tiaa-cref institutional perspectives on the asset class · tiaa-cref institutional perspectives on...

TRANSCRIPT

TIAA-CREF

Institutional Perspectives on the Asset Class: Portfolio Construction Techniques

Sandy LaBaugh Sr. Director & Portfolio Manager – TIAA-CREF

October 8, 2013

1

TIAA-CREF

Agenda

Institutional Perspectives on the Asset Class – aligning portfolio construction

techniques with the goals of your investment strategy. Determining the optimal mix

of geographies, species-types and management styles.

TIAA-CREF introduction

Why invest in real assets such as timberland?

Modern Portfolio Theory – Can it be applied to Timber?

What are some alternative allocation strategies?

How to differentiate between the many different Timberland Investment

Management Organizations (“TIMOs”)?

What are some diversification strategies that could be employed within a global

timberland portfolio?

Strictly for professional use and not for public distribution. 2

TIAA-CREF

TIAA-CREF organization overview

Fortune 100 company providing financial solutions to clients for more than 90 years

Leading provider of U.S. retirement benefits serving nearly four million participants

at more than 15,000 institutions and 27,000 plans

TIAA is one of only three insurance groups in the United States to hold the highest

ratings currently awarded from all four leading independent insurance industry

ratings agencies*

−A.M. Best (A++ as of 5/13)

−Fitch (AAA as of 6/13)

−Moody’s Investors Services (Aaa as of 7/13)

−Standard & Poor’s (AA+ as of 6/13)

7,500 employees with offices across the U.S., England and Luxembourg

A leader on Environmental, Social and Governance issues

Strictly for professional use and not for public distribution. 3

With financial strength

and a heritage of

integrity, TIAA-CREF

offers a wide range of

investment capabilities

and services.

*Per S&P criteria, the downgrade of US long-term government debt limits the highest rating of U.S. insurers to AA+ (the second highest rating available). There is

no guarantee that current ratings will be maintained. Ratings represent a company’s ability to meet policyholders’ obligations and claims and do not apply to

variable annuities, mutual funds or any other product or service not fully backed by TIAA's claims-paying ability.

Sustained

Excellence Award

2010 & 2011

Partner of the

Year Award

2008, 2009 & 2013

Co-founder of

The Farmland

Principles

TIAA-CREF

Equity $215

Private Real Estate

$34 Other**

$17

Alternatives $17

Fixed Income $240

4

TIAA-CREF AUM: $523 billion as of June 30, 2013*

Strictly for professional use and not for public distribution. 4

*Assets are preliminary.

**Other represents consolidated assets not reflected in the asset class breakdowns. The assets in the TIAA General Account, variable annuities, mutual funds and private funds are managed by TIAA, TIAA-CREF Investment Management, LLC, Teachers Advisors, Inc. and TIAA-CREF Alternative Advisors, LLC.

