Example 3 - No Hedge

Accounting

30 April

Loss on futures contract 20000

Futures contract 20000

[To record futures contract as a liability at its fair value ndash 10 x (RM32000 ndash RM30000)]

31 May

Loss on futures contract 25000

Futures contract 25000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM34500 ndashRM32000)]

44

Example 3 - No Hedge

Accounting

30 June

Loss on futures contract 5000

Futures contract 5000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM35000 ndashRM34500)]

Futures contract 50000

Cash 50000

(To record settlement of futures contract)

45

Example 3 - No Hedge

Accounting

30 June

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

46

Example 3 ndash Fair Value Hedge

In a fair value hedge the carrying amount of

the hedged item should be adjusted for the

gain or loss attributable to the hedged risk

even if the hedged item is otherwise measured

at cost as required by other relevant MFRS

The gain or loss on the hedged item should be

recognized in profit or loss

47

Example 3 ndash Fair Value Hedge

30 April

Inventory 20000

Gain on revaluation of inventory

20000

(To adjust inventory to its current fair value ndash 10 x

(RM31000 ndash RM29000)

Loss on futures contract 20000

Futures contract 20000

[To record futures contract as a liability at its fair value ndash 10

x (RM32000 ndash RM30000)]

48

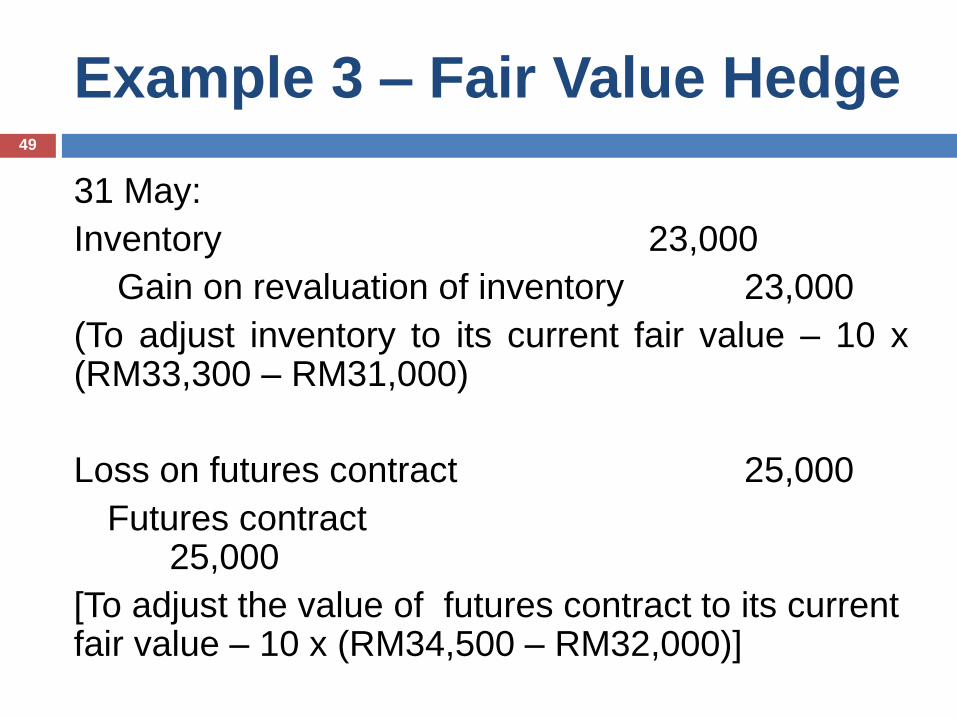

Example 3 ndash Fair Value Hedge

31 May

Inventory 23000

Gain on revaluation of inventory 23000

(To adjust inventory to its current fair value ndash 10 x(RM33300 ndash RM31000)

Loss on futures contract 25000

Futures contract25000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM34500 ndash RM32000)]

49

Example 3 ndash Fair Value Hedge

30 June

Inventory 17000

Gain on revaluation of inventory 17000

(To adjust inventory to its current fair value ndash 10 x(RM35000 ndash RM33300)

Loss on futures contract 5000

Futures contract5000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM35000 ndash RM34500)]

50

Example 3 ndash Fair Value Hedge

30 June

Futures contract 50000

Cash50000

(To record settlement of futures contract)

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

51

Example 3 ndash Cash Flow

Hedge30 April

Cash flow hedge reserve

(Other comprehensive income) 20000

Futures contract20000

31 May

Cash flow hedge reserve

(Other comprehensive income) 25000

Futures contract25000

52

Example 3 ndash Cash Flow

Hedge

30 June

Cash flow hedge reserve

(Other comprehensive income) 5000

Futures contract 5000

Futures contract 50000

Cash 50000

(To record settlement of futures contract)

53

Example 3 ndash Cash Flow

Hedge30 June

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

Sales 50000

Cash flow hedge reserve

(Other comprehensive income) 50000

(To reverse accumulated futures contract loss)

54

Introduction

Accounting standards

1) MFRS 139 Financial Instruments

Recognition and Measurement

2) MFRS 132 Financial Instruments

Presentation

3) MFRS 7 Financial Instruments Disclosures

MFRS 9 Financial Instruments (IFRS 9

issued by IASB in October 2010) (MFRS 139

will be superseded by MFRS 9)

2

Introduction

A financial instrument is any contract that gives

rise to a financial asset of one entity and a

financial liability or equity instrument of another

entity

Financial assets (MFRS 132 para 11)

Financial Liabilities (MFRS 132 para 11)

Financial instruments include primary instruments (such as receivables

payables and equity instruments) and

derivative financial instruments (such as financial

options futures and forwards interest rate swaps

and currency swaps)

3

Recognition amp Measurement

shall recognise a financial asset or a financial

liability in its statement of financial position

when and only when the entity becomes a party

to the contractual provisions of the instrument

Initial measurement - at its fair value

However a financial asset or financial liability not

at fair value through profit or loss should

measured at its fair value plus transaction costs

that are directly attributable to the acquisition or

issue of the financial asset or financial liability

(para 43)

4

Sebsequent Measurement

Financial Assets

Classifies into 4 categories (para 45)

1) A financial asset at lsquofair value through profit or lossrsquo comprises

i lsquoheld-for-tradingrsquo securities

ii rsquodesignatedrsquo securities

2) lsquoheld-to-maturityrsquo investment

3) lsquoloan amp receivablesrsquo

4) lsquoavailable-for-salersquo financial assets

Definition in MFRS 139 para 9

5

Sebsequent Measurement

Financial Liabilities

Measure either at (para 47)

