“to examine the rise of “new age” aviation lessors and the

TRANSCRIPT

“To examine the rise of “new age” aviation lessors and the factors which shall impact their

future success and opportunities in the aircraft leasing sector”

Submitted By: Darragh Patrick McEniry (10368297)

“This dissertation is submitted in partial fulfilment of the

requirements for the Degree of Master of Business Studies,

Waterford Institute of Technology”

Research Supervisor: Mary Cooke

Submitted to: Waterford Institute of Technology

22nd

August 2016

ii

ABSTRACT

“If you want to be a Millionaire, start with a billion dollars and launch a new airline.”

Richard Branson

Aircraft financiers certainly play their part in the above quote. Aircraft leasing has become a

multi-billion dollar industry, serving clients globally. Having developed from humble

beginnings in Shannon, Co. Clare by Dr. Tony Ryan, Ireland has become a genuine leader in

this field. Recent economic issues globally have not dampened the impressive growth of this

industry. However, the sector is not without its issues and significant challenges may stem

this growth in the medium term. Growing competition lessors emanating from emerging

geography are set to challenge legacy lessors, yet little is known about these new entrants.

This study looks to bridge this knowledge gap by engaging industry experts to act as analysts

of these new age lessors and provide an industry led perspective into the challenges set to

face these new players.

A qualitative research approach has been adopted to investigate the research question and

objectives. This consists of nine semi-structured interviews with a combination of industry

stakeholders with vast experience with the leasing sector, thus providing a wide spectrum of

perspectives. These interviews create the foundation of this study to asses these "new age

lessors" prospects by utilising their experience under a broad range of standpoints. Key

weaknesses and business model flaws are identified and discussed. In addition, the impact of

these entrants is developed by those involved within it and future issues are set out.

The study reveals that new age lessors emanating from the Chinese mainland have developed

under government backing and have benefitted from economic issues in the west to expedite

their rise. The findings serve to highlight issues with the business approaches employed at

present, which limit the potential success these new competitors may enjoy, despite their

strong financial clout. Key modifications are provided, in addition to a consensus regarding

the great potential China and their lessors currently possess to become major players.

Unsurprisingly, the future of these lessors and China's economy are deemed intertwined and

so the greatest risk to the development of their leasing industry comes from within. A

roadmap is provided for lessors to alter their existing approach and offset the key risks they

face, in order to successfully challenge the legacy players of the West.

iii

ACKNOWLEDGEMENTS

There are a number of people I would like to acknowledge and give thanks to, due to their

assistance in relation to this completed dissertation and throughout this academic year.

Firstly, I wish to thank my mother for the sacrifices she has made to help me get to this stage

of my education and for all she has done for me to date. It is very much appreciated and will

not be forgotten. I wish to thank my father for his unwavering confidence and faith in me.

Secondly, I wish to thank my supervisor, Ms. Mary Cooke, for her seemingly unlimited

patience and help with my queries, in addition to her time and efforts throughout the process.

Your constant encouragement was crucial to the completion of this study. I would also like to

thank Dr. Sheila O’Donohoe for her support and guidance throughout the year. Both are a

credit to Waterford Institute of Technology and I am very grateful for their assistance.

Thirdly, I wish to thank my colleagues Darren, John and Liam for their constant humour and

help throughout the year. Our frequent trips for coffees, rolls and dome dinners ensured some

level of sanity was regained when we needed it most and gaining three good friends was an

added bonus to the year. I also wish to thank each member of the MBS programme who has

made the journey so worthwhile and interesting throughout the last twelve months. It was a

pleasure. Last but not least, I must thank Cliodhna for her constant support, advice and

patience throughout the year. You made the year that little bit easier and I am very grateful.

Finally, I wish to acknowledge and thank each participant of my study. Your time and

expertise enabled the successful completion of this study and I appreciate each participants

input and help. Special thanks are reserved for Mr. Gerry Power and Mr. Jack O’ Dwyer, who

consistently and selflessly went above and beyond to aide my research and also provided

guidance towards future career decisions.

iv

ETHICAL DECLARATION

I declare that this dissertation is wholly my own work except where I have made

explicit reference to the work of others. I have read the Structured Masters’

Programmes Research Policy, Procedures and Guidelines and hereby declare that this

dissertation is in line with these requirements. I have discussed, agreed and complied

with whatever confidentiality or anonymity terms of reference were deemed

appropriate by those participating in the research and dealt appropriately with any

other ethical matters arising.

I have uploaded the entire dissertation as one file to Turnitin® in Moodle®, examined

my ‘Originality Report’ by viewing the detail behind the overall ‘Similarity Index’,

and have addressed any matches that exceed 3%. I have made every effort to minimise

my overall ‘Similarity Index’ score and the number of matches occurring.

Darragh McEniry Date

v

“The Rise of the New Age

Lessor; A flight towards

success or failure?”

Darragh McEniry

vi

TABLE OF CONTENTS

Contents: ABSTRACT ....................................................................................................................... ii

ACKNOWLEDGEMENTS ............................................................................................. iii

ETHICAL DECLARATION ............................................................................................ iv

TABLE OF CONTENTS .................................................................................................. vi

LIST OF FIGURES .......................................................................................................... ix

LIST OF TABLES ............................................................................................................. x

LIST OF ABBREVIATIONS ........................................................................................... xi

INTRODUCTION ............................................................................................................. 1

1. Introduction ..................................................................................................................... 1

1.1. Purpose of the study .................................................................................................... 1

1.2. Justification of the study ............................................................................................. 1

1.3. Research Question and Objectives of the Study ......................................................... 2

1.4. Research Methodology ................................................................................................ 2

1.5. Method of Study .......................................................................................................... 3

1.6. Value of the Study ....................................................................................................... 3

1.7. Report Outline ............................................................................................................. 4

1.8. Conclusion ................................................................................................................... 5

LITERATURE REVIEW .................................................................................................. 7

2. Introduction ..................................................................................................................... 7

2.1. Aviation Finance in 2016 ............................................................................................ 7

2.2. Lessors ......................................................................................................................... 8

2.3. Aviation Leasing Characteristics .............................................................................. 12

2.4. Ireland and Aviation Leasing .................................................................................... 15

2.5. Aviation Finance as a Global Business ..................................................................... 16

2.6. Leasing’s Value to Airlines ....................................................................................... 18

vii

2.7. Traditional Funding Sources ..................................................................................... 20

2.8. Recent Industry Developments: The Rise of the “New Age Lessor” ....................... 22

2.9. Conclusion ................................................................................................................. 25

RESEARCH METHODOLOGY..................................................................................... 25

3. Introduction ................................................................................................................... 25

3.1. Research Problem Identification ............................................................................... 25

3.2. The Research Question.............................................................................................. 25

3.3. Research Objectives .................................................................................................. 26

3.4. Research Method Considerations .............................................................................. 27

3.5. Research Process ....................................................................................................... 28

3.6. Research Design ........................................................................................................ 29

3.7. Research Philosophies Considered............................................................................ 30

3.8. Research Philosophy Selection and Rationale .......................................................... 31

3.9. Research Method Selection ....................................................................................... 31

3.10. Justification of Semi-Structured Interviews .......................................................... 31

3.11. Sample and Selection Criteria ............................................................................... 32

3.12. Interview Schedule and Participant data ............................................................... 32

3.13. Interviews .............................................................................................................. 33

3.14. Data Analysis Procedures Employed .................................................................... 35

3.15. Ethical Considerations ........................................................................................... 36

3.16. Study Reliability Issues ......................................................................................... 37

3.17. Conclusion ............................................................................................................. 37

FINDINGS ....................................................................................................................... 37

4. Introduction ................................................................................................................... 37

4.1. Growth Factors .......................................................................................................... 38

4.2. Prospects.................................................................................................................... 39

4.3. Leasing Attitudes and Outlooks ................................................................................ 40

viii

4.4. Leasing Industry Experience ..................................................................................... 42

4.5. Aircraft Remarketing................................................................................................. 42

4.6. Transition Costs and the Price of Remarketing ......................................................... 43

4.7. Chinese Lessor Portfolio Risk ................................................................................... 44

4.8. Industry Impacts ........................................................................................................ 46

4.9. Chinese Lessors and Economic Factors .................................................................... 47

4.10. Conclusion ............................................................................................................. 49