Private Real Estate

Core Value-add

Opportunistic Mortgages

Equity

U.S. Emerging Markets

Global REITs

International 130/30

Fixed Income

Core Core Plus

Mortgage-backed Asset-backed

High-yield Emerging Markets

TIPs

Alternatives

Agriculture Private Equity

Energy Timber

Infrastructure

TIAA-CREF

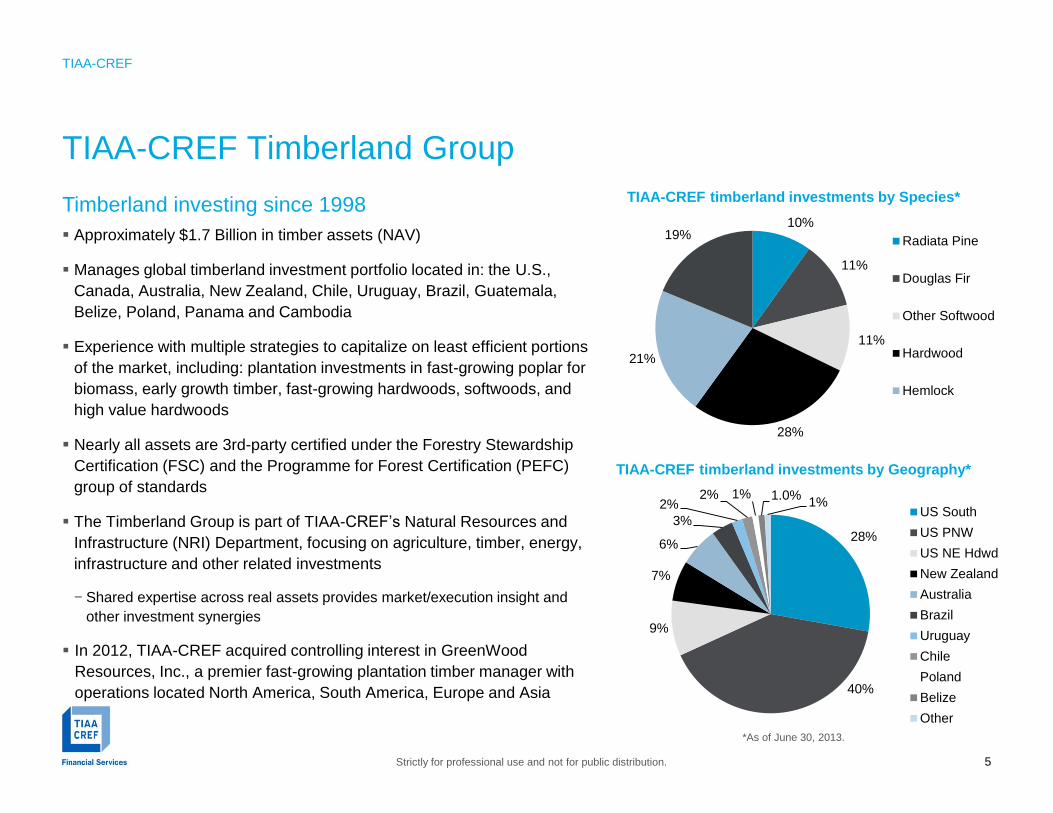

28%

40%

9%

7%

6%

3%

2% 2% 1% 1.0%

1% US South

US PNW

US NE Hdwd

New Zealand

Australia

Brazil

Uruguay

Chile

Poland

Belize

Other

TIAA-CREF Timberland Group

Timberland investing since 1998

Approximately $1.7 Billion in timber assets (NAV)

Manages global timberland investment portfolio located in: the U.S.,

Canada, Australia, New Zealand, Chile, Uruguay, Brazil, Guatemala,

Belize, Poland, Panama and Cambodia

Experience with multiple strategies to capitalize on least efficient portions

of the market, including: plantation investments in fast-growing poplar for

biomass, early growth timber, fast-growing hardwoods, softwoods, and

high value hardwoods

Nearly all assets are 3rd-party certified under the Forestry Stewardship

Certification (FSC) and the Programme for Forest Certification (PEFC)

group of standards

The Timberland Group is part of TIAA-CREF’s Natural Resources and

Infrastructure (NRI) Department, focusing on agriculture, timber, energy,

infrastructure and other related investments

− Shared expertise across real assets provides market/execution insight and

other investment synergies

In 2012, TIAA-CREF acquired controlling interest in GreenWood

Resources, Inc., a premier fast-growing plantation timber manager with

operations located North America, South America, Europe and Asia

Strictly for professional use and not for public distribution. 5

*As of June 30, 2013.