1) Fair value through profit or loss or

2) Amortised costs using effective interest method

6

Derecognition

Financial Assets

An entity shall derecognise a financial asset

when and only when

(a) the contractual rights to the cash flows from

the financial asset expire or

(b) it transfers the financial asset as set out in

para 18 and 19 and the transfer qualifies for

derecognition in accordance with para 20

7

Derecognition

Financial Liabilities

An entity shall remove a financial liability (or a

part of a financial liability) from its statement of

financial position when and only when it is

extinguished

ie when the obligation specified in the contract is

discharged or cancelled or expires

8

HEDGE ACCOUNTING

9

Hedging

Companies are often exposed to risks of

fluctuations in the prices of currencies

commodities or securities that affect profit or

loss

For example companies with foreign currency

transactions are exposed to risk due to changes

in foreign currency exchange rates

Hedging is a risk management strategy used by

companies to manage risk exposures

10

Hedging

The two most common hedging instruments

used by companies are forward contracts and

option contracts

A forward contract is a contract that enables a

company to lock in the price at which it will buy

or sell a certain asset in the future

An option is a contract that grants the holder of

the option the right but not an obligation to buy

or sell a certain asset at a specified price during

a specified period

11

Hedge Accounting

Hedge accounting involves representation of the

effect of the risk management activities in the

financial statements

Hedge accounting specifies how gains or losses

on hedge instrument are to be accounted

12

Hedge Accounting

Hedge accounting allows profit or loss from

change in fair value of the hedged item and loss

and profit from the hedging instrument to be

offset during the same accounting period ndash thereby

reduces the volatility of profit or loss

Hedged item ndash asset liability firm commitment

forecast transaction or net investment in a foreign

operation that expose to risk of changes in fair

value

Hedge instrument ndash a derivative whose value is

expected to offset change in fair value of a hedged

item

13

Hedge Accounting

Hedge accounting is a special accounting amp is

permited under MFRS 139 if and only if all

the conditions in para 88 are met

Whether or not hedge and whether or not to

apply hedge accounting are two separate

issues

Hedge accounting is not compulsory

14

Hedge Accounting

Hedge Effectiveness

For hedge accounting to be used the hedge

must be expected to be highly effective gains

and losses on the hedging instrument is

expected to be almost fully offset losses and

gains on the item being hedged ndash within a

range of 80 to 125

15

Hedge Accounting

Hedge Effectiveness

Example (Ng Eng Juan page 1052)

Gain on hedging instrument RM100

Loss on hedged item RM 70

The hedge is ineffective as

70 100 = 70

100 70 = 143

16

Hedge Accounting

Hedge Effectiveness

Example (Ng Eng Juan page 1052)

Gain on hedging instrument RM100

Loss on hedged item RM90

The hedge is effective as

90 100 = 90

100 90 = 111

17

Hedge Accounting

Hedging of recognized foreign currency

assetsliabilities and hedging of foreign

currency commitments

The hedge is considered effective if the

currency type currency amount and

settlement date of the hedging instrument

match those of the hedge item

18

Hedge Accounting

Hedging accounting are categorized into 3

types (para 86)

(1) fair value hedge

(2) cash flow hedge

(3) hedge of a net investment in a foreign entity

19

Fair Value Hedge

A hedge to manage risk that can affect the fair valueof an asset or liability reported on the statement offinancial position

A hedge of the exposure to changes in fair value ofa recognised asset or liability or an unrecognisedfirm commitment or an identified portion of such anasset liability or firm commitment that is attributableto a particular risk and could affect profit or loss(para 86)

Example if a company has an account receivabledominated in foreign currency then the companyhas a fair value exposure as if the foreign currencydepreciates the company has to write down thereceivable

20

Fair Value Hedge

Accounting treatment (para 89)

a) the gain or loss from remeasuring the hedging instrument at fair value (for a derivative hedging instrument) or the foreign currency component of its carrying amount measured in accordance with MFRS 121 (for a non-derivative hedging instrument) shall be recognised in profit or loss and

b) the gain or loss on the hedged item attributable to the hedged risk shall adjust the carrying amount of the hedged item and be recognised in profit or loss

This applies if the hedged item is otherwise measured at cost Recognition of the gain or loss attributable to the hedged risk in profit or loss applies if the hedged item is an available-for-sale financial asset

21

Fair Value Hedge

On each reporting date

1 The hedge asset or liability is reported at fair

value Changes in fair value is recognized

through profit or loss

2 Hedging instrument is reported at fair value

- eg recognize forward contract an asset or

liability with the counterpart recognized as

again or loss through profit or loss

22

Example 1

M Bhd a Malaysian company sold goods to S acompany in Singapore for S$10000 on 1 April 2012Payment is to be received on 30 September 2012 Tohedge its exposure to foreign currency risk M enteredinto a forward contract with AAA Bank to deliverS$10000 on 30 September 2012 Financial year end ison 31 December The exchange rates are as follows

Date Spot Rate Forward Rate

(30 Sept 2012)

1 April 2012 RM220 = S$100 RM210 = S$100

30 Sept 2012 RM205 = S$100

23

Example 1

In this example the forward contract is

considered an effective hedge as the currency

amount and settlement date of the contract

match those of the hedged item

24

Example 1

Solution

1 April 2012

Accounts receivable (S$) 22000

Sales

22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

25

Example 1

30 Sept 2012

Foreign exchange loss 1500

Accounts receivable (S$) 1500

(To adjust the value of receivable to the new spot rate of RM205 10000 x (RM220 ndash RM205) = 1500)

Forward contract 500

Gain on forward contract 500

[To record the forward contract as an asset at its fair value of RM500 (10000 x (RM210 ndash RM205)]

26

Example 1

30 Sept 2012

Foreign currency (S$) 20500

Accounts receivable (S$)20500

(To record receipt of S$10000 from S at spot rate ofRM205)

Cash 21000

Foreign currency (S$) 20500

Forward contract 500

(To record settlement of contract ndash receipt of RM21000in exchange for S$10000)

27

Cash Flow Hedge

A hedge to manage risk that can affect the amount of

cash flow to be realized in the future

a hedge of the exposure to variability in cash flows that

1) is attributable to a particular risk associated with a

recognised asset or liability (such as all or some

future interest payments on variable rate debt) or a

highly probable forecast transaction and

2) could affect profit or loss

On each reporting date

Hedging instrument is reported at fair value - egrecognize forward contract an asset or liability with thecounterpart recognized as a cash flow hedge reserve(other comprehensive income)

