thursday, 13 may 2010 - mcgill.ca€¦ · $70 billion in inflation-adj. losses over the last...

TRANSCRIPT

Vaughn Cordle, CFA

Royal Aeronautics Society

Thursday, 13 May 2010

2

Fear AND Loathing In the Airline Sector-

The lost decade

Incompetent management?

Powerful unions that take more than their fair share?

Government policies – exclusive focus on consumer prices?

Excess seat capacity production by the airlines ?

Internet transparency in pricing?

Too many airlines – destructive price competition?

Best answer at the end of the presentation

3

$70 billion in inflation-adj. losses over the last decade, $63 billion in the domestic market

Weak and overleveraged balance sheets

Large increases in costs are on the way

Optimal time to maximize share price

Labor issues can be worked out

Weakest airlines must merge to survive

CO had to merge with UA to prevent the a UA merger with US.

4

5

Available Seat Miles (ASMs)(scheduled for the week of May 10, 2010) Relative

(millions) to UA/CO

1 United/Continental 5,116 100%

2 Delta 4,445 87%

3 American 3,243 63%

4 Lufthansa* 3,215 63%

5 United pre-merger 3,018 59%

6 Air France/KLM 2,864 56%

7 British Airways/Iberia 2,688 53%

8 Continental pre-merger 2,097 41%

9 Emirates 2,067 40%

10 Southwest 1,991 39%

11 US Airways 1,713 33%

12 Air China* 1,958 38%

13 Qantas* 1,635 32%

14 China Southern 1,316 26%

15 Cathay Pacific 1,313 26%

16 Singapore Airlines 1,284 25%

17 Ryanair 1,275 25%

18 China Eastern* 1,237 24%

19 Air Canada 1,161 23%

20 Japan Airlines* 1,130 22%

2 American/US Airways 4,956 97%

Source: AirlineForecasts & OAG

6

7

Since the early 90s HHI fell significantly to a nadir low 3 quarters (1Q07) before the credit bubble popped and one of the worst recessions on record.

Easy to see why the losses were so massive for the industry during the down turn. Real average fares in the domestic-only market were 38% lower than in the early 90s, when market concentration was at a peak

Anything below .2 is considered perfect competition, above .6 is considered monopoly concentration