TIAA-CREF timberland investments by Species*

TIAA-CREF timberland investments by Geography*

10%

11%

11%

28%

21%

19% Radiata Pine

Douglas Fir

Other Softwood

Hardwood

Hemlock

TIAA-CREF

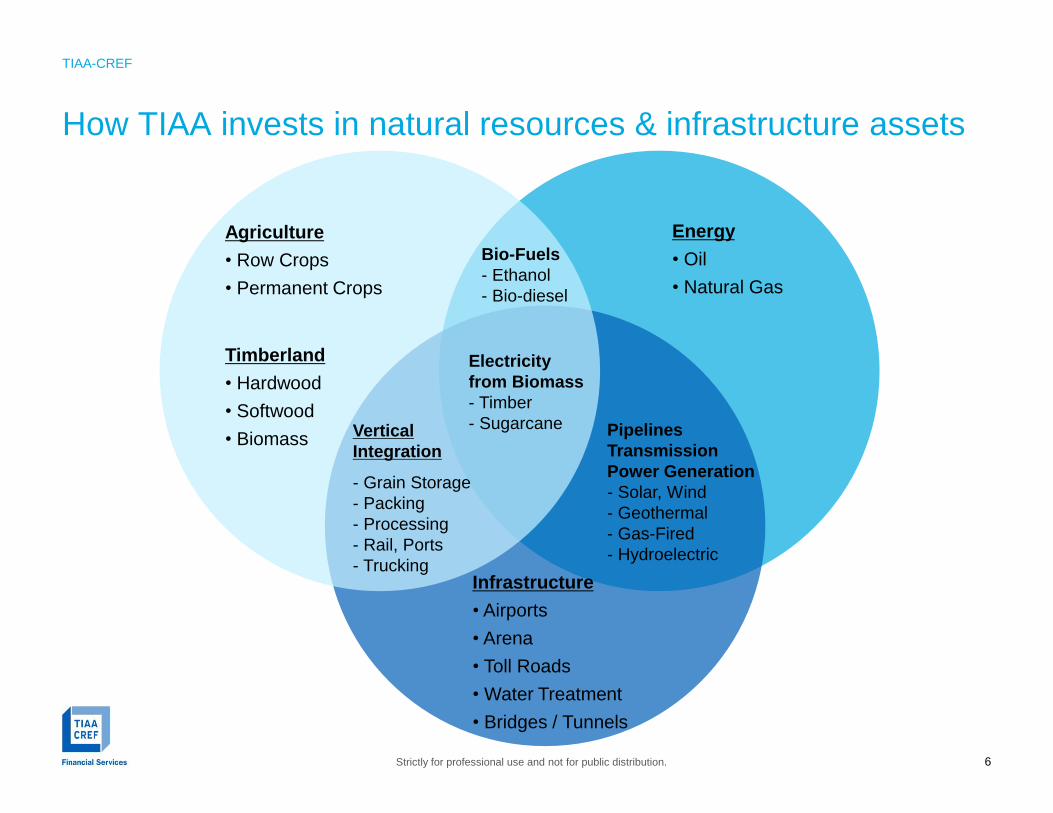

How TIAA invests in natural resources & infrastructure assets

6

Agriculture

• Row Crops

• Permanent Crops

Timberland

• Hardwood

• Softwood

• Biomass

Energy

• Oil

• Natural Gas

Infrastructure

• Airports

• Arena

• Toll Roads

• Water Treatment

• Bridges / Tunnels

Vertical

Integration

- Grain Storage

- Packing

- Processing

- Rail, Ports

- Trucking

Pipelines

Transmission

Power Generation

- Solar, Wind

- Geothermal

- Gas-Fired

- Hydroelectric

Bio-Fuels

- Ethanol

- Bio-diesel

Electricity

from Biomass

- Timber

- Sugarcane

Strictly for professional use and not for public distribution.

TIAA-CREF

15%

Real assets*

U.S. equities

International equities

Fixed income

Short-term/cash

Other alternatives**

Growing institutional demand for real assets Portfolio allocations to real assets are expected to

rise from 5%-10% today to 25% in the next

decade. (JP Morgan research, April 2012)

Average endowment fund allocates 15% to real

assets, including private real estate and natural

resources (oil, gas, timber, commodities and

managed futures).

(NACUBO-Commonfund, January 2013)

Strictly for professional use and not for public distribution. 7

Endowment funds: Asset allocation, 2012

Exposure to real assets continues to rise

*Includes private real estate and natural resources (oil, gas, timber, commodities, and managed

futures)

**Includes hedge funds, private equity, venture capital, distressed debt, and other alternative

investments

***Includes oil, gas, timber, commodities and managed futures; excludes private real estate.

Source: 2012 NACUBO-Commonfund Study of Endowments. Percentages represent dollar-

weighted average allocations across all endowments surveyed.