28

Cash Flow Hedge

Accounting treatment (para 95)

a) the portion of the gain or loss on the hedging

instrument that is determined to be an effective

hedge (see paragraph 88) shall be recognised

in other comprehensive income and

b) the ineffective portion of the gain or loss on the

hedging instrument shall be recognised in profit

or loss

29

Hedges of a net investment

Hedges of a net investment in a foreign operation (ie

the amount of the reporting entityrsquos interest in the net

assets of that operation) including a hedge of a

monetary item that is accounted for as part of the net

investment (see MFRS 121)

shall be accounted for similarly to cash flow hedges (para 102)

a) the portion of the gain or loss on the hedging instrument that is determined to be an effective hedge (see paragraph 88) shall be recognised in other comprehensive income and

b) the ineffective portion shall be recognised in profit or loss

30

Example 2

M Bhd a Malaysian company sold goods to S acompany in Singapore for S$10000 on 1 December2012 Payment is to be received on 1 March 2013 Tohedge its exposure to foreign currency risk M enteredinto a forward contract with AAA Bank to deliverS$10000 on 1 March 2013 Financial year end is on 31December The exchange rates are as follows

Date Spot Rate ForwardRate

(1 March 2013)

1 Dec 2012 RM220 = S$100 RM210 =S$100

31 Dec 2012 RM215 = S$100 RM200 = S$100

1 March 2013 RM185 = S$100

31

Fair Value Hedge

1 Dec 2012

Accounts receivable (S$) 22000

Sales 22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

32

Fair Value Hedge

31 Dec 2012

Foreign exchange loss 500

Accounts receivable (S$) 500

(To adjust the value of receivable to the new spot rate

10000 x RM220 ndash RM215)

Forward contract 980

Gain on forward contract 980

[To record forward contract as an asset at its fair value

10000 x (210 ndash 200) = 1000 Present value = 1000 x

0980 = 980 Assume M has an incremental borrowing rate

of 12 per year (1 per month)]

33

Fair Value Hedge

1 March 2013

Foreign exchange loss 3000

Accounts receivable (S$)3000

(To adjust the value of receivable to the new spotrate - 10000 x RM215 ndash RM185)

Forward contract 1520

Gain on forward contract 1520

[To adjust the value of forward contract to its currentfair value of RM2500 (10000 x (210 ndash 185)RM2500 ndash RM980 = RM1520]

34

Fair Value Hedge

1 March 2013

Foreign currency (S$) 18500

Accounts receivable (S$)

18500

(To record receipt of S$10000 from S at spot rate of

RM185)

Cash 21000

Foreign currency (S$) 18500

Forward contract 2500

(To record settlement of contract ndash receipt of RM21000 in

exchange for S$10000)

35

Cash Flow Hedge

1 Dec 2012

Accounts receivable (S$) 22000

Sales 22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

36

Cash Flow Hedge

31 Dec 2012

Foreign exchange loss 500

Accounts receivable (S$) 500

(To adjust the value of receivable to the new spot rate

10000 x RM220 ndash RM215)

Forward contract 1000

Cash flow hedge reserve

(Other comprehensive income) 1000

[To record forward contract as an asset at its fair value

10000 x (210 ndash 200) = 1000 Present value = 1000 x

0980 = 980 Assume M has an incremental borrowing rate

of 12 per year (1 per month]

37

Cash Flow Hedge

31 Dec 2012

Cash flow hedge reserve

(Other comprehensive income) 500

Gain on forward contract 500

(To offset the foreign exchange loss)

Discount expense 333

Cash flow hedge reserve

(Other comprehensive income) 333

(To record discount expense 10000 x (220 spot rate on 1 Dec

minus 210 forward rate on 1 Dec x 13 - using straight line

method)

the cost of extending credit to S as S$ sold at discount in the 3

month forward market

38

Cash Flow Hedge

1 March 2013

Foreign exchange loss 3000

Accounts receivable (S$) 3000

(To adjust the value of receivable to the new spot rate ndash10000 x RM215 ndash RM1855)

Forward contract 1520

Cash flow hedge reserve

(Other comprehensive income) 1520

[To adjust the value of forward contract to its current fairvalue of RM2500 (10000 x (210 ndash 185) RM2500 ndashRM980 = RM1520]

39

Cash Flow Hedge

1 March 2013

Cash flow hedge reserve

(Other comprehensive income) 3000

Gain on forward contract3000

(To offset the foreign exchange loss)

Discount expense 667

Cash flow hedge reserve

(Other comprehensive income) 667

(To record discount expense ndash the cost of extending creditto S 10000 x (220 spot rate on 1 Dec minus 210 forwardrate on 1 Dec) x 23 ndash using straight line method)

40

Cash Flow Hedge

1 March 2013

Foreign currency (S$) 18500

Accounts receivable (S$)18500

(To record receipt of S$10000 from S at spot rate ofRM185)

Cash 21000

Foreign currency (S$) 18500

Forward contract 2500

(To record settlement of contract ndash receipt of RM21000in exchange for S$10000)

41

Example 3 ndash Hedge of Probable

Forecast Transaction (Future

Sale)(refer page 1087 of Ng Eng Juan (2012) Q5)

On 1 April 20X8 ABC has 10 metric tons of tin

inventory carried at cost of RM22000 per metric

ton (total cost = RM220000)

Intends to sell the tin inventory on 30 June 20X8

On 1 April ABC enters into a futures contract to

sell 10 metric tons of tins at RM30000 per

metric ton on 30 June 20X8

42

Example 3

Date Spot price Futures price

(30 June 20X8)

1 April 20X8 RM29000 RM30000

30 April 20X8 RM31000 RM32000

31 May 20X8 RM33300 RM34500

30 June 20X8 RM35000

43

Example 3 - No Hedge

Accounting

30 April

Loss on futures contract 20000

Futures contract 20000

[To record futures contract as a liability at its fair value ndash 10 x (RM32000 ndash RM30000)]

31 May

Loss on futures contract 25000

Futures contract 25000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM34500 ndashRM32000)]

44

Example 3 - No Hedge

Accounting

30 June

Loss on futures contract 5000

Futures contract 5000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM35000 ndashRM34500)]

Futures contract 50000

Cash 50000

(To record settlement of futures contract)

45

Example 3 - No Hedge

Accounting

30 June

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

46

Example 3 ndash Fair Value Hedge

In a fair value hedge the carrying amount of

the hedged item should be adjusted for the

gain or loss attributable to the hedged risk

even if the hedged item is otherwise measured

at cost as required by other relevant MFRS

The gain or loss on the hedged item should be

recognized in profit or loss

47

Example 3 ndash Fair Value Hedge

30 April

Inventory 20000

Gain on revaluation of inventory

20000

(To adjust inventory to its current fair value ndash 10 x

(RM31000 ndash RM29000)

Loss on futures contract 20000

Futures contract 20000

[To record futures contract as a liability at its fair value ndash 10

x (RM32000 ndash RM30000)]

48

Example 3 ndash Fair Value Hedge

31 May

Inventory 23000

Gain on revaluation of inventory 23000

(To adjust inventory to its current fair value ndash 10 x(RM33300 ndash RM31000)

Loss on futures contract 25000

Futures contract25000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM34500 ndash RM32000)]