DISCUSSION .................................................................................................................. 50

5. Introduction ................................................................................................................... 50

5.1. Objective 1 ................................................................................................................ 50

5.2. Objective 2 ................................................................................................................ 54

5.3. Objective 3 ................................................................................................................ 55

5.4. Conclusions ............................................................................................................... 56

CONCLUSION ................................................................................................................ 57

6. Introduction ................................................................................................................... 57

6.1. Research Question and Objectives of the Study ....................................................... 57

6.2. Summary of Key Findings ........................................................................................ 57

6.3. Study Limitations ...................................................................................................... 58

6.4. Author Recommendations ......................................................................................... 59

6.5. Recommendations for Future Research .................................................................... 60

6.6. Concluding Remarks ................................................................................................. 60

7. Bibliography ................................................................................................................. xii

Appendix A .......................................................................................................................... xii

Appendix B .......................................................................................................................... xv

Appendix C ......................................................................................................................... xvi

Appendix D ........................................................................................................................ xvii

Appendix E ...................................................................................................................... xviii

ix

Word count: 16581

LIST OF FIGURES

Figure 1: PWC Aircraft Leasing Report - Challenges 2011(Source: PWC) ............................. 8

Figure 2: Commercial Aircraft Order Back Log Development 1990-2015 (Source: Ascend

Fleet, January 2016) ................................................................................................................... 8

Figure 3: Global Distribution of Leased Aircraft 2016 (Source AtlasData) ............................ 10

Figure 4: Lessor Share of Western Built Aircraft 2016 (Source: PWC Report, 2016) ........... 11

Figure 5: Lessor Yield and Finance Cost 2014 (Source: Annual Reports and Airline Analyst

2014) ........................................................................................................................................ 13

Figure 6: Selection of Largest Global Lessors 2016 (Source: Wall Street Journal) ................ 15

Figure 7: Historical Growth in Leased Aircraft Fleets ............................................................ 17

Figure 8: Global Fleet Forecast and Leasing Penetration (Source: PWC) .............................. 18

Figure 9: Aircraft Funding Comparison 2013 vs. 2014 ........................................................... 21

Figure 10: Global Distribution of Aircraft Orders 2014 .......................................................... 22

Figure 11: Selected Lessor Fleet value Comparison 2016 (PWC, 2015) ................................ 22

Figure 12: Total Aircraft Assets Held in China 2008-2014 (Source: CAAC) ......................... 23

Figure 13: The Research Onion (Saunders et al 2007, p.102) ................................................. 29

Figure 14: Aircraft with Ceased Operators - Operating Lessor Managed 2000-2015 (Woods,

citing Flightglobal)................................................................................................................... 43

Figure 15: The Leasing Cycle (Source: Author generated based on participant data) ............ 44

Figure 16: Operating Lessor Fleet Share - By Region (Halliday, citing Flightglobal)............ 45

Figure 17: Historical 737 Classic, 737NG and A320 Market Values (Participant Provided

Estimates) ................................................................................................................................. 46

Figure 18: Chinese GDP vs. the World (Source: Donovan, citing World Bank) .................... 48

Figure 19: Aviation Growth in China vs. the World (Source: Woods, citing CAAC) ............ 49

x

LIST OF TABLES

Table 1: Comparison of Research Approaches (Hennink et al, 2011) .................................... 28

Table 2: Interview Schedule .................................................................................................... 33

Table 3: Advantages and Disadvantages of Interview Method (Adapted from Denscombe,

2007, 202) ................................................................................................................................ 34

Table 4: Main Stages of Qualitative Data Analysis Employed (Source: Denscombe et al, 2007

p. 252) ...................................................................................................................................... 36

Table 5: Interviewee Details and Key Information.................................................................. 37

Table 6: Chinese State Backed Airlines ................................................................................... 39

Table 7: Expected Chinese Aircraft Demand 2012-2028 ((DJB, SG and Woods, citing PWC

2012 Figures) ........................................................................................................................... 41

xi

LIST OF ABBREVIATIONS

ATA – Air Transport Authority

AWAS – Ansett Worldwide Aviation Services

BDO – Binder Dijiker Otte and Co.

CAGR – Compounded Annual Growth Rate

CEO – Current Engine Option

CMV – Current Market Value

EIS – Entry into Service

FAA – Federal Aviation Authority

GECAS – General Electric Commercial Aviation Services

IATA – International Air Traffic Association

ISE – Irish Stock Exchange

KPMG - Klynveld Peat Marwick Goerdeler

LCC – Low Cost Carrier

NBA – Narrow Body Aircraft

NEO – New Engine Option

NG – New Generation

OEM – Original Equipment Manufacturer

PE – Private Equity

POA – Plan of Action

PWC – Price Waterhouse Cooper

ROI - Return on Investment

RPKG – Revenue per Passenger Kilometre Growth

WBA – Wide Body Aircraft

CHAPTER ONE

INTRODUCTION

1

Chapter One

INTRODUCTION

1. Introduction

In this chapter, the purpose of the study will be defined and a justification provided. The main

objectives of this report is outlined and the method of study to be used shall be illustrated.

This chapter’s aim is to outline the rationale behind the study, its value and illustrate the

research methodology to be utilised.

1.1. Purpose of the study

The purpose of this study is to examine the research question and to highlight that the

financing needs of the aviation leasing industry has created a unique scenario, allowing the

rise of new age lessors from the Far East to be accelerated recently. In the coming years, the

injection of fresh capital from emerging geography will be welcomed, as it will ensure the

sustained growth of the industry in order to meet client demand. However, the rapid influx of

investment from non-traditional sources and their accompanying aggressive expansion plans

leaves questions about the long term sustainability of this approach by these new comers.

1.2. Justification of the study

A lack of recent academic investigation of this area highlighted the fact that further research

was necessary in order to bridge this knowledge gap. Little is known about the firms involved

other than their financial clout and countries of origin. Secondly, aviation financing is highly

topical, with its frequent appearance in Irish media publications. This is likely to remain the

case, as the demand for financing deliveries of new aircraft peaks when long term financing

becomes unattractive for many traditional financiers and thus allowing new players in.

On the one hand, record order books of aircraft manufacturers reflect a period of strong

orders buoyed by strong demand in the emerging markets. On the other, there are a number of

issues in the markets which may make these orders more difficult to finance, and potentially,

more expensive. The European Sovereign debt crisis, and increased difficulty of accessing

US dollar funding has raised funding pressure. This “perfect storm” is unusual. A number of

predominantly European banks who have historically played a key role are retracting from

the market. This is causing tensions in the funding market, which have been heightened by

the ongoing bank deleveraging process, which in part reflects the impact of new regulations

such as Basel III. Conversely, in tough economic times and a low interest rate environment

2

attractive yields are harder to find. As a result, investors have sought alternative locations for

funds and some have chosen aircraft financing industry for new opportunities. Given that

Ireland has become a major player, as a prime location for this industry, such a study would

be both justified and very relevant to modern commerce in Ireland and abroad.

The author of this study would also cite career aspirations and a strong personal interest in

this field as key reasons behind the decision to complete this study. With this, one can

increase their personal knowledge of the area and complete a study from which others can

learn in the future.

1.3. Research Question and Objectives of the Study

The research question specific to this dissertation can be stated as follows:

“To examine the rise of Chinese aviation lessors and the factors which shall impact their

future success and opportunities in the aircraft leasing sector”

The objectives of this report are:

To examine the nature of the suitability of business models currently employed by

fledging lessors in detail and explore the challenges to their future success

To illustrate the developments which have aided the rise of the new age lessor and

resulting industry impact

To identify the potential impact of Chinese economic issues on the development and

abilities these new age lessors to compete effectively in the future

1.4. Research Methodology

In order to properly research this topic, a number of data collection methods were considered.

As the research is both qualitative and exploratory in nature, the author has deemed

interviews to be the most appropriate primary data collection method. According to

Liamputtong (2010), it is believed that authors research should influence the research model

employed and not the opposite so that the author shall fully investigate a topic. The

interviews were semi-structured in nature and were conducted in person with key personnel

of significant experience and expertise in the area of aviation finance globally. The author has

used a sample of nine aviation finance industry professionals from both Ireland and abroad to

gather data on this topic.