0.4%

1.6%

8.0%

2002 2007 2012

Rapid growth in allocations

Natural resources*** as % of portfolio assets

(excludes private real estate)

TIAA-CREF

Real Assets: Attractive investment characteristics

Potential for diversification, steady income and capital appreciation

Diversification potential on two levels

−Low correlations with traditional asset classes

−Low correlations among sub-categories of real assets

Asset values often correlate with inflation, providing a potential hedge

Inelastic demand and supply often result in hybrid-like return

characteristics

−Stable, bond-like current income

−Equity-like upside potential for capital appreciation

Long-term hold strategy can optimize asset performance

Relatively low volatility for private real asset vehicles*

−Private investments not exposed to market speculation driving

commodity prices

Strictly for professional use and not for public distribution. 8

*Real assets are less liquid than investments that are continuously marked-to-market. Periodic appraised values may exhibit large fluctuations

reflecting economic, asset-specific, currency, political, regulatory, or environmental factors

TIAA-CREF

Real Assets: Compelling Fundamental Factors

Underlying asset values help ensure capital preservation

Population growth and urbanization increase demand

Natural resources are in finite supply with values rising over time

End products meet basic human needs – few substitutes:

−Agriculture: Food, clothing, biofuel

−Energy: Heat, fuel, electric power

−Infrastructure: Foundation for economic development

−Timberland: Building construction, paper products, biofuels

Strictly for professional use and not for public distribution. 9

TIAA-CREF

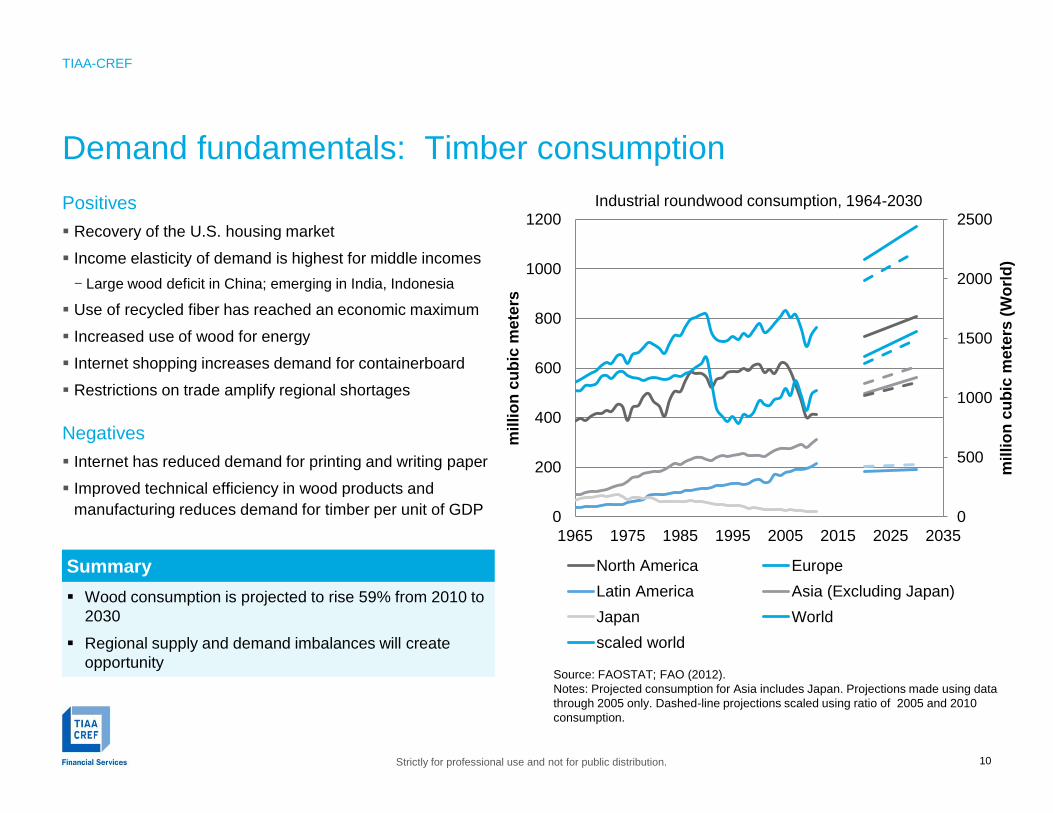

Demand fundamentals: Timber consumption

Positives

Recovery of the U.S. housing market

Income elasticity of demand is highest for middle incomes

− Large wood deficit in China; emerging in India, Indonesia

Use of recycled fiber has reached an economic maximum

Increased use of wood for energy

Internet shopping increases demand for containerboard

Restrictions on trade amplify regional shortages

Negatives

Internet has reduced demand for printing and writing paper

Improved technical efficiency in wood products and

manufacturing reduces demand for timber per unit of GDP

10

0

500

1000

1500

2000

2500

0

200

400

600

800

1000

1200

1965 1975 1985 1995 2005 2015 2025 2035

mil

lio

n c

ub

ic m

ete

rs (

Wo

rld

)

mil

lio

n c

ub

ic m

ete

rs

North America Europe

Latin America Asia (Excluding Japan)

Japan World

scaled world

Source: FAOSTAT; FAO (2012).

Notes: Projected consumption for Asia includes Japan. Projections made using data

through 2005 only. Dashed-line projections scaled using ratio of 2005 and 2010

consumption.

Industrial roundwood consumption, 1964-2030

Wood consumption is projected to rise 59% from 2010 to

2030

Regional supply and demand imbalances will create

opportunity

Summary

Strictly for professional use and not for public distribution.

TIAA-CREF

How to construction a timberland investment portfolio?

Institutional timberland portfolios have historically focused on softwood markets in the U.S., Canada, Australia

and New Zealand –the staple of many institutional timberland portfolios. With increasingly mature institutional