49

Example 3 ndash Fair Value Hedge

30 June

Inventory 17000

Gain on revaluation of inventory 17000

(To adjust inventory to its current fair value ndash 10 x(RM35000 ndash RM33300)

Loss on futures contract 5000

Futures contract5000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM35000 ndash RM34500)]

50

Example 3 ndash Fair Value Hedge

30 June

Futures contract 50000

Cash50000

(To record settlement of futures contract)

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

51

Example 3 ndash Cash Flow

Hedge30 April

Cash flow hedge reserve

(Other comprehensive income) 20000

Futures contract20000

31 May

Cash flow hedge reserve

(Other comprehensive income) 25000

Futures contract25000

52

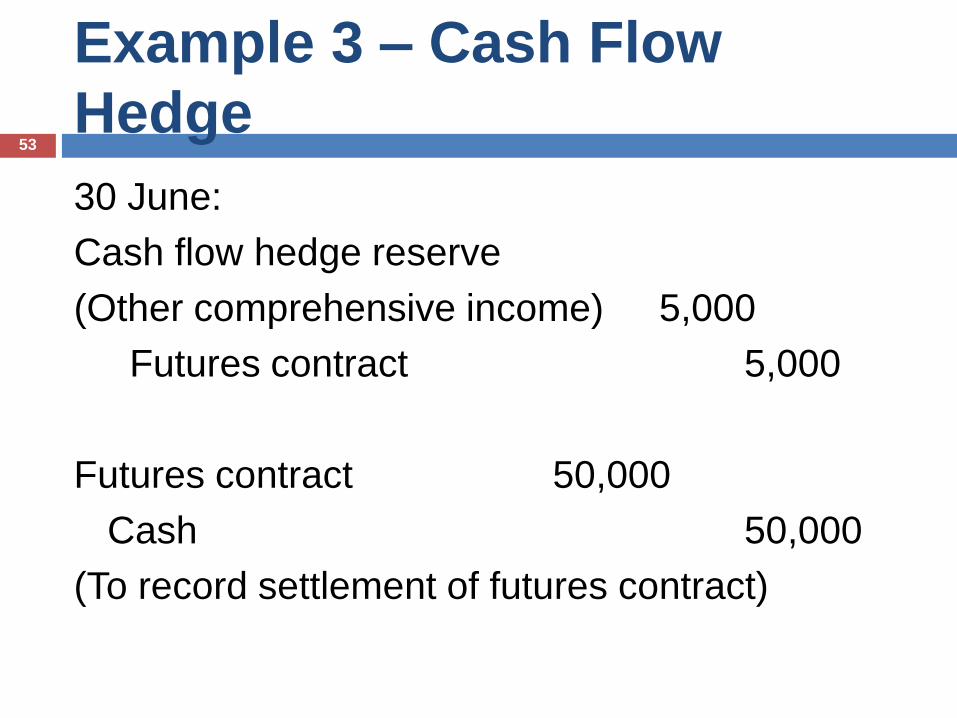

Example 3 ndash Cash Flow

Hedge

30 June

Cash flow hedge reserve

(Other comprehensive income) 5000

Futures contract 5000

Futures contract 50000

Cash 50000

(To record settlement of futures contract)

53

Example 3 ndash Cash Flow

Hedge30 June

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

Sales 50000

Cash flow hedge reserve

(Other comprehensive income) 50000

(To reverse accumulated futures contract loss)

54

Introduction

A financial instrument is any contract that gives

rise to a financial asset of one entity and a

financial liability or equity instrument of another

entity

Financial assets (MFRS 132 para 11)

Financial Liabilities (MFRS 132 para 11)

Financial instruments include primary instruments (such as receivables

payables and equity instruments) and

derivative financial instruments (such as financial

options futures and forwards interest rate swaps

and currency swaps)

3

Recognition amp Measurement

shall recognise a financial asset or a financial

liability in its statement of financial position

when and only when the entity becomes a party

to the contractual provisions of the instrument

Initial measurement - at its fair value

However a financial asset or financial liability not

at fair value through profit or loss should

measured at its fair value plus transaction costs

that are directly attributable to the acquisition or

issue of the financial asset or financial liability

(para 43)

4

Sebsequent Measurement

Financial Assets

Classifies into 4 categories (para 45)

1) A financial asset at lsquofair value through profit or lossrsquo comprises

i lsquoheld-for-tradingrsquo securities

ii rsquodesignatedrsquo securities

2) lsquoheld-to-maturityrsquo investment

3) lsquoloan amp receivablesrsquo

4) lsquoavailable-for-salersquo financial assets

Definition in MFRS 139 para 9

5

Sebsequent Measurement

Financial Liabilities

Measure either at (para 47)

1) Fair value through profit or loss or

2) Amortised costs using effective interest method

6

Derecognition

Financial Assets

An entity shall derecognise a financial asset

when and only when

(a) the contractual rights to the cash flows from

the financial asset expire or

(b) it transfers the financial asset as set out in

para 18 and 19 and the transfer qualifies for

derecognition in accordance with para 20

7

Derecognition

Financial Liabilities

An entity shall remove a financial liability (or a

part of a financial liability) from its statement of

financial position when and only when it is

extinguished

ie when the obligation specified in the contract is

discharged or cancelled or expires

8

HEDGE ACCOUNTING

9

Hedging

Companies are often exposed to risks of

fluctuations in the prices of currencies

commodities or securities that affect profit or

loss

For example companies with foreign currency

transactions are exposed to risk due to changes

in foreign currency exchange rates

Hedging is a risk management strategy used by

companies to manage risk exposures

10

Hedging

The two most common hedging instruments

used by companies are forward contracts and

option contracts

A forward contract is a contract that enables a

company to lock in the price at which it will buy

or sell a certain asset in the future

An option is a contract that grants the holder of

the option the right but not an obligation to buy

or sell a certain asset at a specified price during

a specified period

11

Hedge Accounting

Hedge accounting involves representation of the

effect of the risk management activities in the

financial statements

Hedge accounting specifies how gains or losses

on hedge instrument are to be accounted

12

Hedge Accounting

Hedge accounting allows profit or loss from

change in fair value of the hedged item and loss

and profit from the hedging instrument to be

offset during the same accounting period ndash thereby

reduces the volatility of profit or loss

Hedged item ndash asset liability firm commitment

forecast transaction or net investment in a foreign

operation that expose to risk of changes in fair

value

Hedge instrument ndash a derivative whose value is

expected to offset change in fair value of a hedged

item

13

Hedge Accounting

Hedge accounting is a special accounting amp is

permited under MFRS 139 if and only if all

the conditions in para 88 are met

Whether or not hedge and whether or not to

apply hedge accounting are two separate

issues

Hedge accounting is not compulsory

14

Hedge Accounting

Hedge Effectiveness

For hedge accounting to be used the hedge

must be expected to be highly effective gains

and losses on the hedging instrument is

expected to be almost fully offset losses and

gains on the item being hedged ndash within a

range of 80 to 125

15

Hedge Accounting

Hedge Effectiveness

Example (Ng Eng Juan page 1052)