3

1.5. Method of Study

This study shall be divided into two main sections. The literature review will account for the

first section and will serve to explore the existing research relating to the research topic. Prior

to the current study, a review of secondary research will be carried out in order to fully

understand this expanding sector. This allows a more accurate picture of the topic to be

created and ensures this author’s perspective accurately depicts the current status of aircraft

leasing.

The second section of this report shall consist of primary research into the research problem,

which this author has compiled personally. In order to investigate the research question and

objectives, several interviews were completed with industry professionals. Each interview

served to further the author’s knowledge of this sector. The different fields of expertise of

each respondent provided diverse viewpoints on the industry. The interview process consisted

of prepared questions for each respondent and ensured all answers could be developed and

clarified if necessary, so the author could gain a clear insight into their opinions. The data

collected from each expert was then compared to the data compiled as part of the literature

review. The process served to formulate a discussion and a final conclusion.

1.6. Value of the Study

This study may add value to and serve to assist many individuals and organisations such as:

Practitioner

The findings illustrated in this report will serve to provide the Aviation Finance sector with

relevant and up to date information on the health of their industry after several years of

substantial expansion and growth.

Given the forecasted funding issues for this sector in the medium and long term, the findings

of this report will serve to identify new potential sources of capital emanating from the Far

East and the opportunities available in the region.

The findings may serve as a tool for new age lessors to have their current approach to leasing

critiqued by industry experts and to use this knowledge to ensure sustainable success.

The findings of this report will serve to highlight an opportunity to legacy lessors to learn

more about their new rivals in Asia and to gauge the correct reaction required to keep their

current, respective market footholds.

4

Academic

The findings may be used to contribute to the existing research and understanding of this

global sector in relation to its development and the future investment partners which may

become involved in the industry.

In addition, existing knowledge may be expanded to incorporate the ongoing development of

Asian backed entities as significant players in this industry and to understand their business

offering and techniques more clearly from a neutral standpoint

Investor

An expanded knowledge of this asset class and its merits as a future investment shall serve to

increase its use amongst many investors and allow this asset class to develop as a more

common place investment location for long term investment capital globally.

1.7. Report Outline

Chapter One provides the reader with an introduction to this topic and the rationale behind

commencing this study which has guided the author and shaped the study.

Chapter Two provides an in depth analysis of the available literation and theories which are

applicable to the area of investigation. The purpose of this literature review is to educate the

reader as to the existing research related to this field and provide a background to the analysis

which this author has carried out.

Chapter Three outlines the research methodology which has been adopted for the purposes of

carrying out this investigation. Justification for these decisions shall be provided, in addition

to a frank discussion as to the possible advantages and disadvantages of the methods chosen.

The author shall also outline the limitations of this study and the participants involved.

Chapter Four presents the findings of the study stemming from the collected primary data.

These findings are presented in a manner mirroring the aforementioned research objectives,

using several relevant key headings to provide structure to the illustration of results.

Chapter Five serves to provide a forum for the discussion of the relevant literature analysed

by the author and the findings of his data collection endeavours, whereby definitive answers

to the relevant research objectives and overall research question are provided.

Chapter Six consists of a summation of the study itself, in addition to relevant final comments

and recommendations based on the findings of this study and potential areas of future study.

5

1.8. Conclusion

Ireland is a world leader in relation to all forms of aviation finance. With this, an up to date

status report on this industry appears apt and given its rapid expansion, an in depth analysis

of these new lessors operating abroad in relation to their strength and prospects appears apt.

This study shall be of benefit of all those interested in Irish commerce, global investment

options and especially those with a keen interest in aviation financing industry and its future

direction over the next five to ten years.

CHAPTER TWO

LITERATURE REVIEW

Chapter Two

LITERATURE REVIEW

2. Introduction

Aircraft finance has become a fashionable destination for investors of late, with many

emanating from Asia. However, little investigation into these new entities has occurred. This

author intends to explore the dramatic rise of the “new age lessor”. Specifically the

emergence of strongly backed Chinese lessors, hungry for portfolio expansion and market

share thus posing strong potential competition for legacy players

2.1. Aviation Finance in 2016

Aviation financing is in vogue at present, “as the demand for financing deliveries of new

aircraft peaks at a time when long term financing becomes unattractive for some of the

traditional banks” (PWC 2015, P. 2). Firstly, record order books of aircraft manufacturers

reflect “strong orders buoyed by both new aircraft types and strong demand in the emerging

markets” (Ascend, 2012, P. 4). There are a number of issues in the aircraft finance market

which “make these orders more difficult to finance, and potentially, more expensive, such as

limited access to dollar backed funds” (Deutsch Bank, 2012, P.16). Several European

financial houses who enjoyed a long run affinity with leasing have exited. It has resulted in

issues in the funding market and has been exacerbated “by the ongoing bank deleveraging

process, which in part reflects the impact of new regulations such as Basel III” (PWC, 2015,

P. 5). Considering the economic issues experienced from 2008-2011, it is suggested that

issues in the West have allowed capital rich lessors from the Far East to emerge more easily

than many thought would be possible (Wall Street Journal, July 2016). PWC (2011) provide

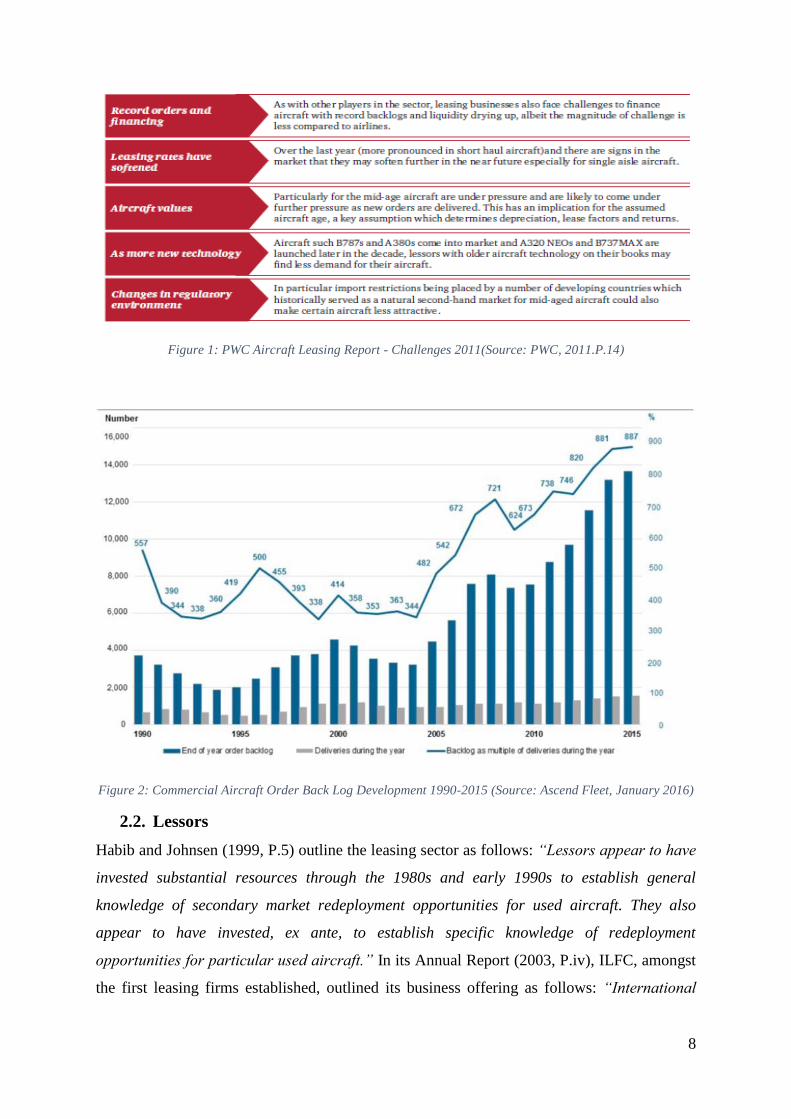

the challenges lessors face:

8

Figure 1: PWC Aircraft Leasing Report - Challenges 2011(Source: PWC, 2011.P.14)

Figure 2: Commercial Aircraft Order Back Log Development 1990-2015 (Source: Ascend Fleet, January 2016)

2.2. Lessors

Habib and Johnsen (1999, P.5) outline the leasing sector as follows: “Lessors appear to have

invested substantial resources through the 1980s and early 1990s to establish general

knowledge of secondary market redeployment opportunities for used aircraft. They also

appear to have invested, ex ante, to establish specific knowledge of redeployment

opportunities for particular used aircraft.” In its Annual Report (2003, P.iv), ILFC, amongst

the first leasing firms established, outlined its business offering as follows: “International

9

Lease Finance Corporation is primarily engaged in the acquisition of new commercial jet

aircraft and the leasing of those aircraft to airlines throughout the world. In addition to its

leasing activity, the Company regularly sells aircraft from its leased aircraft fleet to third

party lessors and airlines” (ILFC, 2003). AWAS, another legacy lessor, states: “At AWAS we

pride ourselves in our ability to optimise return on investment through the effective

management and remarketing of our assets” (AWAS, 2009, P.v).