8

9

10

Regression Statistics

Multiple R 0.77

R Square 0.59

Adjusted R Square 0.58

Standard Error 13331717

Observations 75

Domesitc - 1977-3Q09FARE PAX

FARE 1

PAX -0.93 1

11

pasng rev price Predicted Actual

per enpland elasticity Enplaned Enplaned Stage

passenger demand Passengers Passengers Length

(millions (millions Pax shr

Domestic 104$ -0.54 173 163 89% 1,062

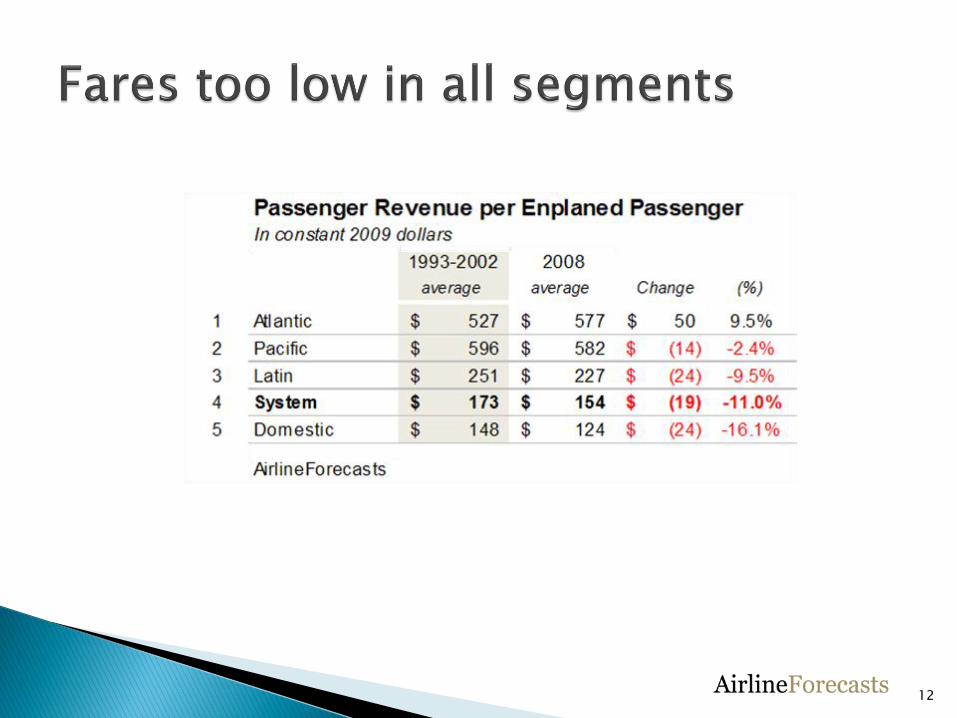

Atlantic 480$ -0.26 4.9 7.5 4% 4,335

Pacific 487$ 0.09 3.2 3.3 2% 4,942

Latin 182$ -1.17 9.6 9.2 5% 1,291

System 130$ -0.62 186 183.3 100% 1,132

12

13

Passenger Yields (pax rev / RPMs)In cents and constant 3Q09 dollars

Average Average Relative Year-over year % chg.

91-'03 2003 2004 2005 2006 2007 2008 2009* 04-'09 Change 03-'09 07-'08 08-'09 07-'09

1 Atlantic 13.2 11.3 11.6 12.0 12.5 13.1 13.3 10.9 12.3 -7% -3% 6% -18% -17%

2 Pacific 14.4 10.1 11.0 11.2 11.6 12.3 12.8 10.8 11.7 -19% 7% 10% -16% -12%

3 Latin 18.2 15.2 14.5 14.0 14.3 14.2 14.7 12.4 14.1 -23% -18% 3% -16% -13%

System 17.3 14.0 13.4 13.4 13.7 13.6 13.9 11.9 13.4 -23% -15% 1% -14% -13%

4 Domestic 18.3 14.6 13.9 13.7 14.1 13.8 14.0 12.1 13.7 -25% -17% -1% -13% -12%

*2009: Three quarter avg. through 3Q09

Source: DOT Form 41 & AIrlineForecasts

14

U.S Passenger Airline Revenue

in $millons 2008 2009 % chng

Total Revenue 145,635 123,224 -15.4%

Passenger Revenue 111,002 91,259 -17.8%

Misc fees/charges/other 27,069 23,452 -13.4%

Baggage Fees 1,146 2,712 136.7%

Freight 3,601 2,438 -32.3%

Cancellation Fees 1,654 2,364 42.9%

Charter Pasn'gr + Prop 667 598 -10.4%

Mail 496 401 -19.1%

Percentage of total revenue

Passenger Revenue 76.2% 74.1%

Misc fees/charges/other 18.6% 19.0%

Baggage Fees 0.8% 2.2%

Freight 2.5% 2.0%

Cancellation Fees 1.1% 1.9%

Charter Pasn'gr + Prop 0.5% 0.5%

Mail 0.3% 0.3%

AirlineForecasts & DOT Form 41

15

Capacity Growth (ASMs)