Gain on hedging instrument RM100

Loss on hedged item RM 70

The hedge is ineffective as

70 100 = 70

100 70 = 143

16

Hedge Accounting

Hedge Effectiveness

Example (Ng Eng Juan page 1052)

Gain on hedging instrument RM100

Loss on hedged item RM90

The hedge is effective as

90 100 = 90

100 90 = 111

17

Hedge Accounting

Hedging of recognized foreign currency

assetsliabilities and hedging of foreign

currency commitments

The hedge is considered effective if the

currency type currency amount and

settlement date of the hedging instrument

match those of the hedge item

18

Hedge Accounting

Hedging accounting are categorized into 3

types (para 86)

(1) fair value hedge

(2) cash flow hedge

(3) hedge of a net investment in a foreign entity

19

Fair Value Hedge

A hedge to manage risk that can affect the fair valueof an asset or liability reported on the statement offinancial position

A hedge of the exposure to changes in fair value ofa recognised asset or liability or an unrecognisedfirm commitment or an identified portion of such anasset liability or firm commitment that is attributableto a particular risk and could affect profit or loss(para 86)

Example if a company has an account receivabledominated in foreign currency then the companyhas a fair value exposure as if the foreign currencydepreciates the company has to write down thereceivable

20

Fair Value Hedge

Accounting treatment (para 89)

a) the gain or loss from remeasuring the hedging instrument at fair value (for a derivative hedging instrument) or the foreign currency component of its carrying amount measured in accordance with MFRS 121 (for a non-derivative hedging instrument) shall be recognised in profit or loss and

b) the gain or loss on the hedged item attributable to the hedged risk shall adjust the carrying amount of the hedged item and be recognised in profit or loss

This applies if the hedged item is otherwise measured at cost Recognition of the gain or loss attributable to the hedged risk in profit or loss applies if the hedged item is an available-for-sale financial asset

21

Fair Value Hedge

On each reporting date

1 The hedge asset or liability is reported at fair

value Changes in fair value is recognized

through profit or loss

2 Hedging instrument is reported at fair value

- eg recognize forward contract an asset or

liability with the counterpart recognized as

again or loss through profit or loss

22

Example 1

M Bhd a Malaysian company sold goods to S acompany in Singapore for S$10000 on 1 April 2012Payment is to be received on 30 September 2012 Tohedge its exposure to foreign currency risk M enteredinto a forward contract with AAA Bank to deliverS$10000 on 30 September 2012 Financial year end ison 31 December The exchange rates are as follows

Date Spot Rate Forward Rate

(30 Sept 2012)

1 April 2012 RM220 = S$100 RM210 = S$100

30 Sept 2012 RM205 = S$100

23

Example 1

In this example the forward contract is

considered an effective hedge as the currency

amount and settlement date of the contract

match those of the hedged item

24

Example 1

Solution

1 April 2012

Accounts receivable (S$) 22000

Sales

22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

25

Example 1

30 Sept 2012

Foreign exchange loss 1500

Accounts receivable (S$) 1500

(To adjust the value of receivable to the new spot rate of RM205 10000 x (RM220 ndash RM205) = 1500)

Forward contract 500

Gain on forward contract 500

[To record the forward contract as an asset at its fair value of RM500 (10000 x (RM210 ndash RM205)]

26

Example 1

30 Sept 2012

Foreign currency (S$) 20500

Accounts receivable (S$)20500

(To record receipt of S$10000 from S at spot rate ofRM205)

Cash 21000

Foreign currency (S$) 20500

Forward contract 500

(To record settlement of contract ndash receipt of RM21000in exchange for S$10000)

27

Cash Flow Hedge

A hedge to manage risk that can affect the amount of

cash flow to be realized in the future

a hedge of the exposure to variability in cash flows that

1) is attributable to a particular risk associated with a

recognised asset or liability (such as all or some

future interest payments on variable rate debt) or a

highly probable forecast transaction and

2) could affect profit or loss

On each reporting date

Hedging instrument is reported at fair value - egrecognize forward contract an asset or liability with thecounterpart recognized as a cash flow hedge reserve(other comprehensive income)

28

Cash Flow Hedge

Accounting treatment (para 95)

a) the portion of the gain or loss on the hedging

instrument that is determined to be an effective

hedge (see paragraph 88) shall be recognised

in other comprehensive income and

b) the ineffective portion of the gain or loss on the

hedging instrument shall be recognised in profit

or loss

29

Hedges of a net investment

Hedges of a net investment in a foreign operation (ie

the amount of the reporting entityrsquos interest in the net

assets of that operation) including a hedge of a

monetary item that is accounted for as part of the net

investment (see MFRS 121)

shall be accounted for similarly to cash flow hedges (para 102)

a) the portion of the gain or loss on the hedging instrument that is determined to be an effective hedge (see paragraph 88) shall be recognised in other comprehensive income and

b) the ineffective portion shall be recognised in profit or loss

30

Example 2

M Bhd a Malaysian company sold goods to S acompany in Singapore for S$10000 on 1 December2012 Payment is to be received on 1 March 2013 Tohedge its exposure to foreign currency risk M enteredinto a forward contract with AAA Bank to deliverS$10000 on 1 March 2013 Financial year end is on 31December The exchange rates are as follows

Date Spot Rate ForwardRate

(1 March 2013)

1 Dec 2012 RM220 = S$100 RM210 =S$100

31 Dec 2012 RM215 = S$100 RM200 = S$100

1 March 2013 RM185 = S$100

31

Fair Value Hedge

1 Dec 2012

Accounts receivable (S$) 22000

Sales 22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

32

Fair Value Hedge

31 Dec 2012

Foreign exchange loss 500

Accounts receivable (S$) 500

(To adjust the value of receivable to the new spot rate

10000 x RM220 ndash RM215)

Forward contract 980

Gain on forward contract 980

[To record forward contract as an asset at its fair value

10000 x (210 ndash 200) = 1000 Present value = 1000 x

0980 = 980 Assume M has an incremental borrowing rate

of 12 per year (1 per month)]

33

Fair Value Hedge

1 March 2013

Foreign exchange loss 3000

Accounts receivable (S$)3000

(To adjust the value of receivable to the new spotrate - 10000 x RM215 ndash RM185)

Forward contract 1520

Gain on forward contract 1520

[To adjust the value of forward contract to its currentfair value of RM2500 (10000 x (210 ndash 185)RM2500 ndash RM980 = RM1520]