investor presence and high market efficiency, timberland investing is posed to expand geographically, and

consequently in terms of species mix as well.

Strictly for professional use and not for public distribution. 11

Forest (>10% tree cover)

Other land

Water

Source: FAO Global Forest Resources Assessment 2010

The World’s Forests

TIAA-CREF

Modern Portfolio Theory: Capital Asset Pricing Model

• Modern portfolio theory (MPT),

introduced by Markowitz in the 1950s,

was an important advance in the

mathematical modeling of finance to find

the best diversification strategy.

• MPT has the aim of selecting a collection

of investment assets that has collectively

lower risk than any individual asset based

on the concept that different types of

assets often change in value in opposite

ways.

• The efficient frontier is the portion of the

opportunity set that offers the highest

expected return for a given level of risk,

and lies at the top of the opportunity set

or the feasible set.

Strictly for professional use and not for public distribution. 12

Example of real asset impact on portfolio performance*

*Illustrative example based on internal TIAA-CREF analysis

TIAA-CREF

Modern Portfolio Theory: Challenges

The framework of MPT makes many assumptions about investors and

markets including:

• All investors are price takers, i.e., their actions do not influence prices

• Correlations between assets are fixed and constant forever

• Asset returns are (jointly) normally distributed random variables

• All investors have access to the same information at the same time

• All securities can be divided into parcels of any size

• MPT does not account for the personal, environmental, strategic, or social

dimensions of investment decisions

• It only attempts to maximize risk-adjusted returns, without regard to other

consequences

• There are no taxes or transaction costs

Strictly for professional use and not for public distribution. 13

TIAA-CREF

14

Timberland value: Top-down approach

Consider macroeconomic trends (GDP, employment,

political environment, exports, currency markets, etc.)

Examine the business environment (ease of doing

business, corruption risk, labor markets, strength of

legality, tax, etc.)

Study the investible universe

What regions grow what species? What are their

long-term prospects?

What are the end markets? How diversified are they?

How mature are the markets? If immature, why?

What financial return can be achieved?

What crops are favored in this region over the

medium to long term? Are others becoming less

relevant?

Any possible non-agricultural uses for the land?

Look at the broader timberland markets

Identify areas where opportunities appear robust

Macroeconomic

conditions, global

perspective

Identify timberland

market themes

Create return

parameters and

market strategy

Implement strategy

with desired vehicle

structure

Strictly for professional use and not for public distribution.

TIAA-CREF

15

Demand fundamentals: U.S. timberland market

The overall forest products industry was impacted by the recession,

most significantly through the fall of the U.S. housing market, but also

through lower consumer demand.

− Production dropped dramatically from 2006 through 2009. Since then, it

has rebounded gradually, as non-housing markets have further

developed (e.g. industrial, energy, infrastructure) and housing has

gradually rebounded.