Leasing companies comprise of “technical, legal and marketing teams that hold extensive

knowledge of this niche market, study carrier capacity requirements, and monitor the use of

their aircraft by clients” (Gavazza 2010, P.10). These “monitoring” costs, as Eisfeldt and

Rampini (2009) and Rampini and Viswanathan (2010) highlight, imply that per-period

charges are larger on leased assets versus owned aircraft. Furthermore, Gavazza (2010), using

aircraft prices and aircraft lease charges, argues that lease rates are 20% higher than implicit

rental rates. This leaves airlines facing a decision between leasing’s higher per-period costs

and ownership’s higher transaction charges. Barrington (1998, P. 17) notes: “The airlines

that use operating leases consider that the flexibility such leases provide makes up for the

fact that the cash costs of the leases can be greater than the cost of acquiring the same

aircraft through ownership.” Morrell (2001, P. 17) lists “no aircraft trading experience

needed” as an advantage of airlines leasing these assets, and “a higher cost than, say, debt

finance for purchase” as a drawback.

In the event of default on a lease prior to bankruptcy, a lessor can seize the aircraft more

easily than a secured lender can in both U.S. and non-U.S. bankruptcies (Krishnan and

Moyer, 1994; Habib and Johnsen, 1999). In U.S.-based Chapter 7 bankruptcies and in most

non-U.S. bankruptcies, a lessor can repossess the asset more rapidly than a debt holder can

(Littlejohns and McGairl, 1998). Thus, since defaults and bankruptcies are frequent in the

airline industry, leasing enhances the efficiency of redeployment by exploiting its stronger

ability to repossess assets through increased client monitoring.

Eisfeldt and Rampini (2009) argue that leasing is particularly attractive to operators who lack

financial strength or have cash flow issues. The clients to lessors are often in their infancy,

display volatile capacity requirements, and are considered to be a high risk customer base due

to increased default likelihood, according to the same authors. Hence, lessors frequently get

aircraft returned, which leads them to further specialize in redeployment and remarketing

(Littlejohns and McGairl, 1998).

10

Shleifer and Vishny (1992, P.10) contend that “the institution of airline leasing seems to be

designed partly to avoid fire sales of assets.” Due to the airline industry being regarded as

highly cyclical, both airline profits and aircraft values carry large financial risk, and they are

almost perfectly correlated (Gavazza 2010). Leasing allows airlines to offset an element of

the asset-ownership risk to operating lessors. The price discounts estimated by Pulvino

(1998) show that even the lowered risk - ownership ratio displayed can cause issues. Lessors

are assumed to offset this risk in a better manner through their knowledge of global markets,

their scale economies, and their diversification of aircraft portfolios types operating in diverse

geographic locations (PWC, 2015). Moreover, the largest lessors (e.g. GECAS) belong to

financial conglomerates, which allows them to diversify the aggregate risk of aircraft

ownership and to have a lower cost of funds, thanks to a higher credit rating (Clarke, 2007).

Figure 3: Global Distribution of Leased Aircraft 2016 (Source AtlasData)

Lessors can infiltrate this sector through three main avenues; (1) they acquire asserts directly

from an OEM; (2) they purchase assets from carriers and lease them back (so called sale-and-

leaseback transactions); and (3) they purchases aircraft from other competitors who have

these assets on lease to clients (Gilligan, 2004). By adopting this approach, a lessor can

develop a portfolio of assets that can be scaled up or down, which depends on the economics

of aircraft ownership and firm strategies (Clarke, 2007). The maturity of this portfolio of

assets is under constant review, due to age sensitive nature of the assets and the value which

they may command on the open market. Gilligan (2004, P.46) examined the relationship

between leasing percentage and aircraft age and observed “that the leasing percentage is

rather constant in the data over the age of aircraft”. Gavazza (2010) contributes that leased

assets are almost one and a half years the junior of airline owned portfolios.

11

Lessors have differing business models. Some focus on new or near new assets with a

preference towards short-haul aircraft types (e.g. Boeing B737 or Airbus A320) (Francis,

Schofield, & Flottau, 2011). Others have portfolios that are older, as they deem value exists

in aircraft that are deemed mid-life. Leasing companies have differing capital structures.

Some are part of large global financial corporations. Others are standalone entities backed by

private equity investors. In recent times, we have also seen” the use of state owned finance

houses doing the will of the government towards infiltrating this sector and providing cheap

finance to domestic leasing entities in their infancy” (Anselmo & Jackman, 2012, P. 31).

Figure 4: Lessor Share of Western Built Aircraft 2016 (Source: PWC Report, 2016)

Gritta and Lippman (2010) provide the history of aircraft leasing since 1960s. Previously,

many airlines utilised the finance lease as an alternative source of funding to gain aircraft.

This gave a major advantage over purchasing the asset outright, i.e. since it was off-balance

sheet financing, the resulting obligations under the lease appeared in the footnotes alone of

the airline balance sheets. Short-term lease agreements were deeply unpopular at the time.

The situation has been altered over the last thirty five years. Since 1976, finance lease are

required to be reported as both a leasehold asset and a long-term liability (Gritta and

Lippman, 2010). As a result, airlines completely altered their approach to aircraft finance.

Short-term operating leases became in vogue, as they are not reported on companies’ balance

sheets. By strategically violating the criteria for capital leases, the airlines once again pushed

the leases off the balance sheet, thus surging the popularity of leasing (Morell, 2001).

12

Gavazza (2010) examined how the liquidity of an aircraft, as an asset, affects whether or not

carriers lease the aircraft they operate, the optimal maturity of lease contracts and the mark-

ups of lease rates over aircraft prices. The results suggest that more-liquid assets are more

likely to be leased, due to their shorter operating leases, longer capital leases; and the fact that

they call for lower mark-ups of lease rates.

2.3. Aviation Leasing Characteristics

Aviation finance is capital-intensive, given its incredible start-up costs. For example, in 2011,

a Boeing 787 Dreamliner costs between US$185–218 million and an Airbus A380-800 starts

at US$375 million per aircraft (Cameron & Serena, 2011, P. 23). Financial institutions now

benefit from the maturity of this asset market, which has led to “a standardisation of the

documentation for the leasing and financing of aircraft” (Deutsch Bank, 2012, P.12). Given

current economic issues, balance sheet commitments from large strategic and traditional

financiers require substitution, and “private equity and hedge funds stand ready to fill this

gap” (Millbank, 2012, P.56). The emerging markets in Asia, the Middle East, Africa and

Latin America only add to the desire for new funding sources to fund such assets (PWC,

2015).

International Accounting Standard (IAS) 17 (2010, 23) defines that “a lease is an agreement

whereby the lessor conveys to the lessee, in return for a payment or series of payments, the

right to use an asset for an agreed period of time”. Leasing agreements are placed into two

main sections, namely a finance lease and an operating lease. Finance lease is defined by the

IAS 17 (201) as “a lease that transfers substantially all the risks and rewards incidental to

ownership of an asset. Title may or may not eventually be transferred”. The related risk

ownership and costs include “accountability for loss, wear and tear, and obsolescence,

whereas ownership benefits encompasses the right of use, gains from asset value appreciation

and possession of the property title” (IAS 2010). Conversely, given that the lessor keeps

ownership, “operating leases serve to divide the legal ownership from its economic use, and

so the asset is an inherent form of collateral in that type of contracts” (Graham, Lemmon,

and Schallheim, 1998; Sharpe and Nguyen, 1995, P. 42).