34

Fair Value Hedge

1 March 2013

Foreign currency (S$) 18500

Accounts receivable (S$)

18500

(To record receipt of S$10000 from S at spot rate of

RM185)

Cash 21000

Foreign currency (S$) 18500

Forward contract 2500

(To record settlement of contract ndash receipt of RM21000 in

exchange for S$10000)

35

Cash Flow Hedge

1 Dec 2012

Accounts receivable (S$) 22000

Sales 22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

36

Cash Flow Hedge

31 Dec 2012

Foreign exchange loss 500

Accounts receivable (S$) 500

(To adjust the value of receivable to the new spot rate

10000 x RM220 ndash RM215)

Forward contract 1000

Cash flow hedge reserve

(Other comprehensive income) 1000

[To record forward contract as an asset at its fair value

10000 x (210 ndash 200) = 1000 Present value = 1000 x

0980 = 980 Assume M has an incremental borrowing rate

of 12 per year (1 per month]

37

Cash Flow Hedge

31 Dec 2012

Cash flow hedge reserve

(Other comprehensive income) 500

Gain on forward contract 500

(To offset the foreign exchange loss)

Discount expense 333

Cash flow hedge reserve

(Other comprehensive income) 333

(To record discount expense 10000 x (220 spot rate on 1 Dec

minus 210 forward rate on 1 Dec x 13 - using straight line

method)

the cost of extending credit to S as S$ sold at discount in the 3

month forward market

38

Cash Flow Hedge

1 March 2013

Foreign exchange loss 3000

Accounts receivable (S$) 3000

(To adjust the value of receivable to the new spot rate ndash10000 x RM215 ndash RM1855)

Forward contract 1520

Cash flow hedge reserve

(Other comprehensive income) 1520

[To adjust the value of forward contract to its current fairvalue of RM2500 (10000 x (210 ndash 185) RM2500 ndashRM980 = RM1520]

39

Cash Flow Hedge

1 March 2013

Cash flow hedge reserve

(Other comprehensive income) 3000

Gain on forward contract3000

(To offset the foreign exchange loss)

Discount expense 667

Cash flow hedge reserve

(Other comprehensive income) 667

(To record discount expense ndash the cost of extending creditto S 10000 x (220 spot rate on 1 Dec minus 210 forwardrate on 1 Dec) x 23 ndash using straight line method)

40

Cash Flow Hedge

1 March 2013

Foreign currency (S$) 18500

Accounts receivable (S$)18500

(To record receipt of S$10000 from S at spot rate ofRM185)

Cash 21000

Foreign currency (S$) 18500

Forward contract 2500

(To record settlement of contract ndash receipt of RM21000in exchange for S$10000)

41

Example 3 ndash Hedge of Probable

Forecast Transaction (Future

Sale)(refer page 1087 of Ng Eng Juan (2012) Q5)

On 1 April 20X8 ABC has 10 metric tons of tin

inventory carried at cost of RM22000 per metric

ton (total cost = RM220000)

Intends to sell the tin inventory on 30 June 20X8

On 1 April ABC enters into a futures contract to

sell 10 metric tons of tins at RM30000 per

metric ton on 30 June 20X8

42

Example 3

Date Spot price Futures price

(30 June 20X8)

1 April 20X8 RM29000 RM30000

30 April 20X8 RM31000 RM32000

31 May 20X8 RM33300 RM34500

30 June 20X8 RM35000

43

Example 3 - No Hedge

Accounting

30 April

Loss on futures contract 20000

Futures contract 20000

[To record futures contract as a liability at its fair value ndash 10 x (RM32000 ndash RM30000)]

31 May

Loss on futures contract 25000

Futures contract 25000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM34500 ndashRM32000)]

44

Example 3 - No Hedge

Accounting

30 June

Loss on futures contract 5000

Futures contract 5000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM35000 ndashRM34500)]

Futures contract 50000

Cash 50000

(To record settlement of futures contract)

45

Example 3 - No Hedge

Accounting

30 June

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

46

Example 3 ndash Fair Value Hedge

In a fair value hedge the carrying amount of

the hedged item should be adjusted for the

gain or loss attributable to the hedged risk

even if the hedged item is otherwise measured

at cost as required by other relevant MFRS

The gain or loss on the hedged item should be

recognized in profit or loss

47

Example 3 ndash Fair Value Hedge

30 April

Inventory 20000

Gain on revaluation of inventory

20000

(To adjust inventory to its current fair value ndash 10 x

(RM31000 ndash RM29000)

Loss on futures contract 20000

Futures contract 20000

[To record futures contract as a liability at its fair value ndash 10

x (RM32000 ndash RM30000)]

48

Example 3 ndash Fair Value Hedge

31 May

Inventory 23000

Gain on revaluation of inventory 23000

(To adjust inventory to its current fair value ndash 10 x(RM33300 ndash RM31000)

Loss on futures contract 25000

Futures contract25000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM34500 ndash RM32000)]

49

Example 3 ndash Fair Value Hedge

30 June

Inventory 17000

Gain on revaluation of inventory 17000

(To adjust inventory to its current fair value ndash 10 x(RM35000 ndash RM33300)

Loss on futures contract 5000

Futures contract5000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM35000 ndash RM34500)]

50

Example 3 ndash Fair Value Hedge

30 June

Futures contract 50000

Cash50000

(To record settlement of futures contract)

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

51

Example 3 ndash Cash Flow

Hedge30 April

Cash flow hedge reserve

(Other comprehensive income) 20000

Futures contract20000

31 May

Cash flow hedge reserve

(Other comprehensive income) 25000

Futures contract25000

52

Example 3 ndash Cash Flow

Hedge

30 June

Cash flow hedge reserve

(Other comprehensive income) 5000

Futures contract 5000

Futures contract 50000

Cash 50000

(To record settlement of futures contract)

53

Example 3 ndash Cash Flow

Hedge30 June

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

Sales 50000

Cash flow hedge reserve

(Other comprehensive income) 50000

(To reverse accumulated futures contract loss)

54

Recognition amp Measurement

shall recognise a financial asset or a financial

liability in its statement of financial position

when and only when the entity becomes a party

to the contractual provisions of the instrument

Initial measurement - at its fair value

However a financial asset or financial liability not

at fair value through profit or loss should

measured at its fair value plus transaction costs

that are directly attributable to the acquisition or

issue of the financial asset or financial liability

(para 43)

4

Sebsequent Measurement

Financial Assets

Classifies into 4 categories (para 45)

1) A financial asset at lsquofair value through profit or lossrsquo comprises

i lsquoheld-for-tradingrsquo securities

ii rsquodesignatedrsquo securities

2) lsquoheld-to-maturityrsquo investment

3) lsquoloan amp receivablesrsquo

4) lsquoavailable-for-salersquo financial assets

Definition in MFRS 139 para 9

5

Sebsequent Measurement

Financial Liabilities

Measure either at (para 47)