− Markets such as the Pacific Northwest, with strong export access, were

less directly impacted.

The U.S. forest products industry is one of the most developed in the world, producing a wide variety of product types from a diverse mix of species and geographies.

Source: RISI

Source: RISI

Strictly for professional use and not for public distribution.

TIAA-CREF

Demand fundamentals: Biomass in Europe

Current situation

2009 EU Renewable Energy Directive: 20% renewable energy target

National Renewable Energy Action Plans (NREAP) indicate large shortfall in

biomass; confirmed by independent research

Sources of supply

Domestic EU pellets: Flat over last 2 years; +5M oven dried metric tons

(“ODMT”) by 2020 (Pöyry)

Imported pellets: +10M ODMT by 2020 (Pöyry)

New plantations required to meet demand

− Outside Europe for EU pellet imports: 1.10 M ha

− Inside Europe for EU pellets: 0.65 M ha

− For wood chips 4.50 M ha

TOTAL 6.25 M ha

Summary

Enormous opportunity exists for developing dedicated biomass plantations

16

0

100

200

300

400

500

600

NREAP Poyry/Eurelectric

Domestic Biomass Supply Biomass Demand

Estimated Biomass Supply and Demand in EU (Million ODMT)

Strictly for professional use and not for public distribution.

TIAA-CREF

Top-down themes: Species mix

With the U.S., Canada, Australia and New Zealand as the traditional timberland investment regions, institutional

portfolios have been largely comprised of softwood species. However, with timberland investments becoming

increasingly global, species mixes within institutional portfolios will likely transition to more equal weighting

between hardwood and softwood varieties.

Strictly for professional use and not for public distribution. 17

Offers access to efficient

commodity markets with easy

institutional opportunities

Linked to inflation

Intermittent cash flows

Emerging opportunity with

potential to create institutional

platform on global scale

Relatively frequent cash flows

compared with other species

Unique international opportunities

with limited institutional presence

to date

More scarce resource

Long term appreciation

Softwood Fast-growing Hardwood Fine Hardwood

TIAA-CREF

Top-down themes: Risk-adjusted real timberland discount rates

With increasing opportunities for international timberland investment, attractive forestry fundamentals must

be balanced with appropriate risk-adjusted returns. The analysis below depicts adjusted and non-adjusted

returns, but realized returns in these countries likely fall somewhere within these ranges.

Strictly for professional use and not for public distribution. 18

0%1%2%3%4%5%6%7%8%9%

10%11%12%13%14%15%

Adjusted for Corruption and Ease Not Adjusted for Corruption and Ease

Countr

y 1

C

ountr

y 2

C

ountr

y 3

C

ountr

y 4

C

ountr

y 5

C

ountr

y 6

C

ountr

y 7

C

ountr

y 8

C

ountr

y 9

C

ountr

y 1

0

Countr

y 1

1

Countr

y 1

2

Countr

y 1

3

Countr

y 1

4

TIAA-CREF

Top-down themes: Geographic allocation

Strictly for professional use and not for public distribution. 19

Most species, both globally and within specific regions, do not have high correlation. This means that forest

product prices do not move in lockstep globally, and diversification may help long-term portfolio performance.

Brazil

Sawlogs

Chile

Sawlogs

Poland

Sawlogs

Spain

Pulplogs (C)

Spain

Pulplogs (NC)

Indonesia

Pulplogs (NC)

US PNW

Sawlogs (DF)

US South

Sawlogs

(Pine)

US South

Pulplogs (C)

Brazil

Sawlogs 1.0

Chile

Sawlogs .0912

1.0

Poland

Sawlogs .3770* .1019 1.0

Spain

Pulplogs (C) .1655 .1033 .4544* 1.0

Spain

Pulplogs (NC) .2442 .0048 .4448* .7631* 1.0

Indonesia

Pulplogs (NC) .2234 .0160 .0792 .0766 .0802 1.0

US PNW

Sawlogs (DF) .2250 .1683 .3365 .2055 -.0401 .1500 1.0

US South

Sawlogs

(Pine)

-.1462 -.3242 -.0142 .0037 -.1624 .0794 .5342* 1.0

US South

Pulplogs (C) .1485 .1663 .1940 -.0367 -.0238 .2596 .3320 .1531 1.0

Source: GWR research; Wood Resources International. Notes: Quarterly price data for the periods: 1Q/2006 to 1Q/2013 for the US; 1Q/1998 to 1Q/2013 for Poland and Indonesia; 1Q/1995 for Brazil, Chile, and Spain. C indicates coniferous and NC non-coniferous; *Significant at the 1% level.