Average Yr-over-yr change Average Relative

91-'03 2003 2004 2005 2006 2007 2008 2009* 04-'09 Change

1 Pacific -1.5% -7.6% 12.1% 11.6% 1.0% 0.5% -0.7% -7.0% 3.4% 4.9

2 Atlantic 3.4% -5.9% 10.8% 6.4% 7.7% 9.8% 9.9% -3.6% 7.3% 3.9

3 Latin 6.5% 0.9% 14.3% 11.0% 6.7% 4.1% 0.7% -1.1% 6.3% -0.2

System 2.0% 0.5% 9.4% 3.2% 0.3% 3.1% -1.5% -6.8% 1.6% -0.4

4 Domestic 2.1% 2.3% 8.6% 1.4% -1.4% 2.2% -3.8% -8.0% 0.2% -1.9

*2009: Three quarter avg. through 3Q09

Source: DOT Form 41 & AIrlineForecasts

16

Net Income Margins per Passenger

Average Average Relative

91-'03 2003 2004 2005 2006 2007 2008 2009* 04-'09 Change

1 Atlantic -2.8% -0.3% 0% -21% 27% 11% -19% -6% -1.2% 1.6

2 Latin 1.6% 4.3% 2% -12% 15% 10% -5% 2% 1.8% 0.2

3 Pacific -3.4% -16.5% -5% -66% 53% 10% -24% -5% -6.1% -2.7

System -1.3% -2.4% -9% -24% 14% 4% -17% -3% -6.0% -4.7

4 Domestic -1.3% -2.3% -12% -22% 9% 2% -18% -3% -7.4% -6.1

*Three quarters to 3Q09

AIrlineForecasts

17

Capital Sturcture Deficit Tangible

Market Book Intangible Tangible Total Book equity

Equity Equity assets Equity Assets to Assets

1 Allegiant 1,016 292 292 500 58%

2 Southwest 9,574 5,220 5,537 14,530 38%

3 Jeblue 1,667 1,510 1,534 6,513 24%

4 AirTran 705 487 487 2,286 21%

5 Alaska 1,583 774 885 5,016 18%

6 Continental 2,836 497 774 (277) 13,318 -2%

7 US Airways 1,100 (447) 616 (1,063) 7,808 -14%

8 American 2,311 (3,892) 981 (4,873) 25,525 -19%

9 Delta 9,759 72 9,794 (9,722) 44,339 -22%

10 United 3,265 (2,887) 2,863 (5,750) 19,952 -29%

Top 10 33,816 1,625 15,028 (12,950) 139,786 -9%

AMR/US 12,070 (3,820) 10,775 (14,595) 33,333 -44%

UAL/CAL 6,101 (2,390) 3,637 (6,027) 33,270 -18%

AirlineForecasts

18

Book Equity Deficit Tangible

Equity Equity % of total % of total

($ millions) Deficit Deficit Assets Revenue

1 Allegiant (167) (167) -33% -25%

2 Southwest (1,588) (1,588) -11% -13%

3 Jeblue 118 118 2% 3%

4 AirTran 85 85 4% 3%

5 Alaska 480 480 10% 13%

6 Continental 2,833 3,607 27% 25%

7 US Airways 2,399 3,015 39% 25%

8 American 10,273 11,254 44% 50%

9 United 7,875 10,738 54% 55%

10 Delta 11,013 20,807 47% 66%

Top 10 Airlines 33,321 48,349 35% 40%

United + Continental 10,708 14,345 43% 43%

American + US Airways 12,672 14,269 43% 42%

AirlineForecasts

19

20

2010 Revenue & Earnings Estimates

Revenue Net Profit Margins

($millions) ($millions)

1 Allegiant 681$ 81$ 12.0%

2 Alaska 3,691 189 5.1%

3 Southwest 11,885 536 4.5%

4 Delta 31,571 1,354 4.3%

5 Hawaii 1,326 49 3.7%

6 United 19,353 638 3.3%

7 Continental 14,231 378 2.7%

8 Airtran 2,690 70 2.6%

9 JetBlue 3,778 88 2.3%

10 US Airways 11,864 259 2.2%

11 American 22,358 333 1.5%

Major Airlines 123,427$ 3,976$ 3.2%

1 Skywest 2,552 96 3.8%

2 Pinnacle 848 25 2.9%

3 Republic 2,041 10 0.5%

United/Continental 33,584 1,016 3.0%

American/US Airways 34,222 592 1.7%

AirlineForecasts

21

2011 Revenue & Earnings Estimates

Revenue Net Profit Margins

($millions) ($millions)

1 Allegiant 817$ 91$ 11.1%

2 Alaska 3,881 209 5.4%

3 Southwest 12,812 670 5.2%

4 Delta 33,427 1,614 4.8%

5 United 20,432 757 3.7%

6 Hawaii 1,357 50 3.7%

7 JetBlue 4,135 149 3.6%

8 Airtran 2,902 87 3.0%

9 Continental 15,101 433 2.9%

10 US Airways 12,444 317 2.6%

11 American 23,723$ 566$ 2.4%

Major Airlines 131,030$ 4,943$ 3.8%

United/Continental 35,533 1,190 3.3%

American/US Airways 36,167 883 2.4%

AirlineForecasts

22

Enterprise Value and CashFlow

CA/UAUA AMR/LCC

$ millions DAL CAL + UAUA Combined AMR + LCC Combined JBLU LUV ALK

Market Cap 9,900 2,870 3,320 6,190 2,340 1,120 3,460 1,690 9,570 1,590

Total Debt 16,916 6,191 9,304 15,495 10,916 4,606 15,522 3,119 3,475 1,476

MRQ Rent 112 229 81 129 171 31 47 26

Annualized MRQ Rent Capitalized at 7.0x 3,136 6,412 2,268 8,680 3,612 4,788 8,400 868 1,316 725

Cash (including restricted cash) 5,369 3,153 3,599 6,752 5,006 1,532 6,538 1,072 2,773 1,171