An additional difference between these forms of leasing is based on the fact that an operating

lease is not capitalized by the lessee, and thus represents a form of off-balance sheet

financing (associated finance obligations remain). Based on this, and according to Gritta,

Lippman, and Chow (1994, P. 32), “the percentage of operating leases in total leases in the

13

US increased from 13% to 82%. Other benefits such as no residual value risk or lower

financial outlay requirements help explain this growth”.

Due to an annual ROI of twelve to fifteen percent, aircraft leasing remains amongst the

profitable aspects to enter within this industry and draws a strong investor base (Leverage

Finance, 2012). For example, investing in airline stocks such as Delta Airlines or Ryanair

provide half this return per annum with higher volatility at present. The first and second lease

cycles of passenger aircraft are “preferred by investors and lenders, due to more stable

risk/reward ratio” (Clarke, 2007, P. 56). That is not to say that “mid-life” narrow body and to

a lesser extent wide body aircraft, do not offer opportunities to lessors to, as Aergo Capital

have illustrated rather well (Irish Independent Report, 2016). In the meantime, freight aircraft

(i.e. aircraft used solely for the transport of goods) represent the second most popular asset

type with “a ROI of around 12%” (PWC, 2015). However, actualising such substantial

returns is based on “an accurate assessment of market trends and a thorough understanding

of the direction that the industry is heading towards” (PWC, 2015, P. 17).

Figure 5: Lessor Yield and Finance Cost 2014 (Source: Annual Reports and Airline Analyst 2014)

Typically, airlines lease aircraft for seven years, although this period has been extended to up

to 10 or 12 years in some recent transactions (Deutsch Bank, 2012). The lessor oversees the

return of rental income from a client and “oversees the technical management of the aircraft

during its lease period” (Clarke, 2007). The individuality of contracts leave such terms open

to alteration as agreed between parties. Airline leases are often less expensive as “major

leasing companies enjoy the benefit of bulk pricing, low margin financing and higher

debt/equity ratios than an airline can or should maintain” (ATA USA 2010, P. 7).

Leasing is now a preferred choice for most airlines today. Operational benefits such as fleet

elasticity, increased access to delivery slots and cash flow measures play a key role. As a

14

result of the above shift, leasing’s market share has increased from “around 12% of the

global fleet in 1990 to over 32% today” (Ascend, 2015, P.12). The lessor market share is

likely to increase again, as airlines look to fill the aforementioned funding gap. This may

potentially increase to a share of “around 50% by 2020” (Avolon, 2015, P.4).

The relationship between lease and debt has undergone plenty debate. Several authors side

against the traditional finance theories and argue that leases complement debt. Eisfeldt and

Rampini (2009, P.14) prove that, due to the ability to repossess the asset, “the debt capacity

of leasing is higher than the capacity of security lending”. Lewis and Schallheim (1992,

P.46) contend that leasing can increase a firm's debt capacity by “selling any extra non-debt

tax shields”. They conclude that the leasing and borrowing dynamic can complement each

other within the firm's capital structure. Similar to this, Ang and Peterson (1984, P.46) find

leasing to be “positively correlated to the company’s debt ratio and that lessee’s used more

long-term debt”, than those who avoid leasing entirely.

The leasing market has been overshadowed by two large lessors, namely GECAS and ILFC

(now AerCap). Beyond this, the Top 10 consists of a variety of operations of a comparably

smaller scale. The ‘Big two’ dominate the market in terms of financial clout, fleet size and

value, and dwarf most competitors. GECAS and ILFC currently operate larger portfolios than

Delta Air Lines, the world’s largest airline by number of aircraft.

A variety of more recently formed lessors (e.g. HKAC, Avolon, Jackson Square etc.) have

emerged looking to challenge the status quo, with funding from a variety of sources,

including sovereign wealth funds (e.g. Saudi Arabia), high net worth individuals and PE

funds. Many of these have moved to quickly gain scale portfolio size, through “the

acquisition of existing companies, purchase and lease back transactions and acquisition of

portfolios from competitors” (PWC, 2015, P.23).

15

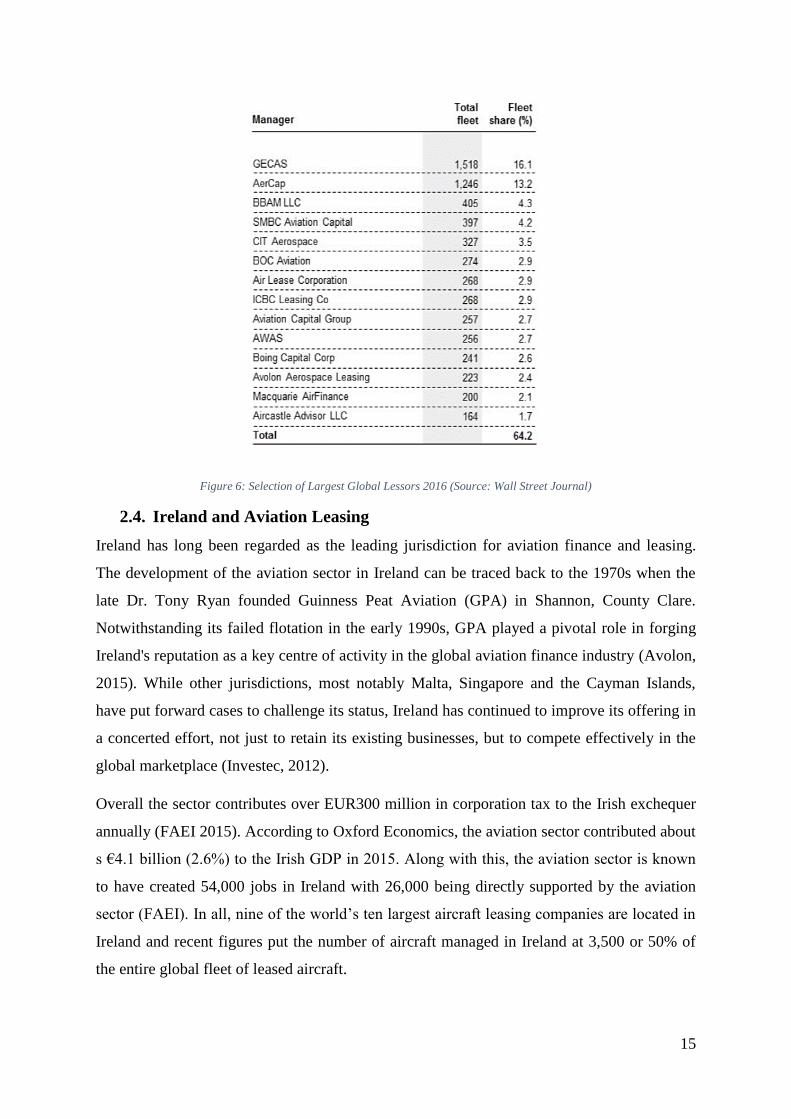

Figure 6: Selection of Largest Global Lessors 2016 (Source: Wall Street Journal)

2.4. Ireland and Aviation Leasing

Ireland has long been regarded as the leading jurisdiction for aviation finance and leasing.

The development of the aviation sector in Ireland can be traced back to the 1970s when the

late Dr. Tony Ryan founded Guinness Peat Aviation (GPA) in Shannon, County Clare.

Notwithstanding its failed flotation in the early 1990s, GPA played a pivotal role in forging

Ireland's reputation as a key centre of activity in the global aviation finance industry (Avolon,

2015). While other jurisdictions, most notably Malta, Singapore and the Cayman Islands,

have put forward cases to challenge its status, Ireland has continued to improve its offering in

a concerted effort, not just to retain its existing businesses, but to compete effectively in the

global marketplace (Investec, 2012).

Overall the sector contributes over EUR300 million in corporation tax to the Irish exchequer

annually (FAEI 2015). According to Oxford Economics, the aviation sector contributed about

s €4.1 billion (2.6%) to the Irish GDP in 2015. Along with this, the aviation sector is known

to have created 54,000 jobs in Ireland with 26,000 being directly supported by the aviation

sector (FAEI). In all, nine of the world’s ten largest aircraft leasing companies are located in

Ireland and recent figures put the number of aircraft managed in Ireland at 3,500 or 50% of

the entire global fleet of leased aircraft.