1) Fair value through profit or loss or

2) Amortised costs using effective interest method

6

Derecognition

Financial Assets

An entity shall derecognise a financial asset

when and only when

(a) the contractual rights to the cash flows from

the financial asset expire or

(b) it transfers the financial asset as set out in

para 18 and 19 and the transfer qualifies for

derecognition in accordance with para 20

7

Derecognition

Financial Liabilities

An entity shall remove a financial liability (or a

part of a financial liability) from its statement of

financial position when and only when it is

extinguished

ie when the obligation specified in the contract is

discharged or cancelled or expires

8

HEDGE ACCOUNTING

9

Hedging

Companies are often exposed to risks of

fluctuations in the prices of currencies

commodities or securities that affect profit or

loss

For example companies with foreign currency

transactions are exposed to risk due to changes

in foreign currency exchange rates

Hedging is a risk management strategy used by

companies to manage risk exposures

10

Hedging

The two most common hedging instruments

used by companies are forward contracts and

option contracts

A forward contract is a contract that enables a

company to lock in the price at which it will buy

or sell a certain asset in the future

An option is a contract that grants the holder of

the option the right but not an obligation to buy

or sell a certain asset at a specified price during

a specified period

11

Hedge Accounting

Hedge accounting involves representation of the

effect of the risk management activities in the

financial statements

Hedge accounting specifies how gains or losses

on hedge instrument are to be accounted

12

Hedge Accounting

Hedge accounting allows profit or loss from

change in fair value of the hedged item and loss

and profit from the hedging instrument to be

offset during the same accounting period ndash thereby

reduces the volatility of profit or loss

Hedged item ndash asset liability firm commitment

forecast transaction or net investment in a foreign

operation that expose to risk of changes in fair

value

Hedge instrument ndash a derivative whose value is

expected to offset change in fair value of a hedged

item

13

Hedge Accounting

Hedge accounting is a special accounting amp is

permited under MFRS 139 if and only if all

the conditions in para 88 are met

Whether or not hedge and whether or not to

apply hedge accounting are two separate

issues

Hedge accounting is not compulsory

14

Hedge Accounting

Hedge Effectiveness

For hedge accounting to be used the hedge

must be expected to be highly effective gains

and losses on the hedging instrument is

expected to be almost fully offset losses and

gains on the item being hedged ndash within a

range of 80 to 125

15

Hedge Accounting

Hedge Effectiveness

Example (Ng Eng Juan page 1052)

Gain on hedging instrument RM100

Loss on hedged item RM 70

The hedge is ineffective as

70 100 = 70

100 70 = 143

16

Hedge Accounting

Hedge Effectiveness

Example (Ng Eng Juan page 1052)

Gain on hedging instrument RM100

Loss on hedged item RM90

The hedge is effective as

90 100 = 90

100 90 = 111

17

Hedge Accounting

Hedging of recognized foreign currency

assetsliabilities and hedging of foreign

currency commitments

The hedge is considered effective if the

currency type currency amount and

settlement date of the hedging instrument

match those of the hedge item

18

Hedge Accounting

Hedging accounting are categorized into 3

types (para 86)

(1) fair value hedge

(2) cash flow hedge

(3) hedge of a net investment in a foreign entity

19

Fair Value Hedge

A hedge to manage risk that can affect the fair valueof an asset or liability reported on the statement offinancial position

A hedge of the exposure to changes in fair value ofa recognised asset or liability or an unrecognisedfirm commitment or an identified portion of such anasset liability or firm commitment that is attributableto a particular risk and could affect profit or loss(para 86)

Example if a company has an account receivabledominated in foreign currency then the companyhas a fair value exposure as if the foreign currencydepreciates the company has to write down thereceivable

20

Fair Value Hedge

Accounting treatment (para 89)

a) the gain or loss from remeasuring the hedging instrument at fair value (for a derivative hedging instrument) or the foreign currency component of its carrying amount measured in accordance with MFRS 121 (for a non-derivative hedging instrument) shall be recognised in profit or loss and

b) the gain or loss on the hedged item attributable to the hedged risk shall adjust the carrying amount of the hedged item and be recognised in profit or loss

This applies if the hedged item is otherwise measured at cost Recognition of the gain or loss attributable to the hedged risk in profit or loss applies if the hedged item is an available-for-sale financial asset

21

Fair Value Hedge

On each reporting date

1 The hedge asset or liability is reported at fair

value Changes in fair value is recognized

through profit or loss

2 Hedging instrument is reported at fair value

- eg recognize forward contract an asset or

liability with the counterpart recognized as

again or loss through profit or loss

22

Example 1

M Bhd a Malaysian company sold goods to S acompany in Singapore for S$10000 on 1 April 2012Payment is to be received on 30 September 2012 Tohedge its exposure to foreign currency risk M enteredinto a forward contract with AAA Bank to deliverS$10000 on 30 September 2012 Financial year end ison 31 December The exchange rates are as follows

Date Spot Rate Forward Rate

(30 Sept 2012)

1 April 2012 RM220 = S$100 RM210 = S$100

30 Sept 2012 RM205 = S$100

23

Example 1

In this example the forward contract is

considered an effective hedge as the currency

amount and settlement date of the contract

match those of the hedged item

24

Example 1

Solution

1 April 2012

Accounts receivable (S$) 22000

Sales

22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

25

Example 1

30 Sept 2012

Foreign exchange loss 1500

Accounts receivable (S$) 1500

(To adjust the value of receivable to the new spot rate of RM205 10000 x (RM220 ndash RM205) = 1500)

Forward contract 500

Gain on forward contract 500

[To record the forward contract as an asset at its fair value of RM500 (10000 x (RM210 ndash RM205)]

26

Example 1

30 Sept 2012

Foreign currency (S$) 20500

Accounts receivable (S$)20500

(To record receipt of S$10000 from S at spot rate ofRM205)

Cash 21000

Foreign currency (S$) 20500

Forward contract 500

(To record settlement of contract ndash receipt of RM21000in exchange for S$10000)

27

Cash Flow Hedge

A hedge to manage risk that can affect the amount of

cash flow to be realized in the future

a hedge of the exposure to variability in cash flows that

1) is attributable to a particular risk associated with a

recognised asset or liability (such as all or some

future interest payments on variable rate debt) or a

highly probable forecast transaction and

2) could affect profit or loss

On each reporting date

Hedging instrument is reported at fair value - egrecognize forward contract an asset or liability with thecounterpart recognized as a cash flow hedge reserve(other comprehensive income)