TIAA-CREF

Top-down approach: Pros and cons

20

While good for framework and strategy creation, top-down analysis must be supplemented by bottom-

up consideration of specific opportunities and on-the-ground resources.

Strictly for professional use and not for public distribution.

Pros Cons

Flexible management allows guidance

of portfolio allocation in response to

most attractive themes

Implementation challenging, due to

market complexity and need for local

presence

Narrows down investible universe in

efficient manner, allowing strategy focus

on market segments

Ability to build presence in market

constrained by diversity and depth of

managers and opportunities

TIAA-CREF

21

Timberland value: Bottom-up approach

Manager quality is critical, as returns within similar

strategies can vary meaningfully

Examine the opportunity set of funds and other

structures, seeking best alignment of interests for your

organizational and investment goals

Consider both manager quality and structural alignment of interests

Funnel opportunities to manageable set

Work through a deep-dive with select managers

See the investment through – manager should provide

periodic updates and strong transparency

Consider projected vs. realized results and differentiate

between factors within and beyond manager control

Narrow down opportunities

Compare results against strategy sought…

Define universe of

vehicles to

implement strategy

Consider investable

opportunity set

Define managers that

best align both

strategy and interests

Strictly for professional use and not for public distribution.

TIMO selection

TIAA-CREF

Direct

Investment

Private timberland investment structures

There are several options for investing in private

timberland depending on investment size and

investor preference.

Strictly for professional use and not for public distribution. 22

Separately

Managed

Account Fund of Funds Commingled

Fund

Investment Manager

Investor

Commingled

Fund

Investment

Manager

Timberland

Properties

Timberland

Properties

Timberland

Properties Timberland

Properties

Investor

TIAA-CREF

The TIMO universe

Research by the International Woodland Company identifies 112 TIMOs, representing a wide range of

geographies and strategies.

Strictly for professional use and not for public distribution. 23

New opportunities are emerging, with 64% of TIMOs having been founded in the last five years.

This opens new geographies and regional strategies, but must be weighed against the investment opportunities and

alignment of interests offered by the manager.

38

34

40

0

10

20

30

40

50

> 2 Years 2-5 Years < 5 Years

North America, 38%

Europe, 39%

South America, 15%

Oceania, 6%

Africa & Asia, 2%

TIMO manager tenure Source: IWC

TIMO manager geography Source: IWC

TIAA-CREF

How to differentiate the many different TIMOs?

Timber Investment Management Organizations (“TIMOs”) are

distinguished by a variety of factors.

Strictly for professional use and not for public distribution. 24

Experience Track record

Strategy Regional focus

Transaction size Fees

Property

management

Vertical integration

Subcontracts

TIAA-CREF

Bottom-up approach: Pros and cons

25

While good for framework and strategy creation, top-down analysis must be supplemented by bottom-

up consideration of specific opportunities and on-the-ground resources.

Strictly for professional use and not for public distribution.

Pros Cons

Ease of implementation and oversight Potential portfolio imbalance by stage,

geography, species, etc.