16

The Irish Stock Exchange ("ISE") has formulated a dedicated exchange for aviation related

debt and other instruments utilised by the leasing sector here. Key to this development is the

international recognition of the capital markets as a key source of financing for aircrafts and

aviation related assets. These markets accounted for $15bn or 15% of the total funding needs

in 2013 (ISE Press release, 2014). Current listings include a $927M EETC from International

Airlines Group, amongst many others.

2.5. Aviation Finance as a Global Business

There is growing competition especially from the Far East as new aircraft deliveries in that

region outpace the more mature European and US markets. This is drawing leasing activity

towards that region. In addition, a number of countries, particularly Singapore, are actively

targeting the aircraft leasing industry with changes to their tax regimes. There are a number

of countries that are tailoring their air safety regulation activities and aircraft registers to

attract business from the leasing industry, with Ireland a prime example followed. With this,

the global nature of this fluid industry is certain to be a positive for investors with many

opportunities.

“At present, there are 23,000 western built jet airliners in service in the world of which 33%

(approx. 7,700) are on operating leases and are owned by leasing companies and financial

institutions“ (IATA, 2015, P.27). In addition, the world fleet is “currently growing at 3.3%

per year, while operating leasing is growing at 5.5%, which serves increasing demand

globally” (Ascend, 2015, P.1). The operating leased fleet is “currently valued at about $175

Billion, consisting of 30 lessors that have fleet values over $1 Billion, the two largest have

fleets valued over $40 Billion” (Anselmo and Jackman, 2012, P.24). Given the asset values

involved, the wide variety of asset types and the scope for investment within the structure of

this industry, investment opportunities are certain to emerge on a regular basis as the industry

looks to bridge potential funding gaps going forward. It is clear this new asset class is to

emerge as a strong alternative to the more traditional assets which attract investors globally.

“In 1990, there were 1,200 aircraft on operating lease, representing 14% of the

commercial jet fleet” (Kruglinki, 1996, P.3). In ten years, the number on lease had risen to

3,400, accounting for 24% of the total and by 2010, the market had reached 6,800 leased jets,

representing over 36% of all commercial jets (Ascend, 2015). The majority of these include

popular A320 and 737 designs, increasing numbers of Boeing 777s and A330s and a large

amount of older equipment (Anselmo and Jackman, 2012).

17

N

Figure 7: Historical Growth in Leased Aircraft Fleets

The leased aircraft share of the global fleet is expected to increase further as global passenger

traffic and commercial jet fleets maintain strong underlying growth trends, forecast at

CAGRs of 5.6% and 4.1%, respectively between 2011 and 2030. This represents incremental

airline fleet growth of 40,000 aircraft over the next 20 years, with between 16,000 and 20,000

additions to the leased fleet. Growth of passenger air travel in emerging countries and regions

plus the growth of low-cost carriers globally are important drivers of aviation growth and

represent key growth opportunities for aircraft lessors.

Based on FAA submissions, “”the commercial air carrier industry will grow by a remarkable

3.7% over the next five years (to 2020)” (2011). System capacity in available seat miles (the

industry measure of aviation related travel demand globally) is “to expand from 4.5% in 2011

and is expected to grow at an average annual rate of 3.6% through 2031” (FAA, 2011, P.

14).

18

Figure 8: Global Fleet Forecast and Leasing Penetration (Source: PWC)

2.6. Leasing’s Value to Airlines

Trubbach (2013, P.20) contributes that large LCCs with “enough funds to cover the

acquisition costs of newly built aircraft” often only use their aircraft for a short time span

before resale, fuelled by “large concessions from OEMS”. Most LCCs lack this financial

clout and therefore cannot execute a similar fleet strategy when they are fledging enterprises,

hence the key role of lessors.

Gavazza (2010) found that high-volatility airlines lease and low-volatility airlines own

aircrafts. This is caused by high-volatility airlines expect to adjust their capacity more

frequently and therefore value leasing more than low-volatility airlines. His 36 empirical

analysis shows that leased aircrafts are parked inactive less frequently than owned aircrafts,

and when under the condition of being used leased aircrafts have a higher capacity utilization

than the owned aircrafts.

Mancilla (2010) provides that a reduction in the requirement for leased aircraft during times

of economic turmoil, which furthers the theory that operating leases have become a

19

significant management tool during a recession. This is due to leasing permitting carriers to

alter capacity quickly, minus the associated asset value risk.

Again, Gavazza (2011) examined the commercial aircraft leasing market with the intuition

that more liquid assets decrease the cost of external financing, this making leasing more

attractive. This is caused by that more liquid assets are more redeploy able and less specific,

which you find in aircrafts. Since more than half of the commercial aircrafts are leased and

there exists an active secondary market, which as mentioned makes aircrafts liquid assets.

One of Gavazza’s findings was that more liquid the aircraft was the more likely to be leased,

and to be an operational lease. Leasing allows also carriers to transfer some risk to the

operating lessors. The lessors are assumed to take the aircraft ownership risk through their

economies of scale, knowledge, diversification of aircrafts and geographic regions, echoing

the work of Pulvino previously.

Oum, Zhang, and Zhang (2000) performed a study about the optimal demand for leased

aircraft. Empirical results based on the model suggested that the optimal demand by 23 major

airlines in the world would range between 40% and 60% of their total fleet, for the reasonable

range of premiums of operating lease.

Clark (2007) explains a relevant advantage of aircraft lease against a loan. Under a loan

structure the repayments are made with constant principal and declining interest, whereas

under a lease structure the repayments are of a mortgage style, with constant payments. The

disadvantage of the loan structure is that it places a burden on the airline cash flow in the

early years, thus the constant payment stream of the lease structure is often the preferred

option.

Gilligan (2004) found an inverse relationship between depreciation and trading volume for

less reliable brands of used business aircraft. Conversely, the author found an increase in the

direct relationship between depreciation and trading volume for aircraft models with

relatively high lease rates.

Gritta and Lynagh (1973) show that airline companies that experience financial difficulties

are the ones that show higher rates of aircraft leasing. For these companies, the paper

suggests that leasing may be the solution today but it also may be tomorrow’s problem.

Airlines appear to be damaging their financial structure, by carrying long-term obligations of

leasing arrangements which accounting authorizes to hide.

20

Likewise, empirical findings from Deloof, Lagaert, and Verschueren (2007) indicate that

leasing is negatively correlated with profitability: firms with low profits and high growth

need more external financing and will therefore have higher fixed-claim financing. Within

airline industry, Erickson and Trevino (1994) expected there would be negative correlation.

The authors criticized that previous leasing literature ignores the effects of profitability on

leasing which results in model misspecification. After performing the tests, lease ratios were

found to be statistically unrelated to profitability.

With all these advantages it is not hard to understand why aircraft leasing penetration rate is

nowadays 39% (according to Ascend), meaning that, on average, airlines fully own 61% of

their fleet.

2.7. Traditional Funding Sources

The need for financial capital is clear and growing. Aircraft are, by definition, long life

capital intensive assets that generate sustained returns in a growing global marketplace.

Institutional investors have developed an improved risk appetite for aircraft assets in both

equity and debt form (Ascend, 2015). This is evolving into increased issuance by leasing

companies and airlines of capital market type instruments.

To date, this active segment of the financial services market is focused largely on dollar-

denominated assets as aircraft are traded around the world using the US currency (Millbank,

2012). With large pools of capital resident in other key currencies, and aircraft operating with

carriers that are centred in those currency blocks, the scope to develop aircraft financing

structures that tap currencies other than the dollar is material.

Another crucial factor to take into account is the diverse support provided to local aviation

industries by the individual government agencies (PWC, 2013). A recent example comes

from Russia where in March, 2014 the local authorities re-introduced a tax exemption on the

import of certain aircraft (including Boeing 737 and Airbus A320) for local carriers (PWC,

2015). The re-introduction allows local operators to save around 40% (approx. $1 billion) on

additional duties and fees. However, not all aircraft operators enjoy the change with the

foreign 50-110-seaters remaining under a normal tax regime. As a result, it hinders their

ability to compete against the operators of their Russian counterparts. Moreover, there is a

chance that Boeing 737 and Airbus 320 might also lose their tax exemption privilege once the

“Irkut MS-21” aircraft model is introduced to the market (Gavazza, 2010).