Enterprise Value 24,583 12,320 11,293 23,613 11,862 8,982 20,844 4,605 11,588 2,620

Rent capitalization multiple: 7.0x

EBITDA Estimates as of 5/12/10:

2010 4,180 1,210 2,422 3,632 1,530 966 2,496 610 1,626 601

2011 4,886 1,464 2,602 4,065 1,978 1,103 3,080 698 1,802 606

EV / EBITDAR

2010 5.3x 5.7x 4.1x 4.8x 5.7x 5.3x 5.5x 6.2x 6.4x 3.7x

2011 4.6x 5.0x 3.8x 4.3x 4.7x 4.8x 4.7x 5.5x 5.8x 3.6x

AirlineForecasts

Oberstar will hold hearings and has tasked the GAO to study the merger

14 high concentration city pairs

DOJ makes decisions based on concentration of specific markets, not system-wide. DOT provides analysis and input

DOT decides international issues and grants ATI for JVs

23

Market Continental United Combined

Cleveland 64.70% 5.00% 69.80%

Houston* 66.10% 1.60% 67.70%

Guam 50.30% 0.00% 50.30%

Denver 1.70% 42.30% 44.00%

San Francisco 3.30% 40.70% 44.00%

Chicago* 1.30% 36.10% 37.50%

Washington D.C.* 2.60% 25.80% 28.40%

New York* 23.10% 3.20% 26.30%

Los Angeles 3.60% 17.20% 20.80%

Tokyo (Narita) 1.80% 5.10% 6.90%

*Includes multiple airportsSource: OAG Schedules

Market Share at Top Hubs (based on Scheduled Seats)

Not all of the cost and revenue synergies will fall to the bottom line. Stated

differently, shareholders will only capture perhaps 1/2 of the $1.8–2.2 billion we are

estimating as the base-case cost/revenue synergies UAL/CAL merger. Even at 1/2, the

leverage to the bottom line is significant, which is why market values will increase

significantly

Timing is very good for a merger in the airline industry. Why? The window to

create the most value is open, but it will start closing as labor pressures for higher

wages ($3.3–6 billion) and higher airport PFC fees ($2 billion higher) and security

costs ($2.7 billion by 2014) kick in. Also, higher fuel costs have become a catalyst,

encouraging CEOs/CFOs to move towards protecting and enhancing shareholder value.

Fuel costs in 2010 will be around $6.4 billion higher than 2009's – $80 base case this

year and $84 in 2011.

24

A merger will be good for the airlines, labor and shareholders. Moreover, it can

benefit the consumer as the industry moves towards a more viable structure that can

afford to properly invest and provide the required level of service.

In the decade ending in 2009, the U.S. airline industry lost over $70 billion in 2009

dollars. Hence the need for greater concentration – i.e., fewer airlines – and pricing

power, which does not exist in the domestic market.

Herfindahl (HHI) concentration analysis : In the domestic-only segment, the value is

around .14 and would increase to .18 after UAL merges CAL. Anything under .2 is

considered close to "perfect competition" and results in destructive price competition

where consumers capture the bulk of the value produced by the industry. However,

with the joint ventures and more concentrated alliances, and the merger, pricing power will result, at least for a period of time.

25

26

DOT Airline Advisor Commission objectives:

• Safety: gotta say this and more money is typically the only way to improve safety.• World-class aviation workforce: skill set or in terms of wages/benefits?• Balancing competitiveness and viability: without mergers, the networks are not viable and will continue a slow liquidation.• Securing funding: charge the airlines or taxpayers, with airlines likely paying for technology that helps the airlines.• Addressing environmental challenges and solutions -carbon taxes are coming and airline passengers will have to pay their fair share.

27

The simple equation:

World class workforce + balance between competitiveness and viability + carbon taxes + funding for ATC and aircraft technology = higher government taxes/fees, security costs, airport charges, ADS-B technology costs, and labor costs for the airlines.

These higher costs must be viewed within the context of a $1.4 to $2 trillion budget deficit and Obama's need to reduce government spending in later years.

Solution:

Allow consolidations and mergers which will allow the industry to pass the increased costs on to consumers of the air transportation system.

Incompetent management?

Powerful unions that take more than their fair share?

Government policies – exclusive focus on consumer prices?

Excess seat capacity production by the airlines

Internet transparency in pricing?

Too many airlines – destructive price competition

Best answers in red

28