Focus on managers which best align

desired strategy and best interests

Vulnerability to macroeconomic or

environmental factors beyond manager

control

TIAA-CREF

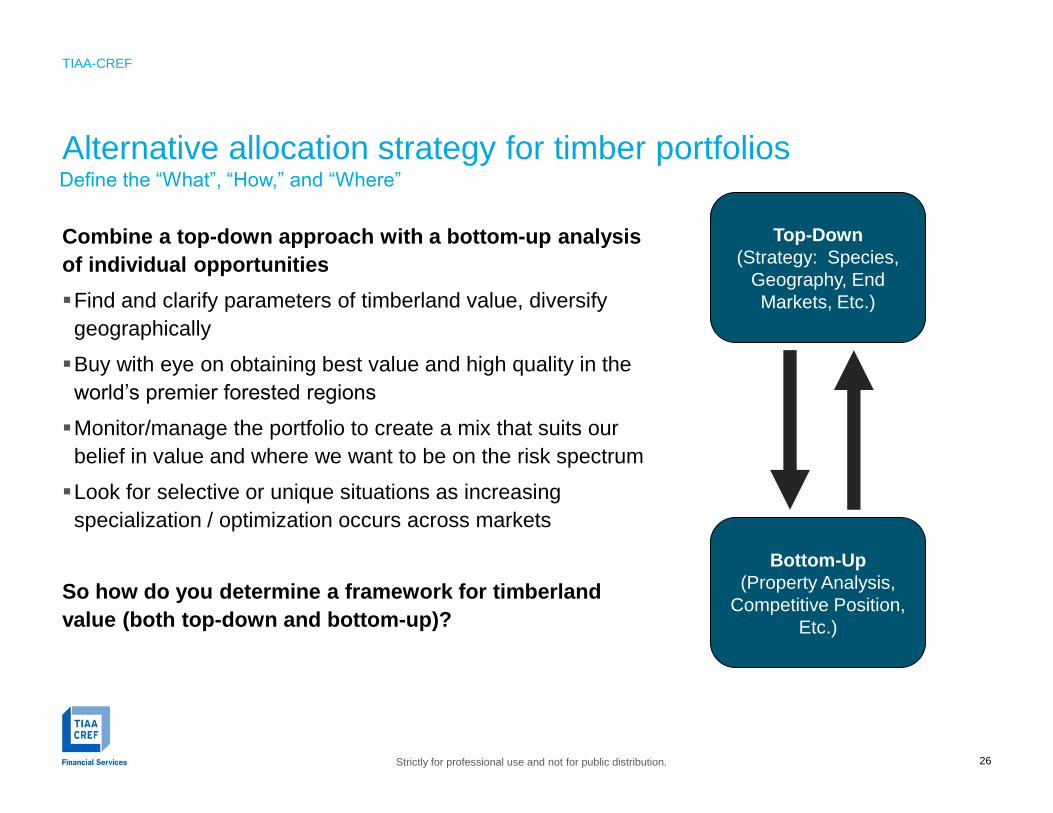

Alternative allocation strategy for timber portfolios

26

Combine a top-down approach with a bottom-up analysis

of individual opportunities

Find and clarify parameters of timberland value, diversify

geographically

Buy with eye on obtaining best value and high quality in the

world’s premier forested regions

Monitor/manage the portfolio to create a mix that suits our

belief in value and where we want to be on the risk spectrum

Look for selective or unique situations as increasing

specialization / optimization occurs across markets

So how do you determine a framework for timberland

value (both top-down and bottom-up)?

Define the “What”, “How,” and “Where”

Top-Down

(Strategy: Species,

Geography, End

Markets, Etc.)

Bottom-Up

(Property Analysis,

Competitive Position,

Etc.)

Strictly for professional use and not for public distribution.

TIAA-CREF

The combined approach

Strictly for professional use and not for public distribution. 27

Define universe of

vehicles to

implement strategy

Consider investable

opportunity set

Define managers that

best align both

strategy and interests

TIMO selection

Macroeconomic

conditions, global

perspective

Identify timberland

market themes

Create return

parameters and

market strategy

Implement strategy

with desired vehicle

structure

Top-down Bottom-up

Allocation risk Pricing risk

Portfolio

construction

and structure

Oversight and risk

management

TIAA-CREF

Future opportunities

Increasing competition has altered institutional timberland investment markets over the last few years, and

investors may increasingly want to take advantage of less efficient markets that offer the strongest return

potential. Often this involves matching attractive property characteristics with resilient markets and

knowledgeable managers who have the ability to add value over the long-term investment period.

Strictly for professional use and not for public distribution. 28

International

Timberland

investing must

balance a range of

outside factors,

including:

Sovereign

Risk

Political

Risk

Legal

Risk

Macro-

Dynamics

Land

Title

Labor

Laws

Environ-

mental