21

Figure 9: Aircraft Funding Comparison 2013 vs. 2014

Historically, the Export Credit Agencies of the key airframe and engine manufacturing

countries, such as the US, UK, France, and Brazil, have recognised the importance of aircraft

manufacturing to the national economies, and so supported aircraft export by offering

guarantees to cover the losses of commercial banks that were lending to relatively risky

airlines (FAEI, 2015). While traditionally, this type of guarantee-based funding has been used

as a backup, over the last four years ECA backed funding has become the funding source of

choice and has been used by “strong” airlines Etihad, Ryanair, and various Chinese carriers

(Anselmo & Jackson, 2012).

We must note that commercial banks still provide the required funding, ECAs provide

guarantees to make good any specific losses incurred by the funding bank in case of default.

Consequently, the credit risk for banks is not the airline, but the sovereign risk of the ECA

involved. The cost of financing through ECA-backed guarantees has historically been lower

than commercially available bank debt. But, due to the New Aircraft Sector Understanding,

the cost has increased since 2013 as premiums are more aligned with market ratios (PWC,

2014).

As aircraft deliveries peak over the next few years, at a time when long term US dollar

financing becomes scarcer for the major European banks, there are significant challenges for

the industry as a whole to find finance for the new deliveries (Ascend, 2015). All the major

22

players in the industry including manufacturers, financiers, airlines and lessors will need to

work harder to attract new investors to the industry.

Figure 10: Global Distribution of Aircraft Orders 2014

2.8. Recent Industry Developments: The Rise of the “New Age Lessor”

After seeing continuous growth since the late 1970s, the operating lease fleet share had

stagnated since 2008. However, that period of apparent stabilization witnessed the rise of a

new player, one that is making a big impact in the industry: the Chinese operating lessor.

Reports from credit rating agencies S&P and Fitch, highlight cautious concern towards these

newcomers, reflected in ratings ranging from BBB- to C grade investments (Reuters 2015).

Figure 11: Selected Lessor Fleet value Comparison 2016 (PWC, 2015)

23

The mainland Chinese operating-lessor fleet has grown from a mere 30 aircraft at the start of

2008 to over 780 aircraft today, representing 9% of the global lessor jet fleet (Investec, 2012).

Including lessors in Hong Kong and Bank of China subsidiary BOC Aviation based in

Singapore, the Greater China share rises to 13.5%. The mainland lessor fleet has grown at a

staggering compound annual growth rate of 38% since 2010, although lessors are still very

much focused on China, with two-thirds of their fleets on lease to Chinese operators (IAA,

2014). The preference of these lessors towards sale and lease back transactions compounds

this (Investec, 2012).

Figure 12: Total Aircraft Assets Held in China 2008-2014 (Source: CAAC)

Flightglobal’s Fleets Analyzer database shows 15 Chinese mainland-based operating lessors

with in-service fleets, but that number is growing as other platforms come online (CAPA,

2014). The mainland Chinese lessors can be divided into three categories: domestic

domiciled, Chinese money invested offshore and Chinese airlines. The domestic-domiciled

lessors base their operations in China and they include mainly the leasing arms of the major

Chinese banks, but also the insurance companies (Ping An Leasing) and manufacturers

(AVIC). Many also hold finance leases in addition to operating leases.

The second category involves Chinese money invested into leasing companies abroad. The

first big example of this was Hong Kong tycoon Li Ka-shing’s investment in 2014 into

Accipiter, a new leasing platform currently operating out of Dublin (Irish Independent

Report, 2014). Although this case did not involve mainland money, the endorsement of the

operating leasing business model by one of Asia’s wealthiest and most respected investors

sent a strong message to the Chinese community (Investec, 2012). This was followed by

24

Bohai’s acquisition of Dublin-based Avolon, perhaps the first, rather than last move in this

direction. These acquisitions further stress that, should Chinese lessors acquire already

established aircraft lessors in Ireland, it would offer them strong bargaining power and

influence in the global aviation industry with manufacturers (Investec, 2012). This is because

it would bring together airlines, leasing and ground handling within one group.

Finally, Chinese airlines are also participating in creating new leasing companies. Motivated

by tax and financing reasons, they lease aircraft to their own airlines using both finance and

operating leases (PWC 2013). Although these lessors do not match the traditional lessor

mold, they may also decide to set up a more global leasing platform as other airlines have

done recently (i.e., Lion Air and Transportation Partners). The number of leased aircraft in

China is forecast to rise 12.5% a year from 2014 to 2019, faster than the 9.3% a year from

2009 to 2014 (Frost & Sullivan).

Leasing overall has grown an average of 32% a year from 2009 to 2014 in China, making it

the world's largest leasing market with CYN2.63 trillion of assets (Frost & Sullivan).

Penetration of leasing in China reached 5.1% at the end of 2015, considerably lower than in

the more developed markets of the US (23.2%) and the UK (28.6%), suggesting considerable

future opportunities (Frost&Sullivan).

For now the gap between the international market leaders and Chinese rivals is large - the

fleet value of the biggest, BOC Aviation, is less than a fifth of GECAS and a quarter of

ILFC's (Reuters, 2015). But Chinese financiers in the aircraft industry have been growing

rapidly for a decade, with additional impetus provided in 2007 when Beijing lifted a 10-year

ban on banks conducting leasing, which had been imposed in response to reckless investment

and poor management in the 1980s and 1990s. In 2007, China permitted state banks to have

leasing units, but the more recent activity in the sector follows Dec-2013's central

government increased urgency for Chinese lessors to become some of the world's largest by

2030 (Reuters, 2015).

For context, the market value of leased aircraft in China is $34.3bn according to Ascend,

which represents approximately 17.1% of leased aircraft globally (2015). Of the 44 lessors

with exposure to China, the largest on a notional basis are ICBC Financial Leasing Co., Ltd.

($3.4bn, 41.4% of fleet market value according to Ascend), AerCap Holdings, N.V. ($3.1bn,

10.4%), GE Capital Aviation Services ($3.1bn, 10.6%), CDB Leasing Co., Ltd. ($2.6bn,

48.9%), and Bank of Communications Finance Leasing Co., Ltd. ($2.5bn, 69.0%).

25

2.9. Conclusion

Following the literature review, it is clear little is known about the lessors emanating from the

Far East of late and previous literature does not account for their presence given the pace of

their development. This study shall focus on these lessors and increase the knowledge

available on key aspects of their business offerings, nature, prospects and growth factors

involved.

CHAPTER THREE

METHODOLOGY

25

Chapter Three

RESEARCH METHODOLOGY

3. Introduction

The objective of this chapter is to provide a description of the research methodology adopted

specifically for the completion of this study. Research can be defined as “a systematic and

organised effort to investigate a specific problem that needs a solution” (Sekaran 2003).

3.1. Research Problem Identification

The research problem is the starting point of all research (Brannick, 1997) and is defined, as

an area of which there is some doubt, or is concerned with a difficult question that needs to

be answered (Rummel, 1964). The ultimate aim of a research project is to discern what it is

you need to know in order to solve problems or at least give further knowledge and therefore

a deeper understanding to a particular area of study (Remenyi, Williams, Money and Swartz,

1998). Sekaran (2003) highlight that a research problem is identified and recognised once a

research gap emerges and the researcher adopts a problem solving approach to this process.

In the literature examined, many different ideologies and business perspectives have emerged

in relation to aircraft leasing and the rise of new age lessors. The latter has been identified

this as one specific aspect which has been left idle in recent times and the much of the

research is outdated due to the fluid nature of aircraft leasing development of late.

The views of Ritchie and Lewis (2003) in relation to the necessary criteria which must be met

in the formulation of the research question; namely it must be definite and logical, focused

but not restrictive, viable given available resources and attractive and interesting for the

researcher to undertake, have also been given careful consideration.

3.2. The Research Question

Both Sekaran (2003) and Bryman & Bell (2007) have attempted to define a research question

of the issues that is to be investigated with a view to finding a definitive answer. This author

can report that his research question emerged from the research problem originally identified.