28

Cash Flow Hedge

Accounting treatment (para 95)

a) the portion of the gain or loss on the hedging

instrument that is determined to be an effective

hedge (see paragraph 88) shall be recognised

in other comprehensive income and

b) the ineffective portion of the gain or loss on the

hedging instrument shall be recognised in profit

or loss

29

Hedges of a net investment

Hedges of a net investment in a foreign operation (ie

the amount of the reporting entityrsquos interest in the net

assets of that operation) including a hedge of a

monetary item that is accounted for as part of the net

investment (see MFRS 121)

shall be accounted for similarly to cash flow hedges (para 102)

a) the portion of the gain or loss on the hedging instrument that is determined to be an effective hedge (see paragraph 88) shall be recognised in other comprehensive income and

b) the ineffective portion shall be recognised in profit or loss

30

Example 2

M Bhd a Malaysian company sold goods to S acompany in Singapore for S$10000 on 1 December2012 Payment is to be received on 1 March 2013 Tohedge its exposure to foreign currency risk M enteredinto a forward contract with AAA Bank to deliverS$10000 on 1 March 2013 Financial year end is on 31December The exchange rates are as follows

Date Spot Rate ForwardRate

(1 March 2013)

1 Dec 2012 RM220 = S$100 RM210 =S$100

31 Dec 2012 RM215 = S$100 RM200 = S$100

1 March 2013 RM185 = S$100

31

Fair Value Hedge

1 Dec 2012

Accounts receivable (S$) 22000

Sales 22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

32

Fair Value Hedge

31 Dec 2012

Foreign exchange loss 500

Accounts receivable (S$) 500

(To adjust the value of receivable to the new spot rate

10000 x RM220 ndash RM215)

Forward contract 980

Gain on forward contract 980

[To record forward contract as an asset at its fair value

10000 x (210 ndash 200) = 1000 Present value = 1000 x

0980 = 980 Assume M has an incremental borrowing rate

of 12 per year (1 per month)]

33

Fair Value Hedge

1 March 2013

Foreign exchange loss 3000

Accounts receivable (S$)3000

(To adjust the value of receivable to the new spotrate - 10000 x RM215 ndash RM185)

Forward contract 1520

Gain on forward contract 1520

[To adjust the value of forward contract to its currentfair value of RM2500 (10000 x (210 ndash 185)RM2500 ndash RM980 = RM1520]

34

Fair Value Hedge

1 March 2013

Foreign currency (S$) 18500

Accounts receivable (S$)

18500

(To record receipt of S$10000 from S at spot rate of

RM185)

Cash 21000

Foreign currency (S$) 18500

Forward contract 2500

(To record settlement of contract ndash receipt of RM21000 in

exchange for S$10000)

35

Cash Flow Hedge

1 Dec 2012

Accounts receivable (S$) 22000

Sales 22000

(To record sales of S$10000 at spot rate of

RM220)

No journal entry for forward contract when the

contract was entered

36

Cash Flow Hedge

31 Dec 2012

Foreign exchange loss 500

Accounts receivable (S$) 500

(To adjust the value of receivable to the new spot rate

10000 x RM220 ndash RM215)

Forward contract 1000

Cash flow hedge reserve

(Other comprehensive income) 1000

[To record forward contract as an asset at its fair value

10000 x (210 ndash 200) = 1000 Present value = 1000 x

0980 = 980 Assume M has an incremental borrowing rate

of 12 per year (1 per month]

37

Cash Flow Hedge

31 Dec 2012

Cash flow hedge reserve

(Other comprehensive income) 500

Gain on forward contract 500

(To offset the foreign exchange loss)

Discount expense 333

Cash flow hedge reserve

(Other comprehensive income) 333

(To record discount expense 10000 x (220 spot rate on 1 Dec

minus 210 forward rate on 1 Dec x 13 - using straight line

method)

the cost of extending credit to S as S$ sold at discount in the 3

month forward market

38

Cash Flow Hedge

1 March 2013

Foreign exchange loss 3000

Accounts receivable (S$) 3000

(To adjust the value of receivable to the new spot rate ndash10000 x RM215 ndash RM1855)

Forward contract 1520

Cash flow hedge reserve

(Other comprehensive income) 1520

[To adjust the value of forward contract to its current fairvalue of RM2500 (10000 x (210 ndash 185) RM2500 ndashRM980 = RM1520]

39

Cash Flow Hedge

1 March 2013

Cash flow hedge reserve

(Other comprehensive income) 3000

Gain on forward contract3000

(To offset the foreign exchange loss)

Discount expense 667

Cash flow hedge reserve

(Other comprehensive income) 667

(To record discount expense ndash the cost of extending creditto S 10000 x (220 spot rate on 1 Dec minus 210 forwardrate on 1 Dec) x 23 ndash using straight line method)

40

Cash Flow Hedge

1 March 2013

Foreign currency (S$) 18500

Accounts receivable (S$)18500

(To record receipt of S$10000 from S at spot rate ofRM185)

Cash 21000

Foreign currency (S$) 18500

Forward contract 2500

(To record settlement of contract ndash receipt of RM21000in exchange for S$10000)

41

Example 3 ndash Hedge of Probable

Forecast Transaction (Future

Sale)(refer page 1087 of Ng Eng Juan (2012) Q5)

On 1 April 20X8 ABC has 10 metric tons of tin

inventory carried at cost of RM22000 per metric

ton (total cost = RM220000)

Intends to sell the tin inventory on 30 June 20X8

On 1 April ABC enters into a futures contract to

sell 10 metric tons of tins at RM30000 per

metric ton on 30 June 20X8

42

Example 3

Date Spot price Futures price

(30 June 20X8)

1 April 20X8 RM29000 RM30000

30 April 20X8 RM31000 RM32000

31 May 20X8 RM33300 RM34500

30 June 20X8 RM35000

43

Example 3 - No Hedge

Accounting

30 April

Loss on futures contract 20000

Futures contract 20000

[To record futures contract as a liability at its fair value ndash 10 x (RM32000 ndash RM30000)]

31 May

Loss on futures contract 25000

Futures contract 25000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM34500 ndashRM32000)]

44

Example 3 - No Hedge

Accounting

30 June

Loss on futures contract 5000

Futures contract 5000

[To adjust the value of futures contract to its current fair value ndash 10 x (RM35000 ndashRM34500)]

Futures contract 50000

Cash 50000

(To record settlement of futures contract)

45

Example 3 - No Hedge

Accounting

30 June

Cash 350000

Sales 350000

(To record sales 10 x RM35000)

Cost of sales 220000

Inventory 220000

(To record cost of sales)

46

Example 3 ndash Fair Value Hedge

In a fair value hedge the carrying amount of

the hedged item should be adjusted for the

gain or loss attributable to the hedged risk

even if the hedged item is otherwise measured

at cost as required by other relevant MFRS

The gain or loss on the hedged item should be