According to Blaxter, Hughes and Tight (2010) the choice of research question is the most

important decision when it comes to undertaking research, as a poorly formulated research

question will lead to poor research (Bryman and Bell, 2007). Saunders, Lewis and Thornton

(2007) agree with this train of thought stating that the initial stage of a research study should

start with the formulating and clarifying of the research question in order to turn a research

26

idea into a feasible research study, with obtainable research objectives. This is a vital

element of the process, as it will aid with the choice of research strategy etc.

Another important requirement is a critical review of the literature. It helps to identify key

academic theories within the research question. The literature review also facilitates the use

of clear and accurate referencing allowing the readers of the study to find the original

publications that are cited in the research (Saunders et al, 2007).

The research question specific to this dissertation can be stated as follows:

“To examine the rise of Chinese aviation lessors and the factors which shall impact their

future success and opportunities in the aircraft leasing sector”

3.3. Research Objectives

Zikmund (2003) adequately outlined what an objective should serve to achieve; namely

provide “the purpose of the research in measurable terms; the definition of what the research

should accomplish. This was central to the selection of the research objectives identified.

Domegan and Fleming (2003, pg. 19) have suggested that “problem definition ends with (a) a

list of objectives or (b) a hypothesis. Objectives are broad statements of intent, while a

hypothesis is a tentative answer to the research question being considered”.

Saunders et al (2007) see the research question acting as a basis to generate more detailed

research questions or research objectives. They define research objectives as “clear, specific

statements that identify what the researcher wishes to accomplish as a result of doing the

research” (Saunders et al, 2007, p. 610).

The following research objectives have emerged from the primary research question:

To examine the nature of the suitability of business models currently employed by

fledging lessors in detail and explore the challenges to their future success

To illustrate the developments which have aided the rise of the new age lessor and

resulting industry impact

To identify the potential impact of Chinese economic issues on the development and

abilities these new age lessors to compete effectively in the future

All of the aforementioned research questions and objectives will be addressed and discussed

in the primary research findings to follow.

27

3.4. Research Method Considerations

There are two types of methods of research which are normally the most used in the

collection of data; namely quantitative and qualitative methods (Ghauri et al., 1995).

Quantitative methodologies consist of systematic empirical studies, which involve

quantifying data through the assistance of statistics (Bryman and Bell, 2007). Data is

collected and transformed into numbers, which can be empirically tested for specific

relationships so that conclusions can be drawn. Therefore, quantitative methods are related to

numerical interpretations (Saunders et al, 2007).

Qualitative research does not rely on statistics or numbers. Qualitative methods often refer to

case studies where the collection of information can be received from the study of a small

number of objects (Bryman and Bell, 2007). Qualitative methodologies emphasize on

understanding, interpretation, observations in natural settings and links to data with an insider

view (Ghauri et al., 1995). According to Bryman and Bell (2007) qualitative research is often

an appropriate approach for research in business and management administration.

The type of research approach to select depends on the study that will be conducted.

However, Gunnarson (2002) argues that the benefit of applying a qualitative methodology is

that the method takes into consideration the overall picture, in a manner a quantified method

cannot. A qualitative approach will be more suitable here as this dissertation is researching

the current opportunities available in the aviation financing industry using stakeholders and

due to the fact that perceptions and opinions are difficult to measure in a quantitative way.

The exploratory character of qualitative market research permits the gathering of new

information on specific areas of research, very often through an intensive dialogue between

the interviewer and the respondent (Broda, 2006; Naderer & Balzer, 2007).

Since fieldwork is done without predetermined categories of analysis, qualitative studies

provide depth and detail. In contrast to quantitative methods, which can statistically measure

the reactions of large groups thanks to a limited set of questions and standardized answer

categories, a qualitative study can never reach the same breadth due to the reduced number of

cases (Patton, 2002). Sayre (2001) provides an overview of the differences between

quantitative and qualitative research, with Hennick (2011) providing a concise table of these;

28

Feature: Qualitative Research Quantitative Research

Table 1: Comparison of Research Approaches (Hennink et al, 2011)

Based on this, a qualitative approach is deemed to offer more and has been selected as the

chosen methodology.

3.5. Research Process

Hair et al (2003) provides this activity grants the researcher a "roadmap with directions" for

completing commerce related research. Sekaran (2003) highlights the importance of the

literature review as the first stage to this process. First developed by Saunders, Lewis and

Thornhill (2007), the process onion has emerged as a guiding light in this regard. A key

lesson is to ensure the data collection method is not a driving force of the research process.

29

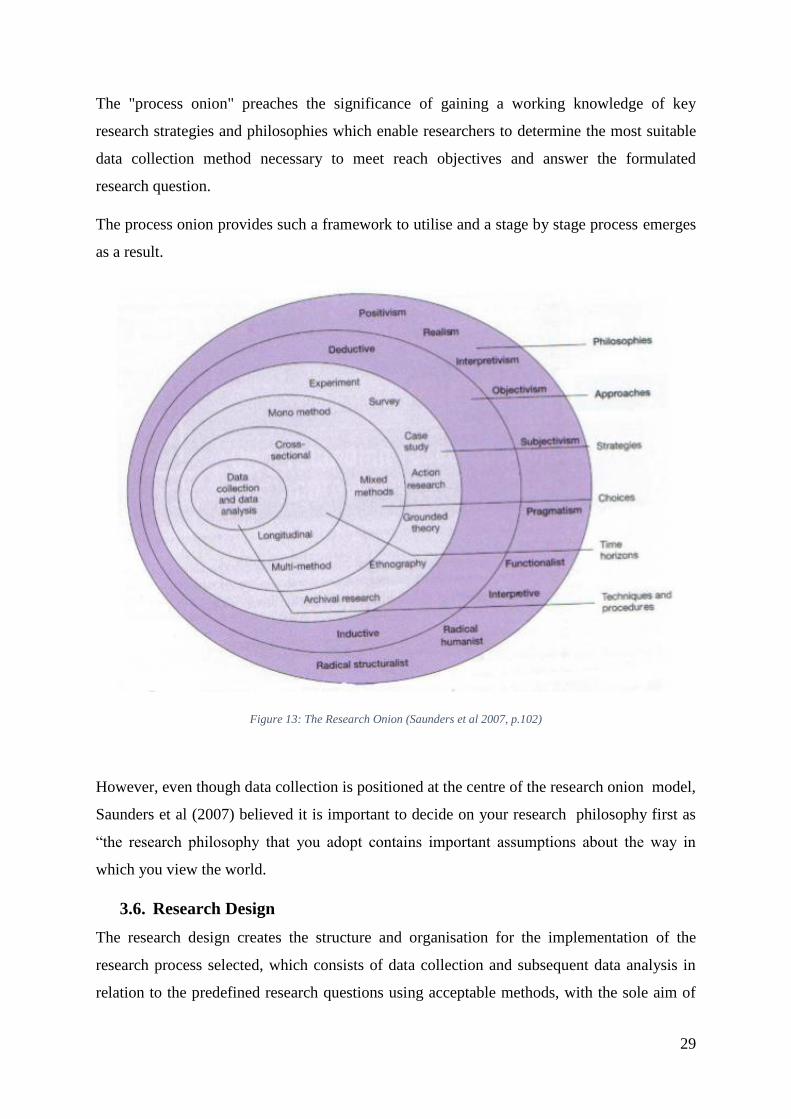

The "process onion" preaches the significance of gaining a working knowledge of key

research strategies and philosophies which enable researchers to determine the most suitable

data collection method necessary to meet reach objectives and answer the formulated

research question.

The process onion provides such a framework to utilise and a stage by stage process emerges

as a result.

Figure 13: The Research Onion (Saunders et al 2007, p.102)

However, even though data collection is positioned at the centre of the research onion model,

Saunders et al (2007) believed it is important to decide on your research philosophy first as

“the research philosophy that you adopt contains important assumptions about the way in

which you view the world.

3.6. Research Design

The research design creates the structure and organisation for the implementation of the

research process selected, which consists of data collection and subsequent data analysis in

relation to the predefined research questions using acceptable methods, with the sole aim of

30

achieving the research objectives cited previously (Easterby-Smith, 1997). It is important to

differentiate between these from the outset, to ensure the proper execution of both by the

researcher (Bryman and Bell, 2007).

3.7. Research Philosophies Considered

A research paradigm describes the philosophical aspects researchers follow and are based on